BAILLIEU HOLST RESEARCH 19 October 2015 Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report. RESEARCH TEAM Nicolas Burgess Head of Research +61 3 9602 9379 [email protected] Nick Caley Analyst – Industrials +61 3 9602 9283 [email protected] Luke Macnab Analyst – Industrials +61 2 9250 8930 [email protected] Josh Kannourakis Analyst – Industrials +61 3 9602 9265 j[email protected] Warren Edney Analyst – Resources +61 3 9602 9384 [email protected] Mathan Somasundaram Analyst – Equity Strategy, Quant +61 2 9250 8947 [email protected] Piers Flanagan Associate Analyst +61 3 9282 8127 [email protected] Australian Equity Research OCTOBER 2015 Top Stock Picks Overall: We select the top picks across our 71 mid and small cap stock universe, as well as the outlook for the economy and equity market. We also provide our key insights from our listed investment company (LIC) coverage. Equity market outlook: We maintain a bullish long term view on the Australian equity market with a 12 month index target level of 6100. Recent profit taking by global investors on currency worries has lowered the market to a fair value level of 5000 with no premium being paid for the substantially high dividend yield. We maintain our positive long term view on the yield trade (i.e. Banks, Div Financials and Telcos) while health care looks the best growth/currency story. We continue to favour the new economy (i.e. MITCH Universe – Media, Information, Telecom, Consumer and Health) over the old economy on a long term view. We expect short term profit taking with US reporting season risk, while China releases long term growth plans and the US Fed pushes back rate rise plans to help drive markets higher for a Christmas rally. Key trends in stock picks: The top stock picks are shown in the table below (alphabetical order). Although Baillieu Holst employs a bottom-up, fundamental approach to stock analysis and valuation, there are some key themes common across the top picks. These include offshore earnings and upside to ongoing AUD weakness, technology and telecommunications, professional services, and, in resources, gold. Listed Investment Companies (LICs): Baillieu Holst provides performance reporting and insights across a universe of 46 listed investment companies. Based on that analysis, our top picks include Diversified United Investments (DUI) in large caps, Future Generation Fund (FGX) in small caps, PM Capital Global Opportunities Fund (PGF) and Magellan Flagship Fund (MFF) in international, and Acorn Capital Investment Fund (ACQ) in the specialty sector. Rating System: The Baillieu Holst stock rating system is based on BUY (stock’s total return is expected to increase by at least 10-15% from the current share price over the next 12 months), HOLD (total return is expected to trade within a range of ±10-15%) and SELL (total return is expected to decrease by at least 10-15%). Each stock is also assigned a risk rating of Low, Medium, High or Speculative. SUMMARY OF TOP PICKS Share Price Stock Code Rating Risk Price Target Analyst Donaco International DNA BUY High 0.80 1.15 Nick Caley Empired EPD BUY High 0.85 1.20 Josh Kannourakis Henderson Group HGG BUY Medium 5.65 7.00 Nicolas Burgess M2 Group MTU BUY Medium 9.50 10.88 Luke Macnab Mantra Group MTR BUY Low 4.11 4.40 Nick Caley Northern Star NST BUY High 3.09 3.57 Warren Edney QMS Media QMS BUY High 0.92 1.10 Nicolas Burgess Saracen Minerals SAR BUY High 0.58 0.64 Warren Edney Shine Corporate SHJ BUY Medium 2.01 3.50 Nick Caley Speedcast International SDA BUY High 4.55 5.01 Luke Macnab Steadfast Group SDF BUY Medium 1.48 1.80 Nicolas Burgess Vita Group VTG BUY Medium 1.67 2.10 Josh Kannourakis Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BAILLIEU HOLST RESEARCH 19 October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RESEARCH TEAM Nicolas Burgess

Head of Research

+61 3 9602 9379

Nick Caley

Analyst – Industrials

+61 3 9602 9283

Luke Macnab

Analyst – Industrials

+61 2 9250 8930

Josh Kannourakis

Analyst – Industrials

+61 3 9602 9265 [email protected]

Warren Edney

Analyst – Resources

+61 3 9602 9384

Mathan Somasundaram

Analyst – Equity Strategy, Quant

+61 2 9250 8947

Piers Flanagan

Associate Analyst

+61 3 9282 8127

Australian Equity Research

OCTOBER 2015

Top Stock Picks

Overall: We select the top picks across our 71 mid and small cap stock universe, as well as the outlook for the economy and equity market. We also provide our key insights from our listed investment company (LIC) coverage.

Equity market outlook: We maintain a bullish long term view on the Australian equity market with a 12 month index target level of 6100. Recent profit taking by global investors on currency worries has lowered the market to a fair value level of 5000 with no premium being paid for the substantially high dividend yield. We maintain our positive long term view on the yield trade (i.e. Banks, Div Financials and Telcos) while health care looks the best growth/currency story. We continue to favour the new economy (i.e. MITCH Universe – Media, Information, Telecom, Consumer and Health) over the old economy on a long term view. We expect short term profit taking with US reporting season risk, while China releases long term growth plans and the US Fed pushes back rate rise plans to help drive markets higher for a Christmas rally.

Key trends in stock picks: The top stock picks are shown in the table below (alphabetical order). Although Baillieu Holst employs a bottom-up, fundamental approach to stock analysis and valuation, there are some key themes common across the top picks. These include offshore earnings and upside to ongoing AUD weakness, technology and telecommunications, professional services, and, in resources, gold.

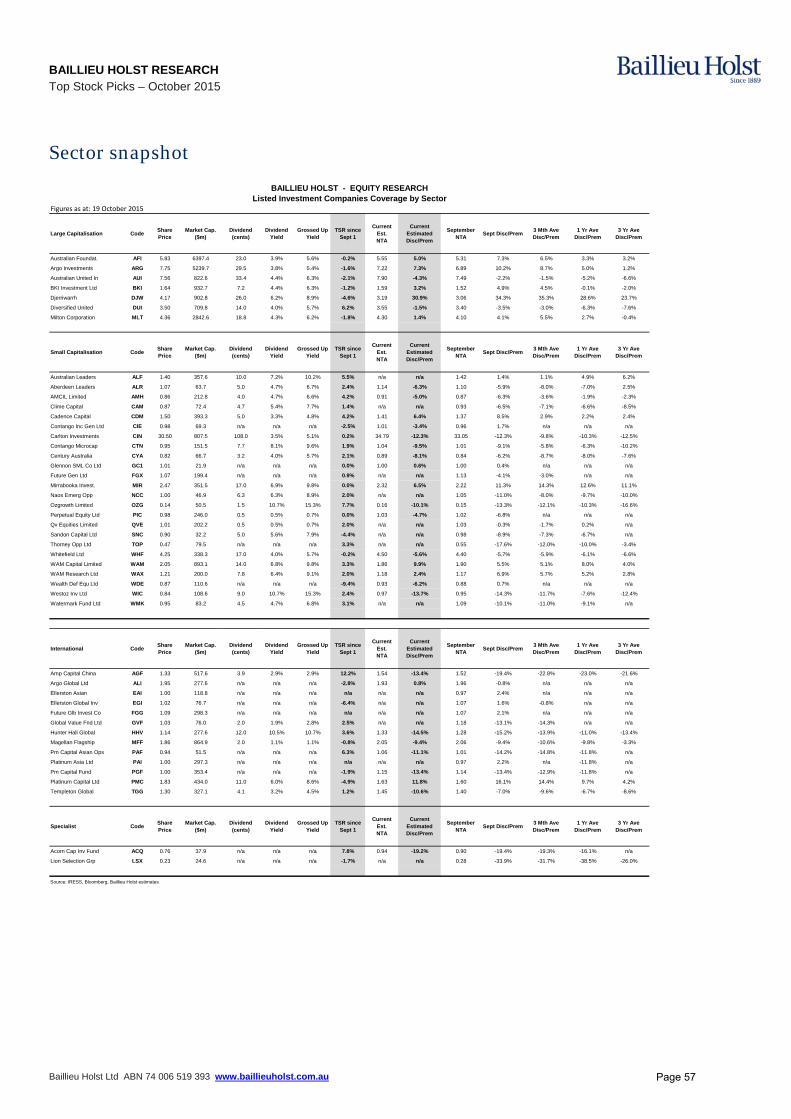

Listed Investment Companies (LICs): Baillieu Holst provides performance reporting and insights across a universe of 46 listed investment companies. Based on that analysis, our top picks include Diversified United Investments (DUI) in large caps, Future Generation Fund (FGX) in small caps, PM Capital Global Opportunities Fund (PGF) and Magellan Flagship Fund (MFF) in international, and Acorn Capital Investment Fund (ACQ) in the specialty sector.

Rating System: The Baillieu Holst stock rating system is based on BUY (stock’s total return is expected to increase by at least 10-15% from the current share price over the next 12 months), HOLD (total return is expected to trade within a range of ±10-15%) and SELL (total return is expected to decrease by at least 10-15%). Each stock is also assigned a risk rating of Low, Medium, High or Speculative.

SUMMARY OF TOP PICKS

Share Price

Stock Code Rating Risk Price Target Analyst

Donaco International DNA BUY High 0.80 1.15 Nick Caley

Empired EPD BUY High 0.85 1.20 Josh Kannourakis

Henderson Group HGG BUY Medium 5.65 7.00 Nicolas Burgess

M2 Group MTU BUY Medium 9.50 10.88 Luke Macnab

Mantra Group MTR BUY Low 4.11 4.40 Nick Caley

Northern Star NST BUY High 3.09 3.57 Warren Edney

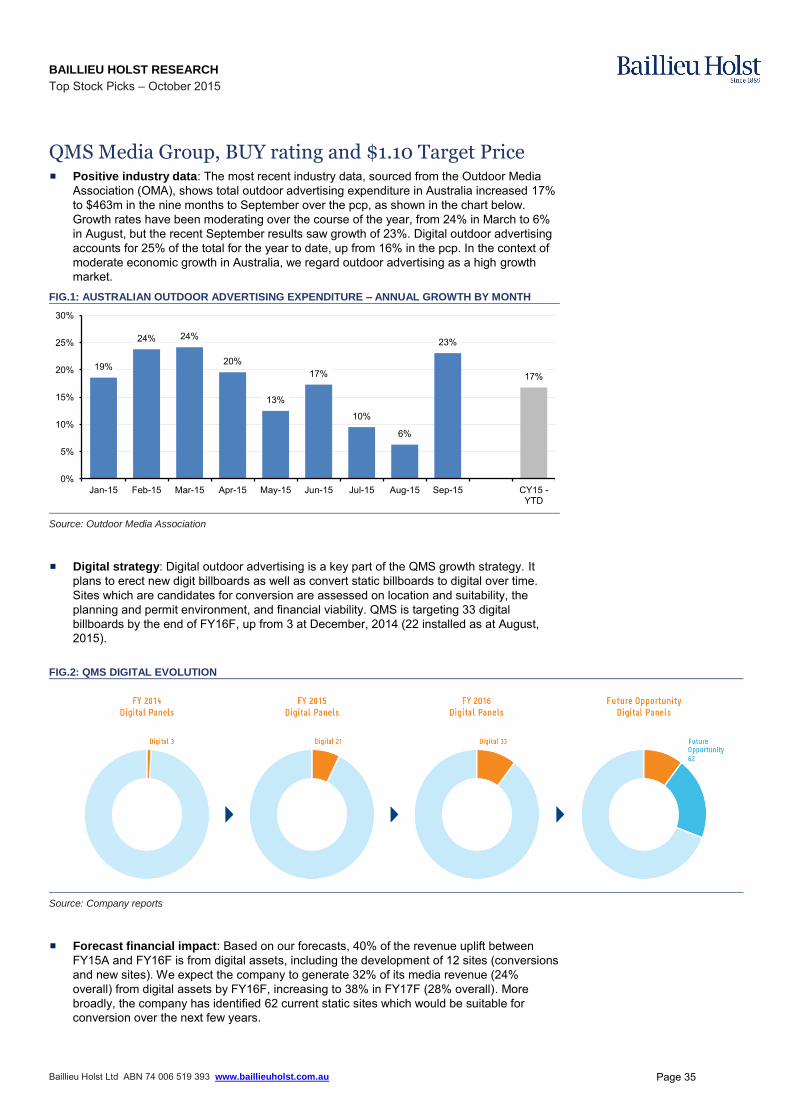

QMS Media QMS BUY High 0.92 1.10 Nicolas Burgess

Saracen Minerals SAR BUY High 0.58 0.64 Warren Edney

Shine Corporate SHJ BUY Medium 2.01 3.50 Nick Caley

Speedcast International SDA BUY High 4.55 5.01 Luke Macnab

Steadfast Group SDF BUY Medium 1.48 1.80 Nicolas Burgess

Vita Group VTG BUY Medium 1.67 2.10 Josh Kannourakis

Page 1

BAILLIEU HOLST RESEARCH Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Coverage Universe – Mid and Small Caps Mkt EPS EPS PE PE DPS DPS DY DY

Company Name Code Analyst P Rec TP Cap '15 '16 '15 '16 '15 '16 '15 '16

Industrials

Collection House CLH Nick Caley 2.20 HOLD 2.45 294 17.1 17.5 12.9 12.6 9.1 10.3 4.1 4.7

Credit Corp Group Ltd CCP Nick Caley 9.84 HOLD 11.40 455 83.0 91.1 11.9 10.8 44.0 48.0 4.5 4.9

Hughes Drilling HDX Josh Kannourakis 0.13 BUY 0.23 27 5.2 4.5 2.5 2.9 0.0 0.0 0.0 0.0

IPH Limited IPH Nick Caley 6.66 HOLD 7.25 1154 19.7 25.1 33.8 25.7 13.5 20.0 2.0 3.0

Logicamms LCM Josh Kannourakis 0.70 BUY 1.05 48 12.0 11.3 5.8 6.2 7.0 5.5 10.0 7.9

MaxiTRANS Industries MXI Josh Kannourakis 0.51 BUY 0.65 94 4.7 5.9 10.9 8.6 2.0 3.7 3.9 7.3

Monadelphous Group MND Josh Kannourakis 7.32 HOLD 8.00 662 113.9 92.6 6.4 7.9 90.0 74.0 12.3 10.1

Silver Chef SIV Nick Caley 8.85 HOLD 8.75 280 51.9 56.4 17.1 15.7 36.0 36.0 4.1 4.1

Tox Free Solutions TOX Josh Kannourakis 2.74 HOLD 2.90 364 16.9 17.9 16.2 15.3 8.5 9.0 3.1 3.3

Wellcom Group Ltd WLL Nicolas Burgess 4.57 BUY 4.70 178 24.9 27.8 18.4 16.4 20.5 22.0 4.5 4.8

Consumer Discretionary

Ainsworth Game Technology Ltd AGI Nick Caley 2.95 BUY 3.90 944 21.8 20.1 13.5 14.7 10.0 13.0 3.4 4.4

Amalgamated Holdings AHD Nick Caley 13.63 HOLD 14.10 2159 67.9 71.7 20.1 19.0 45.0 50.0 3.3 3.7

APN Outdoor Group APO Nicolas Burgess 4.13 BUY 4.50 698 21.0 24.4 19.7 16.9 12.5 14.5 3.0 3.5

Ardent Leisure Group AAD Nick Caley 2.70 BUY 3.00 1219 12.9 16.1 20.9 16.8 12.5 14.0 4.6 5.2

Aristocrat Leisure Ltd ALL Nick Caley 9.03 BUY 9.25 5664 36.6 42.6 24.6 21.2 18.0 23.0 2.0 2.5

Cash Converters CCV Nick Caley 0.52 HOLD 0.60 260 -4.7 7.2 0.0 7.2 2.0 5.3 3.8 10.2

Collins Foods Ltd CKF Josh Kannourakis 3.35 BUY 3.25 312 26.4 28.8 12.7 11.6 11.5 12.5 3.4 3.7

Dominos Pizza Enterprises Ltd DMP Josh Kannourakis 47.03 HOLD 41.51 4056 72.8 93.2 64.6 50.5 50.6 62.0 1.1 1.3

Donaco International DNA Nick Caley 0.80 BUY 1.15 636 1.3 8.4 59.6 9.4 0.0 0.0 0.0 0.0

iCar Asia Ltd ICQ Nick Caley 0.83 BUY 1.05 205 -5.1 -2.0 0.0 0.0 0.0 0.0 0.0 0.0

iSelect ISU Nick Caley 1.77 BUY 2.05 452 8.2 8.3 21.7 21.3 0.0 0.0 0.0 0.0

Jumbo Interactive Ltd JIN Nick Caley 1.05 BUY 1.25 46 1.5 6.8 70.0 15.4 3.0 3.0 2.9 2.9

Mantra Group MTR Nick Caley 4.11 BUY 4.40 1098 15.3 16.9 26.8 24.3 10.0 12.0 2.4 2.9

QMS Media QMS Nicolas Burgess 0.92 BUY 1.10 231 1.0 5.9 92.0 15.6 0.0 1.5 0.0 1.6

Retail Food Group RFG Josh Kannourakis 4.62 BUY 7.50 743 35.6 41.7 13.0 11.1 23.3 27.0 5.0 5.8

Shine Corporate SHJ Nick Caley 2.01 BUY 3.50 343 17.2 19.6 11.7 10.3 3.8 4.8 1.9 2.4

Slater & Gordon Ltd SGH Nick Caley 2.88 BUY 6.00 974 35.4 56.3 8.1 5.1 9.0 10.5 3.1 3.6

Village Roadshow Ltd VRL Nick Caley 7.32 BUY 7.60 1160 31.0 39.7 23.6 18.4 28.0 32.5 3.8 4.4

Vita Group VTG Josh Kannourakis 1.67 BUY 2.10 253 12.4 14.1 13.5 11.9 8.0 9.2 4.8 5.5

Consumer Staple

Bega Cheese BGA Josh Kannourakis 4.67 HOLD 5.25 714 22.6 24.5 20.6 19.1 9.0 10.6 1.9 2.3

Patties Foods Ltd PFL Josh Kannourakis 1.18 HOLD 1.25 164 11.0 11.8 10.7 10.0 5.0 6.5 4.2 5.5

Select Harvests SHV Josh Kannourakis 10.66 HOLD 12.70 766 84.8 87.4 12.6 12.2 55.0 45.0 5.2 4.2

Health Care

1300 Smiles ONT Nick Caley 7.17 BUY 7.80 170 27.8 33.2 25.8 21.6 19.2 21.5 2.7 3.0

Greencross Ltd GXL Josh Kannourakis 6.52 BUY 8.80 751 34.3 39.4 19.0 16.5 17.0 20.0 2.6 3.1

Medibio Ltd MEB Nicolas Burgess 0.40 BUY 0.56 30 -15.5 -1.3 0.0 0.0 0.0 0.0 0.0 0.0

Pacific Smiles Group PSQ Nick Caley 2.15 HOLD 2.55 327 5.7 7.0 32.3 30.5 6.6 6.0 3.1 2.8

Rhinomed RNO Josh Kannourakis 0.03 BUY 0.06 17 -1.1 -0.2 0.0 0.0 0.0 0.0 0.0 0.0

Financials

Austbrokers Holdings Ltd AUB Nicolas Burgess 8.80 BUY 9.60 548 59.1 60.6 14.9 14.5 39.7 40.0 4.5 4.5

Auswide Bank ABA Nick Caley 5.32 BUY 6.40 197 36.0 41.0 14.8 13.0 30.0 34.0 5.6 6.4

Bentham IMF IMF Nick Caley 1.53 BUY 2.25 256 3.8 24.1 40.1 6.3 10.0 13.0 6.6 8.5

BT Investment Management Ltd BTT Nicolas Burgess 9.80 BUY 11.50 2855 45.4 56.1 21.6 17.5 37.0 45.0 3.8 4.6

Emerchants EML Nick Caley 0.75 BUY 1.20 142 1.7 0.9 43.8 82.8 0.0 0.0 0.0 0.0

Equity Trustees Ltd EQT Nicolas Burgess 22.38 BUY 26.00 437 109.0 126.1 20.5 17.7 94.0 107.0 4.2 4.8

Henderson Group HGG Nicolas Burgess 5.65 BUY 7.00 6424 17.4 19.9 15.3 13.4 23.5 26.7 4.2 4.7

IOOF Holdings Ltd IFL Nicolas Burgess 8.94 HOLD 9.50 2629 59.4 62.4 15.1 14.3 53.0 56.0 5.9 6.3

Mortgage Choice Ltd MOC Nick Caley 1.69 HOLD 2.35 209 15.0 16.6 11.2 10.2 15.5 16.5 9.2 9.8

MyState Ltd MYS Nick Caley 4.35 BUY 5.20 380 37.3 36.8 11.7 11.8 28.5 30.5 6.6 7.0

Perpetual Ltd PPT Nicolas Burgess 42.60 HOLD 47.00 1905 283.1 291.5 15.0 14.6 240.0 248.0 5.6 5.8

Steadfast Group SDF Nicolas Burgess 1.48 BUY 1.80 1093 9.8 11.1 15.2 13.3 5.0 6.1 3.4 4.1

Information Technology

Aconex ACX Luke Macnab 4.57 BUY 4.81 765 -7.0 5.5 0.0 83.1 0.0 0.0 0.0 0.0

Altium ALU Nicolas Burgess 4.44 BUY 4.70 572 12.3 14.4 24.9 21.3 16.0 17.8 3.6 4.0

Catapult Group CAT Nicolas Burgess 1.47 HOLD 1.40 177 -2.0 0.5 0.0 294.0 0.0 0.0 0.0 0.0

Computershare Ltd CPU Nicolas Burgess 10.62 HOLD 11.00 5916 59.7 55.1 12.3 13.3 31.0 36.7 2.9 3.5

DTI Group DTI Nick Caley 0.26 BUY 0.60 24 0.1 3.3 185.0 7.8 0.0 0.0 0.0 0.0

Empired EPD Josh Kannourakis 0.85 BUY 1.20 99 4.8 8.1 17.7 10.6 0.0 2.0 0.0 2.4

GBST Holdings GBT Nicolas Burgess 3.81 HOLD 3.90 243 28.3 22.4 13.5 17.0 10.5 9.0 2.8 2.4

Hansen Technologies HSN Nicolas Burgess 2.90 BUY 3.00 498 11.4 13.4 25.4 21.6 6.0 6.6 2.1 2.3

Infomedia IFM Nicolas Burgess 0.78 BUY 1.20 243 4.3 4.7 18.1 16.6 3.9 4.0 5.0 5.1

IProperty Group Ltd IPP Nick Caley 3.41 BUY 3.60 668 0.9 5.5 378.9 62.0 0.0 0.0 0.0 0.0

Legend Corporation LGD Nicolas Burgess 0.26 HOLD 0.28 57 3.1 3.2 8.4 8.1 1.8 1.8 6.7 6.7

Mitula Group MUA Josh Kannourakis 0.96 BUY 1.20 197 3.9 5.8 24.7 16.6 0.0 0.0 0.0 0.0

Smart Parking SPZ Nick Caley 0.15 BUY 0.25 42 -1.8 0.5 0.0 29.0 0.0 0.0 0.0 0.0

Telecommunication Services

BigAir Group BGL Luke Macnab 0.89 BUY 0.99 156 3.9 6.1 22.7 14.5 1.2 1.7 1.4 1.9

M2 Group MTU Luke Macnab 9.50 BUY 10.88 1727 54.3 65.9 17.5 14.4 32.0 37.0 3.4 3.9

SpeedCast International SDA Luke Macnab 4.55 BUY 5.01 549 13.8 17.6 24.3 18.6 7.5 11.0 1.6 2.4

Vocus Communications VOC Luke Macnab 6.33 BUY 6.69 1458 17.7 28.5 35.8 22.2 8.3 8.5 1.3 1.3

Materials

Hillgrove Resources HGO Warren Edney 0.20 BUY 0.42 38 -2.9 -1.3 0.0 0.0 0.0 0.0 0.0 0.0

Northern Star NST Warren Edney 3.09 BUY 3.57 1890 15.5 29.1 19.9 10.6 5.0 9.0 1.6 2.9

Panoramic Resources PAN Warren Edney 0.35 HOLD 0.33 112 -11.5 -8.2 0.0 0.0 1.0 0.0 2.9 0.0

Saracen Mineral Holdings SAR Warren Edney 0.58 BUY 0.64 464 1.4 4.1 40.9 13.9 0.0 0.0 0.0 0.0

Silver Lake Resource SLR Warren Edney 0.25 BUY 0.24 123 -18.7 2.3 0.0 10.7 0.0 0.0 0.0 0.0

Page 2

BAILLIEU HOLST RESEARCH Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Table of Contents

Coverage universe 2

Equity market view and strategy 5

Top Stock Picks:

Donaco International (DNA) 11

Empired (EPD) 14

Henderson Group (HGG) 18

M2 Group (MTU) 22

Mantra Group (MTR) 25

Northern Star (NST) 29

QMS Media (QMS) 33

Saracen Minerals (SAR) 36

Shine Corporate (SHJ) 41

Speedcast International (SDA) 44

Steadfast Group (SDF) 48

Vita Group (VTG) 53

Listed Investment Companies (LICs) 56

Baillieu Holst Research Team 58

Disclaimer 60

Page 3

This page has been left blank intentionally

Page 4

BAILLIEU HOLST QUANT RESEARCH

Top Stock Picks – October 2015 INTERNAL ONLY

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RESEARCH ANALYST

Mathan Somasundaram

+612 9250 8947 [email protected]

Equity Engineer – October 2015

EQUITY STRATEGY

Christmas rally to start after US reporting season profit taking

Global market outlook: Declining global growth has sparked a currency war amongst major economies in a bid for a bigger slice of the shrinking growth pie. Markets are getting used to a slowing China, stabilising Euro, risky Japan and a slowing US heading towards below trend growth. Global markets had a decent recovery in early October, while the US reporting season will continue to test recent optimism. The US Fed continues to support a rate rise in 2015, but the exact timing, magnitude and future moves are likely to be heavily linked to domestic economic recovery and global growth slowdown. We expect the US Fed to push back the rate rise timetable to allow for global economies to absorb and recover from the China slowdown and the Euro refugee issues. We continue to expect the Chinese government to deliver more stimulus and currency devaluation in order to improve manufacturing and domestic spending. We also assume small targeted stimulus in Japan, while substantial QE and refugee spending will be stimulatory for Europe. We continue to see low global growth outlook and a falling domestic currency to support our equity market recovery on the chase for yield.

Local market outlook: Equities will continue to benefit from global demand for better than bond yield income streams from the rising older global demographic. A tidal wave of unemployment, falling real wages, falling living standards, falling disposable income, and a government in survival mode are factors expected to see an ongoing decrease in local consumer sentiment and business capex. The mining boom to manufacturing doom has left Australia with asset bubbles that can’t be sustained without employment and wages growth. The big global consumer bases are the US, Europe and Asia. Global manufacturing will always gravitate towards big consumer bases and low cost regions. Manufacturing will only survive in Australia with government support due to the relative wage cost to FTA partners. Major regions in the currency war are delivering lower cost of production and cost to the market than what Australia can deliver. Australia will continue to attract recession fears as the country sleep walks past a low growth global economy in transition. Corporates are expected to protect their balance sheets, cut costs, buy back shares, drive industry consolidation and maintain yield to drive share price performance. We expect global investors to buy into Australian equity dividend yield as the currency sees support in the high 60s.

Market view: We maintain a bullish long term view on the Australian equity market with a 12 month index target level of 6100. The RBA move in February and May has enabled equities to become the preferred risk/return option for investors wanting better than bond yield return in a rising cost environment. Recent profit taking by global investors on currency worries has lowered the market to a fair value level of 5000 with no premium being paid for the substantially high dividend yield. We maintain our positive long term view on the yield trade (i.e. Banks, Div Financials and Telecommunication services) while health care looks the best growth/currency story. We continue to favour the new economy (i.e. MITCH Universe – Media, Information, Telecom, Consumer and Health) over the old economy on a long term view. We expect short term profit taking with US reporting season risk; while China releases long term growth plans and the US Fed pushes back rate rise plans to help drive markets higher for a Christmas rally.

quan

tstra

tegy

Page 5

BAILLIEU HOLST QUANT RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

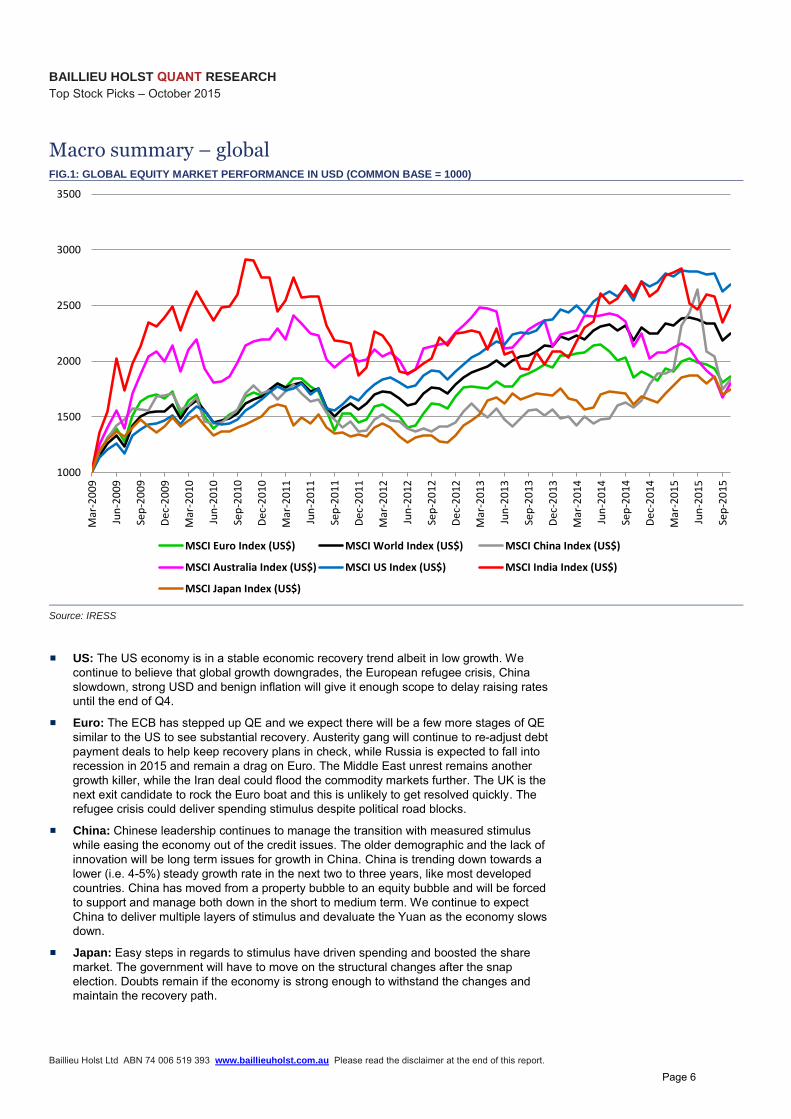

Macro summary – global FIG.1: GLOBAL EQUITY MARKET PERFORMANCE IN USD (COMMON BASE = 1000)

1000

1500

2000

2500

3000

3500

Mar-2009

Jun-2009

Sep-2009

Dec-2009

Mar-2010

Jun-2010

Sep-2010

Dec-2010

Mar-2011

Jun-2011

Sep-2011

Dec-2011

Mar-2012

Jun-2012

Sep-2012

Dec-2012

Mar-2013

Jun-2013

Sep-2013

Dec-2013

Mar-2014

Jun-2014

Sep-2014

Dec-2014

Mar-2015

Jun-2015

Sep-2015

MSCI Euro Index (US$) MSCI World Index (US$) MSCI China Index (US$)

MSCI Australia Index (US$) MSCI US Index (US$) MSCI India Index (US$)

MSCI Japan Index (US$)

Source: IRESS

US: The US economy is in a stable economic recovery trend albeit in low growth. We continue to believe that global growth downgrades, the European refugee crisis, China slowdown, strong USD and benign inflation will give it enough scope to delay raising rates until the end of Q4.

Euro: The ECB has stepped up QE and we expect there will be a few more stages of QE similar to the US to see substantial recovery. Austerity gang will continue to re-adjust debt payment deals to help keep recovery plans in check, while Russia is expected to fall into recession in 2015 and remain a drag on Euro. The Middle East unrest remains another growth killer, while the Iran deal could flood the commodity markets further. The UK is the next exit candidate to rock the Euro boat and this is unlikely to get resolved quickly. The refugee crisis could deliver spending stimulus despite political road blocks.

China: Chinese leadership continues to manage the transition with measured stimulus while easing the economy out of the credit issues. The older demographic and the lack of innovation will be long term issues for growth in China. China is trending down towards a lower (i.e. 4-5%) steady growth rate in the next two to three years, like most developed countries. China has moved from a property bubble to an equity bubble and will be forced to support and manage both down in the short to medium term. We continue to expect China to deliver multiple layers of stimulus and devaluate the Yuan as the economy slows down.

Japan: Easy steps in regards to stimulus have driven spending and boosted the share market. The government will have to move on the structural changes after the snap election. Doubts remain if the economy is strong enough to withstand the changes and maintain the recovery path.

Page 6

BAILLIEU HOLST QUANT RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

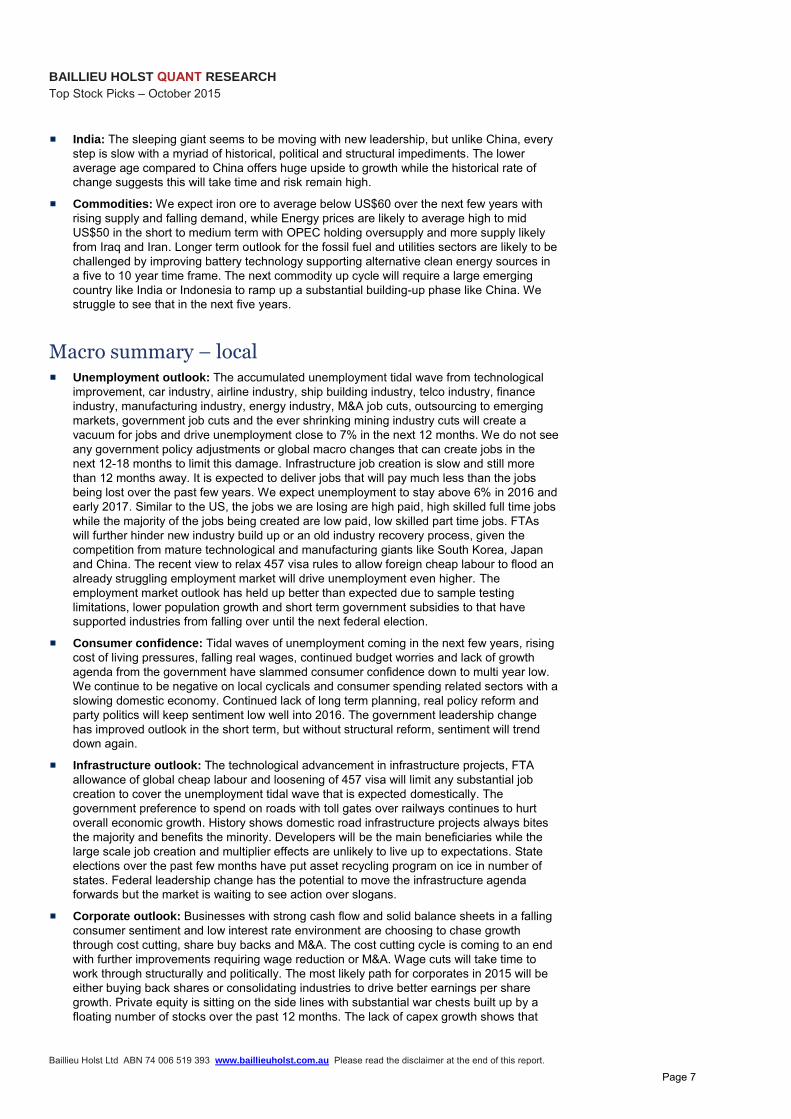

India: The sleeping giant seems to be moving with new leadership, but unlike China, every step is slow with a myriad of historical, political and structural impediments. The lower average age compared to China offers huge upside to growth while the historical rate of change suggests this will take time and risk remain high.

Commodities: We expect iron ore to average below US$60 over the next few years with rising supply and falling demand, while Energy prices are likely to average high to mid US$50 in the short to medium term with OPEC holding oversupply and more supply likely from Iraq and Iran. Longer term outlook for the fossil fuel and utilities sectors are likely to be challenged by improving battery technology supporting alternative clean energy sources in a five to 10 year time frame. The next commodity up cycle will require a large emerging country like India or Indonesia to ramp up a substantial building-up phase like China. We struggle to see that in the next five years.

Macro summary – local

Unemployment outlook: The accumulated unemployment tidal wave from technological improvement, car industry, airline industry, ship building industry, telco industry, finance industry, manufacturing industry, energy industry, M&A job cuts, outsourcing to emerging markets, government job cuts and the ever shrinking mining industry cuts will create a vacuum for jobs and drive unemployment close to 7% in the next 12 months. We do not see any government policy adjustments or global macro changes that can create jobs in the next 12-18 months to limit this damage. Infrastructure job creation is slow and still more than 12 months away. It is expected to deliver jobs that will pay much less than the jobs being lost over the past few years. We expect unemployment to stay above 6% in 2016 and early 2017. Similar to the US, the jobs we are losing are high paid, high skilled full time jobs while the majority of the jobs being created are low paid, low skilled part time jobs. FTAs will further hinder new industry build up or an old industry recovery process, given the competition from mature technological and manufacturing giants like South Korea, Japan and China. The recent view to relax 457 visa rules to allow foreign cheap labour to flood an already struggling employment market will drive unemployment even higher. The employment market outlook has held up better than expected due to sample testing limitations, lower population growth and short term government subsidies to that have supported industries from falling over until the next federal election.

Consumer confidence: Tidal waves of unemployment coming in the next few years, rising cost of living pressures, falling real wages, continued budget worries and lack of growth agenda from the government have slammed consumer confidence down to multi year low. We continue to be negative on local cyclicals and consumer spending related sectors with a slowing domestic economy. Continued lack of long term planning, real policy reform and party politics will keep sentiment low well into 2016. The government leadership change has improved outlook in the short term, but without structural reform, sentiment will trend down again.

Infrastructure outlook: The technological advancement in infrastructure projects, FTA allowance of global cheap labour and loosening of 457 visa will limit any substantial job creation to cover the unemployment tidal wave that is expected domestically. The government preference to spend on roads with toll gates over railways continues to hurt overall economic growth. History shows domestic road infrastructure projects always bites the majority and benefits the minority. Developers will be the main beneficiaries while the large scale job creation and multiplier effects are unlikely to live up to expectations. State elections over the past few months have put asset recycling program on ice in number of states. Federal leadership change has the potential to move the infrastructure agenda forwards but the market is waiting to see action over slogans.

Corporate outlook: Businesses with strong cash flow and solid balance sheets in a falling consumer sentiment and low interest rate environment are choosing to chase growth through cost cutting, share buy backs and M&A. The cost cutting cycle is coming to an end with further improvements requiring wage reduction or M&A. Wage cuts will take time to work through structurally and politically. The most likely path for corporates in 2015 will be either buying back shares or consolidating industries to drive better earnings per share growth. Private equity is sitting on the side lines with substantial war chests built up by a floating number of stocks over the past 12 months. The lack of capex growth shows that

Page 7

BAILLIEU HOLST QUANT RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

corporates are not planning to increase employment substantially in the next year to buffer the rising unemployment.

Property prices: We continue to expect areas of substantial unemployment, concentrated middle to low income earners and over-supplied high density dwellings will experience property price decline in the next 6-12 month time frame. The top end should continue to rise with overseas investors from Europe and Asia continuing to look at Australia as a safer location to park wealth at low currency despite housing bubble worries. Recent housing finance data is beginning to show signs of affordability and consumer confidence taking effect. In a longer term thematic, we expect future generations to prefer renting than buying property and also choosing apartment living to houses. Oversupply of units being built in major cities in the next 12-18 months will drive down unit prices and force the new home buyers with middle to low incomes to high density living due to the unaffordability of stand-alone house prices. We likely expect the London/UK property price paradigm to come to Sydney and Melbourne. We expect inner suburbs in major cities like Melbourne and Sydney to support stretched house prices with China inflow, while the outer suburbs will suffer with affordability and unemployment worries. Rising unemployment, falling real wages, rising costs and an oversupply of units are headwinds the RBA can’t avoid whilst stimulating the economy, but they can buffer the risk to banks. The real structural solution is to limit negative gearing to new dwellings only or limiting number of negative geared properties to take the heat off low income and first home buyers.

Taxation outlook: Due to the current fiscal policy of the government, we expect overall taxation to increase in the next few years to cater to falling tax revenue at federal and state levels. The structural decline in the budget has not been addressed as it is mainly a revenue problem. The current policy solutions are no more than nipping at the edges with minor spending cuts. The federal government has started to talk changes to the federation to clear the path for a GST rise. The majority of the balanced views would suggest some form of income tax cut to balance out the effects on low incomes. Given the track record of the budget in the last 12 months, the public is unlikely to support the GST hike without details. The $80b cuts to education and health will starve the states into doing a deal with the federal government on tax changes. Recent history does not hold well for middle to low income earners and consumer sentiment as a whole. Federal government backflips alongside leadership challenges do not offer us any confidence and we are likely to endure an ineffectual government until the 2016 election.

Currency outlook: We maintain our view that AUDUSD will track down to mid-60s in the medium term with global growth worries, a sliding domestic economy, domestic government inaction, RBA rate cuts and commodity price falls. US rate rise risk, China downgrades, China devaluating the Yuan, emerging market risks and falling commodities will help the devaluation. Substantial rate rise outlook for US or substantial devaluation of the Yuan can move the AUDUSD towards low 60’s to high 50s as it overshoots.

Interest rate outlook: We expect another 50 bps cut in the next 12 months to support the sliding economy. We see very little chance of any rate rise until late 2017. The RBA has made it clear that they also now see the risk to growth and unemployment and want to keep the currency and interest rates low. The surprise rate cut in February and expected rate cut in May have been proven to be wasted cuts on all fronts due to bigger global macro factors in play. The RBA is likely to stay unchanged until US Fed moves.

Page 8

BAILLIEU HOLST QUANT RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Market (S&P 300) FIG.2: INDEX WITH PE BANDS FIG.3: INDEX WITH PB BANDS

1000

2000

3000

4000

5000

6000

7000

8000

9000

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

FIG.4: EARNINGS YIELD TO BOND YIELD GAP AND INDEX FIG.5: DIV YIELD AND BOND YIELD

500

1500

2500

3500

4500

5500

6500

7500

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Earnings Yield to Bond Yiled Gap (%) - LHS Price Index - RHS

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Forward Dividend Yield 10Year Bond Yield Average DY Average BY

FIG.6: EARNINGS GROWTH FIG.7: ROE

0.00

5.00

10.00

15.00

20.00

25.00

30.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

FIG.8: PE FIG.9: EARNINGS REVISION AND PRICE MOMENTUM

7.00

9.00

11.00

13.00

15.00

17.00

19.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

3mth Avg Earnings Revision 3mth Price Momentum

Source: ASX, Baillieu Holst, Bloomberg, IRESS, Thomson Source: ASX, Baillieu Holst, Bloomberg, IRESS, Thomson

Page 9

This page has been left blank intentionally

Page 10

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015 INTERNAL ONLY

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RECOMMENDATIONS

Rating BUY ▲

Risk High Price Target $1.15

Share Price $0.80 SNAPSHOT Monthly Turnover $14.8mn Market Cap $636mn Shares Issued 831.2mn 52-Week High $0.99 52-Week Low $0.54 Sector Consumer Discretionary BUSINESS DESCRIPTION

Donaco International Limited (DNA) owns and operates the Aristo International Hotel & Casino in Lao Cao in northern Vietnam.

12-MONTH PRICE & VOLUME

RESEARCH ANALYST

Nick Caley

+ 613 9602 9283 [email protected]

Nicolas Burgess, CFA

+ 613 9602 9379 [email protected]

Josh Kannourakis

+ 613 9602 9265 [email protected] Disclosure The author owns no shares in DNA.

Donaco International (DNA)

COMPANY REPORT

Looking to chip in History: In 2012 Donaco International (DNA) listed on the ASX through a

back door listing after its assets were acquired by the former ASX listed, Two Way Ltd. As a result of the listing the majority shareholders of DNA became Lim, Keong Yew and Lim, Keong Hoe (the grandsons of the late Tan Sri Lim Goh Tong, who was also the founder of the Genting).

The business: DNA has two principal assets: 1) a 95% stake in the Aristo Hotel and Casino in Lao Cai Vietnam on the Chinese border which opened in 2014 after replacing a more dated asset in the same town; and 2) 100% ownership of the Star Vegas Resort and Club located in Poipet Cambodia on the border of Thailand – the asset was acquired in mid-2015 and will account for over 70% of group revenue from FY16.

Investment attractions: 1) recent trading data from Aristo in Vietnam suggests that DNA is not suffering from the same downturn as the Macau market; 2) the acquisition of Star Vegas in Cambodia is transformational given its scale; 3) Star Vegas is well established, profitable and is of high quality as confirmed by a site visit; 4) DNA is well credentialed in border style gaming and the use of junket operators – Star Vegas recently signed a major deal with junket operator Heng Sheng; 5) acquisition significantly reduces the reliance upon Chinese patronage which has been problematic due to travel warnings and anti-corruption crackdowns; 6) Star Vegas has capacity for more gaming tables and has a high percentage of more stable revenue streams from slot machines; and 7) very strong cash generation.

Key risks: Risks are clearly political in terms of: 1) the licencing and taxation arrangements of both properties remain at the discretion of respective Governments; 2) the DNA model relies upon good relationships between bordering countries; and 3) gambling remaining illegal in mainland China and Thailand.

Investment view: BUY call with a price target of A$1.15. The DNA share price remains weak (single digit FY16 P/E based on our forecasts and consensus) which we attribute to: 1) the global de-rating of casino stocks that are exposed to Chinese patronage; 2) the protracted time in which it has taken DNA to undertake an acquisition after first raising capital in March 2014; and 3) the market’s general lack of familiarity with the

Cambodian casino market – we view these factors as an opportunity for investors where the returns greatly outweigh the risks in our view.

Valuation: Our DCF valuation of A$1.16 is based upon: 1) risk discount rate of 13%; 2) terminal growth rate of 4%; 3) long-term revenue growth of 10% per annum; and 4) long-term EBITDA margin of 65%.

INVESTMENT SUMMARY

Year End: 30 June 2014 (A) 2015 (A) 2016 (E) 2017 (E) 2018 (E)

Revenue $mn 21 33 161 181 202 EBITDA $mn 9.8 13.7 102.2 116.4 129.5 EBIT $mn 9.5 8.9 95.8 109.2 121.4 Reported Profit $mn 6.8 -2.9 58.8 66.9 75.3 Adjusted Profit $mn 7.6 7.5 71.9 81.6 91.4 EPS (Reported) ¢ 2.2 -0.5 6.9 7.8 8.8 EPS (Adjusted) ¢ 2.4 1.3 8.4 9.6 10.7 EPS Growth % 24.3 -44.5 N/A 13.6 12.0 PER (Reported) x 36.8 N/A 11.5 10.1 9.0 PER (Adjusted) x 33.1 59.6 9.4 8.3 7.4 Dividend ¢ 0.0 0.0 0.0 0.0 0.0 Yield % 0.0 0.0 0.0 0.0 0.0 Franking % 0 0 0 0 0

Page 11

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Financial summary Donaco International Ltd

Analyst: Rating: BUY

Date: Price Target:

Share Price ($A): Valuation:

Year End: 30 June Upside/(Downside):

Mkt Cap $636m Risk:

NORM PROFIT & LOSS (A$mn) FY14A FY15A FY16E FY17E FY18E EARNINGS FY14A FY15A FY16E FY17E FY18E

Operating Revenue 20.3 30.8 157.5 176.9 196.9 EPS - Reported 2.2 -0.5 6.9 7.8 8.8Other Revenue 0.1 0.0 0.0 0.0 0.0 EPS - Normalised 2.4 1.3 8.4 9.6 10.7Interest Revenue 1.0 2.0 3.6 4.2 5.0 EPS Growth (%) 24% -44% 531% 14% 12%Total Revenue 21.5 32.8 161.1 181.1 201.9 DPS 0.0 0.0 0.0 0.0 0.0Cost of Goods Sold 1.3 2.2 16.1 18.1 20.2 Franking (%) 0 0 0 0 0Gross Profit 20.2 30.6 145.0 163.0 181.7 Payout Ratio (%) 0% 0% 0% 0% 0%Operating Expenses 7.9 14.4 33.8 36.2 40.4 VALUATION FY14A FY15A FY16E FY17E FY18E

Casino Minority Interests 1.4 0.5 5.4 6.1 6.8 P/E (x) 33.1 59.6 9.4 8.3 7.4EBITDA 9.8 13.7 102.2 116.4 129.5 EV/EBIT (x) 34.5 48.4 6.6 4.9 3.6Depreciation & Amortisation 0.3 4.9 6.4 7.2 8.1 EV/EBITDA (x) 33.5 31.3 6.1 4.6 3.4EBIT 9.5 8.9 95.8 109.2 121.4 Dividend Yield (%) 0.0% 0.0% 0.0% 0.0% 0.0%Net Interest Expense -1.0 -0.4 -0.1 0.3 -0.5 Price/Book (x) 2.5 2.4 1.9 1.5 1.2Net Profit Before Tax 10.6 9.2 95.9 108.8 121.9 Price/NTA (x) 2.6 2.4 3.1 2.2 1.7Income Tax Expense 3.1 2.7 24.0 27.2 30.5 Price/Cash/Flow per Share (x) 25.8 52.9 8.1 7.1 6.4R & D Tax Offset 0.0 1.1 0.0 0.0 0.0 GROWTH FY14A FY15A FY16E FY17E FY18E

Net Profit After Tax - Norm. 7.6 7.5 71.9 81.6 91.4 Op. Rev. Growth (% pcp) 30% 51% 412% 12% 11%Star Vegas Vendor Guarantee 0.0 0.0 13.0 14.7 16.1 Cash Op. Exp. Growth (% pcp) 39% 83% 135% 7% 11%Casino Win Rate Adjustment -0.8 -10.5 0.0 0.0 0.0 EBITDA Growth (% pcp) 41% 40% 645% 14% 11%Net Profit After Tax - Reported 6.8 -2.9 58.8 66.9 75.3 EBIT Growth (% pcp) 42% -7% 980% 14% 11%

NPBT Growth (% pcp) 30% -13% 939% 14% 12%BALANCE SHEET (A$mn) FY14A FY15A FY16E FY17E FY18E NPAT Growth (% pcp) 37% 0% 853% 14% 12%Assets MARGINS & RETURNS FY14A FY15A FY16E FY17E FY18E

Cash 98.0 210.2 184.2 273.9 374.3 Gross Profit Margin % 94% 93% 90% 90% 90%Receivables 0.8 2.1 2.1 2.1 2.1 EBITDA Margin (%) 46% 42% 63% 64% 64%Inventories 1.4 0.7 0.7 0.7 0.7 EBIT Margin (%) 44% 27% 59% 60% 60%Short Term Investments 0.0 0.0 0.0 0.0 0.0 NPBT Margin (%) 50% 28% 59% 60% 60%Other 26.8 12.2 12.2 12.2 12.2 ROIC (%) 9% 4% 35% 32% 26%Total Current Assets 127.0 225.1 199.1 288.8 389.2 ROE (%) 8% 4% 23% 20% 19%Property, Plant & Equipment 4.9 82.1 180.3 178.4 176.2 ROA (%) 6% 3% 16% 14% 14%Construction In Progress 39.2 0.2 0.2 0.2 0.2 Effective Tax Rate (%) 29% 30% 25% 25% 25%Intangibles 9.8 2.4 142.4 142.4 142.4 GEARING FY14A FY15A FY16E FY17E FY18E

Other 1.1 0.5 0.5 0.5 0.5 Net Debt (A$mn) -86 -194 -33 -123 -223Total Non Current Assets 54.9 85.2 323.5 321.6 319.4 Net Debt/Equity (%) -58% -70% -9% -28% -41%Total Assets 181.9 310.3 522.6 610.3 708.6 Int. Cover (x) - EBITDA/Net Int. -9.7 -38.5 -1325.7 347.1 -278.7Liabilities 0.0 0.0 0.0 0.0 0.0 Segmental FY14A FY15A FY16E FY17E FY18E

Payables 12.6 16.0 16.0 16.0 16.0 Revenue

Loans & Borrowings 1.4 3.0 3.0 3.0 3.0 Aristo 20.3 30.8 47.8 55.0 63.3Current Tax 4.9 0.4 0.4 0.4 0.4 Star Vegas 0.0 92.7 109.7 121.9 133.6Provisions 3.1 0.3 0.3 0.3 0.3 Other Revenue 0.1 0.0 0.0 0.0 0.0Total Current Liabilities 22.0 19.7 19.7 19.7 19.7 Interest Revenue 1.0 2.0 3.6 4.2 5.0Loans & Borrowings 10.6 13.2 148.2 148.2 148.2 Total Revenue 21.5 125.5 161.1 181.1 201.9

Provisions 0.0 0.0 0.0 0.0 0.0Total Non Current Laibilities 10.6 13.2 148.2 148.2 148.2

Total Liabilities 32.6 32.9 167.9 167.9 167.9

Contributed Capital 130.0 246.7 246.7 246.7 246.7Reserves -0.5 15.8 15.8 15.8 15.8Retained Earnings 18.7 13.9 85.8 167.4 258.8Minority Interests 1.1 1.0 6.4 12.5 19.3Total Equity 149.2 277.4 354.6 442.4 540.6

CASH FLOW (A$mn) FY14A FY15A FY16E FY17E FY18E

Cash at Start 29.4 99.5 210.2 184.2 273.9

Cash Flow from Ops 9.7 8.5 83.7 95.0 106.3Cash Flow From Investing -41.3 -32.0 -244.7 -5.3 -5.9Cash Flow From Financing 102.3 127.0 135.0 0.0 0.0

Net Cash Flow 70.7 103.6 -26.0 89.7 100.4Cash At End 99.5 210.2 184.2 273.9 374.3

$1.1644.7%

Nick Caley

$0.8019-October-2015

High

$1.15

Page 12

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

FIG.1: STAR VEGAS RESORT & CLUB

Source: DNA

FIG.2: ARISTO INTERNATIONAL HOTEL

Source: DNA

Page 13

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RECOMMENDATIONS

Rating BUY ▲

Risk High Price Target $1.20

Share Price $0.85 SNAPSHOT Monthly Turnover $4.2mn Market Cap $99mn Shares Issued 116.9mn 52-Week High $0.89 52-Week Low $0.58 Sector Information Technology BUSINESS DESCRIPTION EPD is an IT services provider with a diverse range of capabilities aimed at delivering complete (end-to-end) IT solutions for clients in order for them to reach their business objectives.

12-MONTH PRICE & VOLUME

RESEARCH ANALYST

Josh Kannourakis

+ 613 9602 9265 [email protected]

Nicolas Burgess, CFA

+ 613 9602 9379 [email protected]

Nick Caley

+ 613 9602 9283 [email protected] Disclosure The author owns no shares in EPD.

Empired (EPD)

COMPANY REPORT

Rise of the Empired

Investment view: We believe EPD is undervalued in light of its strong growth outlook, high proportion of contracted revenue, positive industry tail-winds driven by market trends and track record of execution. On a relative basis, EPD is trading at substantial discounts to listed peers and we expect this valuation gap to narrow over time. We have a BUY recommendation with a $1.20 price target.

High growth stock: We expect EPD to continue its growth momentum with FY15A to FY18F sales, EBITDA and NPAT CAGRs of 18%, 29% and 37% respectively. Growth will be underpinned by consolidating and extracting value from its recent acquisitions as well as capitalising on positive industry trends which are strongly aligned to EPD’s offering.

High proportion of contracted revenue: EPD has guided to FY16F revenue in the range of $155m to $175m, up 21% to 36% on the pcp. (Our estimate is $165m). Approximately 67% of this estimate is already covered by contracted infrastructure and application managed services, contracted project work and other work in hand. 50% of EPD’s FY16F revenue is on multi-year managed service or project contracts. These contracts have an average weighted contract length of four years.

Positive industry trends: We observe positive industry tail-winds and data supporting the IT services market. This is driven by companies modernizing or replacing older business systems with cloud-based software-as-a-service (SaaS). We expect this trend to support growth across EPD’s core capabilities in cloud services, application development and integration (incl. ERP, CRM and ECM), data analytics, internet of things and mobility solutions for enterprise. We also observe indications of a cyclical upswing, including growth in IT Professional vacancies (a proxy for labour demand) and material earnings revisions from listed peers.

Valuation and price target: Our blended valuation and price target is $1.20 ($1.19 DCF, $1.22 EV/EBITDA), using a blended EV/EBITDA (10% discount to market and comparable peers) and DCF methodology.

Key investment risks: The key risks to our investment thesis and price target include: 1) contract execution with regard to delivery and quality of work and contract renewal risks from counterparties; 2) loss of key personnel within particular business segments; 3) acquisitions not delivering expected returns; and 4) downturn in economic conditions restricting capital allocated to IT spend.

INVESTMENT SUMMARY

Year End: 30 June 2014 (A) 2015 (A) 2016 (E) 2017 (E) 2018 (E)

Revenue $mn 67 128 165 190 210 EBITDA $mn 7.0 11.2 18.1 21.4 24.0 EBIT $mn 5.0 7.3 13.7 16.3 18.7 Reported Profit $mn 3.8 5.3 9.4 11.5 13.7 Adjusted Profit $mn 3.8 5.2 9.4 11.5 13.7 EPS (Reported) ¢ 4.3 4.8 8.1 9.9 11.7 EPS (Adjusted) ¢ 4.3 4.8 8.1 9.9 11.7 EPS Growth % 92.9 11.8 69.2 22.9 18.5 PER (Reported) x 20.0 17.7 10.6 8.6 7.2 PER (Adjusted) x 20.0 17.9 10.6 8.6 7.2 Dividend ¢ 1.0 0.0 2.0 3.0 4.0 Yield % 1.2 0.0 2.4 3.5 4.7 Franking % 100 100 100 100 100

Page 14

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Financial summary Empired

Code: EPD Rating: BUYAnalyst: Josh Kannourakis Price Target: $1.20Date: Upside/downside: 41.7%Share Price: Valuation: $1.20Market Capitalisation: $99m Valuation method:Year End: Risk: HighPROFIT & LOSS (A$m) FY14A FY15A FY16E FY17E FY18E EARNINGS FY14A FY15A FY16E FY17E FY18E

Revenue 68.8 128.3 165.0 190.0 210.0 EPS - Underling cash (diluted) 4.3 4.8 8.1 9.9 11.7Operating costs 45.8 84.1 108.1 124.2 136.9 EPS Growth - underlying 92.9% 12.7% 67.9% 22.9% 18.5%Gross profit 21.0 44.2 56.9 65.8 73.1 EPS - Reported (diluted) 4.3 4.8 8.1 9.9 11.7Other income 2.0 1.7 0.0 0.0 0.0 Diluted shares (m) 89.1 109.9 116.6 116.6 116.6Corporate costs 16.0 34.8 38.8 44.4 49.1 DPS (cps) 1 0.0 2.0 3.0 4.0EBITDA 7.0 11.2 18.1 21.4 24.0 Payout Ratio 23.5% 0.0% 24.8% 30.3% 34.1%Depreciation & Amortisation -2.0 -3.9 -4.4 -5.1 -5.3 Franking 100% 100% 100% 100% 100%Impairment 0.0 0.0 0.0 0.0 0.0EBIT 5.0 7.3 13.7 16.3 18.7 VALUATION FY14A FY15A FY16E FY17E FY18E

Net interest -0.7 -1.3 -1.2 -0.9 -0.4 Underlying cash P/E (x) 20.0 17.7 10.6 8.6 7.2NPBT 4.3 6.0 12.5 15.4 18.2 PEG 0.21 1.40 0.16 0.37 0.39Tax -0.5 -0.7 -3.1 -3.8 -4.6 Price/FCF -77.0 -14.5 11.5 11.8 7.5Minorities 0.0 0.0 0.0 0.0 0.0 EV/EBITDA (x) 15.0 10.0 6.1 5.2 4.3Reported NPAT 3.8 5.3 9.4 11.5 13.7 EV/EBIT (x) 21.0 15.3 8.1 6.8 5.5

Dividend Yield (%) 1.2% 0.0% 2.4% 3.5% 4.7%Non-recurring items (net tax) 0.0 0.0 0.0 0.0 0.0 Price/Book (x) 2.2 1.8 1.7 1.5 1.3Underlying cash profit 3.8 5.2 9.4 11.5 13.7 Price/NTA (x) 11.4 22.8 8.6 5.0 3.4

BALANCE SHEET (A$m) FY14A FY15A FY16E FY17E FY18E GROWTH FY14A FY15A FY16E FY17E FY18E

Assets Revenue growth 48.0% 86.5% 28.6% 15.2% 10.5%Cash 8.1 9.6 6.4 4.8 9.4 Operating cost growth 36.5% 83.6% 28.5% 14.9% 10.2%Receivables 11.1 26.8 32.2 39.9 44.1 EBITDA growth 94.5% 59.5% 62.4% 17.8% 12.3%PPE 12.8 22.3 25.1 25.7 26.1 PBT growth 118.6% 39.0% 108.3% 22.9% 18.5%Intangibles 27.8 48.6 48.3 48.0 47.7 Underlying NPAT growth 144.8% 37.9% 79.5% 22.9% 18.5%Other assets 6.3 14.1 14.1 14.1 14.1 Reported NPAT growth 144.8% 39.0% 78.1% 22.9% 18.5%Total Assets 66.0 121.4 126.0 132.5 141.4 MARGINS & RETURNS FY14A FY15A FY16E FY17E FY18E

Liabilities Gross profit margin 30.5% 34.5% 34.5% 34.6% 34.8%Payables 12.4 24.9 32.0 36.9 40.8 EBITDA Margin 10.2% 8.7% 11.0% 11.3% 11.4%Finanical liabilities 14.0 22.3 18.3 17.3 13.3 EBIT Margin 7.3% 5.7% 8.3% 8.6% 8.9%Provisions 2.4 5.0 5.0 5.0 5.0 NPBT Margin 6.3% 4.7% 7.6% 8.1% 8.7%Tax liabilities 2.8 4.5 4.5 4.5 4.5 ROIC 14.8% 12.1% 15.0% 16.1% 17.4%Other liabilities 0.0 12.0 6.4 0.9 0.9 ROE 15.3% 12.0% 16.7% 18.1% 18.9%Total Liabilities 31.6 68.7 66.2 64.6 64.5 ROA 10.3% 7.8% 11.1% 12.6% 13.6%Equity Effective Tax Rate 12.3% 12.3% 25.0% 25.0% 25.0%Share capital 24.4 37.8 37.8 37.8 37.8 GEARING FY14A FY15A FY16E FY17E FY18E

Retained earnings 9.4 13.6 20.7 28.7 37.8 Net Debt / (cash) (A$m) 6.0 12.7 11.9 12.5 3.9Other equity 0.7 1.4 1.4 1.4 1.4 Enterprise value 105.1 111.8 111.1 111.6 103.0Total shareholders equity 34.5 52.7 59.8 67.9 77.0 Net Debt/Equity (%) 17.4% 24.1% 20.0% 18.4% 5.0%

EBITDA/Net interest 10.3 8.5 15.2 23.0 54.6BV per share (cps) 38.7 47.9 51.3 58.2 66.0 Net Debt/EBITDA 0.85 1.14 0.66 0.58 0.16NTA per share (cps) 7.5 3.7 9.9 17.1 25.1

Operational Data FY14A FY15A FY16E FY17E FY18E

CASH FLOW (A$M) FY14A FY15A FY16E FY17E FY18E Group Revenue 68.8 128.3 165.0 190.0 210.0

Cash at Start 2.1 8.1 9.6 6.4 4.8 Application Services 35.4 93.7 123.8 146.3 168.0Cash from from ops 5.3 5.0 15.5 13.7 18.7 Infrastructure Services 31.4 34.6 41.3 43.7 42.0Capex -6.3 -11.5 -6.9 -5.3 -5.5 Group Gross Profit 21.0 44.2 56.9 65.8 73.1

Free cash flow -1.0 -6.5 8.6 8.4 13.2 Application Services na 33.7 44.6 52.7 60.5Free cash flow per share (cps) -1.1 -5.9 7.4 7.2 11.4 Infrastructure Services na 10.5 12.4 13.1 12.6

Cash flow from investing -22.6 -23.1 -12.5 -10.8 -5.5 Group Gross Profit margin 31.4% 34.5% 34.5% 34.6% 34.8%

Cash flow from financing 23.3 19.8 -6.3 -4.5 -8.6 Application Services na 36.0% 36.0% 36.0% 36.0%Cash at end 8.1 9.6 6.4 4.8 9.4 Infrastructure Services na 30.3% 30.0% 30.0% 30.0%

19/10/2015$0.85

30-JuneDCF / EV/EBITDA

Page 15

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Investment overview

High proportion of contracted revenue and robust pipeline

Strong revenue guidance: EPD has guided to FY16 revenue in the range of $155m to $175m, up 21% to 36% on the pcp. We have adopted the mid-point of guidance, $165m. Around 67% of this estimate is already covered from contracted infrastructure and application managed services, project work related to managed contracts and other work in hand. Therefore, we are comfortable with this estimate despite it being declared at an early stage in the year.

Managed services and work in hand: EPD has ~50% of our FY16F revenue estimate contracted on multi-year managed service and application contracts. We estimate 70-75% of the contracted revenue base (or 35-37.5% of total revenue) is base contracted infrastructure and application managed services, with the remaining 25-30% being from contracted project specific work, generally for managed service clients. Additional work in hand for the beginning of FY16 was ~$30m, with almost all of this from existing clients.

FIG.1: EBITDA GROWTH: ACQUISITION VERSUS ORGANIC ESTIMATES

$60M

$20M

$30M

$55M $165M

0

50

100

150

200

250

Base contractedrevenue

Contracted project work Work in hand Work to be won FY16 Revenue

$M

Weighted average contract length of ~4 years

We assume a revenuepipeline conversion

rate of ~22%

Mid-point of

guidance

Source: Company Reports, Baillieu Holst forecasts

Project pipeline: The Company expects the tangible FY16 revenue pipeline to be ~$250m in FY16. We see this growing over coming years as EPD leverages its strength in Microsoft business solutions and its own “Cohesion” records management software (which is one of three on a panel to upgrade NZ government records management). We currently forecast a 22% conversion rate on the FY16 pipeline ($55m). However, we note historical conversion rates have been between 30% to 50%, albeit on a smaller pipeline of work. EPD has seen strong momentum in conversion rates on contested multi-year contracts. In 2H15, EPD won $65m of the $100m it contested in multi-year managed infrastructure and application services contracts.

Weighted average contract length: We understand ~$50m in long-term contracted revenue were renewed in FY15. Thus, the current weighted average contract length is approximately four years, the longest it has ever been.

Compares favourably to peers: We provide a snapshot of EPD’s comparable companies and their respective revenue analyses looking into contracted and managed services. ASG Group (ASZ) is more or less a pure managed services business and ranks highest in terms of managed services. EPD is clear second, with UXC and SMS Management and Technology (SMX) following in third and fourth respectively. Whilst EPD does deserve to trade at a discount due to its size; ASZ, SMX and UXC are trading on 36%, 57% and 73% EV/EBITDA premiums respectively. Different companies refer to these revenue streams with different wording so the analysis below may not be a completely accurate on a like for like basis. However, it does demonstrate the strength of EPD’s contracted revenue relative to its peers and its attractive valuation differential. We note larger players such as UXC and SMX have managed and contracted services (annuities) as a core strategic growth focus.

Page 16

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

FIG.2: COMPARISION OF CONTRACTED AND MANAGED SERVICES EPD ASZ UXC SMX

FY16 Revenue ($m) 165 180 722.6 356

Contracted Revenue 48% 89% Increasing -

Managed Services 36% 89% - Increasing

FY16 Revenue Growth 29% 10% 5.3% 4%

FY15 Revenue ($m) 128.3 163 686.4 314.4

Contracted Revenue 50% 85% 29% -

Managed Services 35% 85% - 10%

FY15 Revenue Growth 29% 3% 7.0% 13%

Mkt Cap ($m) 95.4 210.9 445.3 359.5

FY16 PE 10.6 14.6 17.1 16.6

FY16 EV/EBITDA 6.1 8.3 9.6 10.6

FY15 Net debt 12.7 11.4 -2.9 -7.5 Source: Company Reports, Baillieu Holst forecasts for EPD, Bloomberg consensus for other companies

Strong track record of earnings growth to continue

We expect EPD to continue its growth momentum with FY15A to FY18F sales, EBITDA and NPAT CAGRs of 18%, 29% and 37% respectively. Growth will be underpinned by consolidating and extracting value from its recent acquisitions as well as capitalising on positive industry trends (in IT spend) which are strongly aligned to EPD’s service offering.

Margin improvement: We expect EBITDA margin expansion of 230bps to drive an FY16F margin of 11.0% (8.7% pcp) and EBITDA growth of 62%. In FY14 EPD’s margins were 10.2%, however they declined in FY15 as the company digested the significant New Zealand based acquisition, Intergen (370 people, $60m revenue), and wore start-up costs for long-term managed contracts. We have only modelled in a modest increase in margins medium-term (FY15-FY18F) to reflect the acknowledgement that EPD has grown exceptionally fast. As with many service based businesses, it may see challenges in continuing to execute at the same level with a substantially higher headcount. Having said that, tailwinds are supportive of margin expansion with scale benefits post acquisitions as well as a higher proportion of application and consulting revenue (which the company expects to contribute 36% GMs versus 30% for infrastructure services). Thus margin risks are weighted to the upside, in our view.

FIG.3: SEGMENT REVENUE SPLIT

24%

53%

73% 75%

0%10%20%30%40%50%60%70%80%90%

100%

FY13 FY14 FY15 FY16F

Application and consulting services Infrastructure services Source: Company Reports, Baillieu Holst forecasts

Page 17

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015 INTERNAL ONLY

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RECOMMENDATIONS

Rating BUY ▲

Risk Medium Price Target $7.00

Share Price $5.65 SNAPSHOT Monthly Turnover $447.5mn Market Cap $3,513mn Shares Issued 629.5mn 52-Week High $6.26 52-Week Low $3.40 Sector Financials BUSINESS DESCRIPTION

Henderson Group (HGG) is an international, UK-based fund manager listed on the ASX and LSE. HGG provides investment management services throughout Europe, North America and Asia.

12-MONTH PRICE & VOLUME

RESEARCH ANALYST

Nicolas Burgess, CFA

+ 613 9602 9379 [email protected]

Nick Caley

+ 613 9602 9283 [email protected]

Josh Kannourakis

+ 613 9602 9265 [email protected] Disclosure The author owns no shares in HGG.

Henderson Group (HGG)

COMPANY REPORT

Top of the world

Overall: Recent equity market volatility provides an opportunity for investors to look again at HGG. In our view, the company remains well placed to benefit from global fund flows and ongoing declines in the AUD. It remains our key pick in the wealth management sector.

Key attractions: We view the key attractions of the HGG investment case as follows. Firstly, the company has a strong capital position, with surplus of £113m over regulatory requirements at 30 June, 2015. The company recently announced a £25m share buyback to be executed in 2H15. Although modest in size (this should reduce issued capital by around 0.8% by our estimates) it nonetheless signals confidence in the outlook. We believe capital management may be an ongoing theme for HGG. Secondly, HGG has an enviable distribution footprint across the key northern hemisphere markets, including the UK (~45% of management fees), Europe (~30% of management fees) and the US (~12% of management fees). This ensures fund flows are diversified across a variety of channels, asset classes and investment capabilities. Lastly, investment performance of flagship funds remains strong, with 83% of funds outperforming their respective benchmarks over three years (slightly less over one year at 76%).

Investment view: We have a BUY rating on the stock. We expect positive capital and fund flow trends to persist. Over the last three years, HGG has transformed its fund flow position from being net outflow to strong net inflow. The company reported fund flows worth 11% of FUM in FY14 and we expect 14% in FY15. As we show overleaf, industry conditions remains generally supportive on ongoing funds flows. Based on our forecasts, we view the price to growth metrics as compelling: FY15F PE of 15.3x offering two year EPS CAGR of 16.4% with a 4.1% dividend yield.

Price target and valuation: Our $7.00 valuation and price target is derived using a blended PE and DCF methodology in GBP, which is then translated into AUD. The assumptions in the DCF include a WACC of 9.7%, a risk free rate of 5.0%, an expected return on the market of 6.0%, a terminal growth rate of 3.0% and a beta of 1.2. For the PE, we value HGG in line with the market (forward PE of 15.5x).

Key risks: Equity market downside, unexpected interruption in fund flows, particularly in the US, UK and European markets, and a material deterioration of investment performance across key funds.

INVESTMENT SUMMARY

Year End: 31 December 2013 (A) 2014 (A) 2015 (E) 2016 (E) 2017 (E)

Revenue £mn 472 529 615 681 726 EBITDA £mn 179.8 204.1 241.6 271.9 298.4 EBIT £mn 176.6 199.4 236.6 266.9 293.4 Reported Profit £mn 125.1 258.5 146.9 185.5 213.5 Adjusted Profit £mn 147.6 167.2 193.4 224.5 243.5 EPS (Reported) ¢ 11.0 22.7 13.2 16.4 18.9 EPS (Adjusted) ¢ 13.0 14.7 17.4 19.9 21.5 EPS Growth % 31.1 13.0 18.4 14.4 8.5 PER (Reported) x 24.2 11.7 20.2 16.2 14.1 PER (Adjusted) x 20.5 18.1 15.3 13.4 12.3 Dividend A¢ 17.1 19.2 23.5 26.7 27.8 Yield % 3.0 3.4 4.2 4.7 4.9 Franking % 0 0 0 0 0

Page 18

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Financial summary Code: Rating: BUY

Analyst: Price Target: $7.00

Date: Upside/downside: 23.9%Share Price: Valuation: $7.00Market Capitalisation: Valuation method: DCF / PE blendYear End: Risk: MediumPROFIT & LOSS (GBPm) FY13A FY14A FY15E FY16E FY17E EARNINGS FY13A FY14A FY15E FY16E FY17E

Total fee income 461.3 518.8 595.0 671.4 716.0 EPS - Underling cash (diluted) 13.0 14.7 17.4 19.9 21.5Investment/interest income 12.0 15.2 21.0 11.0 11.0 EPS Growth - underlying 5.2% 13.0% 18.4% 14.4% 8.5%Total revenue 473.3 534.0 616.0 682.4 727.0 EPS - Reported (diluted) 11.0 22.7 13.2 16.4 18.9Operating expenses -293.5 -329.9 -374.4 -410.5 -428.7 Diluted shares (m) 1137 1140 1114 1130 1130Underlying EBITDA 179.8 204.1 241.6 271.9 298.4 DPS (pps) 8.0 9.0 11.0 12.5 13.0Depreciation -3.2 -4.7 -5.0 -5.0 -5.0 Payout Ratio 62% 61% 63% 63% 60%Underlying EBITA 176.6 199.4 236.6 266.9 293.4 Franking 0% 0% 0% 0% 0%Interest cost -11.1 -11.6 -11.7 -2.8 0.0 VALUATION FY13A FY14A FY15E FY16E FY17E

Underlying PBT 165.5 187.8 224.9 264.1 293.4 P/E (x) 20.5 18.1 15.3 13.4 12.3Tax -17.9 -20.6 -31.5 -39.6 -49.9 EV/EBITA (x) 16.7 14.7 12.3 10.8 9.6Minorities 0.0 0.0 0.0 0.0 0.0 EV/EBITDA (x) 16.4 14.4 12.0 10.6 9.5Underlying cash NPAT 147.6 167.2 193.4 224.5 243.5 Dividend Yield (%) 3.0% 3.4% 4.1% 4.7% 4.9%Amortisation -58.4 -53.7 -60 -50 -40 Price/Book (x) 3.6 3.0 2.8 2.7 2.6Non-recurring items (net tax) 35.9 145.0 13.5 11.0 10.0 Price/NTA (x) 15.3 8.9 6.7 5.6 4.7Reported profit 125.1 258.5 146.9 185.5 213.5 Price/FCF per Share (x) 17.6 25.0 23.9 19.5 15.2

GROWTH FY13A FY14A FY15E FY16E FY17E

BALANCE SHEET (GBPm) FY13A FY14A FY15E FY16E FY17E Revenue growth 24.2% 12.5% 14.7% 12.8% 6.7%Assets Operating cost growth 21.3% 12.4% 13.5% 9.6% 4.4%Cash 216.4 234.5 266.7 141.5 197.5 EBITDA growth 25.1% 13.5% 18.4% 12.6% 9.7%Receivables 217.1 275.9 261.8 302.1 329.4 EBITA growth 25.3% 12.9% 18.6% 12.8% 9.9%Other current assets 277.4 469.9 455.8 496.1 523.4 PBT growth 8.2% 13.5% 19.8% 17.4% 11.1%Fixed Assets 17.0 15.1 15.1 15.1 15.1 Underlying NPAT growth 10.6% 13.3% 15.7% 16.0% 8.5%Intangibles 637.9 677.9 617.9 567.9 527.9 Reported NPAT growth 17.6% 106.6% -43.2% 26.2% 15.1%Other non-current assets -67.9 -36.1 -22.0 -62.3 -89.6 MARGINS & RETURNS FY13A FY14A FY15E FY16E FY17E

Total Assets 1297.9 1637.2 1595.3 1460.4 1503.7 EBITDA Margin 39.0% 39.3% 40.6% 40.5% 41.7%Liabilities EBITA Margin 38.3% 38.4% 39.8% 39.8% 41.0%Debt 148.9 149.4 149.7 0.3 0.3 NPBT Margin 35.9% 36.2% 37.8% 39.3% 41.0%Payables 337.7 316.0 297.5 335.7 358.0 ROIC 19.4% 19.8% 20.8% 22.9% 24.2%Current tax liabilities 60.4 61.9 61.9 61.9 61.9 ROE 18.3% 18.1% 18.7% 20.8% 21.5%Provisions 17.6 12.8 12.8 12.8 12.8 ROA 12.7% 13.6% 14.6% 17.5% 19.8%Other liabilities -102.5 79.1 13.8 -54.0 -99.7 Effective Tax Rate 10.8% 11.0% 14.0% 15.0% 17.0%Total Liabilities 462.1 619.2 535.7 356.7 333.3 GEARING FY13A FY14A FY15E FY16E FY17E

Equity Net Debt / (cash) (GBPm) -67.5 -85.1 -117.0 -141.2 -197.2Share capital 140.4 142.4 161.5 161.5 161.5 Enterprise value (GBPm) 2957 2939 2907 2883 2827Retained earnings 47.8 216.4 238.9 283.0 349.6 Net Debt/Equity (%) -8.1% -8.4% -11.0% -12.8% -16.8%Other equity 647.6 659.2 659.2 659.2 659.2 EBITDA/Net interest -199.8 -56.7 -25.9 -33.3 -27.2Total shareholders equity 835.8 1018.0 1059.6 1103.7 1170.3 OPERATIONAL DATA FY13A FY14A FY15E FY16E FY17E

Group Fees 461.3 518.8 595.0 671.4 716.0

BV per share (pps) 73.5 89.3 95.1 97.7 103.5 Management fees 331.9 403.5 470.4 545.8 612.0NTA per share (pps) 17.4 29.8 39.6 47.4 56.8 Transaction fees 34.9 32.5 35.3 38.2 30.6

Performance fees 94.5 82.8 89.4 87.3 73.4CASH FLOW (GBPm) FY13A FY14A FY15E FY16E FY17E Management fees 331.9 403.5 470.4 545.8 612.0

Cash at start 196.9 216.4 234.5 266.7 141.5 Retail 257.2 315.5 379.8 442.9 503.6Cash flow from Ops 174.9 123.0 125.5 156.3 199.6 Institutional 79.5 83.7 90.6 103.0 108.4Capex -2.8 -1.6 -1.8 -1.9 -2.1Free cash flow 172.1 121.4 123.8 154.4 197.4 Flows 2.9 6.7 10.3 6.3 5.2

Free cash flow per share (pps) 15.1 10.7 11.1 13.7 17.5 Retail 4.4 6.8 8.3 5.6 5.2Cash flow from investing -44.5 0.8 39.7 -0.4 -0.6 Institutional -1.5 -0.1 2.1 0.7 0.0Cash flow from financing -93.3 -112.9 -133.1 -281.1 -143.0Cash at end 216.4 234.5 266.7 141.5 197.5 FUM 63.7 75.5 89.5 105.6 115.8

Retail 39.3 46.0 56.5 64.8 73.1GOCF / EBITDA 132% 116% 100% 104% 104% Institutional 24.5 29.5 33.0 40.7 42.7FCF / Underlying cash NPAT 117% 73% 64% 69% 81%

$6424m31 December

HGGNicolas Burgess19 October, 2015$5.65

Page 19

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Operating environment Overall: Despite some volatility in recent months, the UK and European wealth

management markets have been reasonably resilient in terms of aggregate fund flows, which is positive for HGG.

UK market (~45% of HGG group management fees): After peaking in July, fund flows moderated in August given global equity markets volatility. Interestingly, bond funds suffered net outflows but equity and mixed asset funds were solid.

FIG.1: UK RETAIL WEALTH MANAGEMENT – FUND FLOWS BY MONTH (£BN)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-1

0Se

p-10

Nov

-10

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep-

11N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2Se

p-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep-

13N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4Se

p-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Source: Investment Management Association

FIG.2: UK RETAIL WEALTH MANAGEMENT – FUND FLOWS BY ASSET CLASS (£M)

-1000

-500

0

500

1000

1500

2000

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Equities Bonds Mixed asset Source: Investment Management Association

Page 20

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Europe market (~30% of HGG group management fees): The overall industry posted net outflows in August, given market volatility, as shown in the chart below. Mixed asset funds remained in positive territory, but bond and equity funds suffered outflows.

FIG.3: EUROPEAN RETAIL WEALTH MANAGEMENT – FUND FLOWS BY MONTH (€BN)

-60

-40

-20

0

20

40

60

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-1

0Se

p-10

Nov

-10

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep-

11N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2Se

p-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep-

13N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4Se

p-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Source: Lipper

FIG.4: EUROPEAN RETAIL WEALTH MANAGEMENT – FUND FLOWS BY ASSET CLASS (€BN)

-40

-30

-20

-10

0

10

20

30

40

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09N

ov-0

9Ja

n-10

Mar

-10

May

-10

Jul-1

0Se

p-10

Nov

-10

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep-

11N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2Se

p-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep-

13N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4Se

p-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Mixed asset Bonds Equities Source: Lipper

Page 21

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

INTERNAL ONLY

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

RECOMMENDATIONS

Rating BUY ▲

Risk Medium Price Target $10.88

Share Price $9.50 SNAPSHOT Monthly Turnover $327.9mn Market Cap $1,742mn Shares Issued 183.4mn 52-Week High $11.79 52-Week Low $7.64

Sector Telecommunication Services

BUSINESS DESCRIPTION

M2 is an emerging Australian telco that has grown strong over the last ten years both through acquisition as well as organically. The company’s key strengths are in Small and Medium-sized Enterprises, targeted primarily through the Commander brand, and consumer, primarily through the Dodo brand.

12-MONTH PRICE & VOLUME

RESEARCH ANALYST

Luke Macnab, CFA

+ 612 9250 8930 [email protected]

Nicolas Burgess, CFA

+ 613 9602 9379 [email protected]

Nick Caley

+ 613 9602 9283 [email protected] Disclosure The author owns no shares in MTU.

M2 Group (MTU)

COMPANY REPORT

Merger win-win for MTU and VOC

VOC/MTU merger creates 4th

integrated telco: The two companies are set to join forces under a Scheme of Arrangement whereby MTU holders will receive 1.625 VOC shares for each MTU share. The notional market cap of the Merged Company (MergeCo) will be just over $3bn, with 529m shares on issue. MergeCo will have FY16E revenue of $1.78bn, EBITDA of $367m and Underlying NPAT of $187m, based on adding our previous forecasts for the two companies, excluding any synergy benefits.

MTU represents a discounted entry point: As the notional acquirer, VOC will absorb MTU. As such, to purchase MergeCo today, you can either (1) Buy VOC, or (2) Buy MTU and get VOC stock when the merger is executed in 4-5 months. At current prices, Method (2) means you get an effective 7% discount on the price of VOC. This reflects the risk that the deal does not reach completion (we believe it will proceed). The risk is mitigated by the fact that we had a stand-alone valuation and price target of $11.50 for MTU, so it is still good value if the deal does not proceed.

Strategies are complementary: VOC’s investment in infrastructure and

focus on the enterprise and wholesale markets dovetails nicely with MTU’s infrastructure-light model that focuses on the consumer and SME markets. Total cost synergies are estimated at $40m pa (fully realised by the end of FY18), with a one-off cost of $20m. Additional unspecified revenue synergies are also expected to be realised.

Investment view: We rate MTU as a BUY. We believe that MTU/MergeCo is well positioned to increase its market share as the NBN rollout reaches critical mass in the next two to three years. Its marketing teams should also increase VOC/MergeCo’s penetration into the SME market. Using VOC’s infrastructure for backhaul should mean increased margins for MergeCo.

Price target and valuation: Our valuation and price target is $10.88, based on the combined valuation of MergeCo (ie: adding our valuations of VOC and MTU and dividing by the number of shares on issue post-merger). Standalone, we value MTU at $11.50. This is based on a DCF model with a beta of 1.1 and a WACC of 9.5%.

Key risks: The key risk to our investment thesis is that the VOC/MTU merger doesn’t proceed. This may be due to a regulatory decision (by the ACCC) or corporate action by a third party. However, we believe this is unlikely. There is also a risk that MTU/MergeCo is not able to grow its business at forecast rates as competition in the retail market increases as the NBN rollout ramps up.

INVESTMENT SUMMARY

Year End: 30 June 2014A 2015A 2016E 2017E 2018E

Revenue $mn 1,023 1,114 1,403 1,473 1,546 EBITDA $mn 158.5 169.2 235.0 255.7 273.2 EBIT $mn 112.1 120.2 164.3 197.1 212.0 Reported Profit $mn 67.1 73.7 95.6 119.8 131.5 Adjusted Profit $mn 93.3 99.7 121.0 143.6 155.3 EPS (Reported) ¢ 37.2 40.2 52.1 65.3 71.7 EPS (Adjusted) ¢ 51.7 54.3 65.9 78.3 84.7 EPS Growth % 110.6 5.1 21.3 18.7 8.1 PER (Reported) x 25.6 23.7 18.2 14.5 13.3 PER (Adjusted) x 18.4 17.5 14.4 12.1 11.2 Dividend ¢ 26.0 32.0 37.0 43.0 49.0 Yield % 2.7 3.4 3.9 4.5 5.2 Franking % 100 100 100 100 100

Page 22

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

Financial summary M2 GROUP

Code MTU Rating BUYAnalyst Luke Macnab Price target $10.88Date Upside/downside 15%Share price $9.50 Valuation method DCFMarket capitalisation $1742m Risk MediumYear end 30 June

PROFIT AND LOSS (A$m) EARNINGS (A$m)

Y/e June 30 (A$m) FY14A FY15A FY16E FY17E FY18E Y/e June 30 FY14A FY15A FY16E FY17E FY18E

Revenue 1,023 1,114 1,403 1,473 1,546 Underlying Net profit ($m) 93.3 99.7 121.0 143.6 155.3EBITDA 159 169 235 256 273 EPS (c) 51.5 54.3 65.9 78.3 84.7D&A -46 -49 -71 -59 -61 EPS growth (%) 45% 5% 21% 19% 8%EBIT 112 120 164 197 212 P/E ratio (x) 18.4 17.5 14.4 12.1 11.2Net interest -17 -13 -22 -19 -18 CFPS (c) 47.3 66.5 85.2 92.4 100.0Pre-tax profit 95 107 142 178 194 Price/CF (x) 20.1 14.3 11.1 10.3 9.5Tax -28 -34 -47 -58 -63 DPS ( c ) 26.0 32.0 37.0 43.0 49.0NPAT 67 74 96 120 132 Yield (%) 2.7% 3.4% 3.9% 4.5% 5.2%Minority interests 0 0 0 0 0 Franking (%) 100% 100% 100% 100% 100%Net profit after minorities 67 74 96 120 132 EV/EBITDA 12.6 13.2 9.3 8.3 7.6Underlying 93 100 121 144 155 EV/EBIT 17.8 18.5 13.3 10.8 9.8BALANCE SHEET (A$m)

Y/e June 30 FY14A FY15A FY16E FY17E FY18E PROFITABILITY RATIOS

Cash 41 85 55 45 57 Y/e June 30 FY14A FY15A FY16E FY17E FY18E

Current receivables 98 124 120 125 129 EBITDA/revenue (%) 15.5% 15.2% 16.8% 17.4% 17.7%Inventories 5 8 29 34 38 EBIT/revenue (%) 11.0% 10.8% 11.7% 13.4% 13.7%Other current assets 26 41 34 34 34 Return on assets (%) 7.8% 5.8% 10.7% 13.3% 14.3%Current assets 170 257 237 237 258 Return on equity (%) 20.2% 20.6% 21.0% 23.1% 22.7%

Return on funds empl’d (%) 10.7% 7.9% 10.1% 12.6% 13.5%PPE 61 81 68 80 92 Dividend cover (x) 2.0 1.7 1.8 1.8 1.7Intangible assets 600 912 561 555 543 Effective tax rate (%) 29.1% 31.4% 32.7% 32.5% 32.3%Other non-current assets 31 26 29 29 29Non-current assets 692 1,019 658 663 663 LIQUIDITY AND LEVERAGE RATIOS

Y/e June 30 FY14A FY15A FY16E FY17E FY18E

Total assets 862 1,276 895 900 921 Net debt/(cash) ($m) 255 487 437 387 335Net debt/equity (%) 76.5% 135.9% 95.9% 74.7% 57.7%

Payables 185 269 269 269 269 Net interest cover (x) 6.4 9.4 7.4 10.1 12.0Debt 295 572 492 432 392 Net debt/ EBITDA (x) 1.6 2.9 1.9 1.5 1.2Other liabilities 49 77 61 61 61Total liabilities 529 918 822 762 722

Shareholders’ equity 333 366 456 518 581Minorities 0 -8 0 0 0Total shareholders funds 333 358 456 518 580

Total funds employed 862 1,276 1,278 1,280 1,302

W/A shares on issue 181.0 183.4 183.4 183.4 183.4

CASH FLOW (A$m)

Y/e June 30 FY14A FY15A FY16E FY17E FY18E

NPAT plus discontinued ops. 67 74 122 120 132Non-cash items 47 48 71 59 61Working capital -28 0 -36 -9 -9Other operating cash flow 0 0 0 0 0Operating cashflow 86 122 156 170 183

Capex -13 -18 -35 -37 -39Investments -8 0 0 0 0Other investing cash flow -10 -248 -9 -9 -9Investing cashflow -31 -266 -44 -46 -48

Change in borrowings -33 224 -80 -60 -40Equity raised 1 3 0 0 0Dividends paid -29 -39 -62 -73 -84Other financing cash flow 0 0 0 0 0Financing cashflow -61 188 -142 -133 -124

Net change in cash -7 44 -30 -9 12

Cash at end of period 41 85 55 45 57

16 October, 2015

19 October 2015

Page 23

BAILLIEU HOLST RESEARCH

Top Stock Picks – October 2015

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report.

NBN rollout is key for MTU growth The ramp-up of the NBN rollout over the next few years will be a key driver of

MTU/MergeCo’s revenue and earnings growth. This is because it essentially turns all fixed broadband providers into resellers as they all have to use the NBN to deliver their product. As they will all have roughly the same cost base, MTU’s lower cost to serve and cost to

acquire customers means they are well placed to increase their market share.

To date, MTU has been maintaining its share of the consumer broadband market (around 6-8%) amongst premises which have had the NBN rolled out. This has been achieved through low-cost, targeted marketing in areas where rollout has occurred. In recent months, MTU has stepped up its marketing to include broader campaigns aimed at increasing overall awareness of their brands (both consumer and corporate).

FIG.1: NBN ROLLOUT TO AUSTRALIAN PREMISES (M) FIG.2: AUSTRALIAN FIXED LINE BROADBAND TRAFFIC

0

2

4

6

8

10

12

FY12A FY13A FY14A FY15A FY16F FY17F FY18F FY19E FY20E FY21E

Ready For Service Service Activated