2 - 2 - 1 Prentice Hall Business Publishing, Prentice Hall Business Publishing, Auditing 14/e, Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley The CPA Profession The CPA Profession Chapter 2 Chapter 2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2 - 2 - 11©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley

The CPA ProfessionThe CPA ProfessionChapter 2Chapter 2

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 22

Learning Objective 1Learning Objective 1

Describe the nature of CPA Describe the nature of CPA firms,firms,

what they do, and their what they do, and their structure.structure.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 33

Certified Public Certified Public Accounting FirmsAccounting Firms

The legal right to perform audits is grantedto CPA firms by each state.

CPA firms also provide many other services totheir clients, such as tax and consulting services.CPAs continue to develop new products and services—such as financial planning, business valuation and information technology.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 44

Certified Public Certified Public Accounting FirmsAccounting Firms

Big Four international firms

National firms

Regional and large local firms

Small local firms

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 55

Certified Public Certified Public Accounting FirmsAccounting Firms

The four largest CPA firms in the United Statesare called the “Big Four” international CPA firms.

These four firms have offices in most majorcities in the United States and in manycities throughout the world.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 66

Certified Public Certified Public Accounting FirmsAccounting Firms

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 77

Management consulting services

Tax services

Accounting and bookkeeping services

Activities of CPA FirmsActivities of CPA Firms

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 88

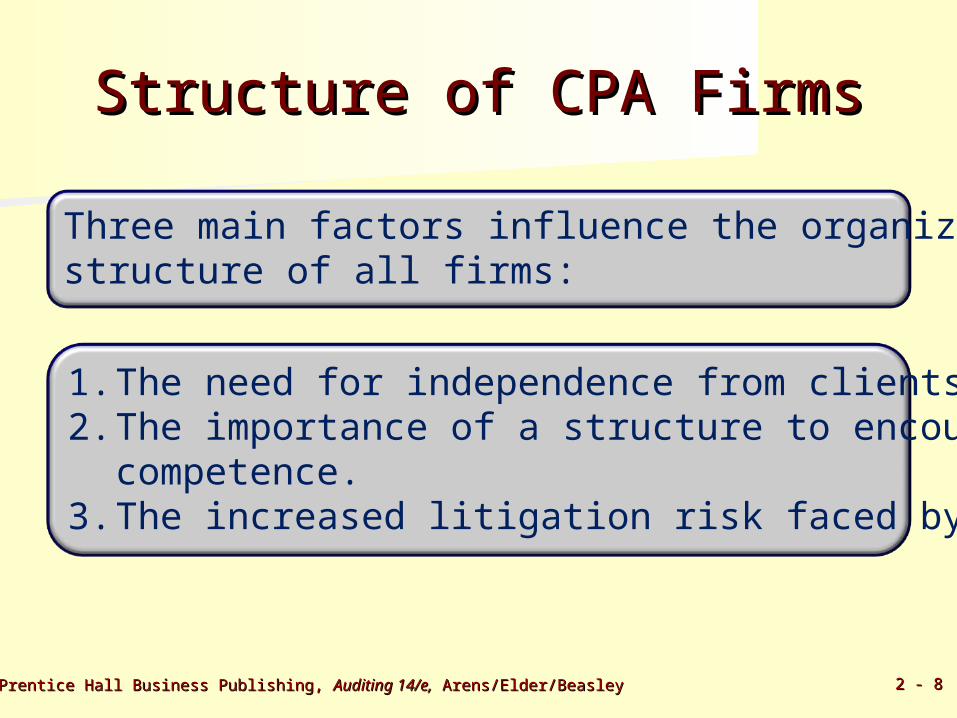

Structure of CPA FirmsStructure of CPA Firms

Three main factors influence the organizationalstructure of all firms:

1.The need for independence from clients.2.The importance of a structure to encourage

competence.3.The increased litigation risk faced by auditors.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 99

Organizational StructureOrganizational Structure Proprietorship Professional corporation General partnership Limited liability company General corporation Limited liability partnership

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1010

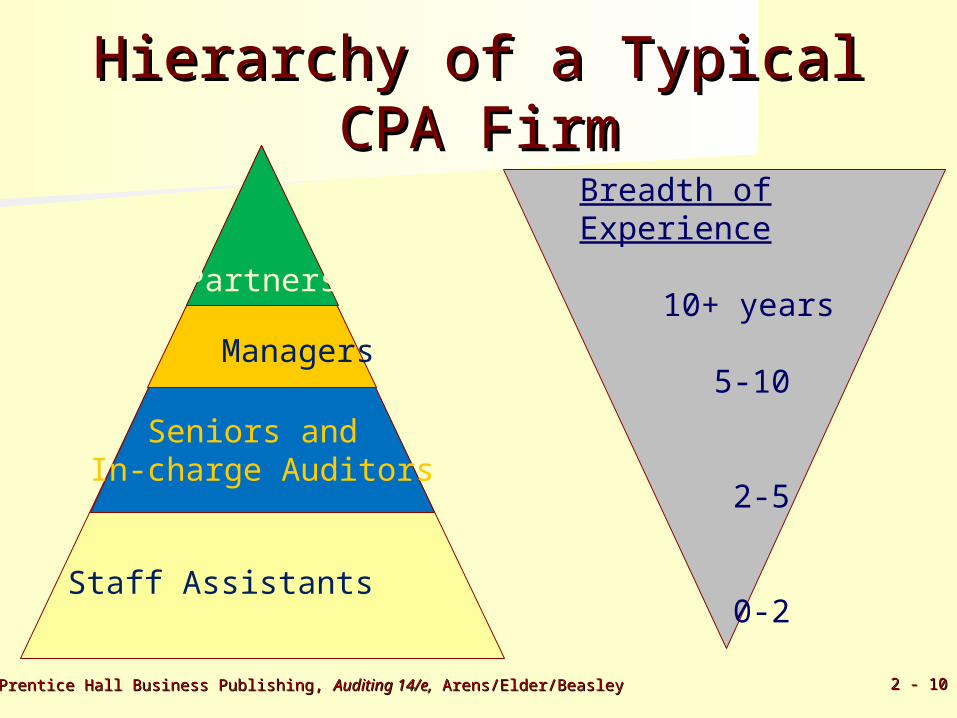

Staff Assistants

Hierarchy of a TypicalHierarchy of a TypicalCPA FirmCPA Firm

Seniors and In-charge Auditors

Managers

Partners

Breadth of Experience

10+ years

5-10

2-5

0-2

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1111

Learning Objective 2Learning Objective 2

Understand the impact of the Understand the impact of the PCAOB andPCAOB and

Sarbanes-Oxley on the CPA Sarbanes-Oxley on the CPA profession.profession.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1212

This Act is considered by many observers tobe the most important legislation affectingthe auditing profession since the 1930s.

Sarbanes-Oxley ActSarbanes-Oxley Act

The provisions of the Act apply to publiclyheld companies and their audit firms.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1313

Sarbanes-Oxley ActSarbanes-Oxley Act

SEC

PCAOB(Public Company

AccountingOversight Board)

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1414

Learning Objective 3Learning Objective 3

Summarize the role of the Summarize the role of the Securities andSecurities and

Exchange Commission in accounting Exchange Commission in accounting andand

auditing.auditing.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1515

The purpose is to assist in providing investorswith reliable information upon which to make investment decisions

The Securities Act of 1933The Securities Exchange Act of 1934

Securities and Exchange Securities and Exchange CommissionCommission

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1616

Securities and Exchange Securities and Exchange CommissionCommission

Form S-1 Form 8-K Form 10-K Form 10-Q

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1717

Learning Objective 4Learning Objective 4

Describe the key functions Describe the key functions performed by the AICPA.performed by the AICPA.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1818

Performs the following services for CPAs: Sets professional requirements Conducts research Publishes materials related to services

performed

AICPAAICPA

Empowered to set standards (guidelines)and rules

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 1919

Establishing StandardsEstablishing Standardsand Rulesand Rules

1.Auditing standards

2.Compilation and review standards

3.Other attestation standards

4.Code of Professional Conduct

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2020

Other AICPA FunctionsOther AICPA Functions

Research and Grants

The CPA examination

Provides seminars and continuing education

Publishes a variety of materials

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2121

Learning Objective 5Learning Objective 5

Understand the role of Understand the role of international auditing standards international auditing standards and their relation to U.S. and their relation to U.S. auditing standards auditing standards

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2222

GAAS and Standards of Performance

Statements on Auditing Statements on Auditing StandardsStandards

Classification of Statements on Auditing Standards

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2323

International StandardsInternational Standardson Auditingon Auditing

IFAC is the worldwide organizationfor the accountancy profession.

The IFAC works to improve theuniformity of auditing practices andrelated services throughout the world.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2424

International StandardsInternational Standardson Auditingon Auditing

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2525

Learning Objective 6Learning Objective 6

Use U.S. auditing standards as a Use U.S. auditing standards as a basis for further studybasis for further study

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2626

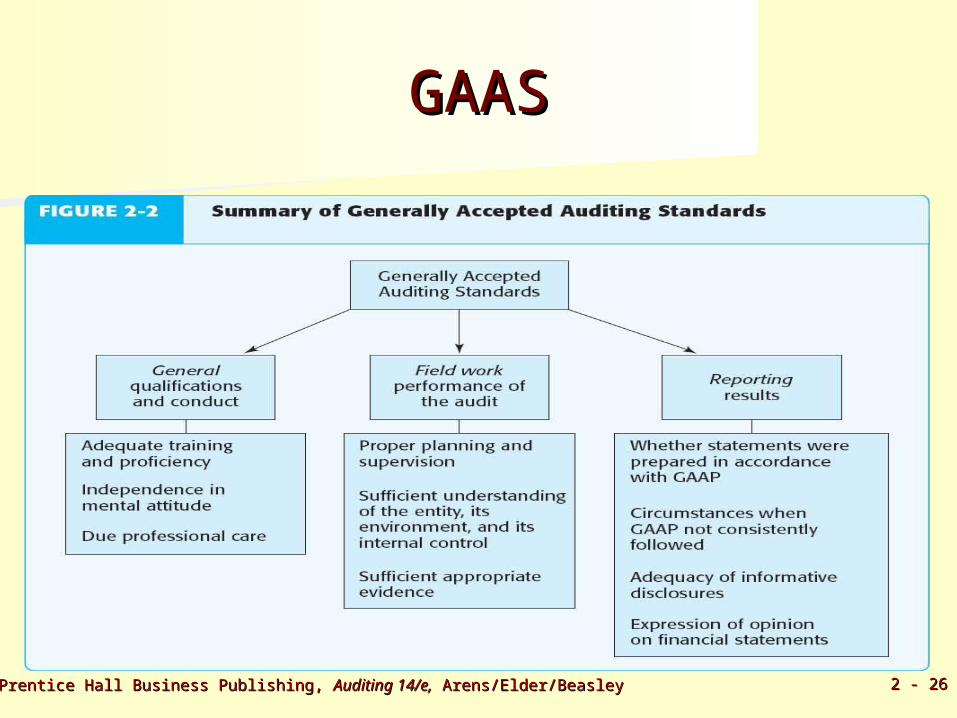

GAASGAAS

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2727

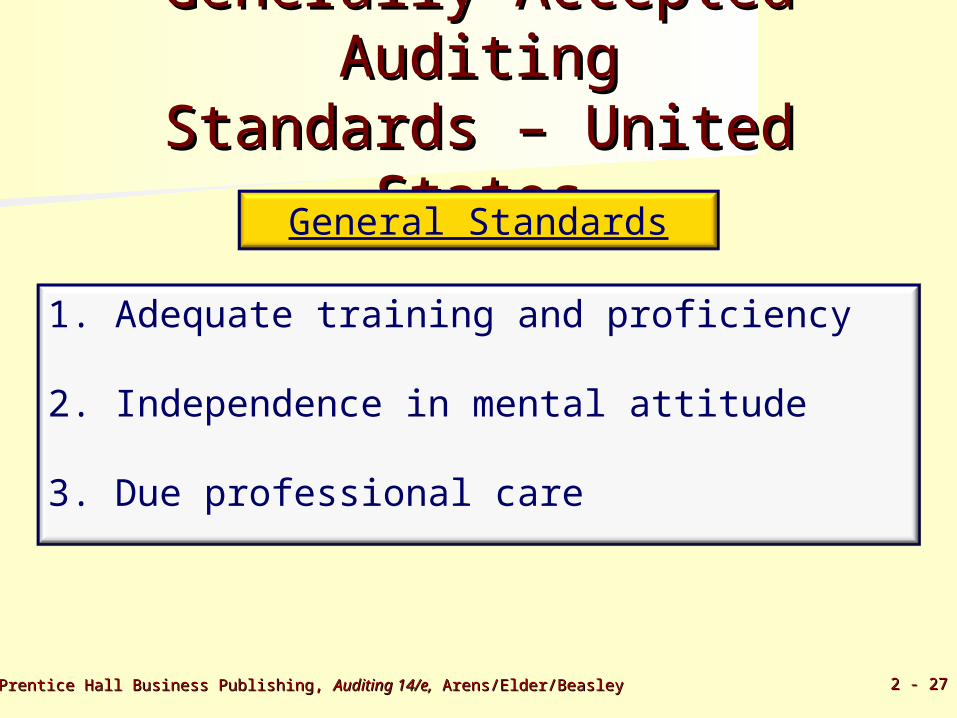

Generally Accepted Generally Accepted AuditingAuditing

Standards – United Standards – United StatesStatesGeneral Standards

1. Adequate training and proficiency

2. Independence in mental attitude

3. Due professional care

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2828

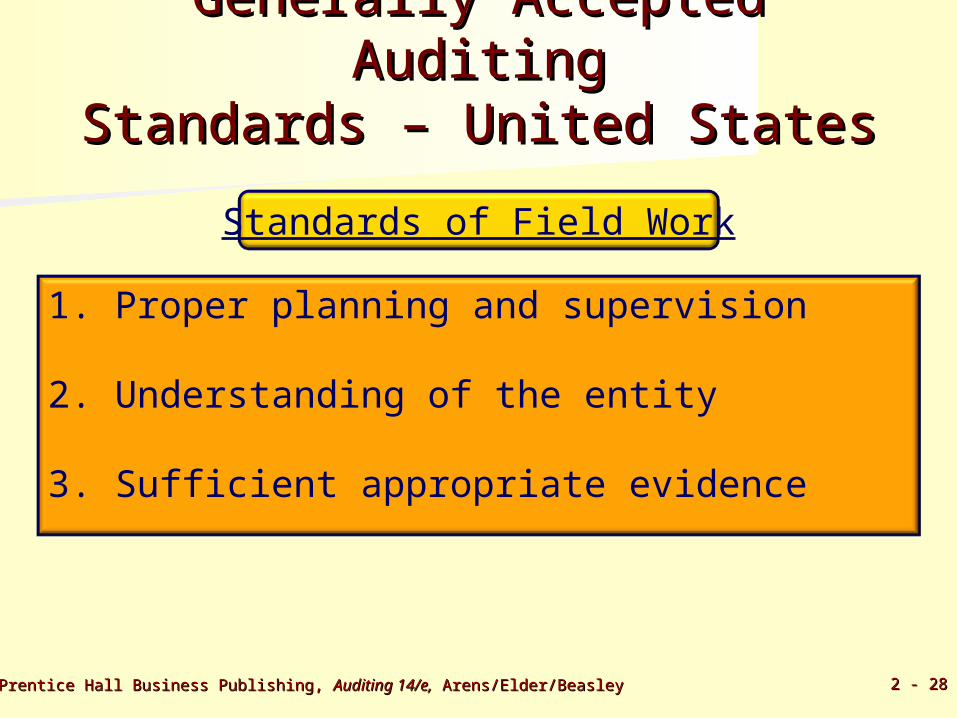

Generally Accepted Generally Accepted AuditingAuditing

Standards – United StatesStandards – United StatesStandards of Field Work

1. Proper planning and supervision

2. Understanding of the entity

3. Sufficient appropriate evidence

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 2929

Generally Accepted Generally Accepted AuditingAuditing

Standards – United Standards – United StatesStatesStandards of Reporting

1. Statements prepared in accordance with GAAP

2. Circumstances when GAAP not followed

3. Adequacy of disclosures

4. Expression of opinion on financial statements

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 3030

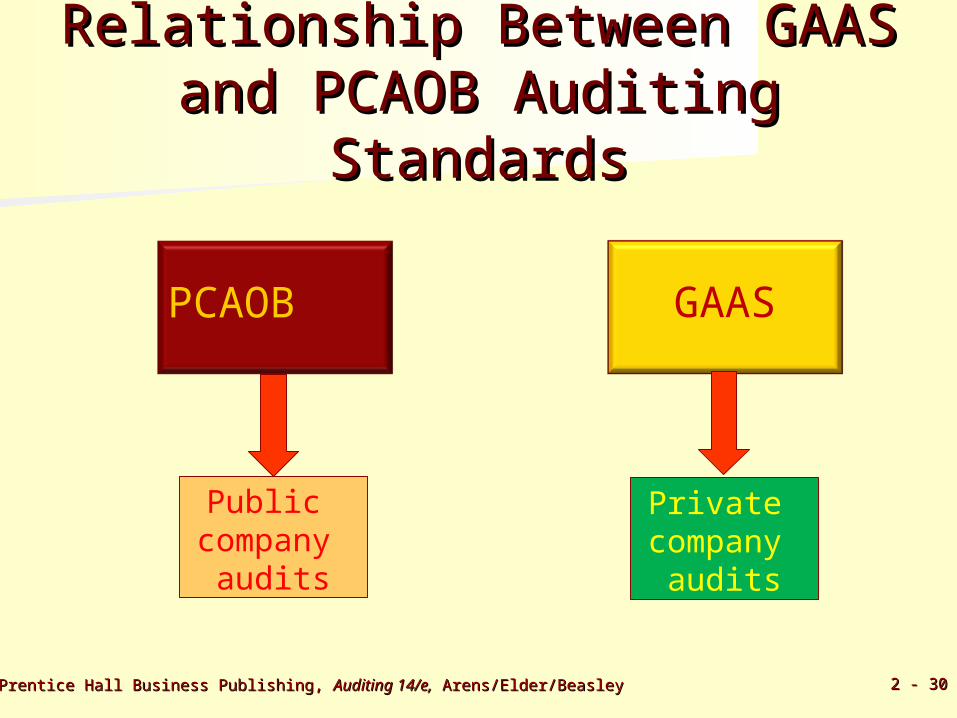

Relationship Between GAAS Relationship Between GAAS and PCAOB Auditing and PCAOB Auditing

StandardsStandards

PCAOB

Public company audits

Private company audits

GAAS

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 3131

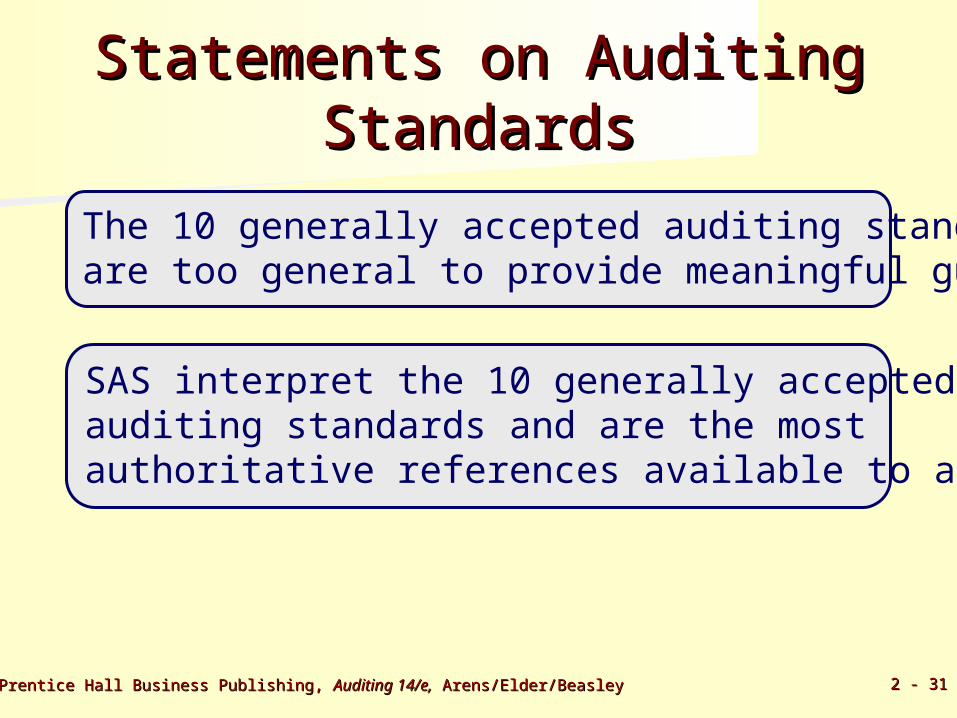

The 10 generally accepted auditing standardsare too general to provide meaningful guidance.

SAS interpret the 10 generally acceptedauditing standards and are the mostauthoritative references available to auditors.

Statements on Auditing Statements on Auditing StandardsStandards

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 3232

Learning Objective 7Learning Objective 7

Identify quality control Identify quality control standards and practices within standards and practices within the accounting profession.the accounting profession.

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 3333

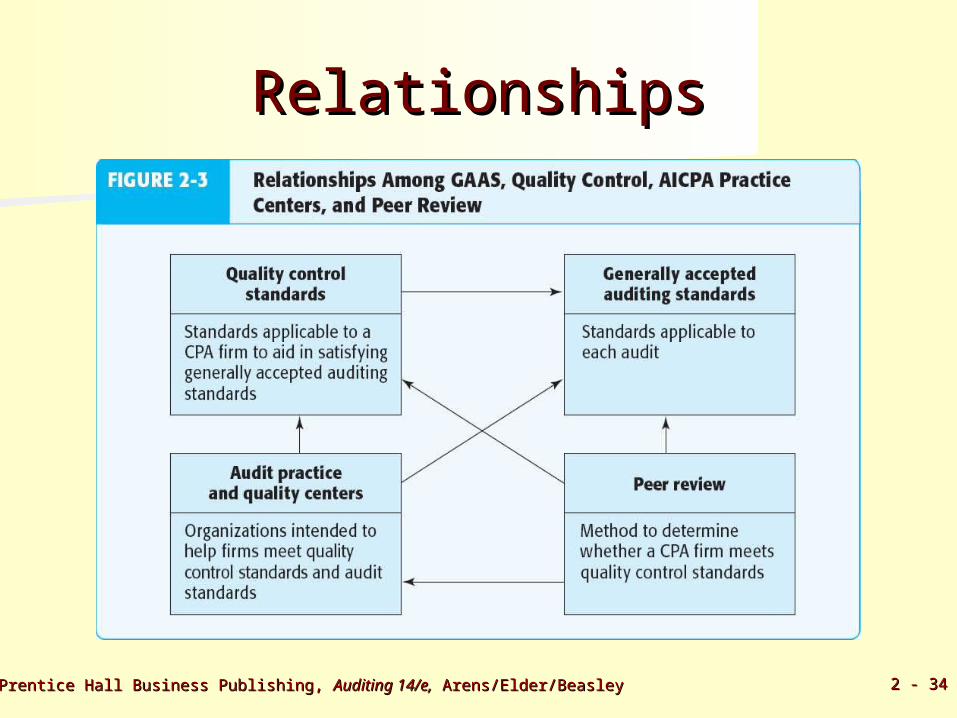

Elements of Quality Elements of Quality ControlControl

Independence, integrity, and objectivity Personnel management Acceptance and continuation of clientsand engagements

Engagement performance Monitoring

©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley 2 - 2 - 3434

RelationshipsRelationships

2 - 2 - 3535©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley

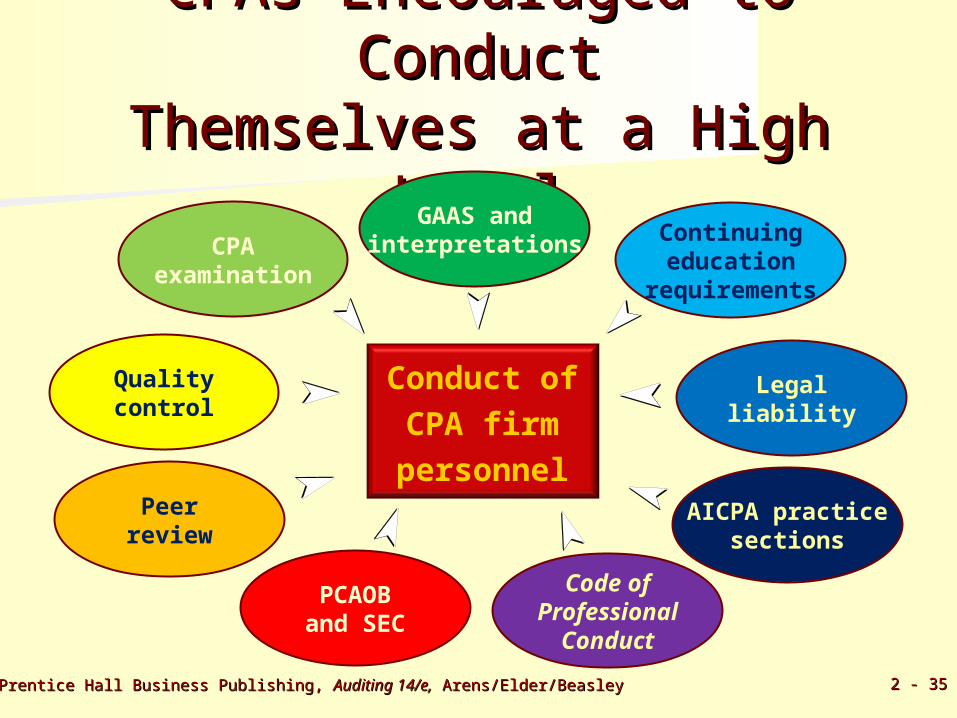

CPAs Encouraged to CPAs Encouraged to ConductConduct

Themselves at a High Themselves at a High LevelLevel

Legalliability

AICPA practicesections

Continuingeducation

requirements

GAAS andinterpretations

Code ofProfessional

Conduct

CPAexamination

Qualitycontrol

Peerreview

PCAOBand SEC

Conduct ofCPA firmpersonnel

2 - 2 - 3636©2012 Prentice Hall Business Publishing, ©2012 Prentice Hall Business Publishing, Auditing 14/e,Auditing 14/e, Arens/Elder/Beasley Arens/Elder/Beasley

End of Chapter 2End of Chapter 2

Related Documents