AUDIT OF PROPERTY, PLANT AND EQUIPMENT (PPE)

Audit of Property, Plant and Equipment (

Nov 30, 2015

explain about ppe

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AUDIT OF PROPERTY, PLANT AND EQUIPMENT (PPE)

NATURE OF PROPERTY, PLANT AND EQUIPMENT

PPE are assets that have an expected lifespan of more than 1 year, are used in the business and are not acquired for resale.

• The primary record for PPE• Includes a detailed record of each piece of

equipment and property owned• The totals for all records in master file equal

the general ledger balances for related account

• It also contains information about property acquired and disposed during the year

Fixed Assets Master File

• Auditors verify manufacturing equipment differently from current asset accounts for :– Usually fewer current period acquisition of

manufacturing equipment– The amount of any given acquisition is often

material– The equipment is likely to be kept and maintained

in the accounting records for several years

Test Categories

Verifying depreciation expenses

Analytic procedures

Verifying current year acquisitions

Verifying current year

disposal

Verifying the ending balance

in the assets account

Verifying the ending balance in accumulated

depreciation

Analytic Procedure

• Include comparison of financial information with :-– Prior periods– Budgets– Forecasts– Similar industries

• Includes consideration of predictable relationships, such as :-– Gross profit to sales– Payroll costs to employees– Financial information and non-financial

information, for examples the CEO’s reports and the industry news.

• Possible sources of information about the client include:– Interim financial information– Budgets– Management accounts– Non-financial information– Bank and cash records– Board minutes– Discussion or correspondence with the client at they year-end

• Table below show type of ratio and trend analysis often performed for manufacturing equipment

Analytic procedures Possible misstatement

Compare depreciation expenses divided by gross manufacturing equipment cost with previous year

Misstatement in depreciation expenses and accumulated depreciation

Compare accumulated depreciation divided by gross manufacturing equipment cost with previous years

Misstatement in accumulated depreciation

Compare annually or monthly repairs and maintenance, supplies expenses, small tool expenses and similar acc with previous years

Expensing amount that should be capitalized

Compare gross manufacturing cost divided some measure of production with previous years

Idle equipment or equipment that was disposed of but not written off

Verifying Current Year Acquisition

• Long term effect on the financial statement• Improper amount will affects :-– The balance sheet until the company dispose of the asset– Income statement effects until the asset fully depreciated

Select a sample of entries in the acquisitions journal and trace to capital asset master file

Select a sample of entries in the acquisitions journal and trace to vendor invoices and receiving reports

Select a sample of entries in the acquisitions journal and physically examine the related assets

Example of procedure

• Testing acquisition :-– Auditor must know the client’s capitalisation policies to

make sure that :-• It is record accordance to accounting standard• Treated consistently in the preceedings year

For example :Client expenses items that less than certain amount, suchas RM1000So, auditor should alerts for the transportation and installation cost.

• Reviewing recorded transactions for proper classification

For example :– Amount recorded as manufacturing

equipment should be classified as office equipment or part of the building

– Possibility for client to improperly capitalised repairs, rent or other expenses

Verifying Current Year Disposal

The auditor’s main

objectives in the

verification of sale,

trade-in, abandonmen

t are :-

•Existing disposal are recorded•Disposals are accurately recorded

•It is the starting point to verify client disposal•Includes date of disposals, name of person who acquire the assets, selling price, original cost of assets, acquisition date and accumulate depreciation of asset•Detail tie-in tests of the schedule is necessary, including footing the schedule, tracing the totals on the schedule to be recorded disposals in the general ledger, and tracing the cost and accumulate depreciation of the disposals to the property master file

Client’s Schedule

of Recorded Disposals

The search for unrecorded disposals is essential. The nature and adequacy of the controls over disposals affect the extent of the search. The following procedures are often used to verify disposals.

• Review whether newly acquired assets replace existing assets• Analyze gains, losses and miscellaneous income from the

disposals of assets• Review plant modifications and changes in product line,

property taxes, or insurance coverage• Make inquiries of management and production personnel

about the possibility of the disposal of assets

Verifying Ending Balance of Asset Account

Auditor’s objectives when auditing manufacturing equipment include determining that :-• Existence - all recorded equipment physically exists on the balance sheet date• Completeness – all equipment owned is recorded

• Auditor have to consider the nature of internal controls over the manufacturing company

• This is including the use of master file for individual fixed asset, adequate physical controls over assets that are easily movable, assignment of identification numbers to each plant asset and periodic physical amount to fixed asset

• A formal method of informing the accounting department of all disposals of fixed asset is also an important control over the balance of fixed asset carried forward into the current year

• After assessing the control risk for the existence objective, the auditors have to decide whether its necessary to verify the existence of individual item of the manufacturing equipment

• If there is a high likelihood of material missing fixed asset still included in the master file, the auditor can select a sample from the master file and examine the actual assets

• In rare cases, the auditor may decide it is necessary for the client to take a complete physical inventory of fixed assets to make sure they all exist

• The auditor normally doesn’t need to test the accuracy or classification of fixed assets recorded in prior periods because they were verified in previous audits at the time they were required

• But the auditor should be aware that companies may occasionally have manufacturing equipment on hand that is no longer used in operations

• In addition to performing procedures to obtain evidence related to balanced-related audit objectives for fixed assets, auditors also perform audit procedures related to the four presentation and disclosure objectives for fixed assets

• A major consideration in verifying disclosures related to fixed assets is the possibility of legal encumbrances

• Next, the proper presentation and disclosure of manufacturing equipment in the financial statement must be evaluated carefully to make sure that accounting standards are followed

• Manufacturing equipment should include the gross cost and should ordinarily be separated from other fixed assets

• Leased property should also be disclosed separately and all liens on property must be included in the footnotes

Verifying Depreciation Expense

Not verified as part of tests of control and substantive tests of transactions

Recorded amounts are determined by internal allocations

Most important balance-related audit objective-accuracy

Auditors focus on determining whether the client followed consistent depreciation policy and the client’s calculation are correct

Auditors weight for

consideration

The policy of depreciating assets

in the year of acquisition and

disposition

The estimated

salvage value

The method of

depreciation

The useful life of current

period acquisitions

Reasonableness testAuditor must consider the physical life if the asset, the expected lifespan and established company policies on trading in equipment

Made by un-depreciated fixed assets by depreciation rate for the year - make

adjustments

If cannot be accomplished - more detailed tests are needed (recomputing, reconciliation)

Verifying Ending Balance In Accumulated Depreciation

It is necessary to evaluate the adequacy of the

allowances for accumulated depreciation each year – to ensure NBV not > realizable

value of the assets

Credit – as a part of depreciation

expenses

Debit – tested as a part of the audit

of disposals of assets

Life manufacturing equipment may be

significantly reduced because of possibilities of

Unexpected physical

deterioration

Modification in operation

Reduction in customer demands

for product

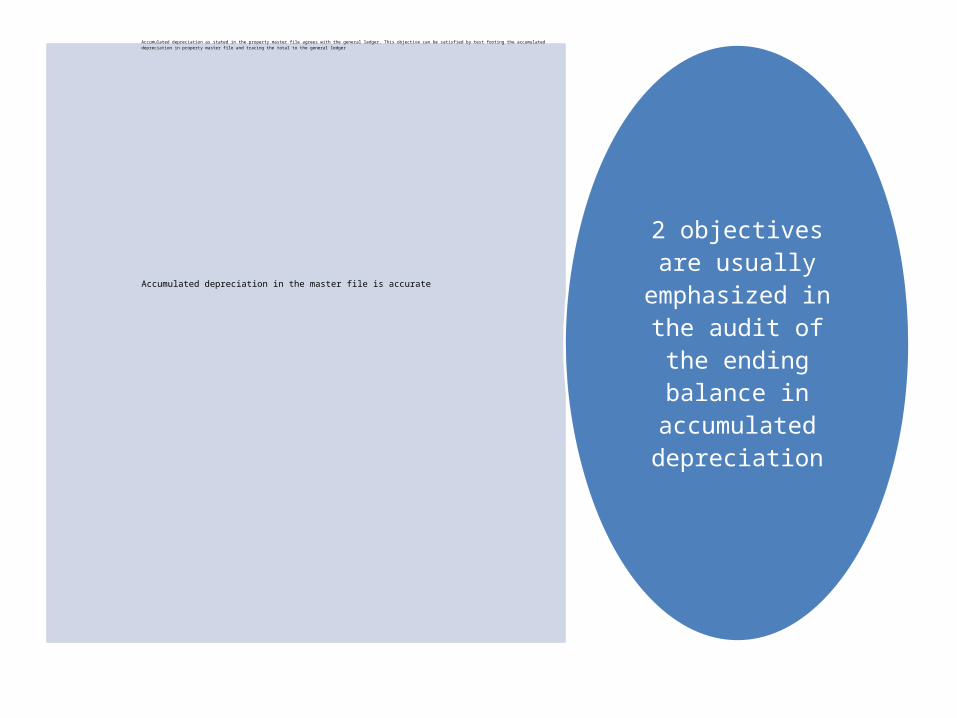

Accumulated depreciation as stated in the property master file agrees with the general ledger. This objective can be satisfied by test footing the accumulated depreciation in property master file and tracing the total to the general ledger

Accumulated depreciation in the master file is accurate2 objectives are

usually emphasized in the audit of the

ending balance in accumulated depreciation

Related Documents