Audit Life Cycle Management Presented by: Vinod Rao (Chief of Internal Audit & Assurance, Indus Towers Limited)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Audit Life Cycle Management

Presented by: Vinod Rao (Chief of Internal Audit & Assurance, Indus Towers Limited)

About the Presenter

2

• Vinod has around 18 years of deep and rich experience in Internal Audit. He has worked for clients across industries, in projects involving risk assessment, SOX, audit planning, executing, and reporting & presentations to Chief Internal Auditors/Audit Committees.

• Most recently, he was with BP Lubricants as General Manager at Global Level supporting the Internal Control team. He was also one of the designated Fraud and Misconduct Responsible persons in the company.

• Previously, Vinod was the Head – Internal Audit at Castrol India reporting to the Chair of the Audit Committee and to the Managing Director, India. Vinod spent close to 5 years in BP and Castrol together.

• Earlier, he spent 6 years at KPMG in Bahrain, and 2 years at KPMG in India. During his stay at Bahrain, he worked on various statutory audits based on IAS/IFRS across manufacturing, retail and financial services. He was also the training champion for International Financial Reporting Standards and KPMG Audit Methodology (KAM) in the last two years of his stint for Bahrain and Doha offices.

• In India, Vinod set up the Internal Audit Practice of KPMG at Pune.

• Vinod’s professional certifications include ACA, ICWA, CISA and CPA.

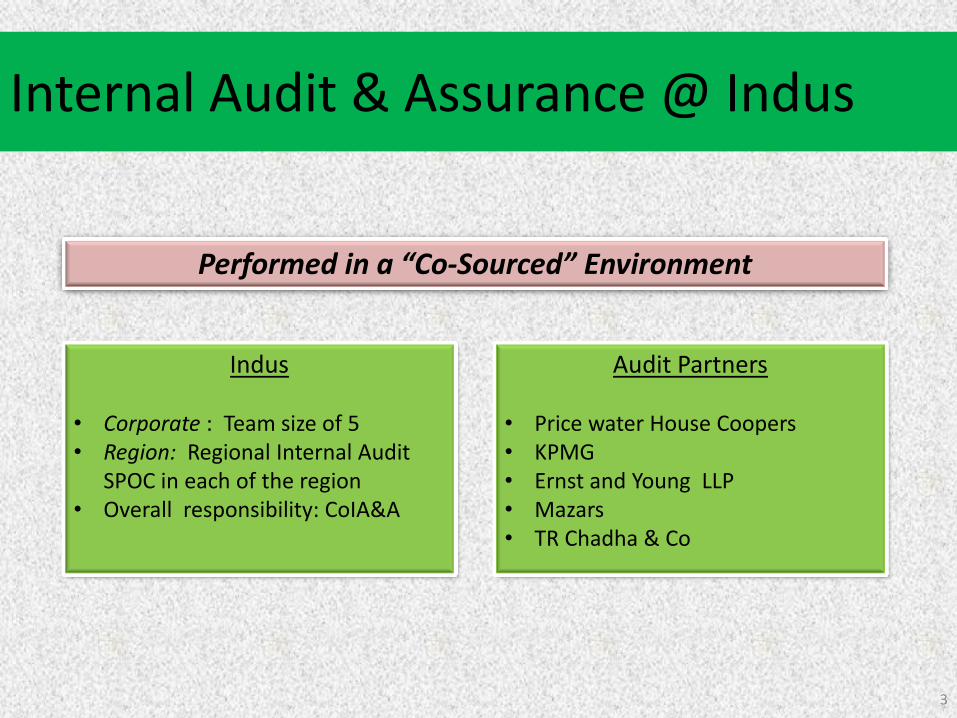

Internal Audit & Assurance @ Indus

3

Performed in a “Co-Sourced” Environment

Indus

• Corporate : Team size of 5 • Region: Regional Internal Audit

SPOC in each of the region • Overall responsibility: CoIA&A

Audit Partners

• Price water House Coopers • KPMG • Ernst and Young LLP • Mazars • TR Chadha & Co

Elements of Audit Life Cycle

Planning

Fieldwork

Scoring Reporting

Action Taken Report

4

Planning: Approach

Previous FY Risk Assessment

Audit Plan

Interviews with: - Management

- Statutory Auditors - Internal Auditors

Risk assessment for previous FY taken as the basis for

current year’s risk assessment.

Interview selective management personnel to gain their

assessment of processes and sub-processes to ensure

coverage of significant balances/accounts

Analyze the results to arrive at changes in the previous

years’ risk assessment at function and processes level

Finalize audit areas to be covered along with their

locations, and time duration for subsequent FY

Results Analysis

Financial statement – sub process mapping

Learnings from previous years’ audits and factored in for

any potential changes required in audit coverage for

subsequent financial year

Key learning from previous financial year

Alignment with key Financial Controls in

previous financial year

Alignment of audit plan with the key financial controls

identified during the previous year

5

Planning: Outcome

Comprehensive plan for FY covering processes/sub-processes, locations,

timelines

6

Process/Sub Process Circle/Corporate Audits to be conducted on

Q1 Q2 Q3 Q4

Finance

Fixed Asset Corporate

Revenue Corporate/Circle

Audit Deliveries

Circle 120

Corporate 10

Total 130

Spread across 13 functions

Scrap review and Special Projects

Fieldwork: Process

7

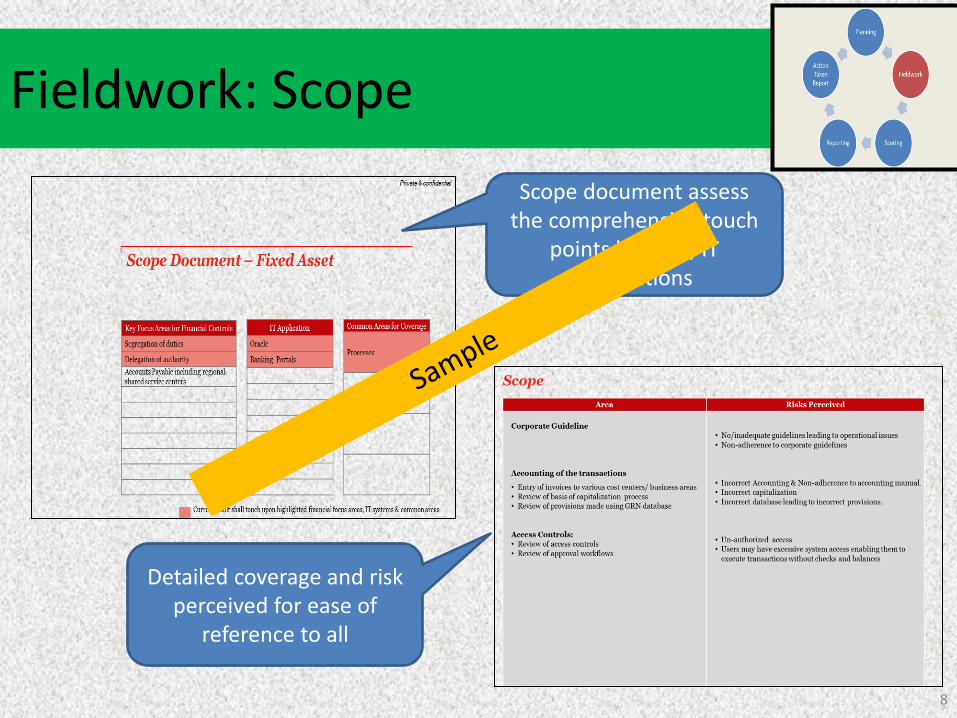

Fieldwork: Scope

Detailed coverage and risk perceived for ease of

reference to all

8

Scope document assess the comprehensive touch

points like KFC, IT applications

Fieldwork: RCM

Area Objective Category

Objective Title Risk

Description Test Title

Test Description Type Risk

Severity

High

Medium

Low

Control Objective Description of test and guidance how to perform the test

Function/Sub process to be

reviewed

Manual/Automated

9

Consider an RCM with - 12 High, 30 Medium, 8 Low

inherent risks

Scoring: Pre - ATR

10

Indus Towers Limited

Audit Scorecard

Function: SCM

Audit: Purchase

Overall

No. of inherent

risk as per RCM

(@corporate)

Weightage Score

Actual

observations as

per Report

Weightage

Non-

Compliance

Score

Compliance

Score

(A) (B) C=(A*B) (D) (E) F = (E*D) G=C-F

H 12 10 120 2 10 20 100

M 30 5 150 7 5 35 115

L 8 2 16 3 2 6 10

Total 50 286 12 61 225

Gross Scorecard H=G/C 79%

Weightage

(in %)

Actual

Repeat

Observation

Deduction

for Repeat

Observation

(I) (J) K=(I*J)

3 2 (6)

2 1 (2)

(8)

71%

Type pf Risk

H

M

Net Scorecard L= (H-K)

Total Deduction (K)

Deduction for Repeat observations: High/Medium Risk

No of inherent risk mentioned in RCM

No of actual observations in report

Scoring: Post - ATR

11

Ratings Initial Audit Observations ‘Open’ observations

Post – ATR – Q1

Post – ATR – Q2

Post – ATR – Q3

Post – ATR – Q4

High 2 1 - - -

Medium 7 3 2 1 -

Low 3 Low points are not tracked for Post -ATR

Closure of observations through ‘ATR’

ensures a higher Post – ATR score

Initial Score of 71% can

increase to 90% if all the

audit observations

get closed

Reporting: Risk Rating Criteria

12

Reporting: IA Report

13

Internal Audit Report issued TO: All stakeholders – Management Committee, Corporate Functional Heads Copied to: Auditees

Reporting: IA Report

14

Reporting: Pentana Upload

15

Post issuance of Internal Audit Report (IAR) , the report is uploaded in Pentana for action tracking

Reporting to Audit Committee

16

Audit completion status and risk categorization Audit Completion

status Report rating

Risk category of observations

Gross audit score

Deductions for repeat

observation

Net audit score

High Medium Low

Q2 2013-14 Audits

Capital Expenditure (CAPEX) Good - 1 1 86% (0%) 86%

Procurement Operations(Ker) Satisfactory - 2 2 80% (0%) 80%

Q3 2013-14 Audits

Rent (Corp) Good - 1 3 90% (2%) 88%

Balance Sheet Review (Corp) Good - 1 2 83% (2%) 81%

Audits completed, final report issued

.Audit Report Branding and scorecard

Good Satisfactory Requires Improvement Unsatisfactory

>80% 71%-80% 60%-70% <60%

Reporting to Audit Committee

17

Action Taken Report summary (ATR): As at 30 November

2013

Observation

Risk Category

Open

observations

last quarter(A)

Observations for

audits completed

in Q2 (B)

Total

Observations

C=(A+B)

Observations

implemented / closed

during the quarter (D)

Observations Open

as at 30 November

2013

(C-D)

High

Medium

Total

Audits

Total High risk

observations (including

Q2)

Open high observations and ageing as at 30 November 2013

Details as per Sl. number on pages 33-39

Not Due

0-3 m 3-6m 6-12m > 12m Total

Revenue

Fixed Assets

Supply Chain

Subtotal (2012-13)

Information Technology

Full Circle Review

Human Resource

Subtotal (2013-14)

Grand Total

Medium risk observations open Open Medium observations and ageing as at 30 November 2013

Not Due 0-3 m 3-6m 6-12m >12m Total

Reporting to Audit Committee

18

Ops Finance HR Legal A

ud

it S

core

No

of

aud

its

76

80

74 76

78

76

78

75

Gross Score

Net Score

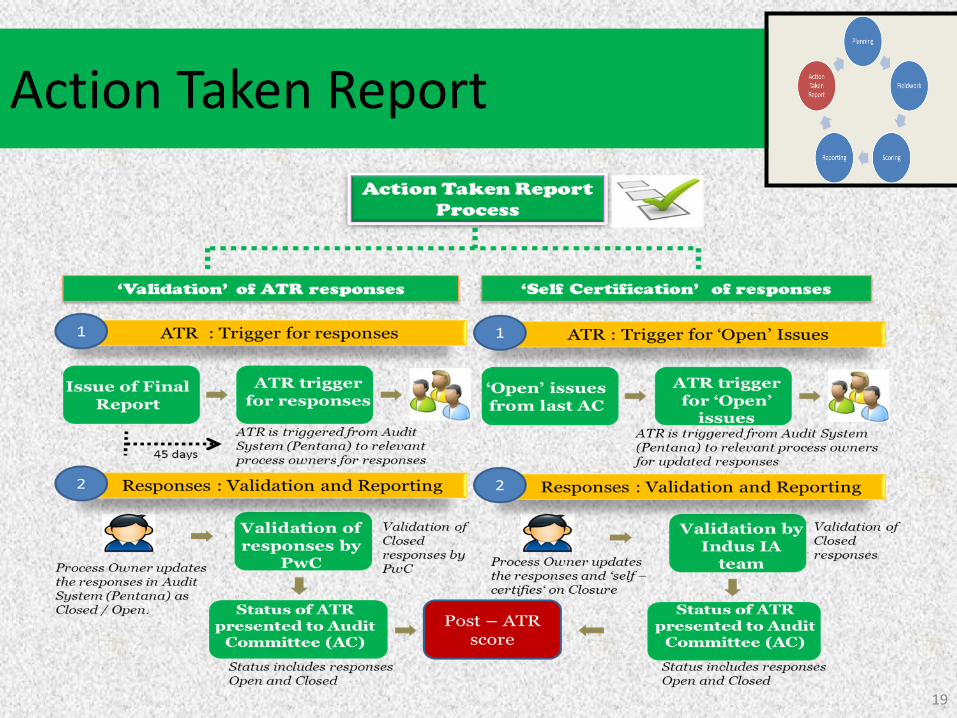

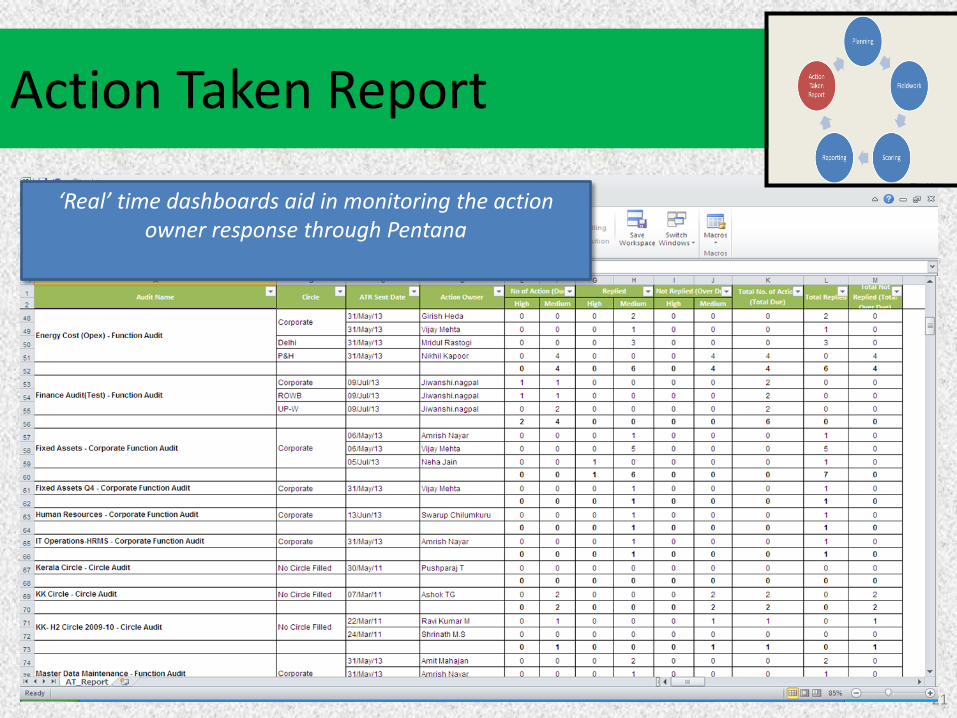

Action Taken Report

19

Action Taken Report

20

All actions are tracked for closure through Pentana system at entity and individual observation level

Action Taken Report

21

‘Real’ time dashboards aid in monitoring the action owner response through Pentana

Internal Audit & Assurance @ Indus

22

Role of the Internal Audit & Assurance SPOC

Internal Audit & Assurance activities

23

24

Related Documents