FAR-4 Miles CPA Review F4-26 4.4) Leases I) Overview of Leases Lease - “Contract” (or part of a contract) between the lessor (“supplier”) and the lessee (“customer”), that conveys the lessee the “right to control the use” of identified lessor’s PP&E (an “identified asset”) for a period of time in exchange for consideration “Contract” - At inception of a contract, an entity shall determine whether that contract is or contains a lease “Identified asset” - typically explicitly specified in the contract (but may also be implicit in the contract) Lessee’s “right to control the use” of the identified asset – Assess whether, throughout the period of use, the lessee has both of the following: Right to obtain substantially all of the economic benefits from use of the identified asset - Ok if the lessor pays a portion of these benefits to the lessor (e.g., lessee is required to pay the lessor a % of sales from use of lessor’s retail space) Right to direct the use of the identified asset - Ok if the lessor has certain protective rights (e.g., requiring lessee to follow particular operating practices) Note: Not a lease if lessor has substantive substitution rights - In this case, lessee does not have the “right to control the use” of an “identified asset” if the lessor has substantive right to substitute the asset throughout the period of use (e.g., lease of a car wherein the lessor has the practical ability to replace the leased car throughout the period of use at the lessor’s discretion), and this replacement would be economically beneficial to the lessor Lessor = Landlord = “Supplier” Lessee = Tenant = “Customer”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FAR-4 Miles CPA Review

F4-26

4.4) Leases

I) Overview of Leases

Lease - “Contract” (or part of a contract) between the lessor (“supplier”) and the lessee

(“customer”), that conveys the lessee the “right to control the use” of identified lessor’s PP&E (an

“identified asset”) for a period of time in exchange for consideration

“Contract” - At inception of a contract, an entity shall determine whether that contract is or

contains a lease

“Identified asset” - typically explicitly specified in the contract (but may also be implicit in the

contract)

Lessee’s “right to control the use” of the identified asset –

Assess whether, throughout the period of use, the lessee has both of the following:

Right to obtain substantially all of the economic benefits from use of the identified asset

- Ok if the lessor pays a portion of these benefits to the lessor (e.g., lessee is required

to pay the lessor a % of sales from use of lessor’s retail space)

Right to direct the use of the identified asset

- Ok if the lessor has certain protective rights (e.g., requiring lessee to follow

particular operating practices)

Note: Not a lease if lessor has substantive substitution rights - In this case, lessee does not

have the “right to control the use” of an “identified asset” if the lessor has substantive right

to substitute the asset throughout the period of use (e.g., lease of a car wherein the lessor

has the practical ability to replace the leased car throughout the period of use at the

lessor’s discretion), and this replacement would be economically beneficial to the lessor

Lessor = Landlord = “Supplier”

Lessee = Tenant = “Customer”

Miles CPA Review FAR-4

F4-27

Lease classification - Both lessee and lessor shall classify each separate lease component at the

commencement date (note: need not reassess lease classification unless contract is modified; or

only for lessee, if there is a change in the lease term)

For Lessee - The lease may be classified as

Finance Lease {if any of the “OWNER” criteria is met}, or

Operating Lease

Note for IFRS: Lessees no longer classify their leases between operating and finance under IFRS.

Instead, IFRS uses a single lessee accounting model wherein all leases are treated as a financing

arrangement (similar to the Finance Leases per US GAAP).

However, per IFRS, lessee recognition & measurement exemption is available for leases of assets

with low value (less than $5,000). For these low-value leases, lessee may elect to recognize the

payments on a straight-line basis over the lease term (whereby these leases would not be

reflected on lessee’s B/S)

For Lessor -

Sales-type Lease {if any of the “OWNER” criteria is met},

Direct financing lease, or

Operating Lease

Note for IFRS: Lessors classify leases as Operating lease or Finance lease.

That is, no separate classification for sales-type or direct financing lease by Lessor in IFRS; both

classified as Finance lease wherein selling profit is recognized at lease commencement.

Lease term - The non-cancellable period for which a lessee has the right to use an underlying asset,

together with the following optional periods:

Periods covered by an option to extend the lease if the lessee is reasonably certain to exercise

that option

Periods covered by an option to terminate the lease if the lessee is reasonably certain not to

exercise that option

Periods covered by an option to extend (or not to terminate) the lease in which exercise of the

option is controlled by the lessor

Substance over form

IFRS = Single model (all leases

treated as finance lease)

IFRS = Finance lease

FAR-4 Miles CPA Review

F4-28

Lease payments - Payments made by lessee to lessor relating to the use of the underlying asset Note:

For Lessee - For both operating as well as finance leases, Lessee is required to recognize a lease liability (@PV of lease payments to be made) on its B/S However, lessee may elect not to recognize lease liability only for short term leases

(with lease term of 12 months or less) For Lessor - For sales-type and direct financing leases, Lessor recognizes a lease receivable

(@PV of lease payments to be received) as part of its Net Investment in Lease on its B/S However, lessor does not recognize any Net Investment in Lease for its operating leases

Lease payments include: Fixed lease payments

Include in-substance fixed payments - Payments that appear variable but are, in effect, unavoidable. E.g.,

- Payments that do not create genuine variability (such as those that result from clauses that do not have economic substance)

- The lower of the payments to be made when a lessee has a choice about which set of payments it makes, although it must make at least one set of payments

Deduct any lease incentives which include

- Payments made by the lessor to (or on behalf of) the lessee

- Loss incurred by lessor in assuming lessee’s preexisting lease with a third party Include variable lease payments that depend on an index or rate (e.g., Consumer Price

Index or a market interest rate), initially measured using the index or rate at the commencement date E.g., Lease requires $10,000 lease payment per year for 3 years that will increase each year based on CPI. The lease liability is calculated based on $10,000 cash lease payment for each of the 3 years (irrespective of the expectation of changes in CPI). Thereafter, say in year 2, if CPI increases by 4%, actual lease payment will be $10,400 of which $10,000 will be treated as the fixed lease payment (used to calculate lease liability) and $400 will be the variable lease payment (not used to calculate lease liability) However, per IFRS, whenever lease payments change due to a change in an index or rate, the lessee needs to remeasure the lease liability based on the new payment amount of $10,400

Optional payments (if any) - Payments to be made in optional periods only if the lessee is reasonably certain to

exercise the option to extend (or not terminate) the lease Optional payments to purchase the underlying asset only if the lessee is reasonably

certain to exercise that purchase option Residual value guarantees -

For lessees, amounts that it is probable will be owed under residual value guarantees. For lessors, amounts at which residual assets are guaranteed by lessee (or a third party)

Lease payments do not include: Variable lease payments other than those included above

Also, lease payments would not include variable lease payments that are based on the usage or performance of the underlying asset (e.g., % of revenues) E.g., If Lessee is required to make variable lease payments each year of the lease @2% of Lessee’s sales generated from the leased building, this variable payment (which is linked to performance and not based on an index/rate) will not be included in the measurement of the lease liability

Any guarantee by the lessee of the lessor’s debt Amounts allocated to non-lease components of the lease contract

Not

Periodic Lease payments (+) Required buyout by lessee

(+) Optional buyout expected to be exercised by lessee

(+) Residual value guarantees

Miles CPA Review FAR-4

F4-29

Discount rate for the lease - used by lessee to calculate & amortize the lease liability (@PV of lease payments) and by lessor to calculate & amortize the Net Investment in Lease (@PV of lease receivable and any unguaranteed residual)

For Lessor - Use the rate implicit in the lease which is the rate wherein

PV of lease payments + PV of amount that lessor expects to derive from the underlying asset

following the end of the lease term =

FV of the underlying asset minus any related investment tax credit retained and expected to be

realized by the lessor (+) Any deferred initial direct costs of the lessor

For Lessee - Use the rate implicit in the lease if readily determinable Otherwise, use lessee’s incremental borrowing rate (i.e., interest rate that lessee would

have to pay to borrow on a collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment)

For lessees which are non-public entities, may make an accounting policy election to use the risk-free discount rate (determined using a period comparable with that of the lease term) for all leases

Points to note while solving problems on leases on the CPA exams:

Who is the Lessor & who is the Lessee?

When is the commencement date of the lease?

What is the lease term?

What are the lease payments?

What is the discount rate?

What is the type of lease - Operating or finance?

For finance leases, know the amortization schedule

Know the journal entries

i.e., Lessor’s Rate

FAR-4 Miles CPA Review

F4-30

II) Operating Lease

Operating Lease:

From the perspective of a lessee - Any lease other than a finance lease

From the perspective of a lessor - Any lease other than a sales-type lease or a direct financing lease

FASB issued ASC 842 to amend accounting & reporting for leases effective fiscal years beginning after Dec

15, 2018 (for issuers) and effective fiscal years beginning after Dec 15, 2019 (for non-issuers). The most

significant change is the lessee model that brings most leases on the lessee’s B/S (thereby avoiding off-B/S

arrangements). Key change in Lessee accounting for operating leases -

Recognize the assets and liabilities that arise from leases (earlier: this was only required for

finance leases, and was not required for operating leases)

- Liability on B/S: Liability to make lease payments (Lease Liability)

- Asset on B/S: Right-of-use asset representing its right to use the underlying asset for the

lease term (Lease Asset)

Recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease

term on a generally straight-line basis (note: this is unlike finance leases wherein interest expense

and amortization expense are recognized each period)

Lessee exception for short-term leases (term of 1 year or less) - Lessee is permitted to make an

accounting policy election by class of underlying asset not to recognize lease assets and lease

liabilities. If a lessee makes this election, it should recognize lease expense for such leases generally

on a straight-line basis over the lease term

Lessee ≠ OWNER

Miles CPA Review FAR-4

F4-31

II A) Operating Lease – Accounting by Lessee & Lessor

Operating Leases: Accounting by Lessee

At commencement date: CAPITALIZE as Right-of-use Asset on B/S and a corresponding Lease Liability [i.e., operating

leases are no longer off-B/S]. J/E: Right-of-use Asset XXX Lease Liability XXX

Lease Liability is the PV of lease payments not yet paid [as of commencement date] - Exclude any “executory cost” for R&M, insurance or tax paid by lessee

Right-of-use Asset = Lease Liability [as of commencement date] (+) Any lease payments made to the lessor at or before the commencement date (–) Any lease incentives received from the lessor [amortized over lease term] (+) Any initial direct costs incurred by lessee [amortized over lease term]

After commencement date: Record Lease payment as a reduction of Lease Liability. J/E: Lease Liability XXX Cash XXX

Expense a Single Lease Cost on a straight-line basis over the lease term. J/E: Lease Expense XXX

Lease Liability XXX Lease (Right-of-use) Asset (plug) XXX

Use straight-line basis unless another systematic and rational basis better represents the pattern in which the lessee expects to consume the right-of-use asset’s future economic benefits

Note: In a finance lease, lessee recognizes interest expense on I/S (as the lease liability is paid) and amortizes the lease asset. However, in an operating lease, the lessee only recognizes a single lease cost which too is recognized on a straight-line basis (such that the lease expense over the lease term is the same $ every period)

Expense any variable lease payments (which are not included in the Lease Liability) in the period in which the obligation for those payments is incurred

Note: In case of operating leases, the Right-of-use Asset is at the same amount as the Lease Liability adjusted for the following

Prepaid or accrued lease payments

Remaining (unamortized) balance of any lease incentives received

Remaining (unamortized) balance of any initial direct costs

Any impairment of the Right-of-use Asset

Pay off

Interest added

to Amortize

on I/S

No longer off-B/S financing

FAR-4 Miles CPA Review

F4-32

Example #1.A.(i): Operating Lease (Lessee) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 3 years @$25,000 payable at the end of each year. The asset life is 10 years. The rate implicit in the lease is 10%. The lease is an operating lease. Record J/E in Lessee’s books.

PV information: PV of ordinary annuity for 3 years @10% is 2.48685

Solution - Part 1 of 2: At commencement date, recognize Lease Asset & Lease Liability PV of lease payments (note this is ordinary annuity) = $25,000 2.48685 = $62,171 J/E to recognize lease asset and lease liability: 1/1/X1 Lease (Right-of-use) Asset 62,171 Lease Liability 62,171

Solution - Part 2 of 2: After commencement date, recognize Lease Expense on I/S, record Lease Payments (in cash), and amortize the Lease Asset & Lease Liability

Amortization schedule:

J/E #1 J/E #2 B/S

Period Actual Lease

Payment

Lease Expense on

I/S

“Interest” @10% of

Lease Liability CV

Plug for Lease Asset

amortization

Lease Asset CV

Lease Liability CV

Reduces Lease

Liability

Expense on I/S

(straight-line)

Increases Lease

Liability

Reduces Lease Asset

1 (1/1/X1) $62,171 $62,171

1 (12/31/X1) $25,000 $25,000 $6,217 18,783 $43,388 $43,388

2 (12/31/X2) $25,000 $25,000 $4,339 20,661 $22,727 $22,727

3 (12/31/X3) $25,000 $25,000 $2,273 22,727 $0 $0

J/E #1: Actual lease payment:

12/31/X1 12/31/X2 12/31/X3

Lease Liability 25,000 25,000 25,000

Cash 25,000 25,000 25,000

J/E #2: Lease expense:

12/31/X1 12/31/X2 12/31/X3

Lease Expense 25,000 25,000 25,000

Lease Liability 6,217 4,339 2,273

Lease (Right-of-use) Asset [plug] 18,783 20,661 22,727

Miles CPA Review FAR-4

F4-33

Example #1.A.(ii): Operating Lease (Lessee) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 3 years @$20,000 payable at the end of Year 1, $25,000 payable at the end of Year 2 and $30,000 payable at the end of Year 3. The asset life is 10 years. The rate implicit in the lease is 10%. The lease is an operating lease. Record J/E in Lessee’s books.

PV information: PV of $1 @10%: 0.90909 if n=1 year | 0.82645 if n=2 years | 0.75131 if n=3 years

Solution - Part 1 of 2: At commencement date, recognize Lease Asset & Lease Liability PV of lease payments = ($20,000 x 0.90909) + ($25,000 x 0.82645) + ($30,000 x 0.75131) = $61,382 J/E to recognize lease asset and lease liability: 1/1/X1 Lease (Right-of-use) Asset 61,382 Lease Liability 61,382

Solution - Part 2 of 2: After commencement date, recognize Lease Expense on I/S, record Lease Payments (in cash), and amortize the Lease Asset & Lease Liability

Amortization schedule:

J/E #1 J/E #2 B/S

Period Actual Lease

Payment

Lease Expense on

I/S

“Interest” @10% of

Lease Liability CV

Plug for Lease Asset

amortization

Lease Asset CV

Lease Liability CV

Reduces Lease

Liability

Expense on I/S

(straight-line)

Increases Lease

Liability

Reduces Lease Asset

1 (1/1/X1) $61,382 $61,382

1 (12/31/X1) $20,000 $25,000 $6,138 18,862 $42,520 $47,520

2 (12/31/X2) $25,000 $25,000 $4,752 20,248 $22,272 $27,272

3 (12/31/X3) $30,000 $25,000 $2,728 22,272 $0 $0

J/E #1: Actual lease payment:

12/31/X1 12/31/X2 12/31/X3

Lease Liability 20,000 25,000 30,000

Cash 20,000 25,000 30,000

J/E #2: Lease expense:

12/31/X1 12/31/X2 12/31/X3

Lease Expense 25,000 25,000 25,000

Lease Liability 6,138 4,752 2,728

Lease (Right-of-use) Asset [plug] 18,862 20,248 22,272

Pay off

Interest added

to Amortize

on I/S

FAR-4 Miles CPA Review

F4-34

Operating Leases: Accounting by Lessor

At commencement date: Continue to record the underlying asset on its B/S (i.e., no change) Defer any initial direct costs

After commencement date: Recognize on I/S: Lease payments as income over the lease term on a straight-line basis, plus Variable lease

payments as income in the period in which the changes in facts & circumstances on which the variable lease payments are based occur

Use straight-line basis for lease payments unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived

Expense any initial direct costs over the lease term on the same basis as lease income Recognize any applicable depreciation/amortization of the underlying lease asset as

expense

Accounting by Lessor if collectability is not probable at commencement date - Lease income shall be the lesser of the income to be recognized (as calculated above) OR the lease payments (including variable lease payments) that have been collected from the lessee

Example #1.B.(i): Operating Lease (Lessor) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 3 years @$25,000 payable at the end of each year. The asset life is 10 years. The rate implicit in the lease is 10%. The lease is an operating lease. Record J/E in Lessor’s books.

At commencement date: No J/E

After commencement date, recognize Lease Income on I/S (straight line):

12/31/X1 12/31/X2 12/31/X3

Cash 25,000 25,000 25,000

Lease Income 25,000 25,000 25,000

Example #1.B.(ii): Operating Lease (Lessor) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 3 years @$20,000 payable at the end of Year 1, $25,000 payable at the end of Year 2 and $30,000 payable at the end of Year 3. The asset life is 10 years, and incremental borrowing rate is 10%. The lease is an operating lease. Record J/E in Lessor’s books.

At commencement date: No J/E

After commencement date, recognize Lease Income on I/S (straight line):

12/31/X1 12/31/X2 12/31/X3

Cash 20,000 25,000 30,000

Rent Receivable 5,000

Lease Income 25,000 25,000 25,000

Rent Receivable 5,000

Lessor = Owner (PP&E on lessor’s books, even though lessee

records ROU asset)

Miles CPA Review FAR-4

F4-35

II B) Lessee optional election for Short-term Operating Lease

Short-term lease - Lease with a lease term of 12 months or less [do not consider any extension option provided it is reasonably certain that the lessee will not exercise the option] and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise

Lessee exception for short-term leases - As an accounting policy, a lessee may elect not to apply the recognition requirements for Operating Leases [covered in (II A)] to short-term leases – i.e., lessee will NOT recognize any Lease (Right-of-use) Asset or Lease Liability on B/S Lessee will recognize the lease payments on I/S on a straight-line basis over the lease term

(plus variable lease payments in the period in which the obligation for those payments is incurred). J/E:

Lease Expense XXX Cash XXX

The accounting policy election for short-term leases shall be made by class of underlying asset to which the right of use relates

Note: For Lessor, similar accounting for all operating leases (whether or not short-term) – i.e., Lessor recognizes the receipt of lease payments on I/S on a straight-line basis over the lease term (plus variable lease payments in the relevant period). J/E: Cash XXX Lease Income XXX

I/S

I/S

FAR-4 Miles CPA Review

F4-36

Lessee & Lessor F/S: Recap

Lessee F/S

Operating Lease (exception option for short-term lease)

Operating Lease

Lessor F/S

Operating Lease

Assets Liabilities & Equity

B/S I/S

(Lease Expense @straight-line)

Assets Liabilities & Equity

B/S I/S

(Lease Expense @straight-line)

ROU Asset Lease Liability

Assets Liabilities & Equity

B/S I/S

Lease Income @straight-line

(Depreciation expense) PP&E

Miles CPA Review FAR-4

F4-37

III) Finance Lease (from a Lessee perspective)

LESSEE - Must meet any one criteria to treat the lease as a Finance Lease (else, treat as Operating Lease): {“OWNER” – as if the lessor is selling the asset to the lessee and the lessee is the new OWNER}

Ownership transfer - The lease transfers ownership of the underlying asset to the lessee by the end of the lease term Ok if the lessee is required to pay a nominal amount for the transfer (e.g., minimum fee

required by the statutory regulation to transfer ownership)

However, this should not be “optional” for the lessee to pay in which case it may meet the “W” of “OWNER” criteria

Written purchase option - The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise E.g., Lessee has a bargain purchase option to purchase the asset from the lessor at a price

which is estimated to be 50% of the asset’s then fair value E.g., The leased asset is vital to lessee’s business and it is reasonably certain that the lessee

will exercise the purchase option

No alternative use - The underlying asset is of a specialized nature such that it is expected to have no alternative use to the lessor at the end of the lease term In other words, the asset is custom-made for the lessee’s use (and no one else will have any

use for it)

Equal or excess PV - The PV of the sum of the lease payments and any residual value guaranteed by the lessee equals or exceeds substantially all of the FV of the underlying asset Reasonable approach to assess this criteria: PV = 90% or more than FV In other words, lessee is heavily investing in the asset by committing to pay a lot of $

Remaining economic life - The lease term is for the major part of the remaining economic life of the underlying asset Reasonable approach to assess this criteria: Lease term covers 75% or more of the

remaining economic life of the underlying asset In other words, lessee will use the underlying asset for most of its life However, if the commencement date falls at or near the end of the economic life of the

underlying asset (say, in the last 25% of the total economic life of the underlying asset), do not use this criterion to classify the lease

Lease terms are as if

Lessee = “OWNER” of the asset

O Title transfer

E.g., Bargain purchase option

W

N

E

R

Substance over Form =

Even though lessor legally owns the asset (i.e., in “form”),

asset moves from Lessor’s to Lessee’s books (as if Lessee is now the “OWNER”)

FAR-4 Miles CPA Review

F4-38

Finance Leases: Accounting by Lessee

At commencement date: CAPITALIZE as Right-of-use Asset on B/S and a corresponding Lease Liability. J/E:

Right-of-use Asset XXX Lease Liability XXX

Lease Liability is the PV of lease payments not yet paid. Includes PV of: Periodic lease payments

(+) Required buyout (if any) (+) Optional buyout which lessee is expected to exercise (if any) (+) Residual Value guarantees (if expected to be paid by lessee)

Exclude any “executory cost” for R&M, insurance or tax paid by lessee

After commencement date: AMORTIZE the Lease Liability over the lease term. J/E:

Interest Expense XXX Lease Liability XXX

Lease Liability XXX Cash XXX

Use an amortization schedule wherein the lease liability is - Increased to reflect the periodic interest on the lease liability and - Reduced to reflect the lease payments made during the period

AMORTIZE the Right-to-use Asset. J/E: Amortization XXX

Accumulated Amortization XXX

Use straight-line basis unless another systematic and rational basis better represents the pattern in which the lessee expects to consume the right-of-use asset’s future economic benefits

Period for amortization: - If “O” or “W” criteria is met - Amortize over asset useful life - Else if “N”, “E” or “R” criteria is met - Amortize over lesser of useful life or lease term

I/S

I/S

Lessee expense on I/S: Operating Lease = Lease expense (rent)

Finance Lease = Interest + Amortization

Amortize over lease life J/E #2

J/E #3

O W N E R O W N E R

J/E #1

Amortize over lease life or asset life

Miles CPA Review FAR-4

F4-39

Example #2.A: Finance Lease (Lessee) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 5 years @$25,000 payable at the end of each year. The asset life is 10 years and Lessor’s Carrying Value is $120,000. At the end of the lease, estimated residual value of the asset is $60,000; however, Lessee has an option of purchasing the asset for $45,000 that Lessee is reasonably certain to exercise. Lessor incurs no initial direct costs in connection with the lease. The rate implicit in the lease is 10%. In Lessee’s books:

1. Record the Journal Entry to Capitalize the Right-of-use asset & Lease liability 2. Amortize the Lease liability 3. Amortize the Right-of-use asset

(PV of ordinary annuity for 5 years @10% is 3.79079 | PV of $1 after 5 years @10% is 0.62092)

Solution - Part 1 of 2 (Capitalize Asset + Liability): Note: The Lease meets the W of the OWNER criteria. Therefore, Lessee treats it as a Finance Lease while the Lessor treats it as a Sales-type lease.

PV of lease payments = $25,000 3.79079 + $45,000 * 0.62092 = $122,711 Journal entry to capitalize on 1/1/11: Right-of-use Asset 122,711 Lease Liability 122,711

Solution - Part 2 of 3 (Amortize the liability): Amortization schedule:

Period Interest @10% of balance CV

Fixed lease payments

Plug for Lease liability amortization

Lease Liability Carrying Value

1 (1/1/X1) $122,711

1 (12/31/X1) $12,271 ($25,000) ($12,729) $109,982

2 (12/31/X2) $10,998 ($25,000) ($14,002) $95,980

3 (12/31/X3) $9,598 ($25,000) ($15,402) $80,578

4 (12/31/X4) $8,058 ($25,000) ($16,942) $63,636

5 (12/31/X5) $6,364 ($25,000) ($18,636) $45,000

5 (12/31/X5) ($45,000) ($45,000) $0

Journal entries for interest expense: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 Interest expense 12,271 10,998 9,598 8,058 6,364 Lease Liability 12,271 10,998 9,598 8,058 6,364 Journal entries for lease payments: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5

Lease liability 25,000 25,000 25,000 25,000 70,000 Cash 25,000 25,000 25,000 25,000 70,000

Solution - Part 3 of 3 (Amortize the asset): Right-of-use Asset = $122,711 Life of the asset = 10 years (need to amortize over asset life on account of ‘W’ condition) Amortization per year = $122,711 / 10 years = $12,271

Journal entry for asset amortization: 12/31/X1 - 12/31/Y0

Amortization 12,271 Accumulated Amortization 12,271

J/E #3

Lease payments = $170,000

PV of Asset = $122,711

Asset Amortization Expense

$122,711 (10 years)

Interest Expense

$47,289 (5 years)

x 10 years = $122,711

Amortize over asset life (10 years) Amortize over lease life (5 years)

Ordinary Annuity

Total = $47,289

Bargain Purchase @ $170,000

J/E #1

J/E #2

O W N E R

FAR-4 Miles CPA Review

F4-40

Example #3.A: Finance Lease (Lessee) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 5 years @$25,000 payable at the end of each year. The asset life is 10 years. FV of the asset is $132,025 while Lessor’s Carrying Value is $120,000. At the end of the lease, estimated residual value of the asset is $60,000; however, Lessee provides a residual value guarantee of $50,000. Lessor incurs no initial direct costs in connection with the lease. The rate implicit in the lease is 10%. In Lessee’s books:

1. Record the Journal Entry to Capitalize the Right-of-use asset & Lease liability 2. Amortize the Lease liability 3. Amortize the Right-of-use asset

(PV of ordinary annuity for 5 years @10% is 3.79079 | PV of $1 after 5 years @10% is 0.62092)

Solution - Part 1 of 2 (Capitalize Asset + Liability): PV of lease payments (including guaranteed residual) = $25,000 3.79079 + $50,000 * 0.62092 = $125,816 Therefore, the PV is 95% of the FV ($132,025) satisfying the E of the OWNER criteria. Therefore, Lessee treats it as a Finance Lease while the Lessor treats it as a Sales-type lease. However, since the guaranteed residual ($50,000) is less than the estimated residual value ($60,000), it is probable that Lessee will not owe anything under the residual value guarantee. Therefore, on 1/1/X1, Lessee capitalizes Right-of-use asset and Lease liability = $25,000 * 3.79079 = $94,770. Journal entry: Right-of-use Asset 94,770 Lease Liability 94,770

Solution - Part 2 of 3 (Amortize the liability): Amortization schedule:

Period Interest @10% of balance CV

Fixed lease payments

Plug for Lease liability amortization

Lease Liability Carrying Value

1 (1/1/X1) $94,770

1 (12/31/X1) $9,477 ($25,000) ($15,523) $79,247

2 (12/31/X2) $7,925 ($25,000) ($17,075) $62,172

3 (12/31/X3) $6,217 ($25,000) ($18,783) $43,389

4 (12/31/X4) $4,339 ($25,000) ($20,661) $22,728

5 (12/31/X5) $2,272 ($25,000) ($22,728) $0

Journal entries for interest expense: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 Interest expense 9,477 7,925 6,217 4,339 2,273 Lease Liability 9,477 7,925 6,217 4,339 2,273 Journal entries for lease payments: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5

Lease liability 25,000 25,000 25,000 25,000 25,000 Cash 25,000 25,000 25,000 25,000 25,000

Solution - Part 3 of 3 (Amortize the asset): Right-of-use Asset = $94,770 Life of the asset = 5 years (need to amortize over lease life on account of ‘E’ condition) Amortization per year = $94,770 / 5 years = $18,954

Journal entry for asset amortization: 12/31/X1 - 12/31/X5

Amortization 18,954 Accumulated Amortization 18,954

Lease payments = $125,000

PV of Asset = $94,770

Asset Amortization Expense

$94,770 (5 years)

Interest Expense

$30,230 (5 years)

Total = $30,230

$125,000

x 5 years = $94,770

O W N E R

J/E #3

J/E #1

J/E #2

Miles CPA Review FAR-4

F4-41

IV) Sales-type or Direct Financing Lease (from a Lessor perspective)

LESSOR - May account for as

Sales-type Lease - If any one of the “OWNER” criteria is met {“OWNER” – as if the lessor is selling the asset to the lessee and the lessee is the new OWNER}

If none of the OWNER criteria is met - Direct financing Lease - recheck the “E” of “OWNER” criteria wherein:

Any residual value guarantees from any other third party other than the lessee (but unrelated to the lessor) is included in the PV, AND

It is probable that the lessor will collect the lease payments plus any amount necessary to satisfy a residual value guarantee

Operating Lease - any lease other than a sales-type lease or a direct financing lease Note for IFRS: Lessors classify leases as Operating lease or Finance lease. That is, no separate classification for sales-type or direct financing lease by Lessor in IFRS; both classified as Finance lease wherein selling profit is recognized at lease commencement.

Sales-type Lease Direct Financing Lease

Criteria & Lessee classification

Lessee meets one of “OWNER” criteria. Therefore, for Lessee = Finance lease For Lessor = Sales-type lease

Lessee does not meet any of “OWNER” criteria. Therefore for Lessee = Operating lease Recheck “E” criteria by including any third-party residual guarantee. If met, for Lessor = Direct Financing lease (though the lessee classification remains as Operating Lease)

Lessor’s Selling Profit (if any)

Recognized as income upfront Deferred (by including in NIL). Recognized as interest income over the lease term

Lessor’s Initial direct costs (if any)

If FV ≠ CV of underlying asset [at lease commencement] - Expense upfront at lease commencement If FV = CV of underlying asset [at lease commencement] - Deferred (by including in NIL). Reduces interest income over the lease term

Deferred (by including in NIL). Reduces interest income over the lease term

If Lessee = OWNER

If Lessee + 3rd party =

O W N E R

FAR-4 Miles CPA Review

F4-42

Sales-type Lease: Accounting by Lessor At commencement date: Derecognize PP&E (underlying asset). J/E:

Net Investment in Lease XXX Selling loss (if any) XXX

PP&E XXX Selling profit (if any) XXX

Recognize: Net Investment in Lease (NIL) = Lease receivable + Unguaranteed residual asset

- Lease receivable is the PV of: Periodic lease payments (+) Required buyout (if any) (+) Optional buyout which lessee is expected to exercise (if any) (+) Residual Value guarantees (if expected to be paid by lessee or any 3rd party)

- Unguaranteed Residual Asset - PV of amount that lessor expects to derive from the underlying asset following the end of the lease term that is not guaranteed by the lessee (or any other 3rd party)

Selling Profit/Loss = FV of the underlying asset (or the sum of Lease receivable + Lease payments prepaid by the Lessee, if lower)

(-) CV of the underlying asset net of any unguaranteed residual asset (-) Any deferred initial direct costs of the lessor

Initial direct costs of the lessor - - If FV ≠ CV of underlying asset, expense [at commencement date]: - If FV = CV of underlying asset, defer and include in NIL [at commencement date].

During the lease term, reduces the Lessor’s Interest Income Note: Rate implicit in the lease is calculated such that deferred initial direct costs

are included automatically in the NIL (i.e., no need to add them separately). In other words, the rate implicit in the lease is reduced

After commencement date: AMORTIZE the NIL over the lease term. J/E:

Net Investment in Lease (NIL) XXX Interest Income XXX

Cash XXX Net Investment in Lease (NIL) XXX

Use an amortization schedule wherein the NIL is periodically: - Increased to reflect Interest Income on the NIL, and - Reduced to reflect the lease payments received by the lessor during the period

Recognize Variable lease payments (that are not included in the NIL) as income on I/S when changes in facts & circumstances on which the variable lease payments are based occur

At the end of the lease term: If the PP&E (underlying asset) reverts back to the lessor at the end of the lease (e.g., in case

of the “N”, “E” or “R” criteria), need to Test NIL for impairment, and derecognize the entire NIL (which includes both the

guaranteed as well as the unguaranteed residual value) Recognize PP&E (underlying asset)

PP&E XXX Net Investment in Lease (NIL) XXX

PP&E off the books and instead recognize NIL

I/S Amortize over lease life

J/E #2

O W N E R

J/E #1

O W N E R

Operating Lease = Lease Income (–) PP&E Depreciation

Sales-type Lease = Any Selling profit (+) Interest Income

I/S

Miles CPA Review FAR-4

F4-43

Direct Financing Lease: Accounting by Lessor vis-à-vis Sales-type Leases

Selling profit (if any) - Deferred [at the commencement date] and included in NIL. During the lease term, recognized as Lessor’s Interest Income At commencement date: Selling profit (if any) reduces NIL After commencement date: Lessor recognizes the selling profit over the lease term in such a

manner so as to produce, when combined with the interest income on the remainder of NIL, a constant periodic rate of return on the lease

In other words, a discount rate (which is higher than the rate implicit in the lease) is used for direct financing leases with a selling profit to amortize the NIL, such that: - Interest income (on the Lease Receivable and Unguaranteed residual asset)

continues to be at the rate implicit in the lease - The excess Interest income is the deferred selling profit recognized for each period

Initial direct costs - Deferred [at the commencement date] and included in NIL. During the lease term, reduces the Lessor’s Interest Income Note: Rate implicit in the lease is calculated such that deferred initial direct costs are

included automatically in the NIL (i.e., no need to add them separately)

Accounting by Lessor if collectability is not probable at commencement date (for both Sales-type & Direct financing leases) - Lessor shall not derecognize the underlying asset but shall recognize lease payments received (including variable lease payments) as a deposit liability until the earlier of either of the following:

Collectibility of the lease payments, plus any amount necessary to satisfy a residual value guarantee provided by the lessee, becomes probable

Contract has been terminated, and the lease payments received from the lessee are non-refundable

Lessor has repossessed the underlying asset, it has no further obligation under the contract to the lessee, and the lease payments received from the lessee are non-refundable

FAR-4 Miles CPA Review

F4-44

Example #2.B: Sales-type Lease (Lessor) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 5 years @$25,000 payable at the end of each year. The asset life is 10 years and Lessor’s Carrying Value is $120,000. At the end of the lease, estimated residual value of the asset is $60,000; however, Lessee has an option of purchasing the asset for $45,000 that Lessee is reasonably certain to exercise. Lessor incurs no initial direct costs in connection with the lease. The rate implicit in the lease is 10%. In Lessor’s books:

1. Record the journal entry to recognize Net Investment in Lease 2. Amortize the Net Investment in Lease

(PV of ordinary annuity for 5 years @10% is 3.79079 | PV of $1 after 5 years @10% is 0.62092)

Solution - Part 1 of 2 (Recognize NIL): Note: The Lease meets the W of the OWNER criteria. Therefore, Lessee treats it as a Finance Lease while the Lessor treats it as a Sales-type lease.

PV of lease payments = $25,000 3.79079 + $45,000 * 0.62092 = $122,711 Lessor’s Journal entry to record NIL (Net Investment in Lease) on 1/1/X1: NIL - Lease receivable 122,711 PP&E 120,000 Selling profit on lease 2,711

Solution - Part 2 of 2 (Amortize NIL): Amortization schedule:

Period Interest @10% of balance CV

Fixed lease payments

Plug for NIL amortization

NIL Carrying Value

1 (1/1/X1) $122,711

1 (12/31/X1) $12,271 ($25,000) ($12,729) $109,982

2 (12/31/X2) $10,998 ($25,000) ($14,002) $95,980

3 (12/31/X3) $9,598 ($25,000) ($15,402) $80,578

4 (12/31/X4) $8,058 ($25,000) ($16,942) $63,636

5 (12/31/X5) $6,364 ($25,000) ($18,636) $45,000

5 (12/31/X5) ($45,000) ($45,000) $0

Journal entries for interest income: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 NIL - Lease receivable 12,271 10,998 9,598 8,058 6,364 Interest income 12,271 10,998 9,598 8,058 6,364 Journal entries for receipt of lease payments: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 Cash 25,000 25,000 25,000 25,000 70,000 NIL - Lease receivable 25,000 25,000 25,000 25,000 70,000

J/E #1

J/E #2

Lease receipts = $170,000

CV = $120,000

Interest Income

$47,289 (5 years)

Ordinary Annuity

Sale @

off the books

Selling Profit

$2,711

Sale @$122,711

PP&E off the books

$120,000

Total = $47,289

$170,000

Miles CPA Review FAR-4

F4-45

Example #3.B: Sales-type Lease (Lessor) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 5 years @$25,000 payable at the end of each year. The asset life is 10 years. FV of the asset is $132,025 while Lessor’s Carrying Value is $120,000. At the end of the lease, estimated residual value of the asset is $60,000; however, Lessee provides a residual value guarantee of $50,000. Lessor incurs no initial direct costs in connection with the lease. The rate implicit in the lease is 10%. In Lessor’s books:

1. Record the journal entry to recognize Net Investment in Lease 2. Amortize the Net Investment in Lease

(PV of ordinary annuity for 5 years @10% is 3.79079 | PV of $1 after 5 years @10% is 0.62092)

Solution - Part 1 of 2 (Recognize NIL): PV of lease payments (including guaranteed residual) = $25,000 3.79079 + $50,000 * 0.62092 = $125,816 Therefore, the PV is 95% of the FV ($132,025) satisfying the E of the OWNER criteria. Therefore, Lessee treats it as a Finance Lease while the Lessor treats it as a Sales-type lease.

Calculating NIL (Net Investment in Lease):

Lease Receivable (PV of lease payments + guaranteed residual) = $25,000 3.79079 + $50,000 * 0.62092 = $125,816 Residual Asset (PV of unguaranteed residual) = $10,000 * 0.62092 = $6,209 Therefore, NIL = $125,816 + $6,209 = $132,025

Lessor’s Journal entry to record NIL (Net Investment in Lease) on 1/1/X1: NIL - Lease receivable 125,816 NIL - Residual asset 6,209 PP&E 120,000 Selling profit on lease 12,025

Solution - Part 2 of 2 (Amortize NIL): Amortization schedule:

Lease Receivable Residual Asset

Period Interest @10% of

balance CV

Fixed lease payments

Plug for amortization

Carrying Value

Interest @10% of

balance CV

Carrying Value

1 (1/1/X1) $125,816 $6,209

1 (12/31/X1) $12,582 ($25,000) ($12,418) $113,397 $621 $6,830

2 (12/31/X2) $11,340 ($25,000) ($13,660) $99,737 $683 $7,513

3 (12/31/X3) $9,974 ($25,000) ($15,026) $84,711 $751 $8,264

4 (12/31/X4) $8,471 ($25,000) ($16,529) $68,182 $826 $9,091

5 (12/31/X5) $6,818 ($25,000) ($18,182) $50,000 $909 $10,000

Journal entries for interest income: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 NIL - Lease receivable 12,582 11,340 9,974 8,471 6,818 NIL - Residual asset 621 683 751 826 909 Interest income 13,202 12,023 10,725 9,297 7,727

Journal entries for receipt of lease payments: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 Cash 25,000 25,000 25,000 25,000 25,000 NIL - Lease receivable 25,000 25,000 25,000 25,000 25,000

Journal entries at the end of the lease on 12/31/X5 (assuming residual value is $60,000 as per estimate): PP&E 60,000 NIL - Lease receivable 50,000 NIL - Residual asset 10,000

CV = $120,000

Interest Income

$52,975 (5 years)

Selling Profit

$12,025

Sale @$132,025

PP&E off the books

$60,000

PP&E residual

$60,000

Lease receipts = $125,000

Total Interest Income = $52,975 $

49

,18

4

$125,000

(+)

$3

,79

1

J/E #1

J/E #2

off the books

FAR-4 Miles CPA Review

F4-46

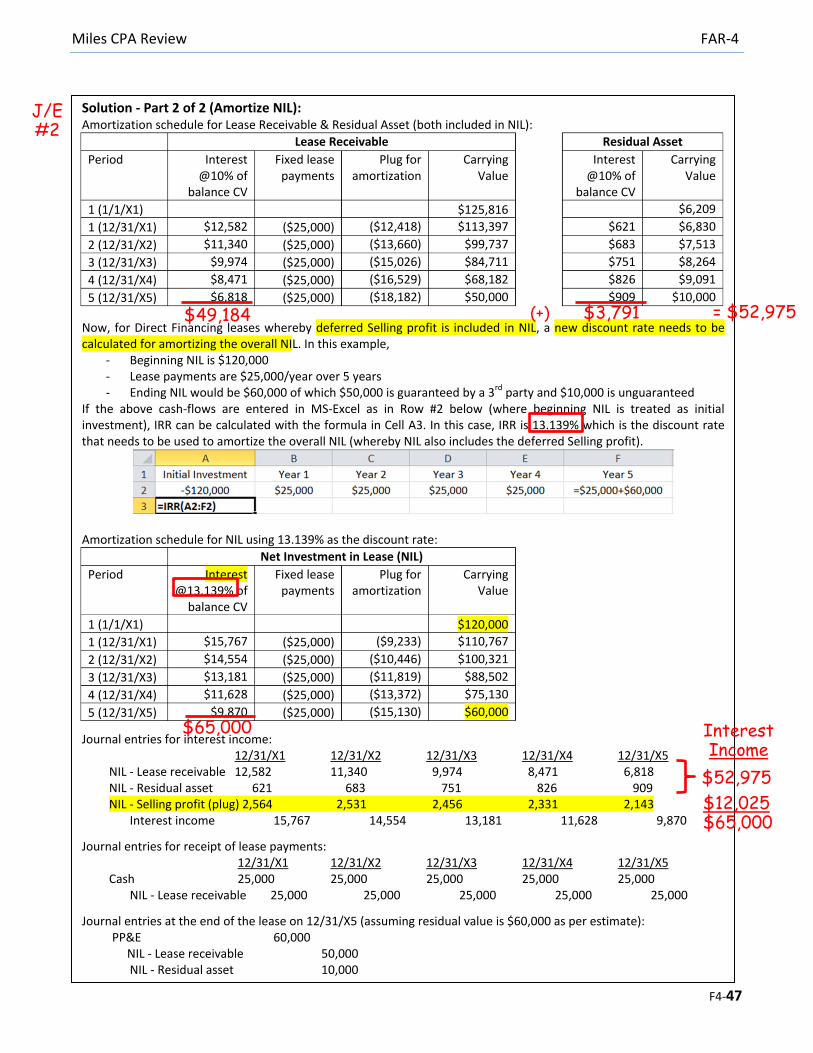

Example #3.C: Direct Financing Lease (Lessor) On 1/1/X1 Lessee Co. leases from Lessor Co. equipment for 5 years @$25,000 payable at the end of each year. The asset life is 10 years. FV of the asset is $132,025 while Lessor’s Carrying Value is $120,000. At the end of the lease, estimated residual value of the asset is $60,000; however, a third party has provides a residual value guarantee of $50,000. Ignore any initial direct costs that the Lessor incurs in connection with the lease. The rate implicit in the lease is 10%. In Lessor’s books:

1. Record the journal entry to recognize Net Investment in Lease 2. Amortize the Net Investment in Lease

(PV of ordinary annuity for 5 years @10% is 3.79079 | PV of $1 after 5 years @10% is 0.62092)

Solution - Part 1 of 2 (Recognize NIL): Lease classification:

- PV of lease payments = $25,000 * 3.79079 = $94,770. Therefore, the PV is <90% of the FV ($132,025) and the

E of the OWNER criteria is not satisfied. Therefore, Lessee classifies it as an Operating Lease - Now, if the sum of PV guarantee by the third party ($50,000 x 0.62092 = $31,046) is added to the PV of lease

payments ($94,770), the total ($125,816) is >=90% of the FV ($132,025). Therefore, Lessor classifies it as a Direct Financing Lease

Calculating NIL (Net Investment in Lease):

Lease Receivable (PV of lease payments + guaranteed residual) = $25,000 3.79079 + $50,000 * 0.62092 = $125,816 Residual Asset (PV of unguaranteed residual) = $10,000 * 0.62092 = $6,209 Less: Selling Profit (deferred) = $12,025 Therefore, NIL = $125,816 + $6,209 - $12,025 = $120,000

Lessor’s Journal entry to record NIL (Net Investment in Lease) on 1/1/X1: NIL - Lease receivable 125,816 NIL - Residual asset 6,209 PP&E 120,000 NIL - Selling profit (deferred) 12,025

Continued on next page …

Lessee = Operating

Lessor = Direct Financing

Unlike Sales-type lease, Selling profit is deferred

CV = $120,000

Interest Income

$52,975 (5 years)

$65,000

Selling Profit

$12,025

PP&E off the books

$60,000

PP&E residual

$60,000

Lease receipts = $125,000

J/E #1

FV @$132,025

Lessor I/S

Sales-type Lease = Any Selling profit (+) Interest Income

Direct Financing Lease = Interest Income

off the books

Miles CPA Review FAR-4

F4-47

Solution - Part 2 of 2 (Amortize NIL): Amortization schedule for Lease Receivable & Residual Asset (both included in NIL):

Lease Receivable Residual Asset

Period Interest @10% of

balance CV

Fixed lease payments

Plug for amortization

Carrying Value

Interest @10% of

balance CV

Carrying Value

1 (1/1/X1) $125,816 $6,209

1 (12/31/X1) $12,582 ($25,000) ($12,418) $113,397 $621 $6,830

2 (12/31/X2) $11,340 ($25,000) ($13,660) $99,737 $683 $7,513

3 (12/31/X3) $9,974 ($25,000) ($15,026) $84,711 $751 $8,264

4 (12/31/X4) $8,471 ($25,000) ($16,529) $68,182 $826 $9,091

5 (12/31/X5) $6,818 ($25,000) ($18,182) $50,000 $909 $10,000

Now, for Direct Financing leases whereby deferred Selling profit is included in NIL, a new discount rate needs to be calculated for amortizing the overall NIL. In this example,

- Beginning NIL is $120,000 - Lease payments are $25,000/year over 5 years - Ending NIL would be $60,000 of which $50,000 is guaranteed by a 3rd party and $10,000 is unguaranteed

If the above cash-flows are entered in MS-Excel as in Row #2 below (where beginning NIL is treated as initial investment), IRR can be calculated with the formula in Cell A3. In this case, IRR is 13.139% which is the discount rate that needs to be used to amortize the overall NIL (whereby NIL also includes the deferred Selling profit).

Amortization schedule for NIL using 13.139% as the discount rate:

Net Investment in Lease (NIL)

Period Interest @13.139% of

balance CV

Fixed lease payments

Plug for amortization

Carrying Value

1 (1/1/X1) $120,000

1 (12/31/X1) $15,767 ($25,000) ($9,233) $110,767

2 (12/31/X2) $14,554 ($25,000) ($10,446) $100,321

3 (12/31/X3) $13,181 ($25,000) ($11,819) $88,502

4 (12/31/X4) $11,628 ($25,000) ($13,372) $75,130

5 (12/31/X5) $9,870 ($25,000) ($15,130) $60,000

Journal entries for interest income: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 NIL - Lease receivable 12,582 11,340 9,974 8,471 6,818 NIL - Residual asset 621 683 751 826 909 NIL - Selling profit (plug) 2,564 2,531 2,456 2,331 2,143 Interest income 15,767 14,554 13,181 11,628 9,870

Journal entries for receipt of lease payments: 12/31/X1 12/31/X2 12/31/X3 12/31/X4 12/31/X5 Cash 25,000 25,000 25,000 25,000 25,000 NIL - Lease receivable 25,000 25,000 25,000 25,000 25,000

Journal entries at the end of the lease on 12/31/X5 (assuming residual value is $60,000 as per estimate): PP&E 60,000 NIL - Lease receivable 50,000 NIL - Residual asset 10,000

Interest Income

$65,000

$49,184 $3,791 (+) = $52,975

$12,025 $65,000

$52,975

J/E #2

FAR-4 Miles CPA Review

F4-48

Lessee & Lessor F/S: Recap

Lessee F/S

Operating Lease (exception option for short-term lease)

Operating Lease

Finance Lease

Assets Liabilities & Equity

B/S I/S

(Lease Expense @straight-line)

Assets Liabilities & Equity

B/S I/S

(Lease Expense @straight-line)

ROU Asset Lease Liability

Assets Liabilities & Equity

B/S I/S

(Amortization of ROU Asset)

(Interest Expense on Lease Liability) ROU Asset Lease Liability

Total expense is front-loaded (i.e., higher in initial years)

Miles CPA Review FAR-4

F4-49

Lessor F/S

Operating Lease

Sales-type Lease

Direct Financing Lease

Assets Liabilities & Equity

B/S I/S

Lease Income @straight-line

(Depreciation expense) PP&E On lessor’s books

Assets Liabilities & Equity

B/S I/S

Interest Income

Selling Profit/(Loss) if any @Year 1

Initial direct costs (if FV ≠ CV) @Year 1

PP&E Off lessor’s books

NIL

Assets Liabilities & Equity

B/S I/S

Interest Income

(Selling Loss) if any @Year 1

PP&E Off lessor’s books

NIL

FAR-4 Miles CPA Review

F4-50

V) Other Lease Accounting Considerations

V A) Presentation Matters

B/S I/S C/F [per US GAAP]

LESSEE

Operating

(Option for

Short-term

Lease)

N/A - Lease Expense

- Variable Lease Expense (if applicable)

Operating

Operating Right-of-use (ROU) Asset

Lease Liability

- Lease Expense

- Variable Lease Expense (if applicable)

Operating

Finance Right-of-use (ROU) Asset

Lease Liability

- Amortization Expense (ROU Asset)

- Interest Expense (on Lease Liability)

- Variable Lease Expense (if applicable)

Lease Liability:

- Principal portion =

Financing

- Interest portion =

Operating

LESSOR

Operating

(whether or

not Short-

term Lease)

PP&E (underlying asset)

Initial direct costs

During lease term:

- Lease Income

- Variable Lease Income (if applicable)

- Initial direct costs

Operating

Sales-type

Lease

PP&E

Net Investment in Lease =

Lease Receivable +

Unguaranteed residual asset +

Initial direct costs (if FV = CV at

commencement date)

At commencement date:

- Selling profit/loss (if any)

- Initial direct costs (if FV ≠ CV)

During lease term:

- Interest Income

- Variable Lease Income (if applicable)

- Impairment (if any)

Operating

Direct

financing

Lease

PP&E

Net Investment in Lease =

Lease Receivable +

Unguaranteed residual asset +

Selling profit (if any) + Initial

direct costs

At commencement date:

- Selling loss (if any)

During lease term:

- Interest Income

- Variable Lease Income (if applicable)

- Impairment (if any)

Operating

Miles CPA Review FAR-4

F4-51

Lessee - Points to note regarding presentation

B/S

Report in B/S (or disclose in Notes to F/S)

Separate $ for

- Operating lease right-of-use assets, and

- Finance lease right-of-use assets

Separate $ for

- Operating lease liabilities, and

- Finance lease liabilities

If a lessee does not present operating lease and finance lease right-of-use assets and lease

liabilities separately in B/S, the lessee shall disclose which line items in B/S include those

right-of-use assets and lease liabilities

Prohibited from presenting both of the following:

Operating lease right-of-use assets in the same line item as finance lease right-of-use

assets

Operating lease liabilities in the same line item as finance lease liabilities

I/S

For operating leases, the lease expense should be evaluated and classified as COGS, SG&A

or another operating expense line item

For finance leases, the interest expense on the lease liability and amortization of the right-

of-use asset shall be presented in a manner consistent with how the entity presents other

interest expense and depreciation/amortization of similar assets, respectively (note that

these are not required to be presented as separate line items)

C/F

Payments arising from operating leases – classify as operating activities

Payments arising from finance leases -

Repayments of the principal portion of the lease liability - classify as financing activities

Interest on the lease liability - classify as operating activity

Variable lease payments not included in the lease liability - classify as operating

activities

FAR-4 Miles CPA Review

F4-52

Disclosures - Lessee shall disclose qualitative & quantitative info about all of the following: Lessee’s leases

Information about the nature of its leases (as well as any subleases), including:

- General description of those leases

- Basis and terms & conditions on which variable lease payments are determined

- Existence and terms & conditions of options to extend or terminate the lease. Lessee should provide narrative disclosure about the options that are recognized as part of its right-of-use assets and lease liabilities and those that are not

- Existence and terms & conditions of residual value guarantees provided by lessee

- Restrictions or covenants imposed by leases; e.g., those relating to dividends or incurring additional financial obligations

Information about leases that have not yet commenced but that create significant rights and obligations for the lessee, including the nature of any involvement with the construction or design of the underlying asset

Any lease transactions between related parties Disclose if lessee accounts uses the exception for short-term leases (and thereby avoids

B/S recognition of right-of-use asset and lease liability). If the short-term lease expense for the period does not reasonably reflect lessee’s short-term lease commitments, lessee shall disclose that fact and the amount of its short-term lease commitments

Significant judgments made in applying lease accounting requirements including Determination of whether a contract contains a lease Allocation of the consideration in a contract between lease and non-lease components

Determination of the discount rate for the lease Amounts recognized in the F/S relating to those leases

Disclose the following amounts relating to a lessee’s total lease cost, which includes both amounts recognized in I/S during the period, any amounts capitalized on B/S and the cash flows arising from lease transactions:

- Finance lease cost, segregated between the amortization of the right-of-use assets and interest on the lease liabilities

- Operating lease cost

- Short-term lease cost, excluding expenses relating to leases with a lease term of one month or less

- Variable lease cost

- Sublease income, disclosed on a gross basis, separate from the finance or operating lease expense

- Net gain or loss recognized from sale and leaseback transactions

- Amounts segregated between those for finance & operating leases for the following items: Cash paid for amounts included in the measurement of lease liabilities,

segregated between operating and financing cash flows Supplemental noncash information on lease liabilities arising from obtaining

right-of-use assets Weighted-average remaining lease term Weighted-average discount rate

Miles CPA Review FAR-4

F4-53

Lessor - Points to note regarding presentation

B/S

For Operating leases - The underlying asset subject to an operating lease continues to be

presented as PP&E

For Sales-Type and Direct Financing leases - Present lease assets (i.e., the aggregate of the

lessor’s Net Investment in sales-type leases and direct financing leases) separately from

other assets

I/S

Income arising from leases should be either presented in I/S or disclose in the notes

If a lessor does not separately present lease income in I/S, the lessor shall disclose which

line items include lease income in I/S

For Sales-Type and Direct Financing leases - Present any profit or loss on the lease

recognized at the commencement date in a manner that best reflects the lessor’s business

model(s). Examples of presentation include the following:

If a lessor uses leases as an alternative means of realizing value from the goods that it

would otherwise sell, the lessor shall present revenue and COGS relating to its leasing

activities in separate line items so that income and expenses from sold and leased items

are presented consistently

- Revenue recognized is the lesser of:

FV of the underlying asset at the commencement date

Sum of the lease receivable and any lease payments prepaid by the lessee

- COGS is the carrying amount of the underlying asset at the commencement date

minus the unguaranteed residual asset

If a lessor uses leases for the purposes of providing finance, the lessor shall present the

profit or loss in a single line item

C/F

Classify cash receipts as operating activities (applies for Operating leases as well as Sales-

Type and Direct Financing leases)

FAR-4 Miles CPA Review

F4-54

Disclosures - Lessor shall disclose qualitative & quantitative info about all of the following: Lessor’s leases

Information about the nature of its leases, including:

- General description of those leases

- Basis and terms & conditions on which variable lease payments are determined

- Existence and terms & conditions of options to extend or terminate the lease

- Existence and terms & conditions of options for lessee to purchase the underlying asset

Any lease transactions between related parties Disclose information about how it manages its risk associated with the residual value of

its leased assets. In particular, a lessor should disclose all of the following:

- Risk management strategy for residual assets

- Carrying amount of residual assets covered by residual value guarantees (excluding guarantees considered to be lease payments for the lessor)

- Any other means by which the lessor reduces its residual asset risk (e.g., buyback agreements or variable lease payments for use in excess of specified limits)

Significant judgments made in applying lease accounting requirements including Determination of whether a contract contains a lease Allocation of the consideration in a contract between lease and non-lease components Determination of the amount the lessor expects to derive from the underlying asset

following the end of the lease term Amounts recognized in the F/S relating to those leases

Disclose lease income recognized in each annual and interim reporting period, in a tabular format, to include the following:

- For sales-type leases and direct financing leases: Profit or loss recognized at the commencement date Interest income either in aggregate or separated by components of NIL

- For operating leases, lease income relating to lease payments

- Lease income relating to variable lease payments not included in the measurement of the lease receivable

Disclose components of its aggregate NIL in sales-type and direct financing leases (i.e., the carrying amount of lease receivables, unguaranteed residual assets, and any deferred selling profit on direct financing leases)

Additional disclosures for sales-type leases and direct financing leases:

- Explain significant changes in the balance of its unguaranteed residual assets and deferred selling profit on direct financing leases

- Disclose a maturity analysis of its lease receivables, showing the undiscounted cash flows to be received on an annual basis for a minimum of each of the first 5 years and a total of the amounts for the remaining years. Disclose a reconciliation of the undiscounted cash flows to the lease receivables recognized in B/S

Additional disclosures for operating leases:

- Disclose a maturity analysis of lease payments, showing the undiscounted cash flows to be received on an annual basis for a minimum of each of the first 5 years and a total of the amounts for the remaining years Note: This maturity analysis need to be disclosed separately from the maturity

analysis required for sales-type leases and direct financing leases

Miles CPA Review FAR-4

F4-55

V B) Lease and non-lease components

Components of a contract - Required to identify the lease and non-lease components of a contract that contains a lease. A contract may also contain multiple lease components

When a contract includes multiple components, need to allocate the consideration in the contract to the various components

Consideration attributable to non-lease components is not a lease payment and, therefore, is not included in the measurement of lease assets or lease liabilities

Separate the various lease components within the contract (e.g., lease of land and movable

equipment in one contract)

An entity shall consider the right to use an underlying asset to be a separate lease component (i.e., separate from any other lease components of the contract) if both of the following criteria are met: The lessee can benefit from the right of use either on its own or together with other

resources that are readily available to the lessee The right of use is neither highly dependent on nor highly interrelated with the other

right(s) to use underlying assets in the contract

Also, separate the lease components from the non-lease components (e.g., maintenance)

Consideration in the contract is allocated to the lease and non-lease components on a relative standalone price basis (for lessees) or in accordance with the Revenue Recognition standards (for lessors)

Consideration attributable to non-lease components is not a lease payment and, therefore, is not included in the measurement of lease assets or lease liabilities

Exception For lessees (practical expedient) - Lessees may make an accounting policy election by class

of underlying asset not to separate lease components from non-lease components. If an entity makes this accounting policy election, it is required to account for the non-lease component together with the related lease components as a single lease component

For lessors (practical expedient) - Lessors may make an accounting policy election by class of underlying asset not to separate lease components from non-lease components

Allowed only if the non-lease components otherwise would be accounted for under the new revenue recognition standards and both of the following are met:

- The timing and pattern of transfer of the non-lease component(s) and associated lease component are the same

- The lease component, if accounted for separately, would be classified as an operating lease

Thereafter,

- If the non-lease component(s) are the predominant component of the combined component, account for the combined component in accordance with Revenue Recognition standards

- Else, account for the combined component as an operating lease

FAR-4 Miles CPA Review

F4-56

Example: Allocation of Consideration to Lease and Non-lease Components of a Contract Lola leases a bulldozer, a truck, and a crane to Tony to be used in Tony’s construction operations for 4 years. Lola also agrees to maintain each piece of equipment throughout the lease term. The total consideration in the contract is $500,000, payable in $125,000 annual installments. The standalone prices for the various components of the lease are as follows: Rental Maintenance Rental + Maintenance Bundle

Bulldozer $190,000 $40,000 $220,000 Truck $120,000 $15,000 $130,000 Crane $215,000 $45,000 $250,000 Total $525,000 $100,000 $600,000

Tony concludes that the leases of the bulldozer, the truck, and the crane are each separate lease components. Allocate the consideration between the various components for Tony assuming:

1. Tony accounts for the non-lease maintenance services components separate from the three separate lease components

2. Tony makes an accounting policy election to use the practical expedient to not separate non-lease from lease components for its leased construction equipment

Solution 1 of 2 (Allocation of consideration to lease and non-lease components of a contract): Tony allocates the consideration in the contract ($500,000) to the lease and non-lease components on a relative basis, utilizing the observable standalone prices:

Rental Maintenance Bulldozer $152,000 $32,000 Truck $96,000 $12,000 Crane $172,000 $36,000 Total $420,000 $80,000

Solution 2 of 2 (Lessee elects practical expedient to not separate lease from non-lease components): Tony does not separate the maintenance services from the related lease components but, instead, accounts for the contract as containing only 3 lease components. Tony allocates the consideration in the contract ($500,000) to the 3 separate lease components on a relative basis utilizing the observable standalone selling price of each separate lease component (inclusive of maintenance services): Rental + Maintenance Bundle

Bulldozer $183,333 Truck $108,333 Crane $208,333 Total $500,000

Miles CPA Review FAR-4

F4-57

Example: Activities or Costs that are not components of a contract Lessor and Lessee enter into a 5-year lease of a building. The contract designates that Lessee is required to pay for the costs relating to the asset, including the real estate taxes and the insurance on the building. The real estate taxes would be owed by Lessor regardless of whether it leased the building and who the lessee is. Lessor is the named insured on the building insurance policy (that is, the insurance protects Lessor’s investment in the building, and Lessor will receive the proceeds from any claim). How should the lessee treat the payment of taxes and insurance if:

1. The annual lease payments are fixed at $12,000 per year, while the annual real estate taxes and insurance premium will vary and be billed to Lessee each year.

2. Fixed annual lease payment is $15,000. There are no additional payments for real estate taxes or building insurance; however, the fixed payment is itemized in the contract (that is, $12,000 for rent, $1,800 for real estate taxes, and $1,200 for building insurance).

Solution 1 of 2 (Payments for Taxes and Insurance are Variable): The real estate taxes and the building insurance are not components of the contract. The contract includes a single lease component— the right to use the building. Lessee’s payments of those amounts solely represent a reimbursement of Lessor’s costs and do not represent payments for goods or services in addition to the right to use the building. However, because the real estate taxes and insurance premiums during the lease term are variable, those payments are variable lease payments that do not depend on an index or a rate and are excluded from the measurement of the lease liability and recognized in I/S as expense. Solution 2 of 2 (Payments for Taxes and Insurance are Fixed): Similar to Solution (1) above, the taxes and insurance are not components of the contract. The contract includes a single lease component, the right to use the building. The $75,000 in payments Lessee will make over the 5-year lease term are all lease payments for the single component of the contract and, therefore, are included in the measurement of the lease liability.

Example: Common Area Maintenance as a component of a contract Leo owns a building in which he leases an office space to Tanya for 3-years in return for a fixed annual payment of $20,000. The annual payment includes rent of $17,500 and common area maintenance of $2,500. Is common area maintenance a separate component of the lease? Solution: Common area maintenance is a component because Leo’s activities transfer services to Tanya. That is, Tanya receives a service from Leo in the form of the common area maintenance activities it would otherwise have to undertake itself or pay another party to provide (e.g., cleaning the lobby for its customers, removing snow from the parking lot for its employees and customers, and providing utilities). Therefore, the contract includes two components—a lease component (i.e., the right to use the building) and a non-lease component (common area maintenance). And the $60,000 consideration in the contract is allocated between those 2 components (i.e., $52,500 for the lease component, and $7,500 for the common area maintenance). The amount of $52,500 allocated to the lease component is the lease payments in accounting for the lease.

FAR-4 Miles CPA Review

F4-58

V C) Initial direct lease costs

Initial direct costs for a lessee or a lessor - Costs to negotiate or arrange a lease. These are

incremental costs of a lease that would not have been incurred if the lease had not been obtained

May include:

Commissions

Payments made to an existing tenant to incentivize that tenant to terminate its lease

Does NOT include costs that would have been incurred regardless of whether the lease was

obtained including:

Fixed employee salaries

General overheads (like depreciation, occupancy and equipment costs, unsuccessful

origination efforts, and idle time)

Costs related to activities performed by the lessor for advertising, soliciting potential

lessees, servicing existing leases, or other ancillary activities

Costs related to activities that occur before the lease is obtained, such as costs of obtaining

tax or legal advice, negotiating lease terms and conditions, or evaluating a prospective

lessee’s financial condition

Accounting for Initial direct lease costs

Lease classification Accounting for Initial Direct Costs (IDCs)

Lessee Operating lease

Defer IDCs by including in Right-of-use asset. Expense over lease term

Finance Lease

Lessor Operating lease Defer IDCs (as Other Assets / Deferred costs). Expense over the lease

term on the same basis as lease income

Sales-type lease

if FV ≠ CV of

underlying asset [at

lease

commencement]

Expense IDCs upfront at lease commencement

Sales-type lease

if FV = CV of

underlying asset [at

lease

commencement]

Defer IDCs by including in Net Investment in Lease (NIL). Reduces the

Lessor’s Interest Income over the lease term

Note: Rate implicit in the lease is calculated such that deferred initial

direct costs are included automatically in the NIL (i.e., no need to add

them separately). In other words, the rate implicit in the lease is

reduced Direct financing

lease

Miles CPA Review FAR-4

F4-59

Example: Initial Direct Costs (Lessee & Lessor) Lessee and Lessor enter into an operating lease. The following costs are incurred in connection with the lease:

Travel costs related to lease proposal $5,000 External legal fees 8,000 Allocation of employee costs for time negotiating lease terms and conditions 4,000 Commissions to brokers 9,000 Total costs incurred by Lessor 26,000

External legal fees $7,000 Allocation of employee costs for time negotiating lease terms and conditions 6,000 Payments made to existing tenant to obtain the lease 12,000 Total costs incurred by Lessee 25,000

Calculate the amount treated as Initial Direct Costs for: (1) Lessor, (2) Lessee

Solution - Part 1 of 2 (Lessor’s Initial Direct Costs): Lessor capitalizes initial direct costs of $9,000, which it recognizes ratably over the lease term, consistent with its recognition of lease income. The $9,000 in broker commissions is an initial direct cost because that cost was incurred only as a direct result of obtaining the lease (that is, only as a direct result of the lease being executed). None of the other costs incurred by Lessor meet the definition of initial direct costs because they would have been incurred even if the lease had not been executed. For example, the employee salaries are paid regardless of whether the lease is obtained, and Lessor would be required to pay its attorneys for negotiating and drafting the lease even if Lessee did not execute the lease.

Solution - Part 2 of 2 (Lessee’s Initial Direct Costs): Lessee includes $12,000 of initial direct costs in the initial measurement of the right-of-use asset. Lessee amortizes those costs ratably over the lease term as part of its total lease cost. Throughout the lease term, any unamortized amounts from the original $12,000 are included in the measurement of the right-of-use asset. The $12,000 payment to the existing tenant is an initial direct cost because that cost is only incurred upon obtaining the lease; it would not have been owed if the lease had not been executed. None of the other costs incurred by Lessee meet the definition of initial direct costs because they would have been incurred even if the lease had not been executed (for example, the employee salaries are paid regardless of whether the lease is obtained, and Lessee would be required to pay its attorneys for negotiating and drafting the lease even if the lease was not executed).

= Lessor’s IDC

= Lessee’s IDC

FAR-4 Miles CPA Review

F4-60

V D) Leasehold Improvements

Leasehold improvements - Improvements made by the lessee to the underlying leased asset (such

as additions, alterations, remodeling, or renovations)

Recognized separately from the underlying Right-of-use Asset. Amortized over the below

period:

Operating lease - Amortize over lesser of useful life or lease term

Finance lease -

If “O” or “W” criteria is met - Amortize over asset useful life

Else if “N”, “E” or “R” criteria is met - Amortize over lesser of useful life or lease term

Miles CPA Review FAR-4

F4-61

VI) Sale Leaseback

Property is sold by the owner and immediately leased back again with the original owner/seller

NOT giving up possession or use of the property on sale

Done mainly for cash management - Seller needs cash as well as continued possession/use of

the property

Determining whether the transfer of the asset is a “Sale” in the first place

If the “leaseback” is an operating lease (from seller-lessee’s perspective), transfer of the asset

is a “Sale”

Accounting by seller-lessee -

Recognize the “Sale” of the transferred asset (per the Revenue Recognition standards).

Therefore, the carrying amount of the underlying asset is now derecognized (since it’s

sold!)

Account for the lease as an Operating lease

Accounting by buyer-lessor -

Recognize the transferred asset (since the asset is purchased by the buyer-lessor!)

Account for the lease as an Operating lease

If the “leaseback” is a finance lease (from seller-lessee’s perspective), transfer of the asset is

NOT a “Sale” (i.e., treat as if no “Sales” has happened)

Rationale: Seller-lessee has not satisfied any performance obligation per Step 5 of the

Revenue Recognition standards [since control of the asset is not transferred to the buyer-

lessor]

Accounting by seller-lessee -

Do not derecognize the transferred asset (since no “sales” has happened per the

Revenue Recognition standards!)

Account for the amount received (from the buyer-lessor) as a financial liability

Accounting by buyer-lessor –

Do not recognize the transferred asset (since no “sales” has happened!)

Account for the amount paid (to the seller-lessee) as a receivable

Leaseback: “Re”-Transfers right to use property

Seller is

Lessee

Sale: Transfers ownership of property Buyer

is Lessor

2 separate &

distinct

transactions

Transfer of the asset is a Sale

No Sale!

FAR-4 Miles CPA Review

F4-62