AT & S Austria Technologie & Systemtechnik Aktiengesellschaft | Fabriksgasse13 | A-8700 Leoben Tel +43 (0) 3842 200-0 | E-Mail [email protected] www.ats.net AT&S first choice for advanced applications Company Presentation February 2015

AT&S Company Presentation February 2015

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AT & S Austria Technologie & Systemtechnik Aktiengesellschaft | Fabriksgasse13 | A-8700 Leoben

Tel +43 (0) 3842 200-0 | E-Mail [email protected]

www.ats.net

AT&Sfirst choice for advanced applications

Company Presentation

February 2015

1

Company Overview

Strategy & Market

Annex

Financials

Table of Contents

2

AT&S – a world leading high-tech PCB company

� Megatrend-driven

markets with attractive

growth potential

� Entering a new high-end

business segment by

2016

� Pure high-end segment play

� Technology & quality leader

� Largest European PCB

producer

� Partner of choice for blue

chip customer base

� Balanced industry portfolio

� Strong Asian production

footprint with focus on

high volume/low mix

� European footprint: high

mix/low volume

� Operational excellence:

Outstanding process

know-how, productivity

and efficiency

� One of the most profitable

players in the industry:

above industry EBITDA

margins

� Strong cash flow generation

� Proven long term successful

financial track record

3

AT&S – Key Facts

Strong track record1 Balanced portfolio/Global customer base2

488514

542590

489

96 103 102127 127

47 42 3154 71

2010/11 2011/12 2012/13 2013/14 Q1-3

2014/15

Revenue EBITDA EBIT

+5% +5% +9%

Revenue growth 7%

In E

UR

m

3

Distribution revenue: Business Unit

Distribution revenue: Customer Region

57%

43%

Mobile Devices &

Substrates

Industrial &

Automotive (inkl.

Medical)

25%

6%

17%

52%

Germany/Austria

Other European

countries

Asia

Americas

4

Global footprint ensures cost efficiency

� European production facilities: high mix/low volume

� Asian production facilities: high volume/low mix

� Sales network spanning three continents

� About ~7,600 employees

Plant Shanghai, China

Staff: ~4.500

Plant Ansan, Korea

Staff: ~250

Plant Nanjangud, India

Staff: ~1.100

Plant Chongqing, China

under construction

Staff: ~500

AT&S Sales OfficesAT&S Plants

Plant Leoben, Austria

Headquarters

Staff: ~ 900

Plant Fehring, Austria

Staff: ~350

►► volatility due to seasonal effects

5

Balanced high-end product portfolio

to level seasonalityCharacteristicCharacteristic Selected ApplicationsSelected ApplicationsSegmentSegment

1) Based on external revenue EUR m in Q3 2014/15

Mobile Devices &

Substrates

Advanced

Packaging

Selected Market

Leaders

Selected Market

Leaders

GoPro

Sony

LG

Canon

Qualcomm

Blackberry

Lenovo

Huawei

Samsung

Xiaomi

ZTE

Intel

Apple

►► stable business due to longer product life

time

� Includes the segment Advanced Packaging (still in the

process of being established) as well as group

management and financial activitiesOthers

(Revenue in EUR m)

(Revenue in EUR m)

Industrial & Auto-

motive & Medical

Revenue

Share1)

Revenue

Share1)

Communication

Computing

Automotive:

Lighting, thermal, sensors,

safety, infotainment,

powertrain

Medical:

Patient monitoring,

Therapy, diagnostic

Industrial:

Instrumentation &

Control, power

solutions, lighting

Consumer

Electronics

Osram

Hella

Siemens

General Electric

Continental

Harmann

EADS

Texas Instruments

ST Microelectronics

Freescale

Semiconductor

RFMD

TDK-Epcos

Qualcomm

74.5 90.1 87.7

69.0 68.0 88.7

120.9

Q1 13/14 Q2 13/14 Q3 13/14 Q4 13/14 Q1 14/15 Q2 14/15 Q3 14/15

57%

43%

66.4 66.3 62.9

69.7 72.6 71.7

65.9

Q1 13/14 Q2 13/14 Q3 13/14 Q4 13/14 Q1 14/15 Q2 14/15 Q3 14/15

6

Company Overview

Strategy & Market

Annex

Financials

Table of Contents

7

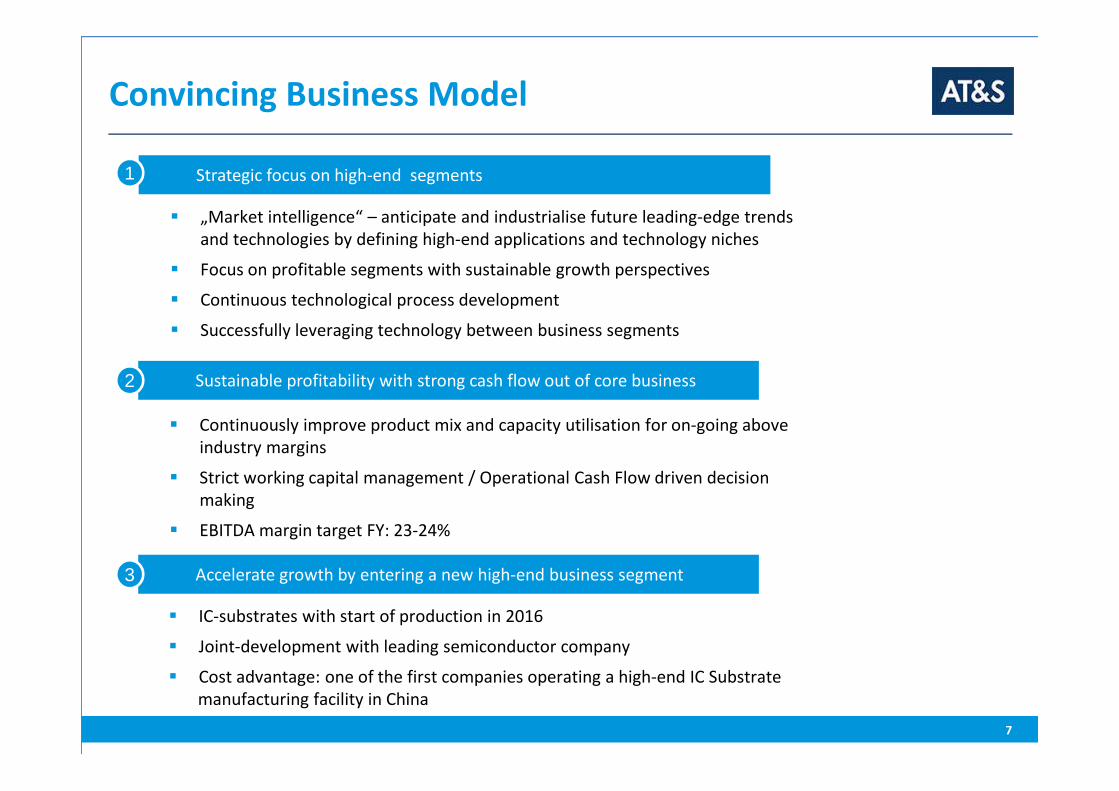

Convincing Business Model

Level of complexity

Strategic focus on high-end segments

� „Market intelligence“ – anticipate and industrialise future leading-edge trends

and technologies by defining high-end applications and technology niches

� Focus on profitable segments with sustainable growth perspectives

� Continuous technological process development

� Successfully leveraging technology between business segments

Sustainable profitability with strong cash flow out of core business

� Continuously improve product mix and capacity utilisation for on-going above

industry margins

� Strict working capital management / Operational Cash Flow driven decision

making

� EBITDA margin target FY: 23-24%

Accelerate growth by entering a new high-end business segment

� IC-substrates with start of production in 2016

� Joint-development with leading semiconductor company

� Cost advantage: one of the first companies operating a high-end IC Substrate

manufacturing facility in China

1

2

3

8

PCB Market Growth outperforms E-Systems Market

1) Market Size 2013 , in USD bn / Source: Prismark, April 2014 2) AT&S addressable Market Size 2013, in USD bn / Source: BPA, Prismark, AT&S, 2013-2014 3)excl. IC Substrates

Business Unit Industry/E-Systems Market Selected Applications E-Systems Market 1)

CAGR 2013-2018

PCB Market Size 2)

CAGR 2013-2018

Mobile Devices

& Substrates

Computing Notebooks, PCs, Server 490 bn 2.7% 17.0 bn 3.1%

Communications Smartphones, Tablets 482 bn 3.1% 15.3 bn 3.7%

Consumer Electronics Cameras 147 bn 3.5% 6.4bn 3%

SubstratesMicroprocessors, Graphic

Processors7.6 bn 4.9%

Industrial &

Automotive &

Medical

Industrial & MedicalInstrumentation & Control,

Therapy, Diagnostic253 bn 5.8%

3.2 bn 12.9%

Medical 1.3 bn 6.8%

AutomotiveLighting, sensors, safety,

infotainment, powertrain178 bn 6.5% 4.3 bn 7.1%

Total Market Size3)

CAGR 2013-20181,678 bn 3.8% 47.5 bn 4.4%

9

Market Player/Position HDI Technology

Source: Prismark, August 2014; NTI CY2013; AT&S Strategy

Market position HDI Technology

Revenue (in USD m)

Rank Country Supplier HDINon HDI

PCB´s

IC-

Substrates

Total

revenue

1 TWN Unimicron 682 671 795 2.148

2 TWN Compeq 538 509 - 1.047

3 AUT AT&S 530 248 - 778

4 KOR SEMCO 480 173 1.212 1.865

5 JPN Ibiden 426 - 1.080 1.506

6 USA TTM 406 962 - 1.368

7 TWN Zhen Ding 343 1.774 - 2.117

8 TWN Tripod 305 1.077 - 1.382

9 KOR DAP 279 21 - 300

10 TWN Unitech 236 304 - 540

(as of 31/12/2014)

Completion of

Infrastructure

Start Equipment

Characterisation

Certification

Start

Training

Start Equipment

Ordering

Plant Lay-out

Product-

Specification

Start of Production

�

10

�

�

�

�

Q4 Q1 Q2 Q3

FY 2013/14

Q4 Q1 Q2 Q3

FY 2014/15

Q3FY 2012/13

Q4 Q1 Q2 Q3

FY 2015/16

Q4 Q1 Q2 Q3

FY 2016/17

Q4

� Investment as at 31/12/2014: € 171.7 m1)

� Characterisations and certification for first line is ongoing

� Start of negotiations about the product mix and the ramp scenarios.

Management Board expects the negotiations to be concluded in the

coming months.

� Start of production is scheduled for 2016

Project Status IC Substrate plant Chongqing

1)Additions to tangible fixed assets as of 31/12/2014 since project start

Start Equipment Installation

11

Driving Future Trends: Internet of Things (IoT) and

Application Structures

� Healthcare

� Glasses

Wearable ElectronicsWearable Electronics

Smart Mobility Smart Mobility � Autonomous Driving

� Car2Car Communication

Smart CitySmart City � Smart Lighting

Smart BuildingsSmart Buildings � Home/Building Automatisation

� Energy Management

Smart Production/Industry 4.0Smart Production/Industry 4.0 � Automatisation/Robotics

� Production Control Systems

Smart HealthcareSmart Healthcare � Connectivity (e.g. online patient

monitoring)

Smart EnergySmart Energy � Smart Metering

� 30-50 Billion of „Things“ will be connected in 2020

� Wearables market forecast: USD 10 – 60 bn by 2018Source: IHS, 2013

12

Company Overview

Strategy & Market

Annex

Financials

Table of Contents

13

Sound top-line growth, above industry margins

and increasing cash conversion

2010/11 2011/12 2012/13 2013/14 � Continuous growth path up to full capacity

utilisation

� Revenue with products out of Asian production

increased from 69% in 2010/11 to 76% in 2013/14

� Next significant step-up in growth: start of

production of IC-substrate in Chongqing in 2016

EBITDA

AND

EBITDA-MARGIN

OPERATING CASH

FLOW / Y-O-Y

DEVELOPMENT

� EBITDA increase due to high capacity utilisation

� Continuous conversion to more high-end product

mix

� EBITDA margin guidance FY: 23-24%

� Operating cash flow generation driven by strong

EBITDA performance

488 514542 590 489

7187

72105 95

Selected Key Financials (EUR m)Selected Key Financials (EUR m)

REVENUE /

Y-O-Y GROWTH

96 103 102 127 127

19.7% 20.0% 18.8%21.5%

26.0%

Q1-3

2014/15

14

Efficient operational cost base

106

75 8296

106114

23,6%

20,1%

16,8%18,6% 19,5% 19,3%

Working Capital Working Capital % of Sales

Working Capital Development in EUR m

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

15

Staff and Capex

STAFF*The increased headcount is primarily based on

the Chongqing project. Decreased number of

staff in core business reflects improved

productivity.

CAPEX (€ in million)

CAPEX increase reflects technology investments in

existing locations and investments in Chongqing

project (whereof € 74m).

Regular Business Employees Project ChongqingCAPEX end of reporting period FY

CAPEX end of reporting period Q1-Q3

* incl. temporary employees , average for the period

115 113

40

90

69.7

130.4

2010/11 2011/12 2012/13 2013/14 Q1-Q3

2013/14

Q1-Q3

2014/15

6,9877,417 7,321

7,0277,526

2010/11 2011/12 2012/13 2013/14 Q1-Q3

2014/15

123539

54

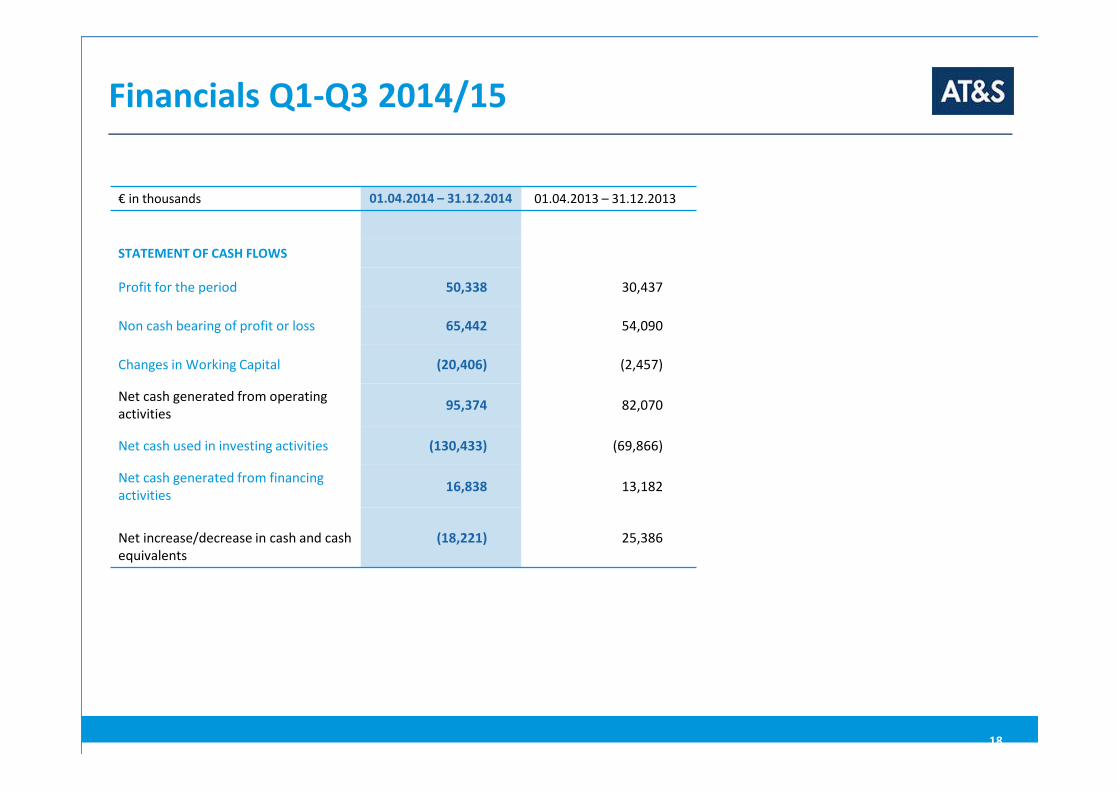

Financials Q1-Q3 2014/15

16

€ in thousands (unless otherwise

indicated)

01.04.2014- 31.12.2014 01.04.2013 – 31.12.2013

STATEMENT OF PROFIT OR LOSS

Revenue 489,416 450,947

produced in Asia 79% 76%

produced in Europe 21% 24%

EBITDA 127,284 100,138

EBITDA margin 26.0% 22.2%

EBIT 70,811 43,458

EBIT margin 14.5% 9.6%

Finance income/(costs) - net (4,376) (9,088)

Income Taxes (16,097) (3,933)

Profit for the period 50,338 30,437

Cash Earnings 106,751 87,084

EPS in € (average number of shares

outstanding)1.29 1.08

Strong sales, improved product mix combined with cost savings translate into strong EBITDA/EBIT

Financials Q1-Q3 2014/15

17

€ in thousands (unless otherwise

indicated)31.12.2014 31.03.2014

STATEMENT OF FINANCIAL POSITION

Non-current assets 624,052 483,858

Current assets 473,496 432,201

Equity 502,803 390,680

Non-current liabilities 403,312 370,336

Current liabilities 191,433 155,043

Total assets 1,097,548 916,059

Net debt 153,716 110,874

Net gearing 30.6% 28.4%

Net working capital 111,432 91,722

Net working capital per revenues 17.1% 15.6%

Equity ratio 45.8% 42.7%

Based on the strong operating performance increase of debt could be limited

Financials Q1-Q3 2014/15

18

€ in thousands 01.04.2014 – 31.12.2014 01.04.2013 – 31.12.20131)

STATEMENT OF CASH FLOWS

Profit for the period 50,338 30,437

Non cash bearing of profit or loss 65,442 54,090

Changes in Working Capital (20,406) (2,457)

Net cash generated from operating

activities95,374 82,070

Net cash used in investing activities (130,433) (69,866)

Net cash generated from financing

activities16,838 13,182

Net increase/decrease in cash and cash

equivalents

(18,221) 25,386

19

€ in millions < 1 Year 1-5 Years > 5 Years Total

Corporate Bond 0.6 99.6 - 100.2

Export Loans 32.0 - - 32.0

Public funds and other - 2.6 1.4 4.0

Bank Borrowings 14.4 204.2 49.5 268.1

Total 31/12/2014 47.0 306.4 50.9 404.3

Total 31/03/2014 46.0 282.9 43.0 371.9

Maturity

Overview Debt Portfolio Duration

AT&S - Stock Profile

Listing Vienna Stock Exchange, Prime Standard

Indices ATX Prime, WBI

ThomsonReuters (A) ATSV.VI

Bloomberg (A) ATS AV

# of shares outstanding 38.85m

Avg. daily volume 65,000

2014 abs performance 24.51%

Dividend 2013/14: EUR 0.20/per share

Dividend yield: 2.3%

Calendar

Annual Results 2014/15 7 May 2015

21st Annual General Meeting 9 July 2015

1st Quarter Results 2015/15 28 July 2015

Ex-dividend day &

dividend payment day 30 July 2015

20

YTD price development/liquidity & Shareholder structure

*including direct and indirect holdings

*

*

ATX Prime AT&S

21

Outlook FY 2014/15

Based on the positive business development of the first nine months and

taking into account the seasonality in the mobile devices & substrates

segment in the fourth quarter – and provided that the macroeconomic

environment and the current exchange rates remain stable – we will enhance

the outlook for the financial year 2014/15: we expect revenue amounting to

€ 623-633 million (previous year: € 589.9 million) and an EBITDA margin

between 23 and 24% (previous year: 21.6%).

22

Company Overview

Strategy & Market

Annex

Financials

Table of Contents

23

HDI microvia printed

circuit boards

HDI any-layer printed

circuit boards

IMS printed

circuit boards

Multilayer

printed circuit boards

AT&S Product Portfolio

Double-sided printed

circuit boards

Flexible printed circuit

boards

Semiflexible printed

circuit boards

Rigid-flexible printed

circuit boards

Flexible printed circuit

boards on aluminium

HDI rigid-flex

printed circuit boards

Management

24

Andreas Gerstenmayer, CEO

� Joined AT&S as CEO in 2010

� Previous positions include:

− 18 years of work experience at Siemens, including Managing Director with Siemens Transportation Systems

GmbH Austria and CEO of the Drive Technology business unit in Graz from 2003 to 2008

− Partner at FOCUSON Business Consulting GmbH after leaving Siemens

� Education and other positions:

− Member of the Research Council of Styria

− Degree in Production Engineering from Rosenheim University of Applied Sciences

Heinz Moitzi, COO

� COO since 2005; with AT&S since 19811)

� Previous positions include:

− Various management positions within AT&S

− Measurement engineer with Leoben University of Mining and Metallurgy

� Education:

− Degree from Higher Technical College of Electrical Engineering

− Studied electrical installation with Stadtwerke Judenburg (Judenburg municipal utility company)

Karl M. Asamer, CFO

� Joined AT&S as CFO in 2014

� Previous positions include:

− Managing Director of GEKA Group in Germany

− Managing Director of Sell GmbH in Germany

� Education:

− Degree: doctorate in business administration in Linz, Austria

1)He was already with the founding company of AT&S

1) High Density Interconnect (laser-drilled printed circuit boards)

25

History

2013 � Collaboration agreement with leading semiconductor

manufacturer to enter IC substrate market

2011 � Acquisition of land and start of construction of a high-end

plant in Chongqing, China

2010 � Relocation of Group Headquarters from Vienna to Leoben

� Ramp-Up plant II in Nanjangud

2009 � Restructuring and reorientation of Leoben plant towards high-

value industrial business

� Focusing Shanghai on high-end mobile devices segment

2008 � Relisting on the Vienna Stock Exchange (Prime Market)

2006 � AT&S buys flexible plant in Korea

2002 � Start of production in new AT&S plant in Shanghai – one of the

world’s leading HDI1) facilities

1999 � AT&S listed on the Neuer Markt at the Frankfurt Stock

Exchange

� AT&S buys PCB plant in India

1994 � Privatisation and acquisition by Hannes Androsch, Willibald

Dörflinger and Helmut Zoidl

1987 � Foundation of AT&S

Five core dimensions of sustainability within AT&S

Energy and

carbon footprintWater

AT&S – a learning

organisationResourcesThinking ahead –

shaping the future

CSR gains importance in long term success

� Improving efficiency

� Motivated and qualified staff

CSR as a key to sustainable business success

26

The importance of sustainability is rising within:

� Authorities

(basis for securing operation licences)

� Customers

(relevant for placing orders)

AT&S saves CO2 and Water…

27

Sustainability – Figures and Fields of Action

AT&S aims to minimise its

environmental footprint by

reducing the CO2 emissions

per m2 PCB attributable to

production processes by 5%

a year.

AT&S aims to reduce

the Group‘s annual

fresh water

consumption per m2

PCB by 3%.

Visit: www.ats.net; Twitter @AT&S IR_PR; YouTube AtundS

28

AT&S – first choice for advanced applications

IR Contact:

Elke Koch

Fabriksgasse 13,

8700 Leoben/Austria

Tel: +43 3842 200 5925

Mobile: +43 676 8955 5925

Fax: +43 3842 200 15909

www.ats.net

Disclaimer

29

This presentation is provided by AT & S Austria Technologie & Systemtechnik Aktiengesellschaft, having its headquarter at Fabriksgasse 13, 8700 Leoben, Austria(“AT&S”), and the contents are proprietary to AT&S and for information only.

AT&S does not provide any representations or warranties with regard to this presentation or for the correctness and completeness of the statements contained therein,and no reliance may be placed for any purpose whatsoever on the information contained in this presentation, which has not been independently verified. You areexpressly cautioned not to place undue reliance on this information.

This presentation may contain forward-looking statements which were made on the basis of the information available at the time of preparation and on management‘sexpectations and assumptions. However, such statements are by their very nature subject to known and unknown risks and uncertainties. As a result, actualdevelopments, results, performance or events may vary significantly from the statements contained explicitly or implicitly herein.

Neither AT&S, nor any affiliated company, or any of their directors, officers, employees, advisors or agents accept any responsibility or liability (for negligence orotherwise) for any loss whatsoever out of the use of or otherwise in connection with this presentation. AT&S undertakes no obligation to update or revise any forward-looking statements, whether as a result of changed assumptions or expectations, new information or future events.

This presentation does not constitute a recommendation, an offer or invitation, or solicitation of an offer, to subscribe for or purchase any securities, and neither thispresentation nor anything contained herein shall form the basis of any contract or commitment whatsoever. This presentation does not constitute any financial analysisor financial research and may not be construed to be or form part of a prospectus. This presentation is not directed at, or intended for distribution to or use by, anyperson or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would becontrary to law or regulation or which would require any registration or licensing within such jurisdiction.

Related Documents

![Investor Presentation - February 2015 [Company Update]](https://static.cupdf.com/doc/110x72/577c87a01a28abe054c4c28a/investor-presentation-february-2015-company-update.jpg)

![Investor Presentation - February 2016 [Company Update]](https://static.cupdf.com/doc/110x72/577c879f1a28abe054c4c05b/investor-presentation-february-2016-company-update.jpg)