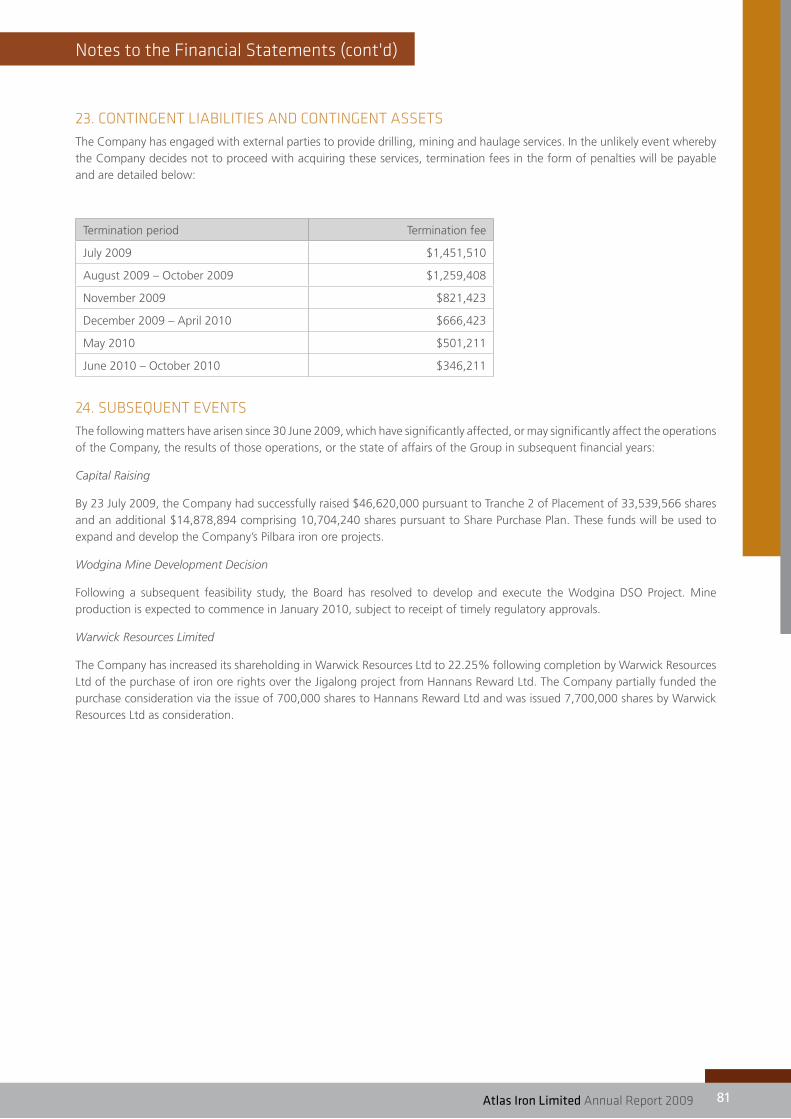

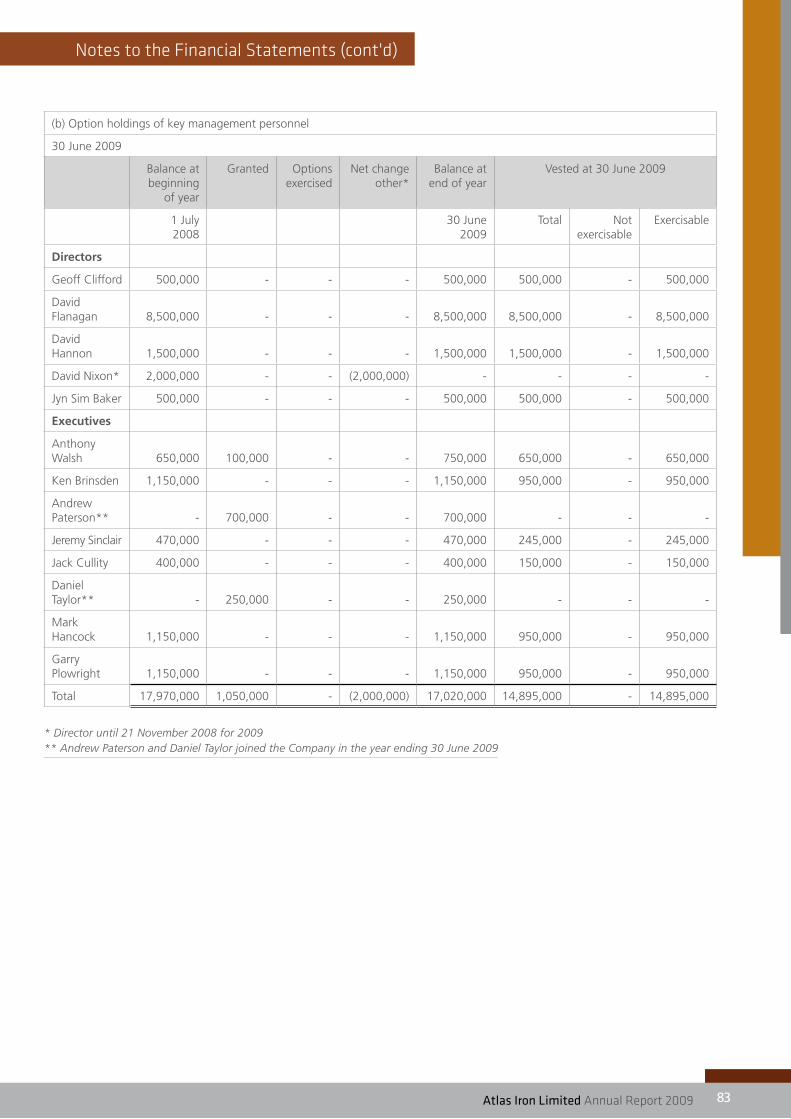

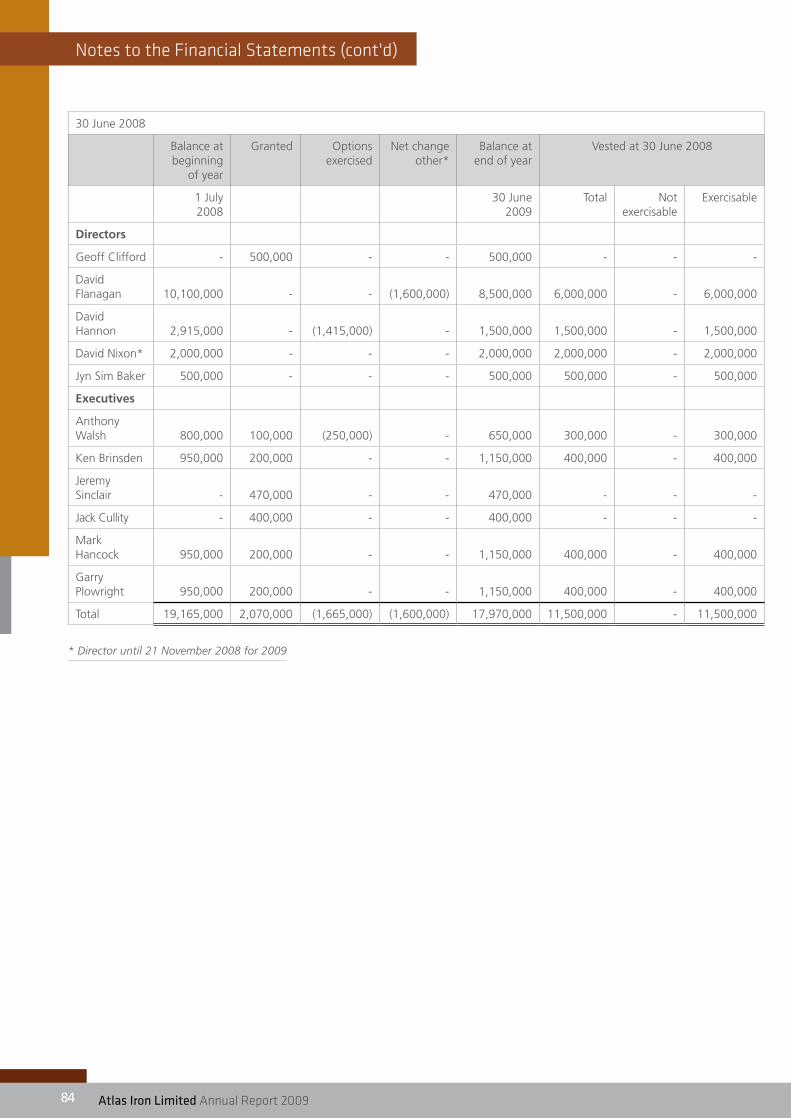

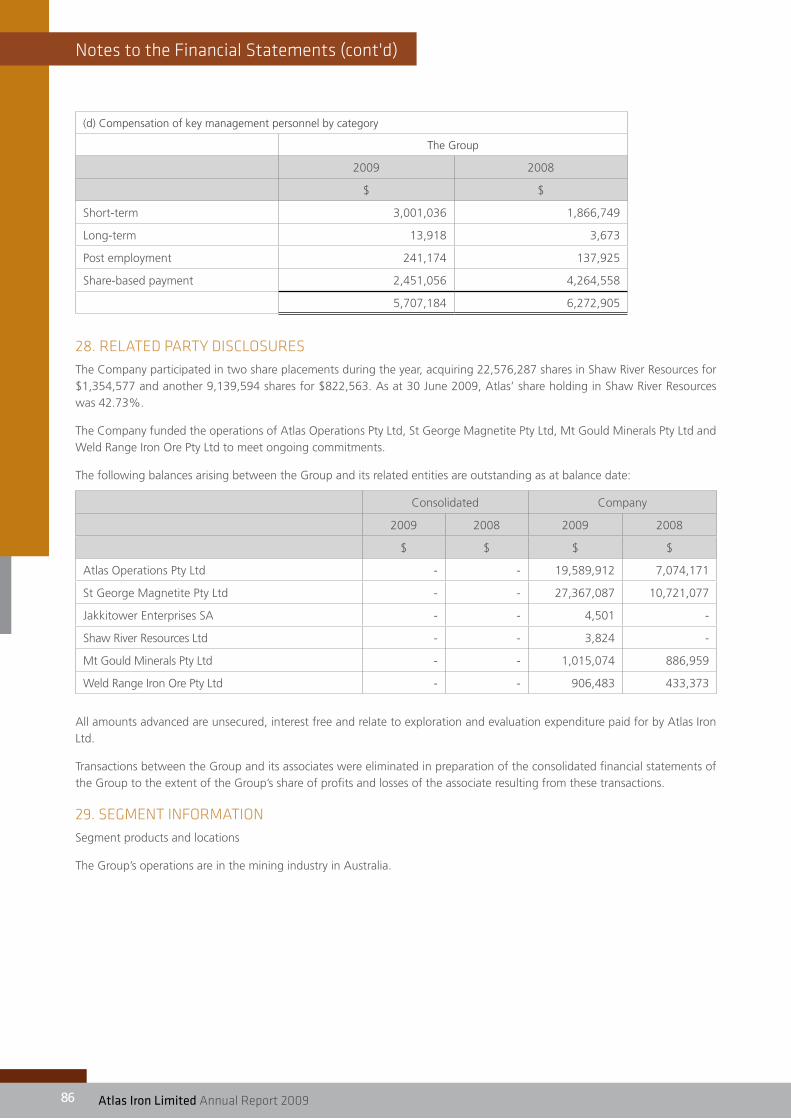

ANNUAL REPORT 2009

Atlas Iron Annual Report 2009

Mar 28, 2016

Atlas is an Australian-owned mineral exploration and mining company which prides itself on its commitment to principles of environmental and social responsibility.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANNUAL REPORT 2009

2

The Company

Corporate InformatIon atLaS' VaLUeS

ABN 63 110 396 168

DiRECTORsGeoff Clifford (Non Executive Chairman)

David Flanagan (Managing Director)

David Hannon (Non Executive Director)

Jyn Sim Baker (Non Executive Director)

COmPANy sECRETARiEsAnthony Walsh

Mark Hancock

REgisTERED OffiCE Ground Floor, 10 Richardson Street

West Perth WA 6005

+61 (0) 8 9476 7900

sOLiCiTORsBlake Dawson

2 The Esplanade

Perth WA 6000

BANkERsNational Australia Bank Limited

100 St. Georges Terrace

Perth WA 6000

shARE REgisTERSecurity Transfer Registrars Pty Ltd

Alexandrea House

Suite 1, 770 Canning Highway

Applecross WA 6153

AUDiTORsStantons International

Level 1, 1 Havelock Street

West Perth WA 6005

iNTERNET ADDREsswww.atlasiron.com.au

AsX CODEShares AGO

DO ThE RighT ThiNg •We are judged by our family and society; make sure

they are proud of everything we do.

BE vERy gOOD AT whAT wE DO •Be safe; minimise impact on the environment; and strive

for and promote excellence in all activities.

kiss A fEw fROgs •Look at and review many opportunities for discovery

and improvement.

LEAvE A fOOTPRiNT •Ensure that wherever we operate we leave a lasting and

strong positive impact.

iNDOmiTABLE sPiRiT •Be resilient and encourage resilience in the face of

challenges.

wiN-wiN •Create long term successful relationships and

engagement where everyone benefits.

ENgAgE EmPLOyEEs •Communicate and work to achieve the business

objectives in a supportive environment.

tabLe of ContentS

2009 Financial Year – Highlights 2

Environment and the Community 3

Operations Review 6

- Overview 6

• Pardoo DSO Project 7

• Wodgina DSO Project 10

• Abydos DSO Project 14

• Mt Webber DSO Project 16

• Turner River DSO Project 18

• Midwest DSO Projects 18

• Ridley Magnetite Project 19

Corporate Activities 21

Sales and Marketing 23

Competent Persons and JORC Compliance Statements 24

Corporate Governance Statement 26

Directors’ Report 36

Income Statement 51

Balance Sheet 52

Statement of Changes in Equity 53

Statement of Cash Flows 54

Notes to the Financial Statements 55

Directors’ Declaration 94

Independent Auditor's Report 95

Auditor’s Independence Letter 97

ASX Additional Information 98

Content

atlas Iron Limited Annual Report 2009 1

2 atlas Iron Limited Annual Report 20092

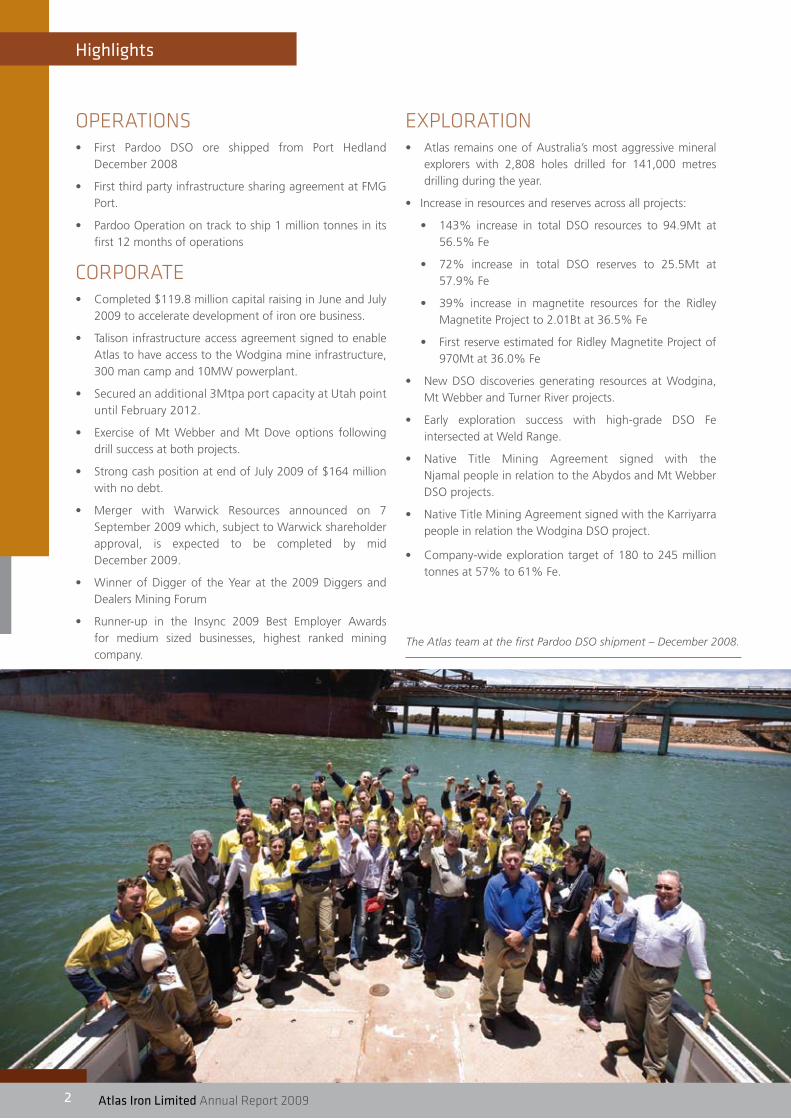

OPERATiONs First Pardoo DSO ore shipped from Port Hedland •December 2008

First third party infrastructure sharing agreement at FMG •Port.

Pardoo Operation on track to ship 1 million tonnes in its •first 12 months of operations

CORPORATE Completed $119.8 million capital raising in June and July •2009 to accelerate development of iron ore business.

Talison infrastructure access agreement signed to enable •Atlas to have access to the Wodgina mine infrastructure, 300 man camp and 10MW powerplant.

Secured an additional 3Mtpa port capacity at Utah point •until February 2012.

Exercise of Mt Webber and Mt Dove options following •drill success at both projects.

Strong cash position at end of July 2009 of $164 million •with no debt.

Merger with Warwick Resources announced on 7 •September 2009 which, subject to Warwick shareholder approval, is expected to be completed by mid December 2009.

Winner of Digger of the Year at the 2009 Diggers and •Dealers Mining Forum

Runner-up in the Insync 2009 Best Employer Awards •for medium sized businesses, highest ranked mining company.

EXPLORATiON Atlas remains one of Australia’s most aggressive mineral •explorers with 2,808 holes drilled for 141,000 metres drilling during the year.

Increase in resources and reserves across all projects:•

143% increase in total DSO resources to 94.9Mt at •56.5% Fe

72% increase in total DSO reserves to 25.5Mt at •57.9% Fe

39% increase in magnetite resources for the Ridley •Magnetite Project to 2.01Bt at 36.5% Fe

First reserve estimated for Ridley Magnetite Project of •970Mt at 36.0% Fe

New DSO discoveries generating resources at Wodgina, •Mt Webber and Turner River projects.

Early exploration success with high-grade DSO Fe •intersected at Weld Range.

Native Title Mining Agreement signed with the •Njamal people in relation to the Abydos and Mt Webber DSO projects.

Native Title Mining Agreement signed with the Karriyarra •people in relation the Wodgina DSO project.

Company-wide exploration target of 180 to 245 million •tonnes at 57% to 61% Fe.

•

Highlights

2 atlas Iron Limited Annual Report 20092

The Atlas team at the first Pardoo DSO shipment – December 2008.

atlas Iron Limited Annual Report 2009 3

Environment and the Community

enVIronment and tHe CommUnIty

Our team are doing a fantastic job of environmental best practice, demonstrating community engagement and social responsibility to providing positive win-win outcomes for the people we interact with. This achievement has been recognised throughout the Pilbara region.”

David Flanagan, Managing Director

With a strong devotion to investment in people, the community and project development, Atlas has endeavoured to set new standards of environmental best practice, community engagement and social responsibility leaving a lasting positive footprint within the areas it operates. During the past year, Atlas has entered into two unique Native Title agreements, to progress access to developing mining centres within the Pilbara region of Western Australia.

In addition to the construction and operation of the Pardoo DSO mine Atlas has also undertaken high level environmental impact assessments covering the two subsequent DSO projects at Wodgina and Abydos. It has involved multiple Aboriginal Heritage surveys, detailed flora and vegetation studies, terrestrial and subterranean fauna surveys, along with impact determination assessments to provide for ongoing and sustainable operations.

ENviRONmENTIn a year of growth in Atlas' environment and land access activities, Atlas has successfully negotiated the state approval regime for the Pardoo DSO Project, developed and implemented compliance procedures, and completed various impact assessments for new mining and exploration projects. Through the engagement and coordination of respected specialist consultants, Atlas successfully completed the Public Environmental Review (PER) assessment and provided effective and achievable Project Environmental Management Plans for the on-going operations. (Hotlink to announcement on environmental approval: www.atlasiron2009ar.com)

Over the past twelve months Atlas has built on the standards, legislations, procedures and systems to identify, assess and manage environmental risk in the areas in which it operates.

Throughout 2009, Atlas has successfully built on its reputation as a responsible proponent within the exploration/mining industry. Atlas has further enhanced its reputation with the ongoing and strategic engagement of indigenous groups, government departments, non-government organisations, land holders, and key stakeholders to ensure all aspects of its activities exceed the legal and social obligations, and are undertaken in a meaningful and sustainable manner. One of the beneficiaries of this engagement is the NorthWest Iron Ore Alliance community fund.

Atlas is an Australian-owned mineral exploration and mining company which prides itself on its commitment to principles of environmental and social responsibility. In accordance with this Environmental and Social Policy, the following operational-specific objectives have been established which represent Atlas' commitment:

Atlas will operate an Integrated Management System 1. (IMS), which accurately defines the environmental and social aspects and impacts of what we do, and build what we learn from this knowledge into clear and concise operational systems, to thus minimise the risk to the environment and the community.

Atlas will employ, to the extent practicable, the principles 2. of pollution prevention, efficient resource use and waste minimisation in all of our activities.

Atlas will set environmental improvement targets based on 3. established criteria and annually report our environmental performance publicly.

Atlas will develop a mine completion and rehabilitation plan 4. that addresses regulatory requirements, risk minimisation, potential future land use and stakeholder issues.

Atlas will identify, report, and remediate environmental 5. incidents, and employ changes that reduce the likelihood and/or consequence of occurrences.

Atlas will actively promote environmental awareness and 6. training among all employees and contractors.

Atlas will respect cultural and heritage values and facilitate 7. cross-cultural awareness.

Atlas will anticipate and respond to community 8. concerns, aspirations and values regarding our activities and foster open dialogue with employees, contractors and the community.

Atlas will strive for continual improvement in environmental 9. and social awareness, and our performance.

Atlas will comply with all legal and regulatory requirements 10. as a minimum operating condition.

Atlas will allocate sufficient resources to ensure these 11. objectives can be achieved.

4 atlas Iron Limited Annual Report 20094

Environment and the Community (cont'd)

By implementing this policy Atlas believes it will:

Ensure that environmental obligations and considerations •form an integral part of our business planning and decision-making processes.

Comply with applicable environmental laws and aspire to •higher standards within our business.

Promote a culture of responsible environmental •management within the organisation.

Protect the natural environment, indigenous and social •surroundings.

Continually improve our environmental performance.•

Comply with applicable environmental laws and aspire to •higher standards within our business.

Communicate openly, effectively and transparently with •all stakeholders on environmental matters.

Engage the community in environmental initiatives aligned •with our business values.

Atlas’ Environmental and Social Policy is based on the recognition that all our activities have impact on the environment. Since it is not possible to eliminate such impact, the Atlas policy is to engineer and conduct operations with the objective of achieving best practice so that adverse effects on the environment and any surrounding community are either avoided or kept to an acceptable level.

COmmUNiTy

“Atlas’ excellent long-term relationship with the Njamal people and the Pilbara Native Title Service helped facilitate engagement on key aspects of this agreement quickly. Atlas came to the negotiating table respecting for the Njamal people’s rights to culture and country. Atlas’ willingness to make a good offer and its commitment to following the correct process insured that a well considered agreement was finalised very quickly.”

Simon Hawkins, Chief Executive Officer, Pilbara Native Title

Service, on the Njamal Native Title agreement with Atlas

Throughout 2009 Atlas has worked with a number of stakeholders, the community and government to establish and maintain better outcomes in the areas it operates. To this end, Atlas held 18 meetings with local community groups and other stakeholders during the year. Atlas has embarked upon a number of incentive programs to promote indigenous business enterprise and partnering throughout both the mining and exploration activities. Atlas is committed to providing outcomes for communities that are sustainable

and can leave a positive footprint. Atlas is constantly looking for win-win outcomes that will promote and enhance Atlas' social licence to operate.

Atlas houses a number of its team and their families in Port Hedland which has allowed them to contribute to the local community. All of the Atlas staff and contractors are encouraged to discover the social, cultural and environmental opportunities available to them within the local community, so they can become active participants within the community.

Also during the year, Atlas has further enhanced strong relationships with the indigenous stakeholders and their representatives in Western Australia. This has been achieved by engagement, transparency of discussion and willingness to listen to the various groups. Accordingly, Atlas’ Indigenous Peoples Policy reflects this commitment to foster new and strengthen existing relationships with the communities. Njamal Traditional Owner Rodney Monaghan said that the Njamal community was happy that the Njamal Native Title agreement with Atlas managed to balance the protection of their country and culture with commercial realities and opportunities. “This agreement recognises the importance of our culture and country, but still shows that Njamal people are serious and fair with their commercial negotiations,” said Mr Monaghan.

Atlas is committed to employing indigenous peoples and during the year has employed indigenous persons from the Ngarla, Njamal and Kariyarra Peoples, being the three native title land holders where Atlas is operating.

Atlas is proud of the relationship it has established with the indigenous stakeholders and their legal representatives in the Pilbara region. Accordingly, Atlas’ Indigenous Peoples Policy reflects the commitment to foster new, and strengthen existing, relationships with the communities we co-exist with.

Atlas is committed to being recognised as a leader in the field of indigenous relations and in partnership with the indigenous people on whose land it operates, will deliver:

Economic opportunity in its exploration and mining •activities.

Culturally and Environmentally sensitive outcomes.•

Leading by example is consistent with our values.•

Promote sustainable commercial relationships with •indigenous peoples.

Continue to develop and increase its indigenous workforce.•

Maintain partnership with the indigenous community •to develop sustainable economic business opportunities wherever appropriate.

Seek to generally improve the wellbeing of indigenous •people in its operating areas.

Operate within existing environmental constraints and •respect the indigenous relationship to the land.

atlas Iron Limited Annual Report 2009 5

Environment and the Community (cont'd)

Encourage other companies, with which we interact, to •engage with native title groups.

Forge new and maintain existing relationships with the •indigenous communities with which it operates; and

Deliver cross cultural awareness training to its workforce.•

Encouraging staff to be involved in the community. Atlas •Managing Director recently joined the board of Youth Focus Inc, a charity whose objective is the prevention of youth suicide and self harm.

sUsTAiNABLE DEvELOPmENTAtlas’ core values and operational strategy has placed the Company ahead of its peers, and paved the way for unprecedented growth opportunities.

By adopting Atlas’ values, its environmental and social policies, and sustainable management systems, the Company has proven it can better manage the risks associated with the business, whilst creating opportunities, reducing costs, and attracting the best people to our company. This is a unique asset that sets Atlas apart from its industry peers, and adds to our ability to attract and retain high calibre personnel.

OCCUPATiONAL hEALTh AND sAfETy

“The Atlas vision is to set new standards of safety and health management. To do this while starting our first mine is a challenge, but our team is up to the task, improving performance and standardising safety management systems across the organisation.”

David Flanagan, Managing Director

At Atlas we care about the health and safety of all of our employees, contractors and visitors to our sites. Atlas is committed to providing an environment where everyone is protected. This is achieved through:

Implementing and communicating high occupational •health, hygiene and safety standards. Implementing effective training and appropriate high quality safety equipment.

Meeting or exceeding all relevant legislative and statutory •obligations.

Continuous review and improvement of our safety •management systems.

Ensuring all our contractors manage health and safety in •line with this policy.

Supporting and engaging injured workers to return to •work as soon as medically fit.

Providing a workplace free of drugs, supported by a •holistic and open approach; and

Managing the impact on fitness for work of fatigue, •stress, physical well being and medical issues.

Our vision is to establish a culture within Atlas where there is no harm to people or the environment.

OCCUPATiONAL hEALTh AND sAfETy PERfORmANCEAtlas continues to strive for an incident-free work place and the safety and health of our employees and contractors is paramount. During the course of the financial year Atlas continued to invest in the development of integrated occupational health and safety management systems, with the focus being on integration across the organisation inclusive of exploration, resource development and the mining disciplines.

Of particular note has been the safety leadership demonstrated by the Pilbara Operations team. They have worked closely with our lead contractors to demonstrate and establish a safe work culture that is having a marked impact on overall safety performance. Having set a tone at Pardoo the team is well placed to facilitate equivalent performance at the soon to be established Wodgina mine site.

Indigenous mining contractors working at the Pardoo mine.

6 atlas Iron Limited Annual Report 20096

Operations Review

operatIonS reVIeW

“Atlas continues to deliver on its publicly stated objectives in project development and production. Whilst the Company is proud of its achievements to date, it is only just the beginning, with substantial production growth to come over the next 12 months to two years.”

Ken Brinsden, Operations Manager

OvERviEwThe Pilbara arguably hosts the largest endowment of iron ore of any region of the world, with Atlas having positioned itself with the most extensive landholding within 150 kilometres of the world’s largest iron ore port, in Port Hedland. Given the seismic shifts that are occurring in global seaborne iron ore trade, the time is right to generate potentially unprecedented opportunities for shareholders, employees, the region’s local communities and the State of Western Australia. With huge demand coming from Asian markets for iron ore, the Pilbara’s unique position in relation to these markets and its undeveloped resources mean the Pilbara is the place to be for an emerging iron ore company.

One of the early movers of the current iron ore juniors in the Pilbara, Atlas listed on the ASX in December 2004 and within 9 months of listing, Atlas had made a Direct Shipping iron ore discovery at its Pardoo Project, 75 kilometres east of Port Hedland. This has since transformed Atlas from iron ore explorer to producer, with Atlas being the only junior iron ore company to move into production in the world’s premier iron ore province.

Atlas commenced iron ore exports through Port Hedland from its Pardoo Mine in December 2008, marking the commencement of what Atlas plans to be a meaningful, positive and long-term contribution to the Pilbara iron ore

industry and its regional communities. Atlas is targeting the export of one million tonnes (Mt) of iron ore in its first year of operations at Pardoo, increasing to 2.5 million tonnes per annum (Mtpa) by 2010. The planned development of the Wodgina DSO Project, from early 2010, will increase the company’s production to 6Mtpa during next year. Subsequent development of the Abydos and Mt Webber Projects will see the company’s production grow to 9Mtpa in 2011, and 12Mtpa by 2012.

In order to further enhance its production profile over time, Atlas continues to pursue strategic, complementary and value-adding acquisitions, predominantly in the Pilbara of Western Australia. Furthermore, Atlas maintained an aggressive exploration program across its prospective Pilbara landholdings with outstanding results, culminating with the announcement of a substantial increase in its resources and reserves position subsequent to year-end. Atlas has defined resources of over 127 million tonnes, and reserves of over 25 million tonnes.

With a growing number of high quality iron ore projects and one of the largest landholdings in the Pilbara (over 8,900 square kilometres) located close to infrastructure, Atlas is effectively defining resources and reserves capable of being mined and exported with relatively low capital expenditure.

With mining having already commenced at Pardoo, and Atlas preparing for the commencement of the mining at Wodgina, Atlas is well positioned to advance a number of projects concurrently in the Pilbara to expand its direct ship iron ore production. Atlas has now developed a team with significant specialist technical skills, with a proven capacity to deliver projects from discovery to production inclusive of managing the approvals process, sourcing funding and engaging all stakeholders. Clearly this retained capacity positions the company well to maximise the returns and minimise risk in future project developments.

Atlas is now well positioned to deliver on its publicly stated production objectives over the coming years, with its project pipeline building and logistics solutions coming to fruition.

Ore being hauled out of the Bobby pit at Pardoo.

atlas Iron Limited Annual Report 2009 7

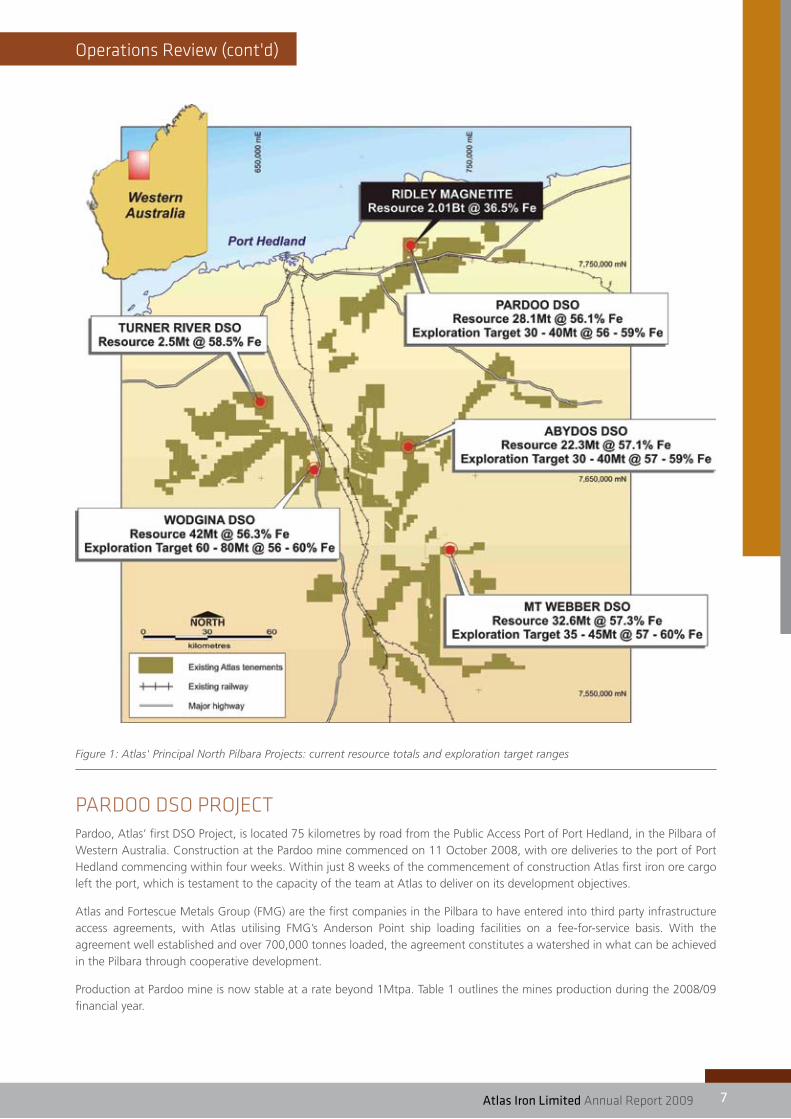

Operations Review (cont'd)

Figure 1: Atlas' Principal North Pilbara Projects: current resource totals and exploration target ranges

PARDOO DsO PROJECTPardoo, Atlas’ first DSO Project, is located 75 kilometres by road from the Public Access Port of Port Hedland, in the Pilbara of Western Australia. Construction at the Pardoo mine commenced on 11 October 2008, with ore deliveries to the port of Port Hedland commencing within four weeks. Within just 8 weeks of the commencement of construction Atlas first iron ore cargo left the port, which is testament to the capacity of the team at Atlas to deliver on its development objectives.

Atlas and Fortescue Metals Group (FMG) are the first companies in the Pilbara to have entered into third party infrastructure access agreements, with Atlas utilising FMG’s Anderson Point ship loading facilities on a fee-for-service basis. With the agreement well established and over 700,000 tonnes loaded, the agreement constitutes a watershed in what can be achieved in the Pilbara through cooperative development.

Production at Pardoo mine is now stable at a rate beyond 1Mtpa. Table 1 outlines the mines production during the 2008/09 financial year.

8 atlas Iron Limited Annual Report 20098

Operations Review (cont'd)

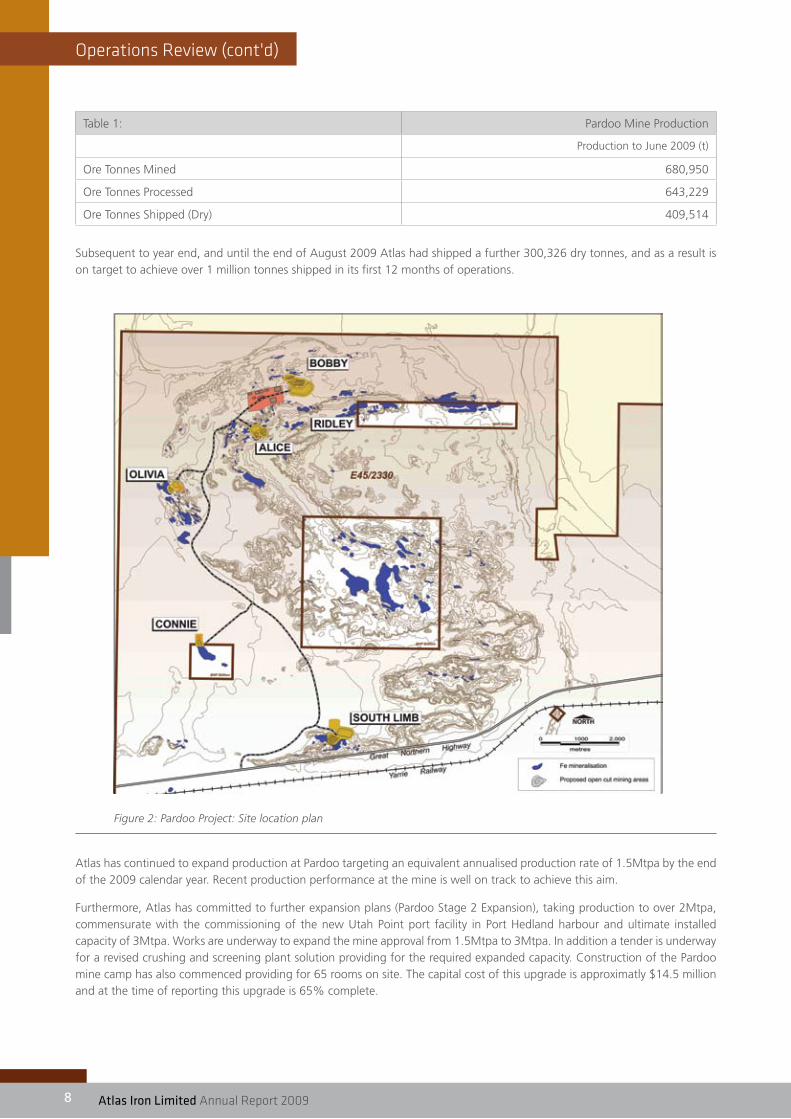

Table 1: Pardoo Mine Production

Production to June 2009 (t)

Ore Tonnes Mined 680,950

Ore Tonnes Processed 643,229

Ore Tonnes Shipped (Dry) 409,514

Subsequent to year end, and until the end of August 2009 Atlas had shipped a further 300,326 dry tonnes, and as a result is on target to achieve over 1 million tonnes shipped in its first 12 months of operations.

Figure 2: Pardoo Project: Site location plan

Atlas has continued to expand production at Pardoo targeting an equivalent annualised production rate of 1.5Mtpa by the end of the 2009 calendar year. Recent production performance at the mine is well on track to achieve this aim.

Furthermore, Atlas has committed to further expansion plans (Pardoo Stage 2 Expansion), taking production to over 2Mtpa, commensurate with the commissioning of the new Utah Point port facility in Port Hedland harbour and ultimate installed capacity of 3Mtpa. Works are underway to expand the mine approval from 1.5Mtpa to 3Mtpa. In addition a tender is underway for a revised crushing and screening plant solution providing for the required expanded capacity. Construction of the Pardoo mine camp has also commenced providing for 65 rooms on site. The capital cost of this upgrade is approximatly $14.5 million and at the time of reporting this upgrade is 65% complete.

atlas Iron Limited Annual Report 2009 9

Operations Review (cont'd)

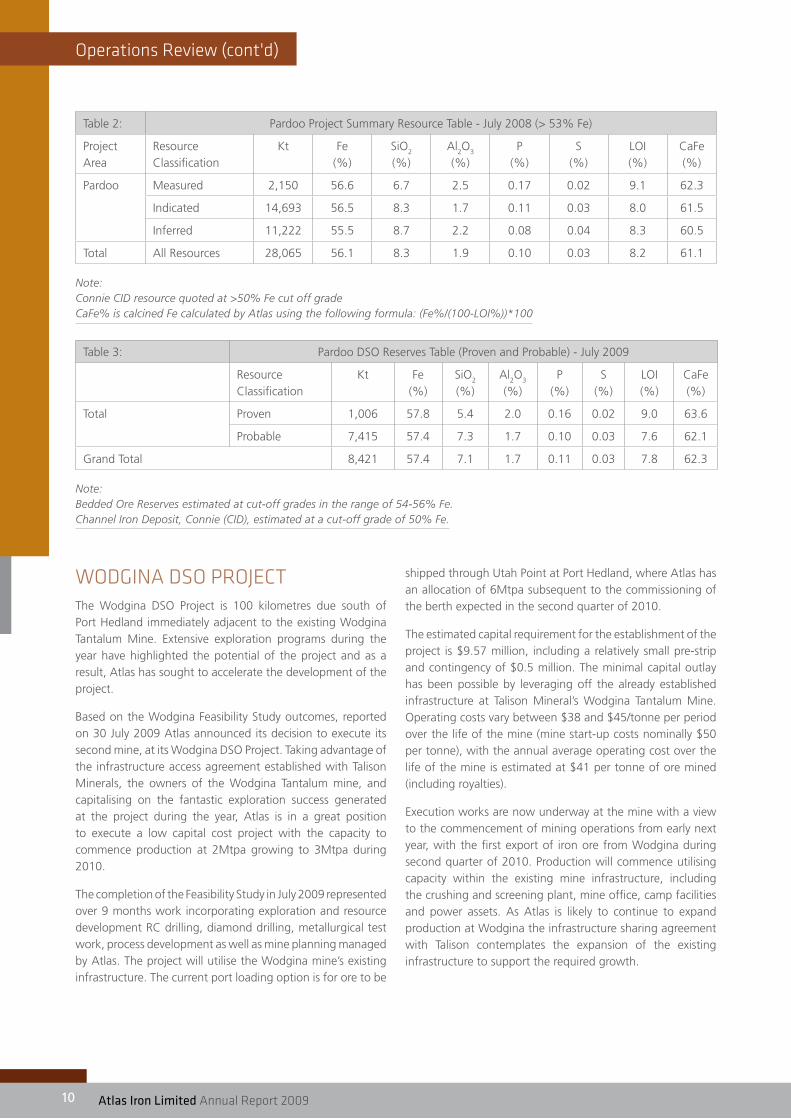

PARDOO DsO - EXPLORATiON & REsOURCEsWith the commencement of mining operations at Pardoo in October 2008, the focus of work at Pardoo shifted from exploration to resource definition and infill drilling aimed at upgrading the Pardoo resource inventory from Inferred to Indicated and Measured category. Six diamond and 1,208 RC holes were completed during the year for a total of 51,925 metres of drilling. DSO resources have increased 17% to 28Mt at 56.1% Fe after mining depletion is accounted for.

Reserves for the Pardoo Project now stand at 8.4Mt at 57.4% Fe, a 14% increase compared to the previous Reserve statement, with improvements in overall Fe grade, and lower Alumina and Phosphorous evident. Please refer to Atlas’ previous Resource and Reserve Update announcement dated 29 July 2009.

Near-mine exploration will resume at Pardoo in quarter four 2009 with the aim of increasing and upgrading known resources and prospects in the Pardoo area in line with the mining schedule.

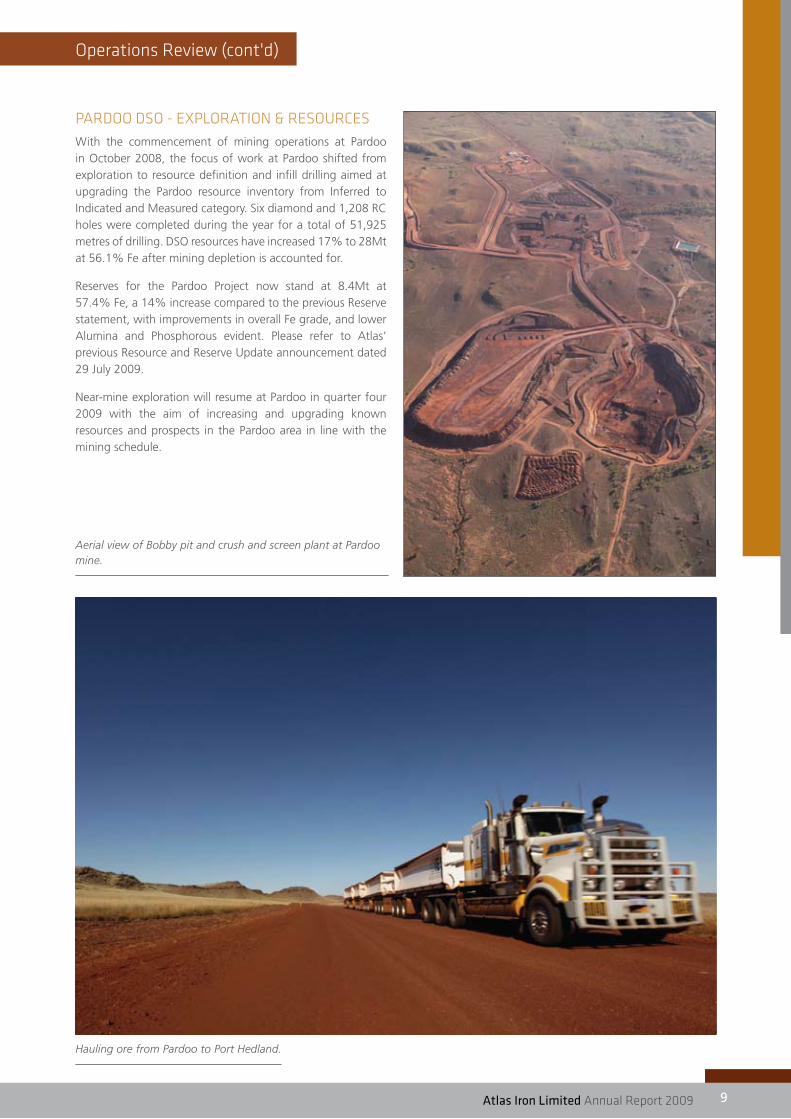

Hauling ore from Pardoo to Port Hedland.

Aerial view of Bobby pit and crush and screen plant at Pardoo mine.

10 atlas Iron Limited Annual Report 200910

Operations Review (cont'd)

Table 2: Pardoo Project Summary Resource Table - July 2008 (> 53% Fe)

Project Area

Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Pardoo Measured 2,150 56.6 6.7 2.5 0.17 0.02 9.1 62.3

Indicated 14,693 56.5 8.3 1.7 0.11 0.03 8.0 61.5

Inferred 11,222 55.5 8.7 2.2 0.08 0.04 8.3 60.5

Total All Resources 28,065 56.1 8.3 1.9 0.10 0.03 8.2 61.1

Note: Connie CID resource quoted at >50% Fe cut off grade CaFe% is calcined Fe calculated by Atlas using the following formula: (Fe%/(100-LOI%))*100

Table 3: Pardoo DSO Reserves Table (Proven and Probable) - July 2009

Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Total Proven 1,006 57.8 5.4 2.0 0.16 0.02 9.0 63.6

Probable 7,415 57.4 7.3 1.7 0.10 0.03 7.6 62.1

Grand Total 8,421 57.4 7.1 1.7 0.11 0.03 7.8 62.3

Note: Bedded Ore Reserves estimated at cut-off grades in the range of 54-56% Fe. Channel Iron Deposit, Connie (CID), estimated at a cut-off grade of 50% Fe.

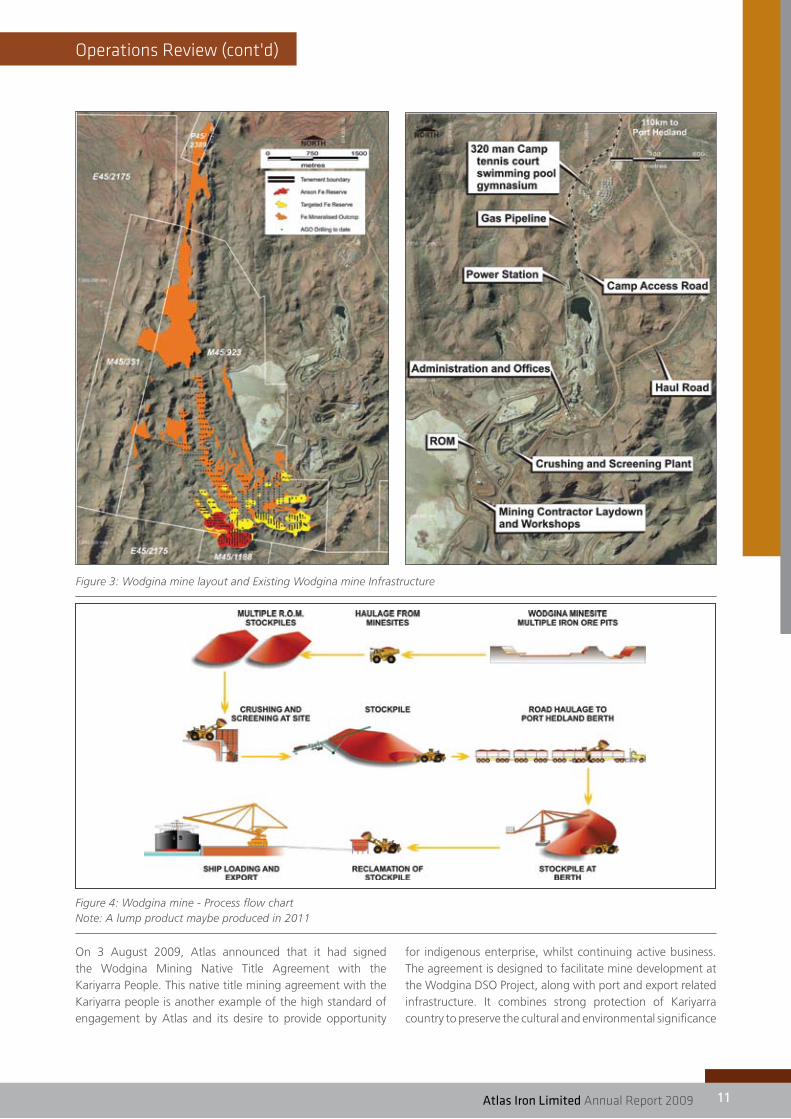

wODgiNA DsO PROJECTThe Wodgina DSO Project is 100 kilometres due south of Port Hedland immediately adjacent to the existing Wodgina Tantalum Mine. Extensive exploration programs during the year have highlighted the potential of the project and as a result, Atlas has sought to accelerate the development of the project.

Based on the Wodgina Feasibility Study outcomes, reported on 30 July 2009 Atlas announced its decision to execute its second mine, at its Wodgina DSO Project. Taking advantage of the infrastructure access agreement established with Talison Minerals, the owners of the Wodgina Tantalum mine, and capitalising on the fantastic exploration success generated at the project during the year, Atlas is in a great position to execute a low capital cost project with the capacity to commence production at 2Mtpa growing to 3Mtpa during 2010.

The completion of the Feasibility Study in July 2009 represented over 9 months work incorporating exploration and resource development RC drilling, diamond drilling, metallurgical test work, process development as well as mine planning managed by Atlas. The project will utilise the Wodgina mine’s existing infrastructure. The current port loading option is for ore to be

shipped through Utah Point at Port Hedland, where Atlas has an allocation of 6Mtpa subsequent to the commissioning of the berth expected in the second quarter of 2010.

The estimated capital requirement for the establishment of the project is $9.57 million, including a relatively small pre-strip and contingency of $0.5 million. The minimal capital outlay has been possible by leveraging off the already established infrastructure at Talison Mineral’s Wodgina Tantalum Mine. Operating costs vary between $38 and $45/tonne per period over the life of the mine (mine start-up costs nominally $50 per tonne), with the annual average operating cost over the life of the mine is estimated at $41 per tonne of ore mined (including royalties).

Execution works are now underway at the mine with a view to the commencement of mining operations from early next year, with the first export of iron ore from Wodgina during second quarter of 2010. Production will commence utilising capacity within the existing mine infrastructure, including the crushing and screening plant, mine office, camp facilities and power assets. As Atlas is likely to continue to expand production at Wodgina the infrastructure sharing agreement with Talison contemplates the expansion of the existing infrastructure to support the required growth.

atlas Iron Limited Annual Report 2009 11

Operations Review (cont'd)

On 3 August 2009, Atlas announced that it had signed the Wodgina Mining Native Title Agreement with the Kariyarra People. This native title mining agreement with the Kariyarra people is another example of the high standard of engagement by Atlas and its desire to provide opportunity

for indigenous enterprise, whilst continuing active business. The agreement is designed to facilitate mine development at the Wodgina DSO Project, along with port and export related infrastructure. It combines strong protection of Kariyarra country to preserve the cultural and environmental significance

Figure 3: Wodgina mine layout and Existing Wodgina mine Infrastructure

Figure 4: Wodgina mine - Process flow chart Note: A lump product maybe produced in 2011

12 atlas Iron Limited Annual Report 200912

Operations Review (cont'd)

of the region. Compliance with heritage protocols, protection of significant sites with good community communication through a monitoring and liaison committee and on-going partnering throughout the operations through employment and contracting opportunities are paramount. (Hotlink to announcement: www.atlasiron2009ar.com)

Atlas’ intention is to continue to support the local Port Hedland community during the execution and ongoing operations at the Wodgina DSO Project. While Atlas will employ a mining work force to be housed in camp facilities based at Wodgina, Atlas’ existing senior mine management team will continue to be based in Port Hedland, and will continue to support the new Wodgina mine in conjunction with their existing responsibilities for the Pardoo site. In conjunction with its contractors, Atlas anticipates employing up to 60 people during the construction phase and up to 130 people during normal operations, inclusive of the required roster coverage across all disciplines.

Mining, crushing and screening operations are expected to be conducted on a continuous shift basis year round. It is Atlas’ intention to continue to employ its personnel and secure support services from a Port Hedland base where possible.

The Project will utilise contractors to maximise flexibility and minimise the capital costs at commencement of Atlas.

EXPLORATiON & REsOURCE DEvELOPmENTWodgina has been the main focus of exploration for Atlas since exploration commenced in November 2008. A total of 20 diamond and 900 RC holes were completed, for 53,874 metres of drilling.

Reconnaissance field work and mapping paid off immediately upon commencement of drilling at Wodgina with the discovery of the Anson deposit, which was intersected by the first hole drilled – WDRC001. An initial 8.1Mt resource was announced for Anson in January 2009, and this early success led to the decision to dedicate additional resources to the project in order to drill out all available targets as quickly as possible. By March 2009 three RC rigs and one diamond rig were drilling simultaneously under the supervision of the combined Exploration and Resource Development teams in a combined program.

As of 30 June 2009 Atlas had defined a total resource of 42.1Mt at 56.3% Fe, using a 53% Fe lower cut-off. This resource estimate is inclusive of infill drilling down to an average hole spacing of 40 metres by 20 metres over the Anson deposit, but not inclusive of additional infill drilling which has since been completed across the Dragon and Constellation deposits. Updated resource estimates for these latter two deposits will be completed later in 2009. Reserves for the Wodgina Project as at the time of reporting are at 9.5Mt at 58.2% Fe. (Hotlink to announcement: www.atlasiron2009ar.com)

Figure 5: Wodgina resource location Wodgina crush and screen plant.

atlas Iron Limited Annual Report 2009 13

Operations Review (cont'd)

lan

Figure 6: Cross-section of the Dragon deposit.

Table 4: Wodgina Project Resource Table - July 2009 >53% Fe

Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Total Measured - - - - - - - -

Indicated 12,050 57.5 6.0 1.8 0.09 0.03 9.1 63.3

Inferred 30,020 55.8 7.3 2.4 0.06 0.07 9.1 61.4

Total All Resources 42,070 56.3 6.9 2.3 0.07 0.06 9.1 61.9

Note: CaFe% is calcined Fe calculated by Atlas using the following formula: (Fe%/(100-LOI%))*100

Table 5: Wodgina DSO Reserves Table (Proven and Probable) - July 2009

Deposit Ore Type Reserve Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Anson Bedded Ore Probable 9,495 58.2 5.3 1.6 0.10 0.03 9.0 64.0

Grand Total 9,495 58.2 5.3 1.6 0.10 0.03 9.0 64.0

Note:

Reserves estimated at a cut-off grade of 55% Fe.

14 atlas Iron Limited Annual Report 200914

Operations Review (cont'd)

One recent highlight of drilling at Dragon and Constellation was the delineation of a zone of high Fe grades and low contaminant levels. This material is expected to improve the potential economics of the project, and will possibly allow lower-grade material to be included in the Wodgina reserves as blending material.

Infill drilling is continuing within the Anson resource to increase ore body definition in preparation for mining under the supervision of the Resource Development team.

Despite the intense pace of exploration at Wodgina in the first half of 2009, significant exploration potential remains. A number of mineralised prospects identified in early reconnaissance drilling at Wodgina South are yet to be followed up, and the area north of Telegraph Gorge known as Wodgina North has not yet been drilled at all. Wodgina North is expected to be drilled in the latter half of 2009, following completion of necessary heritage approvals. This area is thought to have the potential to add significantly to Wodgina’s resource inventory in the year ahead.

AByDOs DsO PROJECTThe Abydos DSO Project is located 100 kilometres south - south east of Port Hedland in Western Australia’s Pilbara region. The Project is situated within an area of known iron ore deposits and contains prospective, archaean banded iron formation sequences. These units and surrounding terrain are prospective for DSO supergene bedded iron deposits (BID), detrital or channel iron deposits (CID) and magnetite deposits.

On the 5th December 2008, Atlas announced that it had signed a Native Title Mining Agreement with the Njamal people with respect to its Abydos Iron Ore Project. The agreement set a new improved standard of engagement and opportunity for indigenous enterprise. The agreement is designed to facilitate and fast-track mine development and combines strong protection of Njamal country with good community communication and on-going partnering throughout the operations. Furthermore the agreement sets up systems for Njamal People and Atlas to develop joint business initiatives. As an alternative to a signature payment, Atlas has agreed to help fund a Njamal business enterprise that will provide further commercial opportunities. The agreement also establishes an innovative heritage framework under which Atlas can accelerate the heritage survey process through appropriate consultation, thereby accessing its exploration and mining areas faster, while at the same time recognising the importance to Njamal People of their cultural sites. (Hotlink to announcement: www.atlasiron2009ar.com)

Following completion of pre feasibility studies (PFS) in July 2008, and with the progress of feasibility and resource development works since, the Abydos DSO project is a mature project ready for development, with mine production

targeted at an initial rate of 2Mtpa, growing to 3Mtpa shortly after. In conjunction with Atlas, Pardoo and Wodgina Mines, Abydos will support Atlas' targeted annualised production rate of 9Mtpa in 2011.

AByDOs miNE LAyOUTThe Abydos PFS has considered road haulage and rail haulage as options to transport Abydos Iron Ore to Port Hedland. In June 2007, Atlas signed a Memorandum of Understanding (MOU) with Fortescue Metals Group (FMG) relating to the use of FMG’s rail and Anderson Point ship loading facilities, for the export of 3Mt of iron ore from the Abydos Project.

Subject to agreement with FMG on commercial terms, Atlas would propose to utilise these facilities for its Abydos exports. In the absence of a rail haulage or port agreement via FMG, Atlas intends to use road trains to haul iron ore to the new public access port facilities at Utah Point in Port Hedland, subject to agreement with the Port Hedland Port Authority on available capacity. The proposed expansion of the public access port facilities at the Utah Point in Port Hedland is scheduled to be commissioned with capacity for up to 18Mtpa from April 2010.

In addition to the advantage of its location just 100 kilometres South-South East of Port Hedland, the Abydos Project tenement package is intersected by the Great Northern highway and FMG’s and BHPB’s railway lines. In addition, power, gas and hi-speed communications infrastructure is located in close proximity via the existing Wodgina Mine infrastructure available to Atlas via the Talison infrastructure sharing agreement.

The combined impact of all available infrastructure provides Atlas with significant advantages in low capital and operating costs. The PFS has now confirmed a relatively low capital cost for commencement of the Abydos Project of $53.3M for the rail haulage option, plus a $10.5M project contingency. Capital costs to establish the road haulage option are $47.2M, plus a $9.2M project contingency.

EXPLORATiON & REsOURCE DEvELOPmENTThe Abydos DSO project was the scene of intense drilling activity prior to the end of 2008, after which rigs and personnel were reassigned to Wodgina. A total of fourteen diamond and 407 RC holes were completed for 23,808 metres. Drilling was focussed on the Lalla Rookh trend, which now contains 17 deposits and prospects including Trigg, the most advanced of the resources and also the largest, with a resource of 11.8Mt at 57.7% Fe.

Resources at Abydos increased by 48% during the year to 22.3Mt at 57.1% Fe as a result of extensional drilling around Trigg, as well as new discoveries at Leighton, Scarborough and Sandtrax. Other prospects which have returned ore-grade intersections but which have not yet been drilled sufficiently

atlas Iron Limited Annual Report 2009 15

Operations Review (cont'd)

for a resource to be estimated include Contacios, Cables and Cove. There are a number of other prospects along the Lalla Rookh trend which are yet to be drilled.

Drilling will resume at Lalla Rookh in quarter four 2009. The primary objective of the year’s drilling campaign will be conversion of existing Inferred resources to Indicated category for inclusion in reserve calculations, but there are also drill metres allocated to exploration of new prospects. Abydos has an exploration target range of 30Mt to 40Mt at 57% to 59% Fe. Reserves for the Abydos Project stand at 7.5Mt at 58.2% Fe.

.

Figure 7: Abydos Lalla Rookh trend - principal prospect locations

Table 6: Abydos Project Resource Table - July 2009 (>50% Fe COG)

Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Total Indicated 10,080 57.8 5.7 1.7 0.05 0.01 9.5 63.9

Inferred 12,240 56.6 6.8 2.2 0.06 0.02 9.4 62.5

Total All Resources 22,320 57.1 6.3 1.9 0.06 0.02 9.4 63.1

Note:

CaFe% is calcined Fe calculated by Atlas using the following formula: (Fe%/(100-LOI%))*100

Table 7: Abydos DSO Reserves Table (Proven and Probable) - July 2009

Deposit Ore Type Reserve Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Trigg Bedded Ore Probable 7,549 58.2 5.2 1.6 0.06 0.01 9.5 64.2

Grand Total 7,549 58.2 5.2 1.6 0.06 0.01 9.5 64.2

Note: Reserves estimated at a cut-off grade of 54% Fe.

Operations Review (cont'd)

16 atlas Iron Limited Annual Report 200916

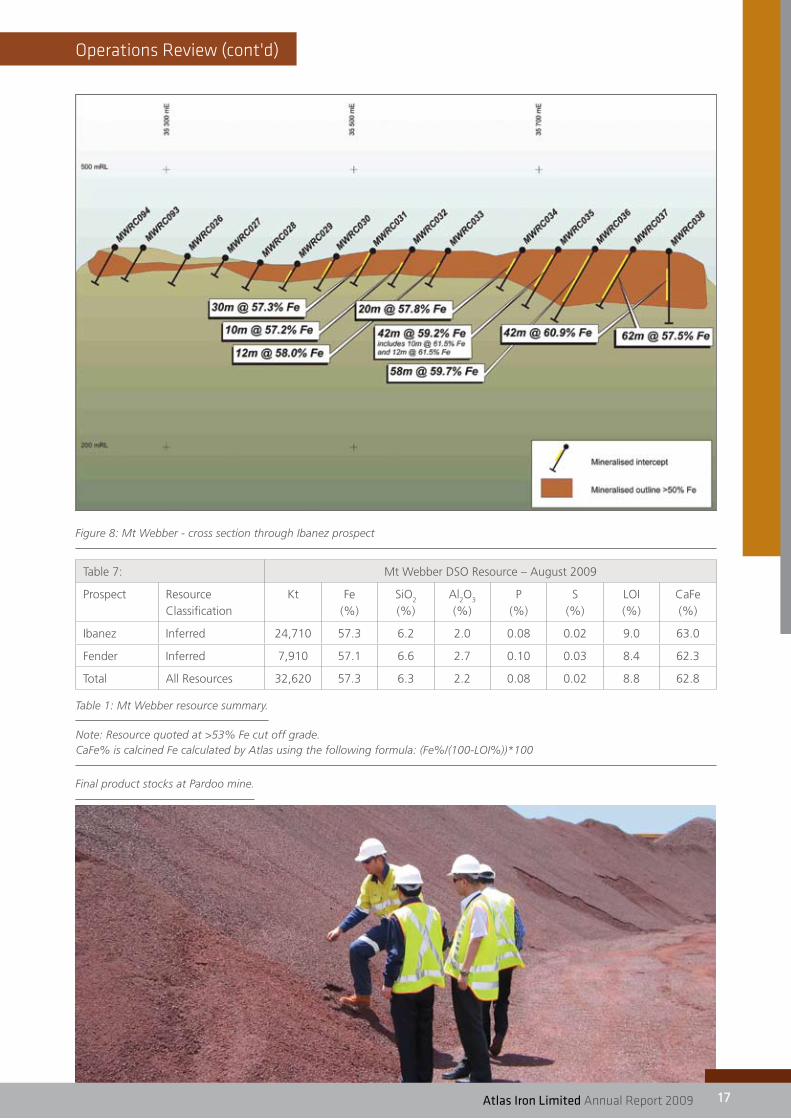

mT wEBBER DsO PROJECTAtlas’ Mt Webber DSO Project is located just 75 kilometres south east of the Wodgina DSO Project and approximately 175 kilometres south east of the Port of Port Hedland. Atlas announced its first resource for the project of over 32 Mt at 57.3% Fe, in August 2009, just 3 months after the commencement of exploration drilling in the area. As a result of this success and the project's proximity to the Wodgina mining centre, Mt Webber will feature in the company’s expansion plans to achieve 12Mtpa by 2012. Pre feasibility studies are planned for the project during the current year.

EXPLORATiON & REsOURCE DEvELOPmENT

First-pass exploration drilling commenced at Mt Webber in late April 2009. By 30 June 2009, Atlas had drilled 178 RC

holes for a total of 7,810 metres, primarily at the Ibanez and Fender prospects, with a number of holes spread across the secondary prospects MW3 and MW4. After a short break in July 2009, drilling has since resumed, with MW2 and MW6 scheduled to be drilled by the end of September 2009.

The Mt Webber drilling was immediately successful in discovering ore-grade iron enrichment with low levels of contaminants. Continuous sub-horizontal zones of near surface enrichment have been identified at Ibanez and Fender. Subsequent to the end of June, resource estimation was completed for these two deposits resulting in an Inferred Resource of 32.6Mt at 57.3% Fe. (Hotlink to announcement: www.atlasiron2009ar.com)

Abydos exploration camp construction and exploration team.

Operations Review (cont'd)

atlas Iron Limited Annual Report 2009 17

Figure 8: Mt Webber - cross section through Ibanez prospect

Table 7: Mt Webber DSO Resource – August 2009

Prospect Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Ibanez Inferred 24,710 57.3 6.2 2.0 0.08 0.02 9.0 63.0

Fender Inferred 7,910 57.1 6.6 2.7 0.10 0.03 8.4 62.3

Total All Resources 32,620 57.3 6.3 2.2 0.08 0.02 8.8 62.8

Final product stocks at Pardoo mine.

Table 1: Mt Webber resource summary.

Note: Resource quoted at >53% Fe cut off grade. CaFe% is calcined Fe calculated by Atlas using the following formula: (Fe%/(100-LOI%))*100

18 atlas Iron Limited Annual Report 200918

Operations Review (cont'd)

TURNER RivER DsO PROJECTThe Turner River project area is located approximately 65 kilometres south of Port Hedland and includes a number of prospects, including potential Bedded Iron Deposits (BID) and Channel Iron Deposits (CID). The Mt Dove prospect, located 11 kilometres from the Great Northern Highway north of Wodgina and within the Turner River project area, is the subject of an iron ore rights agreement with De Grey Mining Limited. Drilling at Mt Dove during the year consisted of a single program of 20 RC holes for 798 metres. As a result of this drilling, an Inferred Resource has been estimated for Mt Dove, containing 2.5Mt at 58.5% Fe.

(Hotlink to July 2009 Resources and Reserves Update: www.atlasiron2009ar.com)

Table 8: Turner River Project Resource Table (50%Fe)

Resource Classification

Kt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

CaFe (%)

Total Inferred 2,470 58.5 6.1 1.8 0.11 0.03 7.9 63.5

Total All Resources 2,470 58.5 6.1 1.8 0.11 0.03 7.9 63.5

Note: Café% is calcined Fe calculated by Atlas using the following formula (Fe%/(100-LOI%))*100

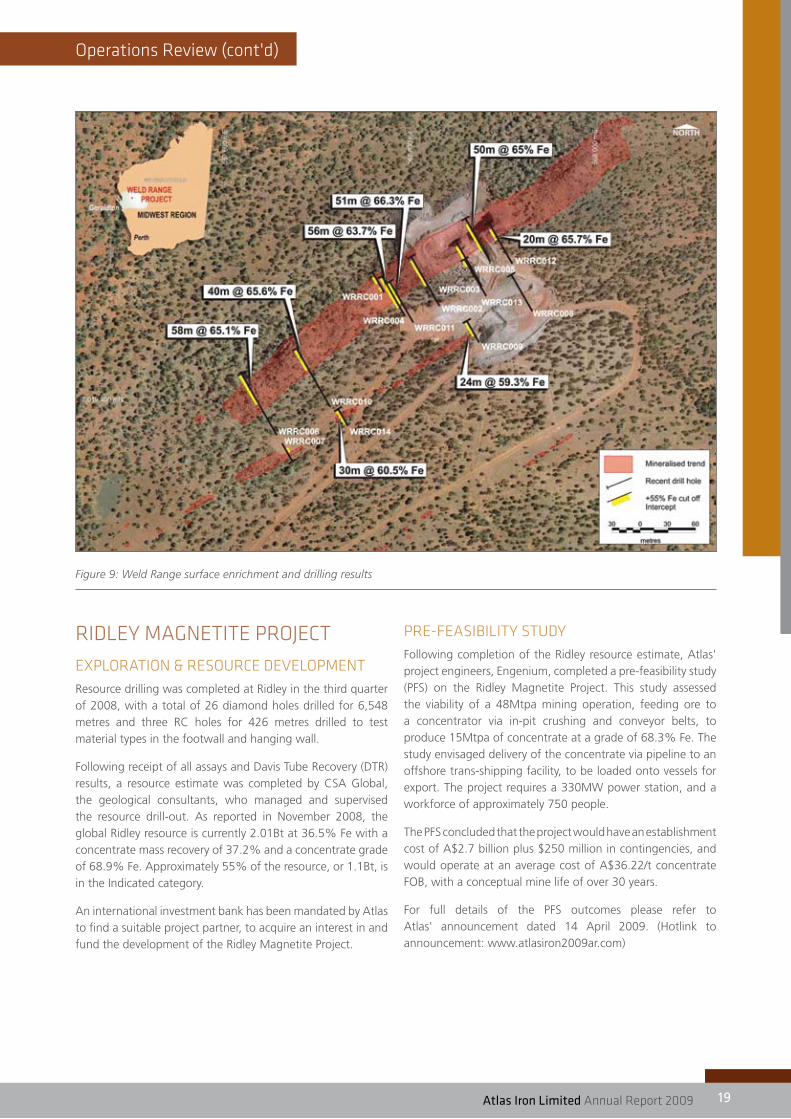

miDwEsT PROJECTsThe Company’s Midwest projects, consisting of Mount Gould and Weld Range in the Murchison Province of Western Australia,

are highly prospective for premium high grade hematite mineralisation. Mount Gould contains the interpreted strike extension to ore currently being mined and exported from Jack Hills. The two projects have the potential to add a combined total of 30 to 40Mt at 60-66% Fe to the Company’s resource inventory.

In September 2008 Atlas drilled a small RC program at its Weld Range project in the Mid West of Western Australia, consisting of 14 RC holes for 1,131 metres. The drilling was designed to test the tenor and width of enrichment along strike and at depth.

Results of the drilling correlated well with surface mapping, with 40 metre lode widths replicated at up to 70 metres vertical depth. The tenor of mineralisation was also highly encouraging, with individual 2 metre samples returning assays as high as 68.7% Fe.

The strategic value of this landholding has been confirmed during the year, with the signing of a State Development Agreement for the Oakajee Port and Rail network on 20 March 2009. The State and Federal Governments have also committed a combined $678 million in funding towards the Oakajee Port Project. The Oakajee Port and Rail developments are expected to service both the Jack Hills / Mt Gould and Weld Range areas, which will support the development of DSO mines at these two projects.

White further work is planned at both the Company’s Mid West projects, but the Pilbara projects remain higher in priority for the medium term.

(Hotlink to October 2008 announcement: www.atlasiron2009ar.com)

atlas Iron Limited Annual Report 2009 19

Operations Review (cont'd)

Figure 9: Weld Range surface enrichment and drilling results

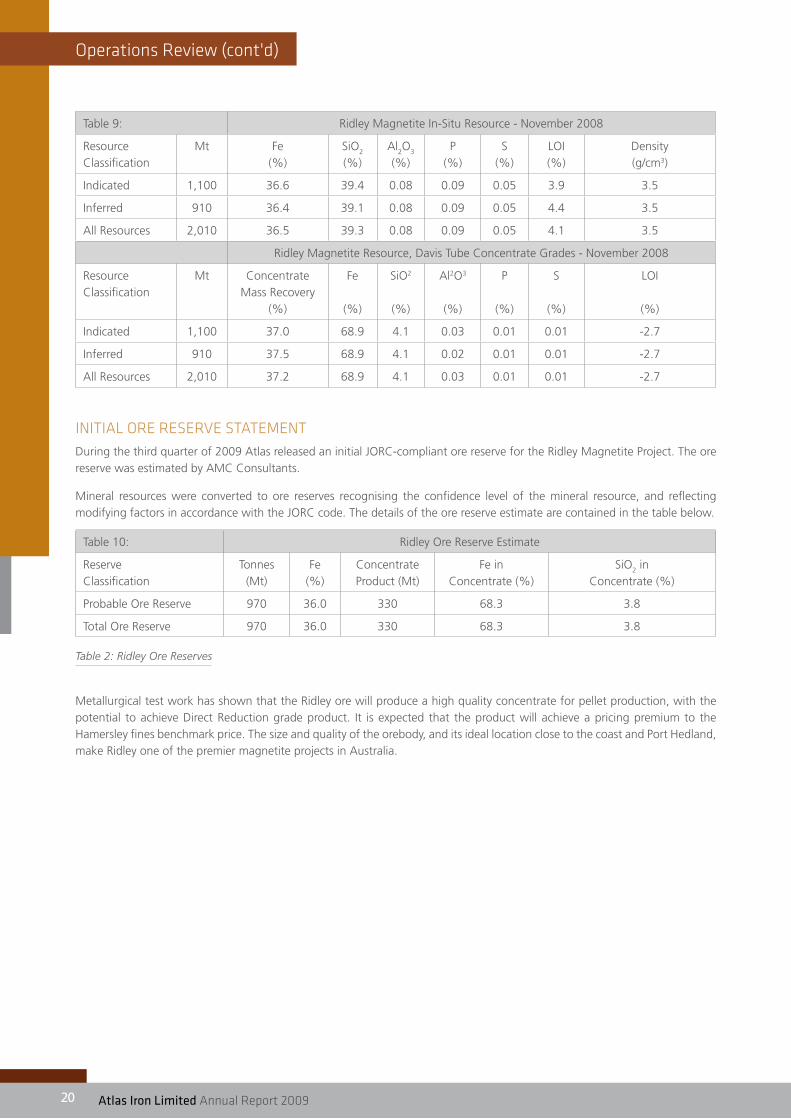

RiDLEy mAgNETiTE PROJECT

EXPLORATiON & REsOURCE DEvELOPmENTResource drilling was completed at Ridley in the third quarter of 2008, with a total of 26 diamond holes drilled for 6,548 metres and three RC holes for 426 metres drilled to test material types in the footwall and hanging wall.

Following receipt of all assays and Davis Tube Recovery (DTR) results, a resource estimate was completed by CSA Global, the geological consultants, who managed and supervised the resource drill-out. As reported in November 2008, the global Ridley resource is currently 2.01Bt at 36.5% Fe with a concentrate mass recovery of 37.2% and a concentrate grade of 68.9% Fe. Approximately 55% of the resource, or 1.1Bt, is in the Indicated category.

An international investment bank has been mandated by Atlas to find a suitable project partner, to acquire an interest in and fund the development of the Ridley Magnetite Project.

PRE-fEAsiBiLiTy sTUDyFollowing completion of the Ridley resource estimate, Atlas' project engineers, Engenium, completed a pre-feasibility study (PFS) on the Ridley Magnetite Project. This study assessed the viability of a 48Mtpa mining operation, feeding ore to a concentrator via in-pit crushing and conveyor belts, to produce 15Mtpa of concentrate at a grade of 68.3% Fe. The study envisaged delivery of the concentrate via pipeline to an offshore trans-shipping facility, to be loaded onto vessels for export. The project requires a 330MW power station, and a workforce of approximately 750 people.

The PFS concluded that the project would have an establishment cost of A$2.7 billion plus $250 million in contingencies, and would operate at an average cost of A$36.22/t concentrate FOB, with a conceptual mine life of over 30 years.

For full details of the PFS outcomes please refer to Atlas' announcement dated 14 April 2009. (Hotlink to announcement: www.atlasiron2009ar.com)

20 atlas Iron Limited Annual Report 200920

Operations Review (cont'd)

Table 9: Ridley Magnetite In-Situ Resource - November 2008

Resource Classification

Mt Fe (%)

SiO2

(%)Al

2O

3

(%)P

(%)S

(%)LOI (%)

Density (g/cm3)

Indicated 1,100 36.6 39.4 0.08 0.09 0.05 3.9 3.5

Inferred 910 36.4 39.1 0.08 0.09 0.05 4.4 3.5

All Resources 2,010 36.5 39.3 0.08 0.09 0.05 4.1 3.5

Ridley Magnetite Resource, Davis Tube Concentrate Grades - November 2008

Resource Classification

Mt Concentrate Mass Recovery

(%)

Fe

(%)

SiO2

(%)

Al2O3

(%)

P

(%)

S

(%)

LOI

(%)

Indicated 1,100 37.0 68.9 4.1 0.03 0.01 0.01 -2.7

Inferred 910 37.5 68.9 4.1 0.02 0.01 0.01 -2.7

All Resources 2,010 37.2 68.9 4.1 0.03 0.01 0.01 -2.7

iNiTiAL ORE REsERvE sTATEmENTDuring the third quarter of 2009 Atlas released an initial JORC-compliant ore reserve for the Ridley Magnetite Project. The ore reserve was estimated by AMC Consultants.

Mineral resources were converted to ore reserves recognising the confidence level of the mineral resource, and reflecting modifying factors in accordance with the JORC code. The details of the ore reserve estimate are contained in the table below.

Table 10: Ridley Ore Reserve Estimate

Reserve Classification

Tonnes (Mt)

Fe (%)

Concentrate Product (Mt)

Fe in Concentrate (%)

SiO2 in

Concentrate (%)

Probable Ore Reserve 970 36.0 330 68.3 3.8

Total Ore Reserve 970 36.0 330 68.3 3.8

Table 2: Ridley Ore Reserves

Metallurgical test work has shown that the Ridley ore will produce a high quality concentrate for pellet production, with the potential to achieve Direct Reduction grade product. It is expected that the product will achieve a pricing premium to the Hamersley fines benchmark price. The size and quality of the orebody, and its ideal location close to the coast and Port Hedland, make Ridley one of the premier magnetite projects in Australia.

atlas Iron Limited Annual Report 2009 21

Corporate Activities

Corporate aCtIVItIeSCapital raisings

In June and July 2009, Atlas completed a $119.8 million fund raising via a placement in two tranches and share purchase plan. Shareholders approved the placement at a general meeting of shareholders on 20 July 2009. Nearly 7,000 shareholders subscribed to the share purchase plan. As a result of this unprecedented demand, Atlas increased the size of the share purchase plan by 27.7% from $11.7 million to $14.8 million.. Despite this increase, Atlas had to scale back each Share Purchase Plan subscription on a pro rata basis by approximately 50%.

Acquisitions

Exercise of Mt Webber option

In May 2009, Atlas, pursuant its option agreement with Haddington Resources Limited announced on 15 January 2008, gave Haddington notice of its intention to exercise its option to acquire the iron ore rights to 6 Pilbara tenements from Haddington and as a result issued Haddington 485,437 Atlas shares, equal to $1,000,000 in Atlas shares at an issue price of $2.06, being the 5 day VWAP prior to the option agreement being signed on 15 January 2008.

Exercise of Mt Dove option

In July 2009, Atlas exercised its option to purchase the iron ore rights over the Mt Dove tenements for consideration as $650,000 cash. De Grey retains a 1% gross value royalty on future iron ore production from the area and also retains rights to all other minerals within the Mt Dove exploration licence

Talison infrastructure access

In the first half of 2009, Atlas entered into agreement with Talison Wodgina Pty Ltd (Talison) a wholly owned subsidiary of Talison Minerals, for the use of infrastructure at the Wodgina Mine to support the commencement and expansion of Atlas’ Wodgina Project development. Talison owns the Wodgina tantalum mine and associated infrastructure, which is located 100 kilometres by road south of Port Hedland, in the Pilbara of Western Australia. Atlas owns 100% of the Fe rights to the tenements immediately adjacent to the Wodgina tantalum mine. The agreement provides Atlas with access to infrastructure that can support its Wodgina iron ore project at a significantly lower cost than a new start up project. Atlas has agreed to a take or pay arrangement for the capital and fixed costs of the capacity for a monthly fee. Atlas paid Talison an initial payment of $3,000,000 payable in Atlas ordinary shares at an issue price calculated at a 5% discount to the 5 day VWAP prior to the formal agreement. (Hotlink to announcement: www.atlasiron2009ar.com)

Port Capacity

In April 2009, Atlas secured additional berth capacity at the Utah Point public access port facility in Port Hedland. Atlas is a foundation customer of the Utah Point facility and had previously secured 3Mtpa of annual capacity to underpin delivery of product from its Pardoo mine. Atlas has been allocated an additional 3Mtpa of capacity by the Port Hedland Port Authority for the period from May 2010 to February 2012, increasing its total allocation to 6Mtpa. Utah Point is currently under construction and is expected to be ready for first export of Atlas’ Pardoo product by the second quarter of 2010, with full commissioning expected later in 2010. (Hotlink to announcement: www.atlasiron2009ar.com)

Capital Structure

At 30 June 2009, Atlas had 342,830,715 shares on issue. The top 20 shareholders hold approximately 59% of the issued capital. Since year end, the Company has issued additional 57 million shares shares pursuant to the second tranche of the placement announced on 15 June 2009, the Share Purchase Plan and the exercise of approximately 9 million unlisted options.

Listed Investments

As part of Atlas' longer term strategy, Atlas has •maintained and increased its interest in ASX-listed Pilbara Iron Ore Explorer, Warwick Resources Limited (www.warwickresources.com.au)

Since year end, Warwick in association with Atlas, acquired the iron ore rights to the Jigalong tenements held with Hannans Reward Limited. This transaction was approved by Warwick shareholders on 20 August 2009. Warwick has a significant landholding in the South East Pilbara which is prospective for iron ore. Warwick has announced inferred resources and exploration targets which can be seen on its website (www.warwickresources.com.au).

On 7 September 2009, Atlas announced that it and •Warwick Resources had reached agreement for Atlas and Warwick to merge by way of Schemes of Arrangement with Warwick shareholders and optionholders. Atlas will issue one Atlas share to Warwick shareholders for every three Warwick shares on issue. Atlas will also issue Atlas shares to Warwick optionholders on a ratio determined by the exercise price and expiry date of the respective options. The Board of Warwick (other than Atlas’ nominee) has unanimously recommended that all Warwick security holders support the Schemes. The Scheme meeting is expected to be held in late November 2009. (Hotlink to announcement: www.atlasiron2009ar.com)

22 atlas Iron Limited Annual Report 200922

Corporate Activities (cont'd)

Atlas has maintained its 43% holding in ASX-listed •Pilbara Manganese Explorer, Shaw River Resources (www.shawriver.com.au). Since year end Shaw River has

announced a $5 million placement to fund its manganese exploration projects. Atlas is participating in this capital raising.

The Atlas Management Team – Jack Cullity, Daniel Taylor, Jeremy Sinclair, Tony Walsh, David Flanagan, Matt Ramsden, Ken Brinsden, Adam Liebenberg, Mark Hancock and Andrew Paterson.

atlas Iron Limited Annual Report 2009 23

sales and marketing

SaLeS and marketIng

EXisTiNg LONg TERm CONTRACTs – PERfORmANCE, PRiCiNgShipments under Pardoo long-term contracts commenced in March. To date, shipments have been made to each of Atlas’ long-term contract customers.

Pricing under our contracts is based on relativity to the Asian Benchmark however, the protracted Benchmark pricing negotiations between China and the large producers has meant that shipments to July 2009 have been priced on a spot basis. (Hotlink to 16 March 2009 announcement: www.atlasiron2009ar.com)

sPOT PRiCiNgEncouragingly, spot prices have risen throughout 2009 from the depths plumbed in November/December 2008. Atlas retains exposure to the movements in the spot price through the mutual fairness clauses in its offtake agreements.

COmPETiTOR ACTiONsSome competitors have been quietly shipping product to China at the 2009 Benchmark price on a provisional basis. During the September quarter of 2009, almost all tonnes sold into China by competitors were fixed at spot prices.

DEmANDChinese iron ore imports in the first seven months of 2009 were 354 million tonnes, up 31.1% year-on-year (84.0 million tonnes higher), equating to an annualised rate of 606 million tonnes. As demand for iron ore has been basically flat year-on-year, this implies a significant reduction in the use and production of domestically produced ore after taking into account the minimal increase in iron ore stockpiles.

fORwARD PRiCiNg OUTLOOkConsensus forecasts for the 2010 Benchmark iron ore price have improved significantly in the last quarter with most taking the view that prices will rise in 2010, with banks and research houses sitting in the range of 0-20%.

Pardoo ore being unloaded in China. Pardoo ore being loaded at Port Hedland.

24 atlas Iron Limited Annual Report 200924

Corporate governance statement (cont'd)

Competent perSonS and JorC CompLIanCe StatementS

Geological Data, Interpretation and Resource Estimation – Mt Webber

The information in this report that relates to mineral resource results is based on information compiled by Mr Shane Tomlinson is a member of the Australian Institute of Geoscientists & Mr Chris Allen is a member of the Australasian Institute of Mining and Metallurgy. Shane Tomlinson is a full time employee of Atlas Iron Limited and Chris Allen is a full time employee of CSA Global Pty Ltd. Shane Tomlinson & Chris Allen have sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which they have undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Shane Tomlinson and Chris Allen consent to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Geological Data, Interpretation and Resource Estimation – Alice, Clare, Hubert, Glenda, and Connie Resources

The information in this report that relates to mineral resource results is based on information compiled by Mr Tony Cormack & Mr Richard Gaze who are members of the Australasian Institute of Mining and Metallurgy. Tony Cormack is a full time employee of Atlas Iron Limited and Richard Gaze is a full time employee of Golder Associates Pty Ltd. Tony Cormack & Richard Gaze have sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which they have undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Tony Cormack and Richard Gaze consent to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Geological Data, Interpretation and Resource Estimation – Bobby, Floyd, Emma, Olivia, Avalon Point, Mettams, Mullaloo, and Trigg Resources

The information in this report that relates to mineral resource results is based on information compiled by Mr Tony Cormack & Mr David Williams who are members of the Australasian Institute of Mining and Metallurgy. Tony Cormack is a full time employee of Atlas Iron Limited and David Williams is a full time employee of CSA Global Pty Ltd. Tony Cormack & David Williams have sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which they have undertaken to qualify as a Competent

Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Tony Cormack and David Williams consent to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Geological Data, Interpretation and Resource Estimation – South Limb and Dean Resources

The information in this report that relates to mineral resource results is based on information compiled by Mr Tony Cormack & Mr Malcolm Titley who are members of the Australasian Institute of Mining and Metallurgy. Tony Cormack is a full time employee of Atlas Iron Limited and Malcolm Titley is a full time employee of CSA Global Pty Ltd. Tony Cormack & Malcolm Titley have sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which they have undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Tony Cormack and Malcolm Titley consent to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Geological Data, Interpretation and Resource Estimation – Mt Dove and Wodgina

The information in this report that relates to mineral resource results is based on information compiled by Mr Tony Cormack who is a member of the Australasian Institute of Mining and Metallurgy. Tony Cormack is a full time employee of Atlas Iron Limited. Tony Cormack has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he has undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Tony Cormack consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

Geological Data, Interpretation and Resource Estimation – Alice Extension

The information in this report that relates to mineral resource results is based on information compiled by Mr Simon Gobbett who is a member of the Australasian Institute of Mining and Metallurgy. Simon Gobbett is a full time employee of Atlas Iron Limited. Simon Gobbett has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he has undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Simon Gobbett consents to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Competent Persons and JORC Compliance statements

atlas Iron Limited Annual Report 2009 25

Competent Persons and JORC Compliance statements (cont'd)

Reserve Estimation

The information in this report that relates to reserve estimations is based on information compiled by Mr Ken Brinsden, who is a member of the Australasian Institute of Mining and Metallurgy. Ken Brinsden is a full time employee of Atlas Iron Limited. Ken Brinsden has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he has undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Ken Brinsden consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

Atlas Iron Limited – Statement on Global Exploration Target

Atlas has reported a total resource inventory of 94.9 million tonnes at 56.5% Fe consisting of resources at Pardoo, Abydos, Mt Dove and Wodgina. While the Company intends to do further exploration on its tenements and remains optimistic it will report additional resources and reserves in the future, any discussion in relation to targets, resources, reserves or ‘ore’ over and above the resource of 94.9 million tonnes at 56.5% Fe is only conceptual in nature. There has been insufficient exploration to define a Mineral Resource over and above the resource of 94.9 million tonnes at 56.5% Fe, and it is uncertain if further exploration will result in the determination of a Mineral Resource over and above the resource of 94.9 million tonnes at 56.5% Fe.

Resource Estimation Ridley Deposit

The information in this report that relates to mineral resource results is based on information compiled by Mr Malcolm Titley who is a member of the Australasian Institute of Mining and Metallurgy. Malcolm Titley is a full time employee of CSA Global Pty Ltd. Malcolm Titley has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he has undertaken to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Malcolm Titley consents to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Ore Reserve Estimation Ridley Deposit

The sections in this report that relate to the Ridley Ore Reserves are based on information compiled under the direction of Mr Bruce Gregory. Mr Gregory is a Member of the Australasian Institute of Mining and Metallurgy and is a full time employee of AMC Consultants Pty Ltd. Mr Gregory has sufficient experience relevant to the style of mineralization and type of deposit under consideration to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration results, Mineral Resources and Ore Reserves’. Mr Gregory consents to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Dollars means Australian dollars.

Adam Liebenberg, Operations Mining Manager.

26 atlas Iron Limited Annual Report 200926

Corporate governance statement (cont'd)Corporate governance statement

Corporate goVernanCe Statement

The Company is committed to implementing and maintaining the highest standards of corporate governance. In determining what those standards should involve, the Company has turned to the ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations. The Company is pleased to advise its practices are largely consistent with those of the ASX guidelines.

In 2008, the Company decided to review all its corporate governance practices and policies in light of the publication of the 2nd Edition of ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations with a view to ensuring the Company’s corporate governance practices and policies are up to date and reflect the Company’s current stage of development as well as accommodating the Company’s future growth.

The Board considers that the Company is now of a size and its affairs of such complexity to justify the formation of a Remuneration Committee and a Nominations Committee. The charters for these two committees were approved in September 2008 and the committees were formed in compliance with the guidelines set out in the 2nd Edition of ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations. The Audit & Risk Committee, the Remuneration Committee and the Nomination Committee each make recommendations to the Board. The Board as a whole addresses the governance aspects of the full scope of the Company's activities to ensure that it adheres to appropriate ethical standards.

ThE BOARD Of DiRECTORsComposition of the Board

On 20 July 2009, shareholders approved a new Constitution that reflected changes to the Corporations Act 2001 and ASX Listing Rules. This ensured that the Company’s Constitution is up to date with best corporate practice. The Company's new Constitution provides that the number of directors shall not be less than three. There is no requirement for any share holding qualification.

As the Company's activities increase in size, nature and scope, the size of the Board will be reviewed periodically, and as circumstances demand. The optimum number of directors required to supervise adequately the Company's organisational nature and structure will be determined by the Board within the limitations imposed by the Constitution, as approved by shareholders on 20 July 2009.

The membership of the Board, its activities and composition, is subject to periodic review. The criteria for determining the identification and appointment of a suitable candidate for the

Board shall include quality of the individual, background of experience and achievement, compatibility with other Board members, credibility within the Company's scope of activities, intellectual ability to contribute to Board duties and physical ability to undertake Board duties and responsibilities.

Directors are initially appointed by the full Board subject to election by shareholders at the next general meeting. Under the Company's Constitution the tenure of a director (other than managing director, and only one managing director where the position is jointly held) is subject to reappointment by shareholders not later than the third anniversary following his or her last appointment. Subject to the requirements of the Corporations Act 2001, the Board does not subscribe to the principle of retirement age and there is no maximum period of service as a director. A managing director may be appointed for any period and on any terms the directors think fit and, subject to the terms of any agreement entered into, may revoke any appointment.

Role of the Board

On 14 June 2007 the Company established a formal Board Charter as per Recommendation 1.1. In broad terms, the Board is accountable to the shareholders and must ensure that the Company is properly managed to protect and enhance shareholders’ wealth and other interests. The Board Charter sets out the role and responsibilities of the Board within the governance structure of the Company and its related bodies corporate (as defined in the Corporations Act).

The Board is responsible for promoting the success of the Company in a way which ensures that the interests of shareholders and stakeholders are promoted and protected. The Board may delegate some powers and functions to the Managing Director for the day-to-day management of the Company. Powers and functions not delegated remain with the Board. The following are regarded as the key responsibilities and functions of the Board:

to develop, review and monitor the Company’s long-•term business strategies and provide strategic direction to management;

to approve the acquisition, establishment, disposal or •cessation of any significant business of the Company;

to ensure policies and procedures are in place to safeguard •the Company’s assets and business and to enable the Company to act ethically and prudently;

to develop and promote a system of corporate governance •which ensures the Company is properly managed and controlled;

to identify the Company’s principal risks and ensure that •it has in place appropriate systems of risk management, internal control, reporting and compliance and that management is taking appropriate action to minimise those risks;

Corporate governance statement (cont'd)

atlas Iron Limited Annual Report 2009 27

Corporate governance statement (cont'd)

to review and approve the Company’s financial •statements;

to monitor management’s performance and the Company’s •financial results on a regular basis;

to appoint, ratify, appraise and determine the remuneration •and benefits of the Managing Director;

to delegate powers to the Managing Director as necessary •to enable the day-to-day business of the Company to be carried on, and to regularly review those delegations;

to ensure that the Company has in place appropriate •systems to comply with relevant legal and regulatory requirements that impact on its operations;

to determine the appropriate capital management for •the Group including share and loan capital and dividend payments;

to determine and regularly review an appropriate •remuneration policy for employees of the Company;

to approve senior management succession plans and •significant changes to organisational structure;

to authorise the issue of shares, options, equity instruments •or other securities; and

establishing procedures which ensure that the Board is •in a position to exercise its powers and to discharge its responsibilities as set out in the Board Charter.

Other than as specifically reserved to the Board in the Board Charter, responsibility for the management of the Company’s business activities is delegated to the Managing Director who is accountable to the Board.

Appointments to Other Boards

Directors are required to take into consideration any potential conflicts of interest when accepting appointments to other Boards. In light of the time commitment required by appointment to the Board, non-executive directors are asked to limit the number of other directorships for the duration of their appointment with the Company. Non-executive directors are asked to provide the Board with details of other commitments and an indication of time involved. The Board will regularly review the time required of a non-executive director and make an assessment as to whether the directors are able to meet their commitment to the Company. The Nominations Committee is charged to regularly review the time required by a Director to effectively undertake his or her Board responsibilities (and Board committee responsibilities, where relevant) and determine whether each Director is meeting that requirement after identifying and considering details of that Director's other commitments.

Chairman

The Chairman of the Board, Mr Geoff Clifford, is an independent, non-executive director and a resident Australian citizen. The Chairman is responsible for leadership and effective performance of the Board and for the maintenance of relations between directors and management that are open, cordial and conducive to productive cooperation. The Chairman’s responsibilities are set out in more detail in the Board Charter and the Company’s Constitution, which is available in the corporate governance section of the Company’s website.

Director Independence

The independence of a Director is assessed in accordance with the guidelines set out in the 2nd Edition of ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations. In accordance with these guidelines, the Board assesses independence with reference to whether a Director is non-executive, not a member of management and who is free of any business or other relationship that could materially interfere with, or could reasonably be perceived to materially interfere with, the independent exercise of their judgement. In making this assessment, the Board considers all relevant facts and circumstances. Relationships that the Board will take into consideration when assessing independence are whether a director:

is a substantial shareholder of the company or an officer •of, or otherwise associated directly with, a substantial shareholder of the Company;

is employed, or has previously been employed in an •executive capacity by the Company or another group member, and there has not been a period of at least three years between ceasing such employment and serving on the Board;

has within the last three years been a principal of a •material professional advisor or a material consultant to the Company or another group member, or an employee materially associated with the service provided;

is a material supplier or customer of the Company or other •group member, or an officer of or otherwise associated directly or indirectly with a material supplier or customer; or

has a material contractual relationship with the Company •or another group member other than as a director.

The test of whether a relationship or business is material is •based on the nature of the relationship or business and on the circumstances and activities of the director. Materiality is considered from the perspective of the Company and its group members, the persons or organisations with which the director has an affiliation and from the perspective of the director. The Board reviews the independence of directors before they are appointed and on an annual

28 atlas Iron Limited Annual Report 200928

Corporate governance statement (cont'd)