CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN CABONNE COUNCIL SEWER Asset Management Plan Version March 2012 AM4SRRC

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

CABONNE COUNCIL

SEWER

Asset Management Plan

Version

March 2012

AM4SRRC

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Document Control Asset Management for Small, Rural or Remote Communities

Document ID: 59_280_110805 am4srrc amp word template v10.4

Rev No Date Revision Details Author Reviewer Approver

1 Draft RB/SM

Asset Management for Small, Rural or Remote Communities Practice Note

The Institute of Public Works Engineering Australia.

www.ipwea.org.au/AM4SRRC

© Copyright 2011 – All rights reserved.

- i -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY .................................................................................................................................. iii 2. INTRODUCTION .............................................................................................................................................. 1

2.1 Background ........................................................................................................................................... 1 2.2 Goals and Objectives of Asset Management ........................................................................................ 1 2.3 Plan Framework .................................................................................................................................... 2 2.4 Core and Advanced Asset Management ............................................................................................... 3 2.5 Community Consultation ...................................................................................................................... 3

3. LEVELS OF SERVICE ........................................................................................................................................ 4 3.1 Customer Research and Expectations ................................................................................................... 5 3.2 Legislative Requirements ...................................................................................................................... 5 3.3 Current Levels of Service ....................................................................................................................... 5 3.4 Desired Levels of Service ....................................................................................................................... 7

4. FUTURE DEMAND .......................................................................................................................................... 8 4.1 Demand Forecast .................................................................................................................................. 9 4.2 Changes in Technology .......................................................................................................................... 9 4.3 Demand Management Plan .................................................................................................................. 9 4.4 New Assets from Growth .................................................................................................................... 10

5. LIFECYCLE MANAGEMENT PLAN .................................................................................................................. 11 5.1 Background Data ................................................................................................................................. 11 5.2 Risk Management Plan ........................................................................................................................ 13 5.3 Routine Maintenance Plan .................................................................................................................. 13 5.4 Renewal/Replacement Plan ................................................................................................................ 15 5.5 Creation/Acquisition/Upgrade Plan .................................................................................................... 17 5.6 Disposal Plan ....................................................................................................................................... 18

6. FINANCIAL SUMMARY ................................................................................................................................. 19 6.1 Financial Statements and Projections ................................................................................................. 19 6.2 Funding Strategy ................................................................................................................................. 23 6.3 Valuation Forecasts ............................................................................................................................. 23 6.4 Key Assumptions made in Financial Forecasts .................................................................................... 25

7. ASSET MANAGEMENT PRACTICES ............................................................................................................... 27 7.1 Accounting/Financial Systems............................................................................................................. 27 7.2 Asset Management Systems ............................................................................................................... 27 7.3 Information Flow Requirements and Processes ................................................................................. 27 7.4 Standards and Guidelines ................................................................................................................... 28

8. PLAN IMPROVEMENT AND MONITORING ................................................................................................... 29 8.1 Performance Measures ....................................................................................................................... 29 8.2 Improvement Plan ............................................................................................................................... 29 8.3 Monitoring and Review Procedures .................................................................................................... 29

REFERENCES .......................................................................................................................................................... 30 APPENDICES .......................................................................................................................................................... 31

Appendix A Maintenance Response Levels of Service ................................................................................... 32 Appendix B Projected 10 year Capital Renewal Works Program ................................................................... 33 Appendix C Planned Upgrade/Exp/New 10 year Capital Works Program ...................................................... 37 Appendix D Abbreviations .............................................................................................................................. 41 Appendix E Glossary ....................................................................................................................................... 42

- ii -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

This page is left intentionally blank.

- iii -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

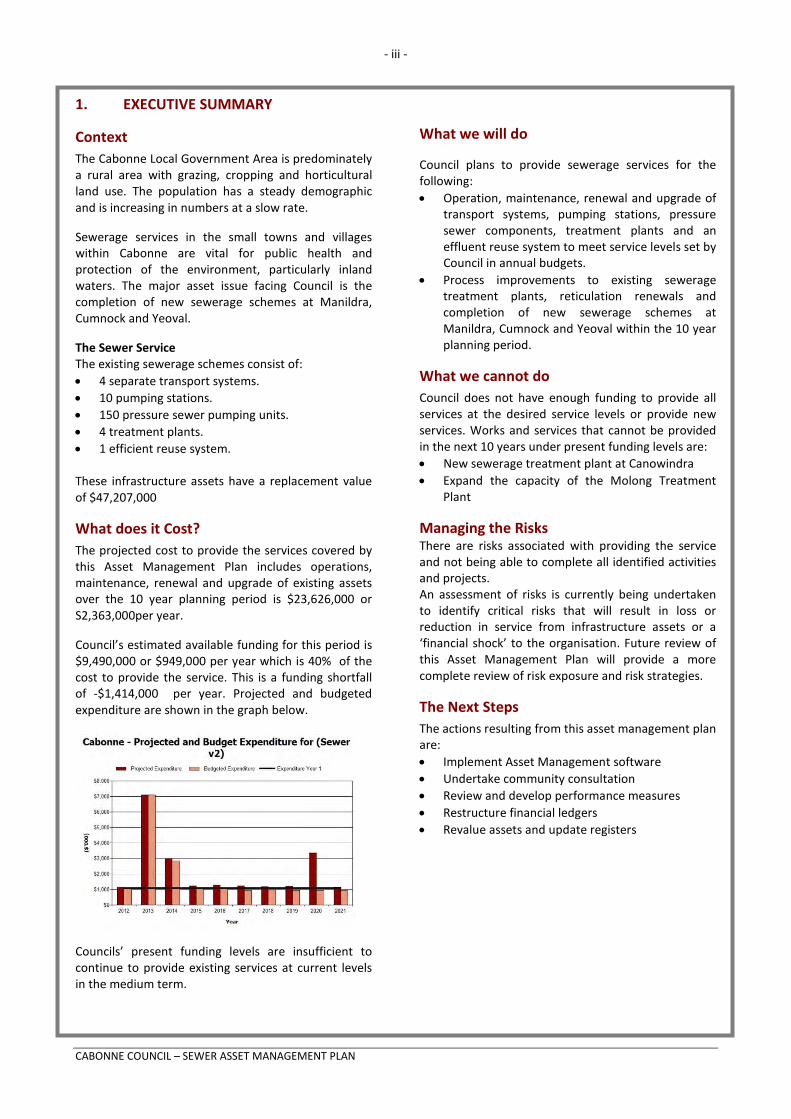

1. EXECUTIVE SUMMARY

Context The Cabonne Local Government Area is predominately a rural area with grazing, cropping and horticultural land use. The population has a steady demographic and is increasing in numbers at a slow rate.

Sewerage services in the small towns and villages within Cabonne are vital for public health and protection of the environment, particularly inland waters. The major asset issue facing Council is the completion of new sewerage schemes at Manildra, Cumnock and Yeoval.

The Sewer Service The existing sewerage schemes consist of: • 4 separate transport systems. • 10 pumping stations. • 150 pressure sewer pumping units. • 4 treatment plants. • 1 efficient reuse system. These infrastructure assets have a replacement value of $47,207,000

What does it Cost? The projected cost to provide the services covered by this Asset Management Plan includes operations, maintenance, renewal and upgrade of existing assets over the 10 year planning period is $23,626,000 or S2,363,000per year.

Council’s estimated available funding for this period is $9,490,000 or $949,000 per year which is 40% of the cost to provide the service. This is a funding shortfall of -$1,414,000 per year. Projected and budgeted expenditure are shown in the graph below.

Councils’ present funding levels are insufficient to continue to provide existing services at current levels in the medium term.

What we will do

Council plans to provide sewerage services for the following: • Operation, maintenance, renewal and upgrade of

transport systems, pumping stations, pressure sewer components, treatment plants and an effluent reuse system to meet service levels set by Council in annual budgets.

• Process improvements to existing sewerage treatment plants, reticulation renewals and completion of new sewerage schemes at Manildra, Cumnock and Yeoval within the 10 year planning period.

What we cannot do Council does not have enough funding to provide all services at the desired service levels or provide new services. Works and services that cannot be provided in the next 10 years under present funding levels are: • New sewerage treatment plant at Canowindra • Expand the capacity of the Molong Treatment

Plant

Managing the Risks There are risks associated with providing the service and not being able to complete all identified activities and projects. An assessment of risks is currently being undertaken to identify critical risks that will result in loss or reduction in service from infrastructure assets or a ‘financial shock’ to the organisation. Future review of this Asset Management Plan will provide a more complete review of risk exposure and risk strategies.

The Next Steps The actions resulting from this asset management plan are: • Implement Asset Management software • Undertake community consultation • Review and develop performance measures • Restructure financial ledgers • Revalue assets and update registers

- iv -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Questions you may have

What is this plan about?

This asset management plan covers the infrastructure assets that serve the Cabonne Community’s Sewerage needs. These assets include pipelines, pumping stations, treatment plants, effluent reuse systems and pressure sewer components throughout the Council area that enable people to be served with a reliable and environmentally sustainable sewerage system.

What is an Asset Management Plan?

Asset management planning is a comprehensive process to ensure delivery of services from infrastructure is provided in a financially sustainable manner.

An asset management plan details information about infrastructure assets including actions required to provide an agreed level of service in the most cost effective manner. The Plan defines the services to be provided, how the services are provided and what funds are required to provide the services.

Why is there a funding shortfall?

Most of the Council’s sewerage infrastructure was constructed from government grants often provided and accepted without consideration of ongoing operations, maintenance and replacement needs.

Many of these assets are approaching the later years of their life and require replacement, services from the assets are decreasing and maintenance costs are increasing.

Councils’ present funding levels are insufficient to continue to provide existing services at current levels in the medium term.

What options do we have?

Resolving the funding shortfall involves several steps: 1. Improving asset knowledge so that data

accurately records the asset inventory, how assets are performing and when assets are not able to provide the required service levels,

2. Improving our efficiency in operating, maintaining, replacing existing and constructing new assets to optimise life cycle costs,

3. Identifying and managing risks associated with providing services from infrastructure,

4. Making tradeoffs between service levels and costs to ensure that the community receives the best return from infrastructure,

5. Indentifying assets surplus to needs for disposal to make saving in future operations and maintenance costs

6. Consulting with the community to ensure that transport services and costs meet community needs and are affordable,

7. Developing partnership with other bodies, where available to provide services;

8. Seeking additional funding from governments and other bodies to better reflect a ‘whole of government’ funding approach to infrastructure services.

What happens if we don’t manage the shortfall?

It is likely that council will have to reduce service levels in some areas, unless new sources of revenue are found. For sewerage systems, the service level reduction may include unacceptable chokes and overflows and poor discharge quality to the environment.

What can we do?

Council can develop options and priorities for future sewerage services with costs of providing the services, consult with the community to plan future services to match the community services needs with ability to pay for services and maximise benefit to the community for costs to the community.

What can you do?

Council will be pleased to consider your thoughts on the issues raised in this asset management plan and suggestions on how Council may change or reduce its sewerage services mix to ensure that the appropriate level of service can be provided to the community within available funding.

.

- 1 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

2. INTRODUCTION

2.1 Background

This asset management plan is to demonstrate responsive management of assets (and services provided from assets), compliance with regulatory requirements, and to communicate funding needed to provide the required levels of service.

The asset management plan is to be read with Council’s Asset Management Policy, Asset Management Strategy and the following associated planning documents:

• Cabonne 2025 – Community Strategic Plan

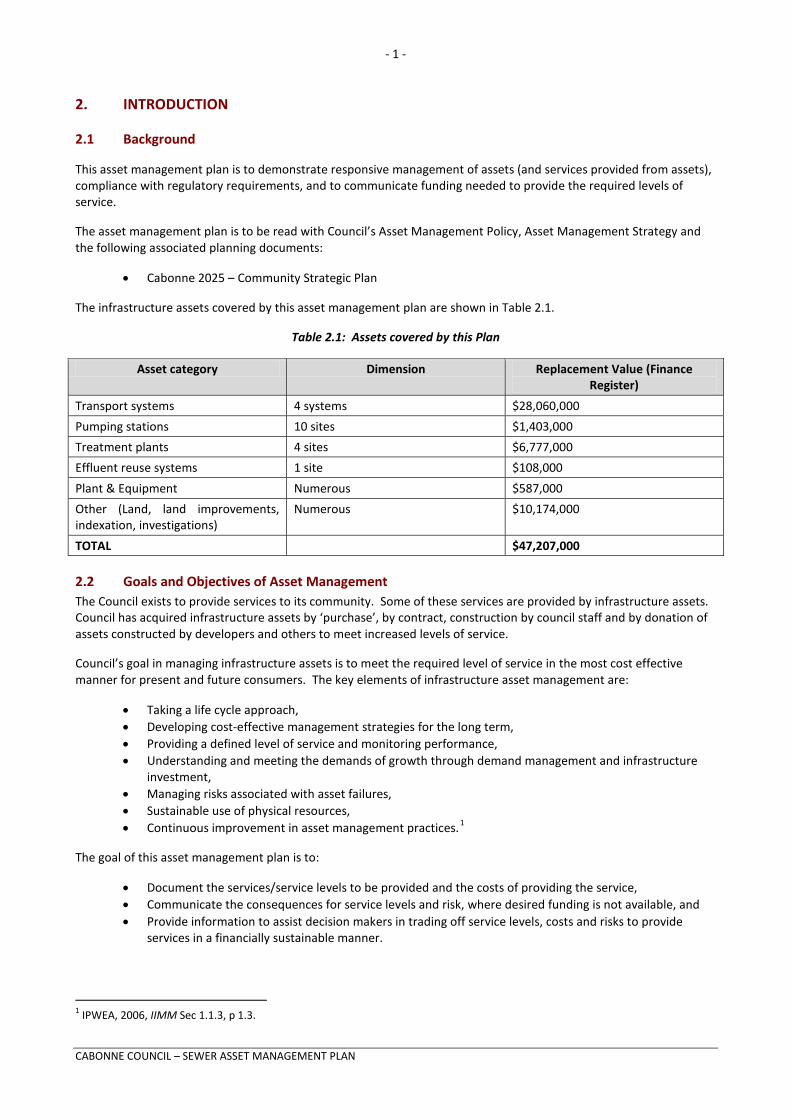

The infrastructure assets covered by this asset management plan are shown in Table 2.1.

Table 2.1: Assets covered by this Plan

Asset category Dimension Replacement Value (Finance Register)

Transport systems 4 systems $28,060,000

Pumping stations 10 sites $1,403,000

Treatment plants 4 sites $6,777,000

Effluent reuse systems 1 site $108,000

Plant & Equipment Numerous $587,000

Other (Land, land improvements, indexation, investigations)

Numerous $10,174,000

TOTAL $47,207,000 2.2 Goals and Objectives of Asset Management The Council exists to provide services to its community. Some of these services are provided by infrastructure assets. Council has acquired infrastructure assets by ‘purchase’, by contract, construction by council staff and by donation of assets constructed by developers and others to meet increased levels of service.

Council’s goal in managing infrastructure assets is to meet the required level of service in the most cost effective manner for present and future consumers. The key elements of infrastructure asset management are:

• Taking a life cycle approach, • Developing cost-effective management strategies for the long term, • Providing a defined level of service and monitoring performance, • Understanding and meeting the demands of growth through demand management and infrastructure

investment, • Managing risks associated with asset failures, • Sustainable use of physical resources, • Continuous improvement in asset management practices.1

The goal of this asset management plan is to:

• Document the services/service levels to be provided and the costs of providing the service, • Communicate the consequences for service levels and risk, where desired funding is not available, and • Provide information to assist decision makers in trading off service levels, costs and risks to provide

services in a financially sustainable manner.

1 IPWEA, 2006, IIMM Sec 1.1.3, p 1.3.

- 2 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

This asset management plan is prepared under the direction of Council’s vision, values, goals and objectives.

Council’s vision is:

Passionate people

Thriving villages and caring communities

Respecting and sustaining our environment

With an agricultural heart

Council’s values are:

In all we do, we will:

Respect each other, our community and the environment in which we live

Have the courage and confidence to ‘have a go’

Balance today’s decisions with the long-term future in mind

Be friendly, approachable and work together

Strive to do our very best and take personal responsibility for our actions

Relevant goals and objectives and how these are addressed in this asset management plan are shown in Table 2.2.

Table 2.2: Organisation Goals and how these are addressed in this Plan

Goal Objective How Goal and Objectives are addressed in AMP

5.3 Sustainable waste management practices are in place across Cabonne

5.3.3 Provide and maintain environmentally sustainable, high quality sewerage facilities

• Levels of service defined in asset management plan

• Strategies defined to manage the life cycle of sewer assets

•

5.3.4 Ensure adequate sewerage treatment and effluent management schemes in Cabonne

Upgrades included in upgrade/new asset plan

2.3 Plan Framework

Key elements of the plan are

• Levels of service – specifies the services and levels of service to be provided by council. • Future demand – how this will impact on future service delivery and how this is to be met. • Life cycle management – how the organisation will manage its existing and future assets to provide the

required services • Financial summary – what funds are required to provide the required services. • Asset management practices • Monitoring – how the plan will be monitored to ensure it is meeting the organisation’s objectives. • Asset management improvement plan

- 3 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

2.4 Core and Advanced Asset Management

This asset management plan is prepared as a first cut ‘core’ asset management plan in accordance with the International Infrastructure Management Manual2. It is prepared to meet minimum legislative and organisational requirements for sustainable service delivery and long term financial planning and reporting. Core asset management is a ‘top down’ approach where analysis is applied at the ‘system’ or ‘network’ level.

2.5 Community Consultation

This ‘core’ asset management plan is prepared to facilitate community consultation initially through feedback on public display of draft asset management plans prior to adoption by Council. Future revisions of the asset management plan will incorporate community consultation on service levels and costs of providing the service. This will assist Council and the community in matching the level of service needed by the community, service risks and consequences with the community’s ability to pay for the service.

2 IPWEA, 2006.

- 4 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

This page is left intentionally blank.

- 5 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

3. LEVELS OF SERVICE

3.1 Customer Research and Expectations

Council has not carried out any research on customer expectations. This will be investigated for future updates of the asset management plan.

3.2 Legislative Requirements

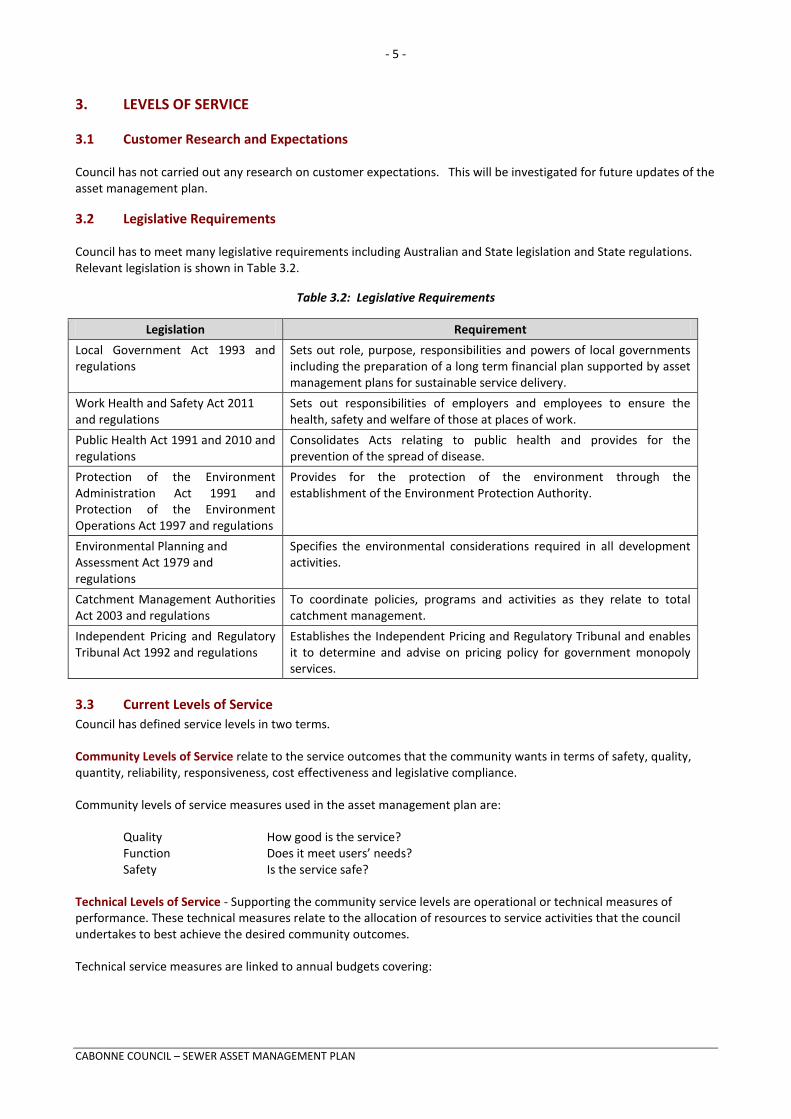

Council has to meet many legislative requirements including Australian and State legislation and State regulations. Relevant legislation is shown in Table 3.2.

Table 3.2: Legislative Requirements

Legislation Requirement

Local Government Act 1993 and regulations

Sets out role, purpose, responsibilities and powers of local governments including the preparation of a long term financial plan supported by asset management plans for sustainable service delivery.

Work Health and Safety Act 2011 and regulations

Sets out responsibilities of employers and employees to ensure the health, safety and welfare of those at places of work.

Public Health Act 1991 and 2010 and regulations

Consolidates Acts relating to public health and provides for the prevention of the spread of disease.

Protection of the Environment Administration Act 1991 and Protection of the Environment Operations Act 1997 and regulations

Provides for the protection of the environment through the establishment of the Environment Protection Authority.

Environmental Planning and Assessment Act 1979 and regulations

Specifies the environmental considerations required in all development activities.

Catchment Management Authorities Act 2003 and regulations

To coordinate policies, programs and activities as they relate to total catchment management.

Independent Pricing and Regulatory Tribunal Act 1992 and regulations

Establishes the Independent Pricing and Regulatory Tribunal and enables it to determine and advise on pricing policy for government monopoly services.

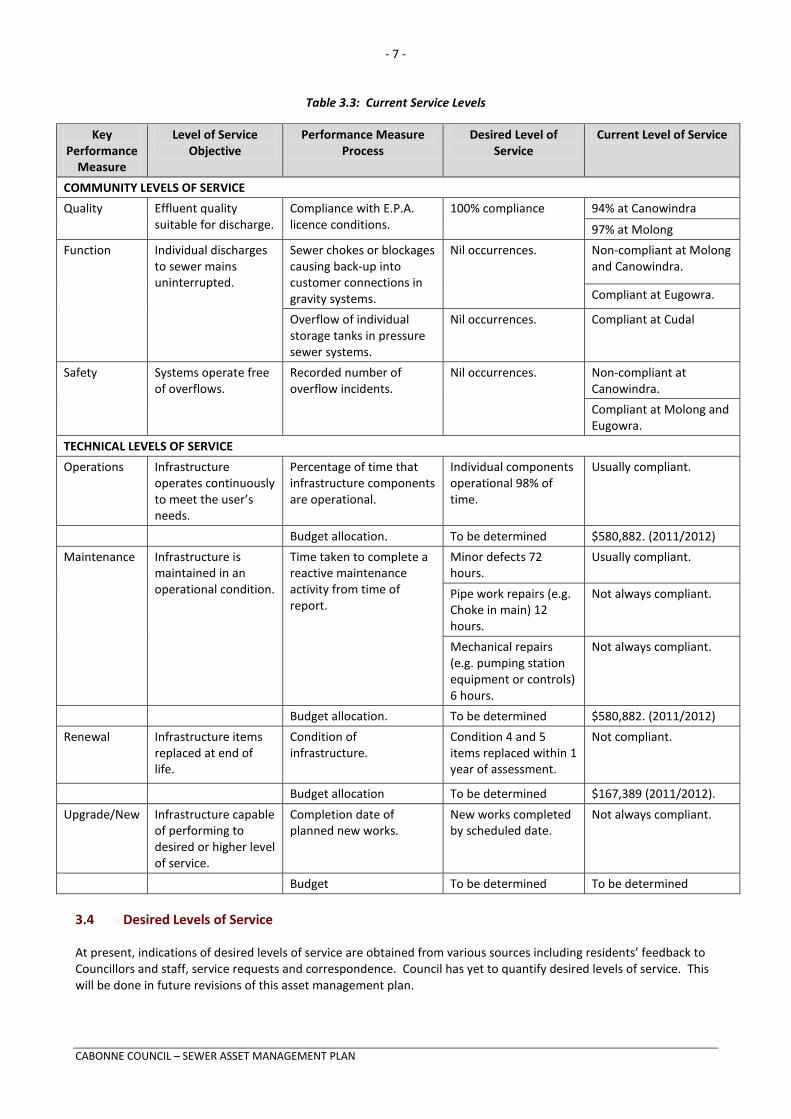

3.3 Current Levels of Service Council has defined service levels in two terms.

Community Levels of Service relate to the service outcomes that the community wants in terms of safety, quality, quantity, reliability, responsiveness, cost effectiveness and legislative compliance.

Community levels of service measures used in the asset management plan are:

Quality How good is the service? Function Does it meet users’ needs? Safety Is the service safe?

Technical Levels of Service - Supporting the community service levels are operational or technical measures of performance. These technical measures relate to the allocation of resources to service activities that the council undertakes to best achieve the desired community outcomes.

Technical service measures are linked to annual budgets covering:

- 6 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

• Operations – the regular activities to provide services such as opening hours, cleansing frequency, mowing frequency, etc.

• Maintenance – the activities necessary to retain an assets as near as practicable to its original condition (eg road patching, unsealed road grading, building and structure repairs),

• Renewal – the activities that return the service capability of an asset up to that which it had originally (eg frequency and cost of road resurfacing and pavement reconstruction, pipeline replacement and building component replacement),

• Upgrade – the activities to provide an higher level of service (eg widening a road, sealing an unsealed road, replacing a pipeline with a larger size) or a new service that did not exist previously (eg a new library).

Council’s current service levels are detailed in Table 3.3.

- 7 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Table 3.3: Current Service Levels

Key Performance

Measure

Level of Service Objective

Performance Measure Process

Desired Level of Service

Current Level of Service

COMMUNITY LEVELS OF SERVICE

Quality Effluent quality suitable for discharge.

Compliance with E.P.A. licence conditions.

100% compliance 94% at Canowindra

97% at Molong

Function Individual discharges to sewer mains uninterrupted.

Sewer chokes or blockages causing back-up into customer connections in gravity systems.

Nil occurrences. Non-compliant at Molong and Canowindra.

Compliant at Eugowra.

Overflow of individual storage tanks in pressure sewer systems.

Nil occurrences. Compliant at Cudal

Safety Systems operate free of overflows.

Recorded number of overflow incidents.

Nil occurrences. Non-compliant at Canowindra.

Compliant at Molong and Eugowra.

TECHNICAL LEVELS OF SERVICE

Operations Infrastructure operates continuously to meet the user’s needs.

Percentage of time that infrastructure components are operational.

Individual components operational 98% of time.

Usually compliant.

Budget allocation. To be determined $580,882. (2011/2012)

Maintenance Infrastructure is maintained in an operational condition.

Time taken to complete a reactive maintenance activity from time of report.

Minor defects 72 hours.

Usually compliant.

Pipe work repairs (e.g. Choke in main) 12 hours.

Not always compliant.

Mechanical repairs (e.g. pumping station equipment or controls) 6 hours.

Not always compliant.

Budget allocation. To be determined $580,882. (2011/2012)

Renewal Infrastructure items replaced at end of life.

Condition of infrastructure.

Condition 4 and 5 items replaced within 1 year of assessment.

Not compliant.

Budget allocation To be determined $167,389 (2011/2012).

Upgrade/New Infrastructure capable of performing to desired or higher level of service.

Completion date of planned new works.

New works completed by scheduled date.

Not always compliant.

Budget To be determined To be determined 3.4 Desired Levels of Service

At present, indications of desired levels of service are obtained from various sources including residents’ feedback to Councillors and staff, service requests and correspondence. Council has yet to quantify desired levels of service. This will be done in future revisions of this asset management plan.

- 8 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

This page is left intentionally blank.

- 9 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

4. FUTURE DEMAND

4.1 Demand Forecast

Factors affecting demand include population change, changes in demographics, seasonal factors, vehicle ownership, consumer preferences and expectations, economic factors, agricultural practices, environmental awareness, etc.

Demand factor trends and impacts on service delivery are summarised in Table 4.1.

Table 4.1: Demand Factors, Projections and Impact on Services

Demand factor Present position Projection Impact on services

Population 3738 (2011, population served with sewerage)

4272 (2031) 14% increase in discharge over 20 years.

Reticulation improvements

High levels of infiltration and inflow.

Infiltration/Inflow surveys leading to reticulation repairs or replacement.

Proportionate reduction in discharge.

Efficient use of water

Implementation of water supply demand management plan, particularly water saving devices.

Small decrease in discharges.

4.2 Changes in Technology

Technology changes forecast to affect the delivery of services covered by this plan are detailed in table 4.2.

Table 4.2: Changes in Technology and Forecast effect on Service Delivery

Technology Change Effect on Service Delivery

Geographic Information System (GIS) Efficiencies in data collection and retrieving information, which ensures more accurate information which improves the decision making process

Management Technology Knowledge of buildings, components, lives and costs is continually being improved.

4.3 Demand Management Plan

Demand for new services will be managed through a combination of managing existing assets, upgrading of existing assets and providing new assets to meet demand and demand management.

Opportunities identified to date for demand management are shown in Table 4.3. Further opportunities will be developed in future revisions of this asset management plan.

Table 4.3: Demand Management Plan Summary

Service Activity Demand Management Plan

Sewerage facilities Development to be encouraged in areas that will maximise use of existing assets without major upgrade, especially “infill” areas.

- 10 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

4.4 New Assets for Growth The new assets required to meet growth will be acquired free of cost from land developments and constructed/acquired by Council. The new contributed and constructed asset values are summarised in Figure 1.

Figure 1: New Assets for Growth

Acquiring these new assets will commit council to fund ongoing operations and maintenance costs for the period that the service provided from the assets is required. These future costs are identified and considered in developing forecasts of future operations and maintenance costs.

- 11 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

5. LIFECYCLE MANAGEMENT PLAN

The lifecycle management plan details how Council plans to manage and operate the assets at the agreed levels of service (defined in Section 3) while optimising life cycle costs.

5.1 Background Data

5.1.1 Physical parameters

The assets covered by this asset management plan are shown in Table 2.1.

Council’s sewerage assets are made up of the following mix:

• Transport system consisting of gravity sewer mains, rising mains and pressurised mains dating back to 1968 and up until 2010.

• Pumping stations including Betts Street Molong (1979), Thistle Street Molong (1979), King Street Molong (1994), Parkes Street Eugowra (1999), Sportsground Eugowra (1999), Nanima Street Eugowra (1999), Anzac Avenue Canowindra (1968), East Street Canowindra (1968), Moyne Canowindra (1970) and South Canowindra (1999).

• Pressure sewer components at Cudal (2010).

• Treatment plants including those at Molong (1979), Canowindra (1968), Eugowra (1999) and Cudal (2010).

• Effluent reuse system at Canowindra (1999).

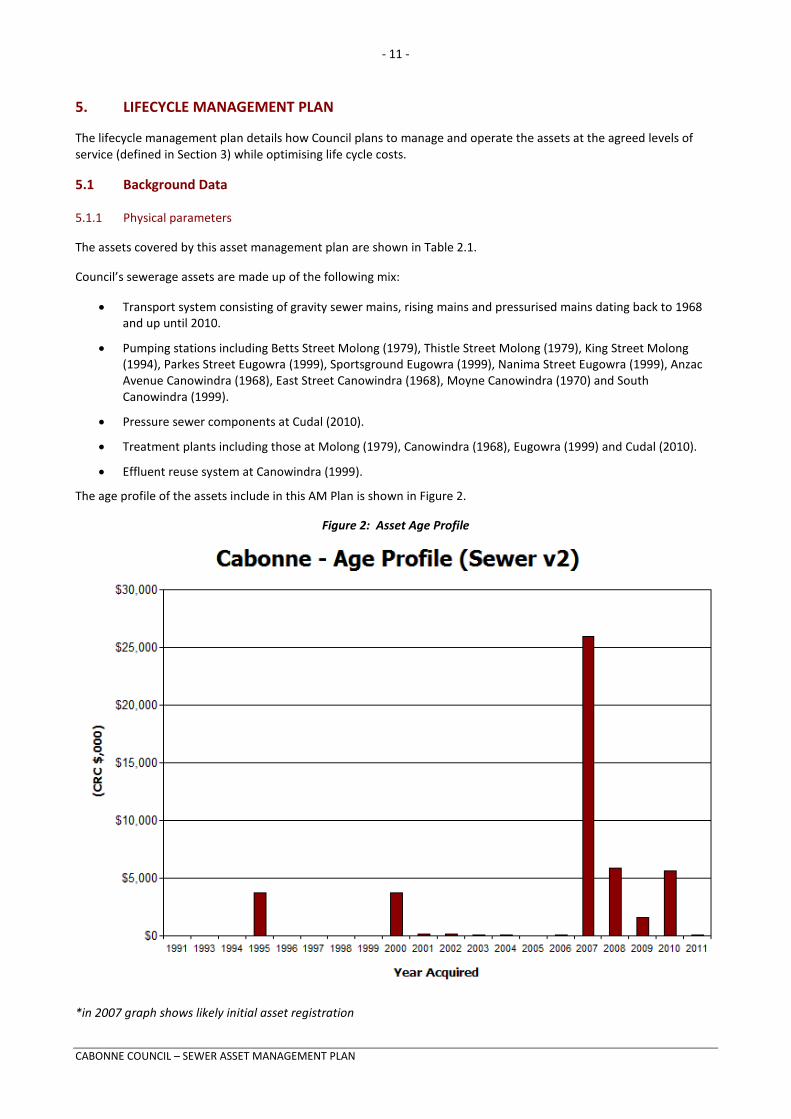

The age profile of the assets include in this AM Plan is shown in Figure 2.

Figure 2: Asset Age Profile

*in 2007 graph shows likely initial asset registration

- 12 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

5.1.2 Asset capacity and performance

Council’s services are generally provided to meet design standards where these are available.

Locations where deficiencies in service performance are known are detailed in Table 5.1.2.

Table 5.1.2: Known Service Performance Deficiencies

Location Service Deficiency

Molong Peak wet weather flows can be excessive. Targeted sewer main renewals needed together with a P.W.W.F. operating scheme and an emergency bypass channel from the flow monitoring point.

Problems experienced with effective drying of sludge. Additional sludge lagoons to be constructed.

Canowindra Occasional exceedance of licence conditions relating to concentration of faecal coliforms and total nitrogen when discharging to the river. Investigate discharge to river from second storage pond.

The above service deficiencies were identified from the Molong Sewerage Treatment Plant Investigation Report (January 2012) and the E.P.A. 2010/2011 annual Return for the Canowindra Sewerage Treatment Plant.

5.1.3 Asset condition

Asset condition information is not currently available, to be added in next update of the asset management plan.

Condition is measured using a 1 – 5 rating system3 as detailed in Table 5.1.3.

Table 5.1.3: IIMM Description of Condition

Condition Rating Description

1 Excellent condition: Only planned maintenance required.

2 Very good: Minor maintenance required plus planned maintenance.

3 Good: Significant maintenance required.

4 Fair: Significant renewal/upgrade required.

5 Poor: Unserviceable. 5.1.4 Asset valuations

The value of assets recorded in the asset register as at 30 June 2011 covered by this asset management plan is shown below. Assets were last revalued at 30 June 2008.

Current Replacement Cost $47,207,000

Depreciable Amount $46,831,000

Depreciated Replacement Cost $30,942,000

Annual Depreciation Expense $717,000

Council’s sustainability reporting reports the rate of annual asset consumption and compares this to asset renewal and asset upgrade and expansion.

Asset Consumption 1.5% (Depreciation/Depreciable Amount)

3 IIMM 2006, Appendix B, p B:1-3 (‘cyclic’ modified to ‘planned’, ‘average’ changed to ‘fair’’)

- 13 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Asset renewal 0% (Capital renewal exp/Depreciable amount)

Annual Upgrade/New 0.3% (Capital upgrade exp/Depreciable amount)

Annual Upgrade/New 0.3% (including contributed assets)

Council is currently renewing assets at 0.8%of the rate they are being consumed and increasing its asset stock by 0.3% each year.

To provide services in a financially sustainable manner, Council will need to ensure that it is renewing assets at the rate they are being consumed over the medium-long term and funding the life cycle costs for all new assets and services in its long term financial plan.

5.1.5 Asset hierarchy

An asset hierarchy provides a framework for structuring data in an information system to assist in collection of data, reporting information and making decisions. The hierarchy includes the asset class and component used for asset planning and financial reporting and service level hierarchy used for service planning and delivery.

Council’s service hierarchy is shown is Table 5.1.5.

Table 5.1.5: Asset Service Hierarchy

Service Hierarchy Service Level Objective

Molong Sewerage Provide an efficient sewerage system with minimal service interruption and environmentally sustainable discharges.

Canowindra Sewerage

Eugowra Sewerage

Cudal Sewerage

5.2 Risk Management Plan

Council’s policy for the management of risk is currently in the early stages of development. As such, some outcomes of this section on the management of risk are yet to be developed by Council. Future review of this Asset Management Plan will provide a more complete review of risk exposure and risk management strategy.

An assessment of risks associated with service delivery from infrastructure assets is currently being undertaken and will identify critical risks that will result in loss or reduction in service from infrastructure assets or a ‘financial shock’ to the organisation. The risk assessment process identifies credible risks, the likelihood of the risk event occurring, the consequences should the event occur, develops a risk rating, evaluates the risk and develops a risk treatment plan for non-acceptable risks. 5.3 Routine Maintenance Plan

Routine maintenance is the regular on-going work that is necessary to keep assets operating, including instances where portions of the asset fail and need immediate repair to make the asset operational again.

5.3.1 Maintenance plan

Maintenance includes reactive, planned and specific maintenance work activities.

Reactive maintenance is unplanned repair work carried out in response to service requests and management/supervisory directions.

- 14 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Planned maintenance is repair work that is identified and managed through a maintenance management system (MMS). MMS activities include inspection, assessing the condition against failure/breakdown experience, prioritising, scheduling, actioning the work and reporting what was done to develop a maintenance history and improve maintenance and service delivery performance.

Specific maintenance is replacement of higher value components/sub-components of assets that is undertaken on a regular cycle including repainting, building roof replacement, etc. This work generally falls below the capital/maintenance threshold but may require a specific budget allocation.

Actual past maintenance expenditure is shown in Table 5.3.1.

Table 5.3.1: Maintenance Expenditure Trends

Year Operations and Maintenance Expenditure

2008/2009 $445,000

2009/2010 $442,000

2010/2011 $541,000 Current maintenance expenditure levels are considered to be inadequate to meet required service levels. Future revision of this asset management plan will include linking required maintenance expenditures with required service levels.

Assessment and prioritisation of reactive maintenance is undertaken by operational staff using experience and judgement.

5.3.2 Standards and specifications

Maintenance work is carried out in accordance with the following Standards and Specifications.

• Operation and Maintenance manuals for Sewerage Treatment Plants. • Manufacturer’s guidelines for specialised equipment.

5.3.3 Summary of future operations and maintenance expenditures

Future operations and maintenance expenditure is forecast to trend in line with the value of the asset stock as shown in Figure 4. Note that all costs are shown in 2012dollar values.

- 15 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Figure 4: Projected Operations and Maintenance Expenditure

Deferred maintenance, ie works that are identified for maintenance and unable to be funded are to be included in the risk assessment process in the infrastructure risk management plan.

Maintenance is funded from the operating budget and grants where available. This is further discussed in Section 6.2.

5.4 Renewal/Replacement Plan

Renewal expenditure is major work which does not increase the asset’s design capacity but restores, rehabilitates, replaces or renews an existing asset to its original service potential. Work over and above restoring an asset to original service potential is upgrade/expansion or new works expenditure.

5.4.1 Renewal plan

Assets requiring renewal are identified from one of three methods provided in the ‘Expenditure Template”.

• Method 1 uses Asset Register data to project the renewal costs for renewal years using acquisition year and useful life, or

• Method 2 uses capital renewal expenditure projections from external condition modelling systems (such as Pavement Management Systems), or

• Method 3 uses a combination of average network renewals plus defect repairs in the Renewal Plan and Defect Repair Plan worksheets on the ‘Expenditure template’.

Method 1 was used for this asset management plan.

The ranking criteria used to determine priority of identified renewal proposals is detailed in Table 5.4.1.

- 16 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Table 5.4.1: Renewal Priority Ranking Criteria

Criteria Weighting

Asset condition 50%

Operational capacity 30%

Percentage of useful life 10%

Number of service requests 10%

Total 100% Renewal will be undertaken using ‘low-cost’ renewal methods where practical. The aim of ‘low-cost’ renewals is to restore the service potential or future economic benefits of the asset by renewing the assets at a cost less than replacement cost.

An example of low cost renewal is relining of pipelines instead of full replacement.

5.4.2 Renewal standards

Renewal work is carried out in accordance with the following Standards and Specifications.

• Manufacturer’s specifications for specialised equipment and products. • WAASA Code

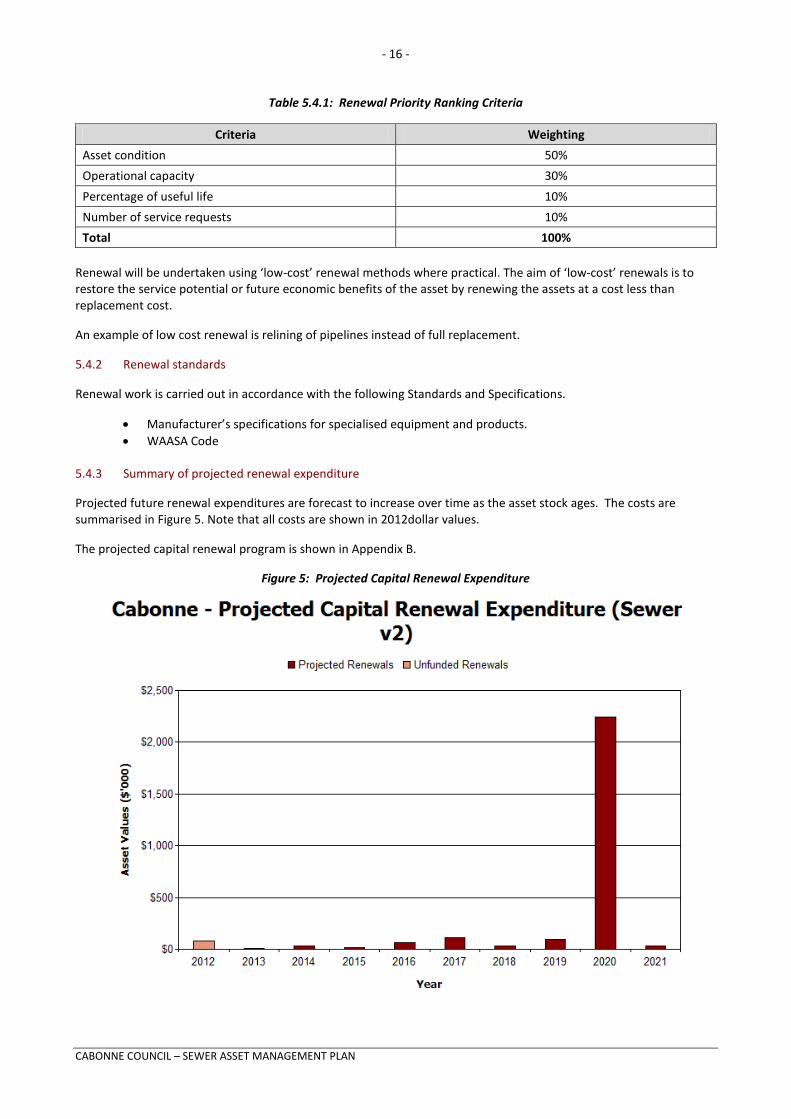

5.4.3 Summary of projected renewal expenditure

Projected future renewal expenditures are forecast to increase over time as the asset stock ages. The costs are summarised in Figure 5. Note that all costs are shown in 2012dollar values.

The projected capital renewal program is shown in Appendix B.

Figure 5: Projected Capital Renewal Expenditure

- 17 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Deferred renewal, ie those assets identified for renewal and not scheduled for renewal in capital works programs are to be included in the risk assessment process in the risk management plan.

Renewals are to be funded from capital works programs and grants where available. This is further discussed in Section 6.2.

5.5 Creation/Acquisition/Upgrade Plan

New works are those works that create a new asset that did not previously exist, or works which upgrade or improve an existing asset beyond its existing capacity. They may result from growth, social or environmental needs. Assets may also be acquired at no cost to the Council from land development. These assets from growth are considered in Section 4.4.

5.5.1 Selection criteria

New assets and upgrade/expansion of existing assets are identified from various sources such as councillor or community requests, proposals identified by strategic plans or partnerships with other organisations. Candidate proposals are inspected to verify need and to develop a preliminary estimate. Verified proposals are ranked by priority and available funds and scheduled in future works programmes. The priority ranking criteria is detailed in Table 5.5.1.

Table 5.5.1: Upgrade/New Assets Priority Ranking Criteria

Criteria Weighting

Imposition of new standards or requirements by higher tiers of government.

40%

Community pressure to reduce periods of interruption to service and/or overflows.

20%

Need to increase capacity because of increase in demand. 40%

Total 100% 5.5.2 Standards and specifications

Standards and specifications for new assets and for upgrade/expansion of existing assets are the same as those for renewal shown in Section 5.4.2.

5.5.3 Summary of projected upgrade/new assets expenditure

Projected upgrade/new asset expenditures are summarised in Figure 6. The projected upgrade/new capital works program is shown in Appendix C. All costs are shown in current 2012 dollar values.

The projected capital upgrade/new program is shown in Appendix C.

- 18 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Figure 6: Projected Capital Upgrade/New Asset Expenditure

New assets and services are to be funded from capital works program and grants where available. This is further discussed in Section 6.2.

5.6 Disposal Plan

Disposal includes any activity associated with disposal of a decommissioned asset including sale, demolition or relocation. Assets identified for possible decommissioning and disposal are shown in Table 5.6, together with estimated annual savings from not having to fund operations and maintenance of the assets. These assets will be further reinvestigated to determine the required levels of service and see what options are available for alternate service delivery, if any.

Where cashflow projections from asset disposals are not available, these will be developed in future revisions of this asset management plan.

Table 5.6: Assets identified for Disposal

Asset Reason for Disposal Timing Net Disposal Expenditure (Expend

+ve, Revenue –ve)

Operations & Maintenance Annual

Savings Nil

- 19 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

6. FINANCIAL SUMMARY

This section contains the financial requirements resulting from all the information presented in the previous sections of this asset management plan. The financial projections will be improved as further information becomes available on desired levels of service and current and projected future asset performance.

6.1 Financial Statements and Projections

The financial projections are shown in Figure 7 for projected operating (operations and maintenance) and capital expenditure (renewal and upgrade/expansion/new assets), net disposal expenditure and estimated budget funding.

Note that all costs are shown in 2012dollar values.

Figure 7: Projected Operating and Capital Expenditure and Budget

*operations and maintenance expenditure combined

6.1.1 Financial sustainability in service delivery

There are three key indicators for financial sustainability that have been considered in the analysis of the services provided by this asset category, these being long term life cycle costs/expenditures and medium term projected/budgeted expenditures over 5 and 10 years of the planning period.

Long term - Life Cycle Cost

Life cycle costs (or whole of life costs) are the average costs that are required to sustain the service levels over the longest asset life. Life cycle costs include operations and maintenance expenditure and asset consumption (depreciation expense). The life cycle cost for the services covered in this asset management plan is $1,660,000 per year (operations and maintenance expenditure plus depreciation expense in year 1).

Life cycle costs can be compared to life cycle expenditure to give an indicator of sustainability in service provision. Life cycle expenditure includes operations, maintenance and capital renewal expenditure in year 1. Life cycle expenditure

- 20 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

will vary depending on the timing of asset renewals. The life cycle expenditure at the start of the plan is $949,000 (operations and maintenance expenditure plus budgeted capital renewal expenditure in year 1).

A shortfall between life cycle cost and life cycle expenditure is the life cycle gap.

The life cycle gap for services covered by this asset management plan is -$711,000 per year (-ve = gap, +ve = surplus).

Life cycle expenditure is 57.2% of life cycle costs giving a life cycle sustainability index of 0.57

The life cycle costs and life cycle expenditure comparison highlights any difference between present outlays and the average cost of providing the service over the long term. If the life cycle expenditure is less than that life cycle cost, it is most likely that outlays will need to be increased or cuts in services made in the future.

Knowing the extent and timing of any required increase in outlays and the service consequences if funding is not available will assist organisations in providing services to their communities in a financially sustainable manner. This is the purpose of the asset management plans and long term financial plan.

Medium term – 10 year financial planning period

This asset management plan identifies the projected operations, maintenance and capital renewal expenditures required to provide an agreed level of service to the community over a 10 year period. This provides input into 10 year financial and funding plans aimed at providing the required services in a sustainable manner.

These projected expenditures may be compared to budgeted expenditures in the 10 year period to identify any funding shortfall. In a core asset management plan, a gap is generally due to increasing asset renewals for ageing assets.

The projected operations, maintenance and capital renewal expenditure required over the 10 year planning period is $2,363,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $949,000 per year giving a 10 year funding shortfall of -$1,414,000 per year and a 10 year sustainability indicator of 0.4 . This indicates that Council has 40% of the projected expenditures needed to provide the services documented in the asset management plan.

Medium Term – 5 year financial planning period

The projected operations, maintenance and capital renewal expenditure required over the first 5 years of the planning period is $3,110,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $949,000 per year giving a 5 year funding shortfall of -$2,161,000 . This is 31% of projected expenditures giving a 5 year sustainability indicator of 0.3.

Financial Sustainability Indicators

Figure 7A shows the financial sustainability indicators over the 10 year planning period and for the long term life cycle.

- 21 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Figure 7A: Financial Sustainability Indicators

Providing services from infrastructure in a sustainable manner requires the matching and managing of service levels, risks, projected expenditures and funding to achieve a financial sustainability indicator of 1.0 for the first years of the asset management plan and ideally over the 10 year life of the AM Plan.

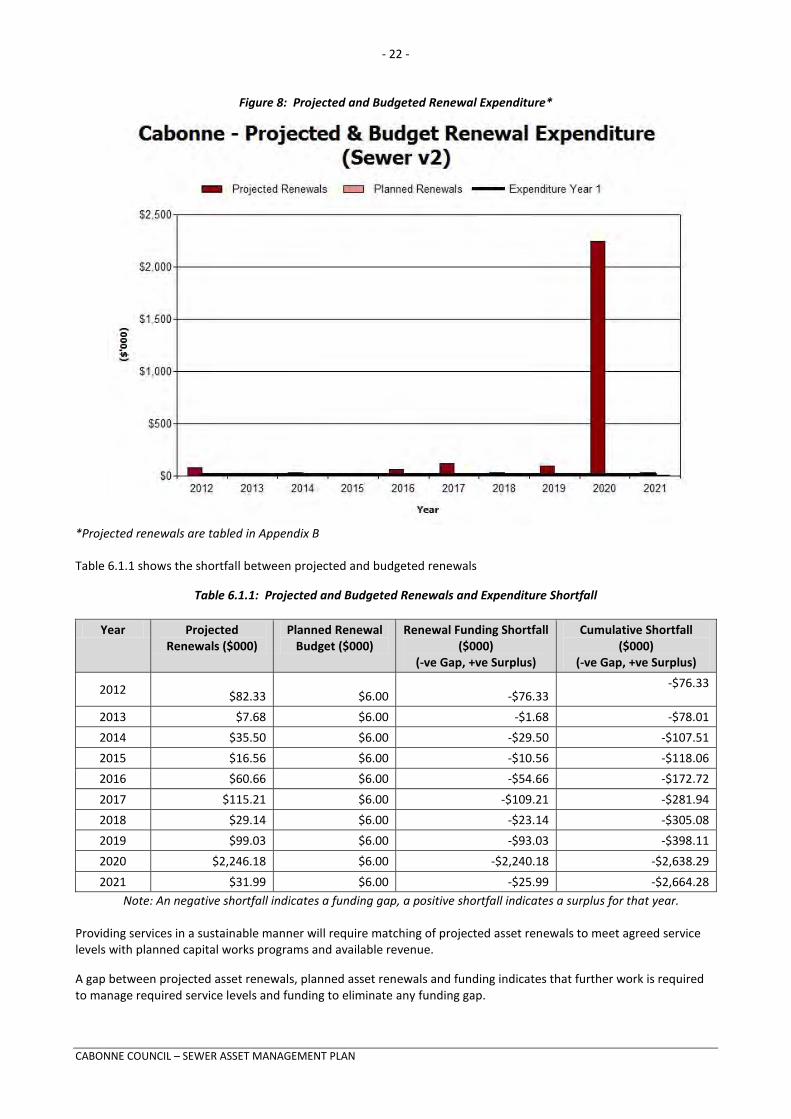

Figure 8 shows the projected asset renewals in the 10 year planning period from Appendix B. The projected asset renewals are compared to budgeted renewal expenditure in the capital works program and capital renewal expenditure in year 1 of the planning period in Figure 8.

- 22 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Figure 8: Projected and Budgeted Renewal Expenditure*

*Projected renewals are tabled in Appendix B

Table 6.1.1 shows the shortfall between projected and budgeted renewals

Table 6.1.1: Projected and Budgeted Renewals and Expenditure Shortfall

Year Projected Renewals ($000)

Planned Renewal Budget ($000)

Renewal Funding Shortfall ($000)

(-ve Gap, +ve Surplus)

Cumulative Shortfall ($000)

(-ve Gap, +ve Surplus)

2012 $82.33 $6.00 -$76.33 -$76.33

2013 $7.68 $6.00 -$1.68 -$78.01

2014 $35.50 $6.00 -$29.50 -$107.51

2015 $16.56 $6.00 -$10.56 -$118.06

2016 $60.66 $6.00 -$54.66 -$172.72

2017 $115.21 $6.00 -$109.21 -$281.94

2018 $29.14 $6.00 -$23.14 -$305.08

2019 $99.03 $6.00 -$93.03 -$398.11

2020 $2,246.18 $6.00 -$2,240.18 -$2,638.29

2021 $31.99 $6.00 -$25.99 -$2,664.28 Note: An negative shortfall indicates a funding gap, a positive shortfall indicates a surplus for that year.

Providing services in a sustainable manner will require matching of projected asset renewals to meet agreed service levels with planned capital works programs and available revenue.

A gap between projected asset renewals, planned asset renewals and funding indicates that further work is required to manage required service levels and funding to eliminate any funding gap.

- 23 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

We will manage the ‘gap’ by developing this asset management plan to provide guidance on future service levels and resources required to provide these services, and review future services, service levels and costs with the community.

6.1.2 Expenditure projections for long term financial plan

Table 6.1.2 shows the projected expenditures for the 10 year long term financial plan.

Expenditure projections are in current (non-inflated) values. Disposals are shown as net expenditures (revenues are negative).

Table 6.1.2: Expenditure Projections for Long Term Financial Plan ($000)

Year Operations & Maintenance

($000)

Projected Capital Renewal ($000)

Capital Upgrade/ New ($000)

Disposals ($000)

2012 $943.00 $82.33 $135.69 $0.00

2013 $945.71 $7.68 $6,157.00 $0.00

2014 $1,068.70 $35.50 $1,900.00 $0.00

2015 $1,106.66 $16.56 $100.00 $0.00

2016 $1,108.65 $60.66 $100.00 $0.00

2017 $1,110.65 $115.21 $0.00 $0.00

2018 $1,110.65 $29.14 $50.00 $0.00

2019 $1,111.65 $99.03 $0.00 $0.00

2020 $1,111.65 $2,246.18 $0.00 $0.00

2021 $1,111.65 $31.99 $0.00 $0.00 Note: All projected expenditures are in 2012values

6.2 Funding Strategy

Projected expenditure identified in Section 6.1 is to be funded from future operating and capital budgets. The funding strategy is detailed in the organisation’s 10 year long term financial plan.

6.3 Valuation Forecasts

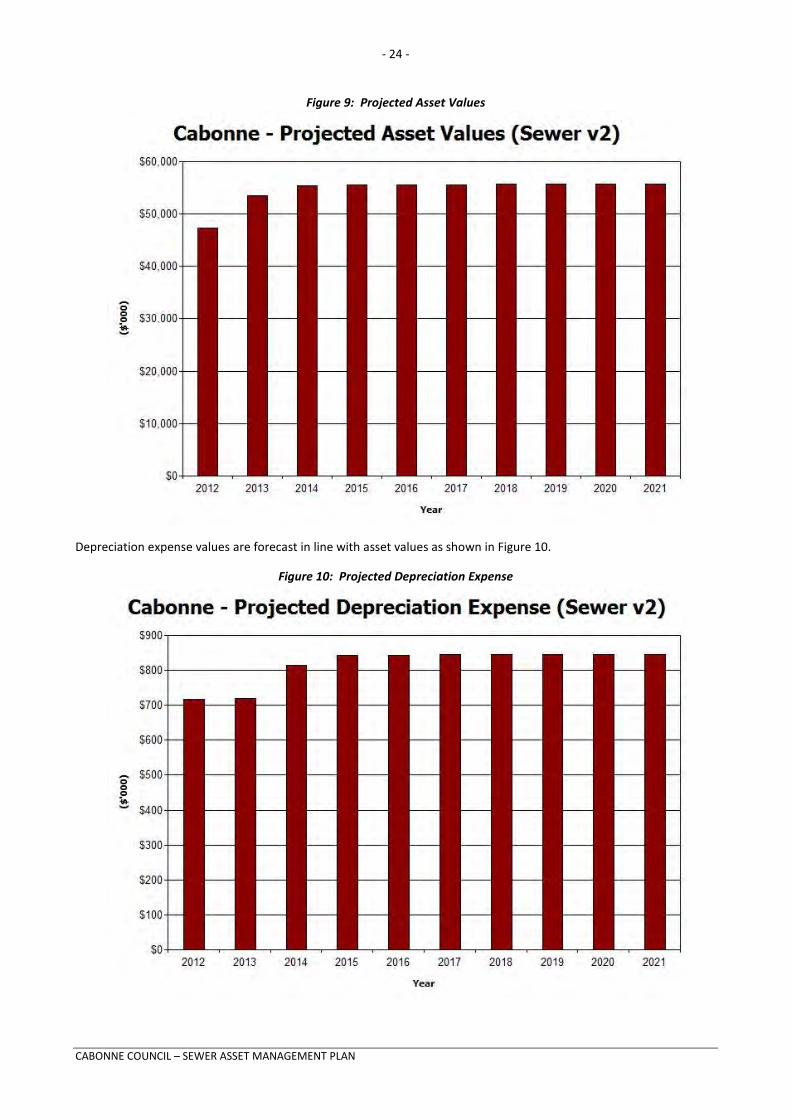

Asset values are forecast to increase as additional assets are added to the asset stock from construction and acquisition by Council and from assets constructed by land developers and others and donated to Council. Figure 9 shows the projected replacement cost asset values over the planning period in 2012dollar values.

- 24 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Figure 9: Projected Asset Values

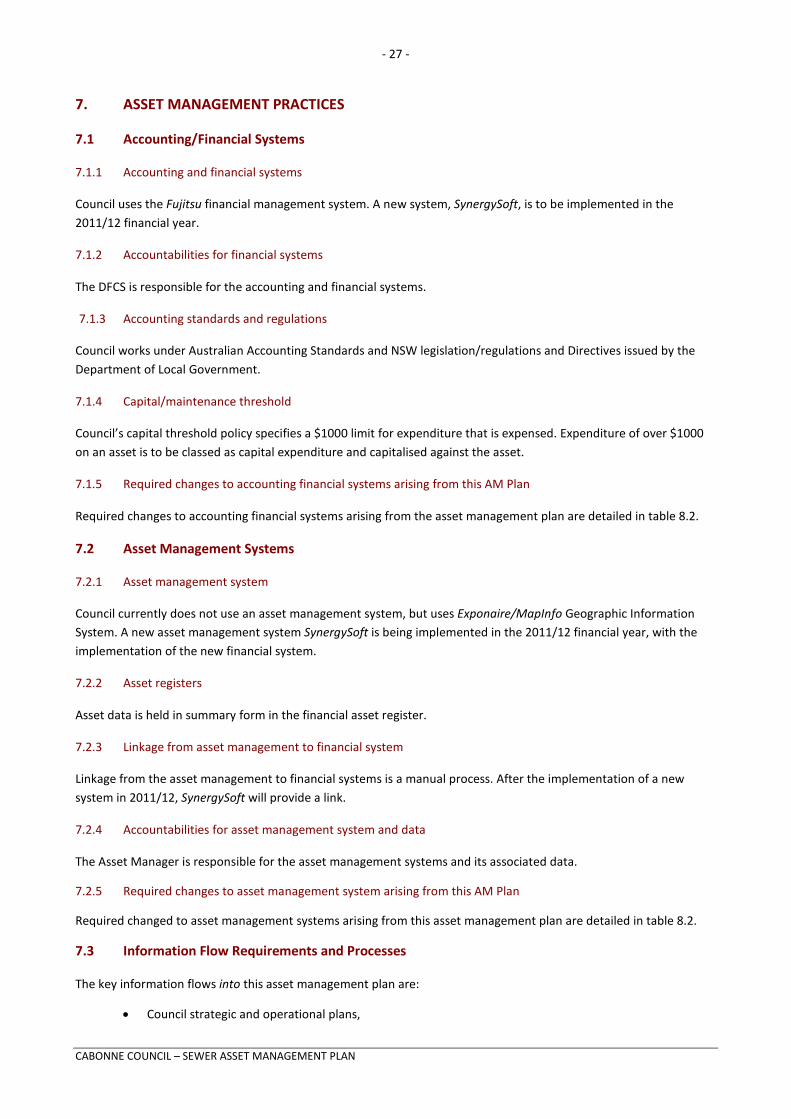

Depreciation expense values are forecast in line with asset values as shown in Figure 10.

Figure 10: Projected Depreciation Expense

- 25 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

The depreciated replacement cost (current replacement cost less accumulated depreciation) will vary over the forecast period depending on the rates of addition of new assets, disposal of old assets and consumption and renewal of existing assets. Forecast of the assets’ depreciated replacement cost is shown in Figure 11. The effect of contributed and new assets on the depreciated replacement cost is shown in the light colour bar.

Figure 11: Projected Depreciated Replacement Cost

6.4 Key Assumptions made in Financial Forecasts

This section details the key assumptions made in presenting the information contained in this asset management plan and in preparing forecasts of required operating and capital expenditure and asset values, depreciation expense and carrying amount estimates. It is presented to enable readers to gain an understanding of the levels of confidence in the data behind the financial forecasts.

Key assumptions made in this asset management plan are:

• Index rates used to revalue assets from last revaluation to current values • Assumptions on the relationships between growth and increases in the asset stock • Assumptions on changes to useful life estimated to reflect improved maintenance and renewal practices • Present service levels will remain constant for the life of the AM Plan.

- 26 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

This page is left intentionally blank.

- 27 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

7. ASSET MANAGEMENT PRACTICES

7.1 Accounting/Financial Systems

7.1.1 Accounting and financial systems

Council uses the Fujitsu financial management system. A new system, SynergySoft, is to be implemented in the 2011/12 financial year.

7.1.2 Accountabilities for financial systems

The DFCS is responsible for the accounting and financial systems.

7.1.3 Accounting standards and regulations

Council works under Australian Accounting Standards and NSW legislation/regulations and Directives issued by the Department of Local Government.

7.1.4 Capital/maintenance threshold

Council’s capital threshold policy specifies a $1000 limit for expenditure that is expensed. Expenditure of over $1000 on an asset is to be classed as capital expenditure and capitalised against the asset.

7.1.5 Required changes to accounting financial systems arising from this AM Plan

Required changes to accounting financial systems arising from the asset management plan are detailed in table 8.2.

7.2 Asset Management Systems

7.2.1 Asset management system

Council currently does not use an asset management system, but uses Exponaire/MapInfo Geographic Information System. A new asset management system SynergySoft is being implemented in the 2011/12 financial year, with the implementation of the new financial system.

7.2.2 Asset registers

Asset data is held in summary form in the financial asset register.

7.2.3 Linkage from asset management to financial system

Linkage from the asset management to financial systems is a manual process. After the implementation of a new system in 2011/12, SynergySoft will provide a link.

7.2.4 Accountabilities for asset management system and data

The Asset Manager is responsible for the asset management systems and its associated data.

7.2.5 Required changes to asset management system arising from this AM Plan

Required changed to asset management systems arising from this asset management plan are detailed in table 8.2.

7.3 Information Flow Requirements and Processes

The key information flows into this asset management plan are:

• Council strategic and operational plans,

- 28 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

• Service requests from the community, • Network assets information, • The unit rates for categories of work/materials, • Current levels of service, expenditures, service deficiencies and service risks, • Projections of various factors affecting future demand for services and new assets acquired by Council, • Future capital works programs, • Financial asset values.

The key information flows from this asset management plan are:

• The projected Works Program and trends, • The resulting budget and long term financial plan expenditure projections, • Financial sustainability indicators.

These will impact the Long Term Financial Plan, Strategic Longer-Term Plan, annual budget and departmental business plans and budgets.

7.4 Standards and Guidelines

Standards, guidelines and policy documents referenced in this asset management plan are:

• Cabonne Council Asset Management Policy • Cabonne Council Asset Accounting Policy • Cabonne Council Capital Threshold Policy • Cabonne Council Asset Management Strategy • Cabonne Council Procedures Manual

- 29 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

8. PLAN IMPROVEMENT AND MONITORING

8.1 Performance Measures

The effectiveness of the asset management plan can be measured in the following ways:

• The degree to which the required cashflows identified in this asset management plan are incorporated into the organisation’s long term financial plan and Community/Strategic Planning processes and documents,

• The degree to which 1-5 year detailed works programs, budgets, business plans and organisational structures take into account the ‘global’ works program trends provided by the asset management plan;

8.2 Improvement Plan

The asset management improvement plan generated from this asset management plan is shown in Table 8.2.

Table 8.2: Improvement Plan

Task No

Task Responsibility Resources Required

Timeline

1 Asset Information System – implement software package, providing asset deterioration modelling and other tools and links to GIS system

2 Revalue sewer assets and update the asset register to ensure the financial and operational technical asset registers reflect the same sewer inventory to ensure data accuracy

3 Finance – restructure ledgers so as to separate operations, maintenance and renewal costs at asset class levels

4 Community consultation – undertake targeted engagement with the community to resolve acceptable and achievable levels of service

5 Review and develop performance measures and reporting

6 Condition rating – refine data collection and analysis processes, including greater levels of componentisation. Develop and implement data capture and conditioning process

7 Carry out Infrastructure Risk Management Planning process to consider the consequences of failure for each asset group, and impact of failure on the community

8 Develop and adopt Asset Management Policy and Strategy

8.3 Monitoring and Review Procedures

This asset management plan will be reviewed during annual budget preparation and amended to recognise any material changes in service levels and/or resources available to provide those services as a result of the budget decision process.

The Plan has a life of 4 years and is due for revision and updating within 2 years of each Council election.

- 30 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

REFERENCES

Cabonne 2025 – Community Strategic Plan, Cabonne Council

Cabonne Council, Budget 2011/12

DVC, 2006, Asset Investment Guidelines, Glossary, Department for Victorian Communities, Local Government Victoria, Melbourne, http://www.dpcd.vic.gov.au/localgovernment/publications-and-research/asset-management-and-financial.

IPWEA, 2006, International Infrastructure Management Manual, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au.

IPWEA, 2008, NAMS.PLUS Asset Management Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/namsplus.

IPWEA, 2009, Australian Infrastructure Financial Management Guidelines, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/AIFMG.

IPWEA, 2011, Asset Management for Small, Rural or Remote Communities Practice Note, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/AM4SRRC.

- 31 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

APPENDICES

Appendix A Maintenance Response Levels of Service

Appendix B Projected 10 year Capital Renewal Works Program

Appendix C Planned Upgrade/Exp/New 10 year Capital Works Program A

Appendix D Abbreviations

Appendix E Glossary

- 32 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Appendix A Maintenance Response Levels of Service

To be developed.

- 33 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

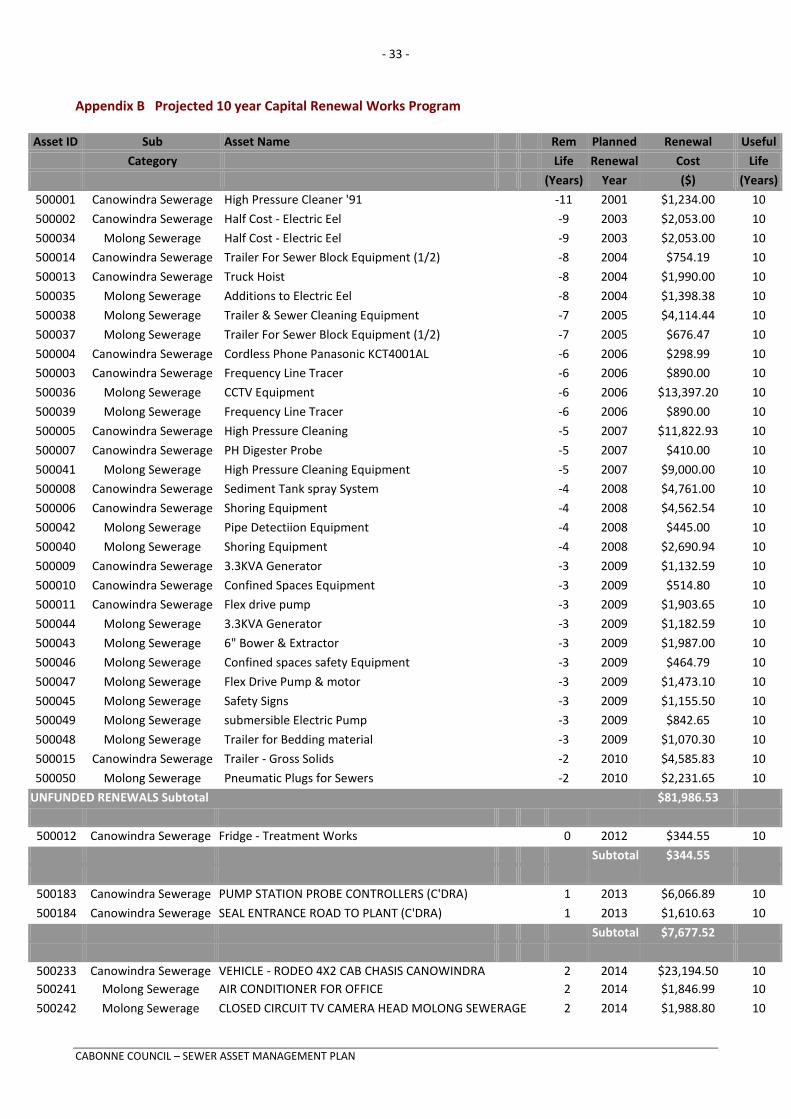

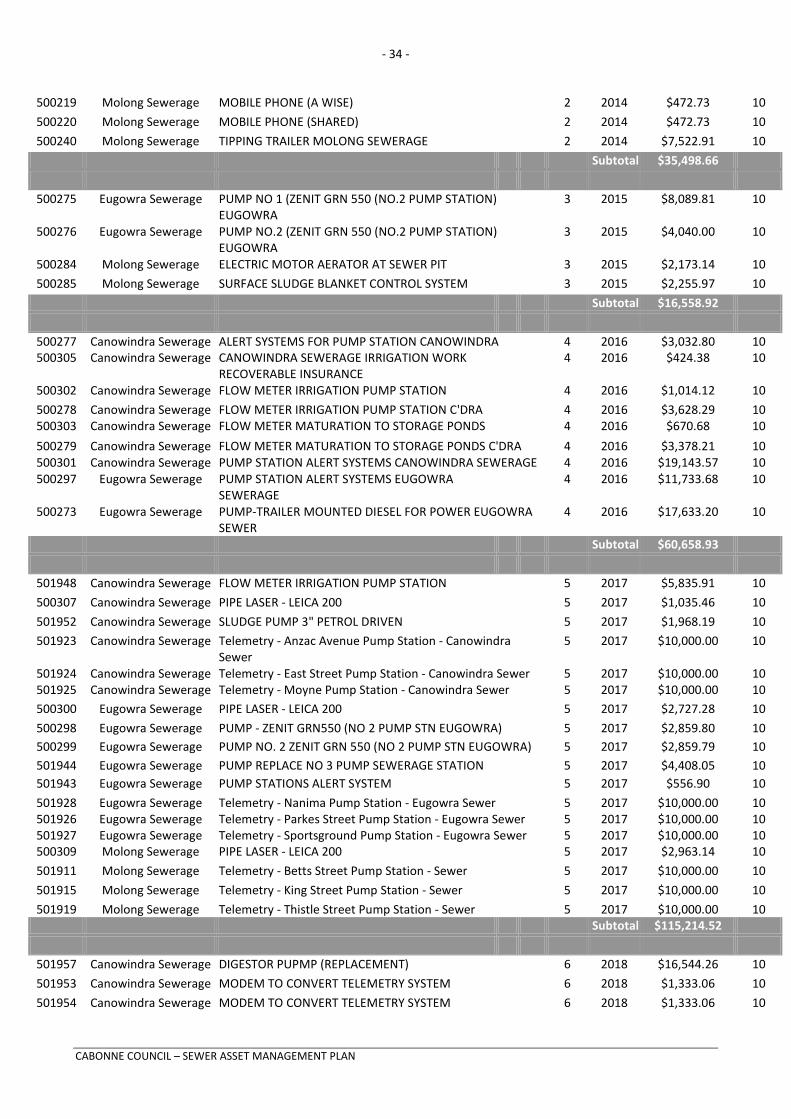

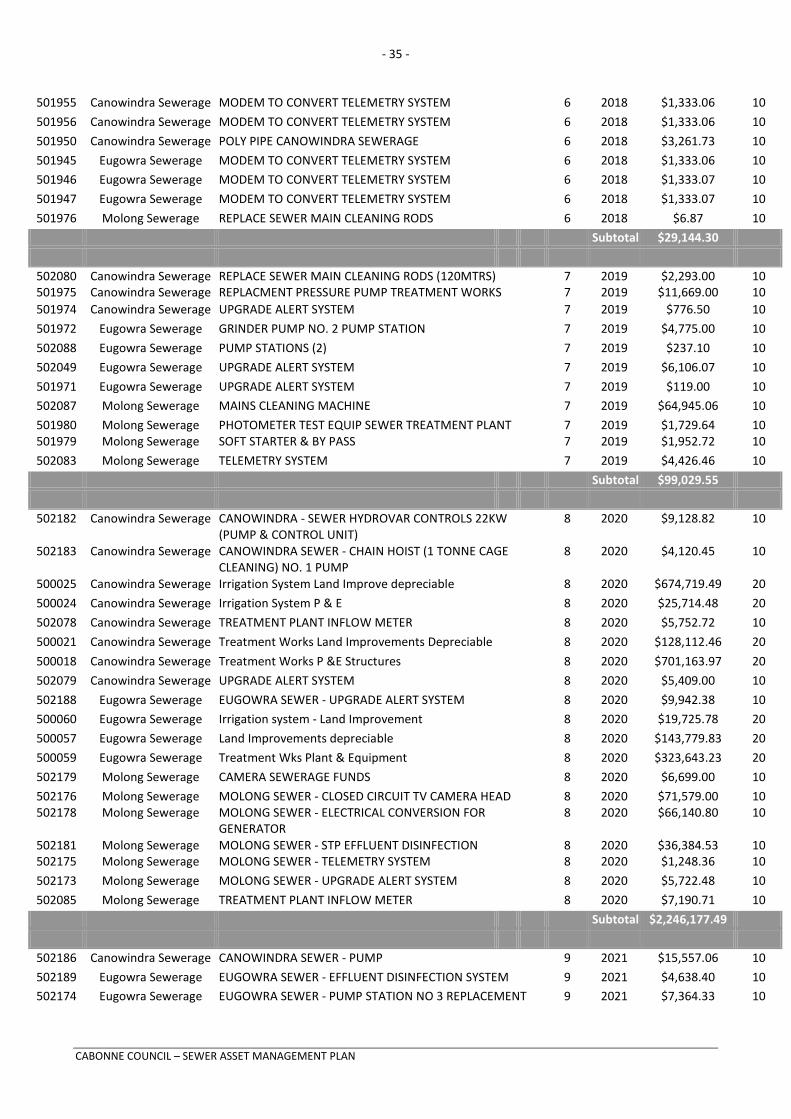

Appendix B Projected 10 year Capital Renewal Works Program

Asset ID Sub Asset Name Rem Planned Renewal Useful

Category Life Renewal Cost Life

(Years) Year ($) (Years)

500001 Canowindra Sewerage High Pressure Cleaner '91 -11 2001 $1,234.00 10

500002 Canowindra Sewerage Half Cost - Electric Eel -9 2003 $2,053.00 10

500034 Molong Sewerage Half Cost - Electric Eel -9 2003 $2,053.00 10

500014 Canowindra Sewerage Trailer For Sewer Block Equipment (1/2) -8 2004 $754.19 10

500013 Canowindra Sewerage Truck Hoist -8 2004 $1,990.00 10

500035 Molong Sewerage Additions to Electric Eel -8 2004 $1,398.38 10

500038 Molong Sewerage Trailer & Sewer Cleaning Equipment -7 2005 $4,114.44 10

500037 Molong Sewerage Trailer For Sewer Block Equipment (1/2) -7 2005 $676.47 10

500004 Canowindra Sewerage Cordless Phone Panasonic KCT4001AL -6 2006 $298.99 10

500003 Canowindra Sewerage Frequency Line Tracer -6 2006 $890.00 10

500036 Molong Sewerage CCTV Equipment -6 2006 $13,397.20 10

500039 Molong Sewerage Frequency Line Tracer -6 2006 $890.00 10

500005 Canowindra Sewerage High Pressure Cleaning -5 2007 $11,822.93 10

500007 Canowindra Sewerage PH Digester Probe -5 2007 $410.00 10

500041 Molong Sewerage High Pressure Cleaning Equipment -5 2007 $9,000.00 10

500008 Canowindra Sewerage Sediment Tank spray System -4 2008 $4,761.00 10

500006 Canowindra Sewerage Shoring Equipment -4 2008 $4,562.54 10

500042 Molong Sewerage Pipe Detectiion Equipment -4 2008 $445.00 10

500040 Molong Sewerage Shoring Equipment -4 2008 $2,690.94 10

500009 Canowindra Sewerage 3.3KVA Generator -3 2009 $1,132.59 10

500010 Canowindra Sewerage Confined Spaces Equipment -3 2009 $514.80 10

500011 Canowindra Sewerage Flex drive pump -3 2009 $1,903.65 10

500044 Molong Sewerage 3.3KVA Generator -3 2009 $1,182.59 10

500043 Molong Sewerage 6" Bower & Extractor -3 2009 $1,987.00 10

500046 Molong Sewerage Confined spaces safety Equipment -3 2009 $464.79 10

500047 Molong Sewerage Flex Drive Pump & motor -3 2009 $1,473.10 10

500045 Molong Sewerage Safety Signs -3 2009 $1,155.50 10

500049 Molong Sewerage submersible Electric Pump -3 2009 $842.65 10

500048 Molong Sewerage Trailer for Bedding material -3 2009 $1,070.30 10

500015 Canowindra Sewerage Trailer - Gross Solids -2 2010 $4,585.83 10

500050 Molong Sewerage Pneumatic Plugs for Sewers -2 2010 $2,231.65 10

UNFUNDED RENEWALS Subtotal $81,986.53

500012 Canowindra Sewerage Fridge - Treatment Works 0 2012 $344.55 10

Subtotal $344.55

500183 Canowindra Sewerage PUMP STATION PROBE CONTROLLERS (C'DRA) 1 2013 $6,066.89 10

500184 Canowindra Sewerage SEAL ENTRANCE ROAD TO PLANT (C'DRA) 1 2013 $1,610.63 10

Subtotal $7,677.52

500233 Canowindra Sewerage VEHICLE - RODEO 4X2 CAB CHASIS CANOWINDRA 2 2014 $23,194.50 10 500241 Molong Sewerage AIR CONDITIONER FOR OFFICE 2 2014 $1,846.99 10

500242 Molong Sewerage CLOSED CIRCUIT TV CAMERA HEAD MOLONG SEWERAGE 2 2014 $1,988.80 10

- 34 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

500219 Molong Sewerage MOBILE PHONE (A WISE) 2 2014 $472.73 10

500220 Molong Sewerage MOBILE PHONE (SHARED) 2 2014 $472.73 10

500240 Molong Sewerage TIPPING TRAILER MOLONG SEWERAGE 2 2014 $7,522.91 10

Subtotal $35,498.66

500275 Eugowra Sewerage PUMP NO 1 (ZENIT GRN 550 (NO.2 PUMP STATION)

EUGOWRA 3 2015 $8,089.81 10

500276 Eugowra Sewerage PUMP NO.2 (ZENIT GRN 550 (NO.2 PUMP STATION) EUGOWRA

3 2015 $4,040.00 10

500284 Molong Sewerage ELECTRIC MOTOR AERATOR AT SEWER PIT 3 2015 $2,173.14 10

500285 Molong Sewerage SURFACE SLUDGE BLANKET CONTROL SYSTEM 3 2015 $2,255.97 10

Subtotal $16,558.92

500277 Canowindra Sewerage ALERT SYSTEMS FOR PUMP STATION CANOWINDRA 4 2016 $3,032.80 10 500305 Canowindra Sewerage CANOWINDRA SEWERAGE IRRIGATION WORK

RECOVERABLE INSURANCE 4 2016 $424.38 10

500302 Canowindra Sewerage FLOW METER IRRIGATION PUMP STATION 4 2016 $1,014.12 10

500278 Canowindra Sewerage FLOW METER IRRIGATION PUMP STATION C'DRA 4 2016 $3,628.29 10 500303 Canowindra Sewerage FLOW METER MATURATION TO STORAGE PONDS 4 2016 $670.68 10

500279 Canowindra Sewerage FLOW METER MATURATION TO STORAGE PONDS C'DRA 4 2016 $3,378.21 10 500301 Canowindra Sewerage PUMP STATION ALERT SYSTEMS CANOWINDRA SEWERAGE 4 2016 $19,143.57 10 500297 Eugowra Sewerage PUMP STATION ALERT SYSTEMS EUGOWRA

SEWERAGE 4 2016 $11,733.68 10

500273 Eugowra Sewerage PUMP-TRAILER MOUNTED DIESEL FOR POWER EUGOWRA SEWER

4 2016 $17,633.20 10

Subtotal $60,658.93

501948 Canowindra Sewerage FLOW METER IRRIGATION PUMP STATION 5 2017 $5,835.91 10

500307 Canowindra Sewerage PIPE LASER - LEICA 200 5 2017 $1,035.46 10

501952 Canowindra Sewerage SLUDGE PUMP 3" PETROL DRIVEN 5 2017 $1,968.19 10

501923 Canowindra Sewerage Telemetry - Anzac Avenue Pump Station - Canowindra Sewer

5 2017 $10,000.00 10

501924 Canowindra Sewerage Telemetry - East Street Pump Station - Canowindra Sewer 5 2017 $10,000.00 10 501925 Canowindra Sewerage Telemetry - Moyne Pump Station - Canowindra Sewer 5 2017 $10,000.00 10

500300 Eugowra Sewerage PIPE LASER - LEICA 200 5 2017 $2,727.28 10

500298 Eugowra Sewerage PUMP - ZENIT GRN550 (NO 2 PUMP STN EUGOWRA) 5 2017 $2,859.80 10 500299 Eugowra Sewerage PUMP NO. 2 ZENIT GRN 550 (NO 2 PUMP STN EUGOWRA) 5 2017 $2,859.79 10 501944 Eugowra Sewerage PUMP REPLACE NO 3 PUMP SEWERAGE STATION 5 2017 $4,408.05 10 501943 Eugowra Sewerage PUMP STATIONS ALERT SYSTEM 5 2017 $556.90 10

501928 Eugowra Sewerage Telemetry - Nanima Pump Station - Eugowra Sewer 5 2017 $10,000.00 10 501926 Eugowra Sewerage Telemetry - Parkes Street Pump Station - Eugowra Sewer 5 2017 $10,000.00 10 501927 Eugowra Sewerage Telemetry - Sportsground Pump Station - Eugowra Sewer 5 2017 $10,000.00 10 500309 Molong Sewerage PIPE LASER - LEICA 200 5 2017 $2,963.14 10

501911 Molong Sewerage Telemetry - Betts Street Pump Station - Sewer 5 2017 $10,000.00 10

501915 Molong Sewerage Telemetry - King Street Pump Station - Sewer 5 2017 $10,000.00 10

501919 Molong Sewerage Telemetry - Thistle Street Pump Station - Sewer 5 2017 $10,000.00 10 Subtotal $115,214.52

501957 Canowindra Sewerage DIGESTOR PUPMP (REPLACEMENT) 6 2018 $16,544.26 10

501953 Canowindra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.06 10

501954 Canowindra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.06 10

- 35 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

501955 Canowindra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.06 10

501956 Canowindra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.06 10

501950 Canowindra Sewerage POLY PIPE CANOWINDRA SEWERAGE 6 2018 $3,261.73 10

501945 Eugowra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.06 10

501946 Eugowra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.07 10

501947 Eugowra Sewerage MODEM TO CONVERT TELEMETRY SYSTEM 6 2018 $1,333.07 10

501976 Molong Sewerage REPLACE SEWER MAIN CLEANING RODS 6 2018 $6.87 10

Subtotal $29,144.30

502080 Canowindra Sewerage REPLACE SEWER MAIN CLEANING RODS (120MTRS) 7 2019 $2,293.00 10 501975 Canowindra Sewerage REPLACMENT PRESSURE PUMP TREATMENT WORKS 7 2019 $11,669.00 10 501974 Canowindra Sewerage UPGRADE ALERT SYSTEM 7 2019 $776.50 10

501972 Eugowra Sewerage GRINDER PUMP NO. 2 PUMP STATION 7 2019 $4,775.00 10

502088 Eugowra Sewerage PUMP STATIONS (2) 7 2019 $237.10 10

502049 Eugowra Sewerage UPGRADE ALERT SYSTEM 7 2019 $6,106.07 10

501971 Eugowra Sewerage UPGRADE ALERT SYSTEM 7 2019 $119.00 10

502087 Molong Sewerage MAINS CLEANING MACHINE 7 2019 $64,945.06 10

501980 Molong Sewerage PHOTOMETER TEST EQUIP SEWER TREATMENT PLANT 7 2019 $1,729.64 10 501979 Molong Sewerage SOFT STARTER & BY PASS 7 2019 $1,952.72 10

502083 Molong Sewerage TELEMETRY SYSTEM 7 2019 $4,426.46 10

Subtotal $99,029.55

502182 Canowindra Sewerage CANOWINDRA - SEWER HYDROVAR CONTROLS 22KW

(PUMP & CONTROL UNIT) 8 2020 $9,128.82 10

502183 Canowindra Sewerage CANOWINDRA SEWER - CHAIN HOIST (1 TONNE CAGE CLEANING) NO. 1 PUMP

8 2020 $4,120.45 10

500025 Canowindra Sewerage Irrigation System Land Improve depreciable 8 2020 $674,719.49 20

500024 Canowindra Sewerage Irrigation System P & E 8 2020 $25,714.48 20

502078 Canowindra Sewerage TREATMENT PLANT INFLOW METER 8 2020 $5,752.72 10

500021 Canowindra Sewerage Treatment Works Land Improvements Depreciable 8 2020 $128,112.46 20

500018 Canowindra Sewerage Treatment Works P &E Structures 8 2020 $701,163.97 20

502079 Canowindra Sewerage UPGRADE ALERT SYSTEM 8 2020 $5,409.00 10

502188 Eugowra Sewerage EUGOWRA SEWER - UPGRADE ALERT SYSTEM 8 2020 $9,942.38 10

500060 Eugowra Sewerage Irrigation system - Land Improvement 8 2020 $19,725.78 20

500057 Eugowra Sewerage Land Improvements depreciable 8 2020 $143,779.83 20

500059 Eugowra Sewerage Treatment Wks Plant & Equipment 8 2020 $323,643.23 20

502179 Molong Sewerage CAMERA SEWERAGE FUNDS 8 2020 $6,699.00 10

502176 Molong Sewerage MOLONG SEWER - CLOSED CIRCUIT TV CAMERA HEAD 8 2020 $71,579.00 10 502178 Molong Sewerage MOLONG SEWER - ELECTRICAL CONVERSION FOR

GENERATOR 8 2020 $66,140.80 10

502181 Molong Sewerage MOLONG SEWER - STP EFFLUENT DISINFECTION 8 2020 $36,384.53 10 502175 Molong Sewerage MOLONG SEWER - TELEMETRY SYSTEM 8 2020 $1,248.36 10

502173 Molong Sewerage MOLONG SEWER - UPGRADE ALERT SYSTEM 8 2020 $5,722.48 10

502085 Molong Sewerage TREATMENT PLANT INFLOW METER 8 2020 $7,190.71 10

Subtotal $2,246,177.49

502186 Canowindra Sewerage CANOWINDRA SEWER - PUMP 9 2021 $15,557.06 10

502189 Eugowra Sewerage EUGOWRA SEWER - EFFLUENT DISINFECTION SYSTEM 9 2021 $4,638.40 10

502174 Eugowra Sewerage EUGOWRA SEWER - PUMP STATION NO 3 REPLACEMENT 9 2021 $7,364.33 10

- 36 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

502180 Molong Sewerage MOLONG SEWER - NUTRIENT REMOVAL TREATMENT UPGRADE

9 2021 $4,429.00 10

Subtotal $31,988.79

Program Total $2,724,279.76

- 37 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

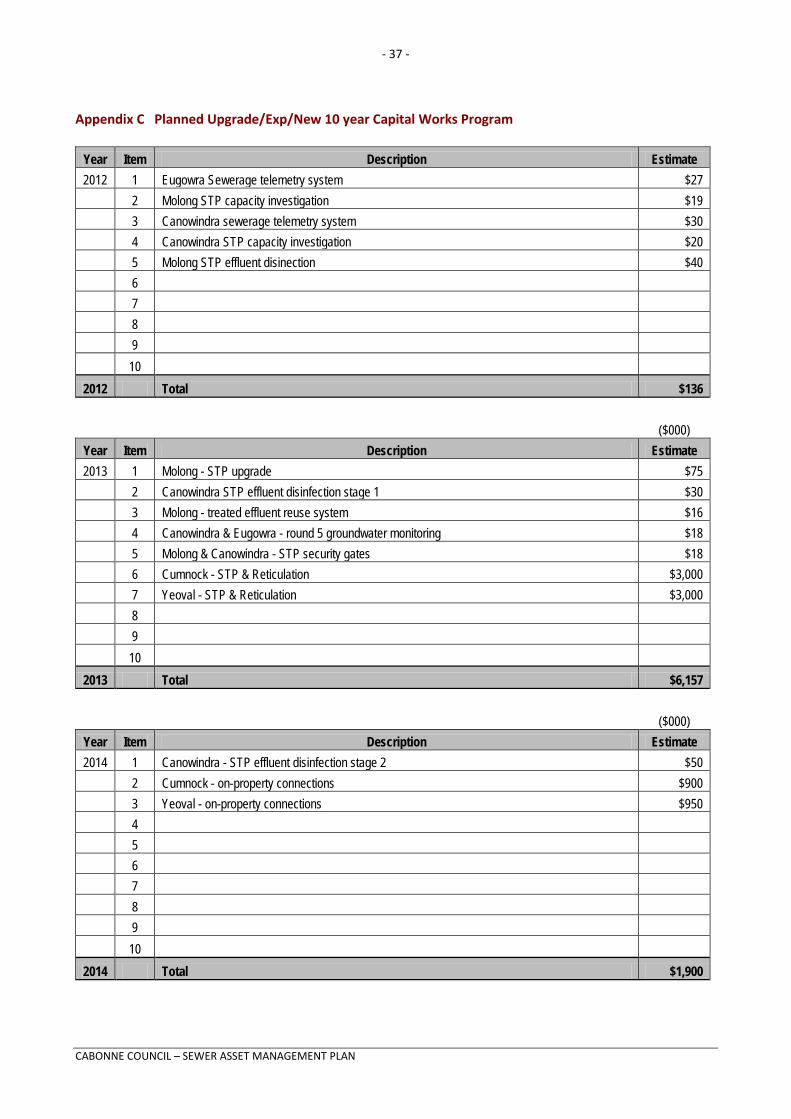

Appendix C Planned Upgrade/Exp/New 10 year Capital Works Program

Year Item Description Estimate 2012 1 Eugowra Sewerage telemetry system $27

2 Molong STP capacity investigation $19 3 Canowindra sewerage telemetry system $30 4 Canowindra STP capacity investigation $20 5 Molong STP effluent disinection $40 6 7 8 9 10

2012 Total $136

($000) Year Item Description Estimate 2013 1 Molong - STP upgrade $75

2 Canowindra STP effluent disinfection stage 1 $30 3 Molong - treated effluent reuse system $16 4 Canowindra & Eugowra - round 5 groundwater monitoring $18 5 Molong & Canowindra - STP security gates $18 6 Cumnock - STP & Reticulation $3,000 7 Yeoval - STP & Reticulation $3,000 8 9 10

2013 Total $6,157

($000) Year Item Description Estimate 2014 1 Canowindra - STP effluent disinfection stage 2 $50

2 Cumnock - on-property connections $900 3 Yeoval - on-property connections $950 4 5 6 7 8 9 10

2014 Total $1,900

- 38 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

($000)

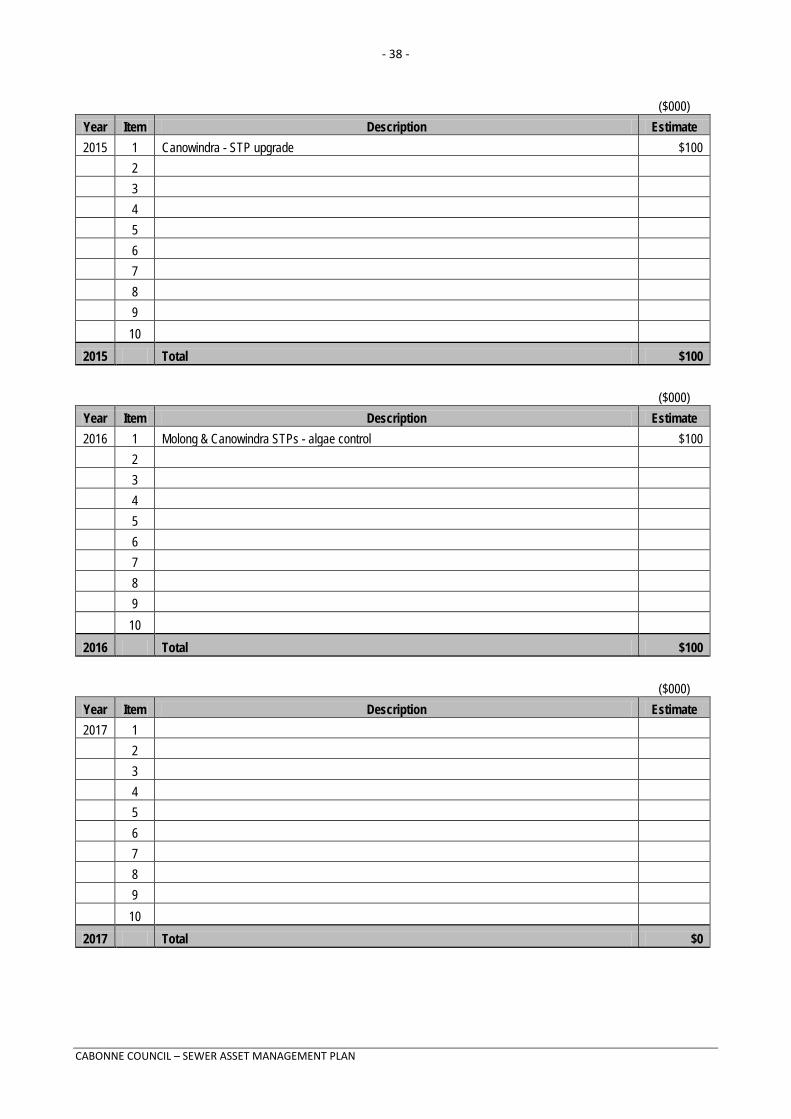

Year Item Description Estimate 2015 1 Canowindra - STP upgrade $100

2 3 4 5 6 7 8 9 10

2015 Total $100

($000) Year Item Description Estimate 2016 1 Molong & Canowindra STPs - algae control $100

2 3 4 5 6 7 8 9 10

2016 Total $100

($000) Year Item Description Estimate 2017 1

2 3 4 5 6 7 8 9 10

2017 Total $0

- 39 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

($000)

Year Item Description Estimate 2018 1 Telemetry upgrades $50

2 3 4 5 6 7 8 9 10

2018 Total $50

($000)

Year Item Description Estimate 2019 1

2 3 4 5 6 7 8 9 10

2019 Total $0

($000) Year Item Description Estimate 2020 1

2 3 4 5 6 7 8 9 10

2020 Total $0

- 40 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

($000)

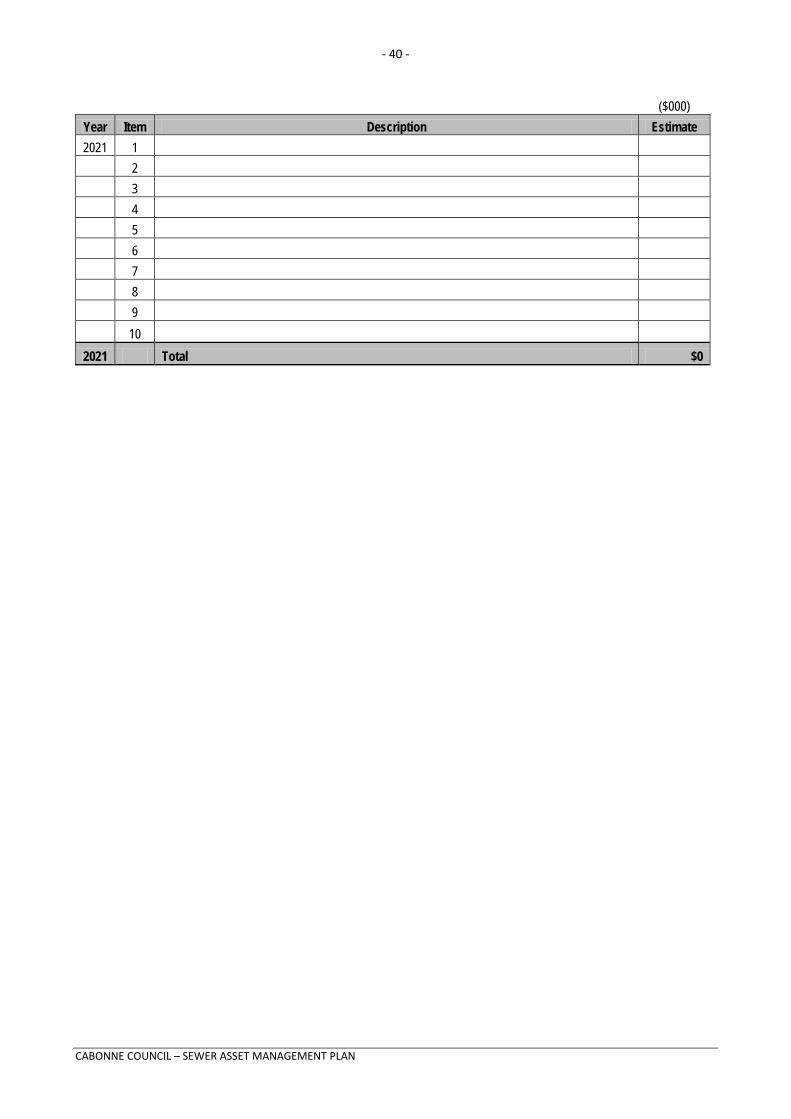

Year Item Description Estimate 2021 1

2 3 4 5 6 7 8 9 10

2021 Total $0

- 41 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

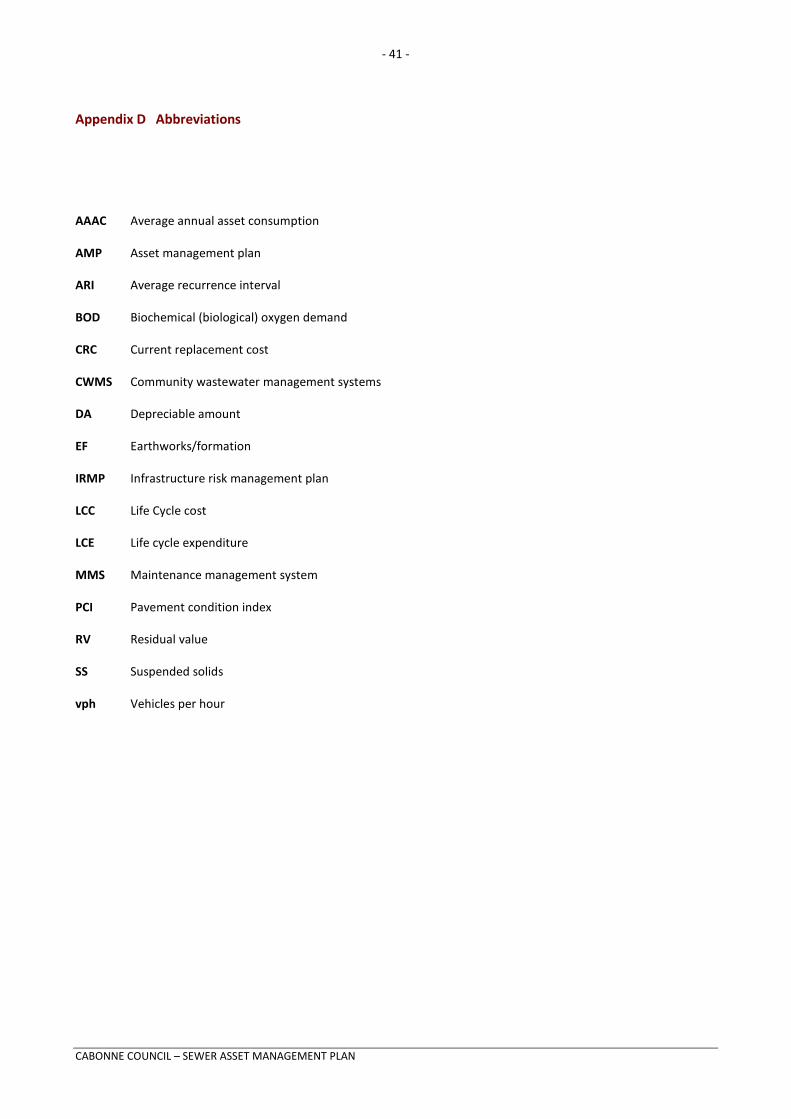

Appendix D Abbreviations

AAAC Average annual asset consumption

AMP Asset management plan

ARI Average recurrence interval

BOD Biochemical (biological) oxygen demand

CRC Current replacement cost

CWMS Community wastewater management systems

DA Depreciable amount

EF Earthworks/formation

IRMP Infrastructure risk management plan

LCC Life Cycle cost

LCE Life cycle expenditure

MMS Maintenance management system

PCI Pavement condition index

RV Residual value

SS Suspended solids

vph Vehicles per hour

- 42 -

CABONNE COUNCIL – SEWER ASSET MANAGEMENT PLAN

Appendix E Glossary Annual service cost (ASC) 1) Reporting actual cost The annual (accrual) cost of providing a service

including operations, maintenance, depreciation, finance/opportunity and disposal costs less revenue.

2) For investment analysis and budgeting An estimate of the cost that would be tendered,

per annum, if tenders were called for the supply of a service to a performance specification for a fixed term. The Annual Service Cost includes operations, maintenance, depreciation, finance/ opportunity and disposal costs, less revenue.

Asset A resource controlled by an entity as a result of past events and from which future economic benefits are expected to flow to the entity. Infrastructure assets are a sub-class of property, plant and equipment which are non-current assets with a life greater than 12 months and enable services to be provided.

Asset class A group of assets having a similar nature or function in the operations of an entity, and which, for purposes of disclosure, is shown as a single item without supplementary disclosure.

Asset condition assessment The process of continuous or periodic inspection, assessment, measurement and interpretation of the resultant data to indicate the condition of a specific asset so as to determine the need for some preventative or remedial action.

Asset management (AM) The combination of management, financial, economic, engineering and other practices applied to physical assets with the objective of providing the required level of service in the most cost effective manner.

Average annual asset consumption (AAAC)* The amount of an organisation’s asset base consumed during a reporting period (generally a year). This may be calculated by dividing the depreciable amount by the useful life (or total future economic benefits/service potential) and totalled for each and every asset OR by dividing the carrying amount (depreciated replacement cost) by the remaining useful life (or remaining future economic benefits/service potential) and totalled for each and every asset in an asset category or class.

Borrowings A borrowing or loan is a contractual obligation of the borrowing entity to deliver cash or another financial asset to the lending entity over a specified period of time or at a specified point in time, to cover both the initial capital provided and the cost of the interest incurred for providing this capital. A borrowing or loan provides the means for the borrowing entity to finance outlays (typically physical assets) when it has insufficient funds of its own to do so, and for the lending entity to make a financial return, normally in the form of interest revenue, on the funding provided.

Capital expenditure Relatively large (material) expenditure, which has benefits, expected to last for more than 12 months. Capital expenditure includes renewal, expansion and upgrade. Where capital projects involve a combination of renewal, expansion and/or upgrade expenditures, the total project cost needs to be allocated accordingly.

Capital expenditure - expansion Expenditure that extends the capacity of an existing asset to provide benefits, at the same standard as is currently enjoyed by existing beneficiaries, to a new group of users. It is discretionary expenditure, which increases future operations and maintenance costs, because it increases the organisation’s asset base, but may be associated with additional revenue from the new user group, eg. extending a drainage or road network, the provision of an oval or park in a new suburb for new residents.

Capital expenditure - new Expenditure which creates a new asset providing a new service/output that did not exist beforehand. As it increases service potential it may impact revenue and will increase future operations and maintenance expenditure.