Asset Management Lecture 10

Asset Management Lecture 10. Table 27.2 Make up a view and replace the one in spreadsheet 27.2. Recalculate the optimal asset allocation and portfolio.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Asset Management

Lecture 10

Table 27.2

Make up a view and replace the one in spreadsheet 27.2. Recalculate the optimal asset allocation and portfolio expected performance.

Table 27.2

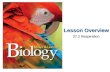

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

)()( MM RVarARE

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

),()()( , SBSBBMB RRCovwRVarwRRCov

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

%40.1%46.5018186.0

00466.0)(

)(

)()( , M

M

MBB RE

RVar

RRCovRE

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

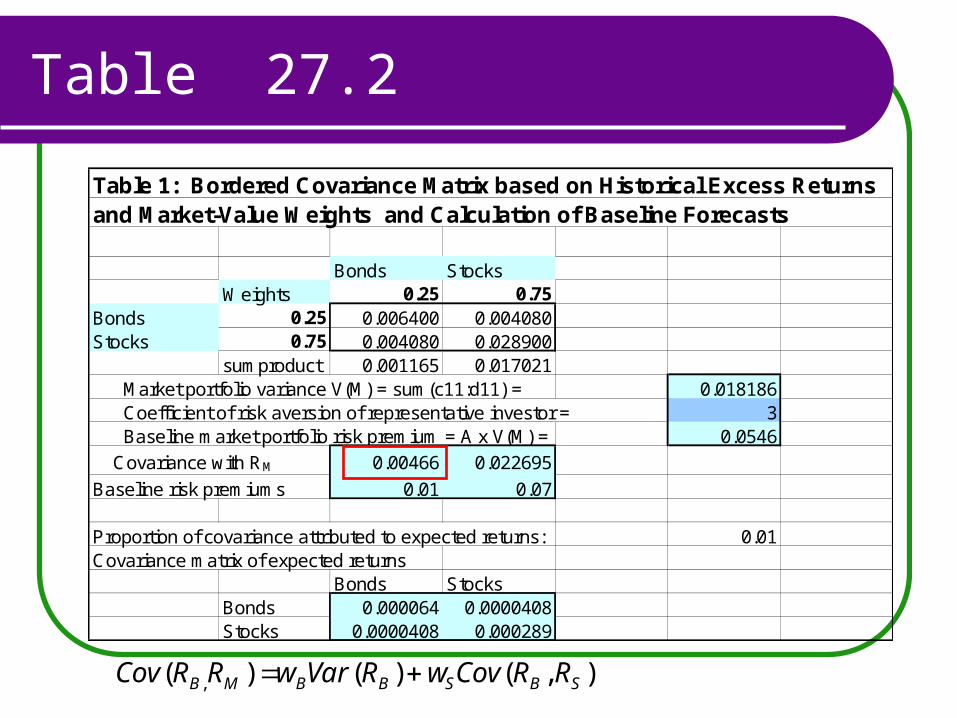

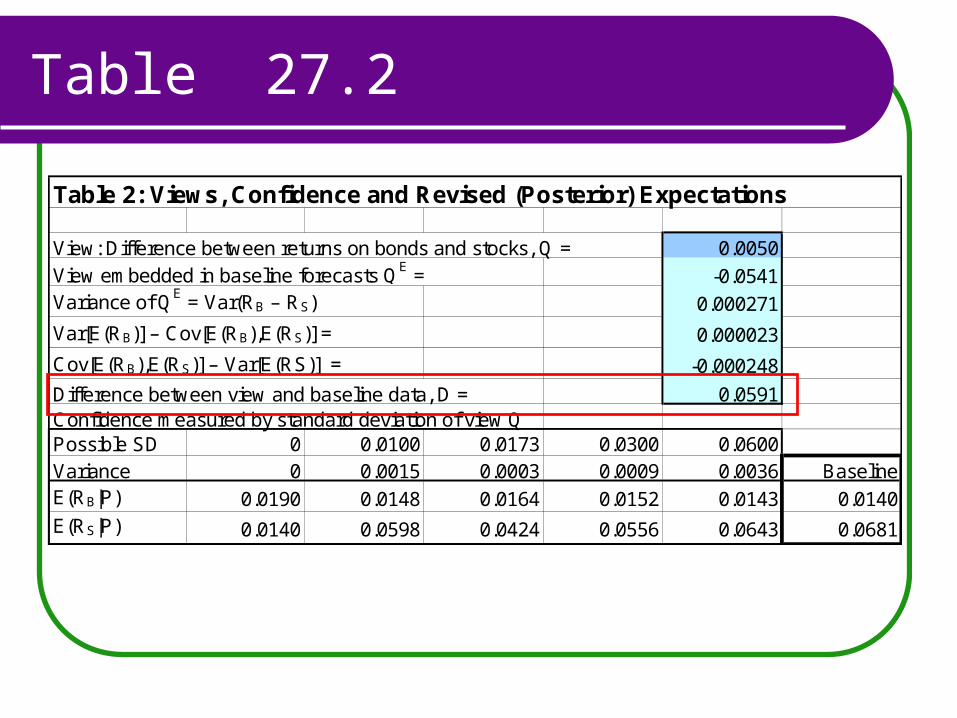

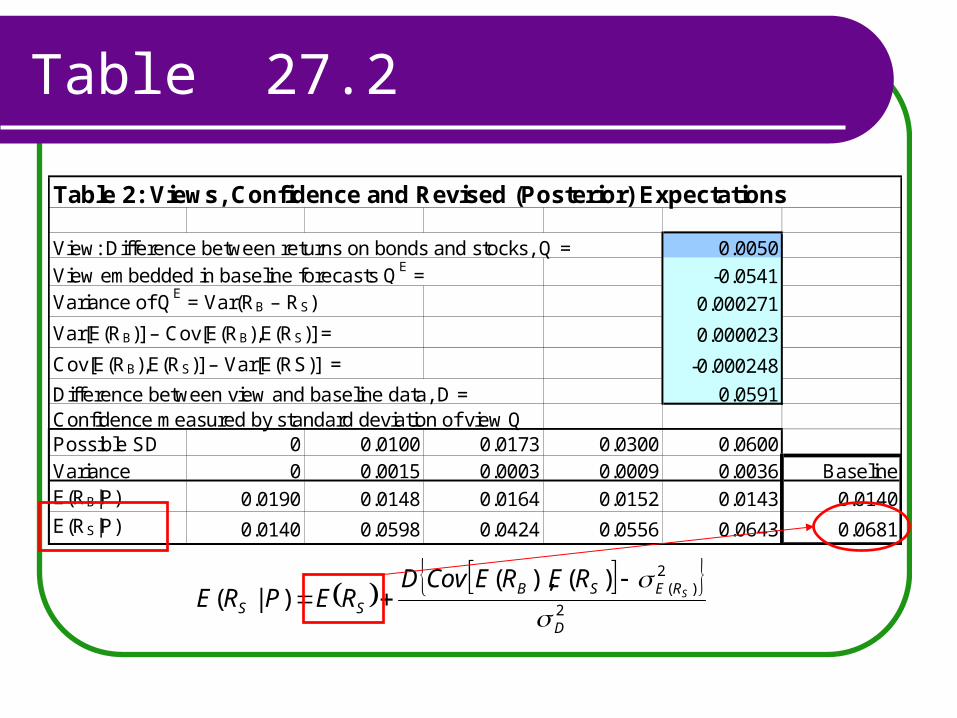

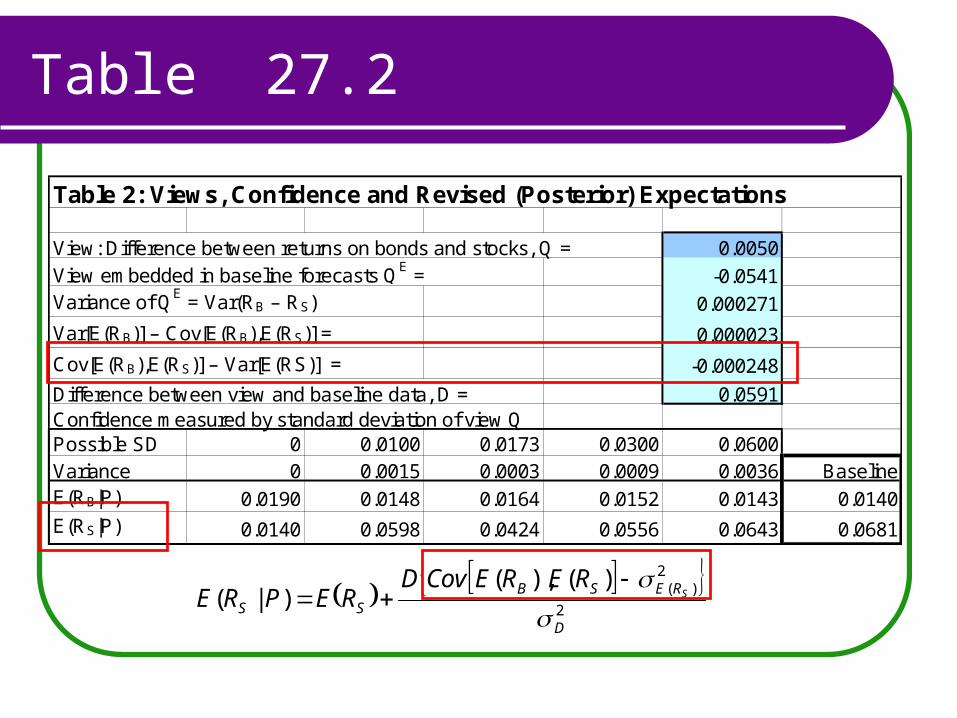

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

Table 27.2

%41.581.640.1'

%)81.6%,40.1())(),((

)1,1(

EE

SBE

PRQ

RERER

P

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

Table 27.2

))()(()(2SB

E REREVarQ ))(),((2)( 2

)(2

)(2

SBREREE RERECovQ

SB

0002714.00000408.02000289.0000064.0)(2 EQ

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

2

2)( )(),(

)|(D

SBREBB

RERECovDREPRE B

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

%40.1%46.5018186.0

00466.0)(

)(

)()( , M

M

MBB RE

RVar

RRCovRE

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

2

2)( )(),(

)|(D

SBREBB

RERECovDREPRE B

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

2

2)( )(),(

)|(D

SBREBB

RERECovDREPRE B

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

)()()( 222 EQD

Table 27.2

)()()( 222 EQD

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

)()()( 10 ttaaatu f

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

2

2)()(),(

)|(D

RESBSS

SRERECovD

REPRE

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

2

2)()(),(

)|(D

RESBSS

SRERECovD

REPRE

Table 27.2

Table 1: Bordered Covariance Matrix based on Historical Excess Returnsand Market-Value Weights and Calculation of Baseline Forecasts

Bonds StocksWeights 0.25 0.75

Bonds 0.25 0.006400 0.004080Stocks 0.75 0.004080 0.028900

sumproduct 0.001165 0.017021 Market portfolio variance V(M) = sum(c11:d11) = 0.018186 Coefficient of risk aversion of representative investor = 3 Baseline market portfolio risk premium = A x V(M) = 0.0546

Covariance with RM 0.00466 0.022695

Baseline risk premiums 0.01 0.07

Proportion of covariance attributed to expected returns: 0.01Covariance matrix of expected returns

Bonds StocksBonds 0.000064 0.0000408Stocks 0.0000408 0.000289

Table 27.2

Table 2: Views, Confidence and Revised (Posterior) Expectations

View: Difference between returns on bonds and stocks, Q = 0.0050View embedded in baseline forecasts QE = -0.0541Variance of QE = Var(RB – RS) 0.000271

Var[E(RB)] – Cov[E(RB),E(RS)] = 0.000023

Cov[E(RB),E(RS)] – Var[E(RS)] = -0.000248

Difference between view and baseline data, D = 0.0591Confidence measured by standard deviation of view QPossible SD 0 0.0100 0.0173 0.0300 0.0600Variance 0 0.0015 0.0003 0.0009 0.0036 BaselineE(RB|P) 0.0190 0.0148 0.0164 0.0152 0.0143 0.0140E(RS|P) 0.0140 0.0598 0.0424 0.0556 0.0643 0.0681

Exercise 27.4

Make up a view and replace the one in spreadsheet 27.2. Recalculate the optimal asset allocation and portfolio expected performance.

Exercise 27.3

Make up new alpha forecasts for your portfolio from Assignment One. Use Traynor Black model to find the optimal portfolio.

The assignment is due on April 14.

Related Documents