Asset allocation: optimising returns in a low return environment Glyn Owen October 2010 RMB Asset Management International Limited (Company Registration No. 3733094) is authorised and regulated by the Financial Services Authority and is a member of the FirstRand Group, and has its registered office at Twenty Gracechurch Street, London, EC3V 0BG

Asset allocation: optimising returns in a low return environment Glyn Owen October 2010 RMB Asset Management International Limited (Company Registration.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Asset allocation: optimising returns in a low return environment

Glyn OwenOctober 2010

RMB Asset Management International Limited (Company Registration No. 3733094) is authorised and regulated by the Financial Services Authority and is a member of the FirstRand Group, and has its registered office at Twenty Gracechurch Street, London, EC3V 0BG

Global imbalances

Source : Bloomberg, Old Mutual. September 2010.

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

US

D, 0

00's

billi

ons

Chinese reserves

The US twin deficit

If we go down they come with us

Source : Bloomberg. September 2010.

Chinese reserves

The US twin deficit

30

35

40

45

50

55

60

65

70

75

2004 2005 2006 2007 2008 2009 2010-2%

-1%

0%

1%

2%

3%

4%

5% ISM PMI (Manufacturing)

US Imports from China

But does superior GDP growth lead to market outperformance?

Source : Bloomberg, Old Mutual. September 2010.

0

20

40

60

80

100

120

Sep 07 Dec 07 Mar 08 Jun 08 Sep 08 Dec 08 Mar 09 Jun 09 Sep 09 Dec 09 Mar 10 Jun 10

Inde

x le

vel (

Reb

ased

)

SHANGHAI SE COMPOSITE NIKKEI 225

Still too much debt

Source : Bloomberg, BCA Research. September 2010.

100%

120%

140%

160%

180%

Non-federal debt as a % of GDP

30%

40%

50%

60%

70%

80%

Federal debt as a % of GDP

60%

80%

100%

120%

140%

Mar 80 Mar 82 Mar 84 Mar 86 Mar 88 Mar 90 Mar 92 Mar 94 Mar 96 Mar 98 Mar 00 Mar 02 Mar 04 Mar 06 Mar 08 Mar 10

Household debt as a % ofpersonal disposable income

6

It’s a two speed world……

Source: Bloomberg, Sarasin & Partners, IMF and WEO September 2010

…..but developed economies still dominant

Source: Bloomberg, September 2010

Share of global GDP

Global real money growth – pushing on a string

Source: Schroders. September 2010.

90

100

110

120

130

140

150

160

170

180

190

200

Dec95

Dec96

Dec97

Dec98

Dec99

Dec00

Dec01

Dec02

Dec03

Dec04

Dec05

Dec06

Dec07

Dec08

Dec09

Re

turn

(R

eb

ase

d)

EM Currency Index versus 50:50 USD:EUR Cash

Any bets on this reversing?

Source : Bloomberg, Investec Asset Management. September 2010.

EM currency index vs. 50:50 USD / EUR

10 year Government bond yields – US, UK, Germany

Source : Bloomberg. September 2010.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

30/0

6/20

00

30/1

2/20

00

30/0

6/20

01

30/1

2/20

01

30/0

6/20

02

30/1

2/20

02

30/0

6/20

03

30/1

2/20

03

30/0

6/20

04

30/1

2/20

04

30/0

6/20

05

30/1

2/20

05

30/0

6/20

06

30/1

2/20

06

30/0

6/20

07

30/1

2/20

07

30/0

6/20

08

30/1

2/20

08

30/0

6/20

09

30/1

2/20

09

30/0

6/20

10

UK US GERMANY

Market expectations of inflation are falling

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan 05 Jul 05 Jan 06 Jul 06 Jan 07 Jul 07 Jan 08 Jul 08 Jan 09 Jul 09 Jan 10 Jul 10

%

US Breakeven 5 Year

Source : Bloomberg. September 2010.

G7 implied forward rates ex. Japan

Source : Bloomberg. September 2010.

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

Se

p-0

0

Ma

r-0

1

Se

p-0

1

Ma

r-0

2

Se

p-0

2

Ma

r-0

3

Se

p-0

3

Ma

r-0

4

Se

p-0

4

Ma

r-0

5

Se

p-0

5

Ma

r-0

6

Se

p-0

6

Ma

r-0

7

Se

p-0

7

Ma

r-0

8

Se

p-0

8

Ma

r-0

9

Se

p-0

9

Ma

r-1

0

%

G7 ex. Japan Forward Rates

Market Implied Official Rates in 5 Years Time

Market Implied 5 Year Yields in 5 Years Time

US existing home sales

Source: Bloomberg, September 201013

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Dec00

Dec01

Dec02

Dec03

Dec04

Dec05

Dec06

Dec07

Dec08

Dec09

US Existing Homes Sales SAAR

US unemployment

Source : Bloomberg. September 2010.

Unemployment in the US

0

1

2

3

4

5

6

7

8

9

10

Feb-07 Aug-07 Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10

Ra

te (

%)

Industrial production

Source: Bloomberg. September 2010.

-50

-40

-30

-20

-10

0

10

20

30

40

Jan 90 Jan 92 Jan 94 Jan 96 Jan 98 Jan 00 Jan 02 Jan 04 Jan 06 Jan 08 Jan 10

Le

ve

l

US Industrial Production UK Industrial Production

Germany Industrial Production Japan Industrial Production

10 year Government bond yields – PIGS

Source : Bloomberg. September 2010.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Jun04

Dec04

Jun05

Dec05

Jun06

Dec06

Jun07

Dec07

Jun08

Dec08

Jun09

Dec09

Jun10

PORTUGAL IRELAND GREECE SPAIN

Liquidity conditions have stabilized

Source : Bloomberg. September 2010.

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan 07 Jul 07 Jan 08 Jul 08 Jan 09 Jul 09 Jan 10 Jul 10

US LIBOR - OIS Spread Euro LIBOR - OIS Spread UK LIBOR - OIS Spread

Credit spreads

Source: Bloomberg. September 2010.

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

Jan 94 Jan 95 Jan 96 Jan 97 Jan 98 Jan 99 Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10

US

Inve

stm

ent

Gra

de

Sp

read

s

0.00

300.00

600.00

900.00

1200.00

1500.00

1800.00

2100.00

US

Hig

h Y

ield

Sp

read

s

US Investment Grade Spreads US High Yield Spreads

Corporate sector in excellent shape

Corporates are sitting on a mountain of cash

Source: RMB Asset Management, BCA. September 2010

M&A activity

Consumer confidence Germany

Source: Bloomberg. September 2010.

German business confidence also strong

-150

-100

-50

0

50

100

Aug00

Aug01

Aug02

Aug03

Aug04

Aug05

Aug06

Aug07

Aug08

Aug09

Aug10

Lev

el (

Ger

man

y Z

WE

)

Source: Bloomberg. September 2010.

Fiscal consolidation

Source: IMF, Economist, Eurostat. September 2010.

0.8

1.3 1.3 1.3

1.5

1.9

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Spain'96-03

Italy '91-97

UK '94-00

Germany'05-07

US '94-98

Canada'93-97

Sweden'94-98

1.5 1.6

1.8

2.0

2.22.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Portgual'11-14

UK '11-14US '11-13Spain '11-13

Greece'10-14

Ireland'10-14

Historical fiscal rebalancing Projected fiscal rebalancing

Historical precedent suggests economies can shrug off some fiscal rebalancing… but there is a limit

Ireland, Greece and likely Spain will be significantly impacted by fiscal cuts

With 2012 election looming US likely to push spending cuts back

Source : Bloomberg. September 2010.

Equity valuations provide strong support

Equities…… the income asset class?

Source : Bloomberg. September 2010.

Dividend Yld (%)

10 Year Gov Bond Yld (%)

Investment Grade Corp

Bond Yld (%)

Dow Jones Industrial Average 2.60 2.54 3.68

S&P 500 1.97 2.54 3.68

FTSE All-Share 3.19 2.99 5.05

FTSE 100 3.30 2.99 5.05

Euro Stoxx 50 4.03 2.32 3.26

Nikkei 225 1.75 0.96 0.66

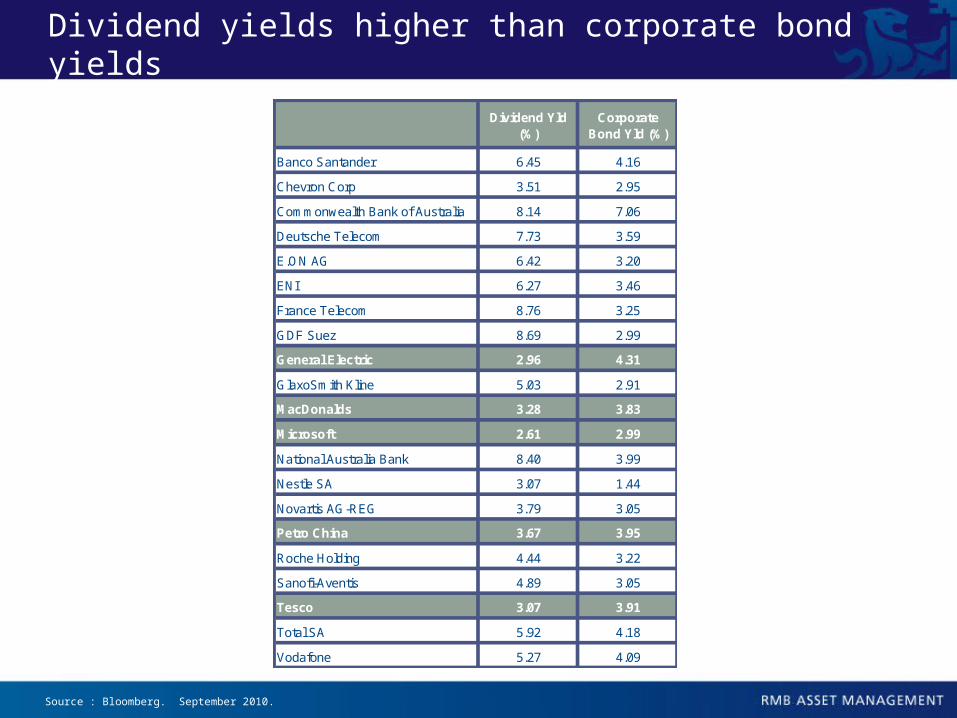

Dividend yields higher than corporate bond yields

Source : Bloomberg. September 2010.

Dividend Yld (%)

Corporate Bond Yld (%)

Banco Santander 6.45 4.16

Chevron Corp 3.51 2.95

Commonwealth Bank of Australia 8.14 7.06

Deutsche Telecom 7.73 3.59

E.ON AG 6.42 3.20

ENI 6.27 3.46

France Telecom 8.76 3.25

GDF Suez 8.69 2.99

General Electric 2.96 4.31

GlaxoSmith Kline 5.03 2.91

MacDonalds 3.28 3.83

Microsoft 2.61 2.99

National Australia Bank 8.40 3.99

Nestle SA 3.07 1.44

Novartis AG-REG 3.79 3.05

Petro China 3.67 3.95

Roche Holding 4.44 3.22

Sanofi-Aventis 4.89 3.05

Tesco 3.07 3.91

Total SA 5.92 4.18

Vodafone 5.27 4.09

Where is investor money flowing…….?

Source : EPFR Global. September 2010.

+USD560 billion

Emerging bubble?

Source : EPFR Global. September 2010.

0

20

40

60

80

100

120

140

160

Jun08

Aug08

Oct08

Dec08

Feb09

Apr09

Jun09

Aug09

Oct09

Dec09

Feb10

Apr10

Jun10

Aug10

Inde

x le

vel (

Reb

ased

)

GOLD SPOT $/OZ JPY-USD X-RATE

Gold: not the only game in town?

Source : Bloomberg. September 2010.

Gold 4.4%

Yen 2.6%

Volatility

Inflation protection: gold vs. TIPS

Source : Bloomberg. September 2010.

80

85

90

95

100

105

110

115

Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10 Jul 10 Aug 10

Inde

x le

vel (

Reb

ased

)

GOLD SPOT $/OZ TSY INFL IX N/B

Gold 3.1%

TIPS 2.0%

Volatility

INFL LINKED BONDS

31

But gold could run further……

Source: Ned Davis September 2010

(COD201007061A_C)

105 115 126 137 150 164 179 195 213 233 254 277 303 330 360 393 429 469 512 558 609 665 726 792 865 943

1030112412261338146015941739189820712260

105 115 126 137 150 164 179 195 213 233 254 277 303 330 360 393 429 469 512 558 609 665 726 792 865 943

1030112412261338146015941739189820712260( ) 1970 Gold Bullion (1/16/1970 - 11/11/1981)

( ) 2001 Gold Bullion (2/15/2001 - 7/02/2010) (Lines indexed to 100 at start.)

Concept Courtesy of Boeckh Investment Letter

M J S D

2002

M J S D

2003

M J S D

2004

M J S D

2005

M J S D

2006

M J S D

2007

M J S D

2008

M J S D

2009

M J S D

2010

M J S D

2011

M J S D

2012

M J S D

M J S D

1971

M J S D

1972

M J S D

1973

M J S D

1974

M J S D

1975

M J S D

1976

M J S D

1977

M J S D

1978

M J S D

1979

M J S D

1980

M J S D

1981

M J S

Gold Bullion Cycles - 1970 vs. 2001

1970 Gold Cycle

( )

2001 Gold Cycle

( )

Daily Data (Log Scale)

Copyright 2010 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. . www.ndr.com/vendorinfo/ . For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

Asset allocation policy

Liquidity underpins asset values

But uncertainty and tail risks are exceptionally high

Therefore diversify across asset classes and avoid extreme positions

Government bonds are expensive – but offer ultimate deflation hedge

High yield credit still reasonable value

Equities on attractive valuations

Bias towards defensiveness within equities

Cash rates close to zero for extended period

Emerging markets offer superior growth but beware of valuations

Still too early for inflation hedges

33

RMB Asset Management is the trading name for RMB Asset Management International Limited. This document does not constitute an offer or solicitation to any person in any jurisdiction in which it is not authorised or permitted, or to anyone who would be an unlawful recipient, and is only intended for use by original recipients and addressees. The original recipient is solely responsible for any actions in further distributing this document, and should be satisfied in doing so that there is no breach of local legislation or regulation. The information is intended solely for use by our clients or prospective clients, and should not be reproduced or distributed except via original recipients acting as professional intermediaries. This document is not for distribution in the United States.Prospective investors should inform themselves and if need be take appropriate advice regarding applicable legal, taxation and exchange control regulations in countries of their citizenship, residence or domicile which may be relevant to the acquisition, holding, transfer, redemption or disposal of any investments herein solicited.Any opinions expressed herein are those at the date this material is issued. Data, models and other statistics are sourced from our own records, unless otherwise stated herein. We believe that the information contained is from reliable sources, but we do not guarantee the relevance, accuracy or completeness thereof. Unless provided under UK law, RMB Asset Management does not accept liability for irrelevant, inaccurate or incomplete information contained, or for the correctness of opinions expressed. We caution that the value of investments in discretionary accounts, and the income derived, may fluctuate and it is possible that an investor may incur losses, including a loss of the principal invested. Past performance is not generally indicative of future performance. Investors whose reference currency differs from that in which the underlying assets are invested may be subject to exchange rate movements that alter the value of their investments.

Important notes

34

Our investment mandates in alternative strategies and hedge funds permit us to invest in unregulated funds that may be highly volatile. Although alternative strategies funds will seek to follow a wide diversification policy, these funds may be subject to sudden and/or large falls in value. The illiquid nature of the underlying funds is such that alternative strategies funds deal infrequently and require longer notice periods for redemptions. These Investments are therefore not readily realisable. If an alternative strategies fund fails to perform, it may not be possible to realise the investment without further loss in value. These unregulated funds may engage in the short selling of securities or may use a greater degree of gearing than is permitted for regulated funds (including the ability to borrow for a leverage strategy). A relatively small price movement may result in a disproportionately large movement in the investment value. The purpose of gearing is to achieve higher returns associated with larger investment exposures, but has concomitant exposure to loss if positive performance is not achieved. Reliable information about the value of an investment in an alternative strategies fund may not be available (other than at the fund’s infrequent valuation points). Under our multi-management arrangements, we selectively appoint underlying sub-investment managers and funds to actively manage underlying asset holdings in the pursuit of achieving mandated performance objectives. Annual investment management fees are payable both to the multimanager and the manager of the underlying assets at rates contained in the offering documents of the relevant portfolios (and may involve performance fees where expressly indicated therein). RMB Asset Management International Limited (Company Registration No. 3733094) is authorised and regulated by the Financial Services Authority and is a member of the FirstRand Group, and has its registered office at 20 Gracechurch Street, London EC3V 0BG. © RMB Asset Management International Limited 2010

Important notes

Related Documents