Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015 ISSN: 2320-5504, E-ISSN-2347-4793 www.apjor.com Page 101 ASSESSING THE RELATIONSHIP BETWEEN INVESTMENT CLIMATE AND DOMESTIC SAVINGS IN INDIA Dr. Manjari Agarwal Assistant Professor School of Management Studies and Commerce Uttarakhand Open University, Haldwani, Uttarakhand ABSTRACT Growth in an economy depends upon the savings and investments along with capital-output ratio which determines level of income. Savings reflects long term economic viability of a country and investment climate reflects the health of a nation's business environment in totality. Further, there are broad and interrelated factors that affect the buoyancy of savings and investments in the country. These can be macro factors at the economy level concerning economy and political stability and the level of policies adopted towards investments. Hence, the present study assesses the relationship between savings and investment climate. It tries to assess that how the savings of the Country is important for shaping the investment climate in the country. It tries to explore the impact of Gross Domestic Savings on the investment climate of the country. The study used Correlation and Johansen Co-integration Method for identifying relationship and on the basis of correlation and co-integration analysis, it was found that savings in the country is an important factor that have significant impact on the investment climate. This means that Gross Domestic Savings should be accelerated in the economy for developing healthy investment climate in the country. Key Words: Investment Climate, Investments, Savings, Granger Causality 1. Introduction Investment is the sacrifice of certain present value for the uncertain future profits. It includes deciding on various aspects like type, amount timing, grade etc. of investments. Broadly speaking an investment decision is a trade-off between risk and return. Accordingly, investment means the engagements of funds with an objective of realizing additional income or growth in investment value at a future date. Investment has been an activity attributable to the rich and business class in the past, but today we find that investment is a word commonly used in households and is quite familiar with people at each cadre. It is an activity by which resources are actually committed to

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 101

ASSESSING THE RELATIONSHIP BETWEEN INVESTMENT CLIMATE AND

DOMESTIC SAVINGS IN INDIA

Dr. Manjari Agarwal

Assistant Professor

School of Management Studies and Commerce

Uttarakhand Open University, Haldwani, Uttarakhand

ABSTRACT

Growth in an economy depends upon the savings and investments along with capital-output ratio which

determines level of income. Savings reflects long term economic viability of a country and investment climate

reflects the health of a nation's business environment in totality. Further, there are broad and interrelated factors

that affect the buoyancy of savings and investments in the country. These can be macro factors at the economy

level concerning economy and political stability and the level of policies adopted towards investments. Hence, the

present study assesses the relationship between savings and investment climate. It tries to assess that how the

savings of the Country is important for shaping the investment climate in the country. It tries to explore the impact

of Gross Domestic Savings on the investment climate of the country.

The study used Correlation and Johansen Co-integration Method for identifying relationship and on the basis of

correlation and co-integration analysis, it was found that savings in the country is an important factor that have

significant impact on the investment climate. This means that Gross Domestic Savings should be accelerated in the

economy for developing healthy investment climate in the country.

Key Words: Investment Climate, Investments, Savings, Granger Causality

1. Introduction

Investment is the sacrifice of certain present value for the uncertain future profits. It includes deciding on various

aspects like type, amount timing, grade etc. of investments. Broadly speaking an investment decision is a trade-off

between risk and return. Accordingly, investment means the engagements of funds with an objective of realizing

additional income or growth in investment value at a future date. Investment has been an activity attributable to the

rich and business class in the past, but today we find that investment is a word commonly used in households and

is quite familiar with people at each cadre. It is an activity by which resources are actually committed to

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 102

production. Investments generally promote larger consumption in future as they lead to more income and larger

capital appreciation. Moreover, Government policies, technology, state of industry and stock of capital also

influence expected future earnings. Further, the amount of investments depends upon surplus funds generated by

individuals and organizations, which in turn get, invested in various investment options. Therefore, investment is

lifeblood of an economy, which flows in all sectors and without which a country is difficult to prosper.

However, on the other hand, savings are the excess of income over expenditure for any economic unit. Saving is

abstaining from present consumption for a future use. Saving refers to the activity by which claims to resources,

which might be put to current consumption, are set aside and are made available for other purpose in future. The

total volume of savings in an economy therefore depends mainly upon the size of its material income and its

average propensity to consume, which in turn, is broadly determined by the level and distribution of the income of

the people. Further, savings in an economy is composed of public and private savings. Public saving comprises of

the saving of the Government through budgetary channels and retained earnings of public enterprises. They are

greatly influenced by economic and fiscal policies, tax rates and investment policies. Private saving includes

household sector savings and business savings. Business saving is also in the form of retained savings, surplus,

provisions etc. They are also called as corporate savings and are greatly influenced by the state of economy and

industry, the fiscal policies etc.

Additionally, finance is a link between savings and investment by which saving are consolidated and put into the

hands of those who are able and willing to invest. It is an activity by which claims are assembled from the savings

either from domestic avenues or from abroad and then placed in the hands of the investors. Therefore, financial

system is significant for capital formation and this capital formation is yet again necessary for the development of

an economy. Thus, the function of financial system is to establish a bridge between savers and investors and

thereby help in removing gaps in the investment process. Hence, the financial system has an important role to play

in the mobilization of savings and their distribution among the various productive activities.

Accordingly, growth in an economy depends upon the savings and investments along with capital-output ratio

which determines level of income. Further, by investing in physical assets capital formation rises, which in turn

returns into increase in output. Thus, the total capital -output ratio for the economy, speaking in macro terms and

the total volume of investments in the economy would determine the growth of output and income.

Particularly in India, the net savers are the household sector whose savings are higher than their investment,

leading to their positive contribution of saving in the economy. On the other hand, business and Government

sectors are negative savers as investments are higher than the savings leading to a net negative contribution. The

foreign sector also contributes to net savings due to larger inflow of funds through commercial borrowings and

other forms of capital inflows. The flow of funds in the form of saving and investment comes from the financial

system and promote production of goods and service in the real sector, leading to increase in output and incomes

of the people. Thus, overall, the importance of financial system is to increase savings and investment in the

economy and to increase these resources flowing into financial assets, which are more productive than physical

assets.

Accordingly, the flow of funds promotes production of goods and service in the real sector, leading to a rise in

output and income of the people. But sometimes it is also said that increase in capital without suitable social,

economic, political conditions cannot cause growth. On the other hand favorable development in the conditions

can achieve much greater growth with minimum of capital. Thus, there are broad and interrelated factors that

affect the buoyancy of savings and investments in the country. These can be macro factors at the economy level

concerning economy and political stability and the level of policies adopted towards investments. Further, these

can be macro economic factors such as fiscal, monetary, exchange rate policies and political stability which affect

growth in investments. There can be other factors like governance and regulatory framework both in the financial

and legal systems and it may also include factors like infrastructural facilities such as transportation, electricity and

communication that are necessary for productive investment in the country. These factors in totality may lead into

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 103

determining investment climate of a country. Thus, the investment climate presents the reasoned expectations

about the competitiveness, growth, prosperity and profitability. As per the definition given by the World Bank in

the World Development Report, 2005 as “The investment climate reflects the many location-specific factors that

shape the opportunities and incentives for firms to invest productively, create jobs, and expand.” Phillips (2006)

divided investment climate into governance and infrastructure components while stating that healthy investment

climate includes economic and political stability, rule of law, adequate infrastructure, tax and regulations

conducive to doing business, labor policies, and access to finance. Stern (2002) notes that it is the “The policy,

institutional, and behavioral environment, both present and expected, that influences the returns and risks

associated with investment. The notion of investment climate focuses on questions of institutions, governance,

policies, stability, and infrastructure that affect not just the level of capital investment but also the productivity of

existing investments indeed, of all factors of production and the willingness to make productive investments for

the longer term.” This conveys that besides the various macroeconomic variables that may affects investment

climate in the county, even savings also plays a predominant role in explaining the investment climate in the

Country.

Further, before 1991 i.e. before liberalization, investment in the prime areas of the economy was under the hands

of public sector, private investments were discouraged. The Government owned and controlled almost all banking

system and prevented foreign and domestic institutions from entering it. The insurance and pension fund industry

was Government owned and had to invest most of its assets in low yielding Government securities. The

Government set nearly all interest rates and financial institutions were directed on how they should allocate some

of their investments. Capital Markets were constrained by few companies and corporate houses. Private companies

in capital markets were small and needed Government approval (including Government determination of price and

terms) on new capital issues. But after the reforms of 1991, there has been a substantial and steady liberalisation of

the economy, which impedes the importance of market forces. Permission is granted for the foreign investment to

enter into debt and equity market. Mutual funds territory is opened for private sector. Government control of the

prices of initial public offering has ended. Finally, better regulation, disclosures and investor protection have

greatly changed the savings and investment patterns of the individuals in the country.

Thus on the basis of the above background the present study assesses the relationship between savings and

investment climate. It tries to assess that how the savings of the Country is important for shaping the investment

climate in the country. It tries to explore the impact of Gross Domestic Savings on the investment climate of the

country. For the purpose of the study, operationally Investment climate is explained as Trade, investments,

industrial and manufacturing conditions in an economy that influences national and international individuals and

institutions for investing money and acquiring stake.

Savings reflects long term economic viability of a country and investment climate reflects the health of a nation's

business environment in totality.

2. Review of Literature The relationship between savings and the investment has been incessant study not only in developing countries but

also in developed countries across the globe. Emmanuel Anorou in the year 2001 conducted a study to explore

relationship between savings and investments in context to ASEAN Countries. The study found long run

equilibrium association between the savings and investments. The study was conducted using Johansen Juselius

Co-integration method, Granger Causality Test and VECM. The study explored that investment causes saving in

the cases of Indonesia and Singapore. For the Philippines, causality runs from saving to investment. However, in

case of Malaysia and Thailand, the study resulted into bi-directional causality between saving and investment.

Jangili Ramesh in the year 2011 investigated the relationship between savings, investments and economic growth

for India. The study found unidirectional causality between savings and investments. It was that higher savings and

investments contribute into higher economic growth. It was also found that saving and investment led growth has

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 104

been contributed by the household sector. The study also found that savings and investments of private sector

endogenously contributed in the growth of economic growth. Further the study also found that economic growth is

possible due to investments in public sector but the economic growth does not contribute in the increase of public

sector investments.

On an different dimension, Bahmani-Oskooee and Chakrabarti (2005) found that there was a significant and

positive relationship between the ratio of Gross Domestic Investments to GDP and the ratio of Gross Domestic

Savings to GDP. They found that a systematic effect of „„country-size‟‟ and „„openness‟‟ on the saving–investment

relationship was robust for Higher- Income Countries. The study was conducted on 126 economies over the period

of 1960 to 2000. The study was concentrated on the exploring the saving-investments relationship for the Higher-

Income, Low Income and Closed economies.

Narayan Paresh Kumar (2005) found that savings and investments are co-integrated for Japan. Further he explored

that bidirectional causality exists between savings and investments. The direction of causation between saving and

investment was explored using the bootstrap approach. Though moderate rate of correlation between the variables.

Further, the study found that shocks to saving and investment have a permanent effect in case of Japan.

Ramesh Mohan (2006) investigated the relationship between the domestic savings and economic growth for

various economies. The study seeks to determine whether the direction of causality in these economies is different

based on their income class: namely low−income, low−middle income, upper−middle income, and high−income

countries. Granger causality tests conducted by the researcher revealed that economic growth rate Granger causes

growth rate of savings in 13 countries.

Komain Jiranyakul and Tantatape Brahmasrene (2008) tested the relationship between savings and investments in

Indonesia, Philippines and Thailand. The study also applied Bound Testing Procedure for co-integration, the

results does not found positive correlation between savings and investments in the Indonesia, Philippines and

Thailand.

Kaya Huseyin (2010) found the relationship between domestic saving –investment relationship in Turkey. The

researcher applied ARDL Bound testing Procedure and Bai and Perron Procedure for founding structural breaks.

The study found strong long-run relationship between total investments and savings. However, the study didn‟t

found any long run relationship between private savings and investments. The study was conducted over the

period to 1984Q1-2007Q3.

Francesca and Fachin (2011) investigated long-run savings-investments relationship in OECD economies over the

period 1970 to 2007. The study concluded that the there is long run savings investments in 18 OECD economies

over the period 1970-2007. The study was undertaken by using new bootstrap test for panel co integration in terms

of short-run and long-run dependence across units.

Nwogwugwu, & Odulukwe (2012) explored the factors that affects the investments in Nigeria. The study used

Johansen and Juselius Method to find co-integration among the variables. They found that long run relationship

exists among the variables. The study found that market size and incremental capital ratios are key drivers of

investments in case of Nigeria. The paper suggested that Nigeria have to improve it Investment Climate and

infrastructure to attract investments in the Country.

Christopher K.U (2013) examined that how Nigerian investment climate can be improved for fostering economic

growth in the Country. The study explored that decline in investment rates is one of the factor for the reduced

economic performance. Accordingly, the study recommended that Nigerian economy should foster investments by

providing favorable fiscal regime and by providing stable macroeconomic framework.

Ogbokor and Musilika (2014) found that there is a unidirectional causality between savings and investments in

Namibia . The study found one way causality between the variables and it was inferred that Savings causes into

Investments in Namibia but not vice versa. The study suggested that there is no co-integration between savings and

investments in the Country. Thus, no long-run equilibrium relationship was derived between Savings and

Investments.

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 105

On exploring in the dimension of FDI, Dollar et. al (2005) analysed the importance of investment climate on

exports and FDI for Latin American and Asian Countries using firm level data. The study concluded that better

investment climate in general encourages FDI. All explanatory variables were considered for the study including

physical and financial infrastructure without giving specific effect of a particular variable.

Similar results were found by Kinda Tidiane (2010) investigated the constraints posed by investment climate in

restricting FDI in seventy seven developing Countries using firm level data. The study suggested that physical and

financial infrastructure magnifies the possibility of attracting FDI.

Thus, from the review of literature, it was found that many studies have been conducted on exploring the

relationship between savings and investments. Further, studies have also been undertaken for finding the

relationship of investment climate on exports and FDI. However, any study of exploring the specific relationship

between savings and investment climate has not yet been traced in context to India. In light of this, the study tried

to fill this gap in some ways by attempting to investigate the relationship between savings and investment climate

in India using relevant econometric techniques.

3. Objectives of the Study

The objective of the study is to find out the correlation and co integration between relationship between savings

and investment climate in India during the period from 1980 to 2013.

4. Hypotheses of the Study

H1: There is a positive correlation between savings and investment climate in India.

H2: The variables savings and investment climate in India are co-integrated.

5. Research Methodology

The present study is based on secondary data on Gross Domestic Savings and Investment climate (proxies) which

have been taken from the database of the World Bank (World Development Indicators). Annual data has been used

in the study over the period of 1980 to 2013. The stated period witnessed significant economic and financial

reforms and hence this period would be able to comprehend about the relationship between the variables.

5.1 Variables of the Study

5.1.1 Gross Domestic Savings: This variable represents the Gross Domestic Product minus final consumption

expenditure/ total consumption in India in a particular year. The data is depicted as current U.S. dollars. This

variable is considered as a proxy of the savings of a country.

Variables for Investigating Investment Climate

As per the literature reviewed various factors has been taken for explaining the investment climate in the country

like macro stability, investments, access to finance, tax regulations, trade regulations, infrastructure, production

capacity, corruption, political stability and the likes. However, for this study the following variables have been

taken to reflect investment climate in the country.

5.1.2 Investments: Investments refers to the total investments in the country. This ratio between the investments

and GDP portrays economic health [in terms of gross capital formation]. As per World Bank, it is measured by the

total value of the gross fixed capital formation and changes in inventories and acquisitions less disposals of

valuables for a unit or sector. Thus, this variable is taken majorily for assessing Investment Climate in India.

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 106

5.1.3 Trade Openness: This variable Trade is the proxy for Trade Openness. It depicts the sum of exports and

imports of goods and services measured as a share of gross domestic product.

5.1.4 Industrial Climate/Contribution: This is variable for depicting the industrial climate of an economy which

in turns affects Investment Climate in the Country. This is an economic indicator that measures changes in output

for the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities. Data is

in constant US$, and not seasonally adjusted. The base year is 2005.

5.1.5 Value Addition by Manufacturing Sector: It is the proxy for manufacturing contribution in the overall

investment climate of the country. Thus, it depicts the total valued added by the Manufacturing units in

intensifying Investment Climate of India. As per the World Bank, Value added is the net output of a sector after

adding up all outputs and subtracting intermediate inputs. It is calculated without making deductions for

depreciation of fabricated assets or depletion and degradation of natural resources. The data is depicted as current

U.S. dollars.

5.2 Method used

5.2.1 Correlation

The correlation assess the relationship between two variables and for studying the same various methods and tools

are used. This statistical tool is widely used for inferring the relationship between the variables of the study. Two

variables are termed to be correlated when increment or decrement in one variable result into corresponding

increment or decrement in the other. Thus, it explains that change in one variable leads to subsequent change in the

other variable. It assesses the degree and direction of the relationship between the variables. However, correlation

does not depict co-integration of the variables.

A mathematical formula for measuring the intensity or the magnitude of linear relationship between two variables

series was suggested by Karl Pearson. The method is;

𝑟 = 𝑑𝑥 𝑑𝑦

𝑑𝑥 2𝑑𝑦 2 or

𝑐𝑜𝑣 (𝑥 ,𝑦)

𝜎𝑥𝜎𝑦

5.2.2Co-integration

Variables are said to be co integrated if long run equilibrium relationship is found among them. If the two series of

Integrated of order one, then the partial difference between them might be stable around a fixed mean. This

narrates that the series are drifting together almost at the same rate. Such series are said to be co-integrated and the

resultant vectors (1,-𝛽0,𝛽1,𝛽2) are called as co integrating vectors. Engle and Granger (1987) defined co-integration as the components of the vector 𝑥𝑡 = (𝑥1𝑡 , 𝑥2𝑡 ……… . . 𝑥𝑛𝑡 ) are

said to be co integrated of order d, b, denoted by 𝑥𝑡~𝐶𝑇(𝑑, 𝑏) explained by if, all components of 𝑥𝑡 are integrated

of order d. and there exists co integrating vector 𝛽 = 𝛽1 , 𝛽2, ……… . such that the linear combination 𝛽𝑥𝑡 =

𝛽1𝑥1𝑡 + 𝛽2𝑥2𝑡 …… . +𝛽𝑛𝑥𝑛𝑡 is integrated of order (d-b) where b>0.

Johansen (1995) developed a maximum likelihood estimation procedure based on reduced rank regression method.

It is used for testing co-integration by interpreting the independent linear combinations for a set of time series

variables that has stationary roots. The Johansen test is based on 𝜆𝑡𝑟𝑎𝑐𝑒 and 𝜆𝑚𝑎𝑥 test statistics for assessing the

co integration among the variables The test for the number of characteristic roots that are insignificantly different

from unity. The trace and max statistics are depicted by ;

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 107

𝜆𝑡𝑟𝑎𝑐𝑒 (𝑟) = −𝑇 ln(1 − 𝜆𝑖 )

𝜆𝑚𝑎𝑥 𝑟, 𝑟 + 1 = −𝑇𝑙𝑛 ln(1 − 𝜆𝑟+1 )

Where

𝜆𝑖 =The estimated values of the characteristics roots obtained from the estimated 𝜋 matrix

T= the number of usable observations.

The trace statistics tests the null hypothesis that the number of co-integrating vectors are less than or equal to r

against a general alternative. Maximum Eigen value statistics tests a null of r co integrating vectors against the

specific alternative of r+1.

6. Results

On the basis of the tests used in e-views, the following results were discerned;

6.1 Correlation:

The Table 1 depicts the findings of Karl Pearson Coefficient of Correlation. The figures of correlation are

duplicated in the matrix. It was found that strong positive correlation existed between the Gross Domestic Savings

and the factors that represented Investment Climate in the Country. It can be interpreted that there is a sound and

positive correlation between Gross Domestic Savings and Industrial Climate. Similarly, there is a positive

relationship between Savings and Investments. Strong Positive relationship was also found between Savings and

Trade Openness. On the similar grounds strong positive correlation was also found between Savings and Valued

addition by Manufacturing Sector.

Thus it can be inferred that higher domestic savings can lead to spur Investment Climate in the Country.

Table: 1 Correlation between Gross Domestic Savings and Proxies for Investment Climate in India.

LNGDS

LNINDUST

RY LNINVST LNTRADE LNMANU

LNGDS 1.000000 0.996952 0.951106 0.962366 0.994841

LNINDUST

RY 0.996952 1.000000 0.940061 0.966709 0.999424

LNINVST 0.951106 0.940061 1.000000 0.924990 0.939161

LNTRADE 0.962366 0.966709 0.924990 1.000000 0.965359

LNMANU 0.994841 0.999424 0.939161 0.965359 1.000000

6.2 Johansen Co-integration Test

To assess the linear combination of integrated variables, Johansen Co-integration was applied to infer the co-

integration between Domestic Savings and Investment Climate. The variable Domestic Savings and proxies for

investment climate were pretested to assess their order of integration. The Augmented Dickey Fuller Test (ADF)

was used in the present study on all the series individually to assess the order of integration. ADF was used in E

views 7 to infer the stationarity of the variables. Accordingly, it was found that all the variables are integrated of

order 1 [I (1)], i.e. they are stationary at first difference (Table 2). Further, a VAR Lag Order Selection Criteria

was used in to assess the lag length criteria. The Johansen test is quite sensitive to the lag length; therefore the lag

length test was used in e views. It was found that t-statistic for two lags is significant at the specified critical value.

Hence, one lag criteria were found appropriate according to these LR (Likelihood Ratio Criterion), AIC (Akaike

Information Criterion), SIC (Schwarz Information Criterion), FPE (Final Prediction Error), HQ (Hannan-Quinn

Information Criterion) criterion. Therefore, lag length 2 has been selected on the basis of multivariate

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 108

generalizations of the all the criteria. The undifferenced data was used in Johansen Co-integration Test in EViews

to assess the co-integration among the series. Further, the same lag length as obtained from VAR Lag Order

Selection Criteria in E Views has been taken.

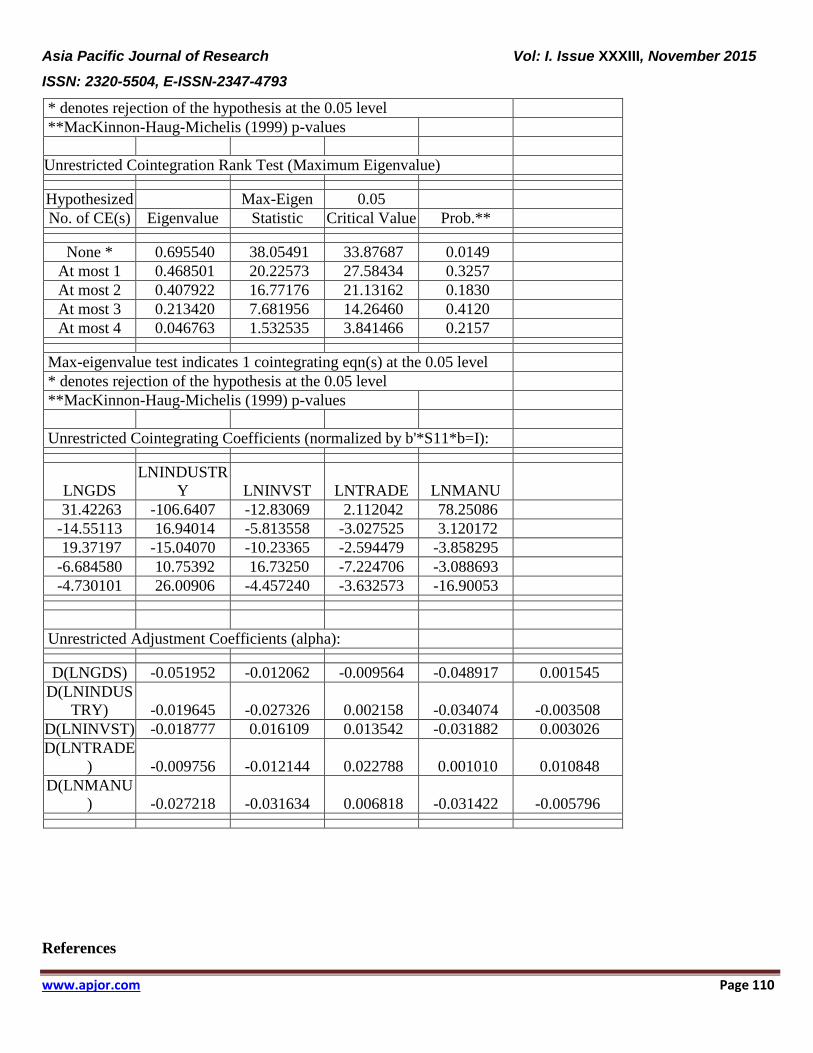

As a guideline if the absolute value of the computed Trace and Maximum Eigen Value exceeds the critical value

then the null hypothesis of no co-integration is rejected and at least one way co integration among the variables is

accepted at 5% level of significance. On the basis of the result of the test as depicted in Table No. 2 it was found

that as per Trace statistics 84.266 is greater than the critical value of 64.819 at 5% significance level, therefore, it

is possible to reject the null hypothesis of no co-integrating vectors and accept the alternative one or more co

integrating equations for the two series. Moreover, The Maximum Eigen Value test results that Maximum Eigen

statistic 38.055 exceeds the 33.87 percent critical value of the 𝜆max 𝑒𝑖𝑔𝑒𝑛 and hence it is possible to reject the

null hypothesis of no co-integrating vectors and accept the alternative one or more co-integrating equations for

Domestic Savings and proxies for Investment Climate series. Thus, the null hypothesis of no co-integration is

strictly rejected at 5% level of significance, implying long run relationship among the variables. Thus, it may be

inferred that there exist long run equilibrium relationship between Gross Domestic savings and Investment Climate

in India.

7. Conclusion

On the basis of the results derived by applying the Correlation and Co-integration test, it was found that strong

correlation was found between Domestic Savings and Investment Climate. This means these two influences each

other in the long run.

Thus, on the basis of correlation and co-integration analysis, it was found that null hypothesis of no correlation and

co-integration between Domestic savings and Investment Climate is strictly rejected and the alternate hypothesis

of significant correlation and co-integration among the Domestic Savings and proxies of investment climate has

been accepted. The results denotes that savings in the country is an important factor that have significant impact on

the investment climate. This means that Gross Domestic Savings should be accelerated in the economy for

developing healthy investment climate in the country. Accordingly, this Gross Domestic Savings may intensify

Investment Climate in long run which will eventually results in attracting foreign savings and thereby maintaining

high growth rate in the economy.

Thus in the nutshell, Domestic Savings and Investment Climate are strongly related to each other in India.

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 109

Tables: Results of the Test used

Table: 2 Results from Johansen Co-integration Test

VAR Lag Order Selection Criteria

Endogenous variables: LNGDS LNINDUSTRY LNINVST

LNTRADE LNMANU

Exogenous variables: C

Date: 07/01/15 Time: 08:47

Sample: 1975 2013

Included observations: 32

Lag LogL LR FPE AIC SC HQ

0 162.6416 NA 3.62e-11 -9.852598 -9.623576 -9.776683

1 278.5395 188.3341* 1.26e-13* -15.53372* -14.15959* -15.07823*

2 303.3228 32.52809 1.45e-13 -15.52017 -13.00094 -14.68512

* indicates lag order selected by the criterion

LR: sequential modified LR test statistic (each test at 5%

level)

FPE: Final prediction error

AIC: Akaike information criterion

SC: Schwarz information criterion

HQ: Hannan-Quinn information criterion

Date: 07/02/15 Time: 07:38

Sample (adjusted): 1982 2013

Included observations: 32 after adjustments

Trend assumption: Linear deterministic trend

Series: LNGDS LNINDUSTRY LNINVST LNTRADE

LNMANU

Lags interval (in first differences): 1 to 1

Unrestricted Cointegration Rank Test (Trace)

Hypothesized Trace 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.695540 84.26690 69.81889 0.0023

At most 1 0.468501 46.21199 47.85613 0.0708

At most 2 0.407922 25.98625 29.79707 0.1291

At most 3 0.213420 9.214491 15.49471 0.3459

At most 4 0.046763 1.532535 3.841466 0.2157

Trace test indicates 1 cointegrating eqn(s) at the 0.05 level

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 110

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized Max-Eigen 0.05

No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.695540 38.05491 33.87687 0.0149

At most 1 0.468501 20.22573 27.58434 0.3257

At most 2 0.407922 16.77176 21.13162 0.1830

At most 3 0.213420 7.681956 14.26460 0.4120

At most 4 0.046763 1.532535 3.841466 0.2157

Max-eigenvalue test indicates 1 cointegrating eqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegrating Coefficients (normalized by b'*S11*b=I):

LNGDS

LNINDUSTR

Y LNINVST LNTRADE LNMANU

31.42263 -106.6407 -12.83069 2.112042 78.25086

-14.55113 16.94014 -5.813558 -3.027525 3.120172

19.37197 -15.04070 -10.23365 -2.594479 -3.858295

-6.684580 10.75392 16.73250 -7.224706 -3.088693

-4.730101 26.00906 -4.457240 -3.632573 -16.90053

Unrestricted Adjustment Coefficients (alpha):

D(LNGDS) -0.051952 -0.012062 -0.009564 -0.048917 0.001545

D(LNINDUS

TRY) -0.019645 -0.027326 0.002158 -0.034074 -0.003508

D(LNINVST) -0.018777 0.016109 0.013542 -0.031882 0.003026

D(LNTRADE

) -0.009756 -0.012144 0.022788 0.001010 0.010848

D(LNMANU

) -0.027218 -0.031634 0.006818 -0.031422 -0.005796

References

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 111

Bahmani-Oskooee and Chakrabarti (2005) Openness, size, and the saving–investment relationship,

[Online] Economic Systems 29 (2005) 283–293, Elsevier, Available:

http://www.researchgate.net/profile/Mohsen_Bahmani-

Oskooee/publication/222568019_Openness_size_and_the_savinginvestment_relationship/links/54a2f7b60c

f256bf8bb0de3a.pdf [Accessed 26/08/2015]

Di Lorio Francesa and Fachin Stefano (2011) A Panel Co-integration Study of the Long-Run Relationship

between Savings and Investments in the OECD Economies, [Online] , Government of the Italian Republic

(Italy), Ministry of Economy and Finance, Department of the Treasury Working Paper No. 3, Available:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1769554, [Accessed 26/08/2015]

Dollar David, Hallward-Driemeier Mary, and Mengistae Taye (2003) Investment Climate and Firm

Performance in Developing Economies, [Online], Economic Development and Cultural Change,

Available: http://www.researchgate.net/publication/24098228, [Accessed 26/08/2015]

Emmanuel Anoruo (2001) Savings –Investment Connection: Evidence from the ASEAN Countries,

[Online], The American Economist, Vol. 45, No. 1 (Spring, 2001) , pp. 46-53, Omicron Delta Epsilon,

Available: http://www.jstor.org/stable/25604213, [Last Accessed 21/11/2015]

Engle and Granger (1987) Co-integration and Error Correction: Representation, Estimation and Testing,

Econometrica, Vol 55, 1987, pp.251-276 as cited in Gujarati D.N., Porter D.Cand Gunasekar S. Basic

Econometrics, Fifth Edition, Mc Graw Hill Education (India) Private Limited: New Delhi

Jangili Ramesh (2011) Causal Relationship between Saving, Investment and Economic Growth for India–

What does the Relation Imply?, [Online], Reserve Bank of India Occasional Papers, Vol. 32, No. 1,

Summer 20, Available: https://rbidocs.rbi.org.in/rdocs/Content/PDFs/A2_V32070212.pdf [Accessed

26/08/2015]

Johansen (1995) The Role of the Constant and Linear Terms in Co-integration Analysis of Non Stationary

Variables, Econometric Reviews, 13 (1994), 205-30

Johansen S and Juselius K. (1990) Maximum Likelihood Estimation and Inference on Co-integration with

Application to the Demand for Money, Oxford Bulletin of Economics and Statistics , 52(1990), 169-209

Kaya Hüseyin (2010) Saving Investment Association in Turkey, [Online], Middle Eastern and North

African Economies, Electronic Journal, Volume 12, Middle East Economic Association and Loyola

University Chicago, September, 2010, Available:

http://ecommons.luc.edu/cgi/viewcontent.cgi?article=1125&context=meea [Accessed 30/06/2015]

Kinda Tidiane (2010) Investment climate and FDI in developing countries: firm-level evidence, [Online],

World development, Elsevier 38, 4, 498--513 Available: http://economics.ca/2008/papers/0339.pdf [

Accessed 26/08/2015 ]

Komain Jiranyakul and Tantatape Brahmasrene (2008) Co-integration between Investment and Saving in

Selected Asian Countries: ARDL Bounds Testing Procedure, [Online], MPRAMunich Personal RePEc

Archive, Available: http://mpra.ub.uni-muenchen.de/45076/1/MPRA_paper_45076.pdf, [Accessed

26/08/2015]

KU Christopher, FO Nwaigwe,(2013) An econometric analysis of the investment climate and growth

potential in Nigeria, [Online], African Journal of Governance and Development Available:

http://www.ajol.info/index.php/ajgd/article/view/93018 [Accessed 26/08/2015]

Mohan Ramesh, (2006) Causal relationship between savings and economic growth in countries with

different income levels, [Online], Economics Bulletin, vol. 5, no. 3 pp. 1−12, Available:

http://www.economicsbulletin.com/2006/volume5/eb−05e20002a.pdf, [Accessed 26/08/2015]

Asia Pacific Journal of Research Vol: I. Issue XXXIII, November 2015

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 112

Narayan Paresh Kumar (2005) The relationship between saving and investment for Japan, [Online], Japan

and the World Economy, Volume 17, Issue 3, August 2005, Pages 293–309, Available:

http://www.sciencedirect.com/science/article/pii/S0922142504000210s, [Last Accessed 21/11/2015]

Nwogwugwu Uche C.C, & Odulukwe Onwuka Kevin (2012) Do Domestic Conditions Matter for

Investments? [Online], Evidence from Nigeria Data, Universal Journal of Management and Social

Sciences Vol. 2, No.11; November 2012, Available: http://cprenet.com/uploads/archive/UJMSS_12-

1204.pdf [Accessed 26/08/2015]

Ogbokor Cyril Ayetuoma and Musilika Oscar Andiya (2014) Investigating the Relationship between

Aggregate Savings and Investment in Namibia: A Causality Analysis, [Online], Research Journal of

Finance and Accounting, ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online), Vol.5, No.6, 2014 82

Available: http://www.iiste.org/Journals/index.php/RJFA/article/view/11914 [Accessed 26/08/2015]

Paliwar Veena K., Money, Finance and Economic activity in India – A CGE Analysis, Economic Journal,

Volume 48, Page no 22.

Phillips Lauren M. (2006) Growth and the Investment Climate: Progress and Challenges for Asian

Economies, [Online], Institute of Development Studies. Available

:http://www.asia2015conference.org/pdfs/Phillips.pdf, [Last Accessed 24/11/2015]

Smith, W. and World Bank, 2004, World Development Report 2005: A Better Investment Climate for

Everyone, [Online], A World Bank Publication, Volumes 33-35. Available:

https://books.google.co.in/books?id=frJPngEACAAJ [Last Accessed 24/11/2015]

Stern, N. (2002) Strategy for Development. Washington, DC, USA: World Bank Publications, 2002. P iv.

in Al-Salem Fouad and Mohammed Mostafa (2012), Factors Affecting The Investment Climate For An

International Financial Center In Kuwait, [Online], The Journal of Applied Business Research –

November/December 2012 Volume 28, Number 6 Available:

http://www.google.co.in/url?sa=t&rct=j&q=&esrc=s&source=web&cd=10&cad=rja&uact=8&ved=0ahUK

Ewjz34-

WzqjJAhWGxI4KHXOcD5sQFghVMAk&url=http%3A%2F%2Fwww.cluteinstitute.com%2Fojs%2Finde

x.php%2FJABR%2Farticle%2Fdownload%2F7350%2F7418&usg=AFQjCNH2DjURHEGYWot7FjySQZ

6SxGETZA&bvm=bv.108194040,d.c2E [Last Accessed 24/11/2015]

Data are compiled from the http://data.worldbank.org/ an open access World Bank database.

Related Documents