Assessing Foreign Exchange Risk FIN 40500: International Finance

Assessing Foreign Exchange Risk FIN 40500: International Finance.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Assessing Foreign Exchange Risk

FIN 40500: International Finance

5.PrPr TailsHeads

There is a “true” probability distribution that governs the outcome of a coin toss

Suppose that we were to flip a coin over and over again and after each flip, we calculate the percentage of heads & tails

FlipsTotal

Headsof

#5.

That is, if we collect “enough” data, we can eventually learn the truth!

(Sample Statistic) (True Probability)

Pro

babi

lity

EventMean

Probability distributions identify the chance of each possible event occurring

1 SD

2 SD

3 SD

-1 SD

-2 SD

-3 SD

65%

95%

99%

Continuous distributions

2,N

Sampling

Suppose that you wanted to learn about the temperature in South Bend

Temperature ~ 2,N

We could find this distribution by collecting temperature data for south bend

N

iixN

x1

1

2

1

22 1

N

ii xx

Ns

Sample Mean

(Average)

Sample Variance

Conditional Distributions

Obviously, the temperature in South Bend is different in the winter and the summer. That is, temperature has a conditional distribution

Temp (Summer) ~ 2, ssN

Temp (Winter) ~ 2, WWN

Regression is based on the estimation of conditional distributions

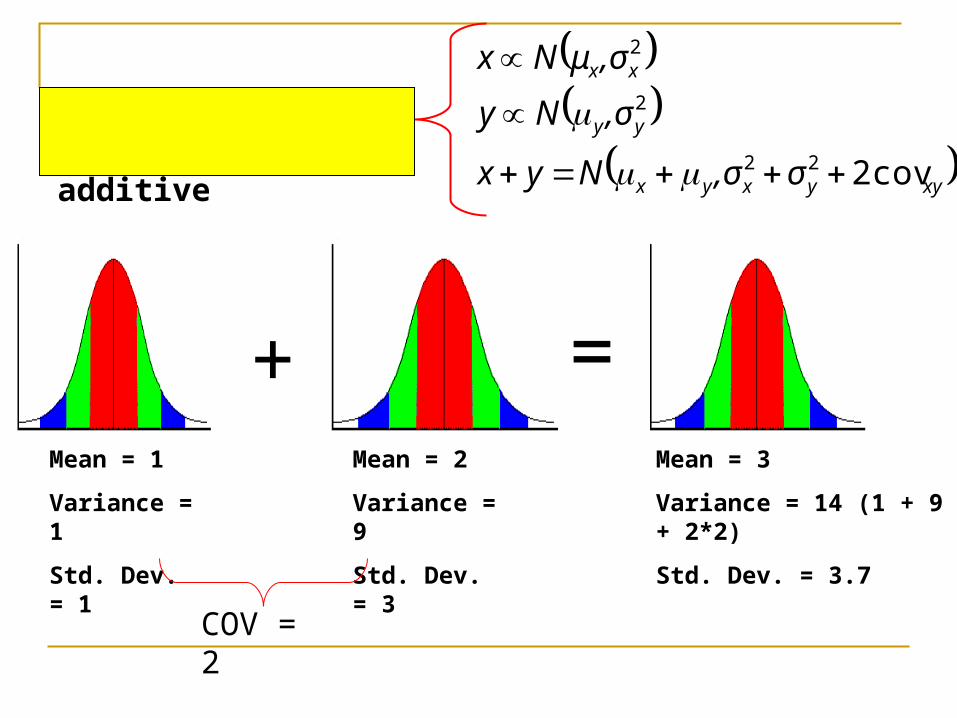

Mean = 1

Variance = 4

Std. Dev. = 2

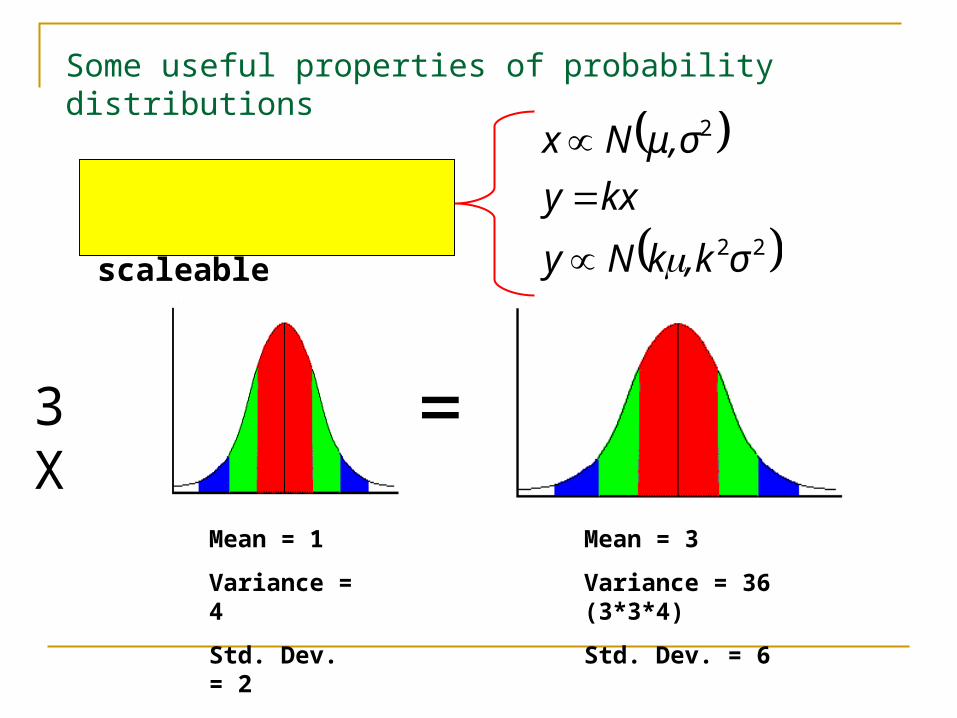

Probability distributions are scaleable

22

2

σ,kkNy

kxy

μ,σNx

3 X =

Mean = 3

Variance = 36 (3*3*4)

Std. Dev. = 6

Some useful properties of probability distributions

Mean = 1

Variance = 1

Std. Dev. = 1

Probability distributions are additive

xyyxyx

yy

xx

σ,σNyx

,σNy

,σμNx

cov222

2

2

+Mean = 2

Variance = 9

Std. Dev. = 3

COV = 2

=Mean = 3

Variance = 14 (1 + 9 + 2*2)

Std. Dev. = 3.7

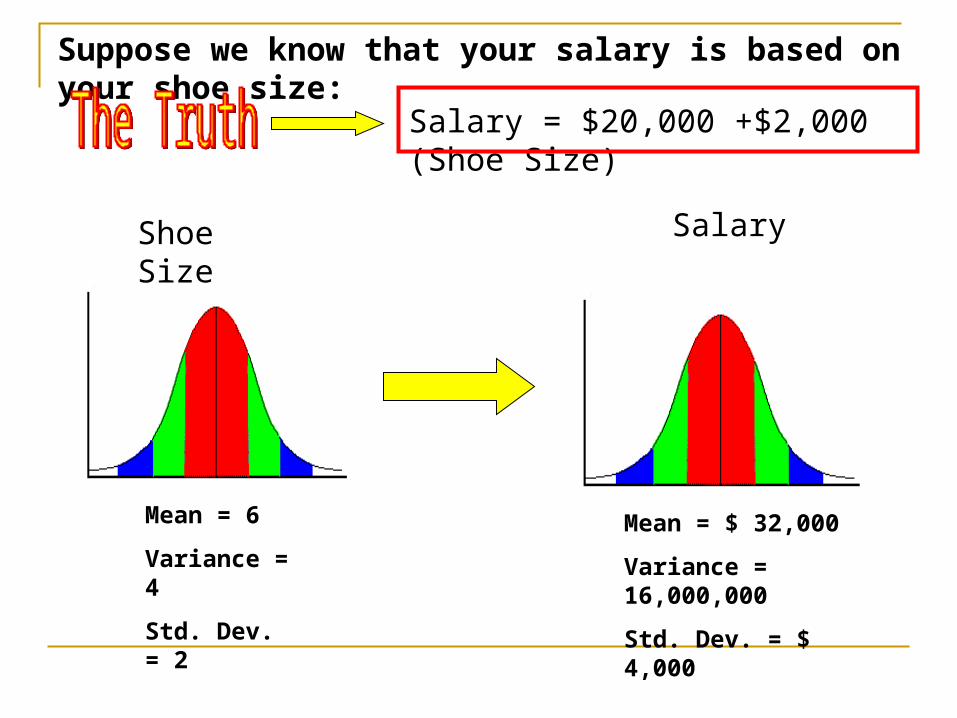

Mean = 6

Variance = 4

Std. Dev. = 2

Mean = $ 32,000

Variance = 16,000,000

Std. Dev. = $ 4,000

Suppose we know that your salary is based on your shoe size:

Salary = $20,000 +$2,000 (Shoe Size)

Shoe Size Salary

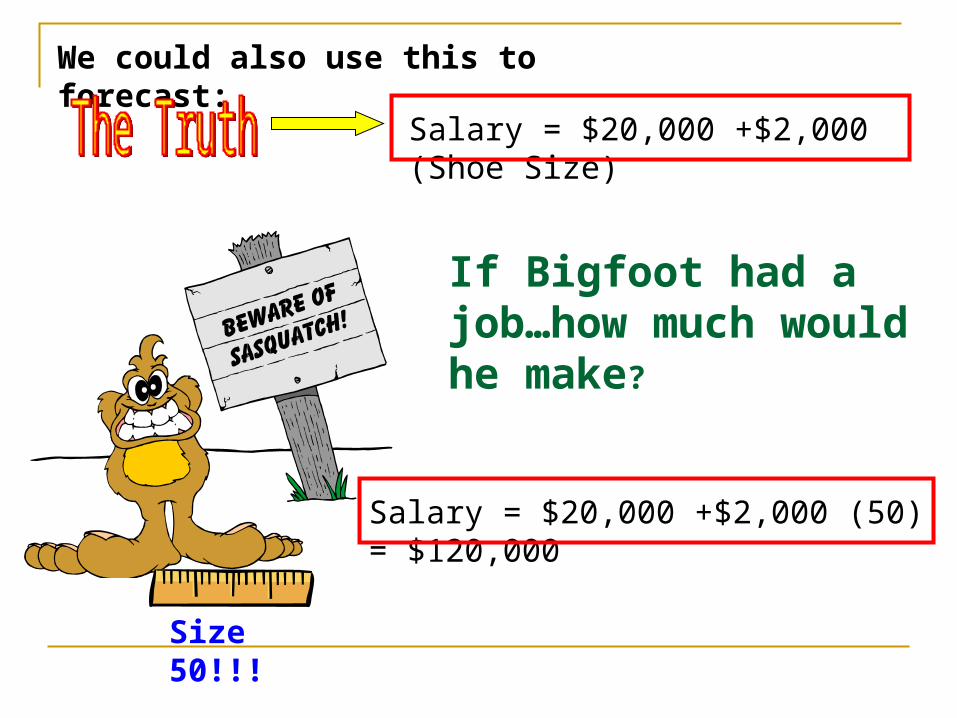

We could also use this to forecast:

Salary = $20,000 +$2,000 (Shoe Size)

If Bigfoot had a job…how much would he make?

Size 50!!!

Salary = $20,000 +$2,000 (50) = $120,000

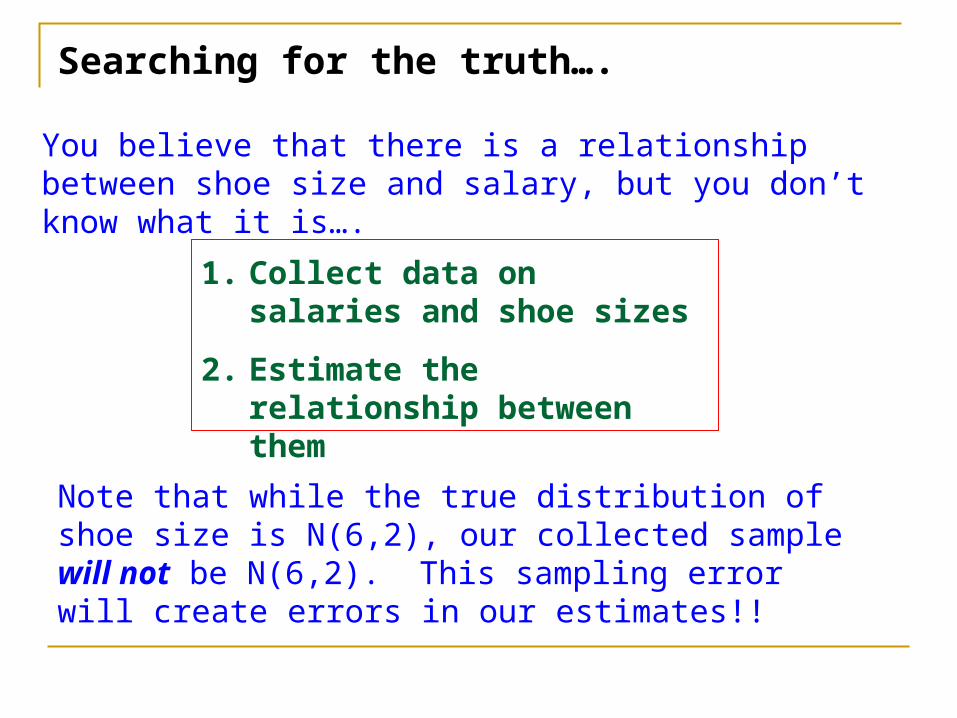

Searching for the truth….

You believe that there is a relationship between shoe size and salary, but you don’t know what it is….

1. Collect data on salaries and shoe sizes

2. Estimate the relationship between them

Note that while the true distribution of shoe size is N(6,2), our collected sample will not be N(6,2). This sampling error will create errors in our estimates!!

0

10000

20000

30000

40000

50000

60000

70000

0 2 4 6 8 10 12 14

Shoe Size

Sala

ry

Salary = a +b * (Shoe Size) + error

a

20,σNerror

Slope = b

We want to choose ‘a’ and ‘b’ to minimize the error!

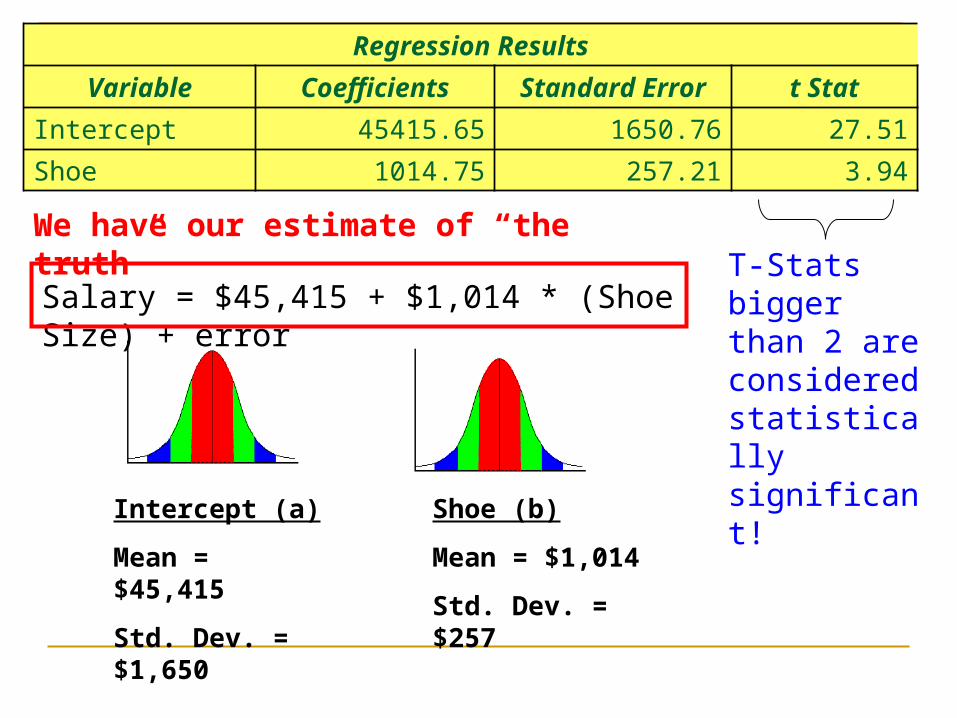

Regression Results

Variable Coefficients Standard Error t Stat

Intercept 45415.65 1650.76 27.51

Shoe 1014.75 257.21 3.94

Salary = $45,415 + $1,014 * (Shoe Size) + error

We have our estimate of “the truth”

Intercept (a)

Mean = $45,415

Std. Dev. = $1,650

Shoe (b)

Mean = $1,014

Std. Dev. = $257

T-Stats bigger than 2 are considered statistically significant!

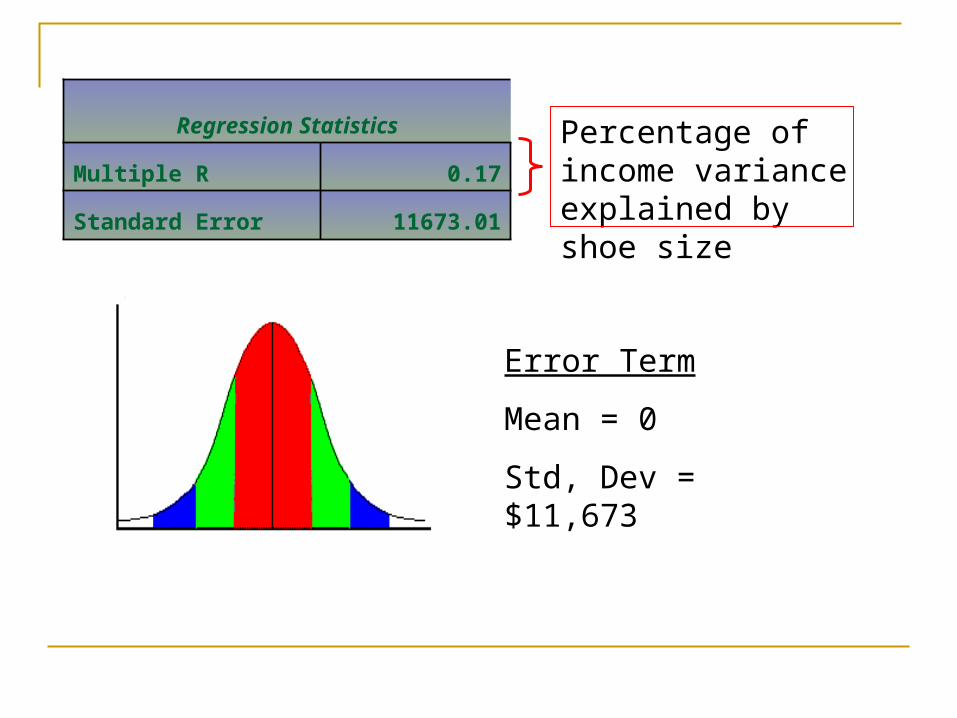

Regression Statistics

Multiple R 0.17

Standard Error 11673.01

Error Term

Mean = 0

Std, Dev = $11,673

Percentage of income variance explained by shoe size

Using regressions to forecast (Remember, Bigfoot wears a size 50)….

Salary = $45,415 + $1,014 * (Shoe Size) + error

50

Mean = $45,415

Std. Dev. = $1,650

Mean = $1,014

Std. Dev. = $ 257

Mean = $0

Std. Dev. = $11,673

Salary Forecast

Mean = $96,115

Std. Dev. = $17,438

438,17$)673,11()257()50()650,1( 2222 StdDev

Given his shoe size, you are 95% sure Bigfoot will earn between $61,239 and $130,991

We’ve looked at several currency pricing models that have potential for being “the truth”

Any combination of these could be “the truth”!!

tt NXe %

*% ttte

*% iiet

1

%%i

itt fEe

Trade Balance Approach

Monetary Approach

Interest Rate Approach

Price Level Approach

1

%%i

itt eEe Technical Approach

-10

-8

-6

-4

-2

0

2

4

6

8

10

-10.0 -5.0 0.0 5.0 10.0 15.0

Inflation Differential

% C

han

ge in

Exch

an

ge R

ate

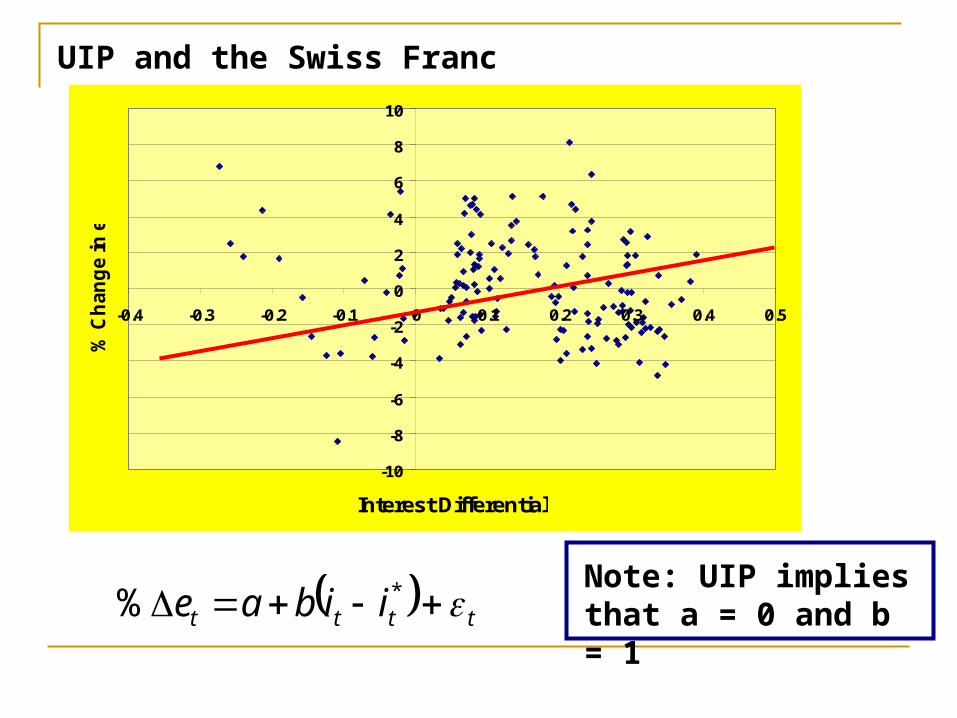

tttt bae *% Note: PPP implies that a = 0 and b = 1

PPP and the Swiss Franc

Regression Results

Variable Coefficients Standard Error t Stat

Intercept .027 .231 .12

Inflation 1.40 .742 1.89

Regression Results

Variable P-value Lower 95% Upper 95%

Intercept .910 -.49 .43

Inflation .06 -.065 2.86

Regression Statistics

R Squared .02

Standard Error 2.69

Observations 155

For every 1% increase in US inflation over Swiss inflation, the dollar depreciates by 1.40%

-10

-8

-6

-4

-2

0

2

4

6

8

10

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101 106 111 116 121 126 131 136 141 146 151

Predicted Actual

Obviously, we have not explained very much of the volatility in the CHF/USD exchange rate

tttt iibae *%Note: UIP implies that a = 0 and b = 1

UIP and the Swiss Franc

-10

-8

-6

-4

-2

0

2

4

6

8

10

-0.4 -0.3 -0.2 -0.1 0 0.1 0.2 0.3 0.4 0.5

Interest Differential

% C

han

ge in

e

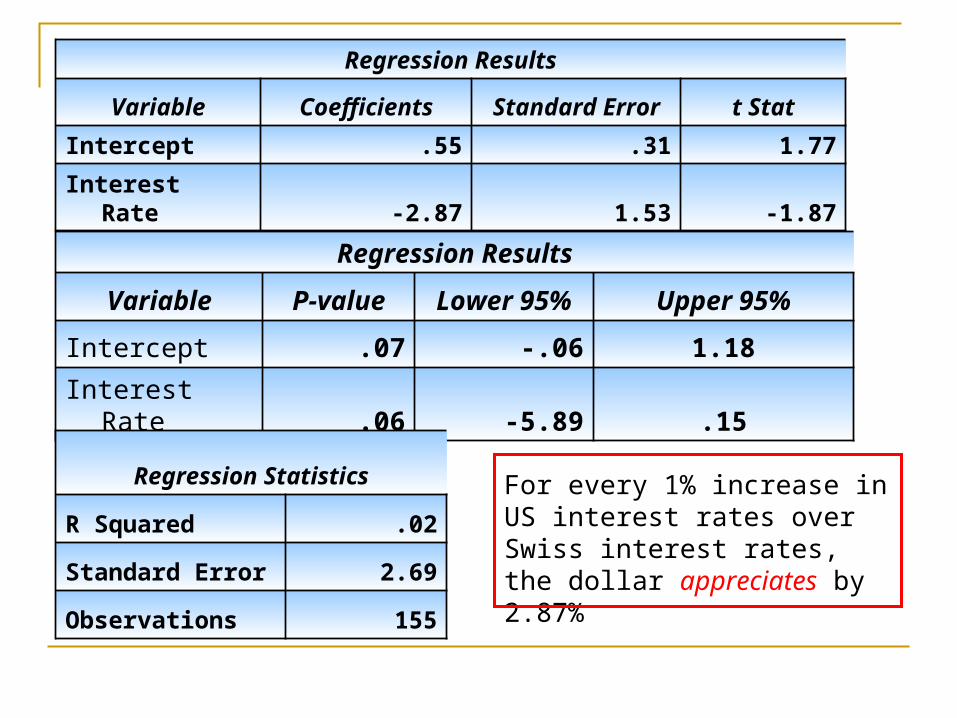

Regression Results

Variable Coefficients Standard Error t Stat

Intercept .55 .31 1.77

Interest Rate -2.87 1.53 -1.87

Regression Results

Variable P-value Lower 95% Upper 95%

Intercept .07 -.06 1.18

Interest Rate .06 -5.89 .15

Regression Statistics

R Squared .02

Standard Error 2.69

Observations 155

For every 1% increase in US interest rates over Swiss interest rates, the dollar appreciates by 2.87%

We still have not explained very much of the volatility in the CHF/USD exchange rate

-10

-8

-6

-4

-2

0

2

4

6

8

10

1 7 13 19 25 31 37 43 49 55 61 67 73 79 85 91 97 103 109 115 121 127 133 139 145 151

Exchange Rate Predicted Exchange Rate

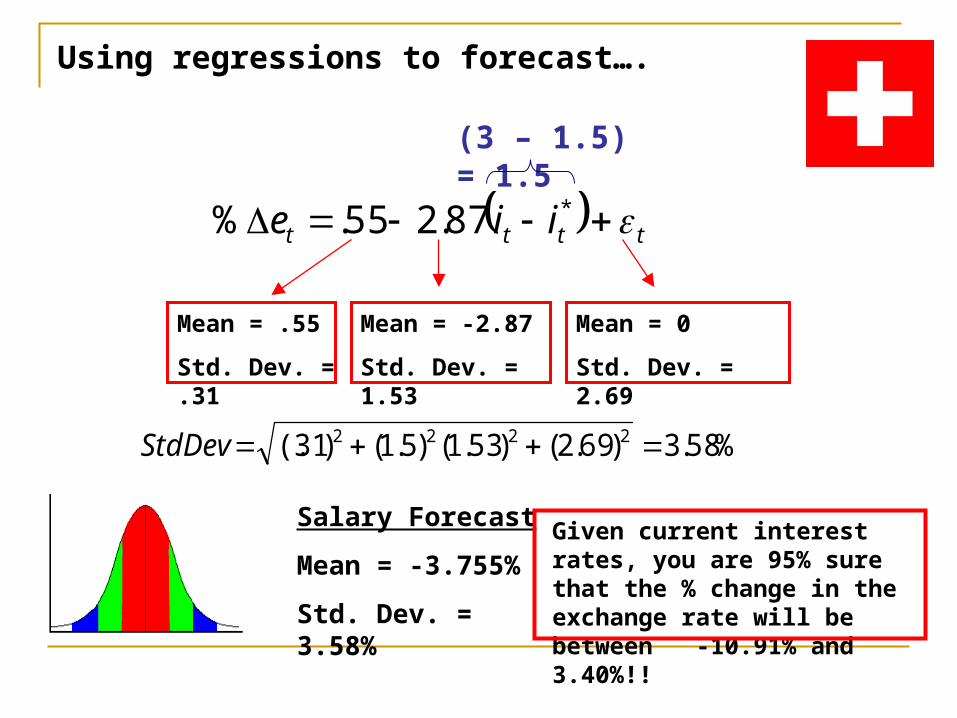

Using regressions to forecast….

(3 – 1.5) = 1.5

Mean = .55

Std. Dev. = .31

Mean = -2.87

Std. Dev. = 1.53

Mean = 0

Std. Dev. = 2.69

Salary Forecast

Mean = -3.755%

Std. Dev. = 3.58%

%58.3)69.2()53.1()5.1()31(. 2222 StdDev

Given current interest rates, you are 95% sure that the % change in the exchange rate will be between -10.91% and 3.40%!!

tttt iie *87.255.%

Technical Analysis Uses prior movements in the exchange rate to predict the future

-10

-8

-6

-4

-2

0

2

4

6

8

10

-10 -8 -6 -4 -2 0 2 4 6 8 10

%Change (t-1)

% C

han

ge (t)

ttt ebae 1%%

Regression Results

Variable Coefficients Standard Error t Stat

Intercept .12 .21 .57

Prior Change .29 .07 3.86

Regression Results

Variable P-value Lower 95% Upper 95%

Intercept .56 -.29 .53

Prior Change .0001 .14 .45

Regression Statistics

R Squared .09

Standard Error 2.59

Observations 154

A 1% depreciation of the dollar is typically followed by a .29% depreciation

BLADES Board & Skate arrived on the action / extreme scene in 1990, and quickly became a trusted source of equipment and service to in-line skaters, skateboarders, and snowboarders.

BLADES got its start in New York and currently operates 15 retail stores in New York, New Jersey, Massachusetts and Pennsylvania.

Increasing competition and rising costs have lowered Blades’ profit margins

Blades could cut costs by importing lower cost components from Thailand

Suppose that Blades makes an agreement to buy plastic components sufficient to produce 72,000 pairs of rollerblades from Thai manufacturers at a price of THB 2,870 per pair. ($1 = THB 38.87). Payment is due in one month (72,000*2,870 = THB 206.64 M)

Trend

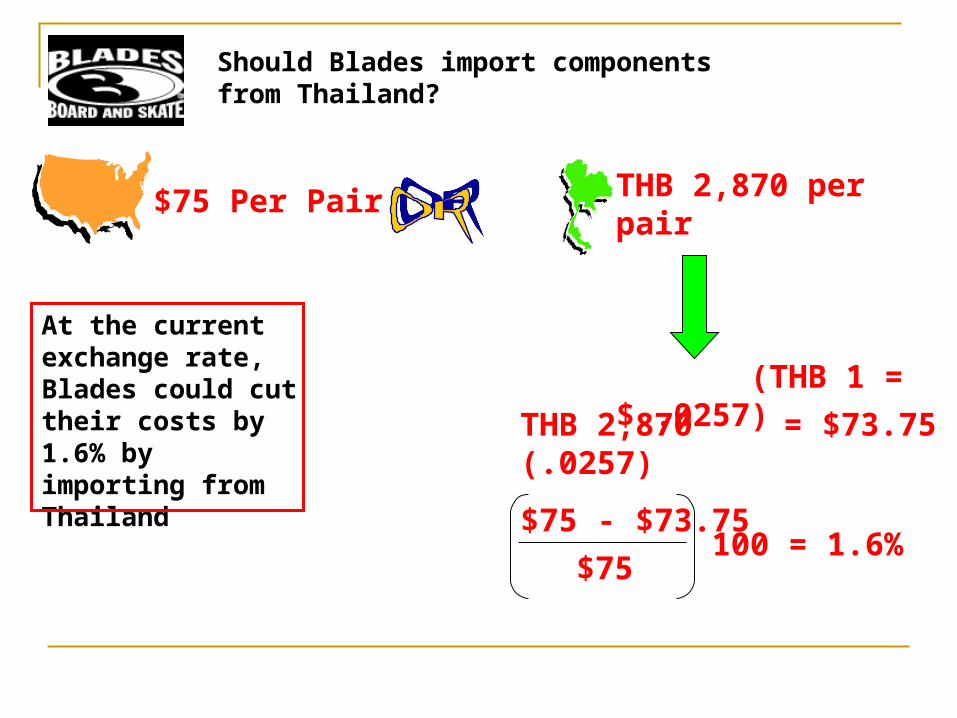

THB 2,870 per pair (THB 1 = $ .0257)

Should Blades import components from Thailand?

$75 Per Pair

THB 2,870 (.0257) = $73.75

$75 - $73.75

$75100 = 1.6%

At the current exchange rate, Blades could cut their costs by 1.6% by importing from Thailand

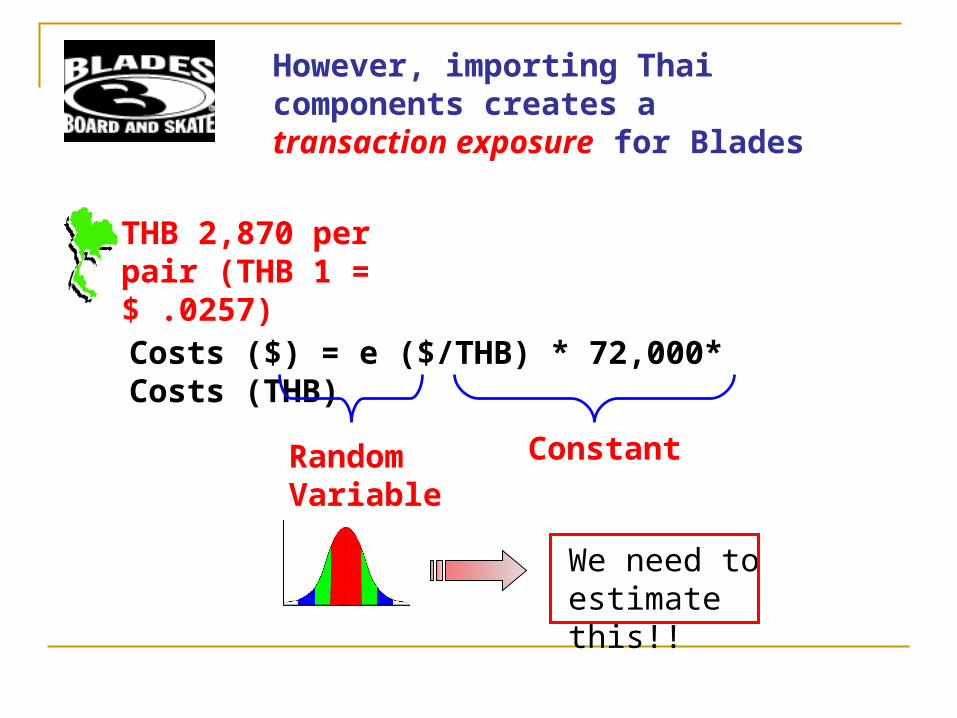

However, importing Thai components creates a transaction exposure for Blades

THB 2,870 per pair (THB 1 = $ .0257)

Costs ($) = e ($/THB) * 72,000* Costs (THB)

ConstantRandom Variable

We need to estimate this!!

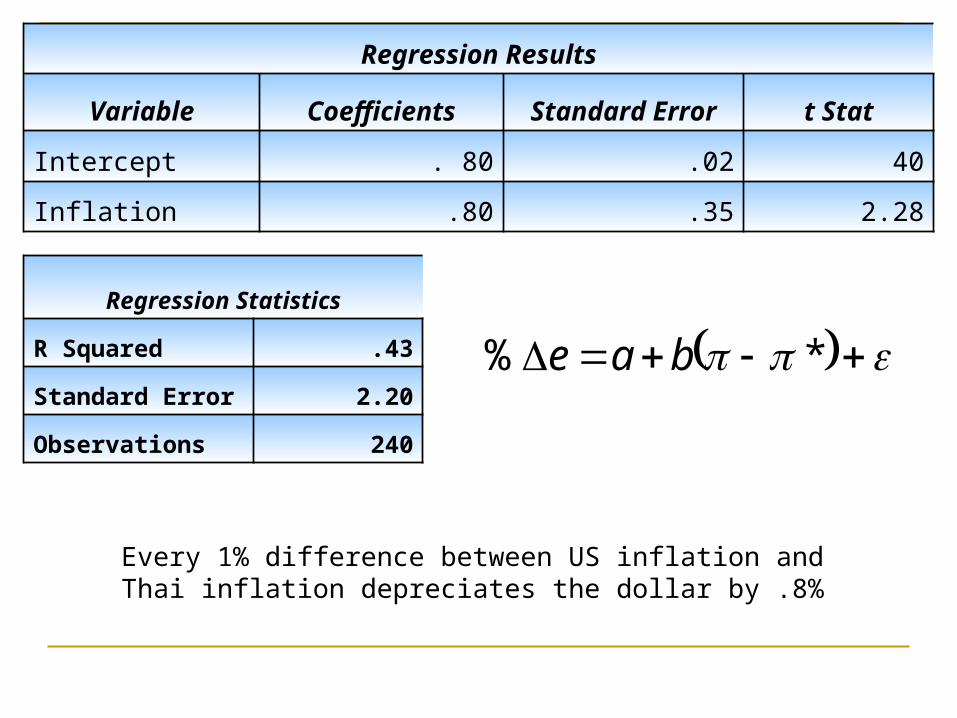

Regression Results

Variable Coefficients Standard Error t Stat

Intercept . 80 .02 40

Inflation .80 .35 2.28

Regression Statistics

R Squared .43

Standard Error 2.20

Observations 240

*% bae

Every 1% difference between US inflation and Thai inflation depreciates the dollar by .8%

US inflation is currently 1% (per month) while inflation in Thailand is 2.25% (per month)

(1 – 2.25) = -1.25

Mean = . 80

Std. Dev. = .02

Mean = .80

Std. Dev. = . 35

Mean = 0

Std. Dev. = 2.20

Forecast

Mean = -.2%

Std. Dev. = 2.25%

%25.2)20.2()25.1()35(.)02(. 2222 StdDev

Your 95% confidence interval for the (monthly) percentage change in the exchange rate is [-4.7% , 4.3% ]

*% bae

Forecast (% Change)

Mean = -.2%

Std. Dev. = 2.25%

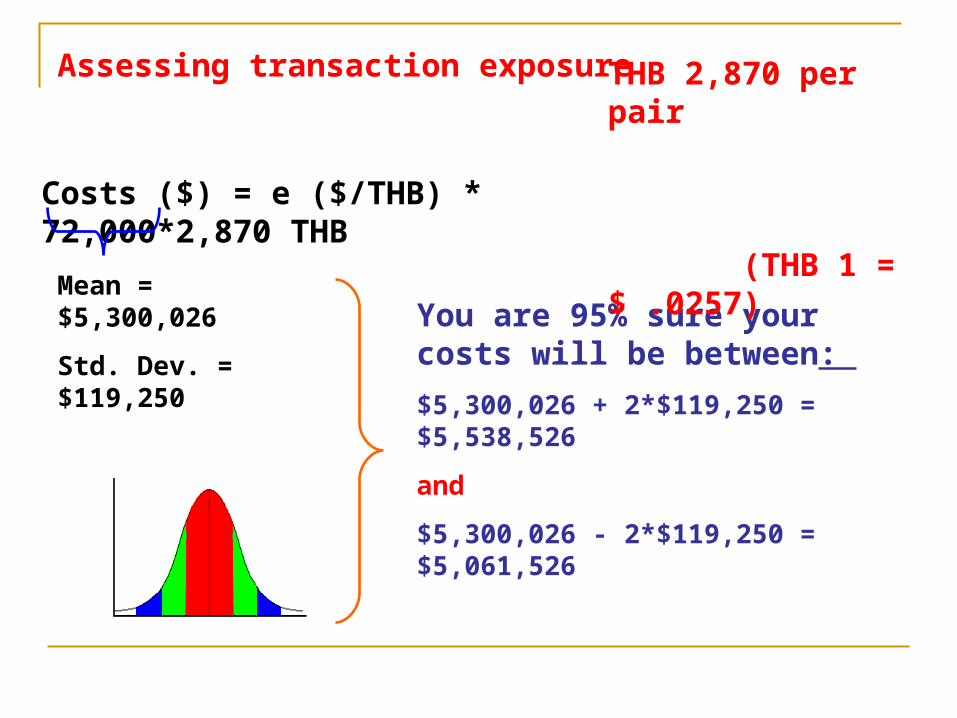

Assessing transaction exposure

Costs ($) = e ($/THB) * 72,000*2,870 THB

THB 2,870 per pair (THB 1 = $ .0257)

Costs

Mean = 72,000*2,870*.0257(1-.002)

= $5,300,026

Std. Dev. = .0225*72000*2870*.0256

= $119,250

Assessing transaction exposure

Costs ($) = e ($/THB) * 72,000*2,870 THB

You are 95% sure your costs will be between:

$5,300,026 + 2*$119,250 = $5,538,526

and

$5,300,026 - 2*$119,250 = $5,061,526

THB 2,870 per pair (THB 1 = $ .0257)

Mean = $5,300,026

Std. Dev. = $119,250

THB 2,870 per pair (THB 1 = $ .0257)

Should Blades import components from Thailand?

$75 Per Pair

Mean = $5,300,026

Std. Dev. = $119,250

Mean = $5,400,000

Std. Dev. = $0

What do you do?

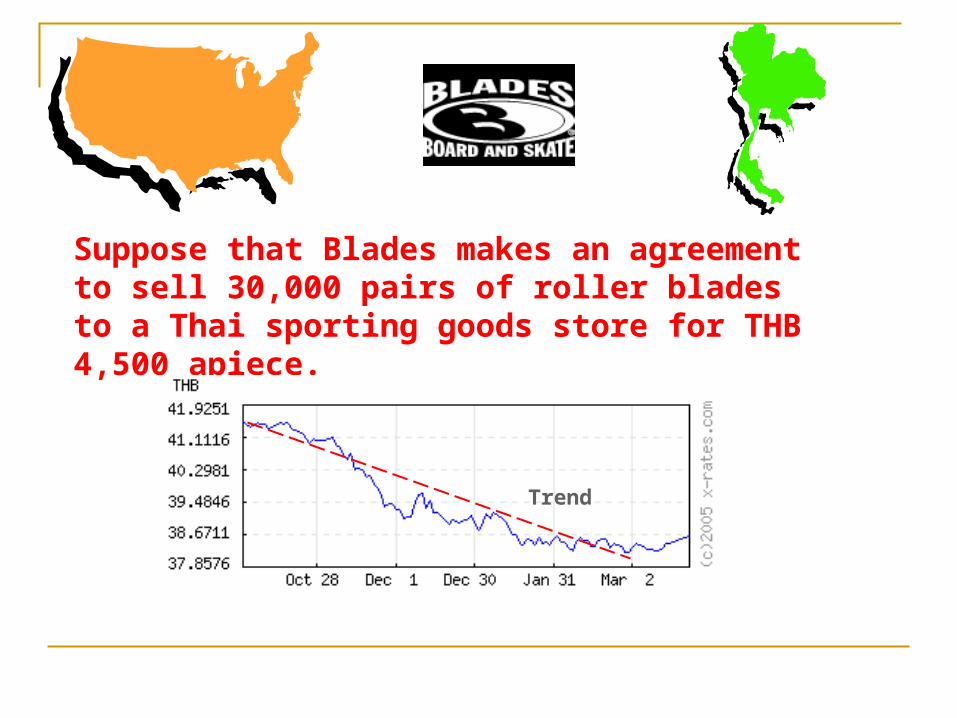

Blades is also thinking about exporting rollerblades to Thailand

Suppose that Blades makes an agreement to sell 30,000 pairs of roller blades to a Thai sporting goods store for THB 4,500 apiece.

Trend

Forecast (% Change)

Mean = -.2%

Std. Dev. = 2.25%

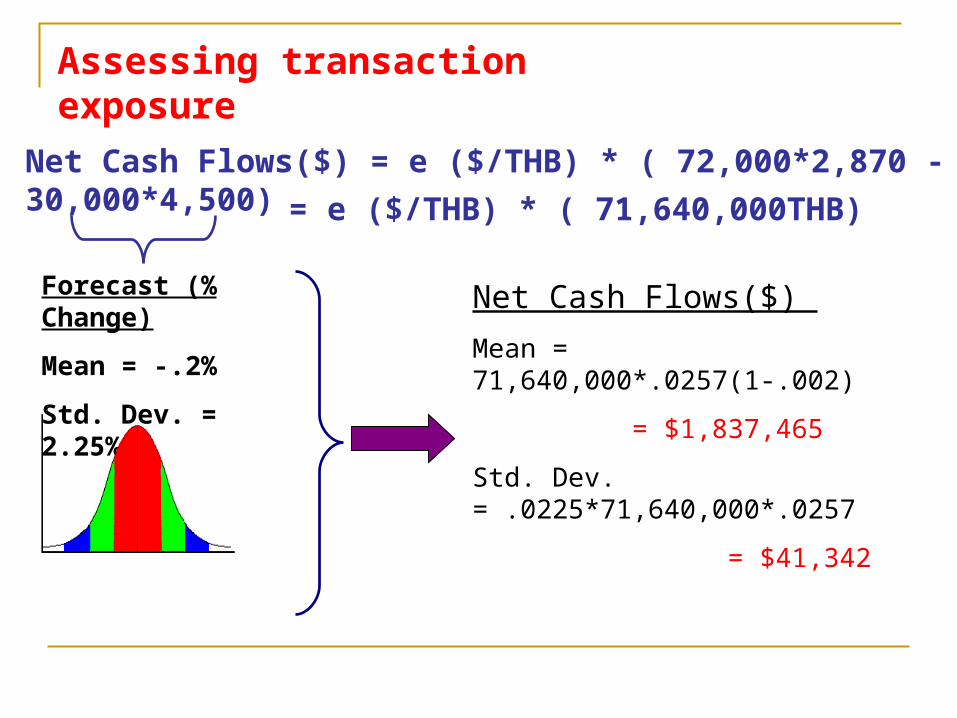

Assessing transaction exposure

Net Cash Flows($) = e ($/THB) * ( 72,000*2,870 - 30,000*4,500)

Net Cash Flows($)

Mean = 71,640,000*.0257(1-.002)

= $1,837,465

Std. Dev. = .0225*71,640,000*.0257

= $41,342

= e ($/THB) * ( 71,640,000THB)

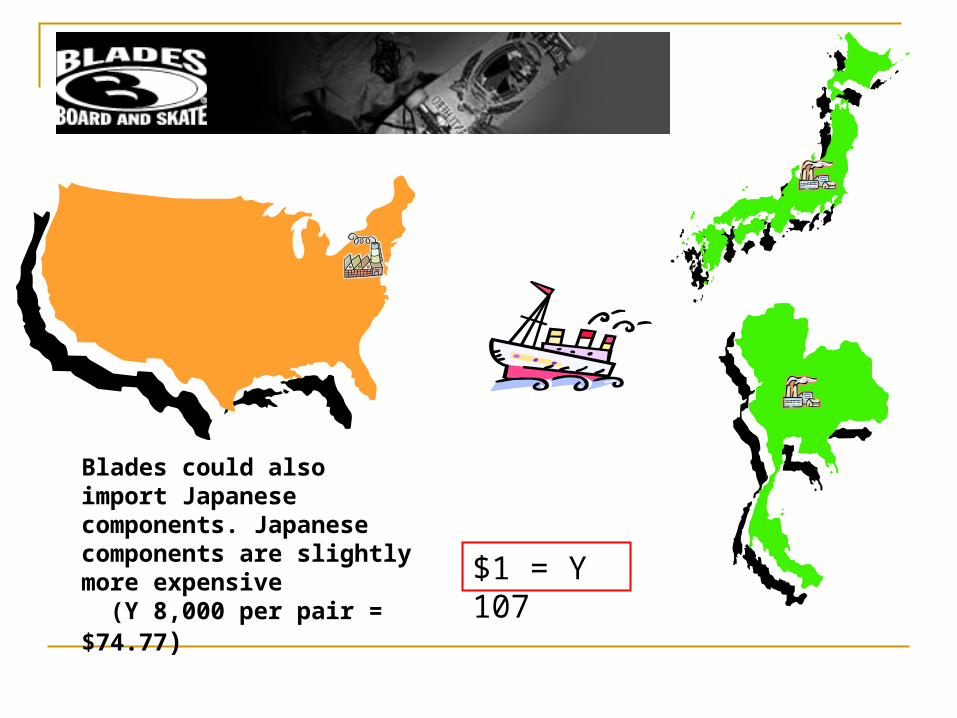

Blades could also import Japanese components. Japanese components are slightly more expensive (Y 8,000 per pair = $74.77) $1 = Y 107

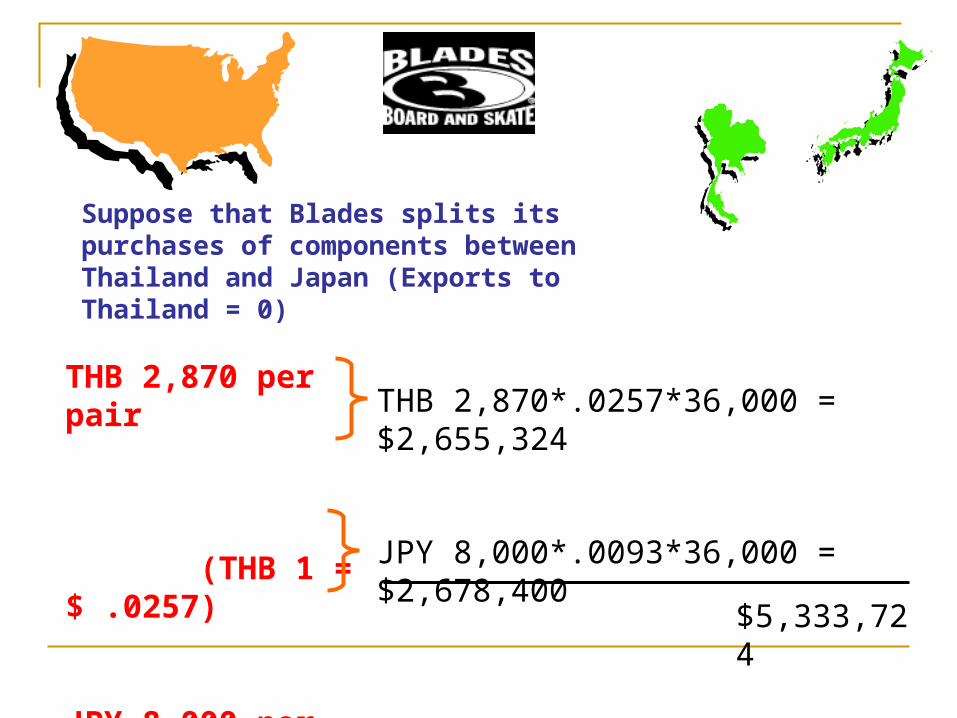

Suppose that Blades splits its purchases of components between Thailand and Japan (Exports to Thailand = 0)

THB 2,870 per pair (THB 1 = $ .0257)

JPY 8,000 per pair (JPY 1 = $ .0093)

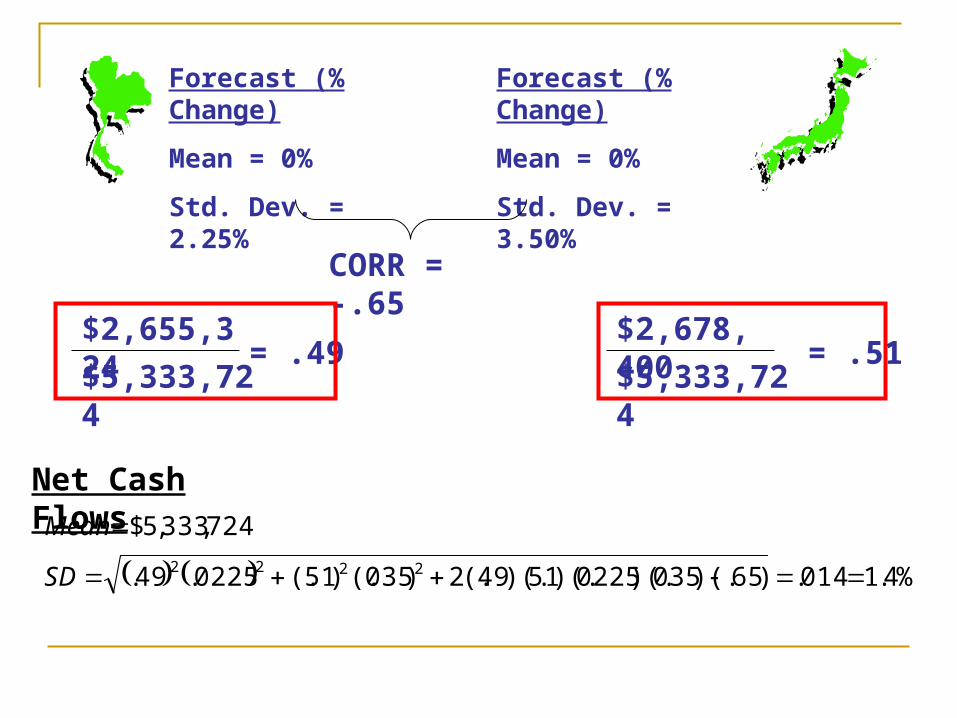

THB 2,870*.0257*36,000 = $2,655,324

JPY 8,000*.0093*36,000 = $2,678,400

$5,333,724

$2,678,400

$5,333,724

Forecast (% Change)

Mean = 0%

Std. Dev. = 2.25%

Forecast (% Change)

Mean = 0%

Std. Dev. = 3.50%

$2,655,324

$5,333,724= .49 = .51

CORR = -.65

Net Cash Flows

%4.1014.)65.)(035)(.0225)(.51)(.49(.2)035(.)51(.0225.49.

724,333,5$

2222

SD

Mean

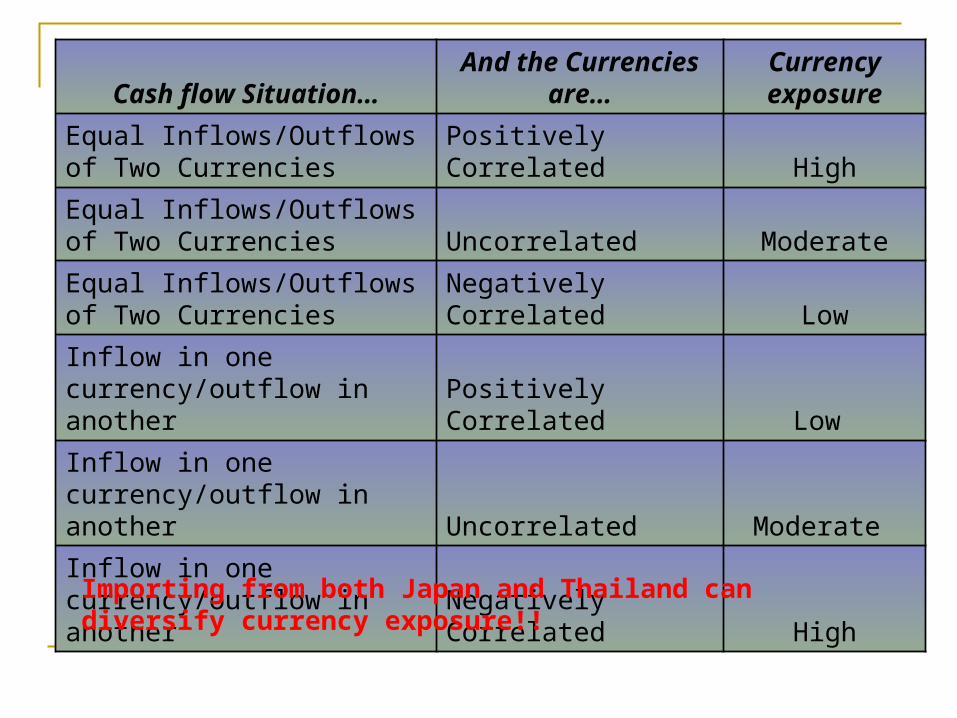

Cash flow Situation…And the Currencies

are…Currency exposure

Equal Inflows/Outflows of Two Currencies Positively Correlated High

Equal Inflows/Outflows of Two Currencies Uncorrelated Moderate

Equal Inflows/Outflows of Two Currencies Negatively Correlated Low

Inflow in one currency/outflow in another Positively Correlated Low

Inflow in one currency/outflow in another Uncorrelated Moderate

Inflow in one currency/outflow in another Negatively Correlated High

Importing from both Japan and Thailand can diversify currency exposure!!

Suppose that Blades is planning to expand sales into England. Should they try and invoice in dollars or Pounds?

Current

GBP 1 = $1.80

Forecast (% Change)

Mean = 0

SD = 2.0%

Contracting sales in GBP creates transaction exposure. However, contracting sales in USD creates economic exposure

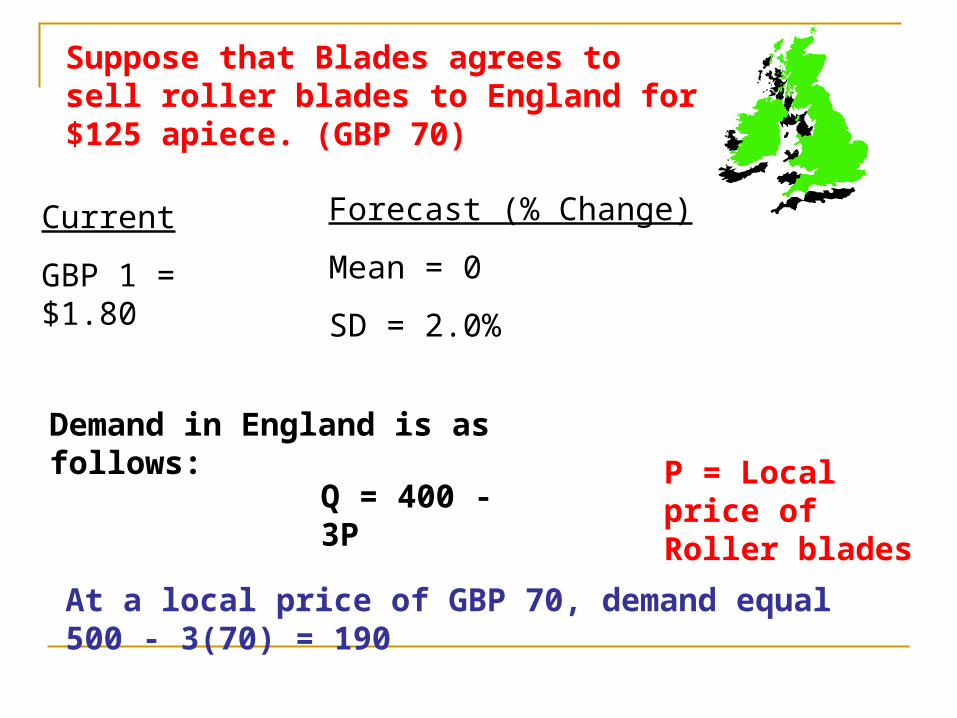

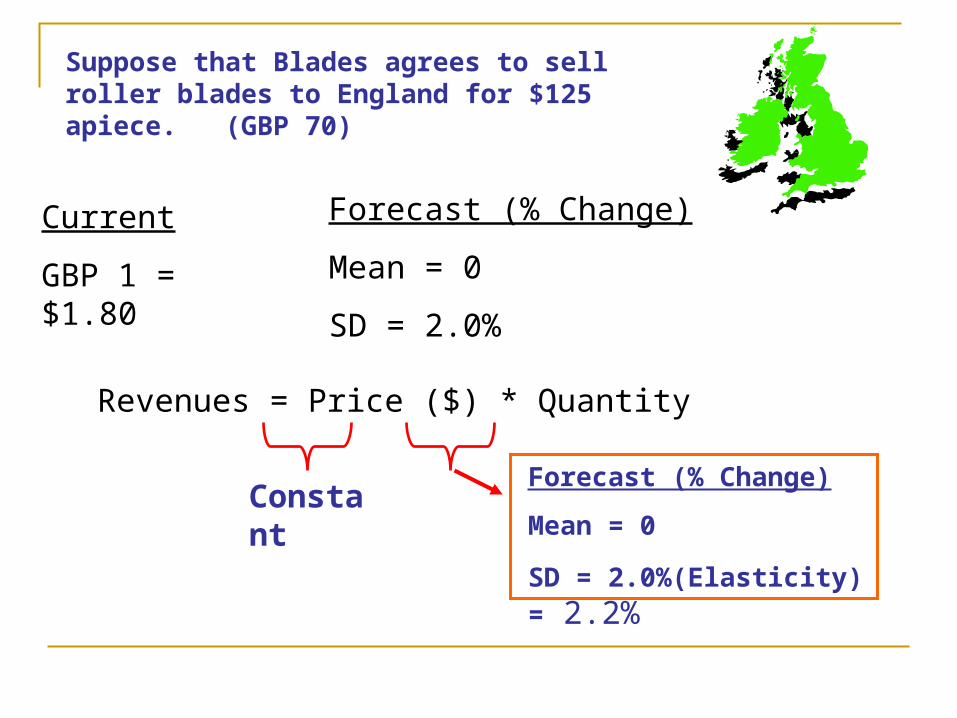

Suppose that Blades agrees to sell roller blades to England for $125 apiece. (GBP 70)

Current

GBP 1 = $1.80

Forecast (% Change)

Mean = 0

SD = 2.0%

Demand in England is as follows:

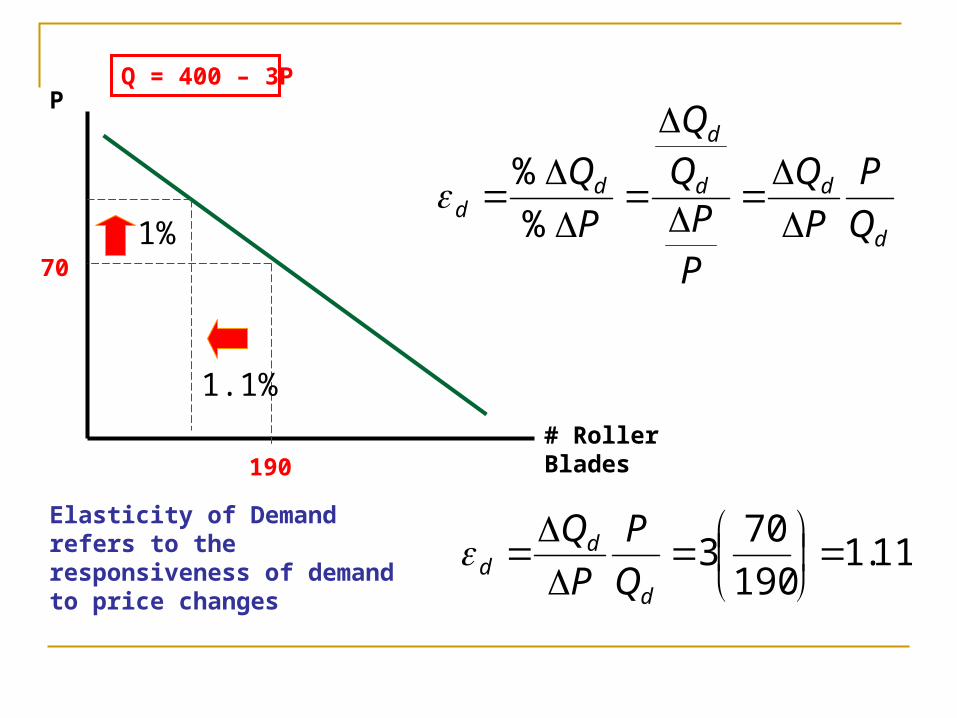

Q = 400 - 3P P = Local price of Roller blades

At a local price of GBP 70, demand equal 500 - 3(70) = 190

11.1190

703

d

dd Q

P

P

QElasticity of Demand refers to the responsiveness of demand to price changes

Q = 400 – 3P

# Roller Blades

P

190

70d

dd

d

dd Q

P

P

Q

PPQ

Q

P

Q

%

%1%

1.1%

Suppose that Blades agrees to sell roller blades to England for $125 apiece. (GBP 70)

Current

GBP 1 = $1.80

Forecast (% Change)

Mean = 0

SD = 2.0%

Revenues = Price ($) * Quantity

ConstantForecast (% Change)

Mean = 0

SD = 2.0%(Elasticity) = 2.2%

Revenues = Price ($) * Quantity

ConstantForecast (% Change)

Mean = 0

SD = 2.0%(Elasticity) = 2.2%

Revenues = e ($/L)* Price (L) * Quantity

Constant

Forecast (% Change)

Mean = 0

SD = 2.0

GBP Pricing (Transaction Exposure)

USD Pricing (Economic Exposure)

Changes in currency prices can have all kinds of economic impacts. A more general way to estimate economic exposure would be as follows:

ttt beaPCF

Percentage change in the exchange rate ($/F)

Percentage change in cash flows (measured in home currency)

Regression Results

Variable Coefficients Standard Error t Stat

Intercept .05 1.5 .03

% Change in Exchange Rate -3.35 .97 -3.45

Regression Statistics

R Squared .63

Standard Error 1.20

Observations 1,000

tt beaPCF

Every 1% depreciation in the dollar relative to the British pound lowers cash flows from England by 3.35%

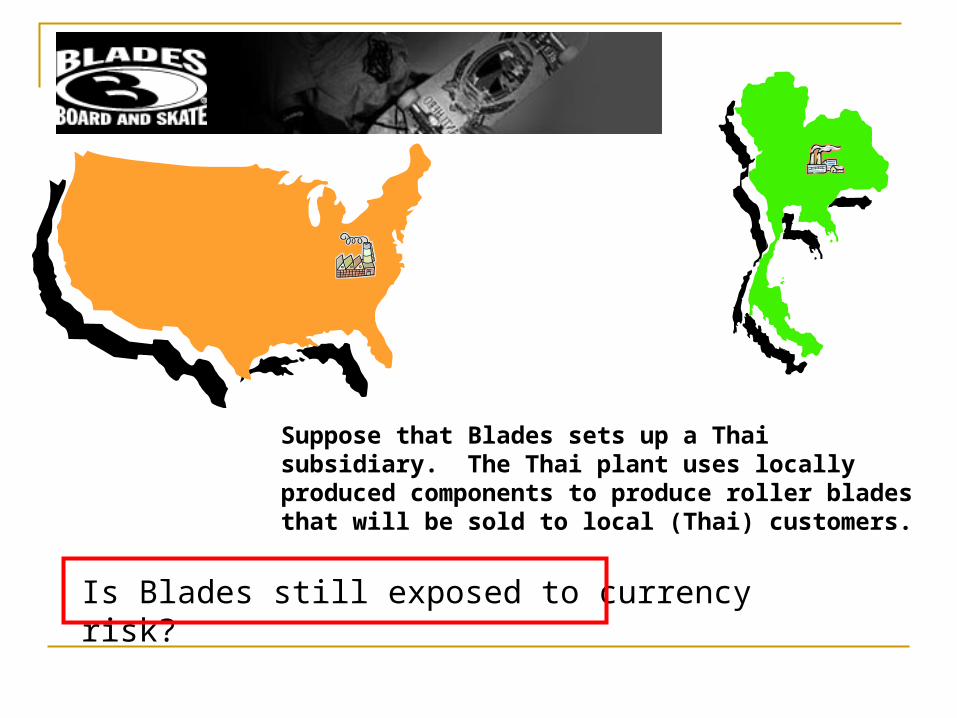

Suppose that Blades sets up a Thai subsidiary. The Thai plant uses locally produced components to produce roller blades that will be sold to local (Thai) customers.

Is Blades still exposed to currency risk?

Blades will need to produce consolidated cash flow and income statements as well as a consolidated balance sheet. Translation exposure refers to the impact of exchange rate changes on these financial statements.

FASB Rule #52 (for US Based MNCs)

The functional currency of an entity is the currency of the economic environment in which the entity operates

The current exchange rate as of the reporting date is used to translate assets/liabilities from the functional currency to the reporting currency

The weighted average exchange rate over the relevant reporting period is used to translate revenues, expenses, gains, and losses

Translated Gains/Losses are not recognized as current net income, but are reported as a second component of stockholders’ equity

Should we be worried about this type of exposure??

Related Documents