ASNP Practical Tax Considerations of Grantor v. Non-Grantor Trusts Vincent J. Russo Vincent J. Russo & Associates, PC Long Island, New York

ASNP Practical Tax Considerations of Grantor v. Non-Grantor Trusts Vincent J. Russo Vincent J. Russo & Associates, PC Long Island, New York.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ASNPPractical Tax Considerations of Grantor v. Non-Grantor Trusts

Vincent J. Russo Vincent J. Russo & Associates, PC

Long Island, New York

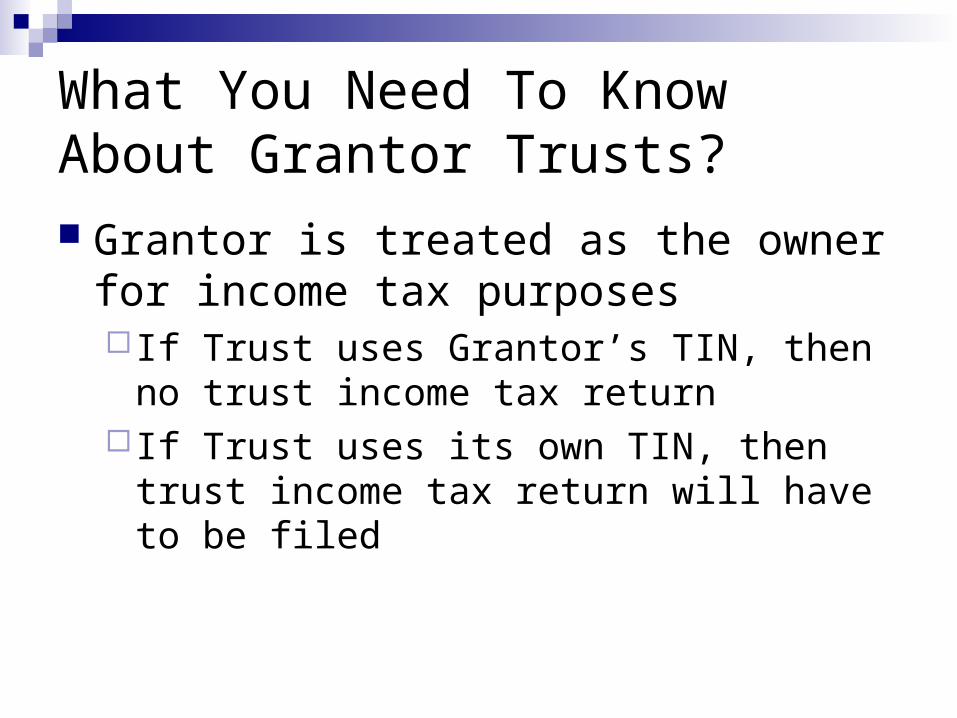

What You Need To Know About Grantor Trusts? Grantor is treated as the owner for income

tax purposes If Trust uses Grantor’s TIN, then no trust

income tax return If Trust uses its own TIN, then trust income

tax return will have to be filed

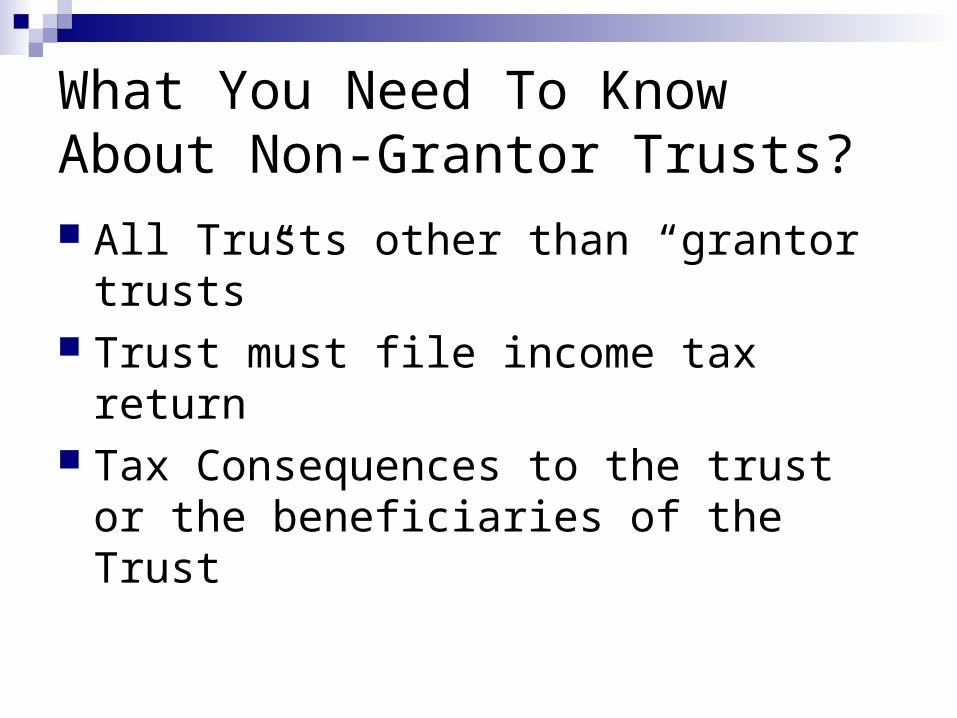

What You Need To Know About Non-Grantor Trusts? All Trusts other than “grantor trusts” Trust must file income tax return Tax Consequences to the trust or the

beneficiaries of the Trust

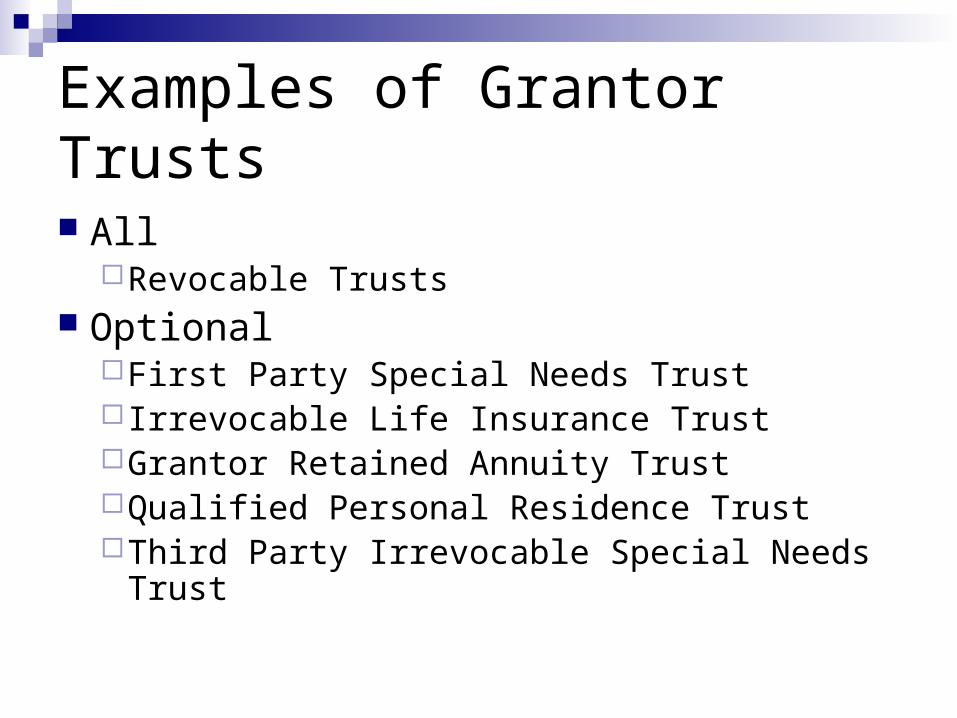

Examples of Grantor Trusts

All Revocable Trusts

Optional First Party Special Needs Trust Irrevocable Life Insurance TrustGrantor Retained Annuity TrustQualified Personal Residence TrustThird Party Irrevocable Special Needs Trust

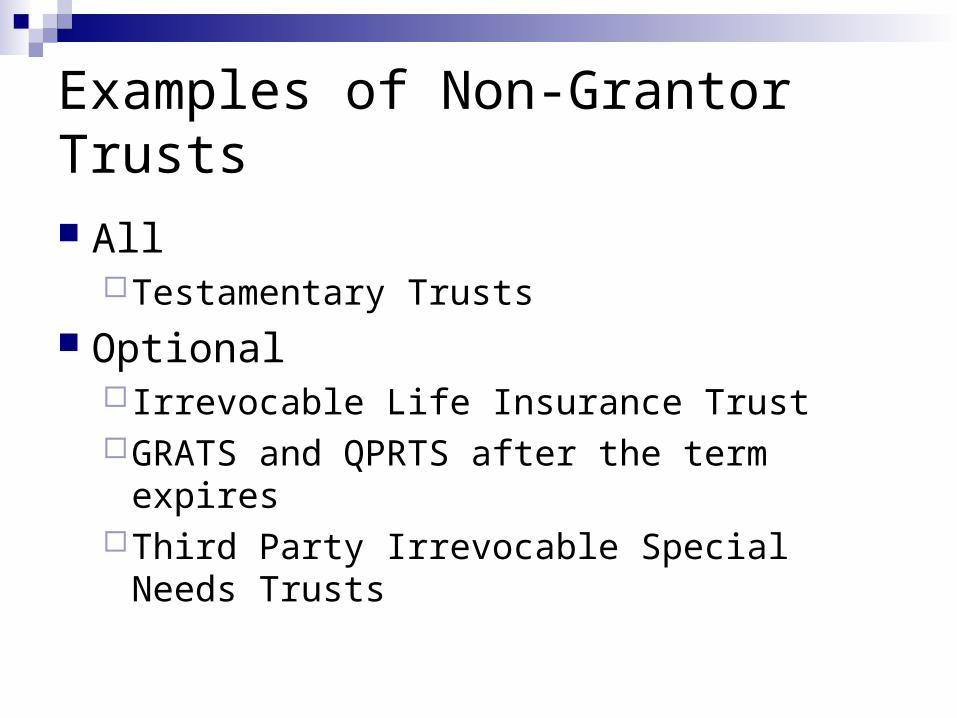

Examples of Non-Grantor Trusts

AllTestamentary Trusts

Optional Irrevocable Life Insurance TrustGRATS and QPRTS after the term expiresThird Party Irrevocable Special Needs Trusts

Advantages of a Grantor Trust

Income tax consequences stay with the grantor Beware of the exception

Lower income tax brackets than a trust Single Individual reaches 35% at $357,700 for 2008 Trust reaches 35% bracket at $10,700 for 2008

Simpler tax filings Easier to explain to the client

Advantages of a Non-Grantor Trust

Spread out the income tax consequences Grantor does not have to come up with

funds to pay tax on “phantom income” Beneficiary who receives the income pays

the income tax Qualified Disability Trust

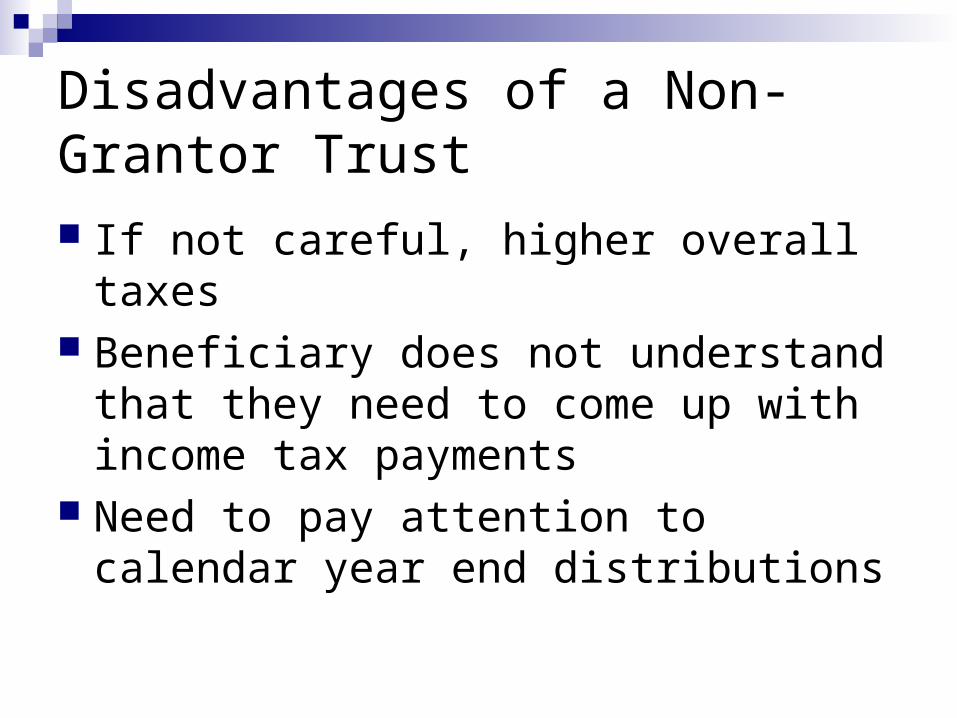

Disadvantages of a Non-Grantor Trust If not careful, higher overall taxes Beneficiary does not understand that they

need to come up with income tax payments

Need to pay attention to calendar year end distributions

First Party Special Needs Trust Set up by parent, grandparent, legal guardian or a

Court To or for the sole benefit of a person who is

disabled and under age 65 Funded with the assets of the person who is

disabled Payback required to reimburse the State for

Medicaid Paid 42 U.S.C. § 1396p (d)(4)(A)

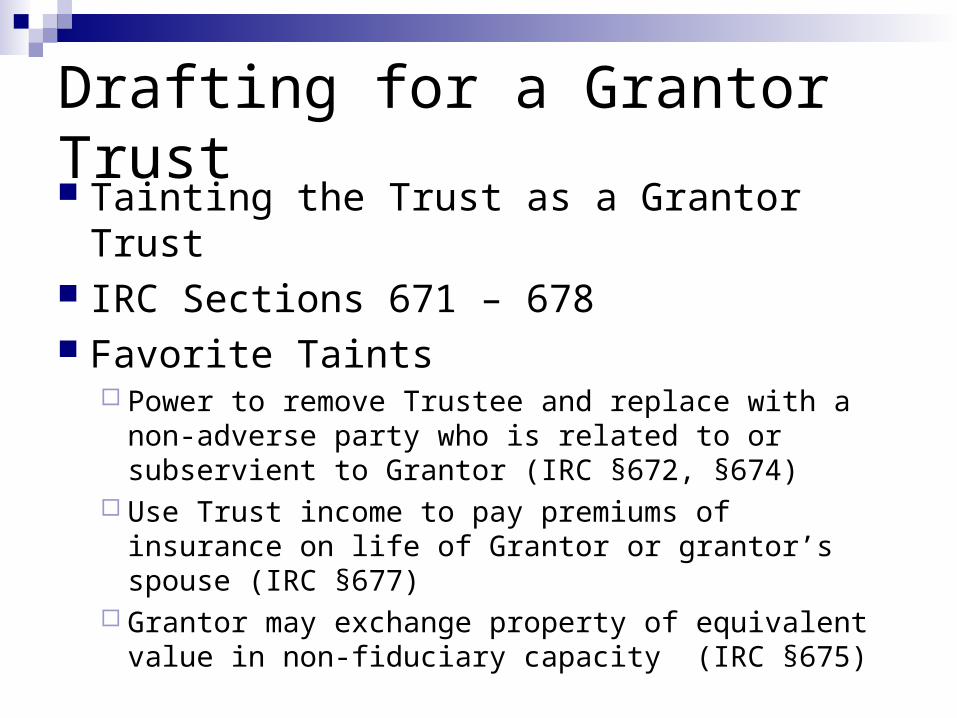

Drafting for a Grantor Trust Tainting the Trust as a Grantor Trust IRC Sections 671 – 678 Favorite Taints

Power to remove Trustee and replace with a non-adverse party who is related to or subservient to Grantor (IRC §672, §674)

Use Trust income to pay premiums of insurance on life of Grantor or grantor’s spouse (IRC §677)

Grantor may exchange property of equivalent value in non-fiduciary capacity (IRC §675)

Drafting for a Grantor Trust Grantor Trust Taints (continued)

Income payable by non-adverse party to the grantor (IRC §677)

Adverse Party - any person who has a substantial beneficial interest in the trust which would be adversely affected (IRC §672)

Taints Not To Be Used Ignore IRC §676 - Power to Revoke

i-GNORE? or eye-GNORE?

What The Grantor Needs To Know

Tax Consequences of the Trust Impact on the Grantor and Beneficiaries, if

any Filing of Tax Returns

Trust Grantor Beneficiary

Gift and Estate Tax Consequences

What the Trustee Needs To Know

Fiduciary Record Keeping Year End Income Tax Planning Filing of Tax Returns

Due April 15th (for Tax Years ended 12/31) Six-Month Extension Available

Extension of time to file (not to pay)

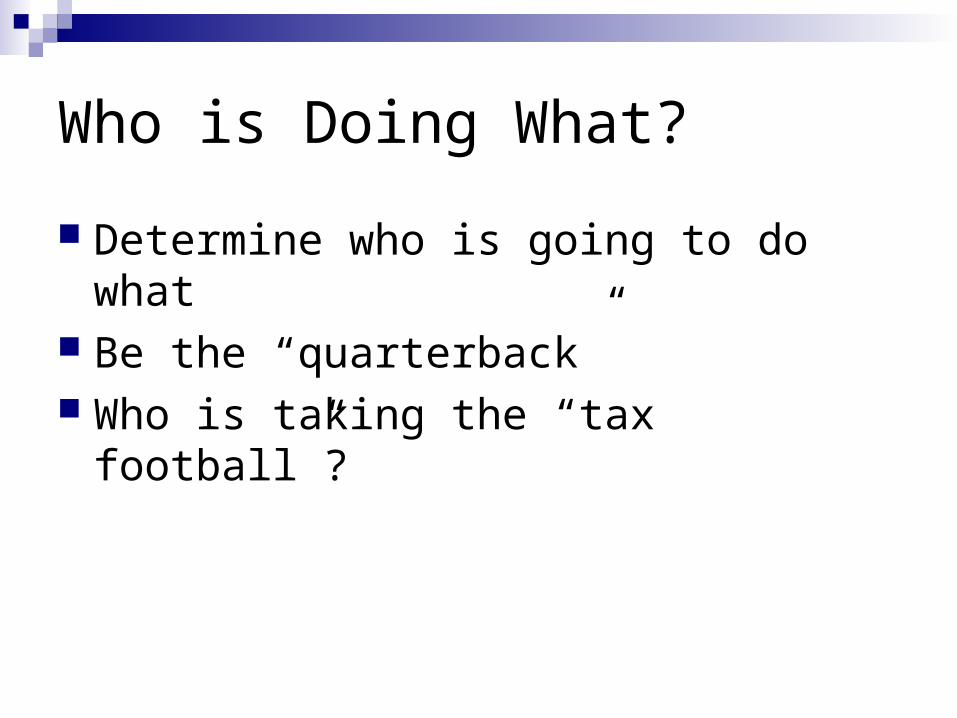

Who is Doing What?

Determine who is going to do what Be the “quarterback” Who is taking the “tax football”?

Role of Tax Practitioner

Offer tax planning strategies Keep client/attorney apprised of need for

estimated tax payments Provide list of tax related information

needed in a timely manner Prepare tax returns Manage tax deadlines

Working With The Accountant Provide the Accountant with:

Copy of Trust Instrument (or Will) Attorney Letter Summarizing Tax Treatment of Trust Necessary Information

Names, addresses and SS# of fiduciaries and beneficiaries TIN for Trust, if applicable List of Trust Assets (to know what 1099 forms, etc. to expect)

Copy of the Estate Tax Return If Trust Assets were included in Grantor’s Estate Form 706 will reflect “step-up” in basis of assets

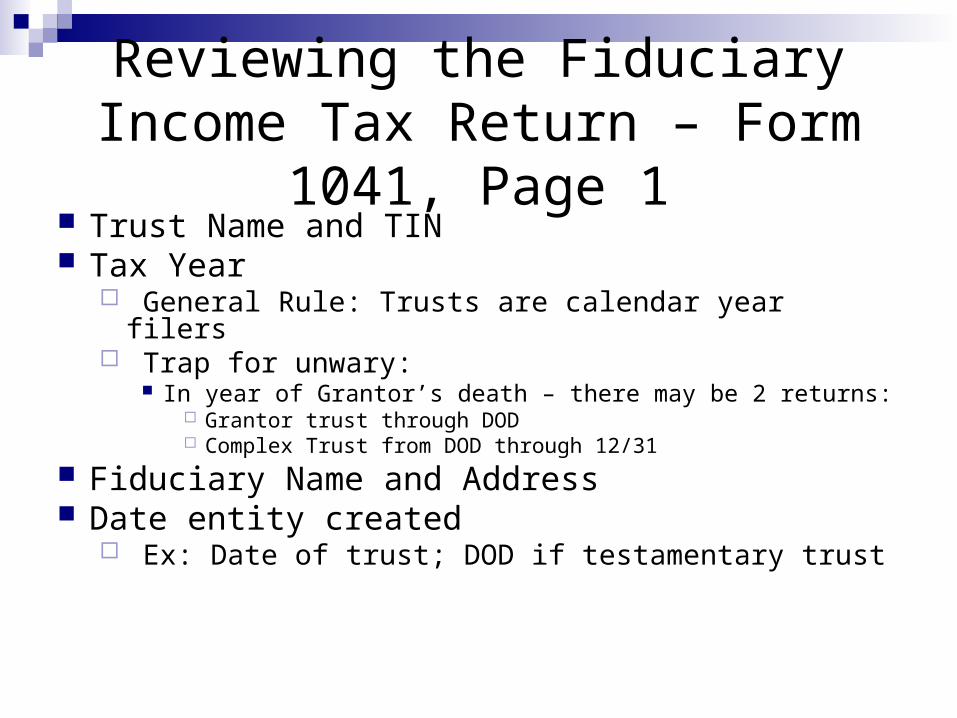

Reviewing the Fiduciary Income Tax Return – Form 1041, Page 1

Trust Name and TIN Tax Year

General Rule: Trusts are calendar year filers Trap for unwary:

In year of Grantor’s death – there may be 2 returns: Grantor trust through DOD Complex Trust from DOD through 12/31

Fiduciary Name and Address Date entity created

Ex: Date of trust; DOD if testamentary trust

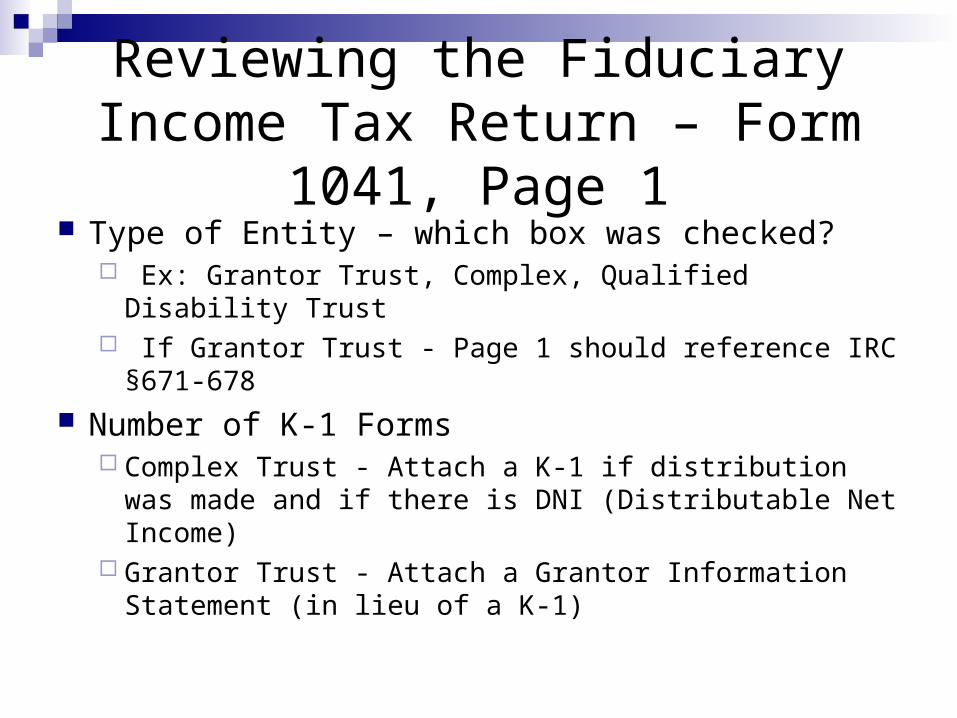

Reviewing the Fiduciary Income Tax Return – Form 1041, Page 1

Type of Entity – which box was checked? Ex: Grantor Trust, Complex, Qualified Disability Trust If Grantor Trust - Page 1 should reference IRC §671-

678

Number of K-1 Forms Complex Trust - Attach a K-1 if distribution was made

and if there is DNI (Distributable Net Income) Grantor Trust - Attach a Grantor Information

Statement (in lieu of a K-1)

Reviewing the Fiduciary Income Tax Return – Form 1041, Page 1

Checkbox for Initial Return/Final Return Checkbox - “May IRS discuss return with

preparer?” Issues to consider if attorney is not the

preparer How well do you and your client know the

preparer? What if the tax preparer contacted the IRS about

the return without your knowledge?

What to Look For When Reviewing Fiduciary Income Tax Returns

Request the Diagnostic Reports generated by the Accountant’s tax preparation software Ensure there were no “Overrides”

If found, ask preparer why the override was necessary What other areas of the return may have been affected

Was a state/local fiduciary return also prepared (if necessary) Be aware there are some differences between

Federal and State tax treatment of certain income/expense items

What to Look For When Reviewing Fiduciary Income Tax Returns

Reminder – Trust is a Cash Method Taxpayer Were all income items reported?

Any missing Bank or Brokerage accounts? Compare 1099 forms to income summary

Were all expenses taken on the return? Legal Fees Trustee Commissions Investment Advisory Fees

Knight v. Commissioner of Internal Revenue, US Supreme Court (decided 1/16/08), 2008-1 USTC ¶50,132

Real Estate Taxes if real property

What to Look For When Reviewing Fiduciary Income Tax Returns

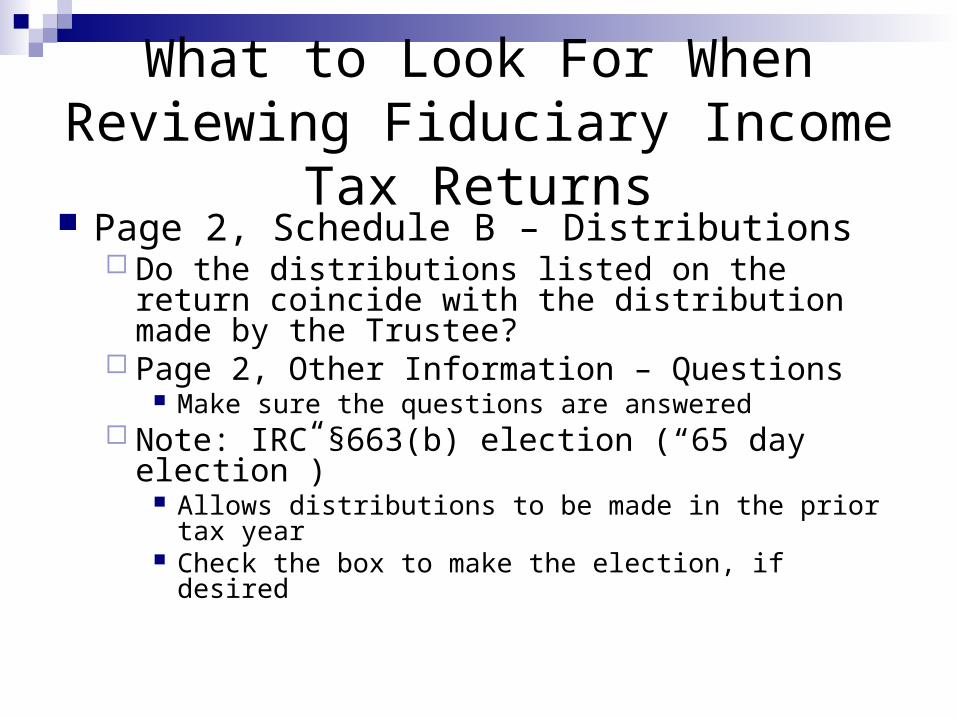

Page 2, Schedule B – Distributions Do the distributions listed on the return coincide with

the distribution made by the Trustee? Page 2, Other Information – Questions

Make sure the questions are answered Note: IRC §663(b) election (“65 day election”)

Allows distributions to be made in the prior tax year Check the box to make the election, if desired

Tax Traps (Issue Awareness)

Income Tax Brackets Kiddie Tax Estimated Tax Payments Distributable Net Income End of Tax Year Distributions State Income Tax Return Requirements Support Obligations

Tax Traps: 2008 Income Tax Brackets

Tax Estate orRate Single Married Trust10% < $8,025 < $16,050 N/A

15% $ 8,026 - $16,051 - < $2,200

32,550 65,100

25% $32,551 - $65,101 - $2,201 -

78,850 131,450 5,150

28% $ 78,851 - $131,451 - $5,151 -

164,550 200,300 7,850

33% $164,551 - $200,301 - $7,851 -

357,700 357,700 10,700

35% over $357,700 over $357,700 over $10,700

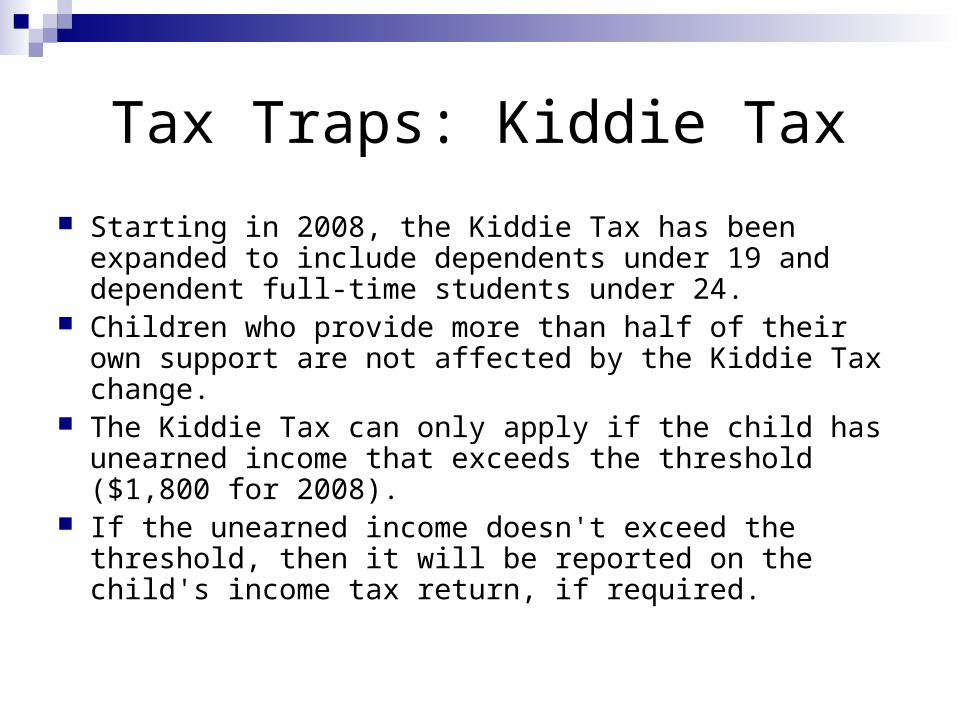

Tax Traps: Kiddie Tax

Starting in 2008, the Kiddie Tax has been expanded to include dependents under 19 and dependent full-time students under 24.

Children who provide more than half of their own support are not affected by the Kiddie Tax change.

The Kiddie Tax can only apply if the child has unearned income that exceeds the threshold ($1,800 for 2008).

If the unearned income doesn't exceed the threshold, then it will be reported on the child's income tax return, if required.

Tax Traps: Kiddie Tax

Parent can make special election to include income on their own return if: The child’s income consists entirely of interest and

dividends; The child's income does not exceed $9,000 for 2008

(Rev. Proc. 2007-66); No estimated tax payments have been made in the

name of the child; and The child is not subject to backup withholding.

Tax Traps:Trust Estimated Tax Payments

If Non-Grantor Trust Be aware of the underpayment of estimated tax

penalties Safe harbor rules

100% of prior year’s tax 110% if AGI is more than $150K

If Grantor Trust Estimates may be needed for the Grantor’s personal

income tax liability No Estimates Needed at Trust Level

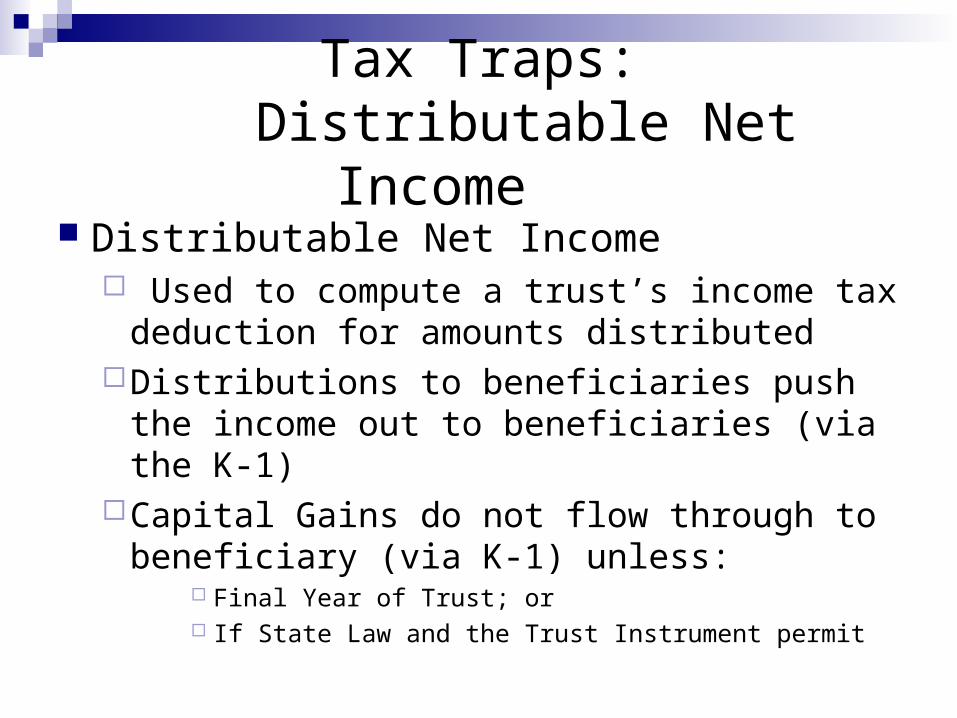

Tax Traps: Distributable Net Income

Distributable Net Income Used to compute a trust’s income tax

deduction for amounts distributedDistributions to beneficiaries push the income

out to beneficiaries (via the K-1)Capital Gains do not flow through to

beneficiary (via K-1) unless: Final Year of Trust; or If State Law and the Trust Instrument permit

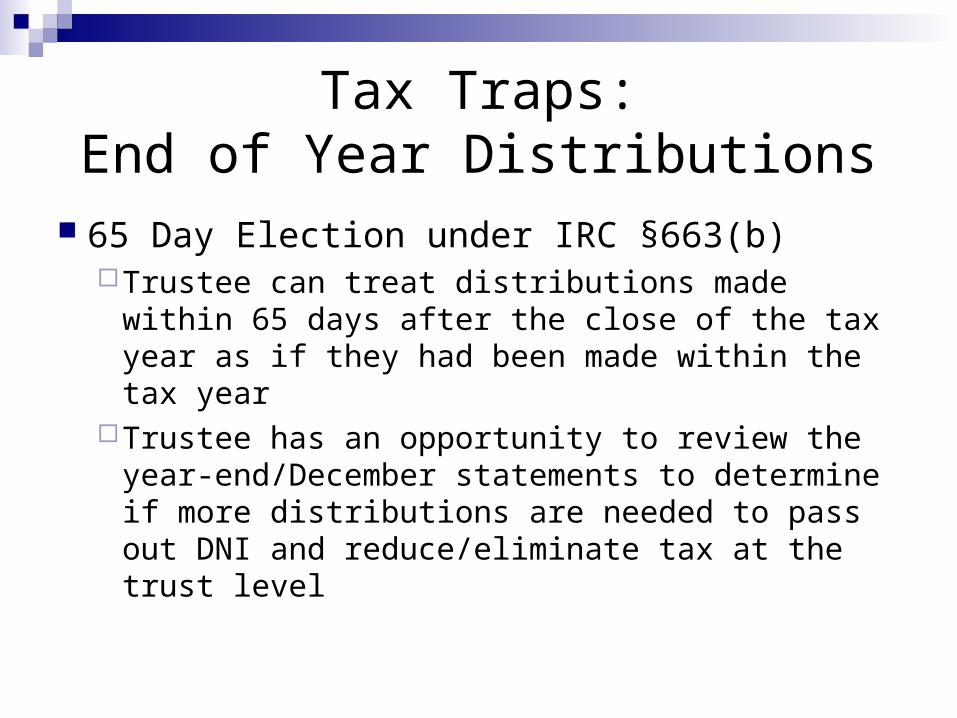

Tax Traps:End of Year Distributions

65 Day Election under IRC §663(b)Trustee can treat distributions made within 65

days after the close of the tax year as if they had been made within the tax year

Trustee has an opportunity to review the year-end/December statements to determine if more distributions are needed to pass out DNI and reduce/eliminate tax at the trust level

Tax Traps: Final Grantor Tax Returns

If Decedent is Grantor - include income from January 1st to DOD Flows through to decedent’s Final 1040

Income from DOD forward reportable on Trust’s separate 1041

IRC §645 election – can elect to treat assets held by Revocable Trust established by decedent as if they are estate’s assets – combined 1041 (for the 1st 2 years of an estate)

Tax Traps:State Income Taxes

State Income Tax Return requirements Be alert as to different tax treatment of items on State

returns Examples:

Interest on U.S. Obligations not taxed at state level Out-of-state municipal bond interest (which is not taxable

on the federal return) may be taxable on the state return There may be a tax exclusion for some pension/annuity

income/IRA distributions

Tax Traps:Support Obligations

Any amount that is used in full or in partial discharge of a legal support obligation of Child is includible in the gross income of the Parent.

The legal obligation of a parent for support is determined under local law (Reg. §1.662(a)-4).

For Example, Joan has a daughter, Annie, age 11 Joan has a legal obligation to provide support to

Annie Grandma sets up a 3rd party SNT allowing the Trustee

to access principal and/or income for the benefit of Annie.

Summary

Attorney has the power to control the tax consequences of Trusts

Determine the best tax plan for the client and his/her family

Draft Carefully Make sure that the Client’s objectives are

not derailed due to the tax drafting

ASNPPractical Tax Considerations of Grantor v. Non-Grantor Trusts

Vincent J. Russo Vincent J. Russo & Associates, PC

Long Island, New York

ASNPPractical Tax Consequences OfGrantor v. Non-Grantor Trusts

Additional Information

2008 Income Tax Brackets

Married Individuals If Taxable Income is:

Not over $16,050 $ 16,051 to $ 65,100 $ 65,101 to $131,450 $131,451 to $200,300 $200,301 to $357,700 Over $357,700

The Tax is: 10% of the taxable income $1,605 plus 15% of excess $8,962.50 plus 25% of excess $25,550 plus 28% of excess $44,828 plus 33% of excess $96,770 plus 35% of excess

2008 Income Tax Brackets

Single Individuals If Taxable Income is:

Not over $8,025 $ 8,026 to $ 32,550 $32,551 to $ 78,850 $78,851 to $164,550 $164,551 to $357,700 Over $357,700

The Tax is: 10% of the taxable income $ 802.50 plus 15% of excess $4,481.25 plus 25% of excess $16,056.25 plus 28% of excess $40,052.25 plus 33% of excess $103,791.75 plus 35% of excess

2008 Income Tax Brackets

Estates & Trusts If Taxable Income is:

Not over $ 2,200 $2,201 to $ 5,150 $5,151 to $ 7,850 $7,851 to $10,700 Over $10,700

The Tax is: 15% of the taxable income $ 330 plus 25% of excess $1,067.50 plus 28% of excess $1,823.50 plus 33% of excess $2,764 plus 35% of excess

Tax Traps: Final Income Tax Returnsof the Decedent

Can deduct Medical expenses paid within one year of death

Opportunity to elect to include accrued US Savings Bond Interest on Final 1040

RMD for IRAs must be taken by 12/31 by named beneficiary if decedent hadn’t yet taken it prior to death Affects clients who schedule “auto-withdrawals” in December or

on a monthly basis

Investment Advisory Fees

Knight v. Commissioner of Internal Revenue

US Supreme Court (decided 1/16/08)2008-1 USTC ¶50,132

Unanimous decision in favor of the Internal Revenue (written by Chief Justice Roberts). The Trustee managing the Pepperidge Farm fortune filed a tax return deducting fees paid for investment advice.

Investment Advisory Fees

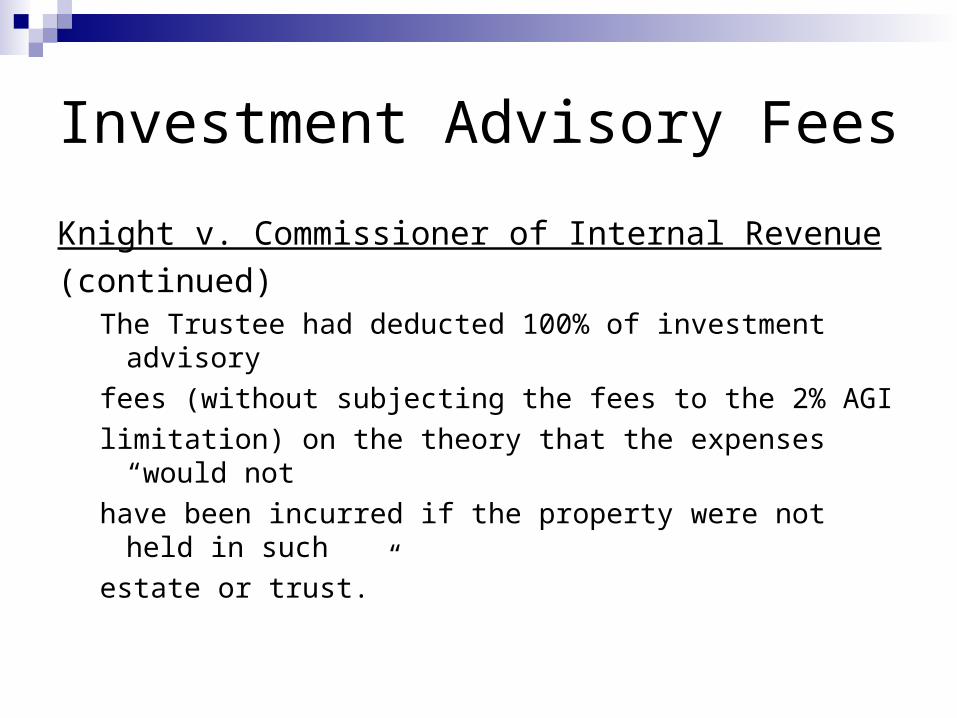

Knight v. Commissioner of Internal Revenue

(continued)The Trustee had deducted 100% of investment advisory

fees (without subjecting the fees to the 2% AGI

limitation) on the theory that the expenses “would not

have been incurred if the property were not held in such

estate or trust.”

Investment Advisory Fees

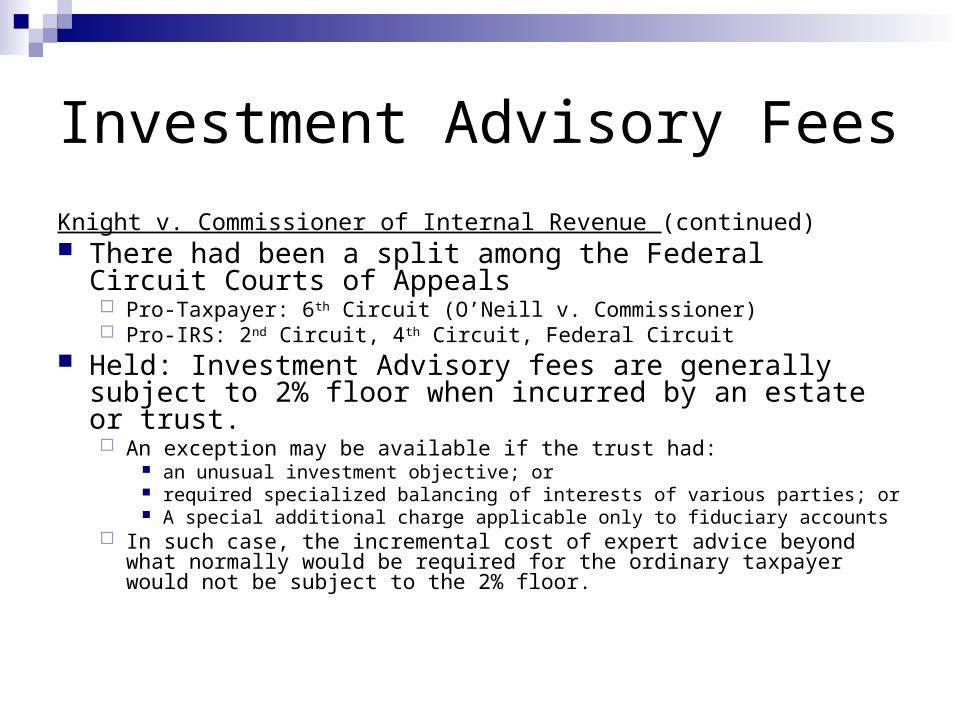

Knight v. Commissioner of Internal Revenue (continued) There had been a split among the Federal Circuit Courts

of Appeals Pro-Taxpayer: 6th Circuit (O’Neill v. Commissioner) Pro-IRS: 2nd Circuit, 4th Circuit, Federal Circuit

Held: Investment Advisory fees are generally subject to 2% floor when incurred by an estate or trust. An exception may be available if the trust had:

an unusual investment objective; or required specialized balancing of interests of various parties; or A special additional charge applicable only to fiduciary accounts

In such case, the incremental cost of expert advice beyond what normally would be required for the ordinary taxpayer would not be subject to the 2% floor.

List of Attachments

Letter to Accountant re: Special Needs Trust Grantor Trust Informational Tax Return Non-Grantor Trust Income Tax Return Knight v. Commissioner of Internal Revenue, US

Supreme Court (decided 1/16/08), 2008-1 USTC

¶50,132 US Supreme Court Decision

ASNPPractical Tax Considerations of Grantor v. Non-Grantor Trusts

Vincent J. Russo Vincent J. Russo & Associates, PC

Long Island, New York

Related Documents