Non-Traditional Actuarial Paths, Innovation and the Transformation to Digital Kevin Pledge CEO and Founder Acceptiv Inc.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Non-Traditional Actuarial Paths, Innovation and the Transformation to Digital

Kevin PledgeCEO and Founder

Acceptiv Inc.

2 22

Question

3 33

How much personal protection life insurance will be sold online 5 years from now?

0 – 9% 20 – 29% 40 – 49% 60 – 69% 80 – 89%

10 – 19% 30 – 39% 50 – 59% 70 – 79% 90 – 100%

4 44

About Me – Early Career

Actuarial Exams Several “traditional” actuarial roles,

including Chief Actuary Less traditional roles

such as compliance and marketing

“Intrepreneur”

5 55

About me – post Y2K

Entrepreneur Served on Microsoft Advisory Board Volunteered for SOA

6 66

Agenda

1. What is innovation?

2. More about me

7 77

What is Innovation?

Dr. Anjan Thakor

SOA Annual Meeting 2012, 2013

Successful Innovation

8 88

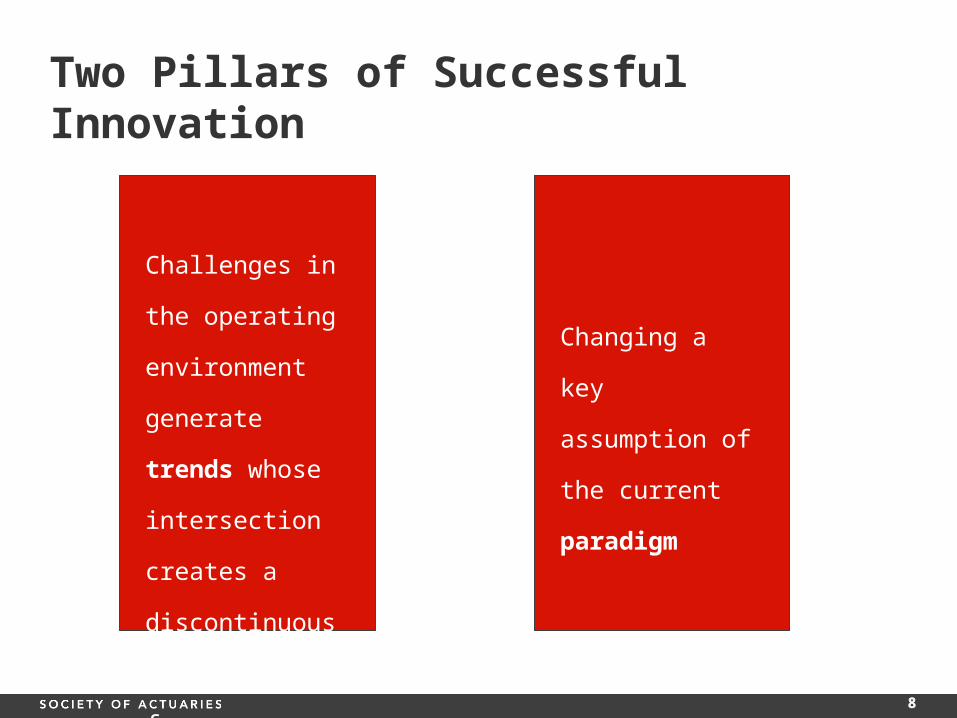

Two Pillars of Successful Innovation

Challenges in the

operating

environment

generate trends

whose intersection

creates a

discontinuous

opportunity for

innovation

Changing a key

assumption of the

current paradigm

9 99

Example Pillar 1: Intersection of Trends

1984 PC manufacturing costs

decreasing PC distribution costs level Consumer preferences

moving to cheaper PCs Working capital is

expensive due to high interest rates

Challenges in the

operating

environment

generate trends

whose intersection

creates a

discontinuous

opportunity for

innovation

10 1010

Example Pillar 2: Change paradigm

PCs must be sold through retail distribution channel to consumers

Changing a key

assumption of the

current paradigm Consumers will buy PC’s through mail order channel

11 1111

Example Pillar 1: Intersection of Trends

1985 Growing wealth and

willingness to pay for fashionable brands

More dual-career couples, more time spent at work

Growing awareness of European cappuccino culture in North America

Challenges in the

operating

environment

generate trends

whose intersection

creates a

discontinuous

opportunity for

innovation

12 1212

Example Pillar 2: Change paradigm

Coffee is a commodity that consumers will never pay a premium for

Changing a key

assumption of the

current paradigm High-quality (Arabica beans) coffee offered

close to places of work is an affordable luxury!

13 1313

What trends are affecting the insurance industry?

What paradigm can be questioned?

14 1414

What is Innovation?

Dr. Samuel Chun SOA Annual Meeting 2014Disruptive Innovation

15 1515

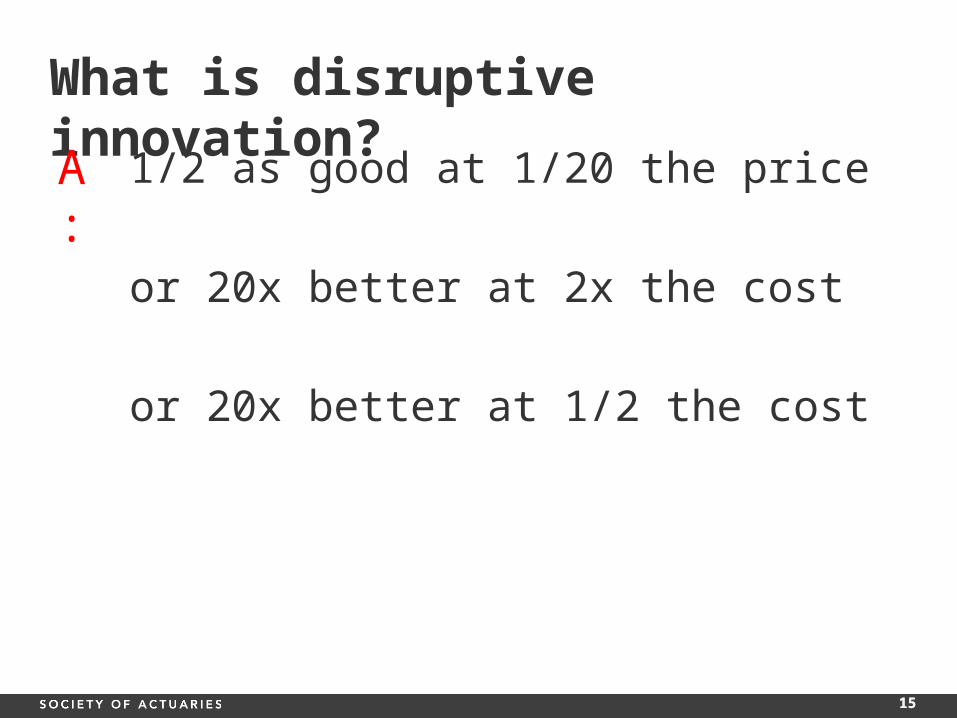

What is disruptive innovation?

1/2 as good at 1/20 the price

or 20x better at 2x the cost

or 20x better at 1/2 the cost

A:

16 1616

The problem with continuous improvement

Margin on a roll of film – a $5bn global business in 1995

Cost of Goods $0.85

Point of Sale $3.50

Price to Dealer $2.70 $0.70

$1.95

$0.85

Dealer Margin

Kodak Margin

17 1717

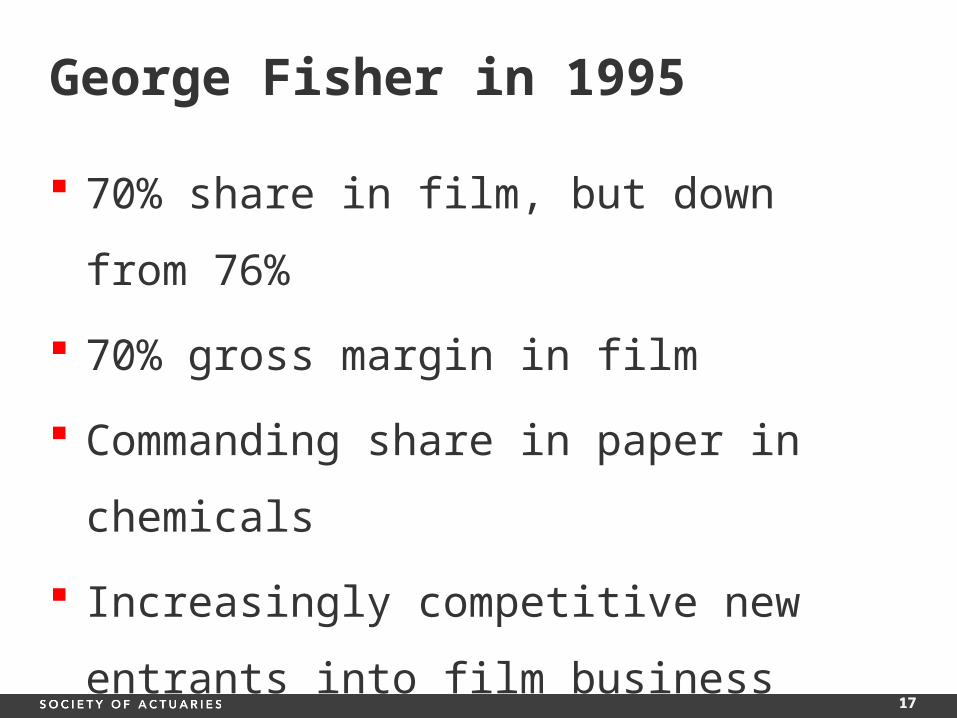

George Fisher in 1995

70% share in film, but down from 76%

70% gross margin in film

Commanding share in paper in chemicals

Increasingly competitive new entrants into

film business

18 1818

Their solution – make it better

19 1919

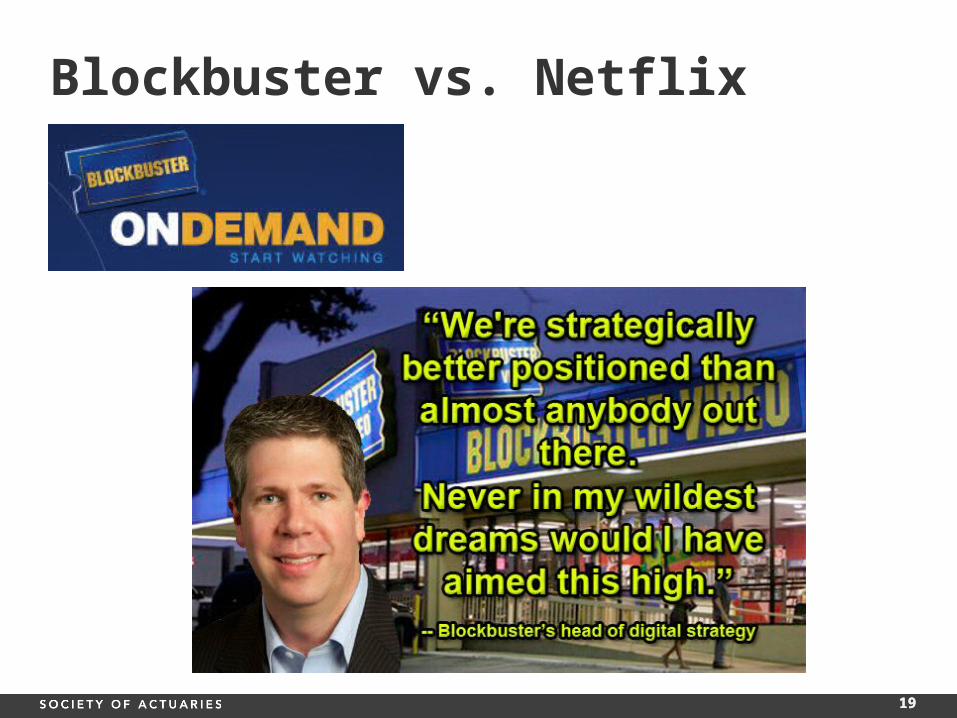

Blockbuster vs. Netflix

20 2020

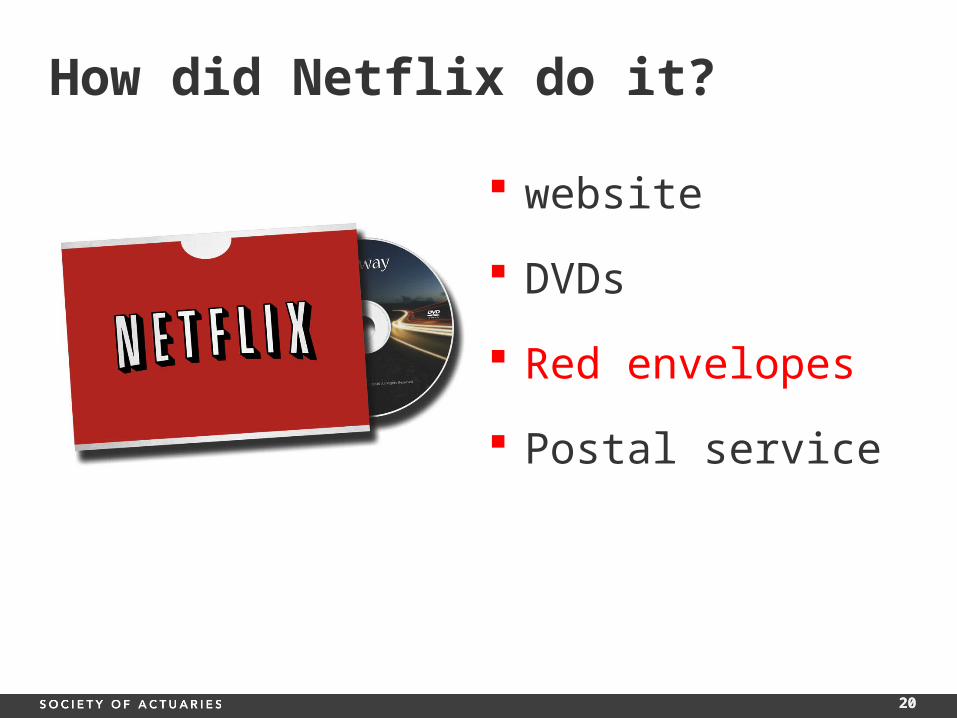

How did Netflix do it?

website

DVDs

Red envelopes

Postal service

21 2121

What makes disruptive innovation difficult

You actually have to do it

22 2222

How do you come up with this?

1. Know your customer

2. Know your value proposition(s)

3. Ask the right questionhow would I obsolete myself?

4. The go do it to yourself first

23 2323

20/20 Hindsight

24 2424

"I know it when I see it.” Supreme Court Justice Potter Stewart

25 2525

Innovation?

26 2626

http://youtu.be/NugRZGDbPFU

27 2727

Steven Johnson

Ideas can take a while to form Often lots of small ideas make up a big

idea Sum of the whole is greater than the parts

28 2828

Founding a company based on great idea

Founded in 2000 based on project I had led at Foresters

Cheaper data management and reporting Several components made this possible,

but the value of the whole was greater than the individual parts

29 2929

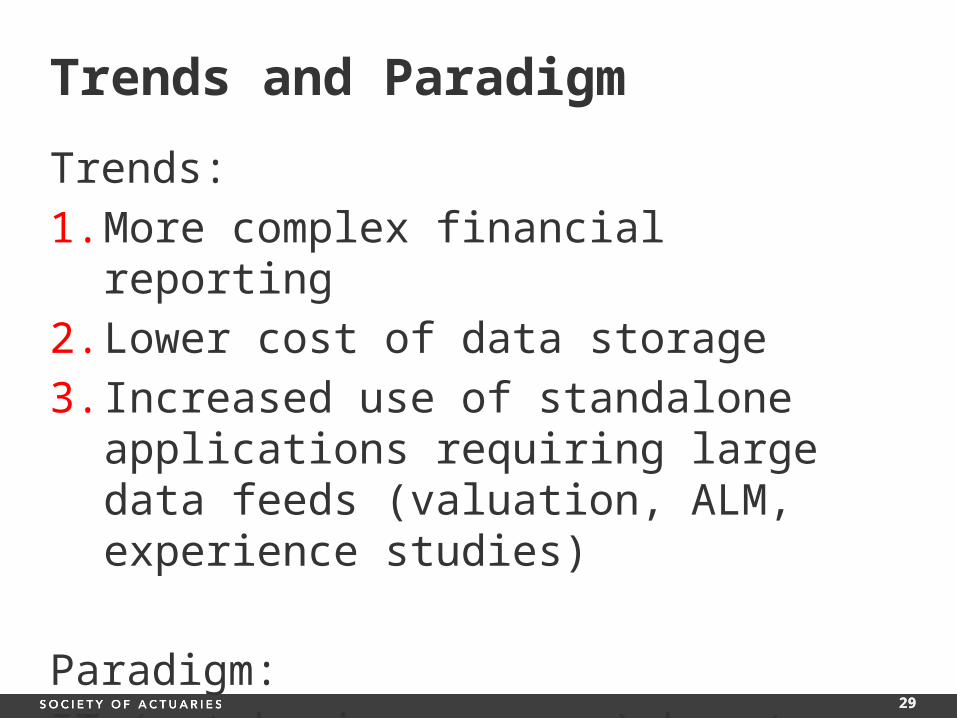

Trends and Paradigm

Trends:

1. More complex financial reporting

2. Lower cost of data storage

3. Increased use of standalone applications requiring large data feeds (valuation, ALM, experience studies)

Paradigm:

IT (not business areas) has to manage data

30 3030

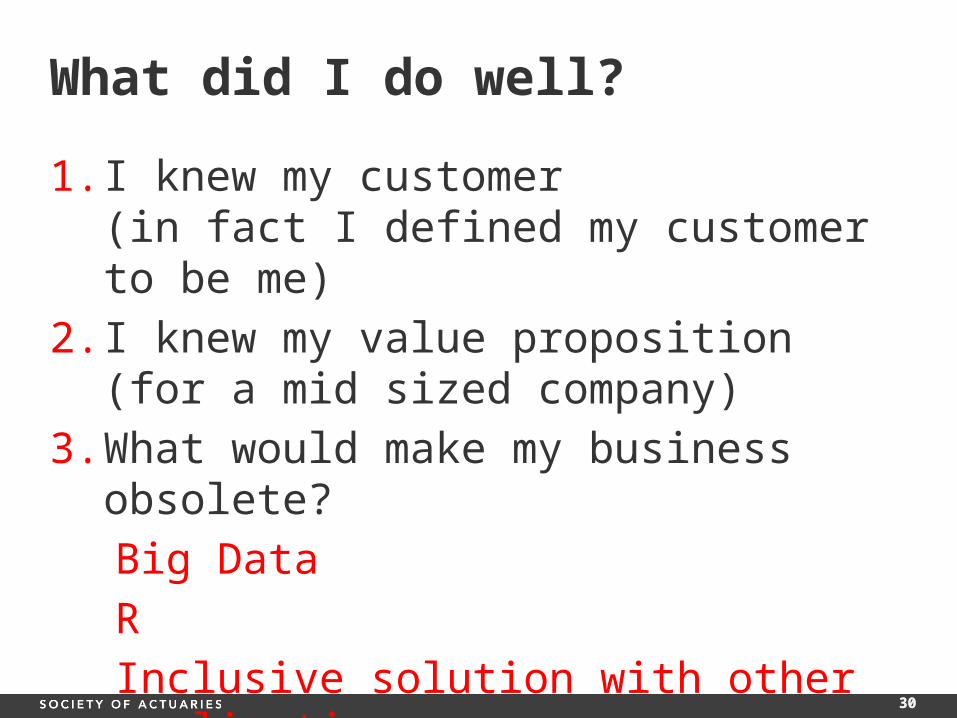

What did I do well?

1. I knew my customer(in fact I defined my customer to be me)

2. I knew my value proposition (for a mid sized company)

3. What would make my business obsolete?

Big Data

R

Inclusive solution with other applications

4. BUT we didn’t do it – why not?

31 3131

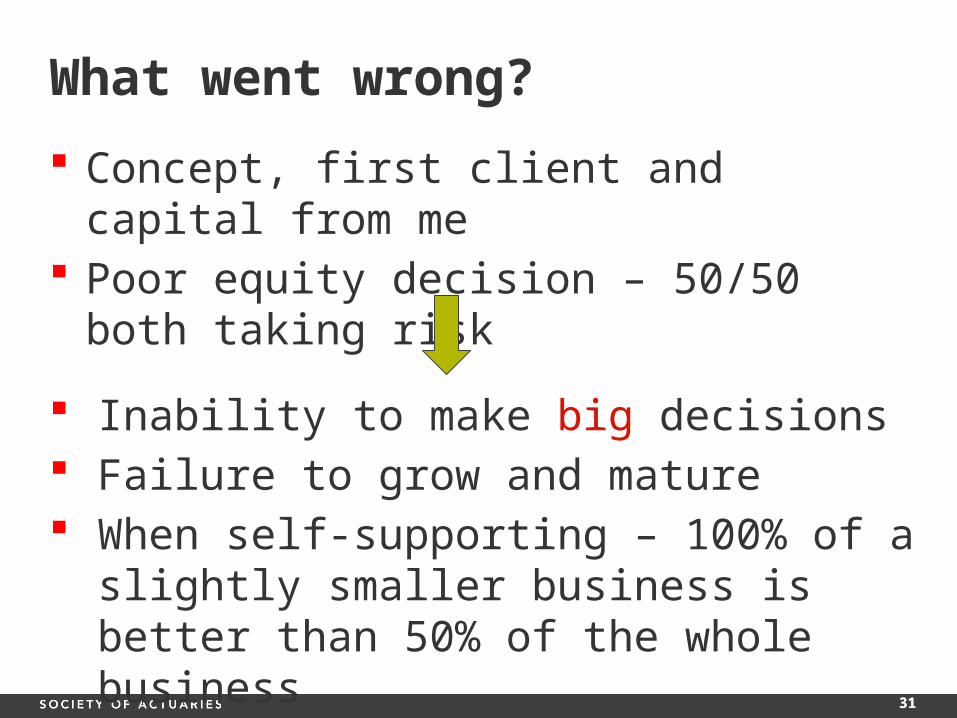

What went wrong?

Concept, first client and capital from me Poor equity decision – 50/50 both taking

risk

Inability to make big decisions Failure to grow and mature When self-supporting – 100% of a slightly

smaller business is better than 50% of the whole business

32 3232

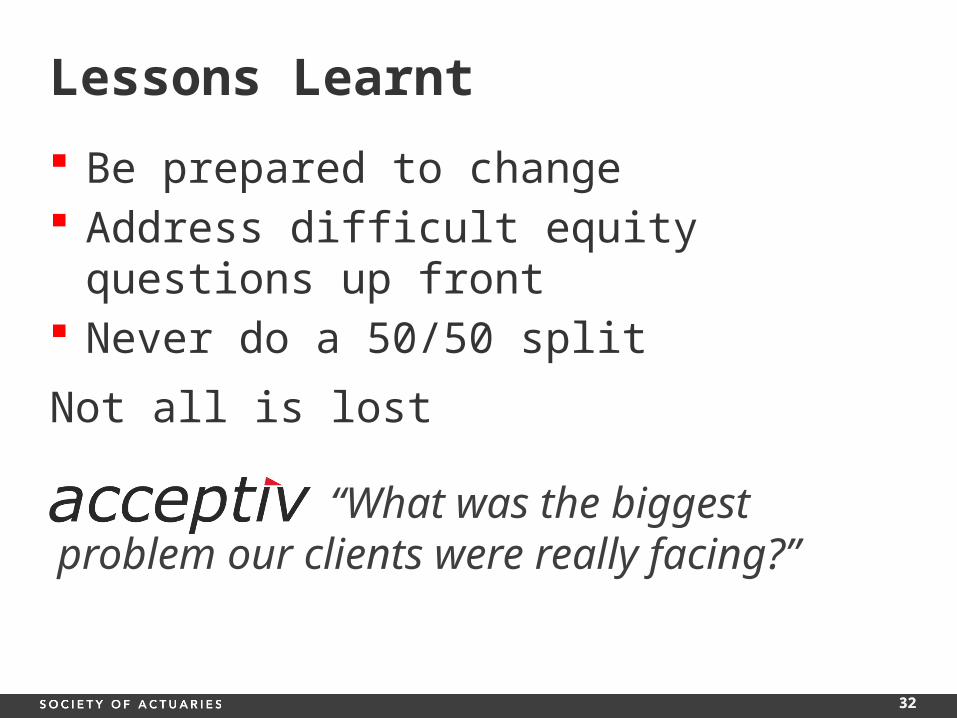

Lessons Learnt

Be prepared to change Address difficult equity questions up front Never do a 50/50 split

Not all is lost

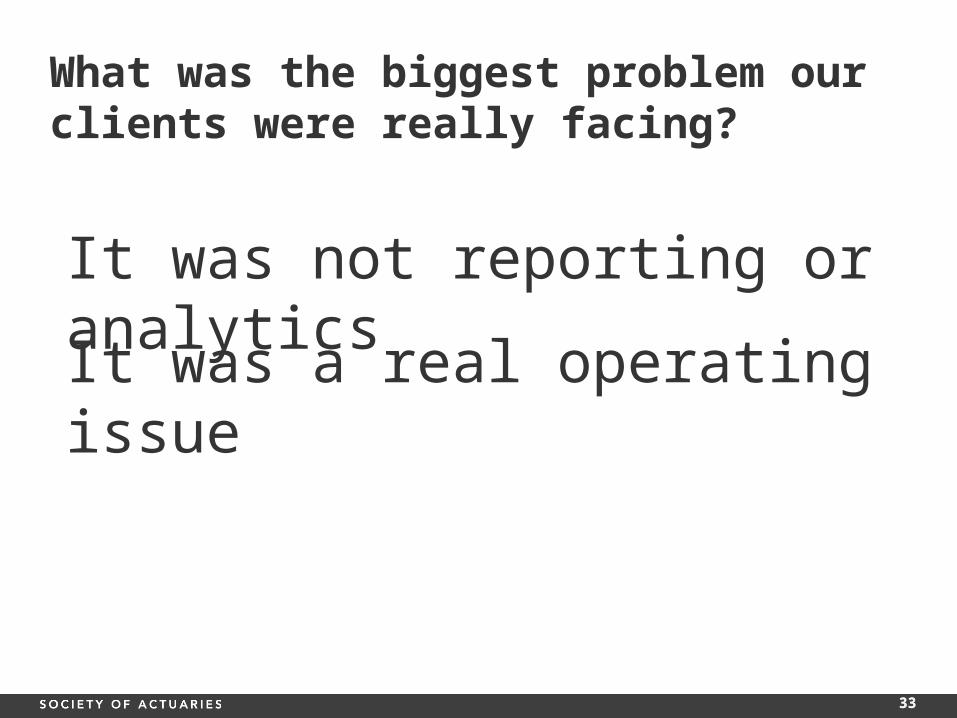

“What was the biggest problem our clients were really facing?”

33 3333

It was not reporting or analytics

What was the biggest problem our clients were really facing?

It was a real operating issue

34 3434

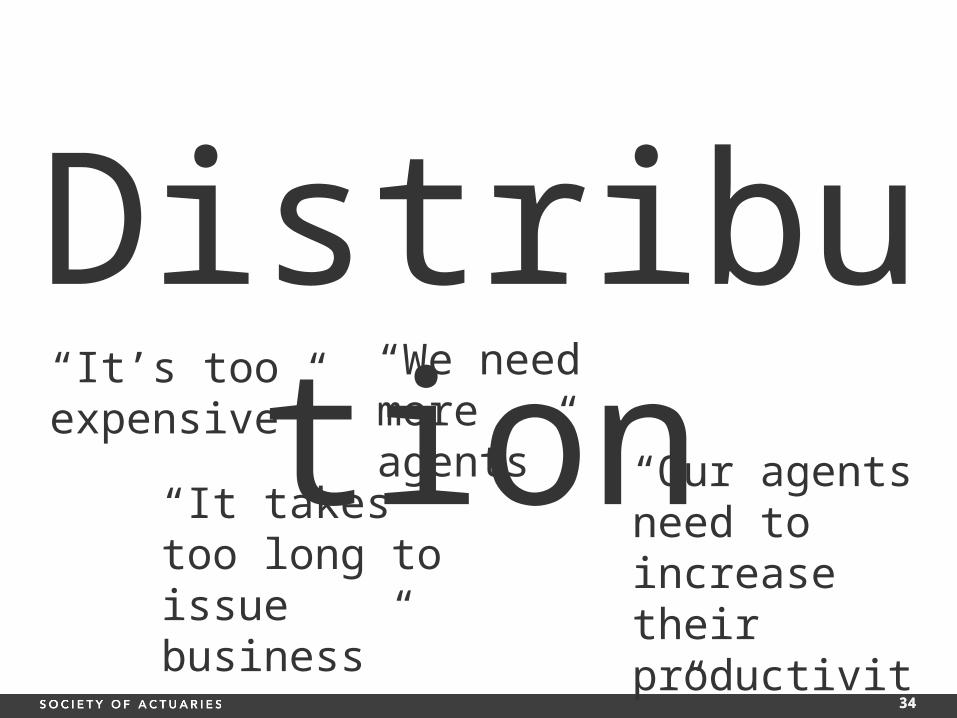

Distribution“It takes too long to issue business”

“It’s too expensive”

“Our agents need to increase their productivity”

“We need more agents”

35 3535

These questions…

Are based on the current paradigm Look for an incremental improvement From the perspective of the current

incumbent – the agent

Time for a fresh look at this…let’s look at it from the perspective of the customer

36 3636

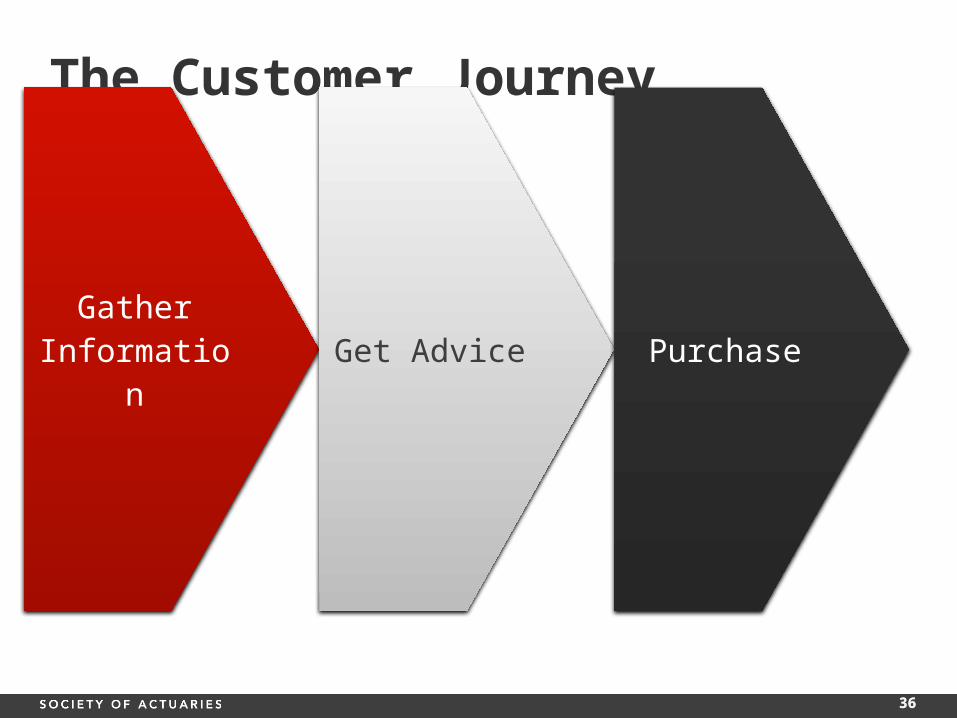

The Customer Journey

Gather Information Get Advice Purchase

37 3737

Where do you go for information?

Gather Information

38 3838

Get Advice

Where do you go for advice?

Get Advice

39 3939

Get Advice

Where do you go for advice?

Get Advice

40 4040

Get Advice

Where do you go for advice?

Get Advice

41 4141

Should you pay more to purchase online?

Purchase

42 4242

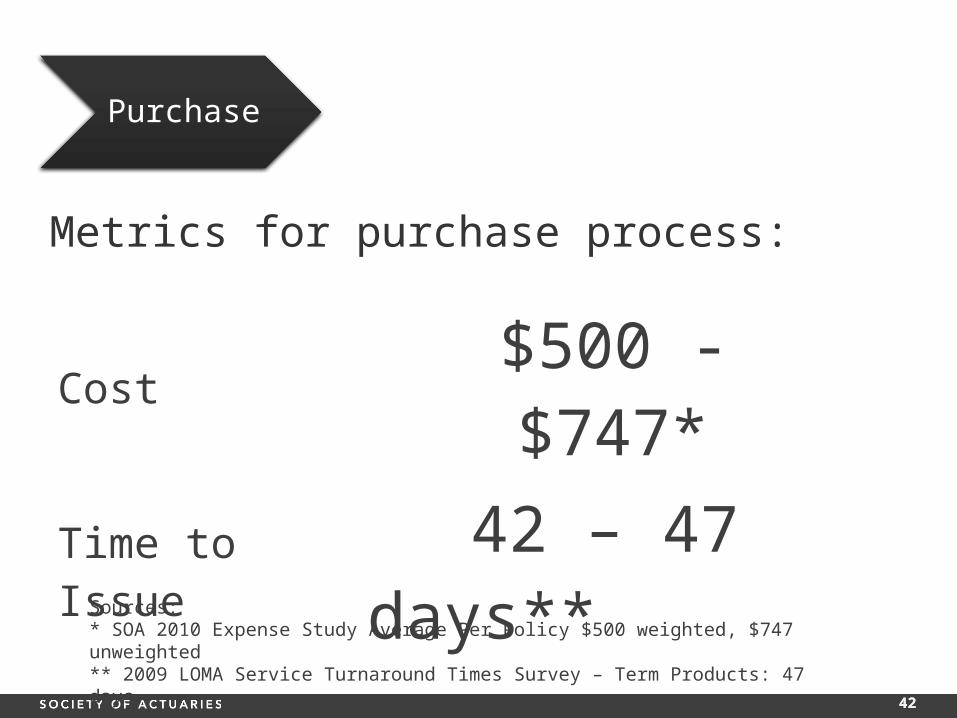

Metrics for purchase process:

Purchase

Cost $500 - $747*

Time to Issue 42 – 47 days**

Sources: * SOA 2010 Expense Study Average Per Policy $500 weighted, $747 unweighted** 2009 LOMA Service Turnaround Times Survey – Term Products: 47 days

43 4343

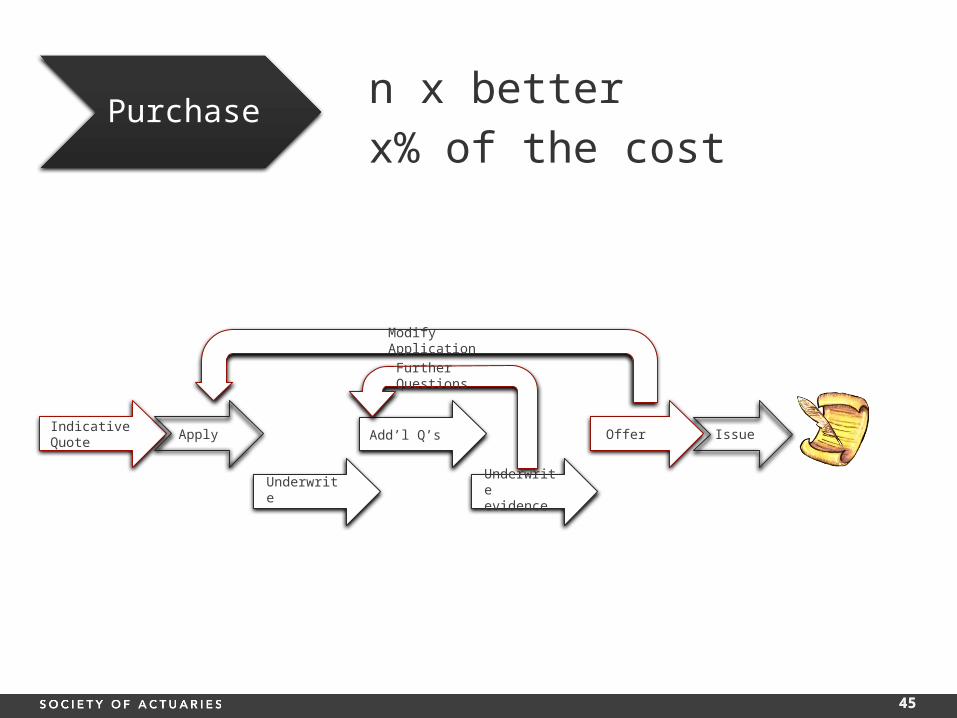

Indicative Quote

Underwrite

IssueOfferAdd’l Q’s

Modify Application

Apply

Underwrite evidence

Further Questions

Purchase

How is this possible?

44 4444

A recent announcement…

minutes not days

Is this innovation?Purchase

45 4545

Indicative Quote

Underwrite

IssueOfferAdd’l Q’s

Modify Application

Apply

Underwrite evidence

Further Questions

Purchasen x better

x% of the cost

46 4646

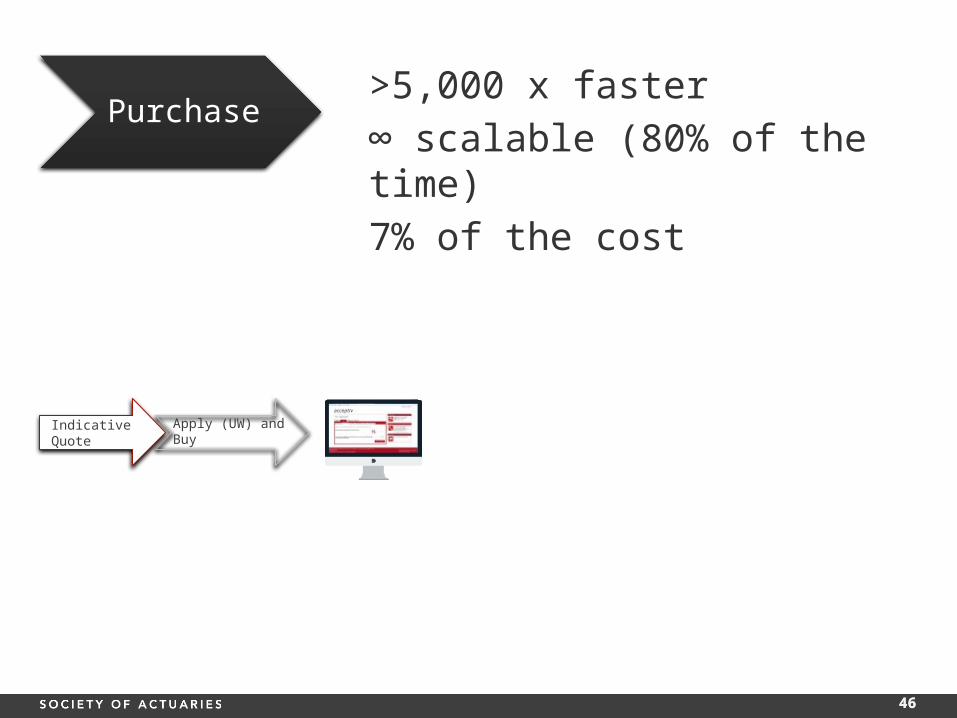

Purchase

Indicative Quote

Apply (UW) and Buy

>5,000 x faster

∞ scalable (80% of the time)

7% of the cost

47 4747

Desire to issue business faster Increasing cost to issue business Increase in online shopping Aging distribution force

Life insurance is sold not bought

Life insurance can be bought and does not need advice

Challenges in

the operating

environment

generate trends

whose

intersection

creates a

discontinuous

opportunity for

innovationChanging a key

assumption of

the current

paradigm

48 4848

How is this working?

49 4949

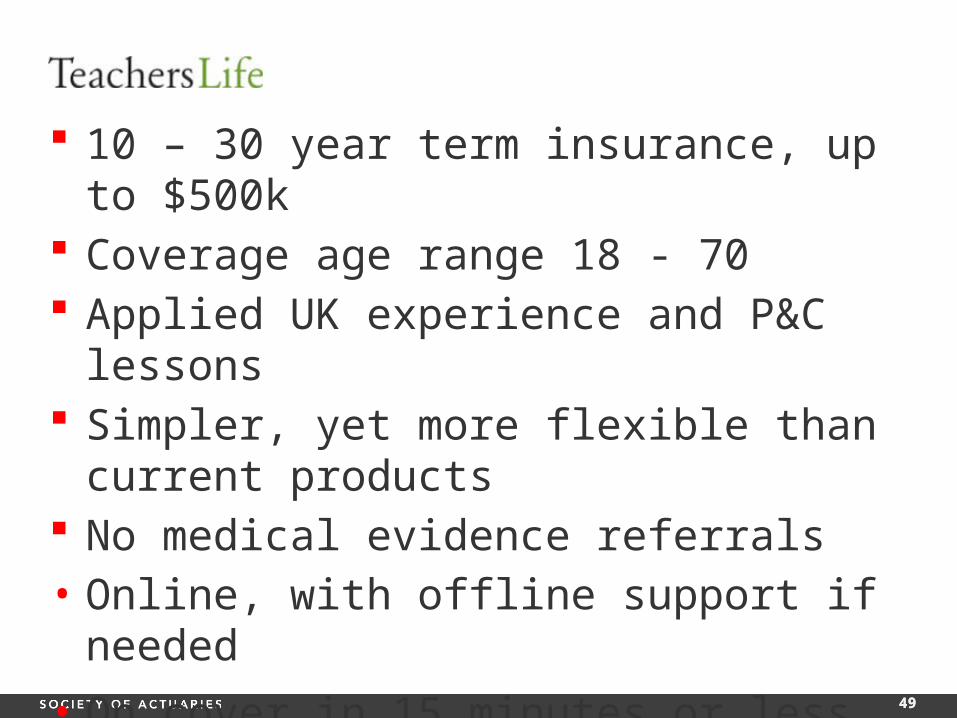

10 – 30 year term insurance, up to $500k Coverage age range 18 - 70 Applied UK experience and P&C lessons Simpler, yet more flexible than current

products No medical evidence referrals• Online, with offline support if needed

• On cover in 15 minutes or less

Full UW + Lower cost = Lower premium

50 5050

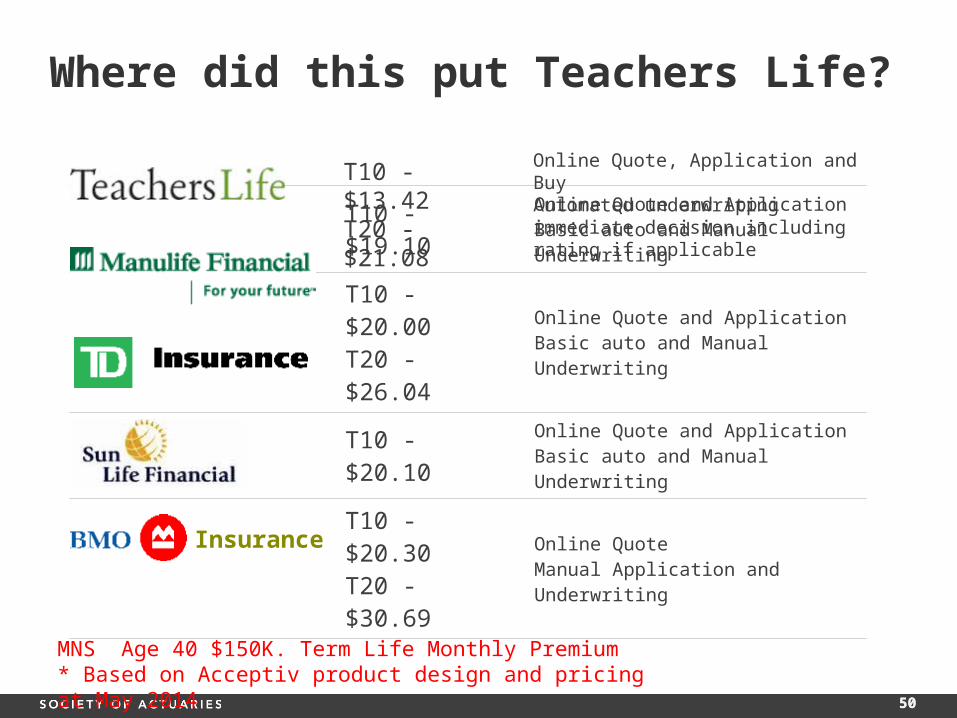

T10 - $19.10Online Quote and ApplicationBasic auto and Manual Underwriting

T10 - $20.00T20 - $26.04

Online Quote and ApplicationBasic auto and Manual Underwriting

T10 - $20.10Online Quote and ApplicationBasic auto and Manual Underwriting

T10 - $20.30T20 - $30.69

Online QuoteManual Application and Underwriting

Where did this put Teachers Life?

MNS Age 40 $150K. Term Life Monthly Premium* Based on Acceptiv product design and pricing at May 2014

Insurance

T10 - $13.42T20 - $21.08

Online Quote, Application and BuyAutomated underwriting immediate decision including rating if applicable

51 5151

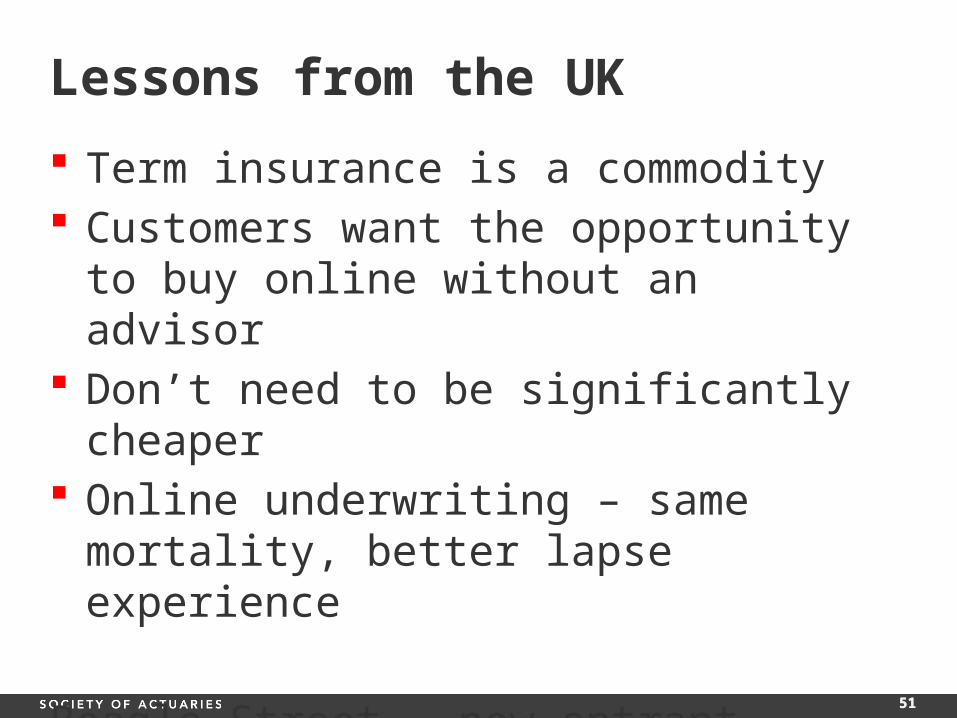

Lessons from the UK

Term insurance is a commodity Customers want the opportunity to buy

online without an advisor Don’t need to be significantly cheaper Online underwriting – same mortality,

better lapse experience

Beagle Street – new entrant launched in 2012 (not really a life insurance company)

52 5252

http://youtu.be/HWF09ya1o5I

Related Documents