Crawford School Dialogue Asia’s Economic Transformation: Implications for Australia Presented by the Arndt-Corden Department of Economics and the Crawford School Tuesday, 12 March, 2011 Weston Theatre, J G Crawford Building 132, Lennox Crossing, ANU

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Crawford School Dialogue

Asia’s Economic Transformation:Implications for AustraliaPresented by the Arndt-Corden Department of Economics and the Crawford School

Tuesday, 12 March, 2011 Weston Theatre, J G Crawford Building 132, Lennox Crossing, ANU

Crawford School Dialogue

Indonesia Presented by Ross H. McLeod, Arndt-Corden Department of Economics

Tuesday, 12 March, 2011 Weston Theatre, J G Crawford Building 132, Lennox Crossing, ANU

One of very few countries not to suffer a severe decline in growth as a result of the GFC• GDP growth rate remained above 4% p.a. (mid-2009)• Recovered to 6.9% by the end of 2010

– Driven mainly by private investment: business confidence high– On supply side, growth is most rapid in services, especially

wholesale/retail trade, hotels and restaurants• Inflation around 7%, c.f. target range 4-6%

– Reflects central bank unwillingness to allow Rp to appreciate• Recent surges in food prices

– Temporary removal of tariffs (rice, wheat, soybeans)– Increased imports of rice

• Financial markets– Exchange rate against $US very stable– Stock market has been booming (but recent signs of nervousness)

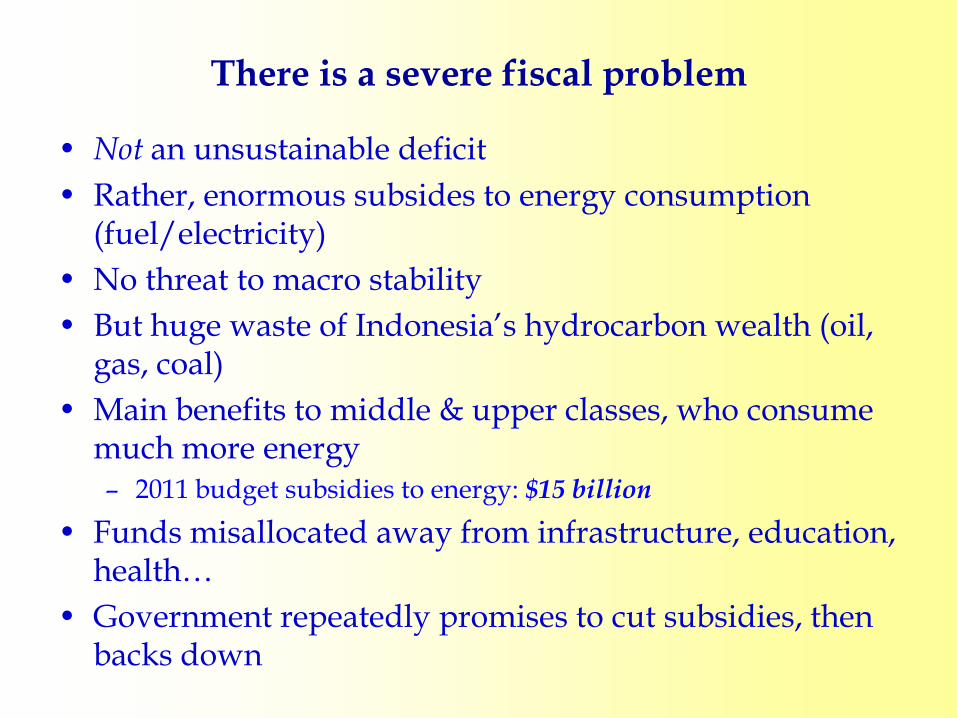

There is a severe fiscal problem

• Not an unsustainable deficit• Rather, enormous subsides to energy consumption

(fuel/electricity)• No threat to macro stability• But huge waste of Indonesia’s hydrocarbon wealth (oil,

gas, coal)• Main benefits to middle & upper classes, who consume

much more energy– 2011 budget subsidies to energy: $15 billion

• Funds misallocated away from infrastructure, education, health…

• Government repeatedly promises to cut subsidies, then backs down

Composition of exports has altered dramatically and unexpectedly over the last two decades

• Earlier high hopes for labour-intensive exports (especially textiles, clothing and footwear) have not come to fruition

• Instead, the big growth has been in coal and palm oil• Country shares of exports have been changing

significantly– Traditional export markets becoming less important– Rapid expansion into ‘new’ Asian markets

Guarding against collapse of financial sector

• Banking sector collapsed in AFC at huge cost to government (perhaps $50 billion)

• By contrast, GFC had little impact:– Only 1 (small) bank failed (Bank Century)– Cost to government ‘only’ about $700 million– But was used as a political lever to get rid of the reformist

finance minister• Reminded policymakers of earlier decision to unify

financial institution supervision in single body (FSA)• New law drafted and discussed, but not yet enacted• Draft is poor: would lead to wasteful/confusing

duplication of supervision in BI and new FSA• Unclear why it should be expected to achieve anything

Economic dynamism comes mainly from the private sector rather than the public sector • Government fails to create sufficient public

infrastructure• Less noticed: it fails to manage such infrastructure well• Both problems clearly evident in dysfunctional large

cities– Traffic congestion– Frequent flooding– Inadequate, poor quality water supply– Depletion of aquifers and consequent land subsidence– Absence of sewerage– Poor environmental quality

• Key to improvement is a shift from government financial support to charging costs to users

Corruption remains a major concern

• Plenty of evidence that the anti-corruption campaign is making little headway

• Gayus Tambunan case highlighted high level corruption in– Tax office– Police– Judiciary– Prisons– Immigration office…

• SBY’s popularity remains high, but his approval rating has fallen a great deal

Indonesia and Australia

• Not major trading partners– Australia not a large market for Indonesian exports– Australia supplies less than 5% of Indonesian imports

• Competing exporters of coal, natural gas, and certain minerals

• Not much Indonesian investment in Australia• Australia invests in mining industry and in certain

services• Indonesian legislation has not created an environment

that is truly welcoming to foreign investment• Significant trend to protectionism in relation to foreign

investment likely to constrain Australia’s role

GDP Growth (Demand side)(% p.a.)

-10

-5

0

5

10

15

20

Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10

Gross Domestic Product (GDP) Private consumptionGovernment consumption Investment

GDP Growth (Supply Side)(% p.a.)

-2

0

2

4

6

8

10

Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10

Gross Domestic Product (GDP) Manufacturing

Construction Trade, hotels & restaurants

0

2,000

4,000

6,000

8,000

10,000

12,000

0

800

1,600

2,400

3,200

4,000

4,800

9-Apr-10 9-Jun-10 9-Aug-10 9-Oct-10 9-Dec-10 9-Feb-11 9-Apr-11

Composite Stock Price Index (CSPI) and Exchange Rate

CSPIExchange rate

CSPI Rp/$

0

4

8

12

16

20

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Trends in Key Manufactured Exports(% of total exports)

Wood Manufactures Paper & Cardboard

Footwear Electrical & telecomm's

Textiles & clothing

0

5

10

15

20

25

30

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Trends in Energy Exports(% of total exports)

Oil

Gas

Coal

0

3

6

9

12

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Trends in Other Natural Resource Exports(% of total exports)

Vegetable Oil & Fats

Crude Rubber

Metalliferous Ores & Metal Scrap

Seafood

Coffee, Tea, Cocoa & Spices

0 10 20 30 40 50

Japan

USA

China

Singapore

India

Malaysia

Others

Country Shares of Indonesian Non-Oil and Gas Exports(%)

1997

2010

0

5

10

15

20

25

1998 2000 2002 2004 2006 2008

Country Shares of Non-Oil & Gas Imports(%)

China Japan USAMalaysia South Korea ThailandAustralia

Related Documents