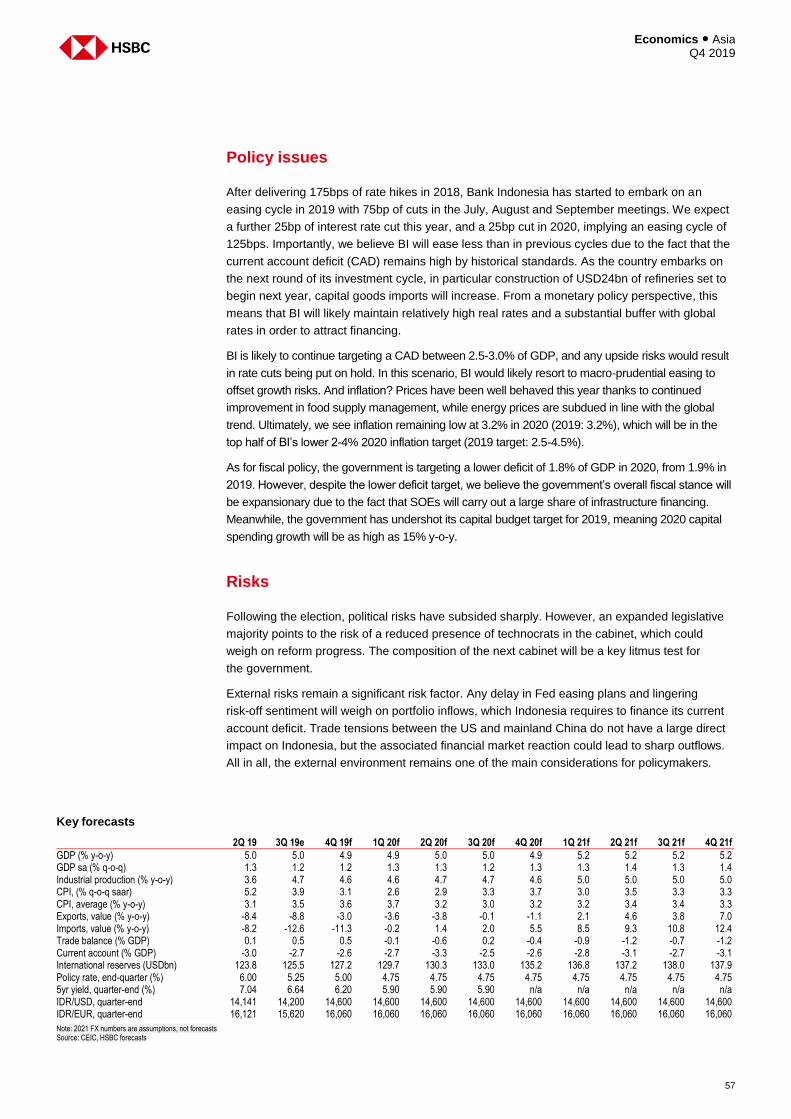

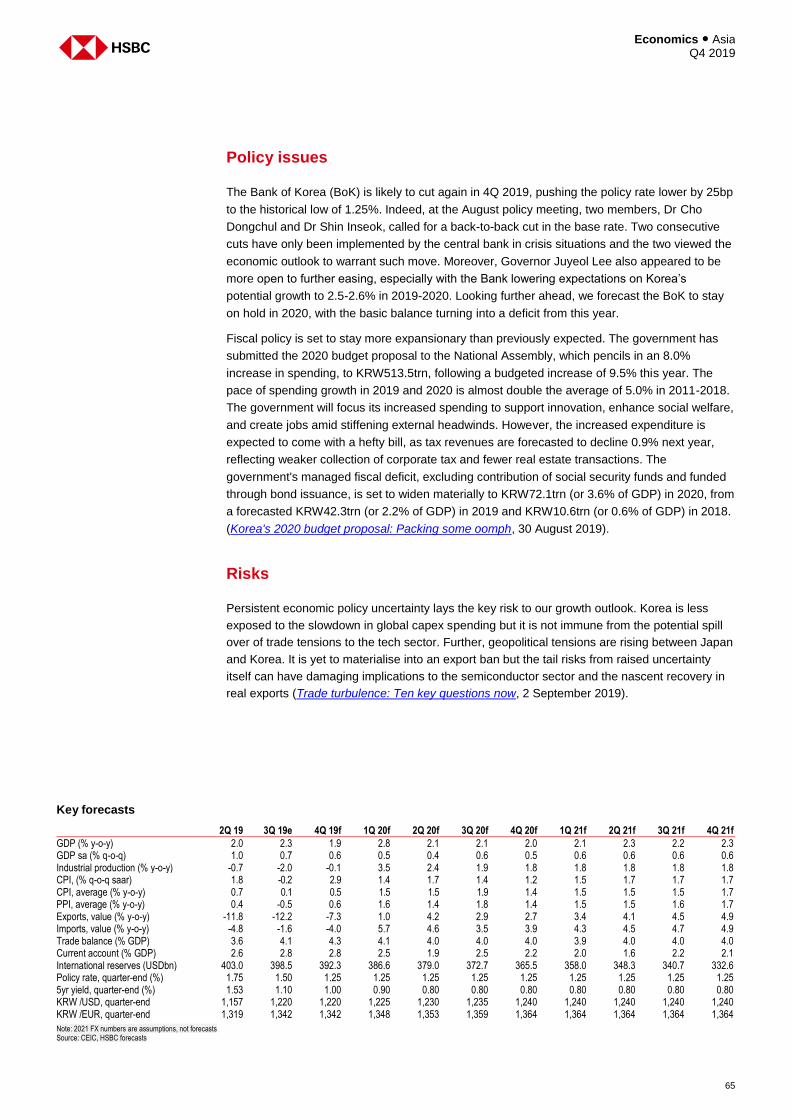

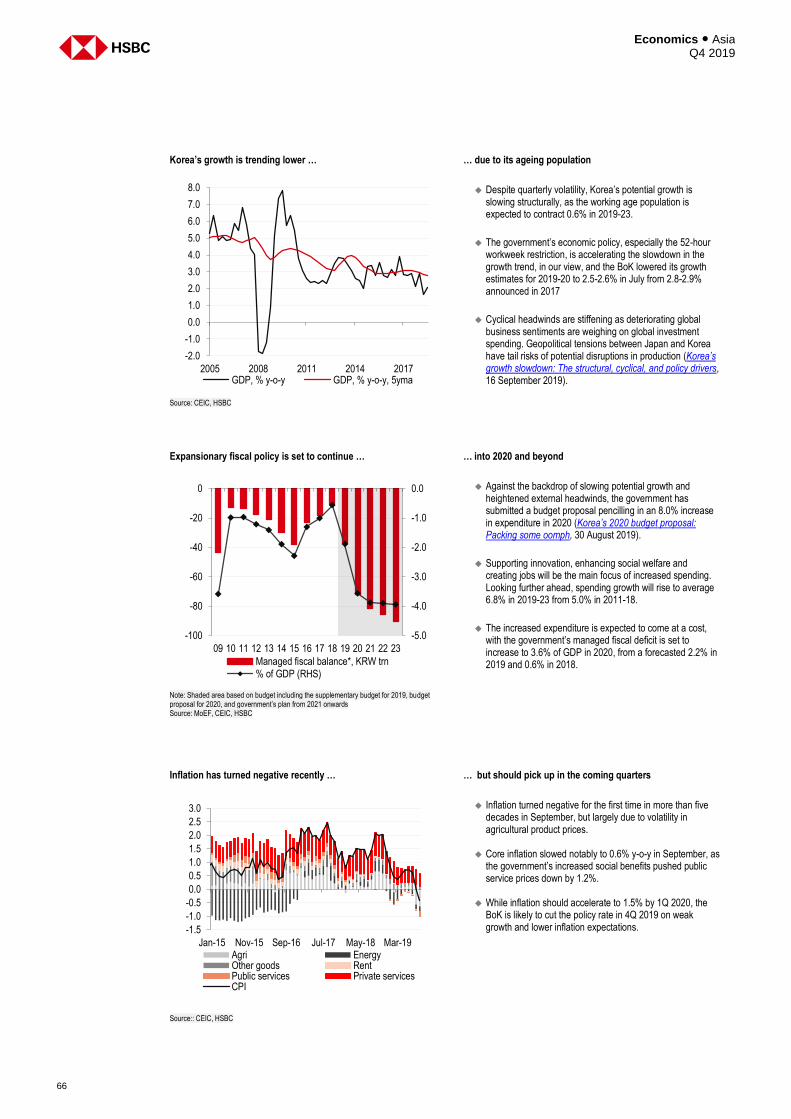

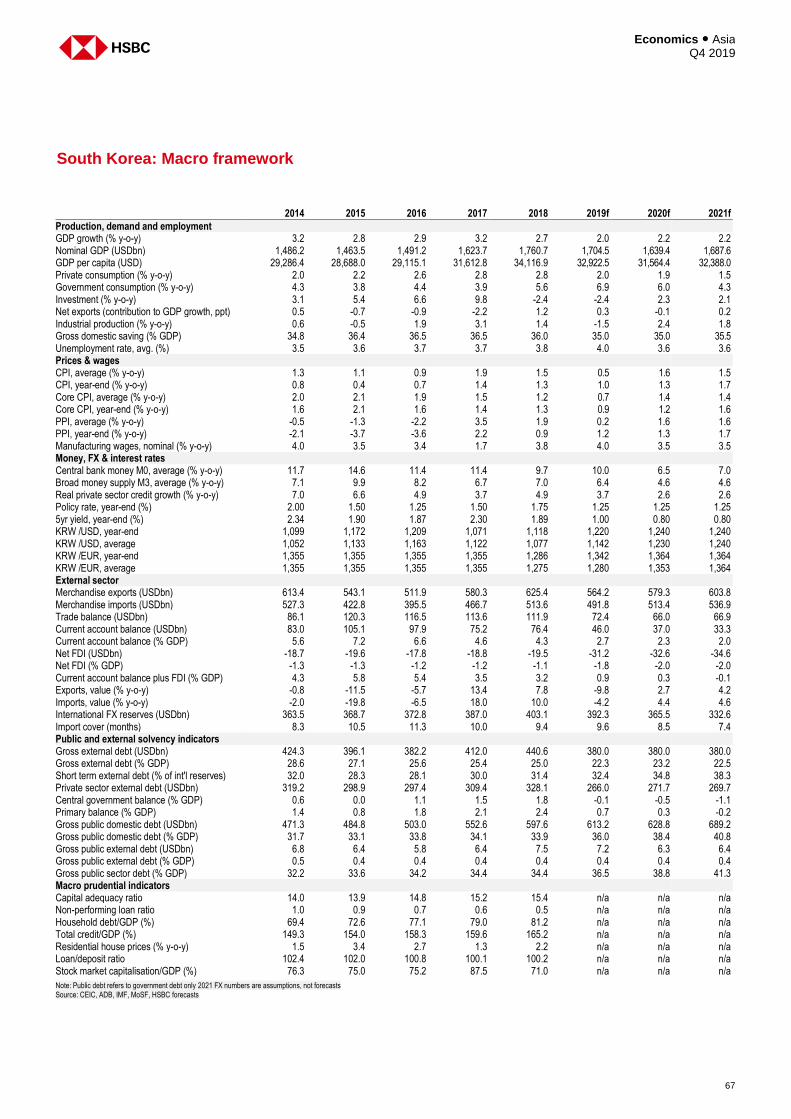

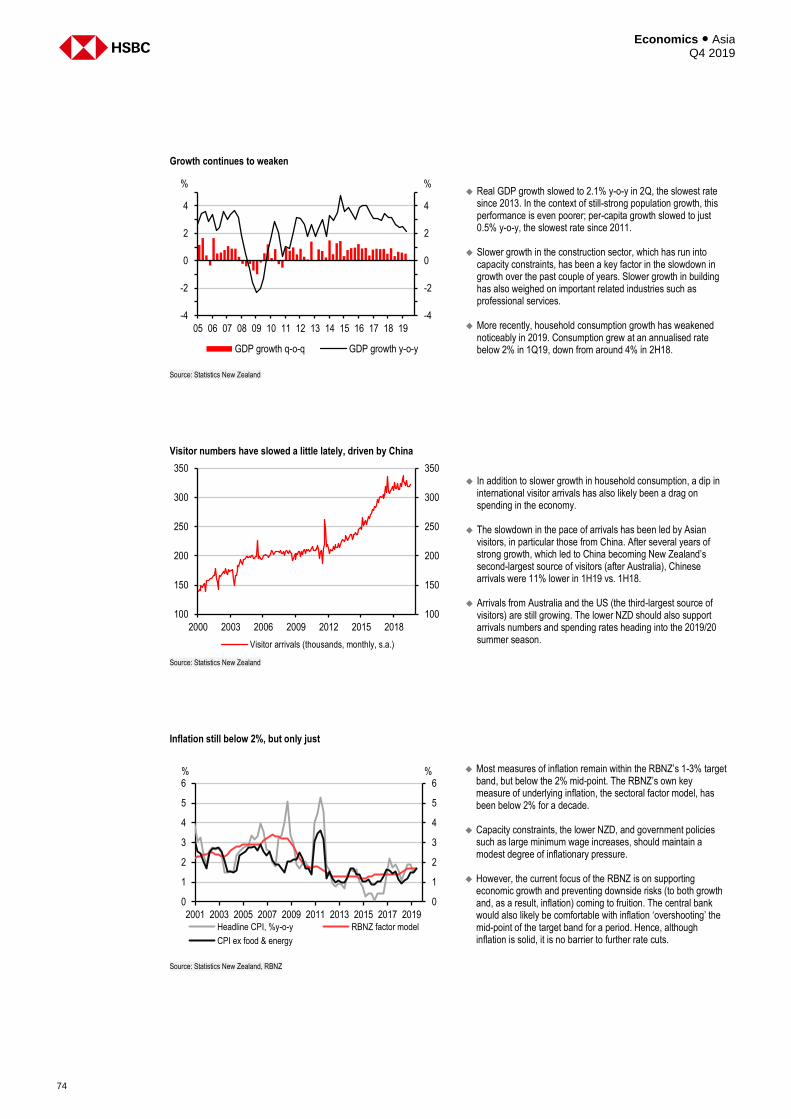

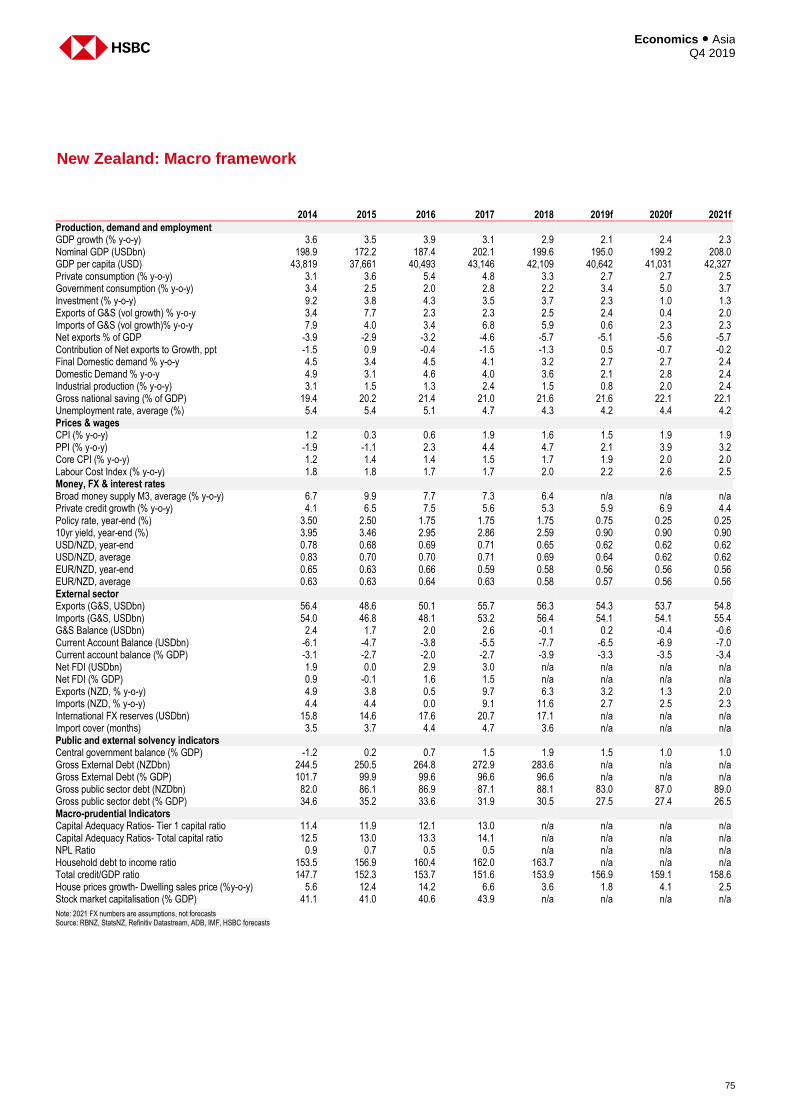

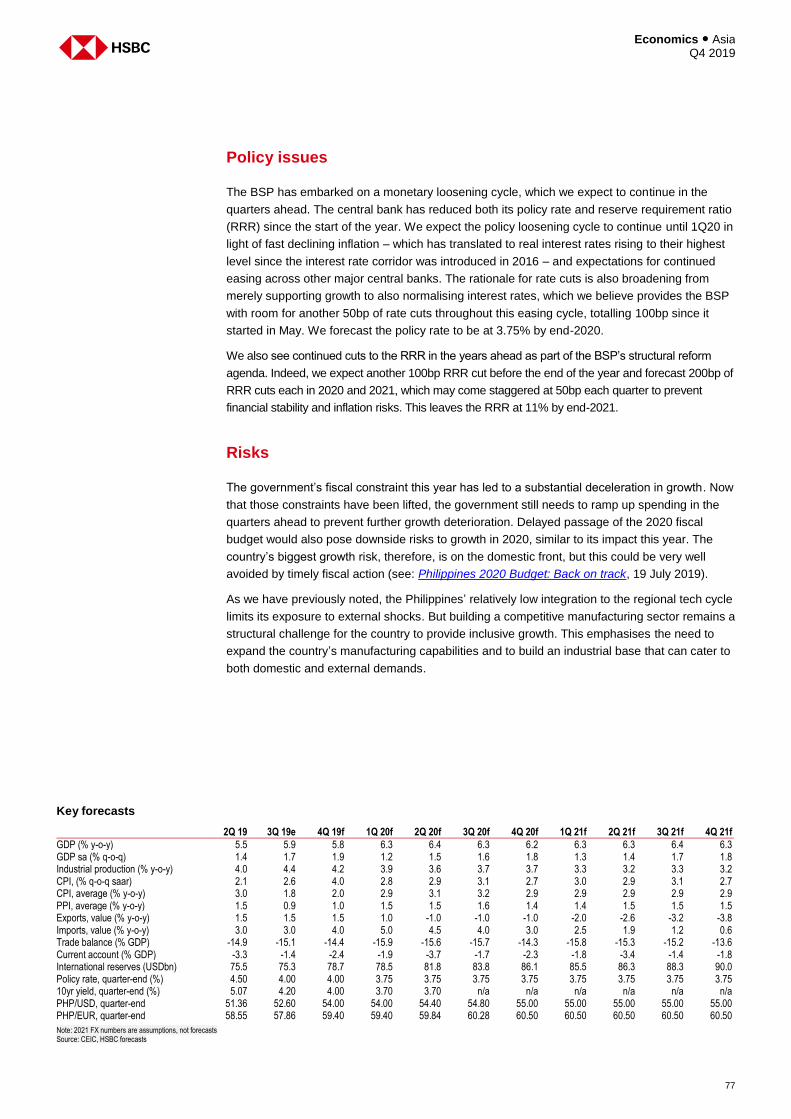

www.research.hsbc.com Disclosures & Disclaimer: This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it. Economics Asia Q4 2019 By: Frederic Neumann and Qu Hongbin Asian Economics Bending, not breaking Trade tensions and wobbly local demand are weighing on growth in China and elsewhere in Asia But further policy easing, both fiscal and monetary, will strengthen resilience across the region… …even if it may take a little while longer for growth to swing back

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.research.hsbc.com

Disclosures & Disclaimer: This report must be read with the disclosures and the analyst certifications inthe Disclosure appendix, and with the Disclaimer, which forms part of it.

Q4 2019

Economics | A

siaA

sian Economics

EconomicsAsia

Q4 2019By: Frederic Neumann and Qu Hongbin

Asian EconomicsBending, not breaking

Trade tensions and wobbly local demand are weighing on growth in China and elsewhere in Asia

But further policy easing, both fiscal and monetary, will strengthen resilience across the region…

…even if it may take a little while longer for growth to swing back

1

Economics ● Asia Q4 2019

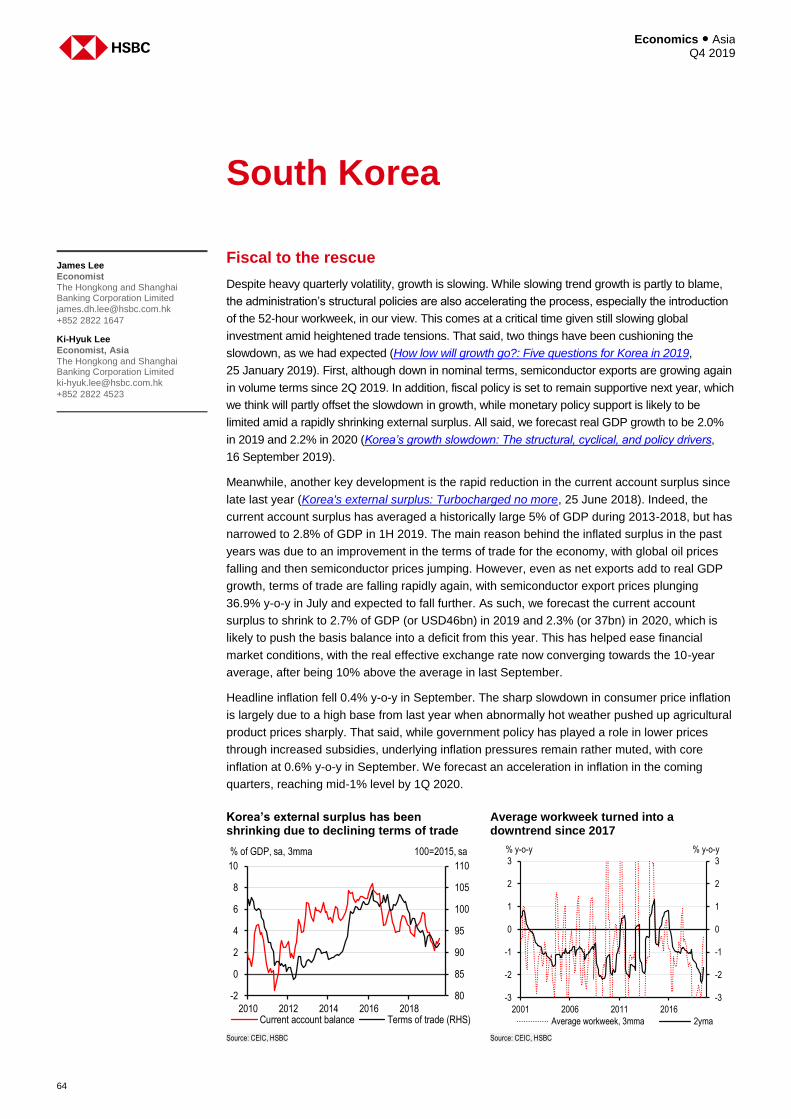

Things have been a little bumpier than expected across Asia, but the

region is firmly holding on to growth. Exports, the main fuel of Asia’s

economic engine, have dried up, with shipments falling for several

months. Trade tensions between the US and China are only partly to

blame: wobbly demand across developed and even many emerging

markets, as well as a tired electronics cycle, have equally weighed on

shipments. Hesitant easing in mainland China has further curtailed

growth, not only domestically, but more broadly across the region.

And yet, all considered, overall demand in Asia is ticking along at a

decent enough pace. To prevent a further slowdown, however, extra

easing, both monetary and fiscal, will be required. Even then, given

continued global headwinds, it will take a little while longer before

Asia swings back with its customary panache.

Not this time

Yes, things feel soggy. Look closely, however, and the region’s economies have arguably held up

better than many others, notably in the West. And yet, without extra stimulus, Asia, too, is bound

to slip further. Good news, then, that there is more easing in the pipeline.

That said, mainland China is not about to pull out the massive reflation investors got accustomed

to over previous cycles. It’s more about fine-tuning the stance, rather than pulling out all the stops:

incremental monetary and fiscal easing will have to do. As a result, HSBC’s Chief China Economist,

Qu Hongbin, expects growth to slow to 5.8% in 2020 from 6.2% this year.

That means that downward pressures on regional, if not global, trade will persist for a while, even

if trade tensions were to ease, say, because of a potential mini-deal between the US and China in

the coming weeks or months.

Further afield, the outlook for demand still looks shaky as well. As HSBC’s Group Chief Economist

Janet Henry and Global Economist James Pomeroy detail in a recent report: while there are lots

of attempts to ‘pump the air’ back into the global economy, growth in developed markets looks set

to slip further (see Global Economics Quarterly: putting the air back in, 26 September, 2019).

Which brings us back to the need for more stimulus. Almost all economies across Asia are

expected to ease monetary policy again in the coming months. Fiscal policy, meanwhile, has

turned more supportive as well, delivering an extra kick to growth from Korea to India, and the

Philippines to Singapore.

Executive summary

Economics ● Asia Q4 2019

2

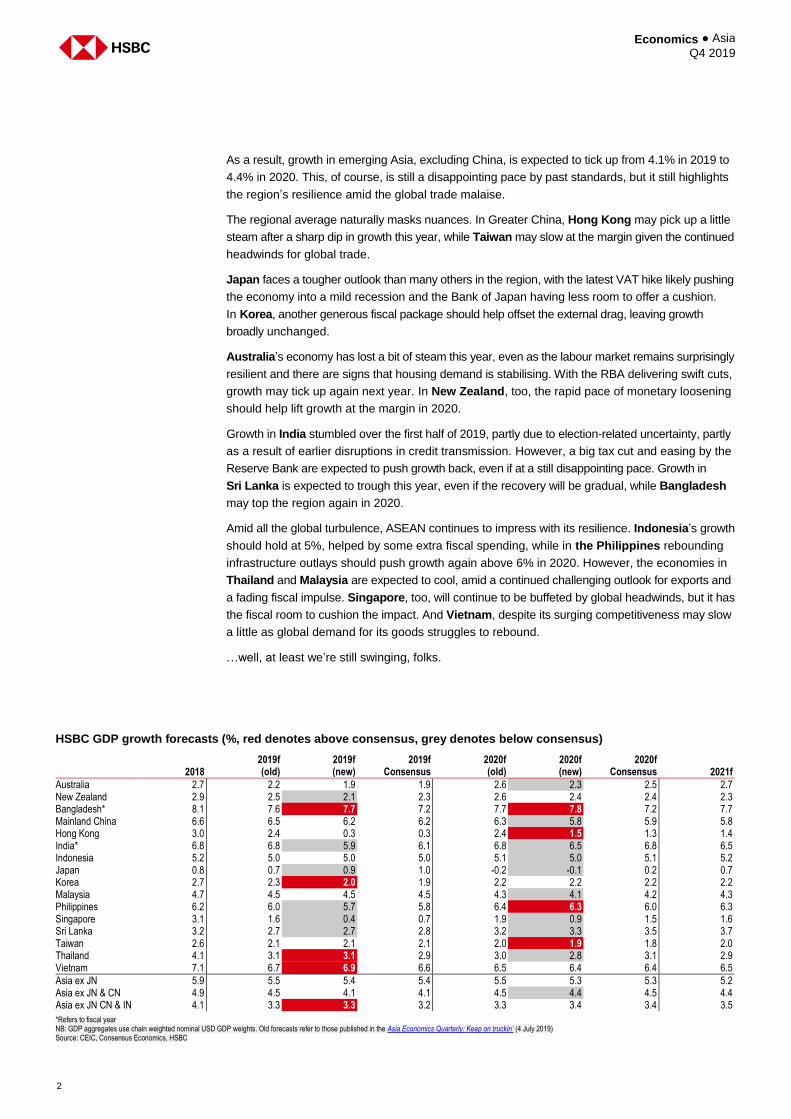

As a result, growth in emerging Asia, excluding China, is expected to tick up from 4.1% in 2019 to

4.4% in 2020. This, of course, is still a disappointing pace by past standards, but it still highlights

the region’s resilience amid the global trade malaise.

The regional average naturally masks nuances. In Greater China, Hong Kong may pick up a little

steam after a sharp dip in growth this year, while Taiwan may slow at the margin given the continued

headwinds for global trade.

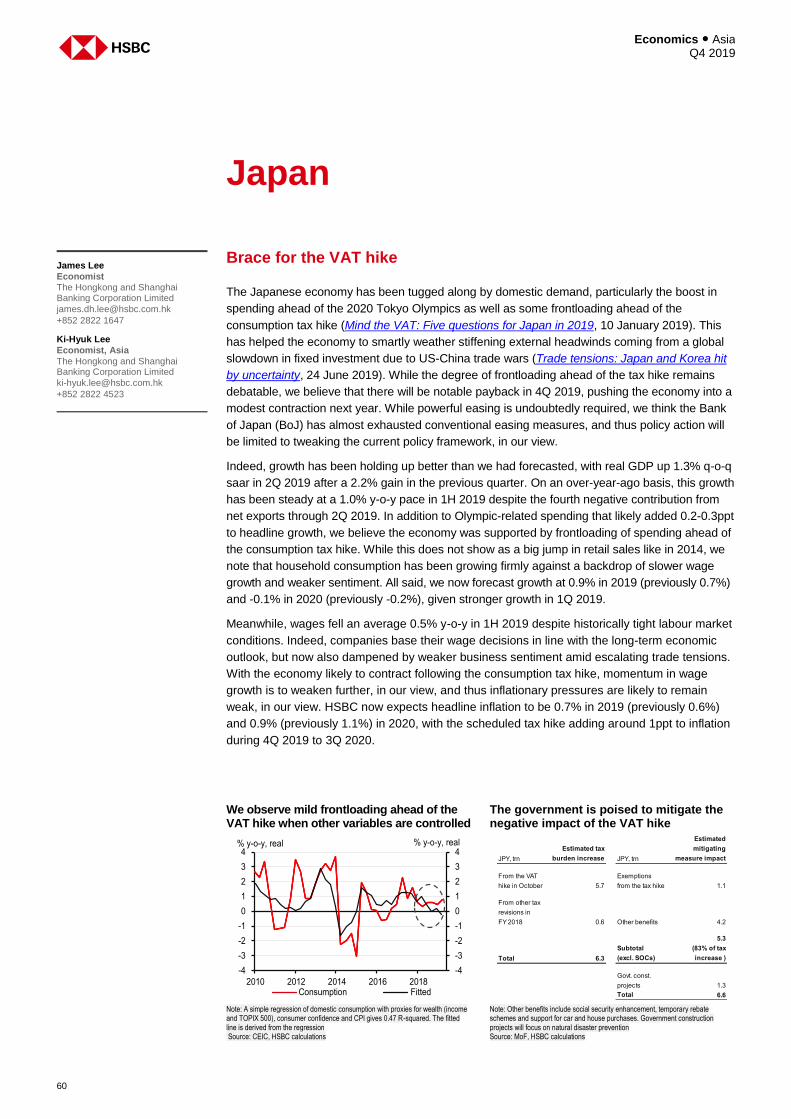

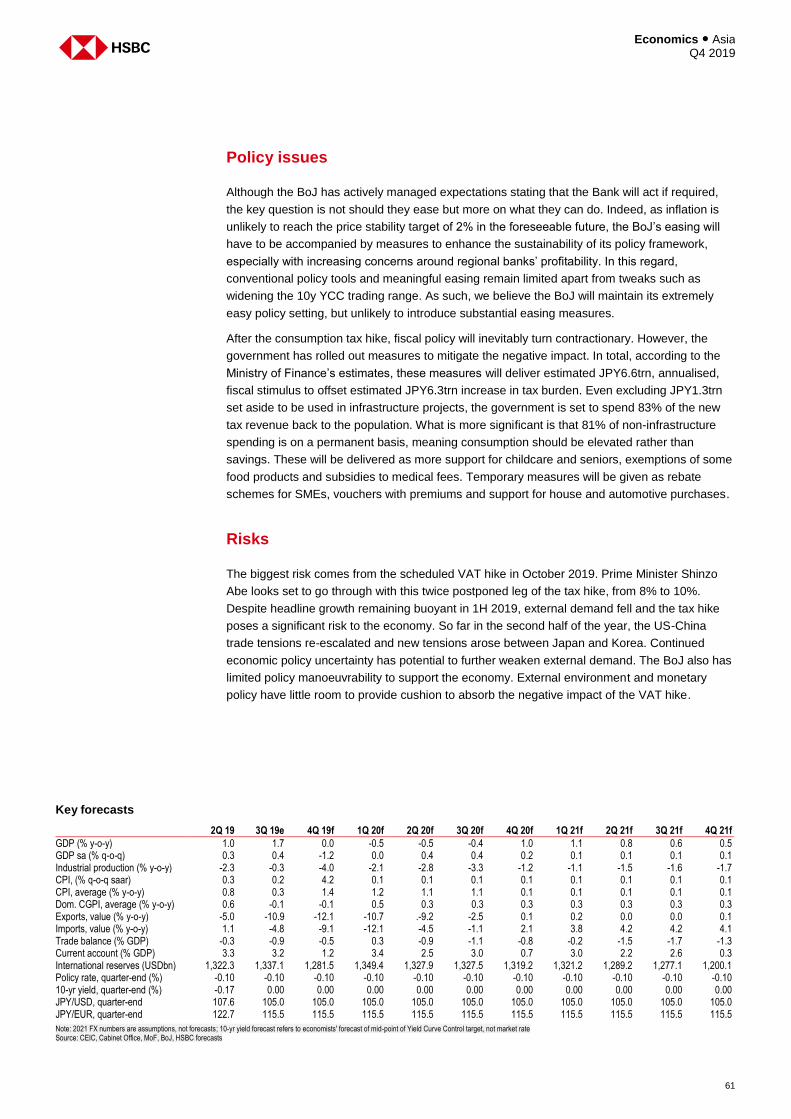

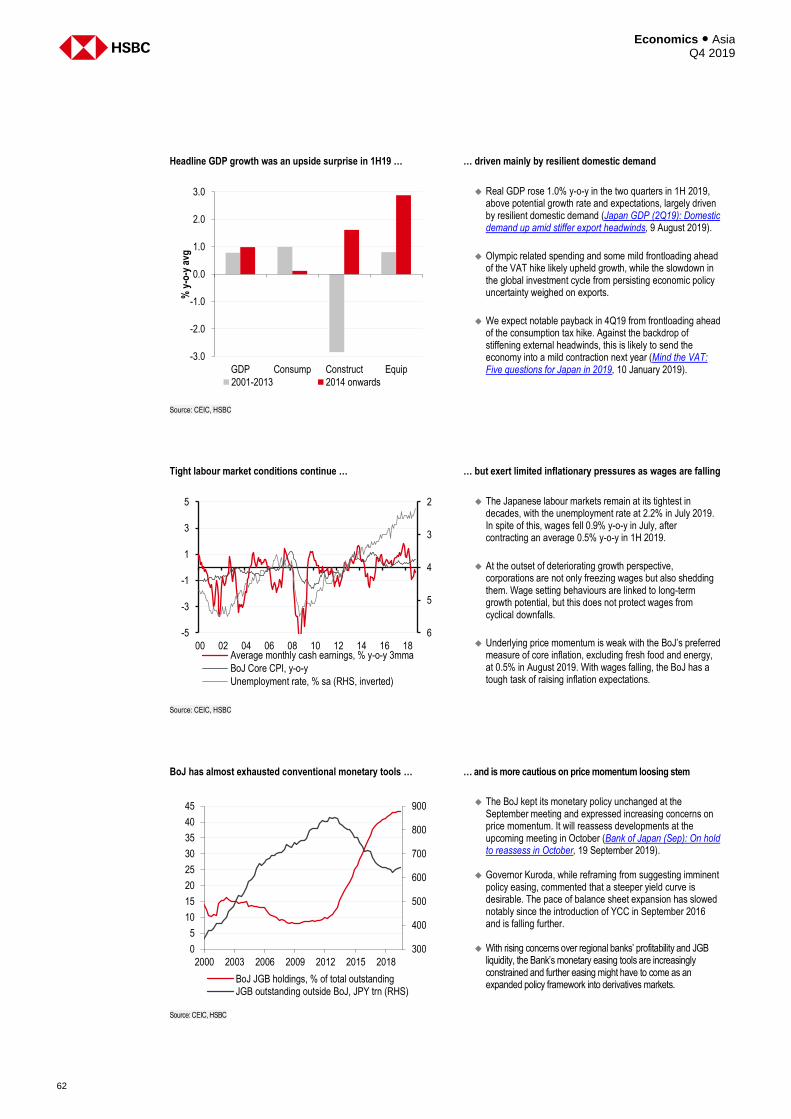

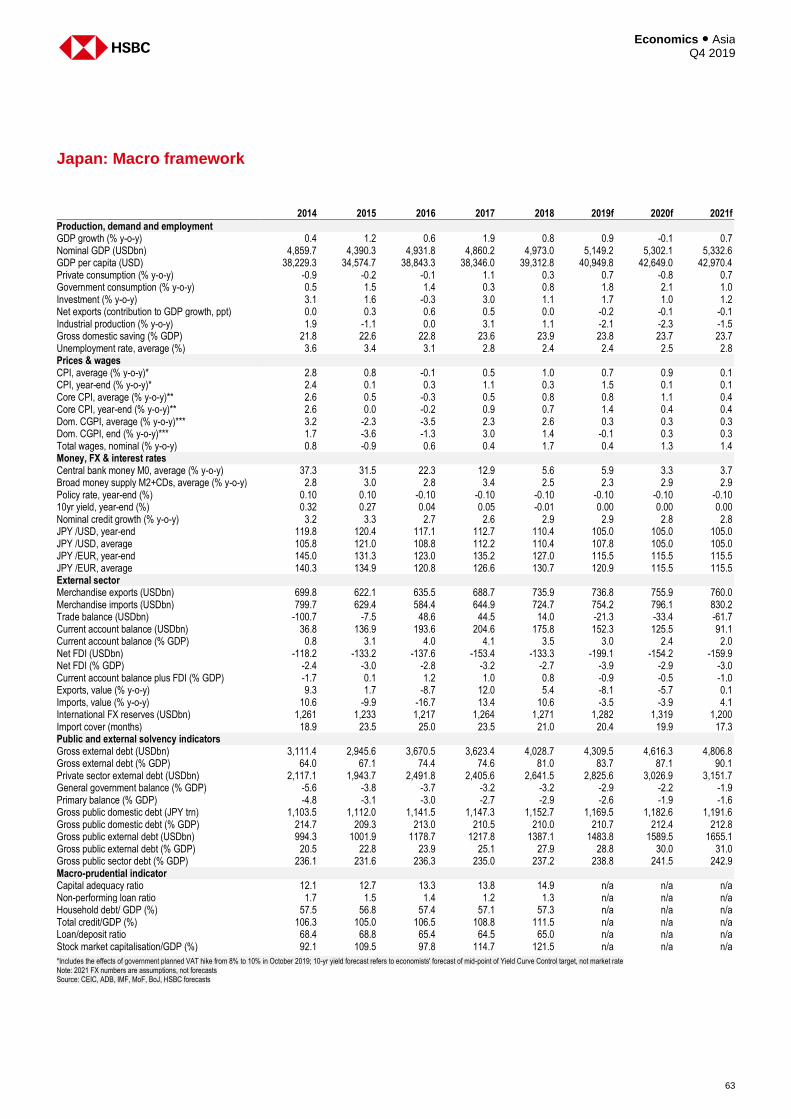

Japan faces a tougher outlook than many others in the region, with the latest VAT hike likely pushing

the economy into a mild recession and the Bank of Japan having less room to offer a cushion.

In Korea, another generous fiscal package should help offset the external drag, leaving growth

broadly unchanged.

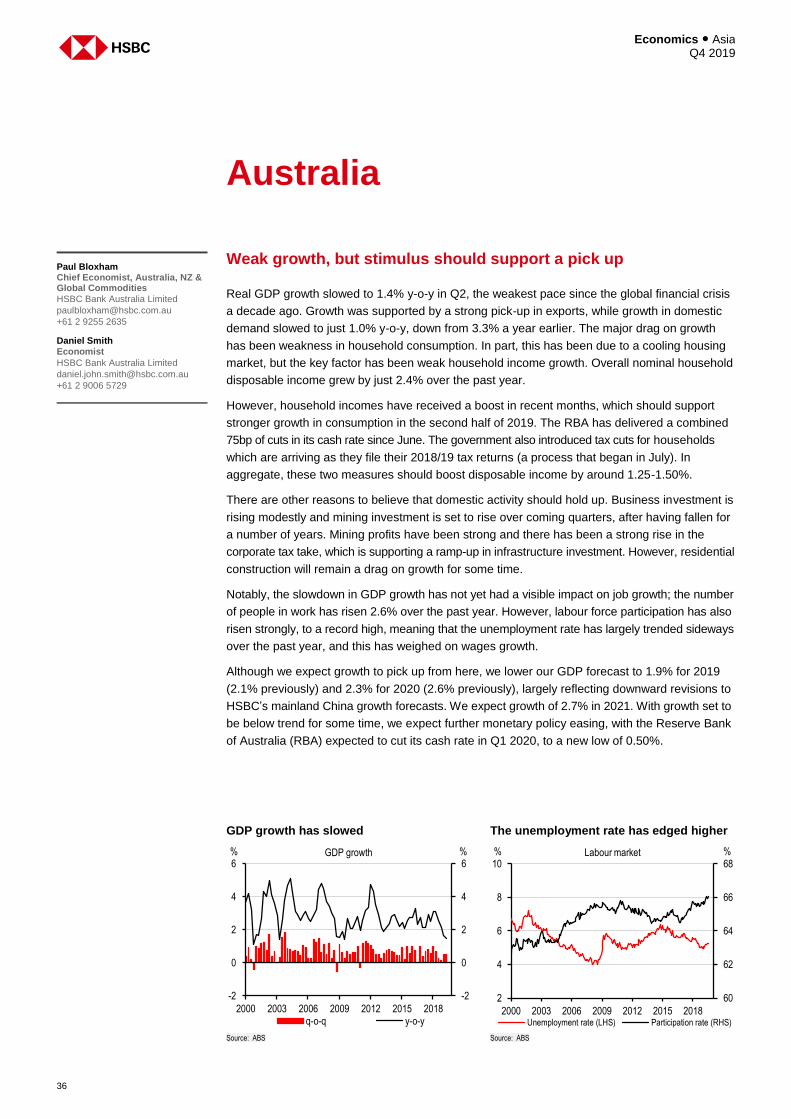

Australia’s economy has lost a bit of steam this year, even as the labour market remains surprisingly

resilient and there are signs that housing demand is stabilising. With the RBA delivering swift cuts,

growth may tick up again next year. In New Zealand, too, the rapid pace of monetary loosening

should help lift growth at the margin in 2020.

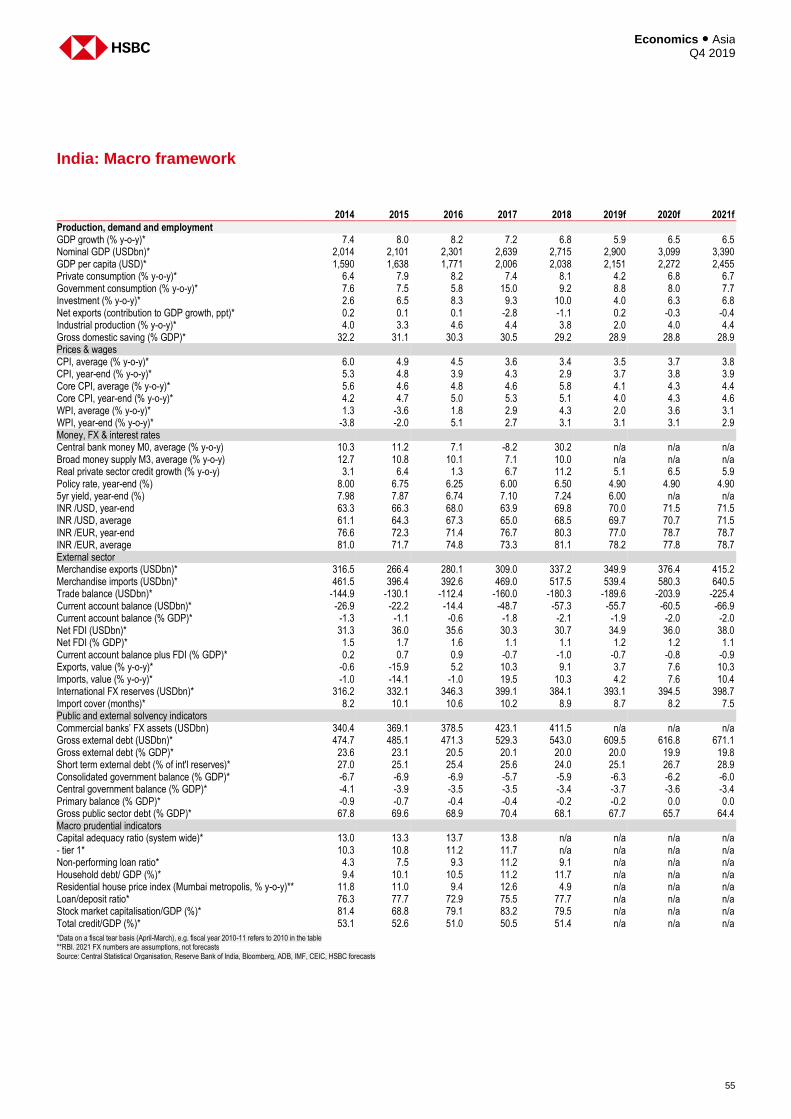

Growth in India stumbled over the first half of 2019, partly due to election-related uncertainty, partly

as a result of earlier disruptions in credit transmission. However, a big tax cut and easing by the

Reserve Bank are expected to push growth back, even if at a still disappointing pace. Growth in

Sri Lanka is expected to trough this year, even if the recovery will be gradual, while Bangladesh

may top the region again in 2020.

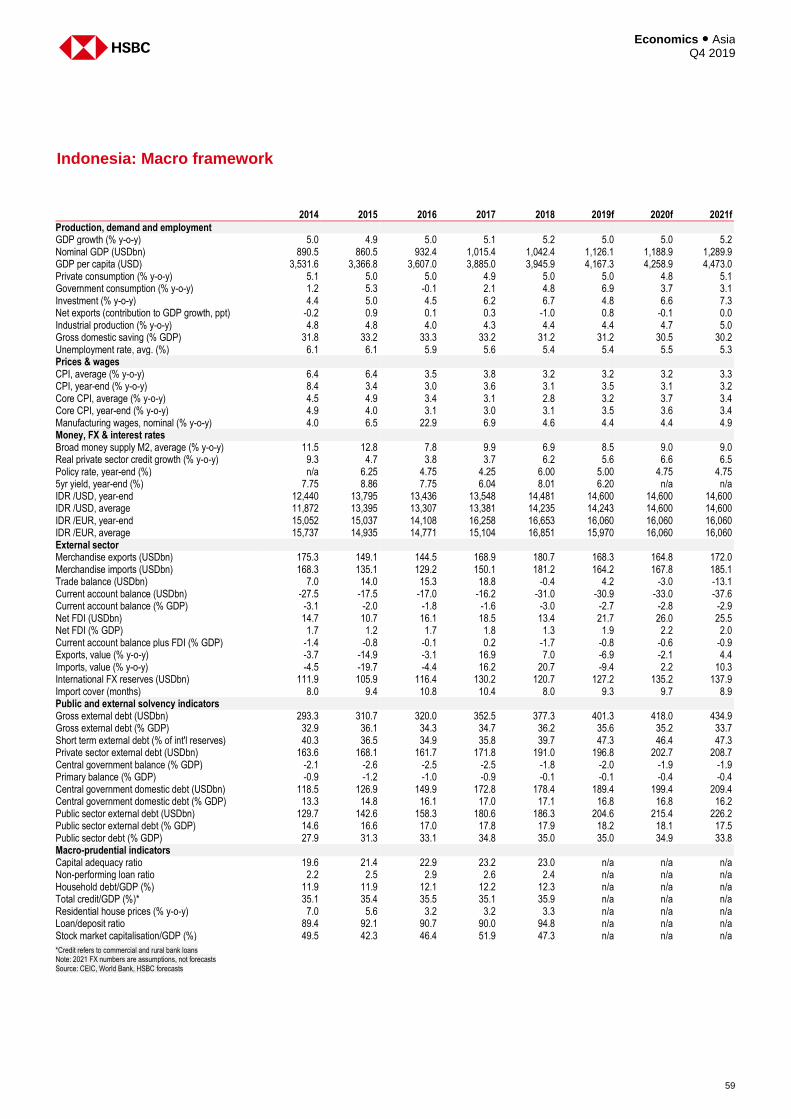

Amid all the global turbulence, ASEAN continues to impress with its resilience. Indonesia’s growth

should hold at 5%, helped by some extra fiscal spending, while in the Philippines rebounding

infrastructure outlays should push growth again above 6% in 2020. However, the economies in

Thailand and Malaysia are expected to cool, amid a continued challenging outlook for exports and

a fading fiscal impulse. Singapore, too, will continue to be buffeted by global headwinds, but it has

the fiscal room to cushion the impact. And Vietnam, despite its surging competitiveness may slow

a little as global demand for its goods struggles to rebound.

…well, at least we’re still swinging, folks.

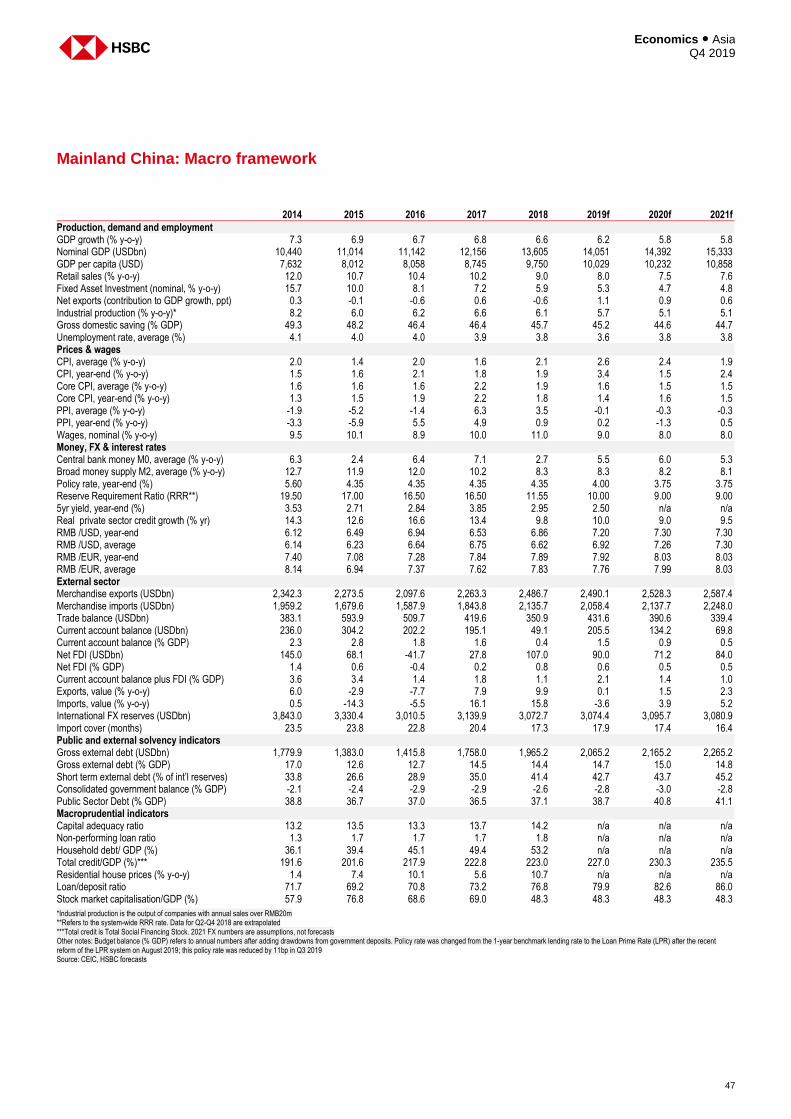

HSBC GDP growth forecasts (%, red denotes above consensus, grey denotes below consensus)

2018

2019f (old)

2019f (new)

2019f Consensus

2020f (old)

2020f (new)

2020f Consensus 2021f

Australia 2.7 2.2 1.9 1.9 2.6 2.3 2.5 2.7 New Zealand 2.9 2.5 2.1 2.3 2.6 2.4 2.4 2.3 Bangladesh* 8.1 7.6 7.7 7.2 7.7 7.8 7.2 7.7 Mainland China 6.6 6.5 6.2 6.2 6.3 5.8 5.9 5.8 Hong Kong 3.0 2.4 0.3 0.3 2.4 1.5 1.3 1.4 India* 6.8 6.8 5.9 6.1 6.8 6.5 6.8 6.5 Indonesia 5.2 5.0 5.0 5.0 5.1 5.0 5.1 5.2 Japan 0.8 0.7 0.9 1.0 -0.2 -0.1 0.2 0.7 Korea 2.7 2.3 2.0 1.9 2.2 2.2 2.2 2.2 Malaysia 4.7 4.5 4.5 4.5 4.3 4.1 4.2 4.3 Philippines 6.2 6.0 5.7 5.8 6.4 6.3 6.0 6.3 Singapore 3.1 1.6 0.4 0.7 1.9 0.9 1.5 1.6 Sri Lanka 3.2 2.7 2.7 2.8 3.2 3.3 3.5 3.7 Taiwan 2.6 2.1 2.1 2.1 2.0 1.9 1.8 2.0 Thailand 4.1 3.1 3.1 2.9 3.0 2.8 3.1 2.9 Vietnam 7.1 6.7 6.9 6.6 6.5 6.4 6.4 6.5

Asia ex JN 5.9 5.5 5.4 5.4 5.5 5.3 5.3 5.2 Asia ex JN & CN 4.9 4.5 4.1 4.1 4.5 4.4 4.5 4.4 Asia ex JN CN & IN 4.1 3.3 3.3 3.2 3.3 3.4 3.4 3.5

*Refers to fiscal year NB: GDP aggregates use chain weighted nominal USD GDP weights. Old forecasts refer to those published in the Asia Economics Quarterly: Keep on truckin’ (4 July 2019) Source: CEIC, Consensus Economics, HSBC

3

Economics ● Asia Q4 2019

Executive summary 1

Key forecasts 4

Monetary policy assumptions 5

Still slippin’ 6

Mainland China: Moderate

stimulus, slower growth 20

Indicators 27

GDP 28

Inflation 29

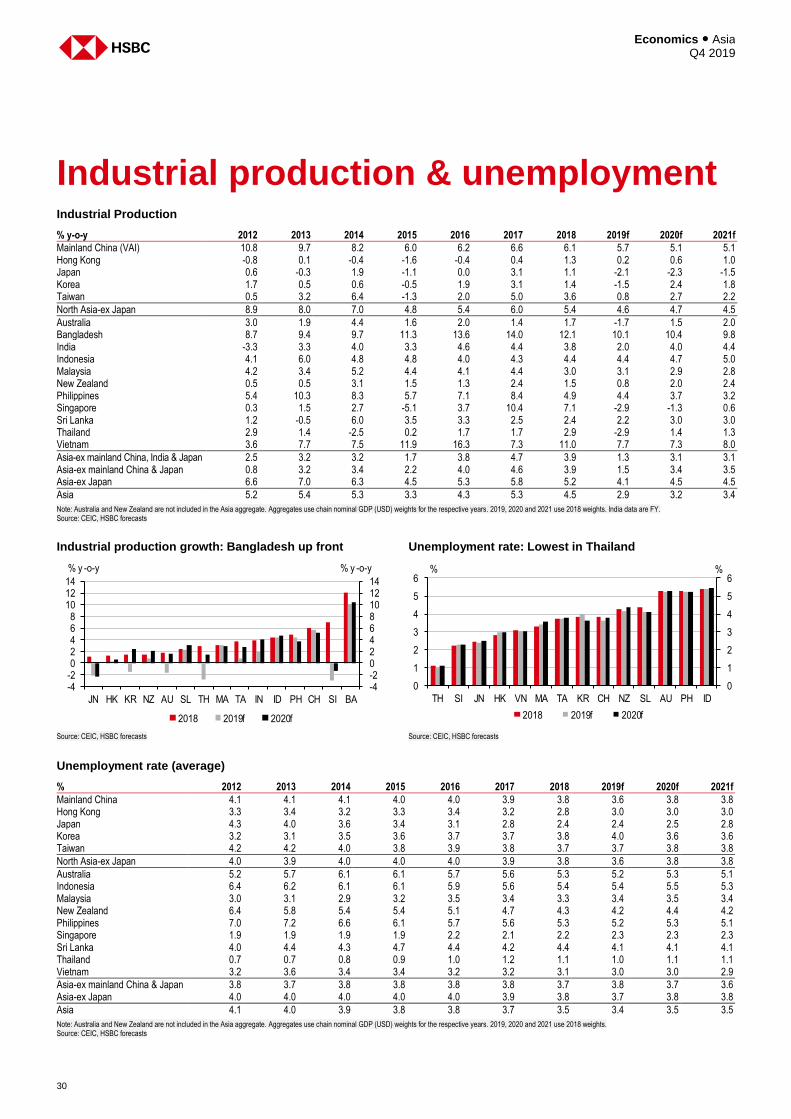

Industrial production & unemployment 30

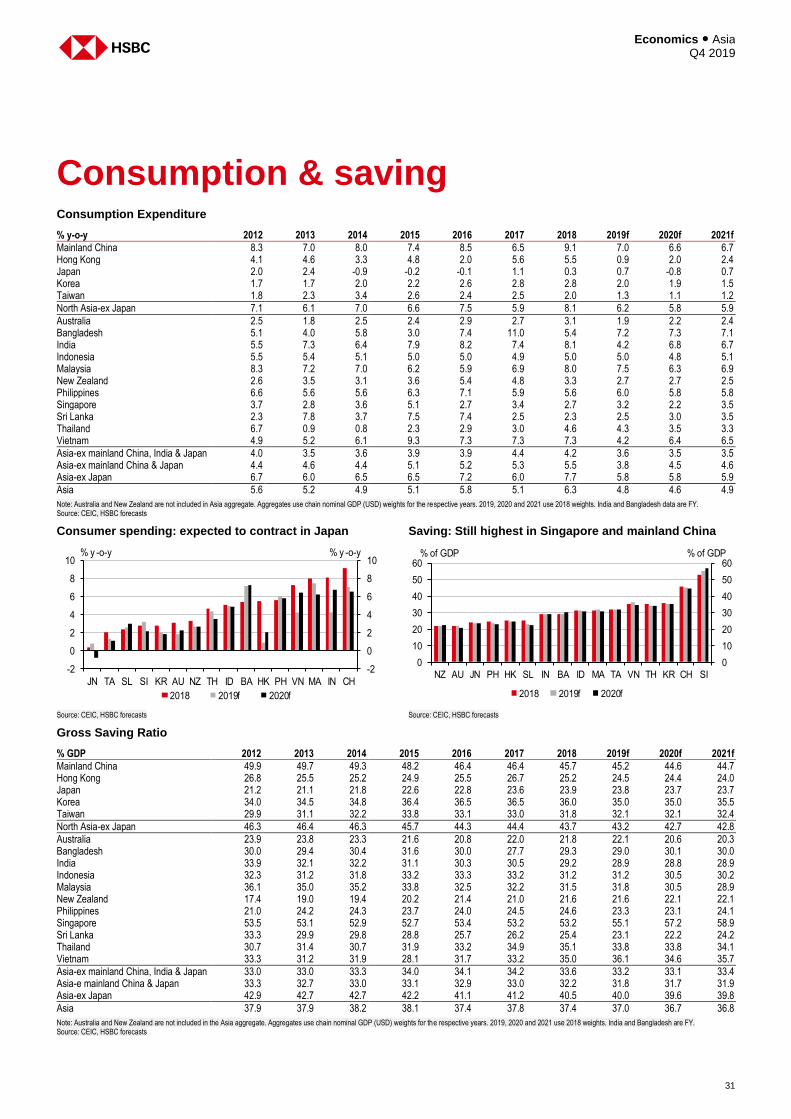

Consumption & saving 31

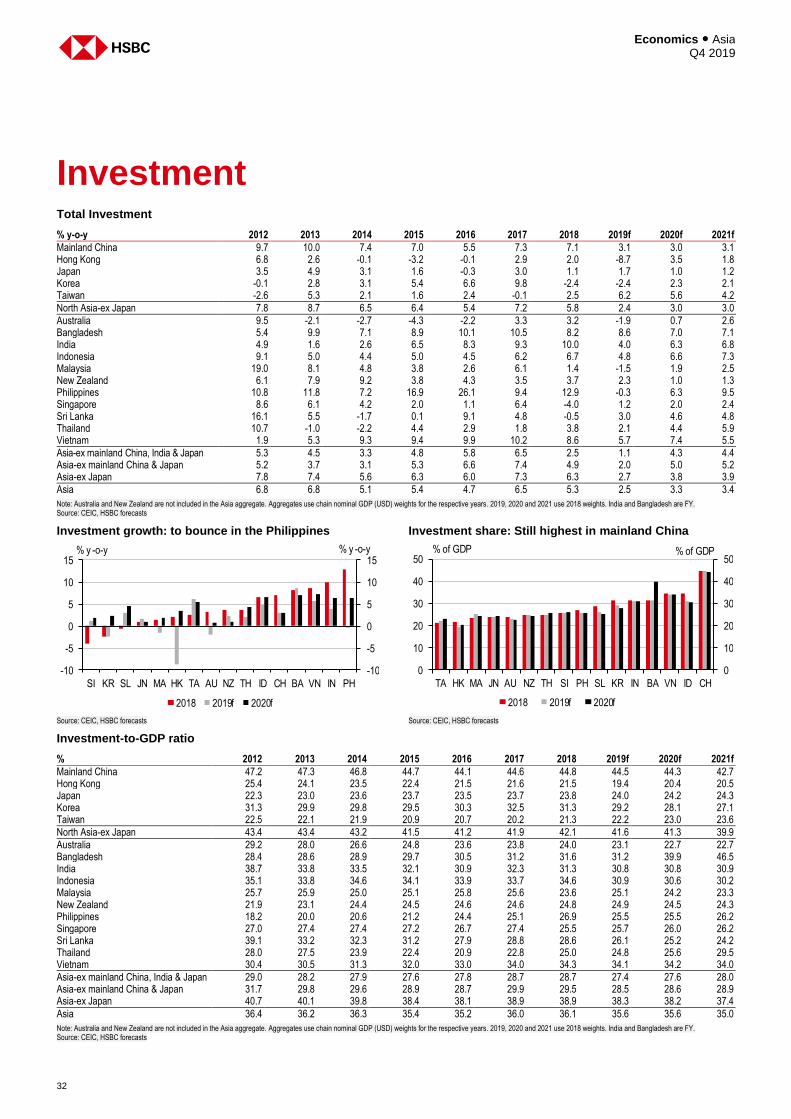

Investment 32

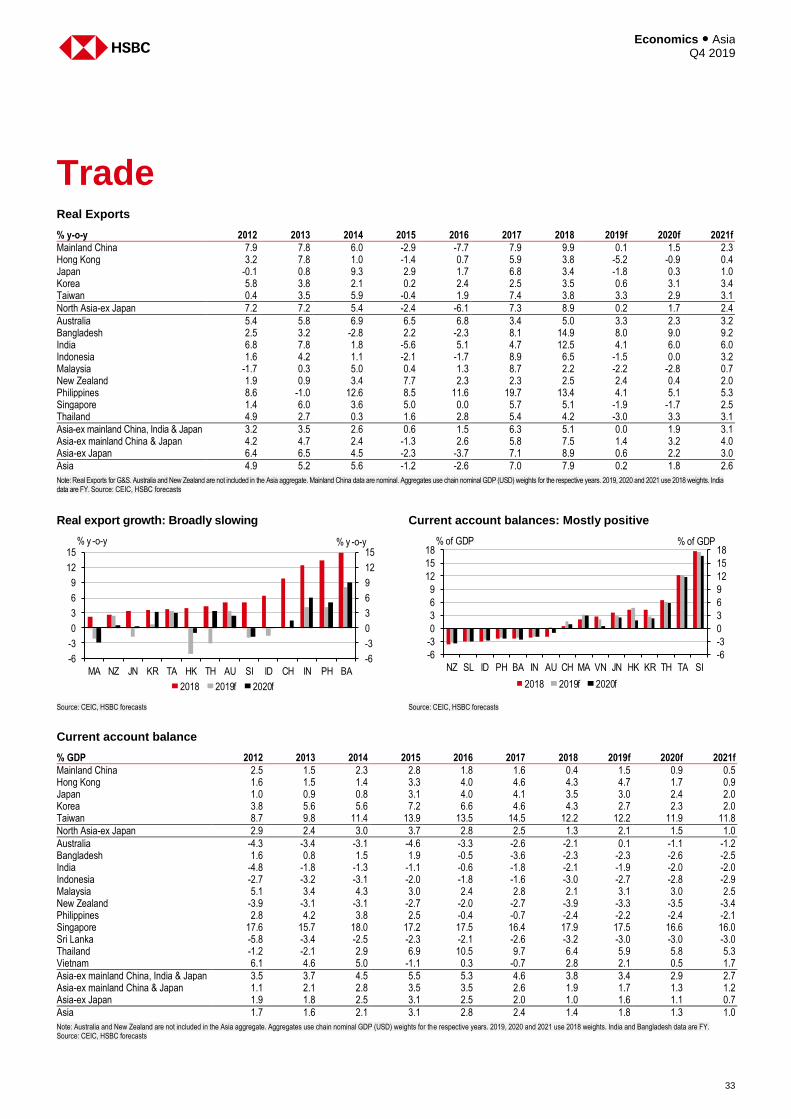

Trade 33

Economy profiles 35

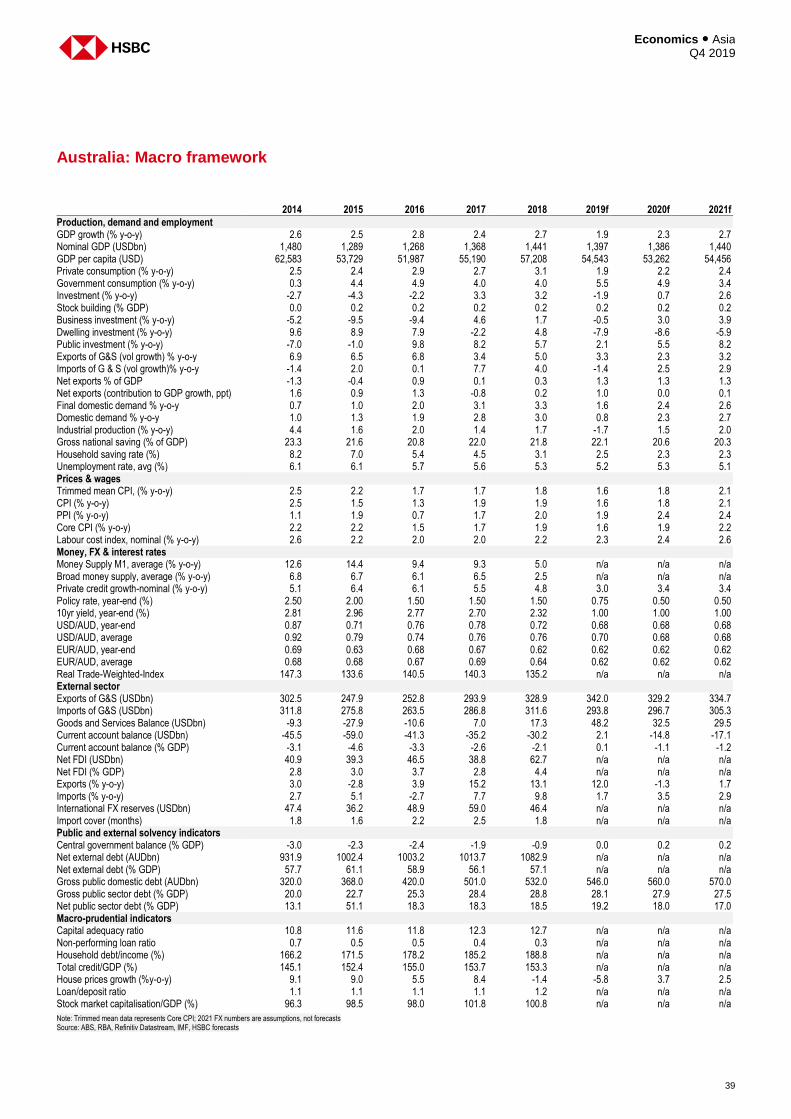

Australia 36

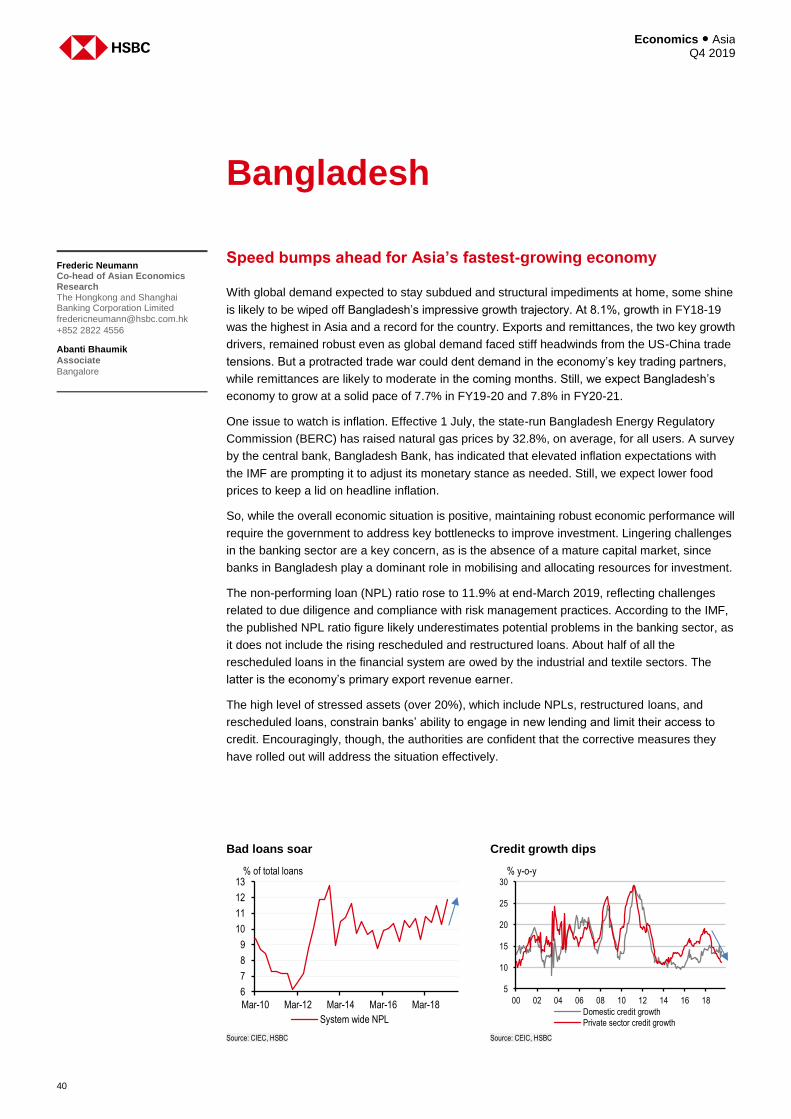

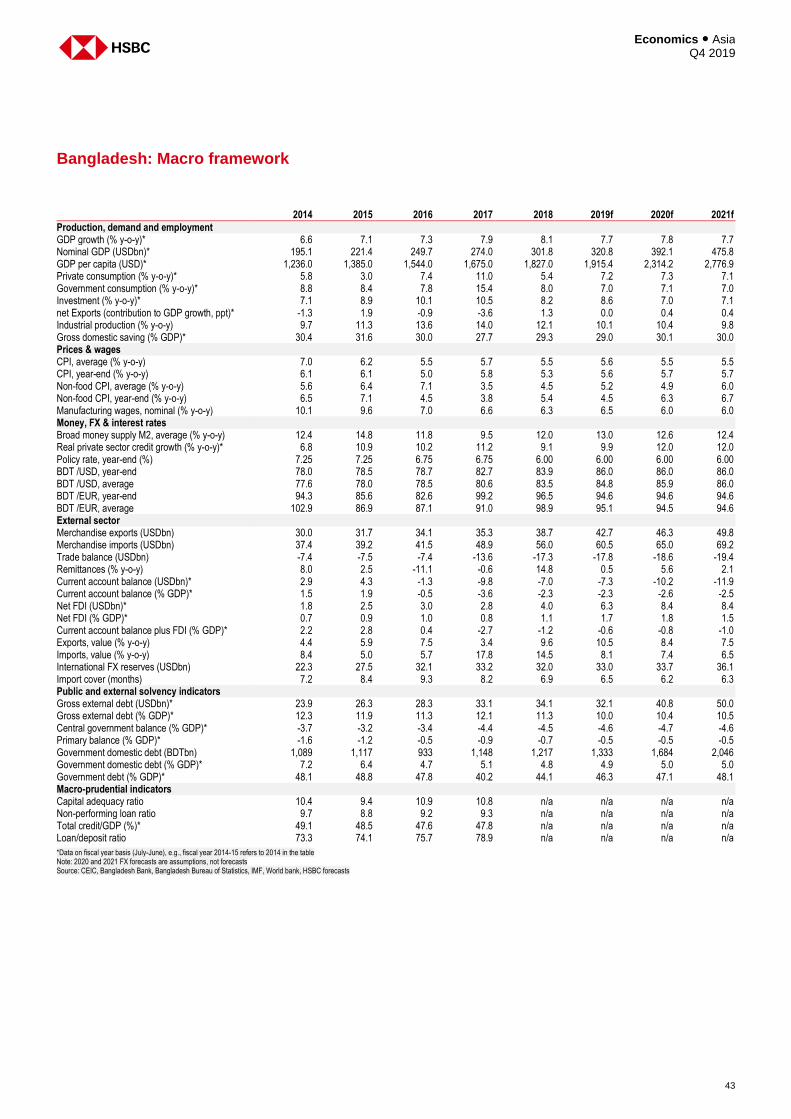

Bangladesh 40

Mainland China 44

Hong Kong 48

India 52

Indonesia 56

Japan 60

South Korea 64

Malaysia 68

New Zealand 72

Philippines 76

Singapore 80

Sri Lanka 84

Taiwan 88

Thailand 92

Vietnam 96

Disclosure appendix 101

Disclaimer 104

Contents

Economics ● Asia Q4 2019

4

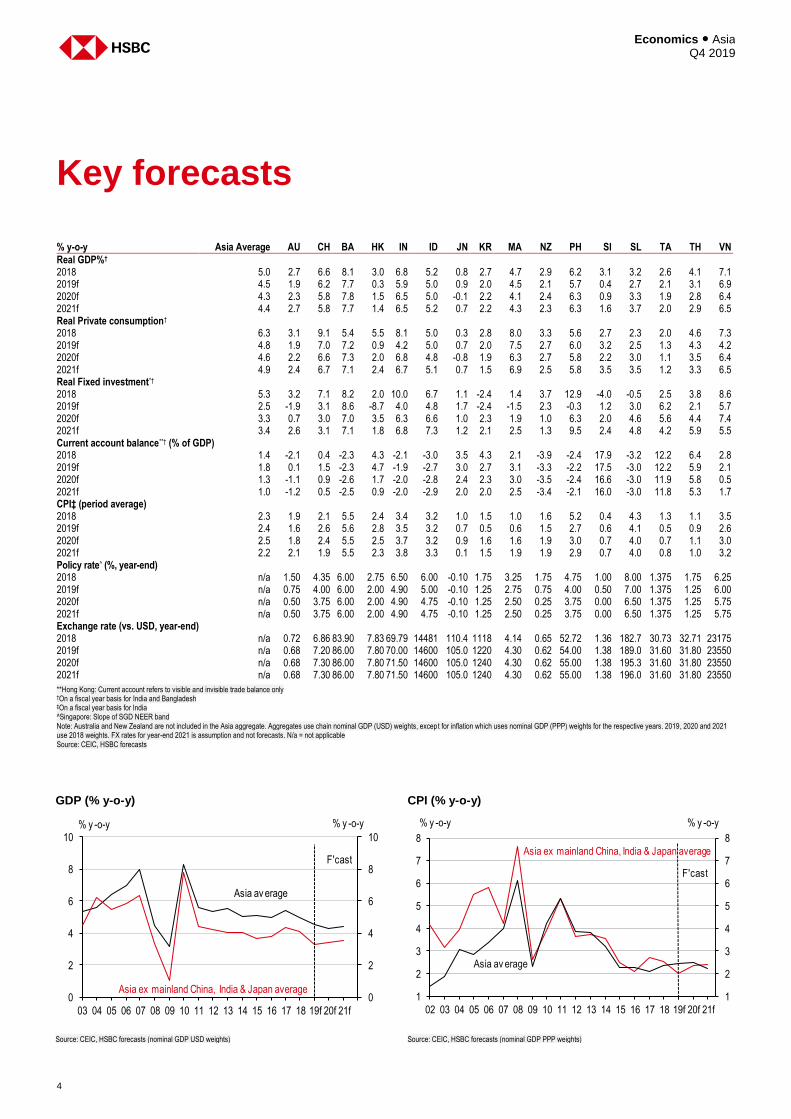

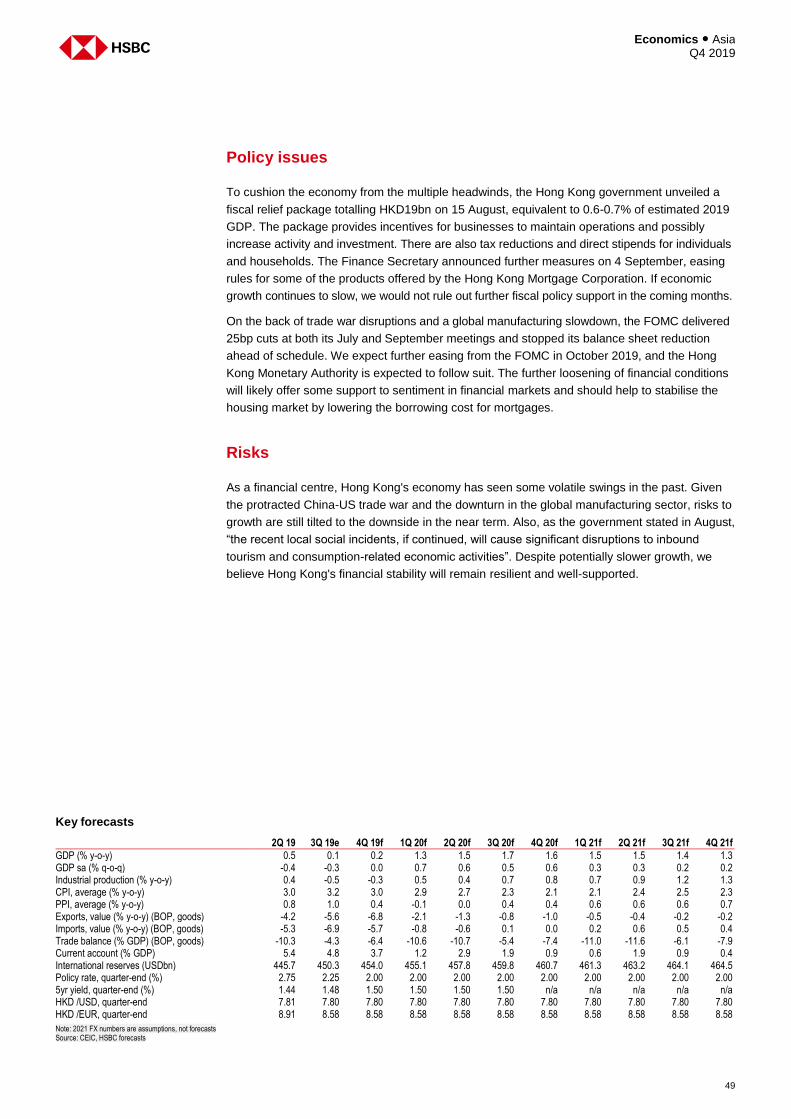

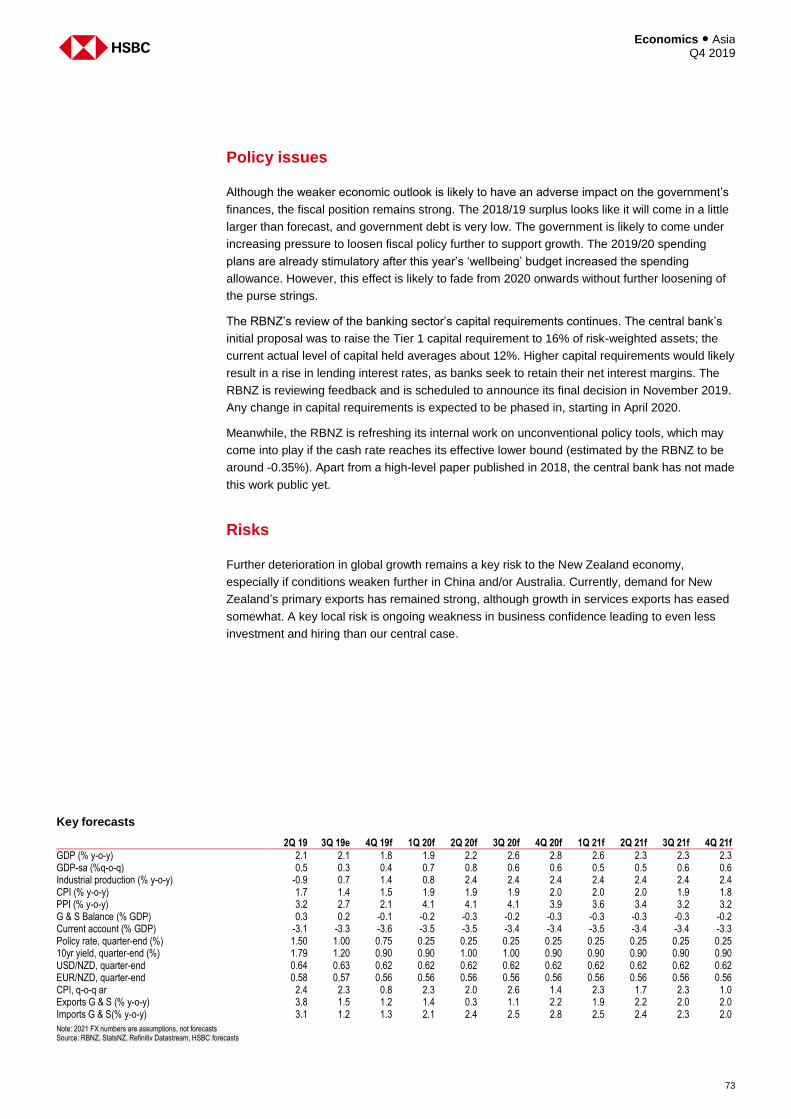

Key forecasts

% y-o-y Asia Average AU CH BA HK IN ID JN KR MA NZ PH SI SL TA TH VN

Real GDP%† 2018 5.0 2.7 6.6 8.1 3.0 6.8 5.2 0.8 2.7 4.7 2.9 6.2 3.1 3.2 2.6 4.1 7.1 2019f 4.5 1.9 6.2 7.7 0.3 5.9 5.0 0.9 2.0 4.5 2.1 5.7 0.4 2.7 2.1 3.1 6.9 2020f 4.3 2.3 5.8 7.8 1.5 6.5 5.0 -0.1 2.2 4.1 2.4 6.3 0.9 3.3 1.9 2.8 6.4 2021f 4.4 2.7 5.8 7.7 1.4 6.5 5.2 0.7 2.2 4.3 2.3 6.3 1.6 3.7 2.0 2.9 6.5 Real Private consumption† 2018 6.3 3.1 9.1 5.4 5.5 8.1 5.0 0.3 2.8 8.0 3.3 5.6 2.7 2.3 2.0 4.6 7.3 2019f 4.8 1.9 7.0 7.2 0.9 4.2 5.0 0.7 2.0 7.5 2.7 6.0 3.2 2.5 1.3 4.3 4.2 2020f 4.6 2.2 6.6 7.3 2.0 6.8 4.8 -0.8 1.9 6.3 2.7 5.8 2.2 3.0 1.1 3.5 6.4 2021f 4.9 2.4 6.7 7.1 2.4 6.7 5.1 0.7 1.5 6.9 2.5 5.8 3.5 3.5 1.2 3.3 6.5 Real Fixed investment*† 2018 5.3 3.2 7.1 8.2 2.0 10.0 6.7 1.1 -2.4 1.4 3.7 12.9 -4.0 -0.5 2.5 3.8 8.6 2019f 2.5 -1.9 3.1 8.6 -8.7 4.0 4.8 1.7 -2.4 -1.5 2.3 -0.3 1.2 3.0 6.2 2.1 5.7 2020f 3.3 0.7 3.0 7.0 3.5 6.3 6.6 1.0 2.3 1.9 1.0 6.3 2.0 4.6 5.6 4.4 7.4 2021f 3.4 2.6 3.1 7.1 1.8 6.8 7.3 1.2 2.1 2.5 1.3 9.5 2.4 4.8 4.2 5.9 5.5 Current account balance**† (% of GDP) 2018 1.4 -2.1 0.4 -2.3 4.3 -2.1 -3.0 3.5 4.3 2.1 -3.9 -2.4 17.9 -3.2 12.2 6.4 2.8 2019f 1.8 0.1 1.5 -2.3 4.7 -1.9 -2.7 3.0 2.7 3.1 -3.3 -2.2 17.5 -3.0 12.2 5.9 2.1 2020f 1.3 -1.1 0.9 -2.6 1.7 -2.0 -2.8 2.4 2.3 3.0 -3.5 -2.4 16.6 -3.0 11.9 5.8 0.5 2021f 1.0 -1.2 0.5 -2.5 0.9 -2.0 -2.9 2.0 2.0 2.5 -3.4 -2.1 16.0 -3.0 11.8 5.3 1.7 CPI‡ (period average) 2018 2.3 1.9 2.1 5.5 2.4 3.4 3.2 1.0 1.5 1.0 1.6 5.2 0.4 4.3 1.3 1.1 3.5 2019f 2.4 1.6 2.6 5.6 2.8 3.5 3.2 0.7 0.5 0.6 1.5 2.7 0.6 4.1 0.5 0.9 2.6 2020f 2.5 1.8 2.4 5.5 2.5 3.7 3.2 0.9 1.6 1.6 1.9 3.0 0.7 4.0 0.7 1.1 3.0 2021f 2.2 2.1 1.9 5.5 2.3 3.8 3.3 0.1 1.5 1.9 1.9 2.9 0.7 4.0 0.8 1.0 3.2 Policy rate^ (%, year-end) 2018 n/a 1.50 4.35 6.00 2.75 6.50 6.00 -0.10 1.75 3.25 1.75 4.75 1.00 8.00 1.375 1.75 6.25 2019f n/a 0.75 4.00 6.00 2.00 4.90 5.00 -0.10 1.25 2.75 0.75 4.00 0.50 7.00 1.375 1.25 6.00 2020f n/a 0.50 3.75 6.00 2.00 4.90 4.75 -0.10 1.25 2.50 0.25 3.75 0.00 6.50 1.375 1.25 5.75 2021f n/a 0.50 3.75 6.00 2.00 4.90 4.75 -0.10 1.25 2.50 0.25 3.75 0.00 6.50 1.375 1.25 5.75 Exchange rate (vs. USD, year-end) 2018 n/a 0.72 6.86 83.90 7.83 69.79 14481 110.4 1118 4.14 0.65 52.72 1.36 182.7 30.73 32.71 23175 2019f n/a 0.68 7.20 86.00 7.80 70.00 14600 105.0 1220 4.30 0.62 54.00 1.38 189.0 31.60 31.80 23550 2020f n/a 0.68 7.30 86.00 7.80 71.50 14600 105.0 1240 4.30 0.62 55.00 1.38 195.3 31.60 31.80 23550 2021f n/a 0.68 7.30 86.00 7.80 71.50 14600 105.0 1240 4.30 0.62 55.00 1.38 196.0 31.60 31.80 23550

**Hong Kong: Current account refers to visible and invisible trade balance only †On a fiscal year basis for India and Bangladesh ‡On a fiscal year basis for India ^Singapore: Slope of SGD NEER band Note: Australia and New Zealand are not included in the Asia aggregate. Aggregates use chain nominal GDP (USD) weights, except for inflation which uses nominal GDP (PPP) weights for the respective years. 2019, 2020 and 2021 use 2018 weights. FX rates for year-end 2021 is assumption and not forecasts. N/a = not applicable Source: CEIC, HSBC forecasts

GDP (% y-o-y) CPI (% y-o-y)

Source: CEIC, HSBC forecasts (nominal GDP USD weights) Source: CEIC, HSBC forecasts (nominal GDP PPP weights)

0

2

4

6

8

10

0

2

4

6

8

10

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19f 20f 21f

Asia av erage

Asia ex mainland China, India & Japan average

F'cast

% y -o-y % y -o-y

1

2

3

4

5

6

7

8

1

2

3

4

5

6

7

8

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19f 20f 21f

% y -o-y % y -o-y

Asia ex mainland China, India & Japan average

Asia av erage

F'cast

5

Economics ● Asia Q4 2019

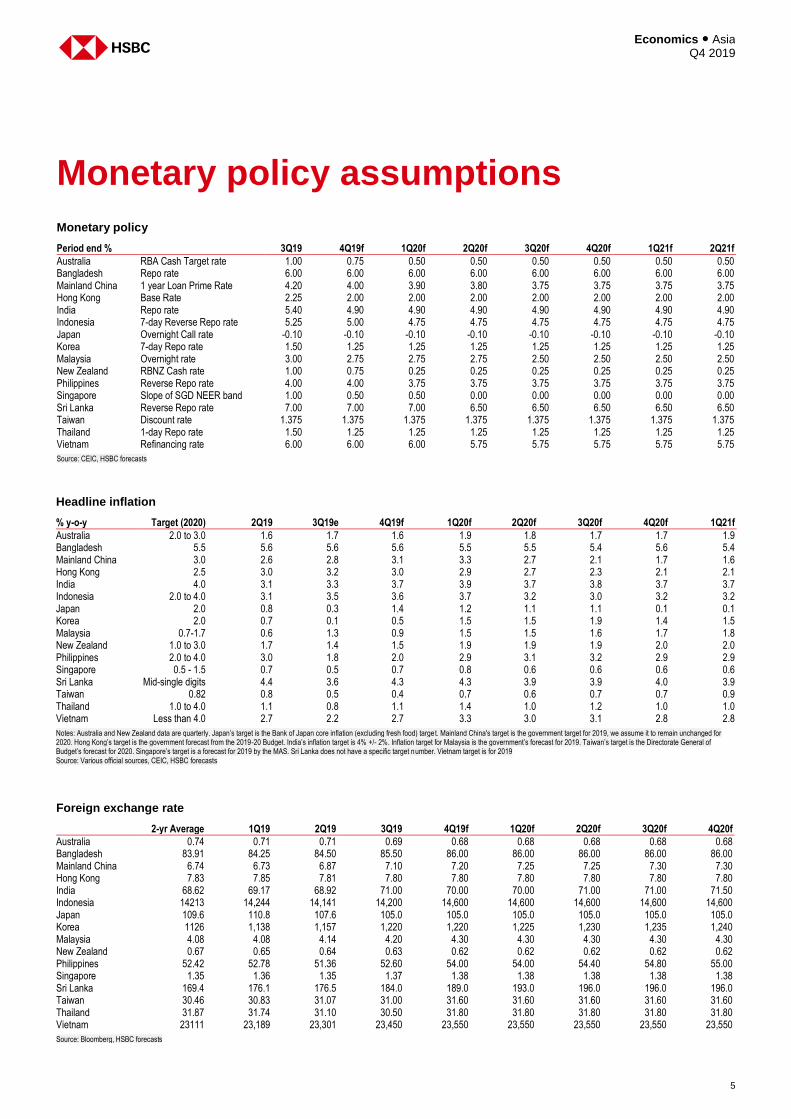

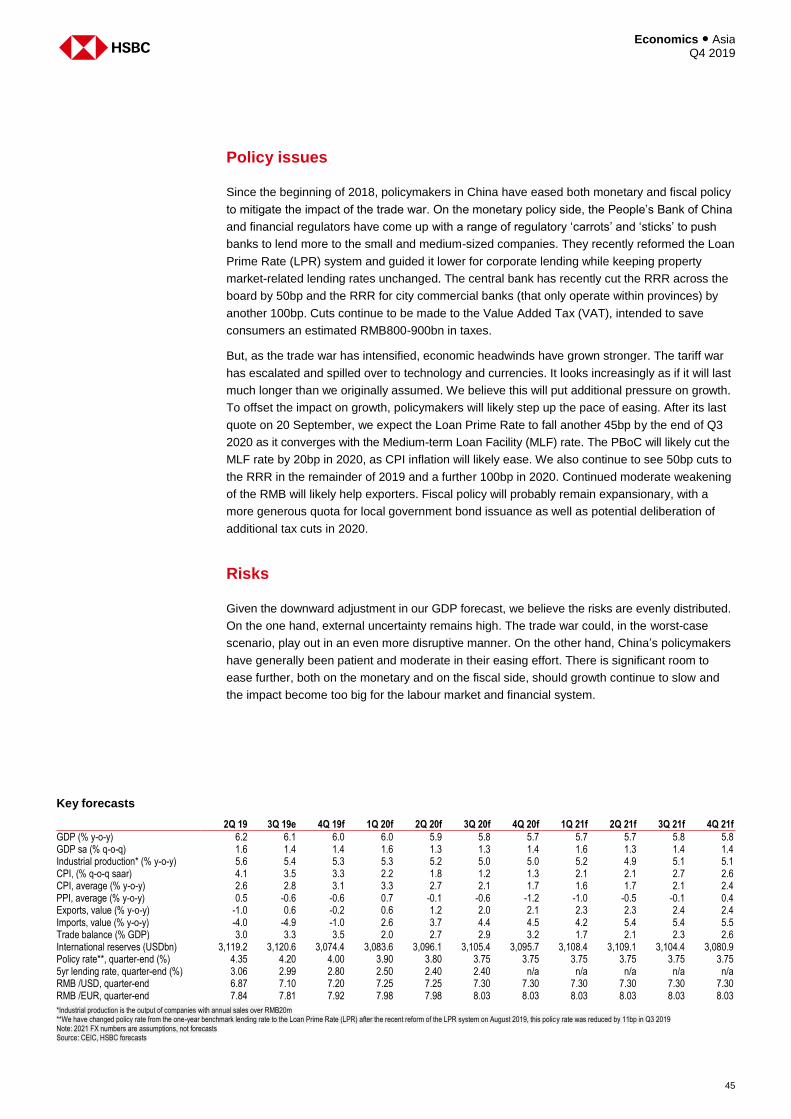

Monetary policy assumptions Monetary policy

Period end % 3Q19 4Q19f 1Q20f 2Q20f 3Q20f 4Q20f 1Q21f 2Q21f

Australia RBA Cash Target rate 1.00 0.75 0.50 0.50 0.50 0.50 0.50 0.50 Bangladesh Repo rate 6.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00 Mainland China 1 year Loan Prime Rate 4.20 4.00 3.90 3.80 3.75 3.75 3.75 3.75 Hong Kong Base Rate 2.25 2.00 2.00 2.00 2.00 2.00 2.00 2.00 India Repo rate 5.40 4.90 4.90 4.90 4.90 4.90 4.90 4.90 Indonesia 7-day Reverse Repo rate 5.25 5.00 4.75 4.75 4.75 4.75 4.75 4.75 Japan Overnight Call rate -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 Korea 7-day Repo rate 1.50 1.25 1.25 1.25 1.25 1.25 1.25 1.25 Malaysia Overnight rate 3.00 2.75 2.75 2.75 2.50 2.50 2.50 2.50 New Zealand RBNZ Cash rate 1.00 0.75 0.25 0.25 0.25 0.25 0.25 0.25 Philippines Reverse Repo rate 4.00 4.00 3.75 3.75 3.75 3.75 3.75 3.75 Singapore Slope of SGD NEER band 1.00 0.50 0.50 0.00 0.00 0.00 0.00 0.00 Sri Lanka Reverse Repo rate 7.00 7.00 7.00 6.50 6.50 6.50 6.50 6.50 Taiwan Discount rate 1.375 1.375 1.375 1.375 1.375 1.375 1.375 1.375 Thailand 1-day Repo rate 1.50 1.25 1.25 1.25 1.25 1.25 1.25 1.25 Vietnam Refinancing rate 6.00 6.00 6.00 5.75 5.75 5.75 5.75 5.75

Source: CEIC, HSBC forecasts

Headline inflation

% y-o-y Target (2020) 2Q19 3Q19e 4Q19f 1Q20f 2Q20f 3Q20f 4Q20f 1Q21f

Australia 2.0 to 3.0 1.6 1.7 1.6 1.9 1.8 1.7 1.7 1.9 Bangladesh 5.5 5.6 5.6 5.6 5.5 5.5 5.4 5.6 5.4 Mainland China 3.0 2.6 2.8 3.1 3.3 2.7 2.1 1.7 1.6 Hong Kong 2.5 3.0 3.2 3.0 2.9 2.7 2.3 2.1 2.1 India 4.0 3.1 3.3 3.7 3.9 3.7 3.8 3.7 3.7 Indonesia 2.0 to 4.0 3.1 3.5 3.6 3.7 3.2 3.0 3.2 3.2 Japan 2.0 0.8 0.3 1.4 1.2 1.1 1.1 0.1 0.1 Korea 2.0 0.7 0.1 0.5 1.5 1.5 1.9 1.4 1.5 Malaysia 0.7-1.7 0.6 1.3 0.9 1.5 1.5 1.6 1.7 1.8 New Zealand 1.0 to 3.0 1.7 1.4 1.5 1.9 1.9 1.9 2.0 2.0 Philippines 2.0 to 4.0 3.0 1.8 2.0 2.9 3.1 3.2 2.9 2.9 Singapore 0.5 - 1.5 0.7 0.5 0.7 0.8 0.6 0.6 0.6 0.6 Sri Lanka Mid-single digits 4.4 3.6 4.3 4.3 3.9 3.9 4.0 3.9 Taiwan 0.82 0.8 0.5 0.4 0.7 0.6 0.7 0.7 0.9 Thailand 1.0 to 4.0 1.1 0.8 1.1 1.4 1.0 1.2 1.0 1.0 Vietnam Less than 4.0 2.7 2.2 2.7 3.3 3.0 3.1 2.8 2.8

Notes: Australia and New Zealand data are quarterly. Japan’s target is the Bank of Japan core inflation (excluding fresh food) targe t. Mainland China's target is the government target for 2019, we assume it to remain unchanged for 2020. Hong Kong’s target is the government forecast from the 2019-20 Budget. India’s inflation target is 4% +/- 2%. Inflation target for Malaysia is the government’s forecast for 2019. Taiwan’s target is the Directorate General of Budget’s forecast for 2020. Singapore’s target is a forecast for 2019 by the MAS. Sri Lanka does not have a specific target number. Vietnam target is for 2019 Source: Various official sources, CEIC, HSBC forecasts

Foreign exchange rate

2-yr Average 1Q19 2Q19 3Q19 4Q19f 1Q20f 2Q20f 3Q20f 4Q20f

Australia 0.74 0.71 0.71 0.69 0.68 0.68 0.68 0.68 0.68 Bangladesh 83.91 84.25 84.50 85.50 86.00 86.00 86.00 86.00 86.00 Mainland China 6.74 6.73 6.87 7.10 7.20 7.25 7.25 7.30 7.30 Hong Kong 7.83 7.85 7.81 7.80 7.80 7.80 7.80 7.80 7.80 India 68.62 69.17 68.92 71.00 70.00 70.00 71.00 71.00 71.50 Indonesia 14213 14,244 14,141 14,200 14,600 14,600 14,600 14,600 14,600 Japan 109.6 110.8 107.6 105.0 105.0 105.0 105.0 105.0 105.0 Korea 1126 1,138 1,157 1,220 1,220 1,225 1,230 1,235 1,240 Malaysia 4.08 4.08 4.14 4.20 4.30 4.30 4.30 4.30 4.30 New Zealand 0.67 0.65 0.64 0.63 0.62 0.62 0.62 0.62 0.62 Philippines 52.42 52.78 51.36 52.60 54.00 54.00 54.40 54.80 55.00 Singapore 1.35 1.36 1.35 1.37 1.38 1.38 1.38 1.38 1.38 Sri Lanka 169.4 176.1 176.5 184.0 189.0 193.0 196.0 196.0 196.0 Taiwan 30.46 30.83 31.07 31.00 31.60 31.60 31.60 31.60 31.60 Thailand 31.87 31.74 31.10 30.50 31.80 31.80 31.80 31.80 31.80 Vietnam 23111 23,189 23,301 23,450 23,550 23,550 23,550 23,550 23,550

Source: Bloomberg, HSBC forecasts

Economics ● Asia Q4 2019

6

Some steadier than others

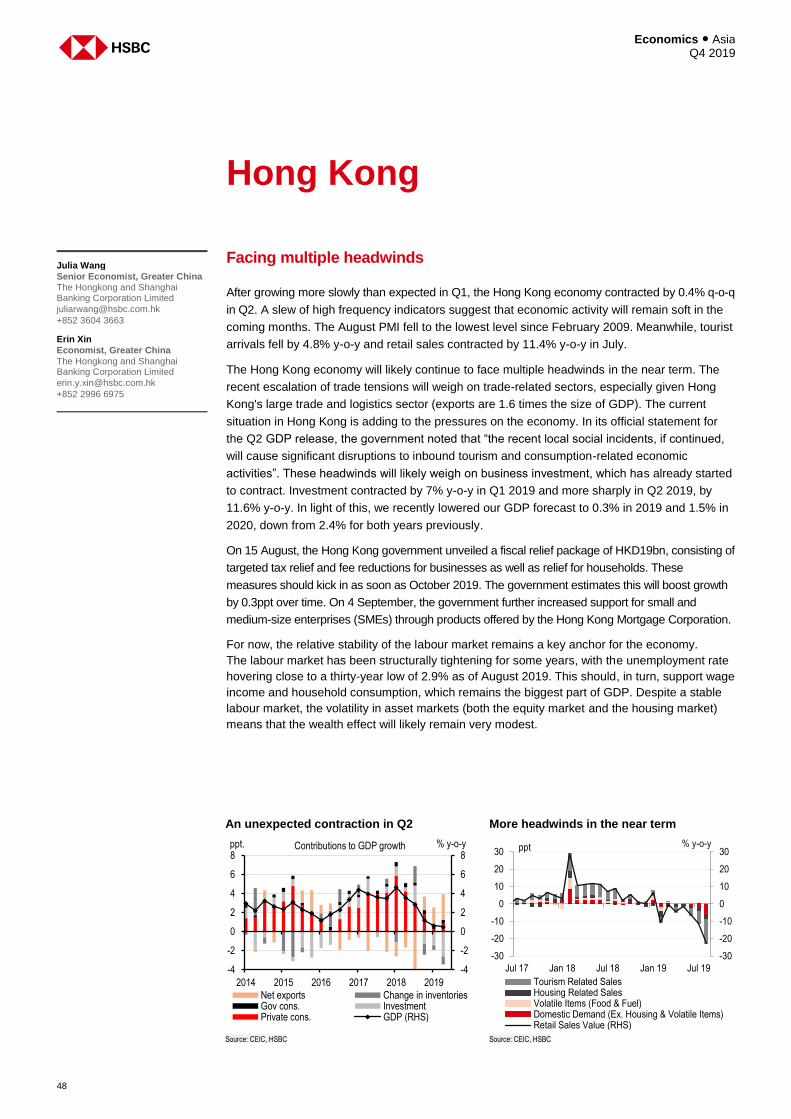

Rough summer. The headlines came hard and fast. The customary seasonal lull that investors

and policymakers once enjoyed seems now part of a cherished past. Tariff tensions escalated

in a matter of days before easing once again; financial markets, not surprisingly, gyrated in a

correspondingly ferocious manner; and the broadly darkening flow of economic data was fitfully

interrupted by tender green shoots.

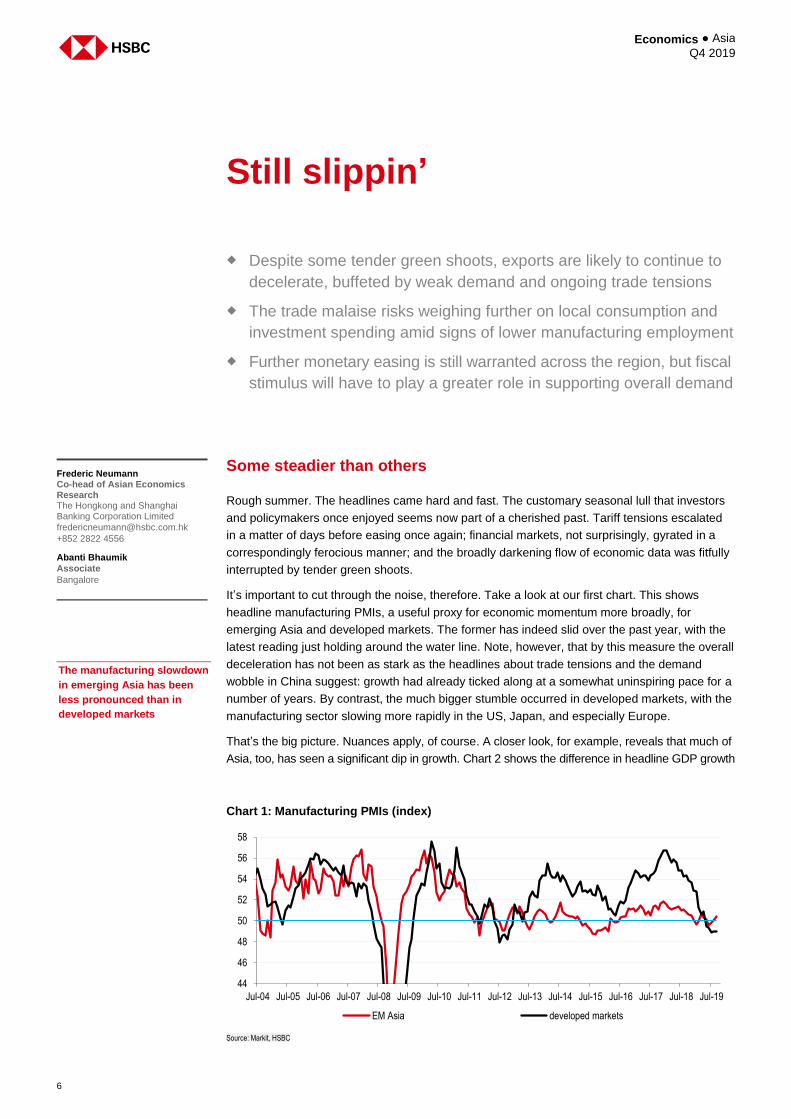

It’s important to cut through the noise, therefore. Take a look at our first chart. This shows

headline manufacturing PMIs, a useful proxy for economic momentum more broadly, for

emerging Asia and developed markets. The former has indeed slid over the past year, with the

latest reading just holding around the water line. Note, however, that by this measure the overall

deceleration has not been as stark as the headlines about trade tensions and the demand

wobble in China suggest: growth had already ticked along at a somewhat uninspiring pace for a

number of years. By contrast, the much bigger stumble occurred in developed markets, with the

manufacturing sector slowing more rapidly in the US, Japan, and especially Europe.

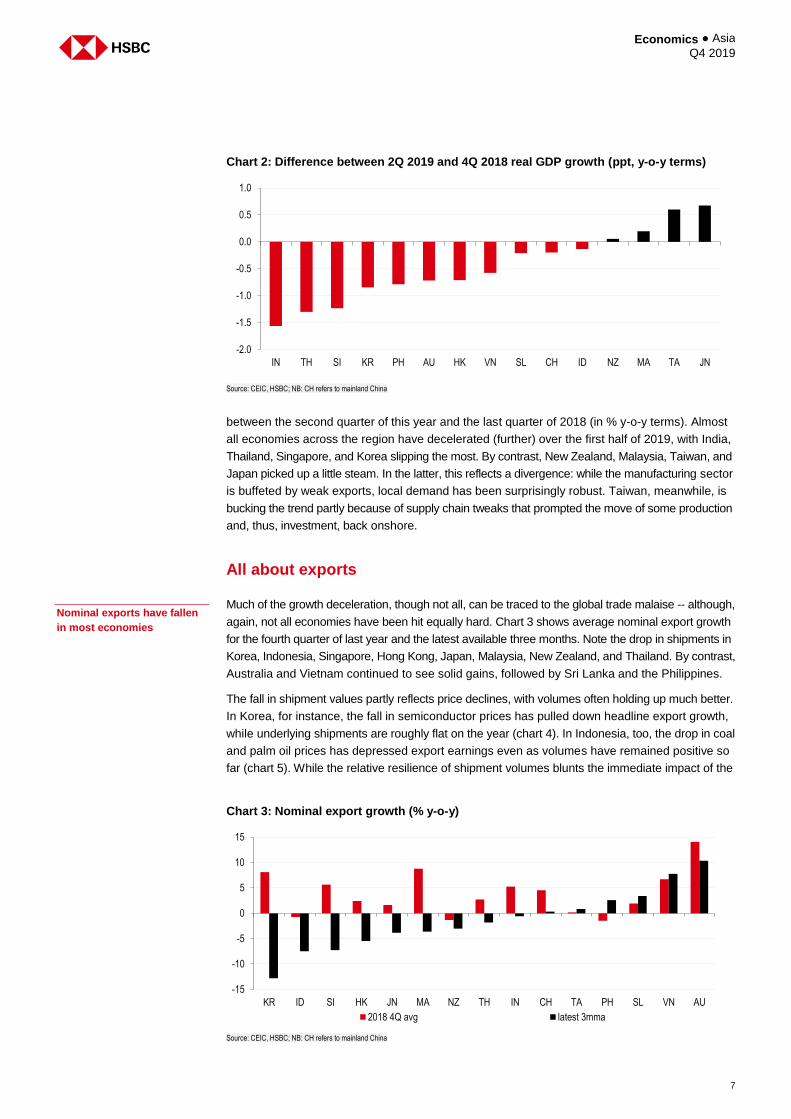

That’s the big picture. Nuances apply, of course. A closer look, for example, reveals that much of

Asia, too, has seen a significant dip in growth. Chart 2 shows the difference in headline GDP growth

Still slippin’

Despite some tender green shoots, exports are likely to continue to

decelerate, buffeted by weak demand and ongoing trade tensions

The trade malaise risks weighing further on local consumption and

investment spending amid signs of lower manufacturing employment

Further monetary easing is still warranted across the region, but fiscal

stimulus will have to play a greater role in supporting overall demand

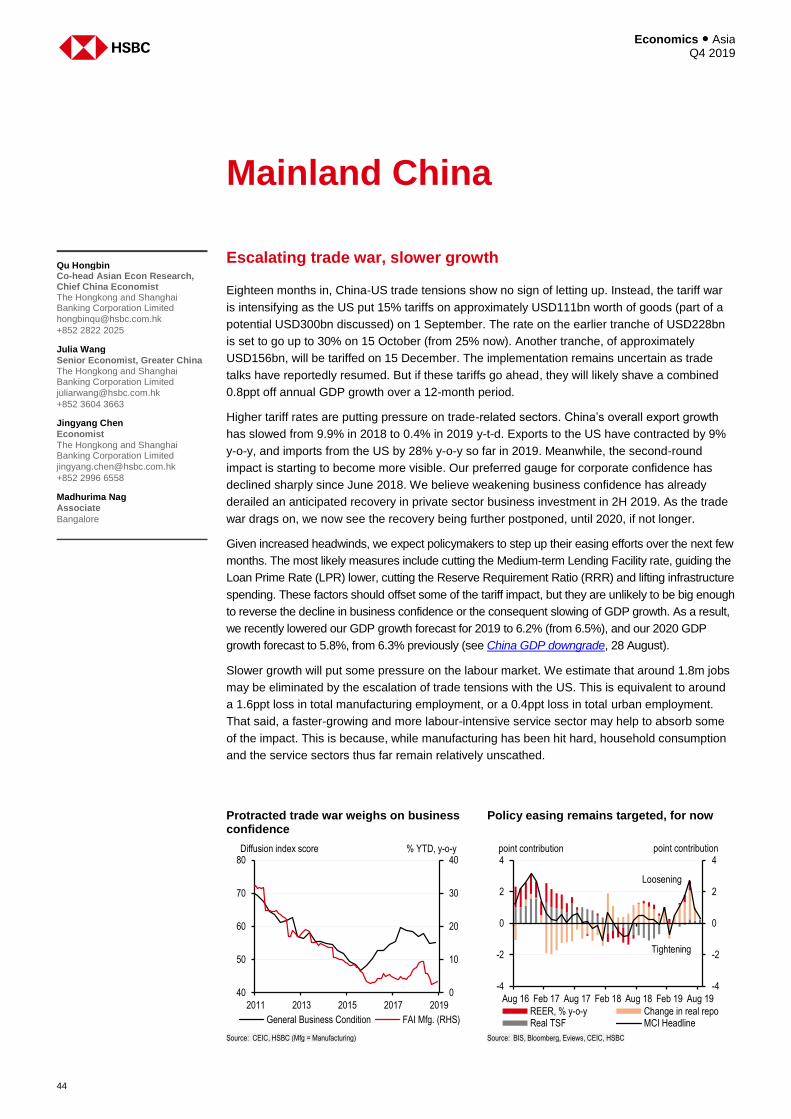

Chart 1: Manufacturing PMIs (index)

Source: Markit, HSBC

Frederic Neumann Co-head of Asian Economics Research The Hongkong and Shanghai Banking Corporation Limited

+852 2822 4556

Abanti Bhaumik

Associate

Bangalore

The manufacturing slowdown

in emerging Asia has been

less pronounced than in

developed markets

44

46

48

50

52

54

56

58

Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 Jul-15 Jul-16 Jul-17 Jul-18 Jul-19

EM Asia developed markets

7

Economics ● Asia Q4 2019

between the second quarter of this year and the last quarter of 2018 (in % y-o-y terms). Almost

all economies across the region have decelerated (further) over the first half of 2019, with India,

Thailand, Singapore, and Korea slipping the most. By contrast, New Zealand, Malaysia, Taiwan, and

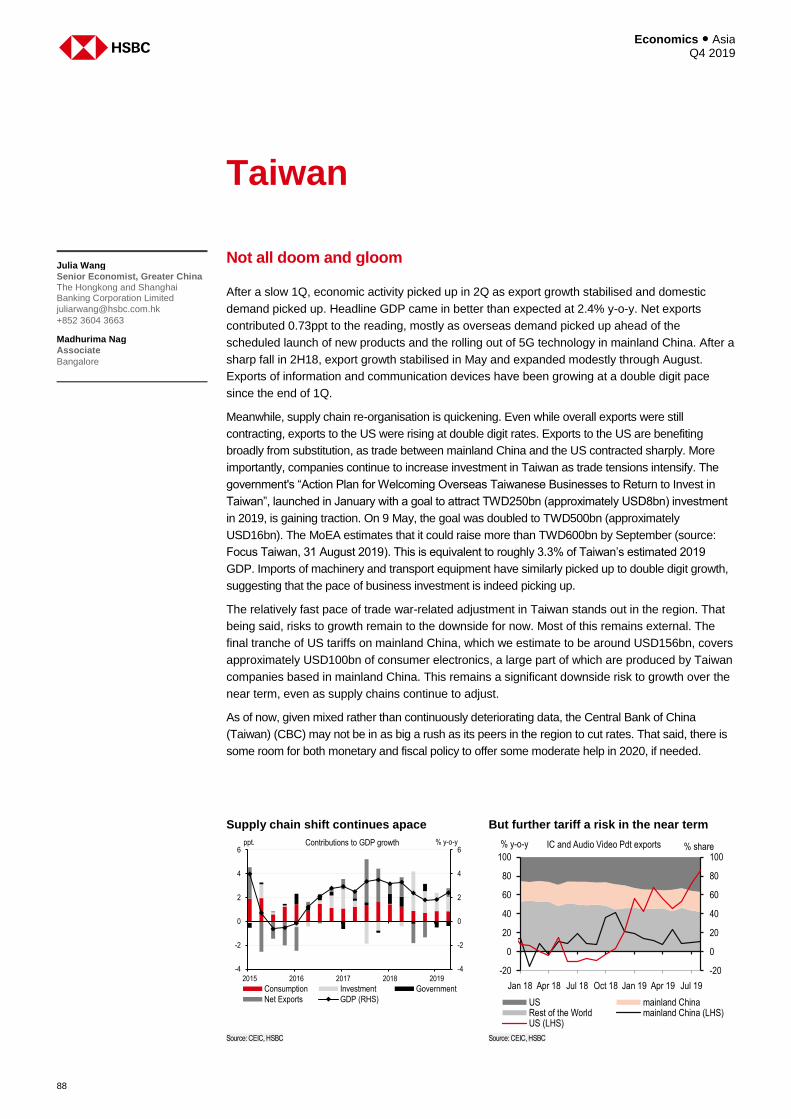

Japan picked up a little steam. In the latter, this reflects a divergence: while the manufacturing sector

is buffeted by weak exports, local demand has been surprisingly robust. Taiwan, meanwhile, is

bucking the trend partly because of supply chain tweaks that prompted the move of some production

and, thus, investment, back onshore.

All about exports

Much of the growth deceleration, though not all, can be traced to the global trade malaise -- although,

again, not all economies have been hit equally hard. Chart 3 shows average nominal export growth

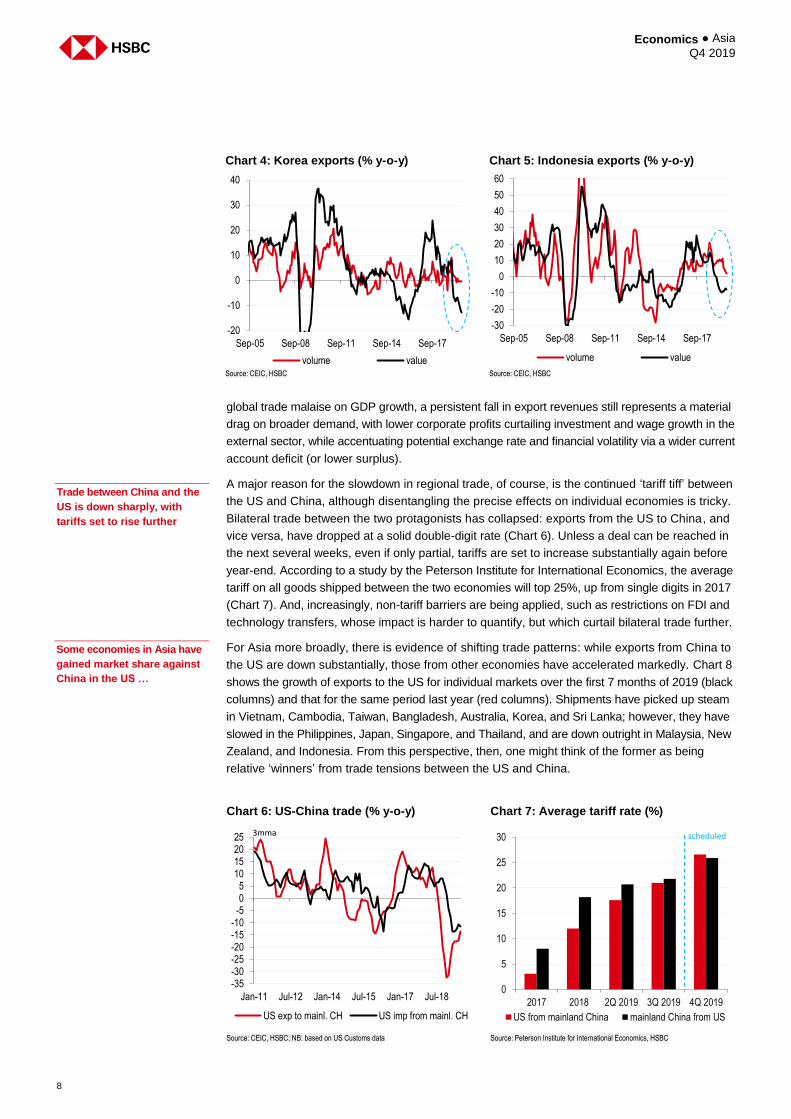

for the fourth quarter of last year and the latest available three months. Note the drop in shipments in

Korea, Indonesia, Singapore, Hong Kong, Japan, Malaysia, New Zealand, and Thailand. By contrast,

Australia and Vietnam continued to see solid gains, followed by Sri Lanka and the Philippines.

The fall in shipment values partly reflects price declines, with volumes often holding up much better.

In Korea, for instance, the fall in semiconductor prices has pulled down headline export growth,

while underlying shipments are roughly flat on the year (chart 4). In Indonesia, too, the drop in coal

and palm oil prices has depressed export earnings even as volumes have remained positive so

far (chart 5). While the relative resilience of shipment volumes blunts the immediate impact of the

Chart 2: Difference between 2Q 2019 and 4Q 2018 real GDP growth (ppt, y-o-y terms)

Source: CEIC, HSBC; NB: CH refers to mainland China

Chart 3: Nominal export growth (% y-o-y)

Source: CEIC, HSBC; NB: CH refers to mainland China

Nominal exports have fallen

in most economies

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

IN TH SI KR PH AU HK VN SL CH ID NZ MA TA JN

-15

-10

-5

0

5

10

15

KR ID SI HK JN MA NZ TH IN CH TA PH SL VN AU

2018 4Q avg latest 3mma

Economics ● Asia Q4 2019

8

global trade malaise on GDP growth, a persistent fall in export revenues still represents a material

drag on broader demand, with lower corporate profits curtailing investment and wage growth in the

external sector, while accentuating potential exchange rate and financial volatility via a wider current

account deficit (or lower surplus).

A major reason for the slowdown in regional trade, of course, is the continued ‘tariff tiff’ between

the US and China, although disentangling the precise effects on individual economies is tricky.

Bilateral trade between the two protagonists has collapsed: exports from the US to China, and

vice versa, have dropped at a solid double-digit rate (Chart 6). Unless a deal can be reached in

the next several weeks, even if only partial, tariffs are set to increase substantially again before

year-end. According to a study by the Peterson Institute for International Economics, the average

tariff on all goods shipped between the two economies will top 25%, up from single digits in 2017

(Chart 7). And, increasingly, non-tariff barriers are being applied, such as restrictions on FDI and

technology transfers, whose impact is harder to quantify, but which curtail bilateral trade further.

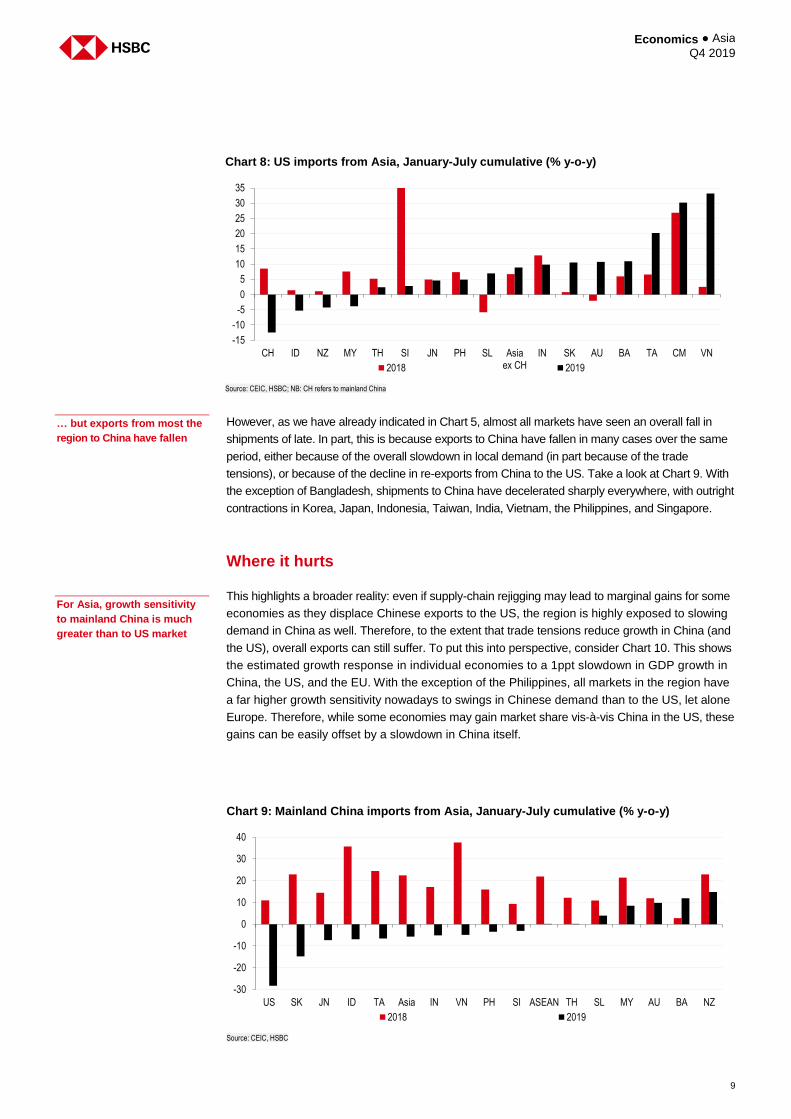

For Asia more broadly, there is evidence of shifting trade patterns: while exports from China to

the US are down substantially, those from other economies have accelerated markedly. Chart 8

shows the growth of exports to the US for individual markets over the first 7 months of 2019 (black

columns) and that for the same period last year (red columns). Shipments have picked up steam

in Vietnam, Cambodia, Taiwan, Bangladesh, Australia, Korea, and Sri Lanka; however, they have

slowed in the Philippines, Japan, Singapore, and Thailand, and are down outright in Malaysia, New

Zealand, and Indonesia. From this perspective, then, one might think of the former as being

relative ‘winners’ from trade tensions between the US and China.

Chart 4: Korea exports (% y-o-y) Chart 5: Indonesia exports (% y-o-y)

Source: CEIC, HSBC Source: CEIC, HSBC

Trade between China and the

US is down sharply, with

tariffs set to rise further

Chart 6: US-China trade (% y-o-y) Chart 7: Average tariff rate (%)

Source: CEIC, HSBC; NB: based on US Customs data Source: Peterson Institute for International Economics, HSBC

Some economies in Asia have

gained market share against

China in the US …

-20

-10

0

10

20

30

40

Sep-05 Sep-08 Sep-11 Sep-14 Sep-17

volume value

-30

-20

-10

0

10

20

30

40

50

60

Sep-05 Sep-08 Sep-11 Sep-14 Sep-17

volume value

-35-30-25-20-15-10-505

10152025

Jan-11 Jul-12 Jan-14 Jul-15 Jan-17 Jul-18

US exp to mainl. CH US imp from mainl. CH

3mma

0

5

10

15

20

25

30

2017 2018 2Q 2019 3Q 2019 4Q 2019

US from mainland China mainland China from US

scheduled

9

Economics ● Asia Q4 2019

However, as we have already indicated in Chart 5, almost all markets have seen an overall fall in

shipments of late. In part, this is because exports to China have fallen in many cases over the same

period, either because of the overall slowdown in local demand (in part because of the trade

tensions), or because of the decline in re-exports from China to the US. Take a look at Chart 9. With

the exception of Bangladesh, shipments to China have decelerated sharply everywhere, with outright

contractions in Korea, Japan, Indonesia, Taiwan, India, Vietnam, the Philippines, and Singapore.

Where it hurts

This highlights a broader reality: even if supply-chain rejigging may lead to marginal gains for some

economies as they displace Chinese exports to the US, the region is highly exposed to slowing

demand in China as well. Therefore, to the extent that trade tensions reduce growth in China (and

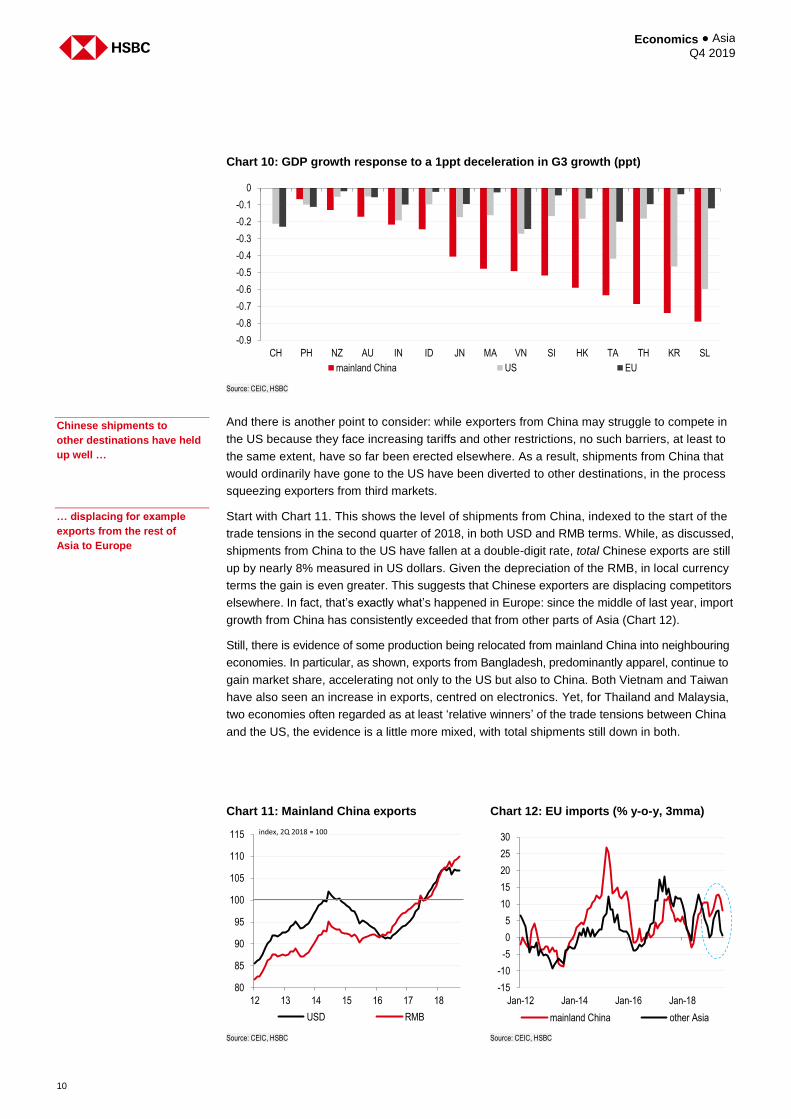

the US), overall exports can still suffer. To put this into perspective, consider Chart 10. This shows

the estimated growth response in individual economies to a 1ppt slowdown in GDP growth in

China, the US, and the EU. With the exception of the Philippines, all markets in the region have

a far higher growth sensitivity nowadays to swings in Chinese demand than to the US, let alone

Europe. Therefore, while some economies may gain market share vis-à-vis China in the US, these

gains can be easily offset by a slowdown in China itself.

Chart 8: US imports from Asia, January-July cumulative (% y-o-y)

Source: CEIC, HSBC; NB: CH refers to mainland China

… but exports from most the

region to China have fallen

Chart 9: Mainland China imports from Asia, January-July cumulative (% y-o-y)

Source: CEIC, HSBC

For Asia, growth sensitivity

to mainland China is much

greater than to US market

-15

-10

-5

0

5

10

15

20

25

30

35

CH ID NZ MY TH SI JN PH SL Asiaex CH

IN SK AU BA TA CM VN

2018 2019

-30

-20

-10

0

10

20

30

40

US SK JN ID TA Asia IN VN PH SI ASEAN TH SL MY AU BA NZ

2018 2019

Economics ● Asia Q4 2019

10

And there is another point to consider: while exporters from China may struggle to compete in

the US because they face increasing tariffs and other restrictions, no such barriers, at least to

the same extent, have so far been erected elsewhere. As a result, shipments from China that

would ordinarily have gone to the US have been diverted to other destinations, in the process

squeezing exporters from third markets.

Start with Chart 11. This shows the level of shipments from China, indexed to the start of the

trade tensions in the second quarter of 2018, in both USD and RMB terms. While, as discussed,

shipments from China to the US have fallen at a double-digit rate, total Chinese exports are still

up by nearly 8% measured in US dollars. Given the depreciation of the RMB, in local currency

terms the gain is even greater. This suggests that Chinese exporters are displacing competitors

elsewhere. In fact, that’s exactly what’s happened in Europe: since the middle of last year, import

growth from China has consistently exceeded that from other parts of Asia (Chart 12).

Still, there is evidence of some production being relocated from mainland China into neighbouring

economies. In particular, as shown, exports from Bangladesh, predominantly apparel, continue to

gain market share, accelerating not only to the US but also to China. Both Vietnam and Taiwan

have also seen an increase in exports, centred on electronics. Yet, for Thailand and Malaysia,

two economies often regarded as at least ‘relative winners’ of the trade tensions between China

and the US, the evidence is a little more mixed, with total shipments still down in both.

Chart 10: GDP growth response to a 1ppt deceleration in G3 growth (ppt)

Source: CEIC, HSBC

Chinese shipments to

other destinations have held

up well …

Chart 11: Mainland China exports Chart 12: EU imports (% y-o-y, 3mma)

Source: CEIC, HSBC Source: CEIC, HSBC

… displacing for example

exports from the rest of

Asia to Europe

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

CH PH NZ AU IN ID JN MA VN SI HK TA TH KR SL

mainland China US EU

80

85

90

95

100

105

110

115

12 13 14 15 16 17 18

USD RMB

index, 2Q 2018 = 100

-15

-10

-5

0

5

10

15

20

25

30

Jan-12 Jan-14 Jan-16 Jan-18

mainland China other Asia

11

Economics ● Asia Q4 2019

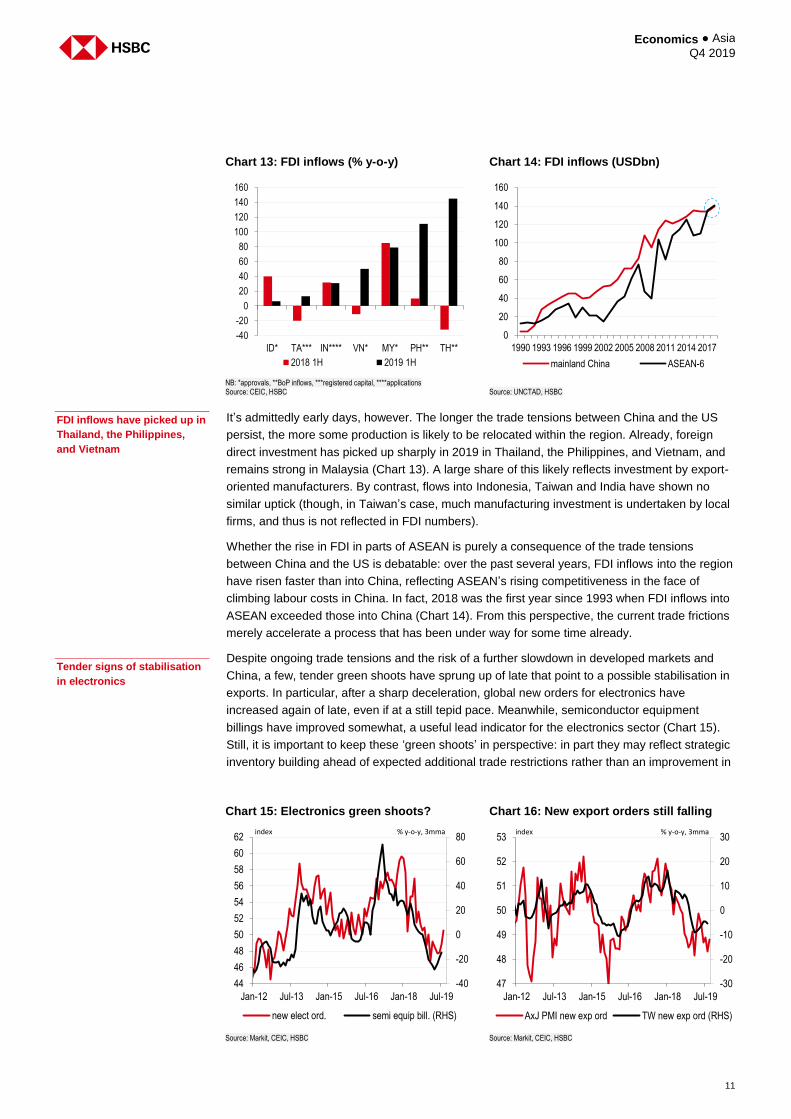

It’s admittedly early days, however. The longer the trade tensions between China and the US

persist, the more some production is likely to be relocated within the region. Already, foreign

direct investment has picked up sharply in 2019 in Thailand, the Philippines, and Vietnam, and

remains strong in Malaysia (Chart 13). A large share of this likely reflects investment by export-

oriented manufacturers. By contrast, flows into Indonesia, Taiwan and India have shown no

similar uptick (though, in Taiwan’s case, much manufacturing investment is undertaken by local

firms, and thus is not reflected in FDI numbers).

Whether the rise in FDI in parts of ASEAN is purely a consequence of the trade tensions

between China and the US is debatable: over the past several years, FDI inflows into the region

have risen faster than into China, reflecting ASEAN’s rising competitiveness in the face of

climbing labour costs in China. In fact, 2018 was the first year since 1993 when FDI inflows into

ASEAN exceeded those into China (Chart 14). From this perspective, the current trade frictions

merely accelerate a process that has been under way for some time already.

Despite ongoing trade tensions and the risk of a further slowdown in developed markets and

China, a few, tender green shoots have sprung up of late that point to a possible stabilisation in

exports. In particular, after a sharp deceleration, global new orders for electronics have

increased again of late, even if at a still tepid pace. Meanwhile, semiconductor equipment

billings have improved somewhat, a useful lead indicator for the electronics sector (Chart 15).

Still, it is important to keep these ‘green shoots’ in perspective: in part they may reflect strategic

inventory building ahead of expected additional trade restrictions rather than an improvement in

Chart 13: FDI inflows (% y-o-y) Chart 14: FDI inflows (USDbn)

NB: *approvals, **BoP inflows, ***registered capital, ****applications Source: CEIC, HSBC

Source: UNCTAD, HSBC

FDI inflows have picked up in

Thailand, the Philippines,

and Vietnam

Chart 15: Electronics green shoots? Chart 16: New export orders still falling

Source: Markit, CEIC, HSBC Source: Markit, CEIC, HSBC

Tender signs of stabilisation

in electronics

-40

-20

0

20

40

60

80

100

120

140

160

ID* TA*** IN**** VN* MY* PH** TH**

2018 1H 2019 1H

0

20

40

60

80

100

120

140

160

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Tho

usan

ds

mainland China ASEAN-6

-40

-20

0

20

40

60

80

44

46

48

50

52

54

56

58

60

62

Jan-12 Jul-13 Jan-15 Jul-16 Jan-18 Jul-19

new elect ord. semi equip bill. (RHS)

index % y-o-y, 3mma

-30

-20

-10

0

10

20

30

47

48

49

50

51

52

53

Jan-12 Jul-13 Jan-15 Jul-16 Jan-18 Jul-19

AxJ PMI new exp ord TW new exp ord (RHS)

index % y-o-y, 3mma

Economics ● Asia Q4 2019

12

underlying demand. In fact, Taiwan’s official new export orders have yet to show positive annual

growth, and average new export orders for the regional manufacturing sector remain close to

their cycle low (Chart 16).

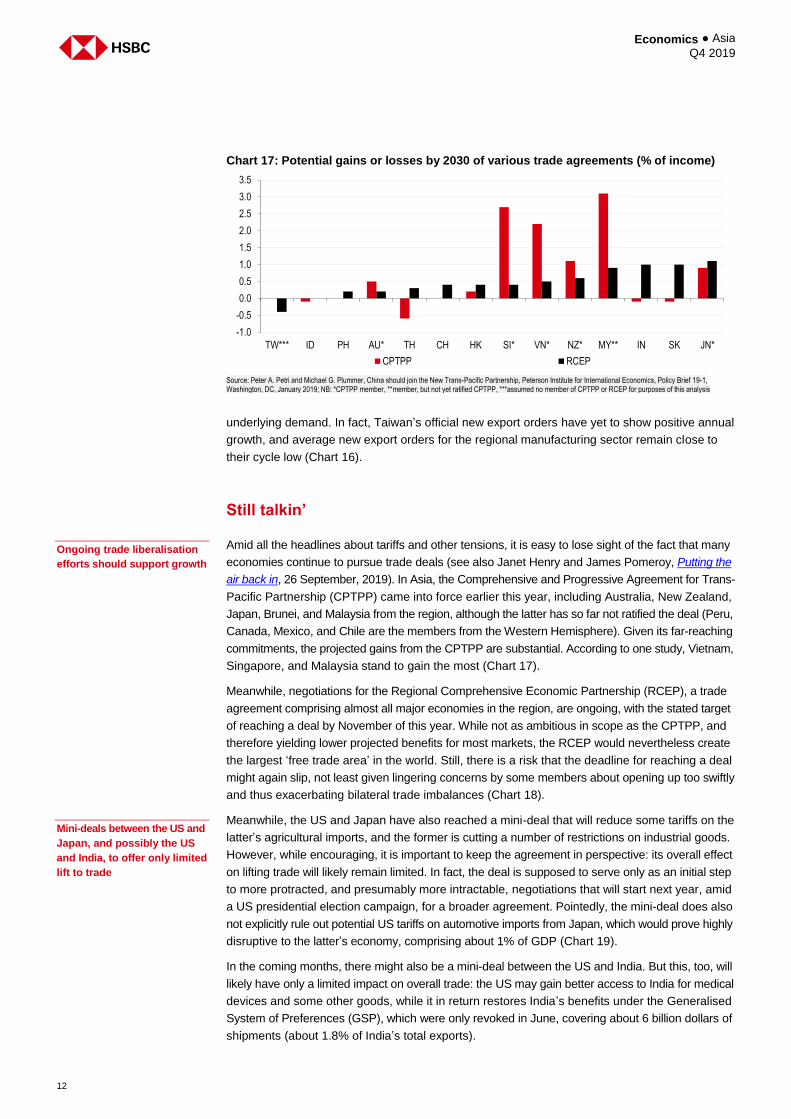

Still talkin’

Amid all the headlines about tariffs and other tensions, it is easy to lose sight of the fact that many

economies continue to pursue trade deals (see also Janet Henry and James Pomeroy, Putting the

air back in, 26 September, 2019). In Asia, the Comprehensive and Progressive Agreement for Trans-

Pacific Partnership (CPTPP) came into force earlier this year, including Australia, New Zealand,

Japan, Brunei, and Malaysia from the region, although the latter has so far not ratified the deal (Peru,

Canada, Mexico, and Chile are the members from the Western Hemisphere). Given its far-reaching

commitments, the projected gains from the CPTPP are substantial. According to one study, Vietnam,

Singapore, and Malaysia stand to gain the most (Chart 17).

Meanwhile, negotiations for the Regional Comprehensive Economic Partnership (RCEP), a trade

agreement comprising almost all major economies in the region, are ongoing, with the stated target

of reaching a deal by November of this year. While not as ambitious in scope as the CPTPP, and

therefore yielding lower projected benefits for most markets, the RCEP would nevertheless create

the largest ‘free trade area’ in the world. Still, there is a risk that the deadline for reaching a deal

might again slip, not least given lingering concerns by some members about opening up too swiftly

and thus exacerbating bilateral trade imbalances (Chart 18).

Meanwhile, the US and Japan have also reached a mini-deal that will reduce some tariffs on the

latter’s agricultural imports, and the former is cutting a number of restrictions on industrial goods.

However, while encouraging, it is important to keep the agreement in perspective: its overall effect

on lifting trade will likely remain limited. In fact, the deal is supposed to serve only as an initial step

to more protracted, and presumably more intractable, negotiations that will start next year, amid

a US presidential election campaign, for a broader agreement. Pointedly, the mini-deal does also

not explicitly rule out potential US tariffs on automotive imports from Japan, which would prove highly

disruptive to the latter’s economy, comprising about 1% of GDP (Chart 19).

In the coming months, there might also be a mini-deal between the US and India. But this, too, will

likely have only a limited impact on overall trade: the US may gain better access to India for medical

devices and some other goods, while it in return restores India’s benefits under the Generalised

System of Preferences (GSP), which were only revoked in June, covering about 6 billion dollars of

shipments (about 1.8% of India’s total exports).

Chart 17: Potential gains or losses by 2030 of various trade agreements (% of income)

Source: Peter A. Petri and Michael G. Plummer, China should join the New Trans-Pacific Partnership, Peterson Institute for International Economics, Policy Brief 19-1, Washington, DC, January 2019; NB: *CPTPP member, **member, but not yet ratified CPTPP, ***assumed no member of CPTPP or RCEP for purposes of this analysis

Ongoing trade liberalisation

efforts should support growth

Mini-deals between the US and

Japan, and possibly the US

and India, to offer only limited

lift to trade

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

TW*** ID PH AU* TH CH HK SI* VN* NZ* MY** IN SK JN*

CPTPP RCEP

13

Economics ● Asia Q4 2019

Wobbles spreadin’

The longer the softness in exports and, hence, manufacturing, persists across the region, the

bigger the risk it will drag down domestic demand further. Already, private consumption and

investment have pulled back in many economies: Chart 20 shows the difference in growth

between the second quarter of this year and the last quarter of 2018 (in y-o-y terms). While

elections or public spending-related uncertainties may have held back especially investment in

the Philippines, India, Thailand, Australia, and Indonesia, ongoing trade tensions may cap any

potential rebound. Meanwhile, private consumption has decelerated as well in most economies, a

process that is less readily attributable to temporary domestic political or budgetary uncertainty.

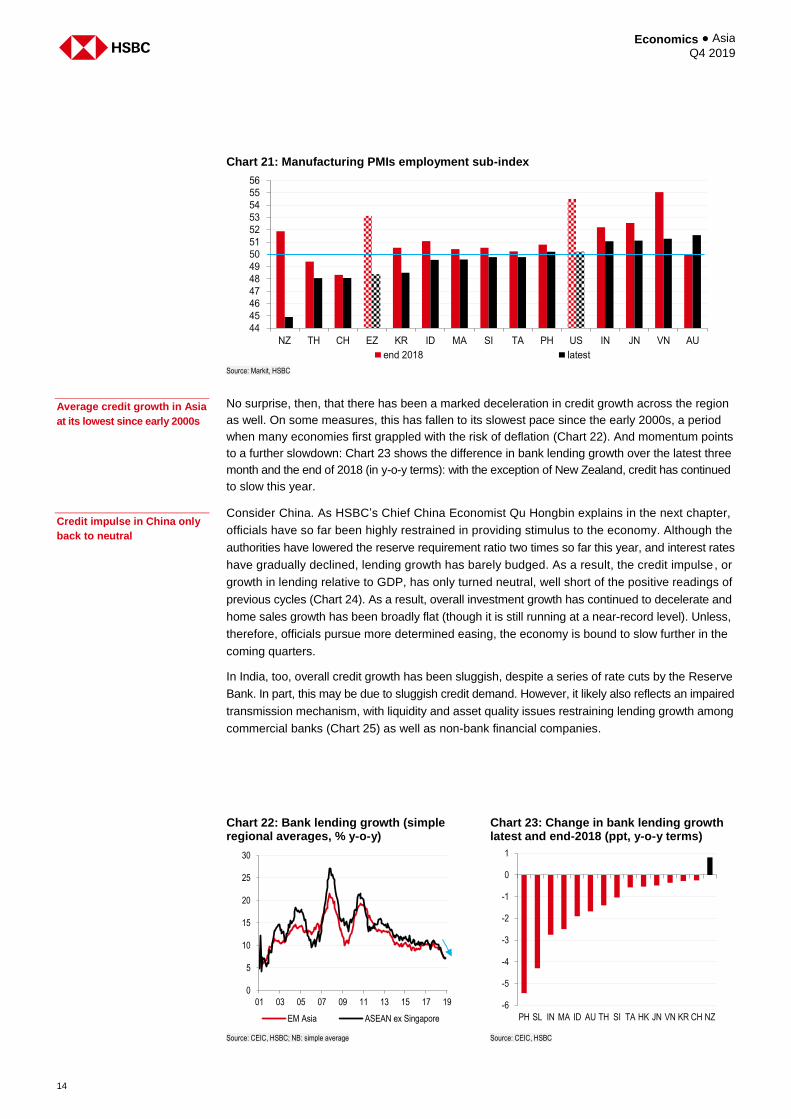

In fact, the latter may reflect growing worries about job prospects. Amid sluggish manufacturing,

companies have started to shed workers, even if at a still relatively gradual pace. Chart 21 shows

the employment sub-index of individual manufacturing PMIs, comparing the average reading for

the fourth quarter of 2018 and the last three months. With the exception of Australia’s gauge, all

measures have pulled back, with only the Philippines, India, Japan, and Vietnam still showing some

job growth. Admittedly, the pull-back in Asia hasn’t been as abrupt as in the Eurozone or the US

(with the exception of New Zealand), but given that the sector tends to account for a larger share of

total employment in the region, the impact on overall consumer sentiment is bound to be significant.

Chart 20: Difference between 2Q 2019 and 4Q 2018 real consumption and investment growth (ppt, y-o-y terms)

Source: CEIC, HSBC

Signs of weaker employment

in manufacturing

Private consumption and

investment slowed in much

of Asia in 1H 2019

Chart 18: India trade with mainland China Chart 19: Japan’s auto export to US

Source: CEIC, HSBC Source: CEIC, HSBC

-14

-12

-10

-8

-6

-4

-2

0

2

4

PH IN HK AU TH MA ID JN KR NZ TA SI

private consumption investment

0

10

20

30

40

50

60

70

80

Sep-03 Sep-06 Sep-09 Sep-12 Sep-15 Sep-18

Tho

usan

ds

Exp. to mainl. CH Imp. from mainl. CH

USD bn, 12m rollsum

20

22

24

26

28

30

32

34

36

38

40

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1996 1999 2002 2005 2008 2011 2014 2017

share of GDP share of exports (RHS)

% %

Economics ● Asia Q4 2019

14

No surprise, then, that there has been a marked deceleration in credit growth across the region

as well. On some measures, this has fallen to its slowest pace since the early 2000s, a period

when many economies first grappled with the risk of deflation (Chart 22). And momentum points

to a further slowdown: Chart 23 shows the difference in bank lending growth over the latest three

month and the end of 2018 (in y-o-y terms): with the exception of New Zealand, credit has continued

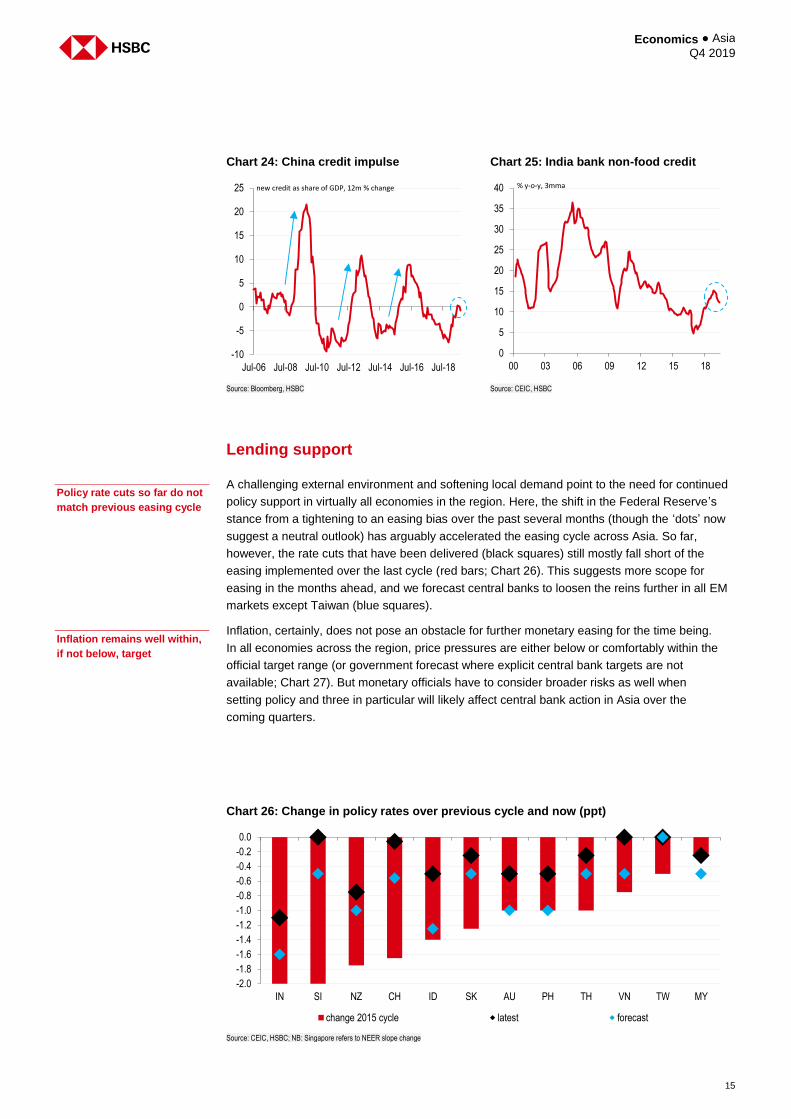

to slow this year. Consider China. As HSBC’s Chief China Economist Qu Hongbin explains in the next chapter,

officials have so far been highly restrained in providing stimulus to the economy. Although the

authorities have lowered the reserve requirement ratio two times so far this year, and interest rates

have gradually declined, lending growth has barely budged. As a result, the credit impulse, or

growth in lending relative to GDP, has only turned neutral, well short of the positive readings of

previous cycles (Chart 24). As a result, overall investment growth has continued to decelerate and

home sales growth has been broadly flat (though it is still running at a near-record level). Unless,

therefore, officials pursue more determined easing, the economy is bound to slow further in the

coming quarters.

In India, too, overall credit growth has been sluggish, despite a series of rate cuts by the Reserve

Bank. In part, this may be due to sluggish credit demand. However, it likely also reflects an impaired

transmission mechanism, with liquidity and asset quality issues restraining lending growth among

commercial banks (Chart 25) as well as non-bank financial companies.

Chart 21: Manufacturing PMIs employment sub-index

Source: Markit, HSBC

Average credit growth in Asia

at its lowest since early 2000s

Chart 22: Bank lending growth (simple regional averages, % y-o-y)

Chart 23: Change in bank lending growth latest and end-2018 (ppt, y-o-y terms)

Source: CEIC, HSBC; NB: simple average Source: CEIC, HSBC

Credit impulse in China only

back to neutral

44

45

46

47

48

49

50

51

52

53

54

55

56

NZ TH CH EZ KR ID MA SI TA PH US IN JN VN AU

end 2018 latest

0

5

10

15

20

25

30

01 03 05 07 09 11 13 15 17 19

EM Asia ASEAN ex Singapore

-6

-5

-4

-3

-2

-1

0

1

PH SL IN MA ID AU TH SI TA HK JN VN KR CH NZ

15

Economics ● Asia Q4 2019

Lending support

A challenging external environment and softening local demand point to the need for continued

policy support in virtually all economies in the region. Here, the shift in the Federal Reserve’s

stance from a tightening to an easing bias over the past several months (though the ‘dots’ now

suggest a neutral outlook) has arguably accelerated the easing cycle across Asia. So far,

however, the rate cuts that have been delivered (black squares) still mostly fall short of the

easing implemented over the last cycle (red bars; Chart 26). This suggests more scope for

easing in the months ahead, and we forecast central banks to loosen the reins further in all EM

markets except Taiwan (blue squares).

Inflation, certainly, does not pose an obstacle for further monetary easing for the time being.

In all economies across the region, price pressures are either below or comfortably within the

official target range (or government forecast where explicit central bank targets are not

available; Chart 27). But monetary officials have to consider broader risks as well when

setting policy and three in particular will likely affect central bank action in Asia over the

coming quarters.

Chart 24: China credit impulse Chart 25: India bank non-food credit

Source: Bloomberg, HSBC Source: CEIC, HSBC

Policy rate cuts so far do not

match previous easing cycle

Inflation remains well within,

if not below, target

Chart 26: Change in policy rates over previous cycle and now (ppt)

Source: CEIC, HSBC; NB: Singapore refers to NEER slope change

-10

-5

0

5

10

15

20

25

Jul-06 Jul-08 Jul-10 Jul-12 Jul-14 Jul-16 Jul-18

new credit as share of GDP, 12m % change

0

5

10

15

20

25

30

35

40

00 03 06 09 12 15 18

% y-o-y, 3mma

-2.0

-1.8

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

IN SI NZ CH ID SK AU PH TH VN TW MY

change 2015 cycle latest forecast

Economics ● Asia Q4 2019

16

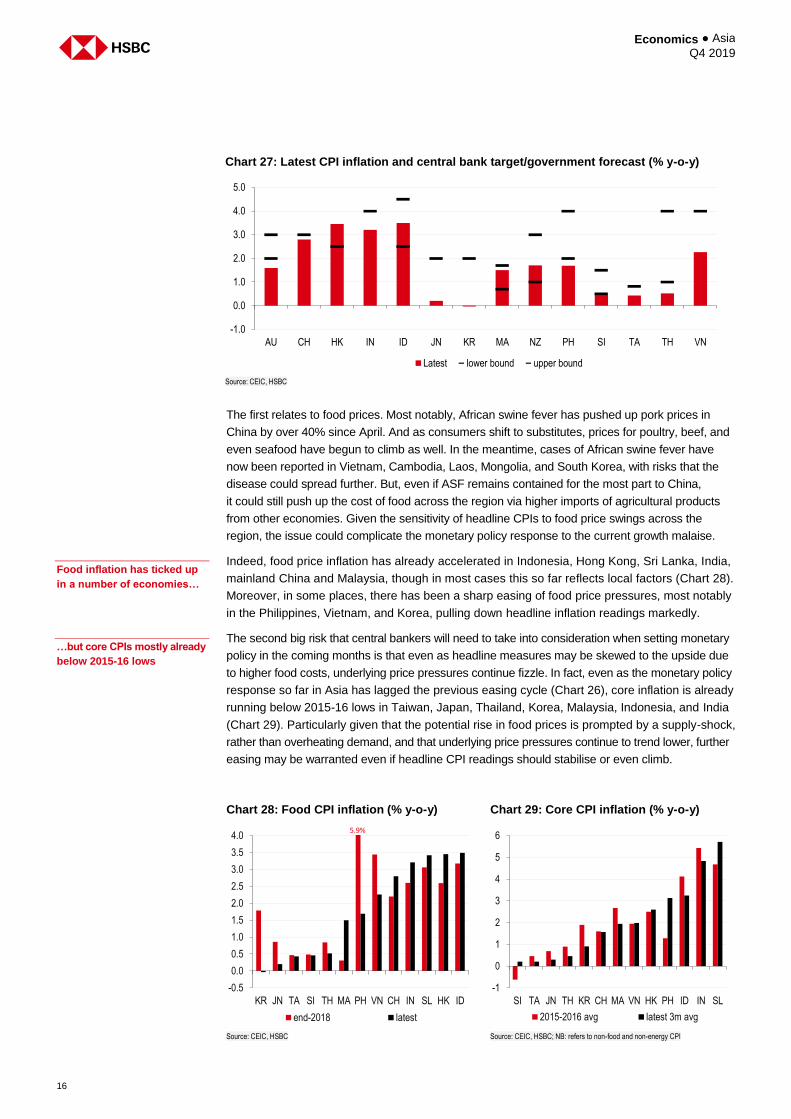

The first relates to food prices. Most notably, African swine fever has pushed up pork prices in

China by over 40% since April. And as consumers shift to substitutes, prices for poultry, beef, and

even seafood have begun to climb as well. In the meantime, cases of African swine fever have

now been reported in Vietnam, Cambodia, Laos, Mongolia, and South Korea, with risks that the

disease could spread further. But, even if ASF remains contained for the most part to China,

it could still push up the cost of food across the region via higher imports of agricultural products

from other economies. Given the sensitivity of headline CPIs to food price swings across the

region, the issue could complicate the monetary policy response to the current growth malaise.

Indeed, food price inflation has already accelerated in Indonesia, Hong Kong, Sri Lanka, India,

mainland China and Malaysia, though in most cases this so far reflects local factors (Chart 28).

Moreover, in some places, there has been a sharp easing of food price pressures, most notably

in the Philippines, Vietnam, and Korea, pulling down headline inflation readings markedly.

The second big risk that central bankers will need to take into consideration when setting monetary

policy in the coming months is that even as headline measures may be skewed to the upside due

to higher food costs, underlying price pressures continue fizzle. In fact, even as the monetary policy

response so far in Asia has lagged the previous easing cycle (Chart 26), core inflation is already

running below 2015-16 lows in Taiwan, Japan, Thailand, Korea, Malaysia, Indonesia, and India

(Chart 29). Particularly given that the potential rise in food prices is prompted by a supply-shock,

rather than overheating demand, and that underlying price pressures continue to trend lower, further

easing may be warranted even if headline CPI readings should stabilise or even climb.

Chart 27: Latest CPI inflation and central bank target/government forecast (% y-o-y)

Source: CEIC, HSBC

Food inflation has ticked up

in a number of economies…

…but core CPIs mostly already

below 2015-16 lows

Chart 28: Food CPI inflation (% y-o-y) Chart 29: Core CPI inflation (% y-o-y)

Source: CEIC, HSBC Source: CEIC, HSBC; NB: refers to non-food and non-energy CPI

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

AU CH HK IN ID JN KR MA NZ PH SI TA TH VN

Latest lower bound upper bound

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

KR JN TA SI TH MA PH VN CH IN SL HK ID

end-2018 latest

5.9%

-1

0

1

2

3

4

5

6

SI TA JN TH KR CH MA VN HK PH ID IN SL

2015-2016 avg latest 3m avg

17

Economics ● Asia Q4 2019

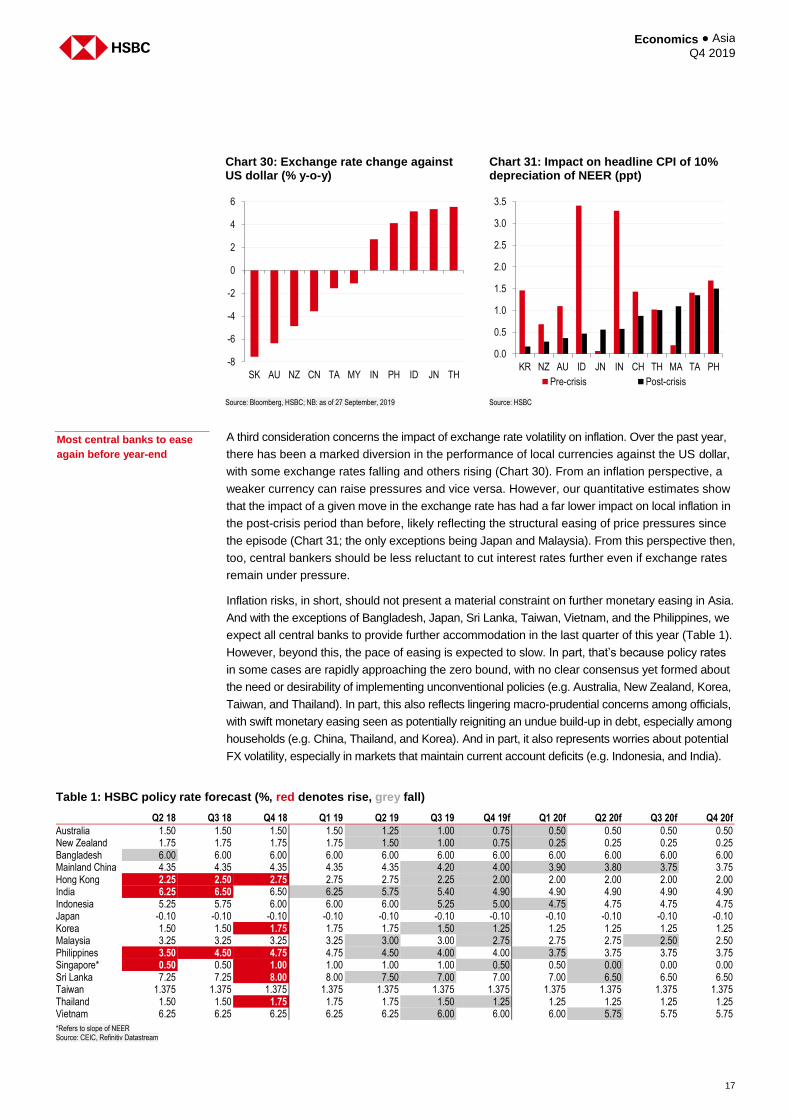

A third consideration concerns the impact of exchange rate volatility on inflation. Over the past year,

there has been a marked diversion in the performance of local currencies against the US dollar,

with some exchange rates falling and others rising (Chart 30). From an inflation perspective, a

weaker currency can raise pressures and vice versa. However, our quantitative estimates show

that the impact of a given move in the exchange rate has had a far lower impact on local inflation in

the post-crisis period than before, likely reflecting the structural easing of price pressures since

the episode (Chart 31; the only exceptions being Japan and Malaysia). From this perspective then,

too, central bankers should be less reluctant to cut interest rates further even if exchange rates

remain under pressure.

Inflation risks, in short, should not present a material constraint on further monetary easing in Asia.

And with the exceptions of Bangladesh, Japan, Sri Lanka, Taiwan, Vietnam, and the Philippines, we

expect all central banks to provide further accommodation in the last quarter of this year (Table 1).

However, beyond this, the pace of easing is expected to slow. In part, that’s because policy rates

in some cases are rapidly approaching the zero bound, with no clear consensus yet formed about

the need or desirability of implementing unconventional policies (e.g. Australia, New Zealand, Korea,

Taiwan, and Thailand). In part, this also reflects lingering macro-prudential concerns among officials,

with swift monetary easing seen as potentially reigniting an undue build-up in debt, especially among

households (e.g. China, Thailand, and Korea). And in part, it also represents worries about potential

FX volatility, especially in markets that maintain current account deficits (e.g. Indonesia, and India).

Chart 30: Exchange rate change against US dollar (% y-o-y)

Chart 31: Impact on headline CPI of 10% depreciation of NEER (ppt)

Source: Bloomberg, HSBC; NB: as of 27 September, 2019 Source: HSBC

Most central banks to ease

again before year-end

Table 1: HSBC policy rate forecast (%, red denotes rise, grey fall)

Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19f Q1 20f Q2 20f Q3 20f Q4 20f

Australia 1.50 1.50 1.50 1.50 1.25 1.00 0.75 0.50 0.50 0.50 0.50 New Zealand 1.75 1.75 1.75 1.75 1.50 1.00 0.75 0.25 0.25 0.25 0.25 Bangladesh 6.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00 Mainland China 4.35 4.35 4.35 4.35 4.35 4.20 4.00 3.90 3.80 3.75 3.75 Hong Kong 2.25 2.50 2.75 2.75 2.75 2.25 2.00 2.00 2.00 2.00 2.00 India 6.25 6.50 6.50 6.25 5.75 5.40 4.90 4.90 4.90 4.90 4.90 Indonesia 5.25 5.75 6.00 6.00 6.00 5.25 5.00 4.75 4.75 4.75 4.75 Japan -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 -0.10 Korea 1.50 1.50 1.75 1.75 1.75 1.50 1.25 1.25 1.25 1.25 1.25 Malaysia 3.25 3.25 3.25 3.25 3.00 3.00 2.75 2.75 2.75 2.50 2.50 Philippines 3.50 4.50 4.75 4.75 4.50 4.00 4.00 3.75 3.75 3.75 3.75 Singapore* 0.50 0.50 1.00 1.00 1.00 1.00 0.50 0.50 0.00 0.00 0.00 Sri Lanka 7.25 7.25 8.00 8.00 7.50 7.00 7.00 7.00 6.50 6.50 6.50 Taiwan 1.375 1.375 1.375 1.375 1.375 1.375 1.375 1.375 1.375 1.375 1.375 Thailand 1.50 1.50 1.75 1.75 1.75 1.50 1.25 1.25 1.25 1.25 1.25 Vietnam 6.25 6.25 6.25 6.25 6.25 6.00 6.00 6.00 5.75 5.75 5.75

*Refers to slope of NEER Source: CEIC, Refinitiv Datastream

-8

-6

-4

-2

0

2

4

6

SK AU NZ CN TA MY IN PH ID JN TH

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

KR NZ AU ID JN IN CH TH MA TA PH

Pre-crisis Post-crisis

Economics ● Asia Q4 2019

18

A bigger push

Broadly, then, monetary policy is starting to lose a bit of its ‘punch’ in Asia. As elsewhere, there is

thus growing pressure for a more determined fiscal push. Already, a number of economies have

implemented sizeable stimulus packages. Earlier this year, Korea and China led the way, with

spending increases and tax cuts, respectively. More recently, India announced a big corporate tax

cut, worth about 0.7% of GDP, and Thailand has unveiled in August a spending and incentive

programme of over USD10bn (see Table 2).

It is important to recognise, however, that headline fiscal support packages do not always translate

into a corresponding lift to growth. For example, tax cuts, whether corporate or personal, may be

saved, rather than spent, amid high debt levels and elevated economic uncertainty. In addition, if

fiscal policy is loosened materially in one year, it can easily turn contractionary the next, especially if

corrective action needs to be taken to balance the books.

While in most economies fiscal policy will provide a positive fiscal impulse next year, this is not

uniformly the case. In Japan, for example, after years of deficit spending, the government proceeded

with a VAT rate increase on 1 October to shore up revenues. This scheduled rise likely pushed up

domestic spending over the previous two quarters, thus explaining the economy’s relative resilience

amid weaker export growth. Despite officials’ plans to cushion the impact with extra spending, the tax

hike is still likely to push the economy into a mild recession in 2020, when the overall fiscal impulse is

estimated to be negative.

Japan’s VAT hike may push

the economy into a mild

recession

Table 2: Fiscal policy outlook

Economy Fiscal plans

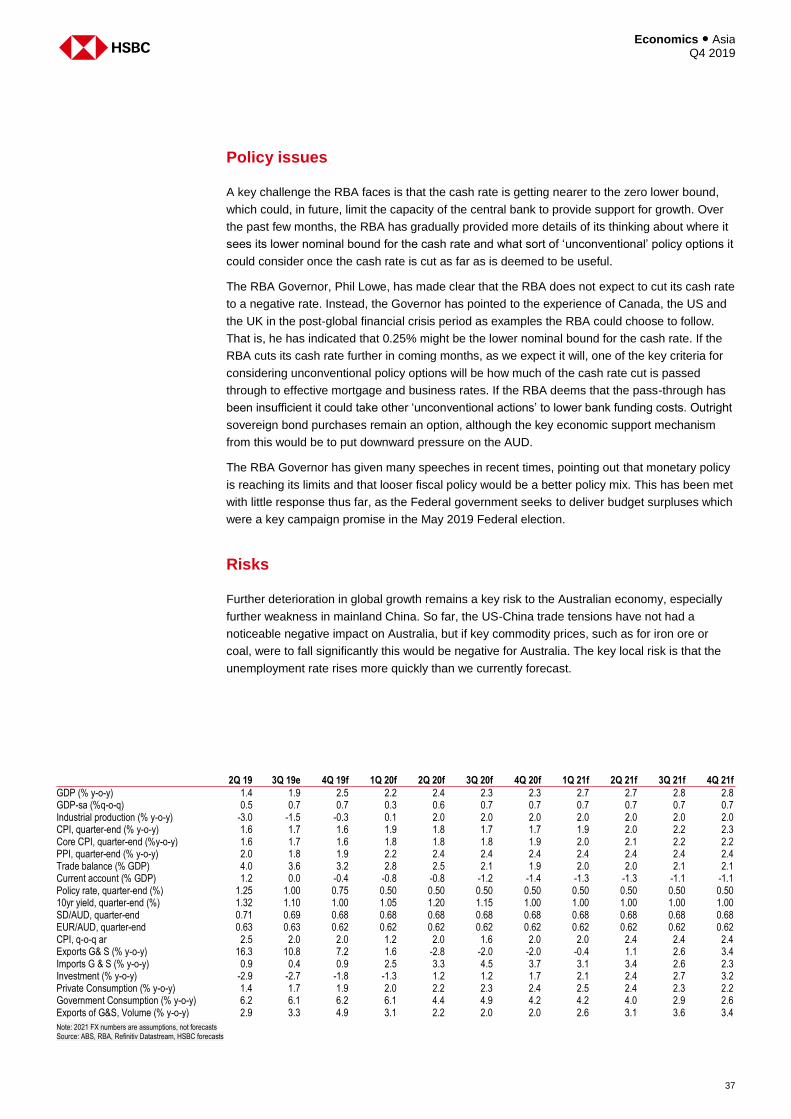

Australia With a budget in balance, low public debt and a triple-A sovereign rating, Australia has plenty of fiscal room to manoeuvre. RBA Governor Lowe has repeatedly suggested that as monetary policy reaches its limits, looser fiscal policy might be a better policy mix. This has been met with little response thus far as the Federal government seeks to deliver budget surpluses which were a key campaign promise in the May 2019 Federal election.

Hong Kong SAR In August, the government unveiled a fiscal package of HKD19bn, consisting of targeted tax relief and fee reductions for businesses and households. These measures were followed by further support for Small and Medium Enterprises (SMEs) through the Hong Kong Mortgage Corporation

India On 20 September, Finance Minister Nirmala Sitharaman announced substantial cuts in the corporate tax rate - the basic rate was cut from 30% to 22% while for new manufacturing firms, it was cut from 25% to 15%, at a cost of INR1450bn (0.7% of GDP) of tax revenues annually.

Indonesia Despite a lower deficit target of 1.8% in 2020, we expect a sizeable overall fiscal impulse due to off-balance sheet SOE spending. The government recently announced plans to gradually cut corporate tax rates from 25% to 20% starting in 2021. Meanwhile, the direct budget impact of the new capital construction, likely to start in 2021, should be manageable with just 19% financed by the budget.

Japan Fiscal policy will turn contractionary after the scheduled consumption tax hike in October. However, the government has rolled out measures to mitigate the negative impact. Even excluding JPY1.3trn set aside to be used in infrastructure projects, the government is set to spend 83% of the new tax revenue, with much of this on a permanent basis. This will be delivered as more support for childcare and seniors and subsidies to medical fees. Temporary measures will be given as rebate schemes for SMEs, vouchers with premiums and support for house and automotive purchases.

Korea Fiscal policy is set to remain supportive, which we think will partly offset the slowdown in growth. The government will focus its increased spending to support innovation, enhance social welfare, and create jobs amid stiffening external headwinds. However, the increased expenditure is expected to come with a hefty bill, as tax revenues may decline 0.9% next year, reflecting weaker collection of corporate tax and fewer real estate transactions.

Mainland China China has stepped up its fiscal stimulus to cushion the economy from the downside risks to growth. It has delivered a fairly sizeable tax cut in 2019, lowering the VAT rate and social security contribution for all corporates by approximately RMB2trn. We expect to see more tax cuts in 2020, which could be an even larger magnitude compared with 2019. Apart from this, local government special bond issuance may also be sped up.

New Zealand New Zealand’s fiscal position remains strong. The 2018/19 surplus looks like it will come in a little larger than forecast, and government debt is very low. The government is likely to come under pressure to loosen fiscal policy further. The 2019/20 spending plans are already stimulatory after this year’s ‘wellbeing’ budget increased the spending allowance. However, this effect is likely to fade from 2020 without further fiscal loosening.

Singapore We expect the government to deliver a highly expansionary FY2020 budget early next year. The fiscal impulse is likely to come in the forms of consumer hand-outs, credits to offset the impact of future Goods and Services Tax hike, and incentives for businesses to prevent payroll reduction.

Taiwan, China The Taiwanese government has been committed to infrastructure spending. Taiwan does have some fiscal policy room, within the constraint of the debt ceiling. W may see a bigger push for expansionary fiscal policy, particularly as Taiwan heads to the polls in January 2020.

Thailand In August, the Thai Cabinet approved a fiscal stimulus package worth USD10.2bn. The measures were wide-ranging, with programs to help low-income households, farmers, the elderly, Small and Medium Enterprises (SMEs), and the tourism sector.

The Philippines The government’s fiscal constraint this year has led to a substantial deceleration in growth. Now that those constraints have been lifted, the government still needs to ramp up spending in the quarters ahead to prevent further growth deterioration. We expect an expansionary fiscal impulse and further monetary loosening to lift growth in 2020 and 2021, but delayed passage of the 2020 budget poses the most significant risk in 2020.

Source: HSBC

19

Economics ● Asia Q4 2019

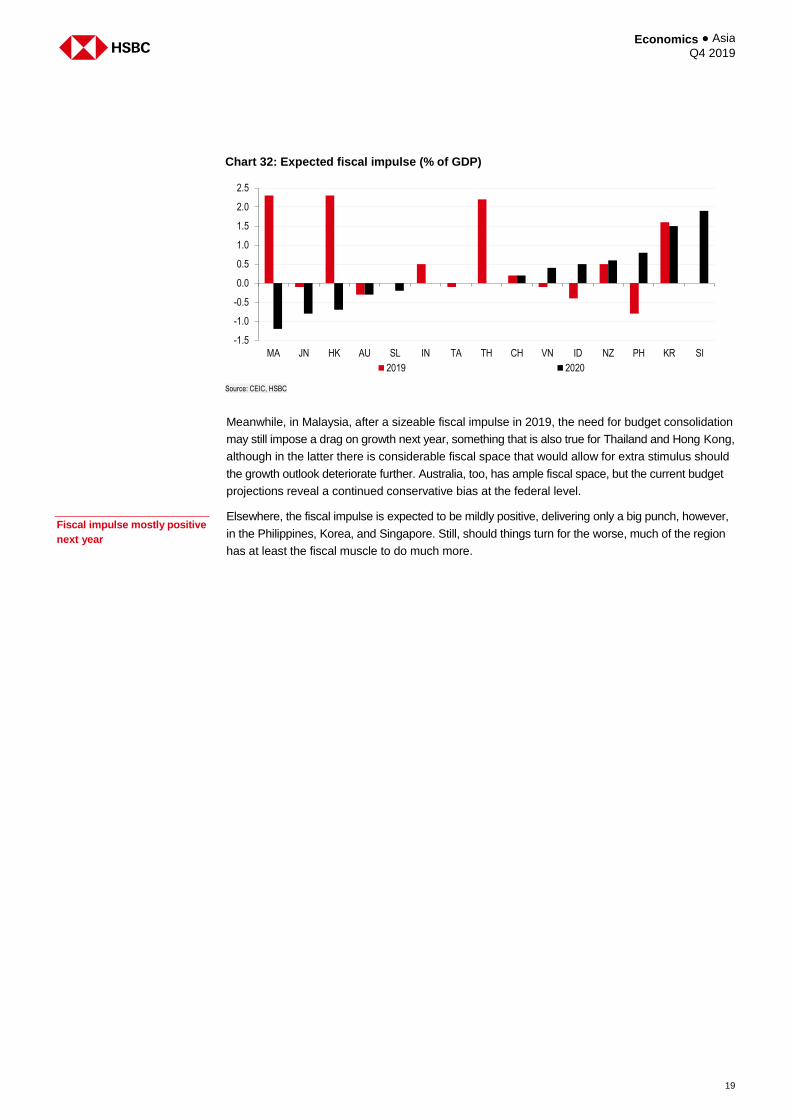

Meanwhile, in Malaysia, after a sizeable fiscal impulse in 2019, the need for budget consolidation

may still impose a drag on growth next year, something that is also true for Thailand and Hong Kong,

although in the latter there is considerable fiscal space that would allow for extra stimulus should

the growth outlook deteriorate further. Australia, too, has ample fiscal space, but the current budget

projections reveal a continued conservative bias at the federal level.

Elsewhere, the fiscal impulse is expected to be mildly positive, delivering only a big punch, however,

in the Philippines, Korea, and Singapore. Still, should things turn for the worse, much of the region

has at least the fiscal muscle to do much more.

Chart 32: Expected fiscal impulse (% of GDP)

Source: CEIC, HSBC

Fiscal impulse mostly positive

next year

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

MA JN HK AU SL IN TA TH CH VN ID NZ PH KR SI

2019 2020

Economics ● Asia Q4 2019

20

Growing headwinds

Headwinds have intensified over the last few months

It has been a head-turning couple of months as the trade war between the US and China has

continued to take the limelight. In the latest escalation of the trade war, the US further increased

tariffs on Chinese goods. China now faces 15% tariffs on an estimated 111bn worth of goods,

and 25% on USD228bn (set to increase to 30% on 15 October). An additional 15% on the

remaining 156bn is expected to come through on 15 December. These tariffs will exert

downward pressure on China’s trade and manufacturing sectors, and we estimate a 0.8ppt drag

on GDP over a 12 month period (see chart 1). Globally, a growth slowdown and manufacturing

malaise are adding to the pressures faced by China.

Mainland China: Moderate

stimulus, slower growth

Intensifying headwinds should prompt more stimulus in the

coming months

Key measures include cutting RRR and lending rates, more SME

lending and infrastructure spending; These stimuli will likely offset

part but not all of the headwinds

Beijing is unlikely to rush into new dramatic stimulus as they want

to balance between reflation and deleveraging

Qu Hongbin Co-head Asian Econ Research, Chief China Economist The Hongkong and Shanghai Banking Corporation Limited

+852 2822 2025

Erin Xin

Economist, Greater China

The Hongkong and Shanghai Banking Corporation Limited

+852 2996 6975

Chart 1. Tariff tracker on impact on China’s growth

Source: CEIC, US Census Bureau, HSBC

0 100 200 300 400 500 600

Value of Chinese goods impacted (USDbn)

$50Bn List(appx $46Bn)

25% tariffs

$200Bn List(appx $182Bn)

25% tariffs

List 4A(appx $111Bn)

10% tariffs1 September

$250Bn List(appx $228Bn)

25% tariffs

$50Bn List(appx $46Bn)

25% tariffs

List 4B (appx $156Bn)

10% tariffs15 December

List 4A (appx $111Bn)

15% tariffs1 September

$250Bn List(appx $228Bn)

30% tariffs15 October

List 4B (appx $156Bn)

15% tariffs15 December

Note: The amount and GDP impact are cumulative; Approximate values are based on calculations of 2018 US import value from the US Census Bureau.

$300Bn List

0.1 ppt.

0.8 ppt

1.3ppt

1.6ppt

21

Economics ● Asia Q4 2019

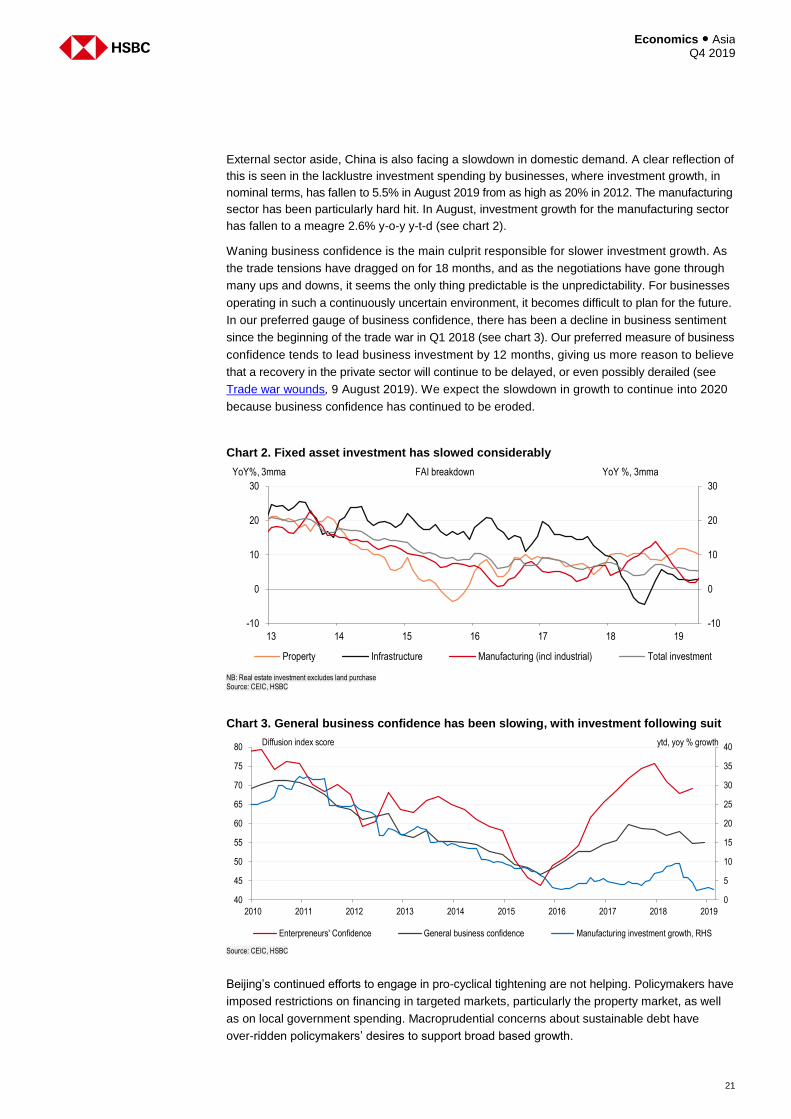

External sector aside, China is also facing a slowdown in domestic demand. A clear reflection of

this is seen in the lacklustre investment spending by businesses, where investment growth, in

nominal terms, has fallen to 5.5% in August 2019 from as high as 20% in 2012. The manufacturing

sector has been particularly hard hit. In August, investment growth for the manufacturing sector

has fallen to a meagre 2.6% y-o-y y-t-d (see chart 2).

Waning business confidence is the main culprit responsible for slower investment growth. As

the trade tensions have dragged on for 18 months, and as the negotiations have gone through

many ups and downs, it seems the only thing predictable is the unpredictability. For businesses

operating in such a continuously uncertain environment, it becomes difficult to plan for the future.

In our preferred gauge of business confidence, there has been a decline in business sentiment

since the beginning of the trade war in Q1 2018 (see chart 3). Our preferred measure of business

confidence tends to lead business investment by 12 months, giving us more reason to believe

that a recovery in the private sector will continue to be delayed, or even possibly derailed (see

Trade war wounds, 9 August 2019). We expect the slowdown in growth to continue into 2020

because business confidence has continued to be eroded.

Chart 2. Fixed asset investment has slowed considerably

NB: Real estate investment excludes land purchase Source: CEIC, HSBC

Chart 3. General business confidence has been slowing, with investment following suit

Source: CEIC, HSBC

Beijing’s continued efforts to engage in pro-cyclical tightening are not helping. Policymakers have

imposed restrictions on financing in targeted markets, particularly the property market, as well

as on local government spending. Macroprudential concerns about sustainable debt have

over-ridden policymakers’ desires to support broad based growth.

-10

0

10

20

30

13 14 15 16 17 18 19

-10

0

10

20

30

YoY %, 3mmaYoY%, 3mma FAI breakdown

Property Infrastructure Manufacturing (incl industrial) Total investment

0

5

10

15

20

25

30

35

40

40

45

50

55

60

65

70

75

80

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

ytd, yoy % growthDiffusion index score

Enterpreneurs' Confidence General business confidence Manufacturing investment growth, RHS

Economics ● Asia Q4 2019

22

In light of these growing headwinds, we recently downgraded our GDP growth forecast to 6.2%

for 2019 (from 6.5% previously) and to 5.8% for 2020 (from 6.3%). For details, see China GDP

downgrade, 28 August 2019. We forecast that growth will remain at 5.8% for 2021.

Policy response: Stepping up, but gradually

Policymakers will step up stimulus to ease pressures on the economy

Faced with so many headwinds, we expect policymakers to step up stimulus with both monetary

and fiscal measures. With monetary policy, there is both the need for more easing as well as

enough policy space to conduct it. For one, core inflation has remained stable and low at below

2% (despite headline inflation picking up recently due to spiking pork prices) (see China inflation,

10 September 2019). The producers’ price index (PPI) has also shown signs of deflation, with

the last two months showing contracting growth, and provides more space to introduce easing

(see PPI in China, 10 September 2019). Secondly, central banks around the world are cutting

rates, led by the US Federal reserve which cut 50bp in Q3 2019, and a forecasted additional

25bp cut in October.

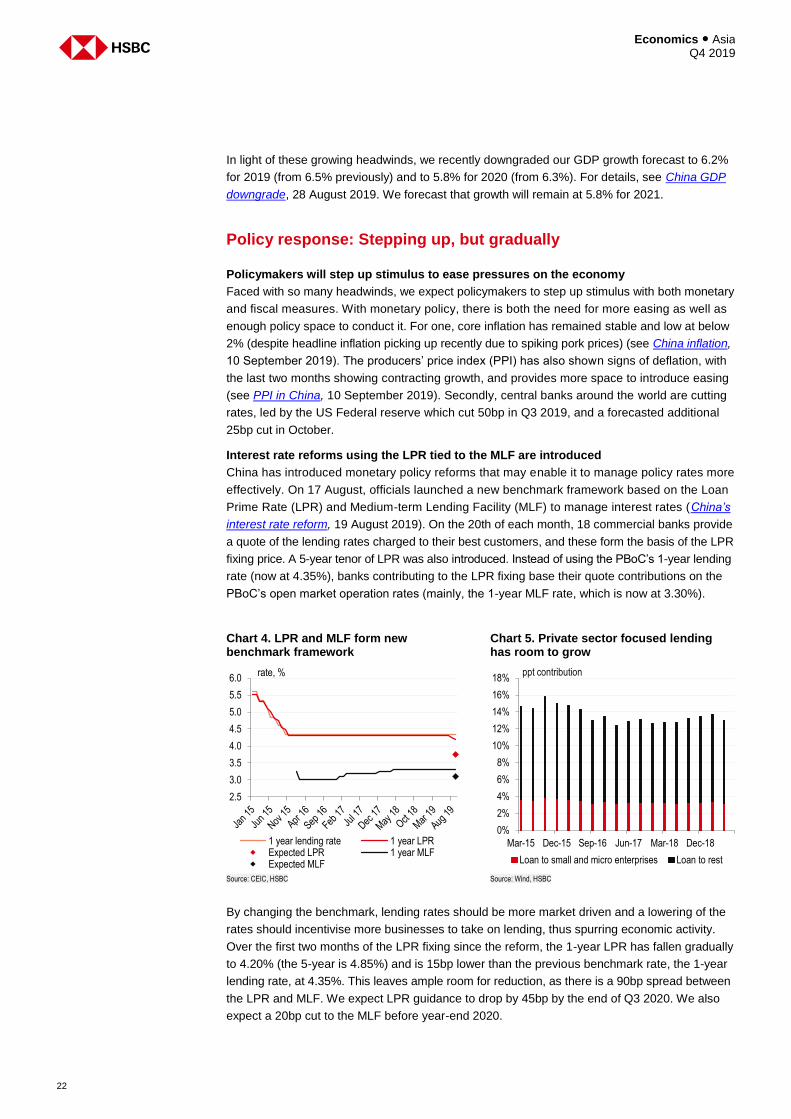

Interest rate reforms using the LPR tied to the MLF are introduced

China has introduced monetary policy reforms that may enable it to manage policy rates more

effectively. On 17 August, officials launched a new benchmark framework based on the Loan

Prime Rate (LPR) and Medium-term Lending Facility (MLF) to manage interest rates (China’s

interest rate reform, 19 August 2019). On the 20th of each month, 18 commercial banks provide

a quote of the lending rates charged to their best customers, and these form the basis of the LPR

fixing price. A 5-year tenor of LPR was also introduced. Instead of using the PBoC’s 1-year lending

rate (now at 4.35%), banks contributing to the LPR fixing base their quote contributions on the

PBoC’s open market operation rates (mainly, the 1-year MLF rate, which is now at 3.30%).

Chart 4. LPR and MLF form new benchmark framework

Chart 5. Private sector focused lending has room to grow

Source: CEIC, HSBC Source: Wind, HSBC

By changing the benchmark, lending rates should be more market driven and a lowering of the

rates should incentivise more businesses to take on lending, thus spurring economic activity.

Over the first two months of the LPR fixing since the reform, the 1-year LPR has fallen gradually

to 4.20% (the 5-year is 4.85%) and is 15bp lower than the previous benchmark rate, the 1-year

lending rate, at 4.35%. This leaves ample room for reduction, as there is a 90bp spread between

the LPR and MLF. We expect LPR guidance to drop by 45bp by the end of Q3 2020. We also

expect a 20bp cut to the MLF before year-end 2020.

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0rate, %

1 year lending rate 1 year LPRExpected LPR 1 year MLFExpected MLF

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18 Dec-18

ppt contribution

Loan to small and micro enterprises Loan to rest

23

Economics ● Asia Q4 2019

Aside from the new interest rate reforms, the PBoC continues to use the reserve requirement ratio

(RRR) to provide monetary relief. A 50bp broad-based cut and a 100bp targeted cut for city

commercial banks were recently implemented and added more liquidity to the market (see PBoC

cuts RRR, more easing to come, 6 September 2019). We expect an additional 50bp cut by year-end

as well as a further 100bp cut in 2020. Moreover, increased lending to the corporate sector,

especially small and medium-sized enterprises (SMEs), will remain a forefront policy objective. In

addition to interest rate reforms aimed at lowering the borrowing rate, policymakers have used a

“carrot and stick” approach to encourage credit lending for the corporate sector throughout the year.

Tools such as targeted and tiered RRR cuts for SME-focused banks can provide further stimulus to

the economy because SMEs traditionally face higher interest rates as lenders view them as riskier.

Table 1. Three VAT cut scenarios expected to take place in 2020

VAT cut scenario Value of tax cut impact Value as a % of GDP, 2020e

Lower 13% to 11%, and lower 9% to 6%, keep 6% unchanged (conservative case)

From RMB925bn to RMB975bn 0.9

Lower 13% to 9%, keep 9% and 6% unchanged (base case)

From RMB1,200bn to RMB1,250bn 1.2

Lower 13% to 9%, and lower 9% to 6%, keep 6% unchanged (stimulative case)

From RMB1,525bn to RMB1,575bn 1.5

Source: Wind, CEIC, HSBC forecasts

From a fiscal policy side, we expect policymakers to continue to build off the momentum seen

earlier this year when they announced an RMB2trn corporate tax package for the year (see

Trade war: A winning strategy, 26 June 2019). Reductions to the valued-added tax and

corporations’ social security contributions helped provide a much needed fiscal boost. An

estimated RMB800-900bn in benefits are expected to come through for the remainder of the

year. More corporate tax cuts could be announced in 2020. These could take the form of further

VAT tax cuts (rates under the current tiered system range from 6 to 13%), a reduction in the

corporate tax rate (now at 25%), and further reduction in corporate social security contributions.

Fiscal stimulus can also take the form of support for infrastructure spending via the issuance of local

government bonds. An increase in the quota as well as pre-issuance for 2020 spending may spur

infrastructure development in the coming quarters. In September, the government already began the

process of asking for local governments’ assessments of their borrowing needs (Caixin, 5 September

2019). This is three months in advance of the same process last year, and the pre-clearance should

speed up issuance in the beginning of the year in 2020, leading to faster allocation of funds.

Chart 6. RRR cuts will be both broad and targeted

Chart 7. Local government bond issuance quotas expected to increase

Source: CEIC, HSBC Source: CEIC, HSBC

0

5

10

15

20

25

2004 2009 2014 2019

RRR, %

All

Large Depository Institutions

Small and Medium Depository Institutions

Medium Depository Institutions

Small Depository Institutions

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2018 2019

Tho

usa

nd

s

bn RMB

Total new issuance General Special

Economics ● Asia Q4 2019

24

To restore confidence, more stimulus is needed

Slowing growth unlikely to be reversed through gradual stimulus

Policy easing has been trickling in for most of the year. But, in spite of the large tax cuts for the

corporate sector and better credit conditions for SMEs that have been pushed through, we have

yet to see a rebound in growth. It seems that the headwinds are overwhelming the effect of the

stimulus measures. While we expect a step-up in stimulus in the coming months, which may

offset some of the downward pressure on growth, the gradual policies will not be enough to

completely reverse the impact of the growing headwinds. Thus, if policy continues at the current

pace, we expect the slowdown in growth to continue into 2020 as business sentiment may fail to

pick up again.

Restoring business confidence needs a more dramatic approach

Like starting a car engine, confidence needs to be jump-started to get going again. Only then

can it reverse course and return to a stable growth path. Instead of gradual easing, a super-

stimulus package is needed to restore business confidence. A more concerted effort to step up

broad-based easing, and all at once, would not only give businesses the direct benefits of the

stimulus measures, but also provide a positive signal that policy will remain accommodative to

help restore confidence.

Why not a super-stimulus?

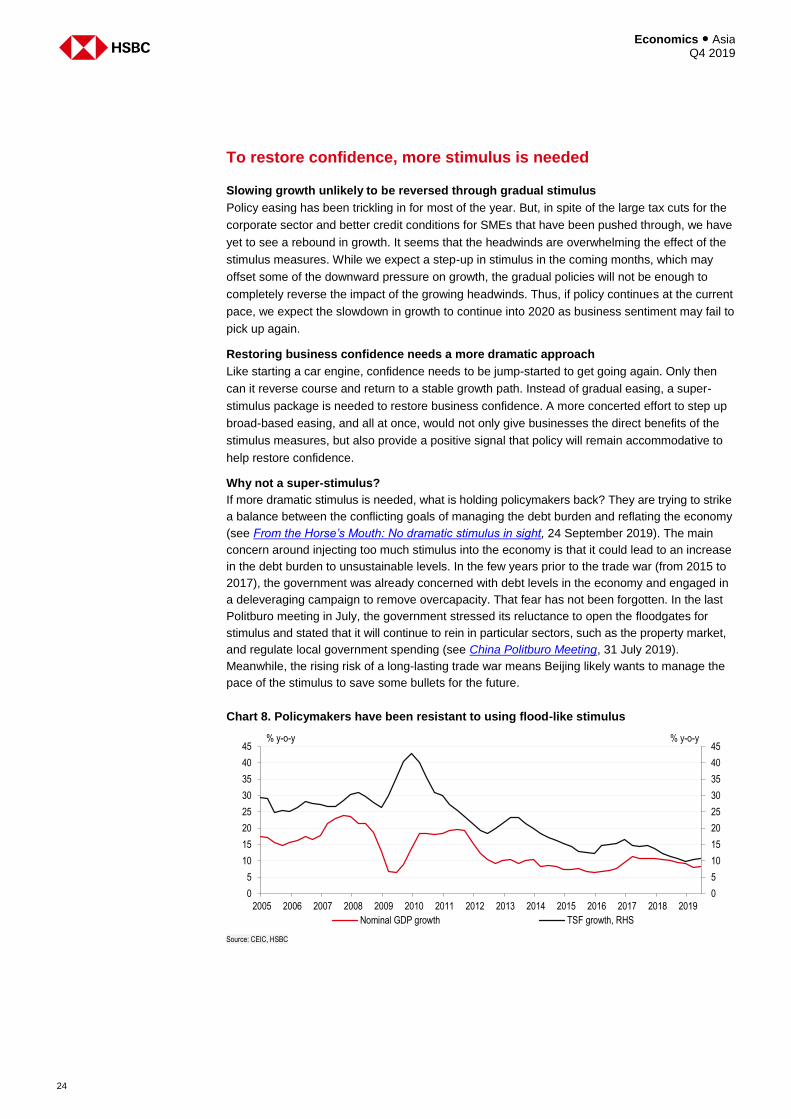

If more dramatic stimulus is needed, what is holding policymakers back? They are trying to strike

a balance between the conflicting goals of managing the debt burden and reflating the economy

(see From the Horse’s Mouth: No dramatic stimulus in sight, 24 September 2019). The main

concern around injecting too much stimulus into the economy is that it could lead to an increase

in the debt burden to unsustainable levels. In the few years prior to the trade war (from 2015 to

2017), the government was already concerned with debt levels in the economy and engaged in

a deleveraging campaign to remove overcapacity. That fear has not been forgotten. In the last

Politburo meeting in July, the government stressed its reluctance to open the floodgates for

stimulus and stated that it will continue to rein in particular sectors, such as the property market,

and regulate local government spending (see China Politburo Meeting, 31 July 2019).

Meanwhile, the rising risk of a long-lasting trade war means Beijing likely wants to manage the

pace of the stimulus to save some bullets for the future.

Chart 8. Policymakers have been resistant to using flood-like stimulus

Source: CEIC, HSBC

0

5

10

15

20

25

30

35

40

45

0

5

10

15

20

25

30

35

40

45

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

% y-o-y% y-o-y

Nominal GDP growth TSF growth, RHS

25

Economics ● Asia Q4 2019

For the property market, the government has emphasised that real estate “should not be used

for speculation”, and is effectively excluded from using the best rate for lending (the 1-year

LPR). In addition, at the beginning of the year, policymakers introduced regulations to curb

inefficient local government spending and to stop the issuance of “hidden” debt. Special local

government bonds are restricted from being used for land reserves and real estate

development. These restrictions on the property market and local government spending are not

likely to let up anytime soon. At the same time, growing deflationary pressures have emerged, as

PPI has contracted for two months in a row, putting a further onus on Beijing to reflate the economy

(PPI in China, 10 September 2019).

Conclusion

In light of intensifying headwinds, policymakers will likely continue to step up easing in the coming

months with a mix of monetary (RRR cuts, cuts to the lending rate, increased lending to SMEs)

and fiscal policies (corporate tax cuts and local government bond issuance). However, the pace

of policy stimulus is too gradual to stabilise growth. More dramatic stimulus is needed to restore

business confidence, the main drag on growth. However, macroprudential concerns still hold

policymakers back, and the likelihood of a super-stimulus package coming through are reduced.

Gradual policy easing can offset some of the headwinds, but not enough to slow the slowdown.

Thus, our outlook for the coming quarters is one of subdued growth. At the end of August, we

adjusted our GDP growth forecast lower to 5.8% in 2020.

Economics ● Asia Q4 2019

26

This page has been left blank intentionally

27

Economics ● Asia Q4 2019

Indicators

Economics ● Asia Q4 2019

28

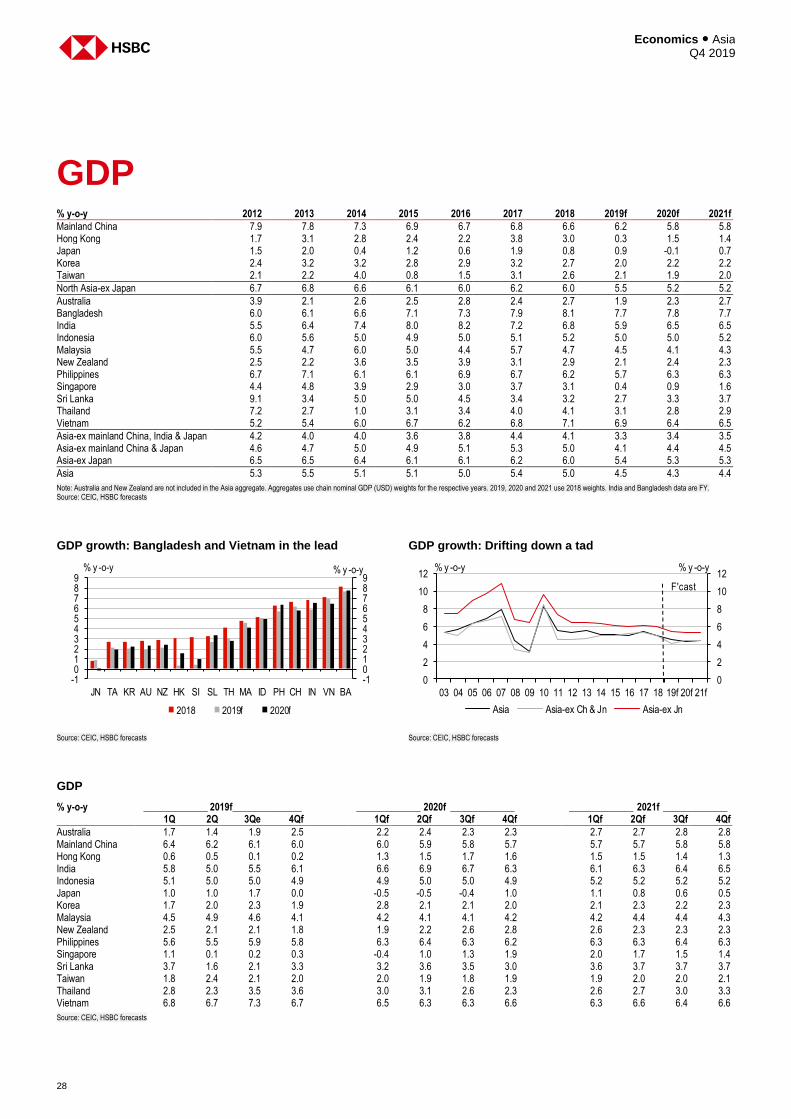

GDP % y-o-y 2012 2013 2014 2015 2016 2017 2018 2019f 2020f 2021f

Mainland China 7.9 7.8 7.3 6.9 6.7 6.8 6.6 6.2 5.8 5.8 Hong Kong 1.7 3.1 2.8 2.4 2.2 3.8 3.0 0.3 1.5 1.4 Japan 1.5 2.0 0.4 1.2 0.6 1.9 0.8 0.9 -0.1 0.7 Korea 2.4 3.2 3.2 2.8 2.9 3.2 2.7 2.0 2.2 2.2 Taiwan 2.1 2.2 4.0 0.8 1.5 3.1 2.6 2.1 1.9 2.0

North Asia-ex Japan 6.7 6.8 6.6 6.1 6.0 6.2 6.0 5.5 5.2 5.2

Australia 3.9 2.1 2.6 2.5 2.8 2.4 2.7 1.9 2.3 2.7 Bangladesh 6.0 6.1 6.6 7.1 7.3 7.9 8.1 7.7 7.8 7.7 India 5.5 6.4 7.4 8.0 8.2 7.2 6.8 5.9 6.5 6.5 Indonesia 6.0 5.6 5.0 4.9 5.0 5.1 5.2 5.0 5.0 5.2 Malaysia 5.5 4.7 6.0 5.0 4.4 5.7 4.7 4.5 4.1 4.3 New Zealand 2.5 2.2 3.6 3.5 3.9 3.1 2.9 2.1 2.4 2.3 Philippines 6.7 7.1 6.1 6.1 6.9 6.7 6.2 5.7 6.3 6.3 Singapore 4.4 4.8 3.9 2.9 3.0 3.7 3.1 0.4 0.9 1.6 Sri Lanka 9.1 3.4 5.0 5.0 4.5 3.4 3.2 2.7 3.3 3.7 Thailand 7.2 2.7 1.0 3.1 3.4 4.0 4.1 3.1 2.8 2.9 Vietnam 5.2 5.4 6.0 6.7 6.2 6.8 7.1 6.9 6.4 6.5

Asia-ex mainland China, India & Japan 4.2 4.0 4.0 3.6 3.8 4.4 4.1 3.3 3.4 3.5 Asia-ex mainland China & Japan 4.6 4.7 5.0 4.9 5.1 5.3 5.0 4.1 4.4 4.5 Asia-ex Japan 6.5 6.5 6.4 6.1 6.1 6.2 6.0 5.4 5.3 5.3

Asia 5.3 5.5 5.1 5.1 5.0 5.4 5.0 4.5 4.3 4.4

Note: Australia and New Zealand are not included in the Asia aggregate. Aggregates use chain nominal GDP (USD) weights for the respective years. 2019, 2020 and 2021 use 2018 weights. India and Bangladesh data are FY. Source: CEIC, HSBC forecasts

GDP growth: Bangladesh and Vietnam in the lead GDP growth: Drifting down a tad

Source: CEIC, HSBC forecasts Source: CEIC, HSBC forecasts

GDP

% y-o-y _____________ 2019f ______________ _____________ 2020f _____________ _____________ 2021f _____________ 1Q 2Q 3Qe 4Qf 1Qf 2Qf 3Qf 4Qf 1Qf 2Qf 3Qf 4Qf

Australia 1.7 1.4 1.9 2.5 2.2 2.4 2.3 2.3 2.7 2.7 2.8 2.8 Mainland China 6.4 6.2 6.1 6.0 6.0 5.9 5.8 5.7 5.7 5.7 5.8 5.8 Hong Kong 0.6 0.5 0.1 0.2 1.3 1.5 1.7 1.6 1.5 1.5 1.4 1.3 India 5.8 5.0 5.5 6.1 6.6 6.9 6.7 6.3 6.1 6.3 6.4 6.5 Indonesia 5.1 5.0 5.0 4.9 4.9 5.0 5.0 4.9 5.2 5.2 5.2 5.2 Japan 1.0 1.0 1.7 0.0 -0.5 -0.5 -0.4 1.0 1.1 0.8 0.6 0.5 Korea 1.7 2.0 2.3 1.9 2.8 2.1 2.1 2.0 2.1 2.3 2.2 2.3 Malaysia 4.5 4.9 4.6 4.1 4.2 4.1 4.1 4.2 4.2 4.4 4.4 4.3 New Zealand 2.5 2.1 2.1 1.8 1.9 2.2 2.6 2.8 2.6 2.3 2.3 2.3 Philippines 5.6 5.5 5.9 5.8 6.3 6.4 6.3 6.2 6.3 6.3 6.4 6.3 Singapore 1.1 0.1 0.2 0.3 -0.4 1.0 1.3 1.9 2.0 1.7 1.5 1.4 Sri Lanka 3.7 1.6 2.1 3.3 3.2 3.6 3.5 3.0 3.6 3.7 3.7 3.7 Taiwan 1.8 2.4 2.1 2.0 2.0 1.9 1.8 1.9 1.9 2.0 2.0 2.1 Thailand 2.8 2.3 3.5 3.6 3.0 3.1 2.6 2.3 2.6 2.7 3.0 3.3 Vietnam 6.8 6.7 7.3 6.7 6.5 6.3 6.3 6.6 6.3 6.6 6.4 6.6

Source: CEIC, HSBC forecasts

-10123456789

-10123456789

JN TA KR AU NZ HK SI SL TH MA ID PH CH IN VN BA

2018 2019f 2020f

% y -o-y % y -o-y

0

2

4

6

8

10

12

0

2

4

6

8

10

12

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19f 20f 21f

F'cast

Asia Asia-ex Ch & Jn Asia-ex Jn

% y -o-y % y -o-y

29

Economics ● Asia Q4 2019

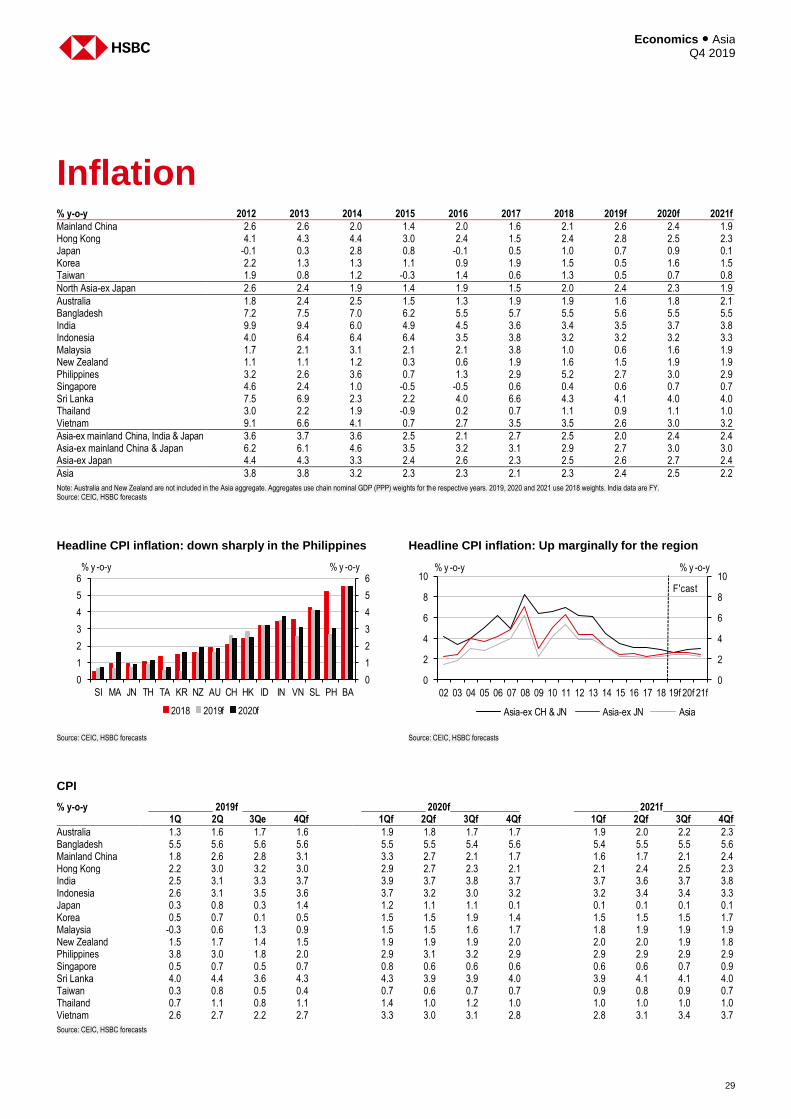

Inflation % y-o-y 2012 2013 2014 2015 2016 2017 2018 2019f 2020f 2021f

Mainland China 2.6 2.6 2.0 1.4 2.0 1.6 2.1 2.6 2.4 1.9 Hong Kong 4.1 4.3 4.4 3.0 2.4 1.5 2.4 2.8 2.5 2.3 Japan -0.1 0.3 2.8 0.8 -0.1 0.5 1.0 0.7 0.9 0.1 Korea 2.2 1.3 1.3 1.1 0.9 1.9 1.5 0.5 1.6 1.5 Taiwan 1.9 0.8 1.2 -0.3 1.4 0.6 1.3 0.5 0.7 0.8