Foreword oreword oreword oreword oreword iii T he Asian Development Outlook 2000 is the 12th in a series of annual economic reports on the devel- oping member countries of the Asian Development Bank. The Outlook provides a comprehensive analy- sis of salient macroeconomic and development issues in individual countries as well as at the regional level, from both positive and normative perspectives. In 1999 the world economy finally shook off the effects of the 1997 Asian crisis and the economic dis- turbances in Russia and Brazil that followed. Within Asia a moderate to strong upswing replaced negative growth in several countries; interest rates decreased and exchange rates stabilized. Domestic demand and export growth improved. Increased confidence in the region’s economic prospects is evident from strength- ened capital inflows from overseas investors, increased vitality of equity markets, and revived consumer con- fidence. All of the countries that were directly affected by the crisis and experienced negative economic growth in 1998 — Indonesia, Republic of Korea, Malaysia, Philippines, and Thailand — recovered to positive growth. The strength of the rebound varied from a strong recovery in the Republic of Korea to a more modest revival in Indonesia. The People’s Republic of China (PRC) and South Asia were insu- lated from the crisis to a certain extent and as a result fared better. In 1999 growth slowed slightly in the PRC, while accelerating by a similar margin in South Asia. Growth in Central Asia showed a strong increase as the effect of the Russian crisis dissipated, and the per- formance of the Pacific economies improved from the previous year. To sustain and further reinvigorate the growth process, developing Asia will have to continue with its agenda of reforms and institutional innovations in areas that are considered weak and vulnerable. In particular the crisis has exposed weaknesses in the banking system, capital markets, and corporate sectors of the affected countries. The scale and complexities of the issues involved are enormous. The crisis has rendered a large part of the banking and corporate sectors financially insolvent. In the immediate after- math of the crisis, the ADB cooperated with other donors in providing emergency financial assistance to stabilize the affected economies and to support urgent structural reforms. On its part, the ADB focused on a structural agenda that included restructuring insolvent financial institutions, improving corporate gover- nance, and deregulating and opening domestic mar- kets. In this regard, the ADB provided loans to assist Indonesia, Korea, and Thailand in implementing financial sector reforms. The crisis countries have made significant progress in bank and corporate sec- tor restructuring and have created new organizational entities to deal with these issues. While much progress has been made, much remains to be done. However, given the willingness and dedication of the governments to address this unfinished agenda of reform and restructuring, we are confident that the results of these structural reforms and review of policies

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

iiiFOREWORD

FFFFForewordorewordorewordorewordoreword

iii

TTTTThe Asian Development Outlook 2000 is the 12th ina series of annual economic reports on the devel-

oping member countries of the Asian DevelopmentBank. The Outlook provides a comprehensive analy-sis of salient macroeconomic and development issuesin individual countries as well as at the regional level,from both positive and normative perspectives.

In 1999 the world economy finally shook off theeffects of the 1997 Asian crisis and the economic dis-turbances in Russia and Brazil that followed. WithinAsia a moderate to strong upswing replaced negativegrowth in several countries; interest rates decreasedand exchange rates stabilized. Domestic demand andexport growth improved. Increased confidence in theregion’s economic prospects is evident from strength-ened capital inflows from overseas investors, increasedvitality of equity markets, and revived consumer con-fidence. All of the countries that were directly affectedby the crisis and experienced negative economicgrowth in 1998 — Indonesia, Republic of Korea,Malaysia, Philippines, and Thailand — recovered topositive growth. The strength of the rebound variedfrom a strong recovery in the Republic of Korea to amore modest revival in Indonesia. The People’sRepublic of China (PRC) and South Asia were insu-lated from the crisis to a certain extent and as a resultfared better. In 1999 growth slowed slightly in the PRC,while accelerating by a similar margin in South Asia.Growth in Central Asia showed a strong increase asthe effect of the Russian crisis dissipated, and the per-

formance of the Pacific economies improved from theprevious year.

To sustain and further reinvigorate the growthprocess, developing Asia will have to continue withits agenda of reforms and institutional innovations inareas that are considered weak and vulnerable. Inparticular the crisis has exposed weaknesses in thebanking system, capital markets, and corporate sectorsof the affected countries. The scale and complexitiesof the issues involved are enormous. The crisis hasrendered a large part of the banking and corporatesectors financially insolvent. In the immediate after-math of the crisis, the ADB cooperated with otherdonors in providing emergency financial assistance tostabilize the affected economies and to support urgentstructural reforms. On its part, the ADB focused on astructural agenda that included restructuring insolventfinancial institutions, improving corporate gover-nance, and deregulating and opening domestic mar-kets. In this regard, the ADB provided loans to assistIndonesia, Korea, and Thailand in implementingfinancial sector reforms. The crisis countries havemade significant progress in bank and corporate sec-tor restructuring and have created new organizationalentities to deal with these issues. While much progresshas been made, much remains to be done.

However, given the willingness and dedicationof the governments to address this unfinished agendaof reform and restructuring, we are confident that theresults of these structural reforms and review of policies

ASIAN DEVELOPMENT OUTLOOK 2000iv

and institutions will result in improved economic effi-ciency, greater transparency, better governance, andimproved social equity. The region will emerge stron-ger and more able to fulfill its potential for sustainedeconomic growth and development.

Part I of this year’s Outlook comprises two chap-ters. The first chapter provides a comprehensive re-view of economic developments in the Asian andPacific region against a background of developmentsin the world economy. In the second chapter, theOutlook presents a progress report on financial andcorporate restructuring in the countries most affectedby the crisis. This chapter develops elements of sucha strategy, as well as an agenda for strengthening on-going reforms, improving governance, reducing fiscalimbalances, and developing financial markets.

Part II discusses the recent economic perfor-mance and short-term prospects for each of the37 developing member countries of the ADB.It also reviews and assesses economic managementand policy and development issues from a medium-term perspective.

Part III discusses the social challenges the Asianregion faces as it moves into the new millennium. Itreviews the record of social achievement, analyzessalient factors behind the social challenge, and rec-ommends policies for change. In addition to poverty,this challenge has many dimensions: low literacy, un-satisfactory education, poor health and nutrition, en-vironmental degradation, income and wealthdisparities, and discrimination. Several conclusionsfollow from the analysis, including the importance of

openness and market orientation in sustaining vibranteconomic growth that includes the poor and disad-vantaged. For growth to be inclusive, renewed andmore focused efforts to invest in human resources andphysical infrastructure are crucial. The ability and willof governments to address social issues through thepolitical process and good governance must bestrengthened. Finally, national governments shouldcreate a fiscally prudent social safety net to safeguardthe nonpoor from a sudden push into poverty, andthe poor from a descent into extreme poverty. Whiledeveloping an agenda to address social issues isprimarily the task of national governments, the inter-national community can assist by increasing foreignassistance (which has declined sharply in recent years);providing international public goods, such as researchon tropical diseases and tropical agriculture, whichconcern the majority of the poor; and improving theglobal trading environment, which remains encum-bered by many restrictions in areas of interests to poorcountries.

The ADB has recently adopted poverty reduc-tion as its overarching objective. This Asian Develop-ment Outlook 2000 provides a useful addition to ourstock of knowledge on both the location and dimen-sions of the poverty problem, as well as specific policiesto address this crucial social challenge in individualcountries.

TADAO CHINOPresident

15SOUTH ASIA

Acronyms and AbbreviationsAcronyms and AbbreviationsAcronyms and AbbreviationsAcronyms and AbbreviationsAcronyms and Abbreviations

xv

ADB Asian Development BankAMC Asset management companyAPEC Asia-Pacific Economic CooperationEU European UnionFDI Foreign direct investmentGDP Gross domestic productGEM Growth Enterprise MarketGNP Gross national productIBRA Indonesian Bank Restructuring AgencyILO International Labour OrganizationIMF International Monetary FundINDRA Indonesian Debt Restructuring AgencyIT Information technologyMENA Middle East-North AfricaNASDAQ National Association of Securities Dealers Automated QuotationsNGO Nongovernmental organizationNPL Nonperforming loanNPRT Nauru Phosphate Royalties TrustOECD Organisation for Economic Co-operation and DevelopmentOPEC Organization of Petroleum Exporting CountriesRERF Reserve Equalization Reserve FundSME Small and medium-size enterpriseSOE State-owned enterpriseUNCTAD United Nations Conference on Trade and DevelopmentWHO World Health OrganizationWTO World Trade Organization

DefinitionsDefinitionsDefinitionsDefinitionsDefinitions

xvi

The classification of economies by major analyticor geographic groupings such as industrial coun-

tries, developing countries, Africa, Latin America,Middle East, Europe, and transitional countries followsthe classification adopted by the InternationalMonetary Fund. Latin America, however, is referredto as developing countries in the Western Hemispherein the IMF classification. Transitional economies inAsia include Kazakhstan, Kyrgyz Republic, Mongolia,Tajikistan, and Uzbekistan.

For purposes of this Outlook the following apply:

! Developing Asia refers to the 37 developingmember countries of the Asian Development Bankdiscussed in this Outlook.

! Newly industrialized economies (NIEs) com-prise Hong Kong, China; Republic of Korea;Singapore; and Taipei,China.

! South Asia comprises Bangladesh, Bhutan, India,Maldives, Nepal, Pakistan, and Sri Lanka.

! Southeast Asia comprises Cambodia, Indonesia,Lao People’s Democratic Republic, Malaysia,Myanmar, Philippines, Thailand, and Viet Nam.

! Central Asian republics comprise Kazakhstan,Kyrgyz Republic, Tajikistan, and Uzbekistan.

! The Pacific comprises Cook Islands, Fiji Islands,Kiribati, Marshall Islands, Federated States ofMicronesia, Nauru, Papua New Guinea, Samoa,Solomon Islands, Tonga, Tuvalu, and Vanuatu.

! East Asia comprises the NIEs, the People’sRepublic of China, and Mongolia.

! Crisis-affected countries comprise Indonesia,Republic of Korea, Malaysia, Philippines, andThailand.

! G7 comprises Canada, France, Germany, Italy,Japan, United Kingdom, and United States.

! Other non-Asian developing economies referto Argentina, Brazil, Chile, Colombia, Egypt, Mexico,Morocco, Turkey, and Venezuela.

Unless otherwise specified, the symbol $ meansUS dollars.

This Outlook is based on data available up to 8 March2000.

3ECONOMIC DEVELOPMENTS AND PROSPECTS

Economic DevelopmentsEconomic DevelopmentsEconomic DevelopmentsEconomic DevelopmentsEconomic Developmentsand Prospectsand Prospectsand Prospectsand Prospectsand Prospects

The year 1999 saw the resolution of the financial crisis in developing Asia and acceleration of globalgrowth, propelled primarily by a buoyant US economy. Led by the newly industrialized economies(NIEs) and the People’s Republic of China (PRC), Asia posted strong growth that meant almosttripling the growth rate from the previous year. Prospects for further acceleration of growth in theregion in the next two years depend on the sustainability of domestic demand, favorable global economicconditions, and progress in corporate and financial sector reforms in the crisis-affected economies.

IIIIIn the fall of 1998, many economies in Asia were inrecession, capital flows had turned negative, Russia

had just defaulted on its official debt, and the outlookfor the region and the world economy were generallypessimistic. Stock markets were languishing and therewas a very real fear that the world economy would tipinto recession. The sharp decline in worldwide eco-nomic growth had brought commodity prices to his-torical lows, with oil prices plummeting by 30 percent.The contagion effect from the Asian crisis was threat-ening Latin America, where the Brazilian currency,the real, was under siege. European banks, curren-cies, and stock markets were badly affected by theRussian devaluation and subsequent default duringJuly and August, and the euro currency area appearedto be faltering. In its fall issue of the 1998 WorldEconomic Outlook, the International Monetary Fund(IMF) slashed its forecast for 1999 world growth from3.7 percent to 2.5 percent, stating, “The risks to thisprojection, however, are predominantly on the down-side. Indeed a significantly worse outcome is clearlypossible.” The IMF would later downgrade its worldgrowth forecast even further, to 2.3 percent.

A year and a half later the outlook for the worldeconomy is, however, much more bullish. The year1999 turned out to be much better than anyone hadexpected. The sharp rebound in global growth has nowgenerated the fear of excess growth and inflation. Howwas such a turnaround possible?

The turning point was probably October 1998,when the Federal Reserve lowered the discount ratefor the second time in two weeks. This sent a strongmessage to the world financial community that theUnited States (US) was ready to take whatever mea-sures necessary to stem the threat. Markets respondedquickly and enthusiastically. At about the same time,the Japanese government passed legislation to dealwith bad loans in the banking system, and a monthlater, passed a stimulus package that worked to bringabout positive growth the coming year. BetweenNovember 1998 and April 1999, the European CentralBank also lowered interest rates in tandem with USrates. Lower interest rates in industrial countries werematched by a further relaxation of monetary policyand fiscal policy in the countries that had been hit bythe crisis in Asia.

ASIAN DEVELOPMENT OUTLOOK 20004

These coordinated efforts on the part of boththe industrial world and the crisis-affected developingcountries in Asia were largely responsible for the up-turn of the world economy in 1999, as it finally shookoff the effects of the 1997 Asian crisis and the eco-nomic disturbances in Russia and Brazil that followed.Growth resumed in some countries and acceleratedin others. The US continued to be the primary engineof growth among industrial countries and showed nosigns of a deceleration in growth, as equity marketscontinued to surge while unemployment and infla-tion remained low. The misery index—the combina-tion of the unemployment rate and the inflationrate—continued to fall (see figure 1.1).

Strong US growth also helped drive the rest ofthe North American Free Trade Area, with Canadaand Mexico also performing well. Europe ended theyear on an increasingly positive note, with Germanyand France providing much of the impetus for growthin the region. Some countries in Asia moved to ahigher growth path while others emerged fromrecession. Eastern and Central Europe made a modestrecovery, supported by improved conditions in Russia,Poland, and the Czech Republic. The result was ro-bust growth in the world economy and a low inflationrate for both industrial and developing economies.

Despite widespread economic success in 1999,there remained reasons for concern. The current ac-count deficit of the United States remains large andthe Japanese internal public debt has increaseddramatically the past few years. There is also the issueof how long the “new industrial revolution,” born ofthe development of the Internet, information tech-nology, and e-commerce, can continue to increaseproductivity and boost equity prices without causinginflation (see box 1.1).

In contrast to the 19th century industrial revo-lution, which featured numerous innovations in manu-facturing, today’s revolution seems to permeate a widersegment of the economy. However, traditional indus-tries are not benefiting much from these innovationsas reflected in a growing disparity in equity marketsbetween the new and older sectors of the economy.

It is difficult to gauge the overall long-run impactof the productivity gains from the new industrial revo-lution on global growth. In the short run, however, itis probably reasonable to assume that advances in

computer and information technology will help drivegrowth in industrial countries. The positive synergiesfrom globalization and new technologies should alsospread to the more progressive developing countries.

THE WORLD ECONOMYTHE WORLD ECONOMYTHE WORLD ECONOMYTHE WORLD ECONOMYTHE WORLD ECONOMY

World GDP growth increased to 3 percent in 1999 andit is likely to improve further, to about 3.5 percent in2000. World trade volume also increased slightly to4 percent in 1999, compared with the downturn of1998 when trade growth moderated to 3.6 percentfrom 9.9 percent the previous year. World trade vol-ume is projected to grow further, to nearly 6 percentin 2000. In 1999, world inflation declined to its lowestlevel in 40 years. This exemplary record reflects theintensified commitment among monetary authoritiesto focus on price stability.

Industrial CountriesIndustrial CountriesIndustrial CountriesIndustrial CountriesIndustrial Countries

GDP growth in the industrial economies reboundedto 2.6 percent in 1999 from 2.4 percent in 1998. TheUnited States and Canada continued to performstrongly in 1999, supported by buoyant domesticdemand. Overall growth in GDP in the euro areadeclined to 2.1 percent in 1999 from 2.8 percent theprevious year. In Japan, stimulative macroeconomicpolicies and the rebound in the Asian economies un-derpinned a modest economic recovery.

Inflation in the industrial economies was1.3 percent in 1999, close to the decade low of1.2 percent the previous year. Productivity increasesexerted downward pressure on prices of final goods.Prices of services, which are primarily determined bylabor costs, also remained low, because real wage in-creases lagged behind productivity growth. Inflationin 2000 may escalate to 1.7 percent, largely due to higheroil prices in the first quarter of the year and somemodest upward pressure on wages as labor marketstighten further.

While interest rates bounced back in the latterpart of 1999 from the crisis-depressed lows of late 1998,equity markets enjoyed stellar performance due to thevigor of output and earnings growth. The tighteningof monetary policy by the major industrial economiesin 1999 caused nominal bond yields to rise.

5ECONOMIC DEVELOPMENTS AND PROSPECTS

In 1999 there was a net outflow of capital fromEurope into Japan (particularly into the equity mar-ket) and the US. The US attracted inflows of $85 bil-lion in direct investment and $241 billion in portfolioinvestment. Direct investment was primarily used forforeign acquisition of US companies. These twosources of inflows, net of outflows, financed the UScurrent account deficit of $316 billion (3.5 percent ofGDP) in 1999. Much of the net capital outflow fromthe European Union (EU) was spent on foreign merg-ers and acquisitions and liabilities issued internation-ally by regional banks. Record levels of foreigninvestment in Japanese equities took place in 1999 aseconomic growth prospects brightened. This helpedsupport the yen and contributed to the buoyancy ofthe Japanese stock market.

The outlook for industrial countries suggests atrend toward convergence of economic growth.Growth in the euro area and in Japan is expected tobe higher and US growth similar to that in 1999.Growth convergence within industrial countries willhelp maintain overall macroeconomic stability withinthe global economy. Nevertheless, policymakersneed to address imbalances in foreign trade amongthe major regions.

TransitionTransitionTransitionTransitionTransition EconomiesEconomiesEconomiesEconomiesEconomies

The transition economies showed clear signs of revivalin 1999 as growth of nearly 1 percent was recordedfollowing a slight contraction in 1998. Industrial out-put was particularly strong in Hungary and Poland, asEastern European countries benefited from the eco-nomic strength of the EU, which replaced Russia asthe major trading partner of many countries in thisregion. Countries that have undertaken structuralreforms, such as Hungary, were well positioned to takeadvantage of improved trade linkages and growingimport demand from the EU. For example, the CzechRepublic, Hungary, and Poland sent a third of theirexports to Germany and two thirds to WesternEurope. Hungary and Poland led the region in growthperformance in 1999, while in the Czech Republic,strong exports to Germany offset the effect of a strongkrona to halt economic deceleration. Boosted byhigher oil prices and the 75 percent depreciation ofthe ruble in the fall of 1998, Russia reported the stron-gest growth in industrial output in seven years as over-all GDP grew by 1.7 percent. The improvedperformance of the region led to large capital inflowsand boosted currency and equity markets. Greater sta-

ASIAN DEVELOPMENT OUTLOOK 20006

bility in Russia, along with increased import demandfrom the EU, improved current account balances inthe region. Inflation also dropped in most countries.

Growth is likely to strengthen further to 2.8 per-cent in 2000, fueled by accelerating export growth tothe EU. The downward trend in inflation and nomi-nal interest rates is likely to continue as risk premi-ums in these countries decline. Entry negotiations intothe EU will continue to dominate the policy agendafor some countries. The political situation in EasternEurope should continue to improve, which will boostbusiness confidence and foreign investment.

THE DEVELTHE DEVELTHE DEVELTHE DEVELTHE DEVELOPING ECONOMIESOPING ECONOMIESOPING ECONOMIESOPING ECONOMIESOPING ECONOMIES

Growth in the developing regions of the world im-proved from 3.2 percent in 1998 to 3.5 percent in 1999.

This was underpinned by the strong rebound indeveloping Asia, where GDP expanded by 6.2 per-cent from 2.3 percent in 1998 on the back of strongexport growth and a revival of domestic demand.Greater strength in the global economy and thedissipation of the contagion effects of the Asian crisisalso contributed to the improved performance ofdeveloping countries.

In growth, the NIEs, the PRC, and South Asianeconomies were the strongest performers among de-veloping countries. Aside from a few countries suchas Mexico, growth in Latin America was modest aspolitical uncertainty dampened economic perfor-mance and market expectations. In Africa, growthvaried substantially. Performance improved in severalsmaller countries that adopted structural reforms,while growth in the larger countries remained modest.

Box 1.1Box 1.1Box 1.1Box 1.1Box 1.1 New Economy: Much Ado about Nothing? New Economy: Much Ado about Nothing? New Economy: Much Ado about Nothing? New Economy: Much Ado about Nothing? New Economy: Much Ado about Nothing?

The New Economy doctrine—sometimes grandiosely labeled asthe New Economy paradigm—holdsthe view that informationtechnology, in conjunction withglobalization, has led to apermanent upsurge in productivityof US workers. This has in turnpushed up the growth rate the USeconomy can achieve withoutrunning up against capacity limits.The conventional view, which isbased on economic theory andhistorical evidence, holds that theUS economy has a “speed limit” ofaround 2-2.5 percent growth. Theproponents of the new economybelieve that the growth potential ofthe US economy has now beenpushed to the range of 3-4 percent,stemming from productivity andefficiency gains arising frominformation technology andglobalization.

What do data tell us aboutproductivity growth in the UnitedStates? It is clear from historical

analysis that productivity growthcomes primarily from technology andnot from improved workforce qualityor equipment per worker. Using amethod that isolates technology fromthe other two sources, the evidencesuggests that the technologycomponent of US productivity sloweddown after 1973 and never reallypicked up again. There were surgesfor short periods (1977-1978, 1983-1986, and 1990-1992), but they allfollowed recessions. The currentproductivity boom began in 1996, butwhat differentiates it from the othersurges is that it did not follow arecession, and it has not reversedafter a few years.

Is the current surge inproductivity permanent? Are we inthe middle of a new industrialrevolution created by the computer,information technology, and theInternet? Several issues must beresolved before we can answer thesequestions with any certainty. First,the computer has been in use for

many years but productivity didn’taccelerate until the early 1990s. Whywas there such a lag? It could bebecause computers were not nearly asproductive until they were linkedtogether, either in local area networksor through the Internet, and thisinterconnectedness took time todevelop and to be “sold” to thepublic. Second, even if the lag can beexplained, how has the productivityin a small sector of the economy hadsuch a beneficial effect on the entireeconomy? Third, and perhaps notquite as important, can thecontributions of these threecomponents of the new industrialrevolution—the computer,information technology, and theInternet—be separated and analyzedindividually?

As we try to answer thesequestions, we acquire a betterunderstanding of whether this isactually in a “new economy,” and ifso, precisely what is raisingproductivity. A plausible answer to

Source: http://www.brookings.org.

7ECONOMIC DEVELOPMENTS AND PROSPECTS

TheTheTheTheThe Non-AsianNon-AsianNon-AsianNon-AsianNon-Asian DevelopingDevelopingDevelopingDevelopingDeveloping EconomiesEconomiesEconomiesEconomiesEconomies

GDP growth in Africa in 1999 was slightly lower at3.1 percent, down from 3.4 percent the previous year.In the Middle East, GDP growth slowed to 1.8 per-cent from 3.2 percent in 1998 because of lower oiloutput. In 1999, growth in Latin America expandedby 0.1 percent as most countries in the region, exceptMexico and Peru, experienced recession.

Africa. Growth performance varied across the region,with many of the smaller countries—Cameroon, Côted’ Ivoire, Ghana, Mozambique, Sudan, Tanzania,Tunisia, and Uganda—performing remarkably well,with growth of 3.9-7 percent. Implementing appro-priate macroeconomic policies and favorable weatherconditions contributed to this relatively strong ex-

pansion. Algeria implemented an extensive set ofstructural reforms over the past five years, and in Tu-nisia consistently strong growth was underpinned byhealthy export performance supported by fiscal con-solidation and a flexible exchange rate policy.

However, growth in three of the largest Africaneconomies was modest. Growth in South Africa re-covered to 0.7 percent in 1999, only a slight improve-ment over 0.5 percent in 1998. Renewed financialmarket confidence; much lower interest rates; andimproved prospects for exports, particularly to Asia,contributed to this recovery. Despite rising oil pricesfollowing the reduction in Organization of PetroleumExporting Countries (OPEC) quotas in the second halfof 1999, lower oil prices in 1998 and early 1999—andthe subsequent reductions in oil production in com-pliance with lower OPEC quotas—reduced GDP

the first question, why the computeris only now so affecting the economy,is provided by a look at history.Economic historian Paul Davidargues that it takes decades for newtechnology to spread to the rest ofthe economy. His research showsthat it took several decades for thetechnology of the electric dynamo todiffuse sufficiently to raise industrialproductivity significantly. The samecould be true for computer use inbusiness, reinforced by the newinformation technology and theInternet.

To look for an answer to thesecond question regarding howproductivity gains may have spilledover from the computer andinformation technology sections,consider inventory control, moreefficient sourcing of inputs bycanvassing suppliers, and Internetretailing. Certainly inventory controlhas been improved by the use ofcomputers, but the cost savings arenot great. Input sourcing andInternet retailing may yieldproductivity advances in the future,

but the savings up to now are small.Instead, it may be that theacceleration in productivity in the1990s results from productivity gainsin the computer industry alone.There is no doubt that a genuineproductivity miracle has occurred inthis industry, and some evidencesuggests that it could have beenresponsible for the small overallacceleration in productivity in theentire economy. This suggests thatthere has been very little measurablediffusion of technology beyondcomputers.

The third question regardinghow much each of the three factorshave contributed individually togrowth may be answered by the sheerstrength in productivity in thecomputer industry. So far, whateverproductivity gains have been madeprobably result primarily from thetechnology revolution in the computerindustry alone and less from theInternet or information technology.

However, it is also plausible thatthe increased productivity has notbeen responsible for the reduced

inflation and unemployment andhigher growth. The InternationalMonetary Fund (IMF), in its latestWorld Economic Outlook 2000 suggeststhat a strong dollar and lower importcosts reduced consumer priceinflation between 1996 and 1998,masking the signs of overheating.Moreover, the IMF argues that thefinancial crisis in 1997-1998 helpedboost capital inflows, which in turnhelped lower interest rates andstrengthen the dollar despite thewidening trade deficit, thereby raisingdemand. The IMF also increased itsestimates of trend productivity,suggesting that the surge inproductivity in the past few years isnot as significant as previouslyestimated.

Whether the US economy hasmoved to a higher and seeminglysustainable growth rate, maintainingfull employment without inflation, istherefore still debatable. Only timewill tell whether the present upsurgein productivity heralded the arrival ofthe New Economy, or just anotherspike in the productivity chart.

ASIAN DEVELOPMENT OUTLOOK 20008

growth in Nigeria to 0.5 percent in 1999. This was ac-companied by rising budget and current account defi-cits. Morocco also grew slowly, as the economy wasadversely affected by a drought that decreasedagricultural output.

The implementation of structural reforms inAfrica has been constrained by the economic difficul-ties brought about by depressed non-oil commodityprices in recent years, and this continued in 1999.However, increased attention to privatization efforts,public sector reforms, and other structural measureshave in part been instrumental in improving thebusiness and investment environment in somecountries. Positive developments in trade and politi-cal cooperation have included the common externaltariff implemented by the West African Economic andMonetary Union, bilateral trade agreements betweenthe EU and some African economies, and plans forfree-trade areas in Eastern and Southern Africa.

Latin America. Many of the countries in this regionexperienced negative growth in 1999 following the1998 Brazilian currency crisis. The recession and de-valuation in Brazil—a major export market for therest of the region—combined with political instabilityin some countries to cause regional GDP growth toslow in 1999 to 0.1 percent from 2.2 percent in 1998.The three big Latin American countries, Argentina,Brazil, and Mexico, faced varying economic situations.Mexico enjoyed relatively robust growth of 3 percent,while Argentina and Brazil were in a recession, withnegative growth rates of 3 and 1 percent, respectively.All three faced difficult conditions in internationalfinancial markets: credit conditions hardened, anddebt-market access was more difficult following theBrady bond default in Ecuador and the consequentpossibility of involving private creditors in restructur-ing. The region weathered the storm largely throughforced adjustment of exchange rate, fiscal policy, orboth. Mexico had essentially separated itself from therest of the region through its strong trade dependenceon the US, which accounts for more than four fifthsof its exports. Besides Mexico, Peru is the only othercountry in the region that achieved growth. It tookadvantage of the recovery in the global demand forindustrial materials to expand production and increaserevenue in its primary and mining sectors.

Investors’ demand for a greater risk premium inview of exchange rate volatility and political instabil-ity, have kept real interest rates at extremely high lev-els in the region. Following the Brazilian devaluationin January 1999, secondary market spreads increasedfor most of the major developing country borrowers,including Latin America. However, there was apartial recovery later in the year as spreads fell some-what. The high-risk premium has curbed net capitalinflows that are needed to finance domesticinvestment. Foreign fund flows into local equity andmoney markets are being deterred because of poorgrowth prospects and exchange rate risk.

Much of the volatility in the region’s currencyand equity markets in 1999 resulted from the elec-tions in Argentina, the chance of debt default inArgentina and Mexico, and slow or negative growththrough much of the region. The recession in LatinAmerica and large public sector debt service worsenedthe region’s public finances in 1999. Even Chile, whichhad fiscal surpluses in the past five years, incurred adeficit. Despite the difficult environment, every ma-jor Latin American country achieved a primarysurplus in 1999.

The Middle East. Many countries in this regionemerged from the global financial crisis relatively un-scathed. The use of foreign exchange reserves andexternal portfolios to finance the fiscal deficits andtrade balances in the short term were used to avertthe contagion effects from other financial markets. Incountries with tighter financing constraints,contractionary expenditure policy, exchange rate de-valuation, and rescheduling of external debt were usedto regain stability.

Saudi Arabia, the main driver of growth in theArabian Peninsula and the Gulf, did not adjust itsspending to the fall in oil prices in 1998, and its gov-ernment was forced to draw on its substantial overseasassets to meet budgeted spending commitments. Fiscalausterity measures were implemented in 1999 andgrowth is expected to resume in 2000. Egypt continuedto drive growth in the Eastern Mediterranean area.Despite a change in the cabinet in 1999, progress ineconomic reform and liberalization propelled GDPgrowth to 6 percent. Growth also increased in Israel,due to greater foreign investment and political stabil-

9ECONOMIC DEVELOPMENTS AND PROSPECTS

ity. Foreign direct investment (FDI) in the Middle Eastand the North Africa (MENA) region continued tolag behind other emerging markets because of the lowlevel of integration with global capital markets. Whileglobal FDI inflow rose by 38.7 percent in 1998 to $643.9billion, inflows into the MENA region fell by 6 percentto $7.2 billion and accounted for only 1.1 percent ofglobal levels, down from 1.7 percent in 1997.

The Asian and PThe Asian and PThe Asian and PThe Asian and PThe Asian and PacificacificacificacificacificDeveloping EconomiesDeveloping EconomiesDeveloping EconomiesDeveloping EconomiesDeveloping Economies

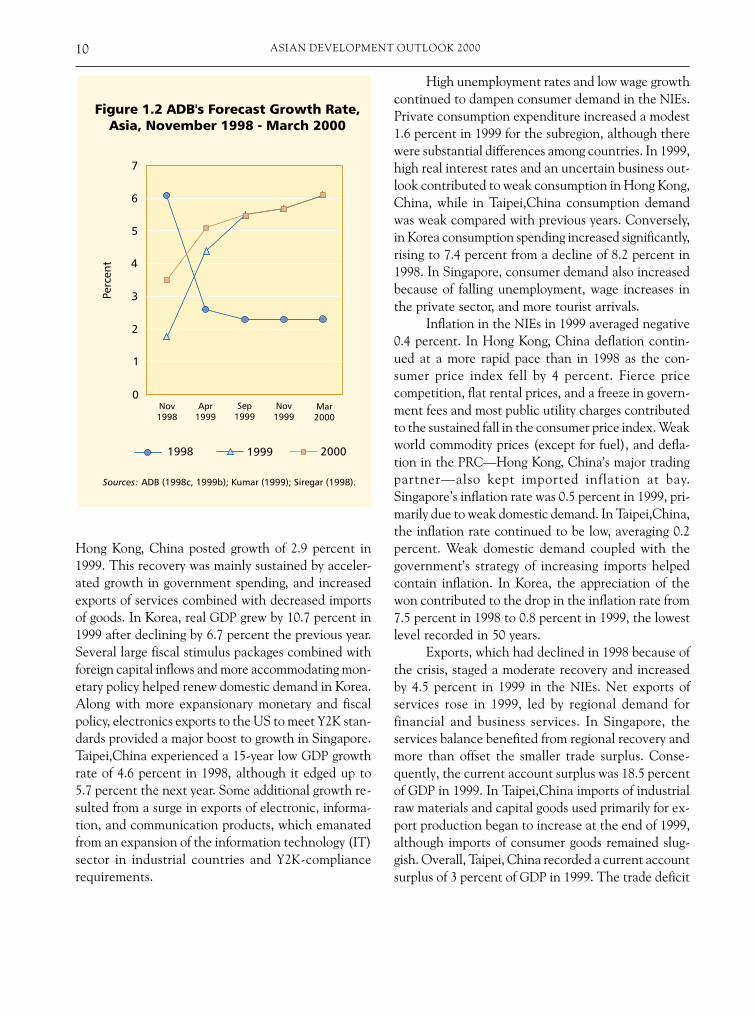

The Asian economic outlook changed dramaticallyin 1999 (figure 1.2). In the fall of 1998, several econo-mies were in recession, capital flows had turned nega-tive, and the outlook was generally pessimistic. Inearly 1999, an average annual growth of 4.4 percentwas forecast for the region. This was revised to 5.7percent in the fourth quarter of 1999, and the actualoutcomes for the year have exceeded 6 percent.

The recovery has been uneven across develop-ing Asia. Growth in the Republic of Korea (hence-forth referred to as Korea) was particularly strong,along with the PRC and India. In tandem with theeconomic recovery in Russia in 1999, most countriesin Central Asia experienced higher rates of growth,although inflation and external imbalances continuedto be relatively high.

The faster-than-expected recovery in the firsthalf of 1999 in most of the crisis-affected countries—Korea, Malaysia, Philippines, and Thailand—resultedfrom stimulative monetary and fiscal policy and in-creased exports, led by a surge in worldwide demandfor electronics. Consumer sentiment also improved,bolstering domestic demand and economic growth. Inthe second half of 1999, the recovery was supportedby continued expansionary policies and progress onimplementing structural reforms to deal with thefinancial crisis.

In the NIEs and in Southeast Asia, either aresumption of growth or increased growth, combinedwith generally buoyant equity markets, helped improveaggregate demand and consumer confidence. Con-sumers began to spend after two years of belt-tighten-ing. A decrease in consumer goods prices in somecountries further increased purchasing power, partlyoffsetting selective wage cuts and high unemployment.

Korea, one of the countries most affected by thefinancial crisis, led the region with double-digiteconomic growth in 1999. Stock rebuilding, increasesin private consumption and investment, and increasedexports boosted Korean production to above precrisislevels. Among the other crisis-affected countriesgrowth ranged from 0.2 to 5.4 percent, as thesecountries also experienced a stronger-than-expectedrecovery from the crisis. Growth in the PRC slowedfrom 7.8 percent in 1998 to 7.1 percent in 1999, as itspump priming of the economy through expansionaryfiscal policy weakened and export growth remainedmodest. South Asia continued to be a strongly per-forming region with an aggregate growth rate accel-eration of 5.5 percent in 1999. Growth in India, thelargest economy in the region, was robust at 5.9 per-cent. A strong increase in industry sector activity waspartially offset by weak agriculture output growth.Other countries in the region, including Bangladeshand Sri Lanka, also did reasonably well.

Currency markets in Asia stabilized in 1999 be-cause of structural reforms, interest rate cuts in mostof the industrial countries, positive expectations aboutthe Japanese economy, and increased financialcommitments from the international community. Con-sequently, foreign capital started returning to Asia.Private capital flows returned to five crisis-affectedcountries—Indonesia, Korea, Malaysia, Philippines,and Thailand—with net private inflows of $5.1 billionin 1999, as opposed to a net outflow of $38.6 billion in1998. In the PRC, net private flows slowed from about$40 billion in 1998 to around $27 billion in 1999, asFDI eased and debts were repaid. At 6.2 percent,growth in the Asian region is expected to remain vir-tually unchanged in 2000. Slower growth in the NIEsand the PRC will be offset by more rapid growth inSoutheast Asia, South Asia, and the Central Asianrepublics.

The Newly Industrialized Economies. The NIEsrebounded strongly in 1999. GDP growth was 7.0 per-cent compared with a contraction of 1.9 percent in1998. There was slight deflationary pressure as the ag-gregate price level fell by 0.4 percent.

Despite the overall revival of the NIEs, economicperformance varied significantly among countries.After a severe recession in 1998, the economy of

ASIAN DEVELOPMENT OUTLOOK 200010

Hong Kong, China posted growth of 2.9 percent in1999. This recovery was mainly sustained by acceler-ated growth in government spending, and increasedexports of services combined with decreased importsof goods. In Korea, real GDP grew by 10.7 percent in1999 after declining by 6.7 percent the previous year.Several large fiscal stimulus packages combined withforeign capital inflows and more accommodating mon-etary policy helped renew domestic demand in Korea.Along with more expansionary monetary and fiscalpolicy, electronics exports to the US to meet Y2K stan-dards provided a major boost to growth in Singapore.Taipei,China experienced a 15-year low GDP growthrate of 4.6 percent in 1998, although it edged up to5.7 percent the next year. Some additional growth re-sulted from a surge in exports of electronic, informa-tion, and communication products, which emanatedfrom an expansion of the information technology (IT)sector in industrial countries and Y2K-compliancerequirements.

High unemployment rates and low wage growthcontinued to dampen consumer demand in the NIEs.Private consumption expenditure increased a modest1.6 percent in 1999 for the subregion, although therewere substantial differences among countries. In 1999,high real interest rates and an uncertain business out-look contributed to weak consumption in Hong Kong,China, while in Taipei,China consumption demandwas weak compared with previous years. Conversely,in Korea consumption spending increased significantly,rising to 7.4 percent from a decline of 8.2 percent in1998. In Singapore, consumer demand also increasedbecause of falling unemployment, wage increases inthe private sector, and more tourist arrivals.

Inflation in the NIEs in 1999 averaged negative0.4 percent. In Hong Kong, China deflation contin-ued at a more rapid pace than in 1998 as the con-sumer price index fell by 4 percent. Fierce pricecompetition, flat rental prices, and a freeze in govern-ment fees and most public utility charges contributedto the sustained fall in the consumer price index. Weakworld commodity prices (except for fuel), and defla-tion in the PRC—Hong Kong, China’s major tradingpartner—also kept imported inflation at bay.Singapore’s inflation rate was 0.5 percent in 1999, pri-marily due to weak domestic demand. In Taipei,China,the inflation rate continued to be low, averaging 0.2percent. Weak domestic demand coupled with thegovernment’s strategy of increasing imports helpedcontain inflation. In Korea, the appreciation of thewon contributed to the drop in the inflation rate from7.5 percent in 1998 to 0.8 percent in 1999, the lowestlevel recorded in 50 years.

Exports, which had declined in 1998 because ofthe crisis, staged a moderate recovery and increasedby 4.5 percent in 1999 in the NIEs. Net exports ofservices rose in 1999, led by regional demand forfinancial and business services. In Singapore, theservices balance benefited from regional recovery andmore than offset the smaller trade surplus. Conse-quently, the current account surplus was 18.5 percentof GDP in 1999. In Taipei,China imports of industrialraw materials and capital goods used primarily for ex-port production began to increase at the end of 1999,although imports of consumer goods remained slug-gish. Overall, Taipei, China recorded a current accountsurplus of 3 percent of GDP in 1999. The trade deficit

11ECONOMIC DEVELOPMENTS AND PROSPECTS

TTTTTable 1.1 able 1.1 able 1.1 able 1.1 able 1.1 Selected Economic Indicators, Developing Asia, 1997-2001Selected Economic Indicators, Developing Asia, 1997-2001Selected Economic Indicators, Developing Asia, 1997-2001Selected Economic Indicators, Developing Asia, 1997-2001Selected Economic Indicators, Developing Asia, 1997-2001(percent)

1997 1998 1999 2000 2001

Gross domestic product (annual change)Developing Asia 6.0 2.3 6.2 6.2 6.0

Newly industrialized economies 5.7 -1.9 7.0 6.5 6.0PRC and Mongolia 8.7 7.8 7.1 6.5 6.0Central Asian republics 3.3 0.8 2.8 3.0 3.6Southeast Asia 3.7 -7.5 3.2 4.6 5.0South Asia 4.7 6.2 5.5 6.4 6.6The Pacific -3.2 1.2 4.4 — —

Inflation (change in CPI)Developing Asia 4.3 5.5 1.6 3.0 3.3

Newly industrialized economies 3.5 3.9 -0.4 1.8 2.6PRC and Mongolia 2.8 -0.8 -1.4 1.8 2.0Central Asian republics 21.4 11.4 21.9 15.1 10.7Southeast Asia 5.5 21.3 7.4 4.7 4.6South Asia 5.6 7.1 4.1 5.0 5.4The Pacific 3.9 9.9 10.4 — —

Current account balance/GDPDeveloping Asia 0.5 4.1 3.8 1.5 0.5

Newly industrialized economies 1.6 9.3 6.4 3.7 2.4PRC and Mongolia 3.3 3.0 1.2 -0.4 -0.9Central Asian republics -4.0 -4.5 -2.0 -2.4 -2.3Southeast Asia -3.4 7.0 7.6 3.3 0.8South Asia -1.4 -1.9 -2.2 -3.9 -3.0The Pacific -0.9 1.8 — — —

— Not available.CPI consumer price index.

Sources: Appendix tables.

narrowed, as there was a significant rebound in re-exports to and from Asia, especially Indonesia, Japan,Korea, and Singapore. In Hong Kong, China exportsrecovered but growth was still negative in 1999. InKorea, export growth recovered strongly to more than10 percent from a 4.7 percent deficit in 1998, as a resultof stronger competitiveness vis-a-vis Japan and re-covery in Asian markets.

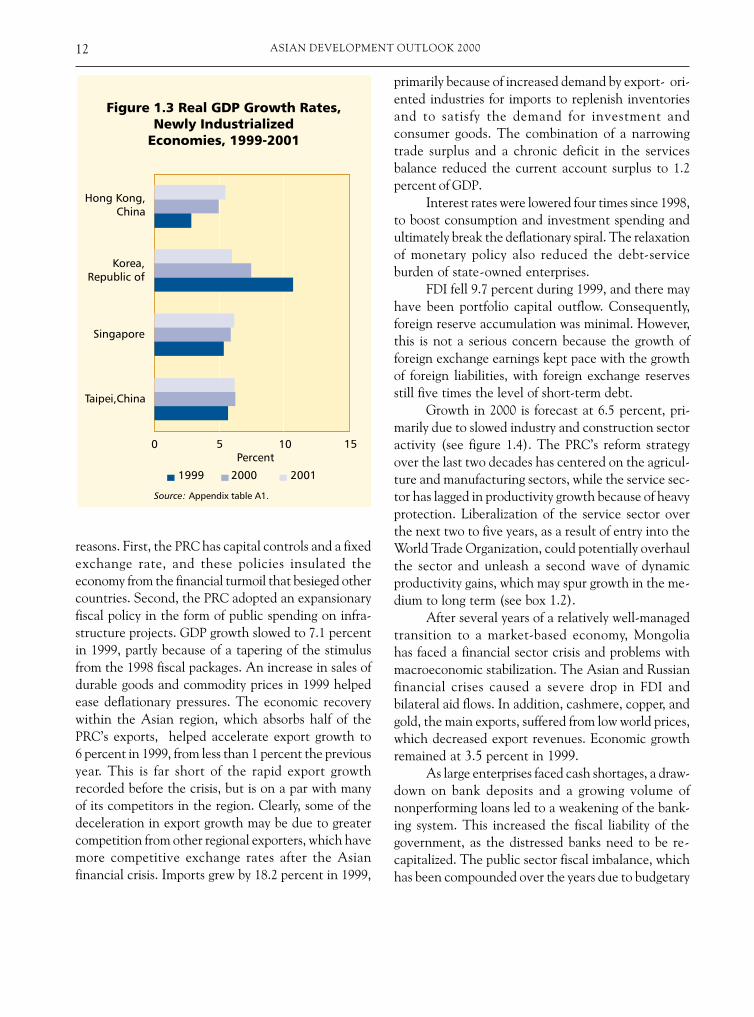

Future economic expansion in the region willbe driven by growth in domestic demand, efficiencygains resulting from progress in structural reforms andIT-related exports. GDP growth in 2000 is forecast tobe 6.5 percent for the NIEs (see figure 1.3). This growthrate, while quite robust, is still somewhat lower thanin 1999, primarily because of a decline in Korea’s growth,

where double-digit growth is not expected to be sus-tained. Export growth in the NIEs is projected to in-crease more, to 8.9 percent in 2000. This would be thehighest growth rate in exports since 1995, but it fallsshort of the average of nearly 15 percent between 1992and 1995. A large-scale restructuring of capacities andpolicy measures to regain competitiveness may be re-quired before the NIEs regain such export dynamism.Import demand will recover sharply as growth returnsand the increased exports in turn drive up demand forraw materials and components.

PRC and Mongolia. Despite the Asian financial crisis,the PRC maintained a robust growth rate of 7.8 per-cent in 1998, and did not fall into recession for two

ASIAN DEVELOPMENT OUTLOOK 200012

reasons. First, the PRC has capital controls and a fixedexchange rate, and these policies insulated theeconomy from the financial turmoil that besieged othercountries. Second, the PRC adopted an expansionaryfiscal policy in the form of public spending on infra-structure projects. GDP growth slowed to 7.1 percentin 1999, partly because of a tapering of the stimulusfrom the 1998 fiscal packages. An increase in sales ofdurable goods and commodity prices in 1999 helpedease deflationary pressures. The economic recoverywithin the Asian region, which absorbs half of thePRC’s exports, helped accelerate export growth to6 percent in 1999, from less than 1 percent the previousyear. This is far short of the rapid export growthrecorded before the crisis, but is on a par with manyof its competitors in the region. Clearly, some of thedeceleration in export growth may be due to greatercompetition from other regional exporters, which havemore competitive exchange rates after the Asianfinancial crisis. Imports grew by 18.2 percent in 1999,

primarily because of increased demand by export- ori-ented industries for imports to replenish inventoriesand to satisfy the demand for investment andconsumer goods. The combination of a narrowingtrade surplus and a chronic deficit in the servicesbalance reduced the current account surplus to 1.2percent of GDP.

Interest rates were lowered four times since 1998,to boost consumption and investment spending andultimately break the deflationary spiral. The relaxationof monetary policy also reduced the debt-serviceburden of state-owned enterprises.

FDI fell 9.7 percent during 1999, and there mayhave been portfolio capital outflow. Consequently,foreign reserve accumulation was minimal. However,this is not a serious concern because the growth offoreign exchange earnings kept pace with the growthof foreign liabilities, with foreign exchange reservesstill five times the level of short-term debt.

Growth in 2000 is forecast at 6.5 percent, pri-marily due to slowed industry and construction sectoractivity (see figure 1.4). The PRC’s reform strategyover the last two decades has centered on the agricul-ture and manufacturing sectors, while the service sec-tor has lagged in productivity growth because of heavyprotection. Liberalization of the service sector overthe next two to five years, as a result of entry into theWorld Trade Organization, could potentially overhaulthe sector and unleash a second wave of dynamicproductivity gains, which may spur growth in the me-dium to long term (see box 1.2).

After several years of a relatively well-managedtransition to a market-based economy, Mongoliahas faced a financial sector crisis and problems withmacroeconomic stabilization. The Asian and Russianfinancial crises caused a severe drop in FDI andbilateral aid flows. In addition, cashmere, copper, andgold, the main exports, suffered from low world prices,which decreased export revenues. Economic growthremained at 3.5 percent in 1999.

As large enterprises faced cash shortages, a draw-down on bank deposits and a growing volume ofnonperforming loans led to a weakening of the bank-ing system. This increased the fiscal liability of thegovernment, as the distressed banks need to be re-capitalized. The public sector fiscal imbalance, whichhas been compounded over the years due to budgetary

13ECONOMIC DEVELOPMENTS AND PROSPECTS

mismanagement, has begun to threaten thegovernment’s ability to complete ongoing reforms.

Mongolia’s short- to medium-term prospectsdepend on the success of banking sector reforms,whether fiscal imbalances are addressed, and thestrength of export performance. GDP growth in 2000is forecast at 4 percent, with the main sources of growthexpected to be mining and manufacturing. Reformsin the agriculture sector, promotion of small-scale in-dustries, and escalating private sector activity (whichconstituted 60 percent of GDP in 1998) are expectedto stimulate growth.

The Central Asian Republics. The economies ofCentral Asia grew at 2.8 percent in 1999, up from theprevious year’s 0.8 percent. Kazakhstan implementedmajor policy adjustments, including floating its cur-rency, the tenge. Stabilization of commodity prices andprudent fiscal policy provided breathing space forimplementing reforms, which helped the economygrow to 1.7 percent in 1999, compared with a 1.9 per-

cent contraction the previous year. The KyrgyzRepublic’s economy was in the middle of a major fis-cal and financial adjustment process, but the GDPgrowth rate in 1999 was 3.6 percent, up from 2.1 per-cent in 1998. The engine of growth was the agricul-ture sector, which grew by 8.7 percent. Tajikistan madesubstantial progress in macroeconomic stabilizationand its transition to a market economy in 1998. Itsthree-year IMF reform program is largely on track.However, GDP growth was only 3.7 percent in 1999,considerably lower than the 1998 rate of 5.3 percent,reflecting stagnant growth in both agriculture andindustry. Uzbekistan, the country with the largestpopulation in Central Asia, is following its own gradualreform program. Foreign exchange controls, thecountry’s policy of self-sufficiency, and rudimentaryfinancial markets all impede more rapid economicprogress. GDP growth in 1999, at 4.4 percent, was thesame rate recorded in 1998.

Future economic performance in the CentralAsian republics will depend on Russia’s continuedeconomic recovery and improvement in internationalcommodity prices (see figure 1.5). The extent to whichthe respective countries are affected by these two fac-tors varies considerably. Political stability will also playa role in the future development of these formerSoviet republics.

The Southeast Asian Economies. The V-shapedrecovery in the crisis countries in this region can beviewed partly as a snapback given the sharp negativegrowth the previous year. Nevertheless, various posi-tive factors, both domestic and external, contributedto the recovery, including increased consumption,stock rebuilding, massive fiscal stimulus, and loosemonetary policy. New policy measures to address cor-porate and financial sector problems also supportedthe recovery, and helped contain and even reduce thelevel of nonperforming loans. The recovery was stimu-lated also by the strengthened Japanese economy andincreased financial resource flows from the interna-tional community, which resulted in improvedbalance-of-payments position in most of thesubregion. Together with inflows of foreign aid andprogress on foreign debt rollovers, capital flows werestabilized, and confidence in these countries was re-stored. The availability of fiscal surpluses, a legacy of

ASIAN DEVELOPMENT OUTLOOK 200014

Source: Institute for International Economics (1999).

past prudent policies, and a favorable external envi-ronment permitted the easing of fiscal and monetarypolicy and reduced interest rates without causing vola-tility in foreign exchange market.

After an initially tenuous start, Southeast Asia’srecovery has proved more rapid and broad-based thananticipated. All the countries in the subregion regis-tered growth in 1999 (see figure 1.6). The GDP growthrate for the subregion was 3.2 percent in 1999, in sharp

With merchandise exports of nearly$200 billion in 1998, the People’sRepublic of China (PRC) is theninth largest exporter in the world.The PRC is expected to join theWorld Trade Organization (WTO) in2000, an event of major economicsignificance for the Chinese andglobal economy. One of the majorobstacles to the PRC’s 13-year bid togain accession to WTO was clearedin November 1999, when the UnitedStates and the PRC signed a bilateraltrade agreement detailing a far-reaching set of commitments thatthe PRC will have to meet as a WTOmember. Although the PRC will nowhave to negotiate similar agreementswith the European Union andseveral other smaller trading partnersbefore it can join WTO, theagreement with the US is pivotal,because the concessions it extractedfrom the PRC are likely to satisfymany other countries. The terms of thebilateral agreement with the USinclude the following• Agriculture: Overall tariffs for allagricultural products are to be cutfrom an average of 22 percent to17.5 percent by January 2004, witheven lower rates for beef; cheese;wine; and a range of fruits, includinggrapes, oranges, apples, cherries, andalmonds. Moreover, market accesswill be further enhanced by aprogressive increase in quotas on

bulk commodities such as corn,cotton, rice, soybean oil, and wheat,and the elimination of health andhygiene standards that are not basedon scientific evidence. The PRC hasalso committed itself to eliminatingexport subsidies and liberalizingdomestic trade in agriculture byallowing private entities to engage inimporting and distributingagricultural products without goingthrough state trading enterprises.• Industry: Average tariffs on allindustrial products are to be cut fromthe 1997 average of 24.6 percent to9.4 percent by 2005, with sharperreductions for tariffs on automobiles(from 80-100 percent to 25 percentby 2006), chemicals, wood, and paper.Quotas for fiber optic cables andother products are to be eliminatedupon the PRC’s accession to WTO,and most of the remaining quotas willbe increased before being phased outby 2005. The PRC will also join theInformation Technology Agreementand eliminate tariffs onsemiconductors, computers, and allInternet-related equipment by 2005.• Services: The PRC is committedto eliminating most foreign equityand geographical restrictions on itsservice sectors within two to six years.It will also accede to WTO’s BasicTelecommunications and FinancialServices agreements. The BasicTelecommunications agreement will

allow up to 49 percent foreignownership in mobile, domestic, andinternational land and sea serviceswithin five to six years and 50percent ownership in paging andvalue-added services within two years.The Financial Services agreementwill phase out all geographicalrestrictions on foreign insurerswithin three years and expand theirscope of activities to include group,health, and pension policies withinfive years. The PRC will also allow50 percent foreign ownership in lifeinsurance joint ventures and 100percent ownership in reinsuranceand nonlife insurance within twoyears. Foreign banks will gain fullmarket access within five years andwill be able to conduct localcurrency transactions with Chineseenterprises and individuals withintwo to five years. Joint venture firmswith minority foreign stakes will alsobe able to underwrite domestic- andforeign-currency-denominatedsecurities.• Trading and distribution rights:The PRC will grant full trading anddistribution rights to foreign firmswithin three years of accession toWTO. This will give foreign firmsthe right to import and exportdirectly without Chineseintermediaries, and to handlewholesaling, retailing, maintenanceand repair, and transportation.

Box 1.2 The People’s Republic of China’s Entryinto the World Trade Organization: Who Wins and Loses?

contrast to a negative growth of 7.5 percent in 1998.Nevertheless, domestic consumption and investment,on average, remained well below precrisis levels.

In the first half of 1999, the recovery in globaldemand for semiconductors, which emanated frompreparations for achieving Y2K compliance, led toa surge in exports from Malaysia, Philippines, andThailand. Among the crisis-affected countries, onlythe Philippines escaped negative export growth in

15ECONOMIC DEVELOPMENTS AND PROSPECTS

Foreign firms will also be able toengage in such auxiliary services asleasing, air courier, warehousing,packaging, and advertising.

These sweeping reforms arelikely to have far-reaching domesticand international implications. Inthe short term, many analysts expectthe reforms to lead to a considerableloss of output and a sharp increase inunemployment. For instance, infarming, cuts in tariffs and increasesin tariff quotas will probably result ina substantial increase in wheatimports, as domestic prices remainfar above world market prices. Thiswill bring about a sharp reduction inoutput and an increase inunemployment. The auto industrywill probably experience a similarsharp reduction in output and jobs,as the new WTO regime slashestariffs and allows foreign carmakersto provide financial assistance tobuyers. This may causerationalization of the fragmented andinefficient car industry that currentlyhas more than 100 manufacturers ofvehicles and components. Manydomestic vehicle makers will notsurvive the cost cutting needed toremain competitive.

WTO membership also willbring far-reaching changes to thefinancial sector. As foreign banks willeventually be allowed to conductlocal currency business with bothChinese firms and individuals,competition within the domesticfinancial sector is certain to intensify.

Domestic banks will need to improvetheir banking practices andstrengthen their balance sheets.Otherwise, they could face a loss ofdeposits to foreign banks that havefewer nonperforming loans and can,therefore, offer higher interest ratesto depositors.

However, over time theefficiency gains from reallocatingboth capital and labor to morecompetitive sectors within theChinese economy should more thanoffset these short-term losses. Thisshould result in increasedproductivity, profitability, investment,and employment. Accession to WTOwould then deepen and accelerateChinese liberalization and help lockin the tenuous domestic reform process.

What will be the probableimpact on the rest of the world whenthe PRC joins WTO? Apart fromincreased access to the PRC’sinternal market, WTO membershipwould make all investors who use thePRC as a production and exportplatform feel more secure aboutaccess to third markets as well as thedomestic market. Foreign retailersand distributors will also be able tosell products and services directly toChinese consumers for the first time.This will give Chinese consumersgreater choice at lower prices.Regional economies are likely to beamong the main beneficiaries of thePRC’s liberalization measures.Established producers of qualityconsumer durable goods, including

Japan; Republic of Korea; andTaipei,China, could gain significantlyfrom better access to the region’ssecond-largest market. SoutheastAsian exporters of natural resourcessuch as Indonesia and agriculturalproducers such as Thailand couldgain from greater access to the PRCmarkets, while Indian pharmaceuticalmanufacturers could potentially gainaccess to the PRC’s highly protectedpharmaceutical market. On theexport side, the PRC’s accession toWTO will make it an even moreformidable competitor in labor-intensive products in the worldmarket such as shoes, toys, bags, andtextiles. Some regional economieswill lose export markets to the PRC inthe textile and apparel sector whenthe Multi-Fibre Agreement quotasare phased out by 2005. Finally, giventhat the PRC’s accession commitmentsto WTO are considerably more liberalthan the commitments of a number ofregional member countries, this couldprompt a further round ofcompetitive liberalization within theregion, as the PRC begins toimplement its WTO commitments.

The PRC’s accession to WTOshould not be seen as a zero sum gamewhere one side loses and the othergains. Although there may be short-term costs for both sides, the long-term benefits from an expansion andliberalization of the world tradingsystem from the PRC’s membershipwould no doubt far outweigh theseshort-term costs.

the past two years, achieving an export growth rate of16.9 percent in 1998 and 18.8 percent in 1999. It wasless constrained by the crisis, as it had undergone amajor restructuring in the 1980s. Its exports also weremore geared to the US market, which remained buoyant.

Consumer spending began to recover in the firsthalf of 1999. In the four crisis-affected countries, con-sumer confidence indicators stabilized and are improv-ing. Even Indonesia, which lags behind the other

countries in the region in terms of consumer confi-dence, registered a private consumption growth rateof 2 percent in 1999, while the Philippines andThailand registered 2.5 percent. Nevertheless, the 1999level of private consumption expenditures remainedbelow precrisis levels.

Pump priming of the regional economies throughlarge fiscal stimulus packages was used extensively in1998 and 1999, causing concern that fiscal imbalances

ASIAN DEVELOPMENT OUTLOOK 200016

were getting out of hand. Assuming a recovery of 50-60 percent of nonperforming loans in these econo-mies, the cost of fiscal support for bank recapitalizationwas expected to be about 15 percent of GDP inMalaysia and more than 30 percent in Indonesia andThailand. Actual recovery rates in 1999 were, how-ever substantially lower.

The improvement in economic performance,combined with the return of portfolio capital to theregion, resulted in a surge in the equity market pricesby 25.4 percent in dollar terms during 1999. This wassignificantly above the 6.7 percent and 4.5 percentrecorded in the US and world stock markets, respec-tively. This boosted confidence in domestic marketsand stimulated consumption spending.

Price stability continued to improve in the re-gion. In Cambodia, Lao People’s Democratic Republic,Philippines, Thailand, and Viet Nam, inflation fell in1999, reflecting lower food prices. Indonesia displayeda dramatic decline in its inflation rate, from 58.5 per-cent in 1998 to around 20.5 percent in 1999, because of

lower food prices and unused industrial capacity. Amore stable political environment and increased for-eign capital inflows also helped stabilize prices, par-ticularly during the second half of the year.

Short-term nominal interest rates across the re-gion remained below precrisis averages, with theexception of Indonesia. Thailand’s three-monthinterest rate of 4.00-4.25 percent in December 1999 issignificantly below the 10.7 percent recorded for1991-1996. The interest rate declines result from im-provements in the balance of payments combined withan expansionary monetary policy. Central banks inthe region kept short-term interest rates low to keepfinancial sector reforms on track and bolster demand.

On the external balance, the substantial currentaccount surpluses that accompanied the initial collapsein economic activity lifted foreign exchange reservesto record levels in Malaysia and the Philippines during1998. Combined with the announcement of structuralreforms and macroeconomic stabilization programs,this led to a resumption of foreign capital inflows andboosted investor sentiment. Strong FDI offset the lowlevel of domestic investment somewhat. Import growthtended to outstrip export growth by a large margin inseveral countries because of rising demand from in-creased industry sector activity. However, imports con-tinued to decline in Indonesia, so the trade and currentaccount balances in the region’s totals changed onlyslightly compared with 1998.

Growth in 1999 emanated from continued im-provement in domestic demand that arose from ex-pansionary macroeconomic policies, combined withimproved external demand that resulted fromexpanded world and intraregional trade. The 2000forecast for Southeast Asia is for a modest strength-ening of growth to 4.6 percent. This upward trendshould be supported by the boom in the electronicsindustry, continued economic growth in the US, likelyupturn in euro area, and the possible continued re-covery of the Japanese economy.

South Asia. South Asia continues to be a strong per-former, largely because of the strength of the Indianeconomy. Growth in the subregion was 6.2 and 5.5percent in 1998 and 1999, respectively. In India, theindustry sector showed signs of an increase after threeyears of sluggish performance. Combined with in-

17ECONOMIC DEVELOPMENTS AND PROSPECTS

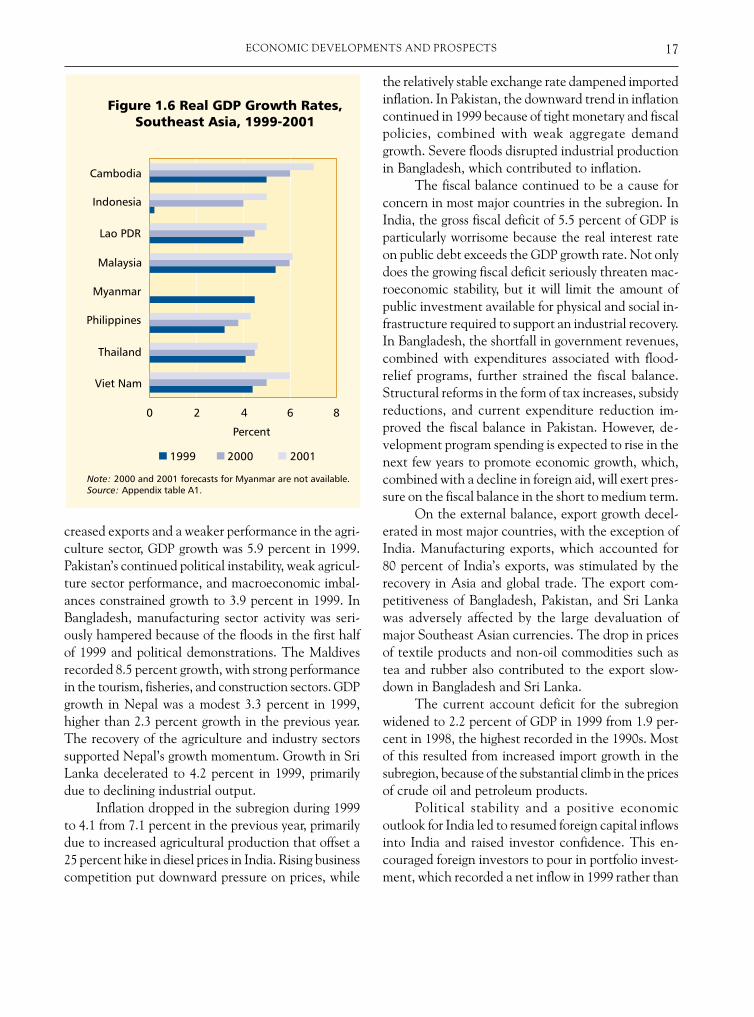

creased exports and a weaker performance in the agri-culture sector, GDP growth was 5.9 percent in 1999.Pakistan’s continued political instability, weak agricul-ture sector performance, and macroeconomic imbal-ances constrained growth to 3.9 percent in 1999. InBangladesh, manufacturing sector activity was seri-ously hampered because of the floods in the first halfof 1999 and political demonstrations. The Maldivesrecorded 8.5 percent growth, with strong performancein the tourism, fisheries, and construction sectors. GDPgrowth in Nepal was a modest 3.3 percent in 1999,higher than 2.3 percent growth in the previous year.The recovery of the agriculture and industry sectorssupported Nepal’s growth momentum. Growth in SriLanka decelerated to 4.2 percent in 1999, primarilydue to declining industrial output.

Inflation dropped in the subregion during 1999to 4.1 from 7.1 percent in the previous year, primarilydue to increased agricultural production that offset a25 percent hike in diesel prices in India. Rising businesscompetition put downward pressure on prices, while

the relatively stable exchange rate dampened importedinflation. In Pakistan, the downward trend in inflationcontinued in 1999 because of tight monetary and fiscalpolicies, combined with weak aggregate demandgrowth. Severe floods disrupted industrial productionin Bangladesh, which contributed to inflation.

The fiscal balance continued to be a cause forconcern in most major countries in the subregion. InIndia, the gross fiscal deficit of 5.5 percent of GDP isparticularly worrisome because the real interest rateon public debt exceeds the GDP growth rate. Not onlydoes the growing fiscal deficit seriously threaten mac-roeconomic stability, but it will limit the amount ofpublic investment available for physical and social in-frastructure required to support an industrial recovery.In Bangladesh, the shortfall in government revenues,combined with expenditures associated with flood-relief programs, further strained the fiscal balance.Structural reforms in the form of tax increases, subsidyreductions, and current expenditure reduction im-proved the fiscal balance in Pakistan. However, de-velopment program spending is expected to rise in thenext few years to promote economic growth, which,combined with a decline in foreign aid, will exert pres-sure on the fiscal balance in the short to medium term.

On the external balance, export growth decel-erated in most major countries, with the exception ofIndia. Manufacturing exports, which accounted for80 percent of India’s exports, was stimulated by therecovery in Asia and global trade. The export com-petitiveness of Bangladesh, Pakistan, and Sri Lankawas adversely affected by the large devaluation ofmajor Southeast Asian currencies. The drop in pricesof textile products and non-oil commodities such astea and rubber also contributed to the export slow-down in Bangladesh and Sri Lanka.

The current account deficit for the subregionwidened to 2.2 percent of GDP in 1999 from 1.9 per-cent in 1998, the highest recorded in the 1990s. Mostof this resulted from increased import growth in thesubregion, because of the substantial climb in the pricesof crude oil and petroleum products.

Political stability and a positive economicoutlook for India led to resumed foreign capital inflowsinto India and raised investor confidence. This en-couraged foreign investors to pour in portfolio invest-ment, which recorded a net inflow in 1999 rather than

ASIAN DEVELOPMENT OUTLOOK 200018

a net outflow as in 1998. However, a deterioration ofthe political environment in Pakistan and Sri Lankaslowed the inflow of foreign capital into these coun-tries. FDI decreased to $225 million in Bangladesh in1999 from $317 million in 1998. Most of the inflowswere to the natural gas and power sectors, which ac-count for 60 percent of total FDI.

Aggregate growth in South Asia for 2000 is fore-cast at 6.4 percent (see figure 1.7). Growth in Indiawill increase slightly, with industry and service sectorgrowth remaining strong. Political stability in the re-gion will be essential in determining the course of eco-nomic policy in the subregion and the prospects forreaching the per capita income levels attained in theNIEs and Southeast Asia. The opening of domesticcapital markets and integration with international fi-nancial markets will increase net capital inflows andimprove the access to international financial markets.These synergies will help alleviate the negative effectsof chronic fiscal deficits, which otherwise would havecrowded out private sector investment in a relativelyclosed economy.

The Pacific. The Pacific subregion as a whole grew by4.4 percent in 1999, compared with 1.2 percent in1998. Sound macroeconomic management and tightmonetary policy in those countries that have their owncurrency contributed to the improved economicperformance in most of the subregion. Papua NewGuinea, the subregion’s largest economy, experiencedan acceleration in real GDP growth of 3.9 percent in1999, despite intensified macroeconomic instability.Faster growth resulted from higher commodity pricesand increased exports. With the exception of Kiribati,Tuvalu, and Vanuatu, all the economies registeredfaster growth in 1999, including the Fiji Islands, wherethe recovery in agricultural production and growth ingarment manufacturing contributed to a 1999 GDPgrowth of 7.8 percent. Inflation in the subregion roseto 10.4 percent in 1999, mostly because inflation inPapua New Guinea rose to 16 percent. The govern-ment failed to secure external funding to finance fis-cal imbalances, and had to rely on domestic financingof the budget deficit and accumulation of arrears ondebt-service payments.

The economic prospects in the short to mediumterm will depend on the success of public sectorreforms, sustained macroeconomic stabilization, andprivate sector development. The potential of this sub-region will not be realized unless macroeconomic sta-bility is sustained and improvements made in theeconomic policy environment. In some countries, eco-nomic policy continues to be characterized by lack oftransparency and predictability that discourages pros-pects for both domestic and foreign investments.

RISKS AND UNCERTRISKS AND UNCERTRISKS AND UNCERTRISKS AND UNCERTRISKS AND UNCERTAINTIESAINTIESAINTIESAINTIESAINTIES

Recovery in Asia was robust during 1999. The trans-formation of developing Asia from financial crisis in1997 and 1998 to the world’s fastest-growing regionhas exceeded all expectations. It took developing Asialess than two years to return to the precrisis level ofindustrial production. Prospects for 2000 depend onsustainability of domestic demand growth, not onlythrough growth in consumption, but also an upturnin investment demand and favorable global economicconditions. Investment may have to rise as capacityutilization rates go up and capacity restructuring oc-curs in response to technological advance and com-

19ECONOMIC DEVELOPMENTS AND PROSPECTS

petitive pressures. However, this is predicated on anupturn in credit growth, which is still uncertain be-cause bank lending remains weak.

Rapid growth in intraregional trade feeding intoincreased domestic demand and higher real incomesis also expected. For these effects to prevail in theAsian subregion, the external environment will alsohave to be favorable. The continued expansion in glo-bal GDP and the expected rise in international tradevolumes, combined with continued firmness in com-modity prices, are crucial in maintaining export growthmomentum. The major concern will be the nature ofcorrection in asset prices in the US, the strength ofthe cyclical upswing in the euro area, and the prospectsfor Japanese recovery. A favorable external environ-ment requires a soft landing for the US economy as afurther tightening of monetary policy accomplishes asmooth transition to slower growth. It also requires astrengthening of the cyclical upswing in the euro areadespite more monetary policy tightening by theEuropean Central Bank and a continuation of theJapanese recovery.

Even as domestic demand conditions in theworld economy improved, OPEC decided in April 1999to cut back production. Unless oil prices moderate,another oil shock could derail Asia’s recovery as wellas the rest of the world economy (see box 1.3).

From a domestic aggregate demand perspective,expansionary domestic policies and rallies in equitymarkets in developing Asia have helped to improvebusiness and consumer sentiment, and have had a salu-tary effect on consumption. These factors seem to beoffsetting the constraints on domestic consumptionimposed by high unemployment rates, slow wagegrowth, and reluctance of banks to lend. The fiscalexpenditures required to fund financial sector bail-outs, combined with ongoing development and recur-ring expenditures, will put additional pressure ongovernment budgets throughout the subregion. Thecost of financing these expenditures will increasebudget deficits further, pushing up prices and interestrates. Unless handled prudently, these pressures coulddampen growth prospects for the Asian region, par-ticularly in the crisis-affected countries where bailoutsare the most costly.

It is worth noting that domestic demand and thestabilization of savings ratios are two sides of the same

coin. Where savings ratios fell in 1999, noticeably inIndonesia, Korea, Singapore, and probably Thailand,domestic demand rallied. However, during 2000, thestrength of that rally may moderate in these countries,unless asset markets continue their upward trend. Inthose countries where 1999 saw little or no saving ratedecline—Hong Kong, China; Malaysia; Philippines;and Taipei,China—domestic demand is likely to bebetter supported in 2000.

Another concern is the continued large exter-nal imbalance in the US. Some of the funding for theUS deficit has come from those seeking a safe havenduring the financial crisis. But with the restoration ofgrowth, these funds are beginning to return to Asiaand other countries. Convergence of growth betweenthe US and the euro area in the next few years mayhelp raise US exports to that area and cut the deficit.However, if US interest rates must be raised to sustainthe capital inflows required to service this debt, it willhave a depressing effect not only on the US economy,but also on the rest of the world. It would result inupward pressure on interest rates in Asia and threatenthe strength of the economic recovery.

Continued commitment to and speedy imple-mentation of structural reforms is necessary in thecrisis-affected countries in developing Asia. In mostof the crisis-affected countries, progress in establish-ing a modern legal and regulatory framework hasoccurred, but there is more to be accomplished. Pub-lic administration reforms are required to improve bu-reaucratic and corruption-prone administrativeprocedures. Corporate governance reforms for chang-ing ownership structure of large business groups andadoption of modern financial management techniquesremain a priority. The region still has an extensiveagenda for restructuring the banking and corporatesectors and making business transactions more trans-parent and accountable. Progress in implementingthese will ensure efficiency in resource allocation andhelp stimulate investment spending. (The next chap-ter of this Outlook addresses these topics in depth.)

In the case of the Central Asian republics andMongolia, risks are related to the success of policymeasures aimed at completing the transition to amarket-based economy and building the necessaryinstitutional structures. Higher energy and primarycommodity prices in 2000 and the emergence of a

ASIAN DEVELOPMENT OUTLOOK 200020

Box 1.3 A Crude Reminder: Will Oil End the Boom?