DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION TM Client-Driven Solutions, Insights, and Access Thursday, 06 February 2014 Asian Daily (Asia Edition) EPS, TP and Rating changes EPS TP (% change) T+1 T+2 Chg Up/Dn Rating Aristocrat Leisure 8 10 10 2 U (U) Downer EDI 0 (2) (2) 8 N (N) AIA Group (20) (10) 0 23 O (O) Bharat Heavy Electricals (6) (1) 0 (38) U (U) Cummins India (4) (5) (1) (15) N (N) Ranbaxy (61) (14) 6 7 N (N) Public Bank (9) (9) 13 4 N (N) Lotte Chemical (15) (1) 0 38 O (O) Kinsus Interconnect Tech 0 2 0 17 O (N) Connecting clients to corporates Singapore Seoul Semiconductor Co Ltd (046890.KQ) Date 17-18 February, Singapore Analyst Keon Han US China Mobile Games and Entertainment Group Limited (CMGE.O) Date 10-12 February, US Analyst Dick Wei Europe HDFC (HDBK.BO) Date 10-13 February, Europe Analyst Ashish Gupta Others PT Indoritel Makmur International Tbk (DNET.JK) Date 13 February, Kuala Lumpur Analyst Ella Nusantoro Contact [email protected] or Your usual sales representative. Top of the pack ... Global Equity Strategy Andrew Garthwaite (3) Equities: Hold your nerve! AIA Group (1299.HK) – Maintain O Arjan van Veen (4) New report: 4Q13 regional trends—Underlying momentum robust, valuation appeal returning Singapore Market Strategy Sanjay Mookim (5) Singapore underperforms the ASEAN markets YTD; the trend should reverse soon Malaysia Market Strategy Tan Ting Min (6) Malaysia: A hiding place? Indonesia Market Strategy Jahanzeb Naseer (7) Assessing the impact of a China slowdown CS pic of the day COSL forward P/E chart—recent market correction provides a good entry point for investors CS's China strategist Vincent Chan’s view is that the HK/China market will likely remain choppy in the near term as global growth concerns linger. That said, HK/China market valuation has been low for some time already, and many risk factors have been discounted, so the recent correction makes the valuation even cheaper. COSL is one of the names we highlight to buy and own after the correction. We believe COSL is one of the few names in HK/China that provide quality earnings growth and high earnings visibility. Source: Datastream, company data, Credit Suisse estimates. 5 7 9 11 13 15 17 2009 2010 2011 2012 2013 2014 +1 S.D. = 13.1x Avg. = 11.2x -1 S.D. = 9.3x (x) CS TP 12x ... and the whole pack Global Global Equity Strategy Andrew Garthwaite (3) Equities: Hold your nerve! Regional Asia Pacific Equity Strategy Sakthi Siva (8) New report: Foreign investor capitulation—any signs? Australia Aristocrat Leisure (ALL.AX) – Maintain U Larry Gandler (9) Looking for the break-out Downer EDI (DOW.AX) – Maintain N Emma Alcock (10) Delivering on cost-outs but markets still tough China China Market Strategy Vincent Chan (11) Bombed out stocks - dominated by Chinese banks and property

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION TM

Client-Driven Solutions, Insights, and Access

Thursday, 06 February 2014

Asian Daily (Asia Edition)

EPS, TP and Rating changes EPS TP

(% change) T+1 T+2 Chg Up/Dn Rating

Aristocrat Leisure 8 10 10 2 U (U) Downer EDI 0 (2) (2) 8 N (N) AIA Group (20) (10) 0 23 O (O) Bharat Heavy Electricals

(6) (1) 0 (38) U (U)

Cummins India (4) (5) (1) (15) N (N) Ranbaxy (61) (14) 6 7 N (N) Public Bank (9) (9) 13 4 N (N) Lotte Chemical (15) (1) 0 38 O (O) Kinsus Interconnect Tech 0 2 0 17 O (N)

Connecting clients to corporates

Singapore

Seoul Semiconductor Co Ltd (046890.KQ) Date 17-18 February, Singapore

Analyst Keon Han

US

China Mobile Games and Entertainment Group Limited (CMGE.O)

Date 10-12 February, US

Analyst Dick Wei

Europe

HDFC (HDBK.BO) Date 10-13 February, Europe

Analyst Ashish Gupta

Others

PT Indoritel Makmur International Tbk (DNET.JK) Date 13 February, Kuala Lumpur

Analyst Ella Nusantoro

Contact [email protected] or Your usual sales representative.

Top of the pack ...

Global Equity Strategy Andrew Garthwaite (3) Equities: Hold your nerve!

AIA Group (1299.HK) – Maintain O Arjan van Veen (4) New report: 4Q13 regional trends—Underlying momentum robust, valuation appeal returning

Singapore Market Strategy Sanjay Mookim (5) Singapore underperforms the ASEAN markets YTD; the trend should reverse soon

Malaysia Market Strategy Tan Ting Min (6) Malaysia: A hiding place?

Indonesia Market Strategy Jahanzeb Naseer (7) Assessing the impact of a China slowdown

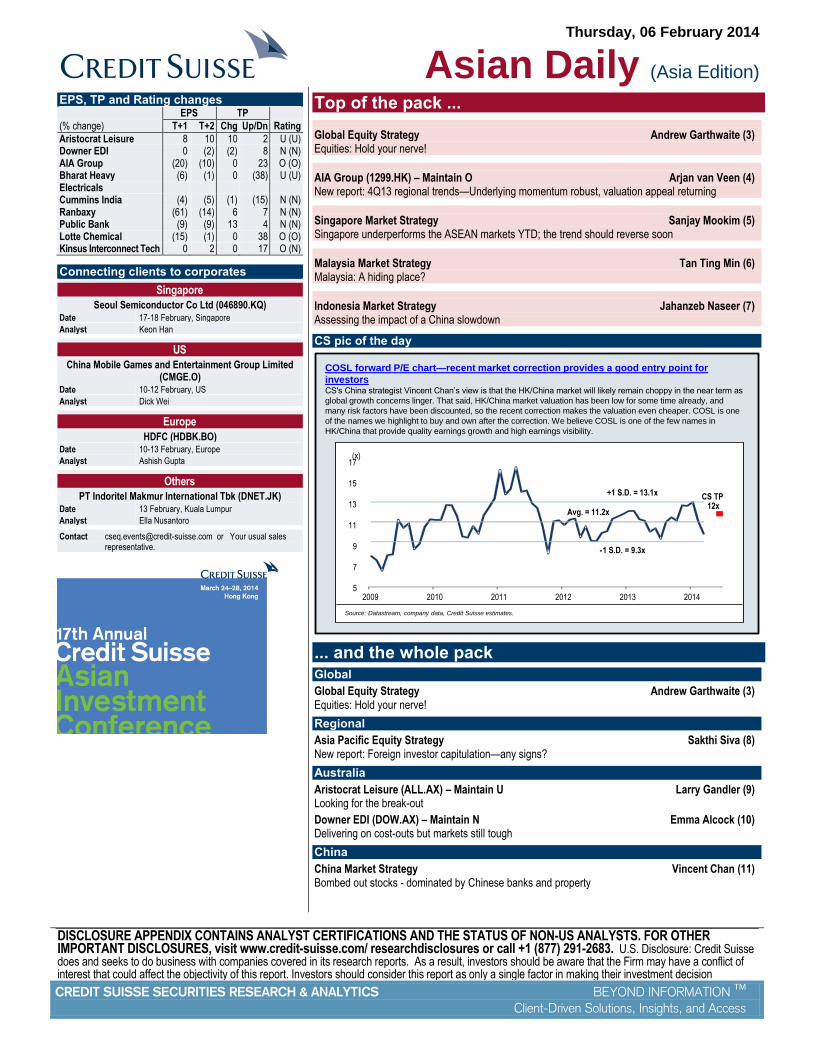

CS pic of the day

COSL forward P/E chart—recent market correction provides a good entry point for

investorsCS's China strategist Vincent Chan’s view is that the HK/China market will likely remain choppy in the near term as

global growth concerns linger. That said, HK/China market valuation has been low for some time already, and

many risk factors have been discounted, so the recent correction makes the valuation even cheaper. COSL is one

of the names we highlight to buy and own after the correction. We believe COSL is one of the few names in

HK/China that provide quality earnings growth and high earnings visibility.

Source: Datastream, company data, Credit Suisse estimates.

5

7

9

11

13

15

17

2009 2010 2011 2012 2013 2014

+1 S.D. = 13.1x

Avg. = 11.2x

-1 S.D. = 9.3x

(x)

CS TP12x

... and the whole pack Global

Global Equity Strategy Andrew Garthwaite (3) Equities: Hold your nerve!

Regional

Asia Pacific Equity Strategy Sakthi Siva (8) New report: Foreign investor capitulation—any signs?

Australia

Aristocrat Leisure (ALL.AX) – Maintain U Larry Gandler (9) Looking for the break-out

Downer EDI (DOW.AX) – Maintain N Emma Alcock (10) Delivering on cost-outs but markets still tough

China

China Market Strategy Vincent Chan (11) Bombed out stocks - dominated by Chinese banks and property

Thursday, 06 February 2014

Asian Daily

- 2 of 35 -

Asian indices – performance (% change) Latest 1D 1W 3M YTD

ASX300 5028 (0.5) (3.0) (6.6) (5.2) CSEALL 6176 (0.7) (0.7) 4.6 4.4 Hang Seng 21269 (0.6) (3.2) (7.7) (8.7) H-SHARE 9471 (0.4) (3.3) (10.3) (12.4) JCI 4384 0.7 1.0 (1.5) 2.6 KLSE 1786 0.4 0.3 (1.0) (4.3) KOSPI 1891 0.2 (1.0) (6.1) (6.0) KSE100 26751 (0.7) 0.4 17.4 5.9 NIFTY 6022 0.4 (1.6) (3.7) (4.5) NIKKEI 14180.4 1.2 (7.8) (1.1) (13.0) TOPIX 1162.6 2.1 (7.4) (2.5) (10.7) PCOMP 5908 0.4 (1.9) (8.8) 0.3 RED CHIP 4046 (0.1) (4.1) (10.3) (11.2) SET 1280 0.3 0.7 (10.8) (1.4) STI 2960 (0.2) (3.3) (7.6) (6.5) TWSE 8264 (2.3) (3.9) (0.2) (4.0) VNINDEX 557 (0.7) 0.5 12.1 10.3

Thomson Financial Datastream

Asian currencies (vs US$) (% change) Latest 1D 1W 3M YTD

A$ 1.1 (0.3) 1.5 (6.4) (0.2) Bt 32.8 0.0 0.7 (4.6) (0.1) D 21060.0 - - 0.2 0.2 JPY 101.4 0.2 1.3 (2.7) 3.8 NT$ 30.3 (0.1) 0.0 (2.9) (1.7) P 45.3 (0.2) (0.2) (4.7) (2.1) PRs 105.5 (0.2) (0.1) 1.8 (0.1) Rp 12194.0 (0.3) (0.2) (6.9) (0.2) Rs 62.6 (0.1) (0.3) (1.5) (1.2) S$ 1.3 (0.0) 0.6 (2.0) (0.4) SLRs 130.7 - 0.1 0.4 0.1 W 1077.9 (0.1) (0.7) (1.6) (2.6)

Thomson Financial Datastream

Global indices (% change) Latest 1D 1W 3M YTD

DJIA 15452.8 0.0 (1.8) (1.1) (6.8) S&P 500 1750.7 (0.3) (1.3) (0.7) (5.3) NASDAQ 4016.9 (0.4) (0.9) 2.0 (3.8) SOX 518.6 0.0 (1.2) 3.1 (3.1) EU-STOX 2801.8 0.1 (1.6) (2.6) (4.0) FTSE 6457.9 0.1 (1.3) (4.3) (4.3) DAX 9116.3 (0.1) (2.4) 1.2 (4.6) CAC-40 4117.8 0.0 (0.9) (3.2) (4.1) 10 YR LB 2.7 1.2 (0.5) (0.3) (12.1) 2 YR LB 0.3 (1.3) (12.4) 2.1 (19.0) US$:E 1.4 0.0 (0.1) 0.1 (1.8) US$:Y 101.4 (0.0) 1.3 (2.7) 3.8 BRENT 106.2 0.2 (2.1) 1.0 (4.2) GOLD 1257.4 0.2 (0.8) (4.1) 4.3 VIX 19.6 2.6 13.0 47.7 42.9

Thomson Financial Datastream

MSCI Asian indices – valuation & perf. EPS grth. P/E (x) Performance

MSCI Index 13E 14E 13E 14E 1D 1M YTD

Asia F X Japan 18 12 11.0 9.8 0.0 -5.1 (7.3)

Asia Pac F X J. 14 12 11.5 10.3 0.0 -5.2 (6.8)

Australia (2) 10 15.5 14.1 (0.3) -5.9 (5.6)

China 11 10 8.9 8.1 (0.2) -8.0 (10.2)

Hong Kong 11 11 14.9 13.5 (1.2) -7.0 (8.3)

India 15 16 14.1 12.3 0.6 -3.5 (5.0)

Indonesia 17 16 13.5 11.6 1.1 3.5 3.3

Japan 34 50 23.2 15.4 (4.6) (12.7) (12.7)

Korea 33 13 8.4 7.3 0.9 -5.5 (9.1)

Malaysia 1 10 16.0 14.6 0.7 -4.0 (5.9)

Pakistan 14 18 9.6 8.1 0.00 -1.6 1.2

Philippines 8 13 17.8 16.5 0.5 -2.4 (2.1)

Singapore 2 9 13.2 12.1 (0.1) -6.2 (7.8)

Sri Lanka 16 11 14.8 13.3 (2.1) 1.6 2.2

Taiwan 33 12 15.0 13.4 (3.2) -4.7 (6.4)

Thailand 19 13 10.8 9.6 0.4 5.5 (1.3) * IBES estimates

China Market Strategy Vincent Chan (12) HOLT analysis on our top picks in these times of uncertainty

Shenzhou International (2313.HK) – Maintain O Eva Wang (13) Time to accumulate after recent market correction

Hong Kong

Macau Gaming Sector Kenny Lau, CFA (14) Continuation of VIP business slowdown drags January GGR growth to 7%

AIA Group (1299.HK) – Maintain O Arjan van Veen (4) New report: 4Q13 regional trends—Underlying momentum robust, valuation appeal returning

India

India Market Strategy Neelkanth Mishra (15) Can the cost-push rise in milk prices offset the decline in vegetable inflation?

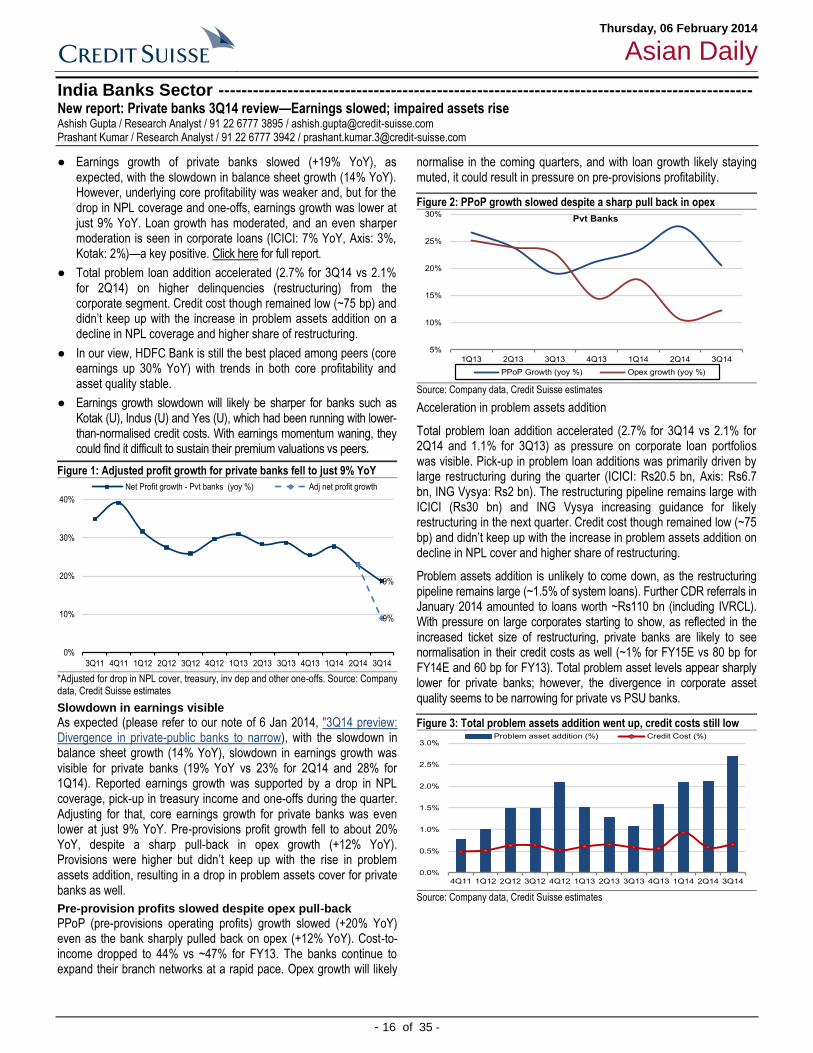

India Banks Sector Ashish Gupta (16) New report: Private banks 3Q14 review—Earnings slowed; impaired assets rise

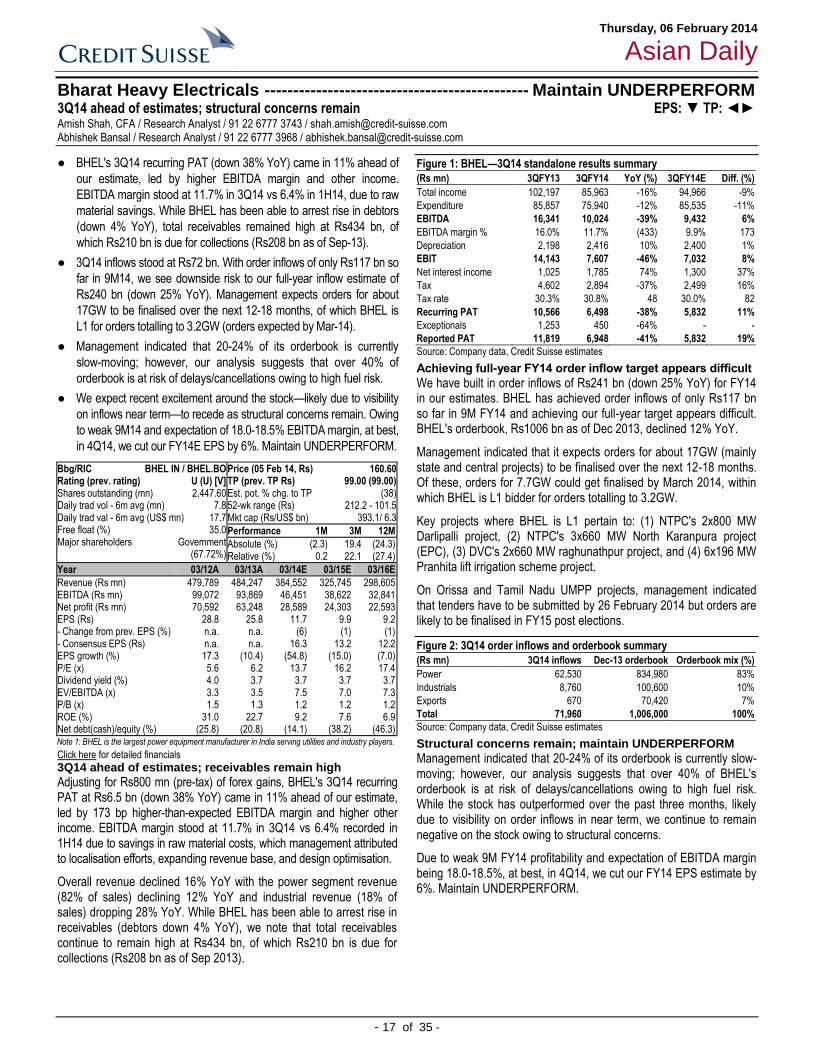

Bharat Heavy Electricals (BHEL.BO) – Maintain U Amish Shah, CFA (17) 3Q14 ahead of estimates; structural concerns remain

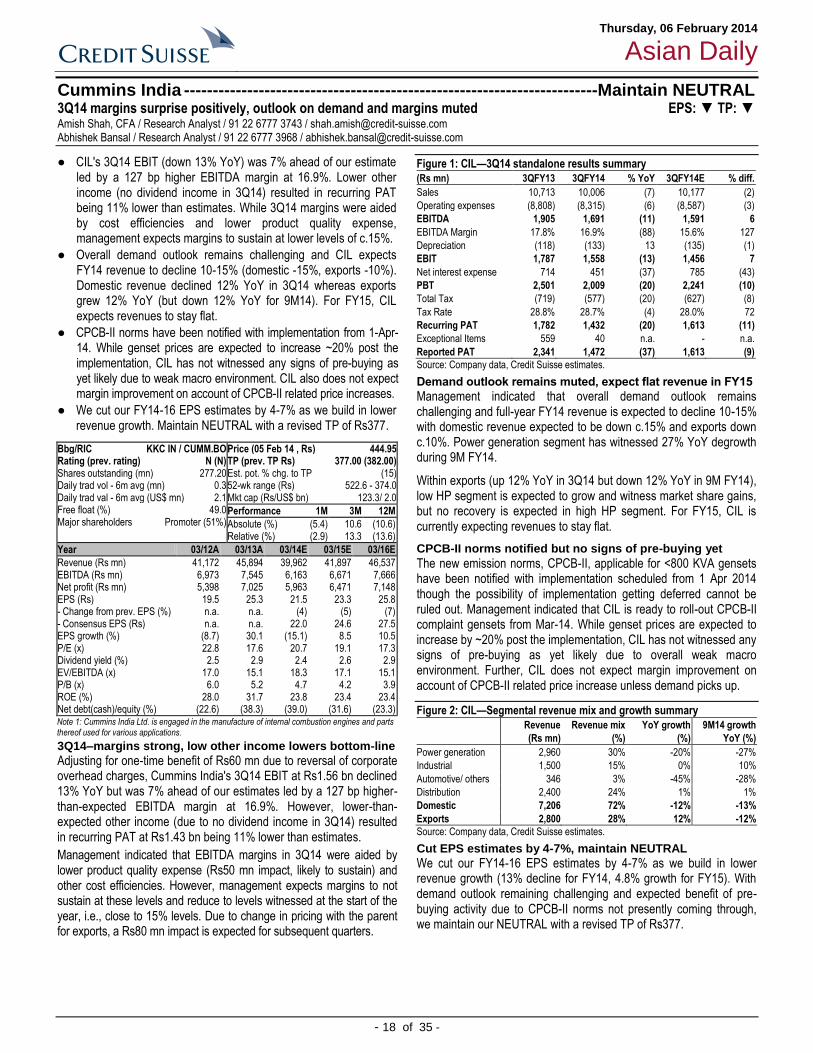

Cummins India (CUMM.BO) – Maintain N Amish Shah, CFA (18) 3Q14 margins surprise positively, outlook on demand and margins muted

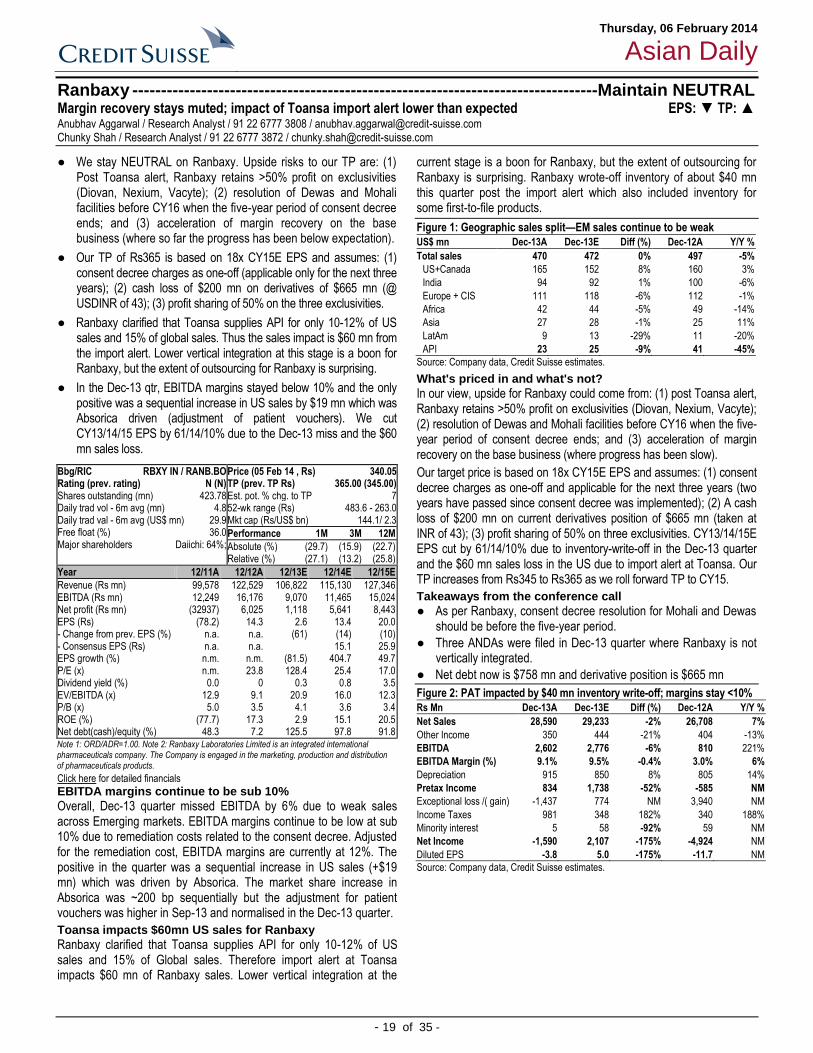

Ranbaxy (RANB.BO) – Maintain N Anubhav Aggarwal (19) Margin recovery stays muted; impact of Toansa import alert lower than expected

Indonesia

Indonesia Economics Robert Prior-Wandesforde (20) 4Q13 GDP: Stronger, not weaker

Indonesia Market Strategy Jahanzeb Naseer (7) Assessing the impact of a China slowdown

Indonesia Retail Sector – Maintain UW Priscilla Tjitra (21) New report: Retail regulations uncovered

Japan

Mitsubishi Gas Chemical (4182.T) – Maintain O Masami Sawato (22) Write-off at Shanghai polycarbonate plant could reduce ¥4 bn loss

Malaysia

Malaysia Market Strategy Tan Ting Min (6) Malaysia: A hiding place?

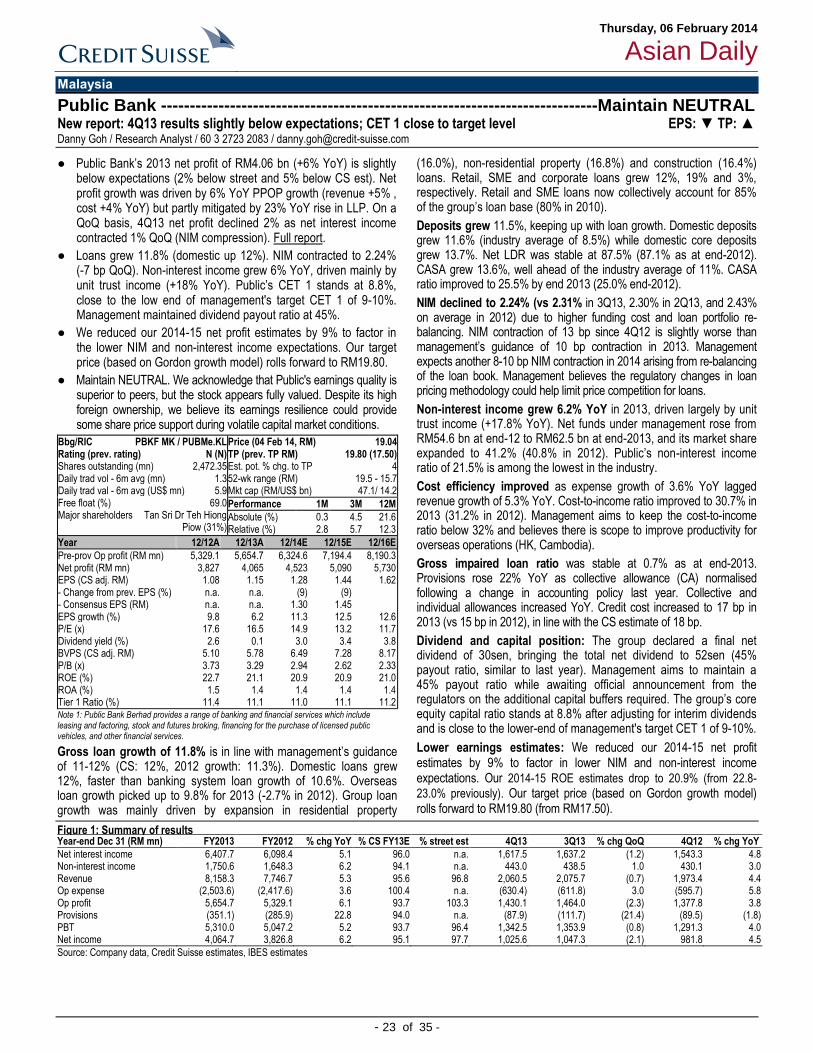

Public Bank (PUBMe.KL) – Maintain N Danny Goh (23) New report: 4Q13 results slightly below expectations; CET 1 close to target level

Pakistan

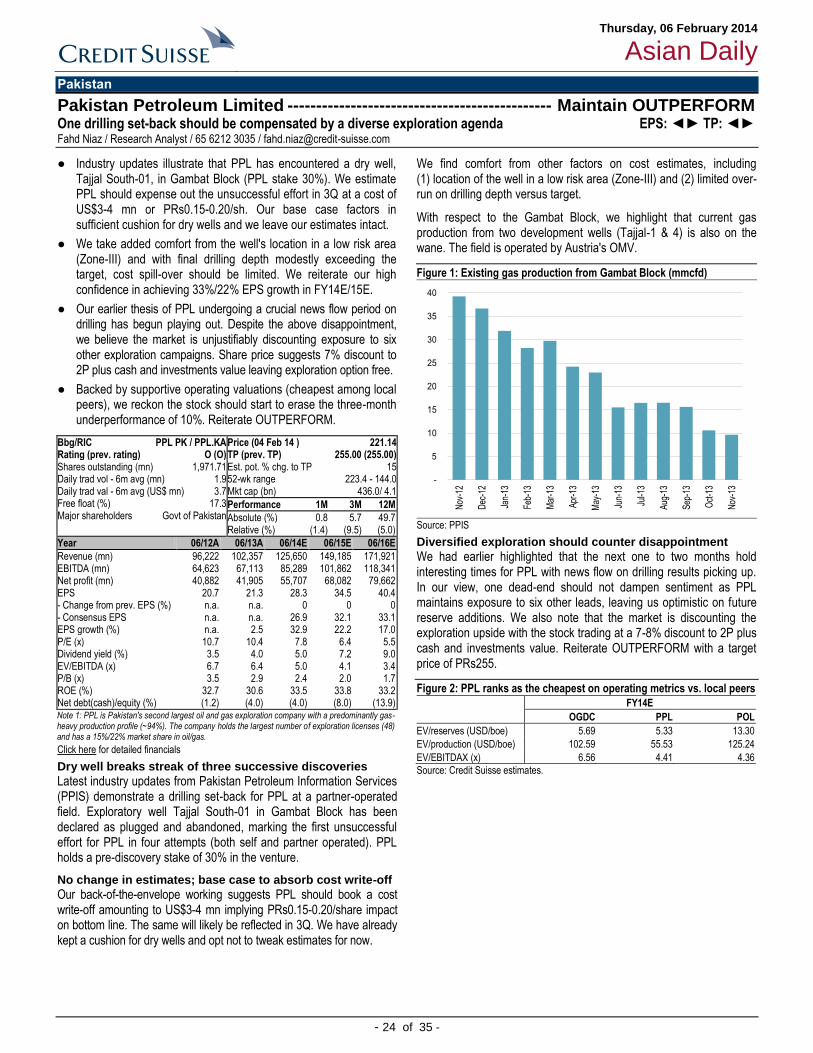

Pakistan Petroleum Limited (PPL.KA) – Maintain O Fahd Niaz (24) One drilling set-back should be compensated by a diverse exploration agenda

Philippines

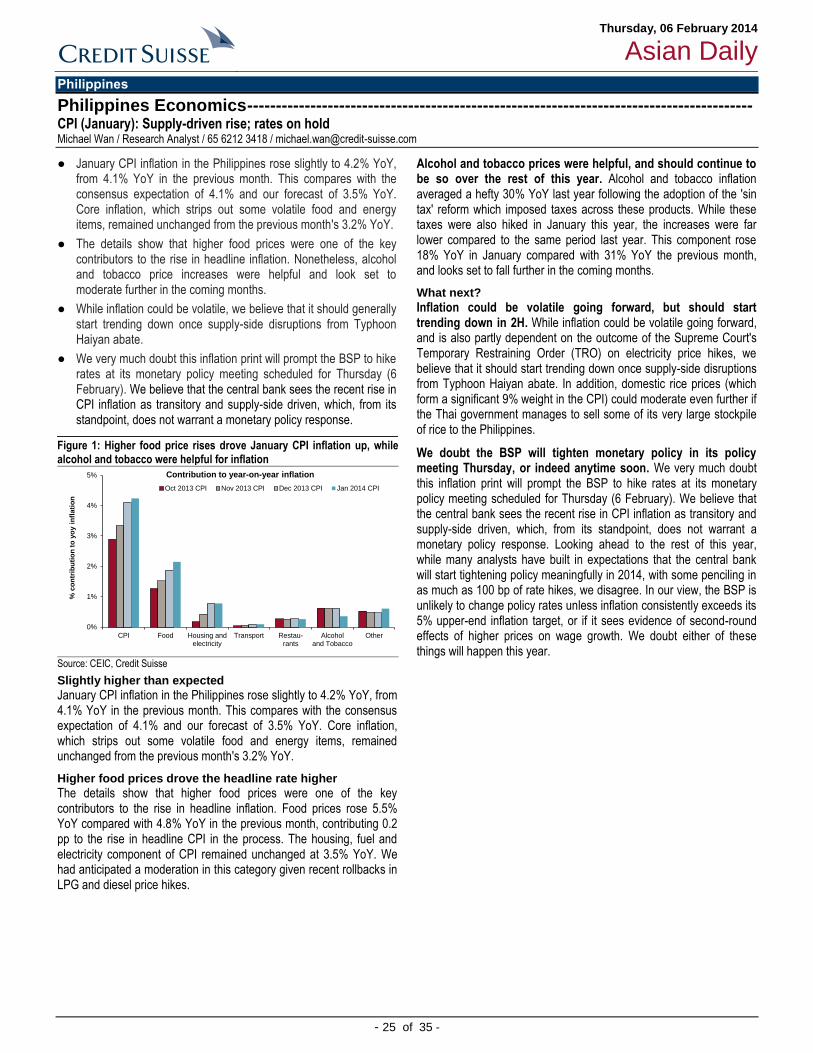

Philippines Economics Michael Wan (25) CPI (January): Supply-driven rise; rates on hold

Singapore

Singapore Market Strategy Sanjay Mookim (5) Singapore underperforms the ASEAN markets YTD; the trend should reverse soon

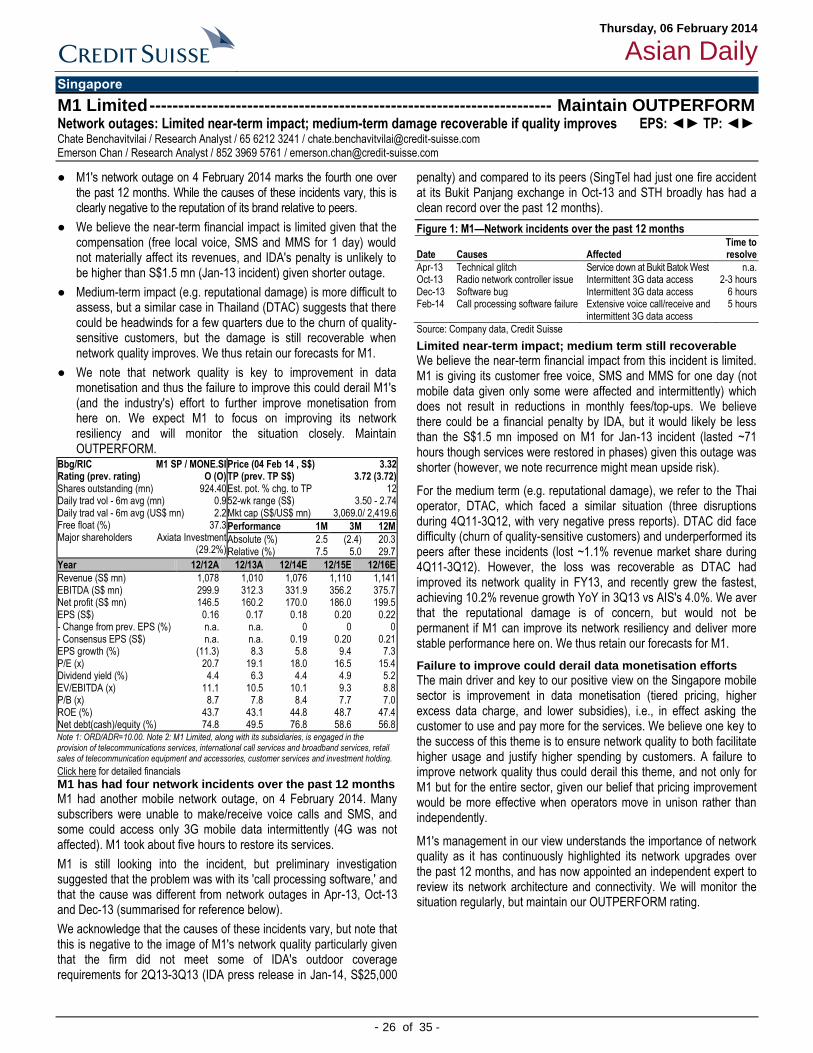

M1 Limited (MONE.SI) – Maintain O Chate Benchavitvilai (26) Network outages: Limited near-term impact; medium-term damage recoverable if quality improves

South Korea

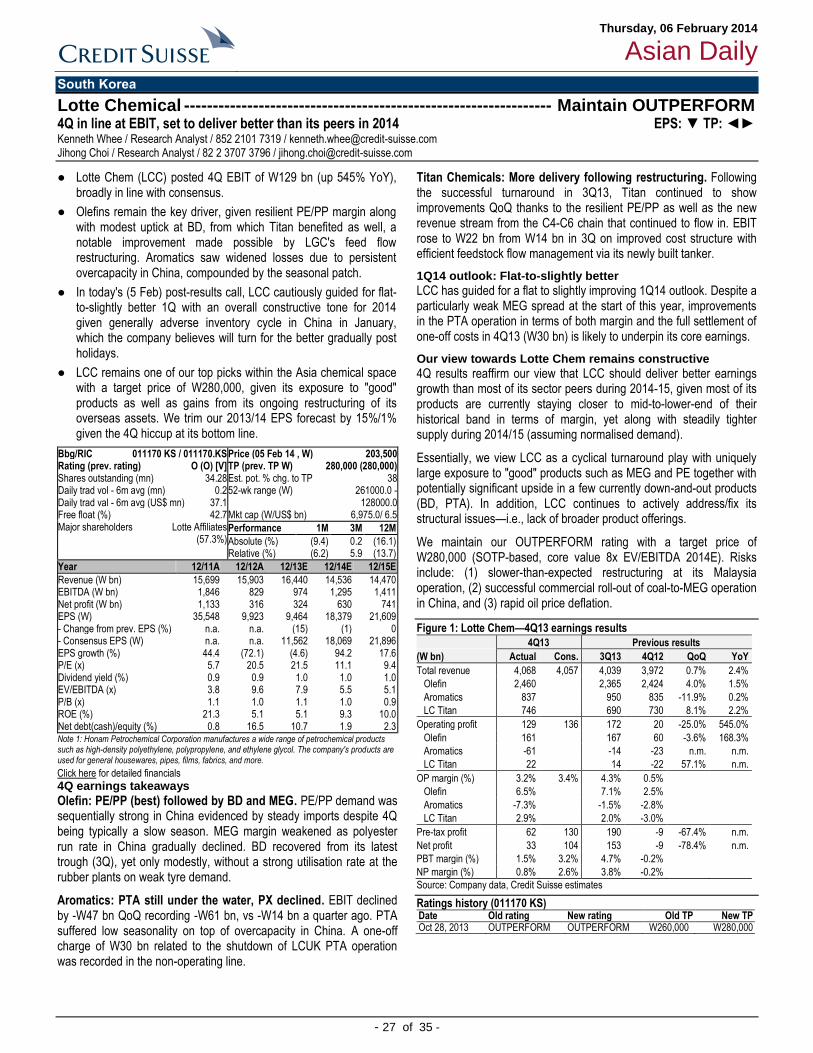

Lotte Chemical (011170.KS) – Maintain O Kenneth Whee (27) 4Q in line at EBIT, set to deliver better than its peers in 2014

Taiwan

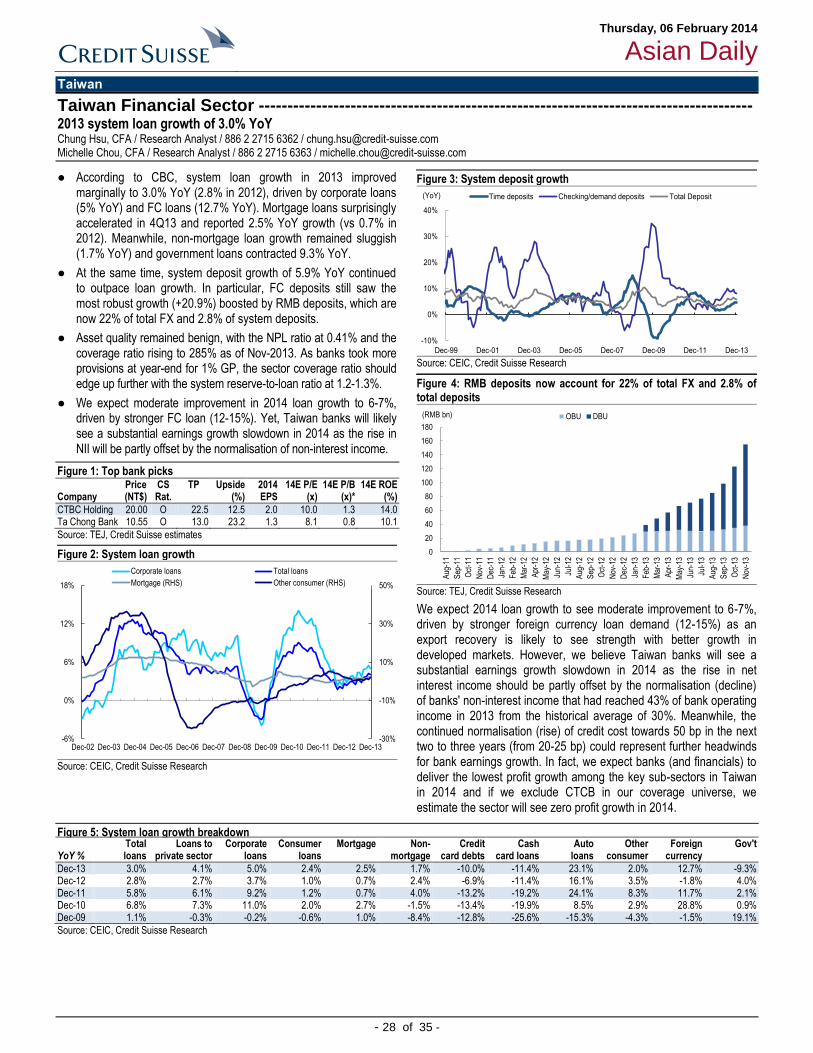

Taiwan Financial Sector Chung Hsu, CFA (28) 2013 system loan growth of 3.0% YoY

Kinsus Interconnect Tech (3189.TW) – Upgrade to O Pauline Chen (29) 4Q13 miss on higher opex, but we expect 2014 ROE to reach to post-2009 high

O=Outperform N=Neutral U=Underperform R=Restricted OW= Overweight MW=Market Weight UW=Underweight

Research mailing options To make any changes to your existing research mailing details, please e-mail us directly at [email protected]

Sales Contact Hong Kong 852 2101 7211 Singapore 65 6212 3052 London 44 20 7888 4367 New York 1 212 325 5955 Boston 1 617 556 5634

Thursday, 06 February 2014

Asian Daily

- 3 of 35 -

Top of the pack ...

Global Equity Strategy ---------------------------------------------------------------------------------------- Equities: Hold your nerve! Andrew Garthwaite / Research Analyst / 44 20 7883 6477 / [email protected]

● Markets have been hit by three headwinds. We believe each is manageable for now. Consequently, we stick to our end-2014 S&P 500 target of 1,960 and overweight equities:

● GEM growth: US export growth to emerging markets has already slowed to 3%, as GEM consumption growth has halved over the past three years. We estimate that 3.5% off exports to EM would take 0.2% off nominal US GDP. Chinese GDP growth would have to be sub-5% or the RMB weaken by 10% for us to alter our positive stance on equities.

● January's US ISM survey was weak, but PMI new orders in Europe and Japan (the regions most exposed to GEM) hit new cycle highs. Consequently, global PMI new orders (on Markit data) were flat in January and continue to point to 3¾%- 4% global GDP growth, compared to the current run-rate of 3%.

● Concerns about the debt ceiling: but Congress appears more bi-partisan. Click here for full report.

Figure 1: Just 24% of NYSE stocks trade above ten-week moving average

Source: NYSE, Thomson Reuters, Credit Suisse research

Other reasons to stay bullish

Valuations: The equity risk premium is 5.5% on our EPS assumptions, still above our estimate of the warranted ERP of 4.7%, while many factors point to an even lower ERP of 4% (cf to a post 1900 average of 3.2%). Excess liquidity growth, at 5%, is consistent with a re-rating of equities.

Positioning: There have been US$100 bn of outflows from global equity funds since 2008, while combined corporate and private equity fire-power stands at US$3.4 tn. Earnings revisions are picking up modestly (and we revise our 2014E US EPS growth to 8.5% from 7.1%); we continue to believe profit margins don’t peak until 2016. Typically a big macro shock or very stretched valuation is required for the S&P to correct by 10%+, and we see no such trigger. Tactical indicators are broadly neutral.

The scope for further monetary easing: Our economists forecast inflation in Japan of 0.7% for 2014 and 0.8% 2015 (vs BoJ target of 2%) and Euro-area inflation of 0.4% in April. Hence, we expect more QE by the BoJ and the ECB to become more aggressive.

Global growth could still match 2013 on conservative assumptions

Even if we assume some pretty pessimistic GDP growth rates, global GDP growth would still end up at 2.8%—only slightly below the 2013 growth rate (Chinese GDP growth of 6% (down from 7.7% last year and compared to a consensus forecast of 7.4% and a CS forecast of 7.3%), Indian growth at 5.4% (i.e., same as 2013, CS is 6.6%) and Brazil at 2.4% (i.e., same as 2013, CS is 3.0%)—with US growth of only 2%, Euro-area growth of only 0.5% and the UK and Japan growing at 1%).

Figure 2: Even if China grows only at 6% and the US at 2%, global growth should still end up at 2.8% this year

Source: Thomson Reuters, Credit Suisse research

If TIPs yield were to fall because of more QE, then the GEM currencies could finance their current account deficits, again!

If we are wrong and emerging market weakness translates into a slowdown in developed market growth, we think the Fed would react to the renewed growth slowdown with a delay in its tapering program, while the ECB and the BoJ would likely introduce further easing measures. Inflation in Japan is, we believe, likely to stay around 0.7%, well below the BoJ target of 2%; European inflation will, according to our European economists, fall to 0.4%. If there were more QE, then real bond yields would fall, and thus, as below, it would be easier to finance current account deficits.

This is an extract from the Global Equity Strategy report published on 5 February 2014. Please see CS's R&A website for more details.

Thursday, 06 February 2014

Asian Daily

- 4 of 35 -

AIA Group ---------------------------------------------------------------------- Maintain OUTPERFORM New report: 4Q13 regional trends—Underlying momentum robust, valuation appeal returning EPS: ▼ TP: ◄► Arjan van Veen / Research Analyst / 852 2101 7508 / [email protected] Frances Feng / Research Analyst / 852 2101 6693 / [email protected]

● We have reviewed the latest industry data and peer results, which highlight the ongoing strength in key markets (Figure 1), in particular, growth acceleration in HK and Singapore. Weaker areas are Korea, Thailand (political) and Australia (group profitability).

● AIA continues to have some growth 'optionality' through M&A given its strong balance sheet, as highlighted by the recent Citibank regional distribution deal. Management continues to execute well on its key strategies of margin enhancement and agent productivity, with room for progress in the medium term.

● Catalyst: Full year 2013 results on 21 February 2014.

● However, we have downgraded our 2013-15 forecasts by 2-20% following marking to market its earnings due to movements in regional equity markets and currencies over the last few months. Our valuation is unchanged at HK$44.00, with currency movements offset by roll-forward. We maintain our OUTPERFORM investment rating and see current valuations as a good entry point for the stock, noting it rarely trades at these levels. Click here for full report.

4Q13 / 1Q14 mark to market: Currency mayhem

We have downgraded our 2013-15 forecasts by 2-20% following marking to market its earnings due to movements in currencies (-4%) over the last few months as well as weaker equity markets (-7%).

On the positive side, we highlight that the ~80 bp improvement in bond yields in 2013 to date has reversed most of the cumulative reduction in average bond yields since listing.

Growth in core markets strong

Following a review of peer results and industry data, we see near-term growth as robust in the region, with main markets (such as Hong Kong and Singapore) showing strong improvement.

On the less positive side, Korean growth has stalled more recently and is likely to remain so given the current (industry-wide) telemarketing ban. Thailand will likely be impacted by current political uncertainty, whilst Australian group risk profit is likely to be a medium-term issue.

Strong balance sheet provides flexibility

AIA’s solvency position looks very strong, with excess capital (above the minimum 150% solvency) totalling US$4.9 bn including the US$1 bn of debt, with further gearing capacity as at 31 May 2013.

AIA generated a free surplus of US$1.9 bn in 1H13, while the new business strain was US$0.7 bn, highlighting its capital generation capacity. As its ‘new generation’ investment-linked products are rolled out, this should reduce the new business strain further.

As such, coupled with plenty of debt capacity, we believe AIA is in a strong position to take advantage of any further M&A opportunities to drive growth, with the recent ING Malaysia acquisition and regional Citibank deal as key examples of this.

Valuation appeal returning in the recent pull-back

Given recent share price weakness, we see some valuation appeal returning to the stock at these levels. Specifically, AIA is now trading on the following multiples (12-month forward): (a) 11x implied value of new business multiple; (b) 16x price to earnings, relative to 17% growth in operating profit in 1H13; and (c) 2.0x price to book (relative to 12% return on equity—which would be 14-15% through use of its excess capital).

Figure 1: AIA mix (%) and NB APE growth (% p.a.) by market / market NB APE growth (% p.a.) AIA % of group 1H13 AIA ANP growth AIA VNB growth Market growth

1H13 1H13 1H13 2012 2H12 1H13 2012 2H12 1H13 10yr 2012 1Q13 2Q13 3Q13 4Q13

ANP VNB VNB ANP ANP ANP VNB VNB VNB CAGR

% US$mn % % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a. % p.a.

Hong Kong 21% 168 24% 16% 21% 34% 20% 23% 20% 16% 5% 14% 21% 21%

Singapore 10% 110 15% 28% 30% -3% 9% 48% 11% 9% 11% 12% 37% 27%

Thailand 17% 146 21% 14% 19% 9% 12% 24% 11% 13% 23% 36% -23% 11%

Malaysia 10% 54 8% 6% 0% 100% 11% 3% 74% 10% 7% na na na na

China 8% 76 11% 0% 1% 11% 22% 10% 27% 20% -6% na 3% na

Korea 12% 45 6% -12% 10% 75% 4% 9% 36% 16% -4% 63% 18% 1% -8%

Other markets 22% 112 16% 4% -8% 29% 41% 41% 70%

AIA Group 711 9% 10% 29% 27% 27% 26% 9% 37% 21% 21%

- excl Group Risk one-off 14% 10% 29% 17% 34% 26% Source: Company data, Credit Suisse estimates

Please click here for the full 29pp report.

Bbg/RIC 1299 HK / 1299.HK Rating (prev. rating) O (O) Shares outstanding (mn) 12,044 Daily trad vol - 6m avg (mn) 22.7 Daily trad val - 6m avg (US$ mn) 109.1 Free float (%) 100.0 Major shareholders Capital 8.6%,

Blackrock 6%

Price (05 Feb 14, HK$) 35.65 TP (prev. TP HK$) 44.00 (44.00) Est. pot. % chg. to TP 23 52-wk range (HK$) 40.1 - 30.1 Mkt cap (HK$/US$ bn) 429.4/ 55.3

Performance 1M 3M 12M

Absolute (%) (6.4) (7.2) 18.6 Relative (%) (0.2) (0.1) 26.8

Year 11/11A 11/12A 11/13E 11/14E 11/15E

Life GWP (US$ bn) 12.4 13.2 14.7 15.7 17.5 P&C GWP (US$ bn) — — — — — Net profit (US$ bn) 1.6 3.0 2.9 3.1 3.8 EPS (US$) 0.13 0.25 0.24 0.26 0.32 - Change from prev. EPS (%) n.a. n.a. (20) (10) (2) - Consensus EPS (US$) n.a. n.a. 0.25 0.29 0.32 EPS growth (%) (40.8) 88.8 (4.2) 7.3 22.5 P/E (x) 34.6 18.3 19.1 17.8 14.5 NTA per share (US$) 1.75 2.19 2.00 2.28 2.53 EV per share (US$) 2.26 2.61 2.75 3.05 3.40 Dividend yield (%) 0.9 1.0 1.2 1.4 1.5 EV/EBITDA (x) 22.1 20.9 19.0 16.2 13.4 P/B (x) 2.6 2.1 2.2 1.9 1.7 ROE (%) 7.8 12.6 11.1 11.5 12.6 P&C combined ratio (%) — — — — —

Note 1: ORD/ADR=4.00. Note 2: AIA Group Limited is an investment holding company. The company and its subsidiaries are engaged in provision of products and services to individuals and businesses for their insurance, protection, savings, investment and retirement needs.

Thursday, 06 February 2014

Asian Daily

- 5 of 35 -

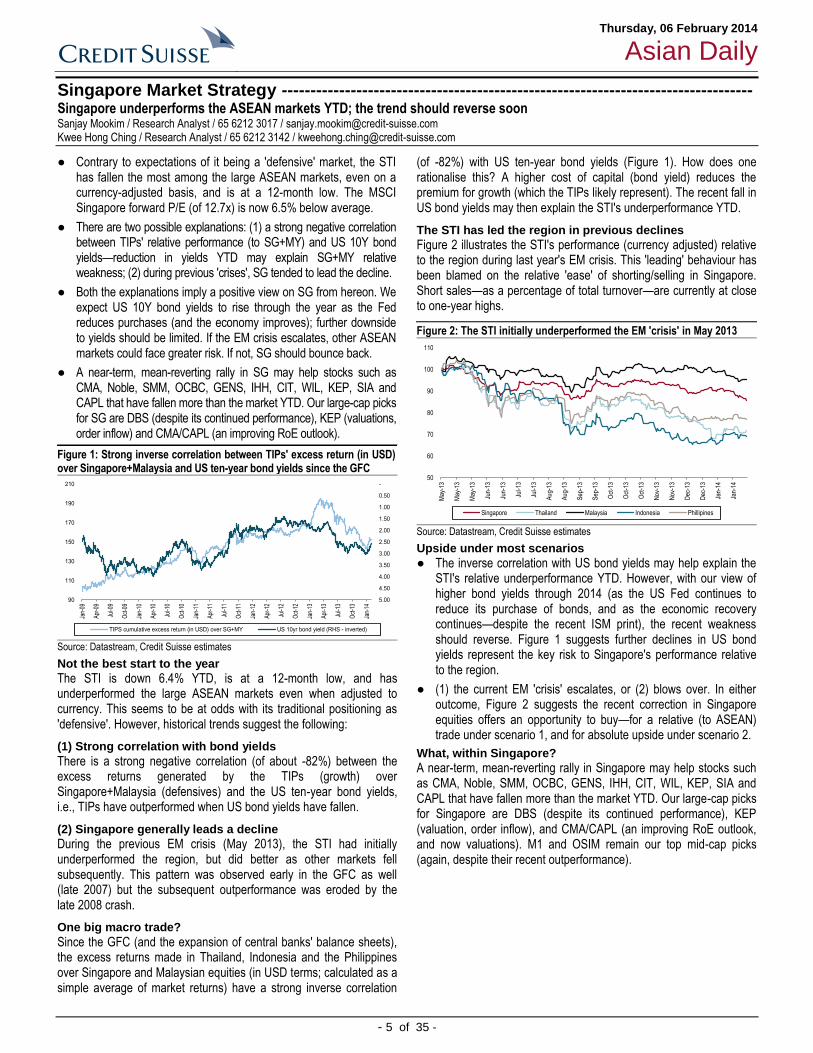

Singapore Market Strategy ---------------------------------------------------------------------------------- Singapore underperforms the ASEAN markets YTD; the trend should reverse soon Sanjay Mookim / Research Analyst / 65 6212 3017 / [email protected] Kwee Hong Ching / Research Analyst / 65 6212 3142 / [email protected]

● Contrary to expectations of it being a 'defensive' market, the STI has fallen the most among the large ASEAN markets, even on a currency-adjusted basis, and is at a 12-month low. The MSCI Singapore forward P/E (of 12.7x) is now 6.5% below average.

● There are two possible explanations: (1) a strong negative correlation between TIPs' relative performance (to SG+MY) and US 10Y bond yields—reduction in yields YTD may explain SG+MY relative weakness; (2) during previous 'crises', SG tended to lead the decline.

● Both the explanations imply a positive view on SG from hereon. We expect US 10Y bond yields to rise through the year as the Fed reduces purchases (and the economy improves); further downside to yields should be limited. If the EM crisis escalates, other ASEAN markets could face greater risk. If not, SG should bounce back.

● A near-term, mean-reverting rally in SG may help stocks such as CMA, Noble, SMM, OCBC, GENS, IHH, CIT, WIL, KEP, SIA and CAPL that have fallen more than the market YTD. Our large-cap picks for SG are DBS (despite its continued performance), KEP (valuations, order inflow) and CMA/CAPL (an improving RoE outlook).

Figure 1: Strong inverse correlation between TIPs' excess return (in USD) over Singapore+Malaysia and US ten-year bond yields since the GFC

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00 90

110

130

150

170

190

210

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

TIPS cumulative excess return (in USD) over SG+MY US 10yr bond yield (RHS - inverted)

Source: Datastream, Credit Suisse estimates

Not the best start to the year

The STI is down 6.4% YTD, is at a 12-month low, and has underperformed the large ASEAN markets even when adjusted to currency. This seems to be at odds with its traditional positioning as 'defensive'. However, historical trends suggest the following:

(1) Strong correlation with bond yields

There is a strong negative correlation (of about -82%) between the excess returns generated by the TIPs (growth) over Singapore+Malaysia (defensives) and the US ten-year bond yields, i.e., TIPs have outperformed when US bond yields have fallen.

(2) Singapore generally leads a decline

During the previous EM crisis (May 2013), the STI had initially underperformed the region, but did better as other markets fell subsequently. This pattern was observed early in the GFC as well (late 2007) but the subsequent outperformance was eroded by the late 2008 crash.

One big macro trade?

Since the GFC (and the expansion of central banks' balance sheets), the excess returns made in Thailand, Indonesia and the Philippines over Singapore and Malaysian equities (in USD terms; calculated as a simple average of market returns) have a strong inverse correlation

(of -82%) with US ten-year bond yields (Figure 1). How does one rationalise this? A higher cost of capital (bond yield) reduces the premium for growth (which the TIPs likely represent). The recent fall in US bond yields may then explain the STI's underperformance YTD.

The STI has led the region in previous declines

Figure 2 illustrates the STI's performance (currency adjusted) relative to the region during last year's EM crisis. This 'leading' behaviour has been blamed on the relative 'ease' of shorting/selling in Singapore. Short sales—as a percentage of total turnover—are currently at close to one-year highs.

Figure 2: The STI initially underperformed the EM 'crisis' in May 2013

50

60

70

80

90

100

110

May

-13

May

-13

May

-13

Jun-

13

Jun-

13

Jul-1

3

Jul-1

3

Aug

-13

Aug

-13

Sep

-13

Sep

-13

Oct

-13

Oct

-13

Oct

-13

Nov

-13

Nov

-13

Dec

-13

Dec

-13

Jan-

14

Jan-

14

Singapore Thailand Malaysia Indonesia Phillipines

Source: Datastream, Credit Suisse estimates

Upside under most scenarios

● The inverse correlation with US bond yields may help explain the STI's relative underperformance YTD. However, with our view of higher bond yields through 2014 (as the US Fed continues to reduce its purchase of bonds, and as the economic recovery continues—despite the recent ISM print), the recent weakness should reverse. Figure 1 suggests further declines in US bond yields represent the key risk to Singapore's performance relative to the region.

● (1) the current EM 'crisis' escalates, or (2) blows over. In either outcome, Figure 2 suggests the recent correction in Singapore equities offers an opportunity to buy—for a relative (to ASEAN) trade under scenario 1, and for absolute upside under scenario 2.

What, within Singapore?

A near-term, mean-reverting rally in Singapore may help stocks such as CMA, Noble, SMM, OCBC, GENS, IHH, CIT, WIL, KEP, SIA and CAPL that have fallen more than the market YTD. Our large-cap picks for Singapore are DBS (despite its continued performance), KEP (valuation, order inflow), and CMA/CAPL (an improving RoE outlook, and now valuations). M1 and OSIM remain our top mid-cap picks (again, despite their recent outperformance).

Thursday, 06 February 2014

Asian Daily

- 6 of 35 -

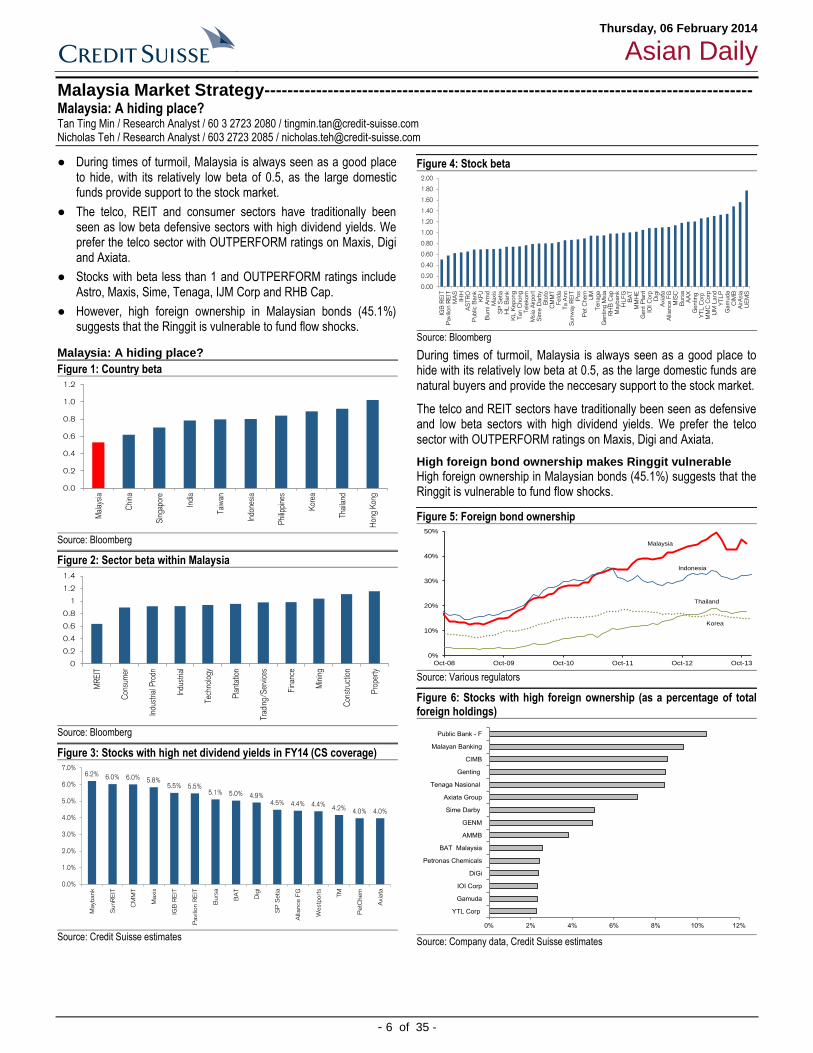

Malaysia Market Strategy ------------------------------------------------------------------------------------- Malaysia: A hiding place? Tan Ting Min / Research Analyst / 60 3 2723 2080 / [email protected] Nicholas Teh / Research Analyst / 603 2723 2085 / [email protected]

● During times of turmoil, Malaysia is always seen as a good place to hide, with its relatively low beta of 0.5, as the large domestic funds provide support to the stock market.

● The telco, REIT and consumer sectors have traditionally been seen as low beta defensive sectors with high dividend yields. We prefer the telco sector with OUTPERFORM ratings on Maxis, Digi and Axiata.

● Stocks with beta less than 1 and OUTPERFORM ratings include Astro, Maxis, Sime, Tenaga, IJM Corp and RHB Cap.

● However, high foreign ownership in Malaysian bonds (45.1%) suggests that the Ringgit is vulnerable to fund flow shocks.

Malaysia: A hiding place?

Figure 1: Country beta

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Mal

aysi

a

Chi

na

Sin

gapo

re

Indi

a

Taiw

an

Indo

nesi

a

Phi

lippi

nes

Kor

ea

Thai

land

Hon

g K

ong

Source: Bloomberg

Figure 2: Sector beta within Malaysia

0

0.2

0.4

0.6

0.8

1

1.2

1.4

MR

EIT

Con

sum

er

Indu

stria

l Pro

dn

Indu

stria

l

Tech

nolo

gy

Pla

ntat

ion

Trad

ing/

Ser

vice

s

Fin

ance

Min

ing

Con

stru

ctio

n

Pro

pert

y

Source: Bloomberg

Figure 3: Stocks with high net dividend yields in FY14 (CS coverage)

6.2% 6.0% 6.0% 5.8%5.5% 5.5%

5.1% 5.0% 4.9%4.5% 4.4% 4.4%

4.2% 4.0% 4.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Mayb

ank

SunR

EIT

CM

MT

Maxi

s

IGB

RE

IT

Pavi

lion R

EIT

Burs

a

BA

T

Dig

i

SP

Setia

Alliance F

G

Westp

ort

s

TM

PetC

hem

Axi

ata

Source: Credit Suisse estimates

Figure 4: Stock beta

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

IGB

RE

ITP

avi

lion R

EIT

MA

SIH

HA

STR

OP

ublic

Bank

KP

JB

um

i A

rmd

Maxi

sS

P S

etia

HL

Bank

KL K

epong

Tan C

hong

Tele

kom

Msi

a A

irport

Sim

e D

arb

yB

toto

CM

MT

Feld

aTa A

nn

Sunw

ay

RE

ITP

os

Pet

Chem

IJM

Tenaga

Genting M

sia

RH

B C

ap

Mayb

ank

HL

FG

BA

TM

MH

EG

ent

Pla

nt

IOI C

orp

Dig

iA

xiata

Alliance F

GM

ISC

Burs

aA

AX

Genting

YTL C

orp

MM

C C

orp

IJM

Land

YTLP

Gam

uda

CIM

BA

irA

sia

UE

MS

Source: Bloomberg

During times of turmoil, Malaysia is always seen as a good place to hide with its relatively low beta at 0.5, as the large domestic funds are natural buyers and provide the neccesary support to the stock market.

The telco and REIT sectors have traditionally been seen as defensive and low beta sectors with high dividend yields. We prefer the telco sector with OUTPERFORM ratings on Maxis, Digi and Axiata.

High foreign bond ownership makes Ringgit vulnerable

High foreign ownership in Malaysian bonds (45.1%) suggests that the Ringgit is vulnerable to fund flow shocks.

Figure 5: Foreign bond ownership

0%

10%

20%

30%

40%

50%

Oct-08 Oct-09 Oct-10 Oct-11 Oct-12 Oct-13

Korea

Indonesia

Thailand

Malaysia

Source: Various regulators

Figure 6: Stocks with high foreign ownership (as a percentage of total foreign holdings)

0% 2% 4% 6% 8% 10% 12%

YTL Corp

Gamuda

IOI Corp

DiGi

Petronas Chemicals

BAT Malaysia

AMMB

GENM

Sime Darby

Axiata Group

Tenaga Nasional

Genting

CIMB

Malayan Banking

Public Bank - F

Source: Company data, Credit Suisse estimates

Thursday, 06 February 2014

Asian Daily

- 7 of 35 -

Indonesia Market Strategy ----------------------------------------------------------------------------------- Assessing the impact of a China slowdown Jahanzeb Naseer / Research Analyst / 852 2101 6554 / [email protected]

● The two external risks that are being talked about on Indonesia are the potential EM contagion and the linkages to slower growth in China. The former was addressed in CS's note (Re-testing

Asian vulnerability). The second we discuss here.

● At 11% of exports, China is Indonesia’s third-biggest partner after ASEAN (22%) and Japan (16%). The four areas of key linkages to China are coal (37% of exports), rubber/industrial inputs (22%), CPO (15%) and manufactured/finished goods (7%).

● Of these the first two are at risk from an industrial slowdown while the latter two geared to consumption are more resilient.

● The decline in coal exports so far is explained by falling coal prices while volumes have continued to rise. Stable-to-slightly higher coal prices (CS forecasts) indicate lower risk going forward. Even assuming the current trajectory of a decline in coal and rubber would result in a loss of US$1.5-2 bn. CPO and finished goods exports have been rising and with higher CPO prices this should more than offset the decline in industrial sector-related exports.

Figure 1: Coal and related materials are the major portion of exports

Coal & related materials

37%

Rubber, leather & related materials

22%

Palm oil & related

materials15%

Manufactured goods7%

Machinery and transport equipment

6%

Chemicals and related products, n.e.s.

6%

Food and live animals4%

Miscellaneous manufactured

articles3%

Commodities and transactions, n.e.s.

0% Beverages and tobacco

0%

Source: Based on 2012 data, UNCTADSTAT, Credit Suisse estimates.

Linkages from softer China growth

Credit Suisse cut its forecast for China's economic growth from 7.7% to 7.3% YoY for 2014. China accounts for about 11% of Indonesia's exports making it the third-biggest trading partner after ASEAN (22%) and Japan (16%), with coal accounting for 37% of exports to China, rubber and other industrial materials about 22% and palm oil 15%. It is prudent to question the impact on the coal and CPO sectors in particular and on Indonesia in general.

Industrial related exports to China declining and consumer related rising

Figure 2 shows that while coal, rubber and other inputs into the manufacturing related sectors have been declining at around 10% a year in 2012 and 2013E, palm oil and other consumer related manufactured goods have been rising at close to 20% a year. This is broadly representative of the slowdown in the Chinese industrial complex and the continued growth in consumer segments. If the trend of declines in coal and other materials continues into 2014, we are likely to see a US$1.5-2 bn decline in exports to China. This decline is likely to be offset by rises in CPO and manufactured goods. So from an overall economic standpoint, the net change is unlikely to be material.

Figure 2: Top 4 contributors of Indonesian exports to China

0

1

2

3

4

5

6

7

8

9

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

US

$ bn

Indonesia export to China - Top 4 contributors in 2012

Coal & related materials Rubber, leather & related materials

Palm oil & related materials Manufactured goods

Source: UNCTADSTAT, Credit Suisse estimates.

The decline in the past had been due to weaker coal prices despite rising volumes

As seen in Figure 3 below, coal export volumes to China have been on the rise. The entire decline in coal exports to China in dollar terms is explained by falling coal prices (down nearly 33% since 2011). With coal prices expected to be flat to slightly up in the coming one to two years, it is unlikely that Indonesian coal exports to China will decline materially even in dollar terms.

The situation in CPO is even more encouraging. The near 20% growth of CPO exports to China has been recorded in the face of a nearly 40% fall in CPO prices over three years. CPO prices have started to recover from that level and CS forecasts suggest a further modest rise (2,600 rm/tn vs 2,370 rm/tn). CPO dollar exports to China therefore are likely to be stronger than what we had seen in the past.

Figure 3: Coal sales volume is relatively stable, yet price is not

-

500

1,000

1,500

2,000

2,500

3,000

3,500

-

1,000

2,000

3,000

4,000

5,000

6,000

2008 2009 2010 2011 2012 2013E

Sales volume ('000 mt)

CPO price (RM/ton) (RHS)

0

20

40

60

80

100

120

140

-

10.0

20.0

30.0

40.0

50.0

60.0

2008 2009 2010 2011 2012 2013E

Total Volume to China (mt)

Coal price - US$/t (RHS)

Source: Company data, Credit Suisse estimates.

Overall numbers suggest limited damage

Our analysis above suggests limited damage to Indonesia's trade balance from slowing China growth. The weakness in coal and CPO stocks could offer an opportunity to buy selectively. We like First Resources, Golden Agri, ADARO and PTBA.

Thursday, 06 February 2014

Asian Daily

- 8 of 35 -

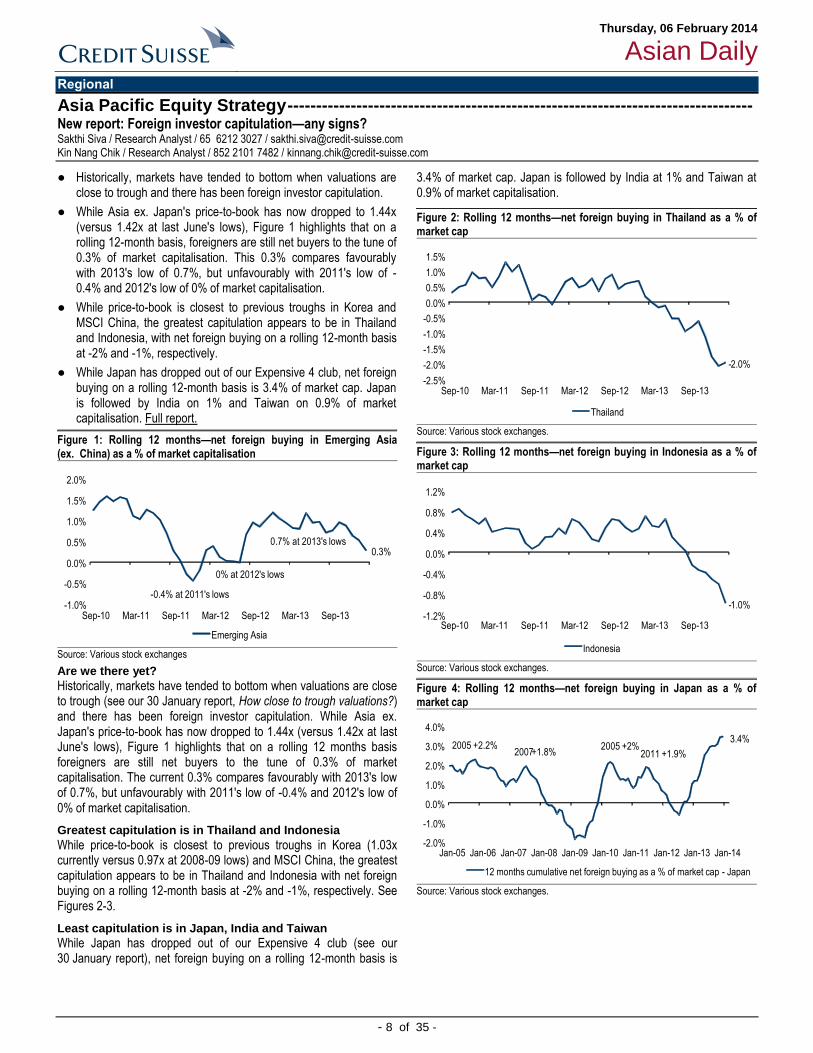

Regional

Asia Pacific Equity Strategy --------------------------------------------------------------------------------- New report: Foreign investor capitulation—any signs? Sakthi Siva / Research Analyst / 65 6212 3027 / [email protected] Kin Nang Chik / Research Analyst / 852 2101 7482 / [email protected]

● Historically, markets have tended to bottom when valuations are close to trough and there has been foreign investor capitulation.

● While Asia ex. Japan's price-to-book has now dropped to 1.44x (versus 1.42x at last June's lows), Figure 1 highlights that on a rolling 12-month basis, foreigners are still net buyers to the tune of 0.3% of market capitalisation. This 0.3% compares favourably with 2013's low of 0.7%, but unfavourably with 2011's low of -0.4% and 2012's low of 0% of market capitalisation.

● While price-to-book is closest to previous troughs in Korea and MSCI China, the greatest capitulation appears to be in Thailand and Indonesia, with net foreign buying on a rolling 12-month basis at -2% and -1%, respectively.

● While Japan has dropped out of our Expensive 4 club, net foreign buying on a rolling 12-month basis is 3.4% of market cap. Japan is followed by India on 1% and Taiwan on 0.9% of market capitalisation. Full report.

Figure 1: Rolling 12 months—net foreign buying in Emerging Asia (ex. China) as a % of market capitalisation

0.3%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13

Emerging Asia

0% at 2012's lows

-0.4% at 2011's lows

0.7% at 2013's lows

Source: Various stock exchanges

Are we there yet?

Historically, markets have tended to bottom when valuations are close to trough (see our 30 January report, How close to trough valuations?) and there has been foreign investor capitulation. While Asia ex. Japan's price-to-book has now dropped to 1.44x (versus 1.42x at last June's lows), Figure 1 highlights that on a rolling 12 months basis foreigners are still net buyers to the tune of 0.3% of market capitalisation. The current 0.3% compares favourably with 2013's low of 0.7%, but unfavourably with 2011's low of -0.4% and 2012's low of 0% of market capitalisation.

Greatest capitulation is in Thailand and Indonesia

While price-to-book is closest to previous troughs in Korea (1.03x currently versus 0.97x at 2008-09 lows) and MSCI China, the greatest capitulation appears to be in Thailand and Indonesia with net foreign buying on a rolling 12-month basis at -2% and -1%, respectively. See Figures 2-3.

Least capitulation is in Japan, India and Taiwan

While Japan has dropped out of our Expensive 4 club (see our 30 January report), net foreign buying on a rolling 12-month basis is

3.4% of market cap. Japan is followed by India at 1% and Taiwan at 0.9% of market capitalisation.

Figure 2: Rolling 12 months—net foreign buying in Thailand as a % of market cap

-2.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13

Thailand

Source: Various stock exchanges.

Figure 3: Rolling 12 months—net foreign buying in Indonesia as a % of market cap

-1.0%-1.2%

-0.8%

-0.4%

0.0%

0.4%

0.8%

1.2%

Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13

Indonesia

Source: Various stock exchanges.

Figure 4: Rolling 12 months—net foreign buying in Japan as a % of market cap

3.4%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

12 months cumulative net foreign buying as a % of market cap - Japan

2005 +2.2%2007+1.8%

2005 +2%2011 +1.9%

Source: Various stock exchanges.

Thursday, 06 February 2014

Asian Daily

- 9 of 35 -

Australia

Aristocrat Leisure -------------------------------------------------------- Maintain UNDERPERFORM Looking for the break-out EPS: ▲ TP: ▲ Larry Gandler / Research Analyst / 61 3 9280 1855 / [email protected] Benjamin Levin / Research Analyst / 61 3 9280 1766 / [email protected]

● We cautiously increase our target price to A$4.50 (from A$4.10) on more favourable fx assumptions and increased installations of North American 'revenue share' slot machines. We upgrade EPS by 8%. We appear in line with consensus.

● ALL gained share in the 'revenue share' segment of the North America slot machine industry in the December Qtr. We have reviewed the Dec Qtr 2013 Eiler-Fantini Quarterly Slot Survey. ALL has not gained share in the 'for sale' segment.

● Our valuation could rise to A$5.20 if Aristocrat demonstrates it is on a break-out market share path towards a 20% ship share with its 20% step-up investment in R&D. Although Eiler-Fantini survey indicates that Aristocrat's allocation of slot manager future purchases is not on a break-out trend yet, management is at least taking the engine into fifth gear.

● ALL is not quite good value but the gap to its peers has narrowed. Our DCF-based target price incorporates 50c for online gaming initiatives. Full report

Click here for detailed financials

The feeble slot player cannot resuscitate replacement demand

We argue that the wave that drove the North America casino expansion of 1988-2007 has plateaued and will not rise again for the foreseeable future.

We remain of the view that slot machine replacement demand is unlikely to 'cycle' upwards. Indeed, we anticipate that the US industry will come to speak more openly about what we call a 'dead market' here in Australia. That is a segment of the slot market where the potential uplift in revenue is insufficient to justify an investment in a machine replacement. Thus, that machine may never get replaced. Therefore, we do not consider replacement demand in the context of the entire US installed base. Replacement demand may hover between 50,000 and 65,000 units for many years to come.

With capacity now exceeding demand, new venues and expansions are also likely to be few in number. We anticipate 10,000 to 20,000 devices

installed by way of new venues or expansions. We therefore expect demand to hover around 70,000 units for the foreseeable future.

Figure 1: Median income fell in the late 2000s for baby boomers born 1946-65

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1990 2000 2010

In 2

012

US

D

Source: US Census Bureau (Measured in 2012 USD)

Aristocrat is taking share in participation

The most recent Eilers-Fantini Slot Survey indicates to us that Aristocrat has gained share in the participation segment. The survey measures about 28% of the North America installed base.

Our A$4.50 valuation is predicated on Aristocrat adding 1,050 'revenue-sharing' installations to 8,600 in FY14 reaching 10,000 by 2015. Aristocrat seems to be aiming for at least 10,000 units spurred by a 20% lift in R&D based on comments from the company's US management. Since 2005, Aristocrat has not expanded its installed base by more than 900 units in a given year.

The valuation leverage in gaming operations is powerful. For every 1000 unit increase in average machine installed base our EPS forecast rises by 5% and our valuation by 42cps. The valuation increase assumes that Aristocrat sustains its share of floor to perpetuity.

Still early days in the 'for sale' segment

With its 20% increase in R&D, Aristocrat is aiming to strongly break out of its traditional 12-14% North America market share range. We model ALL's market share rising to 15% by 2015 and then hovering around there. In essence, our valuation is not incorporating full success.

If we were to value ALL as a 20% ship-share business in North America, we would add 70c to our valuation making it A$5.20.

But, Aristocrat has not yet taken share in the 'for sale' segment. According to the Eiler-Fantini slot survey in Dec Qtr, ALL's ship share was 9% – down from its traditional 12%. However, in the Dec Qtr-13, Aristocrat cycled the release of Wonder 4 from the Dec Qtr-2012 and that game was the major contributor lifting Aristocrat's market share from 12.5% to about 13.5% during FY13. ALL sold 1,700 Wonder 4 gaming machines in its first 12 months since release (FY13.)

This is an extract from the Aristocrat Leisure report published on 4 February 2014. Please see CS's R&A website for more details.

Bbg/RIC ALL AU / ALL.AX Rating (prev. rating) U (U) Shares outstanding (mn) 551.42 Daily trad vol - 6m avg (mn) 1.5 Daily trad val - 6m avg (US$ mn) 7.5 Free float (%) 76.7 Major shareholders

Price (04 Feb 14 , A$) 4.40 TP (prev. TP A$) 4.50 (4.10) Est. pot. % chg. to TP 2 52-wk range (A$) 5.05 - 3.58 Mkt cap (A$/US$ mn) 2,426.2/ 2,154.7

Performance 1M 3M 12M

Absolute (%) (5.4) (9.1) 19.6 Relative (%) (0.6) (2.9) 15.7

Year 09/12A 09/13A 09/14E 09/15E 09/16E

Revenue (A$ mn) 843 814 904 971 1,028 EBITDA (A$ mn) 177.9 188.1 231.0 258.2 277.2 Net profit (A$ mn) 91.7 107.2 130.5 144.5 153.7 EPS (A$) 0.17 0.19 0.24 0.26 0.28 - Change from prev. EPS (%) n.a. n.a. 7.6 9.9 7.2 - Consensus EPS (A$) n.a. n.a. 0.23 0.27 0.29 EPS growth (%) 35.9 15.8 21.5 10.8 8.3 P/E (x) 26.3 22.7 18.7 16.9 15.6 Dividend yield (%) 1.4 3.3 3.8 4.5 4.8 EV/EBITDA (x) 14.7 14.0 11.1 9.9 9.4 P/B (x) 8.7 6.4 5.7 5.2 5.7 ROE (%) 34.4 32.6 32.5 32.4 34.8 Net debt(cash)/equity (%) 69.4 55.5 32.7 26.4 44.0

Note 1: Aristocrat Leisure Limited is an Australia-based company engaged in providing gaming solutions. Aristocrat offers a diverse range of products and services, including electronic gaming machines, interactive video terminal systems and casino management.

Thursday, 06 February 2014

Asian Daily

- 10 of 35 -

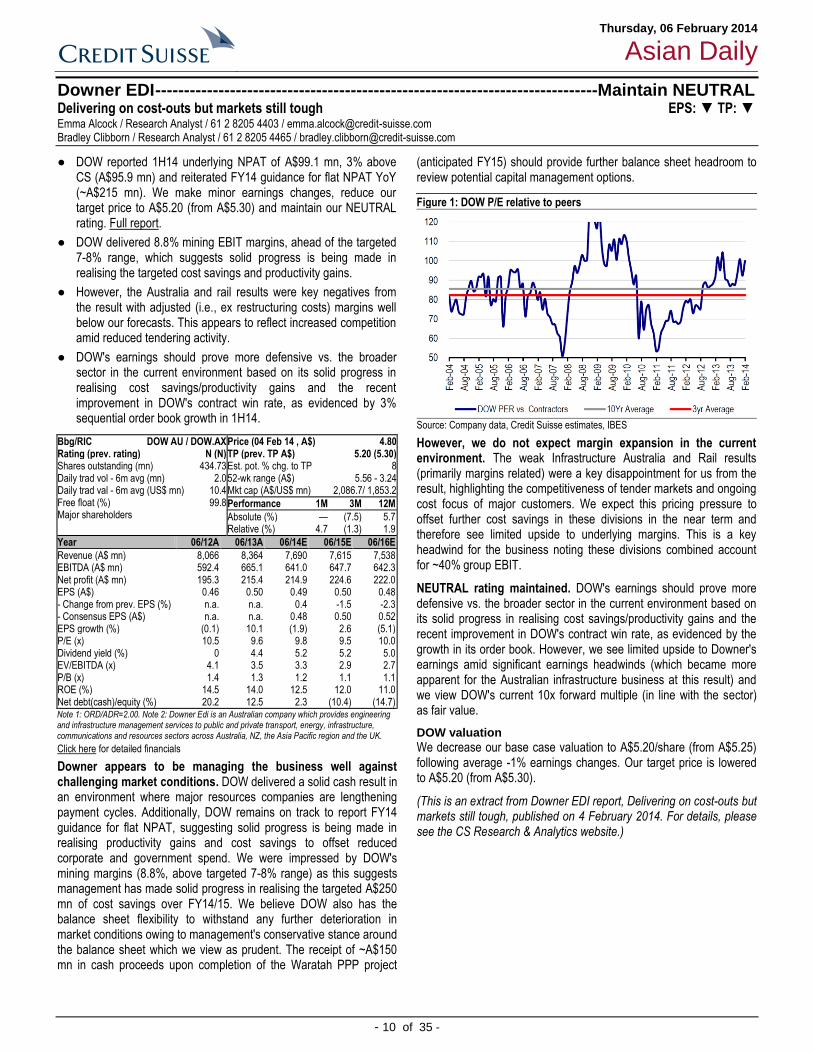

Downer EDI -----------------------------------------------------------------------------Maintain NEUTRAL Delivering on cost-outs but markets still tough EPS: ▼ TP: ▼ Emma Alcock / Research Analyst / 61 2 8205 4403 / [email protected] Bradley Clibborn / Research Analyst / 61 2 8205 4465 / [email protected]

● DOW reported 1H14 underlying NPAT of A$99.1 mn, 3% above CS (A$95.9 mn) and reiterated FY14 guidance for flat NPAT YoY (~A$215 mn). We make minor earnings changes, reduce our target price to A$5.20 (from A$5.30) and maintain our NEUTRAL rating. Full report.

● DOW delivered 8.8% mining EBIT margins, ahead of the targeted 7-8% range, which suggests solid progress is being made in realising the targeted cost savings and productivity gains.

● However, the Australia and rail results were key negatives from the result with adjusted (i.e., ex restructuring costs) margins well below our forecasts. This appears to reflect increased competition amid reduced tendering activity.

● DOW's earnings should prove more defensive vs. the broader sector in the current environment based on its solid progress in realising cost savings/productivity gains and the recent improvement in DOW's contract win rate, as evidenced by 3% sequential order book growth in 1H14.

Click here for detailed financials

Downer appears to be managing the business well against challenging market conditions. DOW delivered a solid cash result in an environment where major resources companies are lengthening payment cycles. Additionally, DOW remains on track to report FY14 guidance for flat NPAT, suggesting solid progress is being made in realising productivity gains and cost savings to offset reduced corporate and government spend. We were impressed by DOW's mining margins (8.8%, above targeted 7-8% range) as this suggests management has made solid progress in realising the targeted A$250 mn of cost savings over FY14/15. We believe DOW also has the balance sheet flexibility to withstand any further deterioration in market conditions owing to management's conservative stance around the balance sheet which we view as prudent. The receipt of ~A$150 mn in cash proceeds upon completion of the Waratah PPP project

(anticipated FY15) should provide further balance sheet headroom to review potential capital management options.

Figure 1: DOW P/E relative to peers

Source: Company data, Credit Suisse estimates, IBES

However, we do not expect margin expansion in the current environment. The weak Infrastructure Australia and Rail results (primarily margins related) were a key disappointment for us from the result, highlighting the competitiveness of tender markets and ongoing cost focus of major customers. We expect this pricing pressure to offset further cost savings in these divisions in the near term and therefore see limited upside to underlying margins. This is a key headwind for the business noting these divisions combined account for ~40% group EBIT.

NEUTRAL rating maintained. DOW's earnings should prove more defensive vs. the broader sector in the current environment based on its solid progress in realising cost savings/productivity gains and the recent improvement in DOW's contract win rate, as evidenced by the growth in its order book. However, we see limited upside to Downer's earnings amid significant earnings headwinds (which became more apparent for the Australian infrastructure business at this result) and we view DOW's current 10x forward multiple (in line with the sector) as fair value.

DOW valuation

We decrease our base case valuation to A$5.20/share (from A$5.25) following average -1% earnings changes. Our target price is lowered to A$5.20 (from A$5.30).

(This is an extract from Downer EDI report, Delivering on cost-outs but markets still tough, published on 4 February 2014. For details, please see the CS Research & Analytics website.)

Bbg/RIC DOW AU / DOW.AX Rating (prev. rating) N (N) Shares outstanding (mn) 434.73 Daily trad vol - 6m avg (mn) 2.0 Daily trad val - 6m avg (US$ mn) 10.4 Free float (%) 99.8 Major shareholders

Price (04 Feb 14 , A$) 4.80 TP (prev. TP A$) 5.20 (5.30) Est. pot. % chg. to TP 8 52-wk range (A$) 5.56 - 3.24 Mkt cap (A$/US$ mn) 2,086.7/ 1,853.2

Performance 1M 3M 12M

Absolute (%) — (7.5) 5.7 Relative (%) 4.7 (1.3) 1.9

Year 06/12A 06/13A 06/14E 06/15E 06/16E

Revenue (A$ mn) 8,066 8,364 7,690 7,615 7,538 EBITDA (A$ mn) 592.4 665.1 641.0 647.7 642.3 Net profit (A$ mn) 195.3 215.4 214.9 224.6 222.0 EPS (A$) 0.46 0.50 0.49 0.50 0.48 - Change from prev. EPS (%) n.a. n.a. 0.4 -1.5 -2.3 - Consensus EPS (A$) n.a. n.a. 0.48 0.50 0.52 EPS growth (%) (0.1) 10.1 (1.9) 2.6 (5.1) P/E (x) 10.5 9.6 9.8 9.5 10.0 Dividend yield (%) 0 4.4 5.2 5.2 5.0 EV/EBITDA (x) 4.1 3.5 3.3 2.9 2.7 P/B (x) 1.4 1.3 1.2 1.1 1.1 ROE (%) 14.5 14.0 12.5 12.0 11.0 Net debt(cash)/equity (%) 20.2 12.5 2.3 (10.4) (14.7)

Note 1: ORD/ADR=2.00. Note 2: Downer Edi is an Australian company which provides engineering and infrastructure management services to public and private transport, energy, infrastructure, communications and resources sectors across Australia, NZ, the Asia Pacific region and the UK.

Thursday, 06 February 2014

Asian Daily

- 11 of 35 -

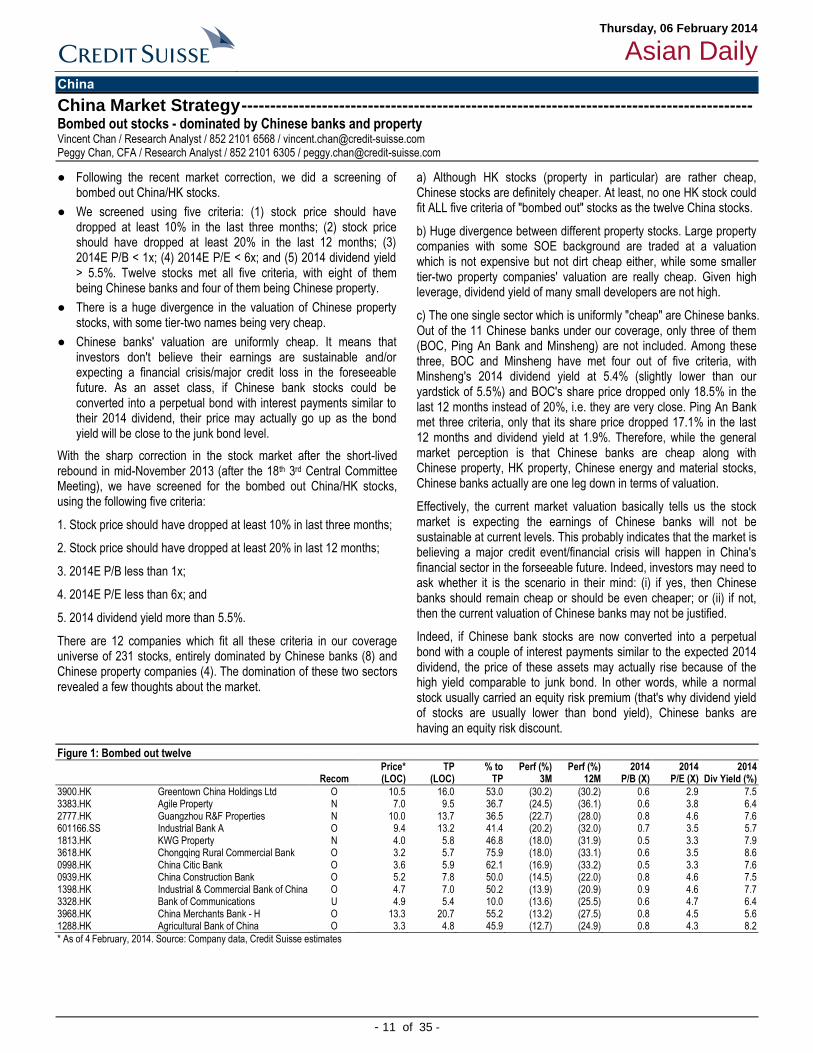

China

China Market Strategy ----------------------------------------------------------------------------------------- Bombed out stocks - dominated by Chinese banks and property Vincent Chan / Research Analyst / 852 2101 6568 / [email protected] Peggy Chan, CFA / Research Analyst / 852 2101 6305 / [email protected]

● Following the recent market correction, we did a screening of bombed out China/HK stocks.

● We screened using five criteria: (1) stock price should have dropped at least 10% in the last three months; (2) stock price should have dropped at least 20% in the last 12 months; (3) 2014E P/B < 1x; (4) 2014E P/E < 6x; and (5) 2014 dividend yield > 5.5%. Twelve stocks met all five criteria, with eight of them being Chinese banks and four of them being Chinese property.

● There is a huge divergence in the valuation of Chinese property stocks, with some tier-two names being very cheap.

● Chinese banks' valuation are uniformly cheap. It means that investors don't believe their earnings are sustainable and/or expecting a financial crisis/major credit loss in the foreseeable future. As an asset class, if Chinese bank stocks could be converted into a perpetual bond with interest payments similar to their 2014 dividend, their price may actually go up as the bond yield will be close to the junk bond level.

With the sharp correction in the stock market after the short-lived rebound in mid-November 2013 (after the 18th 3rd Central Committee Meeting), we have screened for the bombed out China/HK stocks, using the following five criteria:

1. Stock price should have dropped at least 10% in last three months;

2. Stock price should have dropped at least 20% in last 12 months;

3. 2014E P/B less than 1x;

4. 2014E P/E less than 6x; and

5. 2014 dividend yield more than 5.5%.

There are 12 companies which fit all these criteria in our coverage universe of 231 stocks, entirely dominated by Chinese banks (8) and Chinese property companies (4). The domination of these two sectors revealed a few thoughts about the market.

a) Although HK stocks (property in particular) are rather cheap, Chinese stocks are definitely cheaper. At least, no one HK stock could fit ALL five criteria of "bombed out" stocks as the twelve China stocks.

b) Huge divergence between different property stocks. Large property companies with some SOE background are traded at a valuation which is not expensive but not dirt cheap either, while some smaller tier-two property companies' valuation are really cheap. Given high leverage, dividend yield of many small developers are not high.

c) The one single sector which is uniformly "cheap" are Chinese banks. Out of the 11 Chinese banks under our coverage, only three of them (BOC, Ping An Bank and Minsheng) are not included. Among these three, BOC and Minsheng have met four out of five criteria, with Minsheng's 2014 dividend yield at 5.4% (slightly lower than our yardstick of 5.5%) and BOC's share price dropped only 18.5% in the last 12 months instead of 20%, i.e. they are very close. Ping An Bank met three criteria, only that its share price dropped 17.1% in the last 12 months and dividend yield at 1.9%. Therefore, while the general market perception is that Chinese banks are cheap along with Chinese property, HK property, Chinese energy and material stocks, Chinese banks actually are one leg down in terms of valuation.

Effectively, the current market valuation basically tells us the stock market is expecting the earnings of Chinese banks will not be sustainable at current levels. This probably indicates that the market is believing a major credit event/financial crisis will happen in China's financial sector in the forseeable future. Indeed, investors may need to ask whether it is the scenario in their mind: (i) if yes, then Chinese banks should remain cheap or should be even cheaper; or (ii) if not, then the current valuation of Chinese banks may not be justified.

Indeed, if Chinese bank stocks are now converted into a perpetual bond with a couple of interest payments similar to the expected 2014 dividend, the price of these assets may actually rise because of the high yield comparable to junk bond. In other words, while a normal stock usually carried an equity risk premium (that's why dividend yield of stocks are usually lower than bond yield), Chinese banks are having an equity risk discount.

Figure 1: Bombed out twelve Price* TP % to Perf (%) Perf (%) 2014 2014 2014 Recom (LOC) (LOC) TP 3M 12M P/B (X) P/E (X) Div Yield (%)

3900.HK Greentown China Holdings Ltd O 10.5 16.0 53.0 (30.2) (30.2) 0.6 2.9 7.5 3383.HK Agile Property N 7.0 9.5 36.7 (24.5) (36.1) 0.6 3.8 6.4 2777.HK Guangzhou R&F Properties N 10.0 13.7 36.5 (22.7) (28.0) 0.8 4.6 7.6 601166.SS Industrial Bank A O 9.4 13.2 41.4 (20.2) (32.0) 0.7 3.5 5.7 1813.HK KWG Property N 4.0 5.8 46.8 (18.0) (31.9) 0.5 3.3 7.9 3618.HK Chongqing Rural Commercial Bank O 3.2 5.7 75.9 (18.0) (33.1) 0.6 3.5 8.6 0998.HK China Citic Bank O 3.6 5.9 62.1 (16.9) (33.2) 0.5 3.3 7.6 0939.HK China Construction Bank O 5.2 7.8 50.0 (14.5) (22.0) 0.8 4.6 7.5 1398.HK Industrial & Commercial Bank of China O 4.7 7.0 50.2 (13.9) (20.9) 0.9 4.6 7.7 3328.HK Bank of Communications U 4.9 5.4 10.0 (13.6) (25.5) 0.6 4.7 6.4 3968.HK China Merchants Bank - H O 13.3 20.7 55.2 (13.2) (27.5) 0.8 4.5 5.6 1288.HK Agricultural Bank of China O 3.3 4.8 45.9 (12.7) (24.9) 0.8 4.3 8.2

* As of 4 February, 2014. Source: Company data, Credit Suisse estimates

Thursday, 06 February 2014

Asian Daily

- 12 of 35 -

China Market Strategy ----------------------------------------------------------------------------------------- HOLT analysis on our top picks in these times of uncertainty Vincent Chan / Research Analyst / 852 2101 6568 / [email protected]

● In our recent report What stocks to buy after the recent correction, we picked 15 stocks that we like for their long-term fundamentals. In this daily, we attempt to look at these stocks using the HOLT valuation model.

● As a group, these companies exhibited strong value creation with a median CFROI of 11.6% over the past five years, compared to Asia ex-Japan’s 7% over the same period. Although CFROI fell to 9.4% last year, consensus estimates suggest an improvement to 10.6% this year.

● Current market-implied expectations are undemanding with investors pricing for CFROI to decline to 8.1% over the next five years, suggesting that the macro risk factors might have been priced in.

● These companies now have a median HOLT upside of +12% which compares favourably to their historical upside of -3% in the HOLT model.

Figure 1: MSCI China PB

0.5

1.5

2.5

3.5

4.5

5.5

Mar-01 Mar-03 Mar-05 Mar-07 Mar-09 Mar-11 Mar-13

MSCI China - P/B (x)Avg+1SD-1SD

Source: MSCI.

Sharp corrections will create market opportunities

Recent concerns over the US growth/monetary policy, emerging market currency (particularly in the LatAm area), Chinese economy/financial system risks and lack of additional reform measures have triggered a market correction. We believe such sharp corrections will create market opportunities. Our analysts have chosen 15 stocks for their long-term fundamentals.

In this note, we attempt to look at these stocks using the HOLT valuation model. As shown in Figure 2, these companies in aggregate exhibited strong value creation with a median CFROI of 11.6% over the past five years, compared to Asia ex-Japan’s 7% over the same period. Although CFROI fell to 9.4% last year, consensus estimates suggest an improvement to 10.6% this year.

Market-implied expectations undemanding

Current market-implied expectations are undemanding with investors pricing for CFROI to decline to 8.1% over the next five years, suggesting that macro risk factors might have been priced in.

These companies now have a median HOLT upside of +12% which compares favourably to their historical upside of -3% in the HOLT model.

Figure 2: Credit Suisse China top picks under uncertainty

Operation Momentum Valuation

Company Ticker SectorMarket Cap

(USD bn)

CFROI

5yr Median

CFROI

LFY (2012)

Forecast

CFROI

Market

Implied

CFROI (FY5)

CFROI

Momentum

13 Weeks

Relative

Price

Return 4

Weeks

HOLT

Upside

HOLT

Upside

5yr Median

Agricultural Bank of China Limited 1288.HK Financials 137.6 17.5 17.5 13.1 5.9 0.0 (4.2) 54.0 41.9

Anhui Conch Cement Company Limited 0914.HK Materials 19.6 9.1 8.8 10.8 6.8 0.6 12.1 33.0 0.7

BOC Hong Kong (Holdings) Ltd 2388.HK Financials 31.5 13.6 13.6 14.6 16.4 0.1 0.1 (16.0) 0.5

China Longyuan Power Group Limited 0916.HK Utilities 9.8 3.9 5.4 6.0 5.4 0.1 (1.8) 13.0 (30.1)

China Mengniu Dairy Company Limited 2319.HK Consumer Staples 8.1 8.9 7.3 9.5 12.3 (0.2) 2.9 (34.0) (38.6)

China Mobile Limited 0941.HK Telecommunication Services 186.4 11.6 9.4 7.6 (1.3) (0.6) (2.4) 117.0 96.4

China Oilfield Services Ltd 2883.HK Energy 11.6 4.9 4.9 6.8 7.2 0.2 (7.5) (4.0) (37.4)

China Resources Land Limited 1109.HK Financials 13.3 5.1 6.7 7.6 4.4 (0.1) (1.0) 52.0 (11.9)

Chow Tai Fook Jewellery Group Ltd 1929.HK Consumer Discretionary 14.9 18.6 11.6 9.8 8.3 0.1 4.5 (9.0) (2.9)

Henderson Land Development Company Limited0012.HK Financials 14.0 1.7 1.7 0.9 (6.1) (0.0) (1.7) 98.0 36.4

Sands China Limited 1928.HK Consumer Discretionary 61.3 10.0 14.0 28.5 24.7 2.5 (2.2) (20.0) (43.9)

Shenzhou International Group Holdings Ltd 2313.HK Consumer Discretionary 4.3 16.6 15.5 12.9 8.1 (0.5) (6.0) 24.0 100.4

Sihuan Pharmaceutical Holdings Group Ltd 0460.HK Health Care 5.5 18.3 18.3 21.0 18.1 0.7 13.5 (30.0) (23.9)

Tencent Holdings Limited 0700.HK Information Technology 121.9 30.8 30.8 24.6 17.2 0.3 13.4 12.0 40.1

Tsui Wah Holdings Limited 1314.HK Consumer Discretionary 0.8 12.8 6.8 10.6 16.0 (0.7) (8.9) (58.0) (61.3)

Median 11.6 9.4 10.6 8.1 0.1 (1.7) 12.0 (2.9)

Source: Credit Suisse HOLT.

Thursday, 06 February 2014

Asian Daily

- 13 of 35 -

Shenzhou International ---------------------------------------------------- Maintain OUTPERFORM Time to accumulate after recent market correction EPS: ◄► TP: ◄► Eva Wang / Research Analyst / 852 2101 7365 / [email protected] Kenny Lau, CFA / Research Analyst / 852 2101 7914 / [email protected]

● Following the CS China Strategy report, What stocks to buy after recent correction, we'd like to highlight Shenzhou (2313.HK) as one of our picks.

● Despite market concerns on Chinese economic growth and US monetary policy, we believe the impact on Shenzhou should be quite limited given the company's good operational track record, exposure to export markets, strong balance sheet (net cash position) and high visibility of revenue and growth potential.

● We believe the catalysts for the stock include: 1) the release of new garment capacity in 2H14 from Anhui Anqing and Cambodia factories; 2) the new fabric capacity in phase I of Vietnam expansion which will commence operation by the end of 2014.

● We believe a good entry price will be around HK$25.0 (close to current share price), at only 10x 2015E P/E or 12x 2014E P/E. We believe the recent sharp price correction is not justified given the company's solid fundamentals. Our target price of HK$35.00 is based on 14x CY2015E P/E, implying 0.86x PEG with 16% EPS CAGR for 13-15E.

Click here for detailed financials

Shenzhou as one of our picks after recent correction

Following CS China Strategy report, What stocks to buy after recent correction, we'd like to highlight Shenzhou (2313.HK) as one of our picks. Despite market concerns on Chinese economic growth and US monetary policy, we believe the impact on Shenzhou should be quite limited given the company's good operational track record, exposure to export markets, strong balance sheet (net cash position) and high visibility of revenue and growth potential.

We believe the recent sharp share price correction is not justified given the company's solid fundamentals. We recommend investors to buy on dips after the recent correction.

An export player mainly, not relying on domestic market

We believe Shenzhou is one of the companies that should be affected less by China's domestic economic growth, compared to many others.

By geographical breakdown, the company gets around 80% of total revenue from export markets (Japan, Europe, etc.) and only 20% from China's domestic market. Even among its domestic China sales, most are for international brands in China, with little for China brands. Therefore, the concern over China's domestic economic growth should not be a big concern for Shenzhou, in our view.

Figure 1: 1H13 revenue breakdown

Rmb mn % of total YoY%

Japan 1,604 33.6 19.0

Europe 812 17.0 -18.6

US 388 8.1 49.5

China 933 19.5 7.7

Others 1,035 21.7 16.6

Source: Company data.

High order visibility, ~80% full-year revenue secured

Due to Shenzhou's dedicated factories and long-term strategic relationship with its major clients, the company has already secured orders/production plan for its top four clients, Uniqlo, Nike, Adidas and Puma, which accounted for ~80% of its total revenue. Such a high order visibility is quite unique among textile players and makes Shenzhou a resilient player under volatile market environment, rather than a cyclical company like many of its peers.

Figure 2: The top 4 clients

RMB mn 1H13 % of Total YoY%

Uniqlo 1,203 25.2 47.3

Adidas 1,065 22.3 0.0

Nike* 866* 18.2 13.0

Puma 542 11.4 52.0

Subtotal* 3,676* 77.0 22.4

Source: Company data, Credit Suisse estimates.

Note: *Excluding Nike footwear revenue, which was around US$26mn in 1H13 or making Nike's revenue share totaled ~21.6% in 1H13. Data as of 1H13.

Catalysts in 2014-15, undervalued at current share price

We believe the catalysts for the stock include: 1) the release of new garment capacity in 2H14 from the efficiency improvement of newly hired workers in Anhui Anqing and Cambodia factories; 2) the new fabric capacity in phase I of Vietnam expansion which will commence operation by the end of 2014.

We believe a good entry price will be around HK$25.0 (the current share price of HK$25.25 is pretty close), implying only 10x 2015E P/E or 12x 2014E P/E. We believe Shenzhou's fundamentals remain intact, and the recent share price correction offers a good buy-on-dips opportunity for investors seeking long-term stable return. Our target price of HK$35.00 is based on 14x CY2015E P/E, implying 0.86x PEG with 16% EPS CAGR for 13-15E.

Bbg/RIC 2313 HK / 2313.HK Rating (prev. rating) O (O) Shares outstanding (mn) 1,399.00 Daily trad vol - 6m avg (mn) 1.7 Daily trad val - 6m avg (US$ mn) 5.8 Free float (%) 34.1 Major shareholders Mr. Ma Jianrong

(53.6%)

Price (05 Feb 14 , HK$) 25.25 TP (prev. TP HK$) 35.00 (35.00) Est. pot. % chg. to TP 39 52-wk range (HK$) 30.1 - 19.2 Mkt cap (HK$/US$ mn) 35,324.8/ 4,550.6

Performance 1M 3M 12M

Absolute (%) (10.6) (6.1) 31.8 Relative (%) (3.8) 1.2 43.2

Year 12/11A 12/12A 12/13E 12/14E 12/15E

Revenue (Rmb mn) 9,043 8,938 10,108 12,213 14,782 EBITDA (Rmb mn) 2,311 2,163 2,507 3,018 3,592 Net profit (Rmb mn) 1,704 1,620 1,881 2,265 2,737 EPS (Rmb) 1.37 1.24 1.38 1.62 1.96 - Change from prev. EPS (%) n.a. n.a. 0 0 0 - Consensus EPS (Rmb) n.a. n.a. 1.35 1.56 1.86 EPS growth (%) 34.0 (9.1) 10.7 17.6 20.9 P/E (x) 14.4 15.9 14.3 12.2 10.1 Dividend yield (%) 2.1 2.8 2.8 3.3 4.0 EV/EBITDA (x) 12.0 12.1 10.0 8.0 6.4 P/B (x) 4.0 3.2 2.6 2.3 2.0 ROE (%) 31.3 22.9 20.3 20.3 21.3 Net debt(cash)/equity (%) 3.5 (16.7) (24.1) (28.3) (33.2)

Note 1: Shenzhou International provides vertically integrated knitwear manufacturing for well- known retailer brands on an OEM basis. Its products include casual wear, sports wear, lingerie and others. Exports account for around 80% of its total sales.

Thursday, 06 February 2014

Asian Daily

- 14 of 35 -

Hong Kong

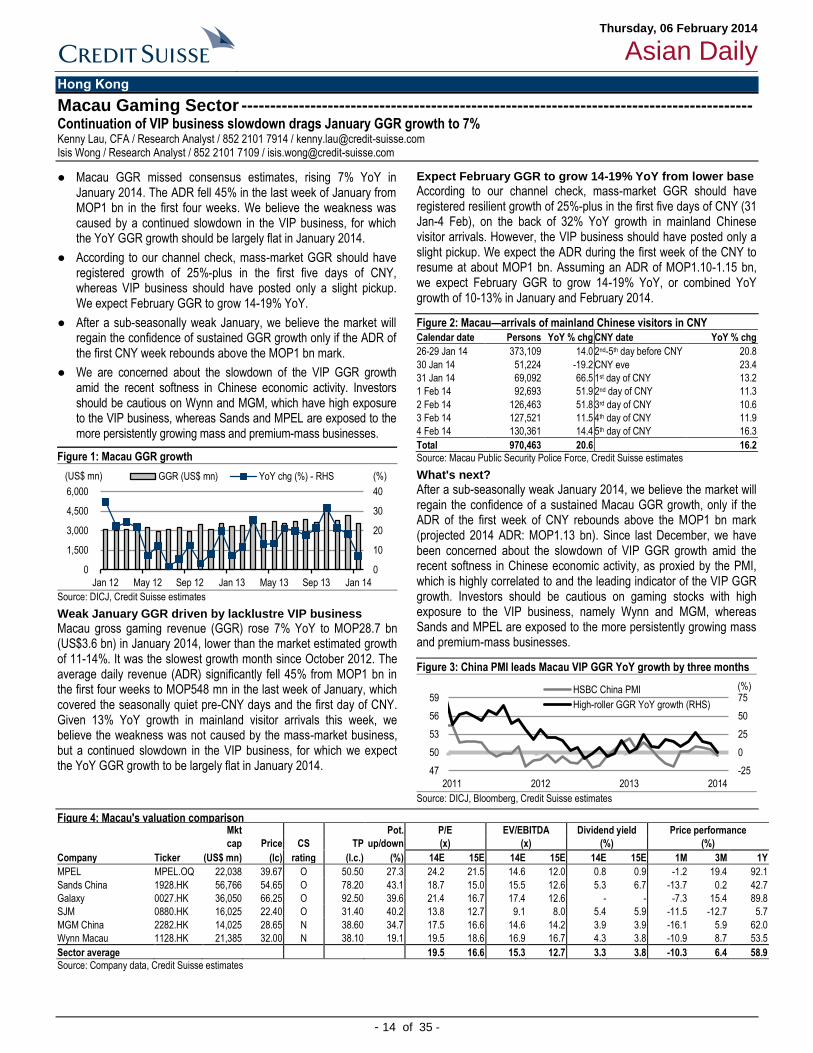

Macau Gaming Sector ----------------------------------------------------------------------------------------- Continuation of VIP business slowdown drags January GGR growth to 7% Kenny Lau, CFA / Research Analyst / 852 2101 7914 / [email protected] Isis Wong / Research Analyst / 852 2101 7109 / [email protected]

● Macau GGR missed consensus estimates, rising 7% YoY in January 2014. The ADR fell 45% in the last week of January from MOP1 bn in the first four weeks. We believe the weakness was caused by a continued slowdown in the VIP business, for which the YoY GGR growth should be largely flat in January 2014.

● According to our channel check, mass-market GGR should have registered growth of 25%-plus in the first five days of CNY, whereas VIP business should have posted only a slight pickup. We expect February GGR to grow 14-19% YoY.

● After a sub-seasonally weak January, we believe the market will regain the confidence of sustained GGR growth only if the ADR of the first CNY week rebounds above the MOP1 bn mark.

● We are concerned about the slowdown of the VIP GGR growth amid the recent softness in Chinese economic activity. Investors should be cautious on Wynn and MGM, which have high exposure to the VIP business, whereas Sands and MPEL are exposed to the more persistently growing mass and premium-mass businesses.

Figure 1: Macau GGR growth

0

10

20

30

40

0

1,500

3,000

4,500

6,000

Jan 12 May 12 Sep 12 Jan 13 May 13 Sep 13 Jan 14

GGR (US$ mn) YoY chg (%) - RHS(US$ mn) (%)

Source: DICJ, Credit Suisse estimates

Weak January GGR driven by lacklustre VIP business

Macau gross gaming revenue (GGR) rose 7% YoY to MOP28.7 bn (US$3.6 bn) in January 2014, lower than the market estimated growth of 11-14%. It was the slowest growth month since October 2012. The average daily revenue (ADR) significantly fell 45% from MOP1 bn in the first four weeks to MOP548 mn in the last week of January, which covered the seasonally quiet pre-CNY days and the first day of CNY. Given 13% YoY growth in mainland visitor arrivals this week, we believe the weakness was not caused by the mass-market business, but a continued slowdown in the VIP business, for which we expect the YoY GGR growth to be largely flat in January 2014.

Expect February GGR to grow 14-19% YoY from lower base

According to our channel check, mass-market GGR should have registered resilient growth of 25%-plus in the first five days of CNY (31 Jan-4 Feb), on the back of 32% YoY growth in mainland Chinese visitor arrivals. However, the VIP business should have posted only a slight pickup. We expect the ADR during the first week of the CNY to resume at about MOP1 bn. Assuming an ADR of MOP1.10-1.15 bn, we expect February GGR to grow 14-19% YoY, or combined YoY growth of 10-13% in January and February 2014.

Figure 2: Macau—arrivals of mainland Chinese visitors in CNY

Calendar date Persons YoY % chg CNY date YoY % chg

26-29 Jan 14 373,109 14.0 2nd-5th day before CNY 20.8

30 Jan 14 51,224 -19.2 CNY eve 23.4

31 Jan 14 69,092 66.5 1st day of CNY 13.2

1 Feb 14 92,693 51.9 2nd day of CNY 11.3

2 Feb 14 126,463 51.8 3rd day of CNY 10.6

3 Feb 14 127,521 11.5 4th day of CNY 11.9

4 Feb 14 130,361 14.4 5th day of CNY 16.3

Total 970,463 20.6 16.2

Source: Macau Public Security Police Force, Credit Suisse estimates

What's next?

After a sub-seasonally weak January 2014, we believe the market will regain the confidence of a sustained Macau GGR growth, only if the ADR of the first week of CNY rebounds above the MOP1 bn mark (projected 2014 ADR: MOP1.13 bn). Since last December, we have been concerned about the slowdown of VIP GGR growth amid the recent softness in Chinese economic activity, as proxied by the PMI, which is highly correlated to and the leading indicator of the VIP GGR growth. Investors should be cautious on gaming stocks with high exposure to the VIP business, namely Wynn and MGM, whereas Sands and MPEL are exposed to the more persistently growing mass and premium-mass businesses.

Figure 3: China PMI leads Macau VIP GGR YoY growth by three months

-25

0

25

50

75

47

50

53

56

59

2011 2012 2013 2014

(%)HSBC China PMI

High-roller GGR YoY growth (RHS)

Source: DICJ, Bloomberg, Credit Suisse estimates

Figure 4: Macau's valuation comparison Mkt Pot. P/E EV/EBITDA Dividend yield Price performance

cap Price CS TP up/down (x) (x) (%) (%)

Company Ticker (US$ mn) (lc) rating (l.c.) (%) 14E 15E 14E 15E 14E 15E 1M 3M 1Y

MPEL MPEL.OQ 22,038 39.67 O 50.50 27.3 24.2 21.5 14.6 12.0 0.8 0.9 -1.2 19.4 92.1

Sands China 1928.HK 56,766 54.65 O 78.20 43.1 18.7 15.0 15.5 12.6 5.3 6.7 -13.7 0.2 42.7

Galaxy 0027.HK 36,050 66.25 O 92.50 39.6 21.4 16.7 17.4 12.6 - - -7.3 15.4 89.8

SJM 0880.HK 16,025 22.40 O 31.40 40.2 13.8 12.7 9.1 8.0 5.4 5.9 -11.5 -12.7 5.7

MGM China 2282.HK 14,025 28.65 N 38.60 34.7 17.5 16.6 14.6 14.2 3.9 3.9 -16.1 5.9 62.0

Wynn Macau 1128.HK 21,385 32.00 N 38.10 19.1 19.5 18.6 16.9 16.7 4.3 3.8 -10.9 8.7 53.5

Sector average 19.5 16.6 15.3 12.7 3.3 3.8 -10.3 6.4 58.9

Source: Company data, Credit Suisse estimates

Thursday, 06 February 2014

Asian Daily

- 15 of 35 -

India

India Market Strategy ------------------------------------------------------------------------------------------ Can the cost-push rise in milk prices offset the decline in vegetable inflation? Neelkanth Mishra / Research Analyst / 91 22 6777 3716 / [email protected] Ravi Shankar / Research Analyst / 91 22 6777 3869 / [email protected]

● Last week milk prices were raised by Rs2/ltr for the second time since October, and retail prices are now tracking 18-23% higher YoY. Thus, milk prices are back at 15-20% growth after a 1.5-year lull (Figure 1).

● The strong correlation between milk costs and prices (Figure 4) suggests a strong cost push. Operating costs in milk production are primarily labour and fodder, and both have been rising. Fodder prices in particular have grown significantly since FY09, and have continued to rise in FY14 (Figure 2).

● The low prices over the last year thus likely hurt supply growth as costs were still rising. As demand grew and supply did not, prices are now rising. Milk has 3.2% weight in the CPI, versus 3.8% for fruits and vegetables: the expected decline in the latter inflation can likely be offset by the spike in milk prices.

● This wage-price spiral in more labour-intensive animal products and fruits/vegetables is the root cause of sticky food inflation (for details see link to our Oct 2013 report), and is unlikely to be broken soon—hence, our UNDERWEIGHT stance on rate-sensitive sectors. We recommend selling L&T, SBI and Tata Steel.

Milk price inflation at 20% YoY after an 18-month lull

Figure 1: After Feb hikes, milk price increases back to 20% YoY levels

0%

5%

10%

15%

20%

25%

30%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

TD

Pos

t Feb

Annual change in milk price (annual)

Source: EA to GoI, BS, IE, Credit Suisse estimates

Last week, milk prices were raised by Rs2/ltr for the second time in four months, and retail prices are now tracking 18-23% higher YoY. Thus, milk prices are back at 15-20% growth after a 1.5-year lull (Figure 1).

Figure 2: Fodder prices have continued to grow at 15-20% for a while

-40%

-20%

0%

20%

40%

60%

80%

0

100

200

300

400