ASEAN TAXES AND PH FISCAL INCENTIVES UP ETC Roundtable discussion on Rationalizing Fiscal Incentives, UPSE, Diliman, QC, PH 24 March 2015 Bienvenido “Nonoy” Oplas, Jr. SEANET Fellow

ASEAN Taxes and Philippines Fiscal Incentives

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ASEAN TAXES AND

PH FISCAL INCENTIVES

UP ETC Roundtable discussion on

Rationalizing Fiscal Incentives, UPSE, Diliman, QC, PH

24 March 2015

Bienvenido “Nonoy” Oplas, Jr.

SEANET Fellow

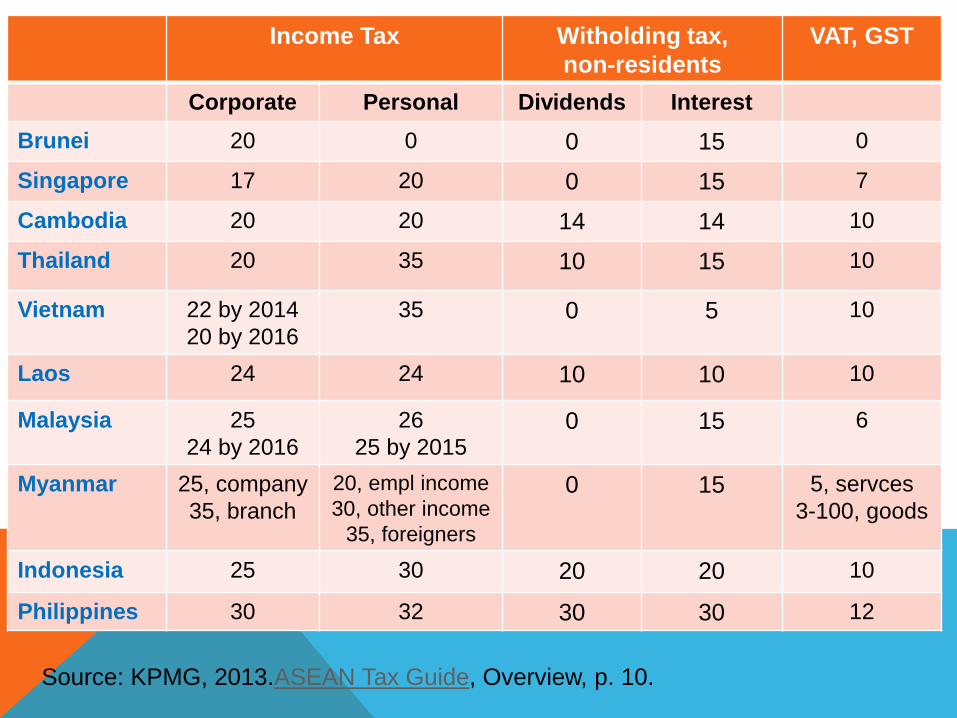

Source: KPMG, 2013.ASEAN Tax Guide, Overview, p. 10.

Income Tax Witholding tax,

non-residents

VAT, GST

Corporate Personal Dividends Interest

Brunei 20 0 0 15 0

Singapore 17 20 0 15 7

Cambodia 20 20 14 14 10

Thailand 20 35 10 15 10

Vietnam 22 by 2014

20 by 2016

35 0 5 10

Laos 24 24 10 10 10

Malaysia 25

24 by 2016

26

25 by 2015 0 15 6

Myanmar 25, company

35, branch

20, empl income

30, other income

35, foreigners

0 15 5, servces

3-100, goods

Indonesia 25 30 20 20 10

Philippines 30 32 30 30 12

Paying Taxes Year Singapore Brunei Malaysia Cambodia Thailand

Rank: out of 2010 5 22 24 58 88

183 (2010),

189 (2015)

countries

2015 5 30 32 90 62

Payments 2010 5 15 12 39 23

(no. per year) 2015 5 27 13 40 22

Time 2010 84 144 145 173 264

(Hours per yr) 2015 82 93 133 173 264

Total tax rate 2010 27.8 30.3 34.2 22.7 37.2

(% of profit) 2015 18.4 15.8 39.2 21.0 26.9

Source: World Bank, Doing Business, 2010 and 2015 Reports

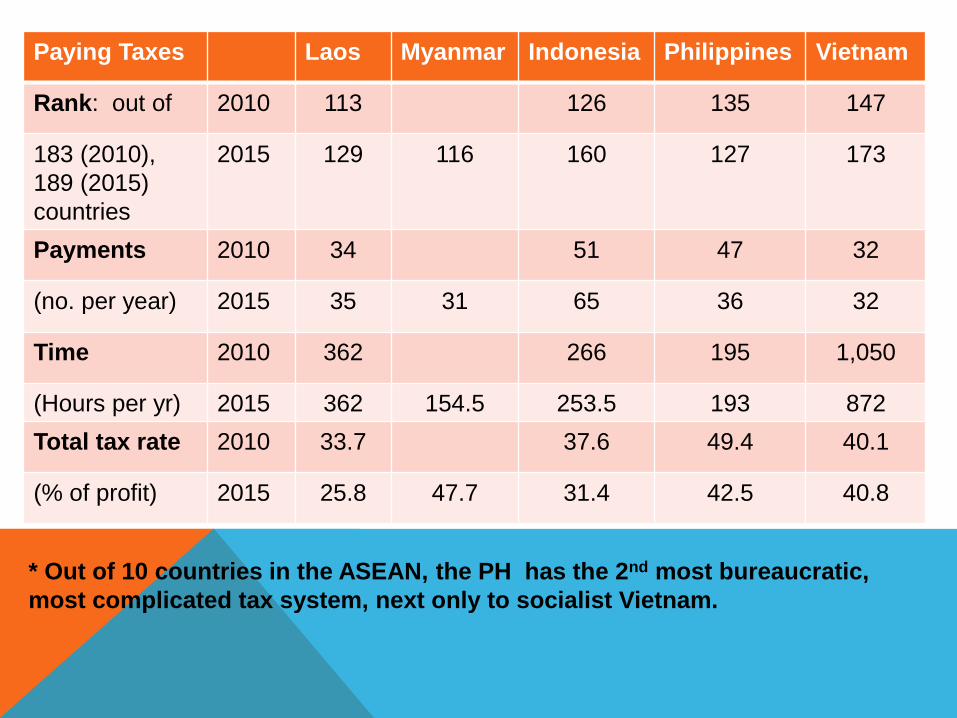

Paying Taxes Laos Myanmar Indonesia Philippines Vietnam

Rank: out of 2010 113 126 135 147

183 (2010),

189 (2015)

countries

2015 129 116 160 127 173

Payments 2010 34 51 47 32

(no. per year) 2015 35 31 65 36 32

Time 2010 362 266 195 1,050

(Hours per yr) 2015 362 154.5 253.5 193 872

Total tax rate 2010 33.7 37.6 49.4 40.1

(% of profit) 2015 25.8 47.7 31.4 42.5 40.8

* Out of 10 countries in the ASEAN, the PH has the 2nd most bureaucratic,

most complicated tax system, next only to socialist Vietnam.

Source: PWC, Paying Taxes (annual reports)

• http://www.pwc.com/gx/en/paying-taxes/assets/paying-taxes-2009.pdf

• http://www.pwc.com/gx/en/paying-taxes/assets/paying-taxes-2012.pdf

• http://www.pwc.com/gx/en/paying-taxes/pdf/pwc-paying-taxes-2015-low-

resolution.pdf

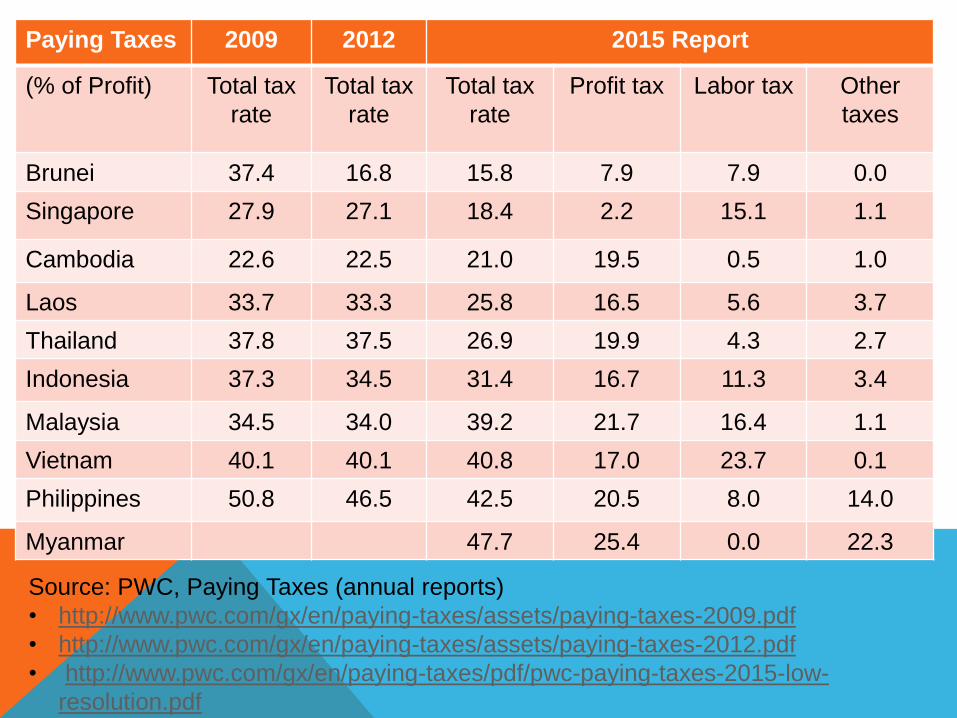

Paying Taxes 2009 2012 2015 Report

(% of Profit) Total tax

rate

Total tax

rate

Total tax

rate

Profit tax Labor tax Other

taxes

Brunei 37.4 16.8 15.8 7.9 7.9 0.0

Singapore 27.9 27.1 18.4 2.2 15.1 1.1

Cambodia 22.6 22.5 21.0 19.5 0.5 1.0

Laos 33.7 33.3 25.8 16.5 5.6 3.7

Thailand 37.8 37.5 26.9 19.9 4.3 2.7

Indonesia 37.3 34.5 31.4 16.7 11.3 3.4

Malaysia 34.5 34.0 39.2 21.7 16.4 1.1

Vietnam 40.1 40.1 40.8 17.0 23.7 0.1

Philippines 50.8 46.5 42.5 20.5 8.0 14.0

Myanmar 47.7 25.4 0.0 22.3

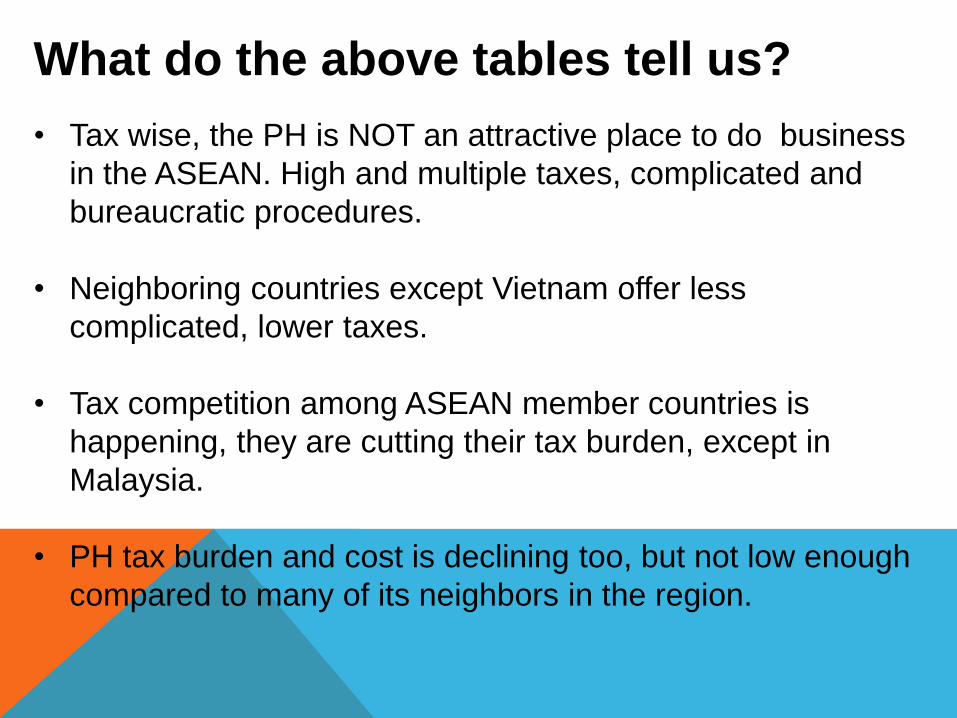

What do the above tables tell us?

• Tax wise, the PH is NOT an attractive place to do business

in the ASEAN. High and multiple taxes, complicated and

bureaucratic procedures.

• Neighboring countries except Vietnam offer less

complicated, lower taxes.

• Tax competition among ASEAN member countries is

happening, they are cutting their tax burden, except in

Malaysia.

• PH tax burden and cost is declining too, but not low enough

compared to many of its neighbors in the region.

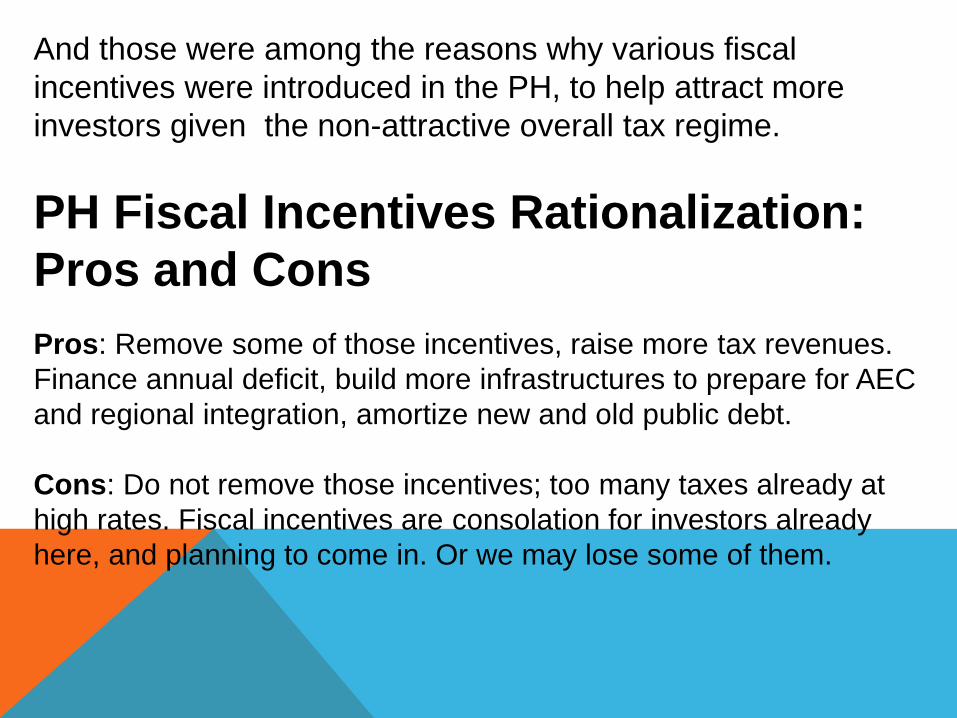

And those were among the reasons why various fiscal

incentives were introduced in the PH, to help attract more

investors given the non-attractive overall tax regime.

PH Fiscal Incentives Rationalization:

Pros and Cons

Pros: Remove some of those incentives, raise more tax revenues.

Finance annual deficit, build more infrastructures to prepare for AEC

and regional integration, amortize new and old public debt.

Cons: Do not remove those incentives; too many taxes already at

high rates. Fiscal incentives are consolation for investors already

here, and planning to come in. Or we may lose some of them.

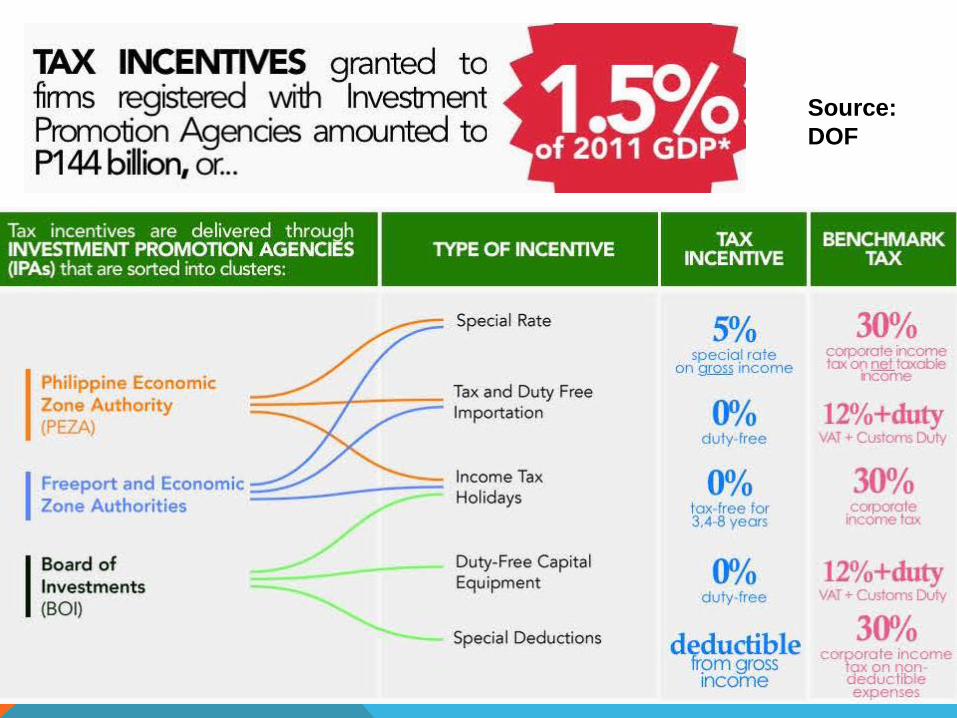

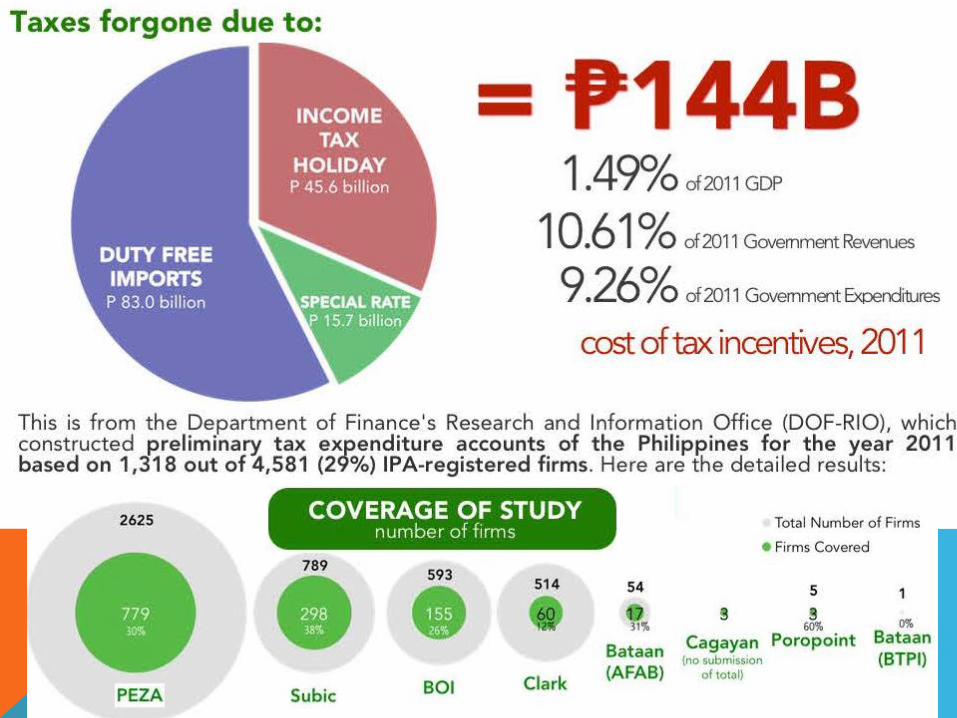

Source:

DOF

“The Aquino administration

wants fiscal incentives

streamlined because these

distort the tax structure of

the Philippine economy and

take away billions of pesos

from government every year

that could be used to

improve the country’s fiscal

position and social services."

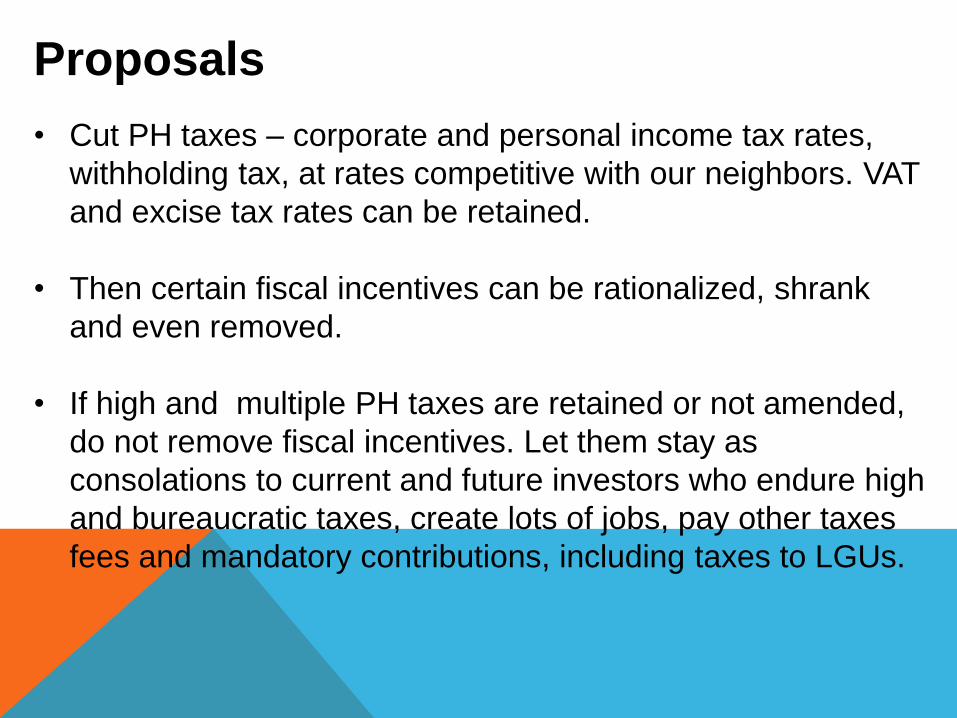

Proposals

• Cut PH taxes – corporate and personal income tax rates,

withholding tax, at rates competitive with our neighbors. VAT

and excise tax rates can be retained.

• Then certain fiscal incentives can be rationalized, shrank

and even removed.

• If high and multiple PH taxes are retained or not amended,

do not remove fiscal incentives. Let them stay as

consolations to current and future investors who endure high

and bureaucratic taxes, create lots of jobs, pay other taxes

fees and mandatory contributions, including taxes to LGUs.

Related Documents