ALABAMA CPA MAGAZINE SEPTEMBER 2014 STATE OF THE SOCIETY

ASCPA September 2014

Apr 03, 2016

Â

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ALABAMA CPA MAGAZINE SEPTEMBER 2014

State of the Society

2 ThE ALABAMA CPA MAGAZINE

The AlAbAmA CPAmAGAZINe

Alabama Society of

Certified Public Accountants

P.O. Box 242987

Montgomery, Alabama 36124-2987

1-800-227-1711

334-834-7650

www.ascpa.org

Officers

Don McCleod, Chair

Dr. Lowell Broom, Chair-Elect

Renee hubbard, Past Chair

BOard Of directOrs

James R. L. Carroll

Caitlin F. Glass

Kate J. ham

Paul Marcus hamilton

M. Buddy Johnsey

Jason L. Miller

Michael C. Reibling

Gregory E. Sellers

Dennis E. Sherrin

Rachel M. Taylor

aicPa cOuncil MeMBers

William h. Carr

Don McCleod

E. Lamar Reeves

Jimmy L. Williamson,

Past Chair, AICPA

The Alabama CPA Magazine is published by

Alabama Society of Certified Public Accountants

as a membership service to Society members.

Views and opinions appearing in this publication

are not necessarily endorsed by the ASCPA. The

deadline for submitting materials for publication is

the first of the month preceding issue date.

Jeannine P. Birmingham, CPA, CAE, CGMA

President and CEO

Diane L. Christy, Editor

message from the Chair...My fellow members of the ASCPA, the state of the Alabama Society of

CPAs is strong. Our investments in some areas continue to perform better than market. Our financial obligations have been consistently paid down and reduced to their lowest levels in years and we have continued to maintain reserves sufficient to meet operational obligations.

Our membership dues continue to rank amongst the lowest of all state societies, and, while CPA membership numbers have remained stable, the number of student members has jumped to its highest level ever. We have added a number of prominent programs over the years to develop our leadership capacity for both the young CPAs as well as the not-so-young CPAs. We have made prudent choices to ensure our sustainability and to enhance our brand image. Indeed, it is a good time for us as the Alabama Society of CPAs.

Nevertheless, there are challenges before us. For example, while we have worked hard to maintain some of the lowest dues amongst professional CPA state societies, we must acknowledge that in an environment of declining market share, our dependency on the largest revenue line item we call CPE cannot be sustained indefinitely.

The increasing pressures from regulatory forces mean that each of us must do our part to support and encourage Jeannine and her staff as they work with great passion to advocate for us when legislative issues arise that threaten our way of life. More so, the existence of new competitive vendors means that each of us must work to challenge ourselves, while encouraging peers and colleagues first choose the ASCPA to fulfill all of our continuing professional educational requirements. The growing complexity of our membership’s interests means that we must support and encourage our board members, our chapter leaders and every stakeholder who is engaged in developing and executing outstanding programs for our membership and for the greater profession at large.

Lastly, the ASCPA has been a positive force for good for more than 95 years because our past leaders have planned every step with great foresight. This is why leadership has once again prepared to face our next great challenge with a simple motto in mind: to protect, to educate and to connect. More of how we plan to protect, educate and connect can be found on our website at ascpa.org. In closing, let me say that as your chairman I believe it is less important how we feel about the changes happening around us, than it is how we act upon those changes that will ultimately shape our great organization, both today and for years to come. I humbly thank you for all that you do.

Don

It’s what CGMA stands for.

A new designation representing accomplished professionals that drive and deliver business success, worldwide.

Find out more at cgma.org

GR WTHCo

pyrig

ht ©

201

2 Am

erica

n In

stitu

te o

f CPA

s. A

ll rig

hts

rese

rved

.

ThE ALABAMA CPA MAGAZINE 3

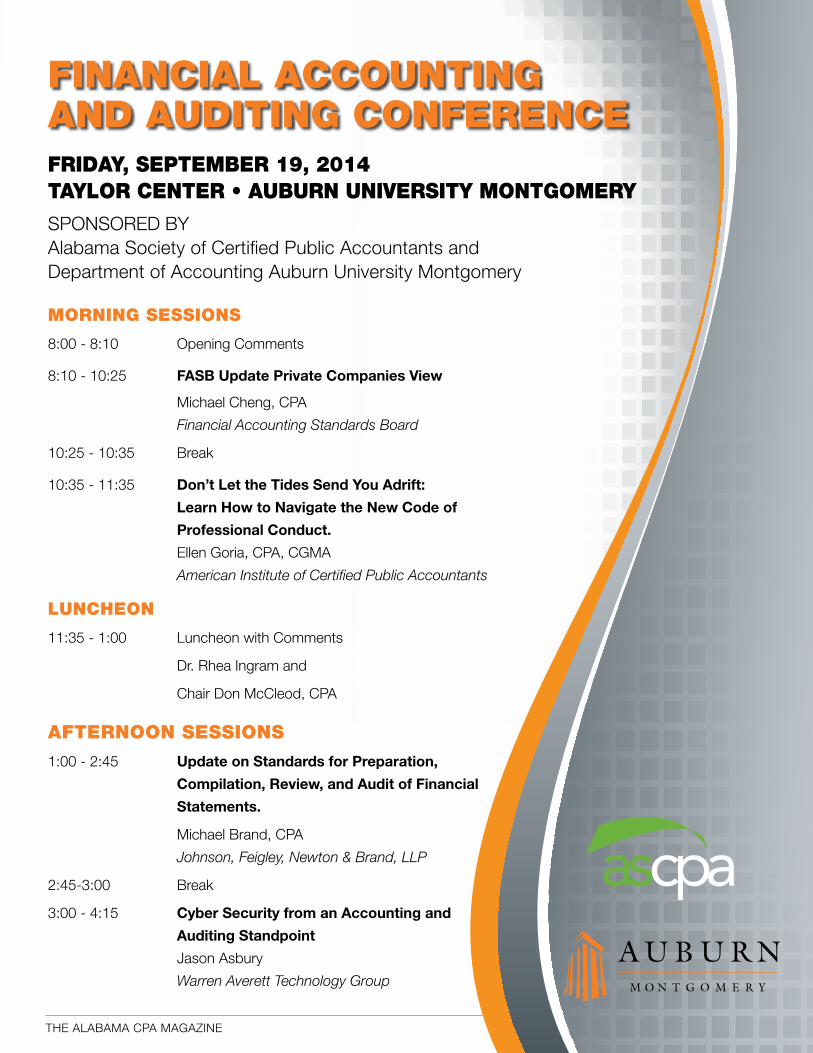

mORNING SeSSIONS

8:00 - 8:10 Opening Comments

8:10 - 10:25 FASB Update Private Companies View

Michael Cheng, CPA

Financial Accounting Standards Board

10:25 - 10:35 Break

10:35 - 11:35 Don’t Let the Tides Send You Adrift:

Learn How to Navigate the New Code of

Professional Conduct.

Ellen Goria, CPA, CGMA

American Institute of Certified Public Accountants

lUNCheON

11:35 - 1:00 Luncheon with Comments

Dr. Rhea Ingram and

Chair Don McCleod, CPA

AFTeRNOON SeSSIONS

1:00 - 2:45 Update on Standards for Preparation,

Compilation, Review, and Audit of Financial

Statements.

Michael Brand, CPA

Johnson, Feigley, Newton & Brand, LLP

2:45-3:00 Break

3:00 - 4:15 Cyber Security from an Accounting and

Auditing Standpoint

Jason Asbury

Warren Averett Technology Group

FINANCIAl ACCOUNTING ANd AUdITING CONFeReNCeFRIdAy, SePTembeR 19, 2014Taylor CenTer • auburn universiTy MonTgoMery

SPONSORED By Alabama Society of Certified Public Accountants and Department of Accounting Auburn University Montgomery

4 ThE ALABAMA CPA MAGAZINE

ThE ALABAMA CPA MAGAZINE 5

TOP TeChNOlOGy TReNdS By Keith Barfield, CPA, CITP

The Gartner Group has released their Top Strategic Technology Trends for 2014 and

it’s a good time to consider the impact of these trends on CPAs and accounting. I ranked the most meaningful and immediate technologies that we are considering at Barfield, Murphy, Shank & Smith and added my observations, both pro and con.

1. Mobile device diversity and management

With 22 million tablet devices already in the market place, this isn’t anything new. The devices are so easy to use, and the apps available are so prolific, that most people have already incorporated these into the workforce. The most widely-discussed problem is the variety of Android versions and capabilities which can create headaches for IT support groups of CPA firms. Some firms have standardized on either Android or Apple and, in my opinion, the Apple operating system reports to be easier to administer. If you have already allowed employees to “bring your own device”, it’s a good idea to focus on your written device usage policies. Let your IT staff research tools to protect and erase firm data contained on everyone’s smart phones and tablets and get them in place.

2. Mobile apps and applicationshey, what’s the difference? I already see lots of competition between mobile apps and applications for lightweight stuff like social media. But for us, tax returns, audits and accounting software are just too complicated to easily run in a mobile app. Do you want to input tax source document numbers on an iPhone? No, you need the speed and comfort of a desktop to make return preparation productive. But what I can foresee is access to information opening up in mobile apps. Think of checking a bank balance; it’s a perfect example. Maybe the next step is a mobile app

looking into the Technology

Crystal ball

developed by your practice management software so you can check your client’s outstanding invoices to your firm, or pull up their latest financial statement on your tablet quickly and easily. Vendors are looking for what you want, so let your voices be heard.

3. The Internet of EverythingI am already seeing the beginnings of this phenomenon. First I saw it in inventory control with companies attaching Radio Frequency Identification Chips (RFID) onto expensive, large construction material sub-assemblies. As costs come down, innovative clients will find new ways to employ this connection to their physical products and assets. The most immediate impact will be at the consumer level. For instance, I use my DirecTV app on my iPhone to record shows that I learn about during the day. est [thermostats which “learn” your preferences]Several of our offices have smart thermostats with motion detectors to determine whether the space is occupied or not; the whole system is controlled remotely by our CIO. A fellow shareholder connects to his Chevy Volt and knows charge status and other statistics by connecting through the internet. As you can see, many things are connected now, but not everything. yet.

4. Hybrid cloud and IT as a service brokerI expect most CPAs have gotten used to the idea of cloud computing and have a pretty good handle on it now. I felt like our first major step into the cloud was implementing XCM’s Accelerated Workflow Automation. It runs in my browser and it’s the first page I open up every morning when I click Internet Explorer. If you have not explored this excellent tool for automating your work flow, seamlessly handled in the cloud, you owe it to yourself to check into it. I felt it gave our firm the reassurance to move our traditional exchange server for email to the cloud utilizing Microsoft Office 365; it’s been another success. So, is it too early to confuse everyone with hybrid cloud?

Like everyone else, I am very sensitive about our hard-earned data files which support all of our tax and audit work. Should I host that in the cloud? What happens to my data if the cloud provider has financial problems and shuts down? On the other hand, can I really compete with top security at a giant like Amazon with scores of security professionals and redundancy options? Maybe, for right now, (since even organizations as large as Target still can’t prevent attacks and penetrations) we will keep our data mostly on-site, try to remain a low profile and be perceived as “not worth hacking”. however, we do have a copy of certain data stored securely in our private extranet to allow clients to access information

easily. So maybe we’re closer to operating on a hybrid cloud than we think!

5. Cloud/client architectureDid we just talk about this? Not exactly. There is a never-ending debate in our world about shifting the processing between the server and the end-user device. In the old mainframe days we called the computers attached “dumb terminals”. The PC changed that and robust applications ran more efficiently on the end-user computers. Then, for security and lock-down purposes, our IT professionals have recently advocated a return to locked-down work stations and return of the processing to a server using tools such as Citrix workstations. It works pretty well in the case of remote employees. But my opinion is that this pendulum swing will never be completely resolved. I think that individual companies will decide where the balance lies based on their corporate culture and philosophy.

6. The era of personal cloudThis is actually exciting to me, but I look at it differently than most. Right now I have 3 small icons on my work computer: Dropbox, Google Drive and MS SkyDrive. All three represent free storage in the cloud. I love the fierce competition that exists among these large companies and results in their extending free limited storage space to me. They seem willing to offer more and more space to dominate this market in order to become the de facto leader. I am secretly hoping that soon online storage will just be free and unlimited. Will I still pay for my Carbonite backup solution? We’ll see.

7. Software-defined anythingThis was least interesting trend to me because it’s just the cloud providers trying to be sure each new one “talks to each other”. Remember those complaints early in your computer career? “My Apple won’t talk to your PC.” The problem is still around and since computing, hardware and storage are becoming a utility, they better get their act together so we don’t have to carry around a pack of European power converters. 8. Smart machinesFinally a solid prediction worth taking note of. This deserves a whole article by itself. Stay tuned.________Keith Barfield is a founding member at Barfield Murphy Shank & Smith and has responsibility for the firm’s information systems. He authors a blog, “Barfield on Tech”, that speaks directly to start-ups and businesses in the technology industry. Barfield was featured in the business advice book CEO Speaks - Sage Advice During Turbulent Times. He often speaks to groups about business consulting, financial statements, organizational planning, and IT topics.

6 ThE ALABAMA CPA MAGAZINE

dOING IT beTTeR

Integrity, objectivity and competence have long been hallmarks of the CPA profession and provide the foundation for CPAs’ reputation in the

marketplace. With accounting issues and the business environment becoming more complex, information-driven and fast-changing, prac-titioners face new challenges in maintaining audit excellence.

To address those challenges, the AICPA has launched the Enhanc-ing Audit Quality (EAQ) initiative, which presents the Institute’s efforts to help auditors of private entity financial statements further improve the quality of the services they provide. Practitioners can give input on those plans by commenting on the AICPA’s newly released discussion paper, Enhancing Audit Quality: Plans and Perspectives for the U.S. CPA Profession. Comments are due November 7, 2014.

Advancing Audit Quality throughout the ProfessionThe discussion paper highlights ways the profession maintains and en-hances audit quality, from establishing requirements for competence, diligence and due care; to setting audit and quality control standards; to administering the Peer Review Program. By summarizing near- and longer-term proposals to continue raising financial statement audit quality, the paper asks for feedback from all parties involved in the audit process of non-public entities. (For purposes of the EAQ, “private enti-ties” refers to all non-SEC registrants, including not-for-profit organiza-tions, employee benefit plans and governmental entities.)

“As they navigate today’s business environment, practitioners are intent on providing high-quality audit services to their clients,” said Jeannine Birmingham. “The profession’s Enhancing Audit Quality initia-tive demonstrates the profession’s continued commitment to quality. It outlines the many areas where stakeholders from our profession’s many constituencies—our own members, peer reviewers, state boards, state societies and regulators—can work together to strengthen audit per-formance.”

EAQ Areas of FocusThe AICPA is looking for input that could help it shape plans and pro-grams proposed by the EAQ effort. The discussion paper poses spe-cific questions through an online community where stakeholders can engage in a productive dialogue. Based on the foundational elements of quality—Competence and Due Care; Standards (Audit and Quality Control); Guidance, Tools, Learning and Resources; and Monitoring and Enforcement—the discussion pa-per proposes significant changes to the following areas, among others:

• Peer Review Program: The AICPA Peer Review Board approved a near-term plan introducing substantial improvements to the current Peer Review Program that range from enhanced peer reviewer quality and in-depth reviews of high-risk industries to improved engagement/firm tracking and more informative review results. In the longer term, an upcoming project will seek to transform the current Peer Review Program into a more real-time practice monitoring system that marries advanced technology and human oversight.

• Auditing and Quality Control Standards: A joint task force con-sisting of representatives from the AICPA’s Auditing Standards Board (ASB), Peer Review Board and others is now gaining stronger insights into audit quality issues. The task force will examine where and how audit concerns occur and their root causes, so appropriate solutions can be explored.

Introducing the Profession’s enhancing Audit Quality Initiative • Evolving the Audit: The AICPA Assurance Services Executive Committee (ASEC) is looking to the future of assurance services and seeking to leverage technology to develop new methodologies that will contribute to a more effective, efficient and timely audit process that will be more relevant to users. ASEC is working to provide insight into the traditional audit approach, how it has evolved and how it might continue to evolve into the future audit.

For More InformationThe AICPA has created an informational webpage, aicpa.org/au-ditquality. This webpage features EAQ-related news and develop-ments, including links to articles and blog posts on AICPA efforts, as well as resources on areas of focus identified by the Peer Review Board. A video featuring AICPA Board Chairman Bill Balhoff, CPA, CFF, CGMA, discussing the EAQ initiative is housed on the site, too. In addition, look for further details from the ASCPA regarding a free AICPA webcast on the EAQ to be held in September.

Your Insights Are Critical you can download, read and provide comments on Enhancing Audit Quality: Plans and Perspectives for the U.S. CPA Profession on the AICPA’s online EAQ Community (aicpa.org/EAQpaper). To comment, you must use your AICPA.org login or create a quick login online. Feedback is due November 7.

CPA APPRECIATION DAY AUBURN FOOTBALL HOMECOMING

Experience a football Saturday on the plains this fall! Bring your group!

(Office colleagues, ASCPA Chapter members, family and friends)

GROUPS OF 15+ RECEIVE BENEFITS INCLUDING: - Group reserved seating

- Prizes via business card drop - Scoreboard Recognition (Groups of 50+)

- Free reserved tailgate spots (Groups of 20+) - Locker room tour (Friday 4-6pm)

Ask about any additional information on Full/Partial Season Tickets as well!!

For tickets please call or email Travis Holtkamp at 334-844-8662 – [email protected]

Auburn vs. Louisiana Tech September 27, 2014

Time: TBD Jordan Hare Stadium Cost - $30 per ticket

*Exclusive Discount for ASCPA Members*

ThE ALABAMA CPA MAGAZINE 7

C H A N G E I S I N E V I T A B L E . D I R E C T I O N I S I N T E N T I O N A L .

PANGEATWO successfully matches clients with talented professionals. Our seasoned understanding of human potential,

including individual strengths, lets us design far-reaching and personalized workforce solutions for employers. Our

experience gives candidates an advantage and creates common ground between companies and professionals.

PANGEATWO is a leader in recruitment and staffing solutions in accounting and financial services. Call today, and we’ll

help you connect talent and potential.

Birmingham, AL 205.444.0080 | Mobile, AL 251.732.3000www.pangeatwo.com

heather melson and Chase Campbell; Audit Supervisor – Taylor martin; Tax Manager – James ezell; Audit Manager – dennis mazingo

blake ethredge, senior accountant at Wilkins Miller hieronymus, has successfully completed the certification process with the Association of Certified Fraud Examiners (ACFE) to earn his designation of Certified Fraud Examiner (CFE). he also holds the certified valuation analyst des-ignation (CVA).

Audit Managers – danielle Carter, Johna-than daniel, Stephen leonard; Tax Man-agers – blake Calloway, Natalie Wilson; Audit Senior Associates – Nolen bevill, lau-ren billings, James Chafin, Natasha Gay, Addie Grissom, Abbay King, Cam-eron Pappas; Tax Senior Associates – Justin detwiler, Kristen lawrence, John lee, Courtney Tibbets

Pearce Bevill Leesburg & Moore announced promotions for their staff: Tax Supervisors –

membeRS IN MOTIONNew Positions and Promotions

Jackson Thornton an-nounced that Allison Guice, ABV, CVA, and ben Wallace have been promoted to senior man-ager. Guice, who joined the firm in 2006, specializes in business valuation. She has served on the steering committee for the Jackson Thornton young Profes-sional’s (JTyP) group since its inception and as trea-surer, vice president, and president of the ASCPA Montgomery Chapter. She currently serves as a mem-ber of the junior board for Child Protect, and on the Montgomery Estate Planning Council Board. Since 2009 she has been a member of the course review committee for the National As-sociation of Certified Valuation Analysts. Guice was recently selected as the 2014 AICPA/AS-CPA Women to Watch - Emerging Leader. She received her undergraduate and graduate de-grees from Auburn University Montgomery.

Ben Wallace joined the firm in 2005, spe-cializes in small business tax and audit. he is a board member and past chairman of the Do-than Area young Professionals, is president of the Dothan Landmarks Foundation, treasurer for the Wiregrass Auburn Club and has served as treasurer for the Dothan Cultural Arts Center. he was recently named one of Dothan Maga-zine’s “Top 40 under 40.” Wallace received his undergraduate and graduate degrees from Au-burn University.

Beason & Nalley, Inc. an-nounced that Casi Posla-jko, CFE, CGFM has been promoted to manager, of the Assurance and Advisory Group. Poslajko provides audit and attest services for government contractors, lo-cal municipalities, employee benefit plans, litiga-tion support, manufacturers and not-for-profit organizations. She earned her accounting and master of accountancy degrees from Auburn University. She is a member of the AICPA, Ac-counting and Financial Women’s Alliance, As-sociation of Certified Fraud Examiners and Association of Governmental Accoun-tants.

Sellers Richardson holman & West has made follow-ing promotions: Tax Senior Manager – ben leaver; Ben Leaver

Allison Guice

Casi Poslajko

Blake Calloway James Ezell

Danielle Carter Heather Melson Chase Campbell

Dennis Mazingo

Johnathan Daniel

Natalie Wilson Taylor Martin

Stephen Leonarad

Ben Wallace

8 ThE ALABAMA CPA MAGAZINE

dOING IT beTTeR

When it comes to the Affordable Care Act (ACA), the employer shared responsibility

provisions remain top of mind for many small business owners. Paychex has been helping employers answer these questions and prepare for the changes. Through this process, Paychex has identified the top three questions and the answers to each.

When do the Employer Shared Responsi-bility (ESR) provisions go into effect?• Originally set to take effect January 1, 2014,

the U.S. Treasury Department announced a one-year delay in the enforcement of the ESR provisions in July of 2013. Final guidance, released February 10, 2014, gave an additional year of transition relief from penalty assessments to certain employers.

For employers with 100 or more full-time employees, including full-time equivalent employees (FTEs), enforcement begins January 1, 2015. For qualified employers with 50 to 99 full-time and FTE employees, the assessment of penalties has been delayed until 2016.

• To qualify for this transition relief, these employers must meet certain conditions. They must not reduce workforce size or hours after February 9, 2014 to stay under the 100-employee threshold. They must not eliminate or materially reduce health coverage offered as of February 9, 2014, and they must certify they met qualifications for this relief in IRC §6056 ESR reporting.

• If they don’t qualify, they will be treated the same as employers with 100 or more full-time and FTE employees and may be subject to penalties beginning in January 2015.

For ESR, what is required to be reported to the Internal Revenue Service (IRS)?• As part of the final guidance released by the

Treasury Department on ESR end-of-year reporting, applicable large employers (ALEs) subject to ESR will be required to provide information as to whether they offered full-time employees and their family members the opportunity to enroll in insurance that provides minimum essential coverage.

• Forms 1094-C and 1095-C must be filed by the employer with the IRS. Additionally, employers must provide Forms 1095-C to their full-time employees, similar to how Forms W-2 are provided.

• Simplified reporting methods are available under certain circumstances. One of these

Employer Shared Responsibility: Top Three Questions from Small Business Owners

• ALEs must provide Forms 1095-C and employee statements to full-time employees on or before January 31, following the end of the calendar year for which the statements apply.

Paychex professionals in the areas of health insurance, risk and compliance are keeping a close eye on the implementation of the ACA and will continue helping business owners navigate the changes. For more information about the latest provisions of the Affordable Care Act and how Paychex can help, please visit www.paychex.com/health-reform.

Navigating health Care Reform with a PeOMore than ever before, companies are outsourcing in order to cut costs and improve efficiency. And it’s not just in production areas, but also in human resources and payroll. There are many reasons for small and mid-sized businesses to use a Professional Employer Organization (PEO) to handle some tasks associated with human resource (hR) management, employee benefits administration, compliance assistance with state and federal laws and regulations, and more. In today’s climate of health care reform it is crucial to analyze whether a PEO maybe right for your client’s company in order to remain compliant with new regulations.

A PEO is a co-employment model where the workforce of a small or mid-sized business becomes a part of a larger benefits and administrative employment group. A PEO allows employees of many companies to adopt large group benefit plans in order to negotiate better rates for all of its members. PEOs specialize in hR management and offer businesses a wide variety of services, including support with employee benefits administration, payroll processing, tax filing, and risk management, which are all tasks that maybe affected by a company’s compliance with applicable laws and regulations.

In this co-employment arrangement, business owners manage their workforce and the day-to-day operations of their business while the PEO takes over some of the hR and payroll-related responsibilities. This, in turn, allows business owners to run their businesses while also providing the very best benefits to their employees. Under this model, there are many advantages, the most important of which is freeing management resources so that they can be focused on employment productivity. A PEO doesn’t just potentially save companies money, but it may also indirectly provide them with more resources to enhance overall profitability.

By aligning with a PEO, a business owner may be able to:

• Gain access to the PEOs broader benefit options, including medical, dental, vision, life, disability, and workers’ compensation insurance, 401(k) plans, and consumer-related health plans such as Flexible Spending Accounts (FSAs) and health Savings Accounts (hSAs).

• Establish support systems without having to invest in specialized personnel or additional technology.

• Get help with all facets of the “employment life cycle”, from hiring and firing employees to job descriptions, employee handbooks, employee retention tools and strategies.

• Contact a trained HR representative for assistance, access employee and management training, speak with safety and risk professionals, and obtain state and federal tax filing services, payroll processing, and other employee-related services (e.g. employee screening and compensation surveys).

PEOs can also help companies navigate the complexities of health care reform. It can guide business owners through the hCR process and offer many solutions to keep them compliant. In addition, government marketplaces will only be providing medial and stand-alone dental benefits. Those companies wanting a full suite of benefit plans will either have to find other independent solutions, or enjoy access to the benefit plans offered by a PEO.

While small businesses sometimes find it difficult to offer their employees multiple benefits options. PEOs help solve this problem by making it easier to provide benefits. By offering benefit plans, small businesses may become better able to attract high-caliber employees and improve employee retention.

methods is designed for employers with 50 to 99 full-time employees to allow them to certify that they qualify for ESR transition relief in 2015 and some months in 2016 in certain cases.

When do employers subject to ESR reporting requirements need to file information with the IRS?• Small business owners need to file Forms

1094-C and 1095-C with the IRS each year, no later than February 28, or if filing electronically, by March 31 following the end of the calendar year for which the return applies.

ThE ALABAMA CPA MAGAZINE 9

Pay it Forward Classroom blitz Continues in 2014Also on the agenda of the young CPA board was the decision to move ahead

with Pay it Forward in 2014. The program has been enormously successful. In the past 6 years more than 20,000 middle and high school students have heard a financial education presentation from an Alabama Society young CPA. The speakers have shared their stories of becoming a CPA as well as discussed the use of credit or the difference between good debt and bad debt. In spring 2013 the Alabama State Department of Education adopted a graduation requirement which included financial literacy and career awareness components. The value of the young CPAs as a consistent resource received even more notice – and appreciation – from the ALSDE.

Last year the young CPAs elected to have an entire week dedicated to Pay it Forward, making it possible for schools and volunteers to be more flexible in their timing. This year the week of November 17-21 has been chosen. Keep an eye out for more information as schools sign up in September and October.

The young CPAs met on Friday, Au-gust 22 to set the course for the next

year. The inspiration for strategic plan-ning by sticky note came from Maryland Association of CPAs’ Executive Director Tom hood, CPA. he declared that 2014 was “The year of the Sticky Note” for the MACPA in their video holiday card.

President of the yCPA Board James Wishon was immediately on board with the concept and the entire board jumped in to make the following determination: how can the ASCPA respond to the needs of younger professionals and in-volve them in Society programs?

The markers raced over the surface of the giant sticky notes, as attendees brainstormed ideas. At several points the participants were reminded that time was passing, but their concentration was so intense that the meeting extended. Board members concluded that there were three areas of interest to them:

• Filling the talent pipeline and integrating new staff into the profession.

• Advocacy in both legislative and regula-tory matters; becoming part of the pro-cess.

• Learning and development which is tailored to young CPAs.

Their suggestions and concerns were passed along to the Society’s Board of Directors, as well as ASCPA staff, to consider when planning programs and activities. S O L U T I O N S

Every position has its own set of expertise, challenges and goals.Whether it’s shortstop or baseman, you have to play to your strengths,but this isn’t a one-man sport and we understand the essence of teamwork.

We believe that when you connect the right person to the right joband the right individual to the right company, it’s like a hand in glove. We’re here to help you find that ideal person to play on the team, and to make sure they can help the team PERFORM FOR SUCCESS.

www.itacsolutions.comTECHNOLOGY | CORPORATE PROFESSIONAL/CLERICAL

GOVERNMENT/ENGINEERING | ACCOUNTING/FINANCE Providing temporary/contract, contract-to-hire, and direct hire staffing solutions.

Birmingham | Mobile | Huntsville | Nashville

L O O K I N G F O R A T E A M P L A Y E R ?

management by Sticky Notes YOUNG CPAS PLAN

FOr 2014/15

reception

Text Box

ThE ALABAMA CPA MAGAZINE 11

meSSAGe FROm The PReSIdeNT

The Alabama Society of CPAs: Another fantastic year to report. We often say how quickly time goes by; the to-do list is long

and the plate is full, but what a wonderful problem to have. your dedicated ASCPA team works hard on your behalf and never takes for granted the status quo. During the 2013-14 year, we continued

to set the bar high for many of our existing programs while introducing a new program or two along the way. Starting in June 2013 we were fortunate to be able to work with the American Institute of CPAs to host the annual Accounting Scholars Leadership Workshop. Twenty-seven minority students from across the southern tier of our country spent two days at the ASCPA learning all things linked

to the accounting profession. The students were wonderful to work with and were a true inspiration. They were engaged, professional, interested and very diverse; a beautiful blend of the future generation CPAs.

2013-14 also saw the largest class of participants in the ASCPA Leadership Academy. We had 33 talented young leaders not only from Alabama but from five other states and Canada. The excitement and energy in Class III was amazing. Our facilitators continue to talk about how great the Alabama program is and how much talent there is in class participants. Academy graduates are encouraged to join an ASCPA chapter or committee as a leader, to consider service on the ASCPA board or to volunteer for a national (AICPA) committee. ASCPA hopes that firms and companies will continue to support young professionals to participate in the academy and to remain engaged in the profession’s many efforts.

Legislation was another priority for the ASCPA this year. We were successful in passing an amendment to the Alabama Uniform Accountancy Act that further defined attest. As certified public accountants, we are the only profession that is authorized, by law, to perform audits of financial statements. however, CPAs provide a wide range of services and are being asked to provide assurance services on entirely new types of engagements. As such, we successfully passed legislation that amended the UAA to include all engagements performed under Statements on Standards for Attestation Engagements (SSAEs) not just examinations of prospective financial information. The ASCPA also helped other business associations see the Taxpayer Bill of Rights (Alabama Taxpayer Fairness Act) to final passage. This bill creates the Alabama Tax Tribunal, an independent newly-formed state agency under the executive branch.

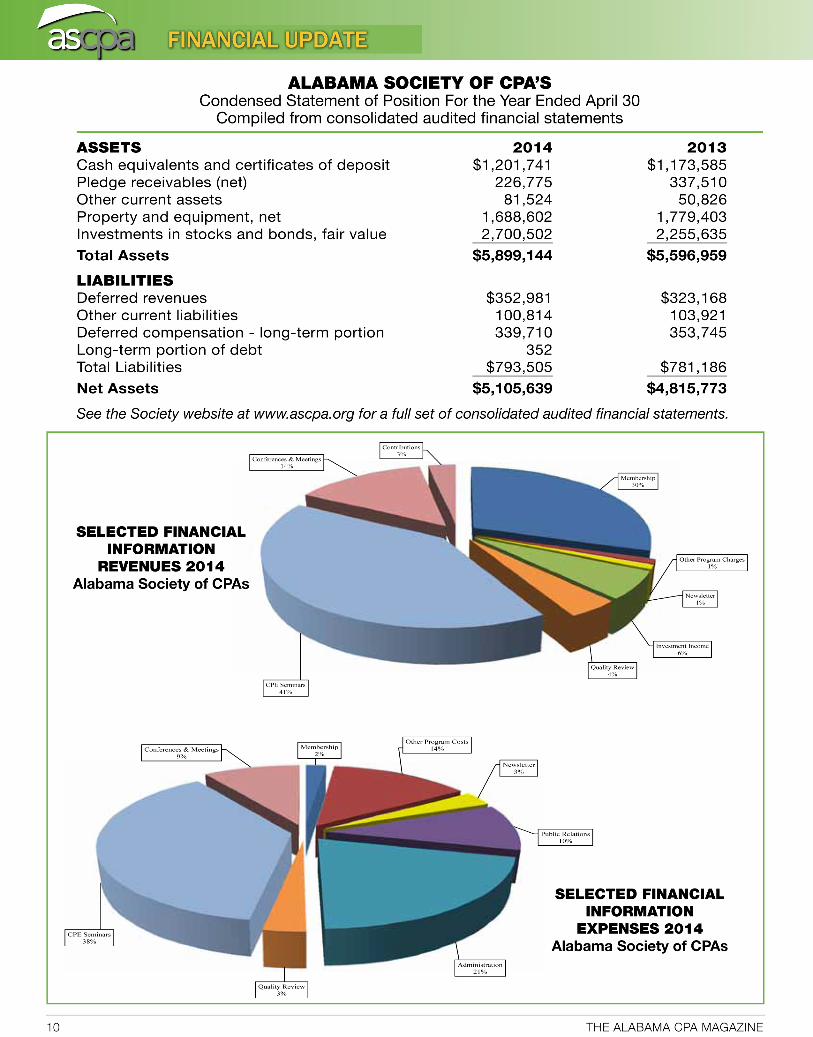

Financially, the ASCPA remains sound; condensed financials are provided on the previous page for you review. you may request a copy of the complete financial statements consolidated with the Alabama CPA PAC, chapters and Educational Foundation. Aldridge Borden & Company of Montgomery is the independent audit firm.

So what is next for the profession and the ASCPA? We are engaged with national task force groups related to the Future of Learning (future of CPE) and Enhanced Audit Quality. Specific to education, we are in the throes of studying how to reinvent classrooms, rethink development models and transition from traditional measurement of continuing education by hours into achieved competencies. The overarching goal is to give CPAs readily accessible education and resources that strengthen their performance and reflect the many ways in which we learn. There will be more to come on this comprehensive project, the future of learning, and how state societies will embrace a radical, professional education shift.

Enhanced Audit Quality presents an entirely new set of challenges for the profession. The accounting profession has a long history of providing high-quality services that protect the public interest. however, based on information from peer reviews, audit concerns sometimes arise from inadequate education or training, noncompliance with certain auditing or control standards, or a lack of experience in specialized areas such as ERISA or Government Audit Standards. Consequently, the profession now has an opportunity to further boost audit quality; with the initiative coming in two phases. The white paper for phase one has been published and is open for comment until November 7, 2014. I hope you will take the opportunity to read and make comments.

If you want to learn more about the Future of Learning project, visit http://futureoflearning.aicpa.org, or if you would like to learn more and provide feedback for the current white paper on audit quality, visit http://aicpa.org/EAQpaper.

“Greatness, it turns out, is largely a matter of conscious choice and discipline.” This quote by Jim Collins, Good to Great, inspires me. It is my passion to serve Alabama CPAs and move our professional organization to something beyond great. I am (you are) fortunate to have an exceptional ASCPA board of directors who are driven to move our state society forward. The directors make dedicated decisions to engage in conversations and to address sometimes difficult issues affecting our future. I hope you will join me in thanking each of them for their commitment and service to the ASCPA.

Jeannine Birmingham

ASCPA hopes that firms and companies will continue to support young professionals to participate in the academy and to remain

engaged in the profession’s many efforts.

12 ThE ALABAMA CPA MAGAZINE

STUdeNT SUCCeSS

In a continuing effort to expand both the breadth and the effectiveness of the Alabama Society’s student

outreach, the ASCPA has become a professional partner of Beta Alpha Psi. This membership will provide access to a whole range of activities with the organization, including invitations to regional and national events. The ASCPA becomes BAP’s ninth state society partner.

Professional Partner Member Benefits/Opportunities• Participation in at least two regional meetings

– Only professional partner members are allowed to present or moderate a professional session and/or judge an event. Provides direct interaction with students and increases company/firm recognition. Over 1,700 students and professors attend the 9 regional meetings.

– State CPA Societies participate in regional meetings associated with their state

• Participation at BAP Annual Meeting

– Only professional partner members are allowed to present or moderate a professional session and/or judge an event. Professional partners are permitted to reach out to their organization’s network to help identify professional session speakers. Provides direct interaction with students and increases company recognition. Over 1,200 students and professors attend the annual meeting.

– Several sessions at the annual meeting are for professors only and allow professional partner members to have direct interaction with faculty advisors.

• Website recognition and link to state society site.

• Right of first refusal for annual meeting sponsorship opportunities.

• Recognition in BAP Annual Report and BAP Annual Meeting Program.

• Recognition from the podium and onscreen at the annual meeting and regional meetings as well as on table tent card.

Attend joint meeting with the board of directors at the annual meeting to provide advice and input regarding the direction of the organization.

This partnership will further enhance the relationship of the ASCPA with the six Beta Alpha Psi chapters: University of Alabama, University of Alabama in huntsville, University of South Alabama, Auburn University, Samford, and University of Alabama at Birmingham.

beTA AlPhA PSIThe International Honor Organization for Financial Information Students and Professionals

2015 Student Guide to Accounting Firms in Alabama

A Society resource to help you recruit and hire future staff!ASCPA is preparing the 2015 Student Guide to Accounting Firms in Alabama. More than 2000 are shared each year, giving students and educators a snapshot of firms around the state. It is a unique chance to attract interest and to promote your firm.

Fees are $100 for a listing in the guide, $500 for a listing plus full page ad on the facing page.

Complete the following information regarding your firm. Scan and email your completed form to Diane Christy, [email protected]. your PAyMENT AND COMPLETED FORM must be submitted by Friday, November 1 for inclusion in the 2015 Student Guide. Copies of the completed guide will be sent to your firm after publication in December.

Firm Name: ______________________________________________________________

Firm Address: ____________________________________________________________

City: ___________________________ State: __________ ZIP Code:_________________

Firm Contact: ____________________________________________________________

E-mail Address: __________________________________________________________

Phone: ______________________________ Fax: _______________________________

Website: ________________________________________________________________

Does your firm have additional offices in other cities, if so where? ________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Total Staff Size: ________ Number of CPAs: ________ Number of Partners: ________

Does your firm offer internships? _______________ Paid or Unpaid? _____________

Does your firm hire for entry-level positions? ______________

Does your firm offer assistance in preparing for the CPA exam? __________________

Is overtime required? ______________________________________________________

Is overnight travel required? ________________________________________________

Does your firm cover the cost of:

Licensing and renewals? _____________________

Membership fees in professional organizations? _____________________

Continuing Professional Education (CPE)? _____________________

p Full page firm listing - $100

p Full page firm listing plus full page ad - $500

Deadline: November 1

ThE ALABAMA CPA MAGAZINE 13

STUdeNT SUCCeSS

Thank you, Fortune Forward

donors!It takes a village, sometimes several villages, to get students fully launched on their careers. The ASCPA is proud to have among the people in its village, generous donors who made $50,000 contributions to the 2011 Fortune Forward campaign. Their willingness to make such an enormous commitment meant that scholarships were named in their honor. These are the recipients of this year’s named scholarships.

Barranco Family Foundation Abigail Missildine Auburn University

Birmingham Chapter Alexis Johnson University of Alabama at Birmingham

Carr Riggs & Ingram Melissa Williams Troy University

Jackson Thornton Shirin Torabinejad huntingdon College

Kassouf & Co. Stephanie howe University of Montevallo

Warren Averett/Wilson Price Jacob Abernathy University of South Alabama

take off the tRaiNiNG WheeLS!Speed your way to the 7th annual

aScPa educator conferenceFriday, october 10, 2014 • 10:00-3:00

9:00-10:00 Registration

10:00-10:10 Welcome Gregory Carnes, Dean, College of Business

University of North Alabama Chair, Education Committee

10:10-11:25 HealthSouth: The Accounting Behind the Fraud Bill Owens, Consultant and Public Speaker

Former CFO, healthSouth

11:25-12:15 Lunch

12:15-1:15 An Update on the Accounting Pilot & Bridge Project: An AP Course for Accounting Madge Gregg, Finance Academy Director, hoover City Schools

1:15 – 1:30 Break

1:30 – 3:00 Fraud Analytics: The Use of Excel and Access Dr. Tina Loraas, Associate Professor of Accounting

Auburn University

3:00 Closing remarks

Eligible for 4.5 hours of A&A credit • $100 • Go to www.ascpa.org to register.

14 ThE ALABAMA CPA MAGAZINE

Feeling Overwhelmed By The Challenge Of Payroll?

Take control of complex payroll needs for yourself or your clients with Microsoft Dynamics GP Payroll.

The powerful Payroll solution (with or without Human Resources) can stand alone to give you a payroll system that assures control,

compliance and accuracy for 10 to 10,000 employees.Microsoft Dynamics GP Payroll can interface with

most accounting systems. And, for a lot less than you think!

Tips

Overtime

401(k)

Payroll Direct DepositAudit Trails

Electronic Tax Filing

Compliance

Payroll Accuracy

W-2s Security

Shift Differentials

Section 125 DeductionsSUTA

Bank Reconciliation

Paid Time Off New Hires

Human Resources

1128 22nd Street South Birmingham, AL 35205

www.kianoff.com

Implementing and Supporting Human Resources & Payroll Solutions Since 1986

Positive Pay

For a free needs analysis to see if Microsoft Dynamics GP Payroll can be your payroll solution, call us at 205-592-9990 or toll-free 1-866-KIANOFF or e-mail: [email protected]

Complex Overtime Rules

ThE ALABAMA CPA MAGAZINE 15

When you sit down with a client, you strive to see their business from their perspective and make recommendations based on their unique situation. We operate similarly.Whether your CPA firm is a one person operation or national in scope, the AICPA Professional Liability Insurance Program offers insurance products and solutions designed to fit your needs.

• Insurance created to cover the unique exposures of CPA firms• Premium credits designed to reflect the way CPAs do business• Quality coverage at a price that fits your budget

Please call Robert Albertini at Aon Insurance Services at 800.221.3023 or visit www.cpai.com/premierad today!

Aon Insurance Services is the brand name for the brokerage and program administration operations of Affinity Insurance Services, Inc. (AR 244489); in CA and MN, AIS Affinity Insurance Agency, Inc. (CA 0795465); in OK, AIS Affinity Insurance Services Inc.; in CA, Aon Affinity Insurance Services, Inc. (0G94493), Aon Direct Insurance Administrator and Berkely Insurance Agency; and in NY, AIS Affinity Insurance Agency.

One or more of the CNA companies provide the products and/or services described. The information is intended to present a general overview for illustrative purposes only. It is not intended to constitute a binding contract. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products and services may not be available in all states and may be subject to change without notice. The statements, analyses and opinions expressed in this publication are those of the respective authors and may not necessarily reflect those of any third parties including the CNA companies. CNA is a registered trademark of CNA FinancialCorporation. Copyright © 2014 CNA. All rights reserved. E-10486-714 AL

Administered by:Underwritten by:Endorsed by:

More than 25,000 CPA firms depend on the AICPA Professional Liability Insurance Program.

The AICPA Professional Liability Insurance Program

looks at insurance from a fresh perspective… YOURS

E-10486-714 AL.indd 1 5/21/14 4:47 PM

16 ThE ALABAMA CPA MAGAZINE

ThE ALABAMA CPA MAGAZINE 17

Marketing is still a fairly new concept for firms. In the minds of most, marketing is

a task of overwhelming proportions. however, it doesn’t have to be. Like anything else, it will take time to get up the marketing learning curve, but no one says you can’t ascend at your own pace.

Like anything else that is unfamiliar, developing a marketing program can be scary. But break it down into management chunks, and it becomes less intimidating. The key is to keep moving forward, continue to ask questions and educate yourself, and set a pace that is comfortable. you don’t have to launch a full marketing program from Day 1. It’s best to take it slowly.

The following are starter initiatives that you can take on to get your marketing program off the ground. Nothing major…and each can happen in good time.

launching Your Marketing Programyou know you want to move forward with

marketing efforts. But like many firm leaders, you don’t know where to start. Make it easy on yourself (and your staff) by focusing on a few activities and slowly growing your program as you become more comfortable. Rest assured that you will eventually fall into your marketing groove. Then before you know it…you’re a marketing sage.

Identify a Marketing Gatekeeper – you’ve got a lot to do, so if you can hand over marketing tasks to a reliable staff member, do it. This person will oversee all marketing initiatives and ensure that the program stays running and on course. your gatekeeper will also keep you informed of campaigns and seek your advice on messaging when needed, but ultimately will be responsible for broad program operation. Look around your office for your gatekeeper. you may be surprised at the creative folks that will want to take this on.

Start Your Plan—A marketing plan provides a blueprint of what tasks need to be accomplished and the proper timeframe for each—keeping you on track and your marketing goals realistic. The plan doesn’t have to be comprehensive, you just have to get something down on paper. For example, create a spreadsheet divided into quarters (Q1-Q4), and then begin to populate the plan with marketing initiatives you would like to accomplish. Start slowly…perhaps one campaign per quarter. Over time, and as you add initiatives, you will start to see an organized plan come together.

Build an Arsenal of Marketing Collateral —It’s difficult to run a marketing program if you

dOING IT beTTeR

marketing at a Pace you Can handledon’t have the proper marketing resources to support it. you can talk all day about what you offer, but eventually a prospect will request follow-up information, such as a brochure, services fact sheet, or a link to your website. Evaluate all the collateral you have on hand (which includes your website) and ask yourself: 1) Does it support my brand? Is it professional looking, well written, and up-to-date? What additional pieces do I need? Be sure that you have the proper marketing collateral in stock before you hit the streets.

Launch that First Campaign—Don’t be scared of hitting the ground running with a few small marketing campaigns. As long as you research your audience and create the right message, there is little that can go wrong. Just ask a few simple questions up front: Who is my audience? Am I communicating to clients or prospects? Am I targeting a specific niche (e.g., dentists)? Once you have all this, create your communication and hit Send!

These steps represent the big rocks of a sound marketing program. Starting with a few manageable tasks helps ease you into marketing and sets the stage for a full program roll out down the road.

Approach marketing slowly to mitigate frustration for both you and your staff. Learning how to run a marketing program by taking small steps allows everyone ample time to absorb new information and processes. It’s also much easier to identify and correct issues when your program is small and confined, opposed to launching a full-scale plan from the get-go. Most importantly, you are far less likely to abandon marketing efforts all together if you take it slow. When people feel overwhelmed, it’s human nature to retreat and avoid. Don’t let that happen. Roll out your program in increments and learn at a pace that is comfortable. you’ll see…you will move from “walk” to “run” mode in no time._____About the Author: Kristy Short, Ed.D, is partner and chief marketing officer at rootWorks (rootWorks.com) and president of rwc360 (rwc360.com)—firms dedicated to providing practice management education, branding, marketing, and public relations services to the accounting profession. She is also a professor of English and marketing. reach her at [email protected].

By Kristy Short, Ed.D

18 ThE ALABAMA CPA MAGAZINE

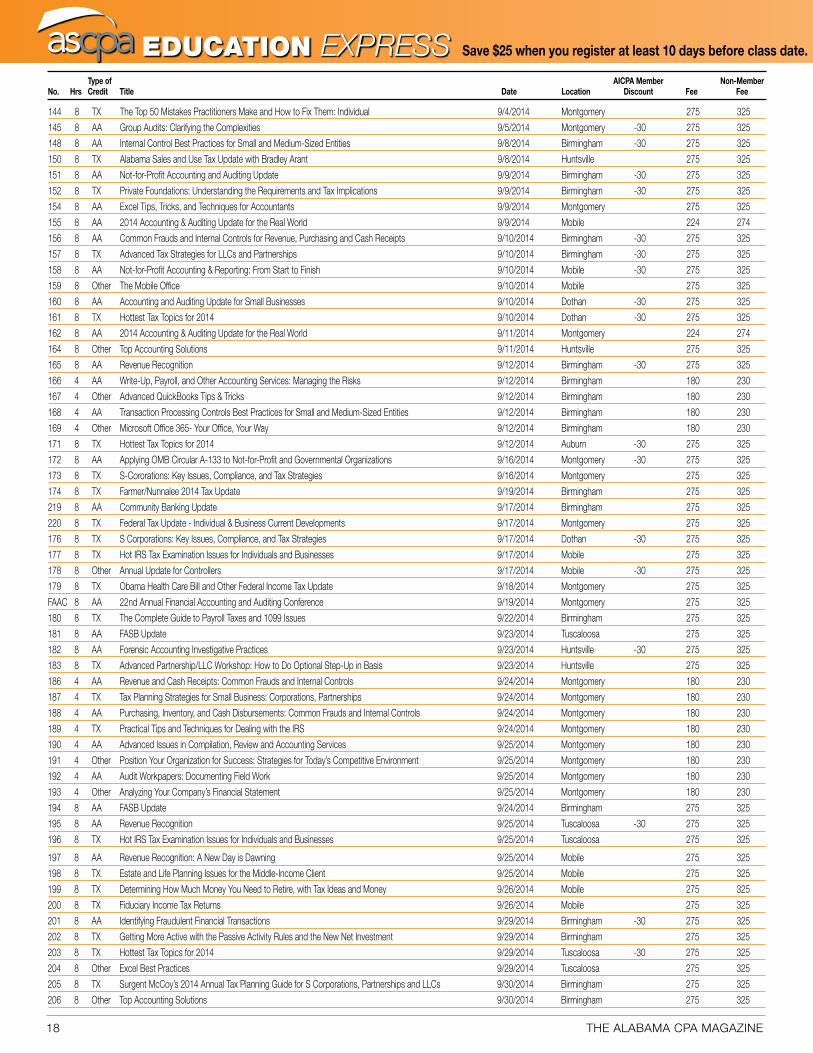

edUCATION ExPrESS Save $25 when you register at least 10 days before class date.

144 8 TX The Top 50 Mistakes Practitioners Make and how to Fix Them: Individual 9/4/2014 Montgomery 275 325

145 8 AA Group Audits: Clarifying the Complexities 9/5/2014 Montgomery -30 275 325

148 8 AA Internal Control Best Practices for Small and Medium-Sized Entities 9/8/2014 Birmingham -30 275 325

150 8 TX Alabama Sales and Use Tax Update with Bradley Arant 9/8/2014 huntsville 275 325

151 8 AA Not-for-Profit Accounting and Auditing Update 9/9/2014 Birmingham -30 275 325

152 8 TX Private Foundations: Understanding the Requirements and Tax Implications 9/9/2014 Birmingham -30 275 325

154 8 AA Excel Tips, Tricks, and Techniques for Accountants 9/9/2014 Montgomery 275 325

155 8 AA 2014 Accounting & Auditing Update for the Real World 9/9/2014 Mobile 224 274

156 8 AA Common Frauds and Internal Controls for Revenue, Purchasing and Cash Receipts 9/10/2014 Birmingham -30 275 325

157 8 TX Advanced Tax Strategies for LLCs and Partnerships 9/10/2014 Birmingham -30 275 325

158 8 AA Not-for-Profit Accounting & Reporting: From Start to Finish 9/10/2014 Mobile -30 275 325

159 8 Other The Mobile Office 9/10/2014 Mobile 275 325

160 8 AA Accounting and Auditing Update for Small Businesses 9/10/2014 Dothan -30 275 325

161 8 TX hottest Tax Topics for 2014 9/10/2014 Dothan -30 275 325

162 8 AA 2014 Accounting & Auditing Update for the Real World 9/11/2014 Montgomery 224 274

164 8 Other Top Accounting Solutions 9/11/2014 huntsville 275 325

165 8 AA Revenue Recognition 9/12/2014 Birmingham -30 275 325

166 4 AA Write-Up, Payroll, and Other Accounting Services: Managing the Risks 9/12/2014 Birmingham 180 230

167 4 Other Advanced QuickBooks Tips & Tricks 9/12/2014 Birmingham 180 230

168 4 AA Transaction Processing Controls Best Practices for Small and Medium-Sized Entities 9/12/2014 Birmingham 180 230

169 4 Other Microsoft Office 365- your Office, your Way 9/12/2014 Birmingham 180 230

171 8 TX hottest Tax Topics for 2014 9/12/2014 Auburn -30 275 325

172 8 AA Applying OMB Circular A-133 to Not-for-Profit and Governmental Organizations 9/16/2014 Montgomery -30 275 325

173 8 TX S-Cororations: Key Issues, Compliance, and Tax Strategies 9/16/2014 Montgomery 275 325

174 8 TX Farmer/Nunnalee 2014 Tax Update 9/19/2014 Birmingham 275 325

219 8 AA Community Banking Update 9/17/2014 Birmingham 275 325

220 8 TX Federal Tax Update - Individual & Business Current Developments 9/17/2014 Montgomery 275 325

176 8 TX S Corporations: Key Issues, Compliance, and Tax Strategies 9/17/2014 Dothan -30 275 325

177 8 TX hot IRS Tax Examination Issues for Individuals and Businesses 9/17/2014 Mobile 275 325

178 8 Other Annual Update for Controllers 9/17/2014 Mobile -30 275 325

179 8 TX Obama health Care Bill and Other Federal Income Tax Update 9/18/2014 Montgomery 275 325

FAAC 8 AA 22nd Annual Financial Accounting and Auditing Conference 9/19/2014 Montgomery 275 325

180 8 TX The Complete Guide to Payroll Taxes and 1099 Issues 9/22/2014 Birmingham 275 325

181 8 AA FASB Update 9/23/2014 Tuscaloosa 275 325

182 8 AA Forensic Accounting Investigative Practices 9/23/2014 huntsville -30 275 325

183 8 TX Advanced Partnership/LLC Workshop: how to Do Optional Step-Up in Basis 9/23/2014 huntsville 275 325

186 4 AA Revenue and Cash Receipts: Common Frauds and Internal Controls 9/24/2014 Montgomery 180 230

187 4 TX Tax Planning Strategies for Small Business: Corporations, Partnerships 9/24/2014 Montgomery 180 230

188 4 AA Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal Controls 9/24/2014 Montgomery 180 230

189 4 TX Practical Tips and Techniques for Dealing with the IRS 9/24/2014 Montgomery 180 230

190 4 AA Advanced Issues in Compilation, Review and Accounting Services 9/25/2014 Montgomery 180 230

191 4 Other Position your Organization for Success: Strategies for Today’s Competitive Environment 9/25/2014 Montgomery 180 230

192 4 AA Audit Workpapers: Documenting Field Work 9/25/2014 Montgomery 180 230

193 4 Other Analyzing your Company’s Financial Statement 9/25/2014 Montgomery 180 230

194 8 AA FASB Update 9/24/2014 Birmingham 275 325

195 8 AA Revenue Recognition 9/25/2014 Tuscaloosa -30 275 325

196 8 TX hot IRS Tax Examination Issues for Individuals and Businesses 9/25/2014 Tuscaloosa 275 325

197 8 AA Revenue Recognition: A New Day is Dawning 9/25/2014 Mobile 275 325

198 8 TX Estate and Life Planning Issues for the Middle-Income Client 9/25/2014 Mobile 275 325

199 8 TX Determining how Much Money you Need to Retire, with Tax Ideas and Money 9/26/2014 Mobile 275 325

200 8 TX Fiduciary Income Tax Returns 9/26/2014 Mobile 275 325

201 8 AA Identifying Fraudulent Financial Transactions 9/29/2014 Birmingham -30 275 325

202 8 TX Getting More Active with the Passive Activity Rules and the New Net Investment 9/29/2014 Birmingham 275 325

203 8 TX hottest Tax Topics for 2014 9/29/2014 Tuscaloosa -30 275 325

204 8 Other Excel Best Practices 9/29/2014 Tuscaloosa 275 325

205 8 TX Surgent McCoy’s 2014 Annual Tax Planning Guide for S Corporations, Partnerships and LLCs 9/30/2014 Birmingham 275 325

206 8 Other Top Accounting Solutions 9/30/2014 Birmingham 275 325

Type of AICPA Member Non-Member No. Hrs Credit Title Date Location Discount Fee Fee

ThE ALABAMA CPA MAGAZINE 19

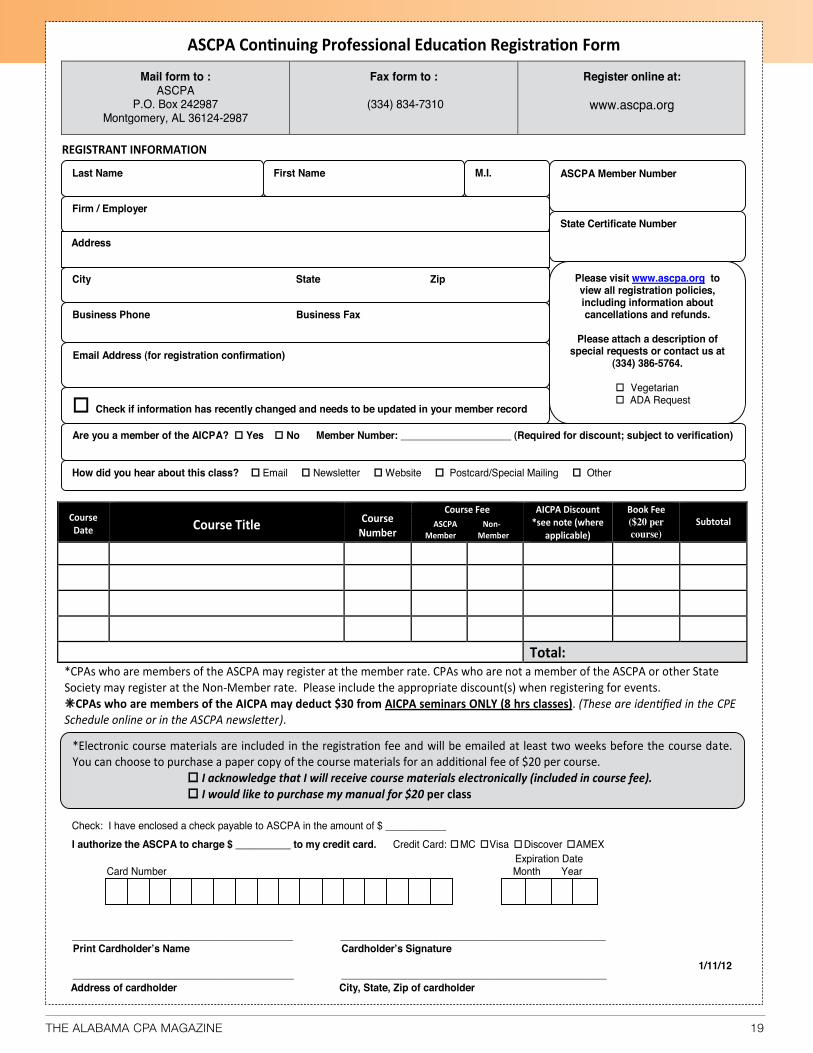

edUCATION ExPrESS Save $25 when you register at least 10 days before class date. ASCPA Continuing Professional Education Registration Form

Mail form to :ASCPA

P.O. Box 242987Montgomery, AL 36124-2987

Fax form to :

(334) 834-7310

Register online at:

www.ascpa.org

REGISTRANT INFORMATION

*CPAs who are members of the ASCPA may register at the member rate. CPAs who are not a member of the ASCPA or other State Society may register at the Non-Member rate. Please include the appropriate discount(s) when registering for events. CPAs who are members of the AICPA may deduct $30 from AICPA seminars ONLY (8 hrs classes). (These are identified in the CPE Schedule online or in the ASCPA newsletter).

Check: I have enclosed a check payable to ASCPA in the amount of $ ___________I authorize the ASCPA to charge $ __________ to my credit card. Credit Card: MC Visa Discover AMEX

Card Number Month Year Expiration Date

Print Cardholder’s Name Cardholder’s Signature________________________________________ ________________________________________________

Address of cardholder City, State, Zip of cardholder

1/11/12

Course Date

Course Title Course Number

Course Fee ASCPA Non-

Member Member

AICPA Discount *see note (where

applicable)

Book Fee ($20 per course)

Subtotal

Total:

Last Name First Name M.I.

City State Zip

Firm / Employer

Email Address (for registration confirmation)

Business Phone Business Fax

Address

Check if information has recently changed and needs to be updated in your member record

Are you a member of the AICPA? Yes No Member Number: ____________________ (Required for discount; subject to verification)

ASCPA Member Number

State Certificate Number

Please visit www.ascpa.org to view all registration policies, including information about cancellations and refunds.

Please attach a description of special requests or contact us at

(334) 386-5764.

Vegetarian ADA Request

How did you hear about this class? Email Newsletter Website Postcard/Special Mailing Other

*Electronic course materials are included in the registration fee and will be emailed at least two weeks before the course date. You can choose to purchase a paper copy of the course materials for an additional fee of $20 per course. I acknowledge that I will receive course materials electronically (included in course fee). I would like to purchase my manual for $20 per class

________________________________________ ________________________________________________

Presorted StdUS Postage

PAIDPermit No. 131Montgomery, AL

The Alabama Society of Certified Public Accountants

1041 Longfield CourtP.O. Box 242987

Montgomery, AL 36124

SEPTEMBER 2014

C l A S S I F I e d

YOUR PRACTICE WANTED: We are North America’s leader in practice sales. Let us navigate the complexi-ties, locate the best match from a deep pool of qualified and serious buyers, and optimize your return on the years invested in building your practice. If you are considering a change, contact Alabama broker Lori Newcomer, CPA, at (888) 277-6040 or [email protected] for a confidential dis-cussion.

PRACTICE FOR SALE: Panama City Beach 55% tax, 32% account-ing, 13% payroll of $155k gross in 2013. Owner open to merger or tran-sitional employment for client reten-tion. Excellent location. 850-588-8527 or [email protected]

ACCOUNTANT WANTED: Expe-rienced controller wanted for sea-food restaurant chain based in Gulf Shores. CPA preferred. Restaurant background is a plus. Responsible for activities at 20 stores in Alabama, Mississippi and Florida, including day-to-day operations, forecasting, tax, reconciling accounts. Send resume to [email protected] or call 251.968.3153 for more information.

Did you know that classified advertising in the Alabama CPA magazine is a member benefit? For a modest sum, you can seek talented staff, look for a new position, rent out excess office space, sell a practice, or even buy one. Don’t overlook this valuable resource. For more information, contact Diane Christy, 334.386.5752 or [email protected].

It’s a light bulb moment when you discover classified advertising with the ASCPA.

On, Thursday, July 31, 2014, Wilkins Miller Hieronymus LLC (WMH) planted a lilac chaste tree in Cooper riverside Park to celebrate the firm’s 5th anniversary. The accounting and

consulting firms of Wilkins Miller, P.C. and Hieronymus, Gaillard & Jones, LLC combined in July 2009 to form WMH, the largest accounting and advisory firm in the Mobile Bay region.

Related Documents