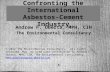

RESEARCH EUREKA RESEARCH www.eurekasecurities.com ANALYST Samudrajit Gohain [email protected] 097488 60335 / 91-33-3918 0386 - 87 Asbestos cement Industry Characteristics High entry barrier due to environmental norms High brand consciousness, limiting growth for new and unbranded players More than 50% of raw material is imported, hence forex movement impact margins Inability to pass on raw material price hike High operating leverage,freig ht cost 10% of topline Cycle is 3-4 years duration Mostly rural centric Asbestos industry in transition: On an uptrend after 4 years of lethargic growth Key characteristic s of asbestos cement industry: Introduction: Indian asbestos industry is more than 60 years old with established players like Visaka Industries, Hyderabad industries, Everest Industries in existence since 1950-60.The industry caters mostly to the roofing demand in the income bracket of Rs4000-5000 per month per family . With an installed capacity of 5 mt at the end of FY10, the industry size is about Rs40bn. Although there are about 17 players, the top 4 companies control about 65-67% market share in asbestos cement industry. More than 70% of asbestos cement demand is met from rural areas, making it unable to pass on raw material costs. The industry is characterize d by a cycle of 3-4 years. U nlike in the past, recently there has been more subdued capacity addition among the top 4 manufacturers, making pricing regime more stable and a continuous uptrend since FY09.The companies use white asbestos (chrysolite) which is environmentally friendly without any known harmful effects. Even advanced countries like USA and Canada has been using this variety of asbestos. Hence despite occasional sound bites about environmental effects, its growth has been consistent across the globe. The last case against asbestos use in India was disposed off way back in 1995. Source: Eureka Research, industry 15th December, 2010 INDIAN ASBESTOS INDUSTRY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 1/31

RESEARCH

EUREKA RESEARCH www.eurekasecurities.com

ANALYST

Samudrajit Gohain

097488 60335 / 91-33-3918 0386 - 87

AsbestoscementIndustry

Characteristics

High entrybarrier due toenvironmental

norms

High brandconsciousness,

limiting growthfor new andunbranded

players

More than50% of rawmaterial is

imported, henceforex movementimpact margins

Inability topass on raw

material pricehike

High operatingleverage,freight cost 10% of

topline

Cycle is 3-4years

duration

Mostlyrural centric

Asbestos industry in transition: On an uptrend after 4 years of lethargic

growth

Key characteristics of asbestos cement industry:

Introduction: Indian asbestos industry is more than 60 years old with

established players like Visaka Industries, Hyderabad industries, Everest

Industries in existence since 1950-60.The industry caters mostly to the

roofing demand in the income bracket of Rs4000-5000 per month per

family. With an installed capacity of 5 mt at the end of FY10, the industry

size is about Rs40bn. Although there are about 17 players, the top 4

companies control about 65-67% market share in asbestos cement

industry. More than 70% of asbestos cement demand is met from rural

areas, making it unable to pass on raw material costs. The industry is

characterized by a cycle of 3-4 years. Unlike in the past, recently there has

been more subdued capacity addition among the top 4 manufacturers,

making pricing regime more stable and a continuous uptrend since

FY09.The companies use white asbestos (chrysolite) which is

environmentally friendly without any known harmful effects. Even

advanced countries like USA and Canada has been using this variety of asbestos. Hence despite occasional sound bites about environmental

effects, its growth has been consistent across the globe. The last case

against asbestos use in India was disposed off way back in 1995.

Source: Eureka Research, industry

15th December, 2010

INDIAN ASBESTOS INDUSTRY

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 2/31

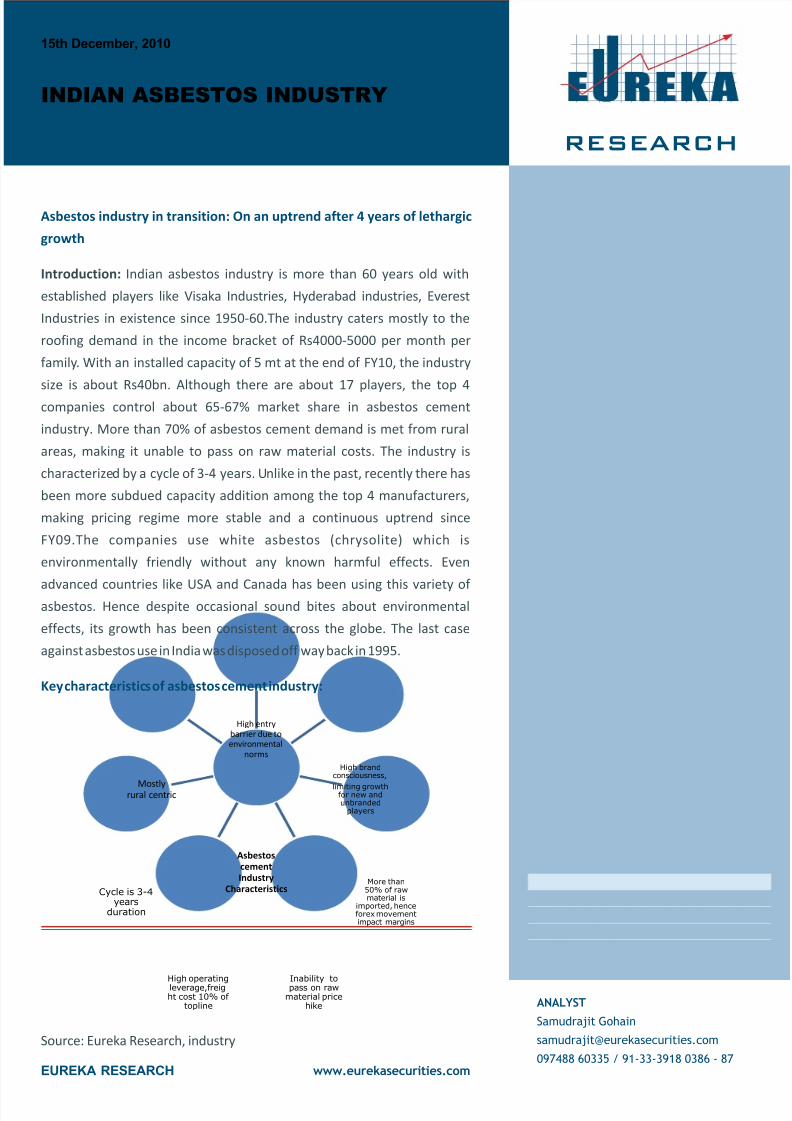

As the above diagram shows, though asbestos cement is a commodity, there are few peculiar characteristics to this industry.

So far because of these characteristics; companies' financial performances have been highly erratic on both top-line and

bottom-line.

The industry (mainly top 4 manufacturers) is likely to benefit from confluence of 5 main factors. These factors have been

visible since beginning of FY10.The industry was besieged with significant finished goods industry between FY05-09 as there

was reckless capacity addition not only by marginal players but also by top 4 manufacturers in anticipation of strong demand

growth. Though demand did pick up during that period, it was exceeded by supply to some extent. Hence, along with uptick

in raw material cost, manufactures were unable to completely sell the products till FY09.

Source: Eureka Research, industry

With more balanced demand supply dynamics these days, companies have been able to pass on hike in raw material cost and

freight cost to customers. With average net realization increasing from Rs6500 per ton in FY05-06, the average EBITDA

margin of the companies increased from 15-16% to 18-19% in recent days. The next 4-5 years is likely to witness a CAGR sale

growth of 9-10% for the top 4 asbestos cement manufacturers.

Asbestos cement sheets being used in different applications

EUREKA RESEARCH 2

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

9-10% CAGR in sale of asbestos cement sale in next4-5 years against 4-5% growth in last 4-5 years

Capacityutilisationmore than

90% in FY10

from 65-70%in FY05-09

Uptick in bankcredit to agriand related

activity(25%CAGR),loan to

SME(42%

CAGR), ruraldeposits withbanks(17%

CAGR) in last4 years

Significantincrease in

rural incomefrom

NREGA,highminimumsupport price

Netrealisationincreasing

fromRs6500/ton in

Fy05-06 toRs8700/ton in

FY10

Better daysvisible asthere has

beensignificant

drop infinished goods

inventoryfrom

2009(22%CAGR inFY05-09)

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 3/31

Huge emerging demand for asbestos cement sheets as rural income grows

The housing shortage in rural India by end of CY2009 was 14.6 million units. Out of this, 11.4 million units on account of replacement and additional 3.2 million units are new units (Source:NABRD).Every year this number is increasing by 3-4%.

Out of the existing rural houses, around 54% still live in so called 'Kuccha' houses with roof made of clay tiles, thatch, wood,

plastic, tarpaulin etc. Rest 46% live in so called 'Pucca' houses. But even then this 'Pucca' house category can be clearly

subdivided into 4 distinct categories like fiber cement with metal roofing, bricks, stone and RCC.

Source: Everest Industries annual report, 2009-10

Among Pucca houses, less than half are made with RCC slabs. The rest are made with ready to use roofing products like fiber

cement roofing and metal roofing. Some roofs are also made with bricks and stone though their number is fast declining.

Although there was price differential between metal roofing like GI sheets and fiber cement sheets in the past, now they

have become quite comparable. Moreover compared to GI sheets, durability and strength of fiber cement sheets is much

better. Hence compared to 4-5% growth of asbestos cement industry in the past, we are likely to see 9-10% growth in coming

days.

The migration from a Kuccha house to a Pucca house is mostly gradual. Hence it is unlikely that a Kuccha house owner will

directly migrate to an RCC roof. Rather he is very likely to use GI or fiber cement roofing. As lakhs of poor Indians experiencean economic upliftment, we are likely to see a huge market potential in fiber cement industry in coming days.

Descending order of seasonal demand growth for asbestos cement sheet (from left to right)

EUREKA RESEARCH 3

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

The cost of a Pucca roof using fiber cement roofing

is 1/3 rd the cost of an RCC

ceiling slab

Q1(April-June)

Q4(January-March)

Q3(October-December)

Q2(July-September)

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 4/31

Construction activity in India for most of the infrastructure activities including home building is seasonal due to prevalence

of rainy season from June-July to September-October. More or less construction activities of all sorts take a back seat during

this rainy season.

Accordingly sales of asbestos cement sheets is also not uniform throughout the year. The best quarter is first (Q1) from April-

June as there is less rainfall and winter effects start receding. This is followed by fourth (Q4) quarter from January to March

though during Q4, winter spell somewhat impacts construction activity in north India, rest of India can easily undertake

construction activities including house building in rural areas.

This is followed by third and second quarter.

But going forward, we believe this trend is likely to change for top three manufacturers (Visaka Industries, Hyderabad

Industries and Everest Industries) as all of them are diversifying into somewhat related but urban and corporate centric

products like panels and boards which are used for interior purposes. These panels and boards can be used throughout the

year and they come at the very fag end of construction activities.

Cement fiber sheet is manufactured using asbestos fiber, ordinary Portland cement (OPC), fly ash, wood pulp and certain

fillers not disclosed by the management. The following pie diagram depicts how 1 tons of cement fiber sheet is composed in

terms of volume and value. Volume wise ordinary Portland cement forms the biggest contribution (45%), followed by fly ash

(30%) and wood pulp (17%). Asbestos fiber consists the smallest (8%).

On the other hand, values wise, asbestos fiber contributes the highest (45%), followed by ordinary Portland cement(40%),

wood pulp(8%) and fly ash (7%).

Cement fiber sheet composition

EUREKA RESEARCH 4

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

Volume wise composition Value wise composition

cement(

OPC)

45%

asbestos

fibre

8%

flyash

30%

woodpul

p & fillers

17%

cement(

OPC)

40%

asbestos

fibre

45%

flyash

7%

woodpul

p & fillers

8%

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 5/31

Raw material procurement policy

(A) Ordinary Portland cement (OPC):

Ordinary Portland cement is procured as per demand schedule.

Companies generally maintain inventory of 15-20days. Hence the

asbestos cement producers have been able to take advantage of

softening of cement prices in last couple of months. The situation is

likely to stay favorable for next 1.5 years as new capacity has been

added significantly in the cement industry and supply is likely to

exceed demand for some more time

(B) Chrysotile (white asbestos) fiber:

India uses only about 6 to 7% of the white asbestos produced in the world and apart from India, Russia, China Indonesia,

Thailand and Brazil are some of the largest users of asbestos cement (AC) sheets. In India, over 90% of asbestos fiber imports

of India go into AC sheet and pipe production.

All the member industries of Chrysotile Asbestos Cement Products

Manufacturers Association (CACPMA) carry out dust level

measurements and health surveillance programs as prescribed by

regulatory authorities. No asbestos related diseases were detected

in a test taken by Directorate General of Factory Advisory Services &

Labour Institutes (DGFASLI) in the employees who are exposed to

chrysotile fiber for the last 20 years

The Ministry of Industry, Ministry of Labour, Ministry of Environment, Ministry of Consumer Affairs, Bureau of Indian

Standards, et al have laid-down regulations, standards, guidelines and recommendations specific to the asbestos industry, in

line with those of International Labour Organization, World Health Organization and other bodies. The Central and State

Pollution Control Boards, Labour and Factory Inspectors also regularly monitor the factories' compliance with the

mandatory safety standards and pollution control levels.

(C) Wood pulp:

The wood pulp is a very important raw material for manufacturing of V-boards (a form of asbestos cement sheet) which is

used further to manufacture V-panels. The manufactures' import wood pulp and Russia has emerged as the major supplier

of wood pulp for Indian asbestos cement manufacturers in recent days.

EUREKA RESEARCH 5

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

200

210

220

230

240

250

260

N o v - 0 8

J a n - 0 9

M a r - 0 9

M a y - 0 9

J u l - 0 9

S e p - 0 9

N o v - 0 9

J a n - 1 0

M a r - 1 0

M a y - 1 0

J u l - 1 0

S e p - 1 0

N o v - 1 0

Cement Prices (Rs/bag)

Source:CMA

22843

27101

32117

38200

15000

20000

25000

30000

35000

40000

FY08 FY09 FY10 FY11E

Landed cost of Chrysotile (Rs/ton)

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 6/31

However the price of imported wood pulp is highly volatile as can

be seen from above graph. Apart from being a key raw material

for paper industry, its landed cost is impacted by rupee

movement. Hence all Indian fiber cement manufactures buy it on

spot basis only. Going forward, landed cost of wood pulp is likely

to remain firm.

(D) Fly ash:

The landed cost of fly ash is around Rs800/ton. Though fly ash is available free at the thermal stations, it is labour cost for

loading and unloading apart from transportation cost which makes it dear. The fly ash is procured as and when required.

There is increasing awareness among corporate and urban population about 'Green Housing' concept. Hence environment

friendly V-boards and V-panels are replacing plywood for interior ceilings, partitions etc. They have longer life compared to

plywood and they are fire and termite resistant. They enable occupants to stay more than two hour without any discomfortin the vicinity of a fire hazard in the building. The V-panels and V-boards offer resistance to moisture and termite as well

unlike plywood.

The V-boards industry is large and fragmented. Boards made of different materials like wood, plywood, gypsum, calcium

silicate and fiber cement have been introduced in the market within the last decade. Current industry size for wood based

products is Rs4200Cr per annum, followed by Gypsum boards (Rs500Cr per annum), fiber cement boards (Rs200Cr) and last

calcium silicate (Rs50Cr) per annum. (Source: Everest Industries)

From asbestos cement sheets to V-boards and V-panels: Urban centric and corporate products

EUREKA RESEARCH 6

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

31696

29353

3910041000

32000

20000

25000

30000

35000

40000

45000

FY09 FY10 Aug-10 Oct-10 Nov-10

Wood pulp prices (Rs/ton)

Everest

Industries &

Visaka

Industries

Non asbestos typeV-board

Hyderabad

Industries V-panels

Manufactured by V-boards on both sides

held together by a

mixture of concrete in

between.

Asbestos Type Non asbestos type V-

panels and V-boards are

more acceptable in India

and abroad.

Raw material cost of non

asbestos type V-panels

is higher compared to

asbestos type.

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 7/31

V-boards and V-panels can be used in false ceilings, partions and wall claddings. They have been used extensively by GMR,

Punj Lloyd, Shapoorji-Pallonji ,Soma Enterprises, TCS, Larsen & Tuorbo etc. They can be used both with and without

lamination depending upon interior decoration style.

They are gaining market share at the cost of plywood based boards and panels. But as corporate are getting concerned about

LEED rating, they are increasingly shifting from plywood to alternative products like asbestos/non asbestos cement sheet .As

the following graph shows there is a huge untapped market potential for these non plywood based players for boards and

panels business.

Source: Eureka Research, industry

They can be laminated and meet all the requirements of interior decorators and architects as the following two pictures

show. They can be used in external wall claddings also as has been the case in recent years.

Explosive growth ahead for cement based V-boards and panels

Application of V-boards and V-panels

EUREKA RESEARCH 7

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

4200

500200 50

0

500

1000

1500

2000

2500

3000

3500

4000

4500

plywood gypsum based cement sheetbased

calcium siliconbased

Market Size (Rs.cr/year)

Huge

opportunity for

non plywood

based players

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 8/31

Source: Eureka Research, industry

As the above pyramid structure shows there is a huge price differential especially between cement sheet based boards and

panels and other type, namely plywood based and gypsum based. Hence going forward, we believe that a huge market

opportunity will be tapped by these three companies (Visaka Industries, Hyderabad Industries and Everest Industries).

As the above diagram shows, it is not only costs but several other physical and qualitative parameters which speak for a

compelling growth story for the cement sheet based boards and panels. They make the whole construction exercise fast and

easy apart from lower cost. Hence a very healthy yearly growth rate which is likely to exceed other competitive products'

growth rate.

EUREKA RESEARCH 8

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

1.2

6.5

7.5

0 1 2 3 4 5 6 7 8

Cement Sheet

Gypsum

Plywood

Cost of panels (Rs./ sq. ft/ mm)

Advantages of c ement based V-boards and panels

Cost wise quiteeconomical

compared toplyboard

Lighter & thinnerthanplywood,brick,quicker & easier to erect

by 3persons,reusable atdifferent locations

Environmentally

friendly, fireresistancecapability,ter-

mite,moisture andsound proof

Enhances LEED

rating of projects, moredurability and

longevity

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 9/31

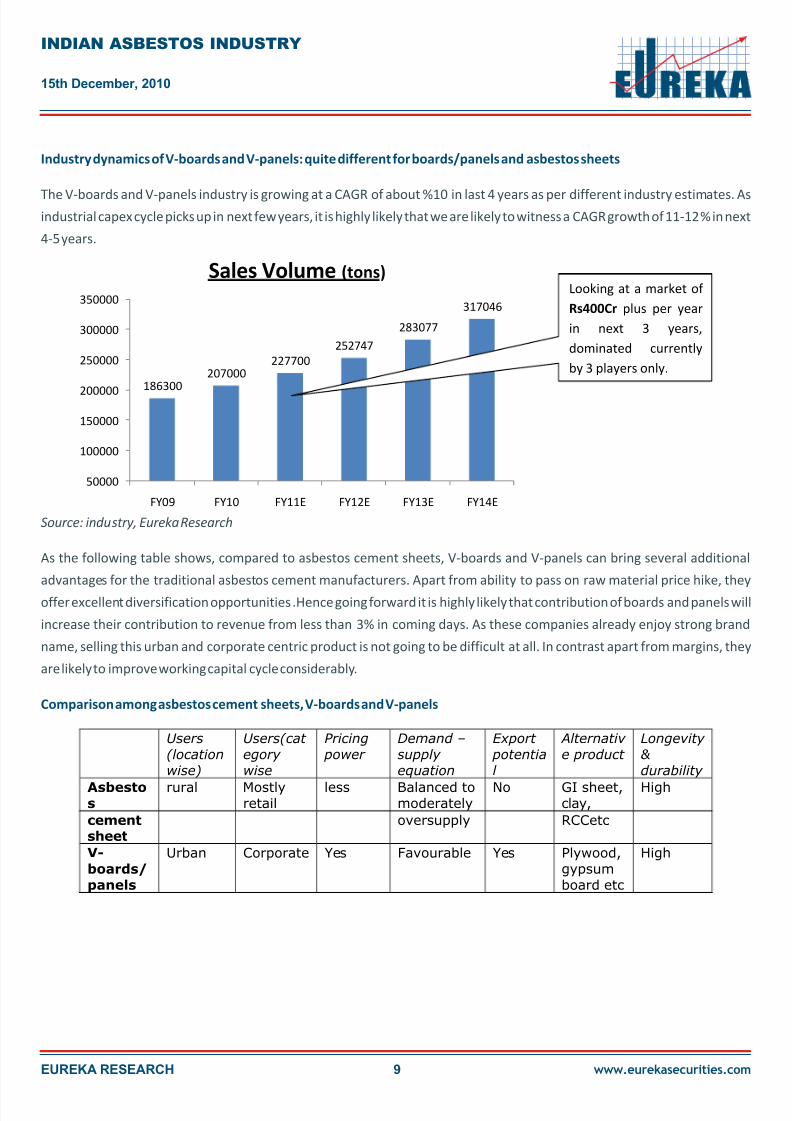

Industry dynamics of V-boards and V-panels: quite different for boards/panels and asbestos sheets

Comparison among asbestos cement sheets, V-boards and V-panels

The V-boards and V-panels industry is growing at a CAGR of about %10 in last 4 years as per different industry estimates. Asindustrial capex cycle picks up in next few years, it is highly likely that we are likely to witness a CAGR growth of 11-12% in next

4-5 years.

Source: industry, Eureka Research

As the following table shows, compared to asbestos cement sheets, V-boards and V-panels can bring several additional

advantages for the traditional asbestos cement manufacturers. Apart from ability to pass on raw material price hike, they

offer excellent diversification opportunities .Hence going forward it is highly likely that contribution of boards and panels will

increase their contribution to revenue from less than 3% in coming days. As these companies already enjoy strong brand

name, selling this urban and corporate centric product is not going to be difficult at all. In contrast apart from margins, they

are likely to improve working capital cycle considerably.

EUREKA RESEARCH 9

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

186300207000

227700

252747

283077

317046

50000

100000

150000

200000

250000

300000

350000

FY09 FY10 FY11E FY12E FY13E FY14E

Sales Volume (tons)Looking at a market of

Rs400Cr plus per year

in next 3 years,

dominated currently

by 3 players only.

cementsheet

oversupply RCCetc

V-boards/panels

Urban Corporate Yes Favourable Yes Plywood,gypsumboard etc

High

Users

(location

wise)

Users(cat

egory

wise

Pricing

power

Demand –

supply

equation

Export

potentia

l

Alternativ

e product

Longevity

&

durability

Asbestos

rural Mostlyretail

less Balanced tomoderately

No GI sheet,clay,

High

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 10/31

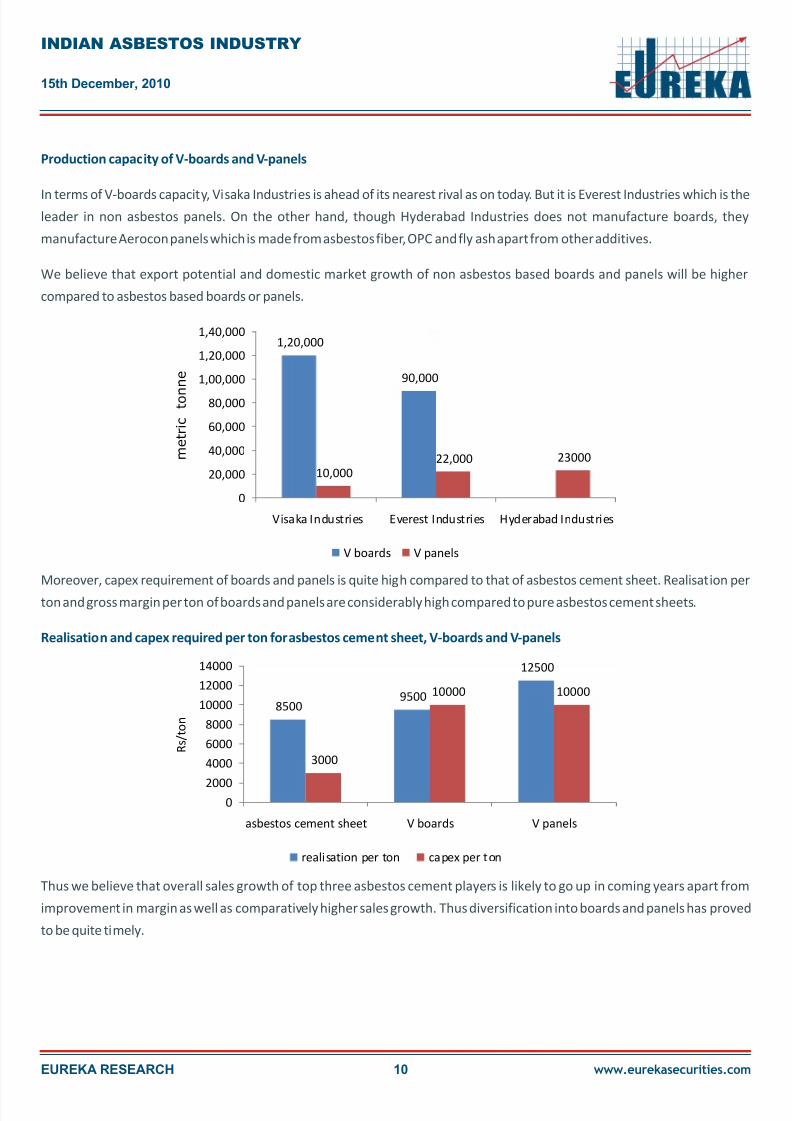

Production capacity of V-boards and V-panels

Realisation and capex required per ton for asbestos cement sheet, V-boards and V-panels

In terms of V-boards capacity, Visaka Industries is ahead of its nearest rival as on today. But it is Everest Industries which is theleader in non asbestos panels. On the other hand, though Hyderabad Industries does not manufacture boards, they

manufacture Aerocon panels which is made from asbestos fiber, OPC and fly ash apart from other additives.

We believe that export potential and domestic market growth of non asbestos based boards and panels will be higher

compared to asbestos based boards or panels.

Moreover, capex requirement of boards and panels is quite high compared to that of asbestos cement sheet. Realisation per

ton and gross margin per ton of boards and panels are considerably high compared to pure asbestos cement sheets.

Thus we believe that overall sales growth of top three asbestos cement players is likely to go up in coming years apart from

improvement in margin as well as comparatively higher sales growth. Thus diversification into boards and panels has proved

to be quite timely.

EUREKA RESEARCH 10

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

1,20,000

90,000

10,00022,000 23000

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

Visaka Industries Everest Industries Hyderabad Industries

m e t r i c

t o n

n e

V boards V panels

85009500

12500

3000

10000 10000

02000

4000

6000

8000

10000

12000

14000

asbestos cement sheet V boards V panels

R s / t o n

realisation per ton capex per ton

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 11/31

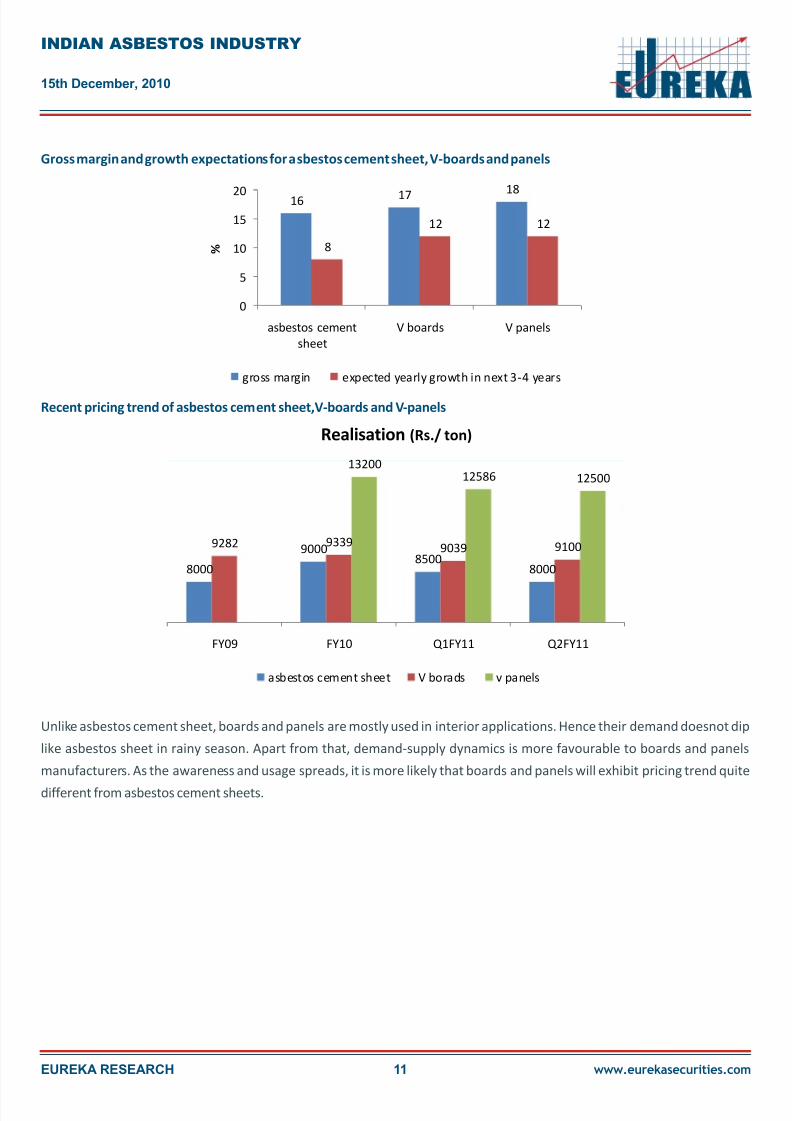

Gross margin and growth expectations for asbestos cement sheet, V-boards and panels

Recent pricing trend of asbestos cement sheet,V-boards and V-panels

Unlike asbestos cement sheet, boards and panels are mostly used in interior applications. Hence their demand doesnot dip

like asbestos sheet in rainy season. Apart from that, demand-supply dynamics is more favourable to boards and panels

manufacturers. As the awareness and usage spreads, it is more likely that boards and panels will exhibit pricing trend quite

different from asbestos cement sheets.

EUREKA RESEARCH 11

INDIAN ASBESTOS INDUSTRY

15th December, 2010

www.eurekasecurities.com

16 1718

8

12 12

0

5

10

15

20

asbestos cement

sheet

V boards V panels

%

gross margin expected yearly growth in next 3-4 years

8000

90008500

8000

9282 93399039 9100

1320012586 12500

FY09 FY10 Q1FY11 Q2FY11

Realisation (Rs./ ton)

asbestos cement sheet V borads v panels

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 12/31

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 13/31

Introduction:

Catering to all India demand

Visaka industries Limited was started in 1985. VIL is the 3rd

largest player (present capacity of 6.52lakh TPA which is likely to go up to

7.62 lakh TPA by FY12E) in Asbestos Cement FibreSheet (CFS) industry with

a significant presence in the Southern markets. The Company is engaged in

two businesses -building products (cement asbestos products, and flat

products like V Boards and V Panels) and textiles. More than 85% of the

company's revenue comes from the building products division. Among

building products division also, it has diversified into fast emerging V blocks

and V panels segments since FY08-09. Though the boards and panels

division contribute about 3% to top line as of now, it is likely to go up in

coming days looking at industry dynamics.

The company has a market share of 16-17% in asbestos cement industry on

all India basis on account of its aggressive marketing and distribution. The

company has already acquired land for additional 1 lakh tonne asbestos

cement capacity in Sambalpur, Orissa. The company has a strong brand

image and enjoys a premium which gets reflected in its high realizations

and margins. With the expected improvement in the realization and

demand for CFS, it is very likely that the company will be able to post a CAGR

growth of 12% for its top line between FY09 and FY12E.

The company has access to its customers through more than 6000 dealer

network in the country. These dealers not only stock products of Visaka

Industries, but also caters to demand for all other house construction

materials like rods, wires etc. For asbestos cement sheets, it has

manufacturing units at: Patancheru (Andhra Pradesh), Paramathi

(Tamilnadu), Midnapur (West Bengal), Vijayawada (Andhra Pradesh),

Tumkur (Karnataka), Rae Bareli (Uttar Pradesh) and Pune(Maharashtra).It

is in the process of adding another 1 lakh tone capacity at Sambalpur in

Orissa, which will come on stream by June,2011.

For flat products(boards and panels), it has factory at Miryalguda (Andhra

Pradesh). For textile products, it has manufacturing location at

Nagpur(Maharashtra).

RESEARCH

EUREKA RESEARCH www.eurekasecurities.com

BUY

VISAKA INDUSTRIES LTD (VIL)

Recommendation

CMP

TARGET

: Rs. 127.00

: Rs. 222.00

COMPANY DETAILS

SHARE HOLDING PATTERN %

BSE Code

NSE Symbol

Bloomberg

Market Cap. (Rs. Crs)

Free Float (Rs. Crs)

52 Week High

52 Week Low

Dividend Yield -%

Beta

Promoter Group

FII

DII

Others

Total

509055

VISAKAIND

VISKI IN

198

129

193

118

4.00

0.98

37.70

3.00

1.33

57.97

100.00

0

10

20

30

40

50

60

70

80

50

70

90

110

130

150

170

190

210

D e c - 0 9

J a n - 1 0

F e b - 1 0

M a r - 1 0

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

N o s . x 1 0 0 0 0

Total Volume

Visaka Industries

ANALYST

Samudrajit Gohain

097488 60335 / 91-33-3918 0386 - 87

13

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 14/31

EUREKA RESEARCH 14

VISAKA

15th December, 2010

www.eurekasecurities.com

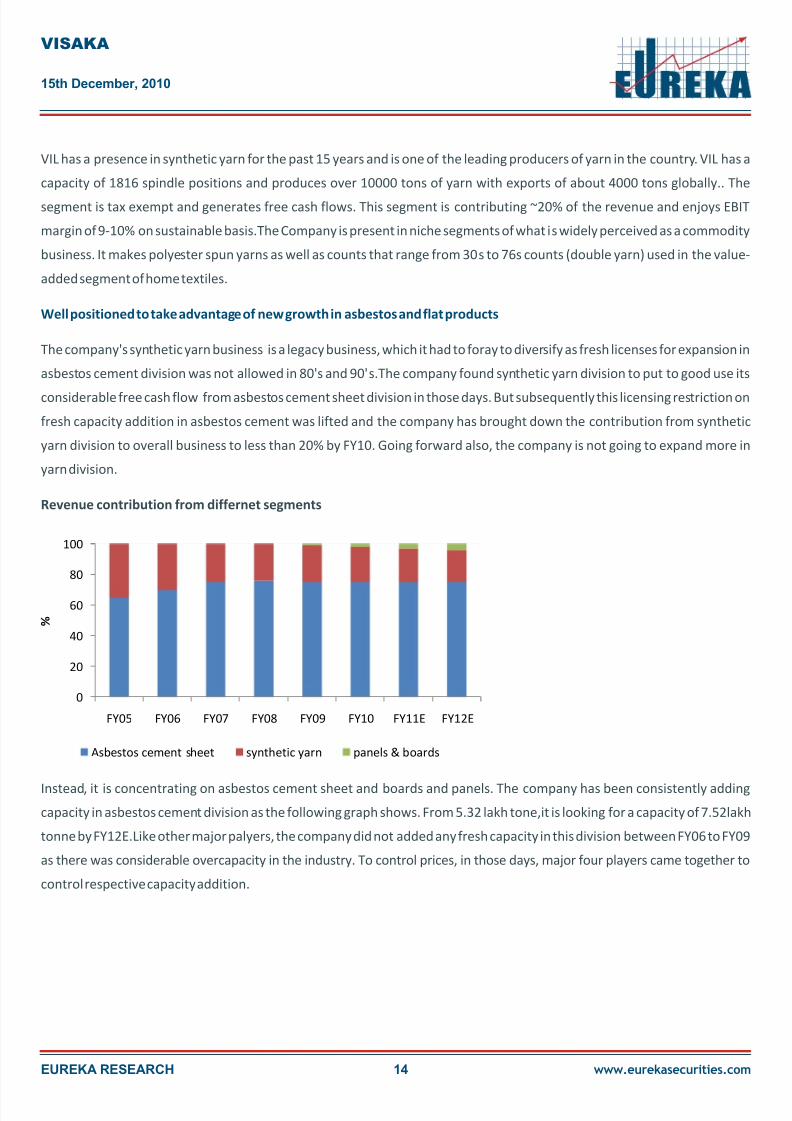

VIL has a presence in synthetic yarn for the past 15 years and is one of the leading producers of yarn in the country. VIL has a

capacity of 1816 spindle positions and produces over 10000 tons of yarn with exports of about 4000 tons globally.. The

segment is tax exempt and generates free cash flows. This segment is contributing ~20% of the revenue and enjoys EBIT

margin of 9-10% on sustainable basis.The Company is present in niche segments of what is widely perceived as a commodity

business. It makes polyester spun yarns as well as counts that range from 30s to 76s counts (double yarn) used in the value-

added segment of home textiles.

The company's synthetic yarn business is a legacy business, which it had to foray to diversify as fresh licenses for expansion in

asbestos cement division was not allowed in 80's and 90's.The company found synthetic yarn division to put to good use its

considerable free cash flow from asbestos cement sheet division in those days. But subsequently this licensing restriction on

fresh capacity addition in asbestos cement was lifted and the company has brought down the contribution from synthetic

yarn division to overall business to less than 20% by FY10. Going forward also, the company is not going to expand more in

yarn division.

Revenue contribution from differnet segments

Instead, it is concentrating on asbestos cement sheet and boards and panels. The company has been consistently adding

capacity in asbestos cement division as the following graph shows. From 5.32 lakh tone,it is looking for a capacity of 7.52lakh

tonne by FY12E.Like other major palyers, the company did not added any fresh capacity in this division between FY06 to FY09

as there was considerable overcapacity in the industry. To control prices, in those days, major four players came together to

control respective capacity addition.

Well positioned to take advantage of new growth in asbestos and flat products

0

20

40

60

80

100

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E

%

Asbestos cement sheet synthetic yarn panels & boards

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 15/31

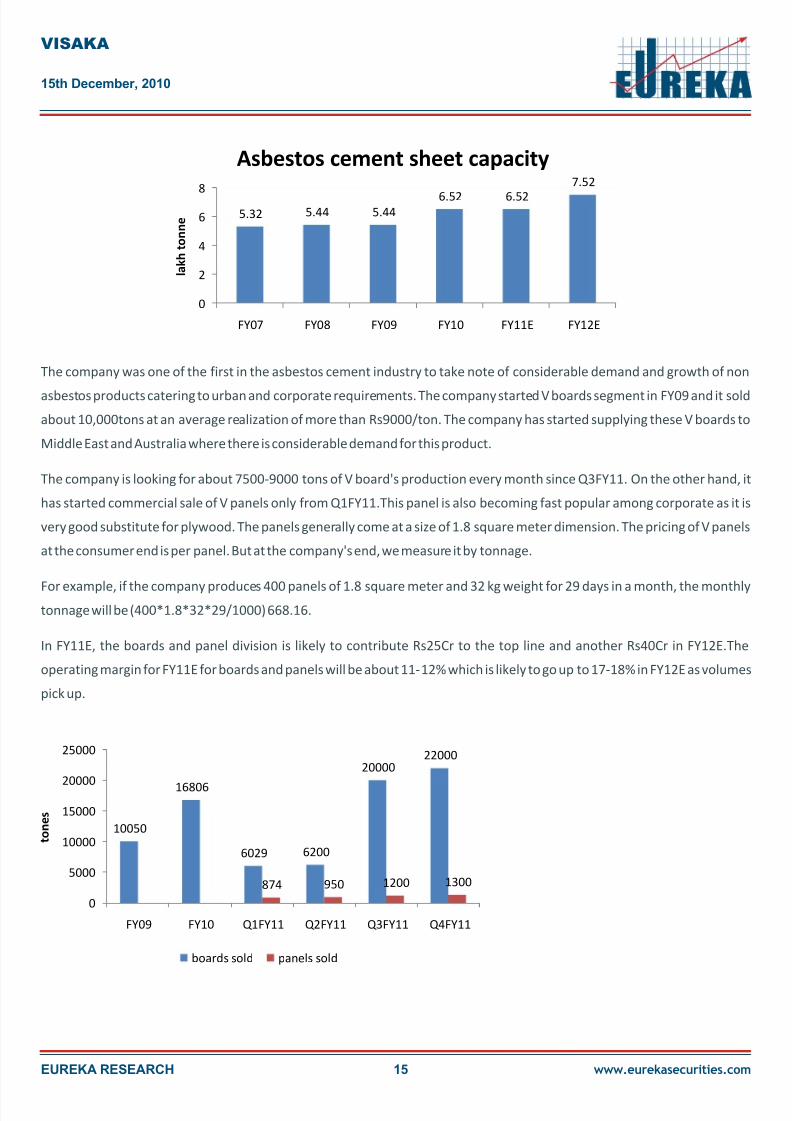

The company was one of the first in the asbestos cement industry to take note of considerable demand and growth of non

asbestos products catering to urban and corporate requirements. The company started V boards segment in FY09 and it sold

about 10,000tons at an average realization of more than Rs9000/ton. The company has started supplying these V boards to

Middle East and Australia where there is considerable demand for this product.

The company is looking for about 7500-9000 tons of V board's production every month since Q3FY11. On the other hand, it

has started commercial sale of V panels only from Q1FY11.This panel is also becoming fast popular among corporate as it is

very good substitute for plywood. The panels generally come at a size of 1.8 square meter dimension. The pricing of V panels

at the consumer end is per panel. But at the company's end, we measure it by tonnage.

For example, if the company produces 400 panels of 1.8 square meter and 32 kg weight for 29 days in a month, the monthlytonnage will be (400*1.8*32*29/1000) 668.16.

In FY11E, the boards and panel division is likely to contribute Rs25Cr to the top line and another Rs40Cr in FY12E.The

operating margin for FY11E for boards and panels will be about 11-12% which is likely to go up to 17-18% in FY12E as volumes

pick up.

EUREKA RESEARCH 15

VISAKA

15th December, 2010

www.eurekasecurities.com

5.32 5.44 5.446.52 6.52

7.52

0

2

4

6

8

FY07 FY08 FY09 FY10 FY11E FY12E

l a k h t o n n e

Asbestos cement sheet capacity

10050

16806

6029 6200

2000022000

874 950 1200 1300

0

5000

10000

15000

20000

25000

FY09 FY10 Q1FY11 Q2FY11 Q3FY11 Q4FY11

t o n e s

boards sold panels sold

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 16/31

Company enjoys a very comfortable working capital cycle

The asbestos cement business has a very comfortable debtor days of 30-40 days.The debtor days cycle is improving fromabout 45 days to less than 30 days in recent days. The finshed goods inventory period is 45 days. This is because, the company

has to cure asbestos cement sheets for 15 days after manufacturing.Except asbestos fiber, which is an imported product,

most other raw materials are procured as and when required.Asbestos fiber is stored for a period from 3-6 months

depending upon inward ship freight condition. Thus overall inventory days has been hovering around 60 days so far. But as V

boards and V panels production and sales pick up in coming days, overall inventory days are likely to come down further as all

the raw materials required for V boards and panels are locally produced.

Huge improvement in operating and free cash flow since FY09.

Like all other companies producing asbestos cement sheets between FY05 to FY08, the company had negligible operating

cash flow compared to sales and negative free cash flow. Since then both the parameters are improving dramatically. The

initial capital requirement for both asbestos cement sheets and boards/panels is not very significant (Rs3000-3500/ton for

asbestos cement sheet and Rs10, 000/boards).All future expansion in next few years are likely to be funded by internal

accruals and debt. ByFY12E, the debt equity ratio is likely to be around 0.3. Hence company will have significant leeway for

leverage.

EUREKA RESEARCH 16

VISAKA

15th December, 2010

www.eurekasecurities.com

63

71

62

69

5559

54 56

30 30 32

40

32 30 31 30

0

10

20

30

40

50

6070

80

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E

Inventory days Debtor days

-60

-40

-20

0

20

40

60

80

100

120

140

FY05 FY06 FY07 FY08 FY09 FY10 FY11E FY12E

R s . C r

operating cash flow free cash flow

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 17/31

Healthy margins and return ratios

The FY10 was a very good year for major asbestos manufacturers in terms of margin. During that year, the company clockedEBITDA margin of about 22%. This was contributed by benign raw material prices and significant demand uptick. Since then

raw material prices especially asbestos fiber, transportation cost and wood pulp cost have significantly gone up. For

example, asbestos fiber price has gone up from about Rs32000/ton from FY10 to more than Rs38000/ton recently. As

asbestos cement manufacturers can not equally pass on raw material price hike, going forward we are likely to witness more

sustainable 16-17% EBITDA margin.

But as margins for boards and panels are high compared to that of asbestos cement sheet, may be margins may improve

after FY12 if there is significant capacity addition in boards and panels division.

Likewise, ROCE and ROE are likely to hover around 20% in coming days. This was the range companies enjoyed till FY06-07 .

Hence we are very much confident that at least pre recession return ratios will be achieved by the company in coming days,

with possibility for upside.

EUREKA RESEARCH 17

VISAKA

15th December, 2010

www.eurekasecurities.com

0

5

10

15

20

25

30

%

ROE ROCE

0

2

4

6

8

10

12

14

16

18

20

%

EBITDA PAT

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 18/31

EUREKA RESEARCH 18

VISAKA

15th December, 2010

www.eurekasecurities.com

Rs.Cr

Net sales

Other income

Total income

Total expenditure

Raw material

As a % of net sales

Decrease/(increase ) in work in progress

Outwards carriage

As a % of net sales

Other operating expenses

As a % of net salesOther expenses

EBITDA

Interest

Depreciation

PBT

Tax

PAT

FY08

433.13

6.45

439.58

395.00

274.89

63.46

(20.05)

32.94

7.60

88.16

20.3519.08

44.58

15.72

15.66

13.19

5.52

7.67

FY09

573.94

11.44

585.38

496.32

295.83

51.54

30.86

47.80

8.33

98.79

17.2123.04

89.06

17.02

16.60

55.43

19.49

35.94

FY10

598.13

8.35

606.48

489.32

336.22

56.21

(25.81)

48.44

8.09

114.45

19.1316.02

117.16

12.40

18.39

86.37

28.48

57.21

FY11E

650

10

660

563.25

356

55

15

52

8.00

120.25

18.520

96.75

11

21

64.75

21.36

43.39

FY12E

708.5

12

720.50

593.13

390

55

(5)

53.13

7.5

135

1920

127.37

8

27

92.37

30.48

61.89

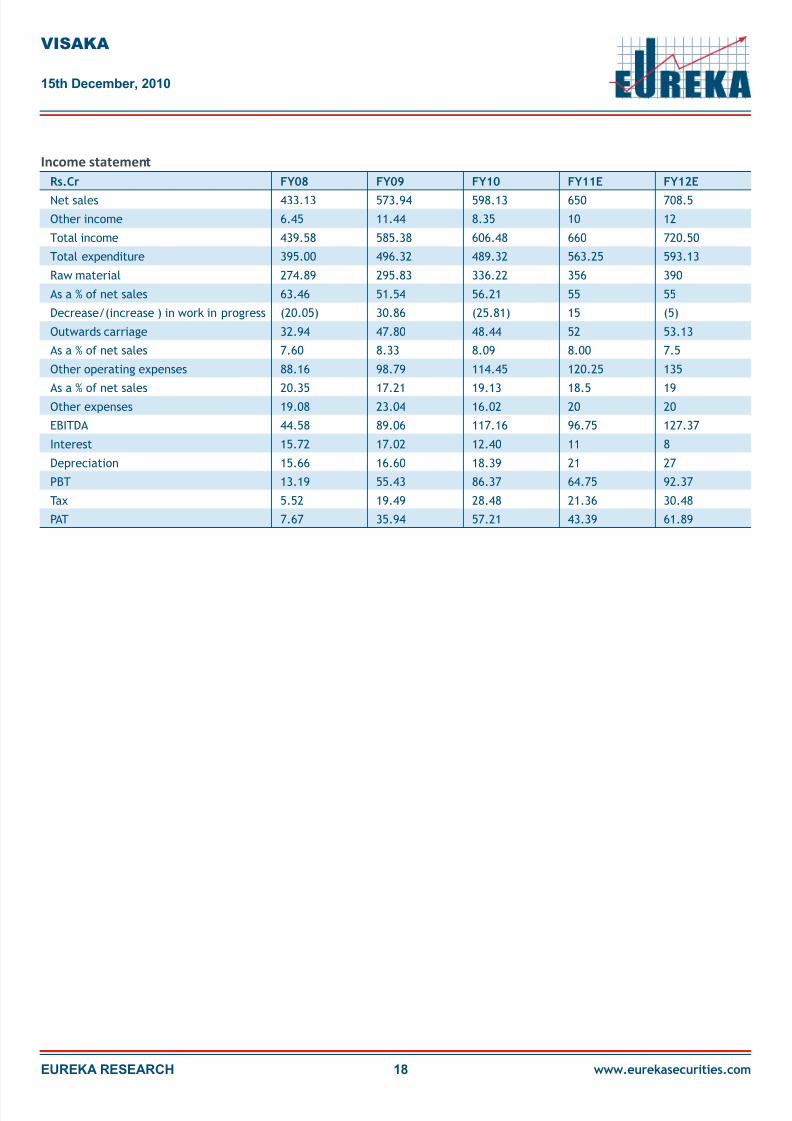

Income statement

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 19/31

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 20/31

Recommendation

The company is well on its track for profitable expansion trajectory. The company is likely to post around 9% growth in its top

line and more than 40% growth in bottom-line between FY11E and FY12E. The company will have significant cash and

equivalents (around Rs50/share) by FY12E. Thus company is likely to enjoy considerable yearly free cash flow for next couple

of years as rural demand is unlikely to dip meaningfully and there is more mutual understanding among top three players in

the asbestos cement industry these days to mitigate price damage from overcapacity.

Currently the management has about 38% stake in the company. We believe that there is significant possibility of share

buyback or increase in dividend payout ratio (currently 50%).

As revenue contribution from non asbestos products pick up in next couple of years, there is significant possibility of rerating

of the company.

The company is likely to post about Rs39 EPS in FY12E. Applying a P/E multiple of 5.5 to FY12E EPS, we arrive a target price of

Rs209.On the other hand applying a EV/EBITDA of 3, we arrive a target price of Rs235.Taking average of both these prices,

we arrive at a target price of Rs222.

EUREKA RESEARCH 20

VISAKA

15th December, 2010

www.eurekasecurities.com

Key ratios

D/E

Debtor days

Inventory turnover ratio(x)

Fixed asset turnover ratio(x)

Working capital turnover(x)

RONW

ROCE

EV/sales

EV/EBITDA

P/BV

P/E

FY08

1.2

45.2

4.6

1.6

2.8

6.2

9.76

0.9

9.99

1.3

27.4

FY09

0.9

33.8

6.4

1.8

3.7

20.71

20.67

0.6

4.3

1.1

5.8

FY10

0.78

30

6.2

1.99

3.14

27.02

26.19

0.6

3.2

1

4.2

FY11E

0.5

31

6.7

1.95

3.45

21

19

0.4

2.73

0.8

4.7

FY12E

0.3

30

6.5

1.86

3.94

19.28

18.50

0.3

1.66

0.6

3.3

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 21/31

Introduction:

Revenue contribution from different segments

Hyderabad Industries Limited (HIL) is a flagship company of the C.K.Birla

group of companies, incorporated on 17 June 1946. HIL's key product range

include Fibre Cement Roofing Sheets sold under the brand name

CHARMINAR, Autoclaved Aerated Concrete Blocks and Panels called

AEROCON, and Calcium Silicate Insulation Product (thermal insulation)

called HYSIL. The company is one of the leading manufacturers of Fibre

Cement Sheets in India with a market share of about 20.5%. After startingout as a roofing manufacturing company, HIL has evolved into a multi

product, green building products organization

HIL has a total of 11 manufacturing facilities across India with an extensive

distribution network of 52 sales depots and more than 5000 sales points.

The company has successfully diversified into allied products like panels

and autoclaved aerated concrete (AAC) blocks from its main product,

asbestos cement sheet. These blocks and panels cater to urban and

corporate consumers unlike rural centric asbestos cement sheets.

RESEARCH

EUREKA RESEARCH www.eurekasecurities.com

BUY

HYDERABAD INDUSTRIES LTD (HIL)

Recommendation

CMP

TARGET

: Rs. 436.00

: Rs. 776.00

COMPANY DETAILS

SHARE HOLDING PATTERN %

BSE Code

NSE Symbol

Bloomberg

Market Cap. (Rs. Crs)

Free Float (Rs. Crs)

52 Week High

52 Week Low

Dividend Yield -%

Beta

Promoter Group

FII

DII

Others

Total

509675

HYDRBADIND

HYI IN

327

196

762

408

3.64

0.81

43.10

3.43

6.76

46.71

100.00

ANALYST

Samudrajit Gohain

097488 60335 / 91-33-3918 0386 - 87

21

0

10

20

30

40

50

60

70

80

90

50

150

250

350

450

550

650

750

850

D e c - 0 9

J a n - 1 0

F e b - 1 0

M a r - 1 0

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

N o s . x 1 0 0 0 0

Total Volume

Hyderabad Industries

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 22/31

But still value wise, the contribution of its asbestos cement sheet is the highest. This is followed by AAC blocks, thermalinsulation products and panels.

The company is likely to maintain asbestos cement division's contribution to top line at about 86-87% in coming days. The

company is trying to cater to urban and corporate demand through AAC blocks and panels. On the other hand, thermal

insulation products cater to industrial demand. With pickup in demand from real estate and industrial capex, both these

divisions are expected to do well in future.

Revenue contribution from different segments

EUREKA RESEARCH 22

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

Thermal insulation products

Panels

AAC blocks

Asbestos cement sheet

cement, power, petrochemical,

fertilizer plants etc.

Partition, Prefabricated House,

Mezzanine flooring, Schools and

Low cost housing

Residential apartments,

Commercial complex, Industrial

complex, mall etc.

Industrial sheds, Agricultural

buildings, Warehouses, Poultry

farms, Garage, Verandahs etc.

uses

HYSIL

Aerocon

Aerocon

Charminar, Malabar

Brand name

89 87.5 86 86.5 87 87 86

3.3 67 6.5 5.2 5.5

6

32.3 2 2.2 3.1 3.3 3.5

4.7 4.2 5 4.8 4.7 4.2 4.5

75

80

85

90

95

100

FY06 FY07 FY08 FY09 FY10 FY11E FY12E

r e v e n u e c o n

t r i b u t i o n ( % )

cement fibre sheet AAC blocks panels thermal insulation products

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 23/31

There is margin disparity as is evident from the above diagram. Thermal insulation products command the highest and

asbestos cement sheet the lowest in EBIT margin.

The company has been steadily adding capacity in asbestos cement division since FY08-09 when the recession in this product

ended. The company is likely to end FY12E with about 10.79 lakh asbestos cement sheet capacity, retaining its number one

position in India.

Capacity utilisation trend of asbestos cement division

Asbestos Cement Division

EUREKA RESEARCH 23

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

6.226.74

7.648.54

8.99

10.79

5.45

6.56.98 7.3

8.09

10.25

0

2

4

6

8

10

12

FY07 FY08 FY09 FY10 FY11E FY12E

L a k h t o n e s

Capacity sales

88

96

91

85

90

95

75

80

85

90

95

100

FY07 FY08 FY09 FY10 FY11E FY12E

%

17

21

18

30

0

5

10

15

20

25

30

35

asbestos cement

sheet

panels AAC block thermal

insulation

products

E B I T m a r g i n ( % )

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 24/31

With rural demand picking up due to good monsoon, hike in minimum support prices and various friendly government

policies, the net realization of asbestos cement division has witnessed firming up in prices. The company's asbestos products

command a premium of 2-4% compared to the next biggest competitor, Visaka Industries. It is likely that this premium in

pricing will be retained in future for strong brand name.

HIL also manufactures various boards and panels that find application in housing, partitioning, interiors etc. HIL also supplies

these panels to the army. HIL is one the largest players in this segment and has developed a patented process to manufacture

the same. The boards and panels contribute about 3% to HIL's topline. HIL has a capacity to produce 4,60,000 numbers of

these panels. The company is currently running at about 70% capacity utilization. The plants are located at Thimmapur (AP)

and Faridabad (Haryana). The raw materials for this product includes flat cement sheets, fillers etc.

Realization trend of asbestos cement division

Panels division

EUREKA RESEARCH 24

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

7064

6212

7533

8358 85009000

0

1000

2000

3000

4000

50006000

7000

8000

9000

10000

FY07 FY08 FY09 FY10 FY11E FY12E

R s / t o n

1566618450

15618

21788

29500

39708

1546817140 17759

21580

29200

39000

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

FY07 FY08 FY09 FY10 FY11E FY12E

N o s .

Production & sale of panels

production sales

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 25/31

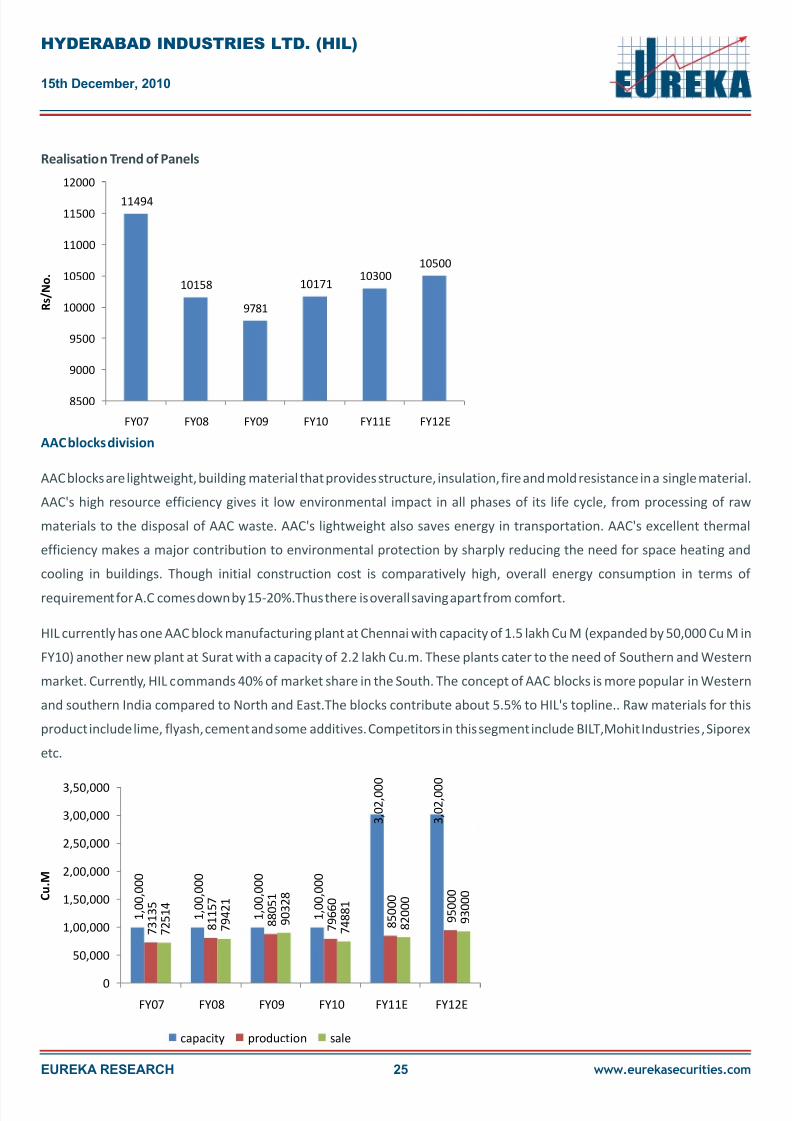

Realisation Trend of Panels

AAC blocks are lightweight, building material that provides structure, insulation, fire and mold resistance in a single material.

AAC's high resource efficiency gives it low environmental impact in all phases of its life cycle, from processing of raw

materials to the disposal of AAC waste. AAC's lightweight also saves energy in transportation. AAC's excellent thermal

efficiency makes a major contribution to environmental protection by sharply reducing the need for space heating and

cooling in buildings. Though initial construction cost is comparatively high, overall energy consumption in terms of

requirement for A.C comes down by 15-20%.Thus there is overall saving apart from comfort.

HIL currently has one AAC block manufacturing plant at Chennai with capacity of 1.5 lakh Cu M (expanded by 50,000 Cu M in

FY10) another new plant at Surat with a capacity of 2.2 lakh Cu.m. These plants cater to the need of Southern and Western

market. Currently, HIL commands 40% of market share in the South. The concept of AAC blocks is more popular in Western

and southern India compared to North and East.The blocks contribute about 5.5% to HIL's topline.. Raw materials for this

product include lime, flyash, cement and some additives. Competitors in this segment include BILT,Mohit Industries , Siporex

etc.

AAC blocks division

EUREKA RESEARCH 25

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

11494

10158

9781

1017110300

10500

8500

9000

9500

10000

10500

11000

11500

12000

FY07 FY08 FY09 FY10 FY11E FY12E

R s / N o .

1 , 0 0 , 0 0 0

1 , 0 0 , 0 0 0

1 , 0 0 , 0 0 0

1 , 0 0 , 0 0 0

3 , 0 2 , 0 0 0

3 , 0 2 , 0 0 0

7 3 1 3 5

8 1 1 5 7

8 8 0 5 1

7 9 6 6 0

8 5 0 0 0

9 5 0 0 0

7 2 5 1 4

7 9 4 2 1

9 0 3 2 8

7 4 8 8 1

8 2 0 0 0

9 3 0 0 0

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

FY07 FY08 FY09 FY10 FY11E FY12E

C u . M

capacity production sale

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 26/31

The AAC blocks business has become competitive in recent times with indiscriminate setting of capacities by several small

players and aggressive marketing by them. But it is highly likely that at some point of time in future, quality consciousness

among customers will emerge and they will go for branded and reputed AAC block manufacturers like Hyderabad Industries.

Currently AAC blocks sold by Hyderabad Industries sell at a premium of 4-5% compared to other players.

Cement, power, petrochemical,fertiliser plants etc are typical users of this division. Due to their superior properties and high

quality, the company's products have good acceptance over its substitutes. Calcium silicate is commonly used as a safe

alternative to asbestos for high temperature insulation materials. Industrial grade piping and equipment insulation is often

fabricated from calcium silicate. Efforts are being made for developing new applications to expand the market size. Rawmaterials for this product include lime, calcium silicate and used glass. Power and fuel costs play a major role in the

production of this product. The company had increased the production capacity at its Dharuhera plant to 6,000 MT per

annum, from 3,500 MT per annum in FY09. In FY10, HIL has increased the capacity by another 2,500 MT taking the total

capacity to 8,500 MT as of 1 April 2010. The company is likely to end FY12E with an installed capacity of 9300 tons.This

product contributes about 4.7% to revenue. HIL has a 76% all India market share in this product. Other players include Mega

Insulation and Nuchem.

The company has been steadily increasing its capacity to cater to the growing demand from user industries.This division has

utilisation rate of around 90%. This division has high EBIT margin in the range of 30%.

Realisation trend of AAC blocks

Thermal insulation division

EUREKA RESEARCH 26

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

2696

3285

3805 39064200

4500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

FY07 FY08 FY09 FY10 FY11E FY12E

R s . C u . M

3 5 0 0

3 5 0 0

6 0 0 0

6 0 0 0

8 5 0 0

9 3 0 0

3 3 3 9

3 8 8 4

4 6 1 6

5 3 5 3

7 2 2 5 8

0 0 0

3 5 7 7

3 9 0 9 4

7 2 8

5 3 3 2

7 2 0 0 7

9 9 0

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY07 FY08 FY09 FY10 FY11E FY12E

t o n n e s

capacity production sale

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 27/31

Pricing trend of thermal insulation products

Considerable operating and free cash flow generation

Like all other companies producing asbestos cement sheets between FY05 to FY08, the company had negligible operating

cash flow compared to sales and negative free cash flow. Since then both the parameters are improving dramatically.

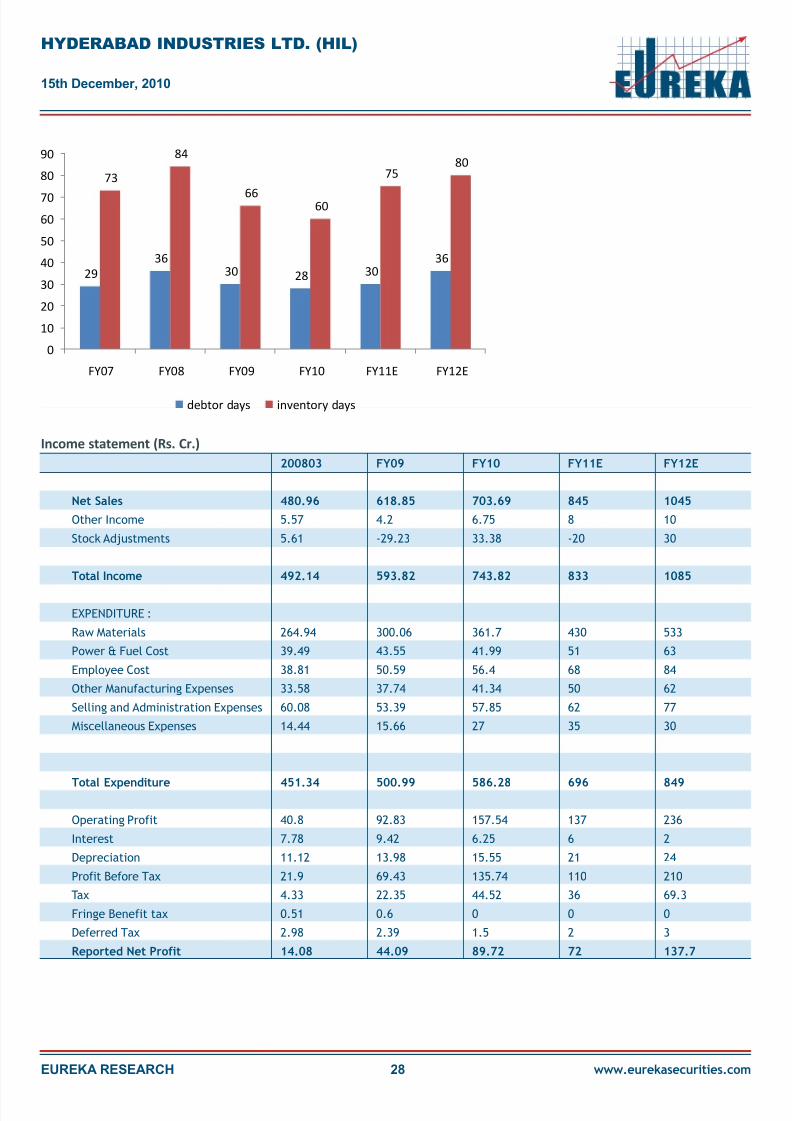

The debtor days in asbestos cement division is about 30-35 days . But as urban centric and corporate sales pick up from

panels , AAC blocks and thermal insulation products, debtor days are likely to slightly go up .Finished goods inventory days in

asbestos cement division is about 45 days, as sheets are cured for 18 days after manufacturing. But inventory days are likely

to go up some what due to pick in volumes from AAC blocks as they are seasonal and currently there is some pressure for

branded players like Hyderabad Industries.

EUREKA RESEARCH 27

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

57,28257,687

61,52762,366

63,000

64,000

52,000

54,000

56,000

58,000

60,000

62,000

64,000

66,000

FY07 FY08 FY09 FY10 FY11E FY12E

R s / t o n

- 8 . 5 7

3 3 . 1 6

7 6 . 6 7

1 0 6 . 1 5

1 1 5

9 1

- 1 . 9

4 . 5

1 9 3

5 . 5 3

4 8

3 1

-20

0

20

40

60

80

100

120

140

FY07 FY08 FY09 FY10 FY11E FY12E

R s . C r

operating cash flow free cash flow

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 28/31

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 29/31

Net cash from operating activities

Net Cash Used in Investing activities

Net Cash Used in Financing activities

Net Inc/(Dec) in Cash and Cash Equivalent

Cash and Cash Equivalents at End of the year

2008

33.16

-28.66

5.32

9.82

16.28

2009

76.67

-57.68

-24.81

-5.82

10.46

20100

106.15

-70.62

-35.49

0.04

10.5

2011E

115

-67.5

-8

39.5

50

2012E

91

-60

-36

-5

45

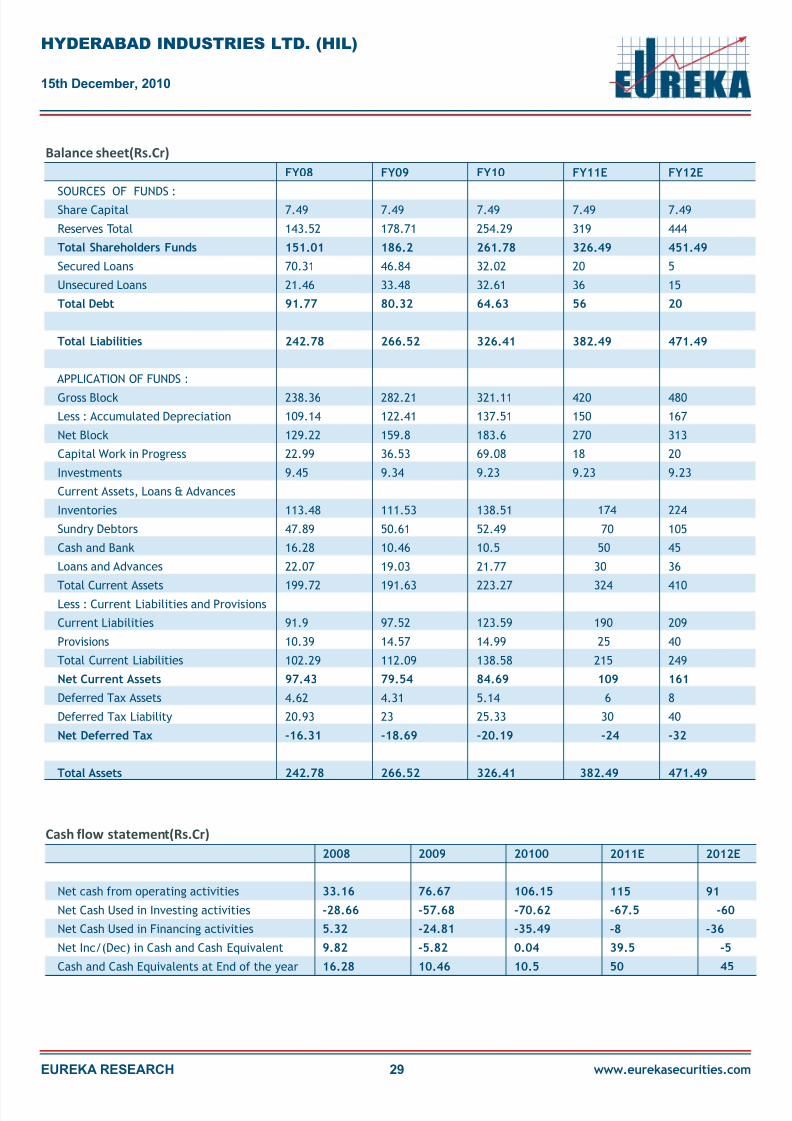

Cash flow statement(Rs.Cr)

SOURCES OF FUNDS :Share Capital

Reserves Total

Total Shareholders Funds

Secured Loans

Unsecured Loans

Total Debt

Total Liabilities

APPLICATION OF FUNDS :

Gross Block

Less : Accumulated Depreciation

Net Block

Capital Work in Progress

Investments

Current Assets, Loans & Advances

Inventories

Sundry Debtors

Cash and Bank

Loans and Advances

Total Current AssetsLess : Current Liabilities and Provisions

Current Liabilities

Provisions

Total Current Liabilities

Net Current Assets

Deferred Tax Assets

Deferred Tax Liability

Net Deferred Tax

Total Assets

FY08

7.49

143.52

151.01

70.31

21.46

91.77

242.78

238.36

109.14

129.22

22.99

9.45

113.48

47.89

16.28

22.07

199.72

91.9

10.39

102.29

97.43

4.62

20.93

-16.31

242.78

FY09

7.49

178.71

186.2

46.84

33.48

80.32

266.52

282.21

122.41

159.8

36.53

9.34

111.53

50.61

10.46

19.03

191.63

97.52

14.57

112.09

79.54

4.31

23

-18.69

266.52

FY10

7.49

254.29

261.78

32.02

32.61

64.63

326.41

321.11

137.51

183.6

69.08

9.23

138.51

52.49

10.5

21.77

223.27

123.59

14.99

138.58

84.69

5.14

25.33

-20.19

326.41

FY11E

7.49

319

326.49

20

36

56

382.49

420

150

270

18

9.23

174

70

50

30

324

190

25

215

109

6

30

-24

382.49

FY12E

7.49

444

451.49

5

15

20

471.49

480

167

313

20

9.23

224

105

45

36

410

209

40

249

161

8

40

-32

471.49

Balance sheet(Rs.Cr)

EUREKA RESEARCH 29

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

www.eurekasecurities.com

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 30/31

Recommendation

The company is likely to post about 24% growth in top line in FY12E over FY11E. As the company enjoys high operating

leverage, the growth in bottom line during the same period is likely to be around 90%. The return ratios of the company are

well above 30%. Moreover due to presence of high margin thermal insulation products and brand premium in other

products, the company is likely to maintain about 21-222% margin at the EBITDA level.

Applying a P/E multiple of 4 to FY12E EPS of 183, we arrive at a price of Rs732. On the other hand, applying an EV/EBITDA of 2.5 to FY12E EBITDA of Rs. 236 Crore, we arrive at price of Rs821.Taking average of both, we arrive at a target price of Rs776.

HYDERABAD INDUSTRIES LTD. (HIL)

15th December, 2010

EUREKA RESEARCH 30 www.eurekasecurities.com

Registered Office :

Corporate Office :

Mumbai Office :

7 Lyons Range, 2nd Floor, Room No. 1, Kolkata - 700001

B3/4, Gillander House, 8 N S Road, 3rd Floor, Kolkata - 700001Phone : 91-33-2210 7500 / 01 / 02, Fax: 91-33-2210 5184

909 Raheja Chamber, 213 Nariman Point, Mumbai-400021Phone : 91-22-2202 5941 / 5942e: [email protected]

DISCLAIMER : The information in this report has been obtained from sources, which Eureka Research believes to be reliable, butwe do not hold ourselves responsible for its completeness in accuracy. All estimates and opinions in this report constitute ourjudgement as of this date and are subject to change without notice. Eureka Researchwill not be responsible for the consequenceof reliance upon our opinion or statement contained herein or for any omission. Any feedback can be mailed to the following ID.

Analyst : Samudrajit Gohain

Email : [email protected]

Phone : 097488 60335 / 91-33-3918 0386 - 87

D/E

Debtor days

Inventory turnover ratio(x)

Fixed asset turnover ratio(x)

Working capital turnover(x)

RONW

ROCE

EV/sales

EV/EBITDA

P/BV

P/E

FY08

0.59

36

4.3

2.0

5.0

9.99

13.22

0.9

11.9

2.4

24.7

FY09

0.53

30

5.5

2.2

7.8

27

31.62

0.7

4.6

1.9

7.9

FY10

0.33

28

6.05

2.55

8.3

41

48.74

0.6

3.3

1.4

4.7

FY11E

0.17

30

4.86

1.87

10.7

22

30

0.43

2.65

1.00

4.53

FY12E

0.04

36

4.67

2.18

6.5

30

45

0.30

1.28

0.74

2.38

Key ratios

8/8/2019 Asbestos Industry Dec10

http://slidepdf.com/reader/full/asbestos-industry-dec10 31/31

Related Documents