Financial Statements and Independent Auditor’s Reports As of and for the Year Ended June 30, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FinancialStatementsandIndependentAuditor’sReports

As of and for the Year Ended June 30, 2016

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

TOWNOFCARLTONLANDING,OKLAHOMA

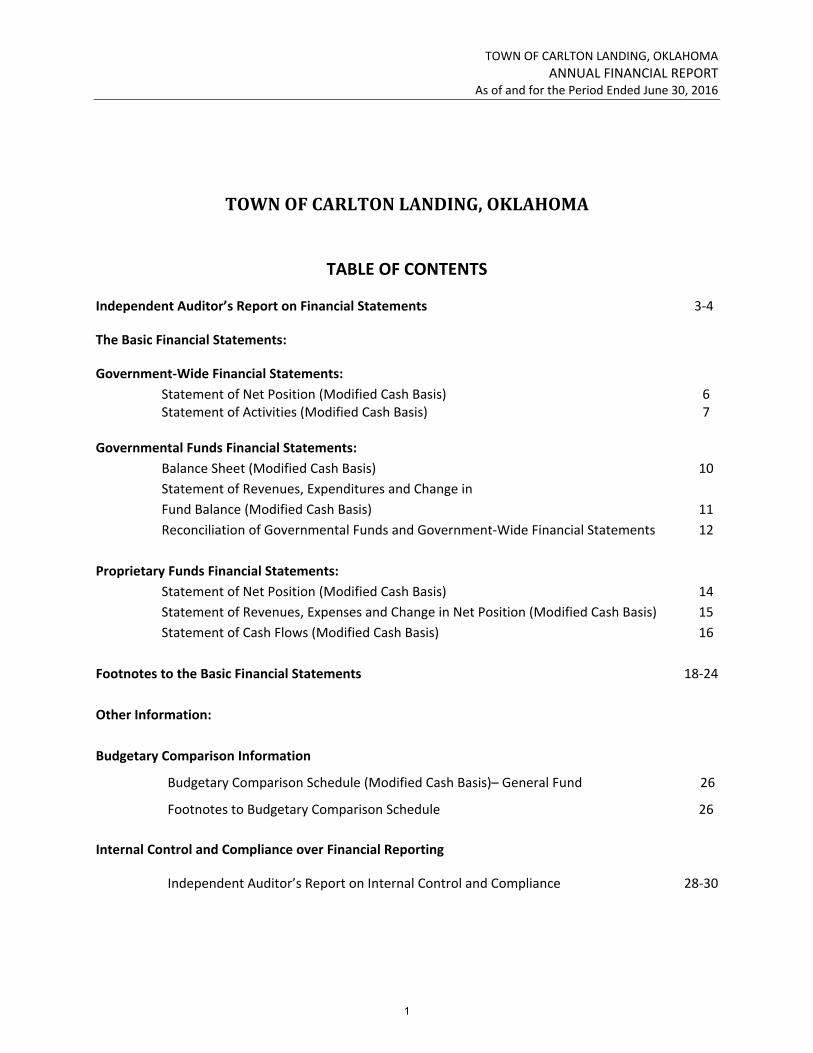

TABLE OF CONTENTS

Independent Auditor’s Report on Financial Statements 3‐4

The Basic Financial Statements:

Government‐Wide Financial Statements:

Statement of Net Position (Modified Cash Basis) 6 Statement of Activities (Modified Cash Basis) 7

Governmental Funds Financial Statements:

Balance Sheet (Modified Cash Basis) 10

Statement of Revenues, Expenditures and Change in

Fund Balance (Modified Cash Basis) 11

Reconciliation of Governmental Funds and Government‐Wide Financial Statements 12

Proprietary Funds Financial Statements:

Statement of Net Position (Modified Cash Basis) 14

Statement of Revenues, Expenses and Change in Net Position (Modified Cash Basis) 15

Statement of Cash Flows (Modified Cash Basis) 16

Footnotes to the Basic Financial Statements 18‐24

Other Information:

Budgetary Comparison Information

Budgetary Comparison Schedule (Modified Cash Basis)– General Fund 26

Footnotes to Budgetary Comparison Schedule 26

Internal Control and Compliance over Financial Reporting

Independent Auditor’s Report on Internal Control and Compliance 28‐30

1

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Board of Trustees

Joanne Chinnici Mayor Jeff Click Vice‐Mayor David Kimmel Craig McCollum

Trustee Trustee

Richard Hardway Trustee

Town Clerk and Treasurer

Jan Summers

10 Boulevard Unit G Carlton Landing, Oklahoma 74332

918‐452‐2218

2

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Elfrink and Associates, PLLC Members of the AICPA, OSCPA, and GFOA

3119 E 87th Street 918-361-2133 Tulsa, Oklahoma 74137 Fax: 918-512-4280

INDEPENDENT AUDITOR’S REPORT

To the Honorable Mayor and Board of Trustees Town of Carlton Landing, Oklahoma Report on the Financial Statements

We have audited the accompanying modified cash basis financial statements of the governmental activities, business‐type activities and each fund for the Town of Carlton Landing, Oklahoma, as of June 30, 2016 and for the year then ended, and the related notes to the financial statements, which collectively comprise the Town’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with the modified cash basis of accounting described in Note 1B; this includes determining that the modified cash basis of accounting is an acceptable basis for the preparation of the financial statements in the circumstances. Management is also responsible for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to error or fraud.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business‐type activities and each fund of

3

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

the Town of Carlton Landing, Oklahoma as of June 30, 2016, and the respective changes in financial position for the year then ended in accordance with the modified cash basis of accounting as described in Note 1B.

Basis of Accounting

We draw attention to Note 1B of the financial statements, which describes the basis of accounting. The financial statements are prepared on the modified cash basis of accounting, which is a special purpose framework other than accounting principles generally accepted in the United States of America. Our opinion is not modified with respect to that matter.

Disclaimer of Opinion on Other Information

Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the Town of Carlton Landing, Oklahoma’s basic financial statements. The budgetary comparison information is presented for purposes of additional analysis and is not a required part of the basic financial statements. Such information has not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on it.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated February 1, 2017 on our consideration of the Town’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Town’s internal control over financial reporting and compliance.

Elfrink and Associates, PLLC

Tulsa, Oklahoma February 1, 2017

4

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

BASIC FINANCIAL STATEMENTS – STATEMENTS OF NET POSITION AND

ACTIVITIES

5

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Statement of Net Position (Modified Cash Basis) – June 30, 2016

See accompanying notes to the basic financial statements

Governmental Business ‐ type

Activities Activities Total

Assets

Cash and cash equivalents 62,558$ ‐$ 62,558$

Due from CLEDT 24,590 ‐ 24,590

Capital assets:

Other capital assets, net of depreciation 11,750 64,874 76,624

Total current assets 98,898 64,874 163,772

Liabilities:

Due to the Town ‐ 24,590 24,590

Project Cost Advancements (related party) ‐ 161,317 161,317

Total liabilities ‐ 185,907 185,907

Net Position:

Net investment in capital assets 11,750 64,874 76,624

Unrestricted (deficit) 87,148 (185,907) (98,759)

Total net position (deficit) 98,898$ (121,033)$ (22,135)$

6

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Statement of Activities (Modified Cash Basis) – Year Ended June 30, 2016

See accompanying notes to the basic financial statements

Net (Expense) Revenue and

Change in Net Position

Charges for Governmental Business ‐type

Functions/Programs Expenses Services Activities Activities Total

Primary government:

Governmental activities:

General government 22,986$ 1,356$ (21,630)$ ‐$ (21,630)$

Public Safety 3,000 ‐ (3,000) ‐ (3,000)

Highways and streets 240 ‐ (240) ‐ (240)

Total governmental activities 26,226 ‐ (24,870) ‐ (24,870)

Business‐type activities:

Economic Development 121,033 ‐ (121,033) (121,033)

Total primary government 147,259$ ‐$ (24,870) (121,033) (145,903)

General revenues:

Taxes:

Sales 89,693 ‐ 89,693

Intergovernmental revenue 1,064 ‐ 1,064

Total general revenues 90,757 ‐ 90,757

Change in net position 65,887 (121,033) (55,146)

Net position ‐ beginning 33,011 ‐ 33,011

Net position ‐ ending 98,898$ (121,033)$ (22,135)$

7

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

THIS PAGE INTENTIONALLY LEFT BLANK

8

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

BASIC FINANCIAL STATEMENTS – GOVERNMENTAL FUNDS

9

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Balance Sheet (Modified Cash Basis) ‐ June 30, 2016

See accompanying notes to the basic financial statements

General

Fund

Assets:

Cash and cash equivalents 62,558$

Due from Trust 24,590

Total Assets 87,148$

Fund Balance:

Unrestricted:

Unassigned 87,148$

Total Fund Balance 87,148$

10

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

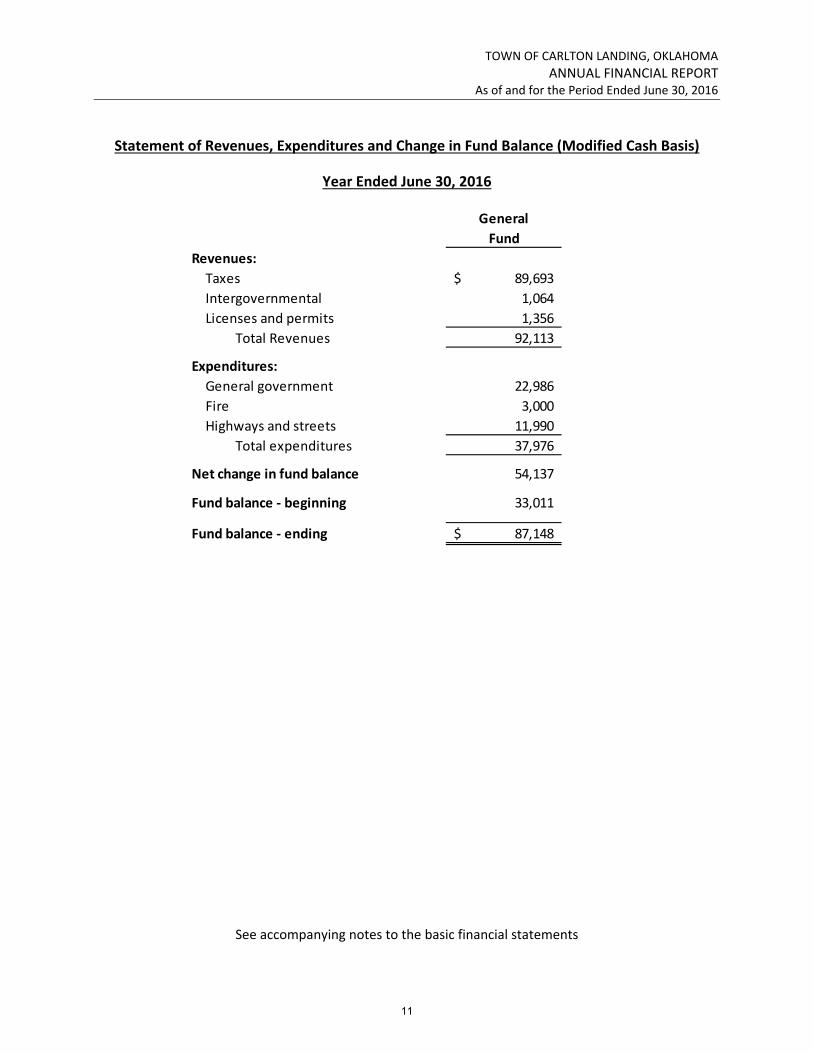

Statement of Revenues, Expenditures and Change in Fund Balance (Modified Cash Basis)

Year Ended June 30, 2016

See accompanying notes to the basic financial statements

General

Fund

Revenues:

Taxes 89,693$

Intergovernmental 1,064

Licenses and permits 1,356

Total Revenues 92,113

Expenditures:

General government 22,986

Fire 3,000

Highways and streets 11,990

Total expenditures 37,976

Net change in fund balance 54,137

Fund balance ‐ beginning 33,011

Fund balance ‐ ending 87,148$

11

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

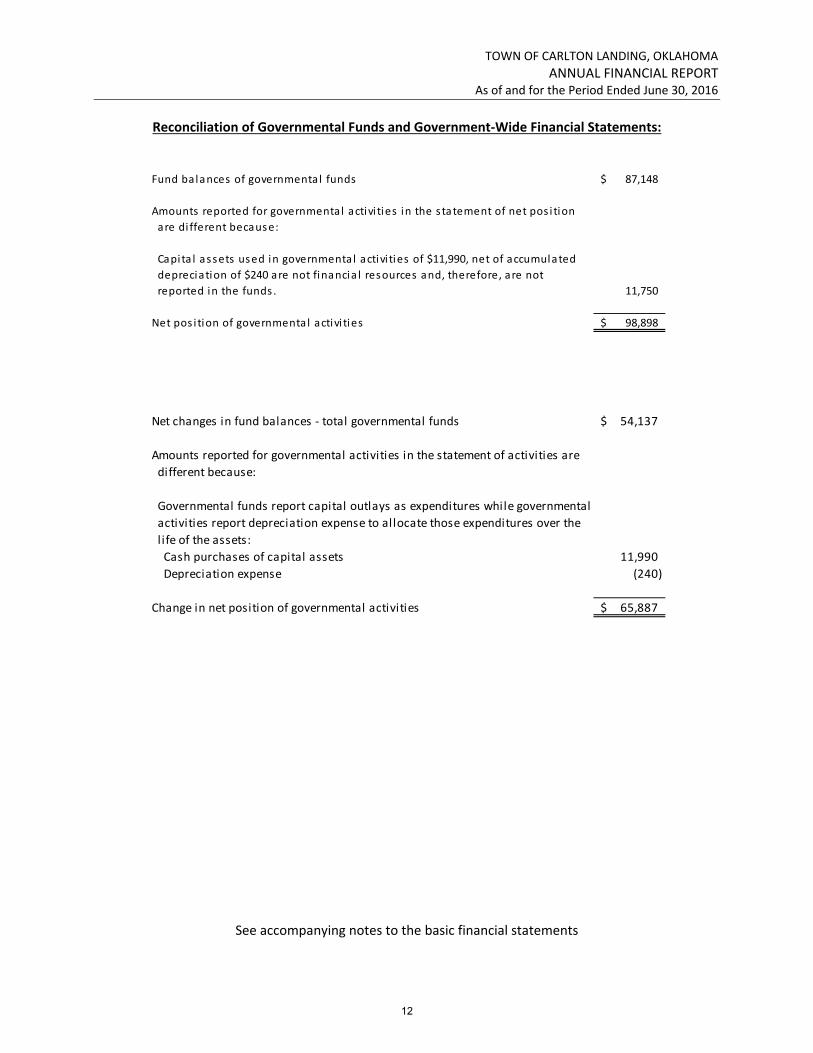

Reconciliation of Governmental Funds and Government‐Wide Financial Statements:

See accompanying notes to the basic financial statements

Fund balances of governmental funds 87,148$

Amounts reported for governmental activi ties in the s tatement of net pos i tion

are di fferent because:

Capi ta l assets used in governmental activi ties of $11,990, net of accumulated

depreciation of $240 are not financia l resources and, therefore, are not

reported in the funds . 11,750

Net pos i tion of governmenta l activi ties 98,898$

Net changes in fund balances ‐ total governmental funds 54,137$

Amounts reported for governmental activities in the statement of activities are

different because:

Governmental funds report capital outlays as expenditures while governmental

activities report depreciation expense to allocate those expenditures over the

l ife of the assets:

Cash purchases of capital assets 11,990

Depreciation expense (240)

Change in net position of governmental activities 65,887$

12

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

BASIC FINANCIAL STATEMENTS – PROPRIETARY FUNDS

13

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Proprietary Fund Statement of Net Position (Modified Cash Basis) – June 30, 2016

See accompanying notes to the basic financial statements

Carlton Landing

Economic Development Trust

ASSETS

Construction in Progress 64,874$

Total assets 64,874

LIABILITIES

Due to Town 24,590

Project Cost Advancements 161,317

Total liabilities 185,907

NET POSITION

Unrestricted (deficit) (121,033)

Total net position (deficit) (121,033)$

14

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Proprietary Fund Statement of Revenues, Expenses and Change in Net Position (Modified Cash Basis)

– Year Ended June 30, 2016

See accompanying notes to the basic financial statements

Carlton Landing

Economic Development Trust

Operating expenses:

Project Planning Expenses 44,820$

Legal Fees 76,213

Total operating expenses 121,033

Change in net position (121,033)

Net position ‐ beginning ‐

Net position ‐ ending (deficit) (121,033)$

15

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Proprietary Fund Statement of Cash Flows (Modified Cash Basis) – Year Ended June 30, 2016

See accompanying notes to the basic financial statements

Carlton Landing

Economic Development Trust

Cash flows from operating activities:

Other operating payments (121,033)$

Net cash used in operating activities (121,033)

Cash flows from non‐capital financing activities:

Increase in Due to Town 24,590

Proceeds from Project Cost Advancements 161,317

Net cash flows from non‐capital financing activities 185,907

Cash flows from capital and related financial activities:

Purchase of capital assets (64,874)

Net cash used in capital and related financing activities (64,874)

Net Change in cash ‐

Reconciliation of operating income to net cash provided:

Operating loss (121,033)$

16

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

FOOTNOTES TO THE BASIC FINANCIAL STATEMENTS

17

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Notes to the Basic Financial Statements

1. Summary of Significant Accounting Policies

A. Financial Reporting Entity

The Town of Carlton Landing, Oklahoma was established on October 21, 2013 to establish and operate public safety, streets, health and welfare, culture and recreation, and administrative activities for the citizens of the Town. The Town’s financial reporting entity is comprised of the following:

Primary Government: Town of Carlton Landing

Component Unit: Carlton Landing Economic Development Trust

In determining the financial reporting entity, the Town complies with the provisions of Governmental Accounting Council Statement No. 14, as amended by Statement No. 61, The Financial Reporting Entity, and includes all component units for which the Town is financially accountable.

Blended Component Unit

Carlton Landing Economic Development Trust – (“CLEDT”) – Created July 19, 2014 to finance, operate, develop, construct, maintain, manage, market, and administer projects for investment and reinvestment on behalf of the Town. The Town’s Board of Trustees also serve as Trustees for the CLEDT.

The component unit is a Public Trust pursuant to Title 60 of Oklahoma State law. Public Trusts have no taxing power. Public Trusts are generally created to finance Town services through issuance of revenue bonds or other non‐general obligation debt and to enable the Town Board of Trustees to delegate certain functions to the governing body of the Trust. The Trust generally retains title to assets which are acquired or constructed with Trust debt or other Trust‐generated resources. The Town, as beneficiary of the Public Trust, receives title to any residual assets when a Public Trust is dissolved.

B. Basis of Presentation and Accounting Government‐Wide Financial Statements: The statements of net position and activities are reported on a modified cash basis of accounting. The modified cash basis of accounting is based on the recording of cash and cash equivalents and changes therein, and only recognizes revenues, expenses, assets and liabilities resulting from cash transactions adjusted only for certain modifications stated below that have substantial support in generally accepted accounting principles (GAAP). These modifications include adjustments for the following balances arising from cash transactions:

capital assets and the depreciation of those assets, where applicable

cash‐based interfund receivables and payables

other cash‐based receivables/payable

18

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

cash transactions for amounts paid on behalf of the entity by other parties

As a result of the use of this modified cash basis of accounting, certain assets and their related revenues (such as accounts receivable and revenue for billed or provided services not yet collected, and accrued revenue and receivables) and certain liabilities and their related expenses (such as accounts payable and expenses for goods or services received but not yet paid, and accrued expenses and liabilities) are not recorded in these financial statements.

The statement of activities presents a comparison between the expenses and program revenues directly associated with different governmental functions to arrive at the net revenue or expense of the function or activity prior to the use of taxes and other general revenues. Program revenues include (1) fees, and service charges generated by the program or activity, (2) operating grants and contributions that are restricted to meeting the operational requirements of the program or activity, and (3) capital grants and contributions that are restricted to meeting the capital requirements of the program or activity and include assets donated by developers. These revenues are subject to externally imposed restrictions to these program uses. The Town does not currently have any program revenues. Taxes and other revenue sources not properly included with program revenues are reported as general revenues.

Governmental Funds:

Currently the Town has only one fund – the General Fund – which accounts for all activities. The governmental funds are reported on a modified cash basis of accounting and current financial resources measurement focus. Only current financial assets and liabilities are generally included on the fund balance sheets. The operating statements present sources and uses of available spendable financial resources during a given period. These fund financial statements use fund balance as their measure of available spendable financial resources at the end of the period.

Proprietary Funds:

The Town accounts for all proprietary activities through the Carlton Landing Economic Development Trust. For purposes of the statement of revenues, expenses and changes in fund net position, operating revenues and expenses are considered those whose cash flows are related to operating activities, while revenues and expenses related to financing, capital and investing activities are reported as non‐operating or transfers and contributions.

The general fund is legally required to adopt an annual budget or appropriations. The public trust (CLEDT) is not required to adopt legal annual appropriations. While the trust develops an annual budget that is required to be approved by the Town (its beneficiary), it is for financial management purposes and does not constitute legal appropriations.

C. Cash, Cash Equivalents, and Investments

Cash and cash equivalents includes all demand and savings accounts, certificates of deposit or short‐term investments with an original maturity of three months or less, and money market accounts. Investments consist of long‐term certificates of deposit and are reported at cost.

19

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

D. Capital Assets and Depreciation

Reported capital assets are limited to those acquired with cash and cash equivalents consistent with the modified cash basis of accounting. The accounting treatment of property, plant and equipment (capital assets) depends on whether the assets are used in governmental fund type or proprietary fund operations and whether they are reported in the government‐wide or fund financial statements. In the government‐wide and proprietary fund financial statements, property, plant and equipment are accounted for as capital assets, net of accumulated depreciation where applicable. In the governmental fund financial statements, capital assets acquired are accounted for as capital outlay expenditures and not reported as capital assets.

Capital assets consist of buildings and building improvements, construction in progress, utility systems, machinery and equipment, and furniture. A capitalization threshold of $2,000 is used to report capital assets.

Depreciable capital assets are depreciated on a straight‐line basis over their estimated useful lives. The estimated useful lives by type of asset are as follows:

Infrastructure 50 years

E. Fund Balances and Net position

Government‐wide Financial Statements: Equity is classified as net position and displayed in three components: 1. Net investment in capital assets – Consists of capital assets including restricted capital assets,

net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowings that are attributed to the acquisition, construction, or improvement of those assets.

2. Restricted net position – Consists of net assets with constraints placed on the use by 1) external groups such as creditors, grantors, contributors, or laws and regulations of other governments, or 2) law through constitutional provisions or enabling legislation.

3. Unrestricted net position‐ All other net assets that do not meet the definition of “restricted” or “net investment in capital assets”.

It is the Town’s policy to first use restricted net position prior to the use of unrestricted net position when an expense is incurred for purposes for which restricted and unrestricted net position are available.

Fund Financial Statements: Governmental fund equity is classified as fund balance. Fund balance is further classified as nonspendable, restricted, committed, assigned, and unassigned. These classifications are defined as:

Nonspendable – includes amounts that cannot be spent because they are either (a) not in spendable form or (b) legally required to be maintained intact.

Restricted ‐ consists of fund balance with constraints placed on the use of resources either by (1) external groups such a creditors, grantors, contributors, or laws or regulations of other governments, or (2) laws through constitutional provisions or enabling legislation

20

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Unrestricted: Committed – includes unrestricted amounts that can only be used for specific purposes pursuant to constraints imposed by formal action of the Town’s highest level of decision‐making authority. The Town’s highest level of decision‐making authority is made by ordinance. Assigned – includes unrestricted amounts that are constrained by the Town’s intent to be used for specific purposes but are neither restricted nor committed. Assignments of fund balance may be made by Town Board action or management decision when the Town’s Board has delegated that authority. Assignments for transfers and interest income for governmental funds are made through budgetary process. Unassigned – all remaining unrestricted fund balances not reported as committed or assigned.

It is the Town’s policy to first use restricted fund balance prior to the use of unassigned fund balance when an expense is incurred for purposes for which both restricted and unrestricted fund balance are available. The Town’s policy for the use of fund balance amounts require that restricted amounts would be reduced first, followed by committed amounts and then assigned amounts when expenditures are incurred for purposes for which amounts in any of those unrestricted fund balance classifications could be used.

F. Internal and Inter‐fund Balances and Transfers

The Town’s policy is to eliminate inter‐fund transfers and balances in the statement of activities and net position to avoid the grossing up of balances. Only the residual balances transferred between governmental and business‐type activities are reported as internal transfers and internal balances then offset in the total column in the government‐wide statements. Internal transfers and balances between funds are not eliminated in the fund financial statements.

G. Use of Estimates

Certain estimates are made in the preparation of the financial statements, such as estimated lives for capital assets depreciation

H. Revenues and expenses

Sales Tax The Town levies a three‐cent sales tax on taxable sales within the Town. The sales tax is collected by the Oklahoma Tax Commission and remitted to the Town in the month following receipt by the Tax Commission.

Expenses In the government‐wide financial statements, expenses, including depreciation of capital assets, are reported by function or activity. In the governmental fund financial statements, expenditures are reported by class as current (further reported by function), capital outlay and debt service.

2. Detailed Notes on Transaction Classes/Accounts

A. Deposits and Investments ‐ at June 30, 2016, the Town’s cash balance of $62,558 was held in a bank demand deposit account.

21

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Custodial Credit Risk Custodial credit risk is the risk that in the event of a bank failure, the government deposits may not be returned to it. The Town is governed by the State Public Deposit Act which requires the Town obtain and hold collateral whose fair value exceeds the amount of uninsured deposits. Investment securities are exposed to custody credit risk if the securities are uninsured, are not registered in the name of the government, and if held by either a counterparty or a counterparty’s trust, department or agent, but not in the government’s name.

As of June 30, 2016, the Town was not exposed to custodial credit risk as defined above.

B. Property Tax Levy

As of June 30, 2016, the Town has not levied any property tax. In accordance with state law, a municipality may only levy a property tax to retire general obligation debt approved by the voters and to pay judgments rendered against the Town.

C. General Obligation Bond Referendum

On February 9, 2016, the qualified voters of the Town of Carlton Landing approved the levy of additional property tax to fund a fire station, parks and recreational facilities, arts and cultural facilities, community buildings, drainage control improvements, and street lighting in the total amount of $9.5 million.

D. Capital Assets and Depreciation

For the year ended June 30, 2016, capital asset balances changed as follows:

Balance at Balance at

July 1, 2015 Additions Deductions June 30, 2016

Governmental:

Capita l assets being depreciated:

Infrastructure ‐$ 11,990$ ‐$ 11,990$

Tota l capi ta l assets being depreciated ‐ 11,990 ‐ 11,990

Less accumulated depreciation:

Infrastructure ‐ 240 ‐ 240

Tota l accumulated depreciation ‐ 240 ‐ 240

Governmenta l , net capi ta l assets ‐$ 11,750$ ‐$ 11,750$

Business‐type:

Capita l assets not being depreciated:

Construction in progress ‐$ 64,874$ ‐$ 64,874$

Bus iness ‐type, net capi ta l assets ‐$ 64,874$ ‐$ 64,874$

22

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

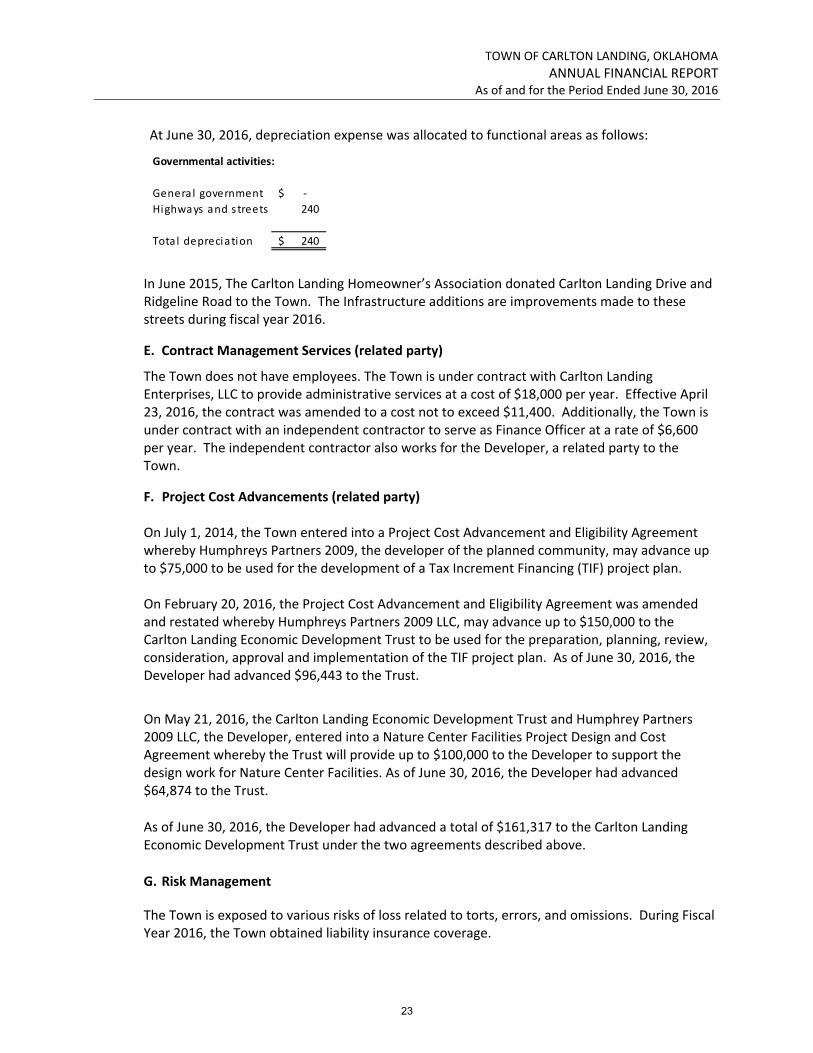

At June 30, 2016, depreciation expense was allocated to functional areas as follows:

In June 2015, The Carlton Landing Homeowner’s Association donated Carlton Landing Drive and Ridgeline Road to the Town. The Infrastructure additions are improvements made to these streets during fiscal year 2016.

E. Contract Management Services (related party)

The Town does not have employees. The Town is under contract with Carlton Landing Enterprises, LLC to provide administrative services at a cost of $18,000 per year. Effective April 23, 2016, the contract was amended to a cost not to exceed $11,400. Additionally, the Town is under contract with an independent contractor to serve as Finance Officer at a rate of $6,600 per year. The independent contractor also works for the Developer, a related party to the Town.

F. Project Cost Advancements (related party) On July 1, 2014, the Town entered into a Project Cost Advancement and Eligibility Agreement whereby Humphreys Partners 2009, the developer of the planned community, may advance up to $75,000 to be used for the development of a Tax Increment Financing (TIF) project plan. On February 20, 2016, the Project Cost Advancement and Eligibility Agreement was amended and restated whereby Humphreys Partners 2009 LLC, may advance up to $150,000 to the Carlton Landing Economic Development Trust to be used for the preparation, planning, review, consideration, approval and implementation of the TIF project plan. As of June 30, 2016, the Developer had advanced $96,443 to the Trust.

On May 21, 2016, the Carlton Landing Economic Development Trust and Humphrey Partners 2009 LLC, the Developer, entered into a Nature Center Facilities Project Design and Cost Agreement whereby the Trust will provide up to $100,000 to the Developer to support the design work for Nature Center Facilities. As of June 30, 2016, the Developer had advanced $64,874 to the Trust.

As of June 30, 2016, the Developer had advanced a total of $161,317 to the Carlton Landing Economic Development Trust under the two agreements described above.

G. Risk Management

The Town is exposed to various risks of loss related to torts, errors, and omissions. During Fiscal Year 2016, the Town obtained liability insurance coverage.

Governmental activities:

General government ‐$

Highways and s treets 240

Tota l depreciation 240$

23

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

H. Commitments and Contingencies

The Town is not involved in any legal proceedings, which normally occur in the course of operations, at this time. While legal proceedings cannot be foreseen, the Town believes that any settlement or judgment would not have a material effect on the financial condition of the Town.

I. Subsequent Events

In November 2016, the Town Trustees authorized the sale of $225,000 in general obligation bonds for park and recreational facilities approved by the qualified voters of the Town during the February 9, 2016 election. On December 14, 2016, the Town Trustees sold the $225,000 general obligation bond, series 2017, to the bidder with the lowest interest cost of 4%. The first principal payment will be due April 1, 2019.

Management has considered events through the date of this report and determined that no additional disclosures are necessary.

24

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

OTHER INFORMATION

25

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Budgetary Comparison Schedule (Modified Cash Basis) – Year Ended June 30, 2016 – UNAUDITED

Footnotes to the Budgetary Comparison Schedule:

1. The budgetary comparison schedule is reported on the same modified cash basis as governmental funds within the basic financial statements

2. The legal level of appropriation control is the department level within a fund. Transfers of appropriation within a fund require Mayor’s approval, while supplemental appropriations require approval of the Town’s Board of Trustees.

Variance with

Actual Final Budget

Original Final Amounts Positive (Negative)

Beginning budgetary fund balance ‐$ ‐$ 33,011$ 33,011$

Resources (inflows):

Taxes 78,000 78,000 89,693 11,693

Intergovernmental ‐ ‐ 1,064 1,064

Licenses and permits ‐ ‐ 1,356 1,356

Advances from related party 18,750 18,750 ‐ (18,750)

Total resources (inflows) 96,750 96,750 92,113 (4,637)

Amounts available for appropriation 96,750 96,750 125,124 28,374

Charges to appropriations (outflows):

General government:

Legal fees 48,750 48,750 5,200 43,550

Management Fees 18,000 18,000 3,521 14,479

Other operations & maintenance 15,250 15,250 14,265 985

Total general government 82,000 82,000 22,986 59,014

Fire 3,000 3,000 3,000 ‐

Street and alleys 11,750 11,750 11,990 (240)

Total charges to appropriations 96,750 96,750 37,976 58,774

Ending budgetary fund balance ‐$ ‐$ 87,148$ 87,148$

GENERAL FUND

Budgeted Amounts

26

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

INTERNAL CONTROL AND COMPLIANCE

27

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

Elfrink and Associates, PLLC Members of the AICPA, OSCPA, and GFOA

3119 E 87th Street 918-361-2133 Tulsa, Oklahoma 74137 Fax: 918-512-4280

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED

IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Honorable Mayor and the Board of Trustees Town of Carlton Landing, Oklahoma

We have audited the modified cash basis financial statements of the Town of Carlton Landing, Oklahoma (“Town”), as of June 30, 2016 and for the year then ended, and the related notes to the financial statements, which collectively comprise the Town’s basic financial statements and have issued our report thereon dated February 1, 2017. As described in Note 1B, the Town of Carlton Landing, Oklahoma has elected to report on a modified cash basis of accounting, which is a special purpose framework other than accounting principles generally accepted in the United States of America. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States.

Internal Control Over Financial Reporting

Management of the Town is responsible for establishing and maintaining effective internal control over financial reporting. In planning and performing our audit, we considered the Town’s internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Town’s internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the Town’s internal control over financial reporting.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses, or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Town’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with

28

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed an instance of noncompliance or other matter that is required to be reported under Government Auditing Standards, described in the accompanying schedule of findings and responses as 2016‐01.

Purpose of This Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Town’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Town’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Elfrink and Associates, PLLC

Tulsa, Oklahoma February 1, 2017

29

TOWN OF CARLTON LANDING, OKLAHOMA

ANNUAL FINANCIAL REPORT As of and for the Period Ended June 30, 2016

SCHEDULE OF FINDINGS AND MANAGEMENT RESPONSES

This schedule is presented as an addendum to accompany the “Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards”. Consideration of items listed should be made in conjunction with that report.

2016‐01 – Project Cost Advancements –

CONDITION: The Town, and the Carlton Landing Economic Development Trust (CLEDT) entered into a Project Cost Advancement and Eligibility Agreement (Agreement) with Humphreys Partners 2009 LLC (Developer). The Developer agrees to advance reasonable costs associated with the preparation, planning, review, consideration, approval and implementation of the Project Plan at a cost not to exceed $150,000, to be reimbursed when the CLEDT begins receiving ad valorem taxes under the Tax Increment Financing plan. The Agreement requires the submission of detailed invoices for review and approval. Not all invoices payable under the Agreement have been submitted for review and approval. The Developer is incurring expenses prior to approval of the CLEDT Board as to the actual cost and nature of the expenditures.

POTENTIAL EFFECT OF CONDITION: The CLEDT Board could authorize payment of funds not properly supported by purchase orders and itemized detail invoices. The CLEDT Board could authorize payment for goods and services outside of the scope of the Advancement and Eligibility Agreement and/or expenditures that may not be advantageous to the public interest of the CLEDT.

CAUSE OF CONDITION: The CLEDT Board has not established operating procedures for review and approval of the cost and nature of the expenditures prior to the commitment and expenditure of funds by the Developer. The CLEDT Board has not issued purchase orders for the expenditures being advanced by the Developer.

CRITERIA: Title 62 Chapter2 Section 310.1 of the Oklahoma Statutes requires that the purchasing officer submit purchase orders or contracts prior to the time of the commitment. Additionally, that Statute requires that after delivery of merchandise or completion of a contract, the supplier shall deliver an invoice. The invoice must be sufficiently itemized to clearly describe each item purchased, its unit price, the number or volume of each item purchased, its total price, the total of the purchase and the date of the purchase. All payments shall be supported by a detailed invoice and that the invoice, purchase order, and other supporting data be submitted to the governing board for consideration of payment.

RECOMMENDATION: The CLEDT Board review and consider approval of the expenditures funded to date through the Developer’s advances. The CLEDT Board implement a procedure to review and approve purchase orders to the entity providing goods or services prior to commitment of funds or recognition of the obligation to reimburse the Developer. The CLEDT Board complete the purchasing cycle for all transactions in a timely manner. The CLEDT Board document the review and approval of the expenditures in the meeting agendas and minutes, when required by policy or statute, prior to recognizing the obligation for reimbursement to the Developer.

MANAGEMENT’S RESPONSE: The Town’s management will follow the established purchase procedure, including approval in advance of commitment, for all purchases of goods and services, including the accrued liabilities that are paid on behalf of the Carlton Landing Economic Development Trust by the developer.

30

Related Documents