Analysing Impact of AS 30, 31, 32 on Banks Finan cial Servi ces Indust ry – Emer ging Trends, Challenges & Way Forward WIRC of ICAI November 20, 2009 Presented by :‐ Ashutosh Pednekar Partner, M P Chitale & Co. 2 Ashutosh Pednekar, Partner, M. P. Chitale & Co. Disclaimers These are my personal views and can not be construed to be the views of M/s.M. P. Chitale & Co., Chartered Accountants ICAI has no responsibility for its contents These views do not and shall not be considered as a professional advice. This presentation should not be reproduced in part or in whole, in any manner or form, without my written permission.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 1/33

Analysing Impact of AS

30, 31, 32 on Banks

Financial Services Industry – Emerging

Trends, Challenges & Way Forward

WIRC of ICAINovember 20, 2009 Presented by :‐

Ashutosh Pednekar Partner, M P Chitale & Co.

2 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Disclaimers

These are my personal views and can not be construed to

be the views of M/s.M. P. Chitale & Co., Chartered

Accountants

ICAI has no responsibility for its contents

These views do not and shall not be considered as a

professional advice.

This presentation should not be reproduced in part or in

whole, in any manner or form, without my written

permission.

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 2/33

3 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Why an AS for Financial Instruments ?

Globalisation of Indian Economy;

Increasing sophistication of financial products andmarkets;

Increased use of derivatives for risk mitigation andtrading;

No comprehensive standard until now (AS -13, AS - 11

and AS - 16 partly deal with the same);

Diverse practices made comparability of performance

difficult.

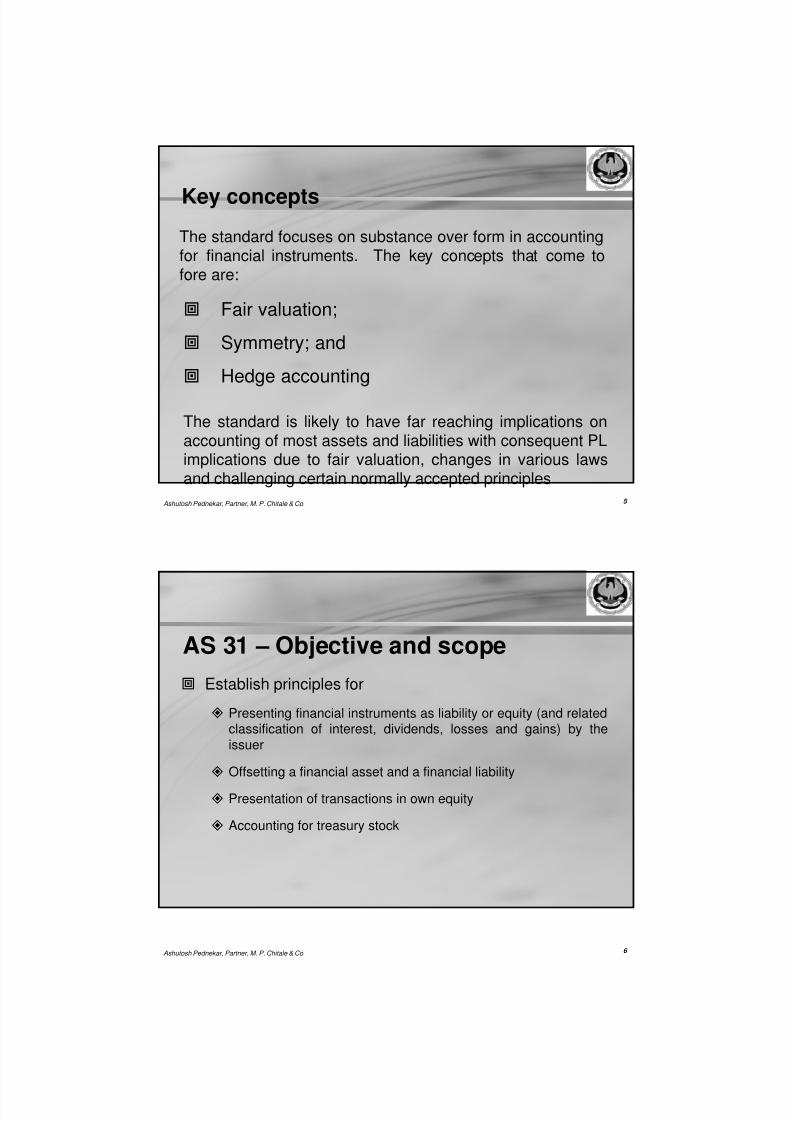

4 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

AS for financial instruments

Recognition

and

derecognition

of

financial

instruments

Measurement

of

financial

instruments

Derivatives

and

hedge

accounting

AS 30

Presentation

AS 31

Disclosure

AS 32

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 3/33

5 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Key concepts

Fair valuation;

Symmetry; and

Hedge accounting

The standard focuses on substance over form in accountingfor financial instruments. The key concepts that come tofore are:

The standard is likely to have far reaching implications onaccounting of most assets and liabilities with consequent PLimplications due to fair valuation, changes in various lawsand challenging certain normally accepted principles

6 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

AS 31 – Objective and scope

Establish principles for

Presenting financial instruments as liability or equity (and relatedclassification of interest, dividends, losses and gains) by theissuer

Offsetting a financial asset and a financial liability

Presentation of transactions in own equity

Accounting for treasury stock

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 4/33

7 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Financial

asset

&

Financial instruments – definition

Contract that gives rise toboth a financial asset of one

entity

Financial

liability

Equity

instrument

A financial liability and /or anequity

instrument of another entity

8 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Financial instruments – examples

Financial assets and liabilities

Trade receivables and payables

Loans receivable and payable

Deposits and advances

Perpetual debt instruments

Contractual rights arising on contingent assets – eg. Guarantees

Finance leases

Following are not financial assets and instruments

Physical assets such as property, plant and equipment

Prepaid expenses (associated with the delivery of goods and servicesand not contractual obligation to pay cash or another financial asset).

Liabilities that are not of a contractual nature (such as income taxes)

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 5/33

9 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

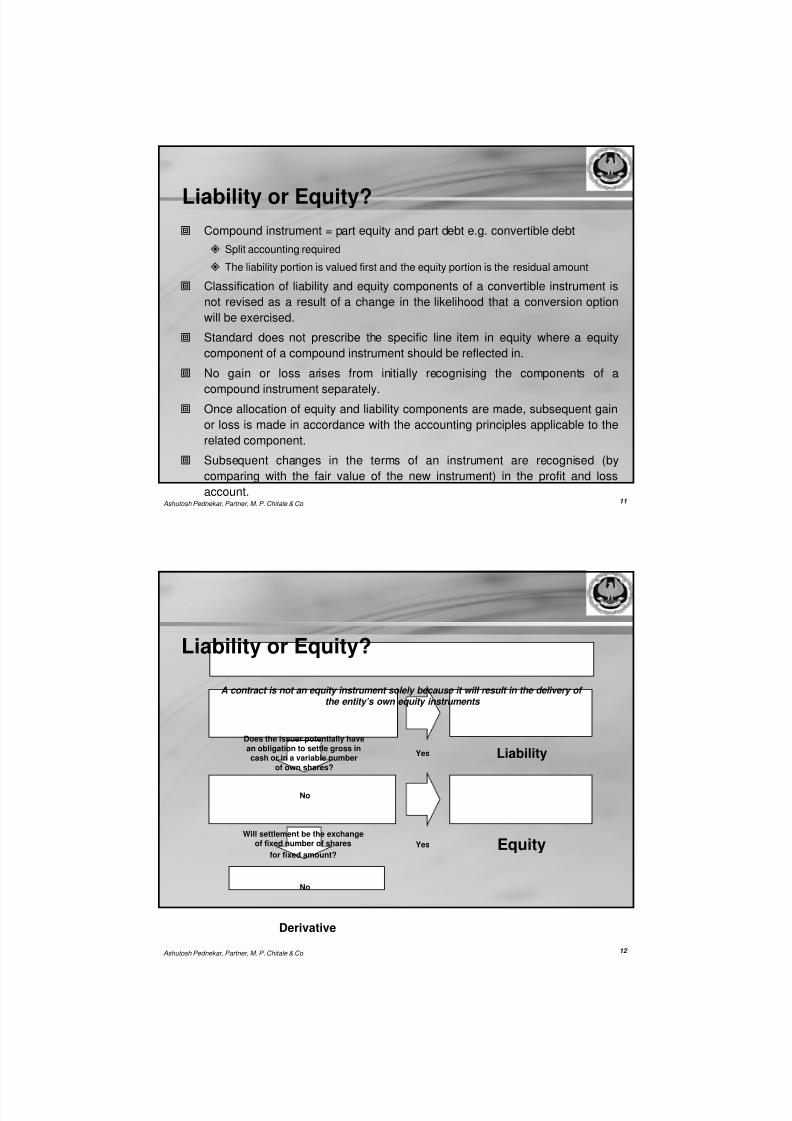

Financial instruments – examples…

Equity instruments

Equity shares

Irredeemable preference shares

Portion of preference shares having discretionary dividends afterreducing liability component

Warrants / written call options that are settled by a fixed number ofown instruments for a fixed amount of cash or another financialasset (equity option component of a convertible bond/debenture)

Derivative financial instruments

Options, futures, forwards, interest rate swaps, currency swapsetc.

IMPACT ANALYSIS

New concept for Indian GAAP

10 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Liability or Equity?

Financial instrument is an equity instrument only if both criteria aremet:

There is no obligation to deliver cash or another financial asset or toexchange financial assets or financial liability; and

The issuer will exchange fixed amount of cash or another financial assetfor a fixed number of its own equity instruments.

Does the entity have an unavoidable contractual obligation to deliver or exchange?

Yes No

Liability Equity

When there is a statutory requirement for classification as equity or liability,compliance with law = compliance with AS

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 6/33

11Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Liability or Equity? Compound instrument = part equity and part debt e.g. convertible debt

Split accounting required

The liability portion is valued first and the equity portion is the residual amount

Classification of liability and equity components of a convertible instrument is

not revised as a result of a change in the likelihood that a conversion option

will be exercised.

Standard does not prescribe the specific line item in equity where a equity

component of a compound instrument should be reflected in.

No gain or loss arises from initially recognising the components of a

compound instrument separately. Once allocation of equity and liability components are made, subsequent gain

or loss is made in accordance with the accounting principles applicable to the

related component.

Subsequent changes in the terms of an instrument are recognised (by

comparing with the fair value of the new instrument) in the profit and loss

account.

12 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Liability or Equity?

Does the issuer potentially have

an obligation to settle gross incash or in a variable number

of own shares?

Will settlement be the exchangeof fixed number of shares

for fixed amount?

Liability

Equity

Derivative

No

No

Yes

Yes

A contract is not an equity instrument solely because it will result in the delivery of the entity’s own equity instruments

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 7/33

13 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

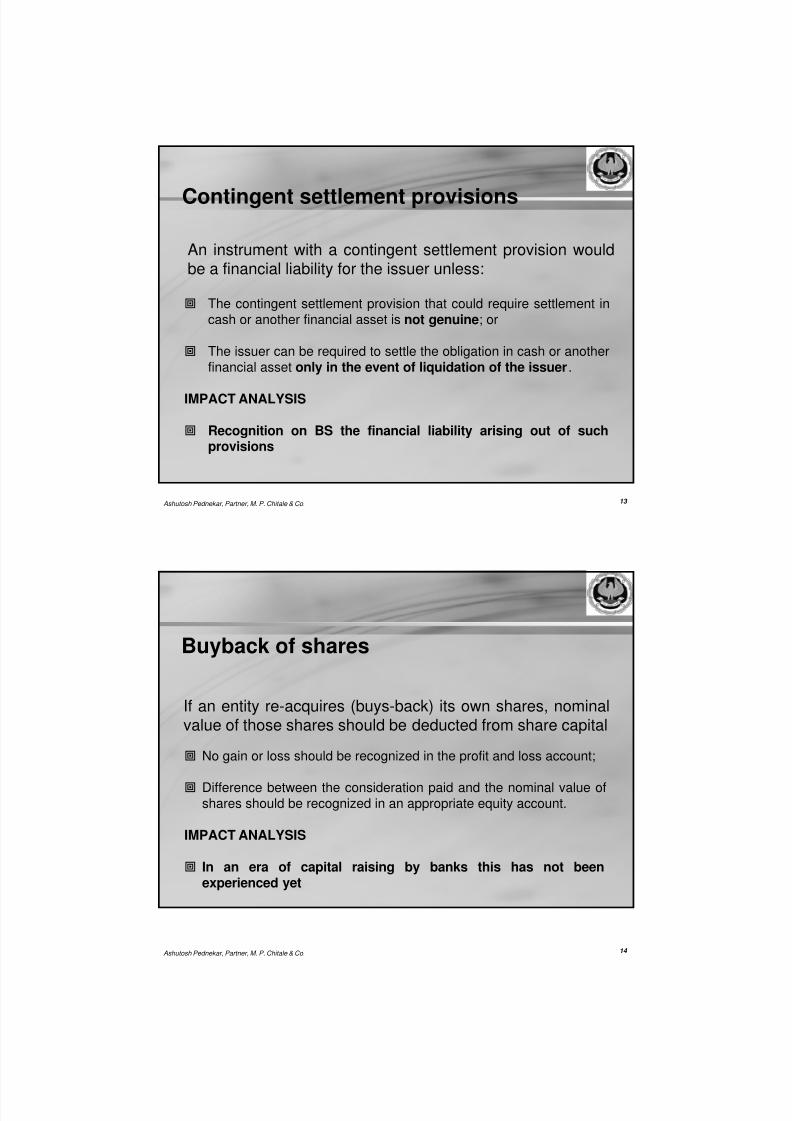

Contingent settlement provisions

An instrument with a contingent settlement provision wouldbe a financial liability for the issuer unless:

The contingent settlement provision that could require settlement incash or another financial asset is not genuine; or

The issuer can be required to settle the obligation in cash or anotherfinancial asset only in the event of liquidation of the issuer.

IMPACT ANALYSIS

Recognition on BS the financial liability arising out of suchprovisions

14 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Buyback of shares

If an entity re-acquires (buys-back) its own shares, nominalvalue of those shares should be deducted from share capital

No gain or loss should be recognized in the profit and loss account;

Difference between the consideration paid and the nominal value ofshares should be recognized in an appropriate equity account.

IMPACT ANALYSIS

In an era of capital raising by banks this has not beenexperienced yet

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 8/33

15 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

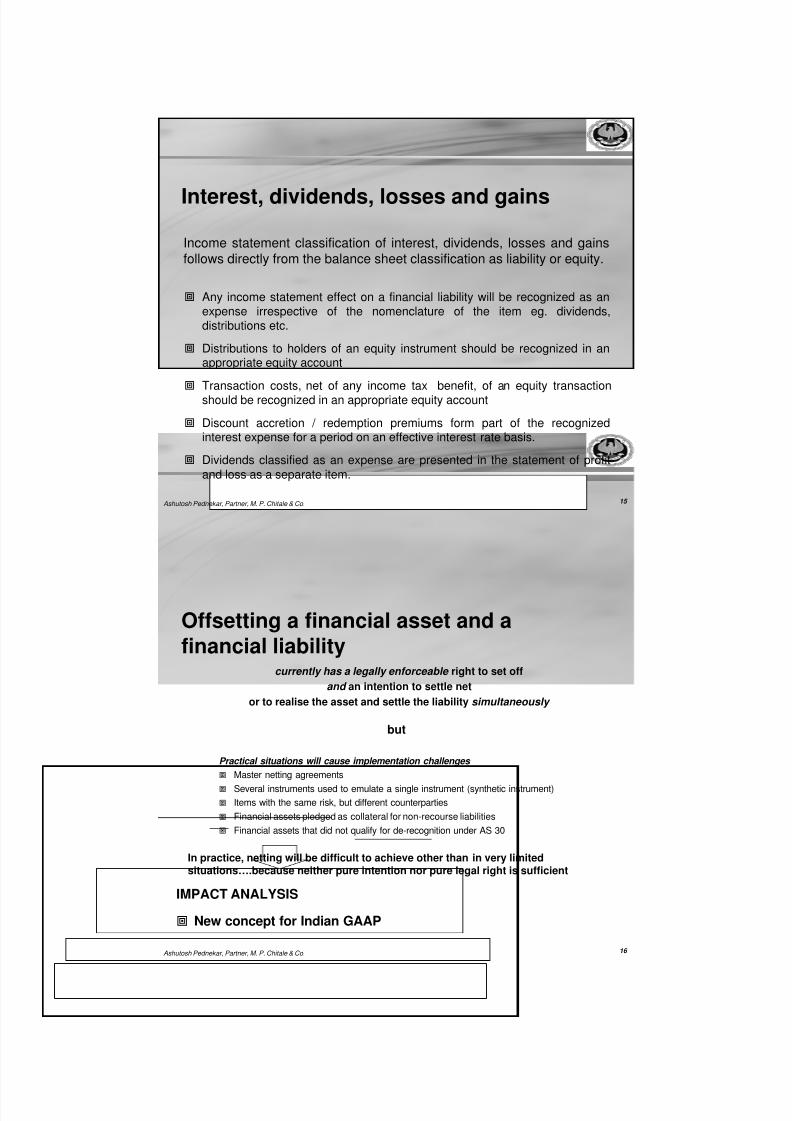

Interest, dividends, losses and gains

Income statement classification of interest, dividends, losses and gainsfollows directly from the balance sheet classification as liability or equity.

Any income statement effect on a financial liability will be recognized as anexpense irrespective of the nomenclature of the item eg. dividends,distributions etc.

Distributions to holders of an equity instrument should be recognized in anappropriate equity account

Transaction costs, net of any income tax benefit, of an equity transactionshould be recognized in an appropriate equity account

Discount accretion / redemption premiums form part of the recognizedinterest expense for a period on an effective interest rate basis.

Dividends classified as an expense are presented in the statement of profit

and loss as a separate item.

16 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Offsetting a financial asset and afinancial liability

currently has a legally enforceable right to set off

and an intention to settle net

or to realise the asset and settle the liability simultaneously

Practical situations will cause implementation challenges

Master netting agreements

Several instruments used to emulate a single instrument (synthetic instrument)

Items with the same risk, but different counterparties

Financial assets pledged as collateral for non-recourse liabilities

Financial assets that did not qualify for de-recognition under AS 30

but

In practice, netting will be difficult to achieve other than in very limitedsituations….because neither pure intention nor pure legal right is sufficient

IMPACT ANALYSIS

New concept for Indian GAAP

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 9/33

17 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

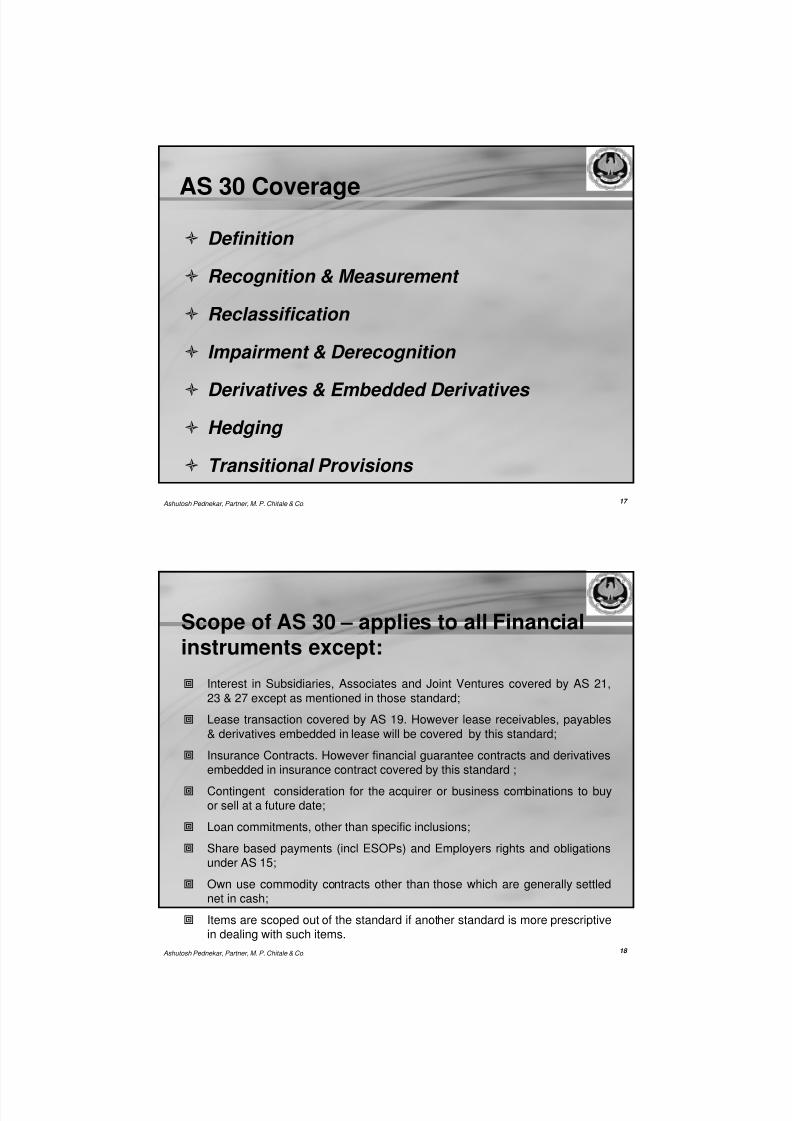

AS 30 Coverage

Definition

Recognition & Measurement

Reclassification

Impairment & Derecognition

Derivatives & Embedded Derivatives

Hedging

Transitional Provisions

18 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Scope of AS 30 – applies to all Financialinstruments except:

Interest in Subsidiaries, Associates and Joint Ventures covered by AS 21,

23 & 27 except as mentioned in those standard;

Lease transaction covered by AS 19. However lease receivables, payables

& derivatives embedded in lease will be covered by this standard;

Insurance Contracts. However financial guarantee contracts and derivativesembedded in insurance contract covered by this standard ;

Contingent consideration for the acquirer or business combinations to buyor sell at a future date;

Loan commitments, other than specific inclusions;

Share based payments (incl ESOPs) and Employers rights and obligationsunder AS 15;

Own use commodity contracts other than those which are generally settlednet in cash;

Items are scoped out of the standard if another standard is more prescriptivein dealing with such items.

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 10/33

19 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Present Classification of financial

instruments by Banks

Presented by way of a note and as Contingent LiabilitiesDerivatives

Category Particulars

Loans Bills Purchased & Discounted

CC, ODs and Loans Repayable on Demand

Term Loans

Further detailed presentation – popularly called 9 –wayclassification

Investments 6 line items to be presented

3 way categorisation HTM, AFS & HFT

Liabilities No specific categorization other than the line itemsspecified in the BR Act format

20 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

AS’ classification of financialinstruments

Category Definition

Financial assetsand financialliabilities at fairvalue through profit

and loss

Classified as held for trading (intended to be activelytraded)

All derivatives are classified as held for trading (exceptthose used as hedging instruments on financial guarantee)

Financial asset or financial liability designated as such atinception (subject to certain conditions)

Held-to-maturityinvestments

Financial assets with fixed or determinable payments andfixed maturity that an entity has the positive intention andability to hold to maturity

Loans andreceivables

Non-derivatives financial assets with fixed or determinablepayments, whether originated or acquired, quoted in anactive market. (Does not need to have a fixed maturity)

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 11/33

21Ashutosh Pednekar, Partner, M. P. Chitale & Co.

AS’ classification of financialinstruments…

Category Definition

Available-for-sale financialassets(AFS)

Non-derivative financial assets designated as AFSor that are not:

Loans or receivables

Held-to-maturity investments

Financial assets at fair value through profitand loss

Other financialliabilities

Financial liabilities that are not classified as “fairvalue through PL”, e.g. Warrants, obligations todeliver cash/cash equivalents/financial assets

22 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Held-to-Maturity Investments

Positive intent and ability to hold to maturity ?

Was any held-to-maturity instrument sold orreclassified in the current or two preceding years?

Yes

Classify as held-to-maturity andmeasure at amortised cost

Near maturity

Isolated event beyond an entity’s control

Collected substantially all principal OR

Insignificant amount in relation to the held-to-maturity portfolio

NoYes

Yes

Reclassify all HTM instruments asavailable-for-sale

No

IMPACT ANALYSIS

RBI permits sale ofHTM portfolio – willthis fail the test ofintention to hold?

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 12/33

23 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

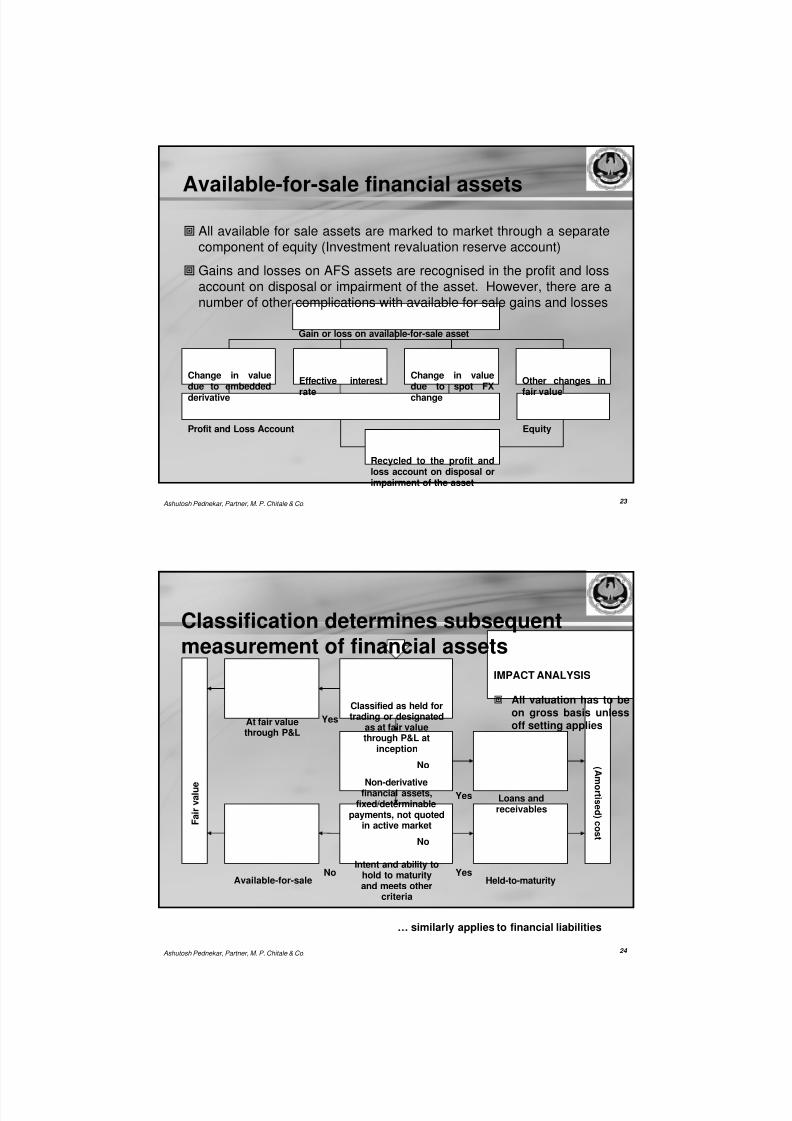

Available-for-sale financial assets

All available for sale assets are marked to market through a separatecomponent of equity (Investment revaluation reserve account)

Gains and losses on AFS assets are recognised in the profit and lossaccount on disposal or impairment of the asset. However, there are anumber of other complications with available for sale gains and losses

Gain or loss on available-for-sale asset

Effective interest

rate

Other changes in

fair value

Change in valuedue to spot FXchange

Change in valuedue to embeddedderivative

EquityProfit and Loss Account

Recycled to the profit andloss account on disposal orimpairment of the asset

24 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Classification determines subsequentmeasurement of financial assets

Available-for-sale

At fair valuethrough P&L

No

Yes

Classified as held fortrading or designated

as at fair valuethrough P&L at

inception

Non-derivativefinancial assets,fixed/determinable

payments, not quotedin active market

Intent and ability tohold to maturityand meets other

criteria

Yes

Yes

No

No

Loans andreceivables

Held-to-maturity

F a i r v a l u e

( A m or t i s e d ) c o s t

… similarly applies to financial liabilities

IMPACT ANALYSIS

All valuation has to beon gross basis unlessoff setting applies

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 13/33

25 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Initial Recognition

Initial Recognition of a FA or FL to be done by an entitywhen, and only when it becomes a party to thecontractual provisions of the instrument

All contractual rights & obligations under derivatives are tobe recognized on balance sheet as asset or liability except:-

If a transfer does not qualify for dercognition then

Transferor does not recognize derivatives of the FA / FL separately

Transferee does not recognize transferred FA / FL as its FA / FL

26 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Initial Recognition…

Recognize assets to be acquired or liabilities to be incurred as

a result of firm commitment to purchase or sell goods or

services only when

At least one of the parties has performed under the agreement or

It is a firm commitment applicable under the Standard But in case of an unrecognized firm commitment that is designated as

“hedged item” in a fair value hedge, any change in net fair value attributable

to hedged risk is recognized as asset or liability after inception of hedge

Don’t recognize FA/FL arising out of planned future transactions no

matter how likely, as entity is not party to the contract

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 14/33

27 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Fair Value = the amount for which an asset could be exchanged, or aliability settled, between knowledgeable, willing parties in an arm’s

length transaction

At fair value + / - directlyattributable transaction cost

Other FA / FL

At fair value ondate ofacquisition orissue

FA / FL @ FVTPL

Original invoice amountif effect of discounting isimmaterial

Short-term receivables / payables with no stated interest

rate

If settlement date accounting is used for an asset that is subsequentlymeasured at cost or amortized cost, then it is initially recognized at FV on

the trade date

Initial Measurement

28 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Fair value (FV)

Presumption of FV

Entity is a going concern, without

the intention or need to liquidate or

curtail materially the scale of operations or

to undertake a transaction on adverse terms

FV is not the amount that would be received or paid in

a forced transaction,

involuntary liquidation or

distress sale

FV reflects credit quality of financial instrument

E.g. Amount lent at below market rate and up-front received as

compensation; discount accreted to the PL A/c using effective

interest rate method

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 15/33

29 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

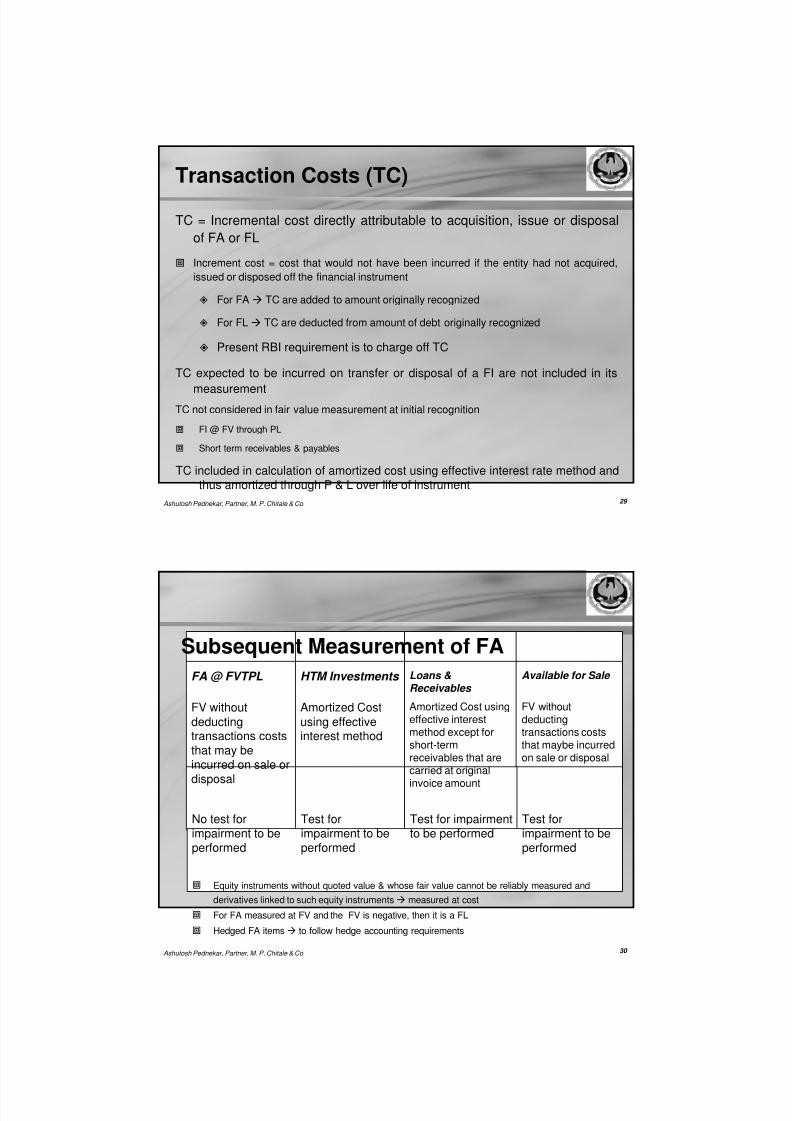

Transaction Costs (TC)

TC = Incremental cost directly attributable to acquisition, issue or disposal

of FA or FL

Increment cost = cost that would not have been incurred if the entity had not acquired,

issued or disposed off the financial instrument

For FA TC are added to amount originally recognized

For FL TC are deducted from amount of debt originally recognized

Present RBI requirement is to charge off TC

TC expected to be incurred on transfer or disposal of a FI are not included in its

measurementTC not considered in fair value measurement at initial recognition

FI @ FV through PL

Short term receivables & payables

TC included in calculation of amortized cost using effective interest rate method andthus amortized through P & L over life of instrument

30 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Subsequent Measurement of FA

Test forimpairment to beperformed

Test for impairmentto be performed

Test forimpairment to beperformed

No test forimpairment to beperformed

Amortized Cost

using effectiveinterest method

HTM Investments

FV without

deductingtransactions coststhat may beincurred on sale ordisposal

FA @ FVTPL

Amortized Cost usingeffective interestmethod except forshort-termreceivables that arecarried at original

invoice amount

Loans &Receivables

FV withoutdeductingtransactions coststhat maybe incurredon sale or disposal

Available for Sale

Equity instruments without quoted value & whose fair value cannot be reliably measured and

derivatives linked to such equity instruments measured at cost

For FA measured at FV and the FV is negative, then it is a FL

Hedged FA items to follow hedge accounting requirements

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 16/33

31Ashutosh Pednekar, Partner, M. P. Chitale & Co.

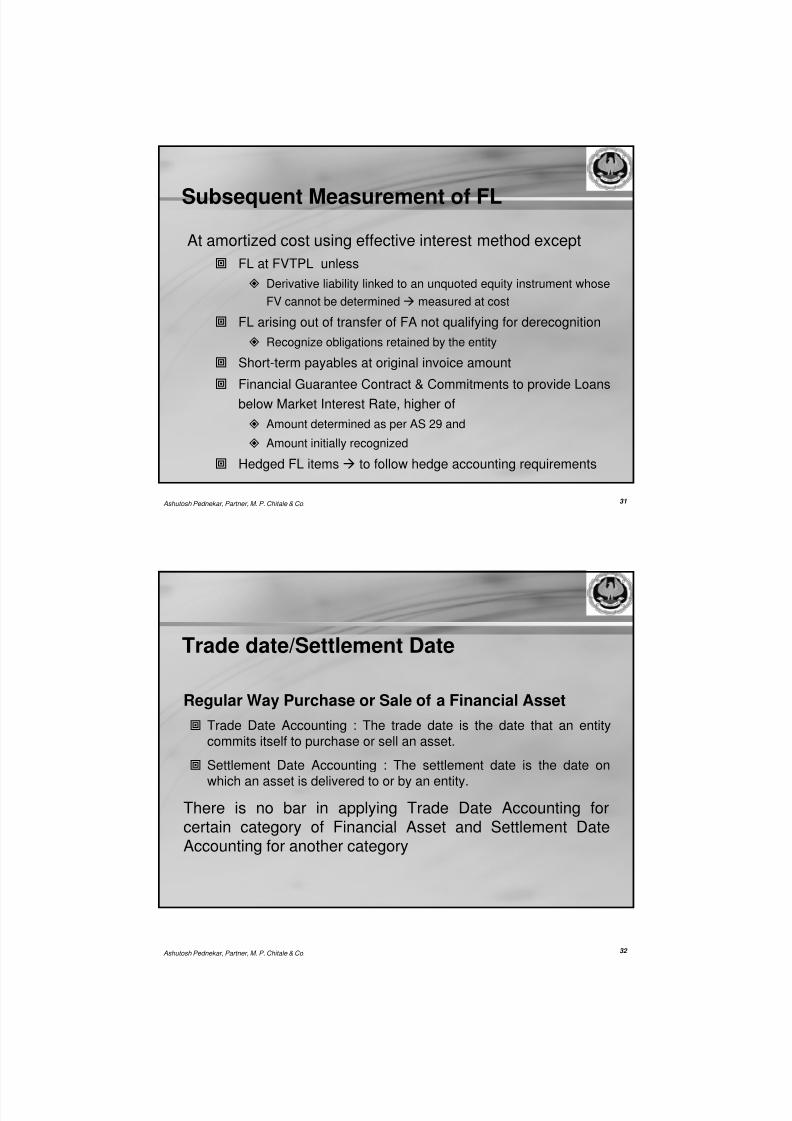

Subsequent Measurement of FL

At amortized cost using effective interest method except

FL at FVTPL unless

Derivative liability linked to an unquoted equity instrument whose

FV cannot be determined measured at cost

FL arising out of transfer of FA not qualifying for derecognition

Recognize obligations retained by the entity

Short-term payables at original invoice amount

Financial Guarantee Contract & Commitments to provide Loans

below Market Interest Rate, higher of

Amount determined as per AS 29 and

Amount initially recognized

Hedged FL items to follow hedge accounting requirements

32 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Regular Way Purchase or Sale of a Financial Asset

Trade Date Accounting : The trade date is the date that an entitycommits itself to purchase or sell an asset.

Settlement Date Accounting : The settlement date is the date on

which an asset is delivered to or by an entity.

There is no bar in applying Trade Date Accounting forcertain category of Financial Asset and Settlement DateAccounting for another category

Trade date/Settlement Date

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 17/33

33 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

ReclassificationsAt fair value through profit or loss category

No reclassification of a financial instrument either into or out of this

category is permissible

HTM Investments to AFS category

Reclassify the investment as ‘available for sale’

Remeasure it at fair value

Recognise the difference between its carrying amount and the fair value in theappropriate equity account (Investment Revaluation Reserve Account).

From AFS to HTM category

the fair value carrying amount on that date becomes its new cost.

Any previous gain or loss recognised directly in the appropriate equityaccount:

Is amortised over the remaining life of the investment using the effectiveinterest rate method.

IMPACT ANALYSIS

RBI permits reclassification – will this be construed asagainst AS 30?

34 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Gains & Losses on changes in FV

FA / FL @ FVTPL

Recognized in P & L

AFS – FA

Appropriate Equity Account (Investment Revaluation Reserve) except

Impairment losses & Foreign Exchange Gains & Losses to P & L

When FA is derecognized, balance in this equity account is transferred

to P & L

FA / FL @ Amortized Cost

Recognized in P & L

Hedged items to follow Hedge Accounting requirements

In case of settlement date accounting

Change in FV between trade date & settlement date is not recognized ifthe FA / FL is carried at cost

Otherwise it is taken to P & L or the Appropriate Equity Account

IMPACT ANALYSIS

AFS presently net negative in PLand net positive is ignored

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 18/33

35 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

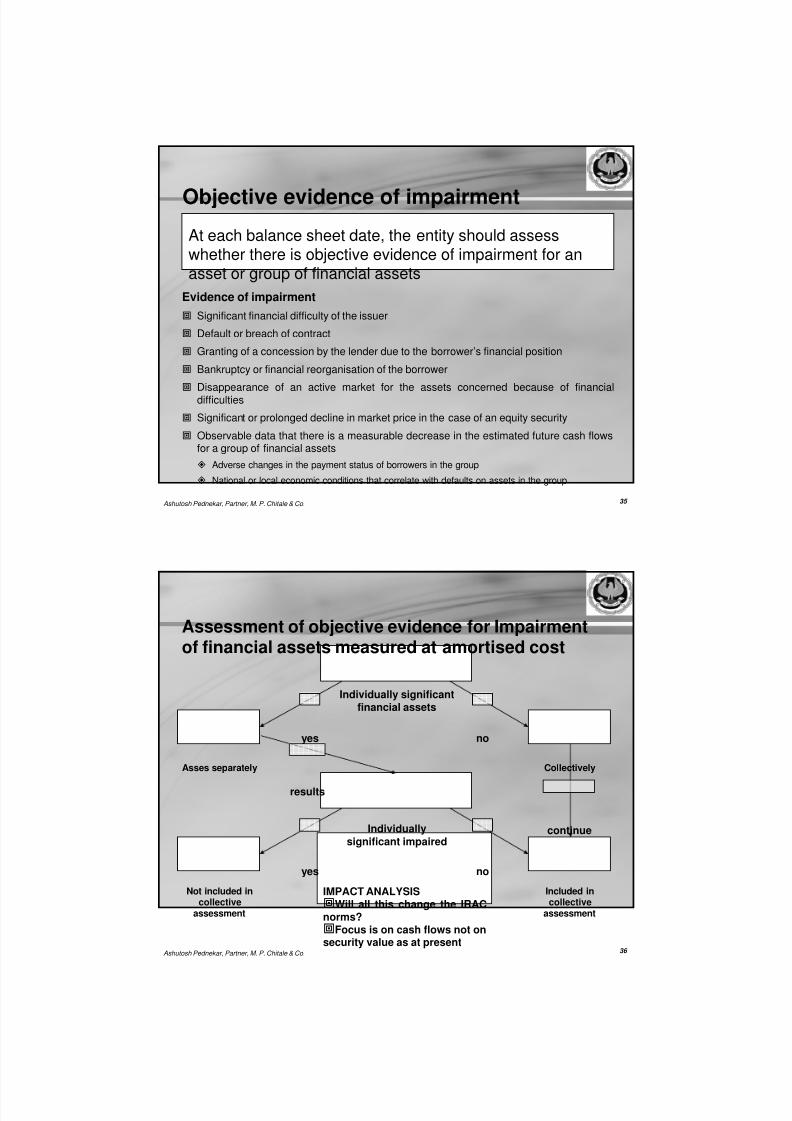

Objective evidence of impairment

Evidence of impairment

Significant financial difficulty of the issuer

Default or breach of contract

Granting of a concession by the lender due to the borrower’s financial position

Bankruptcy or financial reorganisation of the borrower

Disappearance of an active market for the assets concerned because of financialdifficulties

Significant or prolonged decline in market price in the case of an equity security

Observable data that there is a measurable decrease in the estimated future cash flowsfor a group of financial assets

Adverse changes in the payment status of borrowers in the group

National or local economic conditions that correlate with defaults on assets in the group

At each balance sheet date, the entity should assesswhether there is objective evidence of impairment for anasset or group of financial assets

36 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Assessment of objective evidence for Impairmentof financial assets measured at amortised cost

Individually significantfinancial assets

yes no

Individually

significant impaired

Asses separately Collectively

Not included incollective

assessment

yes no

Included incollective

assessment

results

continue

IMPACT ANALYSISWill all this change the IRACnorms?Focus is on cash flows not onsecurity value as at present

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 19/33

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 20/33

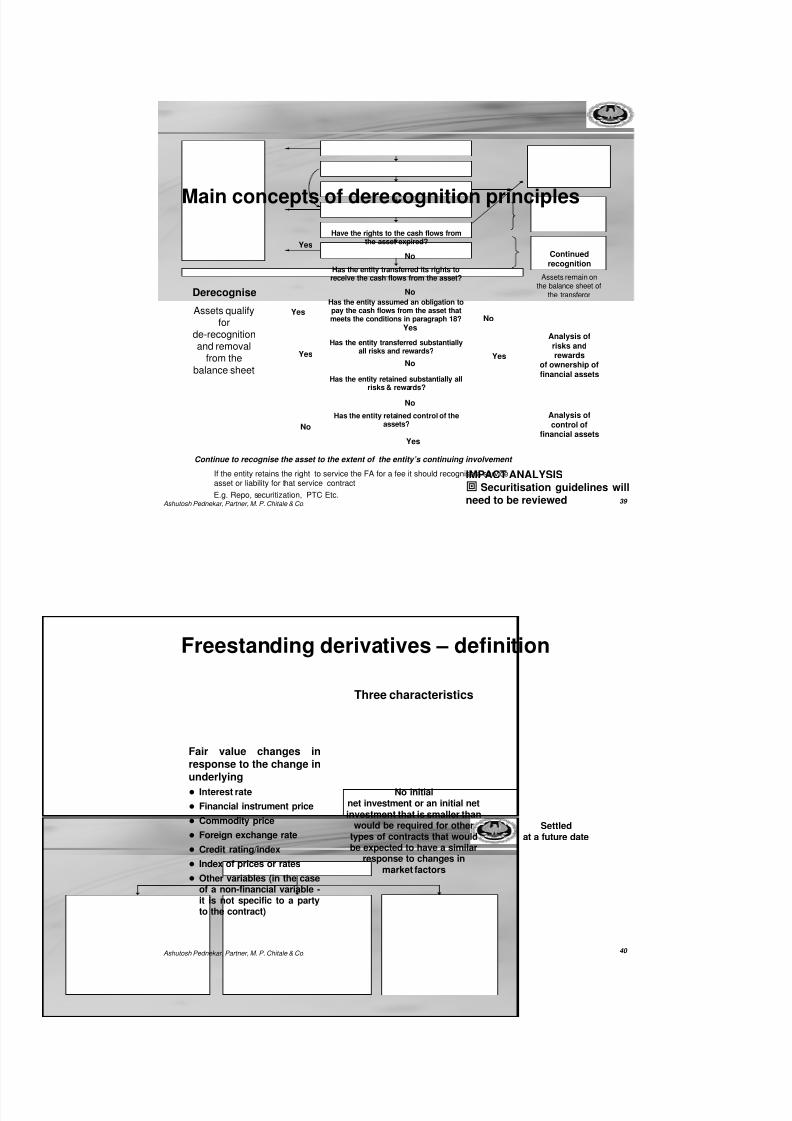

39 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

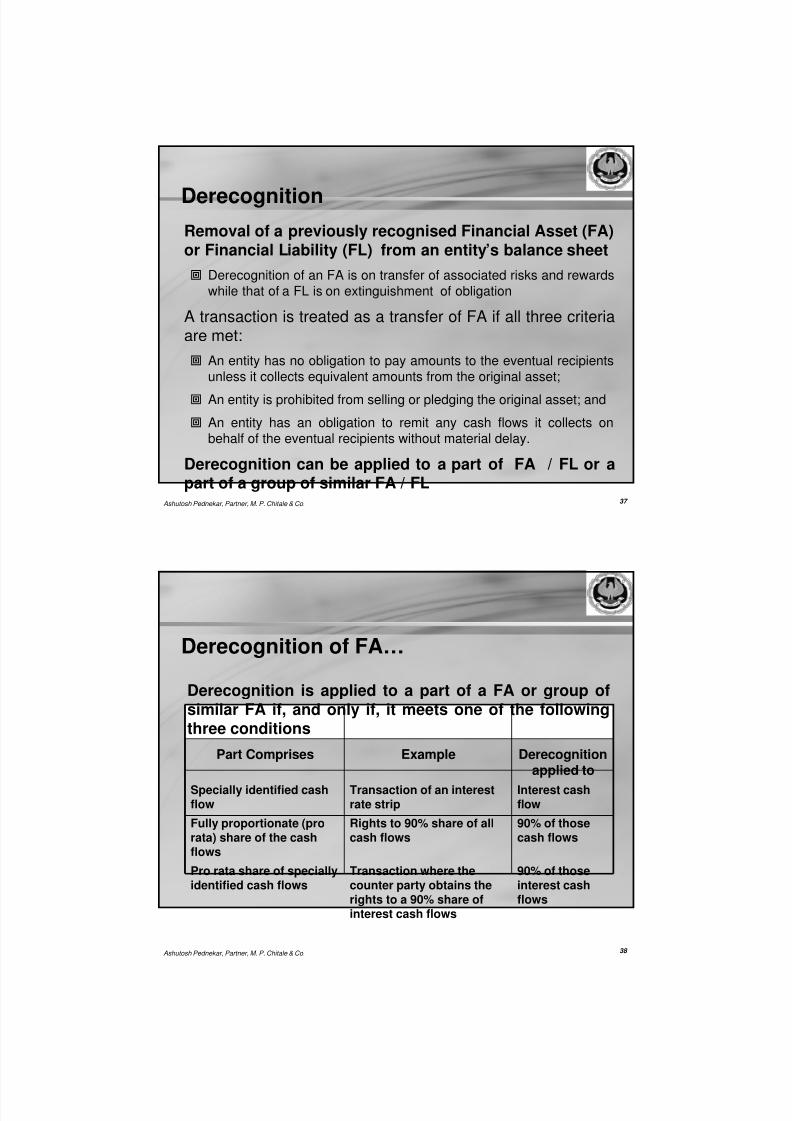

Main concepts of derecognition principles

Continued

recognition

Assets remain onthe balance sheet of

the transferorDerecognise

Assets qualifyfor

de-recognitionand removal

from the

balance sheet

Analysis of

risks andrewards

of ownership of

financial assets

Yes

Yes

Has the entity transferred its rights toreceive the cash flows from the asset?

Has the entity assumed an obligation topay the cash flows from the asset thatmeets the conditions in paragraph 18?

Has the entity retained substantially allrisks & rewards?

Yes

Continue to recognise the asset to the extent of the entity’s continuing involvement

Analysis of

control offinancial assets

Yes

No

Have the rights to the cash flows fromthe asset expired?

Has the entity retained control of theassets?

No

Has the entity transferred substantiallyall risks and rewards?

No

No

No

No

Yes

If the entity retains the right to service the FA for a fee it should recognise a serviceasset or liability for that service contract

Yes

E.g. Repo, securitization, PTC Etc.

IMPACT ANALYSIS Securitisation guidelines willneed to be reviewed

40 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Freestanding derivatives – definition

Fair value changes inresponse to the change inunderlying

Interest rate

Financial instrument price

Commodity price

Foreign exchange rate

Credit rating/index

Index of prices or rates

Other variables (in the caseof a non-financial variable -it is not specific to a partyto the contract)

Three characteristics

No initialnet investment or an initial netinvestment that is smaller than

would be required for othertypes of contracts that wouldbe expected to have a similar

response to changes inmarket factors

Settledat a future date

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 21/33

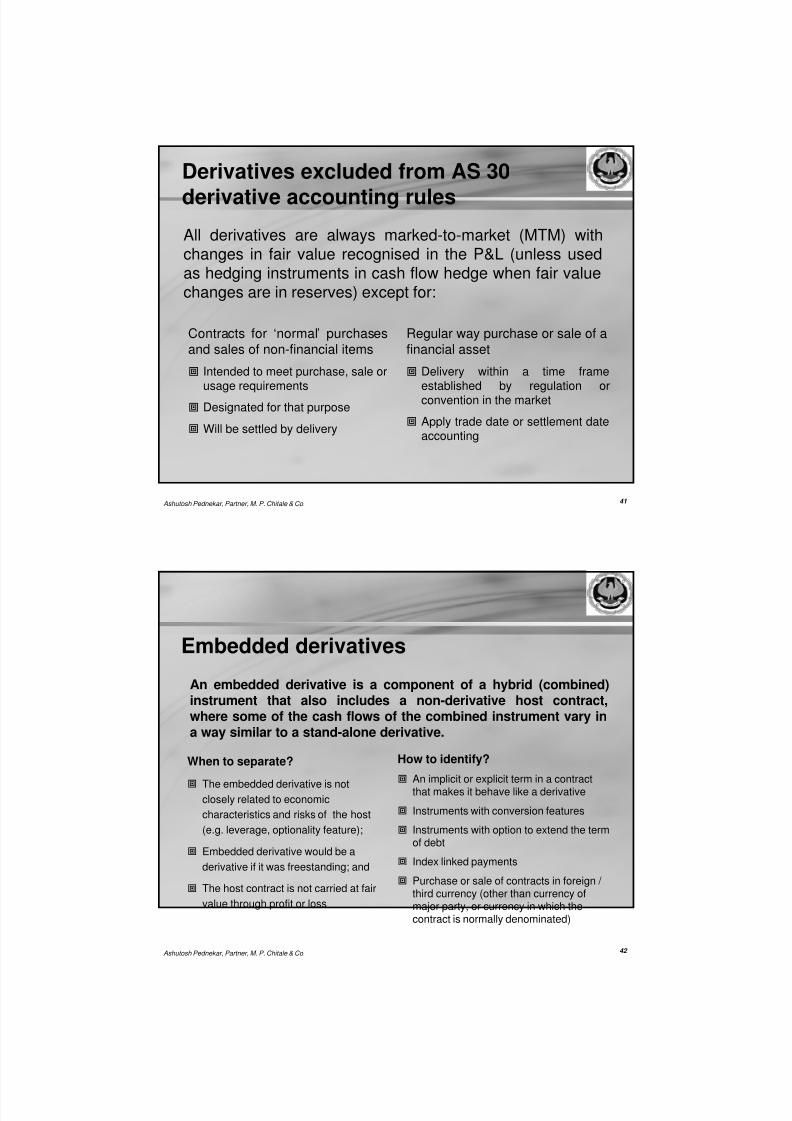

41Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Derivatives excluded from AS 30

derivative accounting rules

All derivatives are always marked-to-market (MTM) withchanges in fair value recognised in the P&L (unless usedas hedging instruments in cash flow hedge when fair valuechanges are in reserves) except for:

Regular way purchase or sale of afinancial asset

Delivery within a time frameestablished by regulation orconvention in the market

Apply trade date or settlement dateaccounting

Contracts for ‘normal’ purchasesand sales of non-financial items

Intended to meet purchase, sale orusage requirements

Designated for that purpose

Will be settled by delivery

42 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Embedded derivatives

How to identify?

An implicit or explicit term in a contractthat makes it behave like a derivative

Instruments with conversion features

Instruments with option to extend the termof debt

Index linked payments

Purchase or sale of contracts in foreign / third currency (other than currency ofmajor party, or currency in which thecontract is normally denominated)

When to separate?

The embedded derivative is notclosely related to economic

characteristics and risks of the host

(e.g. leverage, optionality feature);

Embedded derivative would be a

derivative if it was freestanding; and

The host contract is not carried at fair

value through profit or loss

An embedded derivative is a component of a hybrid (combined)instrument that also includes a non-derivative host contract,where some of the cash flows of the combined instrument vary ina way similar to a stand-alone derivative.

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 22/33

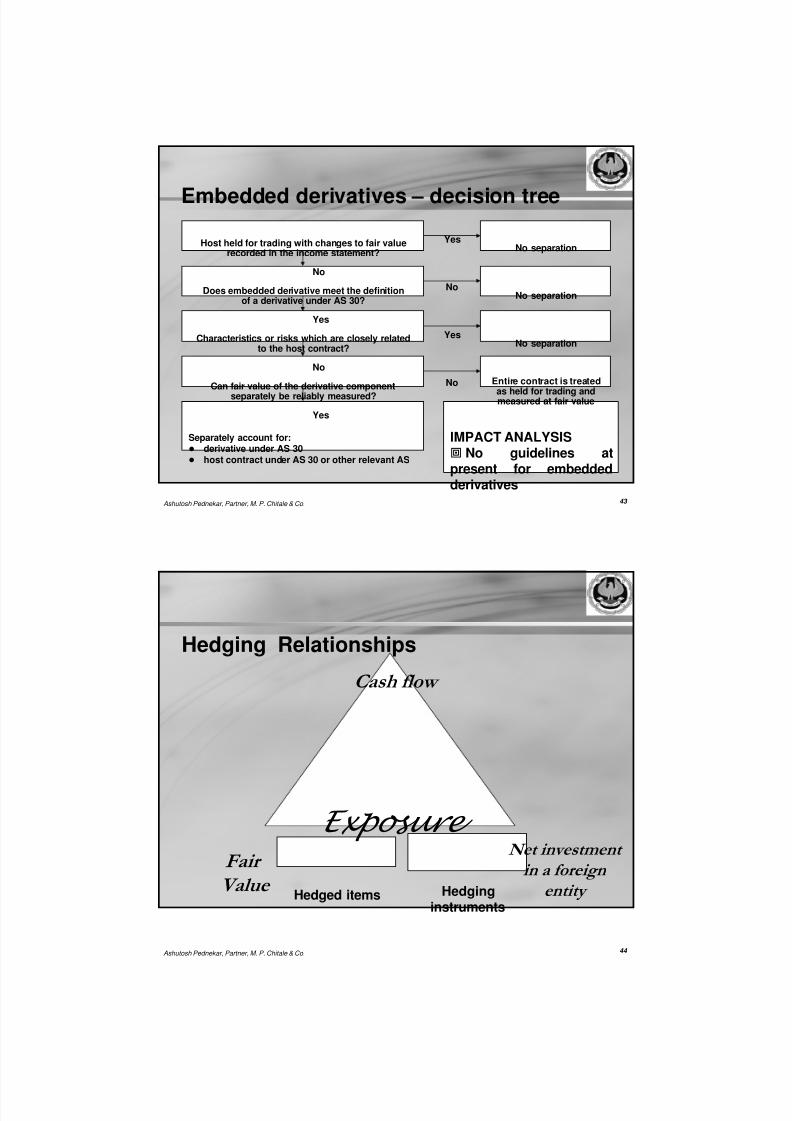

43 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Embedded derivatives – decision tree

YesNo separation

No

Yes

No

No separation

No separation

Entire contract is treated

as held for trading andmeasured at fair value

Separately account for: derivative under AS 30 host contract under AS 30 or other relevant AS

No

Yes

No

Yes

Does embedded derivative meet the definitionof a derivative under AS 30?

Characteristics or risks which are closely relatedto the host contract?

Can fair value of the derivative componentseparately be reliably measured?

Host held for trading with changes to fair valuerecorded in the income statement?

IMPACT ANALYSIS No guidelines atpresent for embeddedderivatives

44 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedging Relationships

Net investment

in a foreign

entity

Cash flow

Fair

Value

Exposure

Hedged items Hedginginstruments

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 23/33

45 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

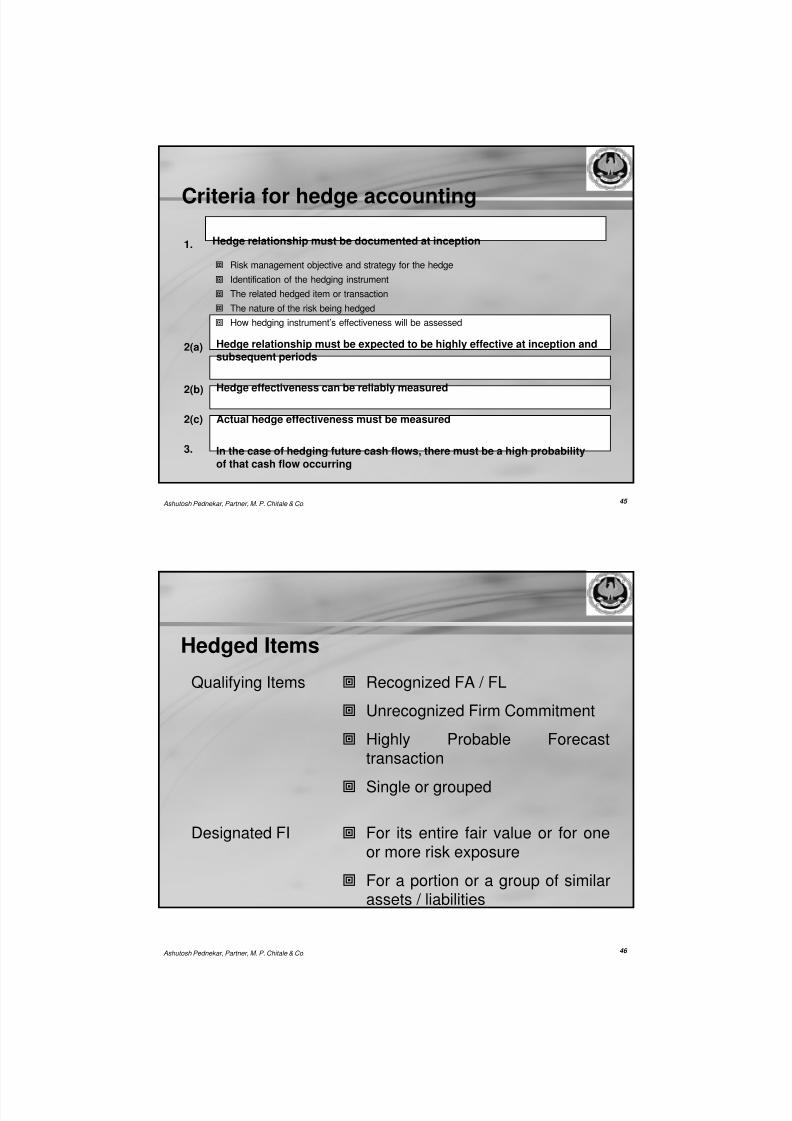

Criteria for hedge accounting

Risk management objective and strategy for the hedge

Identification of the hedging instrument

The related hedged item or transaction

The nature of the risk being hedged

How hedging instrument’s effectiveness will be assessed

1. Hedge relationship must be documented at inception

2(a) Hedge relationship must be expected to be highly effective at inception andsubsequent periods

2(b) Hedge effectiveness can be reliably measured

3. In the case of hedging future cash flows, there must be a high probability

of that cash flow occurring

2(c) Actual hedge effectiveness must be measured

46 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedged Items

Recognized FA / FL

Unrecognized Firm Commitment

Highly Probable Forecasttransaction

Single or grouped

Qualifying Items

For its entire fair value or for oneor more risk exposure

For a portion or a group of similarassets / liabilities

Designated FI

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 24/33

47 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

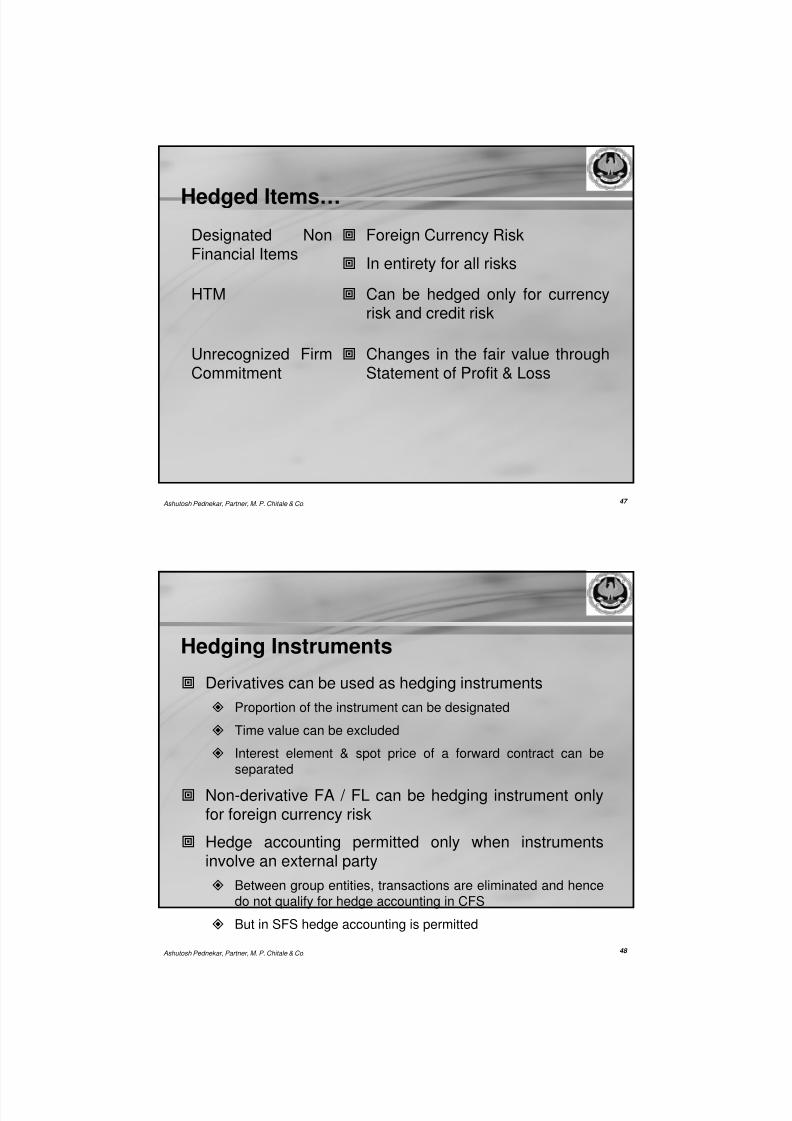

Hedged Items…

Foreign Currency Risk

In entirety for all risks

Designated NonFinancial Items

Can be hedged only for currencyrisk and credit risk

HTM

Changes in the fair value throughStatement of Profit & Loss

Unrecognized FirmCommitment

48 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedging Instruments

Derivatives can be used as hedging instruments

Proportion of the instrument can be designated

Time value can be excluded

Interest element & spot price of a forward contract can beseparated

Non-derivative FA / FL can be hedging instrument onlyfor foreign currency risk

Hedge accounting permitted only when instrumentsinvolve an external party

Between group entities, transactions are eliminated and hencedo not qualify for hedge accounting in CFS

But in SFS hedge accounting is permitted

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 25/33

49 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

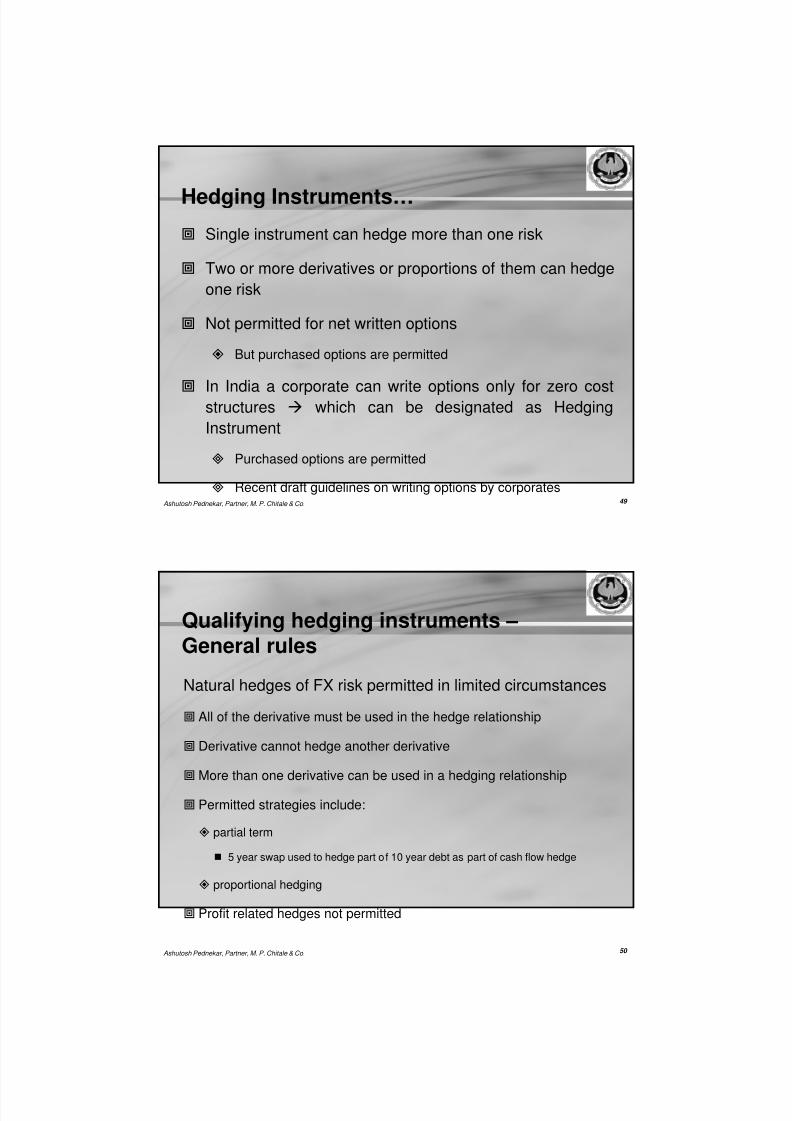

Hedging Instruments…

Single instrument can hedge more than one risk

Two or more derivatives or proportions of them can hedge

one risk

Not permitted for net written options

But purchased options are permitted

In India a corporate can write options only for zero coststructures which can be designated as Hedging

Instrument

Purchased options are permitted

Recent draft guidelines on writing options by corporates

50 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Qualifying hedging instruments –General rules

Natural hedges of FX risk permitted in limited circumstances

All of the derivative must be used in the hedge relationship

Derivative cannot hedge another derivative

More than one derivative can be used in a hedging relationship

Permitted strategies include:

partial term

5 year swap used to hedge part of 10 year debt as part of cash flow hedge

proportional hedging

Profit related hedges not permitted

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 26/33

51Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedge effectiveness

The effectiveness test itself must be stated upfront in the hedgedocumentation. This means that it must be designed and tested toensure that it provides a suitable solution before the hedge commences

There are two components to an effectiveness test:

the prospective test

the retrospective test

Following criteria to be fulfilled at inception & during the life of the hedge

Hedge is expected to achieve offsetting changes in fair value / cash flows

attributable to the hedged risk

Comparing past changes in fair value / cash flows

High statistical correlation between hedged item and hedging instrument

Actual results of hedge are within a range of 80%-125%

52 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedge effectiveness…

Hedging instrument - 120

Hedged item + 100

computed effectiveness is within a range of 80% -125% (83% /

120% in this case)

the hedge relationship is highly effective

nevertheless a loss of 20 has to be recorded in profit and loss

due to ineffectiveness

the fact that the hedge relationship is highly effective does not

lead to ignore the loss incurred due to ineffectiveness

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 27/33

53 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

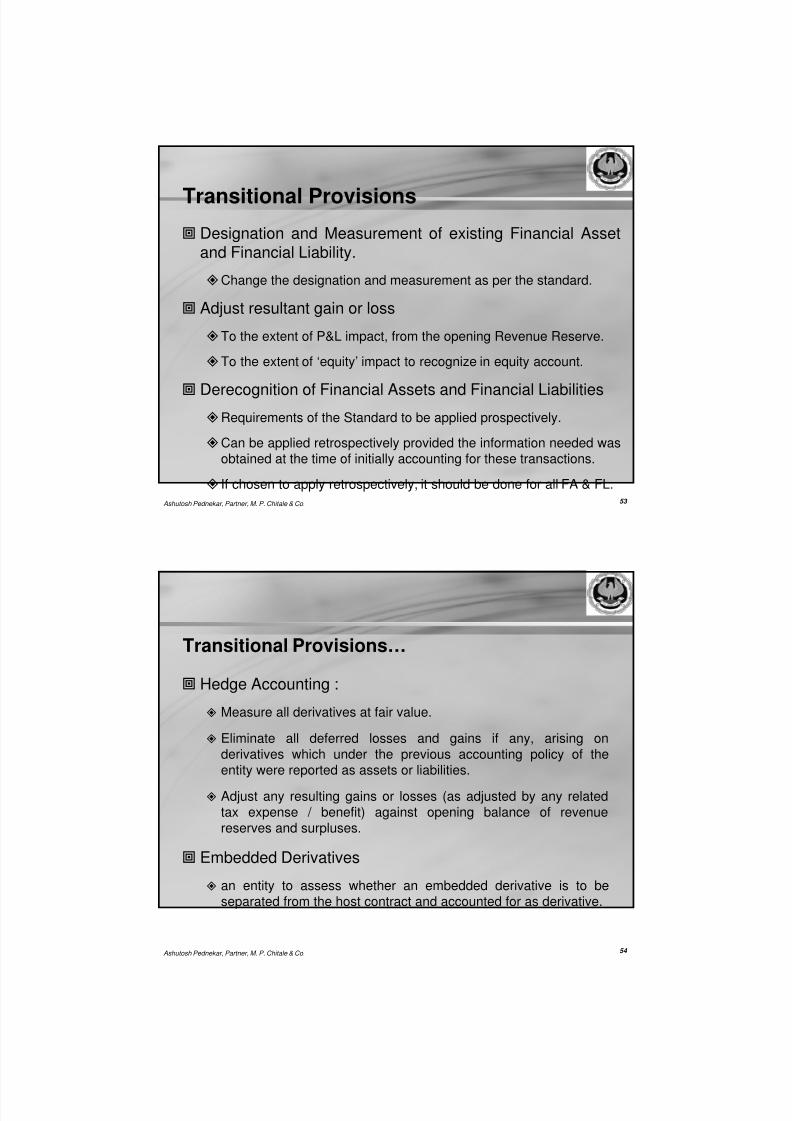

Transitional Provisions

Designation and Measurement of existing Financial Assetand Financial Liability.

Change the designation and measurement as per the standard.

Adjust resultant gain or loss

To the extent of P&L impact, from the opening Revenue Reserve.

To the extent of ‘equity’ impact to recognize in equity account.

Derecognition of Financial Assets and Financial LiabilitiesRequirements of the Standard to be applied prospectively.

Can be applied retrospectively provided the information needed wasobtained at the time of initially accounting for these transactions.

If chosen to apply retrospectively, it should be done for all FA & FL.

54 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Hedge Accounting :

Measure all derivatives at fair value.

Eliminate all deferred losses and gains if any, arising onderivatives which under the previous accounting policy of theentity were reported as assets or liabilities.

Adjust any resulting gains or losses (as adjusted by any relatedtax expense / benefit) against opening balance of revenuereserves and surpluses.

Embedded Derivatives

an entity to assess whether an embedded derivative is to beseparated from the host contract and accounted for as derivative.

Transitional Provisions…

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 28/33

55 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

AS 32’s Genesis of Disclosure

Requires disclosures in the financial statements that enable

users to evaluate

the significance of financial instruments for the entity’s

financial position and performance; and

the nature and extent of risks arising from financial

instruments to which the entity is exposed during the

period and at the reporting date, and how the entity manages those risks.

56 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Some Disclosures: Balance Sheet

Loans or Receivables designated at FV through P & L

Maximum exposure to credit risks

Any products which mitigates the aforesaid credit risks

Changes in FV due to credit risk & methods used to evaluate it

Changes in the fair value of the products mitigating the credit risks

Financial liability at FV through P & L

Changes in fair value due to credit risk and the methods used to evaluate credit risk.

Differences between the carrying amount and the amount that would be contractually required to pay.

Detailed reasons if changes in fair value due to credit risk and methods used to evaluate itare not disclosed for

Loans or receivables.

Financial liabilities at FV through P & L.

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 29/33

57 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

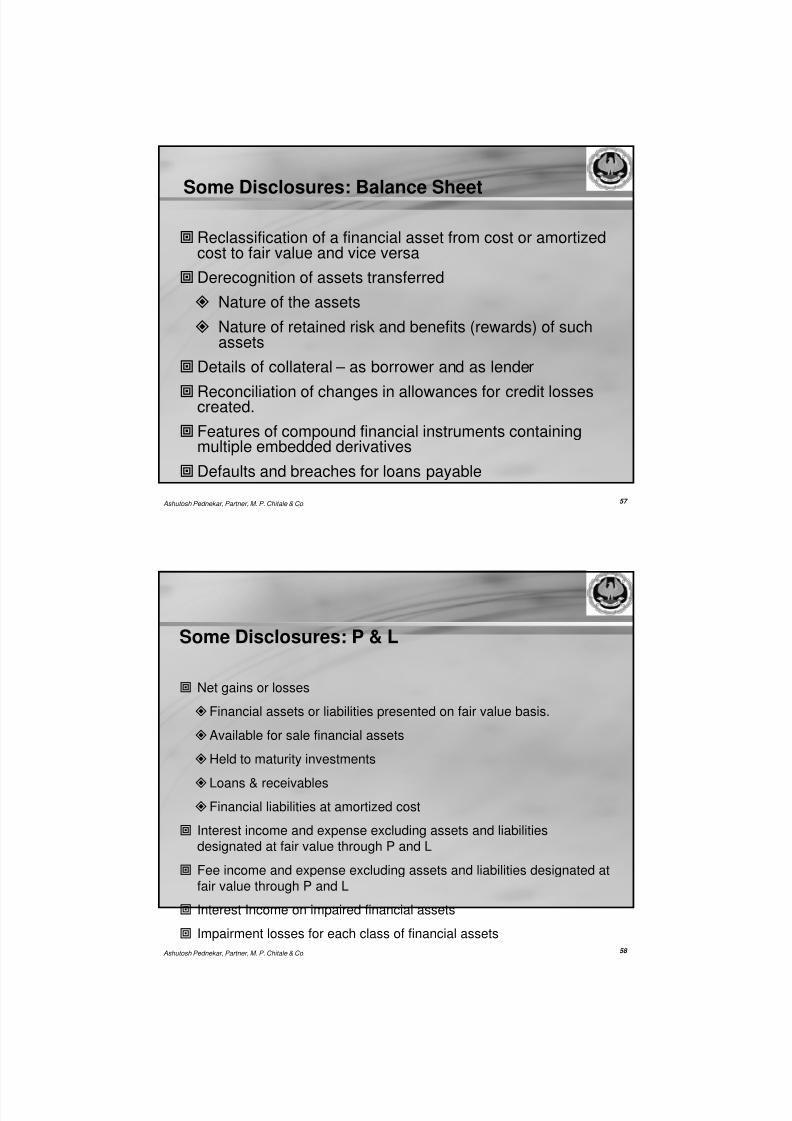

Some Disclosures: Balance Sheet

Reclassification of a financial asset from cost or amortizedcost to fair value and vice versa

Derecognition of assets transferred

Nature of the assets

Nature of retained risk and benefits (rewards) of suchassets

Details of collateral – as borrower and as lender

Reconciliation of changes in allowances for credit lossescreated.

Features of compound financial instruments containingmultiple embedded derivatives

Defaults and breaches for loans payable

58 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Some Disclosures: P & L

Net gains or losses

Financial assets or liabilities presented on fair value basis.

Available for sale financial assets

Held to maturity investments

Loans & receivablesFinancial liabilities at amortized cost

Interest income and expense excluding assets and liabilitiesdesignated at fair value through P and L

Fee income and expense excluding assets and liabilities designated atfair value through P and L

Interest Income on impaired financial assets

Impairment losses for each class of financial assets

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 30/33

59 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

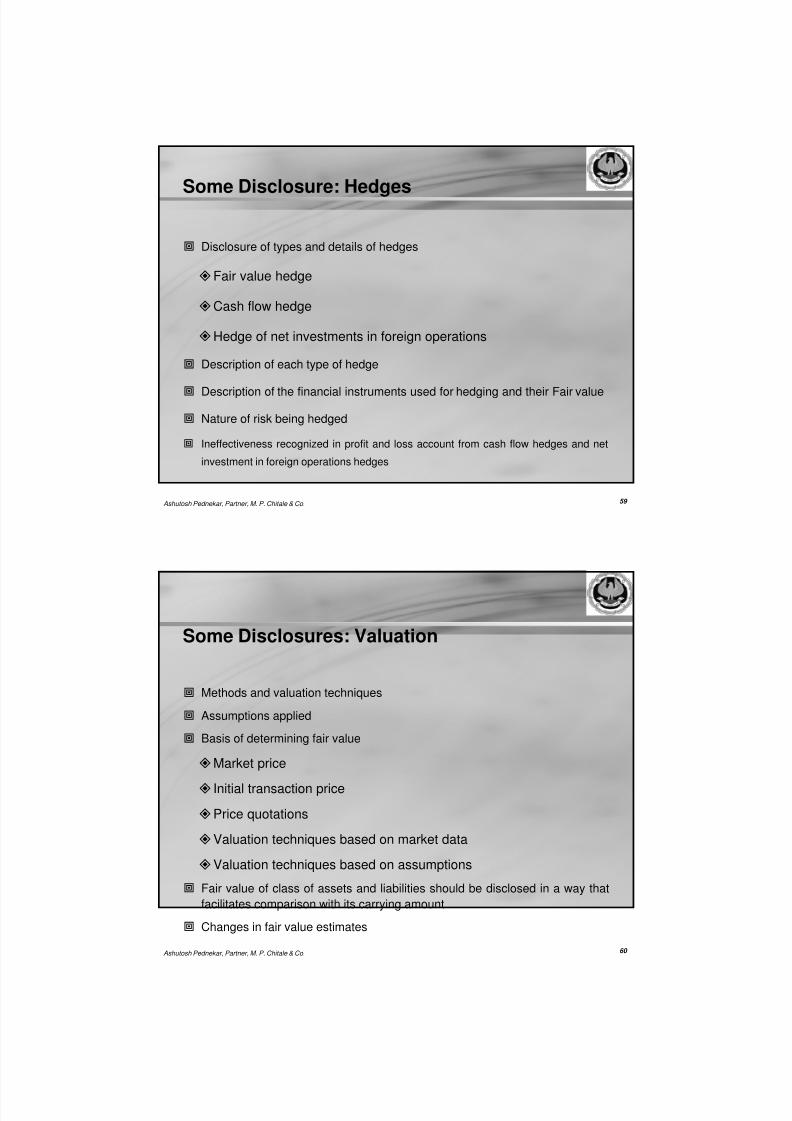

Some Disclosure: Hedges

Disclosure of types and details of hedges

Fair value hedge

Cash flow hedge

Hedge of net investments in foreign operations

Description of each type of hedge

Description of the financial instruments used for hedging and their Fair value

Nature of risk being hedged

Ineffectiveness recognized in profit and loss account from cash flow hedges and net

investment in foreign operations hedges

60 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Some Disclosures: Valuation

Methods and valuation techniques

Assumptions applied

Basis of determining fair value

Market price

Initial transaction price

Price quotations

Valuation techniques based on market data

Valuation techniques based on assumptions

Fair value of class of assets and liabilities should be disclosed in a way that

facilitates comparison with its carrying amount

Changes in fair value estimates

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 31/33

61Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Some Disclosures: Risk

Qualitative disclosures for risk of each class of financial

instruments

The exposures to risks and how they arise

Risk management procedures and methods

Changes in the above from the previous years.

Quantitative disclosures for risk of each class of financial

instruments

Summary quantitative data provided internally to the key

management

Concentration of risks

62 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Some Disclosures: Risk…

Credit Risk

Failure of a party to discharge its obligation in an contract

Liquidity Risk

Failure of a party in meeting obligations associated with financial

liabilities

Market Risk

The risk that the fair value or future cash flows of a financial

instrument will fluctuate because of changes in market prices.

Types of market risk: currency risk, interest rate risk and other

price risk

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 32/33

63 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Impact Analysis Volatility in earnings

Impact on financial statements

MIS comparability over pre AS 30 and post AS 30 era

Performance indicators and ratios

IT systems

Contractual obligations (debt covenant, compensation)

Taxes & Distributable Profits

Managing market, investors and analysts

Greater level of documentation spelling out intentions

Management awareness

Use of experts critical

All this applies for bankers reading their clients’ financial statements

64 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

What now?

RBI has set a group to assess impact and draw up a road map for AS30 implementation in banks

Preparedness to be tested – do a dry run and one more dry run

Get ready for the volatility in the standard

Arising out of the economic crises IASB is in process of revamping IAS

39. Drafts / discussion papers issued on:- IFRS 9

Classification & Measurement lesser number of categories ofFIs

Amortized Cost & Impairment

Hedging

Fair Value Measurement new definition of FV

Credit Risk in Liability Measurement

8/6/2019 As 30 31 32 - Analysing Impact on Banks - 201109

http://slidepdf.com/reader/full/as-30-31-32-analysing-impact-on-banks-201109 33/33

65 Ashutosh Pednekar, Partner, M. P. Chitale & Co.

Thank You

Related Documents