Arizona’s Changing Property Tax Landscape August 6, 2015 ARIZONA GFOA SUMMER TRAINING Presented by: Scott Ruby Randie Stein Darlene Teller, ADOR Gust Rosenfeld P.L.C. Stifel, Nicolaus & Company Economic Research & Analysis 602-257-7432 602-794-4002 602-716-6436 [email protected] [email protected] [email protected]

Arizona’s Changing Property Tax Landscape August 6, 2015 ARIZONA GFOA SUMMER TRAINING Presented by: Scott RubyRandie SteinDarlene Teller, ADOR Gust Rosenfeld.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Arizona’s Changing Property Tax LandscapeAugust 6, 2015

ARIZONA GFOA SUMMER TRAINING

Presented by:

Scott Ruby Randie Stein Darlene Teller, ADORGust Rosenfeld P.L.C. Stifel, Nicolaus & Company Economic Research & Analysis602-257-7432 602-794-4002 [email protected] [email protected] [email protected]

Page 2GFOAz Summer Training 2015

Presentation Overview

• Historical Review of Arizona’s Property Tax LawsScott Ruby, Gust Rosenfeld

• Proposition 117Randie Stein, Stifel

• Property Tax Oversight CommissionDarlene Teller, Arizona Department of Revenue

Results. Relationships. Reputation.Results. Relationships. Reputation.

Historical Review of Arizona’sProperty Tax Laws

Scott W. Ruby, Esq.Gust Rosenfeld, PLC

One E. Washington, Suite 1600Phoenix, Arizona 85004

602-257-7432www.gustlaw.com

1. Constitutional Convention (1910): State issues reflected national political issues of the day progressives v. conservatives.A. Middle class progressive movement/labor movement

was dominant (41 of 52 delegates).(i) Wanted controls put on corporations and their influence on

the legislature:

• Initiative/referendum/recall provisions were the focus of attention.

(ii) Supported labor planks: rights of workers.

I. Constitutional Background.

4

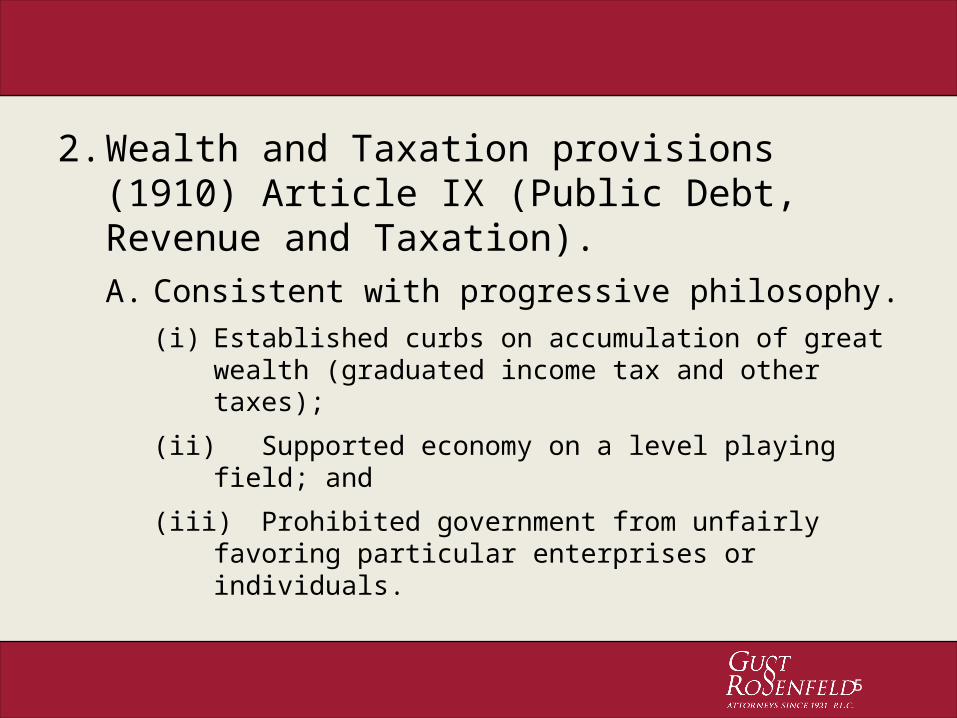

2. Wealth and Taxation provisions (1910) Article IX (Public Debt, Revenue and Taxation).A. Consistent with progressive philosophy.

(i) Established curbs on accumulation of great wealth (graduated income tax and other taxes);

(ii) Supported economy on a level playing field; and

(iii) Prohibited government from unfairly favoring particular enterprises or individuals.

5

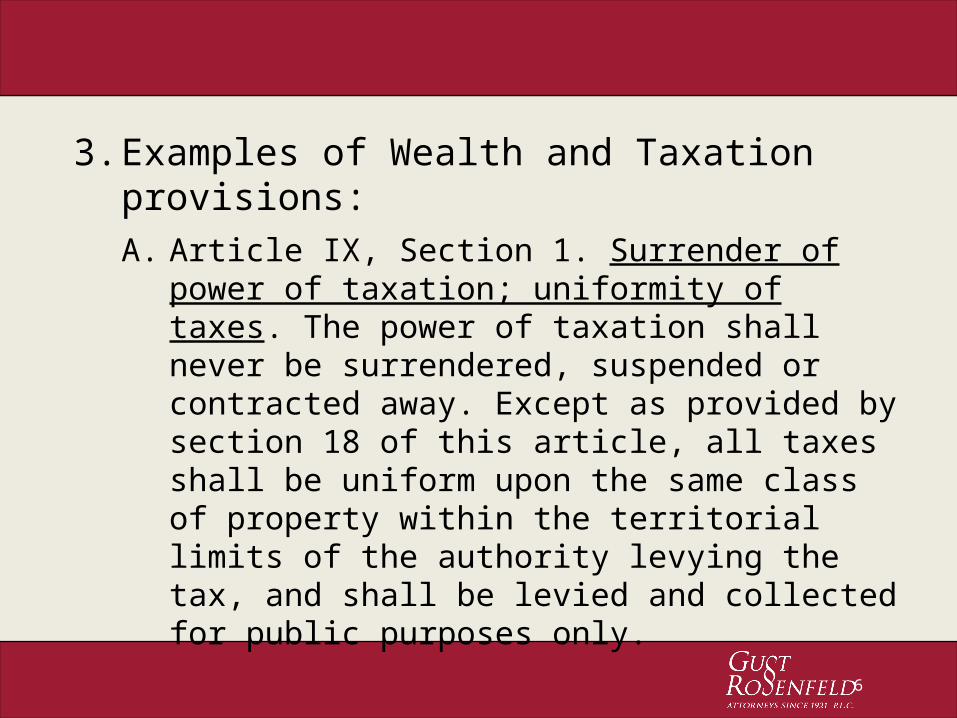

3. Examples of Wealth and Taxation provisions:A. Article IX, Section 1. Surrender of power of taxation;

uniformity of taxes. The power of taxation shall never be surrendered, suspended or contracted away. Except as provided by section 18 of this article, all taxes shall be uniform upon the same class of property within the territorial limits of the authority levying the tax, and shall be levied and collected for public purposes only.

6

B. Article IX, Section 5. Power of State to contract Debt; purposes; limit; restrictions:

The State may contract debts to supply the casual deficits or failures in revenues or to meet expenses not otherwise provided for; but the aggregate amount of such debts....shall never exceed the sum of $350,000....

7

C. Article IX, Section 7. Gift or loan of credit; subsidies; stock ownership; joint ownership.

Neither the state, nor any county, city, town, municipality, or other subdivision of the state shall ever give or loan its credit in the aid of, or make any donation or grant, by subsidy or otherwise, to any individual, association, or corporation, or become a subscriber to, or a shareholder in, any company or corporation, or become a joint owner with any person, company, or corporation, except as to such ownerships as may accrue to the state by operation or provision of law or as authorized by law solely for investment of the monies in the various funds of the state.

8

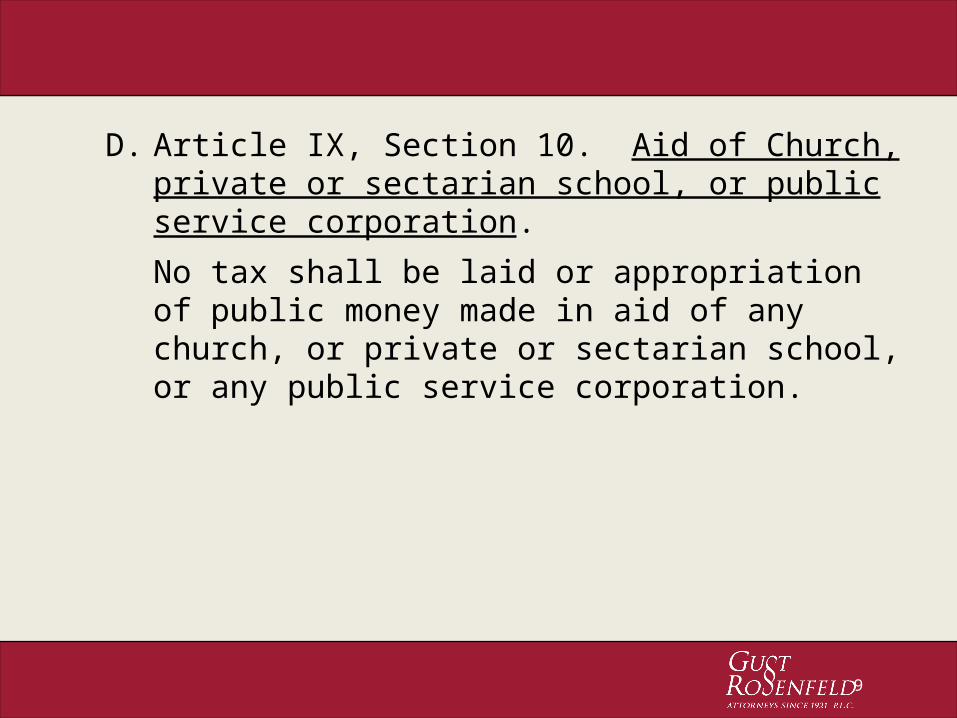

D. Article IX, Section 10. Aid of Church, private or sectarian school, or public service corporation.

No tax shall be laid or appropriation of public money made in aid of any church, or private or sectarian school, or any public service corporation.

9

E. Article IX Section 12. Authority or provide for levy and collection of license and other taxes.

The law-making power shall have authority to provide for the levy and collection of license, franchise, gross revenue, excise, income, collateral and direct inheritance, legacy, and succession taxes, also graduated income taxes, graduated collateral and direct inheritance taxes, graduated legacy and succession taxes, stamp, registration, production, or other specific taxes.

10

F. Article IX, Section 8. Local Debt Limits; Assessment of taxpayers.No county, city, town, school district or other municipal corporation shall for any purpose become indebted in any manner to an amount exceeding 4% of the taxable property in such county, city, town, school district, or other municipal corporation, without the assent of a majority of the property taxpayers...the value of the taxable property therein to be ascertained by the last assessment for state and county purposes...provided, that under no circumstances shall any county or school district become indebted to an amount exceeding 10%...and provided further, that any incorporated city or town, with such assent, may be allowed to become indebted to a larger amount, but not exceeding 5%...for water, artificial light, or sewers...

11

4. Constitutional Amendments.A. From 1912 to present: approximately 250 proposed

amendments, and 118 have passed. Most are technical in nature.

12

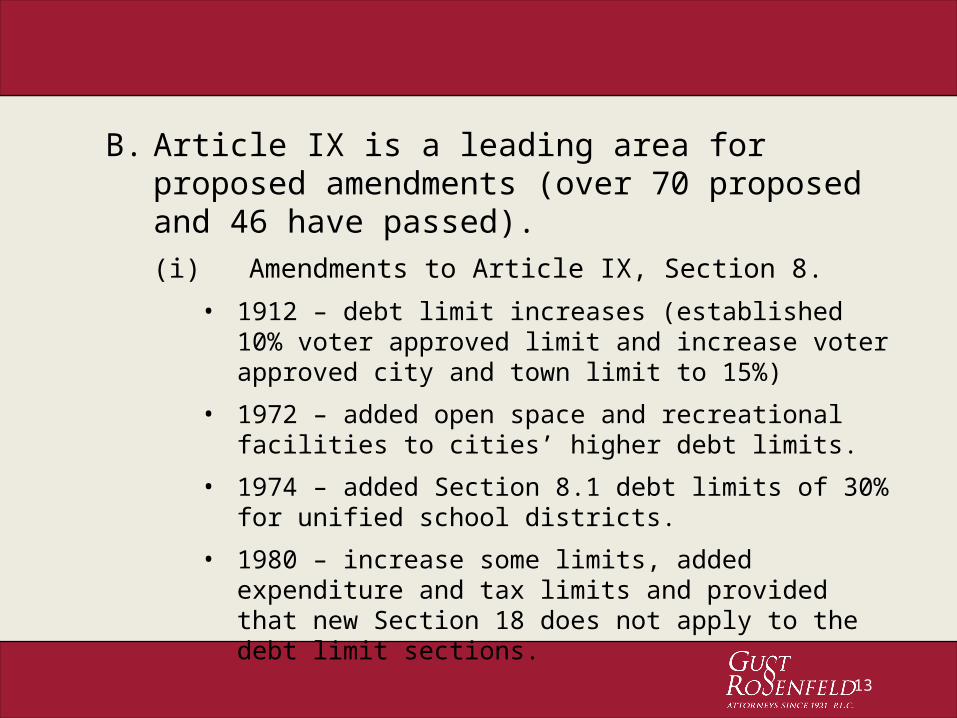

B. Article IX is a leading area for proposed amendments (over 70 proposed and 46 have passed).(i) Amendments to Article IX, Section 8.

• 1912 – debt limit increases (established 10% voter approved limit and increase voter approved city and town limit to 15%)

• 1972 – added open space and recreational facilities to cities’ higher debt limits.

• 1974 – added Section 8.1 debt limits of 30% for unified school districts.

• 1980 – increase some limits, added expenditure and tax limits and provided that new Section 18 does not apply to the debt limit sections.

13

• 2015 – All political subdivisions (including school districts) without voter approval may become indebted up to 6% of the taxable property and, with voter approval:

(a) 15% for elementary and high school districts and counties;

(b) 20% for cities and towns for water, sewer, lights, parks, police, fire and streets;

(c) 30% for unified school districts per Section 8.1; and

(d) the value of taxable property shall be taken from the last assessment for state and county purposes.

14

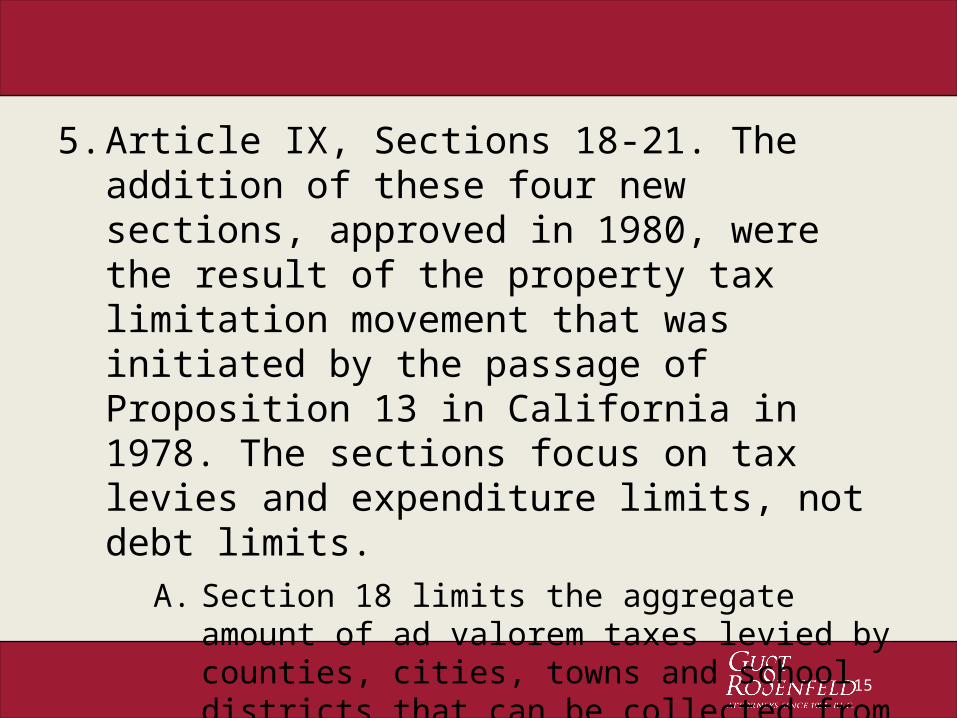

5. Article IX, Sections 18-21. The addition of these four new sections, approved in 1980, were the result of the property tax limitation movement that was initiated by the passage of Proposition 13 in California in 1978. The sections focus on tax levies and expenditure limits, not debt limits.

A. Section 18 limits the aggregate amount of ad valorem taxes levied by counties, cities, towns and school districts that can be collected from residential property to 1% of the property’s full cash value:(i) taxes for debt service are excluded; and

15

(ii) establishes limit on rate of increase in valuation.

B. Section 19 limits the annual increase in local ad valorem taxes to 2% annually.

(i) exceptions for new growth, annexations and voter approved overrides.

C. Sections 20 and 21 limits expenditures over the expenditures in base year 1979-80 to changes in population (or student count) and cost of living.

16

1. 1913 Code indicates what was contemplated by the drafters of the Constitution when, in Article IX, Section 8 reference was made to the value of taxable property as shown by the last assessment.

A. 1913 Code, Section 4849 – All taxable property must be assessed at its full cash value.(i) Full cash value was synonymous with market values.

B. Subsequent Codes (1928, 1939 and current statutes) require assessor to determine full cash value.

C. Assessment ratios did not exist until the 1960s.

II. Arizona Revised Statutes and Judicial Rulings

17

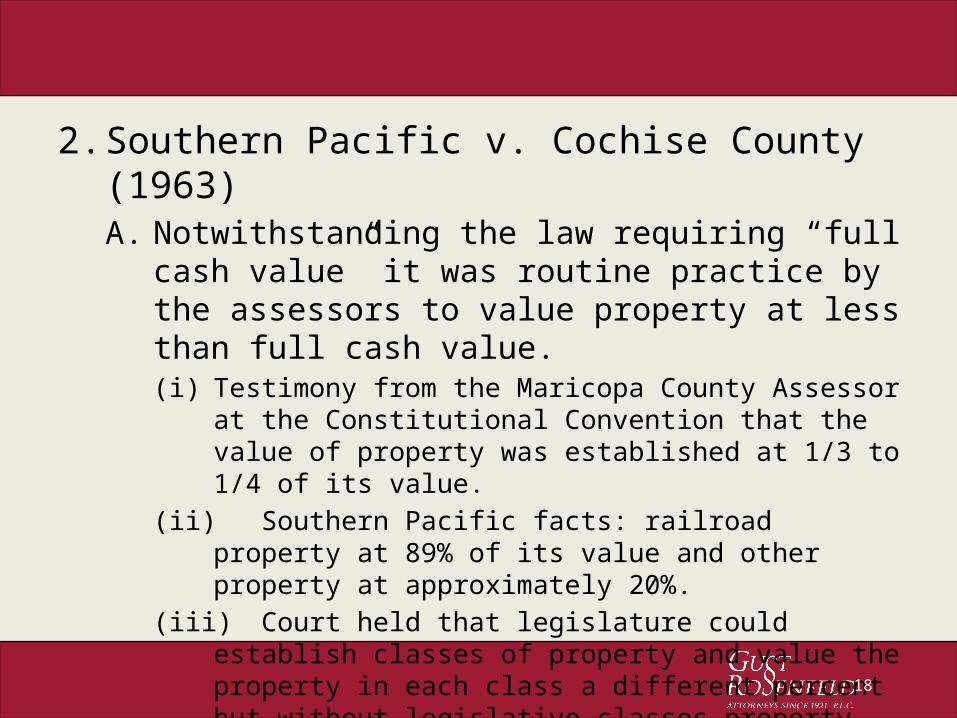

2. Southern Pacific v. Cochise County (1963)A. Notwithstanding the law requiring “full cash value” it

was routine practice by the assessors to value property at less than full cash value.(i) Testimony from the Maricopa County Assessor at the

Constitutional Convention that the value of property was established at 1/3 to 1/4 of its value.

(ii) Southern Pacific facts: railroad property at 89% of its value and other property at approximately 20%.

(iii) Court held that legislature could establish classes of property and value the property in each class a different percent but without legislative classes property had to be uniformly assessed.

18

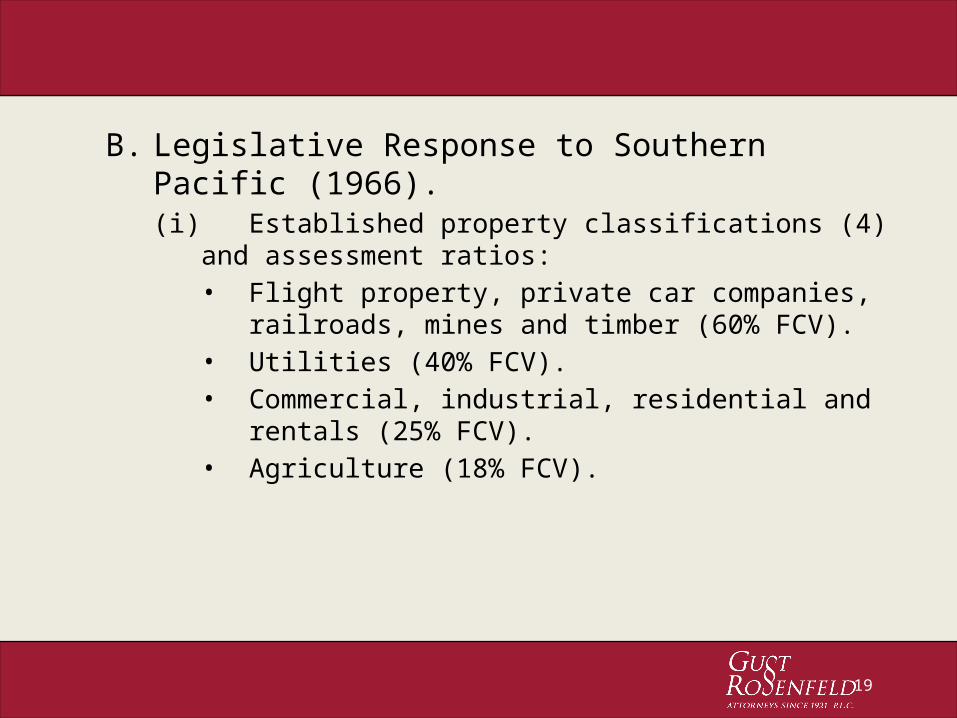

B. Legislative Response to Southern Pacific (1966).(i) Established property classifications (4) and assessment

ratios:• Flight property, private car companies, railroads, mines

and timber (60% FCV).• Utilities (40% FCV).• Commercial, industrial, residential and rentals (25%

FCV).• Agriculture (18% FCV).

19

(ii) The creation of property classes and assessment ratios created a property value described as “assessed valuation”, and such valuation was used for taxing purposes.

• But what about debt limits is the constitutional language “an amount...of the taxable value...ascertained by the last assessment...” now the equivalent of assessed valuation?

(a) No Arizona case answers the question, and the few cases across the country are split (slight majority in favor of full cash value).

20

3. Debt limit statutes.A. In addition to Constitutional debt limits, the legislature

can create statutory debt limits. Numerous statutory debt limits exist.

(i) Cities, towns counties A.R.S. Sections 35-451 and 35-503.

(ii) School districts A.R.S. Section 15-1021.

(iii) Community Facilities Districts A.R.S. Section 48-708.

21

4. Calculation of the statutory limit often differs from the Constitutional test.A. “total assessed valuation of taxable property” A.R.S.

Section 35-451.B. “aggregate net assessed value of property used for the

levy of secondary property taxes” A.R.S. Section 35-503.

C. “60% of the aggregate estimated market value” A.R.S. Section 48-708.

D. “10% of the taxable property used for secondary property tax purposes, as determined pursuant to Title 42, Chapter 15, Article I” (prior language of A.R.S. Section 15-1021).

22

A. Proposition 117(i) Let’s ask Randie

III. Further Confusion

23

PROPOSITION 117

Page 25GFOAz Summer Training 2015

Arizona Property Tax Basics

• Levied by multiple jurisdictions– Cities, Counties, School Districts, Community College Districts, Special Districts– State (minimum QTR only) and County (statewide)

• Levied for two types of purposes– Primary - Maintenance and operations– Secondary - Voter approved bonds, overrides and special districts (i.e. Fire Districts,

Sanitary Districts Community Facilities Districts)

• Property valued by two entities– Locally Assessed – County Assessors– Centrally Valued – Department of Revenue

• Two types of property– Real– Personal

• Three types of tax rates– Rate specific – rate established outside the levying jurisdictions– Levy specific – e.g. bond debt service amount needed for fiscal year– Statewide Truth in Taxation rates

Page 26GFOAz Summer Training 2015

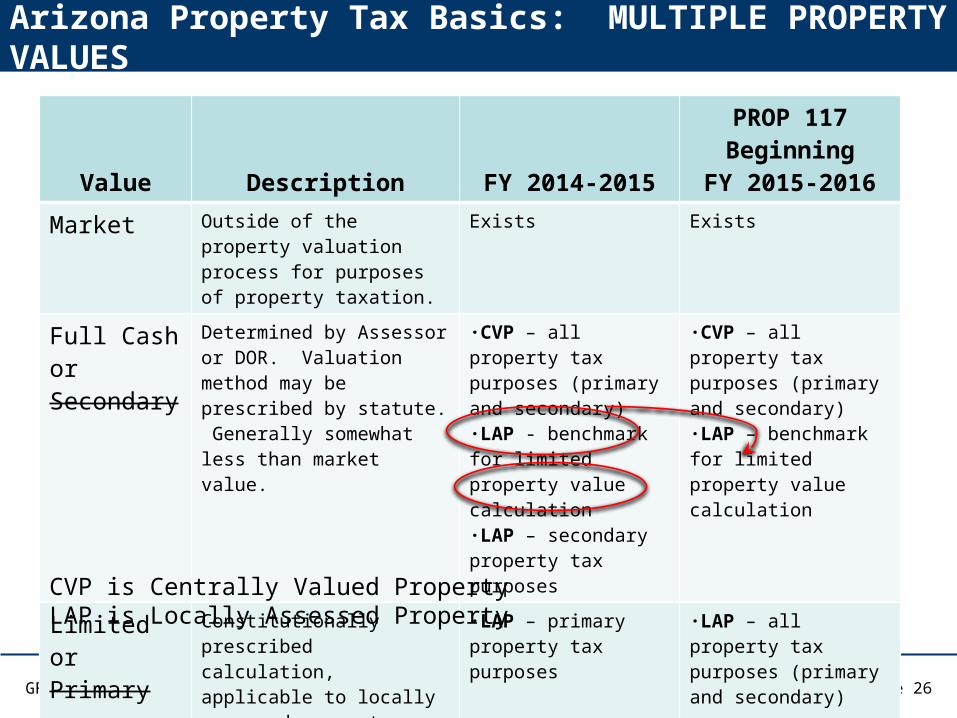

Arizona Property Tax Basics: MULTIPLE PROPERTY VALUES

Value Description FY 2014-2015

PROP 117Beginning

FY 2015-2016

Market Outside of the property valuation process for purposes of property taxation.

Exists Exists

Full Cash or Secondary

Determined by Assessor or DOR. Valuation method may be prescribed by statute. Generally somewhat less than market value.

·CVP – all property tax purposes (primary and secondary)·LAP - benchmark for limited property value calculation·LAP – secondary property tax purposes

·CVP – all property tax purposes (primary and secondary)·LAP – benchmark for limited property value calculation

Limited or Primary

Constitutionally prescribed calculation, applicable to locally assessed property. Never greater than FCV.

·LAP – primary property tax purposes

·LAP – all property tax purposes (primary and secondary)

CVP is Centrally Valued PropertyLAP is Locally Assessed Property

Page 27GFOAz Summer Training 2015

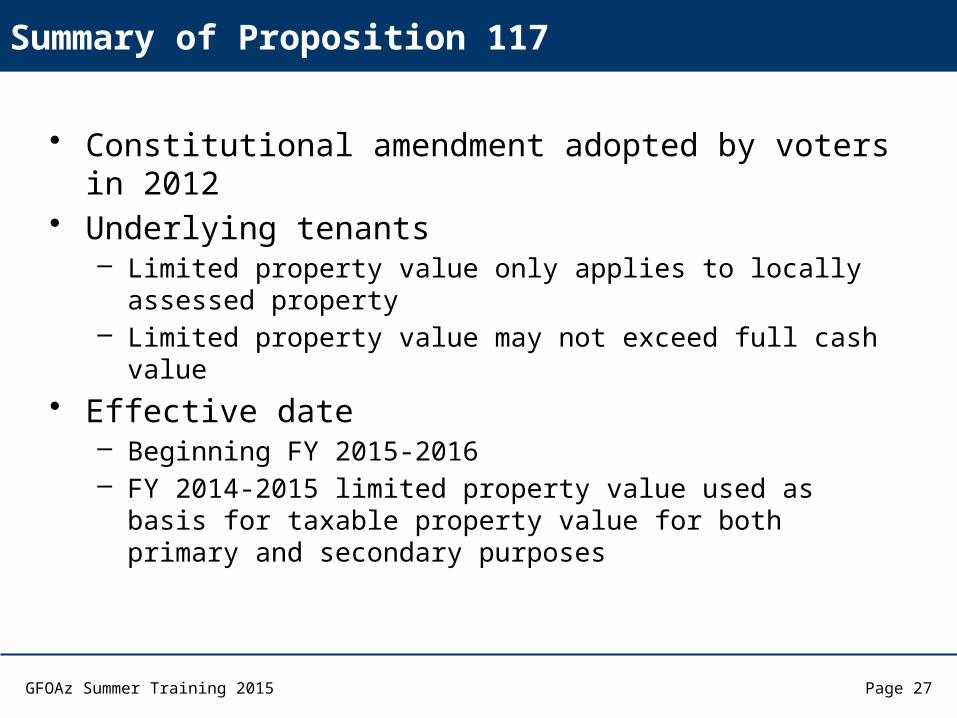

Summary of Proposition 117

• Constitutional amendment adopted by voters in 2012• Underlying tenants

– Limited property value only applies to locally assessed property– Limited property value may not exceed full cash value

• Effective date– Beginning FY 2015-2016– FY 2014-2015 limited property value used as basis for taxable

property value for both primary and secondary purposes

Page 28GFOAz Summer Training 2015

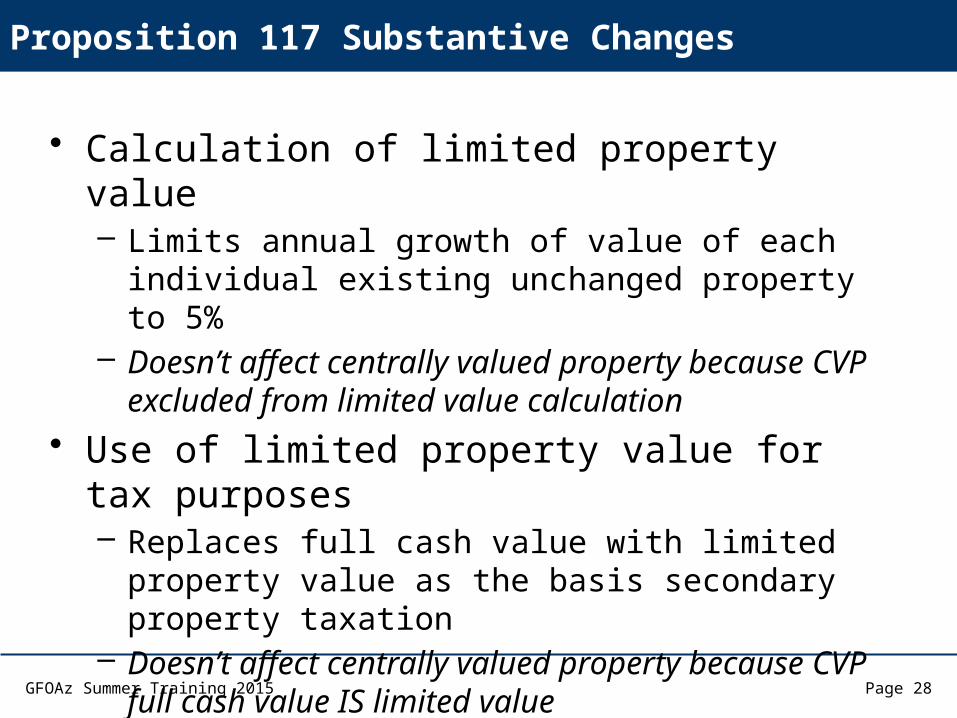

Proposition 117 Substantive Changes

• Calculation of limited property value– Limits annual growth of value of each individual existing

unchanged property to 5%– Doesn’t affect centrally valued property because CVP

excluded from limited value calculation• Use of limited property value for tax purposes

– Replaces full cash value with limited property value as the basis secondary property taxation

– Doesn’t affect centrally valued property because CVP full cash value IS limited value

Page 29GFOAz Summer Training 2015

WARNIN

G:

Complic

ated

and

Unreso

lved

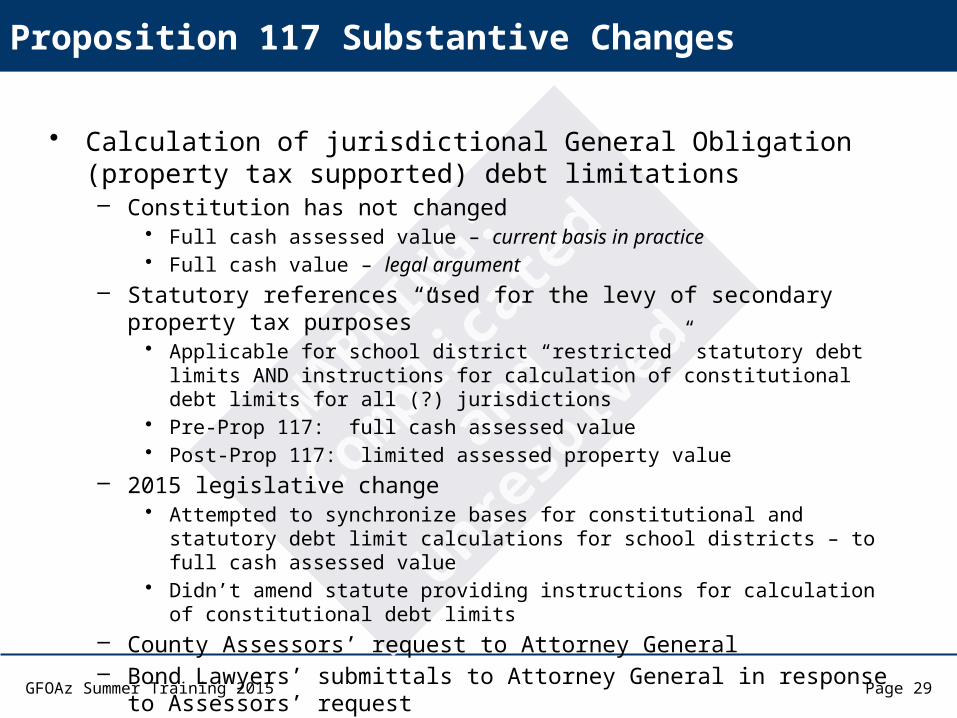

• Calculation of jurisdictional General Obligation (property tax supported) debt limitations– Constitution has not changed

• Full cash assessed value – current basis in practice• Full cash value – legal argument

– Statutory references “used for the levy of secondary property tax purposes”• Applicable for school district “restricted” statutory debt limits AND instructions for

calculation of constitutional debt limits for all (?) jurisdictions• Pre-Prop 117: full cash assessed value• Post-Prop 117: limited assessed property value

– 2015 legislative change• Attempted to synchronize bases for constitutional and statutory debt limit calculations

for school districts – to full cash assessed value• Didn’t amend statute providing instructions for calculation of constitutional debt limits

– County Assessors’ request to Attorney General– Bond Lawyers’ submittals to Attorney General in response to Assessors’ request

Proposition 117 Substantive Changes

Page 30GFOAz Summer Training 2015

Proposition 117 Substantive Changes

FULL CASH VALUE LIMITED PROPERTY VALUE

Total Value(akin to market value)

$100,000 house

Total Value(annual growth limited by constitution)

$90,000 house

Total Assessed Value(after application of assessment ratios)

Total Assessed Value(after application of assessment ratios)

Exempt Amount(pursuant to Constitution, in terms of

assessed value)

Exempt Amount(pursuant to Constitution, in terms of

assessed value)

Net Assessed Value(no longer used as basis for taxation)

$10,000

Net Assessed Value(tax rates applied per $100 of assessed value)

$9,000

Page 31GFOAz Summer Training 2015

PROP 117 IMPLICATIONS IN FY 2015-16

• Property value for secondary tax purposes likely decreased or increased only slightly– Limited value is never greater than current full cash

value– FY 2014 -15 limited value is basis for FY 2015-16

secondary tax base• Property value for primary tax purposes generally

same growth, as under prior limited value provision– Annual growth from year to year may differ– Average growth over time likely similar

Page 32GFOAz Summer Training 2015

Stifel Disclosure

Stifel’s Public Finance Department has prepared this presentation to provide you with general information (as that term is defined in the SEC’s Municipal Advisor Rule) and we are not providing you with any advice or making any recommendation concerning the structure, timing or terms of any issuance of municipal securities or municipal financial products. This presentation may contain information derived from sources other than Stifel. While we believe such information to be accurate and complete, Stifel does not guarantee the accuracy of this information. This material is based on information currently available to Stifel or its sources and is subject to change without notice. Stifel does not provide accounting, tax or legal advice. This presentation may not be distributed or duplicated without the permission of Stifel. Stifel invests significant time and effort in preparing these materials and requests that you respect our prerogative to limit distribution to our clients and as we deem consistent with our business plan.

PROPERTY TAX OVERSIGHT COMMISSION

Page 34GFOAz Summer Training 2015

Property Tax Oversight Commission

• Created by 1987 legislation with first meeting in January 1988

• Established to further public confidence in property tax limitations

• Members include:– David Raber, Director of Revenue serves as chair– Jim Brodnax, Kevin McCarthy, Fred Stiles appointed

jointly by the President and Speaker– Jeff Lindsey appointed by the Governor

• Department of Revenue provides staff• Meets about four times a year

Page 35GFOAz Summer Training 2015

PTOC – Duties of the Commission

• Review property tax levies to ensure they comply with statutory and constitutional limitations– Counties, community colleges, cities and towns and fire

districts were added in 2010• Confirm truth in taxation hearing compliance• Review County School Superintendent’s estimate

for school districts and calculation of minimum school tax rate per § 15-992.B

• Determine school districts with frozen tax rates per § 42-17151.C

• 2015 legislation – SB 1476 and HB 2615

Page 36GFOAz Summer Training 2015

Levy Limit Worksheets

• County Assessors distribute levy limit worksheets by February 10 each year– Values on levy limit worksheet cannot be changed after

February 10 without the PTOC’s approval– Any change in values for the PTOC’s approval are

submitted by the County Assessor or ADOR– Ten days after receipt, jurisdictions are to notify PTOC of

their agreement or disagreement with the levy limit worksheet (§ 42-17054.B)• Failure to act is deemed as agreement (R15-12-204)

Page 37GFOAz Summer Training 2015

Levy Limits – Counties, Colleges, Cities and Towns

• 2% plus new construction– Base starting point is the prior year maximum allowable levy limit even

if a jurisdiction under levied in prior year (Article IX, Section 19 and A.R.S.§42-17051.E)

• Proposition 101 approved by voters in 2006 removed unused taxing capacity based on actual tax levy in 2005

• New construction– Section B is current values but excludes new construction– Section C reflects current values with new construction– New construction is Section C values less Section B values

• Maximum Allowable Tax Rate and Levy Limit– Maximum tax rate is prior year’s maximum allowable levy limit

increased by 2% (Section A) ÷ by values in Section B– Maximum allowable levy limit multiplies maximum tax rate by values in

Section C ÷ 100

Page 39GFOAz Summer Training 2015

Levy Limits and Adopted Tax Rates

• If a political subdivision intends to levy above its allowable levy limit due to involuntary torts, copies of those torts must be submitted to the PTOC on or before the first Monday of July (R15-12-202)

• Tax rates are adopted by the County Board of Supervisors on or before the third Monday in August– Must use values from the February 10 levy limit

worksheet (or PTOC approved change in values)– Tax rate must be rounded to four decimal places– Tax rate and levy must not exceed the maximum

allowable limit per the levy limit worksheet

Page 40GFOAz Summer Training 2015

Review of Adopted Tax Rates

• Three days after final tax rates are determined, the county will notify the PTOC (§ 42-17151.E)

• County Treasurer reports actual collections for prior tax year to confirm jurisdictions did not exceed maximum allowable levy limit

• On or before September 15, the PTOC will notify jurisdictions of any violations (§ 42-17003.B)– If jurisdictions over levied and it’s too late to correct in the current

year, they must reduce levy in the following year• If a jurisdiction disputes the PTOC’s findings, then on or

before October 1 the jurisdiction may request a hearing before the Commission (§ 42-17004.A & R15-12)

Page 41GFOAz Summer Training 2015

Truth in Taxation Hearing

• If proposed tax levy, excluding amounts attributable to new construction, is greater than the amount levied in the prior year, a TNT hearing must be held (§ 42-17107)– TNT tax rate = prior year’s actual levy ÷ current year

value of last year’s property– Staff provides confirmation of the tax rate that will

trigger a TNT hearing– Penalty for non-compliance is to levy no more than the

TNT tax rate the following year

Page 42GFOAz Summer Training 2015

TNT Published Notice

• TNT published notice must use the exact language pursuant to A.R.S.§ 42-17107 and nothing more– If a jurisdiction includes additional comments, they must be outside

of the solid black border• TNT analysis worksheets provides the data required for the

published notice• First publication at least 14 but no more than 20 days before

hearing • Second publication at least 7 but no more than 10 days• Issue a press release containing the TNT notice• Governing body will consider a motion to levy the increased

property taxes by roll call vote• Provide copy of TNT documents 3 days after hearing

Page 44GFOAz Summer Training 2015

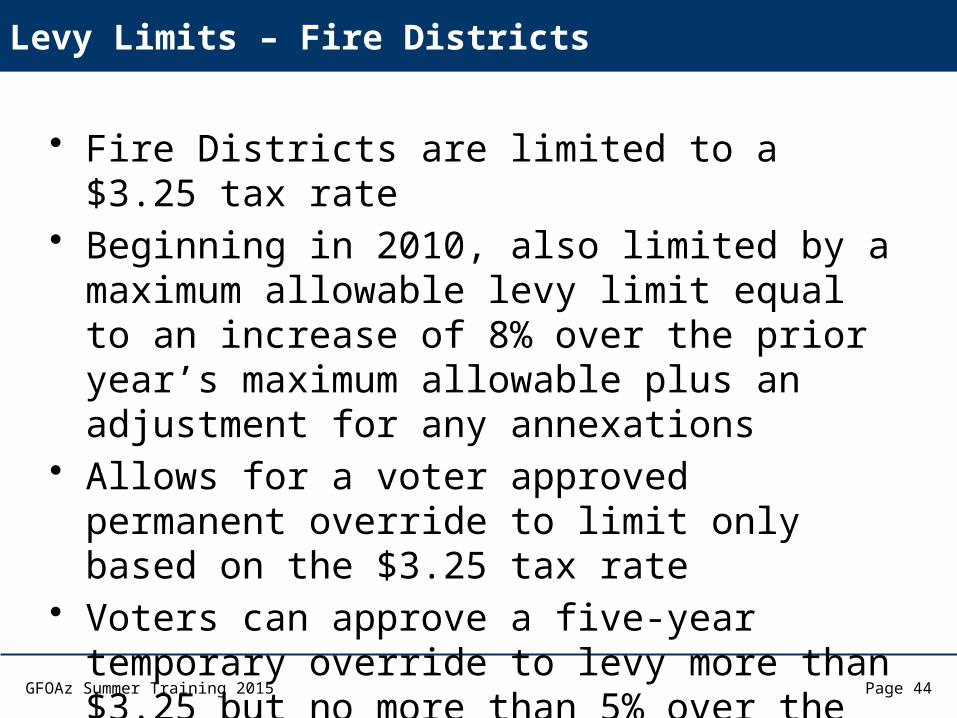

Levy Limits – Fire Districts

• Fire Districts are limited to a $3.25 tax rate• Beginning in 2010, also limited by a maximum

allowable levy limit equal to an increase of 8% over the prior year’s maximum allowable plus an adjustment for any annexations

• Allows for a voter approved permanent override to limit only based on the $3.25 tax rate

• Voters can approve a five-year temporary override to levy more than $3.25 but no more than 5% over the prior year’s actual levy amount

Page 45GFOAz Summer Training 2015

PTOC – Other Duties

• Review County School Superintendent’s calculation of minimum school tax calculation– Minimum school tax applies to districts not eligible for

equalization assistance where the value of property is unusually high relative to the number of enrolled students (§ 15-992)

• Identify school districts that are prohibited from increasing their primary property tax in the following year per § 42-17151.C if:– The district’s primary tax rate exceeded 150% of the QTR

and at least half the residential property had a combined primary tax rate greater than $10

Page 46GFOAz Summer Training 2015

PTOC Contact Information

• David Raber, Chairman• Darlene Teller, PTOC Staff

– (602) 716-6436– [email protected]

• Mailing Address:Arizona Department of Revenue

Property Tax Oversight Commission1600 West Monroe, 9th FloorPhoenix, AZ 85007-2650

• PTOC meeting notices: www.azdor.gov

Related Documents