Economic History Association External Dependence, Demographic Burdens, and Argentine Economic Decline After the Belle Époque Author(s): Alan M. Taylor Source: The Journal of Economic History, Vol. 52, No. 4 (Dec., 1992), pp. 907-936 Published by: Cambridge University Press on behalf of the Economic History Association Stable URL: http://www.jstor.org/stable/2123232 Accessed: 10/03/2010 20:41 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=cup . Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. Cambridge University Press and Economic History Association are collaborating with JSTOR to digitize, preserve and extend access to The Journal of Economic History. http://www.jstor.org

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 1/31

Economic History Association

External Dependence, Demographic Burdens, and Argentine Economic Decline After the BelleÉpoqueAuthor(s): Alan M. TaylorSource: The Journal of Economic History, Vol. 52, No. 4 (Dec., 1992), pp. 907-936Published by: Cambridge University Press on behalf of the Economic History AssociationStable URL: http://www.jstor.org/stable/2123232

Accessed: 10/03/2010 20:41

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at

http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless

you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you

may use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at

http://www.jstor.org/action/showPublisher?publisherCode=cup.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed

page of such transmission.

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of

content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms

of scholarship. For more information about JSTOR, please contact [email protected].

Cambridge University Press and Economic History Association are collaborating with JSTOR to digitize,

preserve and extend access to The Journal of Economic History.

http://www.jstor.org

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 2/31

External Dependence, DemographicBurdens, and Argentine Economic

Decline After the Belle EpoqueALAN M. TAYLOR

Once one of the richest countries in the world, Argentina has been in relative

economic decline for most of the twentieth century. The quantitative records of

income growth and accumulation date the onset of the retardation to around the

time of the Great War, and patterns of aggregate saving and foreign borrowing

show that scarcity of investable resources significantly frustrated interwar devel-

opment. A demographic model of national saving demonstrates that the burdensof rapid population growth and substantial immigration depressed Argentinesaving, contributing significantly to the demise of the Belle Apoque following the

wartime collapse of international financial markets.

It is common nowadays to lump the Argentine economy

in the same category with the economies of other Latin

American nations. Some opinion even puts it among such

less developed nations as India and Nigeria. Yet, most

economists writing during the first three decades of this

century would have placed Argentina among the most

advanced countries-with Western Europe, the UnitedStates, Canada, and Australia. To have called Argentina

"underdeveloped" in the sense that word has todaywould have been considered laughable. Not only was per

capita income high, but its growth was one of the highestin the world.'

-Carlos Diaz-Alejandro

THE MYSTERY OF ARGENTINE ECONOMIC DECLINE

T he record of Argentine economic performance tells a story ofdecline unparalleled n modem times. The country has endured a

The Journal of Economic History, Vol. 52, No. 4 (Dec. 1992). ? The Economic HistoryAssociation. All rights reserved.ISSN 0022-0507.

The author s anAcademyScholarand MellonFellow at the HarvardAcademyforInternationaland Area Studies andthe Department f Economics, HarvardUniversity, Cambridge,MA02138.

This is a much revisedversion of a paperI presentedat the InstitutoTorcuatoDi Tella,BuenosAires, in June 1991 (Taylor, "Birds of Passage"). I thankthe Tinker Foundation, he HarvardCenter or Latin Americanand IberianStudies,the HarvardCenterfor InternationalAffairs,and

the HarvardAcademy for Internationaland Area Studies for financialsupportand researchresources.Ian McLeanandJeffreyWilliamsonhave offeredgenerousguidanceduring hisproject.For theirmany helpfulcomments, suggestions, and datahints I am indebted to RobertoCortdsConde, Gerardo Della Paolera, Ezdquiel Gallo, MarcelaHarriague,Tim Hatton, Juan CarlosKorol, MarkThomas, MalcolmUrquhart,ClaireWaters,and John Womack,Jr., andto seminarparticipants t StanfordUniversity,the Universityof Californiaat Berkeley,and the East-WestCenter at the Universityof Hawaii. This work has also benefited fromthe comments of threeanonymousrefereesandan editorof thisJOURNAL. None of the above bears responsibilityor anyshortcomingsn the article.

' Dfaz-Alejandro,Essays, p. 1.

907

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 3/31

908 Taylor

painfuladjustment o the end of the Belle Epoque, a glitteringperiod inits historythat reached its peak early this century. A visitor to Buenos

Aires then would have marveled at the splendors of the city: theimpressive opera house, the graceful architecture, the sophisticatedrailway system. Today the city presents the same elegant facade, onlyfrayed and decayingat the edges-and the visitor marvels that the citycan function at all, given its dilapidated nfrastructure.The satisfactionof living in one of the richest countries in the world is now a distantmemory for the Argentines,who have struggledto come to terms withtheir sinking status. The downfallof this once developed country is asmuch of an enigma for students of economic history, and the contra-

dictions between her past success andcurrent ailureconstitute "one ofthe most puzzling and misunderstood national stories in the develop-ment literature."2

Even the timing of the decline is a topic of long-standing andcontentious debate. Carlos Diaz-Alejandrohas dated the end of theBelle Epoque as late as the onset of the Great Depressionin 1929, notingthat Argentine per capita income continued to converge upward onAustralian evels into the 1920s.Elsewhere, he used similarevidence on

respectable growth performancerelative to Australia and Canada todismiss Guido Di Tella and ManuelZymelman'sthesis that Argentinaexperienced a "Great Delay" between 1914 and 1933, a delay theyattributedto misguided policies.3 In defense of the early-retardationhypothesis, Di Tella cited the precipitous decline in growth ratesobserved duringWorldWar I-a retardation hat has persisted to thepresent day. By way of explanation, he invoked the closing of thefrontier, as the Pampashadbecomefully occupied around hat time. Heconcluded that the extensive growthstrategy had runits course:

The rate of growthof the economy, after the closing of the frontier, averagedabout 3 per cent per year in the inter-warperiod,and about the same from theSecond World War. But when the actual developmentis comparedwith thepre-1914 performance, or even more so with the expectations nurturedat thebeginningof this century, Argentine performance ooks dismal. It is this falsecomparisonbetween a wronglybasedprojectionandthe actualperformancehathas contributed o the sense of failure whichpermeatesthe Argentines'view ofthemselves as a Nation.4

The nationalsense of failurealludedto makes any debate on such asensitive question politically charged. The Great Depression encour-aged Argentina and other Latin American countries to subscribe to

2 Dfaz-Alejandro,"One HundredYears," p. 230.3 Ibid., p. 232; Diaz-Alejandro,Essays, pp. 51-55; and Di Tella and Zymelman,Las etapas,

chaps. 2-4. The latter used a Rostovianframework o characterizeArgentinegrowth, addinga"great delay" between what they see as Rostovian"preconditions" 1880-1914)and "takeoff"(1933-1952).

4 Di Tella, "Economic Controversies," p. 122; and Dfaz-Alejandro,Essays, p. 53. Dfaz-Alejandroalso acknowledged hat the Pampaswere fullyutilizedby this time.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 4/31

Argentine Economic Decline 909

inward-lookingeconomic policies and import substitution-policieslater to be codifiedand applied by the Economic Commissionfor Latin

America (ECLA) through the efforts of RautlPrebisch and otherstructuralists.Diaz-Alejandrohas distinguishedbetween the efficacy ofthose "reactive" policies in the Depressionyears and their persistenceafter WorldWarII, which inhibitedexport-ledgrowthand placed a dragon Argentinedevelopment.5Clearly, if economic failure can be said topredatethe adoption of import-substitutiondoctrines, the structuralistcamp can evade responsibility for decline and implicate the liberal,export-orientedpolicy regime prevailinguntil 1929.This is a point lost

onneither

Diaz-Alejandro,one of the harshest critics of structuralism,

nor Di Tella, a sometime apologistfor importsubstitution.What, then, marked he endof theBelleEpoque:the GreatWarorthe

GreatDepression? Few of the protagonists n the debate can agree onthe timing, let alone the mechanismsof Argentineeconomic growth-butall agreethat the countryin some sense failed. For the developmenteconomist it is enlightening,even uplifting,to study national successcases: to try to figureout what went rightand how those lessons can beapplied elsewhere. Yet the study of economic failure, though depress-

ing, can be a revealing exercise. More compelling and mysteriousexamplesof failurethan the ruinationof Argentinaare hardto imagine.An array of intriguing questions presents itself: When did the tablesturn?How dramaticwas the decline?Whatwas the basis of the previoussuccess? Why did it disappear?

To answer these questions we must firstassess the quantitativerecordof Argentine growth in an internationalperspective. The issue oflong-runeconomic developmentand the relativeperformanceof differ-ent countries has recently come under close scrutiny. In the historicalarena, the work of Angus Maddison, William Baumol, BradfordDeLong, and other investigatorshas offeredus a detailed perspective ontrends in growthperformanceover the last 100years or more.6In thisspiritI will now review the irregular ecord of Argentineperformance na comparativesetting. Of particularnterest is the commoncomparisonof Argentinawith the other settler economies, Australia and Canada,and the measure of Argentine performancerelativeto the largerOECDgroupof now developed countries.

The relative economic performanceof Argentina in the twentiethcentury is summarized n Table 1. The picture presentedthere imme-diately begins to unravel the confusion in the debate over Argentinefailure:one's view of relativeArgentineretardationdepends entirelyon

5 Prebisch,"Recollections"and "Five Stages"; andDiaz-Alejandro,Essays, "Latin Americain the 1930s,""The 1940s n Latin America,""Some Characteristics," nd"DelinkingNorth andSouth."

6 Maddison,Phases and The WorldEconomy; Baumol, "ProductivityGrowth,Convergenceand Welfare";andDe Long, "ProductivityGrowth, Convergenceand Welfare:Comment."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 5/31

910 Taylor

TABLE 1

COMPARATIVE ECONOMIC GROWTH

1900 1913 1929 1950 1973 1987A. GDP per Capita (international dollars, 1980 prices)

Argentina 1,284 1,770 2,036 2,324 3,713 3,302

Australia 2,923 3,390 3,146 4,389 7,696 9,533

Canada 1,808 2,773 3,286 4,822 9,350 12,702

OECD 1,817 2,224 2,727 3,553 7,852 10,205

B. GDP per Capita (relative to OECD = 1.00)

Argentina 0.71 0.80 0.75 0.65 0.47 0.32

Australia 1.61 1.52 1.15 1.24 0.98 0.93

Canada 1.00 1.25 1.20 1.36 1.19 1.24

C. Growth Rates of GDP per Capita (%)

1900-1913 1913-1929 Retardation

(1) (2) (1) - (2)

Argentina 2.47 0.88 1.59

Australia 1.14 -0.47 1.61

Canada 3.29 1.06 2.23

OECD sample 1.55 1.27 0.25 [0.95]a

28-country sample 1.34 1.02 0.33 [0.98]a

a This denotes a sample average, with the standard deviation shown in brackets.

Note: Panel B is derived from Panel A.

Sources:Maddison,The WorldEconomy,p. 19.

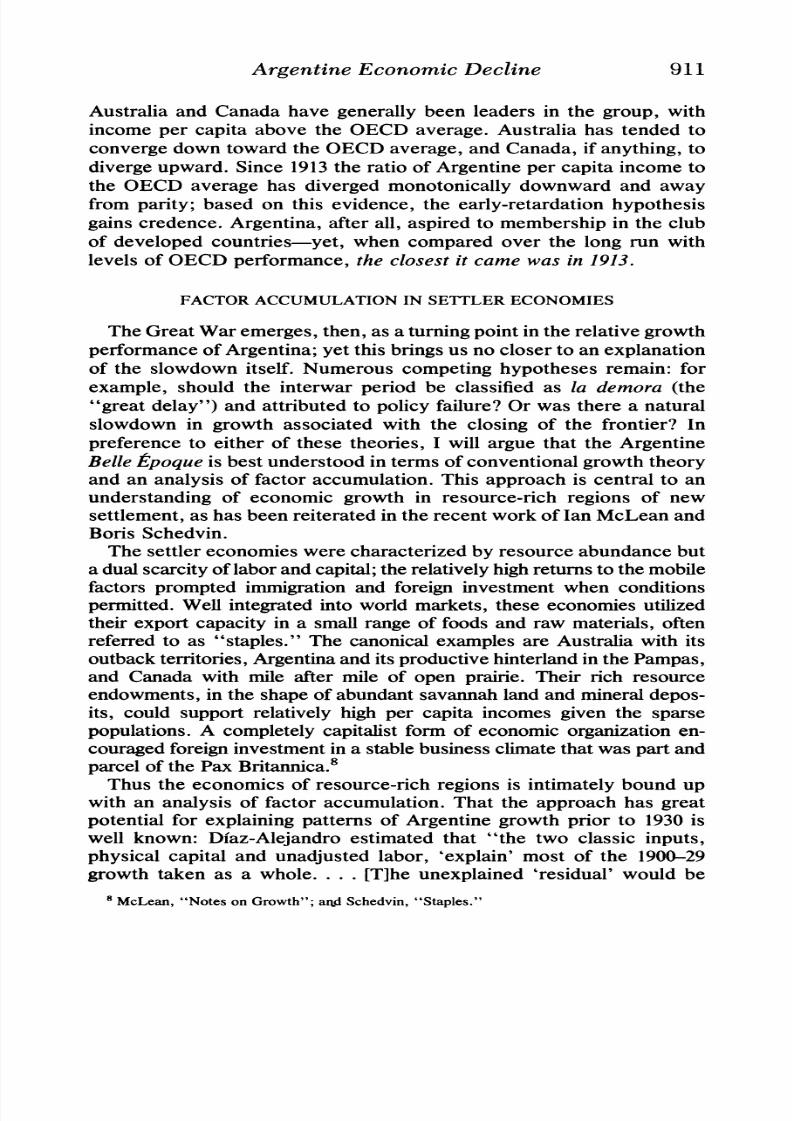

the basis of the comparison. Australiaand Canadaperformeddismallyin the interwarperiod, undergoingretardation relative to the OECDgroupas a whole (their ratio of income per capitarelativeto the OECDaveragefell from 1913 to 1929); n thatcontext, Argentine performance

looks respectable. Furthermore, he table illustrates that the post-1913retardationwas much more serious in the settler economies (rangingfrom 1.59 to 2.23percentagepoints)thanin the OECD (0.25). In a sense,Diaz-Alejandro s rightto praise Argentinafor keeping pace with theother settler economies; but keeping pace with stragglersis no greatfeat. Infact, the settlereconomieswere hitmuchharder hanalmostanyothercountry by the economic shocks associated with the GreatWar,asseen in Maddison's full sample of 28 countries (see panel C). It is

strikingthat among the five hardest hit countries, three were settlereconomies.7Thusa comparisonofjust the settler economies is misleading,tending

to mutualflattery amonga groupof poor performers.Table 1 providesthe more reliable large-sample comparisonwe seek with the OECD.

' The othercountrieswere Mexico (embroiled n a revolution)andthe Philippines,and all fiveexperienceda decline in growth rates of at least 1.59percentagepoints;the next worst case wasItaly,with 1.11percentagepoints. Onlythese five lay more than one standarddeviationbelowthemean retardation.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 6/31

Argentine Economic Decline 911

Australiaand Canadahave generally been leaders in the group, withincome per capita above the OECD average. Australia has tended to

converge down toward the OECDaverage, and Canada, if anything, todiverge upward.Since 1913the ratio of Argentineper capitaincome tothe OECD average has diverged monotonically downward and awayfrom parity; based on this evidence, the early-retardationhypothesisgains credence. Argentina, afterall, aspired to membership n the clubof developed countries-yet, when comparedover the long run withlevels of OECD performance, the closest it came was in 1913.

FACTORACCUMULATION N SEITLER ECONOMIES

TheGreatWaremerges, then, as a turningpointin the relativegrowthperformanceof Argentina;yet this bringsus no closer to an explanationof the slowdown itself. Numerous competing hypotheses remain:forexample, should the interwarperiod be classified as la demora (the"great delay") and attributed o policy failure?Or was there a naturalslowdown in growth associated with the closing of the frontier? Inpreference to either of these theories, I will argue that the Argentine

Belle tpoque is best understood n terms of conventionalgrowth theoryand an analysis of factor accumulation. This approach is central to anunderstandingof economic growth in resource-rich regions of newsettlement,as has been reiterated n the recent work of Ian McLean andBoris Schedvin.

The settlereconomies were characterizedby resource abundancebuta dualscarcityof laborandcapital; herelativelyhighreturns o themobilefactors prompted immigrationand foreign investment when conditions

permitted.Well integrated nto worldmarkets, these economies utilizedtheirexport capacity in a smallrange of foods and raw materials,oftenreferred o as "staples." The canonicalexamplesare Australiawith itsoutback erritories,Argentina nditsproductivehinterlandn thePampas,and Canadawith mile after mile of open prairie.Their rich resourceendowments, n the shapeof abundant avannah and and mineraldepos-its, could support relatively high per capita incomes given the sparsepopulations.A completely capitalistform of economic organization n-couraged oreign nvestment n a stablebusinessclimate hat was partand

parcelof the Pax Britannica.8Thus the economics of resource-richregions is intimatelybound up

with an analysis of factor accumulation. That the approachhas greatpotential for explaining patterns of Argentine growth prior to 1930 iswell known: Dfaz-Alejandroestimated that "the two classic inputs,physical capital and unadjustedlabor, 'explain' most of the 1900-29growth taken as a whole.... [T]he unexplained 'residual' would be

8 McLean, "Notes on Growth";and Schedvin, "Staples."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 7/31

912 Taylor

limited to between 14 and 20 percent of the growth rate."9 In whatfollows I apply the approachto the commoncomparisonof two settler

economies, Australia and Argentina. The same analysis could bepursuedwithCanadaaddedto the sample, of course, but scholars focuson the two SouthernHemisphereregionsbecause they have the richesttraditionof comparativeanalysis in economic history, being similar interms of geographicposition and size.10(Canada,on the otherhand, hascertaindistinctivefeatures, notably its proximityto the United States,that make comparisons slightly more difficult.) It will be seen thatalthough broadly similar factor accumulationpatterns characterizedAustraliaand Argentina,compositional differences stand out, and the

size of the flows differedgreatlybefore and after 1913.This breakpoint,I argue, offers insights into the onset of Argentinedecline.

Population Growth, Path Dependence, and the Demographic Burden

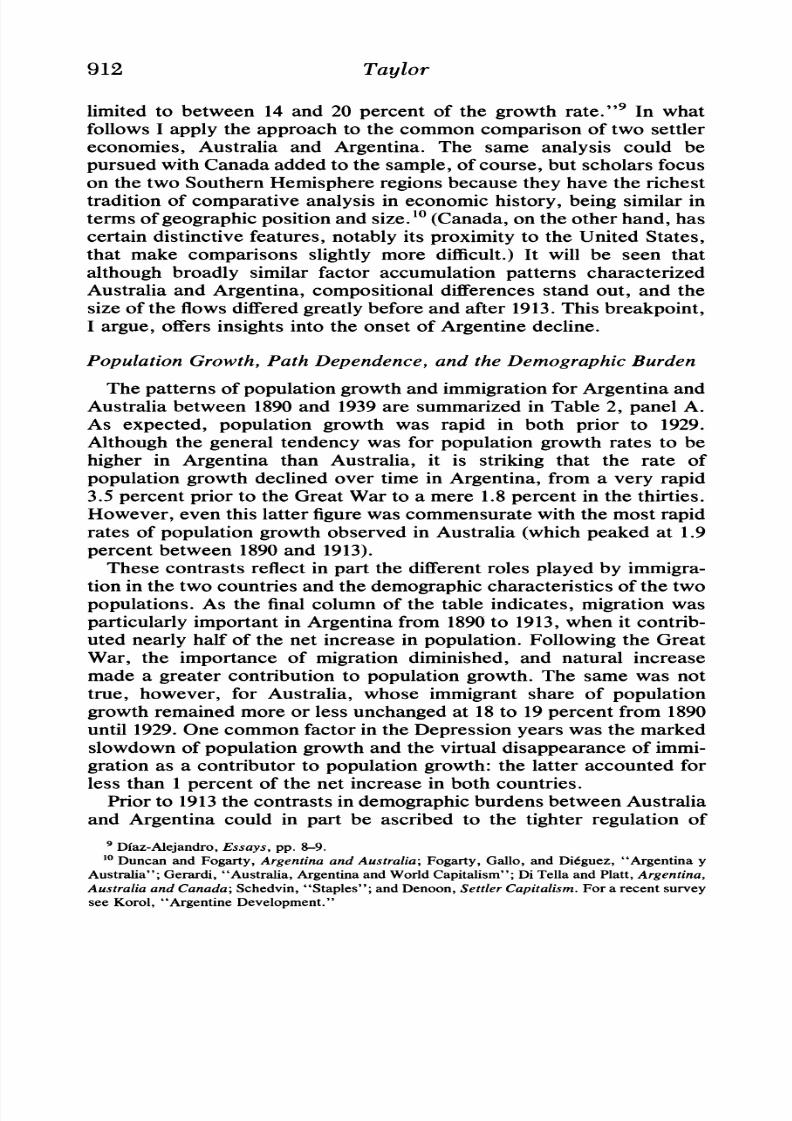

The patterns of populationgrowth and immigration or ArgentinaandAustraliabetween 1890and 1939 are summarized n Table 2, panel A.As expected, population growth was rapid in both prior to 1929.Althoughthe general tendency was for population growth rates to be

higher in Argentina than Australia, it is striking that the rate ofpopulation growth declined over time in Argentina,from a very rapid3.5 percent priorto the Great Warto a mere 1.8 percent in the thirties.However, even this latterfigurewas commensuratewith the most rapidrates of population growth observed in Australia (which peaked at 1.9percent between 1890 and 1913).

These contrasts reflect in partthe differentroles played by immigra-tion in the two countries and the demographiccharacteristicsof the two

populations.As the final column of the table indicates, migrationwasparticularly mportant n Argentina rom 1890 to 1913,when it contrib-uted nearly half of the net increase in population.Followingthe GreatWar, the importance of migration diminished, and natural increasemade a greatercontribution to population growth. The same was nottrue, however, for Australia, whose immigrantshare of populationgrowthremainedmore or less unchangedat 18to 19percentfrom 1890until 1929. One common factor in the Depression years was the markedslowdown of populationgrowthand the virtualdisappearanceof immi-

gration as a contributor o populationgrowth:the latter accounted forless than 1 percent of the net increase in both countries.

Priorto 1913the contrastsin demographicburdensbetween Australiaand Argentina could in part be ascribed to the tighter regulation of

9 Dfaz-Alejandro,Essays, pp. 8-9.10 Duncan and Fogarty, Argentinaand Australia;Fogarty, Gallo, and Didguez, "Argentinay

Australia";Gerardi,"Australia,Argentina nd WorldCapitalism";Di Tella andPlatt, Argentina,Australiaand Canada;Schedvin, "Staples";and Denoon, Settler Capitalism.Fora recent surveysee Korol, "ArgentineDevelopment."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 8/31

Argentine Economic Decline 913

TABLE 2FACTORACCUMULATION:ARGENTINAAND AUSTRALIA,1890-1939

A. PopulationPopulation ShareDue to

Initial GrowthRate Net Natural ImmigrationPopulation (%) Immigration Increase (%)

Argentina1890-1913 3.377 3.5 1.922 2.183 471913-1929 7.482 2.8 0.630 3.633 151929-1939 11.745 1.8 0.014 2.295 0.6

Australia1890-1913 3.107 1.9 0.319 1.395 19

1913-1929 4.821 1.8 0.282 1.293 181929-1939 6.396 0.9 0.001 0.574 0.2

B. Capital

InitialCapital CapitalStock InitialForeign- InitialShareStock GrowthRate(%) OwnedCapital ForeignOwned(%)

Argentina1890-1913 478 4.81913-1929 1,450 2.2 704 481929-1939 2,059 1.1 659 32

Australia1890-1913 1,099 1.91913-1929 1,713 2.3 344 201929-1939 2,470 1.2 545 22

Notes: Population s given in millions, capitalin ? millions,at 1910prices. Growthrates werederived from stocks. The natural increase of populationis populationincrease minus netimmigration.The share due to immigration s net immigrationdividedby population ncrease.Foreign-owned apitalstock was derivedfromthe shareforeignowned usingtotal stock, or viceversa.Sources: For populationand capital stock, see the Appendix. Immigrationwas taken fromMitchell,InternationalHistoricalStatistics, table B7. Argentina'sshareof capitalstock foreignowned is fromLewis, Crisis, p. 49. Australia's oreign-owned apital is equal to the cumulatedcapital nflowdeflatedby the GDPdeflator, rom M. Butlin,"PreliminaryDatabase,"pp. 81-82,111. The monetaryconversionis ?1 equalsA$2.

immigrationin Australia. There the authorities operated a de facto"white Australia" policy and were careful to admit a fairly homoge-neous stream of predominantlyBritishmigrants.11There is still somedebate over whetherthis policy placed a floor underAustralianwagesby generatinglabor scarcity, but such a theory is consistent with our

observations. We can at least be sure that capitalwideningwas less ofa problem for Australia, as a resultof lower migrationrates and slowerpopulationgrowth.'2 Argentina, on the other hand, received a moreheterogeneousstreamof migrants,principally romItalyandSpain.Thesupplyof immigrants ended to be extremelyplentiful,and at times theincentives were so greatas to prompteven temporarymigrationacross

" Offer, The First World War, chap. 12.12 Dfaz-Alejandro, Argentina,AustraliaandBrazil,"p. 103.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 9/31

914 Taylor

the Atlantic. Laborerswould leave southernEurope for Argentinainthe northernwinter, engageas seasonallabor on the Pampas,andreturn

after the southernharvestin time for the startof the northernsummer.Cheappassageencouraged his unparalleled easonalmigration,and thehardy souls who made these formidablevoyages earned the sobriquet"birds of passage.",13

The implicationsof these differentmigratoryenvironmentsareappar-ent from the compositionof the resultingmigrant treams.It is clearthatthe international abor marketsfor Argentinaand Australiawere seg-mentedalong regionaland national ines: over 80 percent of Australianimmigrantshailed from Britain,whereas about the same proportionof

Argentineimmigrantscame fromItaly or Spain.'4Can such segmenta-tion explainthe contrastin ratesof migrationandpopulationgrowth?Itis possible that differences in compositionmay help explaindifferencesin vital statistics, to the extent thatmigrantsembody such demographiccharacteristicswhen they move. Accordingto this view, faster Argen-tinepopulationgrowthfollowed, in part,from a segmented abormarketthat broughtin a relatively fecund Latin immigrant tream.'5

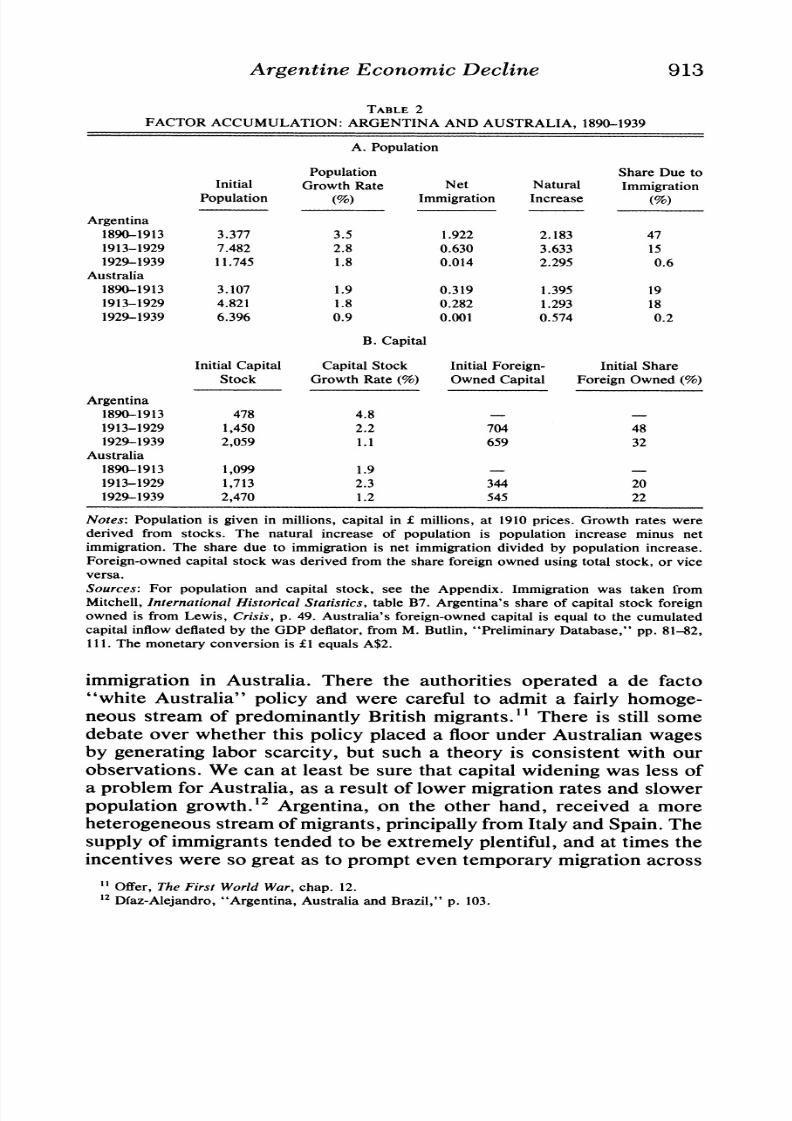

A persuasiveexplanationcan also be madeby comparing he patterns

of migrationwith observed wage gaps between sending and receivingregions, a technique commonly used in migration studies.16Recentattempts by JeffreyWilliamsonandmyself to computerelative levels ofreal wages in an internationallycommensuratefashion for a group ofcountries includingthe settler economies are consistent with the evi-dence sketchedout here. Theprincipalsending regionfor AustraliawasBritain.Australianwages were highrelative to British evels, yet tendedto converge downward over time. Startingwith an 87 percent gap in1870,the Australianwage premiumwas almosteliminatedby 1910 (a 17

percentgap)andhovered around30to 40 percentfrom 1900to 1939(seeFigure 1). The Argentine premium over Italy and Spain-its mainsending regions-was over 100percentfor almostthe entireperiodfrom1890to 1939, if we ignore a brief convergentepisode duringthe GreatWar (when migrationwas almost impossible anyway). Argentinahadmuch larger and more persistent wage gaps relative to her principalsending regions thandid Australia; hus, it is no surprisethat immigra-tion was so potent a force in Argentina.17

Another of the most distinctive dynamics driven by populationgrowthwas the changingage structure.A vast economic-demographic

13 Bungeand GarciaMata, "Argentina";and Dfaz-Alejandro,Essays, pp. 21-28."1 Bungeand GarciaMata,"Argentina,"p. 153;andMcPhee,"Australia,"p. 173.ISSpainand Italy had birth rates muchhigher thanBritain. The rates (per thousand)between

1910and 1914were Argentina,37.9; Italy, 32.0; Spain,31.3; Australia,27.8; Englandand Wales,24.2. Mitchell,InternationalHistoricalStatistics, tableB5.

16 Kelley, "InternationalMigration";Pope, "The Peoplingof Australia"; and Richardson,"BritishEmigration."

17 Williamson,"Evolution."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 10/31

Argentine Economic Decline 915

250

Argentina-ItalyGap

200 -

150 -

100 /Ia

I I ;X.4 h~~~~~~~~~~~~~~~~~~~~.,.W

Argentina-SpainGap

50*U -'a' AsAustralia-Britain ap *

1890 1900 1910 1920 1930

FIGURE I

WAGE GAPS BETWEENARGENTINAAND AUSTRALIAAND THEIR PRINCIPALSENDINGREGIONS,1890-1939

Notes: Figuresarebased on Williamson'sdatabase,which consisted of nationalreal-wage ndicesand internationaleal-wagebenchmarks, alculatedusingpurchasing ower parities.Thepre-1913benchmarks reusedthroughout.Thewage gapis definedas (WR Ws- 1),whereWRs thewagein the receivingregionand Wsthe wage in the sendingregion. Three-yearmovingaveragesaredisplayed.Source:Williamson,"Evolution."

literaturehas explored these mechanisms in great detail, usually in thecontext of the contemporaryThird World.'8 It is obvious that rapidpopulation growthwill tend to swell the share of the young in the agedistribution.Dependingon the vital statistics of the population(espe-cially birthrates), the young cohorts may further increase populationgrowth rates via reproductionon reachingadulthood.Furthermore,,o

18 For a survey see Kelley, "Economic Consequences."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 11/31

916 Taylor

* Canada

0.5

Argentina

a Ad ?

-*

3 101

0.2 o3 = Australia UK 0= United States

0.1 I I I I I I I I

1860 1880 1900 1920 1940 1960 1980

FIGURE 2

DEPENDENCY RATES FOR A SAMPLE OF COUNTRIES, 1850-1990

Note: The dependencyrate is the share of the populationunder15yearsof age.Sources: See the Appendix.

the extent that migrantsself-select fromyoungadultage-groups(whichthey do), the populationof reproductiveage may be furtherenlarged.19

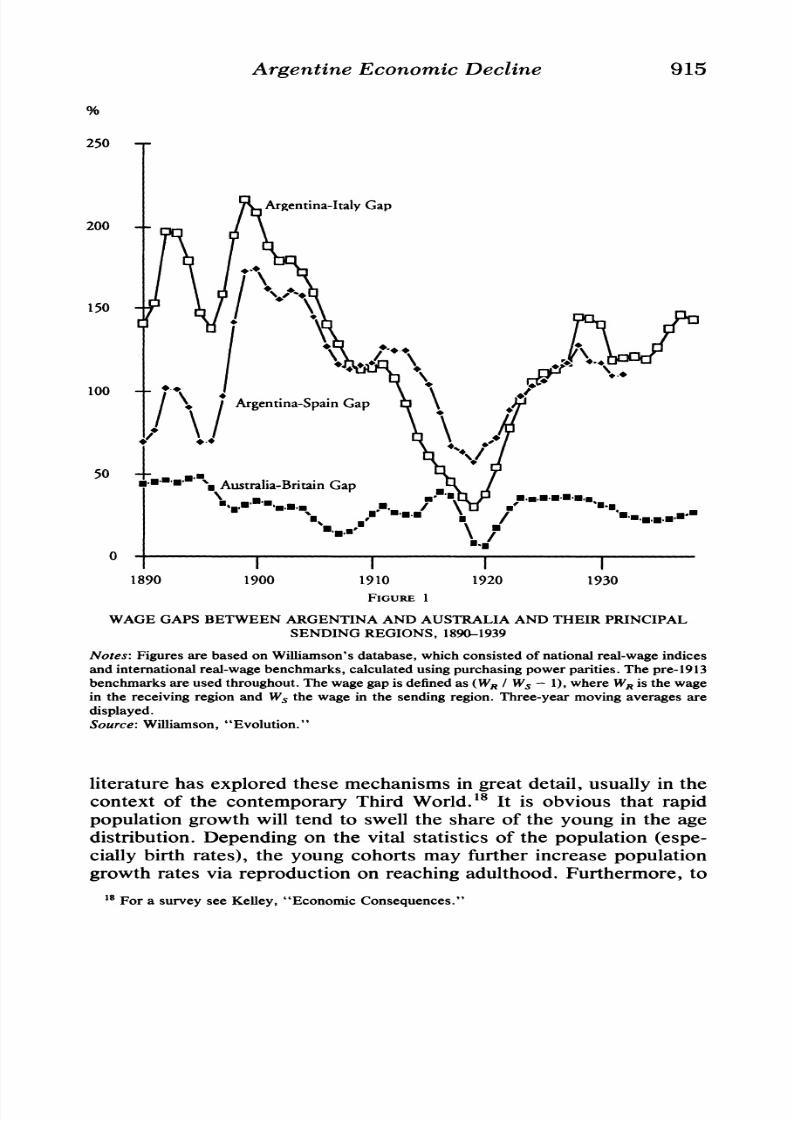

A convenientmeasure of shifts in the age structure s the dependencyrate (defined here as the share of the populationunder 15). Figure 2traces the evolution of the dependencyrate in five economies: four inthe New World (the three settler economies andthe United States) plusthe United Kingdom.The figurereveals that the New Worldgrouphadmuch higher dependency rates in general, an observation consistent

with the theory I've outlined. The Australianand North Americandependencyratesexhibitedonly a smallpercentagepointgaprelative tothe Britishlevel in the 1890 to 1929 period, but the Argentine depen-dency rategap was about twice as large. Furthermore, he dependencyrate followed a patternof seculardecline in all countries:essentially ademographic ransitionassociatedwitha shift to lowerfertilityrates andthe eventual long-run dynamicequilibriumof the age structure. Giventhe dependency rate gap, Argentina ags behind the other New Worldeconomies in the demographic ransitionby a decade or two.

The foregoing is, in effect, a characterizationof Argentinaas a "latestarter," an economy whose developmentalprocess did not get starteduntil very late in the nineteenth century, relative to others. Conse-quently her heavy migrationscame later, and her demographictransi-tion took longer to engage. This sluggish start, I claim, left Argentinamorevulnerableto the economic shocks associatedwith the GreatWarthan were the other settler economies-the demographicburden de-

19 Hall, "Long PeriodEffects."

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 12/31

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 13/31

918 Taylor

plummeted to the 1.1 to 1.2 percent range. Thus Argentina almostexactly paralleledAustraliaafter 1913in terms of capital accumulation

rates. The early-retardation ypothesis, originallyposed in terms of thegrowth of income per capita, is seen to apply here to the remarkableslowdown in Argentineaccumulationrates after the Great War. Thiscan surely be no coincidence; we'll returnto this issue after clarifyingthe role of foreign capital in the two countries.

High rates of capital accumulationdo not, of course, necessarilyimply foreign capital nflows.Afterall, in a closed economy, savingsandinvestment must necessarily balance; yet current-account urplusesordeficits may bridgethe gap in an open economy. Furthermore, n a small

open economy, with a given world interest rate and internationallymobile capital, savings and investment decisions may be completelydelinked. MartinFeldsteinandCharlesHoriokaquestionedthe validityof such assumptionsof capitalmobility,based on their observationthatinvestmentratesand savings rateswere highlycorrelated n a post-1960developed-country sample. On the other hand, Larry Neal, RobertZevin, and otherauthorsstudyingthe operationof capitalmarketsoverthe longer run have emphasized that in the past internationalcapital

marketsmay have been much better integratedthannow, and that thegold-standard years of 1890 to 1914 offer a unique insight into aninternationalcapitalmarketcharacterizedby high mobilityand integra-tion.25

In this context we may view capital flows as a response to theimbalance of domestic savings supply and investment demand. Itfollows that, whereas we know the outflows from Britain were asignificantshare of total Britishsavings, the capitalinflowsmaydiffer nimportance n the variousreceiving regions, dependingon theircontri-

butionto total investment.In fact, viewed from the perspective of the borrowercountry, the

financialflows received by the settler economies look quite dissimilar.In the 1880s Australian nvestment amounted to 19.9 percent of GNP,almost one-halfof which was fundedby capital nflows. In the 1890stheinvestment rate fell to 13.8 percent of GNP, less than a third of whichcame from abroad. Between 1900and 1910 investment accounted for14.2 percent of GNP, and net foreign investment actually turnednegative: - 1.0 percent of GNP.26 Australia gradually reduced itsdependence on foreign savings in the decades before the Great War,savings and investmentrequirementshavingfallen closely into line bythe startof this century. Significantly, he same characterization annotbe applied to Argentina, where foreign control of the capital stockexpanded mmediatelybefore 1913.In 1900 oreignersowned 32percent

25 Feldstein and Horioka, "Domestic Saving";Neal, "Integration";and Zevin, "Are WorldFinancialMarketsMoreOpen?"

26 Edelstein, Overseas Investment, p. 251.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 14/31

Argentine Economic Decline 919

TABLE 3FACTORACCUMULATIONAND CONVERGENCE:

ARGENTINAAND AUSTRALIA, 1890-1939

A. Argentinaand Australia

InitialLevels

Capital Capital GrowthRates(Stock Population Intensity Capital Capital(K) (N) (KIN) Stock Population Intensity

Argentina1890-1913 478 3.377 142 4.8 3.5 1.41913-1929 1,450 7.482 194 2.2 2.8 -0.61929-1939 2,059 11.745 175 1.1 1.8 -0.7

Australia1890-1913 1,099 3.107 354 1.9 1.9 0.01913-1929 1,713 4.821 355 2.3 1.8 0.51929-1939 2,470 6.396 386 1.2 0.9 0.3

B. ArgentinaRelativeto Australia

GrowthRateGap (%)InitialRelative Level (ArgentinaminusAustralia)

(Australia= 100) Capital Capital

Capital Capital Stock Population IntensityStock Population Intensity Growth Growth Growth(K) (N) (KIN) Rate Rate Rate

1890-1913 43 109 40 2.9 1.6 1.41913-1929 85 155 55 -0.1 1.0 -1.11929-1939 83 183 45 -0.1 0.9 - 1.0

Notes: In panel B the levels are derivedfrompanel A by dividingthe Argentine evel by theAustralianevel andmultiplying y 100; he growthrates are derivedby subtractinghe Australianrate from the Argentinerate. K is ? millionsat 1910prices;N is millionsof persons.Source:Table2.

of the capital stock of Argentina, rising to 48 percent by 1913. Incontrast, the estimated share of foreign-owned capital in Australia in1913was 20 percent, considerably ower thaneven the Argentine1900figure (Table 2, panel B).

How can we relate these patternsof capital accumulation-and thefluctuating mportanceof foreigninvestment-to the observedpatternsof economic growth summarized in Table 1? The implications ofstandardneoclassical growth theory requirethat we analyze long-runperformance in terms of capital deepening. In that framework, anincreased level of capital per worker augments labor productivity,raising ncomeper capita.To permita comparisonof capitaldeepening,Table3, panelA recapitulates he patternsof laborandcapitalaccumu-lation seen in Table 2 and computes commensuratecapital intensitiesfor AustraliaandArgentinaover the entireperiod.The derivedpanel Bexpresses Argentine performancerelative to Australia's:first in terms

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 15/31

920 Taylor

of an index numberfor levels (Australiaequal to 100) and second interms of growth-rategaps.

The results in panel A offer a striking confirmation of the early-retardationhypothesisandshedlighton the mixedfortunes of the settlereconomies. Given fast rates of capital accumulationprior to the war,Argentina was able to augment her capital intensity at a rate of 1.4percent per annum between 1900 and 1913: a far better record than inAustralia, where practically no capital deepening was achieved. Incontrast, interwar Argentine performance reveals capital widening.Inhibited by reduced rates of capital accumulation and continuedpopulationgrowth, Argentina made no gains in terms of capital deep-

ening, andits capitalintensity actually ell at a rate of 0.6 to 0.7 percentper annumfrom 1913to 1939.In this latterperiodAustraliacommencedmodest capitaldeepening at the rate of 0.3 to 0.5 percent per annum.

Incomparative erms, panel B tells the story with even greaterclarity.Prior to 1913the Argentinecapitalintensitywas converging up on theAustralian evel, approachingas close as 55 percentin 1913.Thereafter,relative capital widening caused the Argentine capital intensity todiverge from the Australianlevel, revertingto a relative level of 41

percentin 1939.Thislast figure-comparable to the 1890position, whenArgentinahad a capitalintensity level of 40 percent-suggests that overthe intervening50 years Argentinawas unable to achieve any lastingconvergence in capital intensity levels relative to Australia. What ismore, we know fromTable 1thatAustraliacouldnot keep pace withtheOECD average for income per capita growth over the 1900 to 1929period. It is hardlysurprising hat after 1913,when Argentinacould nolonger maintainconvergence in capital intensity relative to a stragglerlike Australia,retardationrelativeto the OECD ensued.

EXTERNALDEPENDENCE AND DEMOGRAPHICBURDENS:

A VULNERABLE GROWTHSTRATEGY

The assertion that Argentineretardationcommenced with the GreatWar is supportedby quantitativeevidence from a numberof differentsources. Intermsof per capitaincome, it was at this time thatArgentinastartedto lag behind the developed countries in growth performance.Even more telling, Argentina failed to advance capital deepeningrelative to Australia,itself a disaster case in terms of interwarretarda-tion and slow growth.

I will argue that the retardationcan best be understoodin terms ofArgentina's historically determinedposition on the eve of the GreatWar, in terms of both populationstructureand foreign capital depen-dence. Faster population growth, with more fecund and numerousimmigrants, endedto burdenArgentinademographically,not simplyinterms of capital widening but in terms of a high dependency rate.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 16/31

Argentine Economic Decline 921

Populous young cohorts threaten growth to the extent that theirconsumption needs diminish savings, with a carryover effect in invest-

ment and accumulation. Admittedly, savings shortfall did not provebothersome to Argentinabefore 1913. Under the stability of the goldstandardample flows of foreign investment could be attracted anddomestic investment sustained.A high-immigrationnd high-overseas-borrowingstrategycould work in a liberal world ordercharacterizedbyfree migrationand internationallymobile capital.

Unfortunately,such a growth strategy was destinedto grindto a halt,given its vulnerability o the economic shocks precipitatedby the GreatWar. Whereas a temporary squeeze in commodity marketshad to beendured, the severe squeeze in factor markets was permanent. Al-though labor migrationrecovered somewhat, the Great War wroughtwholesale changes in the operation of internationalcapital markets. Inaddition to the general retreat of all countries into a more autarkicstance, the keeper of the gold standardwas unableto preserve its roleintact.Wardebts hadbankruptedBritain,who, bailed out by the UnitedStates, emerged from the war unable to continue playing the role ofbanker to the world.

The sudden scarcity of funds had profoundimplicationsfor thosenations heavily dependent on British finance, although the impactvaried fromcountryto country. Foreign ownership of Argentinecapitalmeasured n real termsreached its peak in 1913; n contrast,Australiancapital inflows continued to mount throughthe interwarperiod. Notealso the retreat of foreign capitalfrom Argentina:foreign owners held47.7 percent of the Argentine capital stock of 1913, but the foreignownershipsharedeclinedthroughout he interwarperiodto a mere 20.4

percentin

1940. During this phase, net real additionsto the Argentinecapital stock were fundedentirely by domestic accumulation.The general paucity of overseas fundingfor Argentine investments

duringthe interwarperiodis reflected in the accounts of contemporaryobservers. HaroldPeters recorded that Argentinahad limited successtryingto raisefundsfrom the New Yorkmoney market, notingthat "inthe interimthe Americanmoney markethad been the only source fromwhich extensive capital requirements could be drawn. The UnitedStates became, in a very literal sense, the world's banker." Vernon

Phelps noted that the rapidflow of funds was broughtto an abrupthaltby the outbreak of war, and that thereafter little capital entered until1923;subsequently,the bulk of new investment came from the UnitedStates and practicallynone from Europe. Almost all of the new publicdebt was financed in the New York money market, but prior to 1923advancescouldonly be obtainedover the short term and at highinterestrates.27

27 Peters, Foreign Debt, pp. 101, 123; and Phelps, International Economic Position, chap. 5.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 17/31

922 Taylor

TABLE 4SAVINGS RATES AND DEPENDENCY RATES: THE SETTLER ECONOMIES, 1900-1929

A. Savings Rates (%)

Argentine

Argentina Australia Canada "Savings Rate Gap"

1900-1913 4.52 15.61 15.90 -11.23

1914-1929 5.00 13.41 16.55 -9.99

B. Dependency Rates (%)

Argentine

Argentina Australia Canada "Dependency Rate Gap"

1900-1913 38.92 33.24 33.68 5.46

1914-1929 36.09 30.92 33.53 3.87

Notes: The "Savings Rate Gap" is defined as the Argentine savings rate minus the average of the

Australian and Canadian savings rates. Likewise, the "Dependency Rate Gap" is defined as the

Argentine dependency rate minus the average of the Australian and Canadian dependency rates.

Sources: See the Appendix.

The Argentine economy at the time of the Great War was hard

pressed to perpetuate development in keeping with prewar expecta-tions. A temporarybreakdown in export markets before the recoveryand boom of the twenties constituted a minor hurdle. The dramaticrestructuring n international inancialmarkets proved to be a perma-nent shock that Argentinawas ill equippedto handle. Argentinawashighly dependent on externalfinance:foreign investment accounted forabout half of the Argentine capital stockjust prior to the war, but lessthan a quarter n Australia.

The need for overseas borrowing ollowed directlyfromArgentina'srelativelylow domestic savings capacity. As Table4 shows, Argentinasaved less than 5 percentof national ncome before 1929; n comparison,Australia and Canada saved around 15 percent. Such a low savingcapacity inevitably spelled disaster for capital accumulationonce thestricturesof the interwarcapitalmarketbecameapparent.Unsuccessfulattemptsto raise funds in New York for several years and the inabilityto attract new foreign additionsto the capital stock caused Argentineaccumulationto limp along, relyingon low rates of domestic accumu-

lation to drive new investment.What accounted for low Argentinesaving capacity? Can the demo-graphicburdenexplain the phenomenon?Panel B of Table 4 makes a

These observations end credence to the notion that Argentinawas credit constrainedduring heearly interwarperiod, an identificationproblem that must be addressed to determinewhetherretardationn capital ormationwasdrivenby investmentdemandorsavingssupply. I argue or thelatter,because interest rates rose and quantityconstraintsacted to impede Argentineaccess toforeign oans. Peters,for example, notes that it was not until 1924 hatArgentina ecuredits firstoverseasloan since the war.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 18/31

Argentine Economic Decline 923

heuristic ink between the "savingsrategap" and the "dependency rategap" in the settler economies. Argentinahad a dependency rate about

four orfive percentagepoints higherthanthe Australia-Canada verage,and a savings rate aboutten or eleven points lower. In what follows, byestimating savings functions for the settler economies, I explore howmuchof the difference n savingsratescan be attributed o demographiceffects via the dependencyrate. A naturalcounterfactualexercise is topostulate Argentine performanceunder an alternative (AustralianorCanadian)age structurewith a lower dependency rate. I assume thatArgentine investmentis constrainedat the marginby domestic savingscapacity-a rough approximation o the 1920s in Argentina, given the

abysmal conditions for overseas borrowing. I then calculate counter-factual Argentine savings, investment, and accumulationrates for theinterwar period and project counterfactual economic growth. Thedependencyrateimpacton savingsis found to be largeandsignificant nsettlereconomies, and the demographicburdenborneby Argentinacanexplain a large part of the interwar retardationunder conditions ofinternationalcapital immobility. Despite the restrictive counterfactualassumption,I arguethat this analysis offers a powerful explanationof

the closing of the Belle Epoque.

THE DEMOGRAPHICBURDEN, SAVINGS, AND FINANCIAL

DELINKING: ARGENTINAUNHINGED

I now turn to examine in detail the link between savings and thedemographicburden. An excellent survey of the empiricaland theoret-ical aspects of this issue has been presentedby JeffreyHammer.28Thetheory has its roots in the life-cycle savings hypothesis developed by

Franco Modiglianiand others. Accordingto this approach, populationgrowth will raise consumption (and depress savings) whenever theaverage age of earning exceeds the average age of consuming-arelationshipcertainto hold when the young greatlyoutnumber he old,and furtherreinforcedby the typical life-cycle distributionof income,which tends to peakin middle age. As Hammersummarized:"A rapidlygrowing populationhas a largenumberof youngpeople. Young peopletend to consume more thanthey produce. If there is no countervailingincrease in the income of adults, the effect will be to reduce aggregate

savings."29Unfortunately,these otherwise plausiblepredictionsare very sensi-

tive to the precise theoreticalformulationof the model, and alternativeassumptionscan generate a variety of predictions. Savings decisionschange characterentirely dependingon whether the unit of analysis isthe household or the individual. At the individual level, children

28 Hammer,"PopulationGrowthand Savings."29 Ibid., p. 581.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 19/31

924 Taylor

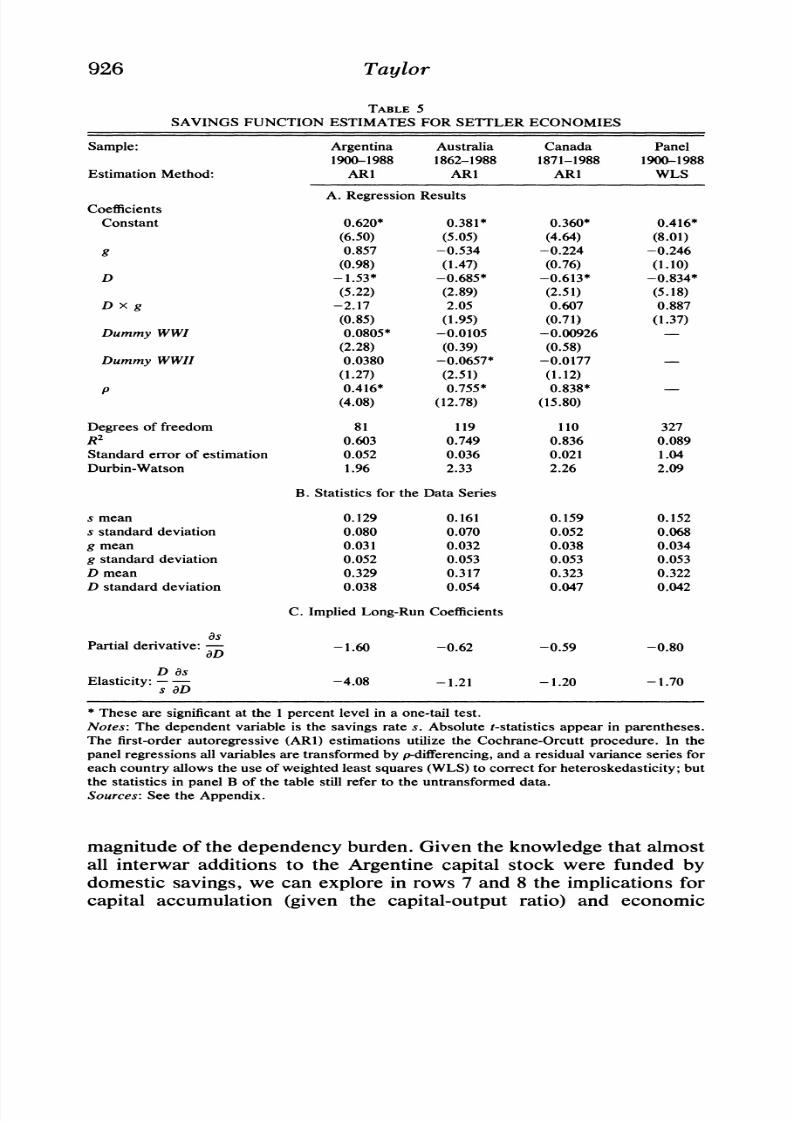

obviously consume more than they produce. In a crude household-based model, life begins at 20, if you will, and the youngergeneration

(excluding children) now unambiguouslyproduces more than it con-sumes. Another possibly inappropriateassumption is that of a fixeddistributionof income across age groups.In thatcase the rate of growthof national income would also be a determinantof savings rates, asAndrew Mason observed.30

Notwithstandingthe theoreticalcomplexities, demographicanalysisof savings has been a controversial element of the empiricaldevelop-ment literaturesince Nathaniel Lefts seminalworkin the late sixties.3'Leff analyzed savings rates in a large cross-section sample includingboth developed and less developed countries; he found that highdependency rates had a significantnegative impact on savings rates.The study generatedmuch criticism because of its sample choice andomittedvariables,andsubsequentwork has revealeda greatdisparity nthe magnitude and significanceof the effect. As Hammerpointed out,many variables in the developmentprocess are highly correlated, and,consequently, cross-countrystudieswill generallysufferfrom collinear-ity problems and a lack of robustness with respect to alternative

specifications. A better approachwould be to use individualcountrytime series data, which "would control for the country-specificvari-ables which determine savings. However, since age distributionschange slowly and populationcensuses are conducted relatively infre-quently, data restrictionsfor such studies are severe."32

Althoughdata restrictionsprecludea time series approachfor manyof today's less developed countries, we are not similarly hamperedwhen dealingwith the settlereconomies, whose documentedmacroeco-nomicexperience stretches back to the turnof the centuryandbeyond.

National saving may easily be calculated using a residual approach,exploiting the current-accountidentity; savings rates may then bederived using an estimate of national income. Time series for realnational income provide estimates of growth rates, and frequent popu-lation censuses allow calculationof the dependency rates, using inter-polation as necessary. In this way, I built up a complete time seriesdatabase for the settler economies, comprisingnational savings rates(s), dependencyrates (D), and growthrates (g).33

Given the eclectic nature of the empiricalandtheoreticalliterature,Ichose a hybrid model to incorporate both the direct effects of the

30 Ibid. See also Samuelson,"An Exact ConsumptionLoan Model"; and Mason, "NationalSavings Rates and PopulationGrowth."

31 Leff, "DependencyRatesand Savings Rates."32 Hammer,"PopulationGrowthand Savings," p. 583.3 The recordsbegin in 1900 or Argentina ECLA,El desarrollo econ6mico de la Argentina), in

1862for Australia N. Butlin,AustralianDomesticProduct), and in 1871for Canada Urquhart,"CanadianEconomicGrowth").However,theearlyECLAestimates orArgentina re of dubiousquality, especially before 1935.See the Appendix.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 20/31

Argentine Economic Decline 925

dependencyrate on savings, in the manner of Leff and his critics, andthe indirect effects operating via the growth rate, following Mason.

AccordinglyI estimated the following savings equationfor Argentina,Australia, and Canada over the entire time series for each country,includingdummyvariables to account for wartime effects.34

St = 830+ 81 gt + (32D, + 133D, gt + f4 (DummyWWI)t

+ /35(DummyWWII)t Et

The results are presentedin Table 5 for various samplechoices. The

first three columns show the basic results on individualcountry timeseries. In the last column, twentieth-centurypanel data are used for athree-country sample. The results do not support the growth rateinteraction heories, as neitherg norD x g has a significantcoefficient.The key findingis that the direct dependency rate impact on savingsrates is large and highly significantin all cases, with an estimatedcoefficient of between -0.59 and -1.60 on the dependency rate,correspondingto the partialderivative ds/dD. Using sample averagesrendersan estimate of the elasticity of the savings rate with respect tothe dependency rate, (Dls)(dslcD), that ranges between -1.20 and-4.08. These figuresare muchlarger,on the whole, than the estimatesfrom contemporarycross-section studies shown in Table 6.

The question remains to what extent the demographicburden de-pressed Argentine savings. The estimated coefficient suggests that aone-percentage-pointallin the dependencyratewould raise the savingsrateby 1.60 percentagepoints. A little mental arithmeticbased on Table4 should convince the reader that the Argentinedependency rate gap

relative to Australiaand Canada accounts for about two-thirdsof theobserved savings rate gap.An assessment of the impact of the dependency rate effect on

Argentineinterwarperformance s offeredin Table7. Row 5 comparesactual Argentinedependency rates with an interwarcounterfactual nwhich Argentinahas the average of Australianand Canadian depen-dency rates. Row 6 reveals that such a counterfactualwould imply atleast a doubling of Argentine saving, a dramatic illustration of the

3 This approachwas inspiredby the pioneeringwork of IanMcLean, who similarlyestimatedsavings functionsfor Australiaand Canada McLean, "Savings n Settler Economies"). He usedthe proportionof the populationaged 45 to 64 years as an explanatoryvariable, n an alternativeinterpretation f the life-cycle hypothesis. My model differs n using the dependency rate as anexplanatoryvariableand admitting nteractionswiththe growthrate. Thus, the coefficientsmay becomparedwiththose in the recent development iterature,n which the dependencyrate is almostalways used. Finally, I prefer to use the autoregressiveARI specification:althougha lagged-dependent-variableLDV) model could not be rejectedusingstandardests, I foundthat the ARIspecification dealt more convincinglywith serial correlation problems, particularlywith theAustraliandata. Nonetheless, the conclusions of this article are equally valid if the LDVspecification s adopted.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 21/31

926 Taylor

TABLE 5

SAVINGS FUNCTIONESTIMATESFOR SETTLERECONOMIES

Sample: Argentina Australia Canada Panel1900-1988 1862-1988 1871-1988 1900-1988EstimationMethod: ARI ARI ARI WLS

A. RegressionResultsCoefficients

Constant 0.620* 0.381* 0.360* 0.416*(6.50) (5.05) (4.64) (8.01)

g 0.857 -0.534 -0.224 -0.246(0.98) (1.47) (0.76) (1.10)

D -1.53* -0.685* -0.613* -0.834*

(5.22) (2.89) (2.51) (5.18)

D x g -2.17 2.05 0.607 0.887(0.85) (1.95) (0.71) (1.37)

Dummy WWI 0.0805* -0.0105 -0.00926

(2.28) (0.39) (0.58)Dummy WWII 0.0380 -0.0657* -0.0177

(1.27) (2.51) (1.12)p 0.416* 0.755* 0.838*

(4.08) (12.78) (15.80)

Degrees of freedom 81 119 110 327R2 0.603 0.749 0.836 0.089

Standard rrorof estimation 0.052 0.036 0.021 1.04Durbin-Watson 1.96 2.33 2.26 2.09

B. Statisticsfor the DataSeries

smean 0.129 0.161 0.159 0.152s standarddeviation 0.080 0.070 0.052 0.068g mean 0.031 0.032 0.038 0.034g standarddeviation 0.052 0.053 0.053 0.053D mean 0.329 0.317 0.323 0.322D standarddeviation 0.038 0.054 0.047 0.042

C. ImpliedLong-RunCoefficients

asPartialderivative: -1.60 -0.62 -0.59 -0.80

aD

D asElasticity:- -4.08 -1.21 -1.20 -1.70

s aD

* These are significantat the 1 percent evel in a one-tailtest.Notes: The dependentvariable s the savingsrate s. Absolute t-statisticsappear n parentheses.The first-orderautoregressive ARI) estimationsutilize the Cochrane-Orcutt rocedure.In thepanel regressionsallvariablesare transformed y p-differencing,nda residualvarianceseriesfor

eachcountryallows the use of weighted eastsquares WLS)to correctforheteroskedasticity; utthe statistics in panel B of the table still refer to the untransformed ata.Sources:See the Appendix.

magnitudeof the dependencyburden.Given the knowledgethat almostall interwar additions to the Argentine capital stock were funded bydomestic savings, we can explore in rows 7 and 8 the implicationsforcapital accumulation (given the capital-outputratio) and economic

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 22/31

Argentine Economic Decline 927

TABLE 6ELASTICITIESOF SAVINGS RATESWITH RESPECTTO DEPENDENCY RATES:

EVIDENCE FROMCROSS-SECTIONAL TUDIES

Study Sample Elasticity

Leff (1969) 74 countries - 1.35*

47 less developed countries - 1.23*Gupta 1971) Poor countries -0.77

Middlecountries -0.62Richcountries -2.70*Totalsample -1.84*

Adams(1971) 47 less developed countries -0.46Leff (1971) 74 countries -0.97*

67 countries -0.99*

Gupta(1975) 40 less developed countries -0.63*Ram(1982) 110countries -0.004

66 less developedcountries 1.3231 developedcountries -1.0870 less developedcountries 0.08

* This indicatesa significanceof the coefficientat the 10percent evel.Notes: The dependency rate used is the proportionof the populationunder 15 yearsof age. Theproportion f the populationover 65 was used in all studies as an additional xplanatoryvariable,exceptinAdams'sand Gupta's 1975).The latteruseda simultaneous quationsmethod,withbothsaving and dependencyrates endogenous.Source:Hammer, "PopulationGrowthand Savings," p. 584.

TABLE 7COUNTERFACTUALARGENTINEINTERWARECONOMICPERFORMANCE

Values

Parameters(1) as /OD -1.60(2) Capital-outputatio 3.38

(3) Capital'sshare in output(%) 60(4) Dependencyrategap (%) 3.87

Actual(%o) Counterfactual%) Actual(%)1913-1929 1913-1929 1900-1913

(5) Dependencyrate 36.1 32.2 38.9(6) Savingsrate 5.00 11.19 4.52(7) Capitalstock growthrate 2.2 4.0 7.7(8) GDPper capita growthrate 0.88 1.98 2.47(9) Argentineretardation 1.59 0.49

(10) OECD retardation 0.25 0.25

Notes: Row 1is the coefficient stimated n Table5, column 1. Row 2 is based on data or 1913 romIEERAL, "Estadfsticas," pp. 114, 120. Row 3 is based on one minus labor's share in outputderived rom Randall p. 30)andis, if anything,a slightunderestimateRandall's iguresare below30 percentfor labor's share for most of the period 1913-1929).Row 4 is from Table 4. Row 5 isderived from Table4 androw 4. Row 6 is derivedfromrows 5 and 1. Row 7 is derivedfromtheAppendixandrows 6 and 3. Row 8 is derived romrows7 and3. Rows 9 and 10 arederivedfromrow 8 and Table 1. Retardation f GDPpercapitagrowthrate, shownin rows 9 and 10, is relativeto Argentina rom 1900to 1913. See the text.Sources:Tables 1, 6, and 7: IEERAL,"Estadfsticas";andRandall,An EconomicHistory. Alsosee the Appendix.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 23/31

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 24/31

Argentine Economic Decline 929

because of the scarcityof domesticcapital,which resultedin large partfromdemographicconstraintson domestic savings. A highdependency

rate, driven by a fast-growingpopulationand substantialimmigration,gave rise to an age structurewith a largeshare of young dis-savers. Theshortfall n availableinvestableresources had to be madeup by capitalinflows-what Jeffrey Williamsonand I viewed as an intergenerationaltransfer from maturesavers in the Old World.35

When internationalcapitalflows were cut off, following the collapseof the internationalcapital market and Britain's retreat into debtorstatus, the balance-of-paymentsgapcould be bridgedno longer,and thedemographicburden forestalled

Argentine accumulationthrough theinterwarperiod. Counterfactualanalysisdemonstratesthat undermoreforgivingcircumstances-a lower dependencyratecomparable o thoseof the other settler economies-Argentine interwarperformancewouldhave been close to the average for the rest of the world economy.36

In the developmentliterature,much ink has been spilledin discussingthe obstacle that externaldependence presents to a developingcountry,and the need for self-sufficiencyand delinkingfrom the core group ofindustrialnations; such argumentsusually fall under the controversial

rubricof dependency theory.37Diaz-Alejandrooffered a scathing cri-tique of such inward-lookingapproachesto developmentin his influen-tial article "DelinkingNorth and South:Unshackledor Unhinged?"Inthe context of Argentineeconomic decline, I have soughtto show thatanotherkind of dependency burden, of the demographicvariety, canrenderexternal dependence in capital marketsa vital underpinning othe developmentprocess. Britishcapitalpaidfora Belle Epoquethat theyoung Argentinepopulationcould not underwritealone: delinked from

this external market Argentina became not unshackled but, indeed,unhinged.

3 TaylorandWilliamson,"CapitalFlows."36 By the 1940s,the Argentinedependencyrate burdenhadalmostdisappeared; nfortunately,

a new autarkicregimehad by thenmade the cost of importedcapital goods very expensive, andaccumulationwas suppressedon that account-but that's anotherstory. See Diaz-Alejandro,Essays; andDe Long, "ProductGrowthandMachinery nvestment."

37 For a survey see Palma, "Dependency." On Latin America, see Kay, Latin AmericanTheories.

Appendix: Data Sources

POPULATION

Argentina

Vaizquez-Presedo,Estadisticas, part 1, pp. 15-16, andpart 2, p. 19.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 25/31

930 Taylor

Australia

Maddison,Phases, appendixB.

CAPITAL STOCK

Argentina

Two series were constructed o provideestimates of the realcapital stock in constantprices. First, a series was based on estimates of real stocks. Post-1913data were takenfrom IEERAL, "Estadisticas," pp. 120-21; 1900to 1913data were takenfrom ECLA,El desarrollo,vol. 5, p. 91;the two series were splicedtogetherat 1913.A second serieswas based on estimates of real investmentderivedfromECLA,El desarrollo,vol. 5, p.

81, and from Di Tella and Zymelman,Los ciclos, pp. 47-86. This second series wascomputed romgrossdomestic fixedcapital ormationdata nconstant1950pesos, usinga depreciationrateof 6 percentandassumingan arbitrarybase stock of 20,000million1950pesos in 1884.Thedepreciationandbase stockparameterswere chosen so thatthesecond series closely matchedthe firstfor trend andcyclical behaviorover the periodof overlap.

The depreciationrate used in the second series is probably an overestimate, beingmuch higher than the rates of depreciationreportedfor Australia.This would tend tounderestimate the growth of the capital stock prior to 1913, thus generating anacceptablebias toward an underestimateof Argentineretardation.To obtain a bench-

markfigurein pounds sterlingthe following procedurewas adopted,using data fromDiaz-Alejandro,Essays, p. 30. According to Diaz-Alejandro, foreigners owned 41percent of the Argentinecapital stock in 1909,an amountequalto US$2,176millionatcurrentprices. Converting o poundssterlingat the parrate of ?1 equal to US$4.8666produces an estimateof ?1,091 millionfor the total capital stock of Argentina n 1909.This is assumed to be the value in 1910pounds sterling, too.

The finalcapitalstock series used is a spliced version of the above two series, usingthe second before 1909 and the first thereafter, normalized to the Diaz-Alejandrobenchmarkn 1909.

Australia

Datasources for 1900to 1939werebasedon the nominal evel of the capital stock inthe sectors thatfollow. Price indices forcapital ormationwere used to deflatethe seriesto 1910/11prices, andhence to obtainvalues in ?1910/11.I assumed?1 to be equaltoA$2. Yearsarefinancialyears,beginningon July 1. All data were taken from M. Butlin,"PreliminaryDatabase,"tables 4.2, 4.8, 4.10, and 4.13.

Sector Deflator Used

Private, plant & equipment Private, nondwelling

Private, nonresidential structures Private, nondwelling

Public, plant & equipment Public, nondwelling

Public, railways Public, nondwelling

Public and private, all dwellings Private, dwelling

For 1880 o 1900,the base stock in 1900was projectedbackward,usingdataon grossdomesticcapitalformationanddepreciationallowances taken from N. Butlin,Austra-lian Domestic Product, pp. 6, 32.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 26/31

Argentine Economic Decline 931

SAVINGS RATES

Nationalsavingwas calculatedresiduallyas investmentplusthe currentaccount in all

cases. The currentaccount equals exports minusimportsplus the service account. Insome cases the service accountwas included n the export or import igures.The savingsrate is defined as national savingdividedby national ncome.

Argentina

For 1900 o 1913,investment n nominal erms was derivedfromrealinvestment andthe price level; from ECLA, El desarrollo, vol. 5, p. 81; and from Della Paolera,"Argentine Economy," p. 186, col. 4. Exports and imports in nominal terms werederived from Della Paolera, "ArgentineEconomy," p. 186, cols. 8 and 10. National

incomein nominal terms was derived from real incomeand the price level; see ibid.,cols. 4 and6. All these were normalized o the IEERAL1913nominalbenchmarks ivenbelow.

For 1913to 1984, investment (includingchange in stocks), exports, imports, andnational ncome (GDP at marketprices) in nominalterms were taken from IEERAL,"Estadisticas;"pp. 136-37.

For 1985 o 1988, investment, exports, imports,and national ncome(GDPat marketprices)in nominalterms were taken fromthe WorldBank, WorldTables 1989-90, pp.92-93.

Australia

For 1861to 1900, investment, currentaccount, and national ncome (GDP at marketprices)in nominal ermswere taken fromN. Butlin, AustralianDomestic Product, pp.6, 16, 22, and410-11.

For 1901 to 1960, investment (including change in stocks), currentaccount, andnational ncome (GDPat marketprices) in nominaltermswere takenfromM. Butlin,"PreliminaryDatabase,"tables 4.1 and 4.17.

For 1961to 1988, investment,currentaccount,andnational ncome(GDPat marketprices) in nominal terms were taken from the Australian National Accounts and

provided by McLean as a supportingdocumentto "Savingin SettlerEconomies."

Canada

For 1870to 1984,I used the implied savingsratio(calculatedresiduallyas describedabove) and Urquhart,"CanadianEconomicGrowth," pp. 18-21.

For 1985to 1988,I used the Gross Domestic Saving plus Net Factor Income fromAbroad, all divided by GDP at marketprices, from the WorldBank, WorldTables1989-90, p. 161.

GROWTH RATES

The growthrate is defined to be the first differenceof the natural ogarithmof realnational ncome.

Argentina

For 1900to 1913,real outputis from Della Paolera, "ArgentineEconomy," p. 186.For 1913to 1984, GDP at marketprices (constant 1960prices) is from IEERAL,

"Estadisticas," pp. 114-15.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 27/31

932 Taylor

For 1984to 1988, the GDP at factor cost, constant 1980prices, is from the WorldBank, World Tables 1989-90, pp. 92-93.

Australia

For 1861to 1901, GDP at marketprices (constant1910/11prices)is fromN. Butlin,Australian Domestic Product, pp. 460-61.

For 1901to 1974, GDPat marketprices (constant1966/67prices)is from M. Butlin,"PreliminaryDatabase," table 4.3.

For 1974to 1988, GDP at factor cost (constant1980prices)is fromthe WorldBank,World Tables 1989-90, pp. 96-97.

Canada

For 1870 to 1985, GDP at marketprices (constant 1981prices) is from Urquhart,"CanadianEconomicGrowth," pp. 8-11.

For 1985to 1988, GDPat factor cost (constant1980prices) is fromthe World Bank,World Tables 1989-90, p. 161.

DEPENDENCY RATES

Dependency rates are based on linear interpolationbetween sample years. Thedependencyrate is definedas the populationunder15years of age divided by the total

population.

Argentina

For 1869 and 1895, Mitchell, International Historical Statistics, pp. 51, 70.

For 1915, 1920, 1925, 1930, 1935,and 1940, Vdzquez-Presedo,Estadisticas, part 2,pp. 38-39.

For 1947, 1960, and 1970, Mitchell, International Historical Statistics, pp. 51, 70.For 1980, United Nations, Demographic Yearbook 1981, pp. 218-19.For 1988, United Nations, Demographic Yearbook 1989, pp. 178-79.

Australia

For 1861, 1871, 1881, 1891,1901,1911, 1921,1933, 1947, 1954,1961, 1971,and 1981,Caldwell,"Population."

For 1988, United Nations, Demographic Yearbook 1989, pp. 196-97.

Canada

For 1851, 1861,1871, 1881,1891, 1901,1911,1921,1931, 1941,1951,1961,and 1971,Mitchell, International Historical Statistics, pp. 47, 57.

For 1980, United Nations, Demographic Yearbook 1981, pp. 214-15.For 1989, United Nations, Demographic Yearbook 1989, pp. 174-75.

United Kingdom

For 1851, 1861, 1871, 1881, 1891, 1901, 1911, 1921, 1931, 1951, 1961, and 1971,Mitchell, European Historical Statistics, pp. 34, 62 (England and Wales).

For 1980, United Nations, Demographic Yearbook1981, pp. 230-31 (EnglandandWales).

For 1988, United Nations, Demographic Yearbook 1989, pp. 194-95.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 28/31

Argentine Economic Decline 933

United States

For 1850, 1860,1870,1880,1890,1900, 1910,1920,1930, 1940,1950,1960,and 1970,

Mitchell, International Historical Statistics, pp. 50, 66-69 (whites only in 1880).For 1981, United Nations, Demographic Yearbook 1981, pp. 218-19.

For 1989, United Nations, Demographic Yearbook 1989, pp. 178-79.

REFERENCES

Baumol,William, "ProductivityGrowth,Convergenceand Welfare:What the Long-

Run Data Show," AmericanEconomicReview,76 (Dec. 1986),pp. 1072-85.Bunge,AlejandroE., andCarlosGarciaMata,"Argentina," n WalterF. Willcox, ed.,

InternationalMigrations(New York, 1931), vol. 2, pp. 143-60.Butlin, M. W., "A PreliminaryAnnual Database 1900/01to 1973/74" (Research

DiscussionPaper No. 7701,Reserve Bankof Australia,Canberra,1977).Butlin, N. G., Australian Domestic Product, Investment and Foreign Borrowing

1861-1938139Cambridge,1962).Caldwell,J. C., "Population,"nWrayVamplew,ed., Australians:Historical Statistics

(Broadway, New SouthWales, 1987), pp. 23-41.CortdsConde, Roberto,El progresoargentino(BuenosAires, 1979).

Della Paolera,Gerardo,"How the ArgentineEconomyPerformedDuringthe Interna-tional Gold Standard:A Reexamination"(Ph.D. diss., University of Chicago,1988).

De Long, J. Bradford,"ProductivityGrowth,Convergenceand Welfare:Comment,"AmericanEconomicReview, 78 (Dec. 1988), pp. 1138-54.

De Long, J. Bradford,"ProductivityGrowthandMachinery nvestment:A Long-RunLook, 1870-1980,"this JOURNAL, 52 (June1992),pp. 307-24.

Denoon, Donald,SettlerCapitalism:TheDynamicsof DependentDevelopment in theSouthernHemisphere(Oxford, 1983).

Diaz-Alejandro,Carlos F., Essays on the EconomicHistory of theArgentineRepublic

(New Haven, 1970).Diaz-Alejandro,CarlosF., "SomeCharacteristics f RecentExport Expansion n Latin

America,"in HerbertGiersch, ed., TheInternationalDivisionof Labor:Problemsand Perspectives(Tubingen,Germany, 1974),pp. 215-36.

Dfaz-Alejandro,CarlosF., "DelinkingNorthandSouth:UnshackledorUnhinged?," nAlbertFishlow et al., eds., Rich and Poor Nations in the WorldEconomy (NewYork, 1978),pp. 87-160.

Dfaz-Alejandro,Carlos F., "The 1940sin LatinAmerica,"in Moshe Syrquin, LanceTaylor, and Larry E. Westphal, eds., Economic Structure and Performance:Essays in Honor of Hollis B. Chenery Orlando,1984),pp. 341-62.

Dfaz-Alejandro,Carlos F., "Latin America in the 1930s," in RosemaryThorp, ed.,LatinAmericain the 1930s: TheRole of thePeriphery n WorldCrisis(New York,1984), pp. 17-49.

Diaz-Alejandro,Carlos F., "Argentina,AustraliaandBrazilbefore 1929,"in GuidoDiTella and D. C. M. Platt, eds., Argentina, Australia and Canada: Studies inComparativeDevelopment,1870-1965(London, 1985),pp. 95-109.

Diaz-Alejandro,CarlosF., "No Less ThanOneHundredYearsof ArgentineEconomicHistory plus Some Comparisons," n AndrdsVelasco, ed., Trade,Developmentand the WorldEconomy: Selected Essays of Carlos F. Diaz-Alejandro Oxford,1988), pp. 230-60.

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 29/31

934 Taylor

Di Tella, Guido, "EconomicControversies n Argentina rom the 1920sto the 1940s,"in Guido Di Tella and D. C. M. Platt, eds., The Political Economy of Argentina

1880-1946(New York, 1986),pp. 120-32.Di Tella, Guido, and D. C. M. Platt, eds., Argentina, Australia and Canada: Studies in

Comparative Development, 1870-1965 (London, 1985).Di Tella, Guido, and Manuel Zymelman, Las etapas del desarrollo economic argentino

(BuenosAires, 1967).Di Tella, Guido, and Manuel Zymelman, Los ciclos economicos argentinos (Buenos

Aires, 1973).Duncan, Tim, and John Fogarty, Argentina and Australia: On Parallel Paths (Carlton:

MelbourneUniversityPress, 1984).ECLA (United Nations, Economic Commission for Latin America), El desarrollo

econ6mico de laArgentina,

5vols. (Santiago de Chile, 1958).Edelstein, Michael, "Foreign Investment and Empire1860-1914,"in RoderickFloud

and Donald McCloskey, eds., The Economic History of Britain Since 1700

(Cambridge,1981),vol. 2, pp. 70-98.Edelstein, Michael, Overseas Investment in the Age of High Imperialism (New York,

1982).Feldstein, Martin, and CharlesHorioka, "Domestic Savingand InternationalCapital

Flows," EconomicJournal, 90 (June1980),pp. 314-29.Fogarty, John,EzdquielGallo, andHector Didguez,"Argentinay Australia,"Instituto

TorcuatoDi Tella serie verde:jornada no. 201(Buenos Aires, 1977).

Gerardi,Ricardo E., "Australia, Argentina and World Capitalism:A ComparativeAnalysis 1830-1945" (University of Sydney Faculty of Economics OccasionalPaperNo. 8, 1985).

Green,Alan, and M. C. Urquhart,"FactorandCommodityFlows in the InternationalEconomyof 1870-1914:A Multi-CountryView," thisJOURNAL, 36(Mar.1976),pp.217-52.

Hall, A. R., "Some Long Period Effects of the Kinked Age Distributionof thePopulation of Australia1861-1961,"The Economic Record, 39 (Mar. 1963),pp.43-52.

Hammer,JeffreyS., "PopulationGrowth and Savingsin LDCs: A Survey Article,"World Development, 14 (May 1986), pp. 579-91.

IEERAL (Institutode EstudiosEcon6micossobrela RealidadArgentinay Latinoamer-icana), "Estadfsticas de la evoluci6n econ6mica de Argentina1913-1984,"Estu-dios, 9 (July/Sept.1986),pp. 103-84.

Kay, Cristobal, Latin American Theories of Development and Underdevelopment (New

York, 1989).Kelley, Allen C., "InternationalMigrationand Economic Growth:Australia, 1865-

1935," this JOURNAL, 25 (Sept. 1965),pp. 333-54.Kelley, AllenC., "EconomicConsequencesof PopulationChange n the ThirdWorld,"

Journal of Economic Literature, 26 (Dec. 1988), pp. 1685-1728.

Kennedy, William P., Industrial Structure, Capital Markets and the Origins of British

Economic Decline (Cambridge, 1987).

Korol, Juan Carlos, "ArgentineDevelopmentin a ComparativePerspective," LatinAmerican Research Review, 26 (Fall 1991).

Leff, Nathaniel H., "Dependency Rates and Savings Rates," American EconomicReview, 59 (Dec. 1969), pp. 886-96.

Lewis, Paul H., The Crisis of Argentine Capitalism (Chapel Hill, NC, 1990).McLean, Ian W., "Notes on Growth in Resource-RichEconomies" (Photocopy,

HarvardUniversity,Mar. 1990).

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 30/31

Argentine Economic Decline 935

McLean, Ian W., "Saving in Settler Economies: Australian and North AmericanComparisons" Photocopy, Universityof Adelaide, Aug. 1991).

McPhee, E. T., "Australia-Its ImmigrantPopulation,"in Walter F. Willcox, ed.,

InternationalMigrations(New York, 1931), vol. 2, pp. 169-78.Maddison,Angus,Phases of CapitalistDevelopment(New York, 1982).Maddison,Angus, The WorldEconomyin the 20th Century Paris, 1989).Mason, Andrew, "NationalSavingRates andPopulationGrowth:A New Model and

New Evidence," in D. Gale Johnsonand RonaldD. Lee, eds., Population Growthand EconomicDevelopment:Issues and Evidence (Madison, 1987),pp. 523-60.

Mitchell,B. R., EuropeanHistorical Statistics, 1750-1975 2nd edn., New York, 1980).Mitchell, B. R., InternationalHistorical Statistics: The Americas and Australasia

(Detroit, 1983).

Neal, Larry, "Integration f InternationalCapitalMarkets:QuantitativeEvidence fromthe Eighteenth o TwentiethCenturies,"thisJouRNAL,50 (June 1985),pp. 219-26.Offer, Avner, The First WorldWar:An AgrarianInterpretation Oxford,1989).Palma, J. G., "Dependency," in John Eatwell, MurrayMilgate, and Peter Newman,

eds., TheNew Palgrave:EconomicDevelopment(New York, 1989), pp. 91-97.Peters, Harold Edwin, TheForeignDebt of theArgentineRepublic(Baltimore, 1934).Phelps, Vernon Lovell, TheInternationalEconomic Position of Argentina(Philadel-

phia, 1938).Pope, David, "Modelling he Peoplingof Australia:19001930," AustralianEconomic

Papers, 20 (Dec. 1981), pp. 258-82.

Prebisch,Raul, "Five StagesinMy Thinking n Development," nGeraldM. MeierandDudley Seers, eds., Pioneers in Development(New York, 1984), pp. 173-204.

Prebisch, Raul, "Argentine Economic Policies since the 1930s: Recollections," inGuido Di Tella and D. C. M. Platt, eds., The Political Economy of Argentina1880-1946(New York, 1986),pp. 133-53.

Randall, Laura,An Economic History of Argentina in the TwentiethCentury (NewYork, 1978).

Richardson,H. W., "BritishEmigrationand OverseasInvestment,1870-1914,"Eco-nomicHistory Review, 2nd series 25 (Feb. 1972),pp. 99-113.

Samuelson,Paul, "An ExactConsumptionLoanModel of InterestWith or Without he

Social Contrivanceof Money," Journal of Political Economy, 66 (Dec. 1958), pp.467-82.

Schedvin, C. Boris, "Staples and Regions of Pax Britannica,"Economic HistoryReview, 2nd series 20 (Nov. 1990),pp. 533-59.

Scobie, JamesR., Revolutionon the Pampas:A Social History of Argentine Wheat,1860-1910(LatinAmericanMonographsNo. 1, Austin, 1964).

Scobie, JamesR., Argentina:A Cityand a Nation (2nd edn., New York, 1971).Sinclair,W. A., TheProcess of EconomicDevelopment n Australia Melbourne,1976).Taylor,Alan M., "Birds of Passageand the Belle Apoque:DivergentDevelopmenton

the DistantSouthernShores, 1870-1939" Photocopy, May 1991).

Taylor,Alan M., andJeffreyG. Williamson, "CapitalFlows to the New World as anIntergenerational ransfer" Harvard nstitutefor Economic ResearchDiscussionPaperNo. 1579, 1991).

United Nations, DemographicYearbook 981(New York, 1983).UnitedNations, DemographicYearbook 989(New York, 1991).Urquhart,M. C., "CanadianEconomic Growth 1870-1980"(Institutefor Economic

ResearchDiscussion PaperNo. 734, Queen's University, Ontario, 1988).Vdzquez-Presedo,Vicente, Estadisticas hist6ricasargentinas,2 vols. (Buenos Aires,

1971-1976).Williamson, Jeffrey G., "The Evolution of Global Labor Marketsin the First and

8/8/2019 Argentine Economic Decline

http://slidepdf.com/reader/full/argentine-economic-decline 31/31

936 Taylor

Second World Since 1830: BackgroundEvidence and Hypotheses" (HarvardInstitutefor EconomicResearch Discussion Paper No. 1571, 1991).

WorldBank, WorldTables1989-90 (Baltimore,1989-1990).