DEC 08, 2014 ASX-ARU TARGET A$0.35 ARAFURA RESOURCES LTD. //Rare Earths INITIATING COVERAGE Magnet Materials Matter Magnet Materials Matter – Arafura’s Nolans Project can produce an industry leading amount of neodymium and praseodymium, to be used by rare earth magnet makers whose products are destined for the automotive, alternative energy and aerospace industries. Stable Location – Australia is as good and as stable a mining jurisdiction as one could find. Decades of Production – Nolans has a 40+ year mine life, at planned 20,000 tpa equivalent TREO production rate. Economically Viable – Our worst-case REO price deck suggests that Arafura can generate slim but positive cash flows in any rare earth market, and this with current estimated production costs. If programs with Chinese partners bear fruit and operating costs can be driven lower, then Arafura will reap additional rewards. Known Minerals – The minerals in the Nolans deposit are rare-earth bearing phosphates and silicates, which makes their processing a low-risk affair. Societal Acceptance – The region around the proposed mine is mining country. The project should not suffer from protests regarding its operation in the area. Positive Recommendation – Using our recently published base-case REO price deck, we are initiating coverage on Arafura with a AU$0.35 target price. We believe that every rare earths investor should hold Arafura, as it is one of a very few strategic-grade projects outside of China. Jon Hykawy, PhD President [email protected] Tom Chudnovsky Managing Partner [email protected] S T O R M C R O W New Old Rang Posive N/A Target A$0.35 N/A Shares O/S FD ~451.7M Recent Price AUS$0.05 Market Cap AUS$22.5M Net Cash ~AUS$20M See the end of report for important disclosures

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DEC 08, 2014 ASX-ARU

TARGET A$0.35

ARAFURA RESOURCES LTD.

//Rare Earths

INITIATING COVERAGE Magnet Materials Matter

Magnet Materials Matter – Arafura’s Nolans Project can produce an

industry leading amount of neodymium and praseodymium, to be used by

rare earth magnet makers whose products are destined for the automotive,

alternative energy and aerospace industries.

Stable Location – Australia is as good and as stable a mining jurisdiction as

one could find.

Decades of Production – Nolans has a 40+ year mine life, at planned 20,000

tpa equivalent TREO production rate.

Economically Viable – Our worst-case REO price deck suggests that Arafura

can generate slim but positive cash flows in any rare earth market, and this

with current estimated production costs. If programs with Chinese partners

bear fruit and operating costs can be driven lower, then Arafura will reap

additional rewards.

Known Minerals – The minerals in the Nolans deposit are rare-earth bearing

phosphates and silicates, which makes their processing a low-risk affair.

Societal Acceptance – The region around the proposed mine is mining

country. The project should not suffer from protests regarding its operation

in the area.

Positive Recommendation – Using our recently published base-case REO

price deck, we are initiating coverage on Arafura with a AU$0.35 target

price. We believe that every rare earths investor should hold Arafura, as it is

one of a very few strategic-grade projects outside of China.

Jon Hykawy, PhD President

Tom Chudnovsky Managing Partner

S T O R M C R O W

New

Old

Rating Positive N/A

Target A$0.35 N/A

Shares O/S FD ~451.7M

Recent Price AUS$0.05

Market Cap AUS$22.5M

Net Cash ~AUS$20M

See the end of report for important disclosures

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 2

Summary

It would be a considerable understatement to say that rare earths (REEs) are

out of favour with financial investors. What was one of the hottest areas in

the resource investment universe in 2010 and 2011 has become colder than

almost any other segment of the resource market. The two companies at the

forefront of the REE industry outside China, Molycorp (MCP-NYSE) and Lynas

(LYC-ASX), have been unable to generate profits, with market consensus

laying the blame at the feet of ongoing technical problems. As far as financial

investors are concerned, both Molycorp and Lynas are essentially worthless.

Still, there is a continuing strong need for REEs among end-users, and the need

for a reliable and secure supply of REEs is especially important to users outside

China. The mantra for end-users of all materials for which the supply is

controlled by China seems to be geographical diversification. It naturally

follows that it is necessary to finance new projects to meet this need.

There are a number of reasons why REEs remain important in the foreseeable

future, and why unreliable and restrictive supply from China carries too much

risk for end-users. Rare earth-based magnets, especially the neodymium iron

boron (NdFeB) magnet, remain the highest strength magnets available. In

various uses, such as for motors in the automobile industry, within direct-

drive generators in the wind industry, or many electrical applications within

the aerospace sector, NdFeB magnets provide a combination of performance,

size and weight that is unobtainable without sacrificing other criteria using

substitutes. The issue of cost is always a factor, but at current rare earth

prices, and indeed the historical prices of rare earths outside of the bubble

years of 2010 and 2011, REEs have been cost effective for all the above

industries.

Yet at the same time as many industries would benefit from enhanced access

to reasonably priced rare earths, China is consolidating its REE industry using

six state-owned or state-controlled enterprises. While the WTO ruling against

China regarding export quotas on a number of materials, including REEs, was

initially viewed as a victory, even the most benevolent observer would allow

that consolidation such as this creates a less transparent rare earth market.

The US Department of Energy has certainly taken notice, and its First Strategic

Pillar within its Critical Materials Strategy, “Diversifying global supply chains

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 3

to mitigate supply risk”, is nothing but a call to action regarding critical

materials that are controlled by any one nation. It is clear that there is a

definite need for new REE mines in order to guarantee a reliable ex-China

supply.

Nolans – The Magnetic Materials Mine

Arafura Resources (ASX: ARU) of Perth, Australia, is 100% owner of the Nolans

Rare Earths Project in the Northern Territory, Australia. At present, the

Nolans Project is at an advanced feasibility stage. The Nolans Bore rare earths

deposit, with defined resources of more than 1.2 million tonnes of REO

extending from surface to a depth of 220 meters, is one of the largest and

lowest risk REE deposits in the world.

Exhibit 1: Nolans Project location in Northern Territory, Australia

Source: Arafura Resources

Arafura is planning to locate facilities for mining, ore beneficiation and

hydrometallurgical processing on site at Nolans. The refining of

hydrometallurgical concentrates into five saleable products (oxides of

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 4

neodymium/praseodymium, samarium/europium/gadolinium, a mixture of

all the heavier REEs, lanthanum and cerium) will take place offshore.

Exhibit 2: Schematic View of Project Components

Source: Arafura Resources

What makes the Nolans Bore deposit truly interesting is the proportion of

certain critical rare earths within the deposit, most especially the magnet

materials neodymium (Nd) and praseodymium (Pr). Nd and Pr are the REEs

used in the highest-strength permanent magnets, important to the

automotive, wind turbine and aerospace industries. This resource

composition positions Arafura as a prospective world-leading feedstock

provider for the growing rare earth magnet market.

Planned output from Nolans of 20,000 tonnes of TREO each year includes

11,350 tonnes of TREO in hydrometallurgical concentrates earmarked for

offshore separation. At this level, production of mixed Nd/Pr and dysprosium

(Dy), which is vital to the use of NdFeB magnets in high power applications,

stands above all other existing light REE producers. In fact, production from

Nolans would rival the combined Phase 1 production levels from Molycorp

and Lynas. Production from Nolans is scheduled to commence in 2019.

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 5

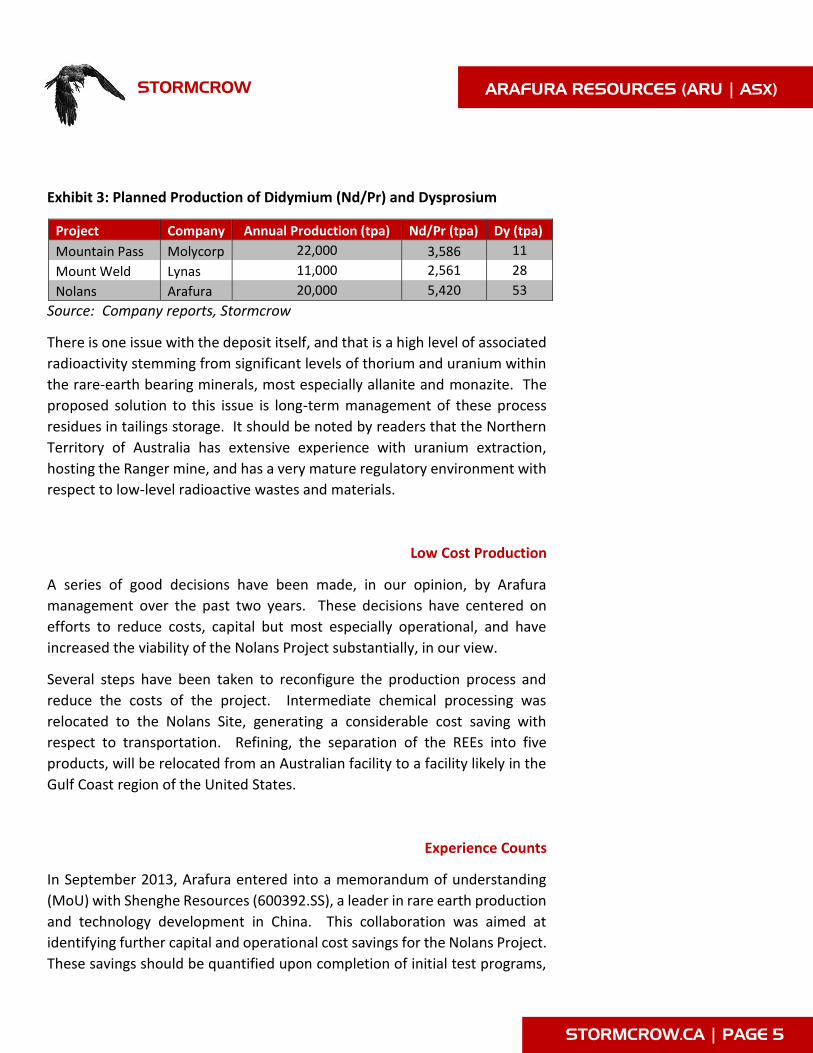

Exhibit 3: Planned Production of Didymium (Nd/Pr) and Dysprosium

Project Company Annual Production (tpa) Nd/Pr (tpa) Dy (tpa)

Mountain Pass Molycorp 22,000 3,586 11

Mount Weld Lynas 11,000 2,561 28

Nolans Arafura 20,000 5,420 53

Source: Company reports, Stormcrow

There is one issue with the deposit itself, and that is a high level of associated

radioactivity stemming from significant levels of thorium and uranium within

the rare-earth bearing minerals, most especially allanite and monazite. The

proposed solution to this issue is long-term management of these process

residues in tailings storage. It should be noted by readers that the Northern

Territory of Australia has extensive experience with uranium extraction,

hosting the Ranger mine, and has a very mature regulatory environment with

respect to low-level radioactive wastes and materials.

Low Cost Production

A series of good decisions have been made, in our opinion, by Arafura

management over the past two years. These decisions have centered on

efforts to reduce costs, capital but most especially operational, and have

increased the viability of the Nolans Project substantially, in our view.

Several steps have been taken to reconfigure the production process and

reduce the costs of the project. Intermediate chemical processing was

relocated to the Nolans Site, generating a considerable cost saving with

respect to transportation. Refining, the separation of the REEs into five

products, will be relocated from an Australian facility to a facility likely in the

Gulf Coast region of the United States.

Experience Counts

In September 2013, Arafura entered into a memorandum of understanding

(MoU) with Shenghe Resources (600392.SS), a leader in rare earth production

and technology development in China. This collaboration was aimed at

identifying further capital and operational cost savings for the Nolans Project.

These savings should be quantified upon completion of initial test programs,

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 6

and will be incorporated, along with results from an ongoing Chinese

optimization program of ore beneficiation and hydrometallurgical processes,

in the Definitive Feasibility Study (DFS) that is scheduled to be completed by

the end of calendar 2015.

Sales and Marketing Uber Alles

It is clear that we are no longer in the REE boom period of 2010 and 2011,

when financial investors supported several viable “cheap and cheerful” rare

earth projects, and, let us be honest, a host of poor projects that never stood

any chance of becoming producers. In the wake of skyrocketing prices

through latter 2010 and early 2011, avoidance of rare earth use became a

priority, demand and then prices collapsed, and financial investors lost all

interest in the space, including the best projects. What this means for

prospective rare earth producers today is that success can only come with the

support of strategic investors or end-users from the established REE markets

in Japan, Europe, South Korea and the United States. And we have also had

conversations with end-users that have indicated that they would even be

happy buying their REEs from a Chinese company, or Chinese-backed

company, providing the production of those REEs remains outside direct

Chinese governmental control.

To this end, Arafura has been taking steps in the right direction. The company

has signed a MoU with ThyssenKrupp (TKA.DE), for supply of up to 3,000

tonnes per year of REE products, and a more formal off-take agreement is

now being negotiated. Arafura has also signed a MoU with a South Korean

multinational organization for the sale of another 3,000 tonnes of REE

products. It is true that a pessimist might note that MoUs for 6,000 tonnes of

product per year does not guarantee the sale of the full 11,350 tonnes per

year of production. However, we would note that pessimists have also

insisted that the rare earth market has vanished, so for a company that will

not even begin ramping commercial production until 2019, we would suggest

that negotiating 6,000 tonnes of sale at this point in time represents a very

strong start.

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 7

Ticking Every Box

As we have noted in the discussion regarding our recently published base-case

REO price deck, the lack of financial investor interest in the space means that

it will be the needs of strategic investors and/or large end-users that will

dictate the projects chosen to become future suppliers. And these strategic

parties have a slightly different emphasis on the criteria that identify the best

projects. Stormcrow believes these criteria will include factors such as the

ability of a prospective mine to supply for a long period of time, geopolitical

stability of the nation hosting the deposit, a low level of remaining technical

and social acceptance risk, high levels of production of the truly critical rare

earths, and economic viability of the project, itself.

Arafura delivers on all counts. With a mine life of more than 40 years, it is

clear that operational life is not an issue. Australia, and more particularly the

Northern Territory, is as stable a mining jurisdiction as one could hope to find.

Nolans Bore contains monazite, and monazite is a well-known REE-bearing

mineral with well understood flow sheets for production. The proposed

operation is in a mining area sufficiently removed from major communities,

and thus does not present an overly large risk regarding project acceptability

among the local population. We have already seen that Nolans would rank

among the best producers of magnet materials for its size. Finally, we can

show that even using our pessimistic REO price deck, one that was built to

answer questions regarding just how bad the rare earth market can possibly

get, Nolans would generate positive cash flow at currently projected costs per

kilogram of TREO produced of AU$15.67. The financial returns are

considerably stronger given our base-case price deck, as we shall see.

Cash Flow Model

We have recently published our argument for a “base-case” price deck for

REOs, through 2025. Please see our report entitled The Rare Earth Market

Keeps Changing, published in November 2014. The results of this pricing

study are shown below:

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 8

Exhibit 4: “Base Case” REO Price Deck

Source: Stormcrow

We use this “base-case” rare earth price deck as one of our assumptions. To

simplify our analysis further, we also make the following assumptions:

1. We do not ascribe any value to any other project, owned in whole or in

part by Arafura, or to any other resources, other than REEs mined from

Nolans Bore.

2. We assume the production of five saleable products from Nolans Bore:

lanthanum oxide, cerium oxide, didymium oxide, samarium-europium-

gadolinium (SEG) mixed oxides and all heavier rare earths as a mixed

oxide (HREOs).

3. We ascribe no value to the final potentially saleable product from the

project, cerium carbonate. The only likely market for this product is in

China, and given that domestic Chinese production of all cerium

chemicals is likely sufficient for some time to come, we will be

conservative and not attribute revenue to this product.

4. We assume that the values of lanthanum and cerium oxides are as given

by our pricing model.

5. We assume the value of didymium oxide is given entirely by the price of

neodymium oxide in our pricing model, as recent prices for

praseodymium oxide are likely skewed higher by purchases made for the

ceramics market for small quantities of pure praseodymium oxide.

Magnet use does not require separated praseodymium oxide.

6. We assume the value of SEG oxide is its value as separated and purified

REOs less 20%.

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 9

7. We assume the value of HREO from Nolans Bore is its value as separated

and purified REOs less 15%.

8. We believe that the above discounts are reasonable for mixed

concentrates in this form. We have analyzed historical pricing of

separated rare earths produced from ionic clays and the price paid for

ionic clay mixed concentrate, all quoted by Asian Metal. These data show

a 28% discount for a mixed concentrate that still contains large amounts

of lanthanum, cerium and didymium oxides. We believe it correct that a

purer concentrate can command a higher price, as there is simply less

refining to do.

9. We assume operating costs of AU$15.67 per kg, as per Arafura’s

September 2014 Nolans Development Report, and assume operating

costs in their entirety are borne by the project starting in 2019.

10. We assume capital costs of AU$1.41 billion, as per Arafura’s September

2014 report. Capital costs are split 60% debt, 40% equity. Debt carries a

10 year term, with interest rates of 6%.

11. The project takes two years to ramp to full production, with production

of 5,000 tonnes of TREO in 2019 and 9,000 tonnes of TREO in 2020.

Annual production of 20,000 tpa equivalent is achieved in 2021.

12. We apply a 8x terminal multiple to the project in 2026, owing to decades

of remaining production. It would be incorrect to assign zero value to the

remaining production levels.

13. Our DCF analysis assumes a discount rate of 19%. We believe that

venture capital discount rates of 20% or higher are excessive, given the

lack of technical and market risk, and we believe our chosen rate properly

reflects the capital risk of the project.

14. We assume, as have Arafura management, an AU$ to US$ exchange curve

sourced from Access Economics, a leading Australian forecaster. The

curve predicts an exchange rate of 0.838 in 2016, when the bulk of capex

is shown to be injected to the project. We assume rates in 2019 and later

are the average of the curve, at 0.855, as we do believe that China and

the global appetite for commodities will improve, and the AU$ will

strengthen compared to the US$. The current exchange rate is roughly

0.84.

So, with these assumptions we obtain the following cash flow model

through 2025:

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 10

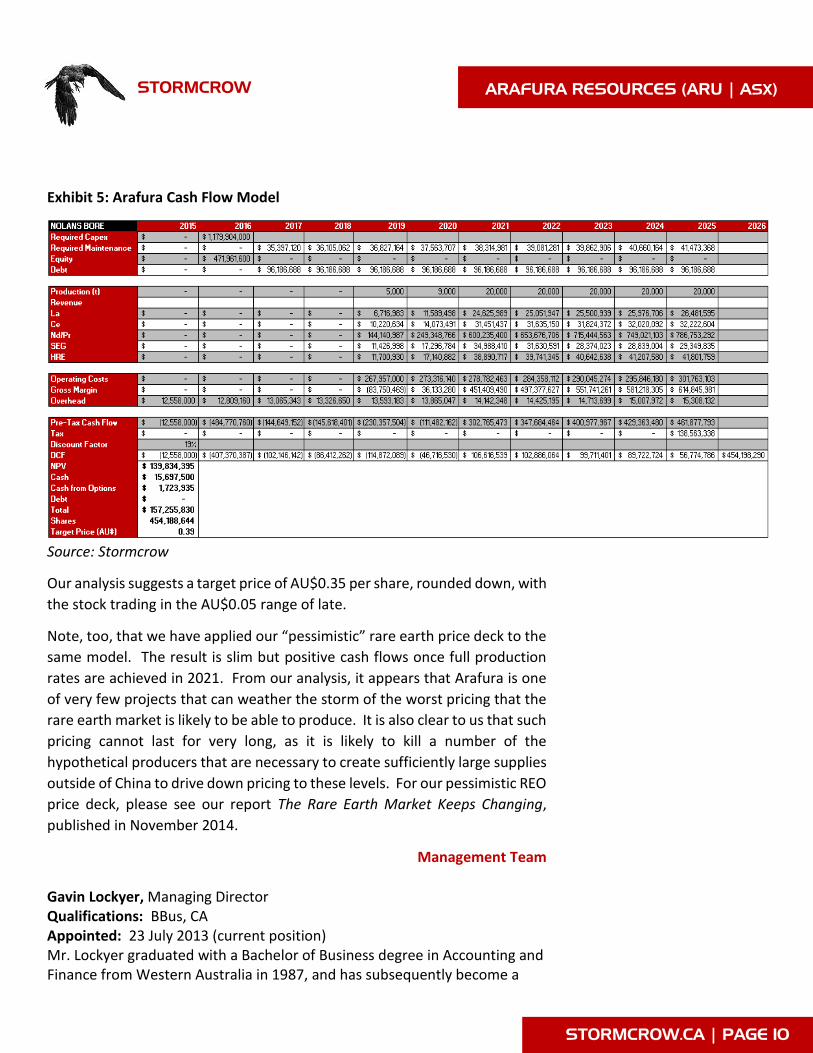

Exhibit 5: Arafura Cash Flow Model

Source: Stormcrow

Our analysis suggests a target price of AU$0.35 per share, rounded down, with

the stock trading in the AU$0.05 range of late.

Note, too, that we have applied our “pessimistic” rare earth price deck to the

same model. The result is slim but positive cash flows once full production

rates are achieved in 2021. From our analysis, it appears that Arafura is one

of very few projects that can weather the storm of the worst pricing that the

rare earth market is likely to be able to produce. It is also clear to us that such

pricing cannot last for very long, as it is likely to kill a number of the

hypothetical producers that are necessary to create sufficiently large supplies

outside of China to drive down pricing to these levels. For our pessimistic REO

price deck, please see our report The Rare Earth Market Keeps Changing,

published in November 2014.

Management Team

Gavin Lockyer, Managing Director Qualifications: BBus, CA Appointed: 23 July 2013 (current position) Mr. Lockyer graduated with a Bachelor of Business degree in Accounting and Finance from Western Australia in 1987, and has subsequently become a

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 11

member of both the Institute of Chartered Accountants and the Finance & Treasury Association of Australia. He joined Arafura in 2006 as CFO and Company Secretary after having served as Financial Controller with the Tethyan Copper Company Limited. Mr. Lockyer previously held a number of senior finance and treasury positions in global mining companies Newcrest and Newmont following an international investment banking career with BankWest and ANZ in Australia, and Bankers Trust and Deutsche Bank in London.

Peter Sherrington, Chief Financial Officer & Company Secretary Qualifications: BBus, CA Appointed: 24 July 2013 (current position) Mr. Sherrington holds a Bachelor of Business in Accounting and Finance, and is a member of the Institute of Chartered Accountants. He commenced employment with Arafura in 2008 as Commercial Manager and was appointed CFO in July 2013. He has in excess of 20 years experience in professional and corporate roles in Perth. Prior to working with Arafura he held senior finance and commercial positions with a number of ASX and unlisted entities. He has also worked in accounting public practice for 10 years in the areas of business services and corporate advisory.

Richard Brescianini, General Manager Exploration & Development Qualifications: BSc (Hons) Appointed: 18 March 2007 Mr. Brescianini is a graduate in Geology and Geophysics, and has extensive private and public sector experience in the minerals industry, in a career that spans over 20 years. From 1987 to 1999, he worked with BHP Minerals on base and precious metals exploration programs throughout Australasia and North America, contributing to significant economic discoveries at Eloise (copper-gold) and Cannington (silver-lead-zinc). Mr. Brescianini led the Northern Territory Government’s Geological Survey as its Director from 2003 to 2007, and was responsible for major geoscience initiatives and investment attraction strategies. Prior to that, he was the Survey’s Chief Geophysicist.

Neil Graham, General Manager Operations & Technology Qualifications: BSc (Hons) Chemical Engineering, C.Eng. Appointed: 1 September 2010 Mr. Graham has more than 25 years of international experience in the chemical industry, encompassing design, construction, and commissioning of both start-up and brownfield installations, in addition to substantial

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 12

operations management experience of facilities in several different countries. He is a chartered engineer who commenced his professional career at BP prior to joining ICI, where he was involved in major project design and implementation roles. He developed the Asian market presence of Rittershaus & Blecher and subsequently completed several technical and site manager roles with Huntsman Pigments before becoming the Group Sulphate Manufacturing Director. More recently, Mr. Graham was responsible for Orica’s largest and most complex facility, worldwide, at Gladstone, Queensland, producing ammonium nitrate, sodium cyanide and chloralkali products. He joined Arafura Resources in September 2010.

Brian Fowler, General Manager NT & Sustainability Appointed: 24 July 2013 (current position) Mr. Fowler has worked for over 40 years in private sector mineral companies, developing a range of commodities, including rare earths, base metals and gold. He has significant experience in a number of disciplines including environmental management, safety management, community engagement, project permitting and approvals, and land access. He has worked at various mining operations and in exploration throughout Australasia. In these roles, Mr. Fowler has been involved in taking projects from discovery, through production, to mine closure, rehabilitation and compliance management. Prior to joining Arafura in 2007, Mr. Fowler worked with Newmont Australia and Normandy Mining in a variety of senior management roles. He is a member of the Northern Territory Mining Board, Management Board of the Northern Territory Minerals Council of Australia, and a member of Work Health & Safety Advisory Council of the Northern Territory.

Conclusions – Magnet Materials Matter

We will reiterate our opening thought. Most financial investors have chosen

to ignore rare earth companies at present. We believe this is a mistake,

because REEs are a critical material with long-term value. Investors that are

interested in the space strategically, those that have to remain interested in

the REE industry, are not likely to let a good opportunity go to waste.

We believe that Arafura remains one of the best opportunities in the rare

earth market. Arafura represents a low-risk, prospectively very long-lived

producer of low-cost critical rare earths. Financially, it can suffer the very

STORMCROW

ARAFURA RESOURCES (ARU | ASX)

STORMCROW.CA | PAGE 13

worst that the rare earth market can throw at it, and generate strong profits

in a base-case market. It remains one of the very few companies in the space

that can make those claims, joining Molycorp, Lynas, Rare Element Resources

(RES-US) and Quest Rare Metals (QRM-TSX). This does not imply that all of

these companies will survive to reach production, but they stand a far better

chance in this market than most of their so-called peers.

We are initiating coverage on Arafura Resources with a positive

recommendation and a target price of AU$0.35. Arafura has every

characteristic of a project that will be supported by strategic investors,

including end-users. The Nolans Bore deposit is located in mining-friendly

Australia, and can produce for many decades. Arafura can produce industry-

leading levels of neodymium and praseodymium, to be turned into magnets

and used in the automotive, alternative energy and aerospace industries. The

project is economically viable, even if REE prices approach worst-case levels.

And the company has few, if any, remaining technical or social acceptability

hurdles. We believe that Arafura is a name that every interested rare earths

investor must own.

Keywords

Important Disclosures

Stormcrow Capital Ltd. (“Stormcrow”) is a financial and technical/scientific consulting firm that provides its clients with some or all of the following services: (i) an assessment of the client’s industry, business plans and operations, market positioning, economic situation and prospects; (ii) certain technical and scientific commentary, analysis and advice that is within the expertise of Stormcrow’s staff; (iii) advice regarding optimization strategies for the client’s business and capital structure; and (iv) opinions regarding the future expected value of the client’s equity securities so as to allow the client to then make capital market, capital budgeting and capital structure plans. Stormcrow does not provide securities trading services, equity sales or distribution services, securities underwriting services, or investment banking services. Stormcrow does publish research reports for general and regular circulation. With the consent of Stormcrow’s client, the client and/or its industry sector may be the subject of an investment or financial research report, newsletter, bulletin or other publication by Stormcrow where such publication is made publicly available at www.stormcrow.ca or elsewhere or is otherwise distributed by Stormcrow. Any such publication is limited to generic, non-tailored advice or opinions and should not be construed as investment advice that is suitable for the reader or recipient. Stormcrow does not offer personalized or tailored investment advice to anyone and its research reports should not be relied upon in making any investment decisions. Rather, investors should speak with their personal financial advisor(s).

The primary issuer discussed herein is a client of Stormcrow, and as such, Stormcrow has agreed to provide the Company with a variety of consulting services. The fixed rate fee that the Company pays to Stormcrow is not contingent on the content or conclusions of any of Stormcrow’s research reports and is not contingent on the price, or price movement, of any securities.

None of Stormcrow’s officers, directors, or significant shareholders own, directly or indirectly, shares in the Company. It is a policy of Stormcrow and its employees to refrain from trading in a manner that is contrary to, or inconsistent with, Stormcrow’s most recent published recommendations or ratings, except in circumstances of unanticipated extreme financial hardship.

Stormcrow intends to provide regular market updates on the affairs of the Company (at Stormcrow’s discretion) and make these updates publicly available at www.stormcrow.ca. Readers who wish to receive notice when such updates become available, should email to [email protected] with the subject heading “Get Update Notifications”.

All information used in the publication of this report has been compiled from publicly available sources that Stormcrow believes to be reliable. Stormcrow does not guarantee the accuracy or completeness of the information found in this report and Stormcrow may not have undertaken any independent investigation to confirm or verify such information. Opinions contained in this report represent the true opinion of Stormcrow and the author(s) at the time of publication.

The securities described in this research report may not be eligible for sale in all jurisdictions or to certain categories of investors. This report and the content herein should not be construed by anyone as a solicitation to effect, or attempt to effect, any transaction in a security. This document was prepared and was made available for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned herein. The

Industry Rare Earths, Critical Materials, Critical Metals, Mining, Industrial Minerals

Relevant

Companies

GREAT WESTERN MINERALS – GWG:TSXV ARAFURA RESOURCES – ARU:ASX MOLYCORP – MCP:NYSE FRONTIER RARE EARTHS – FRO:TSX RARE ELEMENT RES’S — RES:TSX UCORE RARE METALS – UCU:TSXV AVALON RARE METALS – AVL:TSX QUEST RARE MINERALS – QRM:TSX

MONTERO MINING – MON:TSXV PEAK RESOURCES – PEK:ASX LYNAS CORP – LYC:ASX NORTHERN MINERALS – NTU:ASX NAMIBIA RARE EARTHS – NRE:TSX HUDSON RESOURCES – HUD:TSXV MATAMEC EXPLO – MAT:TSXV STANS ENERGY CORP – HRE:TSXV

Why do we use keywords?

We feel people who could stand to benefit from the contents of this report, are not solely ones who already follow the specific company or sector discussed herein. As such, we hope to provide this free service to as wide an audience as possible—and keywords help to this end.

STORMCROW.CA | PAGE 15

STORMCROW

Sovereign Metals Inc. (SVM | ASX)

securities referred to herein should be considered speculative in nature and should be considered to involve a high amount of financial risk where investors may lose all of their investment.

Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. No representation is being made that any investment or security will or is likely to achieve the return or performance estimated herein. There can be sharp differences between expected performance results and the actual results.

Dissemination of Research

Since Stormcrow does not rely on earning commission fees from institutional agency trading services, or investment banking revenues, this research report is widely available to the public via its website: www.stormcrow.ca

Investment Rating Criteria

We do not provide an investment rating, beyond indicating whether the target price exceeds current trading ranges by a reasonable range, indicated as “Positive”, or whether the target price is either below or roughly equivalent to the current trading range, indicated as “Negative”. Each investor has an individual target return in mind, we leave it to the individual investor to determine how our target and the current price fit within their portfolio.

Related Documents