www.digitaltvresearch.com April 2018 Editor: Simon Murray Tel: +44 20 8248 5051 Free newsletter published: Four times/year [email protected] Copyright: Digital TV Research Ltd Copyright notice: No part of this publication may be copied, duplicated or photocopied without written consent from Digital TV Research Ltd. Table of contents: • Africa to add 17.4 million pay TV subs • Competition bites for MENA pay TV • Latin America pay TV decelerates • US pay TV revenues to fall by $27 billion • Eastern Europe to add 17m digital pay TV subs • Ghana pay TV subscriber and revenue prospects • Saudi Arabia pay TV subscriber and revenue prospects • Costa Rica pay TV subscriber and revenue prospects • Canada pay TV subscriber and revenue prospects • Hungary pay TV subscriber and revenue prospects

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.digitaltvresearch.com

April 2018

Editor: Simon Murray

Tel: +44 20 8248 5051

Free newsletter published: Four times/year

Copyright: Digital TV Research Ltd

Copyright notice: No part of this publication may be copied, duplicated or photocopied without written consent from Digital TV

Research Ltd.

Table of contents:

• Africa to add 17.4 million pay TV subs

• Competition bites for MENA pay TV

• Latin America pay TV decelerates

• US pay TV revenues to fall by $27 billion

• Eastern Europe to add 17m digital pay TV subs

• Ghana pay TV subscriber and revenue prospects

• Saudi Arabia pay TV subscriber and revenue prospects

• Costa Rica pay TV subscriber and revenue prospects

• Canada pay TV subscriber and revenue prospects

• Hungary pay TV subscriber and revenue prospects

April 2018

Digital TV Research publication schedule for 2018 Title Publication Price

1 Sub-Saharan Africa Pay TV Forecasts January £1200/€1440/$1560

2 Middle East & North Africa Pay TV Forecasts

January £1200/€1440/$1560

3 Asia Pacific Pay TV Forecasts March £1200/€1440/$1560

4 Latin America Pay TV Forecasts March £1200/€1440/$1560

5 North America Pay TV Forecasts March £500/€600/$650

6 Eastern Europe Pay TV Forecasts March £1200/€1440/$1560

7 Western Europe Pay TV Forecasts May £1200/€1440/$1560

8 Global Pay TV Subscriber Forecasts May £1500/€1800/$1950

9 Global Pay TV Revenue Forecasts June £1500/€1800/$1950

10 Global Pay TV Operator Forecasts June £1500/€1800/$1950

11 Pay TV Operator Prospects June £800/€960/$1040

12 Pay TV Revenue Prospects July £800/€960/$1040

13 Netflix Forecasts July £600/€720/$780

14 Sub-Saharan Africa OTT TV & Video Forecasts August

£1000/€1200/$1300

15 Middle East & North Africa OTT TV & Video Forecasts

August £1000/€1200/$1300

16 Asia Pacific OTT TV & Video Forecasts September £1000/€1200/$1300

17 Latin America OTT TV & Video Forecasts September £1000/€1200/$1300

18 North America OTT TV & Video Forecasts September £500/€600/$650

19 Eastern Europe OTT TV & Video Forecasts October £1000/€1200/$1300

20 Western Europe OTT TV & Video Forecasts

October £1000/€1200/$1300

21 Global OTT TV & Video Forecasts October £1800/€2160/$2340

22 Global SVOD Forecasts November £1500/€1800/$1950

23 OTT TV & Video Prospects November £1000/€1200/$1300

24 SVOD Prospects December £900/€1080/$1170

PLEASE CLICK HERE FOR MORE INFORMATION ON OUR LATEST PUBLICATIONS

PLEASE CLICK HERE TO ACCESS OUR CORPORATE BROCHURE

April 2018

Africa to add 17.4 million pay TV subs

The number of pay TV subscribers in Sub-Saharan Africa will increase by 74% between 2017 and 2023 to reach 40.89 million. However, the Sub-Saharan Africa Pay TV Forecasts report estimates that subscriber growth will outstrip revenue progress. Pay TV revenues will climb by 41% to $6.64 billion by 2023, up by $2 billion on 2017.

Simon Murray, Principal Analyst at Digital TV Research, explained: “Pay TV competition in Sub-Saharan Africa is becoming more and more intense, especially given the launch of Kwese TV in 14 countries during 2017.”

Murray continued: “Pay TV operators in most countries have lowered subscription fees and/or subsidized/given away equipment as competition intensifies. By no means are all of the existing pay TV platforms are expected to survive in the long run. Having said that, several pay TV operators are booming.”

Kenya will continue to show considerable digital TV growth, but it is overcrowded. Kenya now boasts two pay DTT platforms, a cable network and five main satellite TV operators – too many for a country with only 4.01 million TV households.

From the 23.49 million pay TV subscribers at end-2017, 13.78 million were satellite TV and 9.11 million DTT. By 2023, satellite TV will contribute 20.89 million and DTT 17.53 million. This means an extra 7 million pay satellite TV subscribers and 8 million pay DTT homes.

Nigeria will have the most pay TV subscribers by 2023 – having overtaken South Africa in 2021. The top eight countries will supply three-quarters of the total in 2023.

April 2018

Source: Digital TV Research

Multichoice had 12.48 million subs across satellite TV platform DStv and DTT platform GOtv by end-2017, which will grow to 16.66 million by 2023. France’s Vivendi had 2.96 million subs to its Canal Plus satellite TV platform and Easy TV by end-2017; forecast to climb by nearly 2 million to 4.87 million by 2023.

StarTimes/StarSat will enjoy the most impressive growth: from 6.23 million subs at end-2017 to 13.42 million by 2023 – growing from half the Multichoice total in 2017 to 81% of its total by 2023.

Nigeria, 9,685

S Africa, 9,281

Kenya, 2,888Tanzania, 2,269

DRC, 2,035

Uganda, 1,767

Cote D'Ivoire, 1,384

Angola, 1,056

Others, 10,523

Pay TV subs by country in 2023 (000)

April 2018

Competition bites for MENA pay TV

Pay TV revenues for the 20 countries covered in the eighth edition of the Middle East and North Africa Pay TV Forecasts report will reach $3.62 billion in 2023 – up by only 7.8% on 2017. Pay TV revenues will fall in 2018. They will be flat in 2019 before starting a slow recovery.

Concentrating just on the 13 Arabic-speaking countries, pay TV revenues will grow by 24% from $1.18 billion in 2017 to $1.46 billion in 2023, despite pay TV subscriptions rising by 47% over the same period to 5.84 million. If subscriptions are growing faster than revenues, then ARPUs must be falling.

Simon Murray, Principal Analyst at Digital TV Research, said: “The region has always been difficult for pay TV, with many homes receiving many FTA channels and rampant piracy being commonplace. beIN is shaking up the market with its strong slate of exclusive sports rights. beIN is now providing more entertainment content.”

beIN’s moves have hit long-established rival OSN. OSN benefits from exclusive long-term deals with all of the Hollywood studios. However, OSN has struggled to push its subscriber base much beyond 1 million subscribers.

Murray explained: “Competition is increasing – not only from beIN, but also from the multitude of SVOD platforms that have launched in recent years. These platforms compete more directly against OSN than beIN due to their emphasis on drama. No SVOD platforms can compete against beIN with live sports provision.”

Murray continued: “OSN’s reaction was to cut its subscription prices substantially in February 2017. Digital TV Research believes that further cuts will be made as OSN struggles to hold on to its subscriber base until its fees are just above beIN’s.”

OSN’s revenues will reach $498 million in 2023 – down from $700 million in 2015. beIN’s revenues will exceed OSN’s in 2022. beIN’s revenues will double between 2016 and 2023. beIN will overtake OSN by subscriber numbers in 2018. beIN is forecast to have 1.87 million satellite TV subscribers by 2023 – ahead of OSN’s 1.46 million [so excluding subscribers to their channels on other platforms such as IPTV and cable].

April 2018

Source: Digital TV Research

beIN’s sister company Digiturk will retain regional market leadership despite more intense competition in Turkey. Israel will experience cord-cutting. Israel will lose 27,000 pay TV subs between 2017 to 2023. We forecast that Israeli pay TV revenues will fall from more than $1 billion in 2015 to $767 million in 2023 as cheaper OTT platforms force traditional pay TV operators to lower their fees.

2017 2023

Other 580 874

Yes 462 385

HOT 472 359

D-Smart 125 124

TTNet 27 126

Turksat 81 76

Digiturk 688 655

beIN 269 521

OSN 622 498

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Pay TV revenue growth by operator ($m)

April 2018

Latin America pay TV decelerates

Although the economic recession waned somewhat in 2017, the Latin American pay TV sector was still affected. According to the eighth edition of the Latin America Pay TV Forecasts report, the number of pay TV subscribers was flat year-on-year.

Fewer than 5 million additional pay TV subscribers are expected between 2017 and 2023 – bringing the total to almost 76 million. Pay TV penetration will not climb beyond the current 44% of TV households.

Source: Digital TV Research Ltd

Simon Murray, Principal Analyst at Digital TV Research, said: “Given its continuing economic and social problems, Brazil lost 1 million pay TV subscribers between 2015 and 2017. Its peak year of 2014 will not be bettered until 2023.”

Murray continued: “Mexico recorded impressive growth in 2016, but its pay TV subscriber count fell in 2017. It will continue to decline until a slow recovery starts in 2020. The 2023 total will be just under the 2016 peak. However, it’s not all bad news as Claro and Telefonica will enter Argentina and Mexico, although this is likely to involve OTT.”

Mexico overtook Brazil in 2016 to become Latin America’s largest pay TV market, despite Brazil having twice as many TV households as Mexico. Brazil has been losing subscribers since November 2014. However, Brazil will regain top slot in 2023 - just.

2017 2018 2023

Others 18,552 18,953 20,808

Colombia 5,557 5,691 6,161

Argentina 9,253 9,388 9,599

Brazil 18,181 17,839 19,656

Mexico 19,417 19,283 19,560

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Latin America pay TV subscribers by country (000)

April 2018

Pay TV revenues in Latin America [subscriptions and PPV] will grow by only 1.0% between 2017 and 2023 to $19.74 billion. Revenues will fall in 2017, 2018 and 2019 before a slow recovery begins.

Brazil ($7.01 billion in 2023) will remain the top country by pay TV revenues by some distance, followed by Mexico ($2.49 billion) and Argentina ($2.49 billion). Brazilian subscription rates are much higher than Mexican ones. Brazil’s 2023 total will be lower than 2017 and the peak year of 2014.

Two operators dominate pay TV in Latin America. Claro/America Movil had 13.91 million pay TV subscribers (Down by 500,000 on the previous year) by end-2017 and DirecTV/Sky had 21.31 million. These two companies accounted for nearly half of the region’s pay TV subs by end-2017.

April 2018

US pay TV revenues to fall by $27 billion

US pay TV revenues peaked in 2015, at $101.71 billion, according to the eighth edition of the North America Pay TV Forecasts report. A $26.58 billion decline (26%) is forecast between 2015 and 2023 to take the total down to $75.13 billion.

Cable TV revenues peaked in 2010 at $54.11 billion, but they will fall to $36.75 billion by 2023. Cable will lose nearly 12 million subscribers between 2010 and 2023 (although most of the heaviest losses have already taken place).

Simon Murray, Principal Analyst at Digital TV Research, added: “Cable TV is not the only platform to suffer. Satellite TV and IPTV are also losing subscribers and revenues. Much of this is due to the operators shifting their subscribers to online platforms. However, growth from vMVPDs is not expected to make up completely for the subscriber and revenue shortfalls from traditional pay TV.”

IPTV’s fall is mainly due to AT&T encouraging its U-Verse subscribers to convert to DirecTV, its other pay TV asset. This is the reverse of what has happened in most other countries. IPTV revenues spiked in 2015 at $9.60 billion, and they will halve to $4.77 billion in 2023. The number of IPTV subs topped 12.00 million in 2014, but it will decline to 6.26 million in 2023.

Satellite TV revenues will fall from $39.78 billion in 2017 to $33.61 billion in 2023 – or down by 16%. Satellite TV subscriptions will drop by 4.08 million between end-2017 and 2023; having fallen by nearly 3 million in 2017 alone. DISH is pushing its vMVPD platform Sling TV hard, with DirecTV Now also making an impact.

The number of US traditional pay TV subscribers will fall from a zenith of 100.34 million in 2012 to 90.35 million by end-2017 and down to 80.33 million in 2023. Pay TV penetration will fall from 87.6% of TV households in apex year 2013 to 66.7% in 2023.

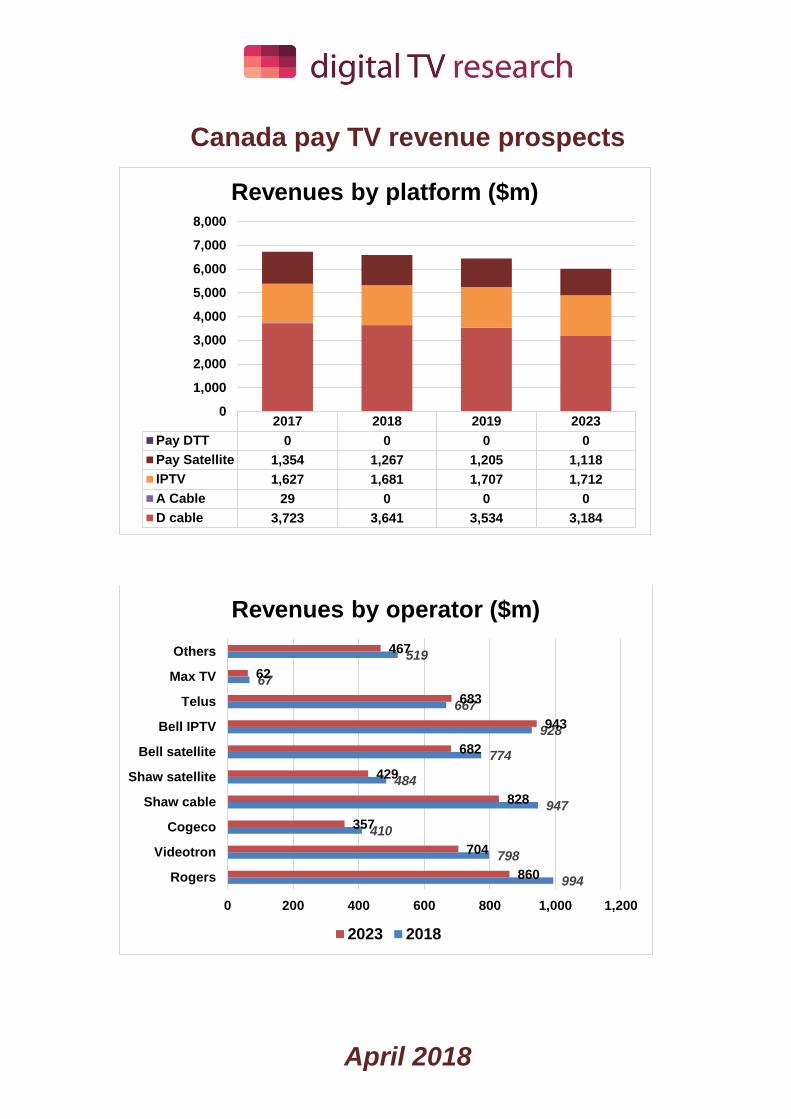

Although Canada is losing pay TV subscribers, its problems are not as severe as its Southern neighbor. Pay TV penetration reached a highpoint in 2013 at 85.1%. The level will fall to 74.8% by 2023. However, the number of pay TV subscribers will be 11.17 million by 2023 – about the same as 2017. Pay TV revenues will fall from a peak of US$6.82 billion in 2015 to US$6.01 billion by 2023.

April 2018

Eastern Europe to add 17m digital pay TV subs

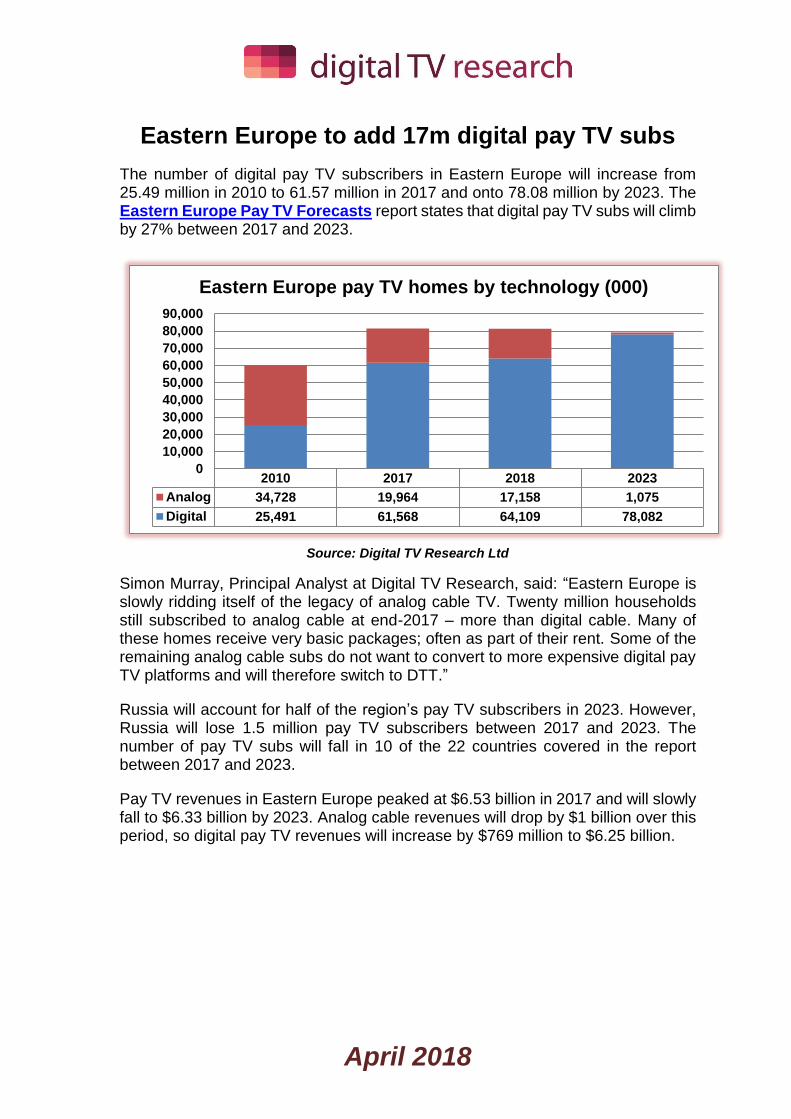

The number of digital pay TV subscribers in Eastern Europe will increase from 25.49 million in 2010 to 61.57 million in 2017 and onto 78.08 million by 2023. The Eastern Europe Pay TV Forecasts report states that digital pay TV subs will climb by 27% between 2017 and 2023.

Source: Digital TV Research Ltd

Simon Murray, Principal Analyst at Digital TV Research, said: “Eastern Europe is slowly ridding itself of the legacy of analog cable TV. Twenty million households still subscribed to analog cable at end-2017 – more than digital cable. Many of these homes receive very basic packages; often as part of their rent. Some of the remaining analog cable subs do not want to convert to more expensive digital pay TV platforms and will therefore switch to DTT.”

Russia will account for half of the region’s pay TV subscribers in 2023. However, Russia will lose 1.5 million pay TV subscribers between 2017 and 2023. The number of pay TV subs will fall in 10 of the 22 countries covered in the report between 2017 and 2023.

Pay TV revenues in Eastern Europe peaked at $6.53 billion in 2017 and will slowly fall to $6.33 billion by 2023. Analog cable revenues will drop by $1 billion over this period, so digital pay TV revenues will increase by $769 million to $6.25 billion.

2010 2017 2018 2023

Analog 34,728 19,964 17,158 1,075

Digital 25,491 61,568 64,109 78,082

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Eastern Europe pay TV homes by technology (000)

April 2018

Digital TV Research publication schedule for 2017 Title Publication Price

Asia Pacific Pay TV Forecasts March £1200/€1440/$1560

Western Europe Pay TV Forecasts May £1200/€1440/$1560

Global Pay TV Subscriber Forecasts May £1800/€2160/$2340

Global Pay TV Revenue Forecasts May £1800/€2160/$2340

Global Pay TV Operator Forecasts May £1800/€2160/$2340

Netflix Forecasts June £750/€900/$975

Global Pay TV Subscriber Databook June £750/€900/$975

Global Pay TV Revenue Databook June £750/€900/$975

Global Pay TV Operator Databook June £750/€900/$975

Sub-Saharan Africa OTT TV & Video Forecasts July

£1000/€1200/$1300

Middle East & North Africa OTT TV & Video Forecasts July

£1000/€1200/$1300

Asia Pacific OTT TV & Video Forecasts August £1000/€1200/$1300

Latin America OTT TV & Video Forecasts August £1000/€1200/$1300

North America OTT TV & Video Forecasts September £600/€720/$780

Eastern Europe OTT TV & Video Forecasts

September £1000/€1200/$1300

Western Europe OTT TV & Video Forecasts

October £1000/€1200/$1300

Global OTT TV & Video Forecasts October £1800/€2160/$2340

Global AVOD Forecasts October £1000/€1200/$1300

Global SVOD Forecasts October £1500/€1800/$1950

Online TV Piracy Forecasts November £1200/€1440/$1560

SVOD Digest November £500/€600/$650

OTT & Pay TV Forecasts December £1500/€1800/$1950

PLEASE CLICK HERE FOR MORE INFORMATION ON OUR LATEST PUBLICATIONS

PLEASE CLICK HERE TO ACCESS OUR CORPORATE BROCHURE

Discounts are available for multiple report purchases.

Please contact [email protected]

April 2018

Ghana pay TV subscriber prospects

2017 2018 2019 2023

A terres 350 127 0 0

Pay DTT 277 295 318 417

Free DTT 1,022 1,297 1,465 1,671

Free satellite 93 104 115 157

Pay Satellite 204 249 298 450

IPTV 0 4 11 66

A Cable 0 0 0 0

D cable 0 0 0 0

0

500

1,000

1,500

2,000

2,500

3,000

Subscribers by platform (000)

10

154

295

50

39

18

176

417

146

177

0 50 100 150 200 250 300 350 400 450

Canal Plus

DStv

Gotv

StarSat

Others

Subscribers by operator (000)

2023 2018

April 2018

Ghana pay TV revenue prospects

2017 2018 2019 2023

Pay DTT 16 17 18 24

Pay Satellite 50 52 59 74

IPTV 0 0 1 4

A Cable 0 0 0 0

D cable 0 0 0 0

0

20

40

60

80

100

120

Revenues by platform ($m)

4

44

16

2

1

6

42

24

11

20

0 10 20 30 40 50

Canal Plus

DStv

Gotv

StarSat

Others

Revenues by operator ($m)

2023 2018

April 2018

Saudi Arabia pay TV subscriber prospects

2017 2018 2019 2023

A terres 0 0 0 0

Pay DTT 0 0 0 0

Free DTT 632 573 523 427

Free satellite 4,137 4,225 4,305 4,671

Pay Satellite 757 785 812 934

IPTV 384 453 511 641

A Cable 0 0 0 0

D cable 0 0 0 0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Subscribers by platform (000)

447

337

303

149

0

561

374

404

237

0

0 100 200 300 400 500 600

beIN

OSN

Invision

eLife

Others

Subscribers by operator (000)

2023 2018

April 2018

Saudi Arabia pay TV revenue prospects

2017 2018 2019 2023

Pay DTT 0 0 0 0

Pay Satellite 273 265 254 287

IPTV 104 126 144 189

A Cable 0 0 0 0

D cable 0 0 0 0

0

50

100

150

200

250

300

350

400

450

500

Revenues by platform ($m)

112

153

85

41

0

157

130

119

70

0

0 20 40 60 80 100 120 140 160 180

beIN

OSN

Invision

eLife

Others

Revenues by operator ($m)

2023 2018

April 2018

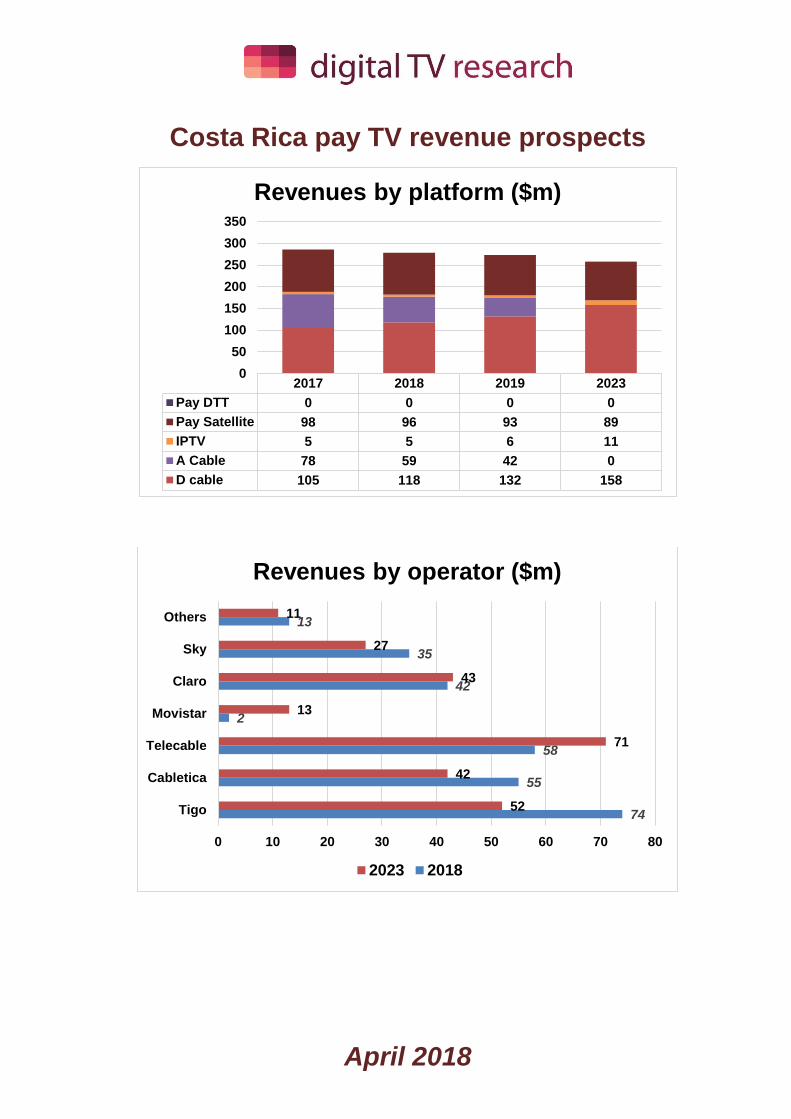

Costa Rica pay TV subscriber prospects

2017 2018 2019 2023

A terres 182 118 0 0

Pay DTT 0 0 0 0

Free DTT 208 281 404 413

Free satellite 173 175 178 187

Pay Satellite 257 260 263 277

IPTV 18 22 27 51

A Cable 222 168 114 0

D cable 325 379 436 569

0200400600800

1,0001,2001,4001,600

Homes by platform (000)

215

168

183

18

147

61

36

175

151

256

54

170

51

39

0 50 100 150 200 250 300

Tigo

Cabletica

Telecable

Movistar

Claro

Sky

Others

Subscribers by operator (000)

2023 2018

April 2018

Costa Rica pay TV revenue prospects

2017 2018 2019 2023

Pay DTT 0 0 0 0

Pay Satellite 98 96 93 89

IPTV 5 5 6 11

A Cable 78 59 42 0

D cable 105 118 132 158

0

50

100

150

200

250

300

350

Revenues by platform ($m)

74

55

58

2

42

35

13

52

42

71

13

43

27

11

0 10 20 30 40 50 60 70 80

Tigo

Cabletica

Telecable

Movistar

Claro

Sky

Others

Revenues by operator ($m)

2023 2018

April 2018

Canada pay TV subscriber prospects

2017 2018 2019 2023

A terres 0 0 0 0

Pay DTT 0 0 0 0

Free DTT 2,986 3,188 3,298 3,615

Free satellite 143 144 145 149

Pay Satellite 2,034 1,933 1,860 1,793

IPTV 2,034 1,933 1,860 1,793

A Cable 57 0 0 0

D cable 6,297 6,276 6,247 6,215

02,0004,0006,0008,000

10,00012,00014,00016,000

Homes by platform (000)

1,694

1,632

703

1,632

708

1,214

1,587

1,151

113

661

1,678

1,616

696

1,616

656

1,126

1,745

1,262

114

666

0 500 1,000 1,500 2,000

Rogers

Videotron

Cogeco

Shaw cable

Shaw satellite

Bell satellite

Bell IPTV

Telus

Max TV

Others

Subscribers by operator (000)

2023 2018

April 2018

Canada pay TV revenue prospects

2017 2018 2019 2023

Pay DTT 0 0 0 0

Pay Satellite 1,354 1,267 1,205 1,118

IPTV 1,627 1,681 1,707 1,712

A Cable 29 0 0 0

D cable 3,723 3,641 3,534 3,184

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Revenues by platform ($m)

994

798

410

947

484

774

928

667

67

519

860

704

357

828

429

682

943

683

62

467

0 200 400 600 800 1,000 1,200

Rogers

Videotron

Cogeco

Shaw cable

Shaw satellite

Bell satellite

Bell IPTV

Telus

Max TV

Others

Revenues by operator ($m)

2023 2018

April 2018

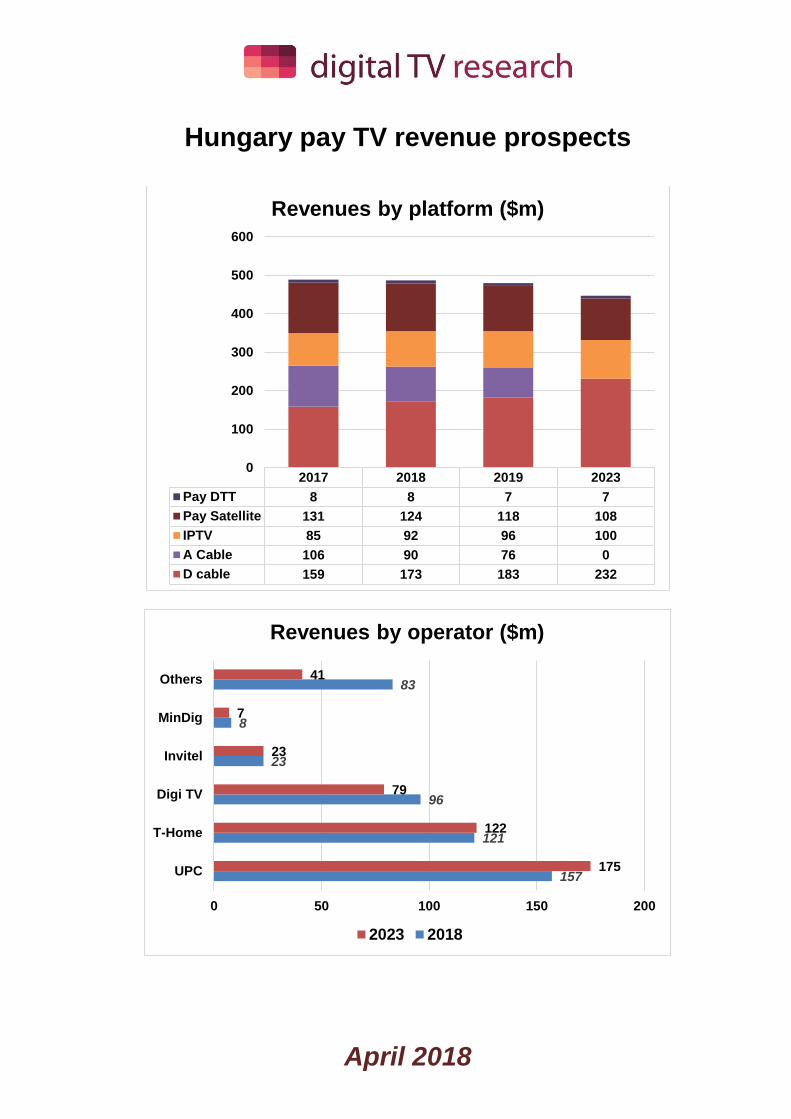

Hungary pay TV subscriber prospects

2017 2018 2019 2023

A terres 0 0 0 0

Pay DTT 91 86 82 77

Free DTT 285 300 315 365

Free satellite 78 78 78 77

Pay Satellite 846 803 769 710

IPTV 733 780 816 883

A Cable 823 702 583 0

D cable 1,053 1,150 1,244 1,728

0500

1,0001,5002,0002,5003,0003,5004,0004,500

Homes by platform (000)

959

1,055

782

179

86

458

1,179

1,173

681

189

77

99

0 200 400 600 800 1,000 1,200 1,400

UPC

T-Home

Digi TV

Invitel

MinDig

Others

Subscribers by operator (000)

2023 2018

April 2018

Hungary pay TV revenue prospects

2017 2018 2019 2023

Pay DTT 8 8 7 7

Pay Satellite 131 124 118 108

IPTV 85 92 96 100

A Cable 106 90 76 0

D cable 159 173 183 232

0

100

200

300

400

500

600

Revenues by platform ($m)

157

121

96

23

8

83

175

122

79

23

7

41

0 50 100 150 200

UPC

T-Home

Digi TV

Invitel

MinDig

Others

Revenues by operator ($m)

2023 2018

Related Documents