Philippine Interpretations Committee Approved Q&As on Philippine Financial Reporting Standards June 30, 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Philippine Interpretations Committee

Approved Q&As onPhilippine FinancialReportingStandardsJune 30, 2021

Philippine Interpretations Committee

i

Table of Contents

Preface .......................................................................................................................................xApproved PIC Q&As as of June 30, 2021 ................................................................................1

General Q&As .........................................................................................................................2

Q&A No. 2013-02: Conforming Changes to PIC Q&As – Cycle 2013 ...................................2

Q&A No. 2015-01: Conforming Changes to PIC Q&As – Cycle 2015 ...................................5

Q&A No. 2016-01: Conforming Changes to PIC Q&As – Cycle 2016 ...................................7

Q&A No. 2017-01: Conforming Changes to PIC Q&As – Cycle 2017 ...................................9

Q&A No. 2018-13: Conforming Changes to PIC Q&As – Cycle 2018 .................................12

Q&A No. 2019-04: Conforming Changes to PIC Q&As – Cycle 2019 .................................15

Q&A No. 2020-01: Conforming Changes to PIC Q&As – Cycle 2020 .................................18

PFRS 1, First-time Adoption of Philippine Financial Reporting Standards .............................21

Q&A No. 2011 – 05 (amended July 2019): PFRS 1 – Fair Value or Revaluation as DeemedCost ...................................................................................................................................21

PFRS 3, Business Combinations ...........................................................................................29

Q&A No. 2011 - 02: PFRS 3.2 – Common Control Business Combinations .......................29

Q&A No. 2012 - 01 (amended June 2018): PFRS 3.2 – Application of the Pooling ofInterests Method for Business Combinations of Entities under Common Control inConsolidated Financial Statements ....................................................................................33

Q&A No. 2012 – 02 (amended July 2019): Cost of a new building constructed on the site ofa previous building .............................................................................................................43

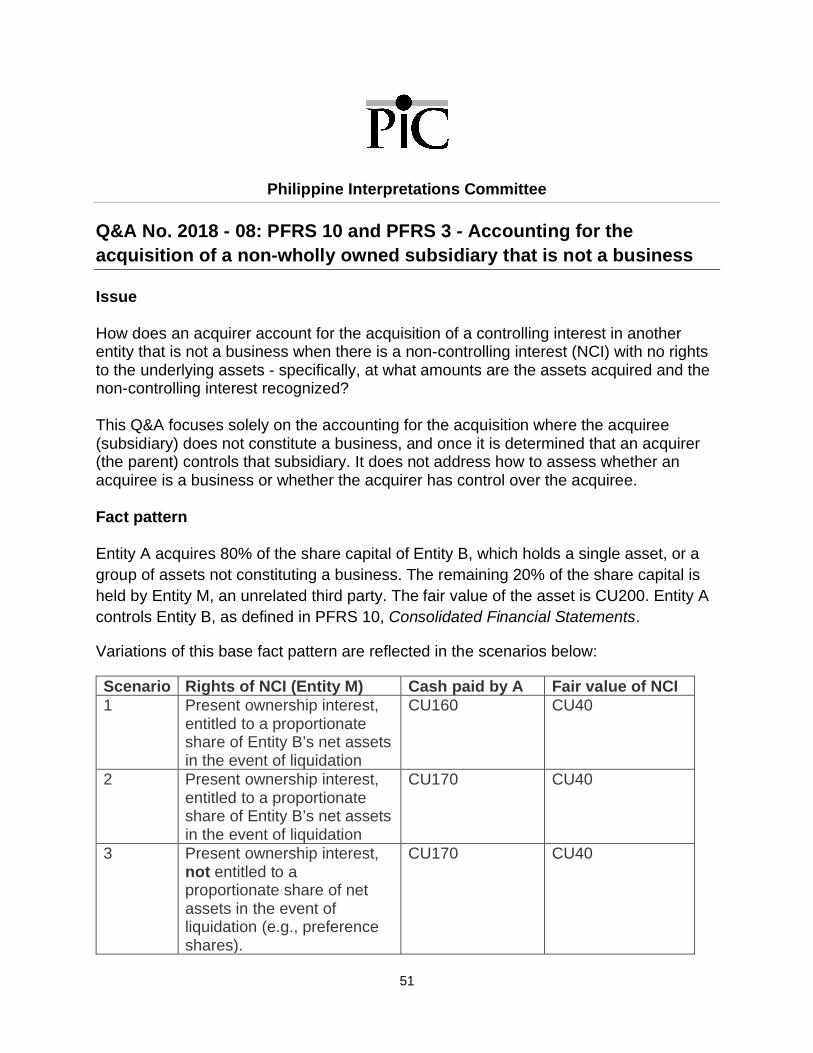

Q&A No. 2018 - 08: PFRS 10 and PFRS 3 - Accounting for the acquisition of a non-whollyowned subsidiary that is not a business .............................................................................51

PFRS 7, Financial Statements: Disclosures...........................................................................55

Q&A No. 2017 – 05 (amended June 2018): PFRS 7 – Frequently asked questions on thedisclosure requirements of financial instruments under PFRS 7, Financial Instruments:Disclosures ........................................................................................................................55

PFRS 9, Financial Instruments ..............................................................................................62

Philippine Interpretations Committee

ii

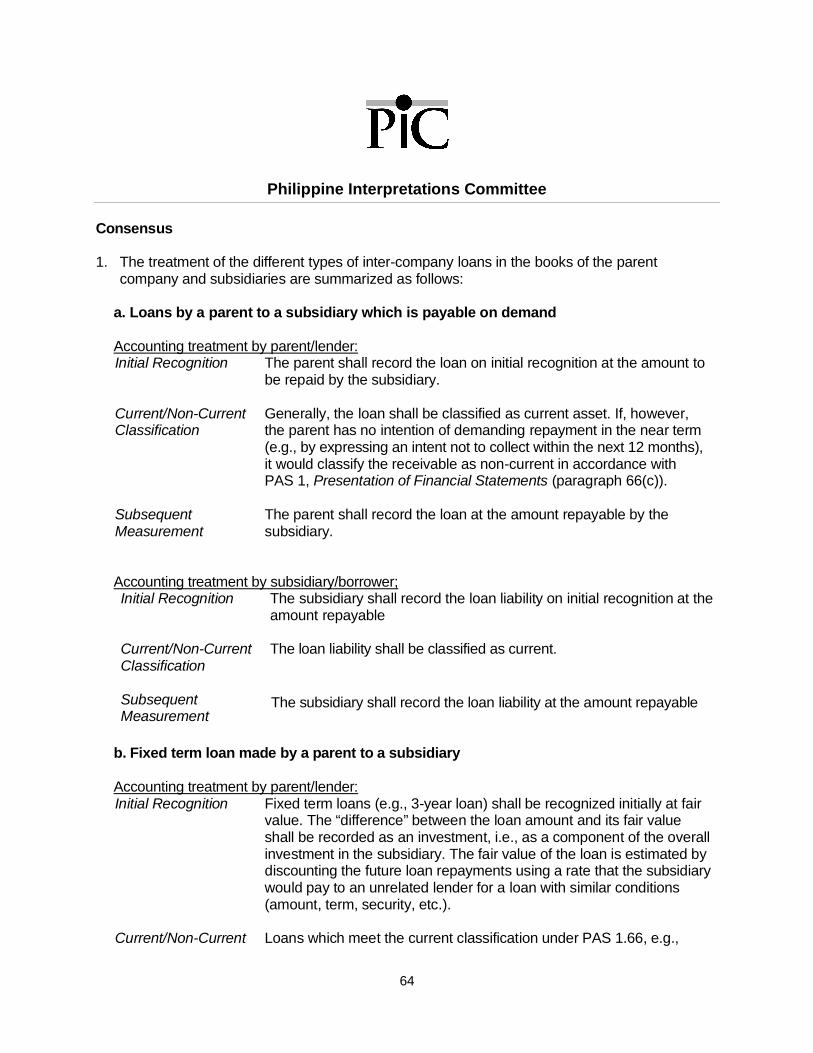

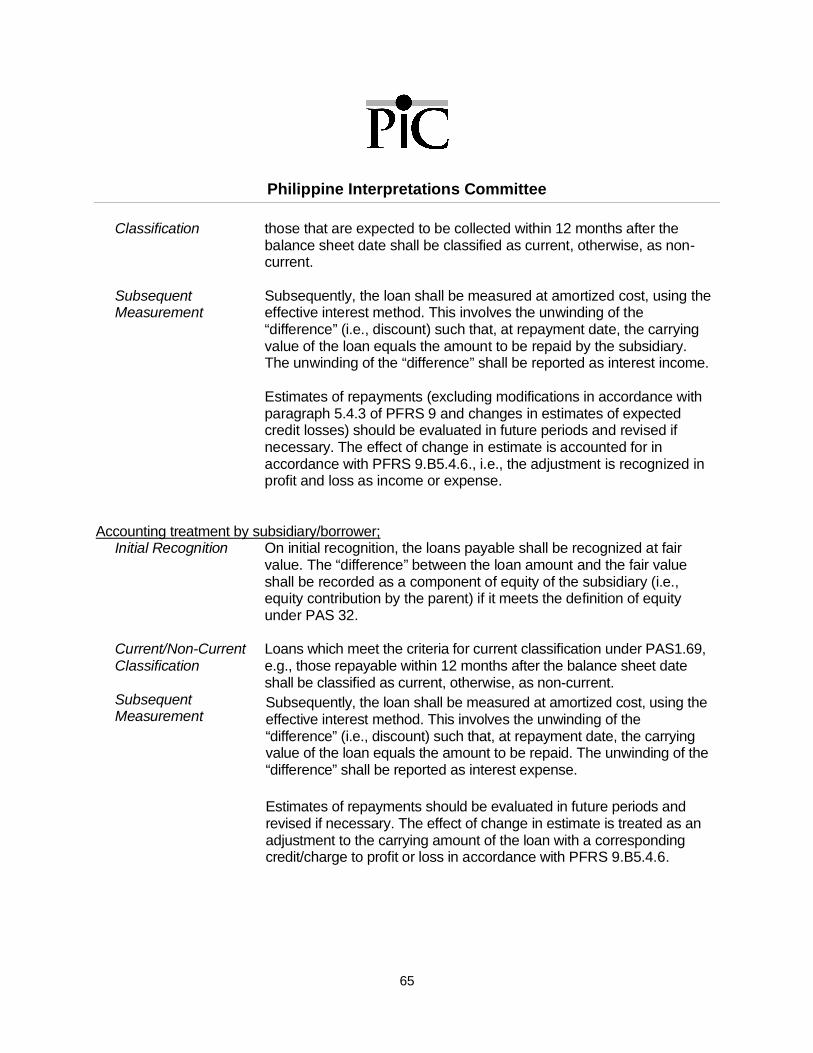

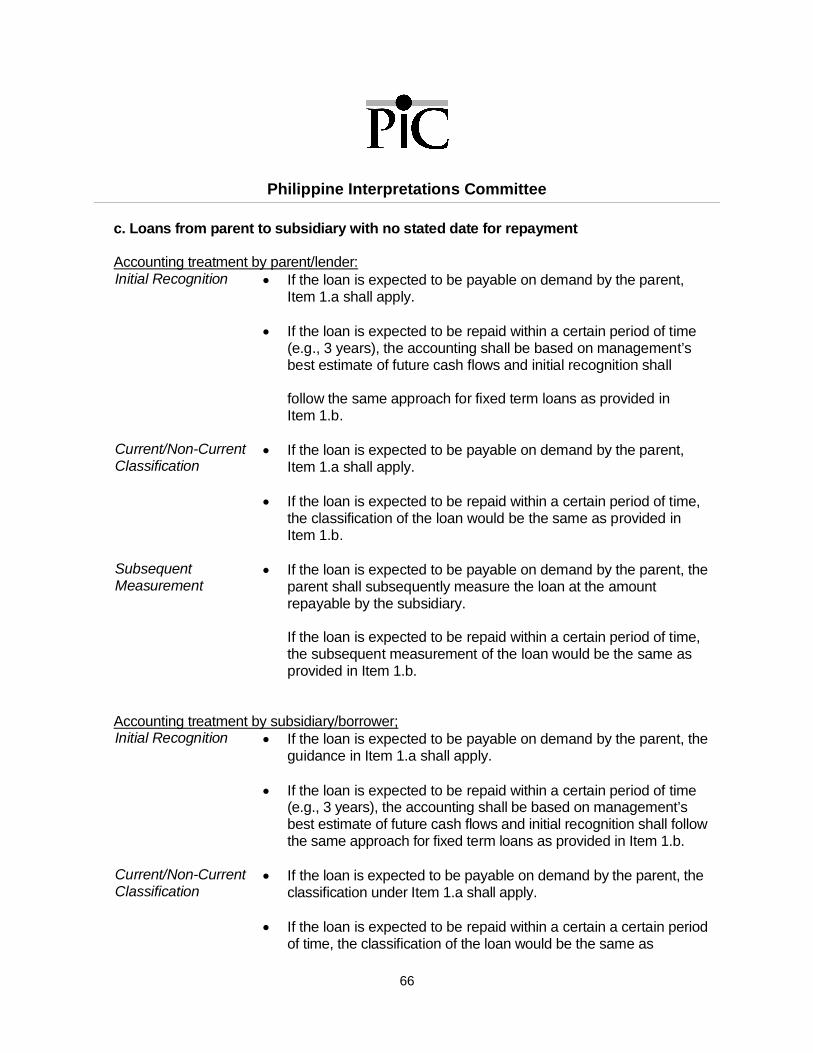

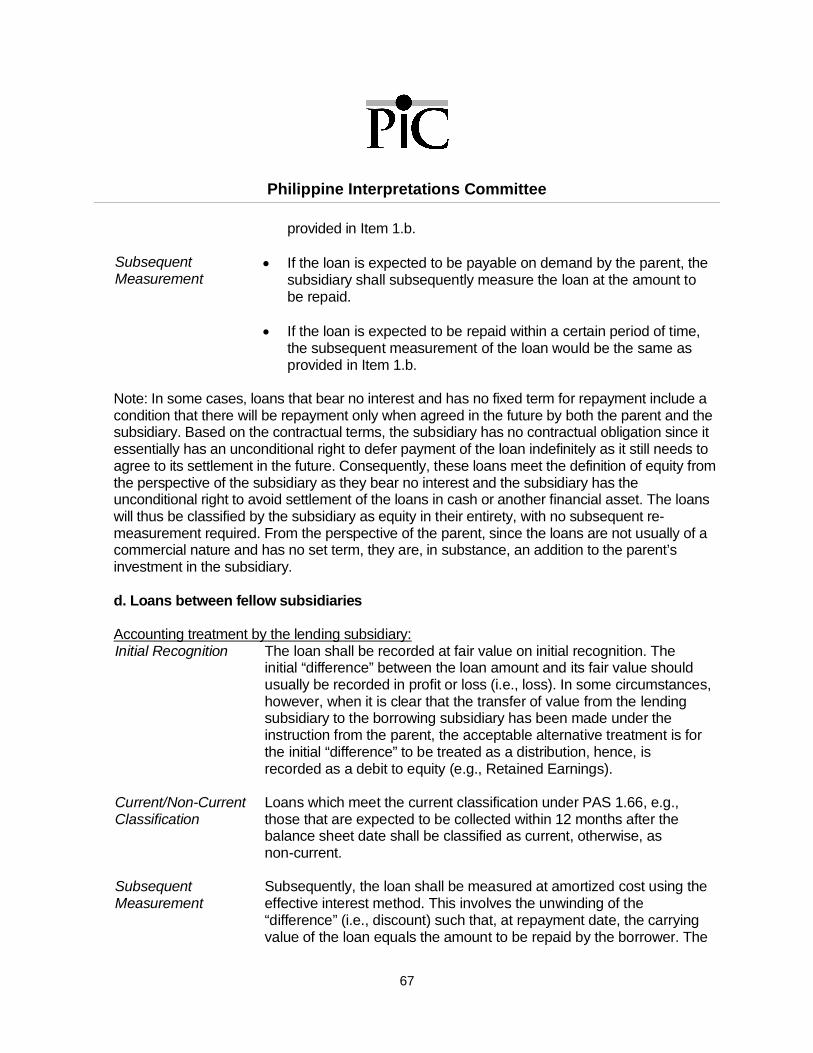

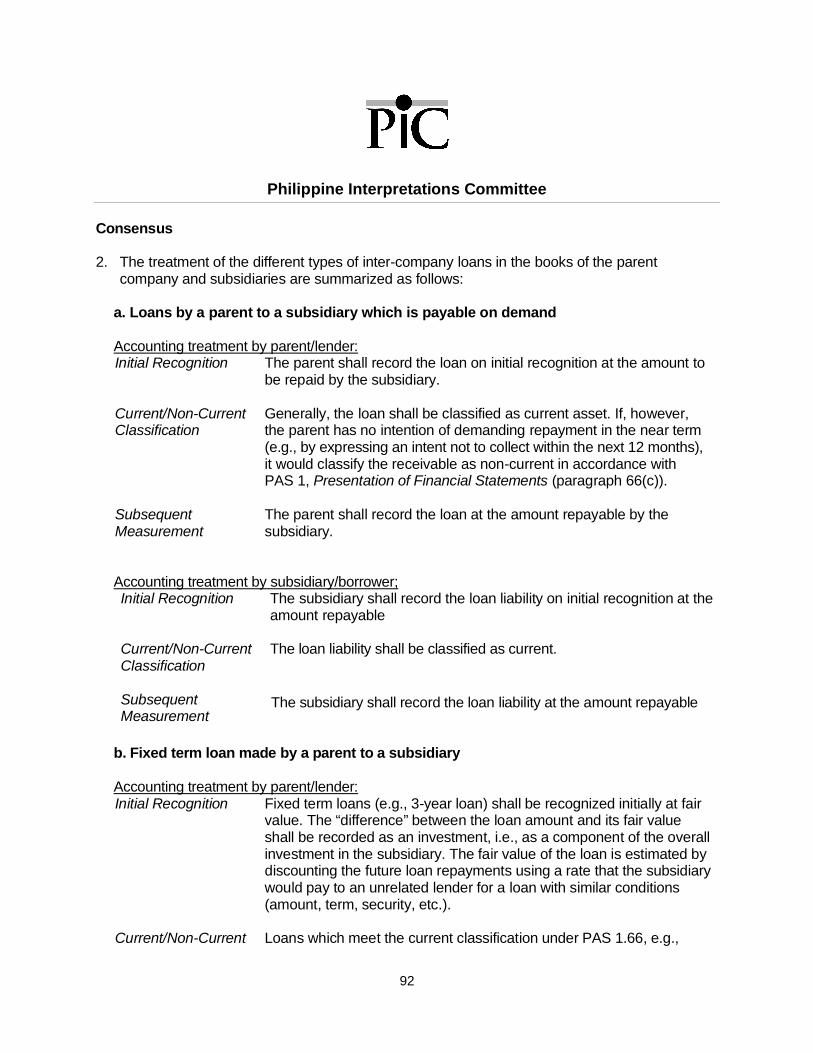

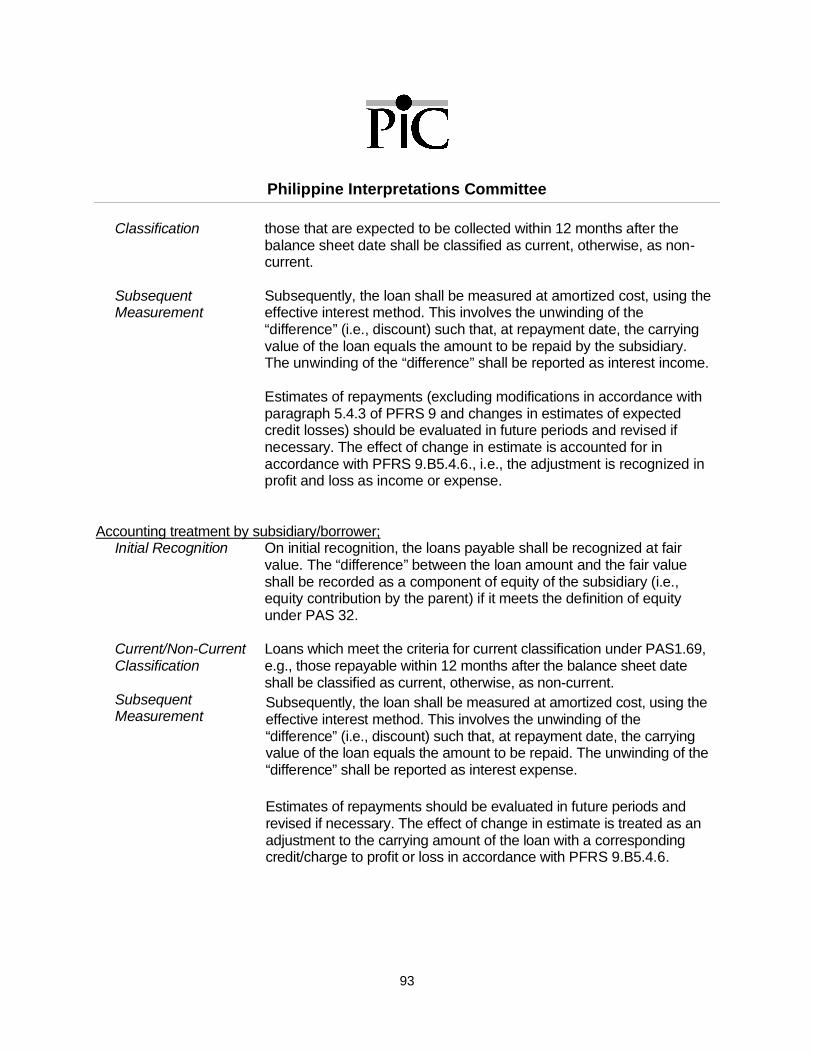

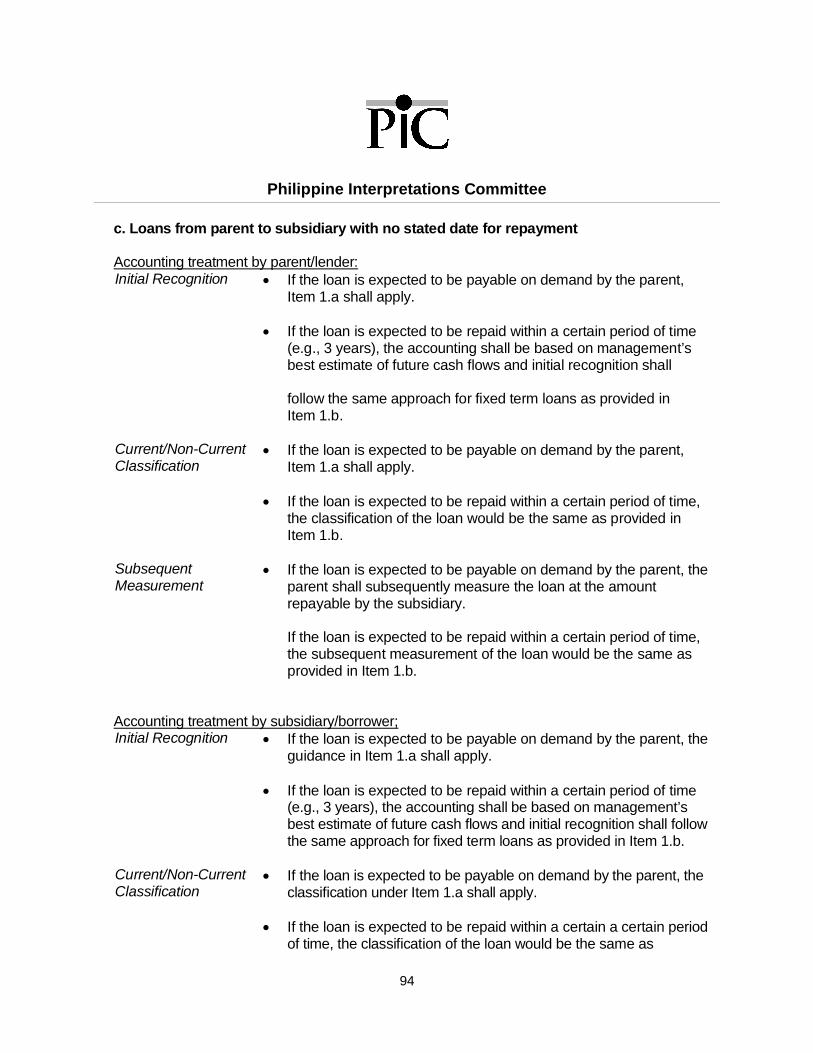

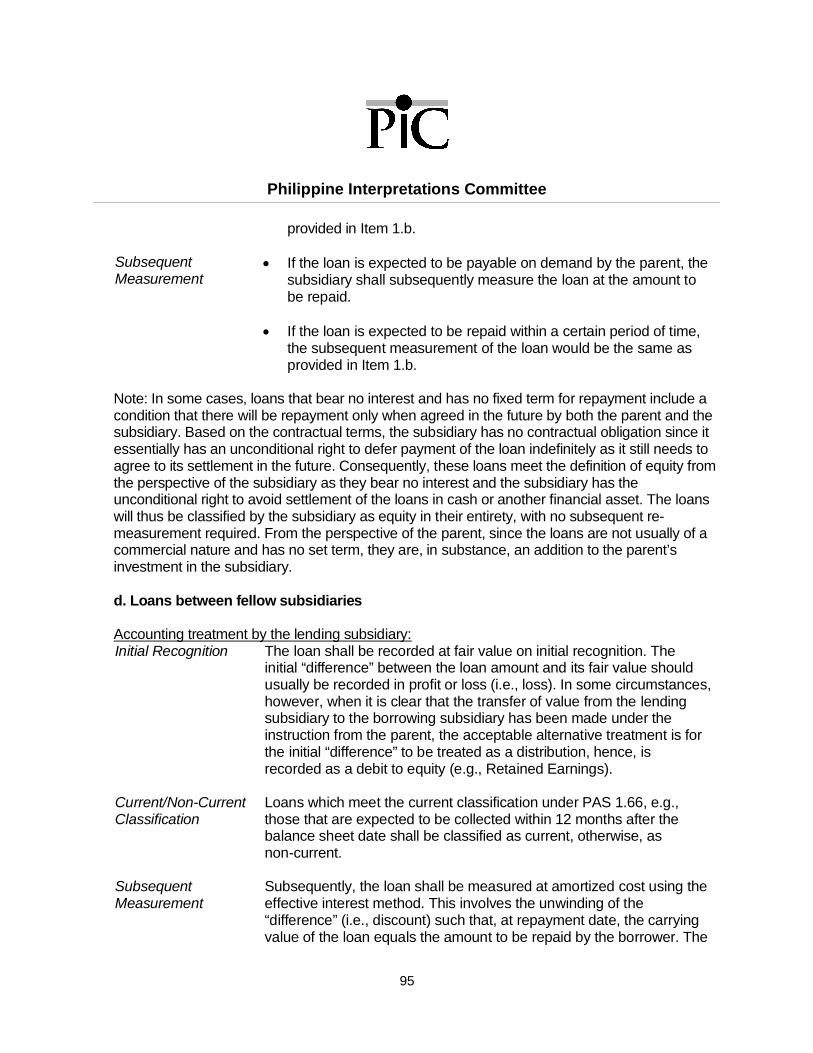

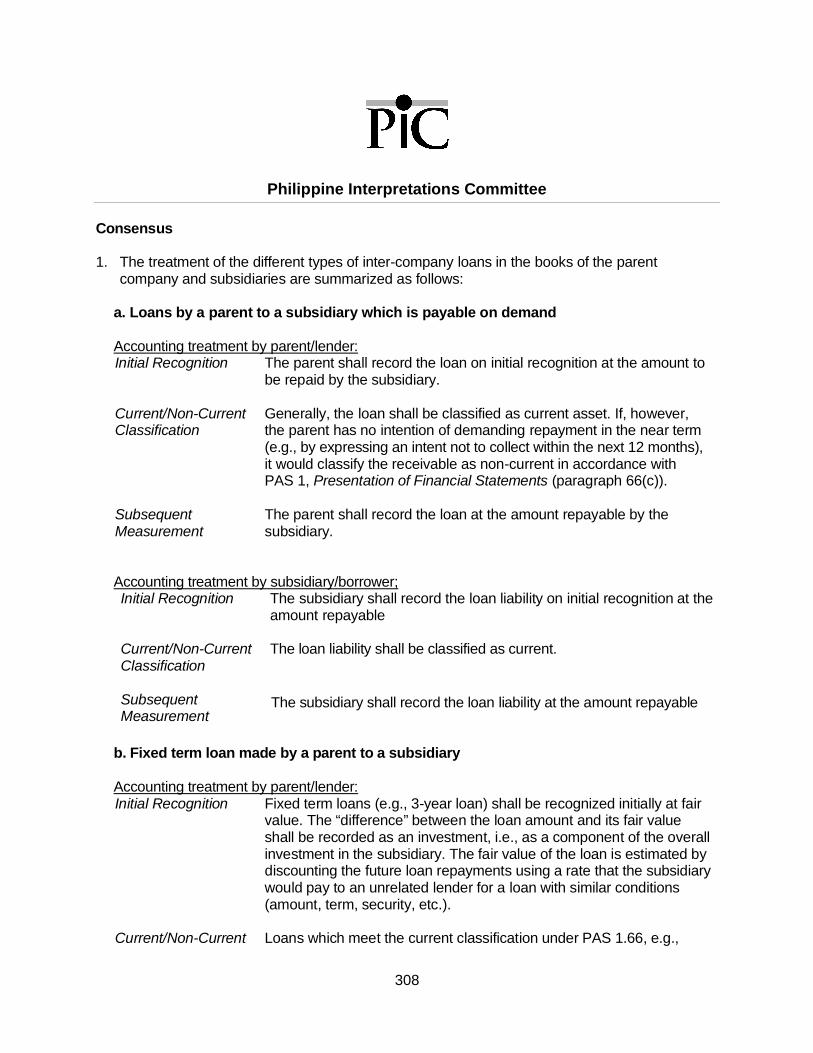

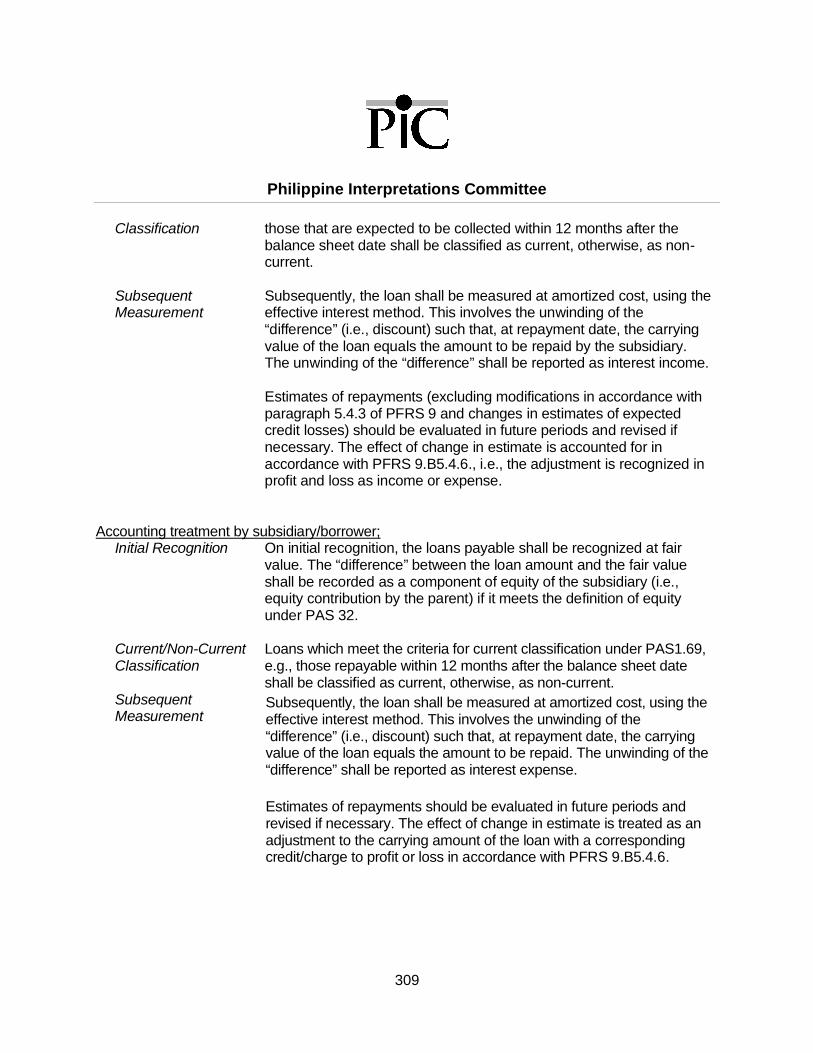

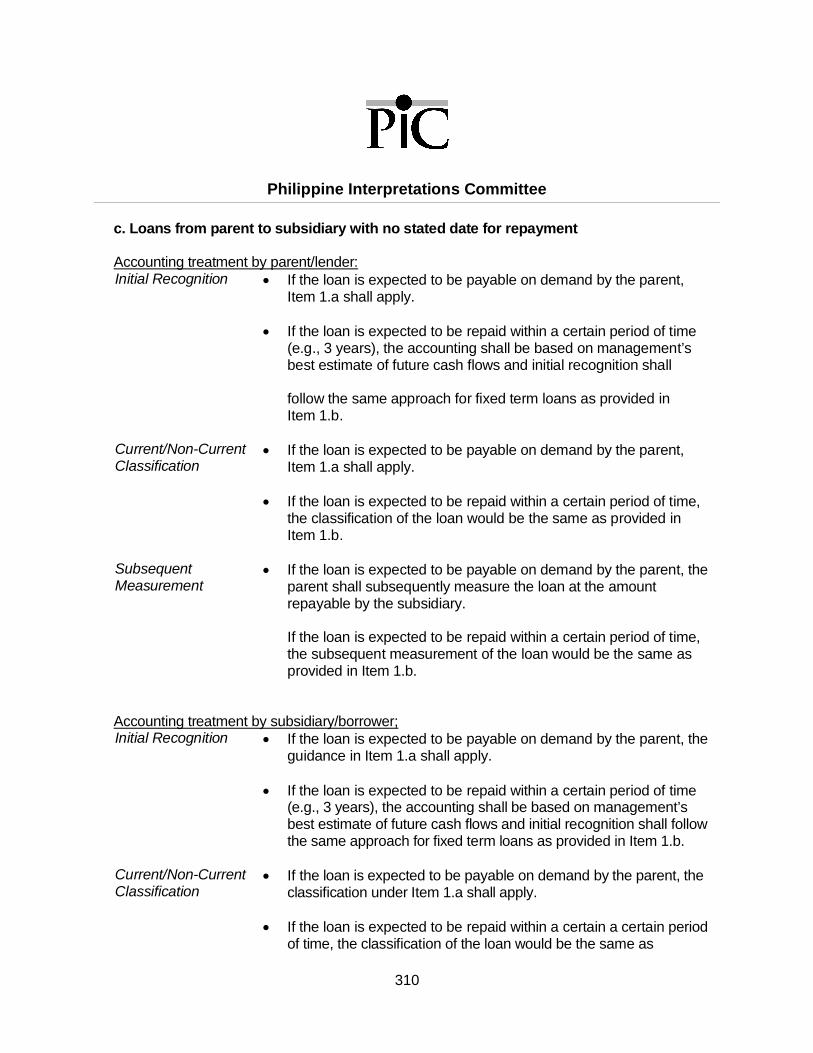

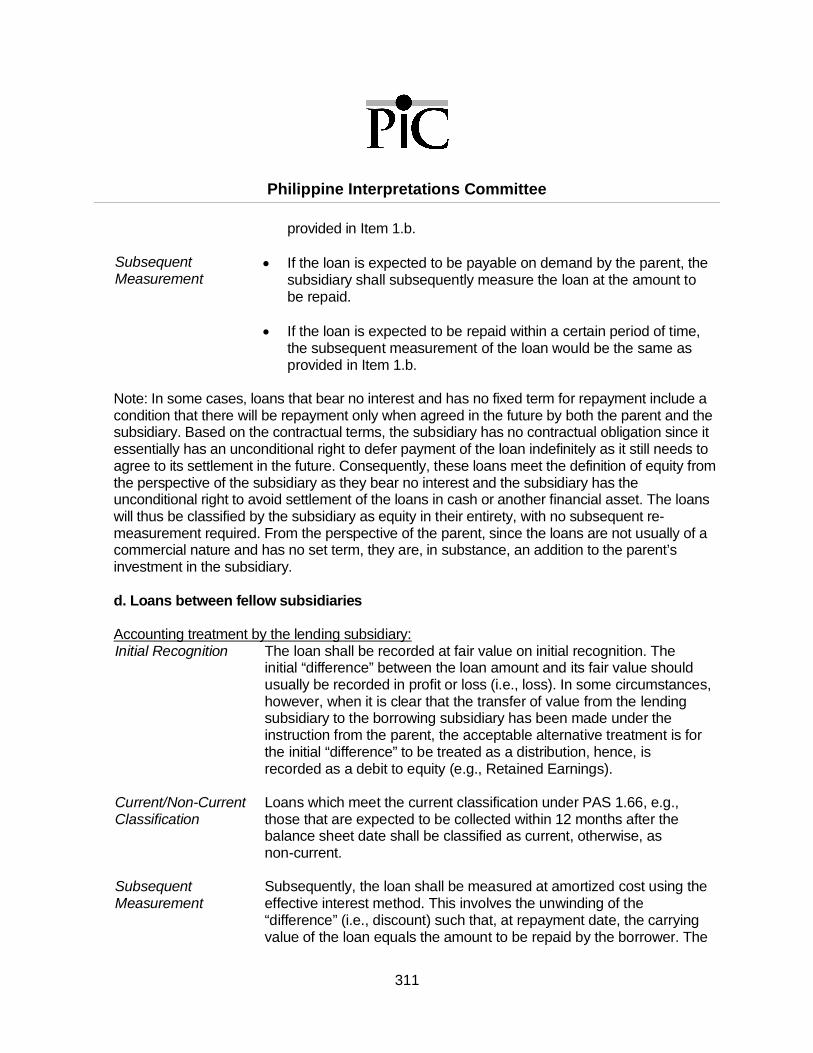

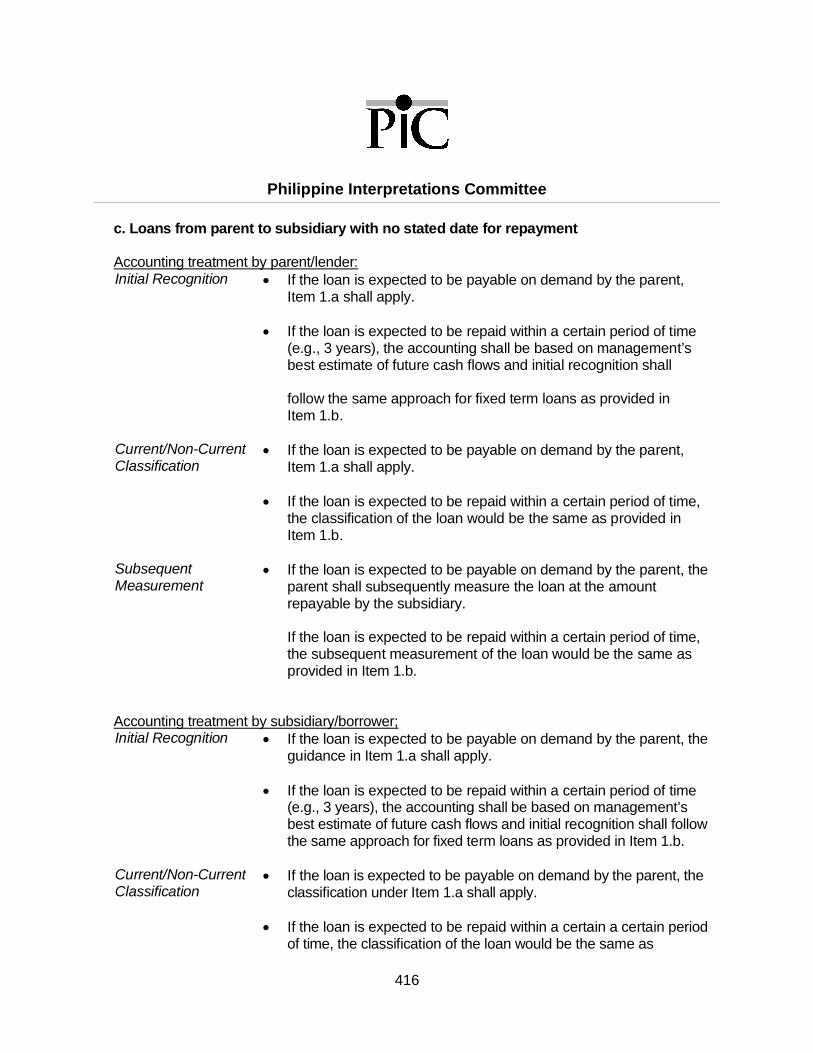

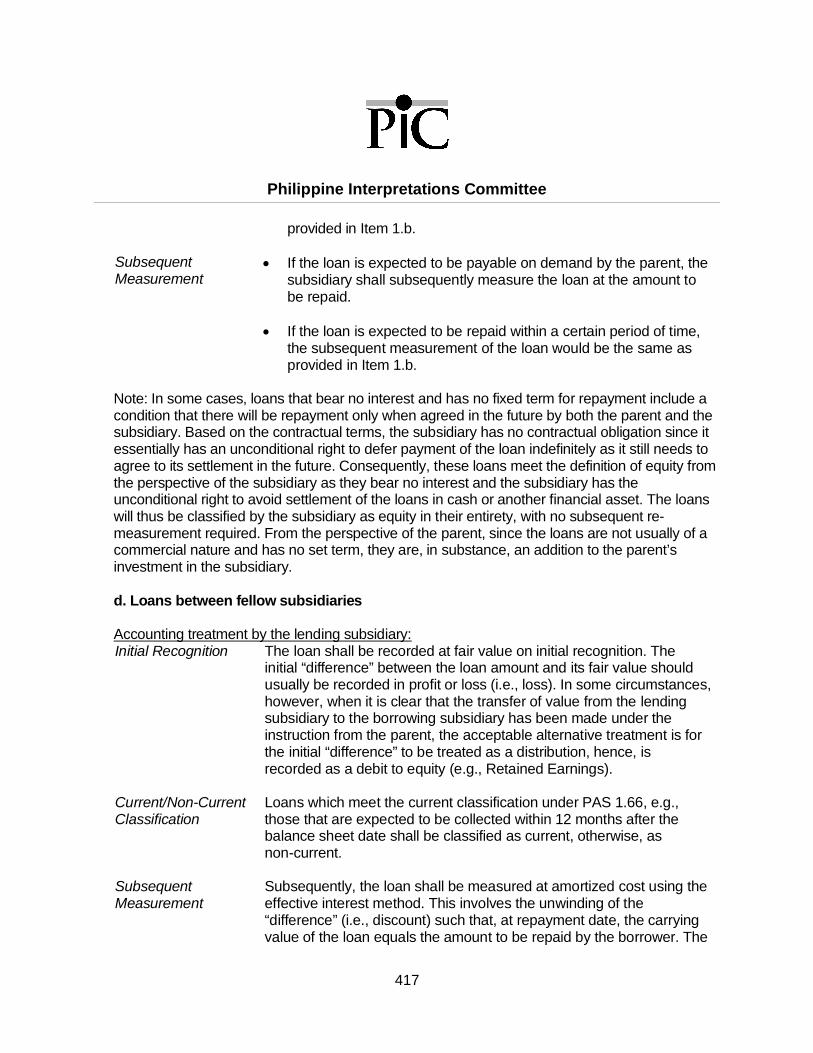

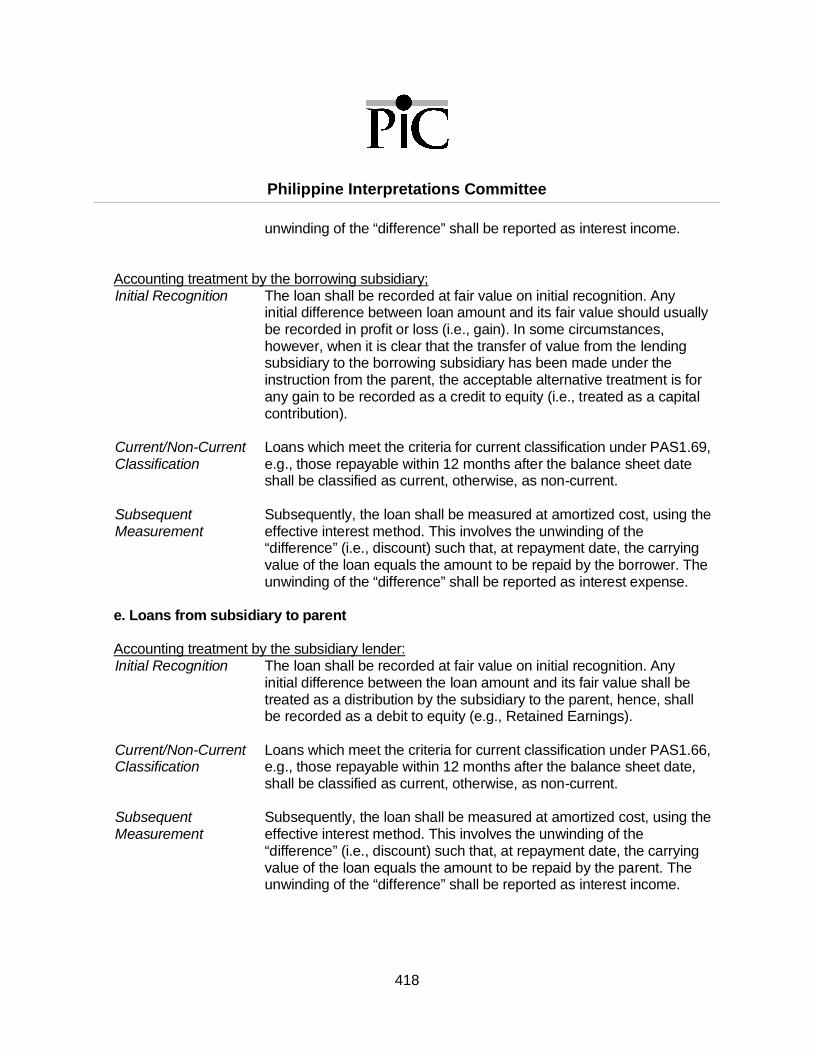

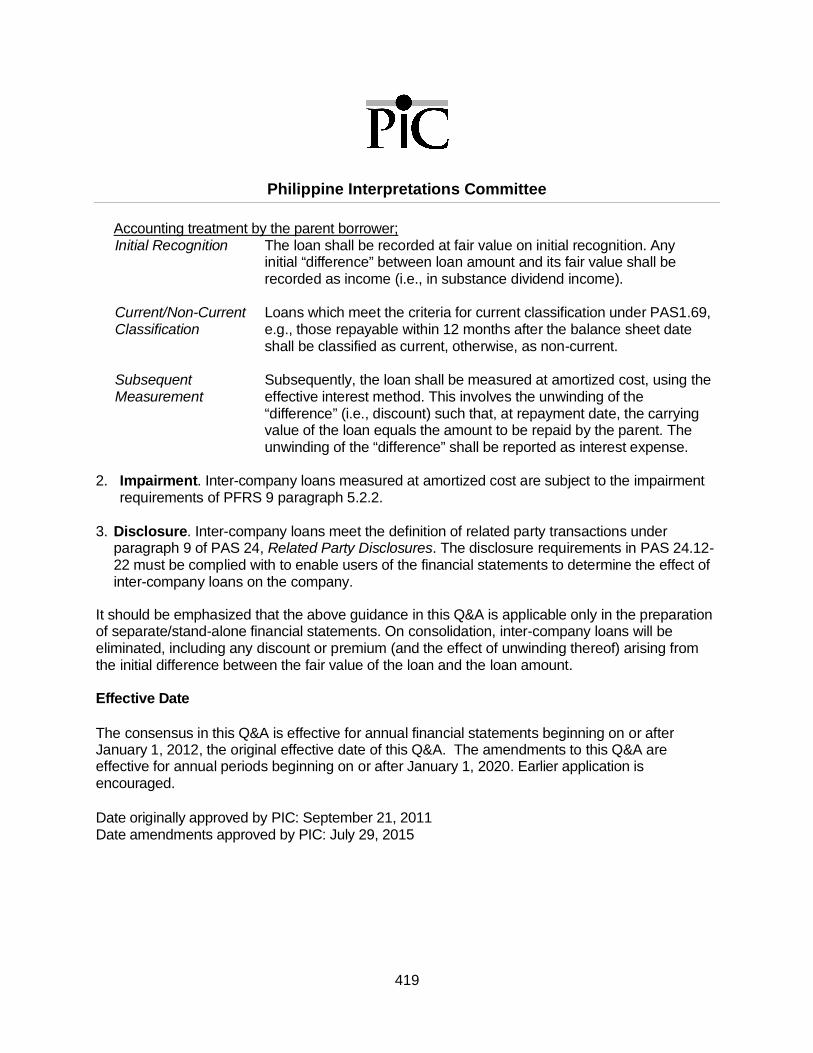

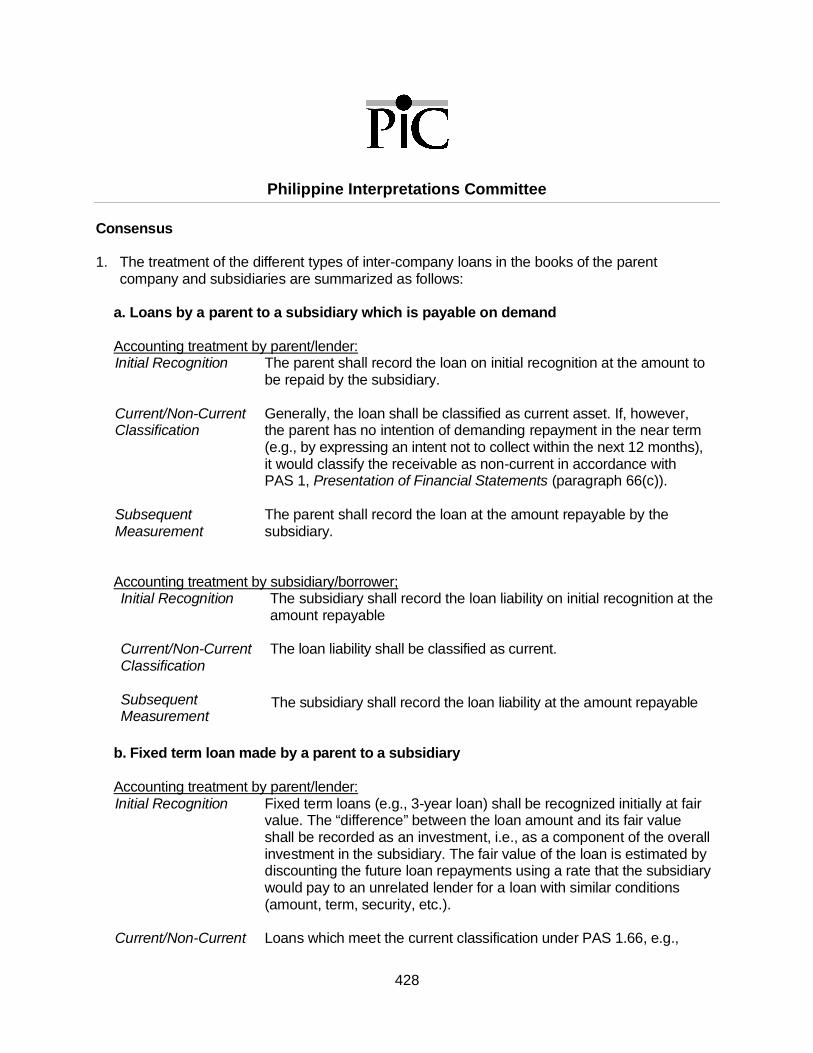

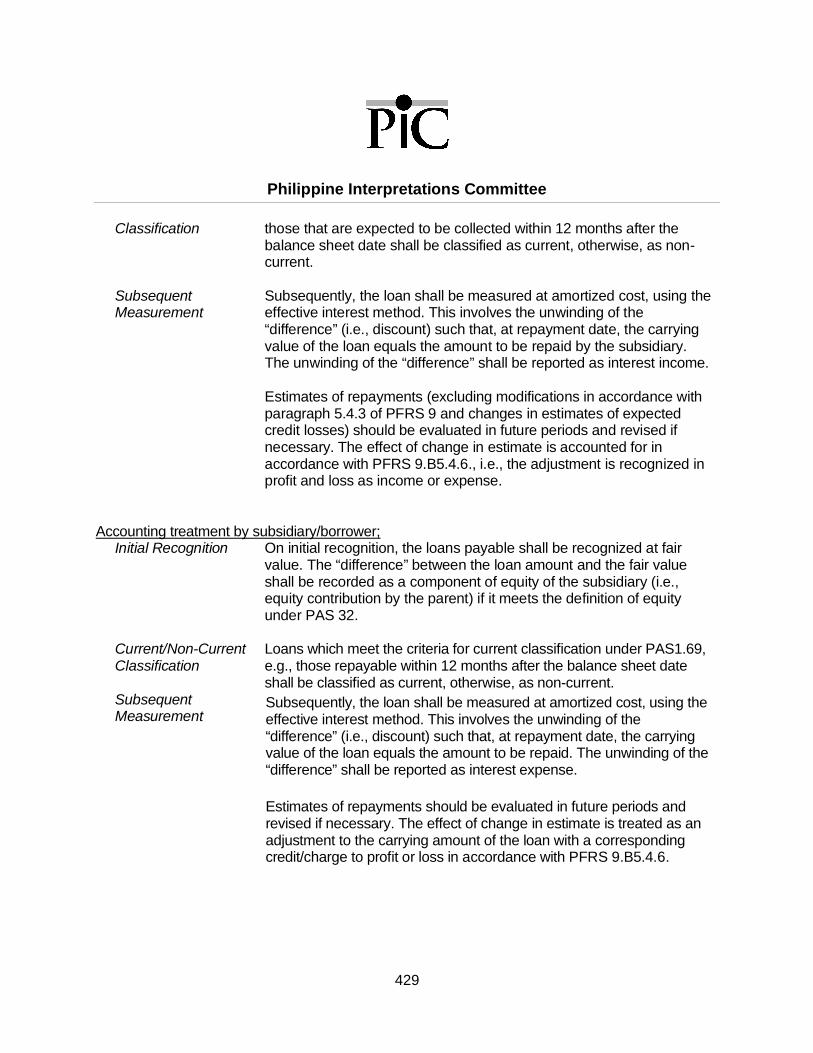

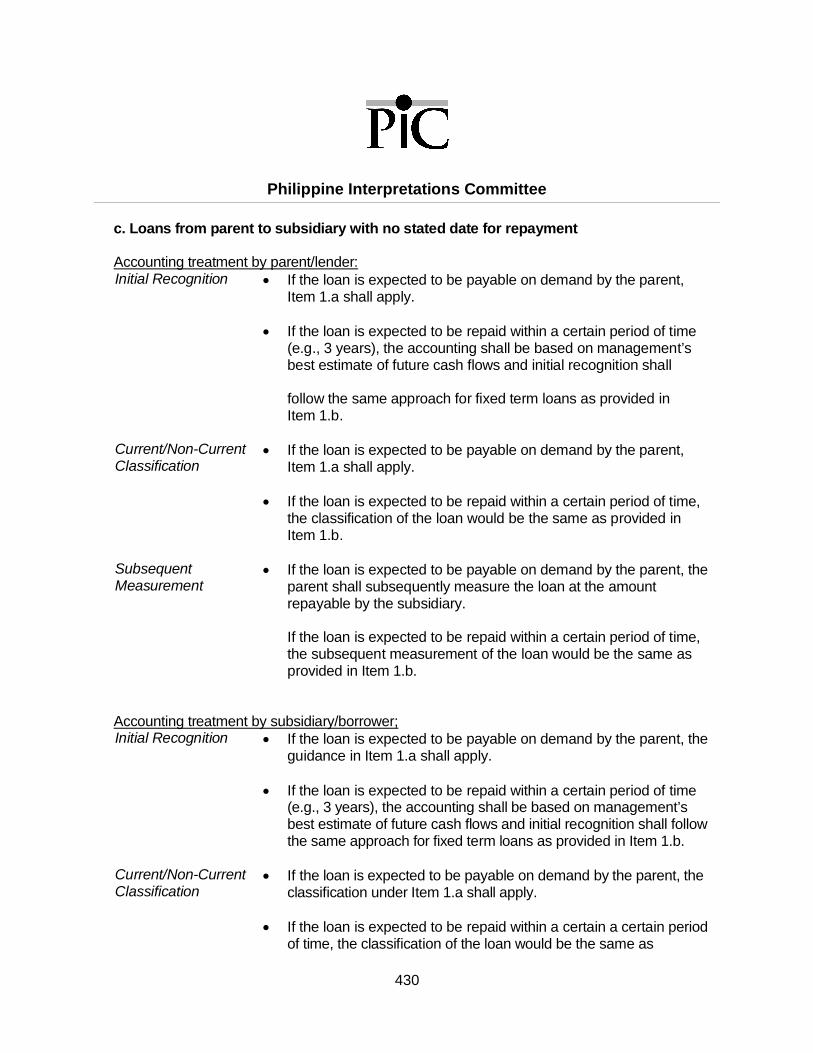

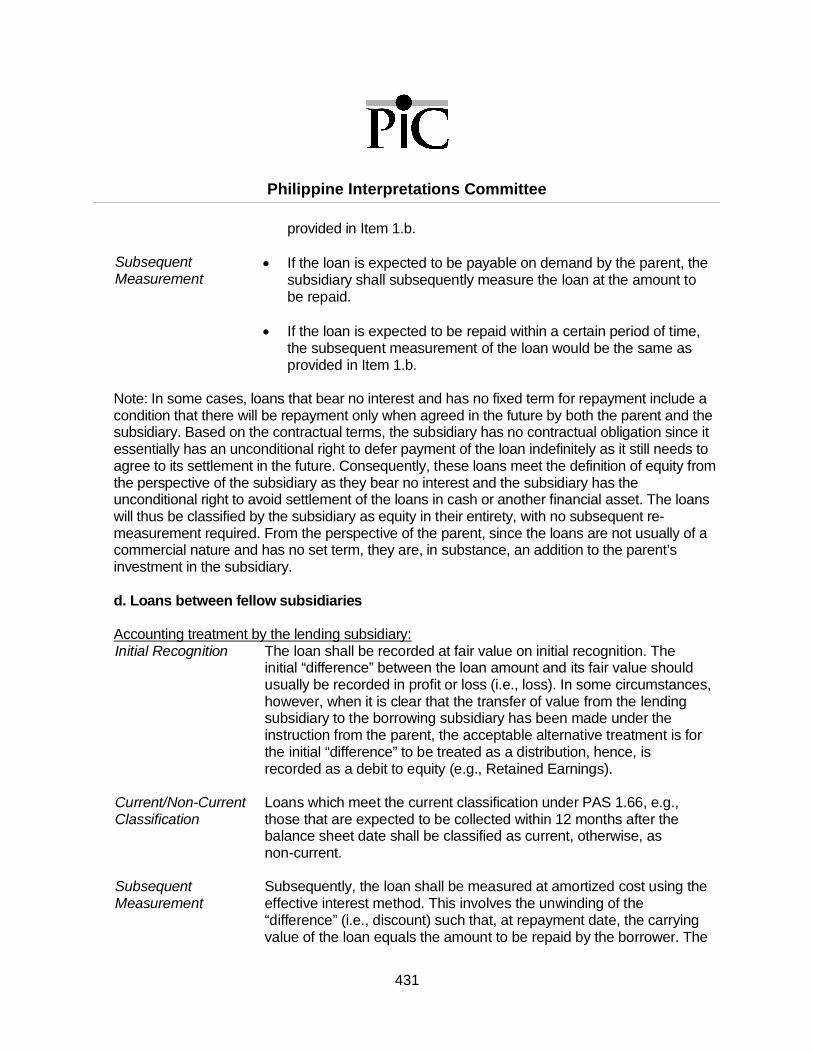

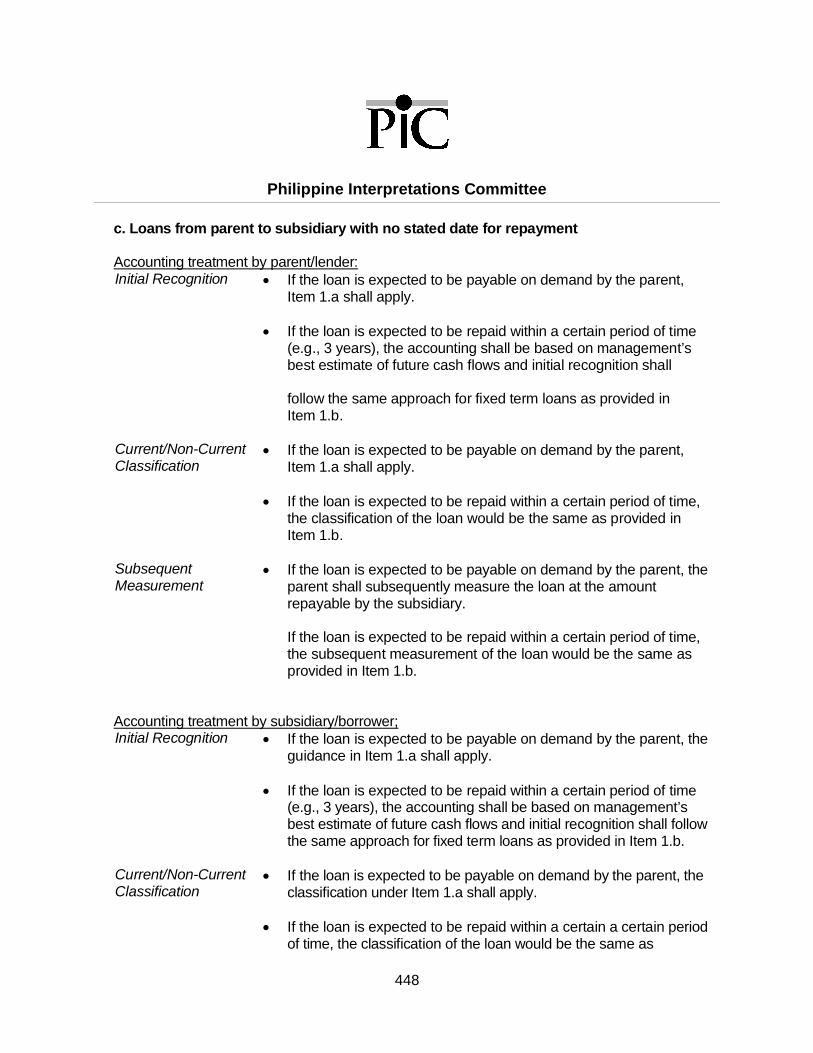

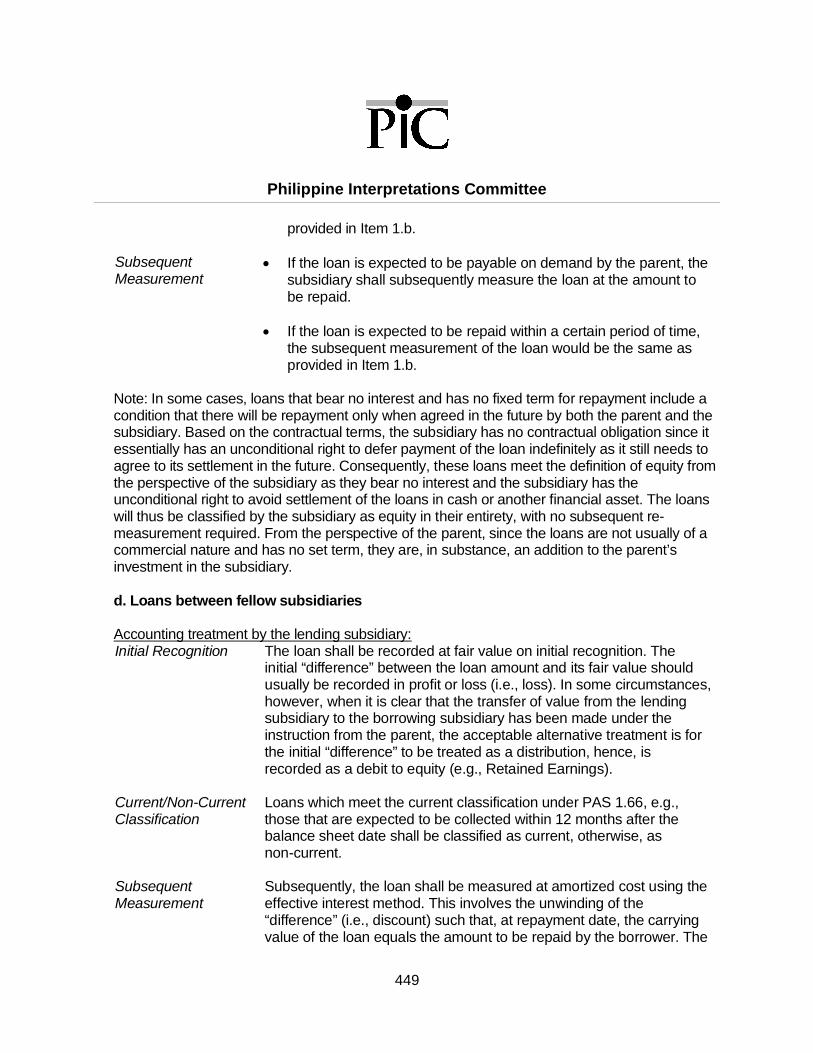

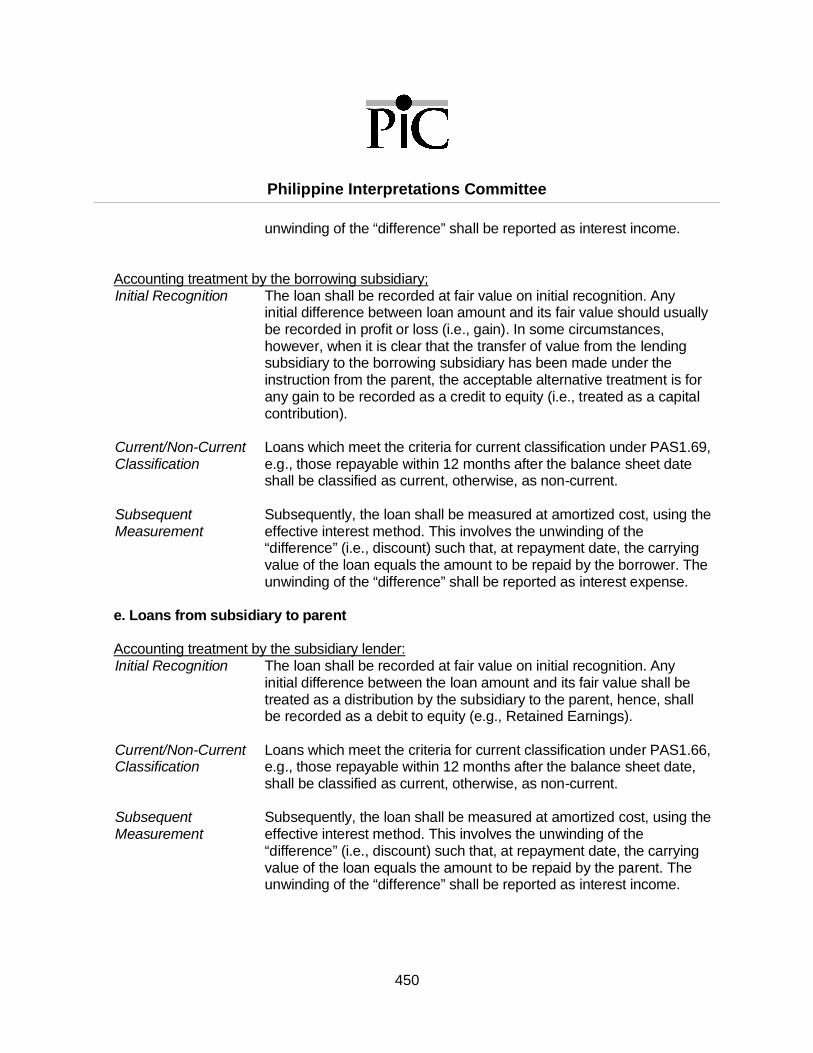

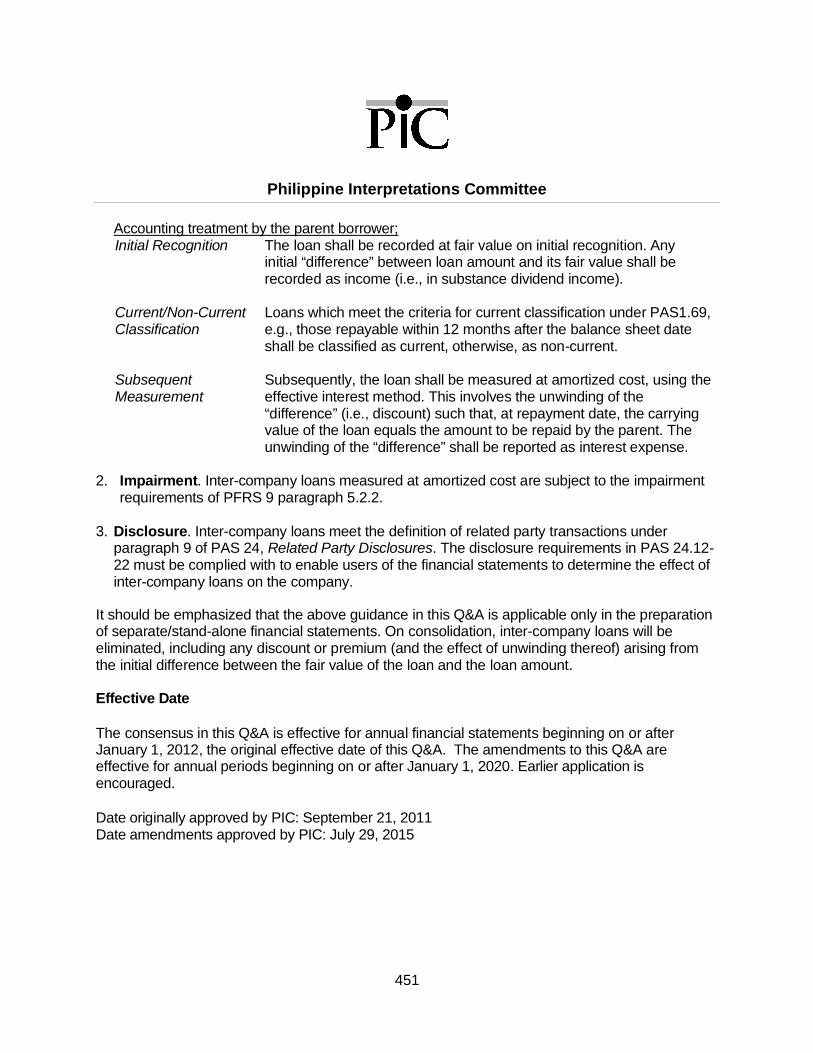

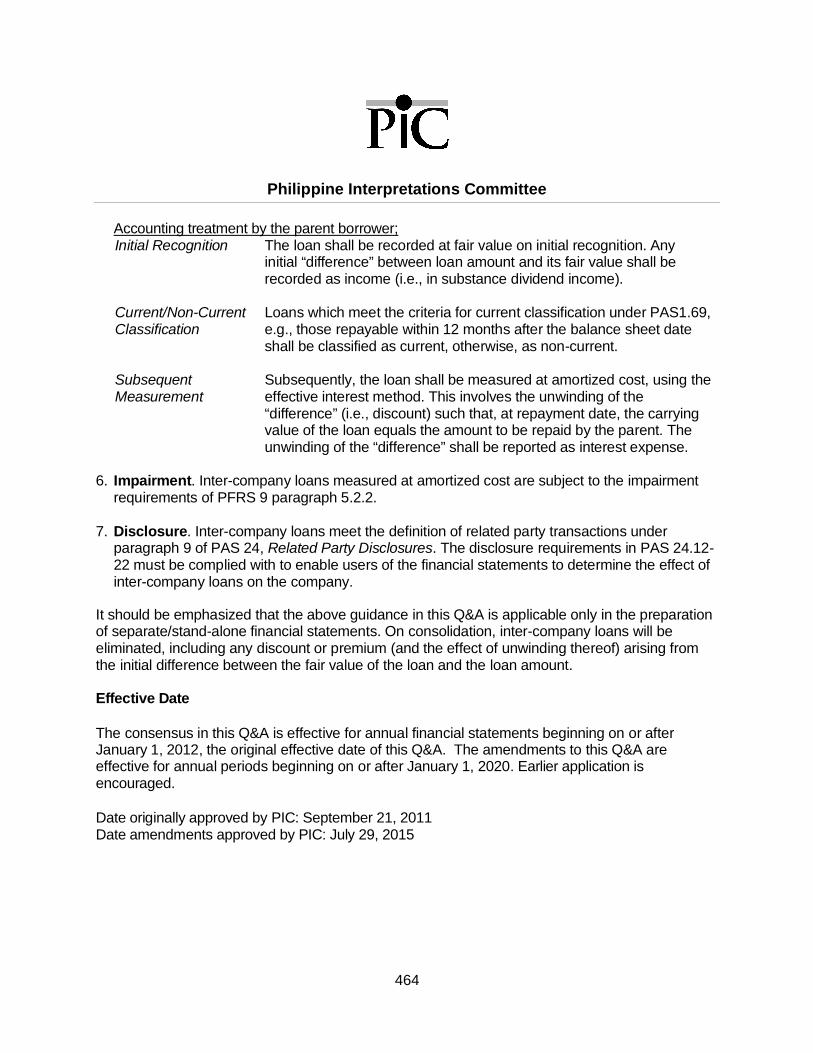

Q&A No. 2011 - 03 (amended June 2020): Accounting for Inter-company Loans...............62

PFRS 10, Consolidated Financial Statements .......................................................................71

Q&A No. 2006 – 02 (amended May 2017): PFRS 10.4(a) – Clarification of criteria forexemption from presenting consolidated financial statements ............................................71

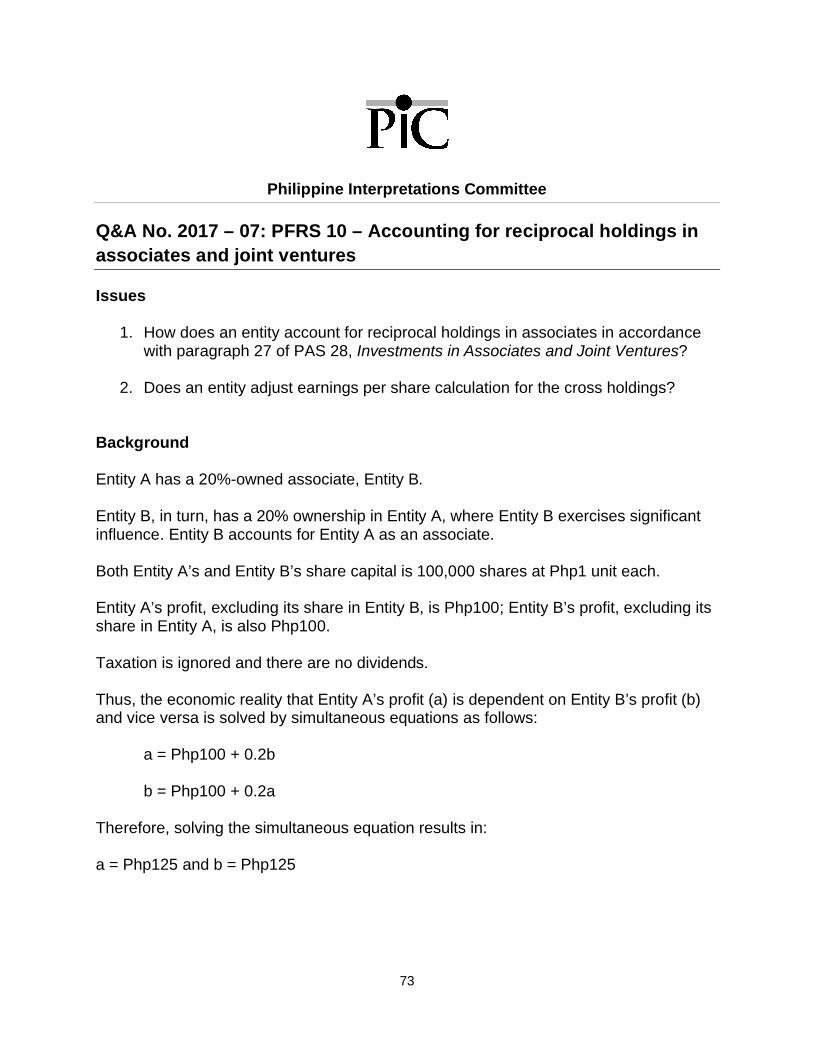

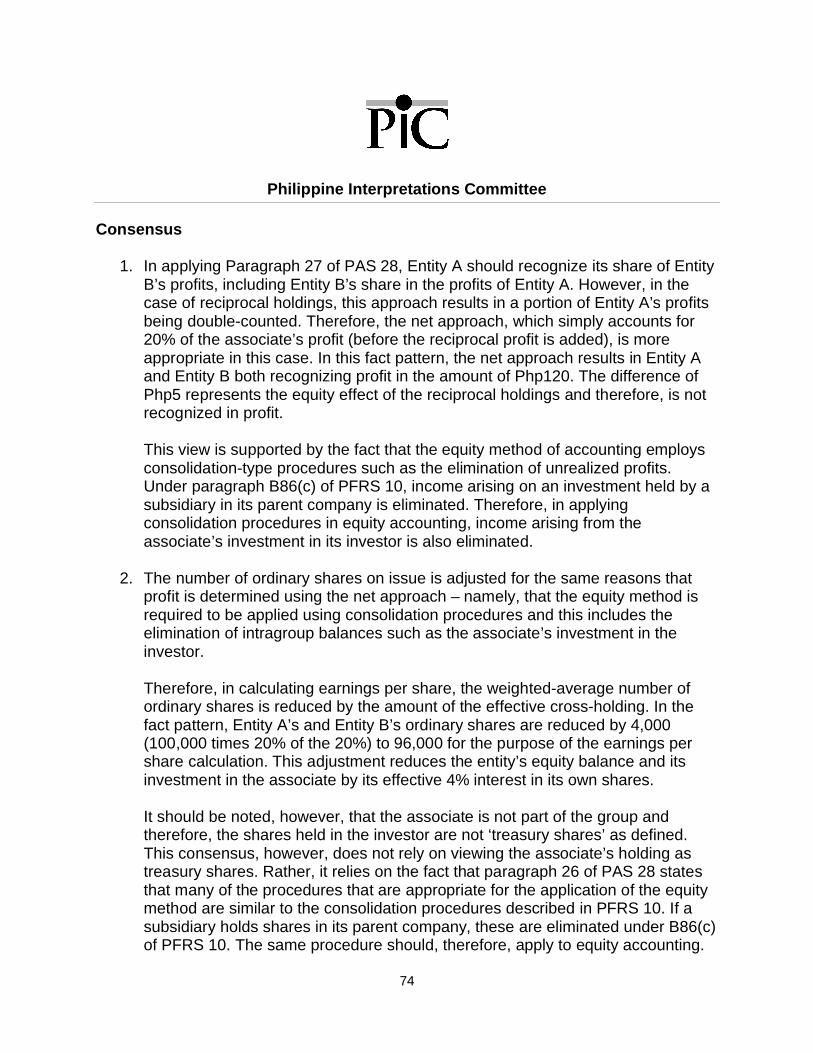

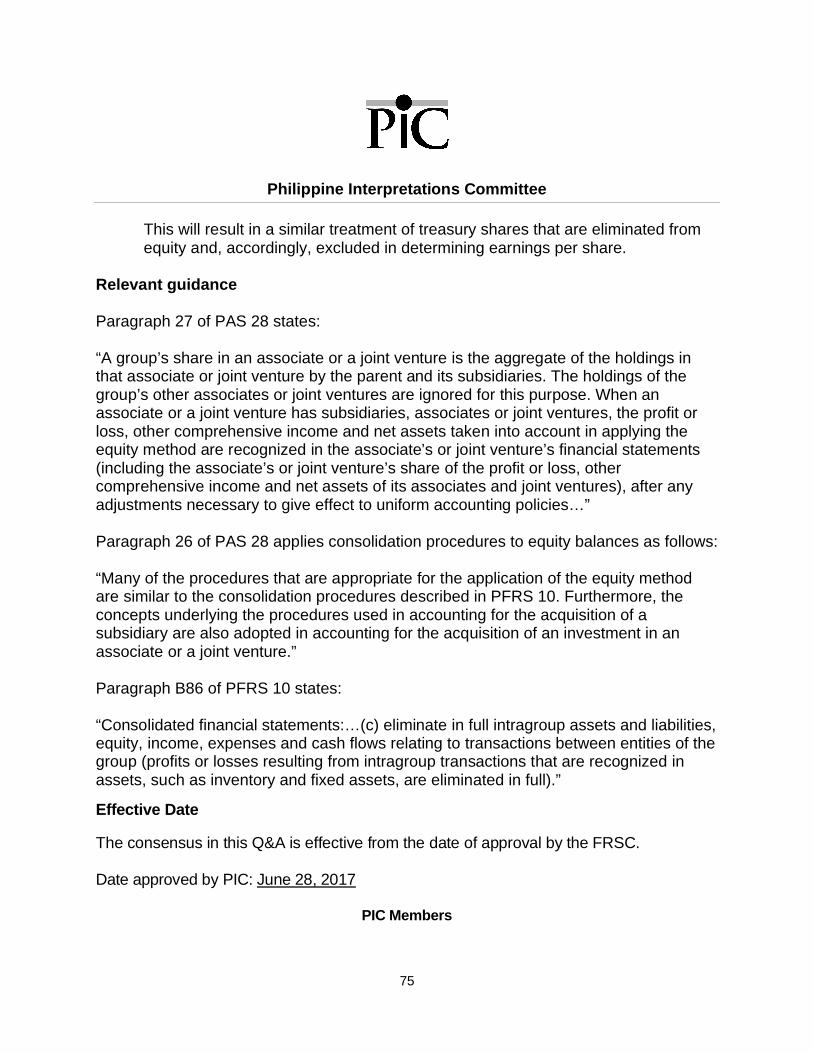

Q&A No. 2017 – 07: PFRS 10 – Accounting for reciprocal holdings in associates and jointventures .............................................................................................................................73

Q&A No. 2017 – 08 (amended June 2020): PFRS 10 – Requirement to prepareconsolidated financial statements where an entity disposes of its single investment in asubsidiary, associate or joint venture .................................................................................77

Q&A No. 2017 – 11: PFRS 10 and PAS 32 - Transaction costs incurred to acquireoutstanding non-controlling interest or to sell non-controlling interest without a loss ofcontrol ................................................................................................................................81

Q&A No. 2018 - 08: PFRS 10 and PFRS 3 - Accounting for the acquisition of a non-whollyowned subsidiary that is not a business .............................................................................86

PFRS 13, Fair Value Measurement .......................................................................................90

Q&A No. 2011 - 03 (amended June 2020): Accounting for Inter-company Loans...............90

Q&A No. 2018 - 03: PFRS 13, PAS 16 and PAS 36 - Fair value of property, plant andequipment and depreciated replacement cost ....................................................................99

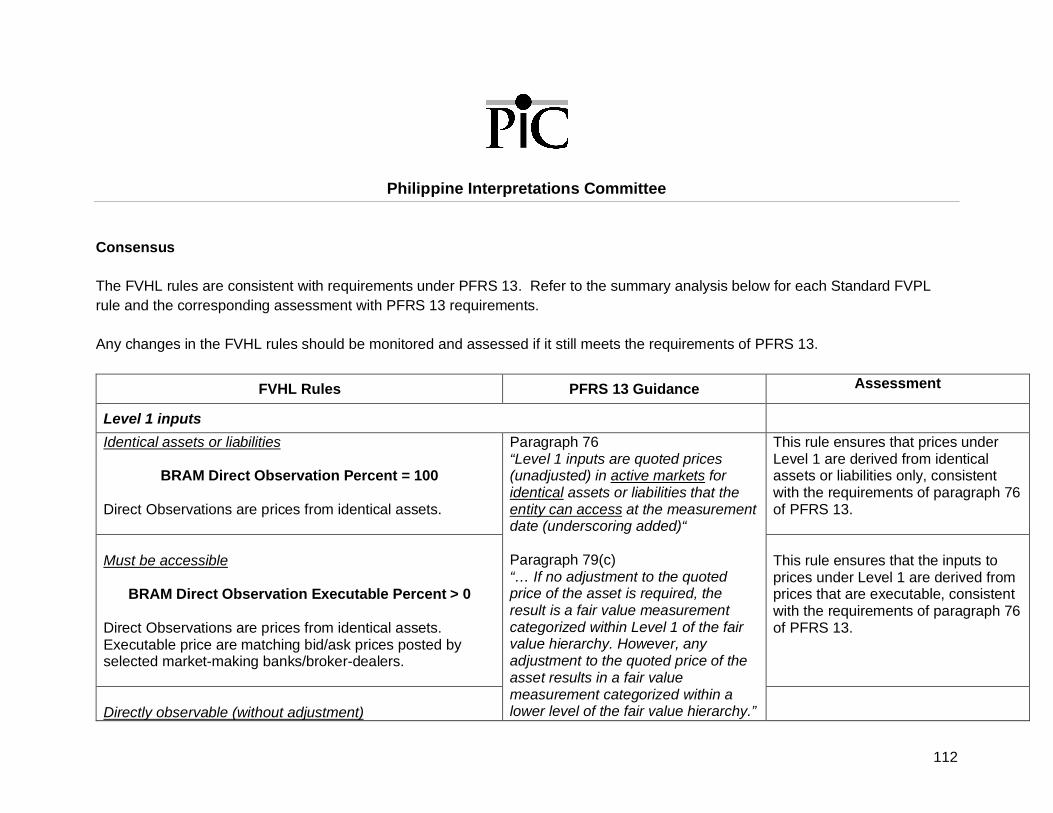

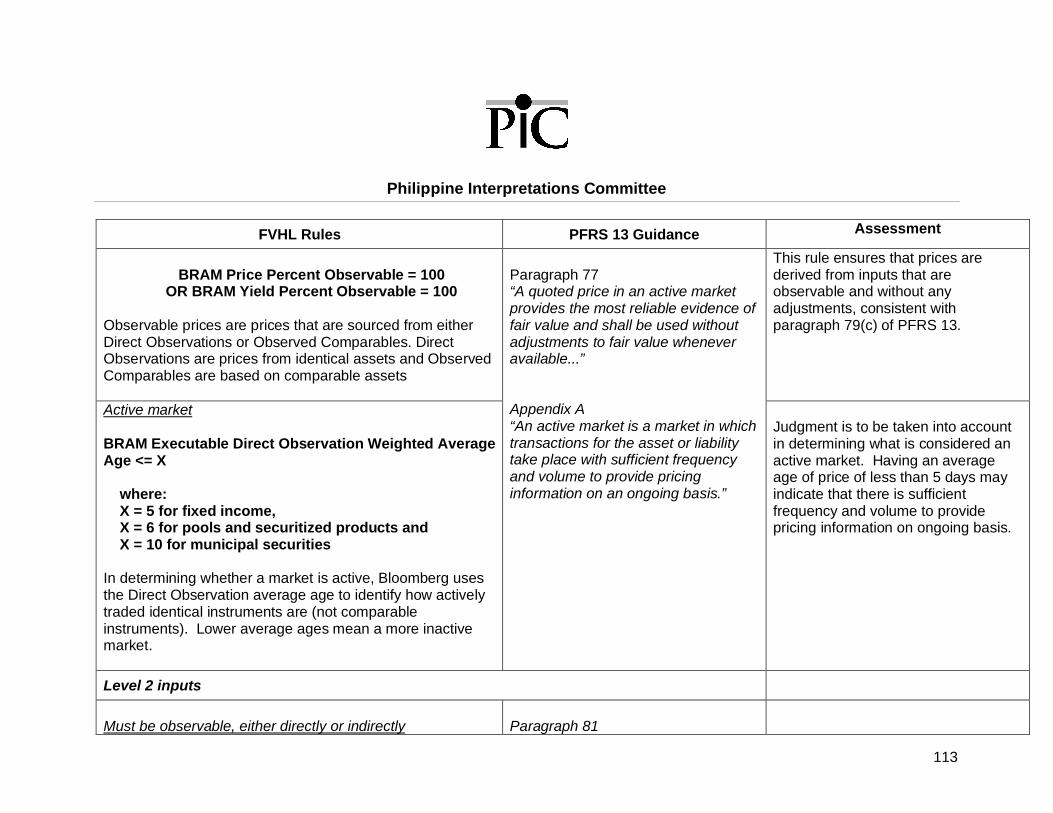

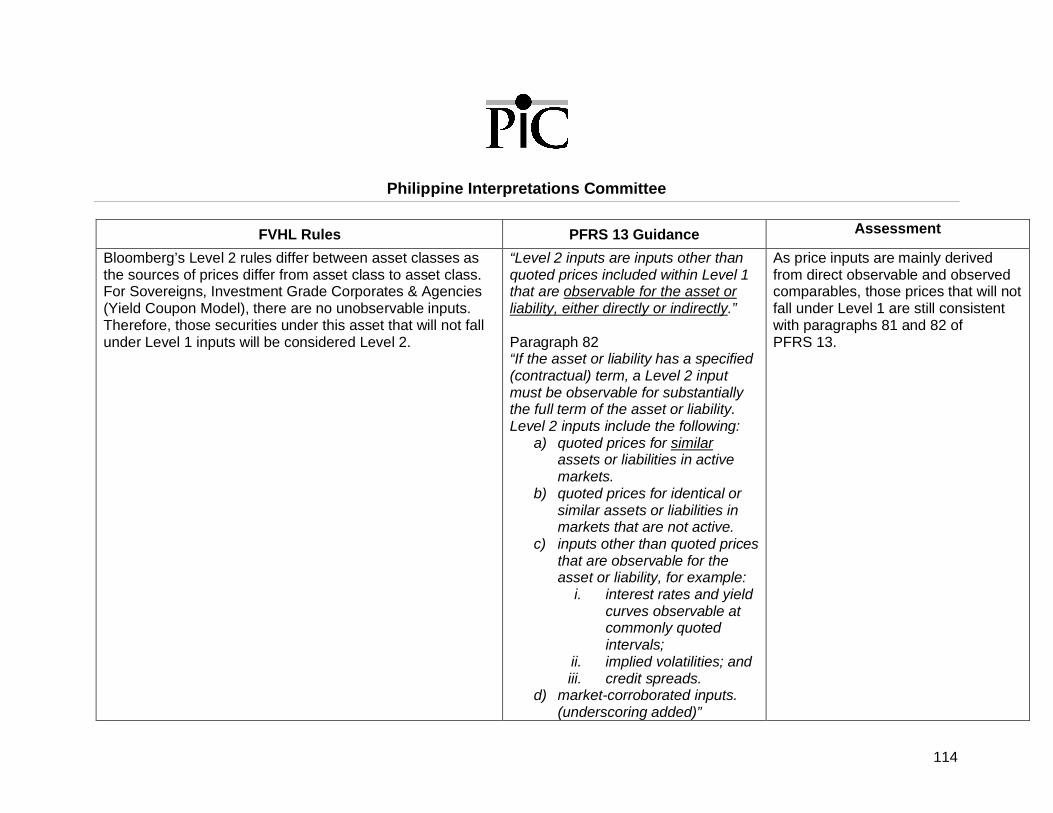

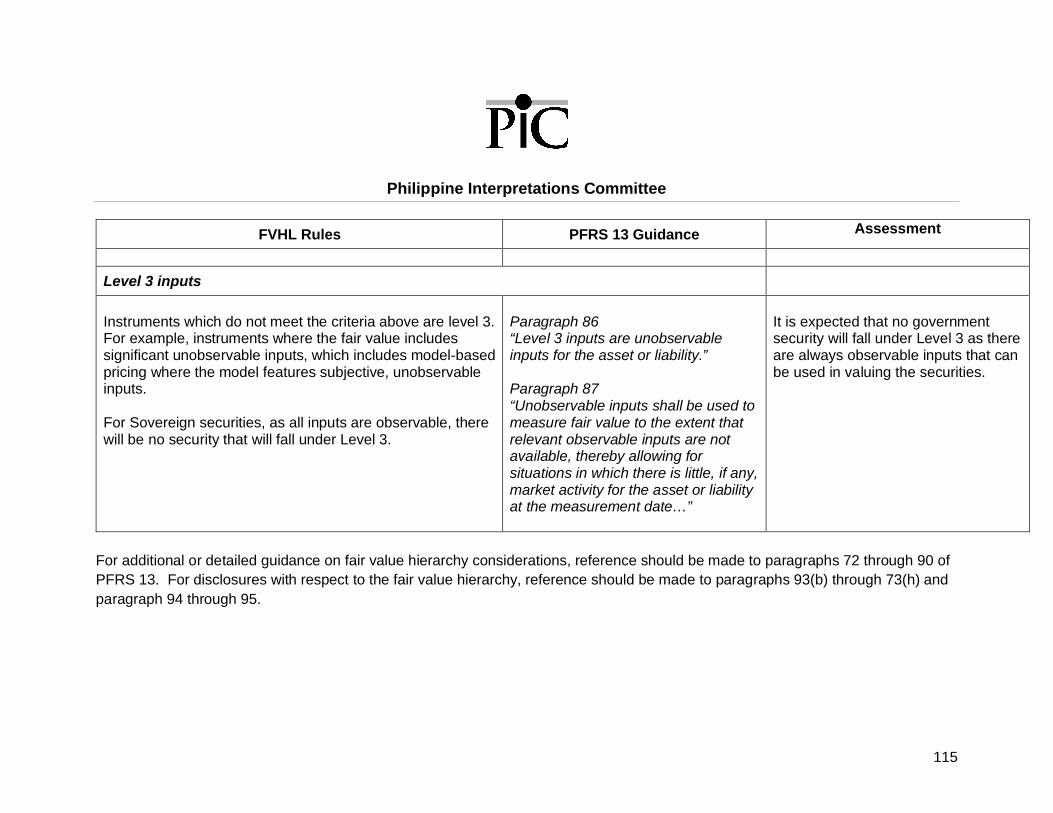

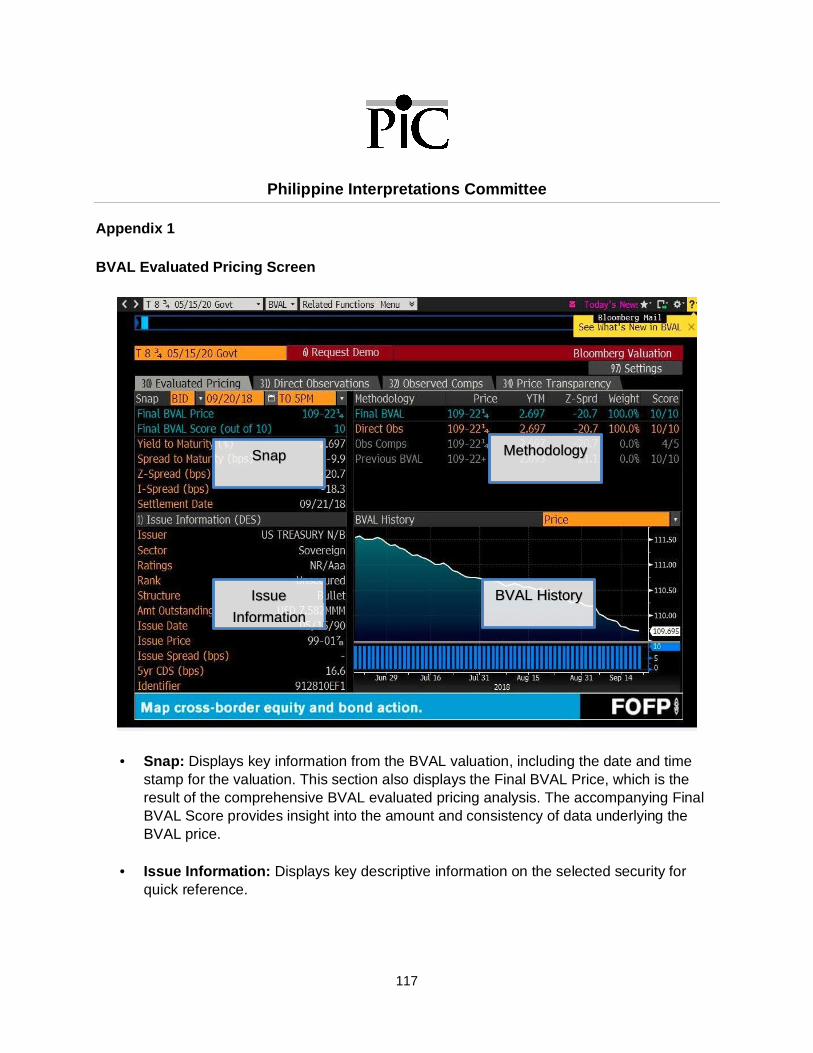

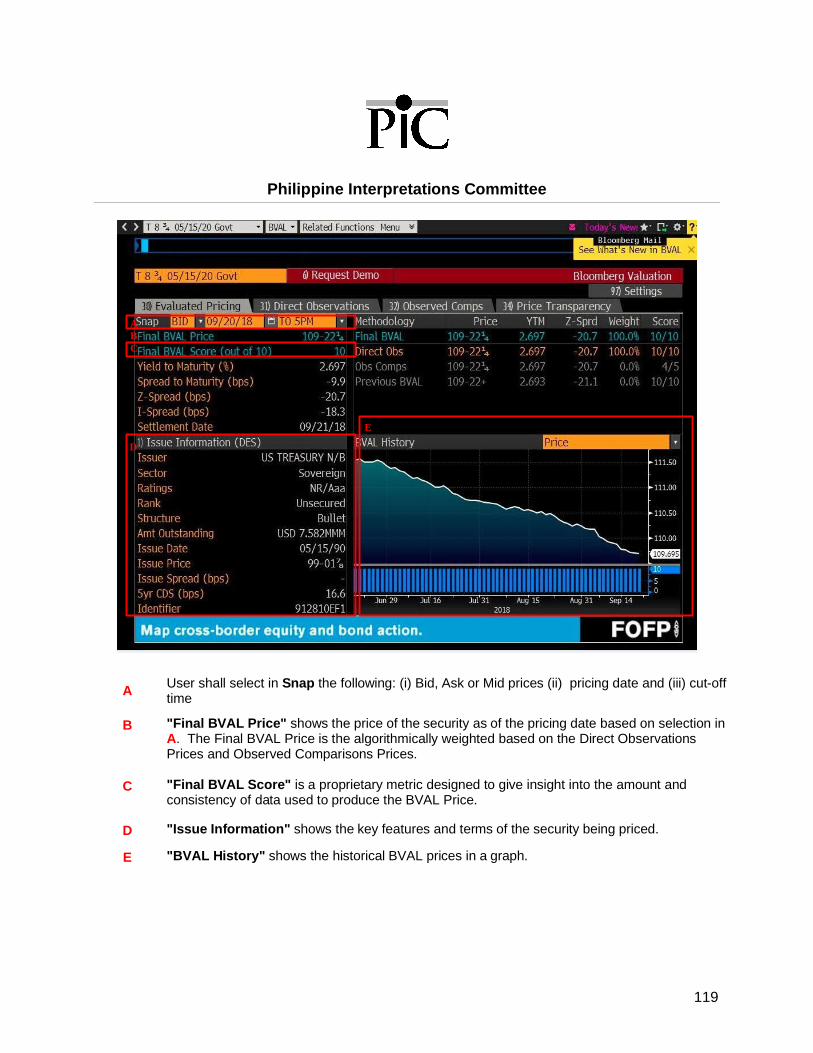

Q&A No. 2018 - 16: PFRS 13 - Level of fair value hierarchy of government securities usingBloomberg’s standard rule on fair value hierarchy............................................................ 103

PFRS 15, Revenue from Contracts with Customers ............................................................ 127

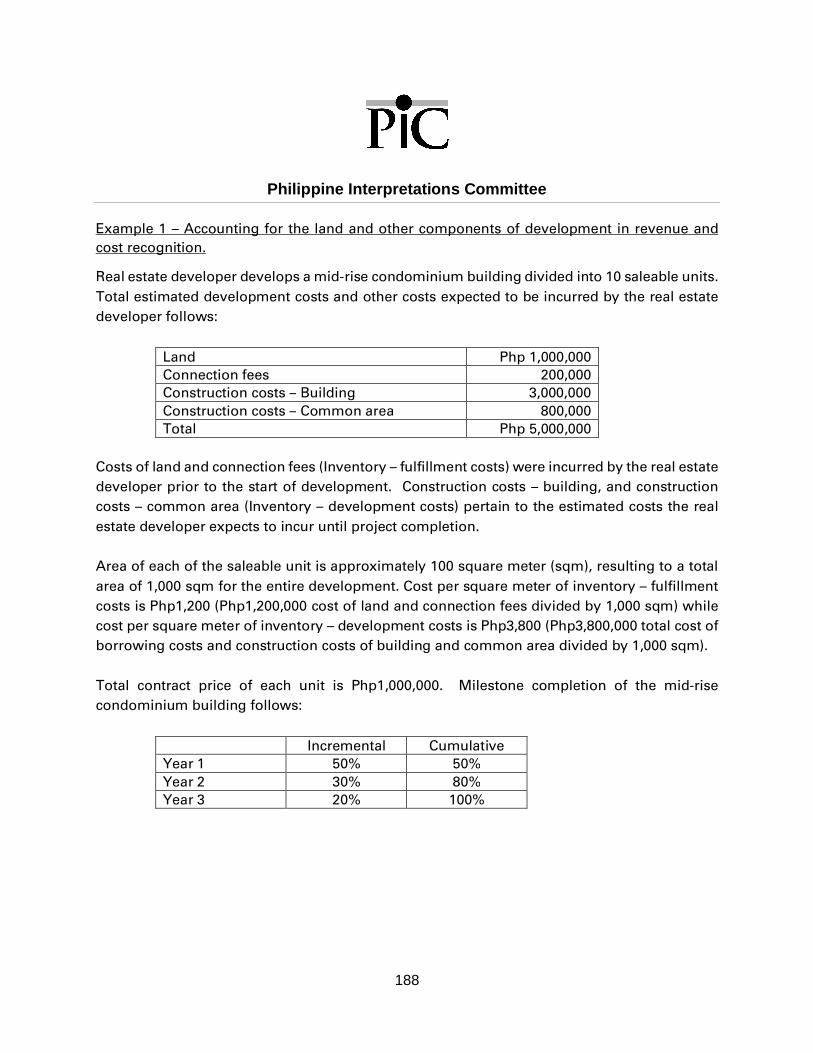

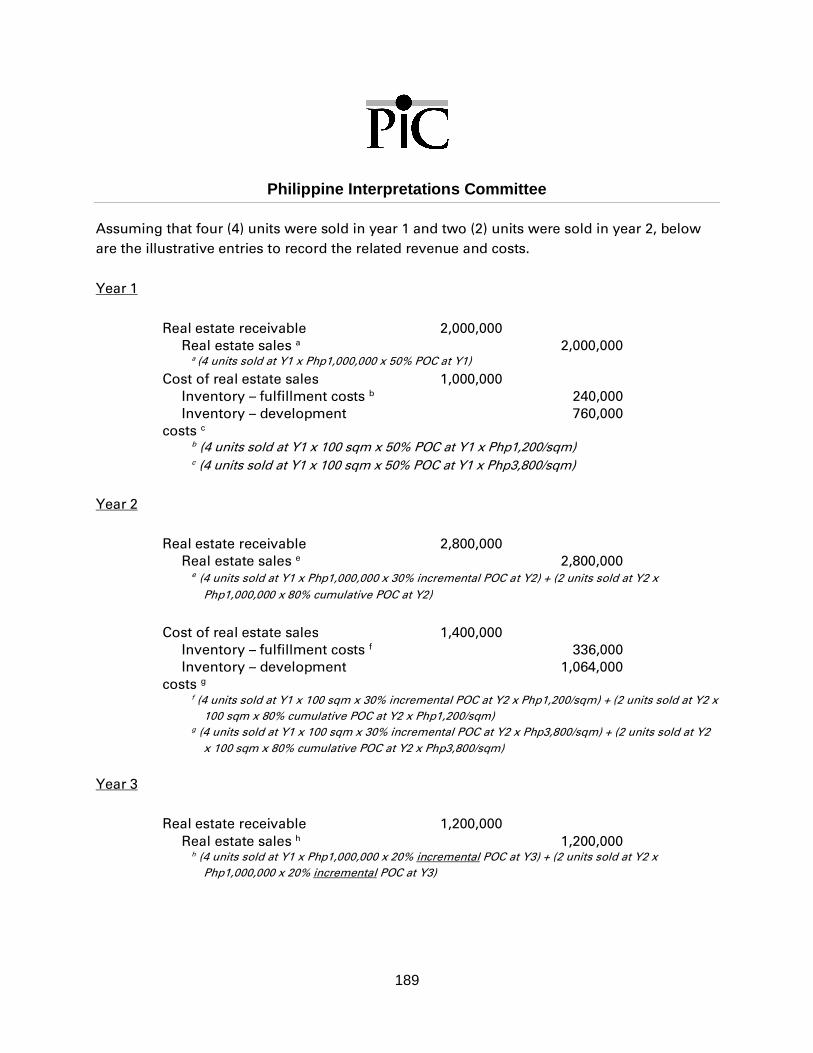

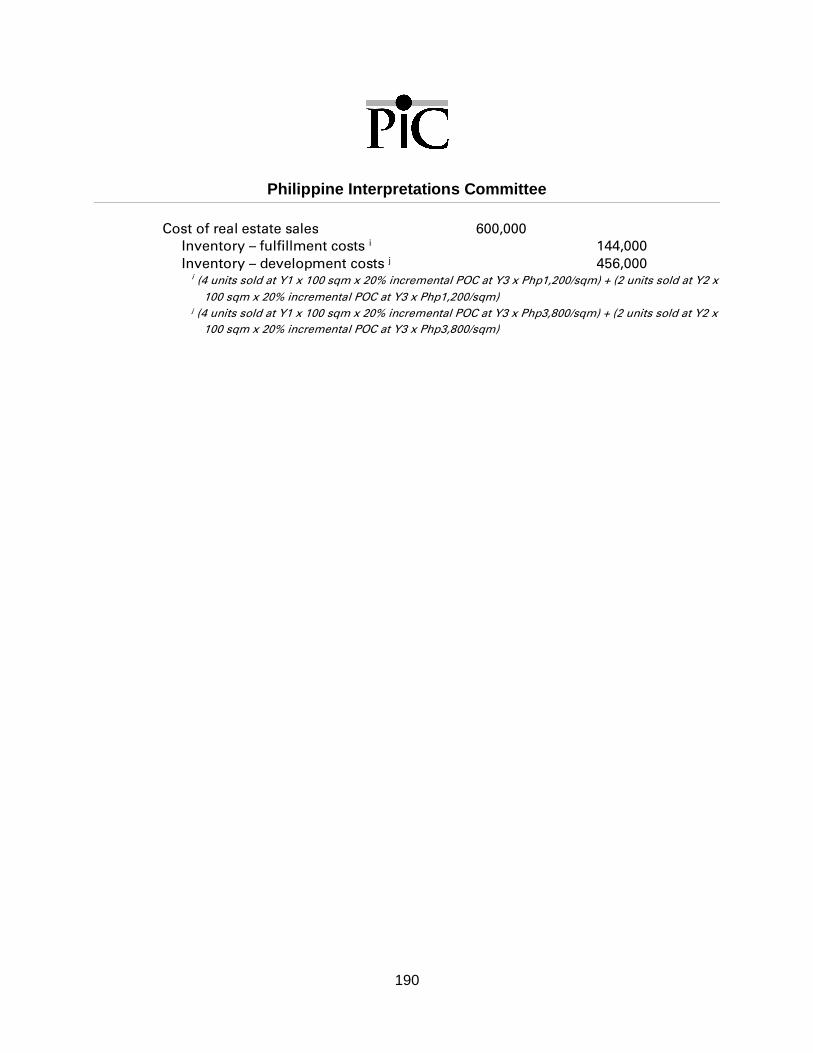

Q&A No. 2016 – 04: Application of PFRS 15 “Revenue from Contracts with Customers” onSale of Residential Properties under Pre-completion Contracts ....................................... 127

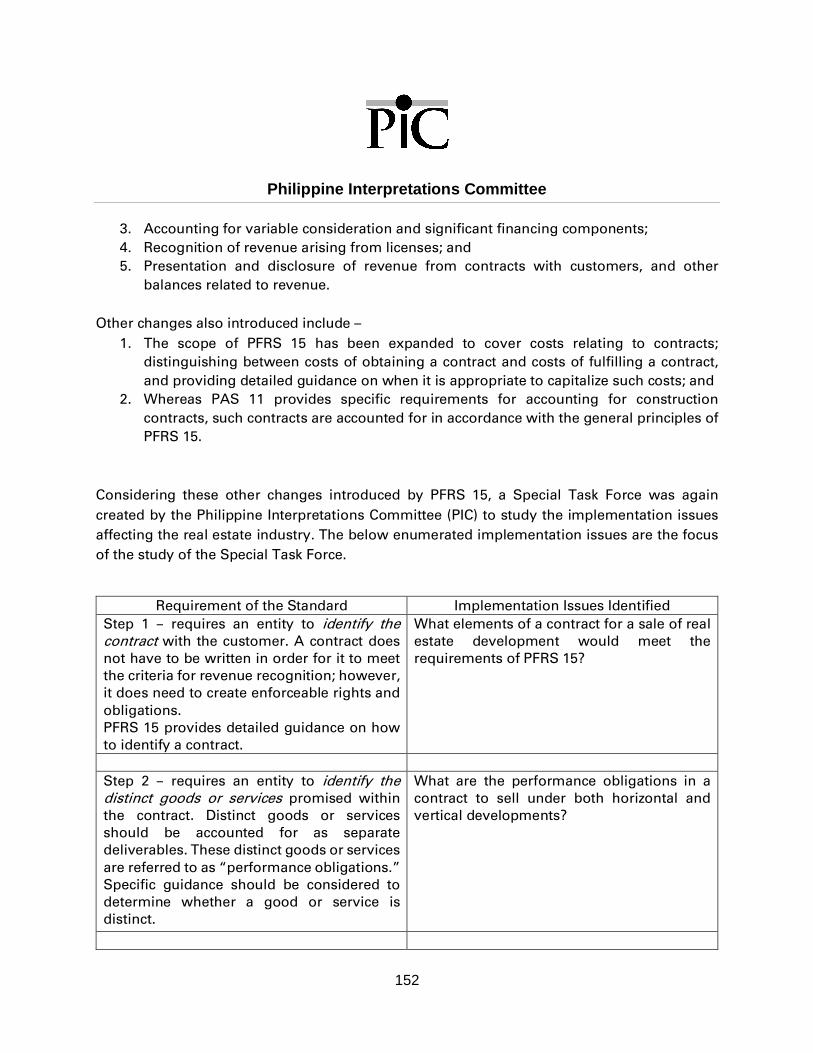

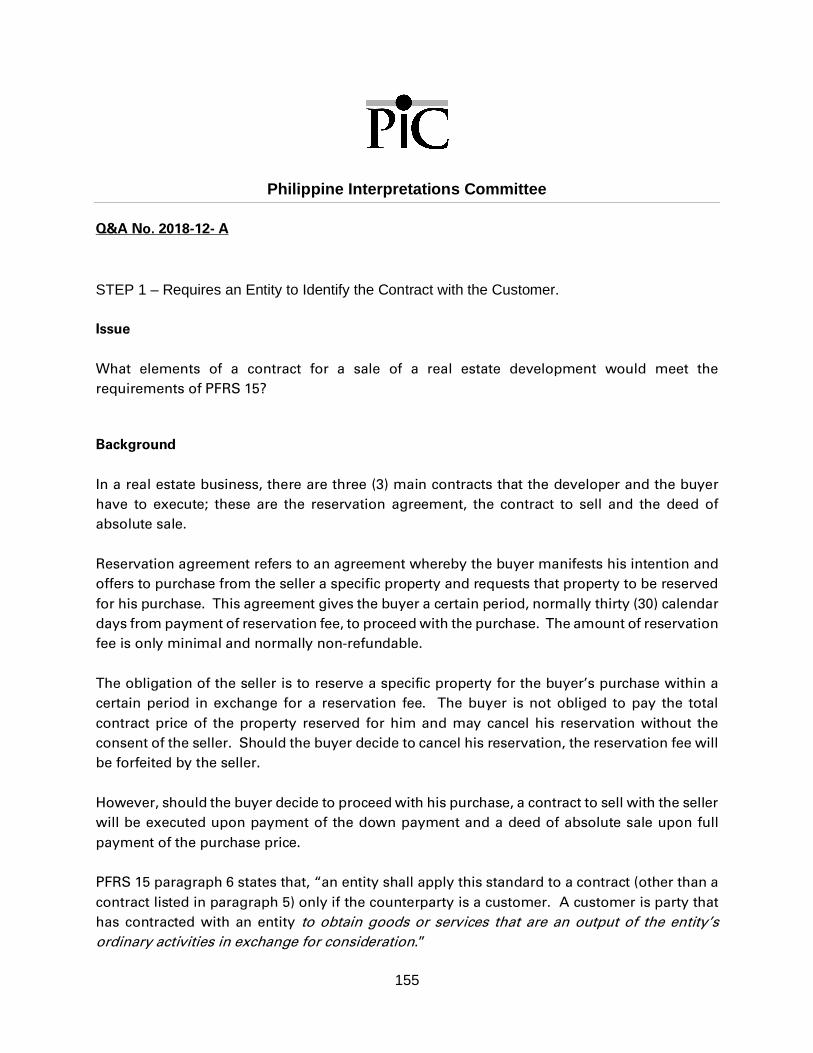

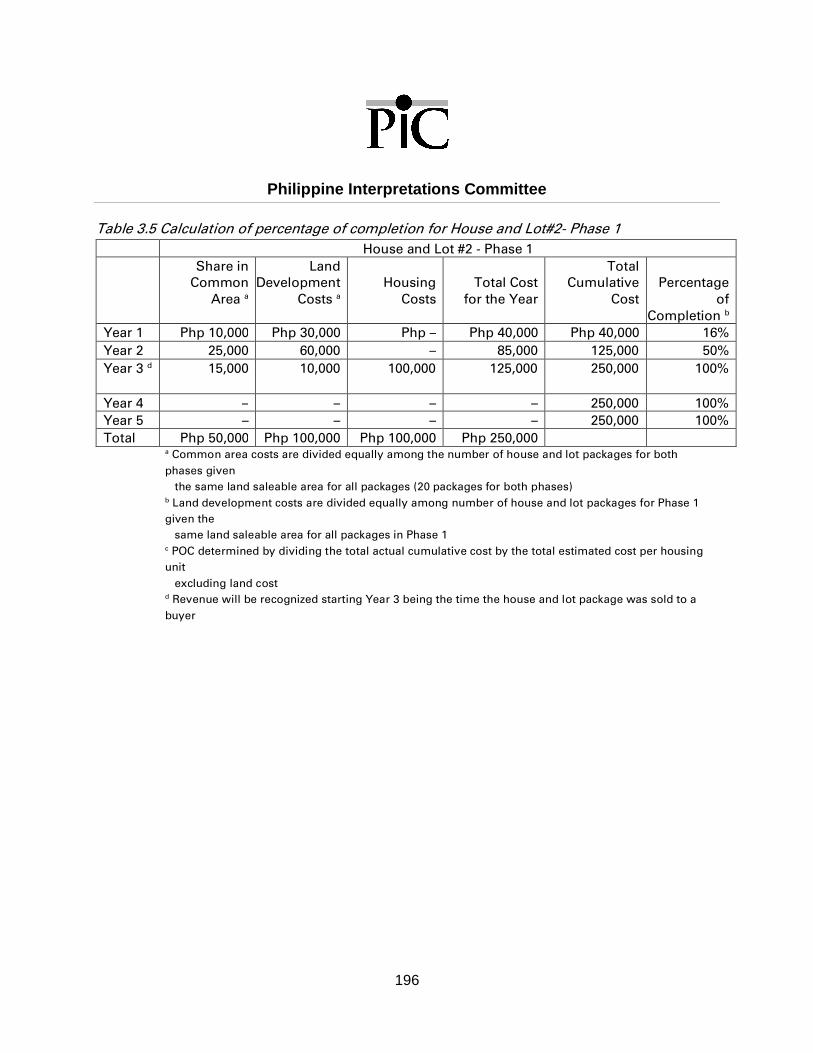

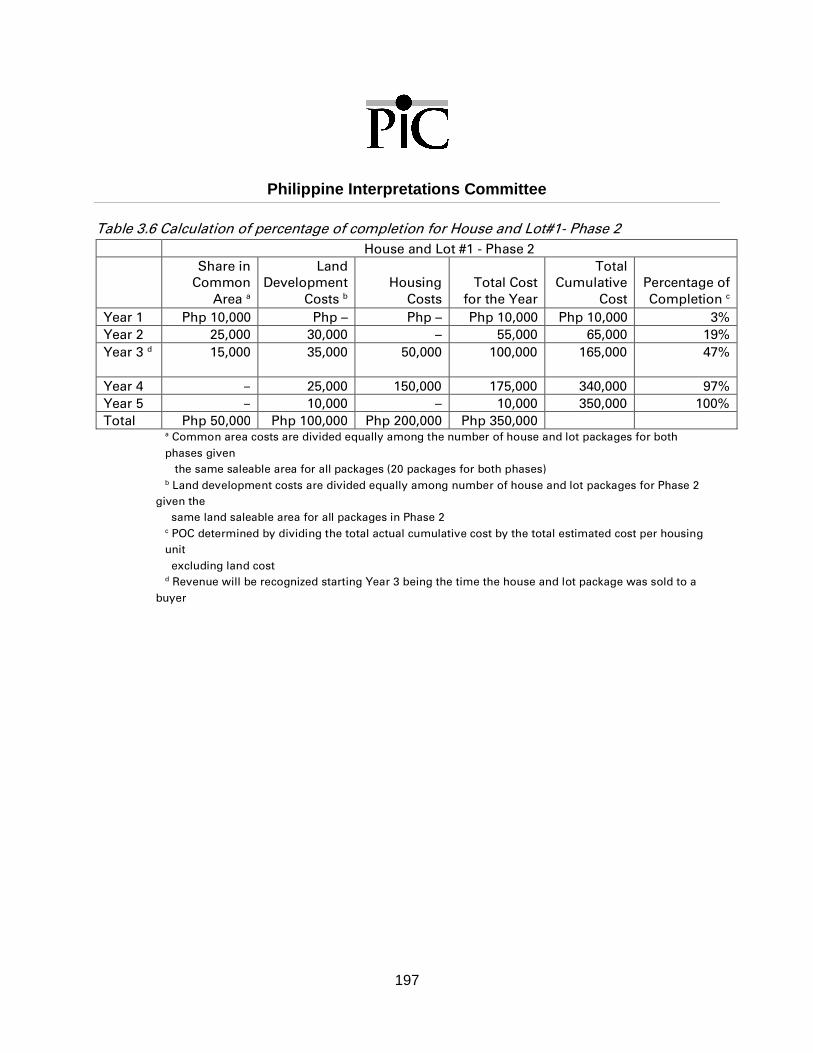

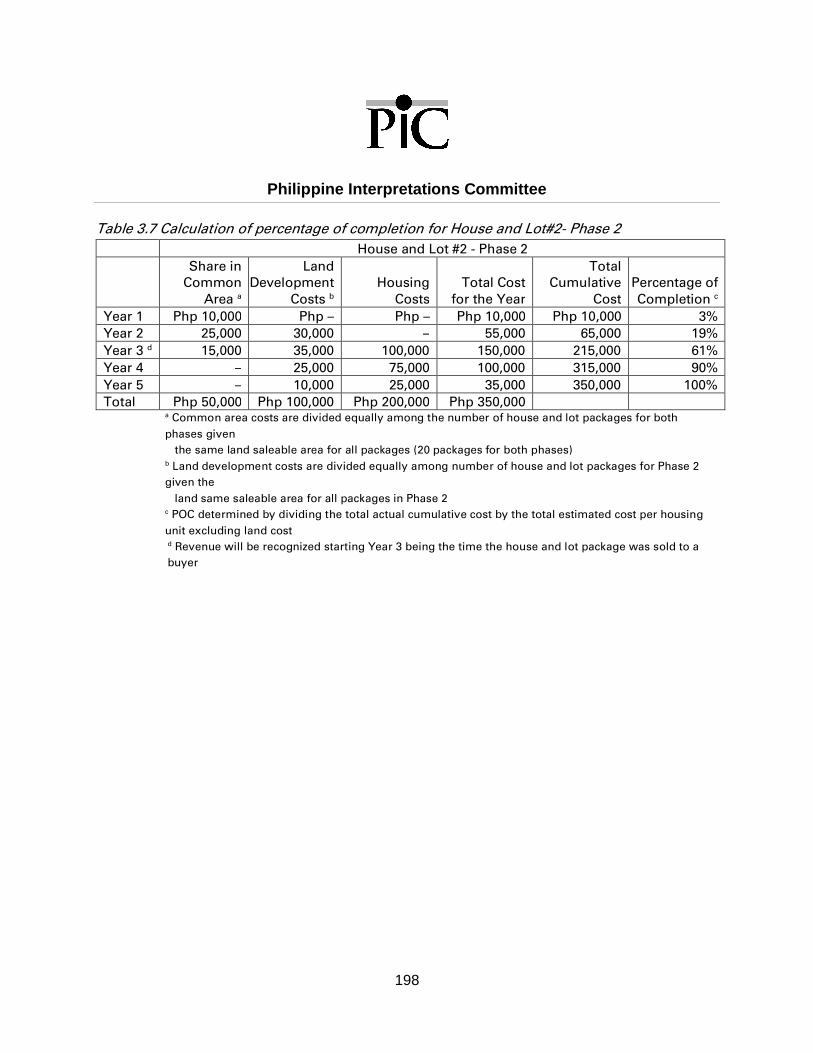

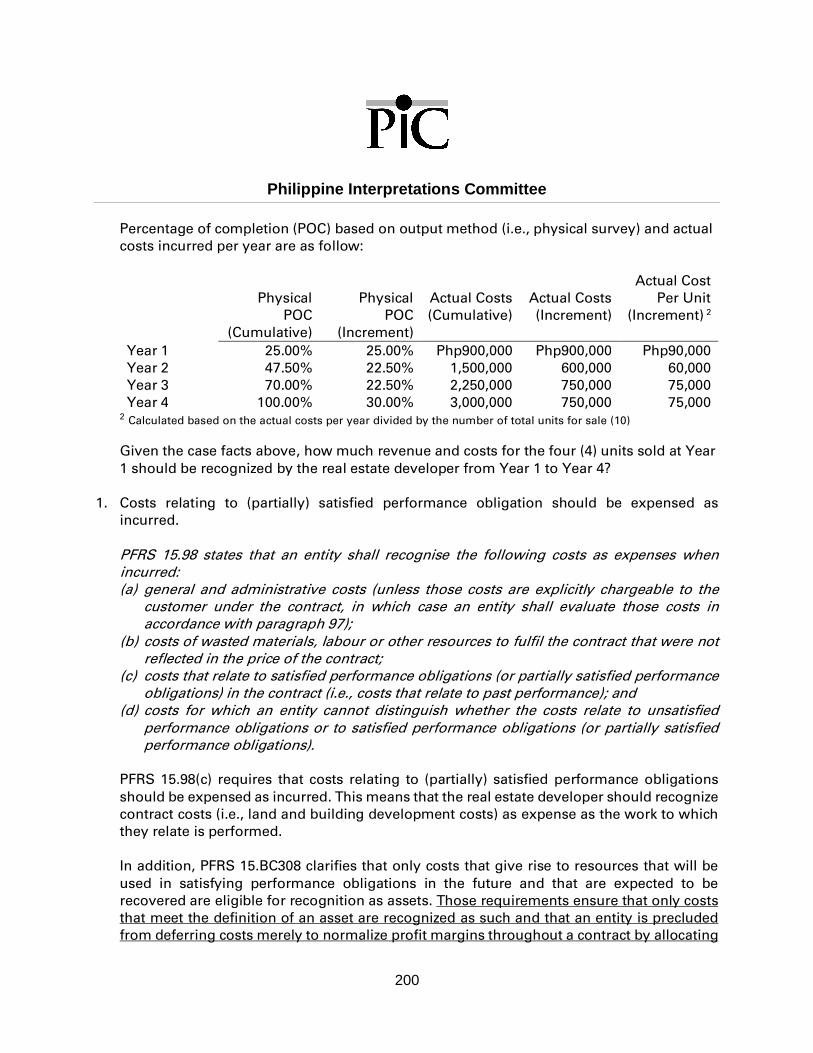

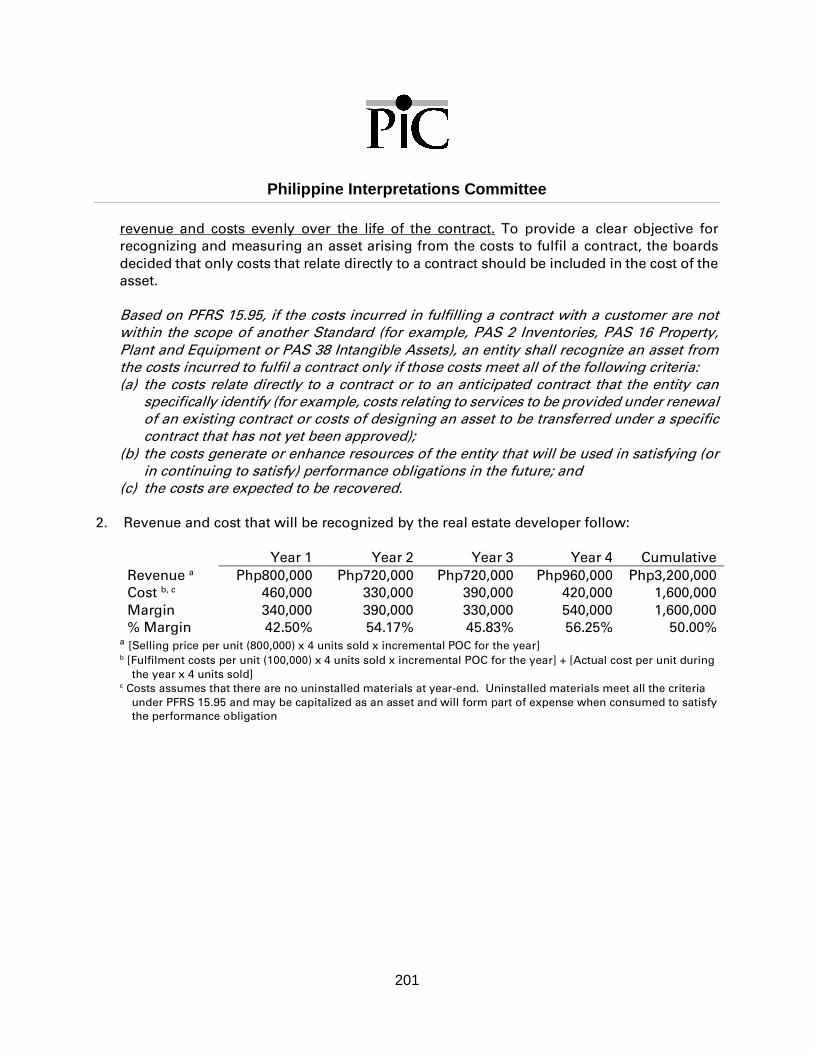

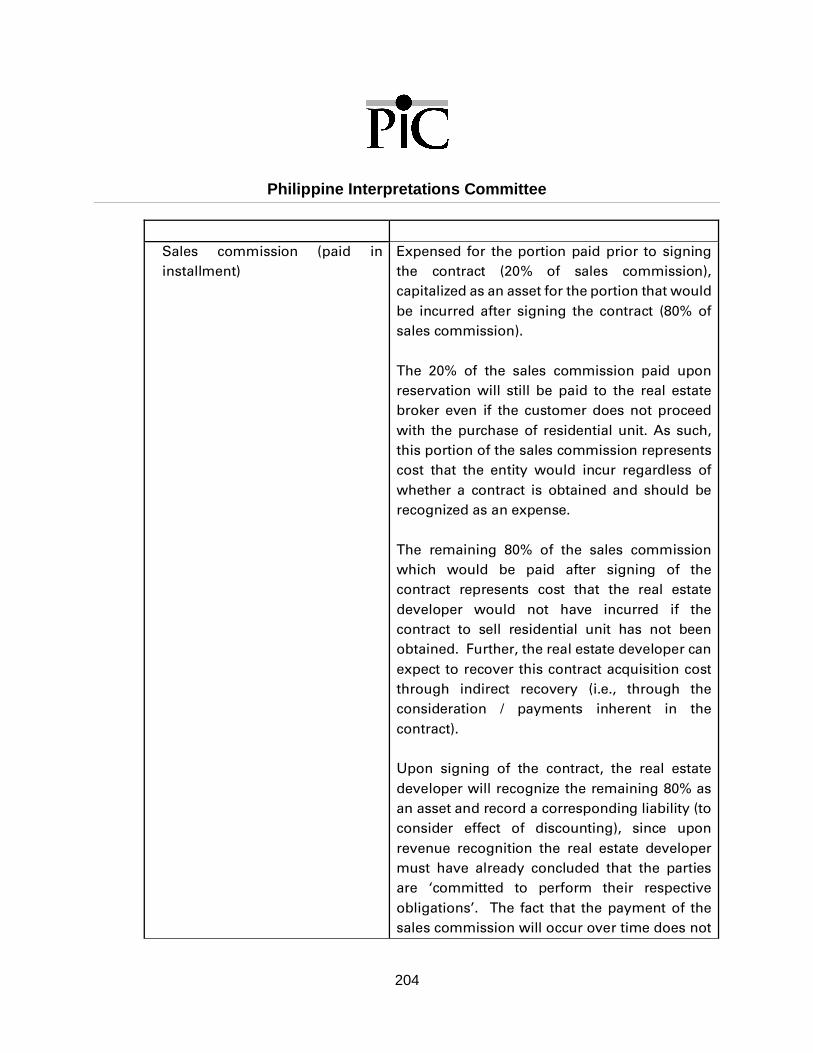

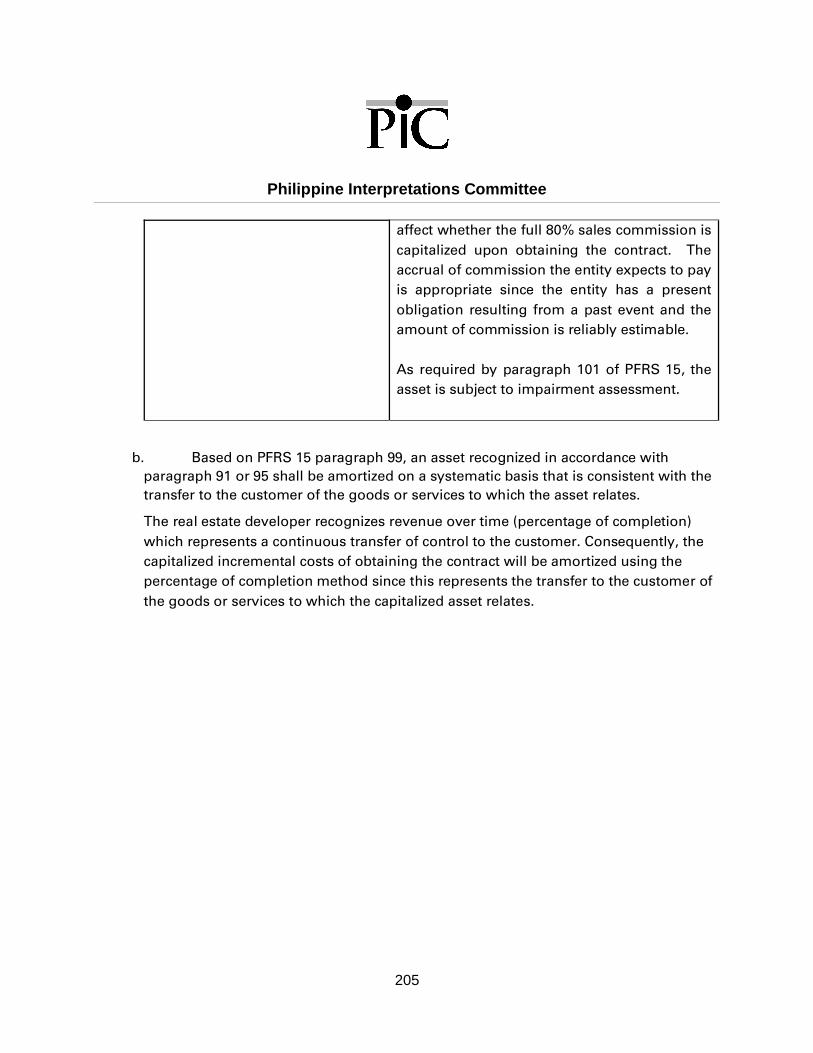

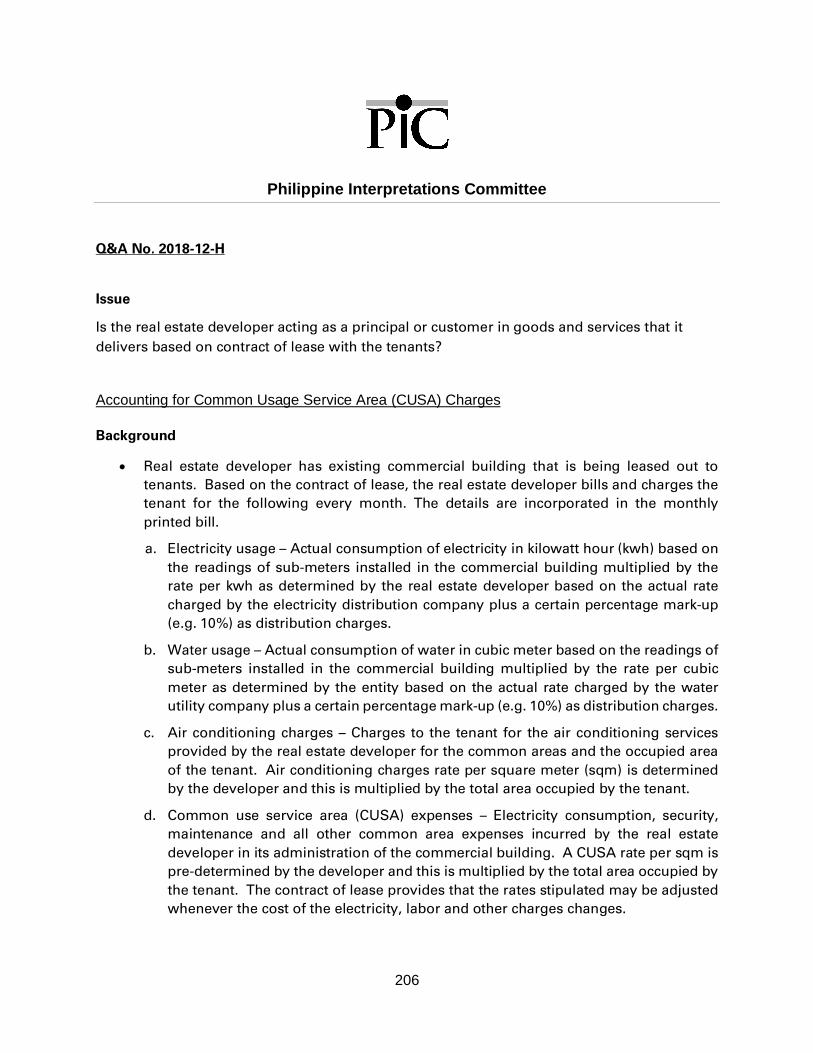

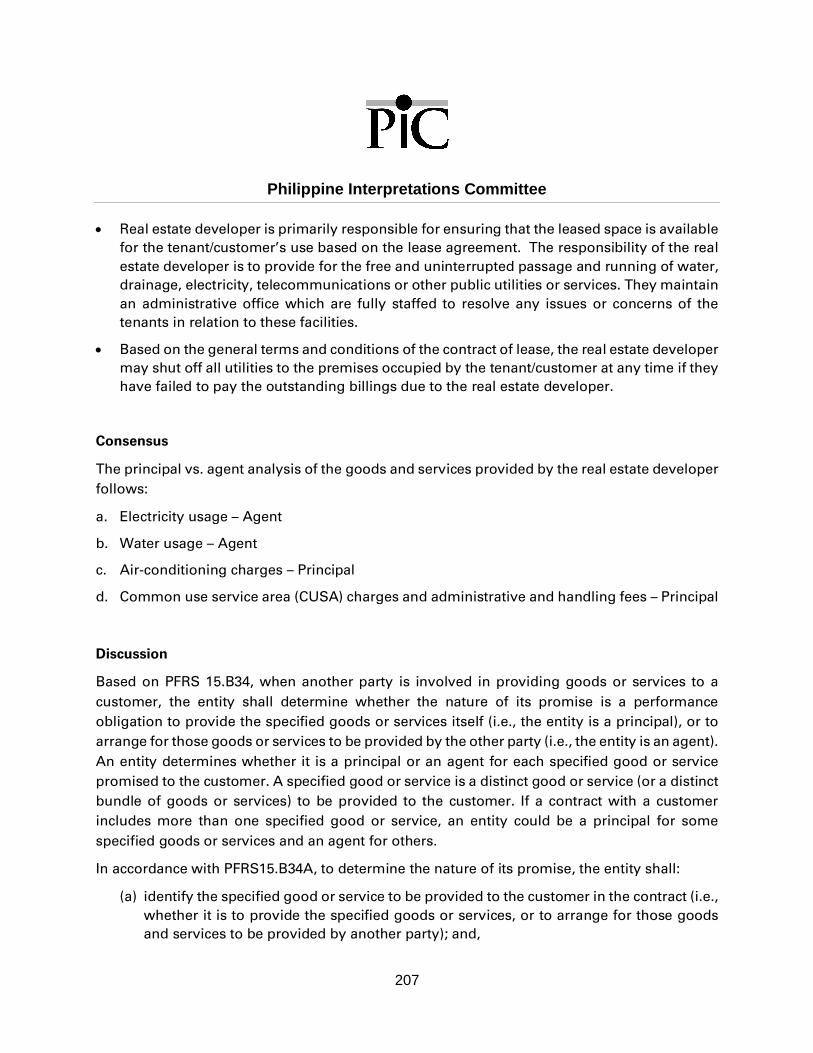

Q&A No. 2018 – 12: PFRS 15 implementation issues affecting the real estate industry ... 151

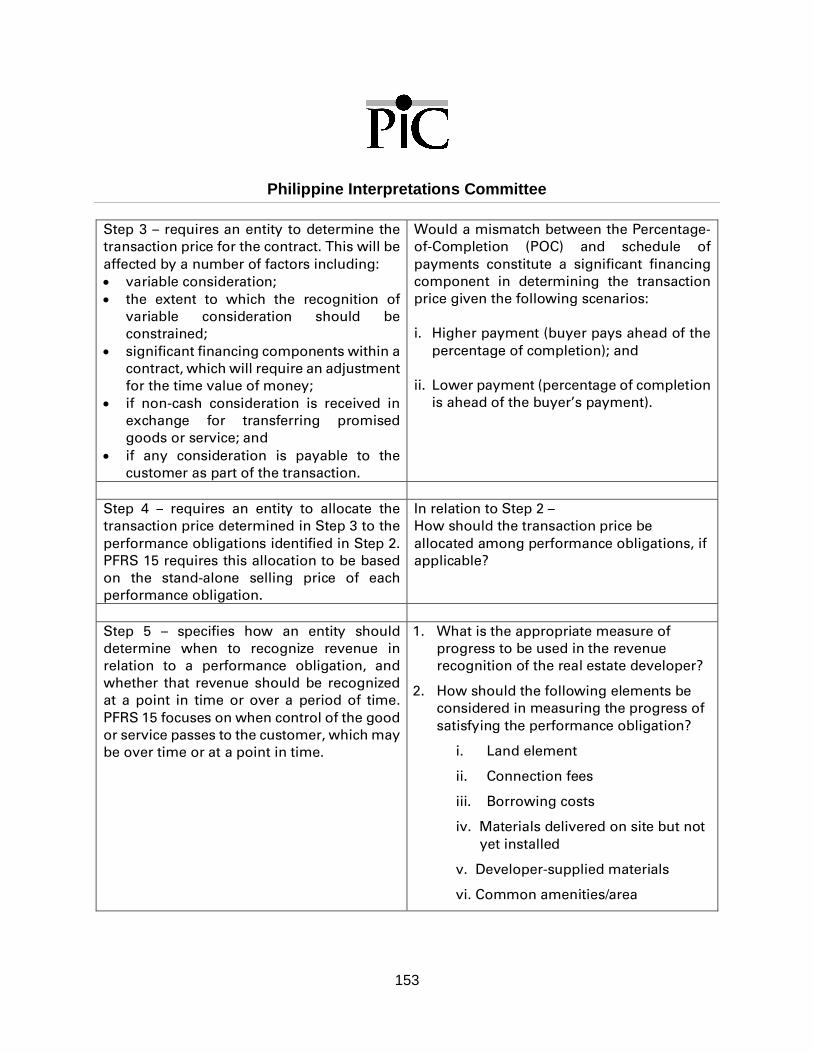

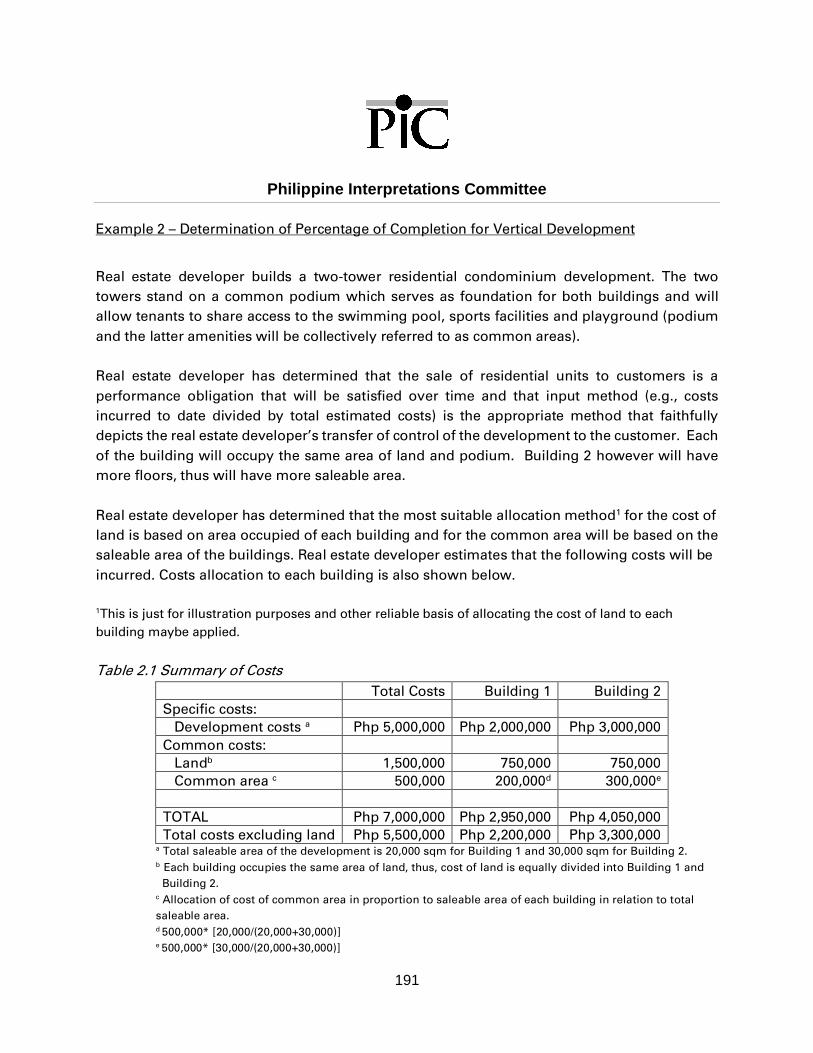

SUMMARY OF THE IMPLEMENTATION ISSUES IDENTIFIED BY THE SPECIAL TASKFORCE......................................................................................................................... 151STEP 1 – Requires an Entity to Identify the Contract with the Customer. ..................... 155STEP 2 – Requires an Entity to Identify the Distinct Goods or Services Promised withinthe Contract (Horizontal Development) ......................................................................... 158STEP 2 – Requires an Entity to Identify the Distinct Goods or Services Promised withinthe Contract (Vertical Development) ............................................................................. 164STEP 3 – Requires an Entity to Determine the Transaction Price for the Contract ....... 167

Philippine Interpretations Committee

iii

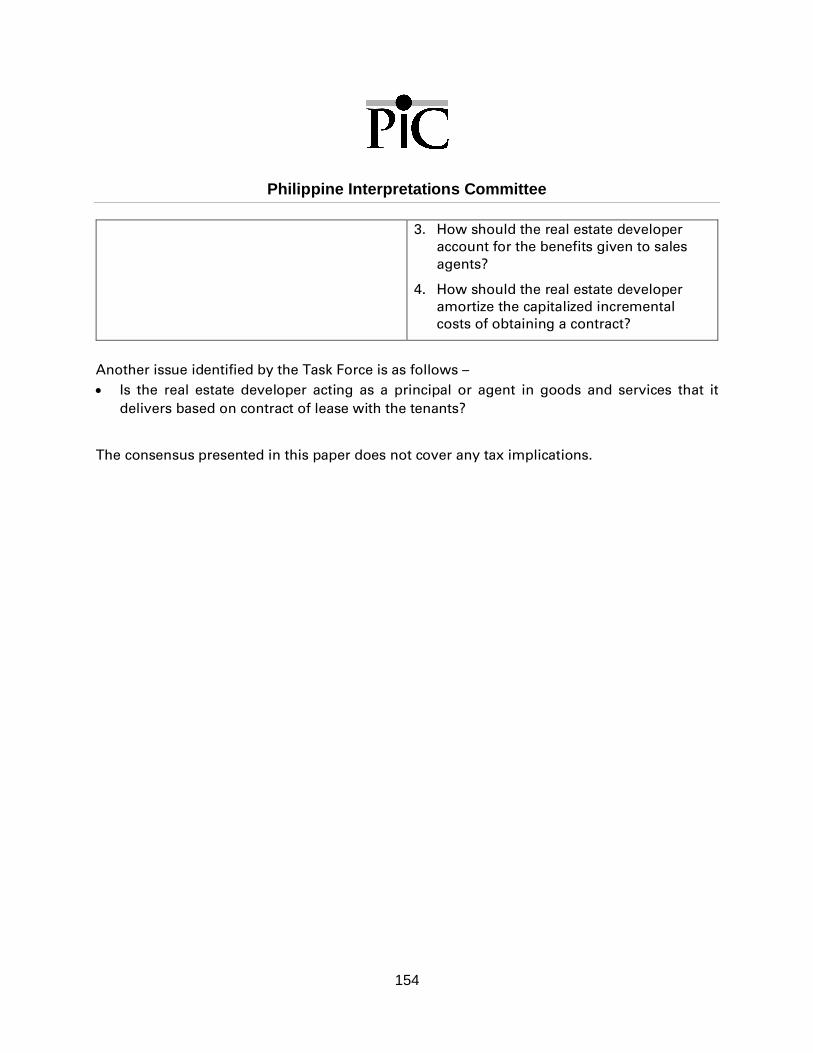

STEP 5 – Specifies How an Entity Should Determine When to Recognize Revenue inRelation to a Performance Obligation (Measurement of Progress) ............................... 180STEP 5 – Specifies How an Entity Should Determine When to Recognize Revenue inRelation to a Performance Obligation (Measurement of Progress) ............................... 199STEP 5 – Specifies How an Entity Should Determine When to Recognize Revenue inRelation to a Performance Obligation (Costs to Obtain a Contract) .............................. 202Accounting for Common Usage Service Area (CUSA) Charges ................................... 206

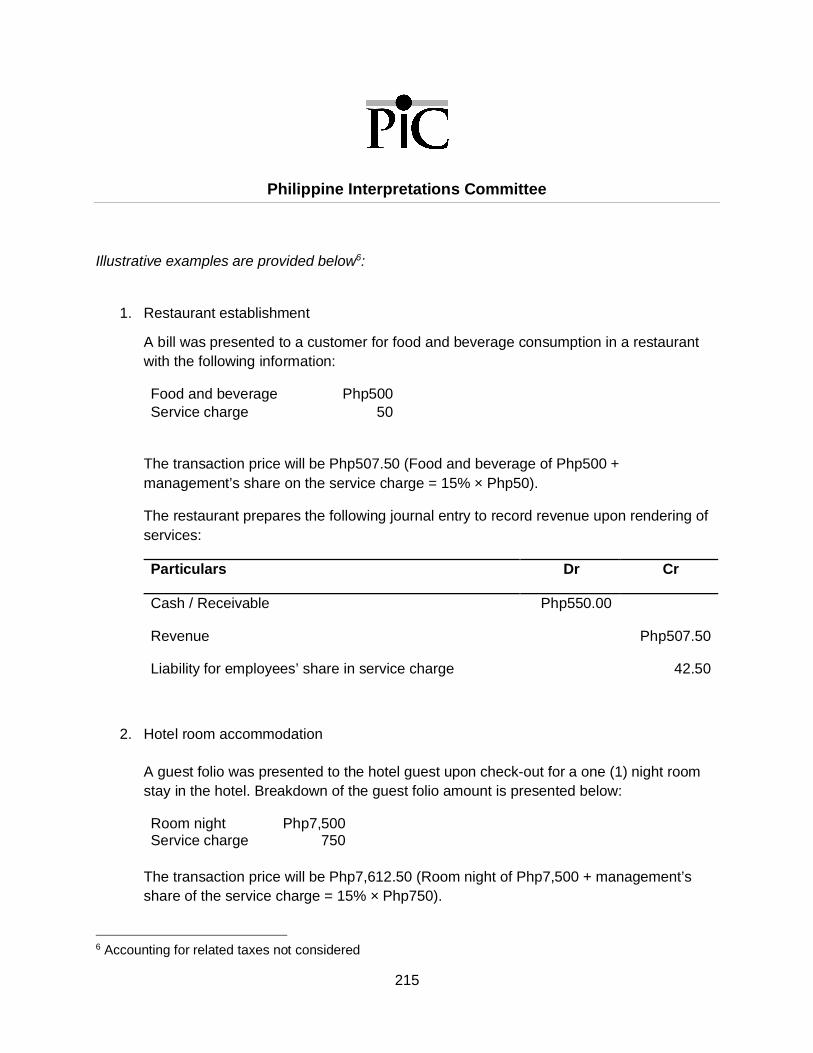

Q&A No. 2019 – 01: Accounting for service charges under PFRS 15, Revenue fromContracts with Customers ................................................................................................ 213

Q&A No. 2019 – 03: Revenue recognition guidance for sugar millers .............................. 218

Q&A No. 2020 – 02: Conclusion on PIC QA 2018-12E: On certain materials delivered onsite but not yet installed.................................................................................................... 224

Q&A No. 2020 – 03: Q&A No. 2018-12-D: STEP 3 – On the accounting of the differencewhen the percentage of completion is ahead of the buyer’s payment ............................... 229

Q&A No. 2020 – 04 (Addendum to PIC Q&A 2018-12-D): PFRS 15 - Step 3 - Requires andEntity to Determine the Transaction Price for the Contract ............................................... 234

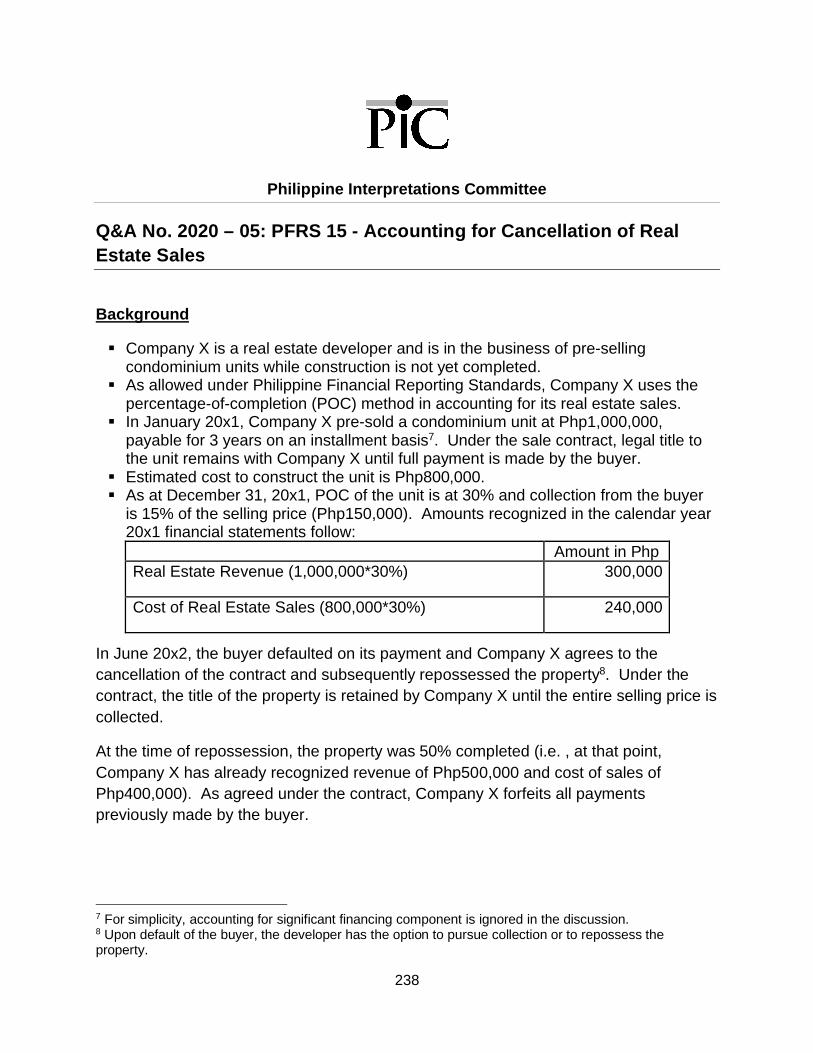

Q&A No. 2020 – 05: PFRS 15 - Accounting for Cancellation of Real Estate Sales........... 238

PFRS 16, Leases ................................................................................................................ 252

Q&A No. 2019 – 08: Accounting for Asset Retirement or Restoration Obligation with theAdoption of PFRS 16, Leases .......................................................................................... 252

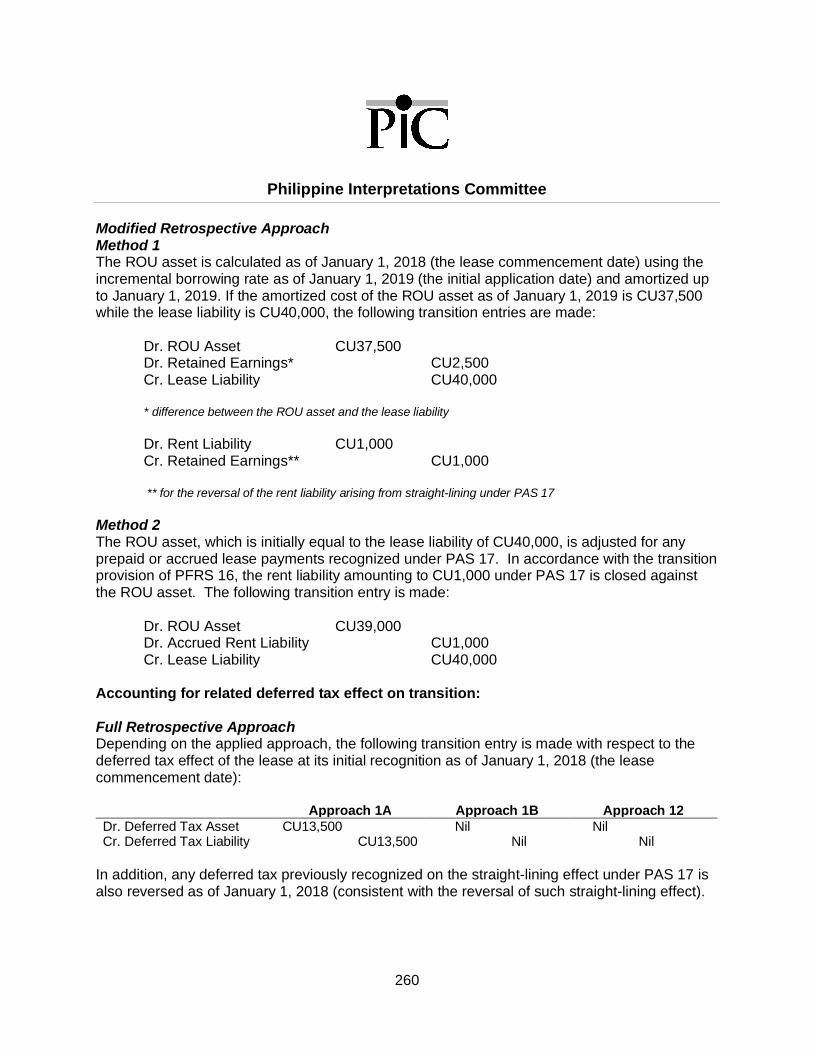

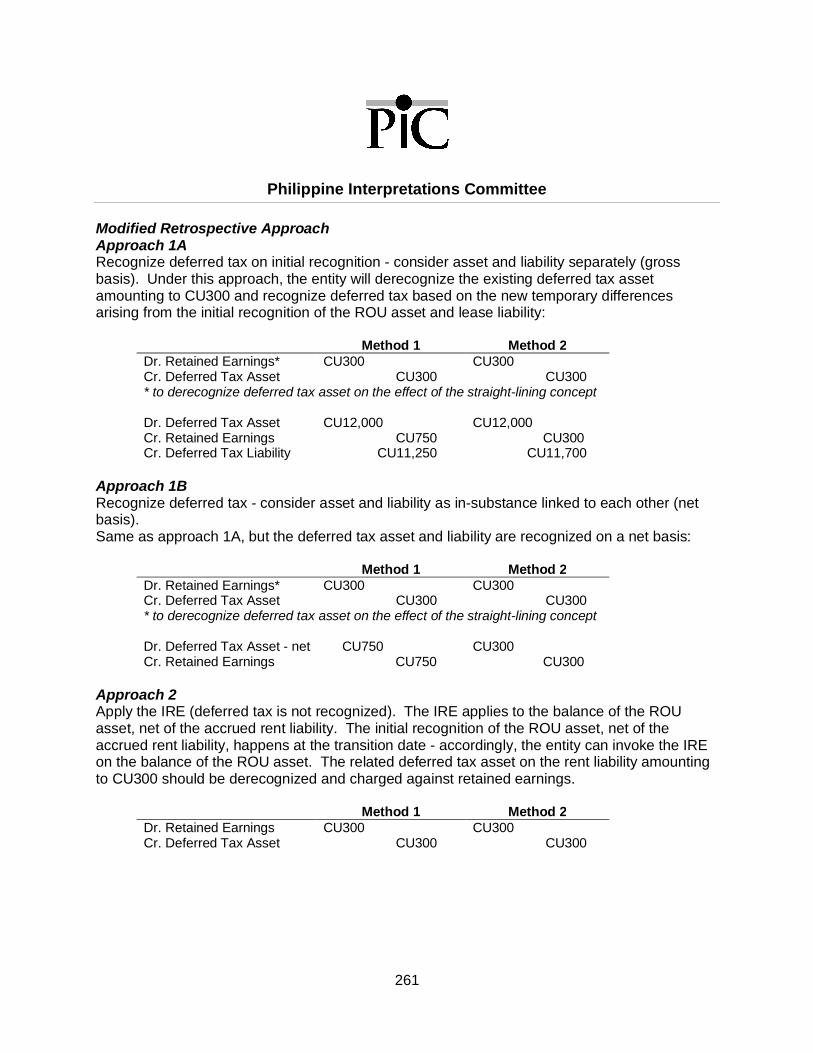

Q&A No. 2019 – 09: Accounting for Prepaid Rent or Rent Liability Arising from Straight-lining under PAS 17 on Transition to PFRS 16 and the Related Deferred Tax Effects ..... 256

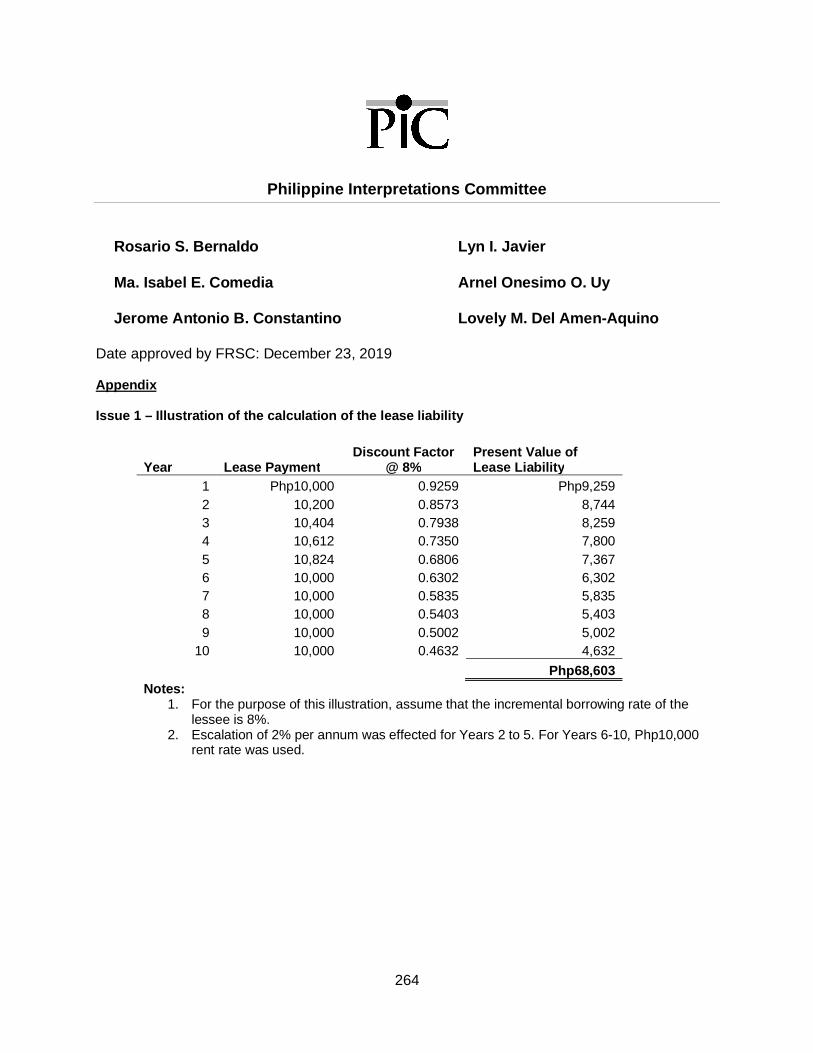

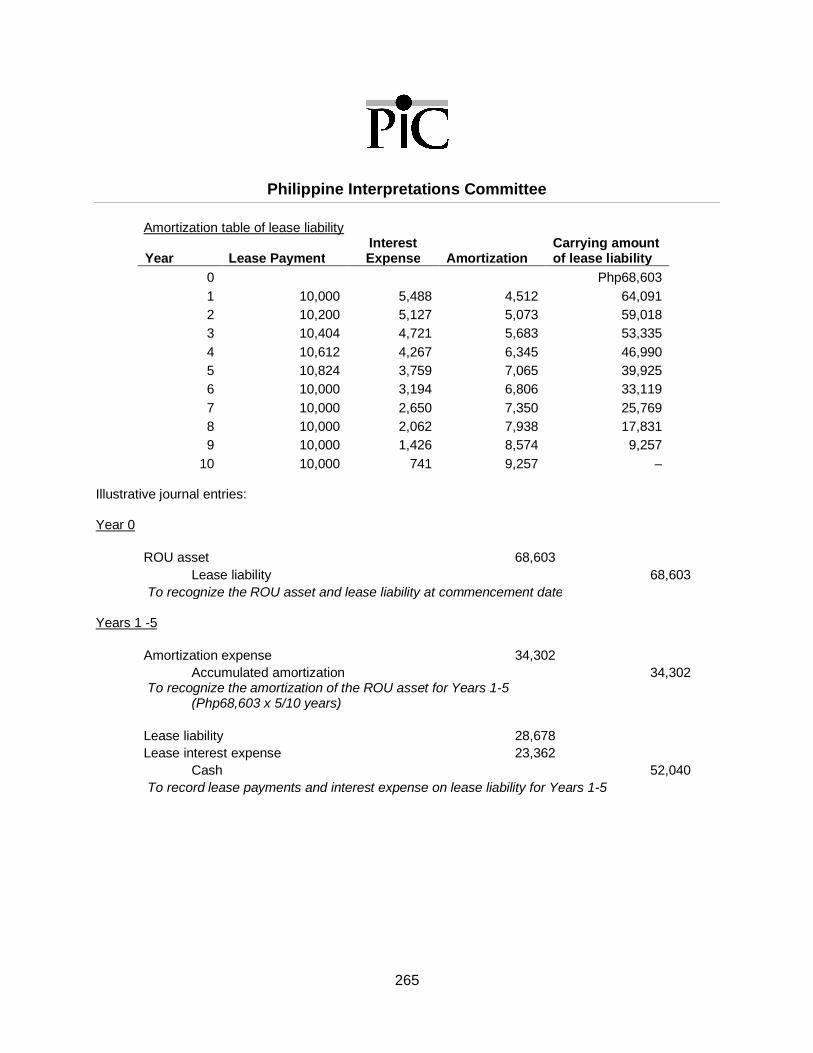

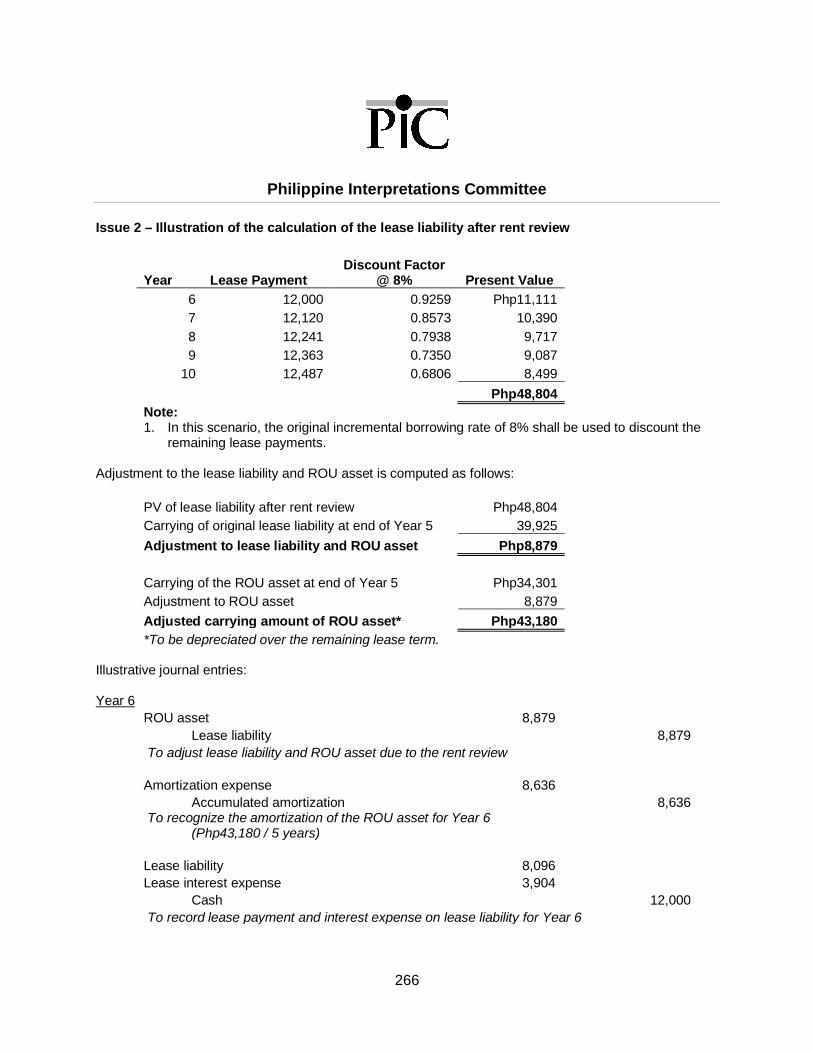

Q&A No. 2019 – 10: Accounting for variable payments with rent review .......................... 262

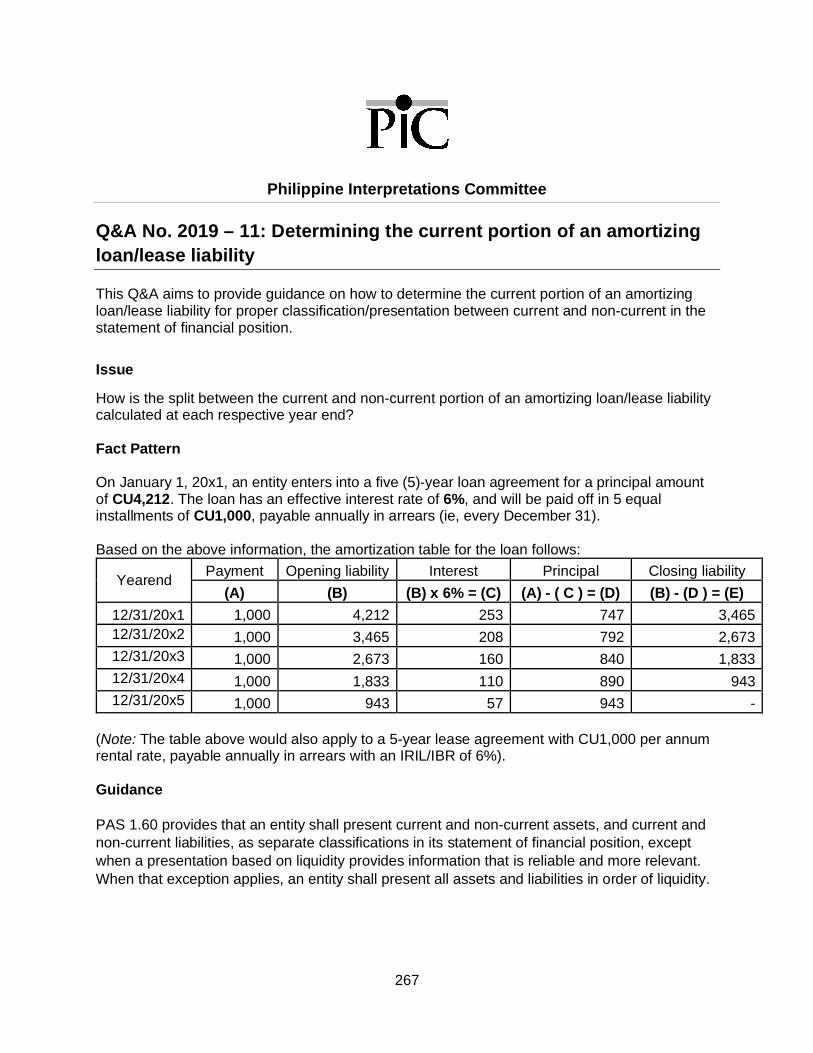

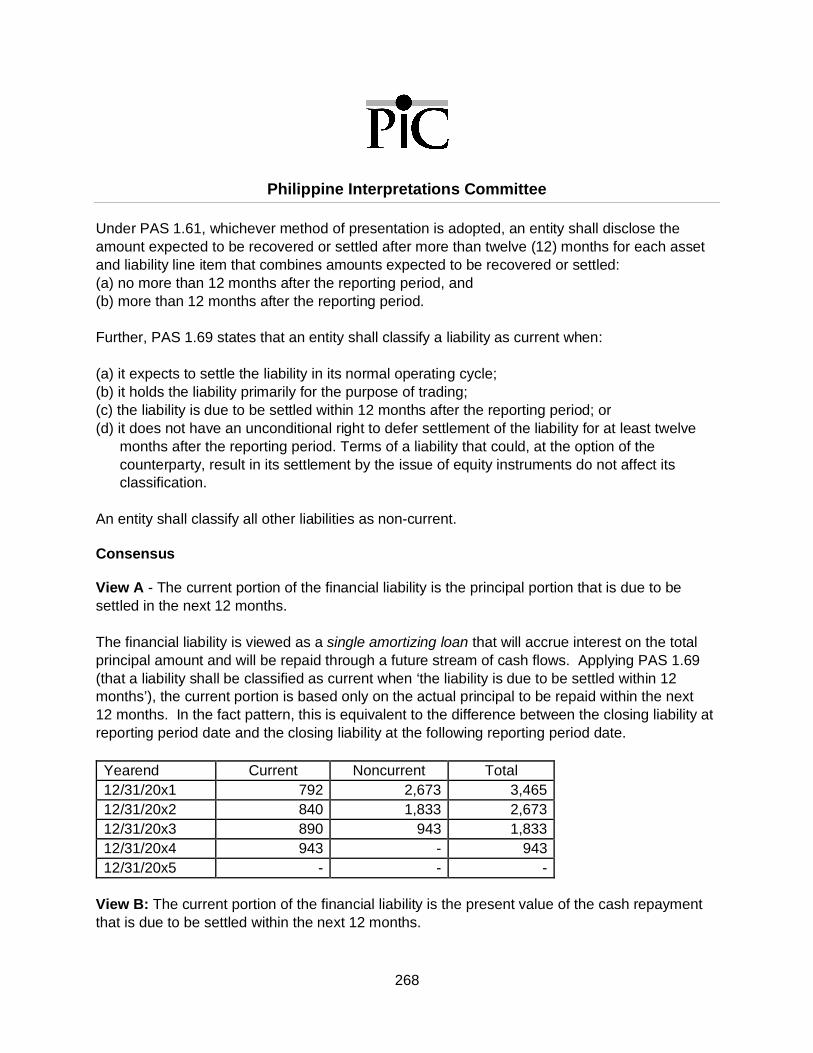

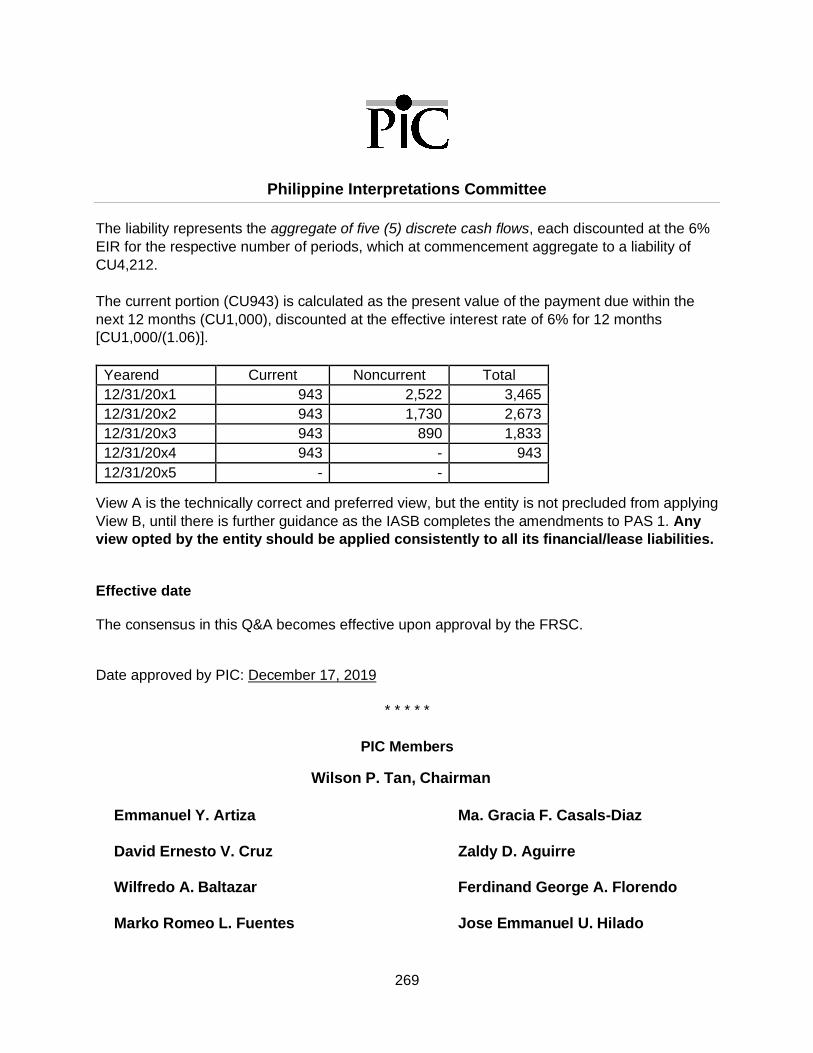

Q&A No. 2019 – 11: Determining the current portion of an amortizing loan/lease liability. 267

Q&A No. 2019 – 12: Determining the lease term under PFRS 16, Leases ....................... 270

Q&A No. 2019 – 13: Determining the lease term of leases that are renewable subject tomutual agreement of the lessor and the lessee ................................................................ 274

Q&A No. 2020 – 06: Accounting for payments between and among lessors and lessees 277

PAS 1, Presentation of Financial Statements ...................................................................... 295

Q&A No. 2009 – 01 (amended June 2020): Framework 3.9 and PAS 1.25 – Financialstatements prepared on a basis other than going concern ............................................... 295

Philippine Interpretations Committee

iv

Q&A No. 2010 – 02 (amended June 2018): PAS 1R.16 – Basis of preparation of financialstatements ....................................................................................................................... 299

Q&A No. 2010 – 03: PAS 1R.16 – PAS 1 Presentation of Financial Statements – Current/non-current classification of a callable term loan .............................................................. 303

Q&A No. 2011 – 03 (amended June 2020): Accounting for Inter-company Loans ............ 306

Q&A No. 2016 – 03 (amended June 2020): Accounting for Common Areas and the RelatedSubsequent Costs by Condominium Corporations ........................................................... 315

Q&A No. 2018 – 15 (amended July 2019): PAS 1- Classification of Advances toContractors in the Nature of Prepayments: Current vs. Non-current ................................ 320

PAS 2, Inventories ............................................................................................................... 325

Q&A No. 2012 - 02: Cost of a new building constructed on the site of a previous building ........................................................................................................................................ 325

Q&A No. 2017 – 02 (amended July 2019): Capitalization of depreciation of right-of-useasset cost as part of construction costs of a building ........................................................ 333

Q&A No. 2017 - 06: PAS 2, 16 and 40 – Accounting for Collector’s Items ....................... 338

Q&A No. 2018 - 10: PAS 2 - Scope of disclosure of inventory write-downs ...................... 342

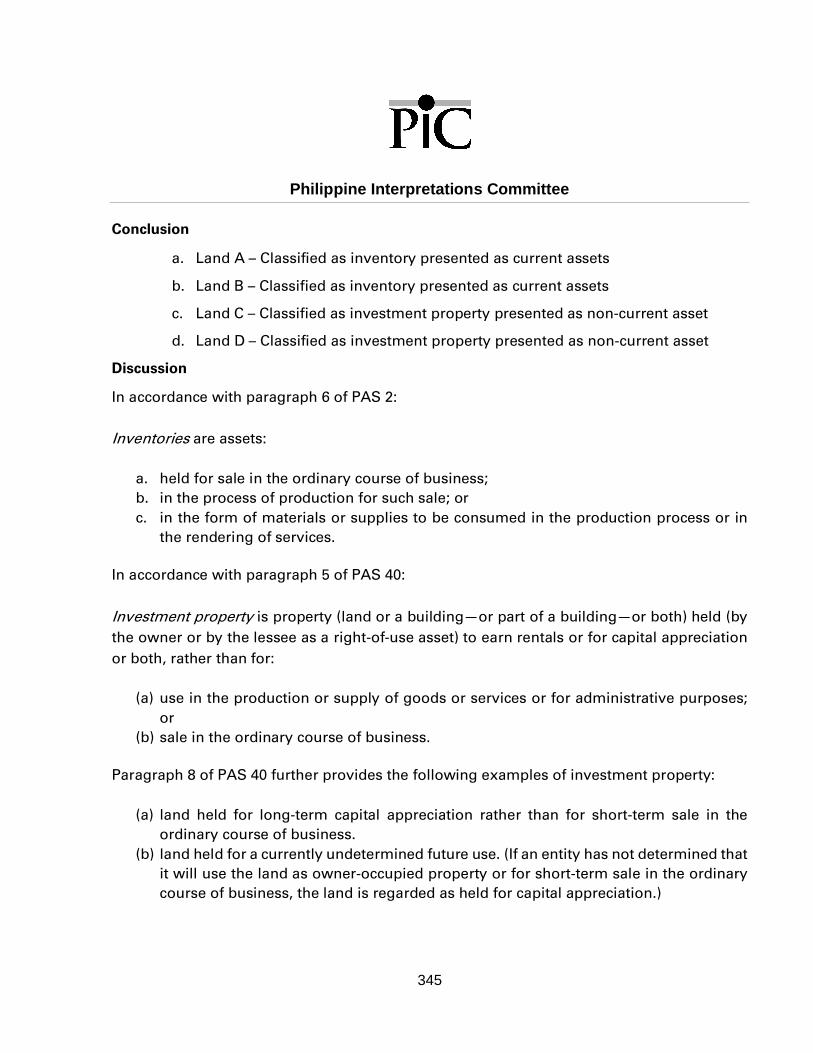

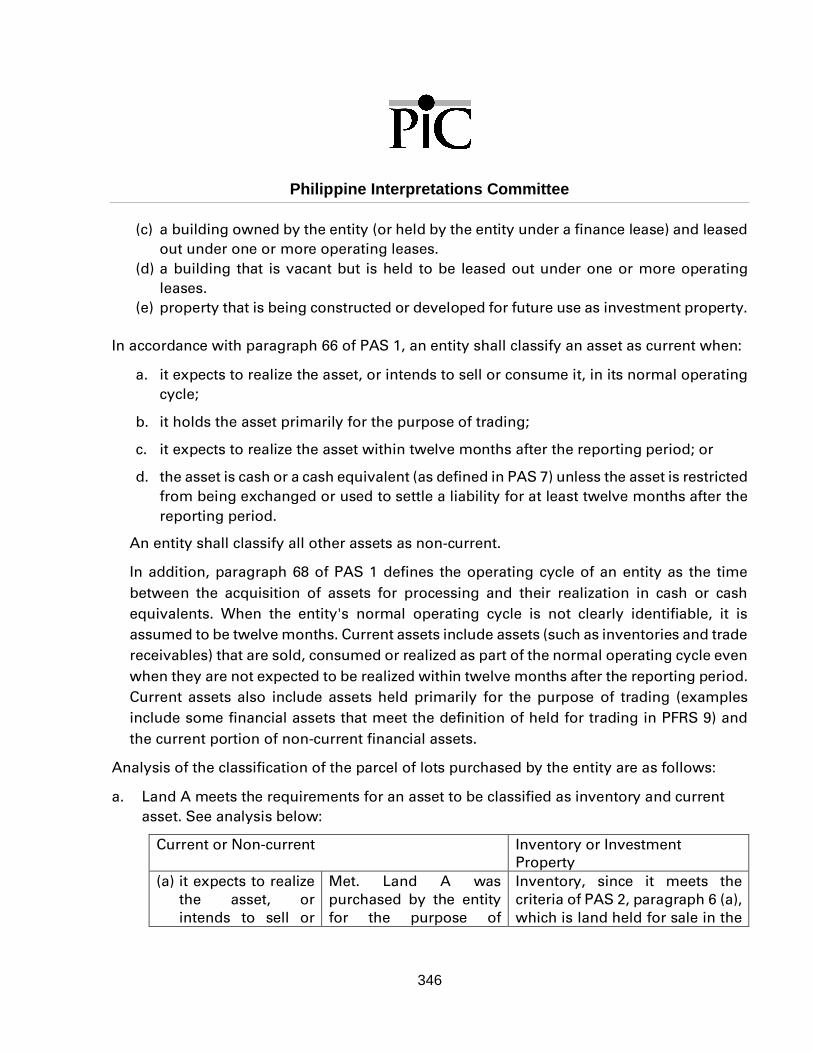

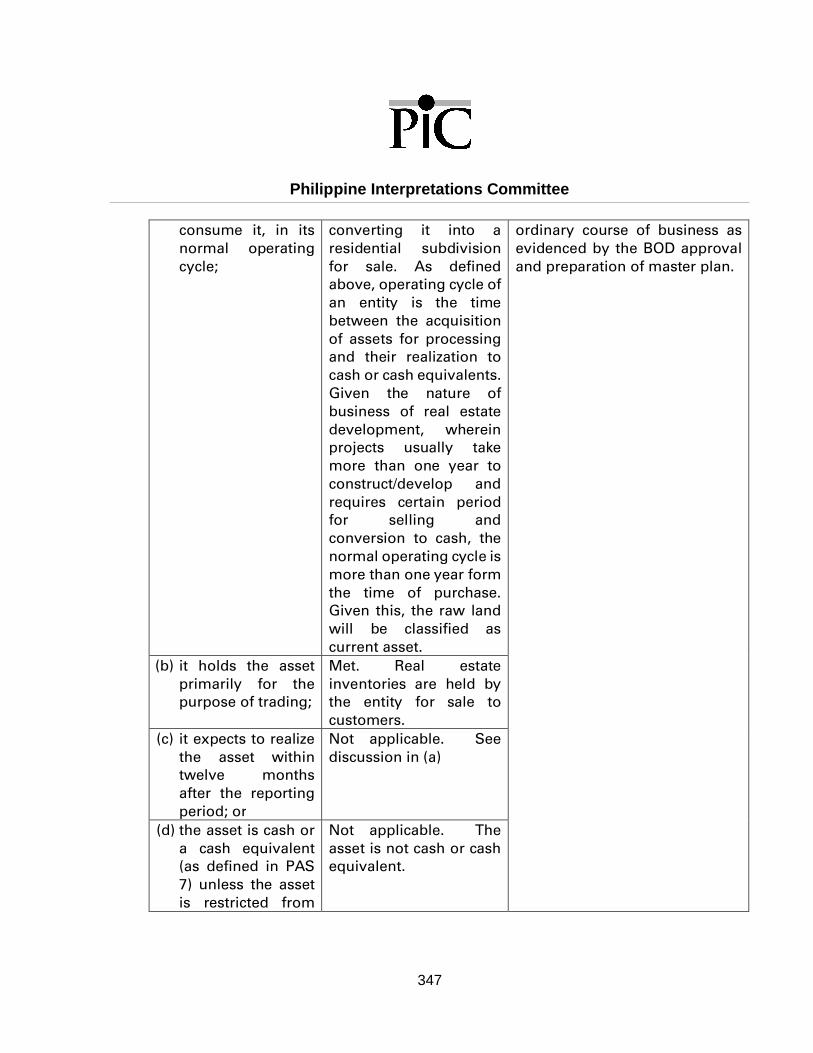

Q&A No. 2018 - 11: Classification of land by real estate developer .................................. 344

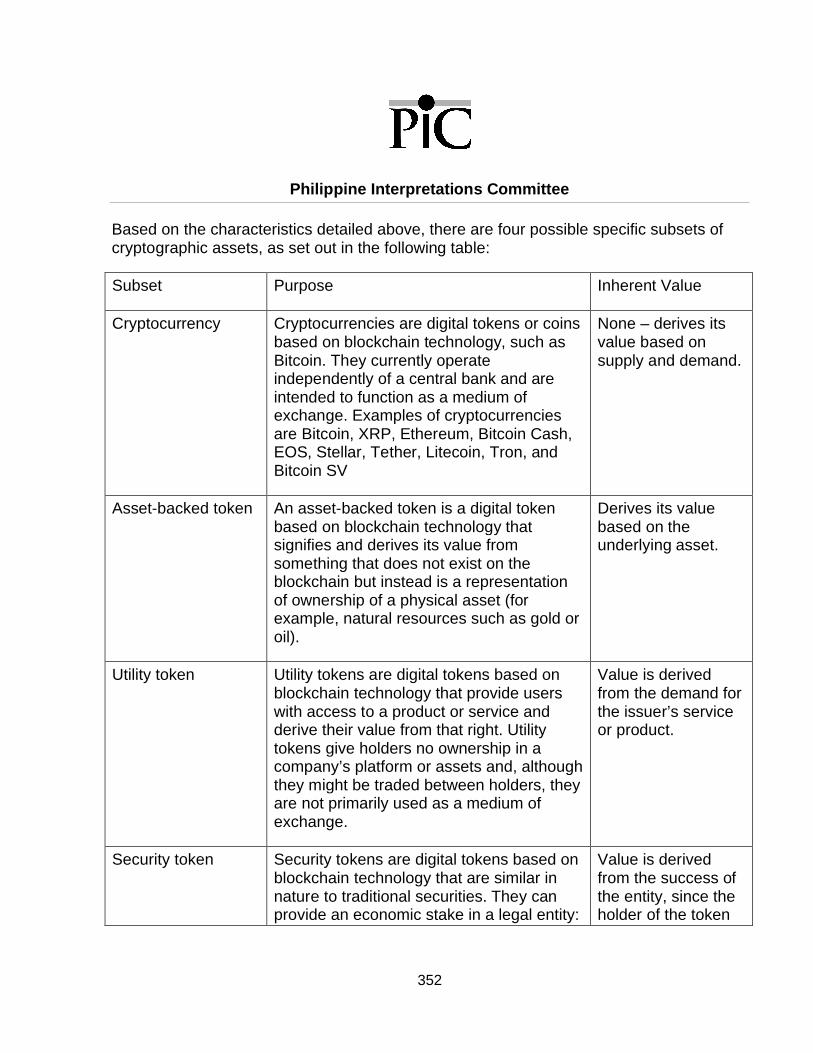

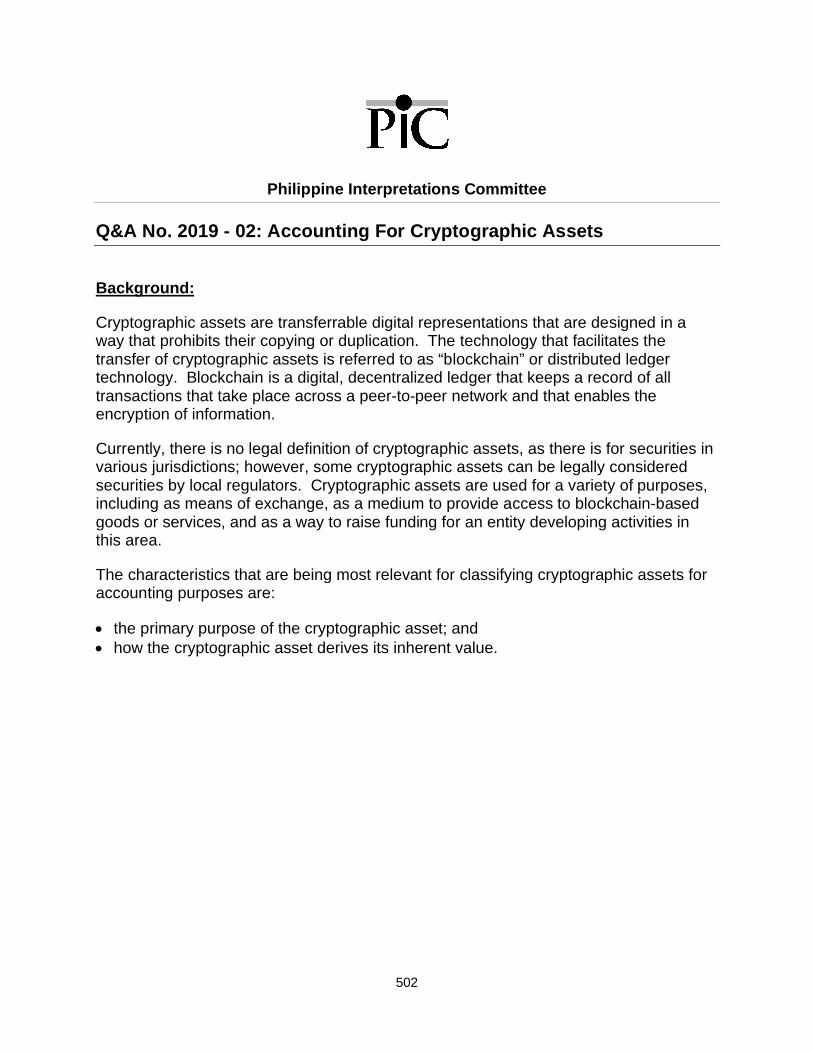

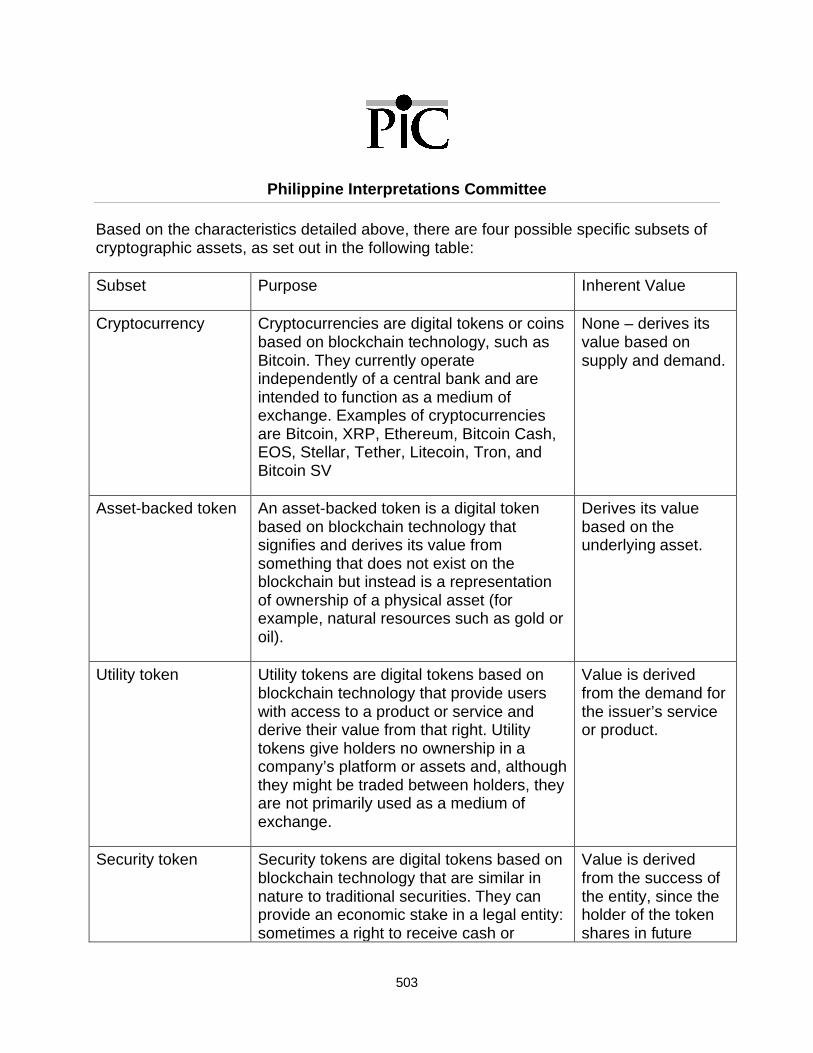

Q&A No. 2019 - 02: Accounting For Cryptographic Assets .............................................. 351

PAS 8, Accounting Policies, Changes in Accounting Estimates and Errors ......................... 364

Q&A No. 2017 - 12: Subsequent Treatment of Equity Component Arising fromIntercompany Loans ........................................................................................................ 364

Q&A No. 2018 - 01: PAS 8 - Voluntary changes in accounting policy ............................... 367

PAS 12, Income taxes ......................................................................................................... 370

Q&A No. 2020 - 07: Accounting for the Proposed Changes in Income Tax Rates under theCorporate Recovery and Tax Incentives for Enterprises Act (CREATE) Bill ..................... 370

PAS 16, Property, Plant and Equipment .............................................................................. 379

Q&A No. 2012 - 02: Cost of a new building constructed on the site of a previous building ........................................................................................................................................ 379

Q&A No. 2017 – 02 (amended July 2019): Capitalization of depreciation of right-of-useasset cost as part of construction costs of a building ........................................................ 387

Q&A No. 2017 - 06: PAS 2, 16 and 40 – Accounting for Collector’s Items ....................... 392

Philippine Interpretations Committee

v

Q&A No. 2018 - 03: PFRS 13, PAS 16 and PAS 36 - Fair value of property, plant andequipment and depreciated replacement cost .................................................................. 396

PAS 19, Employee Benefits (Revised)................................................................................. 400

Q&A No. 2008 – 01 (Amended April 2016): PAS 19.83 – Rate used in discounting post-employment benefit obligations ........................................................................................ 400

Q&A No. 2013 – 03 (Revised): PAS 19 – Accounting for Employee Benefits under aDefined Contribution Plan subject to Requirements of Republic Act (RA) 7641, ThePhilippine Retirement Law ............................................................................................... 402

PAS 21, The Effects of Changes in Foreign Exchange Rates .............................................. 409

Q&A No. 2018 – 09: PAS 21 - Classification of deposits and progress payments asmonetary or non-monetary items ..................................................................................... 409

PAS 24, Related Party Disclosures ..................................................................................... 412

Q&A No. 2011 – 03 (amended June 2020): Accounting for Inter-company Loans ............ 412

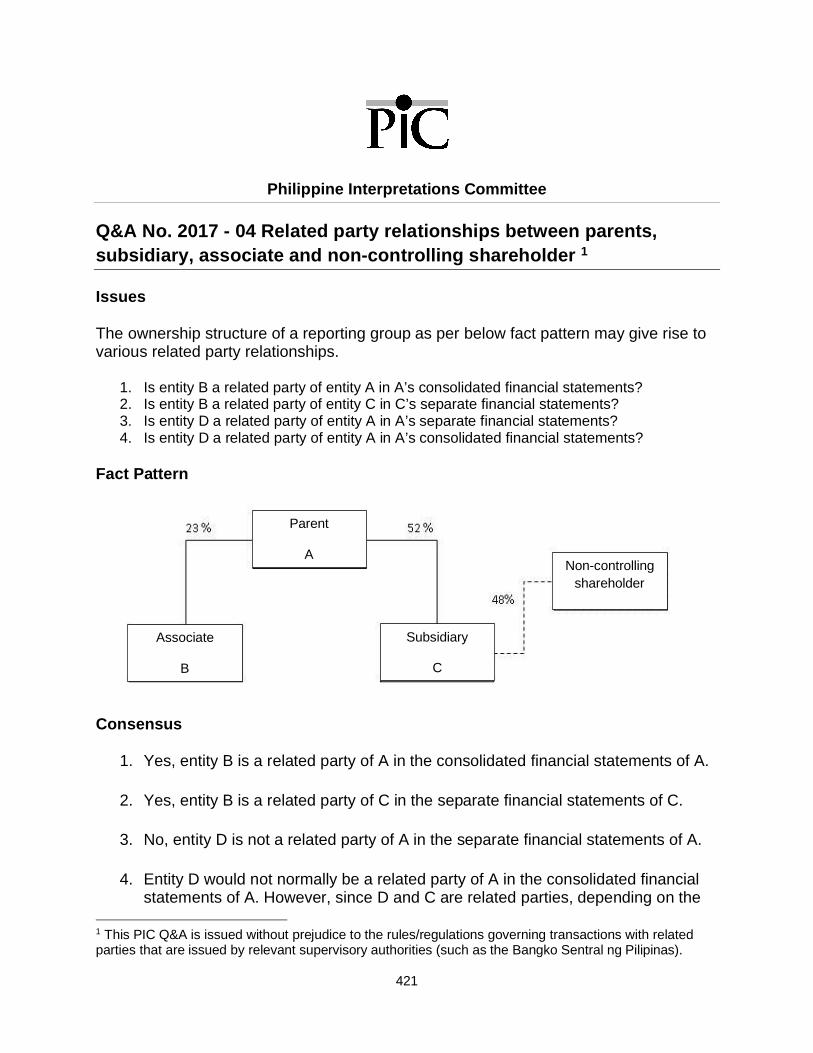

Q&A No. 2017 - 04 Related party relationships between parents, subsidiary, associate andnon-controlling shareholder .............................................................................................. 421

PAS 27, Separate Financial Statements .............................................................................. 426

Q&A No. 2011 - 03 (amended June 2020): Accounting for Inter-company Loans............. 426

Q&A No. 2018 - 06: PAS 27 - Cost of investment in subsidiaries in separate financialstatements when pooling is applied in consolidated financial statements ......................... 435

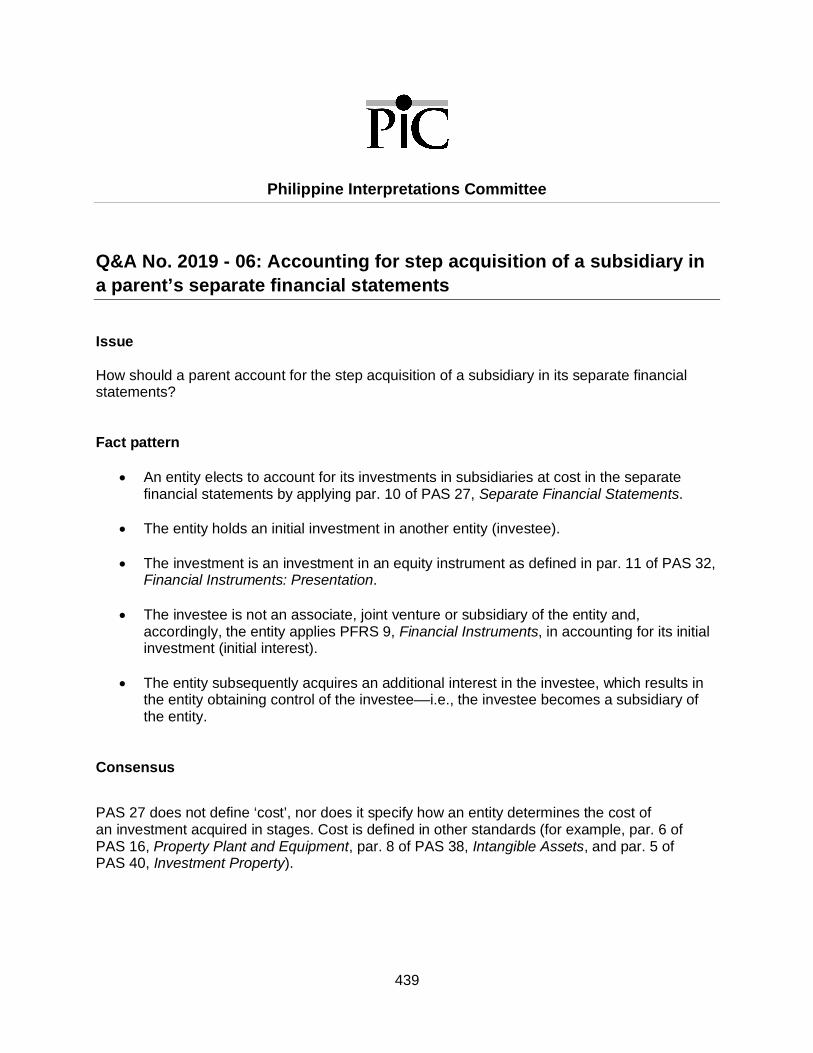

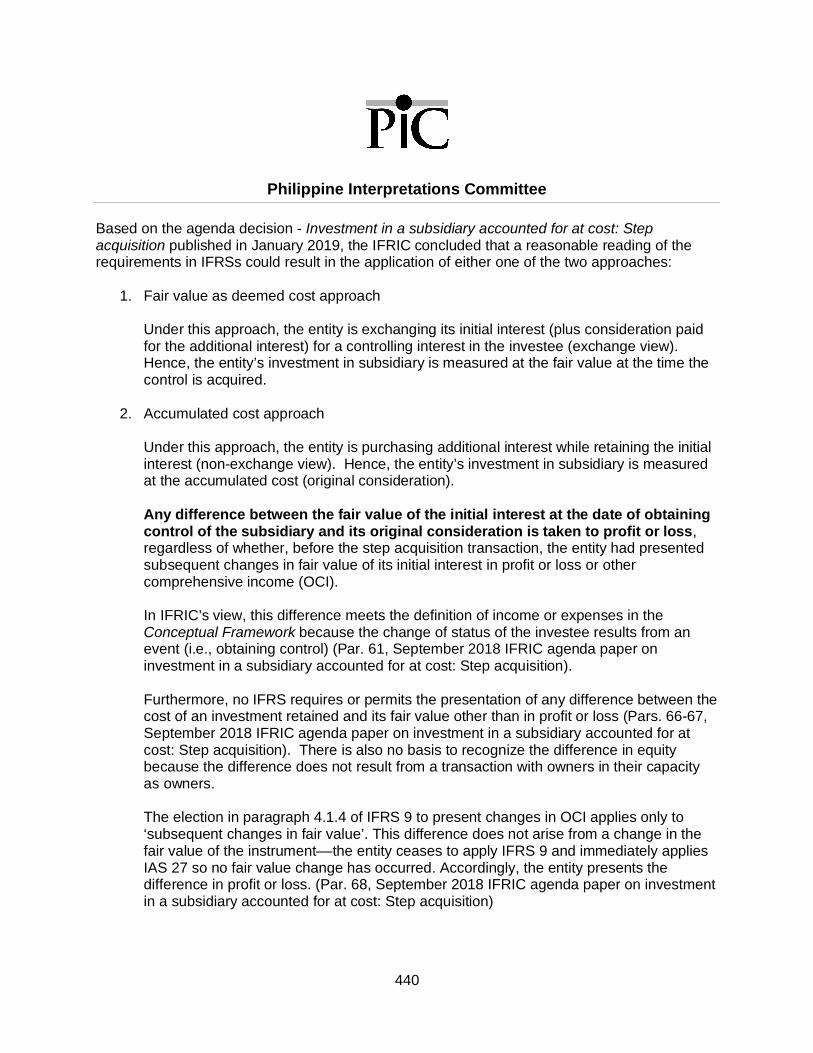

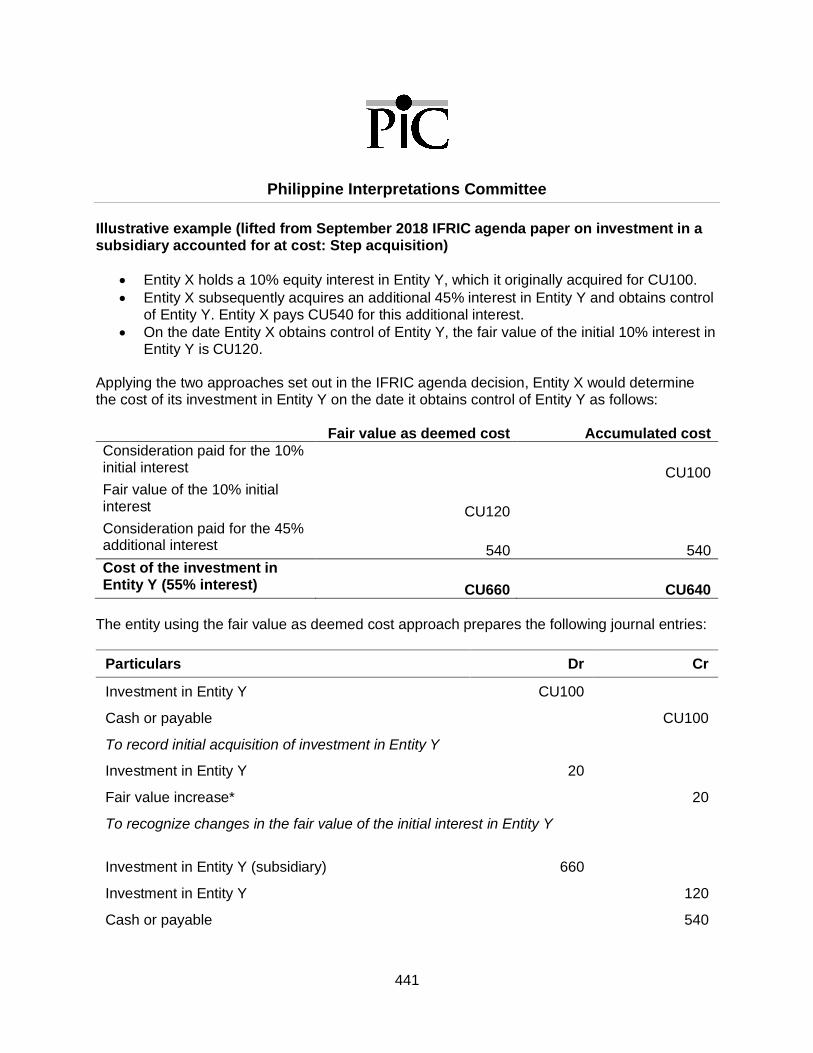

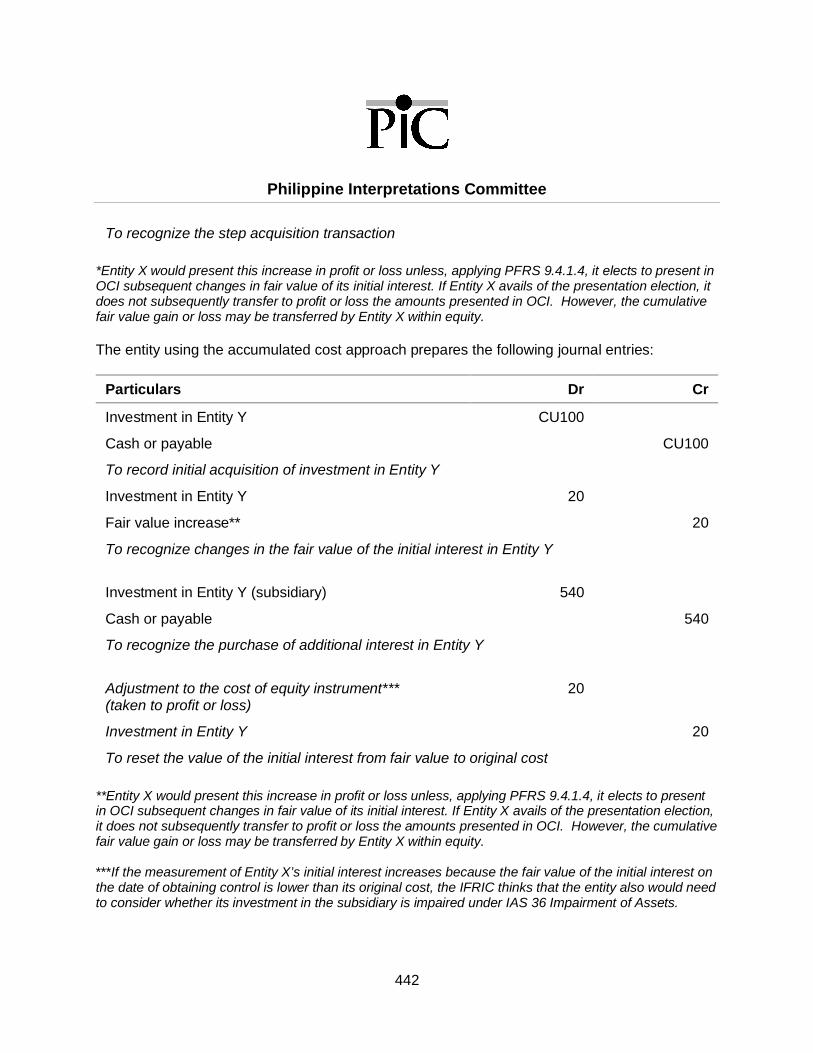

Q&A No. 2019 - 06: Accounting for step acquisition of a subsidiary in a parent’s separatefinancial statements ......................................................................................................... 439

PAS 28, Investments in Associates and Joint Ventures ....................................................... 444

Q&A No. 2011 - 03 (amended June 2020): Accounting for Inter-company Loans............. 444

Q&A No. 2017 – 03: PAS 28 - Elimination of profits and losses resulting from transactionsbetween associates and/or joint ventures......................................................................... 453

PAS 32, Financial Instruments: Presentation ....................................................................... 457

Q&A No. 2011 - 03 (amended June 2020): Accounting for Inter-company Loans............. 457

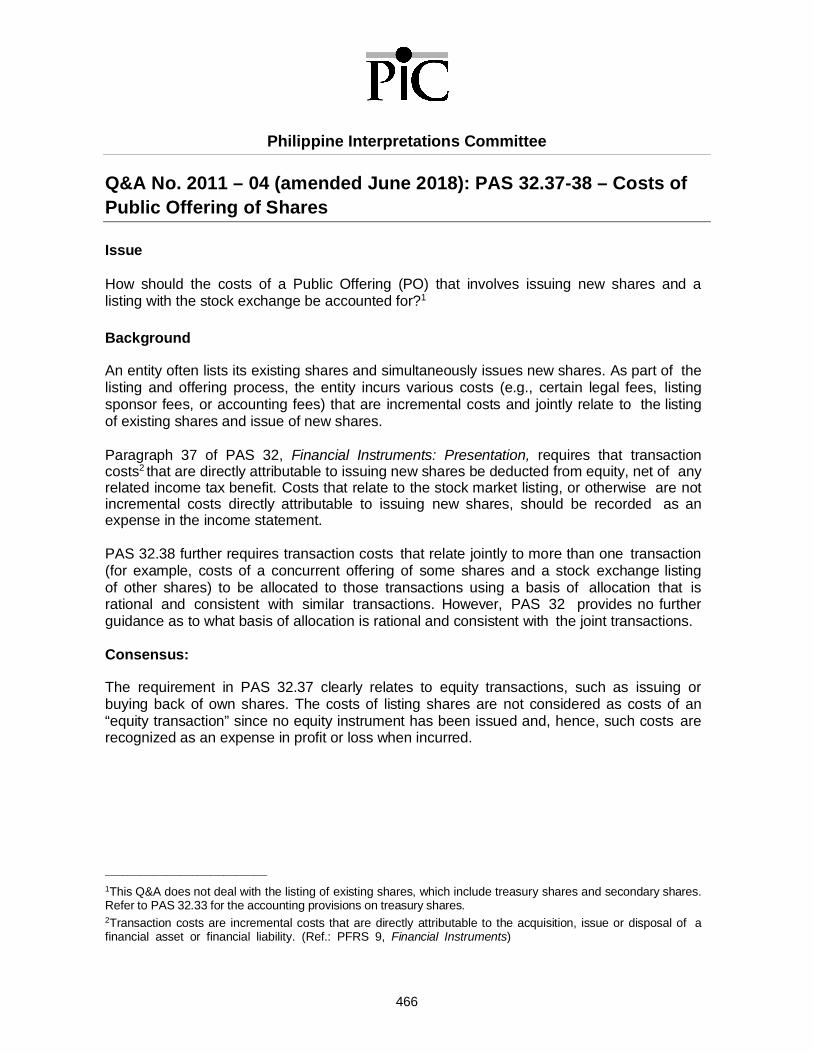

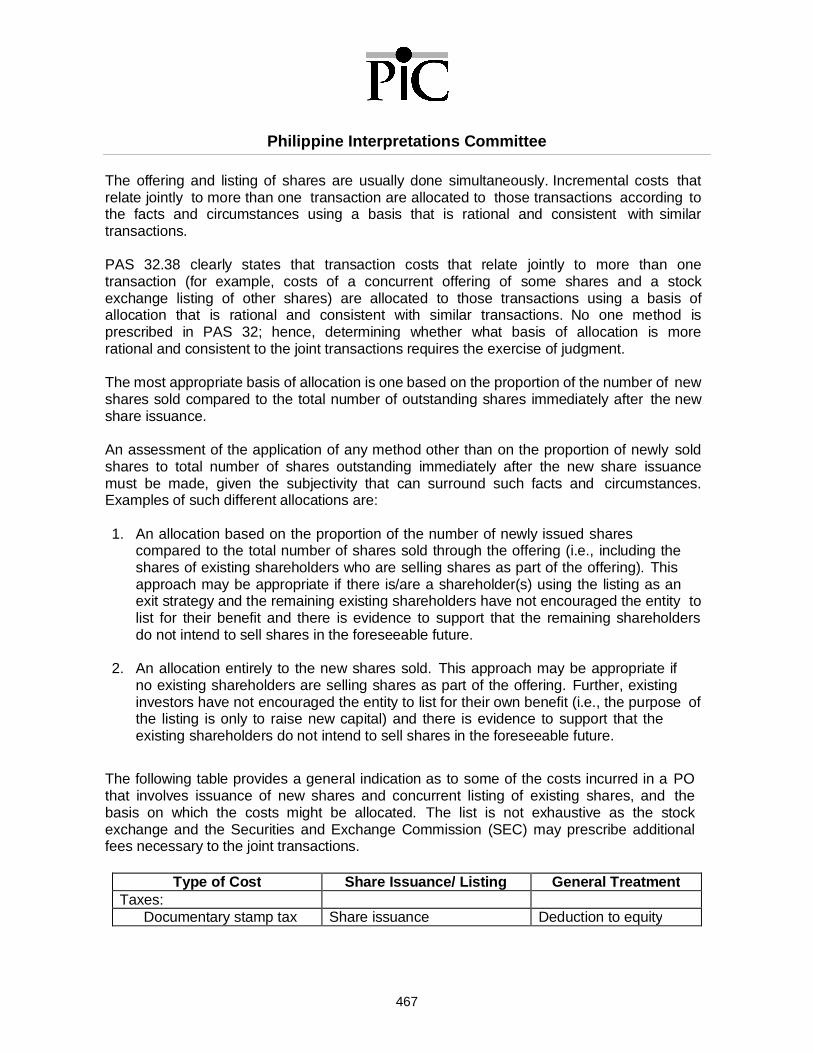

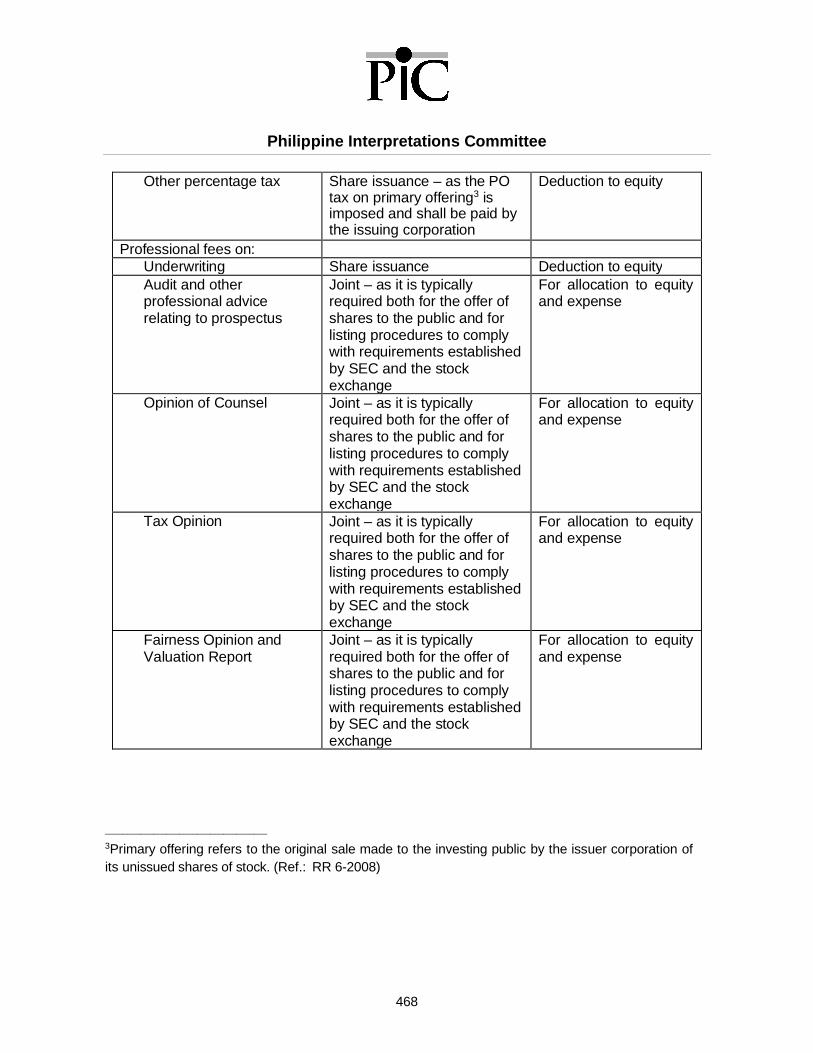

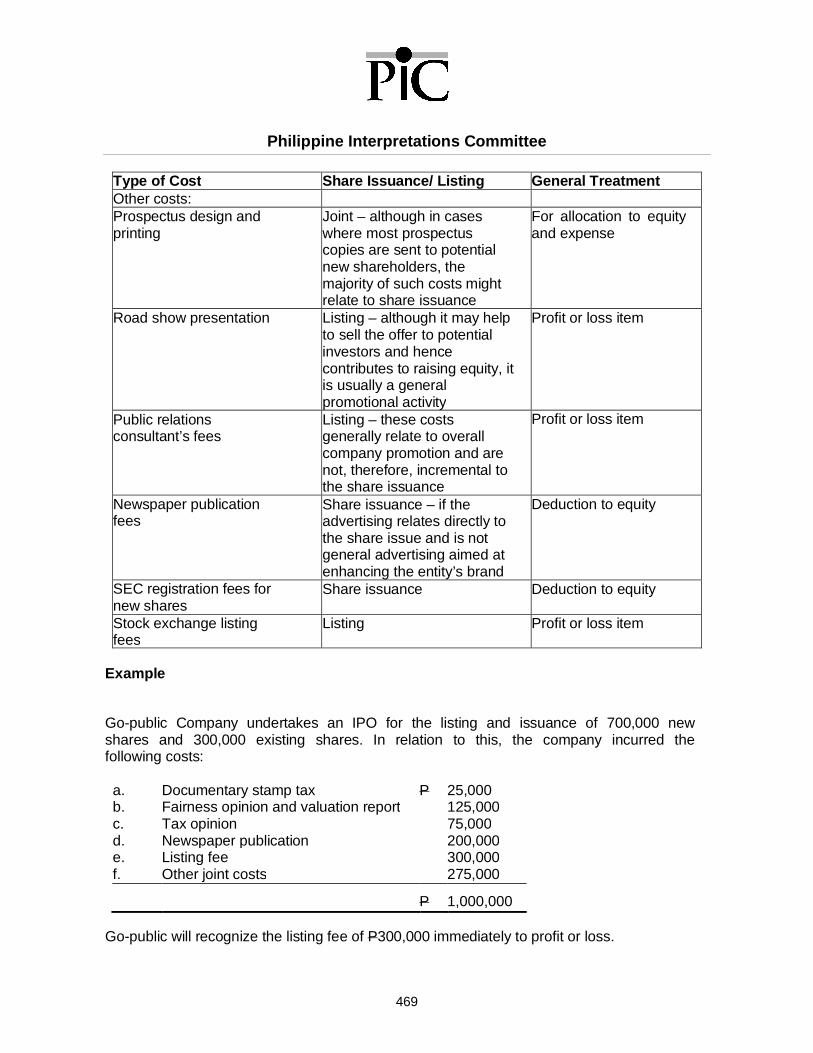

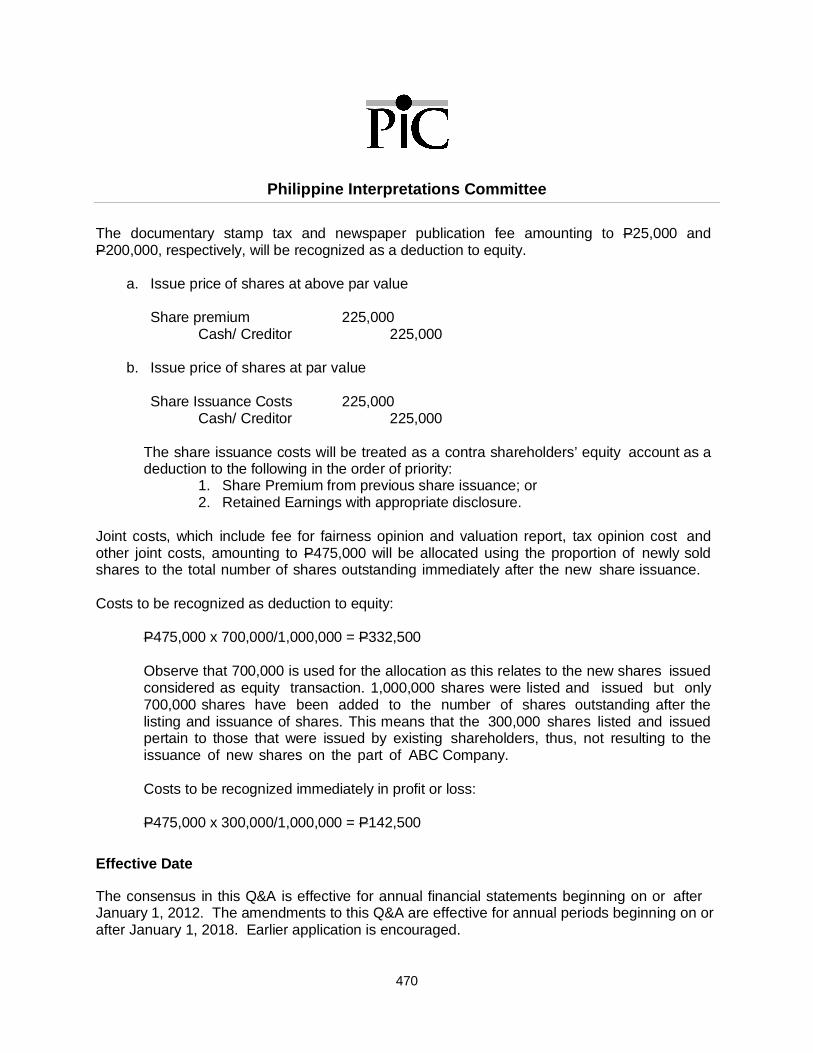

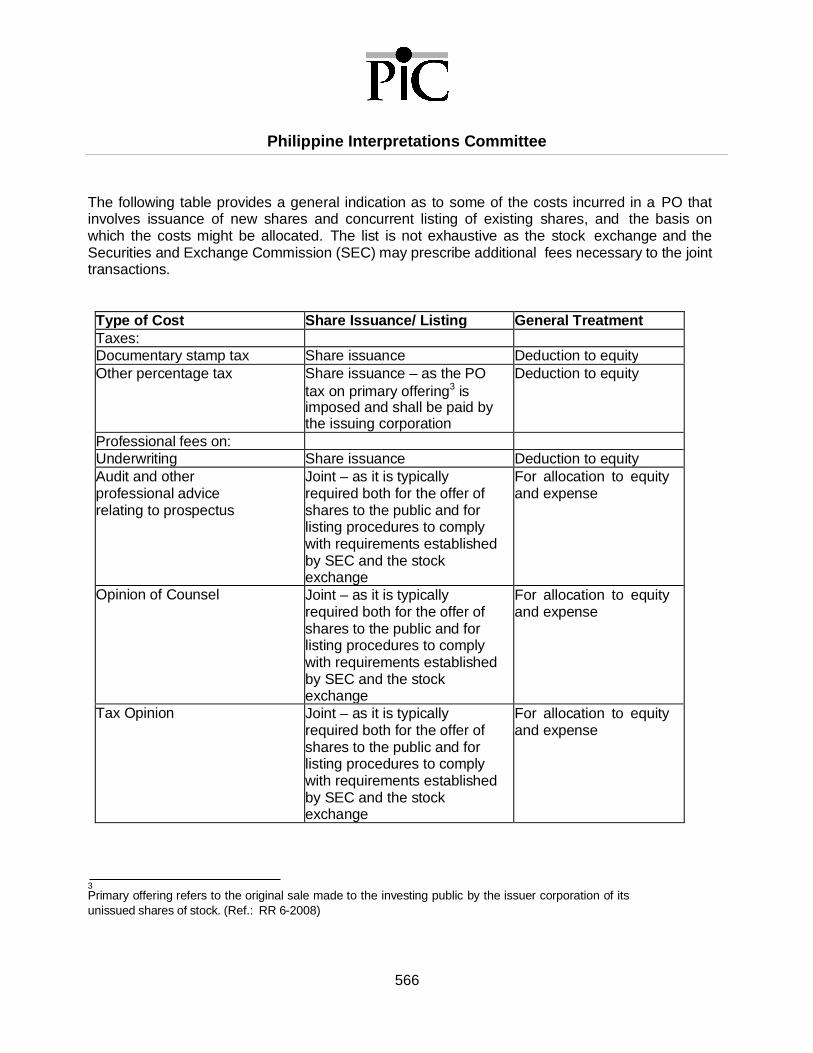

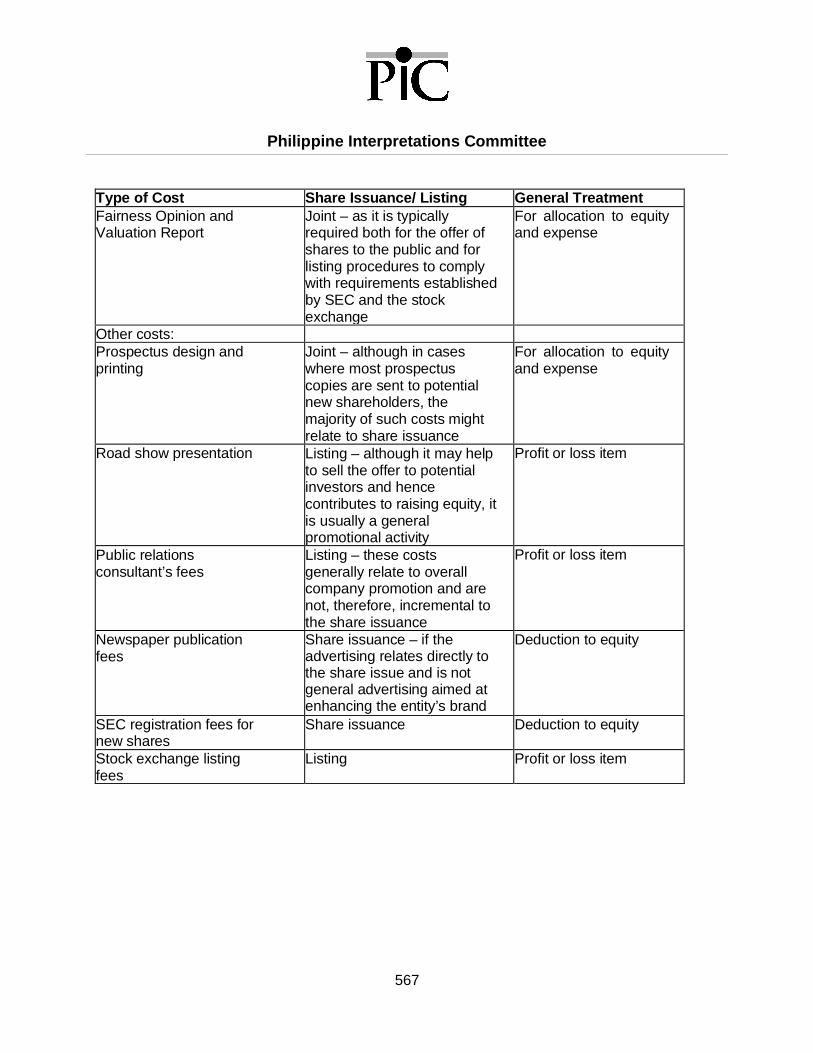

Q&A No. 2011 – 04 (amended June 2018): PAS 32.37-38 – Costs of Public Offering ofShares ............................................................................................................................. 466

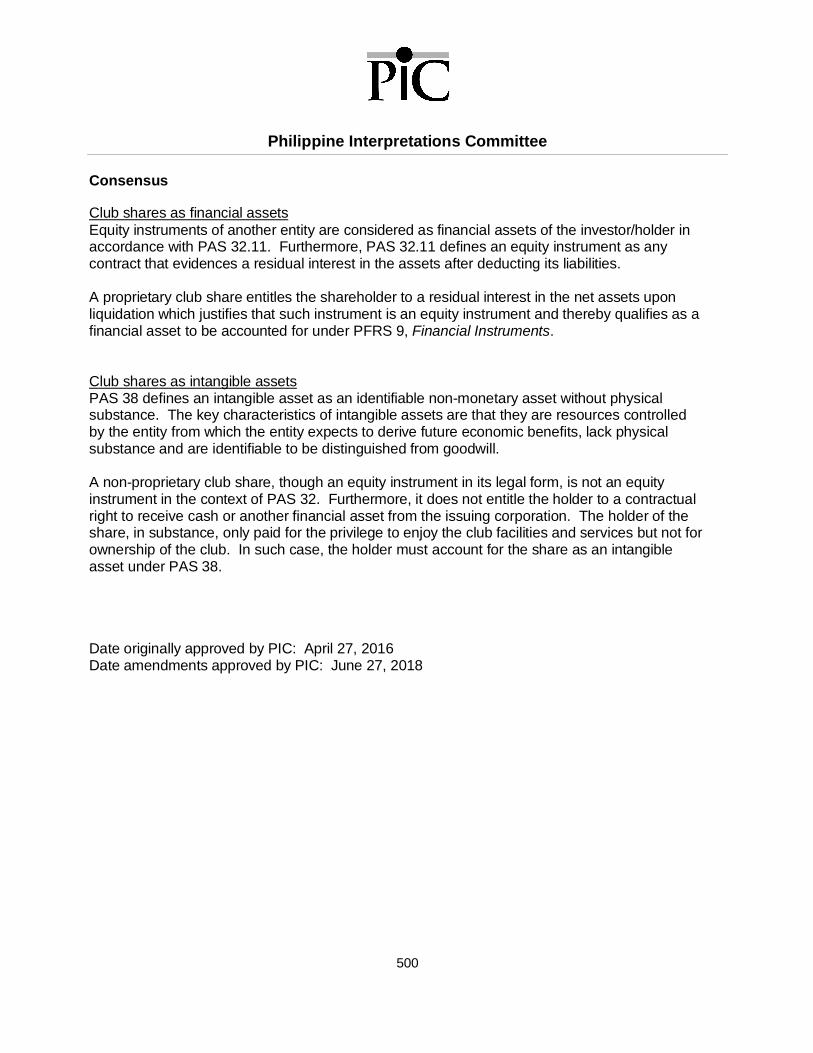

Q&A No. 2016-02: PAS 32 and PAS 38 (amended June 2018) – Accounting Treatment ofClub Shares Held by an Entity ......................................................................................... 472

Philippine Interpretations Committee

vi

Q&A No. 2017 – 11: PFRS 10 and PAS 32 - Transaction costs incurred to acquireoutstanding non-controlling interest or to sell non-controlling interest without a loss ofcontrol .............................................................................................................................. 476

Q&A No. 2019 – 07: Classification of Members’ Capital Contributions of Non-Stock Savingsand Loan Associations (NSSLA) ...................................................................................... 481

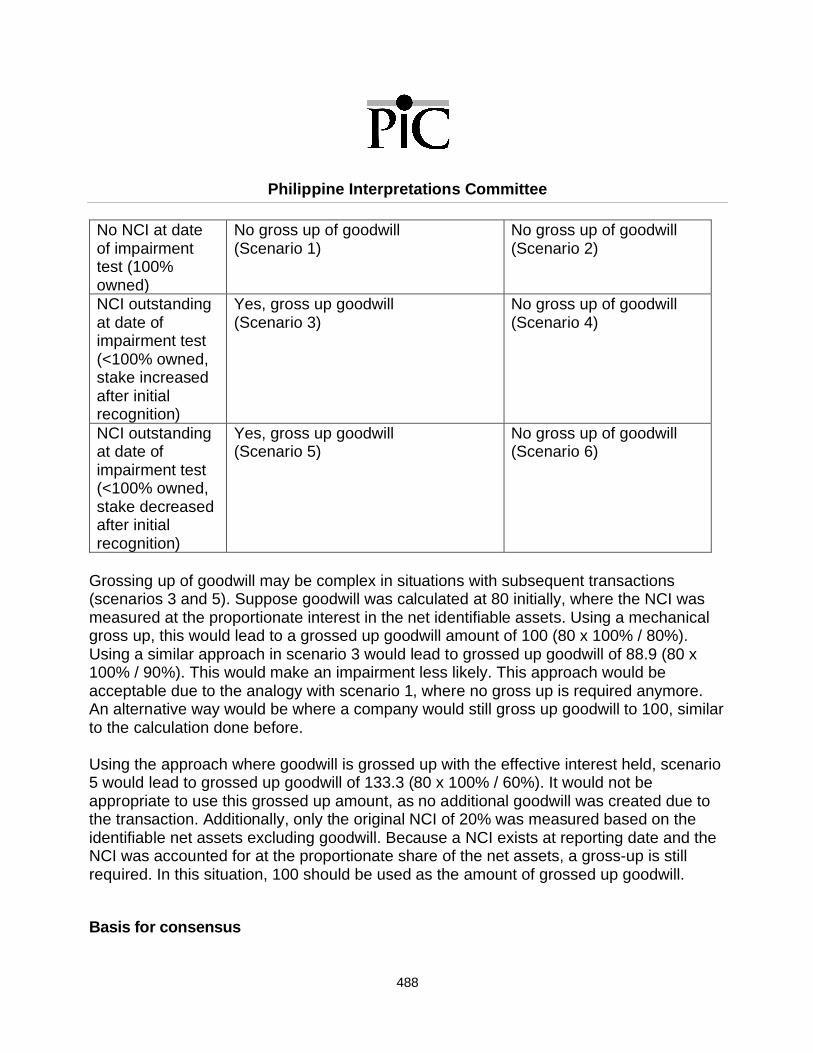

PAS 36, Impairment of Assets ............................................................................................. 486

Q&A No. 2018-02: PAS 36 - Non-controlling interests and goodwill impairment test ........ 486

Q&A No. 2018 - 03: PFRS 13, PAS 16 and PAS 36 - Fair value of property, plant andequipment and depreciated replacement cost .................................................................. 491

PAS 37, Provisions, Contingent Liabilities and Contingent Assets ....................................... 495

Q&A No. 2018 – 05 (amended July 2019): PAS 37 - Liability arising from maintenancerequirement of an asset held under a lease ..................................................................... 495

PAS 38, Intangible Assets ................................................................................................... 498

Q&A No. 2016-02: PAS 32 and PAS 38 (amended June 2018) – Accounting Treatment ofClub Shares Held by an Entity ......................................................................................... 498

Q&A No. 2019 - 02: Accounting For Cryptographic Assets .............................................. 502

PAS 40, Investment Property .............................................................................................. 514

Q&A No. 2007 – 03: PAS 40.27 – Valuation of bank real and other properties acquired(ROPA) ............................................................................................................................ 514

Q&A No. 2012 - 02: Cost of a new building constructed on the site of a previous building ........................................................................................................................................ 516

Q&A No. 2017 - 06: PAS 2, 16 and 40 – Accounting for Collector’s Items ....................... 524

Q&A No. 2017 – 10 (amended July 2019): PAS 40 - Separation of property andclassification as investment property ................................................................................ 528

Q&A No. 2018 - 11: Classification of land by real estate developer .................................. 533

PAS 41, Agriculture ............................................................................................................. 539

Q&A No. 2018 – 04: PAS 41 - Inability to measure fair value reliably for biological assetswithin the scope of PAS 41, Agriculture ........................................................................... 539

Amended PIC Q&As as of June 30, 2021 ............................................................................. 543Q&A No. 2006 – 02 (amended May 2017): PFRS 10.4(a) - Clarification of criteria forexemption from presenting consolidated financial statements .......................................... 544

Philippine Interpretations Committee

vii

Q&A No. 2008–01 (amended April 2016): PAS 19.83 – Rate used in discounting post-employment benefit obligations ........................................................................................ 546

Q&A No. 2009 – 01 (amended June 2018): Framework.4.1 and PAS 1.25 - Financialstatements prepared on a basis other than going concern ............................................... 548

Q&A No. 2010 – 02 (amended June 2018): PAS 1R.16 – Basis of preparation of financialstatements ....................................................................................................................... 552

Q&A No. 2011 – 03 (amended June 2020): Accounting for Inter-company Loans ............ 556

Q&A No. 2011 – 04 (amended June 2018): PAS 32.37-38 – Costs of Public Offering ofShares ............................................................................................................................. 564

Q&A No. 2011 – 05 (amended June 2018): PFRS 1.D1-D8 – Fair Value or Revaluation asDeemed Cost ................................................................................................................... 570

Q&A No. 2012 – 01 (amended June 2018): PFRS 3.2 – Application of the Pooling ofInterests Method for Business Combinations of Entities under Common Control inConsolidated Financial Statements .................................................................................. 578

Q&A No. 2016 – 02 (amended June 2018): PAS 32 and PAS 38 – Accounting Treatment ofClub Shares Held by an Entity ......................................................................................... 589

Q&A No. 2016 – 03 (amended June 2020): Accounting for Common Areas and the RelatedSubsequent Costs by Condominium Corporations ........................................................... 593

Q&A No. 2017 – 05 (amended June 2018): PFRS 7 – Frequently asked questions on thedisclosure requirements of financial instruments under PFRS 7, Financial Instruments:Disclosures ...................................................................................................................... 598

Q&A No. 2018 – 07 (amended June 2018): PAS 27 and PAS 28 - Cost of an associate,joint venture, or subsidiary in separate financial statements ............................................. 605

Q&A No. 2011 – 05 (amended July 2019): PFRS 1.D1-D8 – Fair Value or Revaluation asDeemed Cost ................................................................................................................... 610

Q&A No. 2011 - 06 (amended July 2019): PFRS 3, Business Combinations (2008), andPAS 40, Investment Property – Acquisition of investment properties – asset acquisition orbusiness combination?..................................................................................................... 619

Q&A No. 2012 – 02 (amended July 2019): Cost of a new building constructed on the site ofa previous building ........................................................................................................... 629

Q&A No. 2017 – 02 (amended July 2019): Capitalization of operating lease costdepreciation of right-of-use asset as part of construction costs of a building .................... 637

Philippine Interpretations Committee

viii

Q&A No. 2017 – 10 (amended July 2019): PAS 40 - Separation of property andclassification as investment property ................................................................................ 642

Q&A No. 2018 - 05 (amended July 2019): PAS 37 - Liability arising from maintenancerequirement of an asset held under a lease ..................................................................... 647

Q&A No. 2018 – 15 (amended July 2019): PAS 1- Classification of Advances toContractors in the Nature of Prepayments: Current vs. Non-current ................................ 650

Q&A No. 2009 – 01 (amended June 2020): Framework 3.94.1 and PAS 1.25 - Financialstatements prepared on a basis other than going concern ............................................... 655

Q&A No. 2011 – 03 (amended June 2020): Accounting for Inter-company Loans1........... 659

Q&A No. 2016-03 (amended June 2020): Accounting for Common Areas and the RelatedSubsequent Costs by Condominium Corporations ........................................................... 668

Q&A No. 2017 – 08 (amended June 2020): PFRS 10 – Requirement to prepareconsolidated financial statements where an entity disposes of its single investment in asubsidiary, associate or joint venture ............................................................................... 673

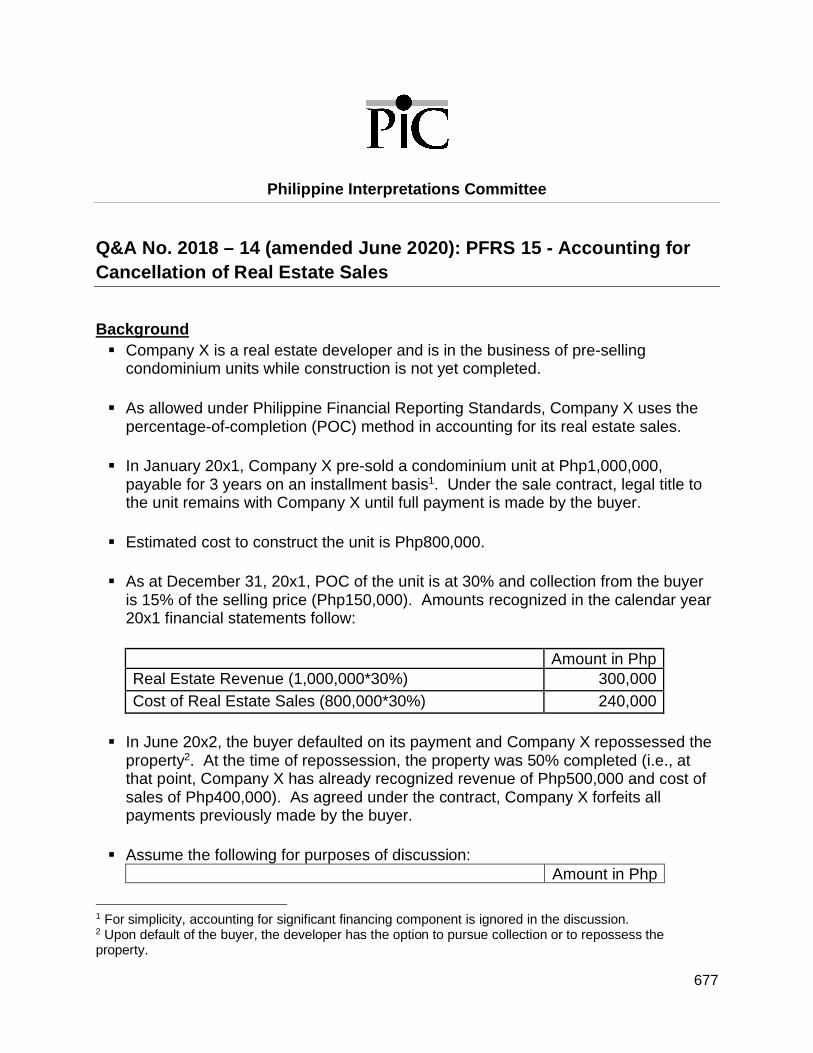

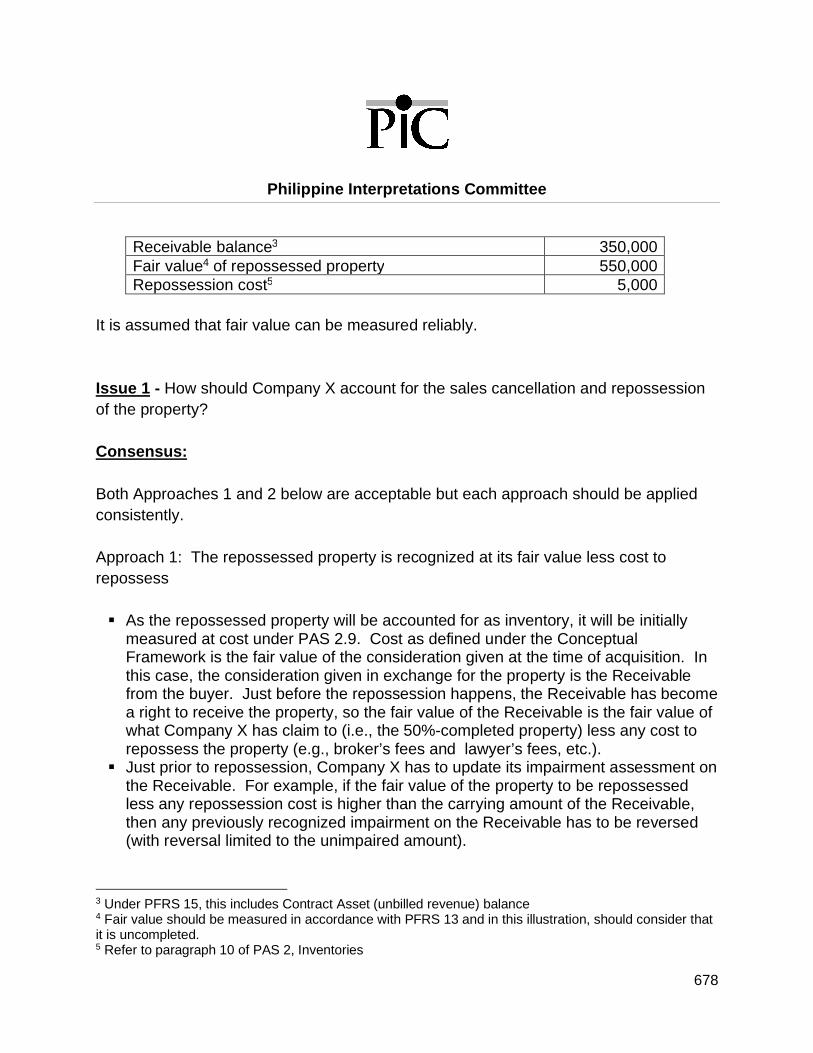

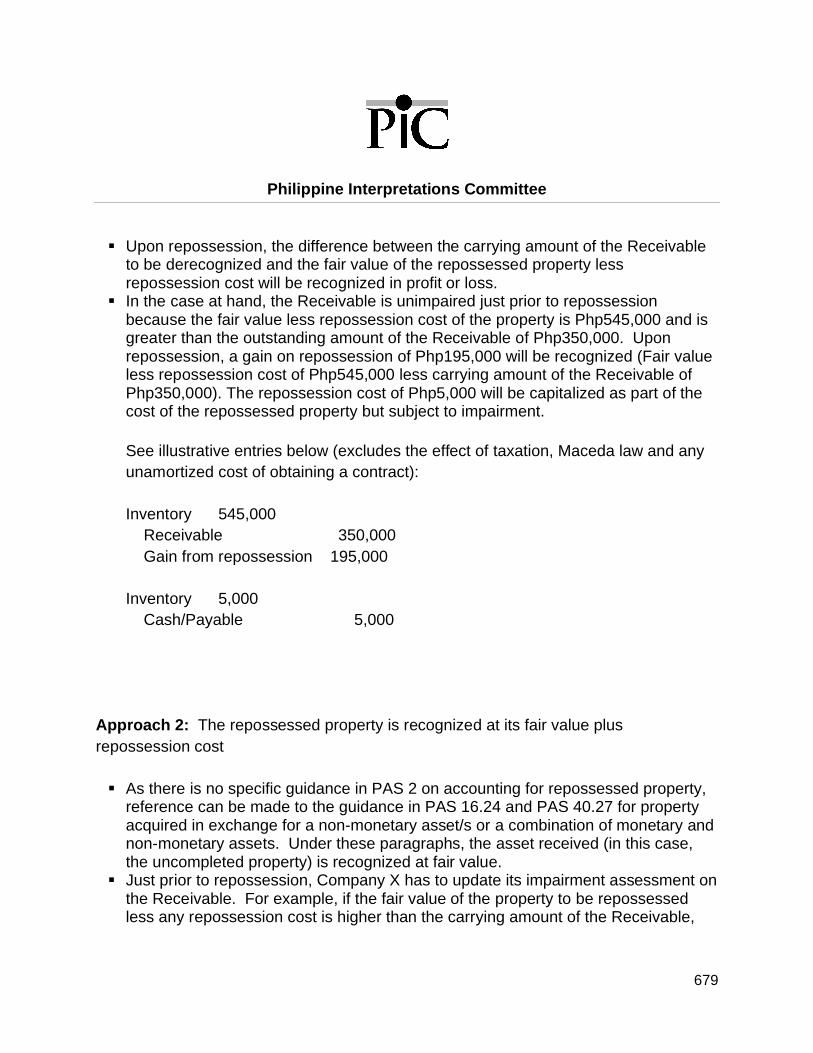

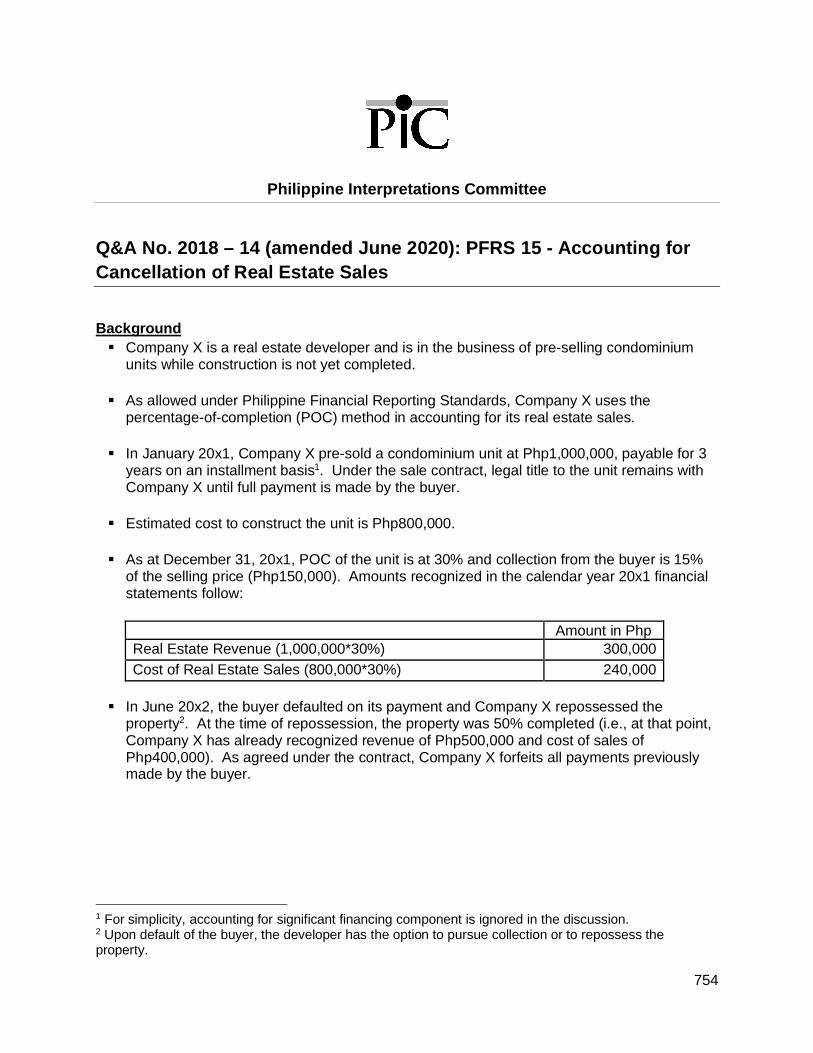

Q&A No. 2018 – 14 (amended June 2020): PFRS 15 - Accounting for Cancellation of RealEstate Sales ..................................................................................................................... 677

Withdrawn and superseded PIC Q&As as of June 30, 2021 ............................................... 688Q&A No. 2006 – 01: PAS 18, Appendix, paragraph 9 – Revenue recognition for sales ofproperty units under pre-completion contracts ................................................................. 689

Q&A No. 2007 – 01: PAS 1.103(a) – Basis of preparation of financial statements if an entityhas not applied PFRSs in full ........................................................................................... 693

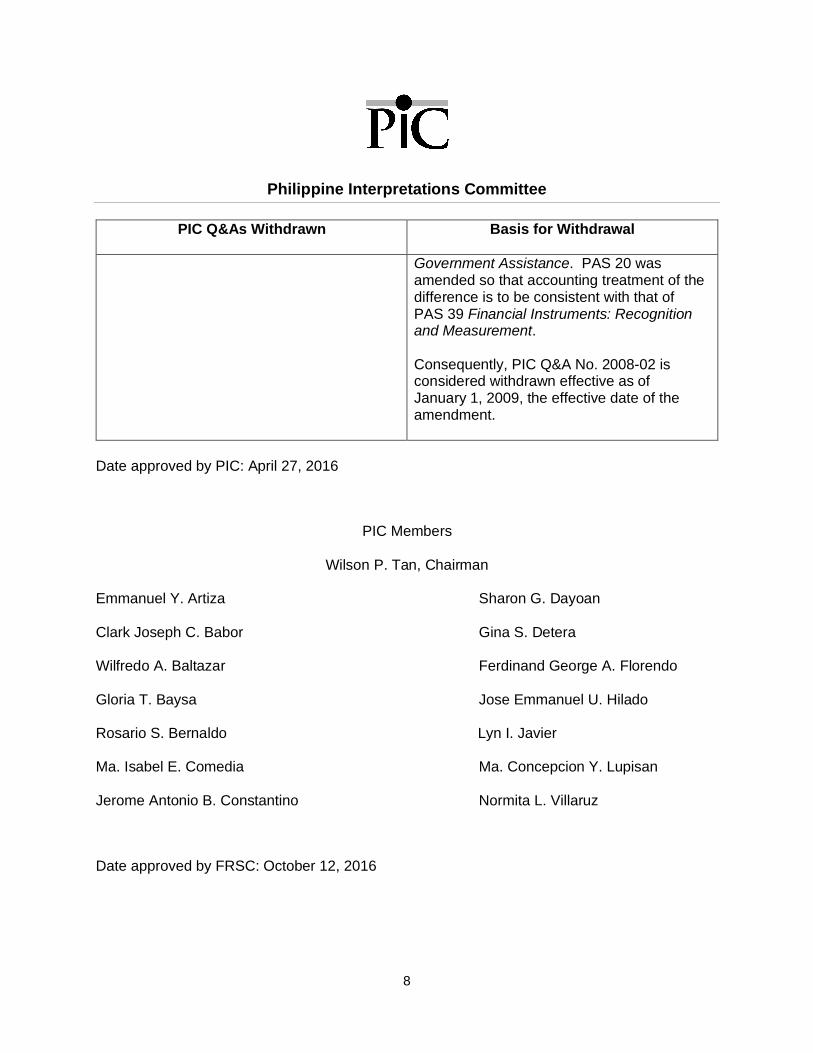

Q&A No. 2007 – 02: PAS 20.24, 20.37 and PAS 39.43 – Accounting for government loanswith low interest rates ...................................................................................................... 697

Q&A No. 2007 – 04: PAS 101.7 – Application of criteria for a qualifying NPAE ................ 700

Q&A No. 2008 – 01: PAS 19.78 – Rate used in discounting post-employment benefitobligations........................................................................................................................ 702

Q&A No. 2008 – 02: PAS 20.43 – Accounting for government loans with low interest ratesunder the amendments to PAS 20 ................................................................................... 704

Q&A No. 2009 – 02: PAS 39.AG71-72 – Rate used in determining the fair value ofgovernment securities in the Philippines .......................................................................... 707

Q&A No. 2010 – 01: PAS 39.AG71-72 – Rate used in determining the fair value ofgovernment securities in the Philippines .......................................................................... 715

Philippine Interpretations Committee

ix

Q&A No. 2011 - 01: PAS 1.10(f) – Requirements for a Third Statement of Financial Position ........................................................................................................................................ 726

Q&A No. 2011 – 06 (amended July 2019): PFRS 3, Business Combinations (2008), andPAS 40, Investment Property – Acquisition of investment properties – asset acquisition orbusiness combination?..................................................................................................... 732

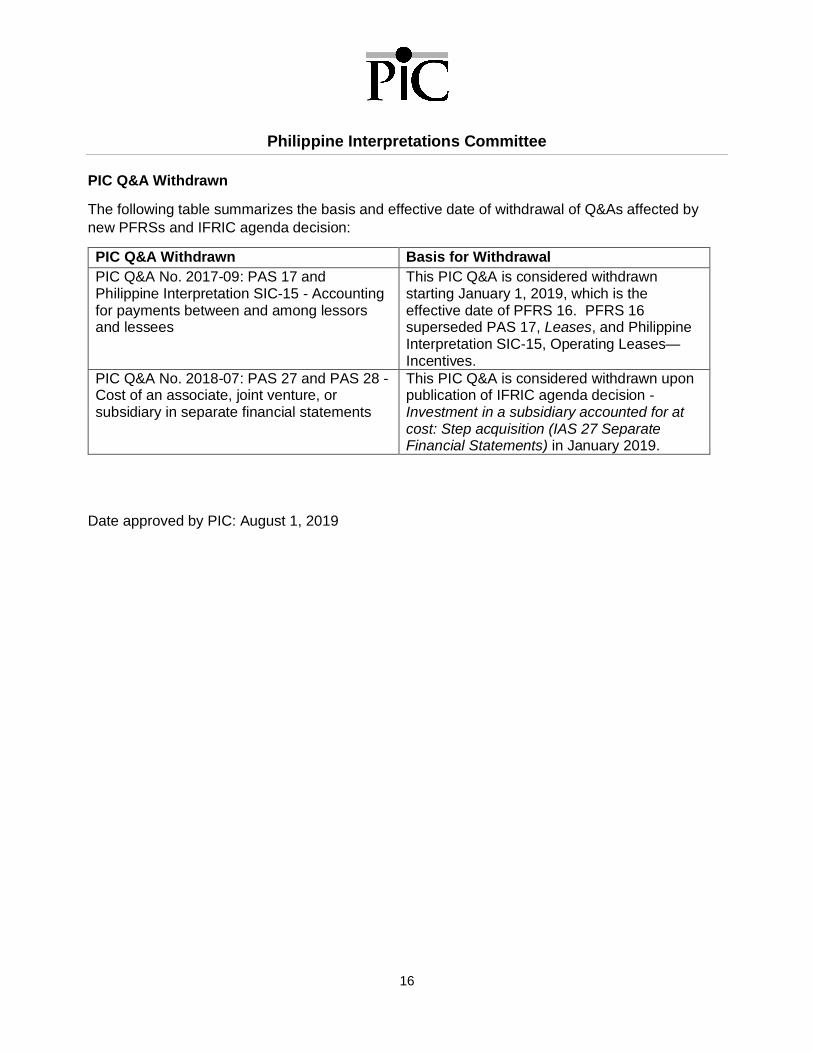

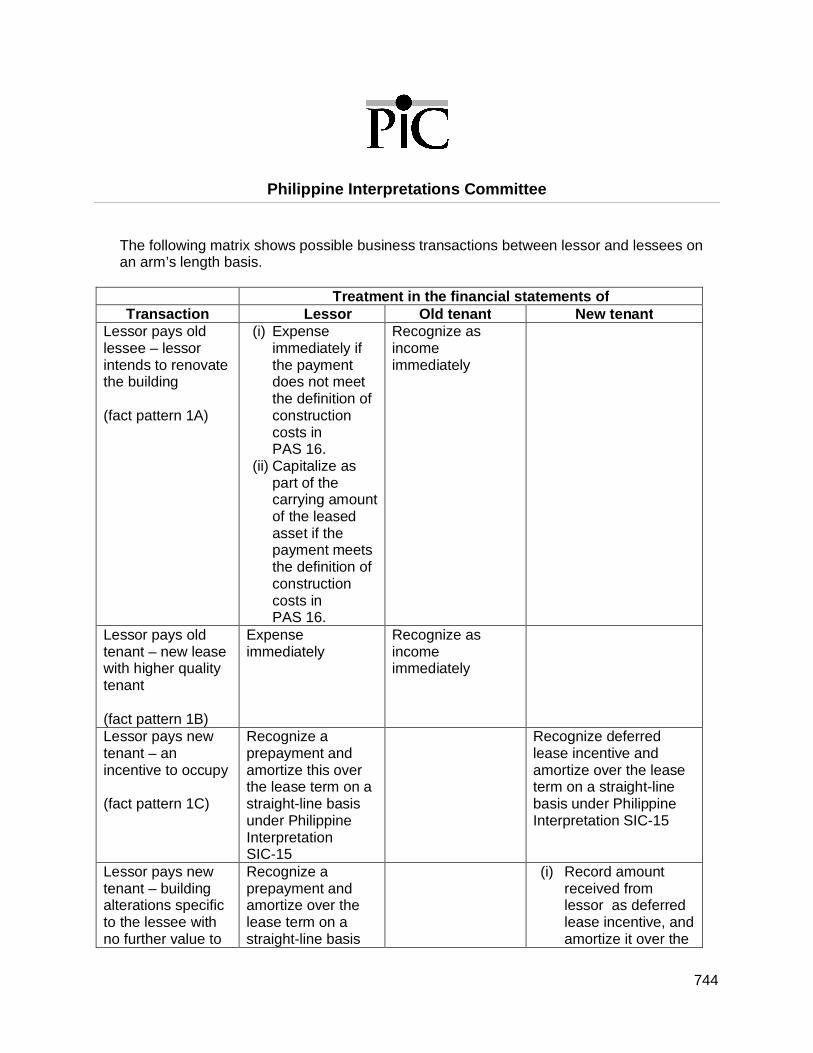

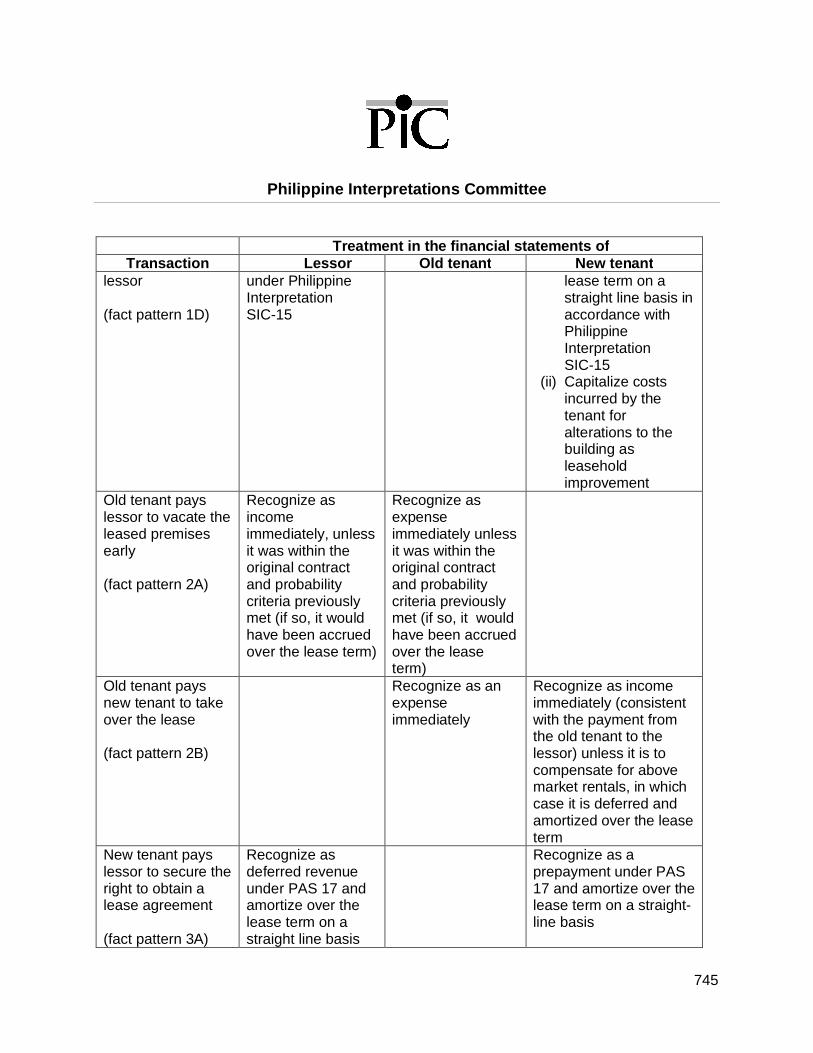

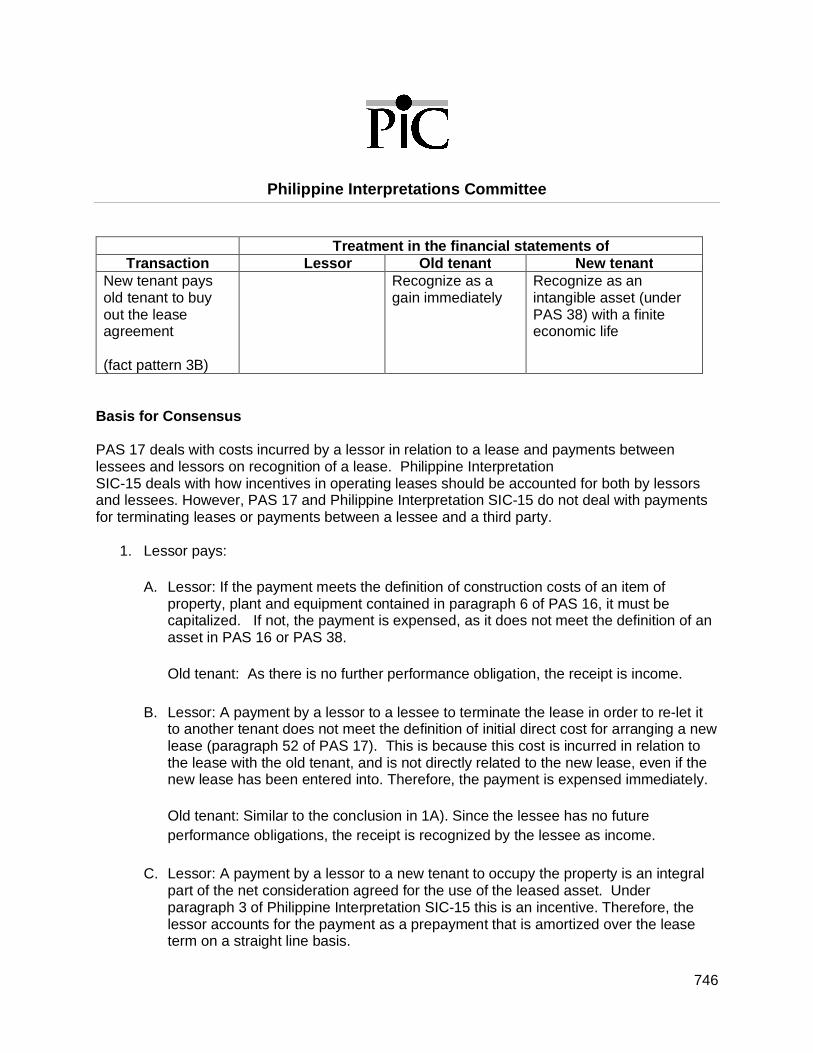

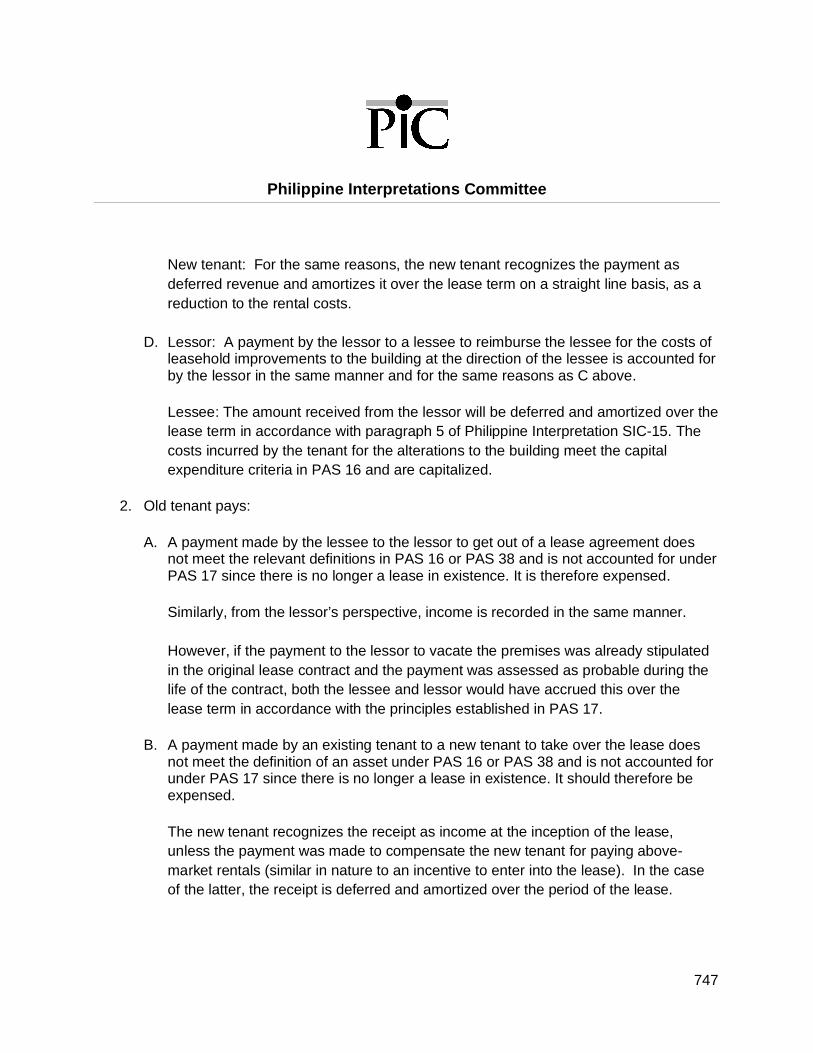

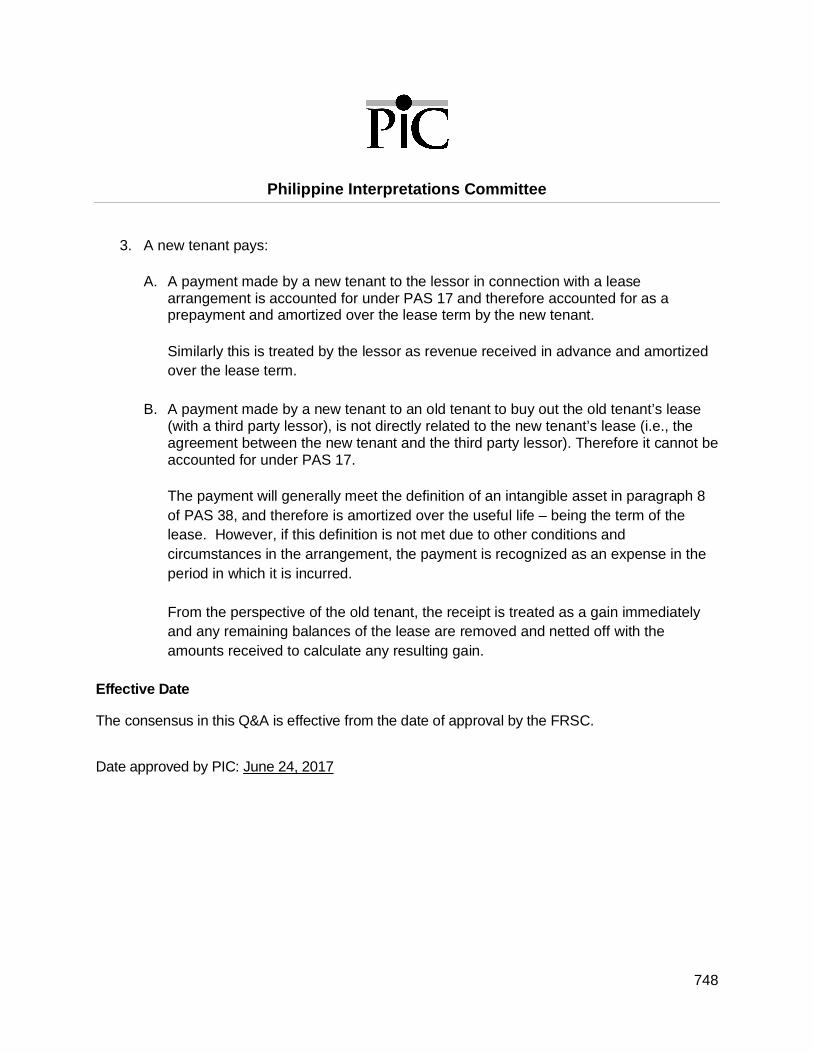

Q&A No. 2017 – 09: PAS 17 and Philippine Interpretation SIC-15 - Accounting forpayments between and among lessors and lessees ........................................................ 741

Q&A No. 2018 – 07 (amended June 2018): PAS 27 and PAS 28 - Cost of an associate,joint venture, or subsidiary in separate financial statements ............................................. 750

Q&A No. 2018 – 14 (amended June 2020): PFRS 15 - Accounting for Cancellation of RealEstate Sales ..................................................................................................................... 754

PFRS for Small and Medium-sized Entities (SMEs) ............................................................. 764

Q&A No. 2013 - 01: Applicability of SMEIG Final Q&As on the application of IFRS for SMEsto Philippine SMEs ........................................................................................................... 764

Appendix ............................................................................................................................... 767List of Approved Q&As as of June 30, 2021 by date of issuance ......................................... 767

Philippine Interpretations Committee

x

Preface

The International Financial Reporting Standards (IFRSs), locally referred to as PhilippineFinancial Reporting Standards (PFRSs), has become a buzzword, not only in the accountingworld, but also in the business sector. The initial adoption of PFRSs in 2005 was one of themost daunting tasks as far as application of the accounting standards is concerned. This difficulttask continues to date. The continuing review and revisions or amendments of the PFRSs andthe actual implementation of these standards continue to pose challenges for both the usersand the preparers of financial statements.

Being principles-based standards, there are instances when provisions of PFRSs require theexercise of significant judgment in its interpretation. Hence, guidance is needed in theimplementation of these standards. The need for such guidance was what prompted thecreation of the Philippine Interpretations Committee or PIC.

The main objective of the PIC is to provide implementation guidance on Philippine AccountingStandards (PASs) and Philippine Financial Reporting Standards (PFRSs) issued by theFinancial Reporting Standards Council (FRSC). These PASs and PFRSs are primarily basedon accounting pronouncements issued by the International Accounting Standards Board, theglobal standard-setting body that issues IFRSs.

Composed of 15 members from various accounting firms, business organizations, the academeand regulators, the PIC deals with accounting issues that are considered to have significantimpact to companies operating in the Philippines.

The main product of the work of the PIC is the PIC Questions and Answers (Q&As). These PICQ&As make reference to the related paragraphs in the PFRSs. The issues and the backgroundof such are discussed thoroughly, ending with a consensus that lead to their resolution and,hence, a clearer guidance in the implementation of the standards.

In the past, these Q&As were released individually. However, the current PIC members thinkthat it is high time that these Q&As be consolidated and issued in one comprehensivepublication that would be a valuable reference and a useful resource for users of financialaccounting information, whether they be from public practice, commerce, the academe or thegovernment.

Philippine Interpretations Committee

xi

This publication is the compilation of the PIC Q&As approved by the PIC as of June 30, 2021,grouped according to their related standards. It also contains the PIC Q&As superseded as ofthe same date.

Philippine Interpretations Committee

xii

Date approved by PIC: June 30, 2021

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Ma. Gracia F. Casals-Diaz

Christian Francis S. Felismino Zaldy D. Aguirre

Joeffrey Mark P. Ferrer Ferdinand George A. Florendo

Gerry I. Piator Eduardo M. Olbes

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Arnel Onesimo O. Uy

Jerome Antonio B. Constantino Lovely M. Del Amen-Aquino

Date approved by FRSC: August 11, 2021

Philippine Interpretations Committee

1

Approved PIC Q&As as ofJune 30, 2021

Philippine Interpretations Committee

2

General Q&As

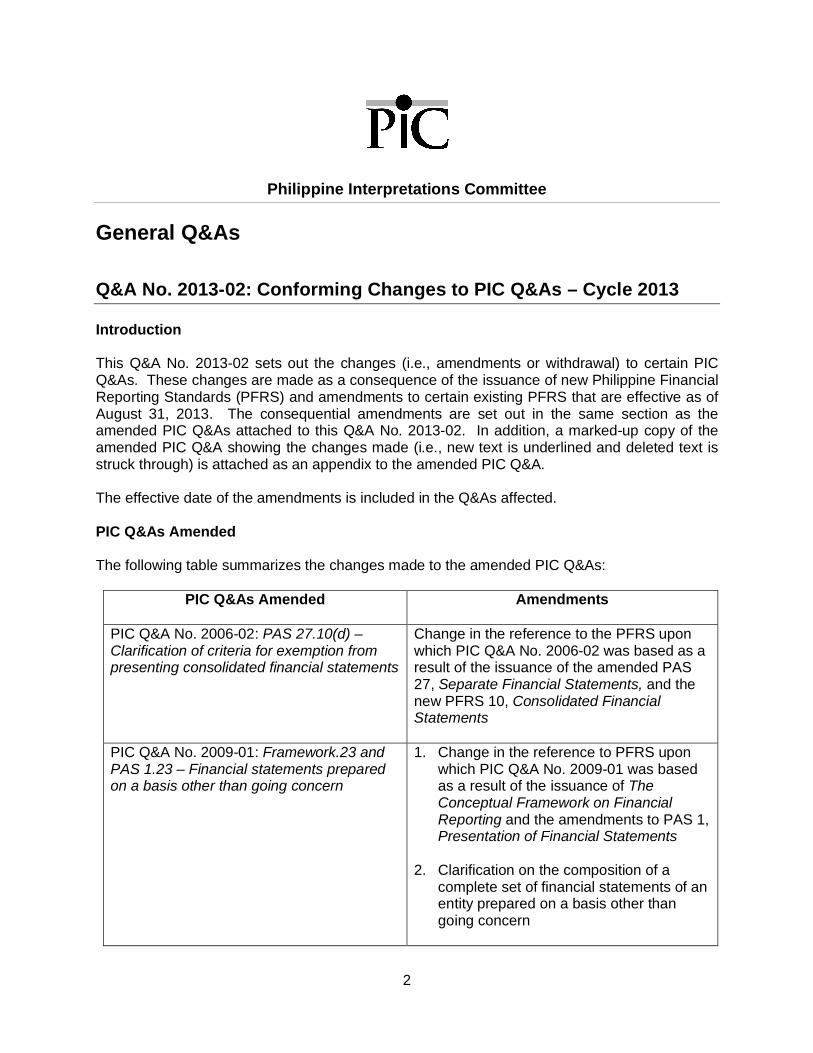

Q&A No. 2013-02: Conforming Changes to PIC Q&As – Cycle 2013

Introduction

This Q&A No. 2013-02 sets out the changes (i.e., amendments or withdrawal) to certain PICQ&As. These changes are made as a consequence of the issuance of new Philippine FinancialReporting Standards (PFRS) and amendments to certain existing PFRS that are effective as ofAugust 31, 2013. The consequential amendments are set out in the same section as theamended PIC Q&As attached to this Q&A No. 2013-02. In addition, a marked-up copy of theamended PIC Q&A showing the changes made (i.e., new text is underlined and deleted text isstruck through) is attached as an appendix to the amended PIC Q&A.

The effective date of the amendments is included in the Q&As affected.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&As Amended Amendments

PIC Q&A No. 2006-02: PAS 27.10(d) –Clarification of criteria for exemption frompresenting consolidated financial statements

Change in the reference to the PFRS uponwhich PIC Q&A No. 2006-02 was based as aresult of the issuance of the amended PAS27, Separate Financial Statements, and thenew PFRS 10, Consolidated FinancialStatements

PIC Q&A No. 2009-01: Framework.23 andPAS 1.23 – Financial statements preparedon a basis other than going concern

1. Change in the reference to PFRS uponwhich PIC Q&A No. 2009-01 was basedas a result of the issuance of TheConceptual Framework on FinancialReporting and the amendments to PAS 1,Presentation of Financial Statements

2. Clarification on the composition of acomplete set of financial statements of anentity prepared on a basis other thangoing concern

Philippine Interpretations Committee

3

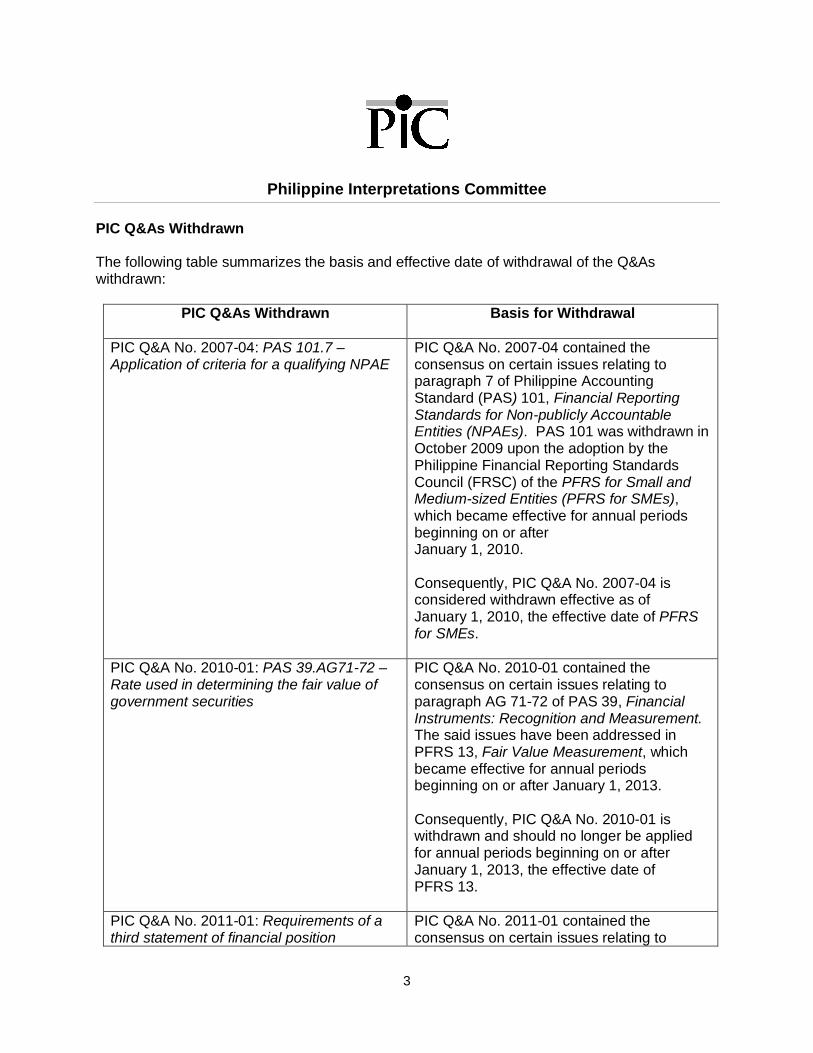

PIC Q&As Withdrawn

The following table summarizes the basis and effective date of withdrawal of the Q&Aswithdrawn:

PIC Q&As Withdrawn Basis for Withdrawal

PIC Q&A No. 2007-04: PAS 101.7 –Application of criteria for a qualifying NPAE

PIC Q&A No. 2007-04 contained theconsensus on certain issues relating toparagraph 7 of Philippine AccountingStandard (PAS) 101, Financial ReportingStandards for Non-publicly AccountableEntities (NPAEs). PAS 101 was withdrawn inOctober 2009 upon the adoption by thePhilippine Financial Reporting StandardsCouncil (FRSC) of the PFRS for Small andMedium-sized Entities (PFRS for SMEs),which became effective for annual periodsbeginning on or afterJanuary 1, 2010.

Consequently, PIC Q&A No. 2007-04 isconsidered withdrawn effective as ofJanuary 1, 2010, the effective date of PFRSfor SMEs.

PIC Q&A No. 2010-01: PAS 39.AG71-72 –Rate used in determining the fair value ofgovernment securities

PIC Q&A No. 2010-01 contained theconsensus on certain issues relating toparagraph AG 71-72 of PAS 39, FinancialInstruments: Recognition and Measurement.The said issues have been addressed inPFRS 13, Fair Value Measurement, whichbecame effective for annual periodsbeginning on or after January 1, 2013.

Consequently, PIC Q&A No. 2010-01 iswithdrawn and should no longer be appliedfor annual periods beginning on or afterJanuary 1, 2013, the effective date ofPFRS 13.

PIC Q&A No. 2011-01: Requirements of athird statement of financial position

PIC Q&A No. 2011-01 contained theconsensus on certain issues relating to

Philippine Interpretations Committee

4

PIC Q&As Withdrawn Basis for Withdrawal

paragraph 10 (f) of PAS 1, Presentation ofFinancial Statements. The said issues havebeen clarified upon the issuance of theAnnual Improvements to PFRS 2009-2011Cycle, which became effective for annualperiods beginning on or after January 1,2013.

Consequently, PIC Q&A No. 2011-01 iswithdrawn and should no longer be appliedfor annual periods beginning on or afterJanuary 1, 2013, the effective date of theAnnual Improvements to PFRS 2009-2011Cycle.

Date approved by PIC: September 25, 2013

PIC Members

Dalisay B. Duque, Chairman

Wilfredo A. Baltazar Edmund A. Go

Rosario S. Bernaldo Lyn I. Javier

Sharon S. Dayoan Ma. Concepcion Y. Lupisan

Gina S. Detera Wilson P. Tan

Ma. Gracia F. Casals-Diaz Normita L. Villaruz

Date approved by FRSC: October 8, 2014

Philippine Interpretations Committee

5

Q&A No. 2015-01: Conforming Changes to PIC Q&As – Cycle 2015

Introduction

This Q&A No. 2015-01 sets out the amendments to certain PIC Q&As. These changes are madeas a consequence of the issuance of new Philippine Financial Reporting Standards (PFRS) andamendments to certain existing PFRS that are effective as of January 1, 2013. The consequentialamendments are set out in the same section as the amended PIC Q&As attached to this Q&ANo. 2015-01. In addition, a marked-up copy of the amended PIC Q&A showing the changesmade (i.e., new text is underlined and deleted text is struck through) is attached as an appendixto the amended PIC Q&A.

The effective date of the amendments is included in the Q&As affected.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&As Amended Amendments

PIC Q&A No. 2012-01: PFRS 3.2 –Application of the Pooling of Interests Methodfor Business Combinations of Entities underCommon Control in Consolidated FinancialStatements

Change in the reference to the PFRS uponwhich PIC Q&A No. 2012-01 was based as aresult of the issuance of the amendedPAS 27, Separate Financial Statements, andthe new PFRS 10, Consolidated FinancialStatements

PIC Q&A No. 2011-03: Accounting for Inter-company Loans

1. Change in the reference to PFRS uponwhich PIC Q&A No. 2011-03 was basedas a result of the following:

a. Issuance of The ConceptualFramework on Financial Reporting

b. Issuance of the amended PAS 27,Separate Financial Statements, andPAS 28, Consolidated FinancialStatements

2. Minor changes in the wordings

Date approved by PIC: July 29, 2015

Philippine Interpretations Committee

6

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Sharon G. Dayoan

Clark Joseph C. Babor Gina S. Detera

Wilfredo A. Baltazar Ferdinand George A. Florendo

Gloria T. Baysa Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Ma. Concepcion Y. Lupisan

Jerome Antonio B. Constantino Normita L. Villaruz

Date approved by FRSC: October 14, 2015

Philippine Interpretations Committee

7

Q&A No. 2016-01: Conforming Changes to PIC Q&As – Cycle 2016

Introduction

This Q&A No. 2016-01 sets out the changes (i.e., amendments or withdrawal) to certain PICQ&As. These changes are made as a consequence of the issuance of new Philippine FinancialReporting Standards (PFRS) and amendments to certain existing PFRS that are effective as ofDecember 31, 2015. The consequential amendments are set out in the same section as theamended PIC Q&As attached to this Q&A No. 2016-01. In addition, a marked-up copy of theamended PIC Q&A showing the changes made (i.e., new text is underlined and deleted text isstruck through) is attached as an appendix to the amended PIC Q&A.

The effective date of the amendments is included in the Q&As affected.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&As Amended Amendments

PIC Q&A No. 2008-01: Rate used indiscounting post-employment benefitobligations

Changed in the reference to the PFRS uponwhich PIC Q&A No. 2008-01 was based as aresult of the issuance of the revised PAS 19,Employee Benefits.

PIC Q&A No. 2011-05: Fair Value orRevaluation as Deemed Cost

Deleted reference to PIC Q&A No. 2011-01,which was withdrawn in 2013.

PIC Q&As Withdrawn

The following table summarizes the basis and effective date of withdrawal of the Q&Aswithdrawn:

PIC Q&As Withdrawn Basis for Withdrawal

PIC Q&A No. 2008-02: PAS 20.43 –Accounting for Government Loans with LowInterest Rates

PIC Q&A No. 2008-02 contained theconsensus on certain issue relating toparagraph 43 of Philippine AccountingStandard (PAS) 20, Accounting forGovernment Grants and Disclosure of

Philippine Interpretations Committee

8

PIC Q&As Withdrawn Basis for Withdrawal

Government Assistance. PAS 20 wasamended so that accounting treatment of thedifference is to be consistent with that ofPAS 39 Financial Instruments: Recognitionand Measurement.

Consequently, PIC Q&A No. 2008-02 isconsidered withdrawn effective as ofJanuary 1, 2009, the effective date of theamendment.

Date approved by PIC: April 27, 2016

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Sharon G. Dayoan

Clark Joseph C. Babor Gina S. Detera

Wilfredo A. Baltazar Ferdinand George A. Florendo

Gloria T. Baysa Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Ma. Concepcion Y. Lupisan

Jerome Antonio B. Constantino Normita L. Villaruz

Date approved by FRSC: October 12, 2016

Philippine Interpretations Committee

9

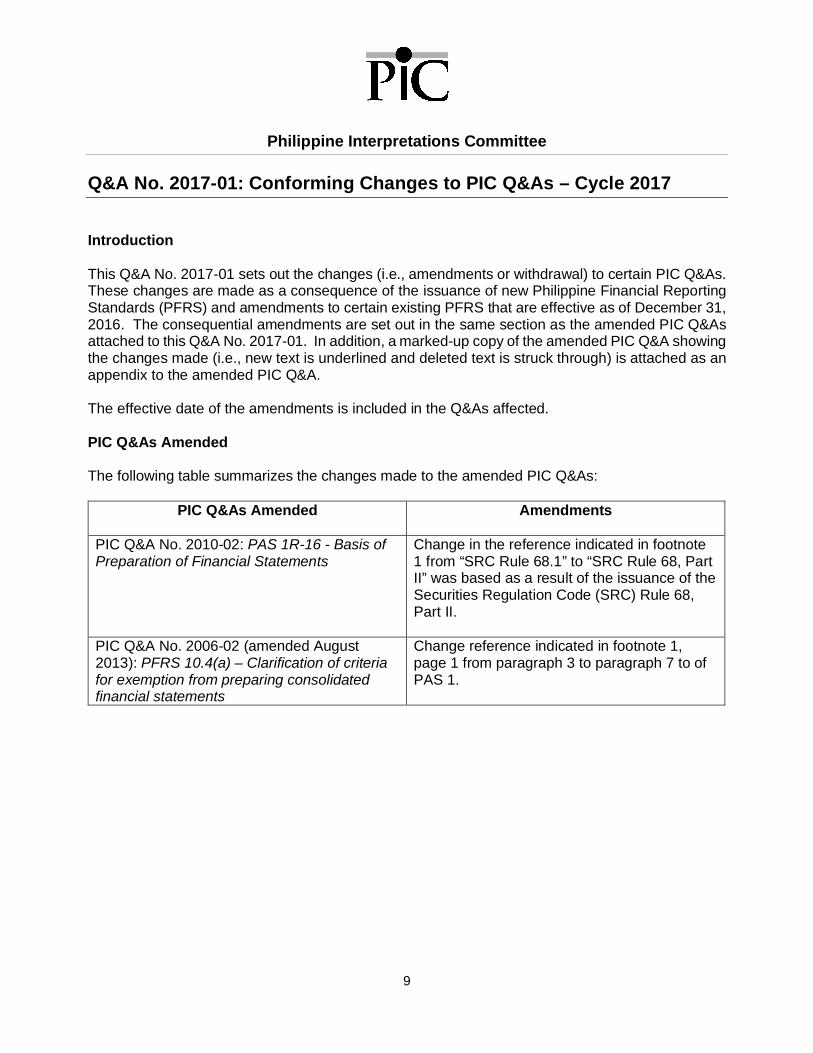

Q&A No. 2017-01: Conforming Changes to PIC Q&As – Cycle 2017

Introduction

This Q&A No. 2017-01 sets out the changes (i.e., amendments or withdrawal) to certain PIC Q&As.These changes are made as a consequence of the issuance of new Philippine Financial ReportingStandards (PFRS) and amendments to certain existing PFRS that are effective as of December 31,2016. The consequential amendments are set out in the same section as the amended PIC Q&Asattached to this Q&A No. 2017-01. In addition, a marked-up copy of the amended PIC Q&A showingthe changes made (i.e., new text is underlined and deleted text is struck through) is attached as anappendix to the amended PIC Q&A.

The effective date of the amendments is included in the Q&As affected.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&As Amended Amendments

PIC Q&A No. 2010-02: PAS 1R-16 - Basis ofPreparation of Financial Statements

Change in the reference indicated in footnote1 from “SRC Rule 68.1” to “SRC Rule 68, PartII” was based as a result of the issuance of theSecurities Regulation Code (SRC) Rule 68,Part II.

PIC Q&A No. 2006-02 (amended August2013): PFRS 10.4(a) – Clarification of criteriafor exemption from preparing consolidatedfinancial statements

Change reference indicated in footnote 1,page 1 from paragraph 3 to paragraph 7 to ofPAS 1.

Philippine Interpretations Committee

10

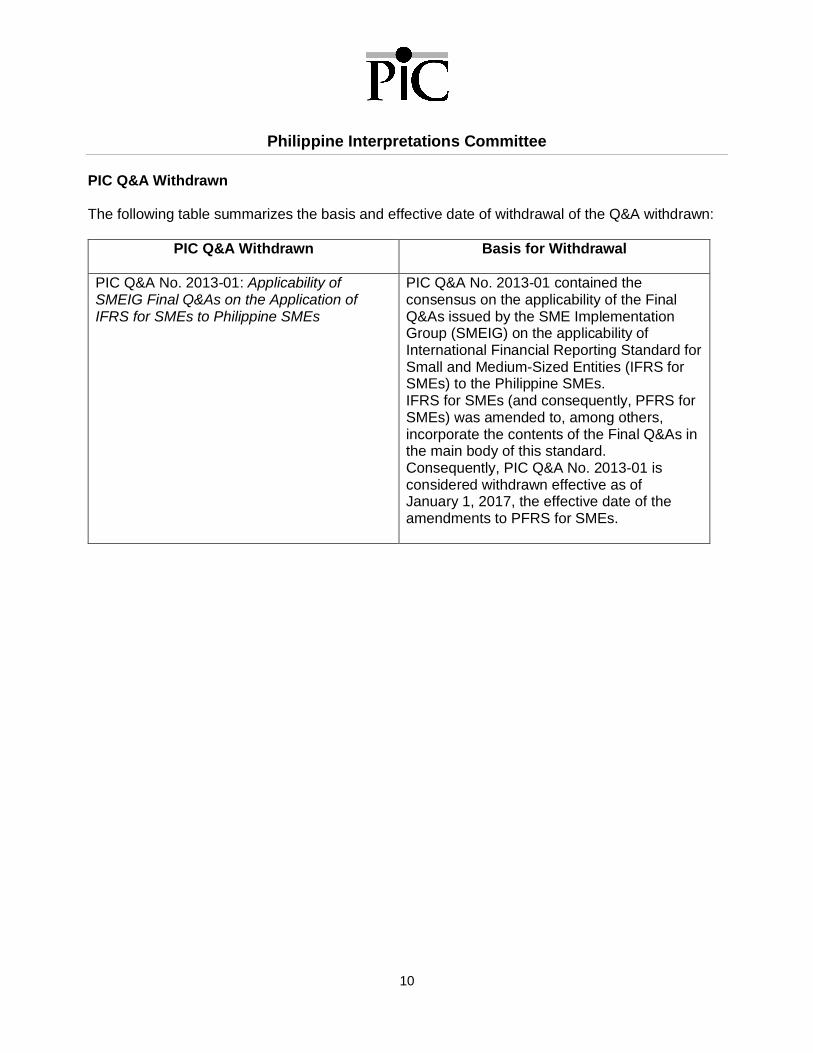

PIC Q&A Withdrawn

The following table summarizes the basis and effective date of withdrawal of the Q&A withdrawn:

PIC Q&A Withdrawn Basis for Withdrawal

PIC Q&A No. 2013-01: Applicability ofSMEIG Final Q&As on the Application ofIFRS for SMEs to Philippine SMEs

PIC Q&A No. 2013-01 contained theconsensus on the applicability of the FinalQ&As issued by the SME ImplementationGroup (SMEIG) on the applicability ofInternational Financial Reporting Standard forSmall and Medium-Sized Entities (IFRS forSMEs) to the Philippine SMEs.IFRS for SMEs (and consequently, PFRS forSMEs) was amended to, among others,incorporate the contents of the Final Q&As inthe main body of this standard.Consequently, PIC Q&A No. 2013-01 isconsidered withdrawn effective as ofJanuary 1, 2017, the effective date of theamendments to PFRS for SMEs.

Philippine Interpretations Committee

11

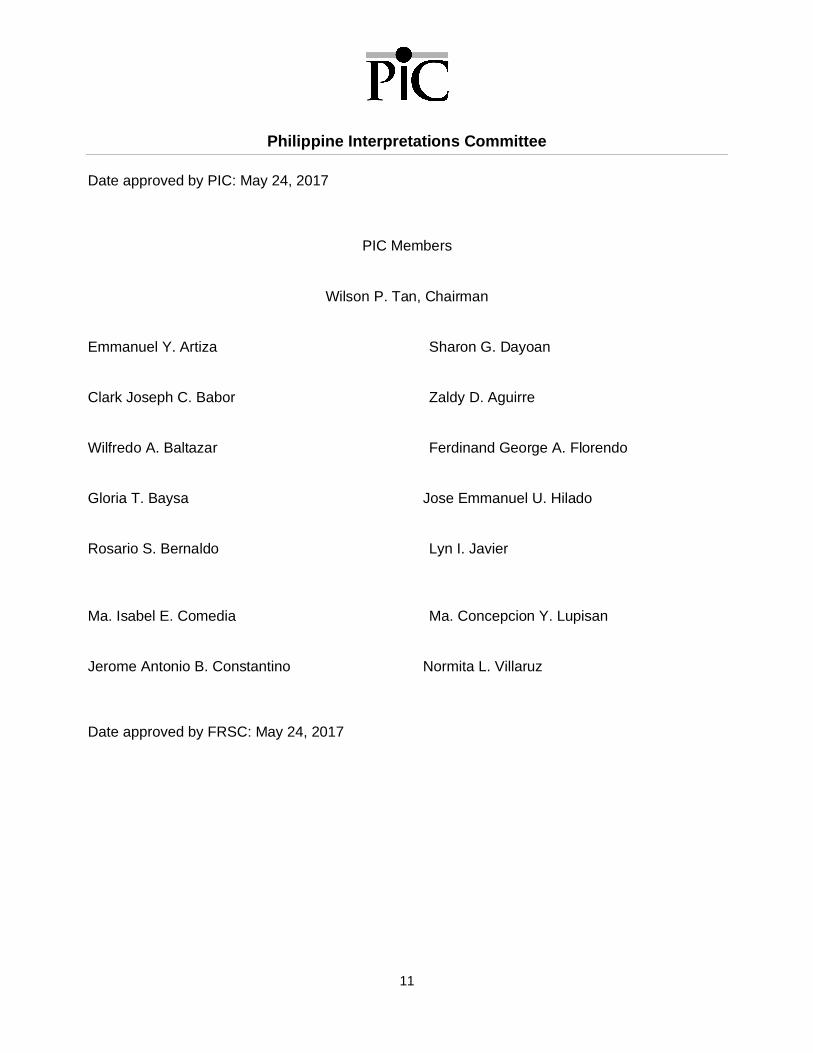

Date approved by PIC: May 24, 2017

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Sharon G. Dayoan

Clark Joseph C. Babor Zaldy D. Aguirre

Wilfredo A. Baltazar Ferdinand George A. Florendo

Gloria T. Baysa Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Ma. Concepcion Y. Lupisan

Jerome Antonio B. Constantino Normita L. Villaruz

Date approved by FRSC: May 24, 2017

Philippine Interpretations Committee

12

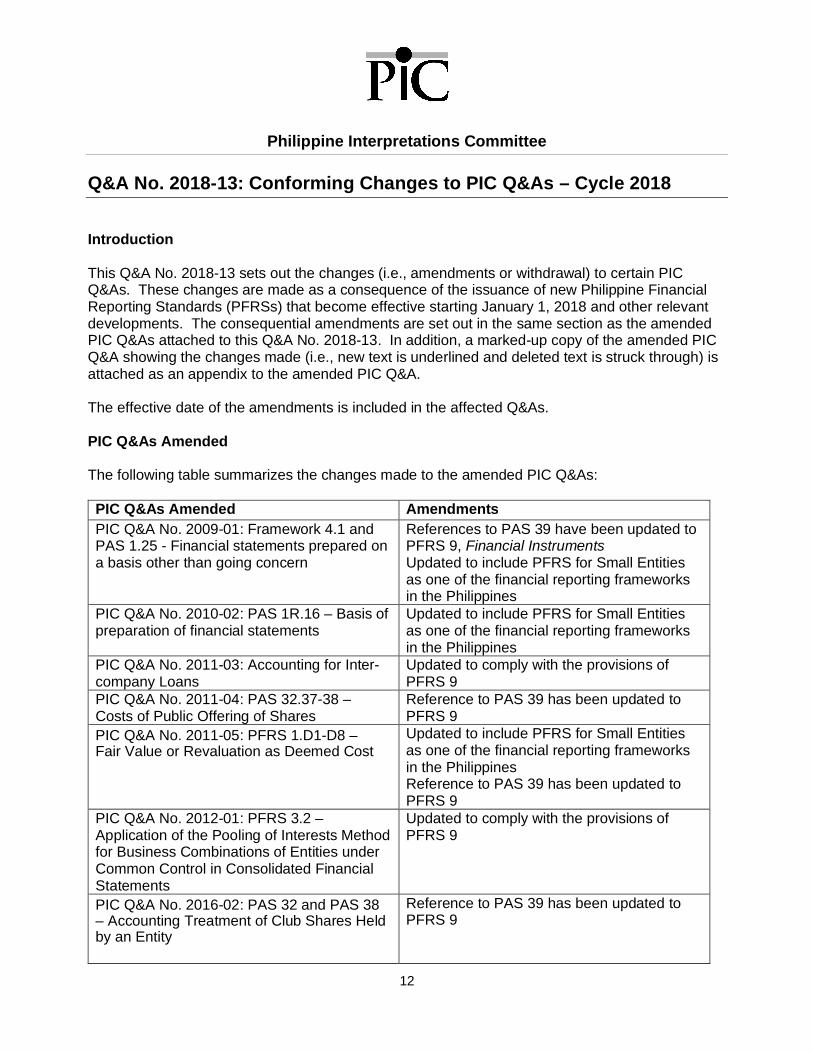

Q&A No. 2018-13: Conforming Changes to PIC Q&As – Cycle 2018

Introduction

This Q&A No. 2018-13 sets out the changes (i.e., amendments or withdrawal) to certain PICQ&As. These changes are made as a consequence of the issuance of new Philippine FinancialReporting Standards (PFRSs) that become effective starting January 1, 2018 and other relevantdevelopments. The consequential amendments are set out in the same section as the amendedPIC Q&As attached to this Q&A No. 2018-13. In addition, a marked-up copy of the amended PICQ&A showing the changes made (i.e., new text is underlined and deleted text is struck through) isattached as an appendix to the amended PIC Q&A.

The effective date of the amendments is included in the affected Q&As.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&As Amended AmendmentsPIC Q&A No. 2009-01: Framework 4.1 andPAS 1.25 - Financial statements prepared ona basis other than going concern

References to PAS 39 have been updated toPFRS 9, Financial InstrumentsUpdated to include PFRS for Small Entitiesas one of the financial reporting frameworksin the Philippines

PIC Q&A No. 2010-02: PAS 1R.16 – Basis ofpreparation of financial statements

Updated to include PFRS for Small Entitiesas one of the financial reporting frameworksin the Philippines

PIC Q&A No. 2011-03: Accounting for Inter-company Loans

Updated to comply with the provisions ofPFRS 9

PIC Q&A No. 2011-04: PAS 32.37-38 –Costs of Public Offering of Shares

Reference to PAS 39 has been updated toPFRS 9

PIC Q&A No. 2011-05: PFRS 1.D1-D8 –Fair Value or Revaluation as Deemed Cost

Updated to include PFRS for Small Entitiesas one of the financial reporting frameworksin the PhilippinesReference to PAS 39 has been updated toPFRS 9

PIC Q&A No. 2012-01: PFRS 3.2 –Application of the Pooling of Interests Methodfor Business Combinations of Entities underCommon Control in Consolidated FinancialStatements

Updated to comply with the provisions ofPFRS 9

PIC Q&A No. 2016-02: PAS 32 and PAS 38– Accounting Treatment of Club Shares Heldby an Entity

Reference to PAS 39 has been updated toPFRS 9

Philippine Interpretations Committee

13

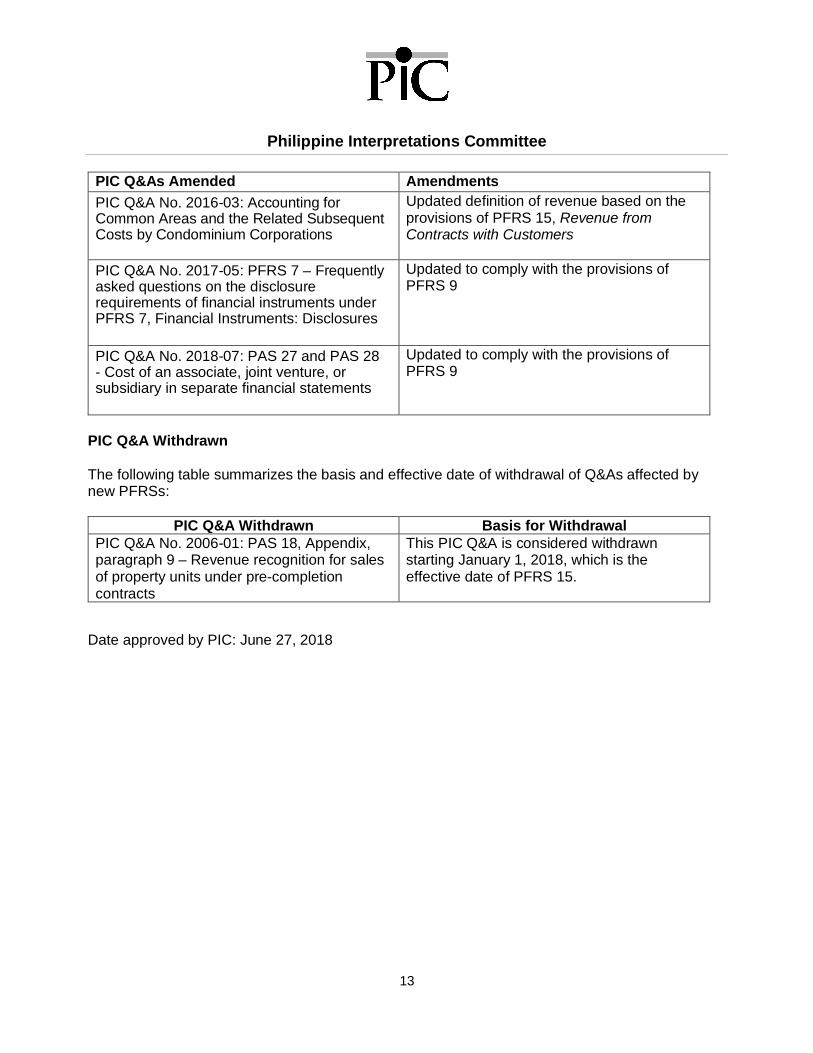

PIC Q&As Amended AmendmentsPIC Q&A No. 2016-03: Accounting forCommon Areas and the Related SubsequentCosts by Condominium Corporations

Updated definition of revenue based on theprovisions of PFRS 15, Revenue fromContracts with Customers

PIC Q&A No. 2017-05: PFRS 7 – Frequentlyasked questions on the disclosurerequirements of financial instruments underPFRS 7, Financial Instruments: Disclosures

Updated to comply with the provisions ofPFRS 9

PIC Q&A No. 2018-07: PAS 27 and PAS 28- Cost of an associate, joint venture, orsubsidiary in separate financial statements

Updated to comply with the provisions ofPFRS 9

PIC Q&A Withdrawn

The following table summarizes the basis and effective date of withdrawal of Q&As affected bynew PFRSs:

PIC Q&A Withdrawn Basis for WithdrawalPIC Q&A No. 2006-01: PAS 18, Appendix,paragraph 9 – Revenue recognition for salesof property units under pre-completioncontracts

This PIC Q&A is considered withdrawnstarting January 1, 2018, which is theeffective date of PFRS 15.

Date approved by PIC: June 27, 2018

Philippine Interpretations Committee

14

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Ma. Gracia F. Casals-Diaz

Chase M. Sarmiento Zaldy D. Aguirre

Wilfredo A. Baltazar Ferdinand George A. Florendo

Gloria T. Baysa Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Arnel Onesimo O. Uy

Jerome Antonio B. Constantino Lovely M. Del Amen

Date approved by FRSC: October 10, 2018

Philippine Interpretations Committee

15

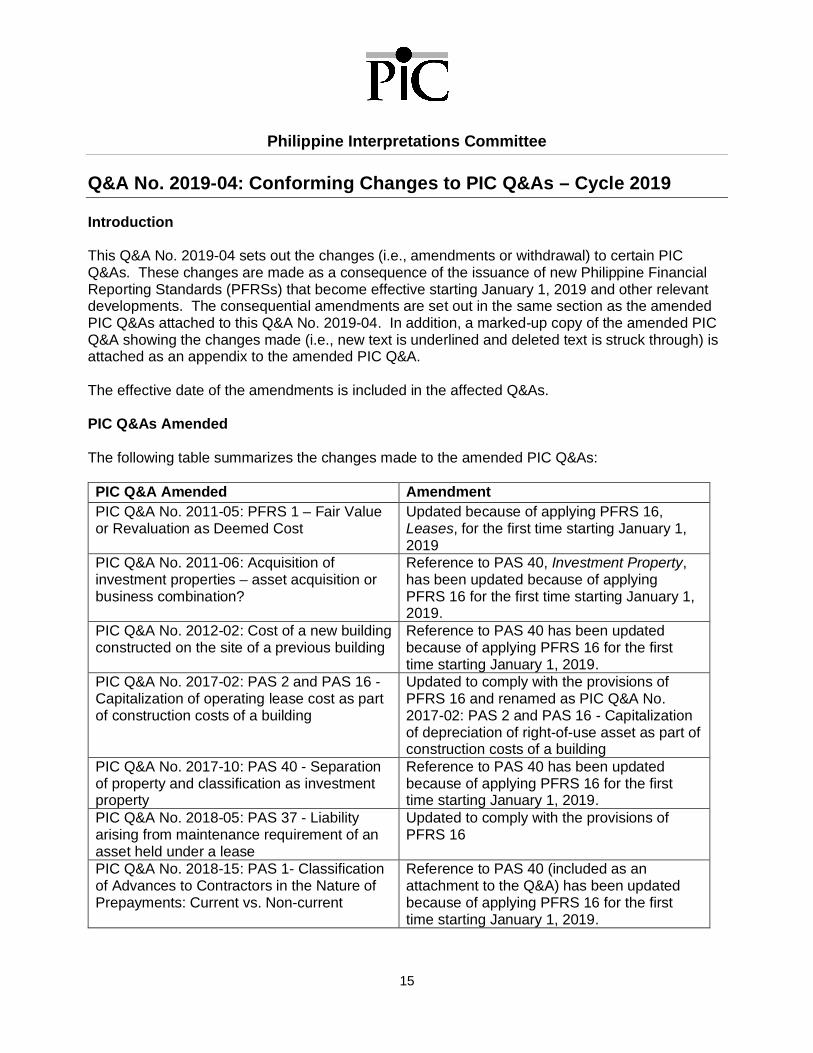

Q&A No. 2019-04: Conforming Changes to PIC Q&As – Cycle 2019

Introduction

This Q&A No. 2019-04 sets out the changes (i.e., amendments or withdrawal) to certain PICQ&As. These changes are made as a consequence of the issuance of new Philippine FinancialReporting Standards (PFRSs) that become effective starting January 1, 2019 and other relevantdevelopments. The consequential amendments are set out in the same section as the amendedPIC Q&As attached to this Q&A No. 2019-04. In addition, a marked-up copy of the amended PICQ&A showing the changes made (i.e., new text is underlined and deleted text is struck through) isattached as an appendix to the amended PIC Q&A.

The effective date of the amendments is included in the affected Q&As.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&A Amended AmendmentPIC Q&A No. 2011-05: PFRS 1 – Fair Valueor Revaluation as Deemed Cost

Updated because of applying PFRS 16,Leases, for the first time starting January 1,2019

PIC Q&A No. 2011-06: Acquisition ofinvestment properties – asset acquisition orbusiness combination?

Reference to PAS 40, Investment Property,has been updated because of applyingPFRS 16 for the first time starting January 1,2019.

PIC Q&A No. 2012-02: Cost of a new buildingconstructed on the site of a previous building

Reference to PAS 40 has been updatedbecause of applying PFRS 16 for the firsttime starting January 1, 2019.

PIC Q&A No. 2017-02: PAS 2 and PAS 16 -Capitalization of operating lease cost as partof construction costs of a building

Updated to comply with the provisions ofPFRS 16 and renamed as PIC Q&A No.2017-02: PAS 2 and PAS 16 - Capitalizationof depreciation of right-of-use asset as part ofconstruction costs of a building

PIC Q&A No. 2017-10: PAS 40 - Separationof property and classification as investmentproperty

Reference to PAS 40 has been updatedbecause of applying PFRS 16 for the firsttime starting January 1, 2019.

PIC Q&A No. 2018-05: PAS 37 - Liabilityarising from maintenance requirement of anasset held under a lease

Updated to comply with the provisions ofPFRS 16

PIC Q&A No. 2018-15: PAS 1- Classificationof Advances to Contractors in the Nature ofPrepayments: Current vs. Non-current

Reference to PAS 40 (included as anattachment to the Q&A) has been updatedbecause of applying PFRS 16 for the firsttime starting January 1, 2019.

Philippine Interpretations Committee

16

PIC Q&A Withdrawn

The following table summarizes the basis and effective date of withdrawal of Q&As affected bynew PFRSs and IFRIC agenda decision:

PIC Q&A Withdrawn Basis for WithdrawalPIC Q&A No. 2017-09: PAS 17 andPhilippine Interpretation SIC-15 - Accountingfor payments between and among lessorsand lessees

This PIC Q&A is considered withdrawnstarting January 1, 2019, which is theeffective date of PFRS 16. PFRS 16superseded PAS 17, Leases, and PhilippineInterpretation SIC-15, Operating Leases—Incentives.

PIC Q&A No. 2018-07: PAS 27 and PAS 28 -Cost of an associate, joint venture, orsubsidiary in separate financial statements

This PIC Q&A is considered withdrawn uponpublication of IFRIC agenda decision -Investment in a subsidiary accounted for atcost: Step acquisition (IAS 27 SeparateFinancial Statements) in January 2019.

Date approved by PIC: August 1, 2019

Philippine Interpretations Committee

17

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Ma. Gracia F. Casals-Diaz

David Ernesto V. Cruz Zaldy D. Aguirre

Wilfredo A. Baltazar Ferdinand George A. Florendo

Marko Romeo L. Fuentes Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Arnel Onesimo O. Uy

Jerome Antonio B. Constantino Lovely M. Del Amen-Aquino

Date approved by FRSC: August 14, 2019

Philippine Interpretations Committee

18

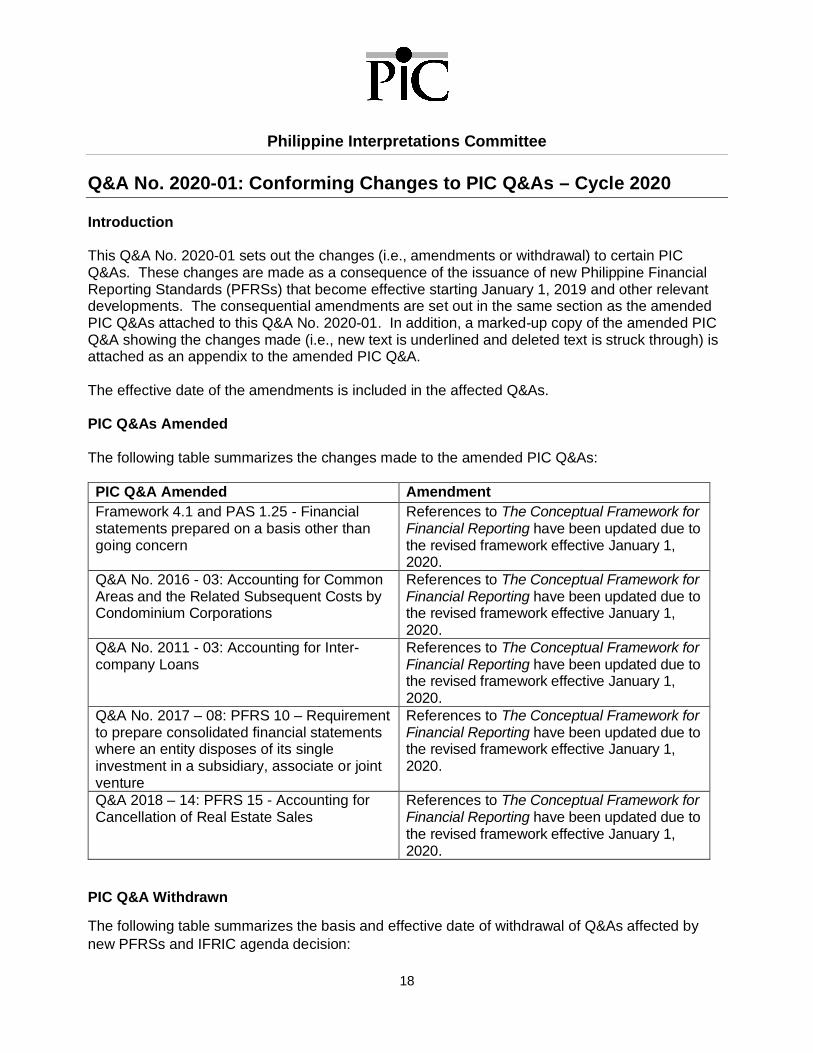

Q&A No. 2020-01: Conforming Changes to PIC Q&As – Cycle 2020

Introduction

This Q&A No. 2020-01 sets out the changes (i.e., amendments or withdrawal) to certain PICQ&As. These changes are made as a consequence of the issuance of new Philippine FinancialReporting Standards (PFRSs) that become effective starting January 1, 2019 and other relevantdevelopments. The consequential amendments are set out in the same section as the amendedPIC Q&As attached to this Q&A No. 2020-01. In addition, a marked-up copy of the amended PICQ&A showing the changes made (i.e., new text is underlined and deleted text is struck through) isattached as an appendix to the amended PIC Q&A.

The effective date of the amendments is included in the affected Q&As.

PIC Q&As Amended

The following table summarizes the changes made to the amended PIC Q&As:

PIC Q&A Amended AmendmentFramework 4.1 and PAS 1.25 - Financialstatements prepared on a basis other thangoing concern

References to The Conceptual Framework forFinancial Reporting have been updated due tothe revised framework effective January 1,2020.

Q&A No. 2016 - 03: Accounting for CommonAreas and the Related Subsequent Costs byCondominium Corporations

References to The Conceptual Framework forFinancial Reporting have been updated due tothe revised framework effective January 1,2020.

Q&A No. 2011 - 03: Accounting for Inter-company Loans

References to The Conceptual Framework forFinancial Reporting have been updated due tothe revised framework effective January 1,2020.

Q&A No. 2017 – 08: PFRS 10 – Requirementto prepare consolidated financial statementswhere an entity disposes of its singleinvestment in a subsidiary, associate or jointventure

References to The Conceptual Framework forFinancial Reporting have been updated due tothe revised framework effective January 1,2020.

Q&A 2018 – 14: PFRS 15 - Accounting forCancellation of Real Estate Sales

References to The Conceptual Framework forFinancial Reporting have been updated due tothe revised framework effective January 1,2020.

PIC Q&A Withdrawn

The following table summarizes the basis and effective date of withdrawal of Q&As affected bynew PFRSs and IFRIC agenda decision:

Philippine Interpretations Committee

19

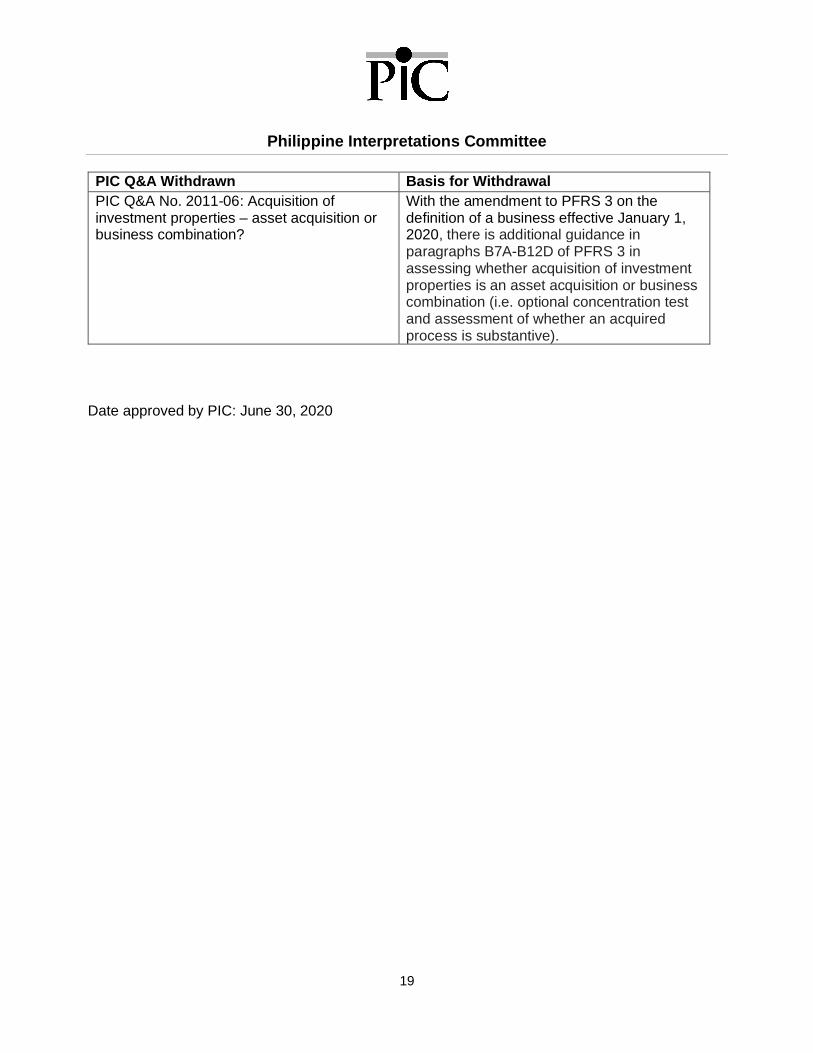

PIC Q&A Withdrawn Basis for WithdrawalPIC Q&A No. 2011-06: Acquisition ofinvestment properties – asset acquisition orbusiness combination?

With the amendment to PFRS 3 on thedefinition of a business effective January 1,2020, there is additional guidance inparagraphs B7A-B12D of PFRS 3 inassessing whether acquisition of investmentproperties is an asset acquisition or businesscombination (i.e. optional concentration testand assessment of whether an acquiredprocess is substantive).

Date approved by PIC: June 30, 2020

Philippine Interpretations Committee

20

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Ma. Gracia F. Casals-Diaz

David Ernesto V. Cruz Zaldy D. Aguirre

Joeffrey Mark P. Ferrer Ferdinand George A. Florendo

Marko Romeo L. Fuentes Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Arnel Onesimo O. Uy

Jerome Antonio B. Constantino Lovely M. Del Amen-Aquino

Date approved by FRSC: August 19, 2020

Philippine Interpretations Committee

21

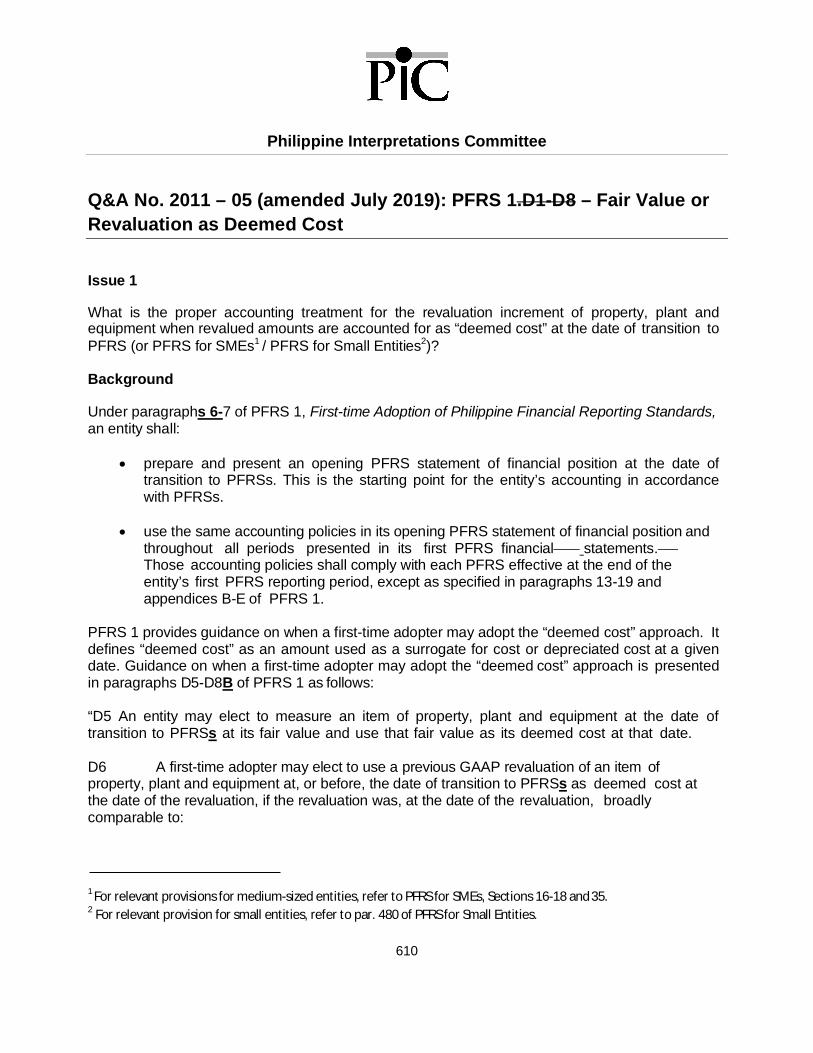

PFRS 1, First-time Adoption of Philippine Financial ReportingStandards

Q&A No. 2011 – 05 (amended July 2019): PFRS 1 – Fair Value orRevaluation as Deemed Cost

Issue 1

What is the proper accounting treatment for the revaluation increment of property, plant andequipment when revalued amounts are accounted for as “deemed cost” at the date of transition toPFRS (or PFRS for SMEs1 / PFRS for Small Entities2)?

Background

Under paragraphs 6-7 of PFRS 1, First-time Adoption of Philippine Financial Reporting Standards,an entity shall:

prepare and present an opening PFRS statement of financial position at the date oftransition to PFRSs. This is the starting point for the entity’s accounting in accordancewith PFRSs.

use the same accounting policies in its opening PFRS statement of financial position andthroughout all periods presented in its first PFRS financial statements. Thoseaccounting policies shall comply with each PFRS effective at the end of the entity’s firstPFRS reporting period, except as specified in paragraphs 13-19 and appendices B-E ofPFRS 1.

PFRS 1 provides guidance on when a first-time adopter may adopt the “deemed cost” approach. Itdefines “deemed cost” as an amount used as a surrogate for cost or depreciated cost at a givendate. Guidance on when a first-time adopter may adopt the “deemed cost” approach is presentedin paragraphs D5-D8B of PFRS 1 as follows:

“D5 An entity may elect to measure an item of property, plant and equipment at the date oftransition to PFRSs at its fair value and use that fair value as its deemed cost at that date.

D6 A first-time adopter may elect to use a previous GAAP revaluation of an item ofproperty, plant and equipment at, or before, the date of transition to PFRSs as deemed cost atthe date of the revaluation, if the revaluation was, at the date of the revaluation, broadlycomparable to:

1 For relevant provisions for medium-sized entities, refer to PFRS for SMEs, Sections 16-18 and 35.2 For relevant provision for small entities, refer to par. 480 of PFRS for Small Entities.

Philippine Interpretations Committee

22

(a) fair value; or

(b) cost or depreciated cost in accordance with PFRSs, adjusted to reflect, forexample, changes in a general or specific price index.

D7 The elections in paragraphs D5 and D6 are also available for:

(a) investment property, if an entity elects to use the cost model in PAS 40,Investment Property;

(aa) right-of-use assets (PFRS 16, Leases); and

(b) intangible assets that meet:

(i) the recognition criteria in PAS 38 (including reliable measurement of originalcost); and

(ii) the criteria in PAS 38 for revaluation (including the existence of an activemarket).

An entity shall not use these elections for other assets or for liabilities.

D8 A first-time adopter may have established a deemed cost in accordance with previous GAAPfor some or all of its assets and liabilities by measuring them at their fair value at one particulardate because of an event such as a privatization or initial public offering.

(a) If the measurement date is at or before the date of transition to PFRSs, the entitymay use such event-driven fair value measurements as deemed cost for PFRSsat the date of that measurement.

(b) If the measurement date is after the date of transition to PFRSs, but during theperiod covered by the first PFRS financial statements, the event-driven fair valuemeasurements may be used as deemed cost when the event occurs. An entityshall recognize the resulting adjustments directly in retained earnings (or ifappropriate, another category of equity) at the measurement date. At the date oftransition to PFRSs, the entity shall either establish the deemed cost by applyingthe criteria in paragraphs D5–D7 or measure assets and liabilities in accordancewith the other requirements in this PFRS.”

D8A Under some national accounting requirements exploration and development costs for oiland gas properties in the development or production phases are accounted for in costcenters that include all properties in a large geographical area. A first-time adopter usingsuch accounting under previous GAAP may elect to measure oil and gas assets at thedate of transition to PFRSs on the following basis:

(a) exploration and evaluation assets at the amount determined under the entity’sprevious GAAP; and

Philippine Interpretations Committee

23

(b) assets in the development or production phases at the amount determined for thecost center under the entity’s previous GAAP. The entity shall allocate this amountto the cost center’s underlying assets pro rata using reserve volumes or reservevalues as of that date.

The entity shall test exploration and evaluation assets and assets in the developmentand production phases for impairment at the date of transition to PFRSs in accordancewith PFRS 6, Exploration for and Evaluation of Mineral Resources, or PAS 36respectively and, if necessary, reduce the amount determined in accordance with (a) or(b) above. For the purposes of this paragraph, oil and gas assets comprise only thoseassets used in the exploration, evaluation, development or production of oil and gas.

D8B Some entities hold items of property, plant and equipment, right-of-use assets orintangible assets that are used, or were previously used, in operations subject to rateregulation. The carrying amount of such items might include amounts that weredetermined under previous GAAP but do not qualify for capitalization in accordance withPFRSs. If this is the case, a first-time adopter may elect to use the previous GAAPcarrying amount of such an item at the date of transition to PFRSs as deemed cost. Ifan entity applies this exemption to an item, it need not apply it to all items. At the date oftransition to PFRSs, an entity shall test for impairment in accordance with PAS 36 eachitem for which this exemption is used. For the purposes of this paragraph, operationsare subject to rate regulation if they are governed by a framework for establishing theprices that can be charged to customers for goods or services and that framework issubject to oversight and/or approval by a rate regulator (as defined in PFRS 14,Regulatory Deferral Accounts).

When the Philippines transitioned to PFRS, certain entities adjusted or classified the values ofproperty, plant and equipment, intangible assets, and investment property under previous GAAP intheir statement of financial position using the deemed cost as one of the voluntary exemptions,taking the resulting adjustment as an adjustment to retained earnings or to another category ofequity, referred to herein as “Revaluation Reserve.”

An entity that used a Revaluation Reserve account either:

(a) recycled the balance of the Revaluation Reserve to retained earnings using the sameestimated useful life and method of depreciation/amortization used for depreciating therelated asset adjusted to deemed cost. The amount recycled to retained earningseffectively offsets the increase in depreciation/amortization expense charged to profitor loss; or

(b) maintained the Revaluation Reserve at its original amount and recycled such amountone time to retained earnings when the related asset is fully depreciated or disposedof. This is usually accompanied by a note disclosure as to the portion of revaluationreserve already absorbed through depreciation.

In either approach, the related asset is no longer subsequently revalued since its measurement basis

Philippine Interpretations Committee

24

has been treated as deemed cost.

Paragraphs 30 to 31C of PFRS 1 and paragraphs D5 to D8B of Appendix D to PFRS 1 enumeratethe bases of deemed cost that a first-time adopter of PFRSs may use. However, those paragraphsdo not specify directly where the increase in carrying values of the assets should be adjusted –whether as an adjustment to retained earnings or to another equity category.

Further, Paragraph 11 of PFRS 1 states that: “The accounting policies that an entity uses in itsopening PFRS statement of financial position may differ from those that it used for the same dateusing its previous GAAP. The resulting adjustments arise from events and transactions before thedate of transition to PFRSs. Therefore, an entity shall recognize those adjustments directly inretained earnings (or, if appropriate, another category of equity) at the date of transition to PFRSs.”This provision would normally be interpreted to mean that the effect of most adjustments toassets and liabilities in the first-time adopter’s opening PFRS balance sheet would be reflectedin retained earnings.

Making the adjustment to retained earnings under PFRS 1 is also consistent with the requirement ofPAS 8, Accounting Policies, Changes in Accounting Estimates and Errors. PAS 8.26 states that:“…When an entity applies a new accounting policy retrospectively, it applies the new accountingpolicy to comparative information for prior periods as far back as is practicable. Retrospectiveapplication to a prior period is not practicable unless it is practicable to determine the cumulativeeffect on the amounts in both the opening and closing statements of financial position for thatperiod. The amount of the resulting adjustment relating to periods before those presented in thefinancial statements is made to the opening balance of each affected component of equity ofthe earliest prior period presented. Usually the adjustment is made to retained earnings…”

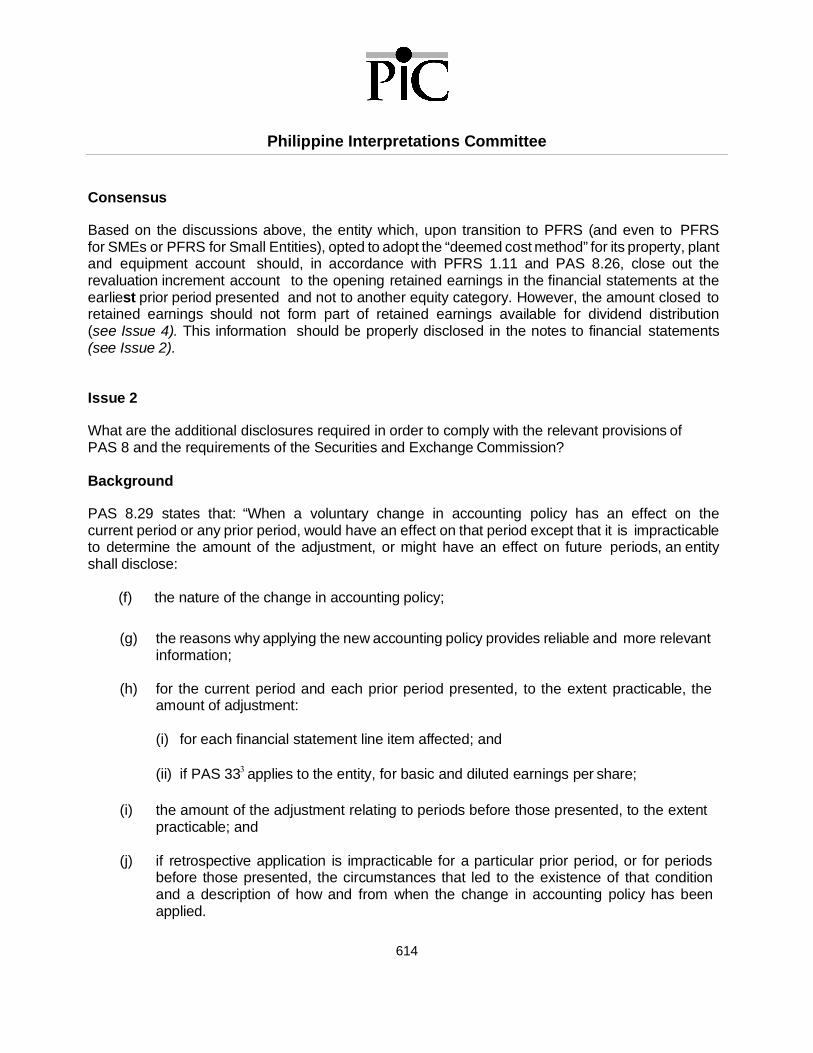

Consensus

Based on the discussions above, the entity which, upon transition to PFRS (and even to PFRSfor SMEs or PFRS for Small Entities), opted to adopt the “deemed cost method” for its property, plantand equipment account should, in accordance with PFRS 1.11 and PAS 8.26, close out therevaluation increment account to the opening retained earnings in the financial statements at theearliest prior period presented and not to another equity category. However, the amount closed toretained earnings should not form part of retained earnings available for dividend distribution(see Issue 4). This information should be properly disclosed in the notes to financial statements(see Issue 2).

Issue 2

What are the additional disclosures required in order to comply with the relevant provisions ofPAS 8 and the requirements of the Securities and Exchange Commission?

Background

PAS 8.29 states that: “When a voluntary change in accounting policy has an effect on thecurrent period or any prior period, would have an effect on that period except that it is impracticable

Philippine Interpretations Committee

25

to determine the amount of the adjustment, or might have an effect on future periods, an entityshall disclose:

(a) the nature of the change in accounting policy;

(b) the reasons why applying the new accounting policy provides reliable and more relevantinformation;

(c) for the current period and each prior period presented, to the extent practicable, theamount of adjustment:

(i) for each financial statement line item affected; and

(ii) if PAS 33applies to the entity, for basic and diluted earnings per share;

(d) the amount of the adjustment relating to periods before those presented, to the extentpracticable; and

(e) if retrospective application is impracticable for a particular prior period, or for periodsbefore those presented, the circumstances that led to the existence of that conditionand a description of how and from when the change in accounting policy has beenapplied.

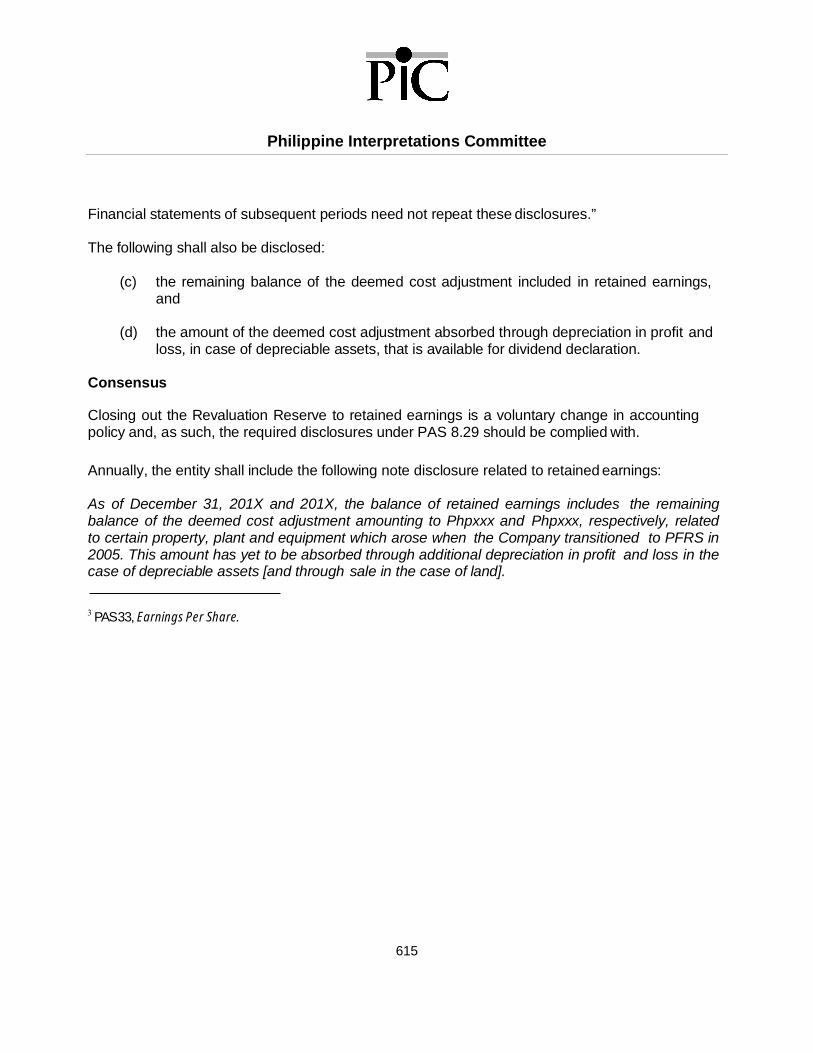

Financial statements of subsequent periods need not repeat these disclosures.”

The following shall also be disclosed:

(a) the remaining balance of the deemed cost adjustment included in retained earnings,and

(b) the amount of the deemed cost adjustment absorbed through depreciation in profit andloss, in case of depreciable assets, that is available for dividend declaration.

Consensus

Closing out the Revaluation Reserve to retained earnings is a voluntary change in accountingpolicy and, as such, the required disclosures under PAS 8.29 should be complied with.

Annually, the entity shall include the following note disclosure related to retained earnings:

As of December 31, 201X and 201X, the balance of retained earnings includes the remainingbalance of the deemed cost adjustment amounting to Phpxxx and Phpxxx, respectively, relatedto certain property, plant and equipment which arose when the Company transitioned to PFRS in2005. This amount has yet to be absorbed through additional depreciation in profit and loss in thecase of depreciable assets [and through sale in the case of land].

PAS 33, Earnings Per Share.

Philippine Interpretations Committee

26

Issue 3

Is a third statement of financial position required in compliance with PAS 1.10(f)?

Background

Paragraph 10(f) of PAS 1 requires a statement of financial position as at the beginning of theearliest comparative period when an entity:

applies an accounting policy retrospectively,

makes a retrospective restatement of items in its financial statements, or

reclassifies items in its financial statements.”

This means that in all cases above, any material adjustments to previously reported amountsand presentation give rise to the requirement for an additional statement of financial position.

The third statement of financial position is a requirement under PFRS when retrospective changeshave been performed but is not required under PFRS for SMEs and PFRS for Small Entities.

Consensus

Closing out the Revaluation Reserve to retained earnings does not affect any other item within acomparative statement of financial position and thus does not change any information previouslyprovided to financial statement users. In such a case, the inclusion of an additional statement offinancial position would not significantly influence the economic decisions of users in evaluatinghistorical financial information and thus is not considered material to financial statements preparedin accordance with PFRS. A disclosure about the closing out of the Revaluation Reserve tothe opening retained earnings account will be sufficient for this purpose.

In determining whether it is necessary to present a third statement of financial position, theentities should consider the materiality of the information that would be contained in a thirdstatement of financial position and whether this would affect economic decisions made by auser of the financial statements. In doing so, it would be useful to take into consideration factors,such as:

the nature of the change and the alternative disclosures provided,

whether the change in accounting policy actually affected the financial position at thebeginning of the comparative period (if the accounting policy allows a prospective orlimited retrospective application) , and

additionally, specific views from regulators that should be considered in this assessment.

Philippine Interpretations Committee

27

Issue 4

How would the adjustment of the Revaluation Reserve against retained earnings affect anentity’s compliance with SEC Memorandum Circular 11 Series of 2008 (SEC MC 11-2008)?

Background

SEC MC 11-2008 provides guidelines on the determination of retained earnings available fordividend declaration. It requires the submission of a reconciliation schedule for this purpose.Section 5 of SEC MC 11-2008 enumerates the unrealized items that shall be considered as notavailable for dividend declaration.

Consensus

The deemed cost adjustment can be categorized under SEC MC 11-2008 as an unrealized itemunder the group “Other unrealized gains or adjustments to retained earnings brought about bycertain transactions accounted for under the PFRS.” Examples of which are as follows: accretionincome under PFRS 9, Financial Instruments, day 1 gains on initial recognition of financialinstruments, reversal of revaluation increment to retained earnings, and the negative goodwill oninvestments in associate. Consequently, retained earnings shall be reduced by the amount of theremaining balance of the deemed cost adjustment to arrive at retained earnings available fordividend declaration.

Effective Date

The consensus in and amendments to this Q&A are effective from the date of approval by theFRSC.

Date originally approved by PIC: October 20, 2011Date amendments approved by PIC: August 1, 2019

Philippine Interpretations Committee

28

PIC Members

Wilson P. Tan, Chairman

Emmanuel Y. Artiza Ma. Gracia F. Casals-Diaz

Chase M. Sarmiento Zaldy D. Aguirre

Wilfredo A. Baltazar Ferdinand George A. Florendo

Gloria T. Baysa Jose Emmanuel U. Hilado

Rosario S. Bernaldo Lyn I. Javier

Ma. Isabel E. Comedia Arnel Onesimo O. Uy

Jerome Antonio B. Constantino Lovely M. Del Amen

Date originally approved by FRSC: January 25, 2012Date amendments approved by FRSC: August 14, 2019

Philippine Interpretations Committee

29

PFRS 3, Business Combinations

Q&A No. 2011 - 02: PFRS 3.2 – Common Control BusinessCombinations

Issue

How should business combinations involving entities under common control be accounted for,given that these are outside the scope of PFRS 3, Business Combinations?

Background

Business combinations involving entities under common control are excluded from the scope ofPFRS 3, Business Combinations (PFRS 3.2(c)). There are, however, no specific rules underexisting PFRS which prescribe how common control combinations shall be accounted for. ThisQ&A seeks to provide guidance in accounting for common control combinations in order tominimize diversity in current accounting practices until further guidance is provided by theInternational Accounting Standards Board (IASB).

A business combination is a “common control combination” if the combining entities orbusinesses are ultimately controlled by the same party or parties both before and after thebusiness combination, and that control is not transitory1. This means that the same party orparties have the ultimate control over the combining entities or businesses both before and afterthe business combination.

Some examples of common control combinations include:

combinations between subsidiaries of the same parent; the acquisition of a business between entities in the same group; and, the insertion of a new parent company at the top of a group.

Common control combinations are typically accounted for using the “pooling of interestsmethod” and, in some cases where there is commercial substance to the transaction, using the“acquisition method” under PFRS 3.

1 Judgment is required to assess whether the common210 control is transitory or not. The conclusion thatcommon control is transitory may lead to the inclusion of the business combination within the scope ofPFRS 3 so that it shall be accounted for using the acquisition method.

Philippine Interpretations Committee

30

Consensus

1. PAS 8, Accounting Policies, Changes in Accounting Estimates and Errors, requires that inthe absence of specific guidance in PFRS, management shall use its judgment indeveloping and applying an accounting policy that is relevant and reliable (PAS 8.10). Themost relevant and reliable accounting policies for common control business combinationwould either be:

a. the pooling of interests method2; orb. the acquisition method in accordance with PFRS 3.

2. The pooling of interests method is widely accepted in accounting for common controlcombinations. This method is prescribed under the US generally accepted accountingprinciples (GAAP) and permitted under the UK GAAP. The relevant guidance on pooling ofinterests method is provided under Financial Accounting Standards Board AccountingStandards Codification (FASB ASC) 805-50.

3. Common control business combinations shall be accounted for using either the pooling ofinterests method or the acquisition method. However, where the acquisition method ofaccounting is selected, the transaction must have commercial substance from theperspective of the reporting entity.

4. When evaluating whether the transaction has commercial substance, the following factorsmay be considered:

a. the purpose of the transaction;b. the involvement of outside parties in the transaction, such as non-controlling

interests or other third parties;c. whether or not the transaction is conducted at fair value;d. the existing activities of the entities involved in the transactions;e. whether or not the transaction is bringing entities together into a “reporting entity”

that did not exist before;f. where a new company is established, whether it is undertaken as an integral part of

an Initial Public Offering (IPO) or spin-off or other change in control and significantownership; and,

g. the extent to which an acquiring entity’s future cash flows are expected to change asa result of the business combination in which:

i. the configuration (risk, timing, and amount) of the cash flows of the assetreceived differs from the configuration of the cash flows of the assettransferred; or

2 A related guidance on the application of pooling of interests method shall be covered by a separate PICQ&A.

Philippine Interpretations Committee

31

ii. the entity-specific value of the portion of the entity’s operations affected bythe transaction changes as a result of the combination; and

iii. the difference in item i and item ii above is significant relative to the fair valueof the assets exchanged.

5. Since the acquisition method results in a reassessment of the value of the net assets of oneor more of the entities involved and/or the generation of goodwill, there must be commercialsubstance to the combination before it can be applied. PFRS contains limited circumstanceswhen net assets may be restated to fair value and restricts the recognition of internallygenerated goodwill, and common control business combination cannot be used tocircumvent this limitation by applying the acquisition method.

6. The accounting policy for common control business combination shall be appliedconsistently for similar transactions.

7. The following shall be disclosed in addition to required disclosures under applicablePAS/PFRS:

a. accounting policy applied for common control business combination and the rationalefor applying that policy;

b. any significant/relevant details on the common control business combination;c. if the pooling of interests method is applied, an entity shall likewise disclose how the

methodology was applied; and,d. if the acquisition method is used, an entity shall disclose the factors considered to

support its conclusion that the transaction has commercial substance.

Effective DateThe consensus in this Q&A is effective for annual financial statements beginning on or afterJanuary 1, 2012. Earlier application is encouraged.

Philippine Interpretations Committee

32

Q&A approved by PIC: August 24, 2011

PIC Members

Dalisay B. Duque, Chairman

Wilfredo A. Baltazar Judith V. Lopez

Rosario S. Bernaldo Ma. Concepcion Y. Lupisan

Ma. Elenita B. Cabrera/Rufo R. Mendoza Edmund A. Go

Ma. Gracia F. Casals-Diaz Ruby R. Seballe

Sharon G. Dayoan Wilson P. Tan

Lyn I. Javier/Reynold E. Afable Normita L. Villaruz

Q&A approved by FRSC: November 23, 2011

Philippine Interpretations Committee

33

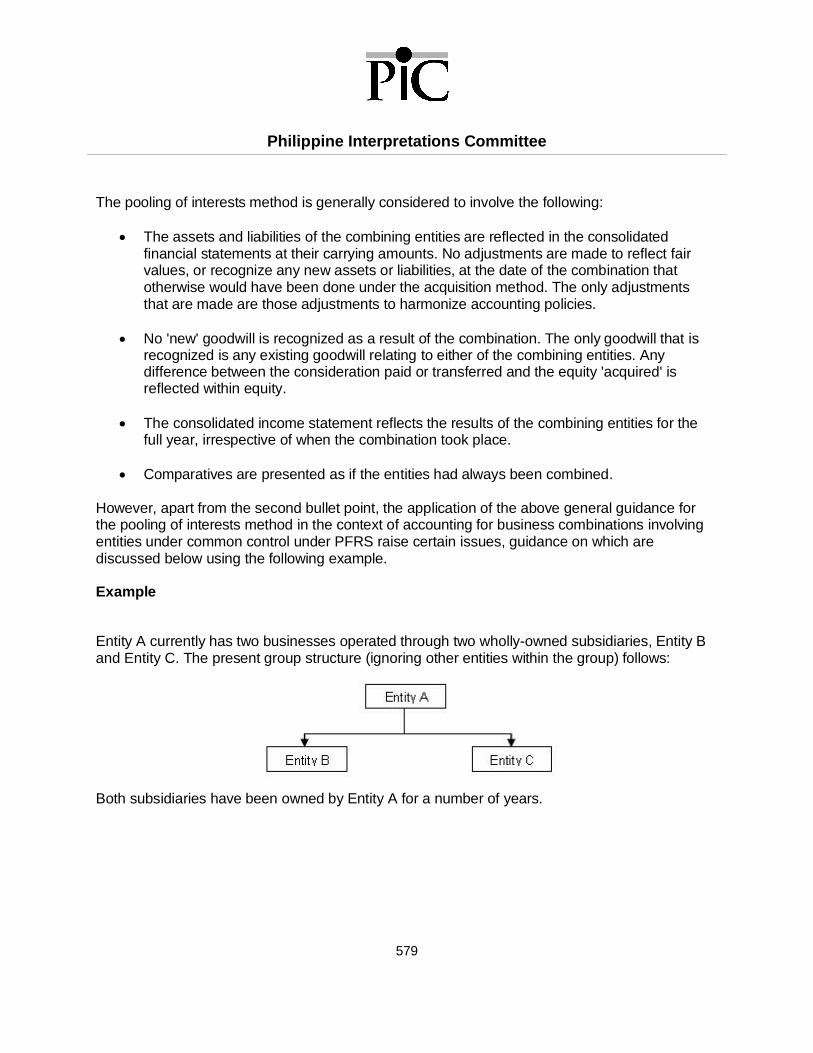

Q&A No. 2012 - 01 (amended June 2018): PFRS 3.2 – Application of thePooling of Interests Method for Business Combinations of Entitiesunder Common Control in Consolidated Financial Statements

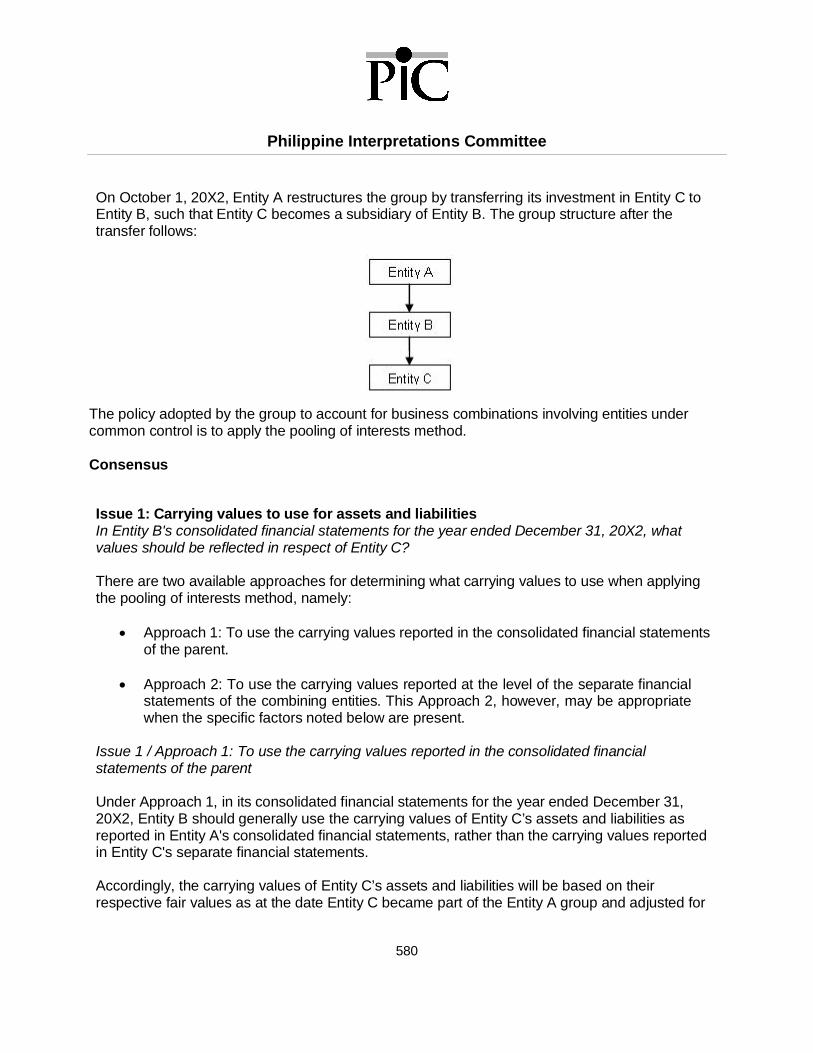

Issues

1. What carrying values shall an entity use when applying the pooling of interests method forcommon control business combinations in its consolidated financial statements?