Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc. March 24, 2015 Ryan Severino, CFA Senior Economist and Director of Research Twitter: @rseverino_reis 2015: A Year of Change for Real Estate

AppFolio Webinar: First Look at 2015: Early Economic Forecast for Property Managers

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

March 24, 2015

Ryan Severino, CFASenior Economist and Director of ResearchTwitter: @rseverino_reis

2015: A Year of Change for Real Estate

1! 2015 © AppFolio, Inc..!!

AppFolio!

• Property management and accounting!• Online rent collection (free)!• Prospect / guest card tracking!• Vacancy Marketing!• Website!• Online applications & leases!• Resident Screening!• Mobile Inspections!

…So You Run A More Successful Business!

Complete Solution Includes:!Web-Based Property Management Software!

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

• Oh, how the US economy grew in 2014.

• Review of major demographic forces.

• Recent trends in the housing market.

• Broader trends that have changed the strategic landscape for

housing (and that will continue to influence investment and

development decisions in the near term).

• Update on capital markets.

2

Agenda

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

4.9

1.20.4

3.2

0.2

3.1 2.7

1.4

-2.7

2

-1.9

-8.2

-5.4

-0.5

1.3

3.9

1.7

3.92.7 2.5

-1.5

2.9

0.8

4.6

2.31.6

2.5

0.1

2.71.8

4.53.5

-2.1

4.6 5

2.2

-10

-8

-6

-4

-2

0

2

4

6

1

4.6

2.1 2.4

4.1

2.11.4

1.8

0.5

-0.8

0.7

-2.9

-4.7

-1.4-1.8

2.4

0

2.2

3.32.6

4.2

2

0.8

1.81.4

2.8

1.31.9 1.9

3.6

1.8 2

3.7

1.2

2.53.2

4.2

-6

-4

-2

0

2

4

6

3

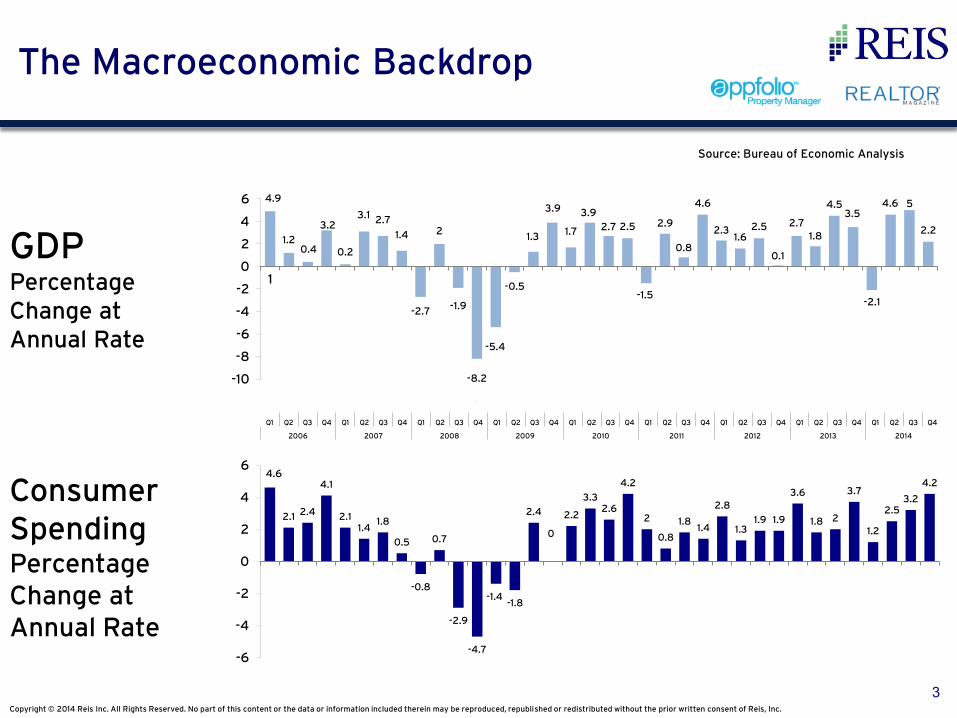

The Macroeconomic Backdrop

GDPPercentage Change at Annual Rate

Consumer SpendingPercentage Change at Annual Rate

Source: Bureau of Economic Analysis

4.9

1.20.4

3.2

0.2

3.12.7

1.4

-2.7

2

-1.9

-8.2

-5.4

-0.5

1.3

3.9

1.7

3.9

2.7 2.5

-1.5

2.9

0.8

4.6

2.31.6

2.5

0.1

2.7

1.8

4.5

3.5

-2.1

4.65

2.6

-10

-8

-6

-4

-2

0

2

4

6

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0

50

100

150

200

250

300

350

400

450

Jan

Feb

Mar

Ap

rM

ayJ

un

Ju

lA

ug

Sep Oct

No

vD

ecJ

anF

ebM

arA

pr

May

Ju

nJ

ul

Au

gS

ep Oct

No

vD

ecJ

anF

ebM

arA

pr

May

Ju

nJ

ul

Au

gS

ep Oct

No

vD

ecJ

anF

ebM

arA

pr

May

Ju

nJ

ul

Au

gS

ep Oct

No

vD

ecJ

anF

eb

2011 2012 2013 2014 '15

Pay

rolls

(T

ho

usa

nd

s)

Monthly Net Change 12-month Rolling Avg

Payroll Growth Accelerated in 2014

Source: BLS4

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 4Q11 3Q12 2Q13 1Q14 4Q14

Long Run Inflation Target

Annualized Inflation Rate

5

Inflation AcceleratingCurrent Inflation Rate vs. Long Run Inflation Target

Annualized Inflation Rate, 2004Q2-2014Q4

Source: Moody’s Analytics

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

-15,000,000 -10,000,000 -5,000,000 0 5,000,000 10,000,000 15,000,000

0 - 4

5 - 9

10 - 14

15 - 19

20 - 24

25 - 29

30 - 34

35 - 39

40 - 44

45 - 49

50 - 54

55 - 59

60 - 64

65 - 69

70 - 74

75 - 79

80 - 84

85 + Male

Female

Population Pyramid

6Source: Census

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

43.4

43.6

43.8

44.0

44.2

44.4

44.6

44.8

45.0

45.2

45.4

2014 2016 2018 2020 2022 2024 2026 2028 2030

Ann

ual

Cha

nge

Peo

ple

in M

illio

ns

Age 20-29 Growth Rate

Echo Boom Times Ahead

7Source: Moody’s Analytics

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Less than 25 25 - 29 30 - 34 35 - 44 US (total) 45 - 54 55 - 64 65 and older

1984 1994 2004 4Q 2014

Trends in Homeownership Across Age Groups

Source: Census

8

Homeownership Rates by Age of Householder

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0%

10%

20%

30%

40%

50%

60%

70%

18-20 21-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

% of Households Living in Multi-Unit Buildings, by Age of Householder, 2013

Renter Lifecycle

9Source: Census, Trulia

% of Households Living in Multi-Unit Buildings, by Age of Householder – 2013

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

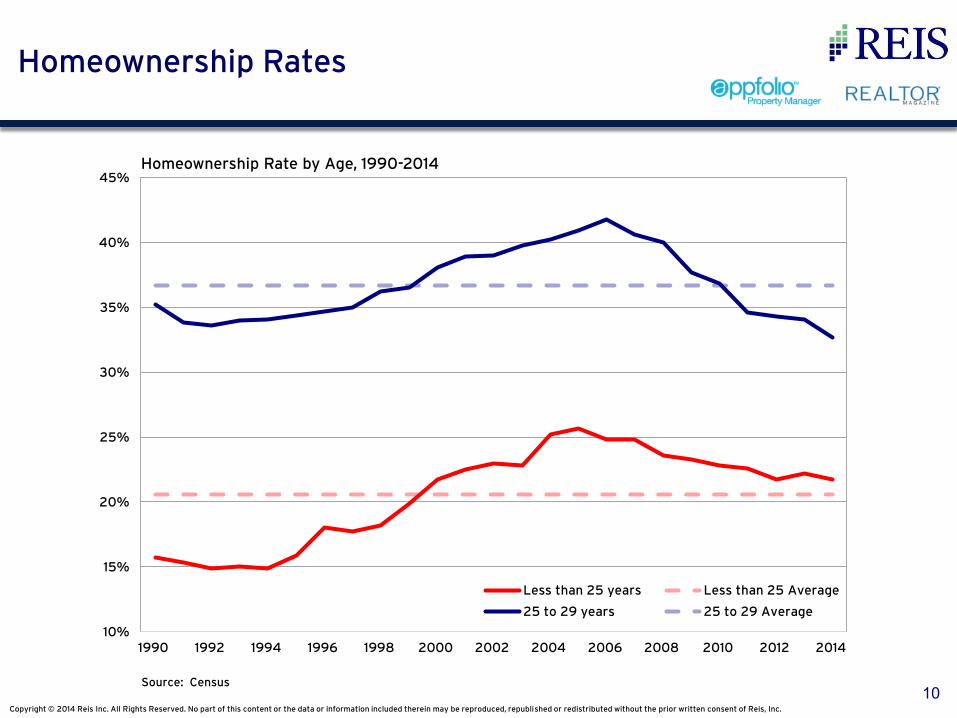

10%

15%

20%

25%

30%

35%

40%

45%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Less than 25 years Less than 25 Average

25 to 29 years 25 to 29 Average

Homeownership Rate by Age, 1990-2014

Homeownership Rates

Source: Census10

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

Homeownership Rate by Age, 1990-2014

40%

44%

48%

52%

56%

60%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

30 to 34 30 to 34 Average

Homeownership Rates

Source: Census11

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Very Good Somewhat Good Neutral Somewhat Bad Very Bad

Renter Owner

Is Housing a Good or Bad Investment?

Source: New York Fed’s Survey of Consumer Expectations12

Per

cen

t o

f S

urv

ey R

esp

on

den

ts

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

13

400

500

600

700

800

900

1000

1100

1200

2008 2009 2010 2011 2012 2013 2014 2015

Th

ou

san

ds,

An

nu

aliz

ed

Housing Starts Building Permits

Housing Starts & Building Permits

Source: Census

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

Year Qt rAsking

Rent

Percent

Change

Effect ive

Rent

Percent

Change

Vacancy

Rat e

2007 4 $1,026 1.0% $974 1.0% 5.7%2008 1 $1,035 0.9% $982 0.8% 6.0%2008 2 $1,046 1.0% $992 1.0% 6.1%2008 3 $1,052 0.6% $998 0.6% 6.2%2008 4 $1,050 -0.2% $993 -0.4% 6.7%2009 1 $1,045 -0.5% $983 -1.1% 7.4%2009 2 $1,039 -0.5% $974 -0.9% 7.7%2009 3 $1,033 -0.5% $971 -0.3% 7.9%2009 4 $1,026 -0.7% $964 -0.7% 8.0%2010 1 $1,028 0.2% $967 0.3% 8.0%2010 2 $1,033 0.4% $975 0.7% 7.8%2010 3 $1,038 0.5% $981 0.7% 7.1%2010 4 $1,043 0.5% $987 0.6% 6.6%2011 1 $1,048 0.4% $992 0.5% 6.2%2011 2 $1,054 0.6% $998 0.6% 5.9%2011 3 $1,060 0.7% $1,005 0.7% 5.6%2011 4 $1,065 0.4% $1,011 0.5% 5.3%2012 1 $1,071 0.6% $1,020 0.9% 5.0%2012 2 $1,082 1.1% $1,033 1.3% 4.8%2012 3 $1,092 0.9% $1,043 0.9% 4.7%2012 4 $1,098 0.6% $1,050 0.6% 4.6%2013 1 $1,104 0.5% $1,056 0.6% 4.4%2013 2 $1,112 0.7% $1,064 0.8% 4.3%2013 3 $1,123 1.0% $1,075 1.1% 4.3%2013 4 $1,133 0.9% $1,085 0.9% 4.3%2014 1 $1,141 0.7% $1,093 0.8% 4.1%2014 2 $1,152 1.0% $1,105 1.1% 4.1%2014 3 $1,165 1.1% $1,117 1.2% 4.2%

2014 4 $1,172 0 .6% $1,124 0 .6% 4 .2%

National Apartment MarketQuarterly and Annual Market Conditions

14Source: Reis; 79 of 275 Apartment Markets

• National vacancy was unchanged during the quarter at 4.2%. For 2014, national vacancy was down only 10 basis points.

• Asking and effective rent growth decelerated versus the third quarter, both increasing by 0.6%.

• Annual rent growth for 2014 strongest since 2007.

YearAsking

Rent

Percent

Change

Effect ive

Rent

Percent

Change

Vacancy

Rat e

2005 $944 2.5% $891 3.0% 5.7%

2006 $982 4.0% $930 4.4% 5.8%2007 $1,026 4.4% $974 4.7% 5.7%2008 $1,050 2.4% $993 2.0% 6.7%2009 $1,026 -2.3% $964 -2.9% 8.0%

2010 $1,043 1.7% $987 2.3% 6.6%2011 $1,065 2.1% $1,011 2.4% 5.3%2012 $1,098 3.1% $1,050 3.9% 4.6%2013 $1,133 3.2% $1,085 3.3% 4.3%2014 $1,172 3.5% $1,124 3.6% 4.2%

2015 $1,213 3.5% $1,161 3.3% 4.8 %

2016 $1,251 3.1% $1,194 2.8 % 5.1%

2017 $1,28 4 2.7% $1,222 2.4% 5.4%

2018 $1,315 2.4% $1,250 2.2% 5.5%

2019 $1,344 2.2% $1,28 0 2.4% 5.8 %

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

-50%

0%

50%

100%

150%

200%

250%

300%

350%

1979 1983 1987 1991 1995 1999 2003 2007 2011

Lowest Quintile 21st to 80th Percentiles

81st to 99th Percentiles Top 1 Percent

Cumulative Growth in Average Inflation-Adjusted After-Tax Income, by Income Group

Income Inequality

Source: Congressional Budget Office 15

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

3.6%

3.8%

Asking Rent Effective Rent

1988-1993 2010-2014

16

Average Annual Apartment Rent Growth1988-1993 vs. 2010-2014

Source: Reis Inc

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

9.6%

7.4% 7.1% 7.1%

4.0% 3.7%

1.3% 1.3% 1.1% 0.8%

-0.2%

-10%

-5%

0%

5%

10%

15%

20%

San Jose Oakland-East Bay

Denver SanFrancisco

Chicago USAggregate

FairfieldCounty

Wichita Little Rock Westchester District ofColumbia

17

Top and Bottom Apartment MarketsYear-Over-Year Comparisons for the Fourth Quarter of 2014

Effective Revenue Per Unit, Percent Change 2013Q4-2014Q4

Source: Reis

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

6.0%

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Mean Cap Rate 12 Month Rolling Cap Rate

National Apartment MarketCap Rate Trends

18Source: Reis

5.8%

6.2%

6.6%

7.0%

7.4%

7.8%

2Q07 3Q07 4Q07 1Q08 2Q08 3Q084Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

Mean Cap Rate 12 Month Rolling Cap Rate

Cap

Rat

e

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0

50

100

150

200

250

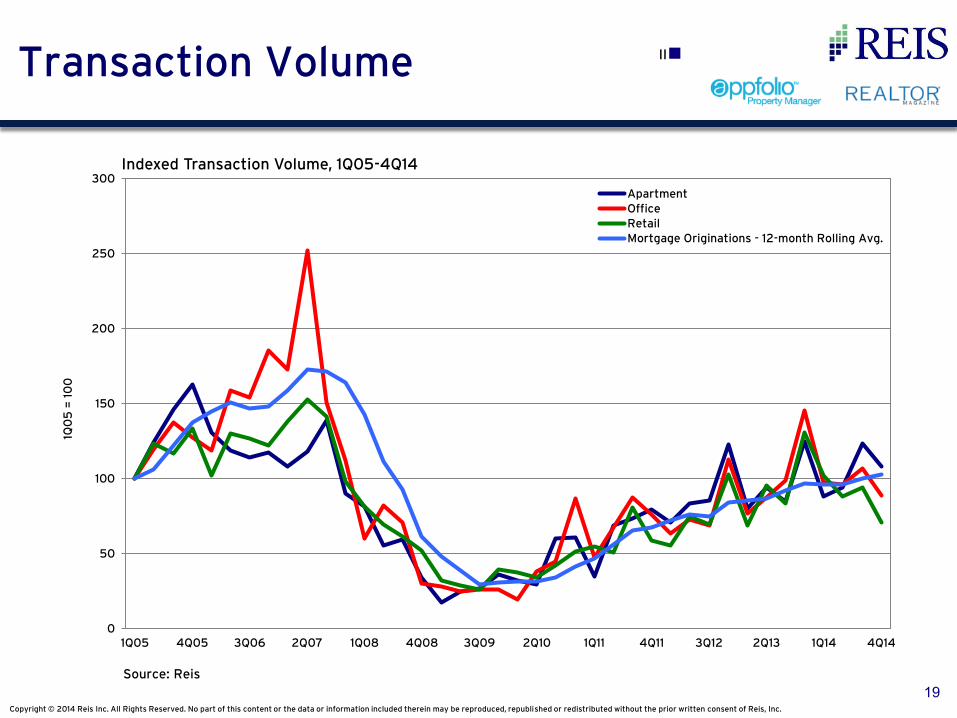

300

1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 4Q11 3Q12 2Q13 1Q14 4Q14

1Q0

5 =

10

0

ApartmentOfficeRetailMortgage Originations - 12-month Rolling Avg.

19

Source: Reis

Transaction Volume

Indexed Transaction Volume, 1Q05-4Q14

II

Copyright © 2015 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0

10

20

30

40

50

60

70

First Holding Period Second Holding Period Third Holding Period Fourth Holding Period

Ave

rag

e H

old

ing

Per

iod

(M

on

ths)

Property Transactions Before 2009

Property Transactions After 2009

20

Source: Reis

Longer Holding Periods

Average Holding Period – Gateway Markets’ Apartment Transactions

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

0%

2%

4%

6%

8%

10%

12%

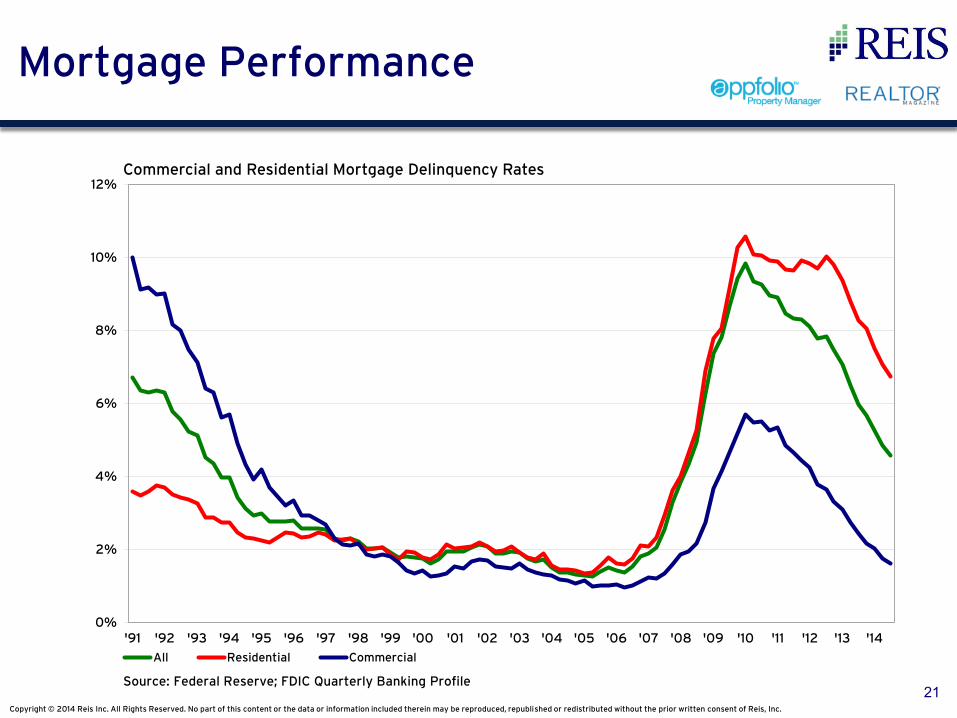

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

All Residential Commercial

Commercial and Residential Mortgage Delinquency Rates

21Source: Federal Reserve; FDIC Quarterly Banking Profile

Mortgage Performance

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

• Multifamily fundamentals remained strong, but vacancies may really

begin to rise this year.

• The for-sale housing market is rebounding and should accelerate along

with the macroeconomy.

• The US is unlikely to be bogged down in stagnation; but given our

integration with the global economy, non-domestic idiosyncratic factors

(very challenging to forecast) now represent the highest risk to the

rosiest of predictions for US growth in 2015.

22

Summary and Conclusions

Copyright © 2014 Reis Inc. All Rights Reserved. No part of this content or the data or information included therein may be reproduced, republished or redistributed without the prior written consent of Reis, Inc.

March 24, 2015

Ryan Severino, CFASenior Economist and Director of ResearchTwitter: @rseverino_reis

2015: A Year of Change for Real Estate

Related Documents

![Sometimes Our Customers Bake Us A Cake [AppFolio Customer Love]](https://static.cupdf.com/doc/110x72/554d1e87b4c905ab268b476f/sometimes-our-customers-bake-us-a-cake-appfolio-customer-love.jpg)