Answers to activities, practice exercises and exam practice questions 1 Double-entry bookkeeping: cash transactions Practice exercises 1 Debit account Credit account 1 Noel pays a cheque into his business bank account as capital Bank Noel – Capital 2 Purchases some goods for resale and pays by cheque Purchases Bank 3 Sells some goods and banks the takings Bank Sales 4 Pays rent by cheque Rent payable Bank 5 Purchases shop fittings and pays by cheque Shop fittings Bank 6 Cashes cheque for personal expenses [1] Drawings Bank 7 Pays wages by cheque Wages Bank 8 Returns goods to supplier and banks refund Bank Purchases returns 9 Receives rent from tenant and banks cheque Bank Rent receivable 10 Refunds money to customer by cheque for goods returned [2] Sales returns Bank 11 Motor vehicle purchased and paid for by cheque Motor vehicles Bank 12 Pays for petrol for motor vehicle and pays by cheque [3] Motor expenses Bank 2 Bank account $ $ May 1 Martine – capital 300 May 3 Rent payable 100 May 2 Charline – loan 1 000 May 4 Shop fittings 400 May 5 Purchases returns 20 May 4 Purchases 300 May 6 Sales 40 May 7 Wages 60 May 8 Drawings 100 Martine capital account $ $ May 1 Bank 300 Charline – Loan account $ $ May 2 Bank 1 000 [3] The costs of running motor vehicles (petrol, licence, insurance, repairs, etc.) are not debited to the motor vehicles account. A new account, motor expenses, is opened to record them. [ 1] The cheque which Noel cashed was for his personal expenses. It is therefore debited to the Drawings account. This text has not been through the Cambridge endorsement process. All answers that appear in this publication have been written by the author. 2 [2] Following the principle of purchases returns, sales returns are always debited to their own account, never to the sales account.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Answers to activities, practice exercises and exam practice questions

1 Double-entry bookkeeping: cash transactionsPractice exercises1 Debit account Credit account

1 Noel pays a cheque into his business bank account as capital

Bank Noel – Capital

2 Purchases some goods for resale and pays by cheque

Purchases Bank

3 Sells some goods and banks the takings

Bank Sales

4 Pays rent by cheque Rent payable Bank5 Purchases shop fittings and

pays by chequeShop fittings Bank

6 Cashes cheque for personal expenses [1]

Drawings Bank

7 Pays wages by cheque Wages Bank8 Returns goods to supplier and

banks refundBank Purchases returns

9 Receives rent from tenant and banks cheque

Bank Rent receivable

10 Refunds money to customer by cheque for goods returned [2]

Sales returns Bank

11 Motor vehicle purchased and paid for by cheque

Motor vehicles Bank

12 Pays for petrol for motor vehicle and pays by cheque [3]

Motor expenses Bank

2 Bank account $ $

May 1 Martine – capital 300 May 3 Rent payable 100May 2 Charline – loan 1 000 May 4 Shop fittings 400May 5 Purchases

returns20 May 4 Purchases 300

May 6 Sales 40 May 7 Wages 60May 8 Drawings 100

Martine capital account$ $

May 1 Bank 300

Charline – Loan account$ $

May 2 Bank 1 000

[3] The costs of running motor vehicles (petrol, licence, insurance, repairs, etc.) are not debited to the motor vehicles account. A new account, motor expenses, is opened to record them.

[1] The cheque which Noel cashed was for his personal expenses. It is therefore debited to the Drawings account.

This text has not been through the Cambridge endorsement process.

All answers that appear in this publication have been written by the author.

2

[2] Following the principle of purchases returns, sales returns are always debited to their own account, never to the sales account.

Rent payable account$ $

May 3 Bank 100

Shop fittings account$ $

May 4 Bank 400

Purchases account$ $

May 4 Bank 300

Purchases returns account$ $

May 5 Bank 20

Sales account$ $

May 6 Bank 40

Wages account$ $

May 7 Bank 60

Drawings account$ $

May 8 Bank 100

Notes:

1 The narrative must always contain the name of the account where the opposite entry can be made.

2 Purchases returns are always posted to their own account, never to the credit of the purchases account.

3 a Debit account Credit account

July 1 Lee started business by paying $20 000 of his savings into a business bank account

Bank Capital

He also had $500 in cash which he decided to use to pay cash expenses for the business

Cash Capital

2 Bought some goods for resale for $1300, paying by cheque Purchases Bank3 Paid $2500 by cheque to rent some business premises Rent payable Bank4 Bought some office furniture by cheque for $750 Office furniture Bank

Bought office stationery for $120, paying by cash Stationery Cash6 Sold some goods for $1700 and paid the money into the bank Bank Sales

Sold more goods for $180. He received cash for this sale Cash Sales

8 Retuned some faulty goods valued at $60 to the supplier and received a cheque refund

Bank Purchases returns

9 A customer returned some faulty goods. Lee gave the customer a cash refund of $25

Sales returns Cash

10 Sold goods for $420. Lee received cash for the goods. He kept $200 as business cash and banked the rest

Cash Bank

Sales

11 Lee took cash drawings of $160 Drawings Cash

3

Answers to activities, practice exercises and exam practice questions: Chapter 1

b Bank account$ $

July 1 Capital 20 000 July 2 Purchases 1 300July 6 Sales 1 700 July 3 Rent 2 500July 8 Purchases returns 60 July 4 Office furniture 750July 10 Sales 220

Cash account$ $

July 1 Capital 500 July 4 Stationery 120July 6 Sales 180 July 9 Sales returns 25July 10 Sales 200 July 11 Drawings 160

Capital account$ $

July 1 Bank 20 000Cash 500

Purchases account$ $

July 2 Bank 1 300

Sales account$ $

July 6 Bank 1 700Cash 180

July 10 Bank 220Cash 200

Purchases returns account$ $

July 8 Bank 60

Sales returns account$ $

July 9 Cash 25

Rent account$ $

July 3 Bank 2 500

Office furniture account$ $

July 4 Bank 750

Cambridge International AS and A Level Accounting

4

Stationery account$ $

July 4 Cash 120

Drawings account$ $

July 11 Cash 160

4 Debit account Credit account1 Local taxes paid by cheque Taxes Bank

2 Bank pays interest to trader Bank Interest received3 Other operating expenses paid by cheque Other operating expenses Bank4 Postage and stationery paid by cheque Postage and stationery Bank5 Telephone bill paid by cheque Telephone Bank6 Carriage inwards paid by cheque Carriage inwards Bank7 Carriage outwards paid by cheque Carriage outwards Bank8 Interest paid by cheque to brother in

respect of a loan received from himInterest payable Bank

9 Interest paid to bank Interest payable / bank interest

Bank

5 Bank account $ $

June 1 Farook – capital 15 000 June 2 Premises 8 000Amna – loan 5 000 June 3 Office furniture 2 000

June 5 Sales 1 500 June 4 Purchases 5 000June 10 Sales 2 400 June 6 Insurance 600June 12 Purchase returns 900 June 7 Motor van 3 000June 13 Insurance 100 June 8 Motor expenses 50June 14 Office furniture 800 June 9 Purchases 2 000

June 10 Wages 400June 11 Sales returns 1 200June 13 Drawings 200June 15 Loan 1 000

Capital account$ $

June 1 Bank 15 000

Loan account$ $

June 15 Bank 1 000 June 1 Bank 5 000

Premises account$ $

June 2 Bank 8 000

Answers to activities, practice exercises and exam practice questions: Chapter 1

5

Office furniture account$ $

June 3 Bank 2 000 June 14 Bank 800

Purchases account$ $

June 4 Bank 5 000June 9 Bank 2 000

Sales account$ $

June 5 Bank 1 500June 10 Bank 2 400

Insurance account$ $

June 6 Bank 600 June 13 Bank 100

Motor van account$ $

June 7 Bank 3 000

Motor expenses account$ $

June 8 Bank 50

Wages account$ $

June 10 Bank 400

Sales returns account$ $

June 11 Bank 1 200

Purchases returns account$ $

June 12 Bank 900

Drawings account$ $

June 13 Bank 200

Exam practice questionsMultiple-choice questions1 B

2 B

3 D

4 B

6

Cambridge International AS and A Level Accounting

2 Double-entry bookkeeping: credit transactionsPractice exercises1 Khor account

$ $June 10 Purchases returns [1] 180 June 1 Purchases 2 700June 30 Bank 2 394June 30 Discounts received 126

Lim account $ $

June 30 Bank 2 394 June 15 Purchases 2 520June 30 Discounts received 126

Lai account $ $

June 5 Sales 600 June 25 Sales returns 180June 30 Bank 399June 30 Discounts allowed 21

Chin account $ $

June 20 Sales 1 300 June 30 Bank 1 235June 30 Discounts allowed 65

Purchases account $ $

June 1 Khor 2 700June 15 Lim 2 520

Purchases returns account $ $

June 10 Khor 180

Sales account $ $

June 5 Lai 600June 20 Chin 1 300

Sales returns account $ $

June 25 Lai 180 [2]

[1] The goods which Geraud returned to Khor will have had the trade discount deducted from them when they were purchased. This must be adjusted when the goods are returned. Their cost was $200 - 10% trade discount of $20 = 180.

[2] The same is true for the goods returned by Lai, which had cost $200 but need to have the 10% trade discount deducted.

7

Answers to activities, practice exercises and exam practice questions: Chapter 2

Bank account $ $

June 30 Lai 399 June 30 Khor 2 394June 30 Chin 1 235 June 30 Lim 2 394

Discounts received account $ $

June 30 Khor 126June 30 Lai 126

Discounts allowed account $ $

June 30 Lai 21June 30 Chin 65

Note:

Remember trade discount is never entered in the ledger.

2 In the books of Brian:

Ken account $ $

April 1 Sales 1 500 April 2 Purchases 400April 3 Sales 600 April 6 Purchases 720April 12 Bank 380 April 10 Bank 1 455

Discount received 20 Discount allowed 45

Sales account $ $

April 1 Ken 1 500April 3 Ken 600

Purchases account $ $

April 2 Ken 400April 6 Ken 720

Bank account $ $

April 10 Ken 1 455 April 12 Ken 380

Discounts allowed account $ $

April 10 Ken 45

Discounts received account $ $

April 12 Ken 20

Cambridge International AS and A Level Accounting

8

In the books of Ken:

Brian account $ $

April 2 Sales 400 April 1 Purchases 1 500April 6 Sales 720 April 3 Purchases 600April 10 Bank 1 455 April 12 Bank 380

Discount received 45 Discount allowed 20

Sales account $ $

April 2 Brian 400April 6 Brian 720

Purchases account $ $

April 1 1 500April 3 600

Bank account $ $

April 10 Brian 380 April 12 Brian 1 455

Discounts allowed account $ $

April 12 Brian 20

Discounts received account $ $

April 10 Brian 45

3 Adams account $ $

July 5 Purchases returns 510 July 1 Purchases 4 250July 14 Bank 3 590

Discount received 150

Bond account $ $

July 14 Bank 2 160 July 4 Purchases 2 250Discount received 90

Astle account $ $

July 9 Purchases returns 640 July 7 Purchases 5 600July 14 Bank 4 712

Discount received 248

Answers to activities, practice exercises and exam practice questions: Chapter 2

9

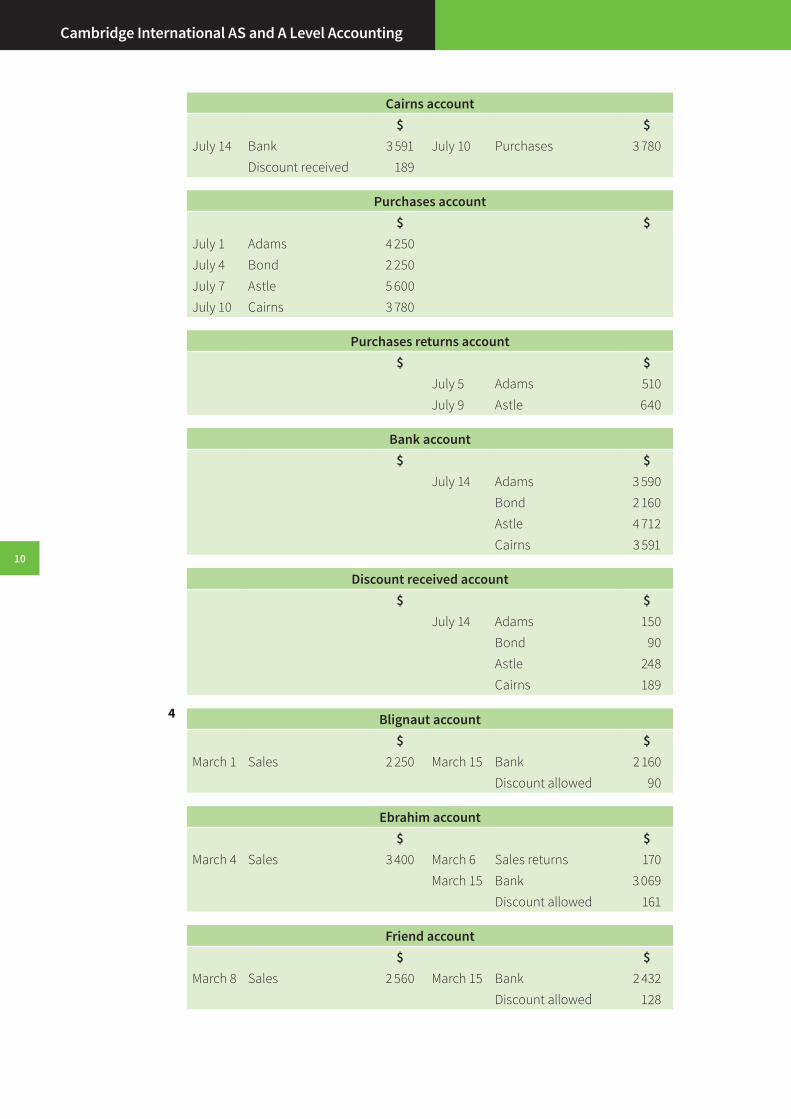

Cairns account $ $

July 14 Bank 3 591 July 10 Purchases 3 780Discount received 189

Purchases account $ $

July 1 Adams 4 250July 4 Bond 2 250July 7 Astle 5 600July 10 Cairns 3 780

Purchases returns account $ $

July 5 Adams 510July 9 Astle 640

Bank account $ $

July 14 Adams 3 590Bond 2 160Astle 4 712Cairns 3 591

Discount received account $ $

July 14 Adams 150Bond 90Astle 248Cairns 189

4 Blignaut account $ $

March 1 Sales 2 250 March 15 Bank 2 160Discount allowed 90

Ebrahim account $ $

March 4 Sales 3 400 March 6 Sales returns 170March 15 Bank 3 069

Discount allowed 161

Friend account $ $

March 8 Sales 2 560 March 15 Bank 2 432Discount allowed 128

Cambridge International AS and A Level Accounting

10

Flower account $ $

March 12 Sales 1 800 March 14 Sales returns 315March 15 Bank 1 426

Discount allowed 59

Sales account $ $

March 1 Blignaut 2 250March 4 Ebrahim 3 400March 8 Friend 2 560March 12 Flower 1 800

Sale returns account $ $

March 6 Ebrahim 17014 Flower 315

Bank account $ $

March 15 Blignaut 2 160Ebrahim 3 069Friend 2 432Flower 1 426

Discount allowed account $ $

March 15 Blignaut 90Ebrahim 161Friend 128Flower 59

Exam practice questionsMultiple-choice questions1 A

2 B

3 A

Answers to activities, practice exercises and exam practice questions: Chapter 2

11

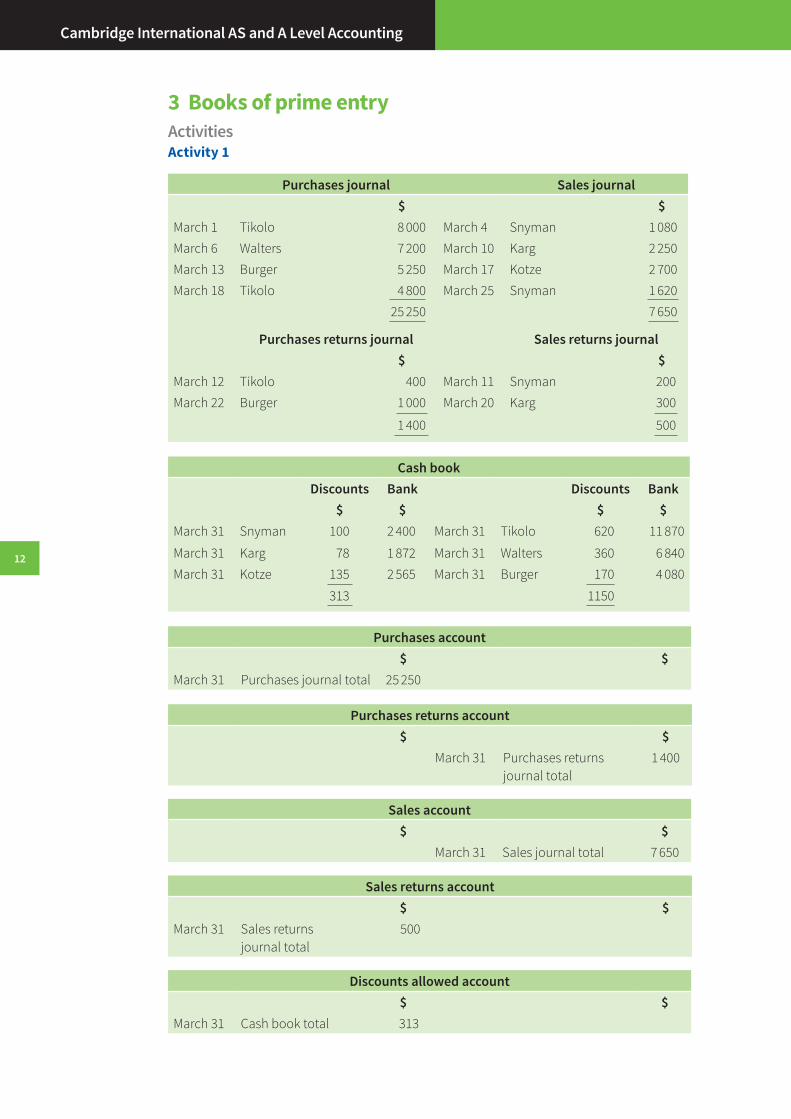

3 Books of prime entryActivitiesActivity 1

Purchases journal Sales journal $ $

March 1 Tikolo 8 000 March 4 Snyman 1 080March 6 Walters 7 200 March 10 Karg 2 250March 13 Burger 5 250 March 17 Kotze 2 700March 18 Tikolo 4 800 March 25 Snyman 1 620

25 250 7 650

Purchases returns journal Sales returns journal$ $

March 12 Tikolo 400 March 11 Snyman 200March 22 Burger 1 000 March 20 Karg 300

1 400 500

Cash bookDiscounts Bank Discounts Bank

$ $ $ $March 31 Snyman 100 2 400 March 31 Tikolo 620 11 870

March 31 Karg 78 1 872 March 31 Walters 360 6 840March 31 Kotze 135 2 565 March 31 Burger 170 4 080

313 1150

Purchases account $ $

March 31 Purchases journal total 25 250

Purchases returns account $ $

March 31 Purchases returns journal total

1 400

Sales account $ $

March 31 Sales journal total 7 650

Sales returns account $ $

March 31 Sales returns journal total

500

Discounts allowed account $ $

March 31 Cash book total 313

12

Cambridge International AS and A Level Accounting

Discounts received account $ $

March 31 Cash book total 1 150

Tikolo account $ $

March 12 Purchases returns 400 March 1 Purchases 8 000March 31 Bank 11 780 March 18 Purchases 4 800March 31 Discounts received 620

Walters account $ $

March 31 Bank 6 840 March 6 Purchases 7 200Discounts received 360

Burger account $ $

March 22 Purchases returns 1 000 March 13 Purchases 5 250March 31 Bank 4 080March 31 Discounts received 170

Snyman account $ $

March 4 Sales 1 080 March 11 Sales returns 200March 25 Sales 1 620 March 31 Bank 2 400

March 31 Discounts allowed 100

Karg account $ $

March 10 Sales 2 250 March 20 Sales returns 300March 31 Bank 1 872March 31 Discounts allowed 78

Kotze account $ $

March 17 Sales 2 700 March 31 Bank 2 565March 31 Discounts allowed 135

Activity 2

Cash bookDisc Cash Bank Disc Cash Bank

$ $ £ $ $ $March 1 Sales 1 100 March 2 Electricity 130March 3 Sales 900 March 4 Bank 1 700March 4 Cash 1 700 March 5 Other operating expenses 25March 6 Bank 800 March 6 Cash 800

March 7 Purchases 750

13

Answers to activities, practice exercises and exam practice questions: Chapter 3

Activity 3

Accounts Dr Cr $ $

a A & Co. 120A. Cotter 120

Correction of credit note no. 964 received from A and Co. Ltd. in the sum of $120 debited to A. Cotter in error.

b Purchases 400Hussain 400

Correction of invoice no. 104 in the sum of $400 received from Hussain omitted from the purchases journal.

c Maya 45Sales 45

Correction of posting error: invoice no. 6789 in the sum of $150 sent to Maya entered in the sales journal as $105.

d Machinery 2 300Purchases 2 300

Correction of purchase of machine posted in error to purchases account.

e Sales returns 68Hanif 68

Correction of omission of credit note no.23 for $68 and sent to Hanif, omitted from the sales returns journal.

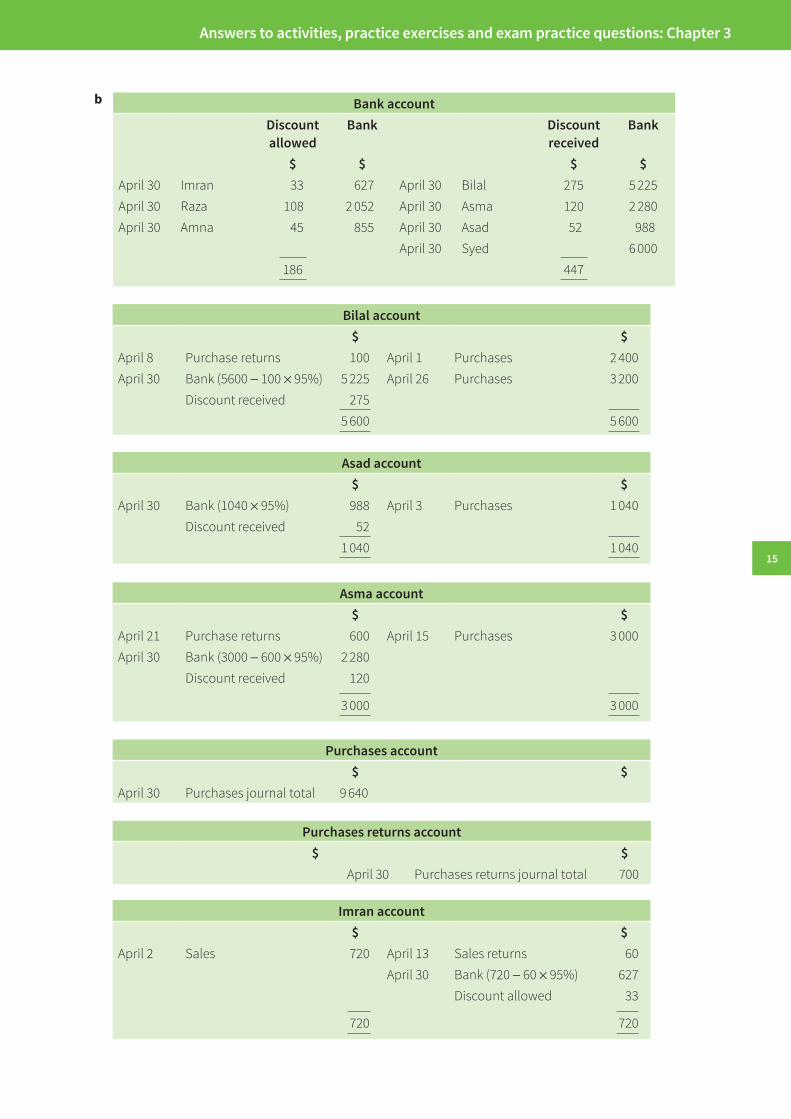

Practice exercises1 a Purchases journal Purchases returns journal

$ $April 1 Bilal 2 400 April 8 Bilal [1] 100April 3 Asad 1 040 April 21 Asma [1] 600April 15 Asma 3 000April 26 Bilal 3 200

9 640 700

Sales journal Sales returns journal $ $

April 2 Imran 720 April 13 Imran [1] 60April 10 Raza 880 April 24 Amna [1] 300April 16 Amna 1 200April 17 Raza 1 280

4 080 360

Journal

Accounts Dr Cr $ $

5 April Motor vehicles/delivery van 6 000Syed 6 000

Purchase of delivery van, from Syed, invoice no. 324.

[1] It is assumed that the value of the goods returned were after adjusting for the trade discount. Whether a returns amount given needs to be adjusted for the trade discount should be clear.

14

Cambridge International AS and A Level Accounting

b Bank accountDiscount allowed

Bank Discount received

Bank

$ $ $ $April 30 Imran 33 627 April 30 Bilal 275 5 225April 30 Raza 108 2 052 April 30 Asma 120 2 280April 30 Amna 45 855 April 30 Asad 52 988

April 30 Syed 6 000186 447

Bilal account $ $

April 8 Purchase returns 100 April 1 Purchases 2 400April 30 Bank (5600 - 100 × 95%) 5 225 April 26 Purchases 3 200

Discount received 2755 600 5 600

Asad account $ $

April 30 Bank (1040 × 95%) 988 April 3 Purchases 1 040Discount received 52

1 040 1 040

Asma account $ $

April 21 Purchase returns 600 April 15 Purchases 3 000April 30 Bank (3000 - 600 × 95%) 2 280

Discount received 120

3 000 3 000

Purchases account $ $

April 30 Purchases journal total 9 640

Purchases returns account $ $

April 30 Purchases returns journal total 700

Imran account $ $

April 2 Sales 720 April 13 Sales returns 60April 30 Bank (720 - 60 × 95%) 627

Discount allowed 33

720 720

Answers to activities, practice exercises and exam practice questions: Chapter 3

15

Raza account $ $

April 10 Sales 880 April 30 Bank (2160 × 95%) 2 052April 17 Sales 1 280 Discount allowed 108

2 160 2 160

Amna account $ $

April 16 Sales 1 200 April 24 Sales returns 300April 30 Bank (1200 - 300 × 95%) 855

Discount allowed 45

1 200 1 200

Sales account $ $

April 30 Sales journal total 4 080

Sales returns account $ $

April 30 Sales returns journal total 360

Discount allowed account $ $

April 30 Bank 176

Discount received account $ $

April 30 Bank 447

Syed account $ $

April 30 Bank 6 000 April 5 Del. Van (Inv 324) 6 000

Delivery van account $ $

April 5 Syed 6 000

Cambridge International AS and A Level Accounting

16

2 Date Accounts Dr Cr $ $

a March 3 Machinery 10 000Mumtaz 10 000

Purchase of machinery on credit on invoice 506.

b March 6 Sales 675Wayne 675

Correction of invoice 495 entered twice in error.

c March 7 Delivery van 4 250

Younas 4 250

Purchase of new delivery van from Younas on invoice 998.

d March 10 Sales returns 190

Browne 190

Credit note 103 omitted from sales returns journal.

e March 15 Geeta 1 300

Sandra 1 300

Transfer of invoice no. 854 from Sandra posted to Geeta’s account in error.

Exam practice questionsMultiple-choice questions1 C

2 B

3 B

4 C

Answers to activities, practice exercises and exam practice questions: Chapter 3

17

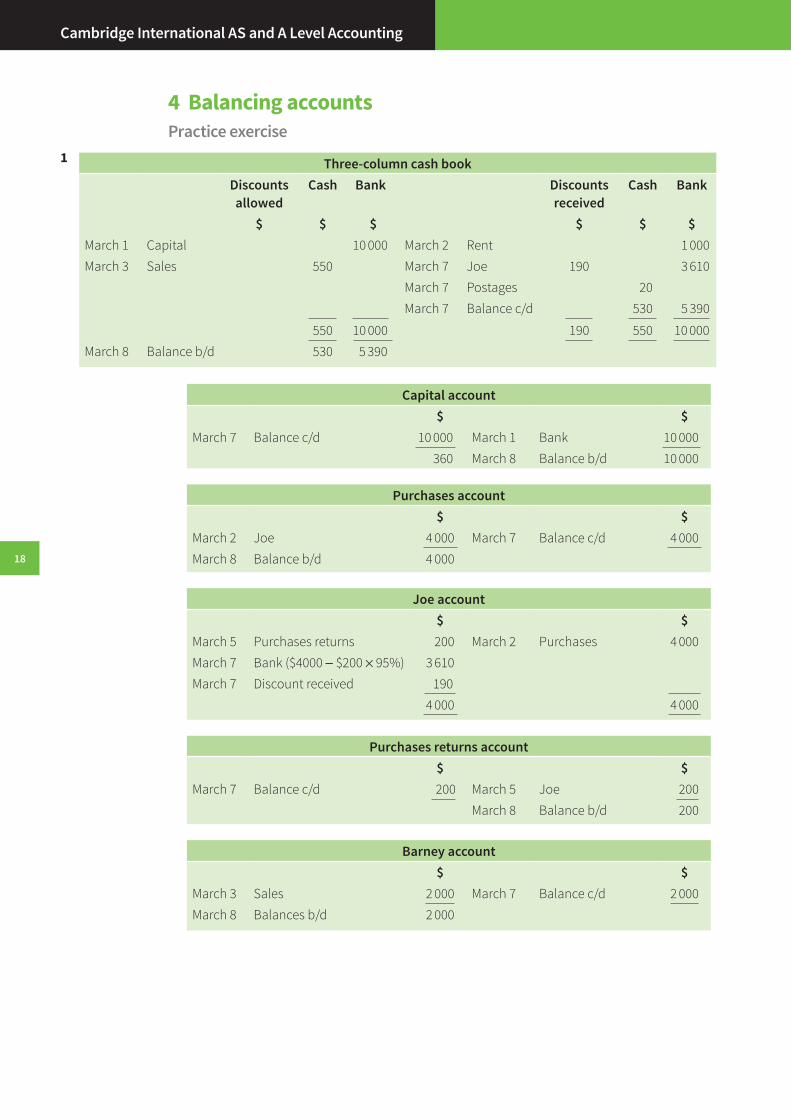

4 Balancing accountsPractice exercise

1 Three-column cash bookDiscounts allowed

Cash Bank Discounts received

Cash Bank

$ $ $ $ $ $March 1 Capital 10 000 March 2 Rent 1 000March 3 Sales 550 March 7 Joe 190 3 610

March 7 Postages 20March 7 Balance c/d 530 5 390

550 10 000 190 550 10 000March 8 Balance b/d 530 5 390

Capital account $ $

March 7 Balance c/d 10 000 March 1 Bank 10 000360 March 8 Balance b/d 10 000

Purchases account $ $

March 2 Joe 4 000 March 7 Balance c/d 4 000March 8 Balance b/d 4 000

Joe account $ $

March 5 Purchases returns 200 March 2 Purchases 4 000March 7 Bank ($4000 − $200 × 95%) 3 610March 7 Discount received 190

4 000 4 000

Purchases returns account $ $

March 7 Balance c/d 200 March 5 Joe 200March 8 Balance b/d 200

Barney account $ $

March 3 Sales 2 000 March 7 Balance c/d 2 000March 8 Balances b/d 2 000

Cambridge International AS and A Level Accounting

18

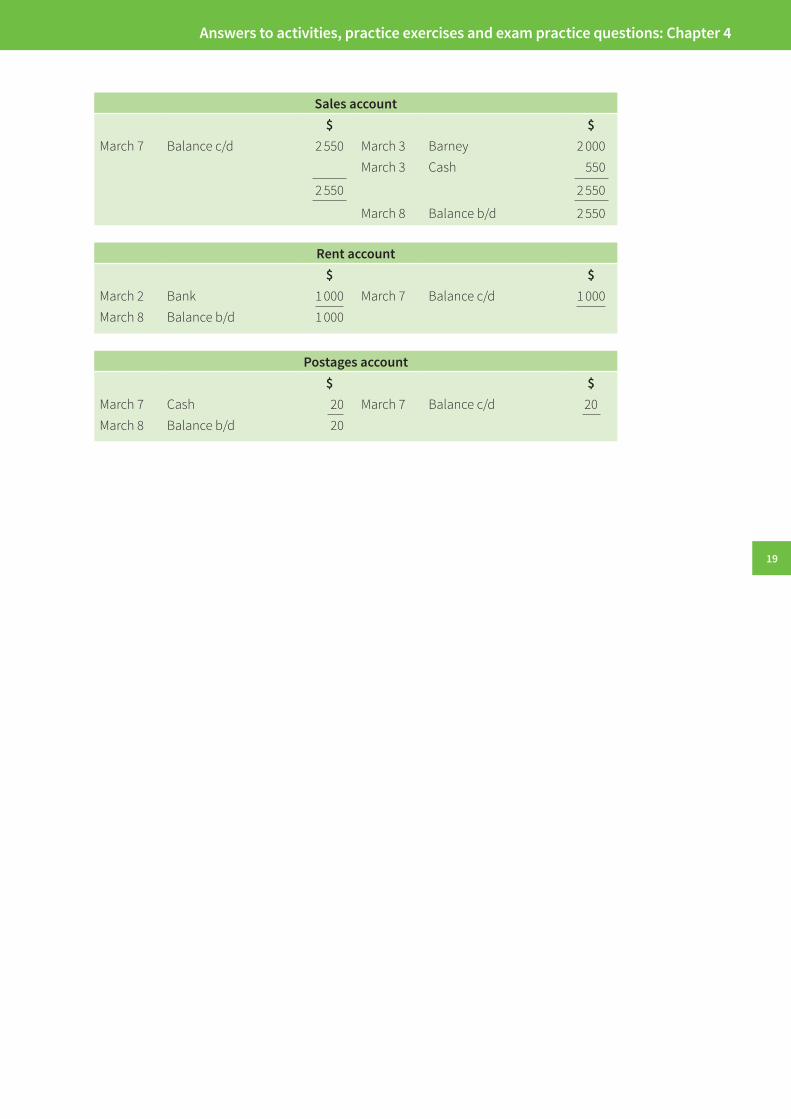

Sales account $ $

March 7 Balance c/d 2 550 March 3 Barney 2 000March 3 Cash 550

2 550 2 550

March 8 Balance b/d 2 550

Rent account $ $

March 2 Bank 1 000 March 7 Balance c/d 1 000March 8 Balance b/d 1 000

Postages account $ $

March 7 Cash 20 March 7 Balance c/d 20March 8 Balance b/d 20

Answers to activities, practice exercises and exam practice questions: Chapter 4

19

5 The classification of accounts and division of the ledgerActivitiesActivity 1

Account Personal Non-current asset

Current asset Revenue or other income

Expense

Capital ✓

Sales returns ✓

Delivery vans ✓

Purchases ✓

Rent payable ✓

Trade receivables2 ✓ ✓

Inventory ✓

Discount allowed ✓

Drawings ✓

Bank1 ✓

Rent receivable ✓

Trade payables3 ✓

Computer ✓

Wages ✓

Discount received ✓

Notes:

1 The bank account would be a ‘current liability’ if it was overdrawn.

2 Trade payables is the International Accounting Standards terminology for the aggregate amount owing to suppliers. It is not literally a personal account but is a description given to the total of the credit balances on the supplier personal accounts. Trade payables are presented as a ‘current liability’ in the statement of financial position (see later chapters) at the end of an accounting period.

3 Trade receivables is the International Accounting Standards terminology for the aggregate amount receivable from customers. It is not literally a personal account but is a description given to the total of the debit balances on the customer personal accounts. Trade receivables are presented as a ‘current asset’ in the statement of financial position (see later chapters) at the end of an accounting period.

20

Cambridge International AS and A Level Accounting

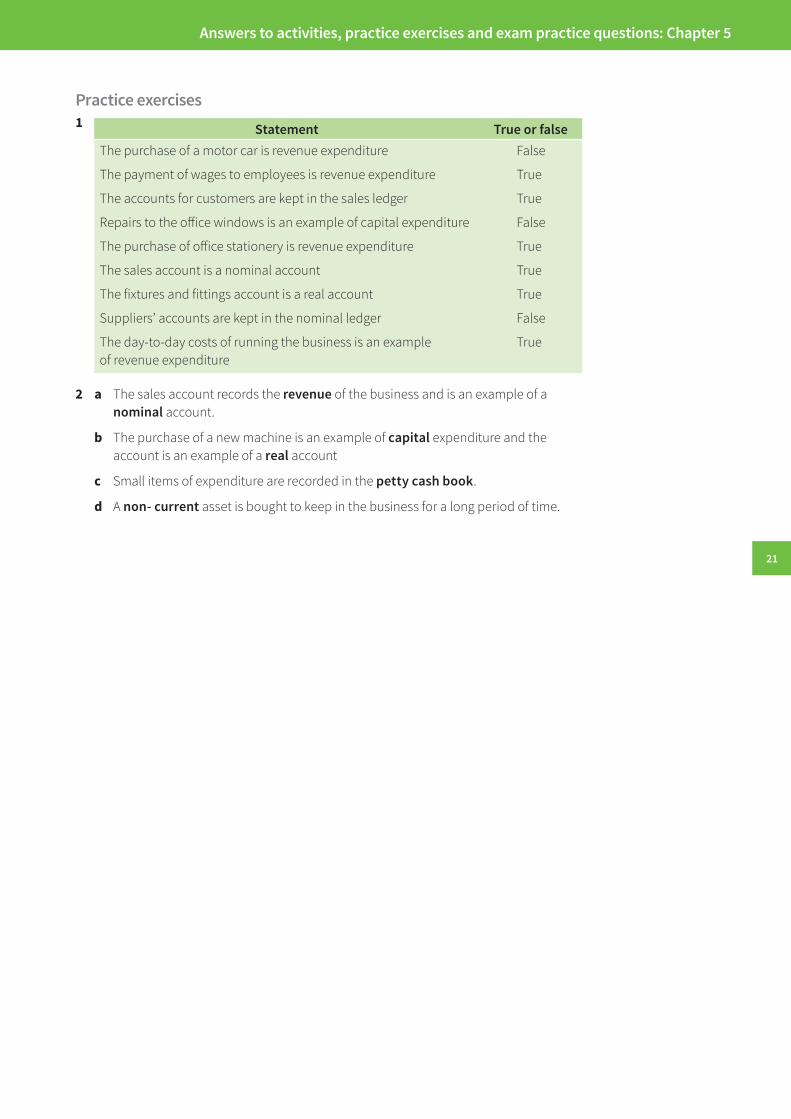

Practice exercises1 Statement True or false

The purchase of a motor car is revenue expenditure False

The payment of wages to employees is revenue expenditure True

The accounts for customers are kept in the sales ledger True

Repairs to the office windows is an example of capital expenditure False

The purchase of office stationery is revenue expenditure True

The sales account is a nominal account True

The fixtures and fittings account is a real account True

Suppliers’ accounts are kept in the nominal ledger False

The day-to-day costs of running the business is an example of revenue expenditure

True

2 a The sales account records the revenue of the business and is an example of a nominal account.

b The purchase of a new machine is an example of capital expenditure and the account is an example of a real account

c Small items of expenditure are recorded in the petty cash book.

d A non- current asset is bought to keep in the business for a long period of time.

21

Answers to activities, practice exercises and exam practice questions: Chapter 5

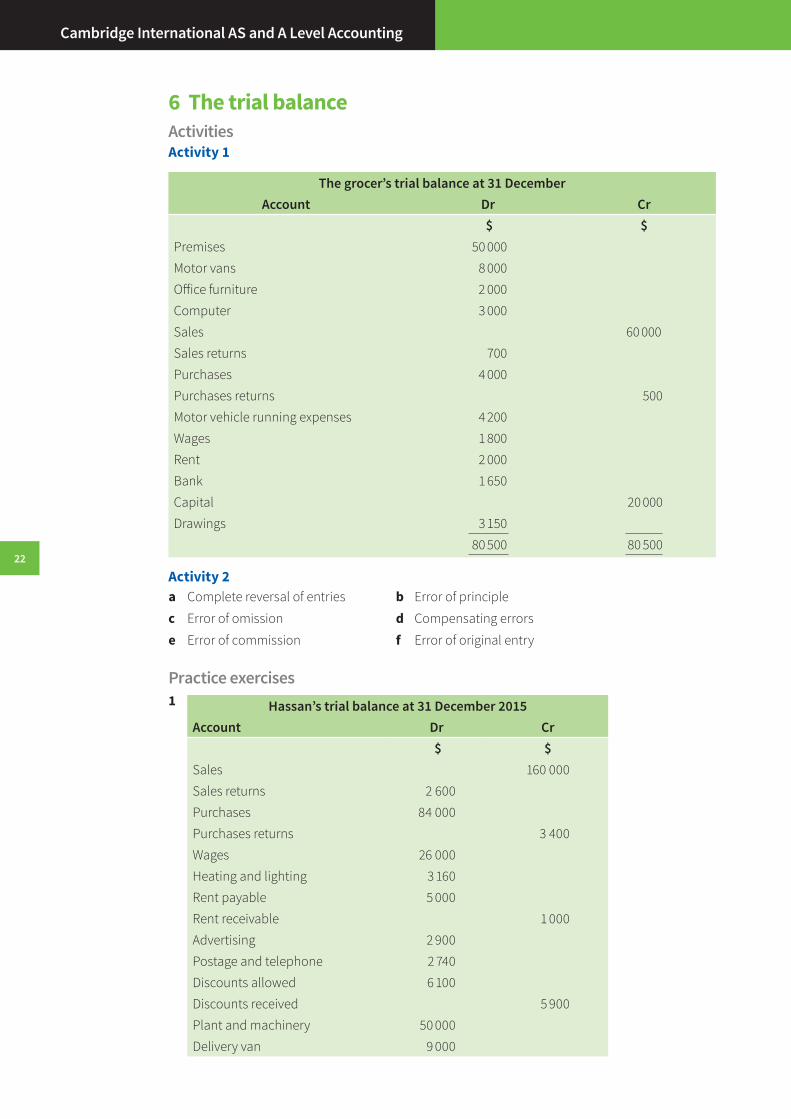

6 The trial balanceActivitiesActivity 1

The grocer’s trial balance at 31 December Account Dr Cr

$ $Premises 50 000Motor vans 8 000Office furniture 2 000Computer 3 000Sales 60 000Sales returns 700Purchases 4 000Purchases returns 500Motor vehicle running expenses 4 200Wages 1 800Rent 2 000Bank 1 650Capital 20 000Drawings 3 150

80 500 80 500

Activity 2a Complete reversal of entries b Error of principle

c Error of omission d Compensating errors

e Error of commission f Error of original entry

Practice exercises1 Hassan’s trial balance at 31 December 2015

Account Dr Cr$ $

Sales 160 000Sales returns 2 600Purchases 84 000Purchases returns 3 400Wages 26 000Heating and lighting 3 160Rent payable 5 000Rent receivable 1 000Advertising 2 900Postage and telephone 2 740Discounts allowed 6 100Discounts received 5 900Plant and machinery 50 000Delivery van 9 000

22

Cambridge International AS and A Level Accounting

$ $Bank 2 300Trade receivables 7 400Trade payables 3 700Drawings 8 800Capital 36 000

210 000 210 000

Notes:

• Items in the debit column are mainly assets or expenses.

• Items in the credit column are mainly income or liabilities.

2 Andrea’s corrected trial balance at 31 December 2015Account Dr Cr

$ $

Premises 70 000

Plant and machinery 30 000

Office equipment 5 000

Wages 7 600

Rent payable 4 000

Heating and lighting 1 500

Other operating expenses 1 720

Sales 133 000

Purchases 57 000

Discounts allowed 2 450

Discounts received 1 070

Bank 2 910

Trade receivables 14 000

Trade payables 10 140

Purchases returns 2 400

Sales returns 3 150

Rent receivable 1 200

Capital 80 000

Drawings 28 480

227 810 227 810

Exam practice questionsMultiple-choice questions1 B

2 B

3 C

4 C

23

Answers to activities, practice exercises and exam practice questions: Chapter 6

7 Income statements for sole tradersActivitiesActivity 1

LizTrading section of the income statement for the year ended 31 March 2016

Debit Credit$ $

Purchases 68 000 Sales 150 000Less: purchases returns 1 700 Less: sales returns 4 200

66 300 145 800

Activity 2

RodneyTrading section of the income statement for the year ended 30 September 2015

Debit Credit$ $

Purchases 84 000 Sales 140 000Less: purchases returns 1 400 Less: sales returns 1 200

82 600 138 800Less: closing inventory 4 900Cost of sales 77 700Gross profit 61 100

138 800 138 800

Activity 3

SofiaIncome statement for the year ended 31 December 2015

$ $Revenue 200 000Less: sales returns 6 300

193 700Cost of salesPurchases 86 500Less: purchases returns 5 790

80 710Less: inventory at 31 December 2015 10 000 70 710Gross profit 122 990Add: rent received 3 000Add: discounts received 3 210

129 200Less:Wages 61 050Rent payable 12 000Electricity 5 416Insurance 2 290

Cambridge International AS and A Level Accounting

24

Income statement for the year ended 31 December 2015$ $

Motor van expenses 11 400Discounts allowed 5 110Other operating expenses 3 760Loan interest 1 000 102 026Profit for the year 27 174

Activity 4

KhorExtract from the income statement for the year ended 31 December 2015

$ $ $Revenue 48 000Less: sales returns 1 600Less: cost of sales 46 400Opening inventory 4 000Purchases 21 000Less: purchases returns 900 20 100

24 100Less: closing inventory 7 500 16 600Gross profit 29 800

Activity 5

LamarIncome statement for the year ended 31 March 2016

$ $ $Revenue 104 000Less: sales returns 3 700

100 300

Less: cost of salesOpening inventory 6 000Purchases 59 000Less: purchases returns 2 550 56 450

62 450Less: closing inventory 10 000 52 450Gross profit 47 850Rent receivable 1 800Discounts receivable 770

50 420Less:Wages 13 000

Rent payable 2 000Heating and lighting 2 700Repairs to machinery 4 100

(cont.)

Answers to activities, practice exercises and exam practice questions: Chapter 7

25

Income statement for the year ended 31 March 2016$ $ $

Discounts allowed 1 030Loan interest 750 23 580Profit for the year 26 840

Activity 6

SaraIncome statement for the year ended 31 March 2016

$ $ $Sales 40 000Less: cost of salesOpening inventory 5 000Purchases 20 500Carriage inwards 1 320 21 820

26 820Less: closing inventory 3 000Cost of sales 23 820Gross profit 16 180Less:Wages 6 000Rent 10 000Electricity 2 600Carriage outwards 1 080Other operating expenses 1 250 20 930Loss for the year (4 750)

Practice exercises1 Hadlee

Income statement for the year ended 31 December 2015$ $ $

Sales 72 800Less: sales returns 1 600

71 200Less: cost of salesOpening inventory 11 000Purchases 28 540Less: purchases returns 2 144

26 39637 396

Less: closing inventory 9 000 28 396Gross profit 42 804Less: expensesWages 3 100Rent 4 000Heating and lighting 5 120

26

Cambridge International AS and A Level Accounting

$ $ $Advertising 2 400Other operating expenses 2 010Loan interest 250

16 880Profit for the year 25 924

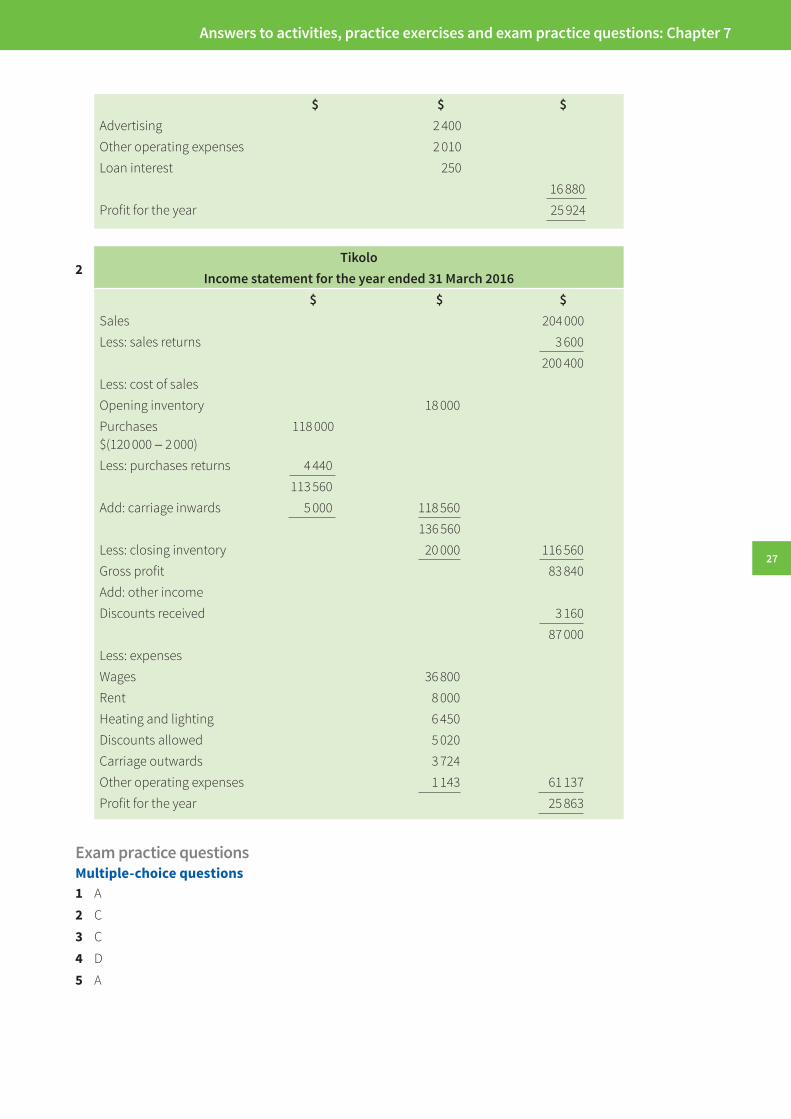

2 Tikolo

Income statement for the year ended 31 March 2016$ $ $

Sales 204 000Less: sales returns 3 600

200 400Less: cost of salesOpening inventory 18 000Purchases $(120 000 − 2 000)

118 000

Less: purchases returns 4 440113 560

Add: carriage inwards 5 000 118 560136 560

Less: closing inventory 20 000 116 560Gross profit 83 840Add: other incomeDiscounts received 3 160

87 000Less: expenses Wages 36 800Rent 8 000Heating and lighting 6 450Discounts allowed 5 020Carriage outwards 3 724Other operating expenses 1 143 61 137Profit for the year 25 863

Exam practice questionsMultiple-choice questions1 A

2 C

3 C

4 D

5 A

Answers to activities, practice exercises and exam practice questions: Chapter 7

27

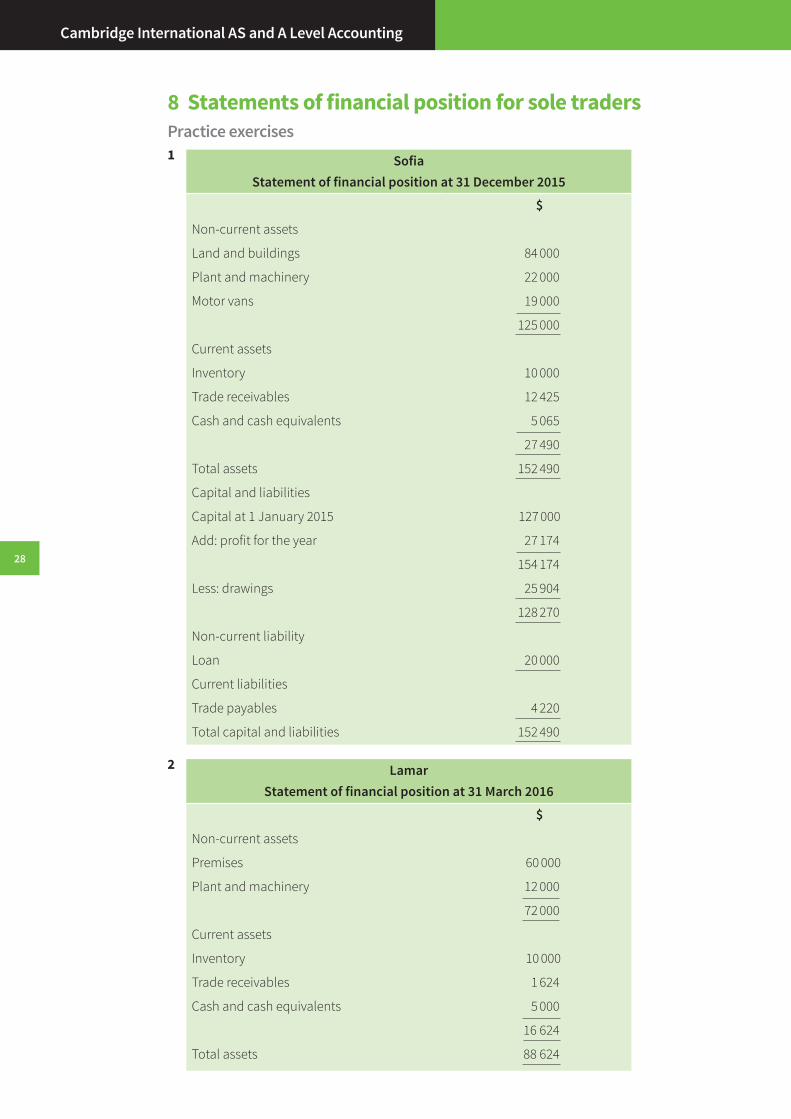

8 Statements of financial position for sole tradersPractice exercises1 Sofia

Statement of financial position at 31 December 2015

$

Non-current assets

Land and buildings 84 000

Plant and machinery 22 000

Motor vans 19 000

125 000

Current assets

Inventory 10 000

Trade receivables 12 425

Cash and cash equivalents 5 065

27 490

Total assets 152 490

Capital and liabilities

Capital at 1 January 2015 127 000

Add: profit for the year 27 174

154 174

Less: drawings 25 904

128 270

Non-current liability

Loan 20 000

Current liabilities

Trade payables 4 220

Total capital and liabilities 152 490

2 LamarStatement of financial position at 31 March 2016

$

Non-current assets

Premises 60 000

Plant and machinery 12 000

72 000

Current assets

Inventory 10 000

Trade receivables 1 624

Cash and cash equivalents 5 000

16 624

Total assets 88 624

Cambridge International AS and A Level Accounting

28

$

Capital and liabilities

Capital at 1 April 2016 55 000

Add: profit for the year 26 840

81 840

Less: drawings 10 096

71 744

Non-current liability

Loan 15 000

Current liabilities

Trade payables 1 880

Total capital and liabilities 88 624

3 Hadlee

Statement of financial position at 31 December 2015

$

Non-current assets

Plant and machinery 25 000

Office furniture 6 000

31 000

Current assets

Inventory 9 000

Trade receivables 4 740

Cash and cash equivalents 3 327

17 067

Total assets 48 067

Capital and liabilities

Opening capital 20 000

Add: profit for the year 25 924

45 924

Less: drawings (4 833)

41 091

Non-current liabilities

Loan 5 000

Current liabilities

Trade payables 1 976

Total capital and liabilities 48 067

Answers to activities, practice exercises and exam practice questions: Chapter 8

29

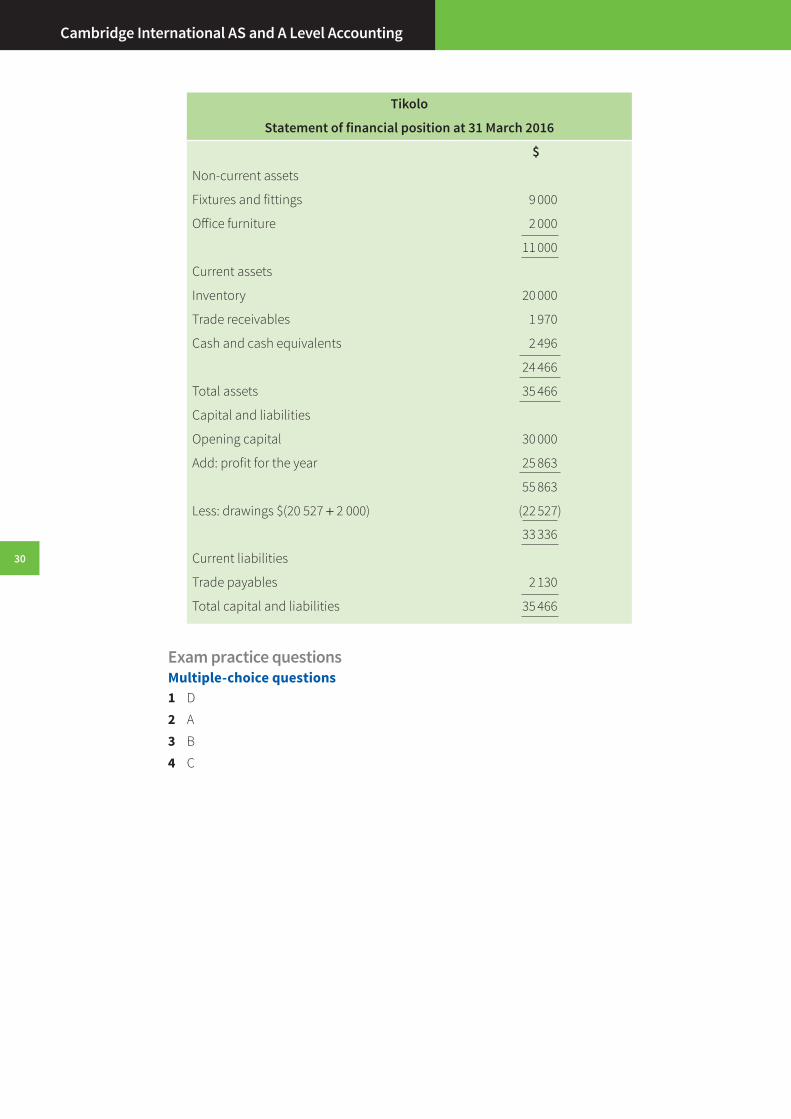

Tikolo

Statement of financial position at 31 March 2016

$

Non-current assets

Fixtures and fittings 9 000

Office furniture 2 000

11 000

Current assets

Inventory 20 000

Trade receivables 1 970

Cash and cash equivalents 2 496

24 466

Total assets 35 466

Capital and liabilities

Opening capital 30 000

Add: profit for the year 25 863

55 863

Less: drawings $(20 527 + 2 000) (22 527)

33 336

Current liabilities

Trade payables 2 130

Total capital and liabilities 35 466

Exam practice questionsMultiple-choice questions1 D

2 A

3 B

4 C

Cambridge International AS and A Level Accounting

30

9 Accounting principles or conceptsExam practice questionsMultiple-choice questions1 B

2 A

3 A

4 B

5 B

6 D

Answers to activities, practice exercises and exam practice questions: Chapter 9

31

10 Accruals and prepayments (the matching concept)ActivitiesActivity 1a

b Alexander’s total telephone expense for the year is $3410. This is made up of calls $(1450 + 360) = $1810 + line rental $(2000 − 400) = $1600.

c The amount of $360 for calls owing will appear under current liabilities. The figure of $400 will appear under current assets. Never net off the two amounts.

Activity 2

Rent payable account2015 2015

$ $Dec 31 Bank 1 000 Dec 31 Income

statement800

Dec 31 Balance c/d (rent prepaid)

200

1 000 1 0002016

Jan 1 Balance b/d 200

Electricity account2015 2015

$ $Dec 31 Bank 630 Dec 31 Income

statement810

Dec 31 Balance c/d (accrued expense)

180

810 8102016

Jan 1 Balance b/d 180

Telephone account2015 2015

$ $Dec 31 Bank 1 450 Dec 31 Balance c/d

(rental prepaid)400

Dec 31 Bank 2 000 Dec 31 Income statement

3 410

Dec 31 Balance c/d (calls owing)

360

3 810 3 8102016 2016

Jan 1 Balance b/d 400 Jan 1 Balance b/d 360

32

Cambridge International AS and A Level Accounting

Stationery account2015 2015

$ $Dec 31 Bank 420 Dec 31 Income

statement410

Dec 31 Balance c/d (amount owing)

130

Dec 31 Balance c/d (inventory)

140

550 5502016

Jan 1 Balance b/d 140 Jan 1 Balance b/d 130

Rent receivable account2015 2015

$ $Dec 31 Income

statement

400Dec 31 Bank

300

Dec 31 Balance c/d (rent owing)

100

400 4002016

Jan 1 Balance b/d 100

Activity 3a Devram

Income statement for the year ended 31 December 2015$ $

Gross profit 30 000Rent $(2 600 − 300) 2 300Electricity $(926 + 242) 1 168Stationery $(405 + 84 − 100) 389Motor expenses $(725 + 160) 885Interest on loan $(500 + 500) 1 000 5 742Profit for the year 24 258

Note:

Unpaid interest on the loan must be accrued although it is not mentioned in the question.

b DevramStatement of financial position at 31 December 2015

$ $Non-current assets 40 000Current assetsInventory 7 000Stationery inventory 100 7 100Trade receivables 1 600

(cont.)

33

Answers to activities, practice exercises and exam practice questions: Chapter 10

Statement of financial position at 31 December 2015$ $

Other receivables: prepaid rent 300Cash and cash equivalents 2 524

11 524Total assets 51 524Capital and liabilitiesCapital at 1 January 2015 20 000Profit for the year 24 258

44 258Less: drawings 5 120

39 138Non-current liabilitiesLong-term loan 10 000Current liabilitiesTrade payables 1 400Other payables $(242 + 84 + 160 + 500)

986

2 386Total capital and liabilities 51 524

Practice exercises1 a Prudence; accruals

b AntoniaIncome statement for the year ended 31 December 2015

$ $ $Sales 120 000Less: sales returns 7 300

112 700Less: cost of salesOpening inventory 5 660Purchases 62 400Less: purchases returns 4 190

58 21063 870

Less: closing inventory 8 000 55 870Gross profit 56 830Less: expensesWages $(17 310 + 558) 17 868Rent $(3 200 − 800) 2 400Heating and lighting $(2 772 + 328) 3 100Motor expenses 1 284Loan interest $(500 + 250) 750

25 402 Profit for the year 31 428

34

Cambridge International AS and A Level Accounting

c AntoniaStatement of financial position at 31 December 2015

$Non-current assetsPremises 24 000Motor vehicles 7 400

31 400Current assetsInventory 8 000Trade receivables 12 440Other receivables: prepaid rent 800Cash and cash equivalents 5 055

26 295Total assets 57 695Capital and liabilitiesOpening capital 16 000Profit for the year 31 428

47 428Less: drawings 7 036

40 392Non-current liabilitiesLoan 10 000Current liabilitiesTrade payables 6 167Other payables $(558 + 328 + 250) 1 136

7 303Total capital and liabilities 57 695

d The loan received is shown as a non-current liability as it is not due for repayment within 12 months from the date of the statement of financial position (31 December 2015). Any part of it which becomes due for repayment within 12 months will be shown as a current liability.

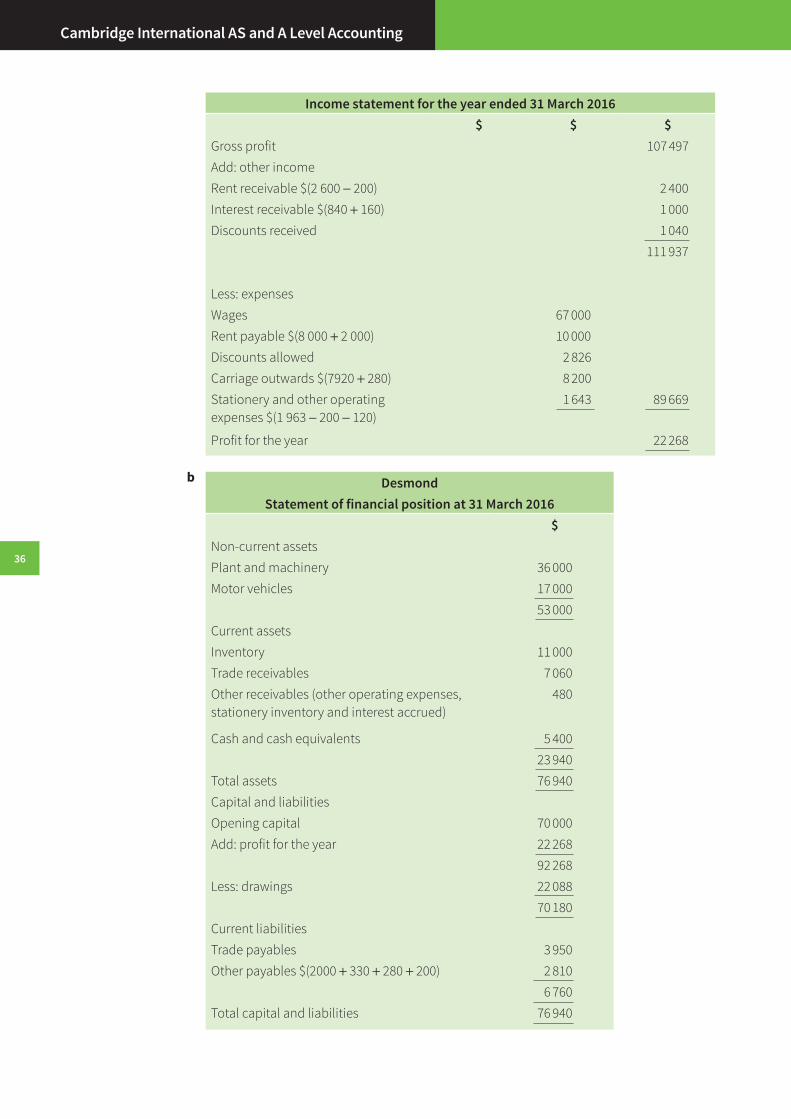

2 a DesmondIncome statement for the year ended 31 March 2016

$ $ $Sales 219 740Less: sales returns 17 420

202 320Less: cost of salesOpening inventory 9 000Purchases 100 100Less: purchases returns 8 777

91 323Add: carriage inwards $(5 170 + 330) 5 500 96 823

105 823Less: closing inventory 11 000 94 823

(cont.)

Answers to activities, practice exercises and exam practice questions: Chapter 10

35

Income statement for the year ended 31 March 2016$ $ $

Gross profit 107 497Add: other incomeRent receivable $(2 600 − 200) 2 400Interest receivable $(840 + 160) 1 000Discounts received 1 040

111 937

Less: expensesWages 67 000Rent payable $(8 000 + 2 000) 10 000Discounts allowed 2 826Carriage outwards $(7920 + 280) 8 200Stationery and other operating expenses $(1 963 − 200 − 120)

1 643 89 669

Profit for the year 22 268

b DesmondStatement of financial position at 31 March 2016

$Non-current assetsPlant and machinery 36 000Motor vehicles 17 000

53 000Current assetsInventory 11 000Trade receivables 7 060Other receivables (other operating expenses, stationery inventory and interest accrued)

480

Cash and cash equivalents 5 40023 940

Total assets 76 940Capital and liabilitiesOpening capital 70 000Add: profit for the year 22 268

92 268Less: drawings 22 088

70 180Current liabilitiesTrade payables 3 950Other payables $(2000 + 330 + 280 + 200) 2 810

6 760Total capital and liabilities 76 940

Cambridge International AS and A Level Accounting

36

c Carriage inwards is the cost of bringing the goods from the supplier. It is regarded as part of the cost of the item bought and appears in the calculation of the cost of sales.

Carriage outwards is the cost of delivering goods to the customer. It is regarded as a business expense and appears with other expenses in the income statement.

3 a The annual financial statements of a business are prepared using the accruals basis. Expenses of the period are matched with the income of the same period. It doesn’t matter whether or not the expenses have been paid. Therefore, any amounts owing but unpaid for in a particular year are brought into the financial statements for that year (accruals). Any amounts paid during the year, but relating to a future period (prepayments) are excluded from the financial statements for that year.

b b

Exam practice questionsMultiple-choice questions1 D

2 B

3 B

4 A

Rent account2015 2015

$ $Jan 1 Balance b/d 2 000 Dec 31 Income statement

$(2 000 + [3 × 2 500])9 500

Dec 31 Bank $(2500 × 4)

10 000

Dec 31 Balance c/d 2 500

12 000 12 0002016

Jan 1 Balance b/d 2 500

Electricity account 2015 2015

$ $Dec 31 Bank 1 800 Jan 1 Balance b/d 150

Balance c/d ($480 ÷ 3 × 2)

320

Dec 31 Income statement

1 970

2 120 2 1202016

Jan 1 Balance b/d 320

Answers to activities, practice exercises and exam practice questions: Chapter 10

37

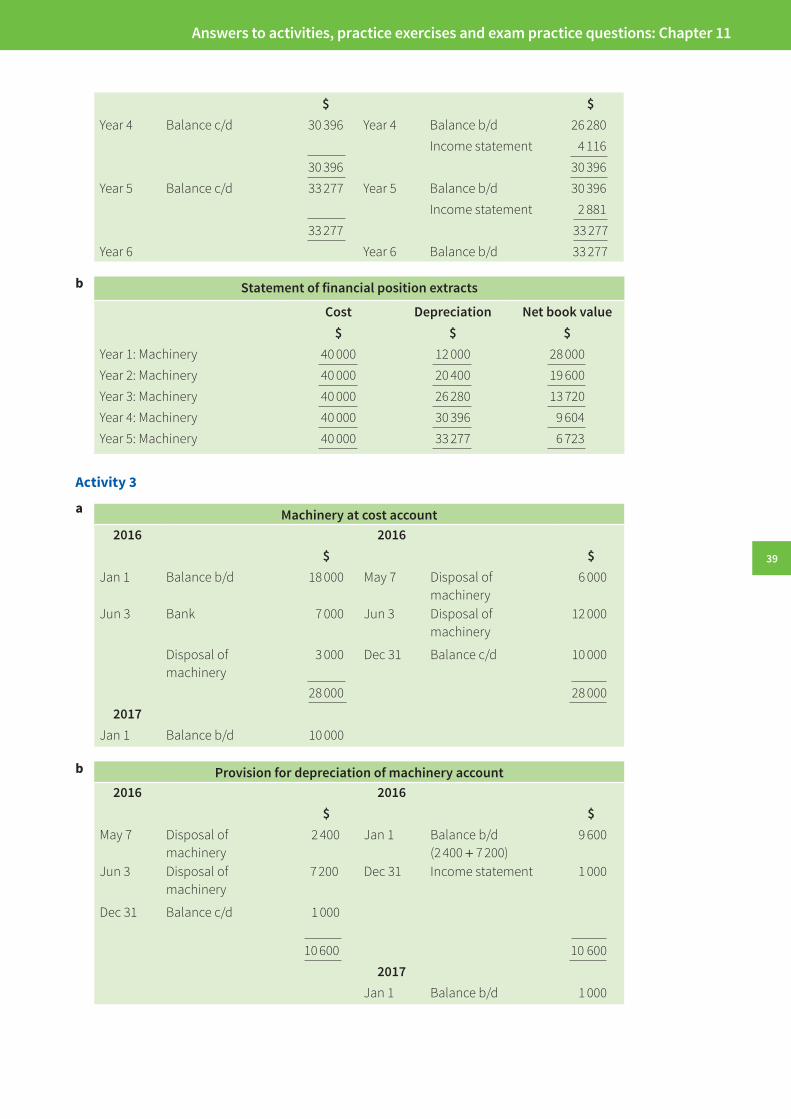

11 Provisions for the depreciation of non-current assetsActivitiesActivity 1a

b Statement of financial position extractsCost Depreciation Net book value

$ $ $Year 1: Motor vehicles 18 000 2 000 16 000Year 2: Motor vehicles 18 000 4 000 14 000Year 3: Motor vehicles 18 000 6 000 12 000Year 4: Motor vehicles 18 000 8 000 10 000Year 5: Motor vehicles 18 000 10 000 8 000Year 6: Motor vehicles 18 000 12 000 6 000Year 7: Motor vehicles 18 000 14 000 4 000

Activity 2a

Provision for depreciation of machinery account $ $

Year 1 Balance c/d 12 000 Year 1 Income statement 12 000Year 2 Balance c/d 20 400 Year 2 Balance b/d 12 000

Income statement 8 40020 400 20 400

Year 3 Balance c/d 26 280 Year 3 Balance b/d 20 400Income statement 5 880

26 280 26 280

Cambridge International AS and A Level Accounting

Provision for depreciation of motor vehicles account$ $

Year 1 Balance c/d 2 000 Year 1 Income statement 2 000Year 2 Balance c/d 4 000 Year 2 Balance b/d 2 000

Income statement 2 0004 000 4 000

Year 3 Balance c/d 6 000 Year 3 Balance b/d 4 000Income statement 2 000

6 000 6 000Year 4 Balance c/d 8 000 Year 4 Balance b/d 6 000

Income statement 2 0008 000 8 000

Year 5 Balance c/d 10 000 Year 5 Balance b/d 8 000Income statement 2 000

10 000 10 000Year 6 Balance c/d 12 000 Year 6 Balance b/d 10 000

Income statement 2 00012 000 12 000

Year 7 Balance c/d 14 000 Year 7 Balance b/d 12 000Income statement 2 000

14 000 14 000Year 8 Year 8 Balance b/d 14 000

38

$ $Year 4 Balance c/d 30 396 Year 4 Balance b/d 26 280

Income statement 4 11630 396 30 396

Year 5 Balance c/d 33 277 Year 5 Balance b/d 30 396Income statement 2 881

33 277 33 277Year 6 Year 6 Balance b/d 33 277

b Statement of financial position extracts

Cost Depreciation Net book value$ $ $

Year 1: Machinery 40 000 12 000 28 000Year 2: Machinery 40 000 20 400 19 600Year 3: Machinery 40 000 26 280 13 720Year 4: Machinery 40 000 30 396 9 604Year 5: Machinery 40 000 33 277 6 723

Activity 3

a Machinery at cost account2016 2016

$ $Jan 1 Balance b/d 18 000 May 7 Disposal of

machinery6 000

Jun 3 Bank 7 000 Jun 3 Disposal of machinery

12 000

Disposal of machinery

3 000 Dec 31 Balance c/d 10 000

28 000 28 0002017

Jan 1 Balance b/d 10 000

b Provision for depreciation of machinery account2016 2016

$ $May 7 Disposal of

machinery2 400 Jan 1 Balance b/d

(2 400 + 7 200)9 600

Jun 3 Disposal of machinery

7 200 Dec 31 Income statement 1 000

Dec 31 Balance c/d 1 000

10 600 10 6002017

Jan 1 Balance b/d 1 000

Answers to activities, practice exercises and exam practice questions: Chapter 11

39

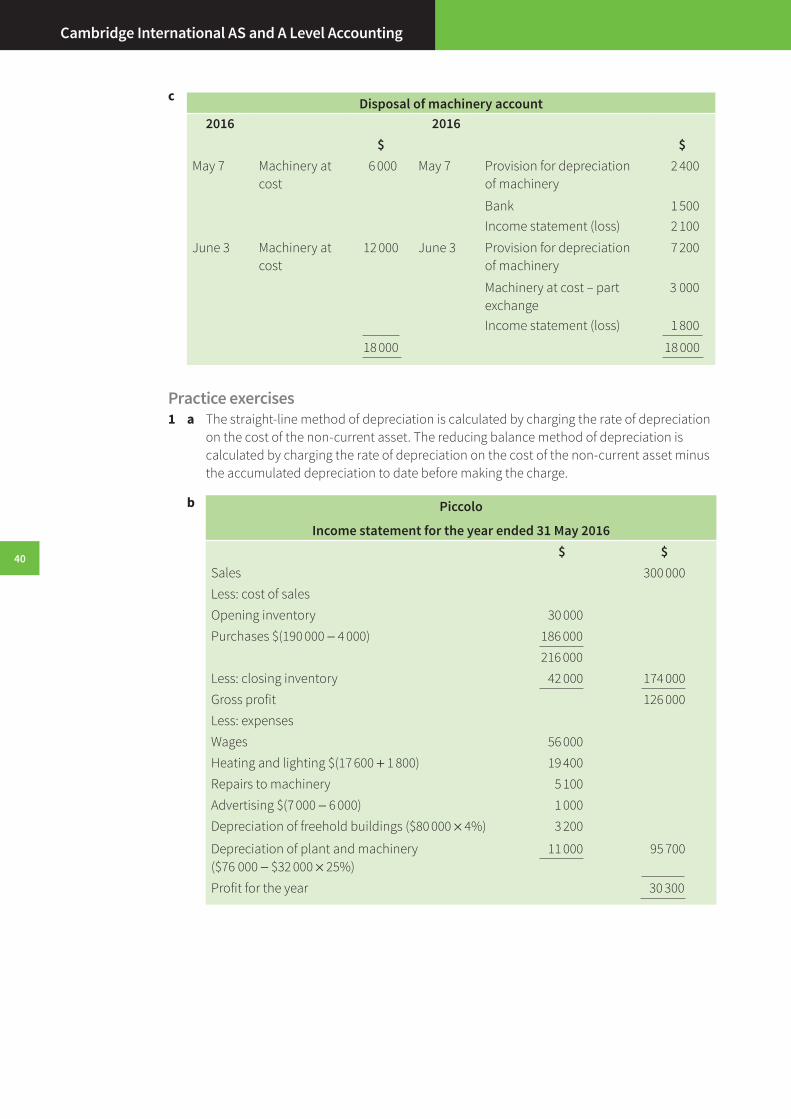

c Disposal of machinery account2016 2016

$ $May 7 Machinery at

cost6 000 May 7 Provision for depreciation

of machinery2 400

Bank 1 500Income statement (loss) 2 100

June 3 Machinery at cost

12 000 June 3 Provision for depreciation of machinery

7 200

Machinery at cost – part exchange

3 000

Income statement (loss) 1 800

18 000 18 000

Practice exercises1 a The straight-line method of depreciation is calculated by charging the rate of depreciation

on the cost of the non-current asset. The reducing balance method of depreciation is calculated by charging the rate of depreciation on the cost of the non-current asset minus the accumulated depreciation to date before making the charge.

b Piccolo

Income statement for the year ended 31 May 2016$ $

Sales 300 000Less: cost of salesOpening inventory 30 000Purchases $(190 000 − 4 000) 186 000

216 000Less: closing inventory 42 000 174 000Gross profit 126 000Less: expensesWages 56 000Heating and lighting $(17 600 + 1 800) 19 400Repairs to machinery 5 100Advertising $(7 000 − 6 000) 1 000Depreciation of freehold buildings ($80 000 × 4%) 3 200

Depreciation of plant and machinery ($76 000 − $32 000 × 25%)

11 000 95 700

Profit for the year 30 300

40

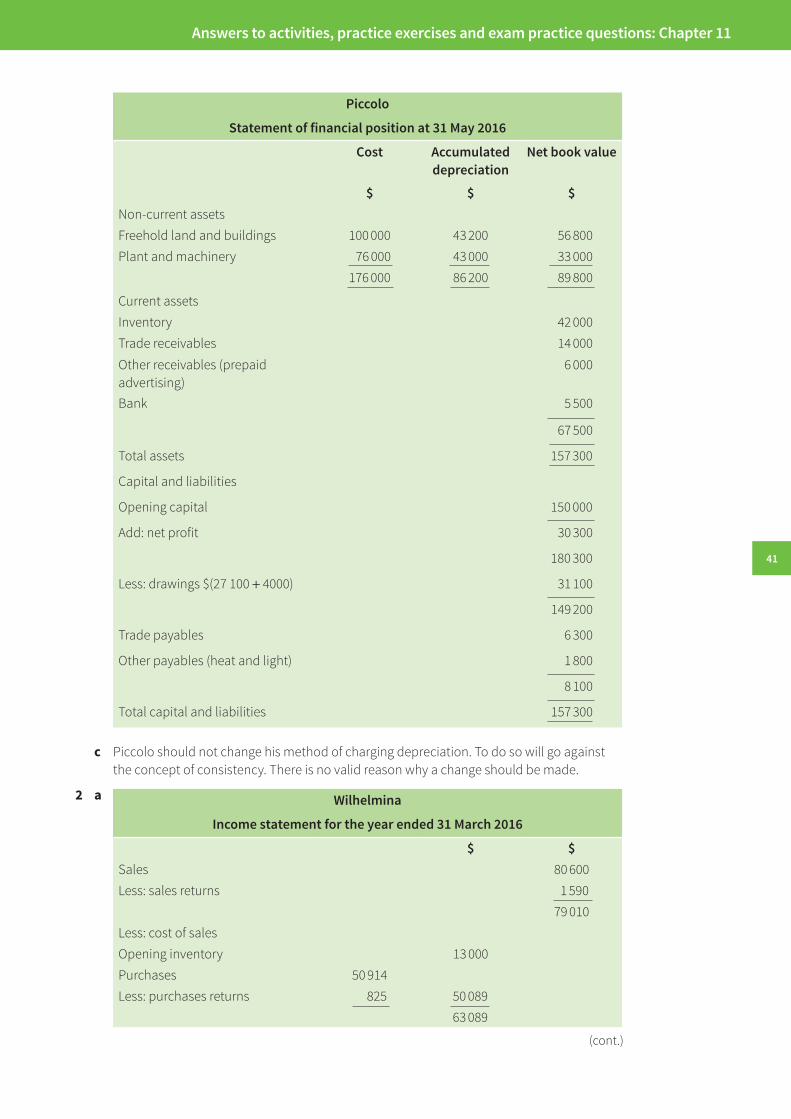

Cambridge International AS and A Level Accounting

Piccolo

Statement of financial position at 31 May 2016

Cost Accumulated depreciation

Net book value

$ $ $Non-current assetsFreehold land and buildings 100 000 43 200 56 800Plant and machinery 76 000 43 000 33 000

176 000 86 200 89 800

Current assetsInventory 42 000Trade receivables 14 000

Other receivables (prepaid advertising)

6 000

Bank 5 500

67 500

Total assets 157 300

Capital and liabilities

Opening capital 150 000

Add: net profit 30 300

180 300

Less: drawings $(27 100 + 4000) 31 100

149 200

Trade payables 6 300

Other payables (heat and light) 1 800

8 100

Total capital and liabilities 157 300

c Piccolo should not change his method of charging depreciation. To do so will go against the concept of consistency. There is no valid reason why a change should be made.

2 a

Wilhelmina

Income statement for the year ended 31 March 2016

$ $Sales 80 600Less: sales returns 1 590

79 010Less: cost of salesOpening inventory 13 000Purchases 50 914Less: purchases returns 825 50 089

63 089

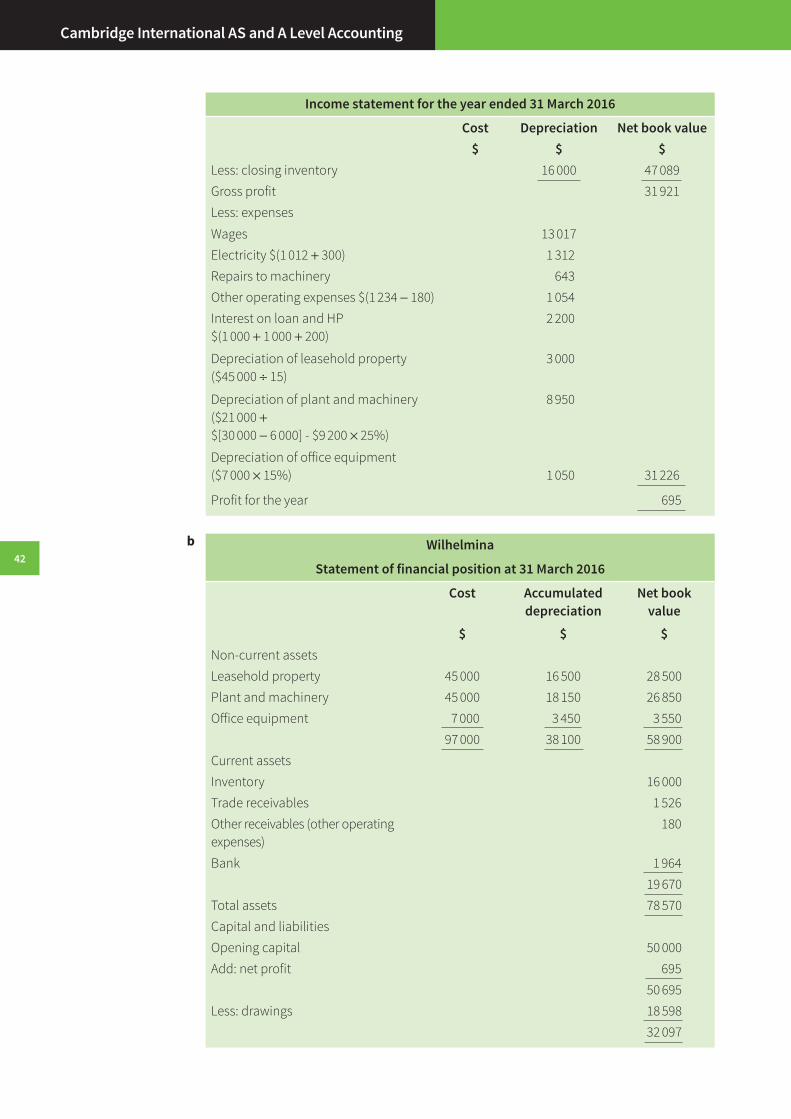

(cont.)

Answers to activities, practice exercises and exam practice questions: Chapter 11

41

Income statement for the year ended 31 March 2016

Cost Depreciation Net book value$ $ $

Less: closing inventory 16 000 47 089Gross profit 31 921Less: expenses

Wages 13 017Electricity $(1 012 + 300) 1 312Repairs to machinery 643Other operating expenses $(1 234 − 180) 1 054Interest on loan and HP $(1 000 + 1 000 + 200)

2 200

Depreciation of leasehold property ($45 000 ÷ 15)

3 000

Depreciation of plant and machinery ($21 000 + $[30 000 − 6 000] - $9 200 × 25%)

8 950

Depreciation of office equipment ($7 000 × 15%)

1 050

31 226

Profit for the year 695

b Wilhelmina

Statement of financial position at 31 March 2016

Cost Accumulated depreciation

Net book value

$ $ $Non-current assetsLeasehold property 45 000 16 500 28 500Plant and machinery 45 000 18 150 26 850Office equipment 7 000 3 450 3 550

97 000 38 100 58 900Current assetsInventory 16 000Trade receivables 1 526Other receivables (other operating expenses)

180

Bank 1 96419 670

Total assets 78 570Capital and liabilitiesOpening capital 50 000Add: net profit 695

50 695Less: drawings 18 598

32 097

Cambridge International AS and A Level Accounting

42

$ $ $Non-current liabilitiesLoan (repayable 2020) 20 000Trade payables 973Other payables (electricity and loan)

1 300

Loan for machinery (including accrued interest $200)

24 200

26 473Total capital and liabilities 78 570

Notes:

• Hire purchase is not on the syllabus. However, the amount due to the company from whom the machinery was bought is $24 000 $(30 000 − 6 000). This is added on to the cost of the machinery $(21 000 + 24 000).

• Interest to be paid over the course of HP agreement is $800 (4 × $200) and as the agreement was for one year and began on 1 January 2016, three month’s interest,

( 3

12 or 1

4 × $800 = $200) must be accrued at 31 March 2016.

• The entire loan for the machinery is repayable within 12 months from the date of the statement of financial position. This means that the whole of the amount is treated as a current liability.

Exam practice questionsMultiple-choice questions1 D

2 C

3 A

4 A

Structured question1 a Businesses will use different methods of depreciation because non-current assets

lose value at different rates during their working life. For example, a motor vehicle will depreciate more in the early years of its life. Thus, the reducing balance method of depreciation is best for this asset. On the other hand, something like office furniture will lose its value evenly over its life and is depreciated using the straight-line method.

b

Asset disposal account 2016 2016

$ $May 31 Motor vehicles

at cost8 000 May 31 Motor vehicles

accumulated depreciation

4 000

Bank 3 000Income statement 1 000

8 000 8 000

Answers to activities, practice exercises and exam practice questions: Chapter 11

43

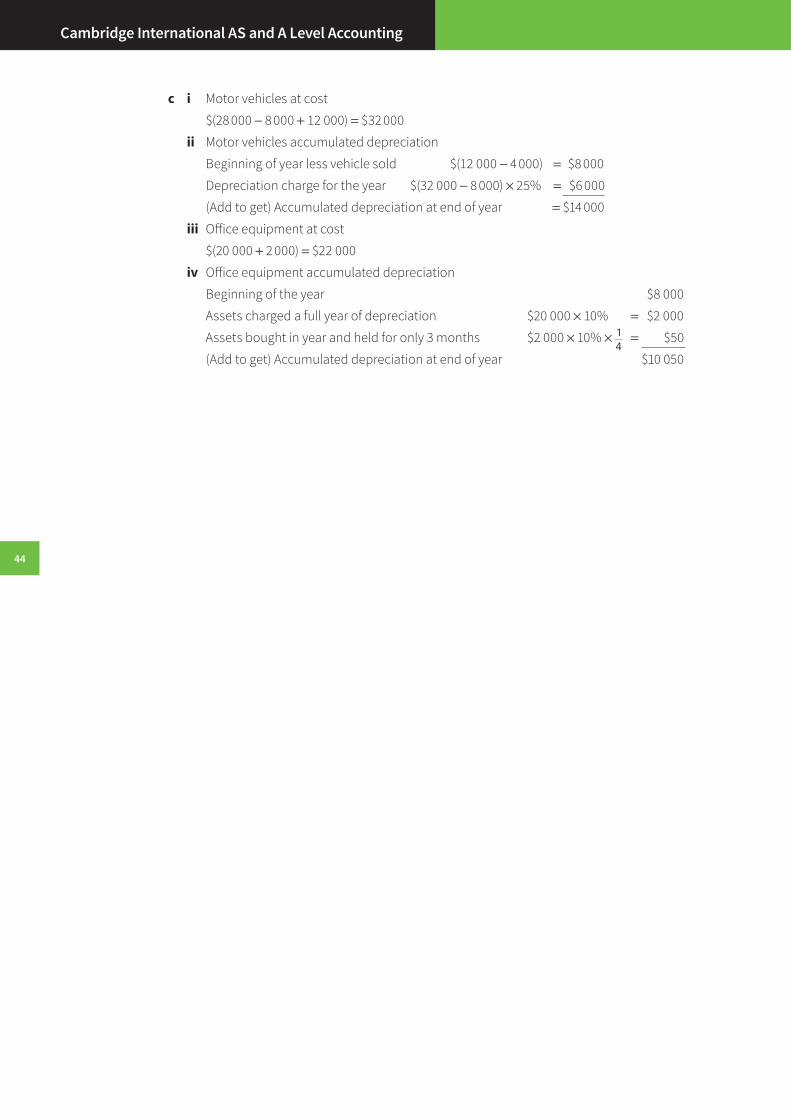

c i Motor vehicles at cost

$(28 000 − 8 000 + 12 000) = $32 000

ii Motor vehicles accumulated depreciation

Beginning of year less vehicle sold $(12 000 − 4 000) = $8 000

Depreciation charge for the year $(32 000 − 8 000) × 25% = $6 000

(Add to get) Accumulated depreciation at end of year = $14 000

iii Office equipment at cost

$(20 000 + 2 000) = $22 000

iv Office equipment accumulated depreciation

Beginning of the year $8 000

Assets charged a full year of depreciation $20 000 × 10% = $2 000

Assets bought in year and held for only 3 months $2 000 × 10% × 14

= $50

(Add to get) Accumulated depreciation at end of year $10 050

Cambridge International AS and A Level Accounting

44

12 Irrecoverable and doubtful debtsActivitiesActivity 1a 2012: $(4 000 + 1 150) = $5 150 2013: $(6 400 + 1 375) = $7 775 2014: $(7 500 + 1 125) = $8 625 2015: $(3 000 + 1 250) = $4 250 2016: $(8 300 + 1 420) = $9 720

b

Practice exercises1 a

Provision for doubtful debts account$ $

2012 2012Mar 31 Balance c/d 5 150 Mar 31 Income statement 5 150

Apr 1 Balance b/d 5 1502013 2013

Mar 31 Balance c/d 7 775 Mar 31 Income statement 2 6257 775 7 775

Apr 1 Balance b/d 7 7752014 2014

Mar 31 8 625 Mar 31 Income statement 8508 625 8 625

Apr 1 Balance b/d 8 6252015 2015

Mar 31 Income statement 4 375Balance c/d 4 250

8 625 8 625Apr 1 Balance b/d 4 250

2016 2016Mar 31 Balance c/d 9 720 Mar 31 Income statement 5 470

9 720 9 720Apr 1 Balance b/d 9 720

DavidIncome statement for the year ended 31 March 2016

$ $ $Revenue $(210 000 − 4 000) 206 000Less: sales returns 9 240

196 760Less: cost of salesOpening inventory 4 000Purchases 84 000Less: purchases returns 5 112

78 888Add: carriage inwards 1 840 80 728

84 728

Answers to activities, practice exercises and exam practice questions: Chapter 12

(cont.)

4545

Income statement for the year ended 31 March 2016$ $ $

Less: closing inventory $(5 000 + 3 000) 8 000 76 728Gross profit 120 032Add: other incomeReduction in provision for doubtful debts |$(800 − 550)

250

Discounts received 2 480122 762

Less: expensesWages $(37 000 + 400) 37 400Rent $(7 600 − 1600) 6 000Telephone $(900 + 100) 1 000Electricity $(1 027 + 360) 1 387Postage and stationery 359Carriage outwards 1 220Discounts allowed 6 015Irrecoverable debts $(3 100 +1 700) 4 800Depreciation of leasehold premises ($70 000 × 5%)

3 500

Depreciation of delivery vans ($18 000 − $3 600 × 25%)

3 600

Depreciation of office furniture ($3 000 × 10%)

300

65 581

Profit for the year 57 181

Notes:

1 The calculation for the adjustment is as follows:

Trade receivables account$ $

Opening balance 19 800 Goods on sale or return 4 000Specific irrecoverable debt 1 700Specific provision 3 100Balance 11 000

19 800 19 800

Provision required = 11 000 × 5% = $550

Existing provision $800

Reduction in provision $250

2 It would have been possible to combine the specific provision for the irrecoverable debt into the provision for doubtful debts account. This would be shown as:

Provision for doubtful debts account$ $

Specific irrecoverable debt 3 100 Opening balance 800Balance c/d 550 Income statement 2 850

3 650 3 650

Cambridge International AS and A Level Accounting

46

3 The net effect on the income statement is the same. In the statement above there is a credit of $250, being the reduction in the provision, and expenses of $3100 included in the figure for irrecoverable debts. You can use either approach. In practice it is usual to keep irrecoverable debts and the provision for doubtful debts as two separate accounts.

b

Note:

The total assets equal the total capital and liabilities, thus the statement of financial position balances. If you don’t get the two figures the same then look for the difference, but don’t waste time.

David

Statement of financial position at 31 March 2016

Cost Accumulated depreciation

Net book value

$ $ $Non-current assetsLeasehold premises 70 000 8 500 61 500Delivery vans 18 000 7 200 10 800Office furniture 3 000 1 800 1 200

91 000 17 500 73 500Current assetsInventory 8 000Trade receivables $(19 800 − 4 000 − 1 700 − 3 100)

11 000

Less: provision for doubtful receivables 550 10 450Other receivables (rent prepaid) 1 600Cash and cash equivalents 1 245

21 295Total assets 94 795Capital and liabilitiesOpening capital 50 000Add: profit for the year 57 181

107 181Less: drawings 20 446

86 735Current liabilitiesTrade payables 7 200Other Payables $(400 + 360 + 100) 860

8 060Total capital and liabilities 94 795

Answers to activities, practice exercises and exam practice questions: Chapter 12

47

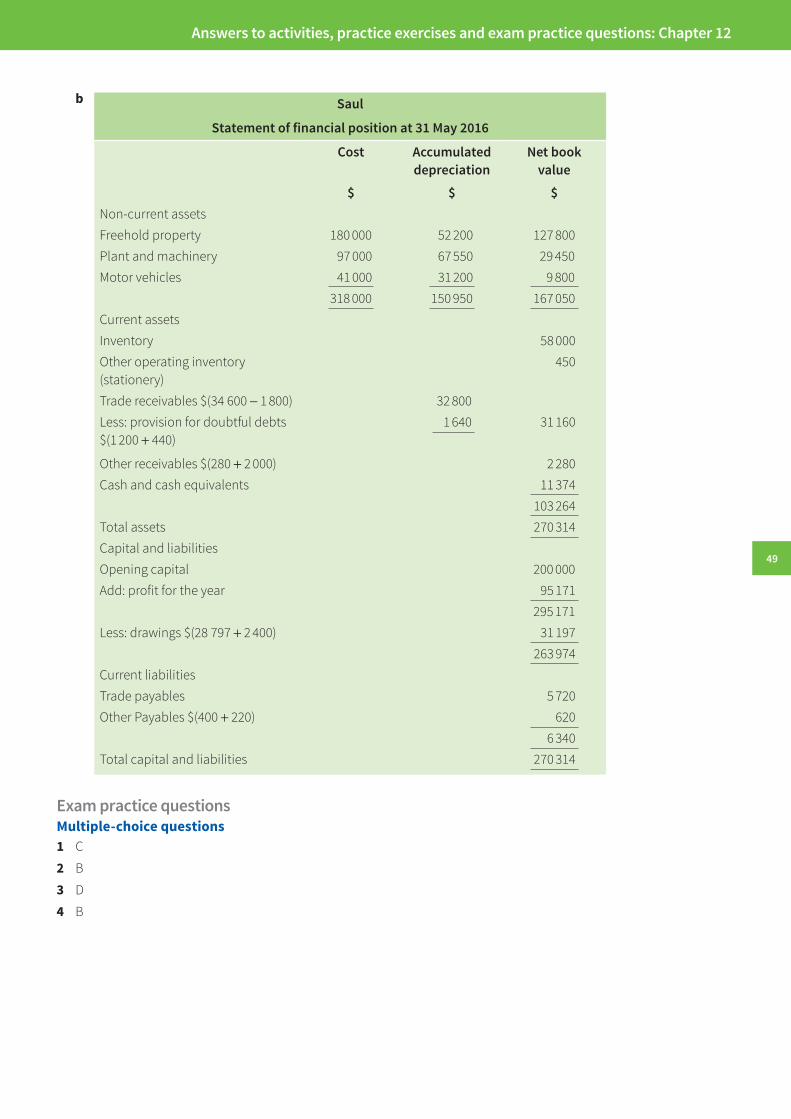

2 a Saul

Income statement for the year ended 31 May 2016

$ $ $Sales 700 000Less: sales returns 6 670

693 330Less: cost of salesOpening inventory 40 000Purchases (410 890 − 2 400) 408 490Less: purchases returns 3 112 405 378

445 378Add: carriage inwards 4 240

449 618Less: closing inventory 58 000 391 618Gross profit 301 712Add: other incomeRent receivable $(1 020 + 280) 1 300Discounts received 2 942

305 954Less: expensesWages 137 652Rent payable $(10 000 − 2 000) 8 000Heating and lighting $(4 720 + 400) 5 120Telephone and postage 3 217Stationery $(6195 + 220 − 450) 5 965Repairs to machinery 17 600Discounts allowed 3 220Carriage outwards 1 819Increase in provision for doubtful debts[($34 600 − $1 800) × 5%] − 1 200 440Irrecoverable debt written off 1 800Depreciation − Freehold property ($180 000 × 4%)

7 200

Depreciation − Plant and machinery ($97 000 × 15%)

14 550

Depreciation − Motor vehicles ($41 000 − 27 000 × 30%)

4 200

210 783

Profit for the year 95 171

Cambridge International AS and A Level Accounting

48

b Saul

Statement of financial position at 31 May 2016

Cost Accumulated depreciation

Net book value

$ $ $Non-current assetsFreehold property 180 000 52 200 127 800Plant and machinery 97 000 67 550 29 450Motor vehicles 41 000 31 200 9 800

318 000 150 950 167 050Current assetsInventory 58 000Other operating inventory (stationery)

450

Trade receivables $(34 600 − 1 800) 32 800Less: provision for doubtful debts $(1 200 + 440)

1 640 31 160

Other receivables $(280 + 2 000) 2 280Cash and cash equivalents 11 374

103 264Total assets 270 314Capital and liabilitiesOpening capital 200 000Add: profit for the year 95 171

295 171Less: drawings $(28 797 + 2 400) 31 197

263 974Current liabilitiesTrade payables 5 720Other Payables $(400 + 220) 620

6 340Total capital and liabilities 270 314

Exam practice questionsMultiple-choice questions1 C

2 B

3 D

4 B

Answers to activities, practice exercises and exam practice questions: Chapter 12

49

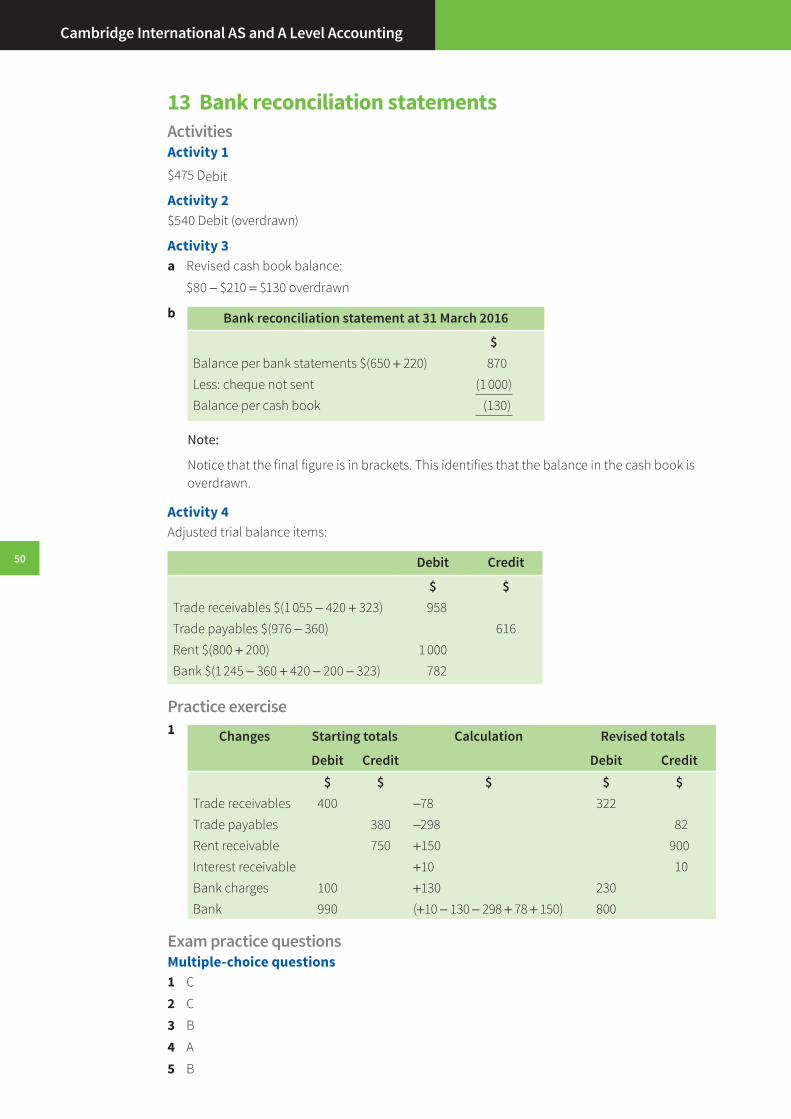

13 Bank reconciliation statementsActivitiesActivity 1$475 Debit

Activity 2$540 Debit (overdrawn)

Activity 3a Revised cash book balance:

$80 − $210 = $130 overdrawn

b Bank reconciliation statement at 31 March 2016

$Balance per bank statements $(650 + 220) 870 Less: cheque not sent (1 000)Balance per cash book (130)

Note:

Notice that the final figure is in brackets. This identifies that the balance in the cash book is overdrawn.

Activity 4Adjusted trial balance items:

Debit Credit

$ $Trade receivables $(1 055 − 420 + 323) 958Trade payables $(976 − 360) 616Rent $(800 + 200) 1 000 Bank $(1 245 − 360 + 420 − 200 − 323) 782

Practice exercise1

Changes Starting totals Calculation Revised totals

Debit Credit Debit Credit$ $ $ $ $

Trade receivables 400 −78 322Trade payables 380 −298 82Rent receivable 750 +150 900Interest receivable +10 10Bank charges 100 +130 230Bank 990 (+10 − 130 − 298 + 78 + 150) 800

Exam practice questionsMultiple-choice questions1 C

2 C

3 B

4 A

5 B

50

Cambridge International AS and A Level Accounting

50

14 Control accountsActivitiesActivity 1

Byit Limited Purchase ledger control account

2016 $ 2016 $Mar 1 Balance b/d 16 Mar 1 Balance b/d 10 000Mar 31 Purchases returns 824 Mar 31 Purchases journal 33 700

Bank 27 500 Balance c/d 156Discounts received 1 300Balance c/d 14 216

43 856 43 856Apr 1 Balance b/d 156 Apr 1 Balance b/d 14 216

Activity 2

Soldit Limited Sales ledger control account

2016 $ 2016 $May 1 Balance b/d 27 640 Balance b/d 545May 31 Sales journal 109 650 Sales returns 2 220

Irrecoverable debt recovered 490 Bank 98 770Balance c/d 800 Discounts allowed 3 150

Bank – irrecoverable debt recovered

490

Purchase ledger contra

2 624

Balance c/d 30 781138 580 138 580

Jun 1 Balance b/d 30 781 Jun 1 Balance b/d 800

Activity 3a Purchase ledger

balancesSales ledger

balancesDebit Credit Debit Credit

$ $ $ $Before amendment 64 7 217 Before amendment 23 425 390Deduct invoice entered twice

(100) Correction of invoice $326 entered as $362

(36)

–

Debit balance incorrectly listed as credit balance

50

(50)

Corrected balances 23 389 390

Corrected balances 114 7 067

51

Answers to activities, practice exercises and exam practice questions: Chapter 14

52

b Corrected purchase ledger control2015 $ 2015 $

Dec 31 Cancellation of invoice 100 Dec 31 Balance b/d 7 847Discounts received 84 Balance c/d 114

Sales ledger contra –Trazom

710

Balance c/d 7 0677 961 7 961

2016 2016Jan 1 Balance b/d 114 Jan 1 Balance b/d 7 067

Corrected sales ledger control2015 $ 2015 $

Dec 31 Balance b/d 22 909 Dec 31Sales journal understatement

800 Purchase ledger contra – Trazom

710

Balance c/d 390 Balance c/d 23 38924 099 24 099

2016 2016Jan 1 Balance b/d 23 389 Jan 1 Balance b/d 390

c Amended profit for the year ended 31 December 2015$

Profit per draft income statement 31 000Add:Reduction in purchases 100Discounts received omitted 84Increase in sales 800Amended profit for the year 31 984

d Statement of financial position extract at 31 December 2015$ $

Trade receivablesSales ledger 23 389Purchase ledger 114 23 503Trade payablesPurchase ledger 7 067Sales ledger 390 7 457

Cambridge International AS and A Level Accounting

52

53

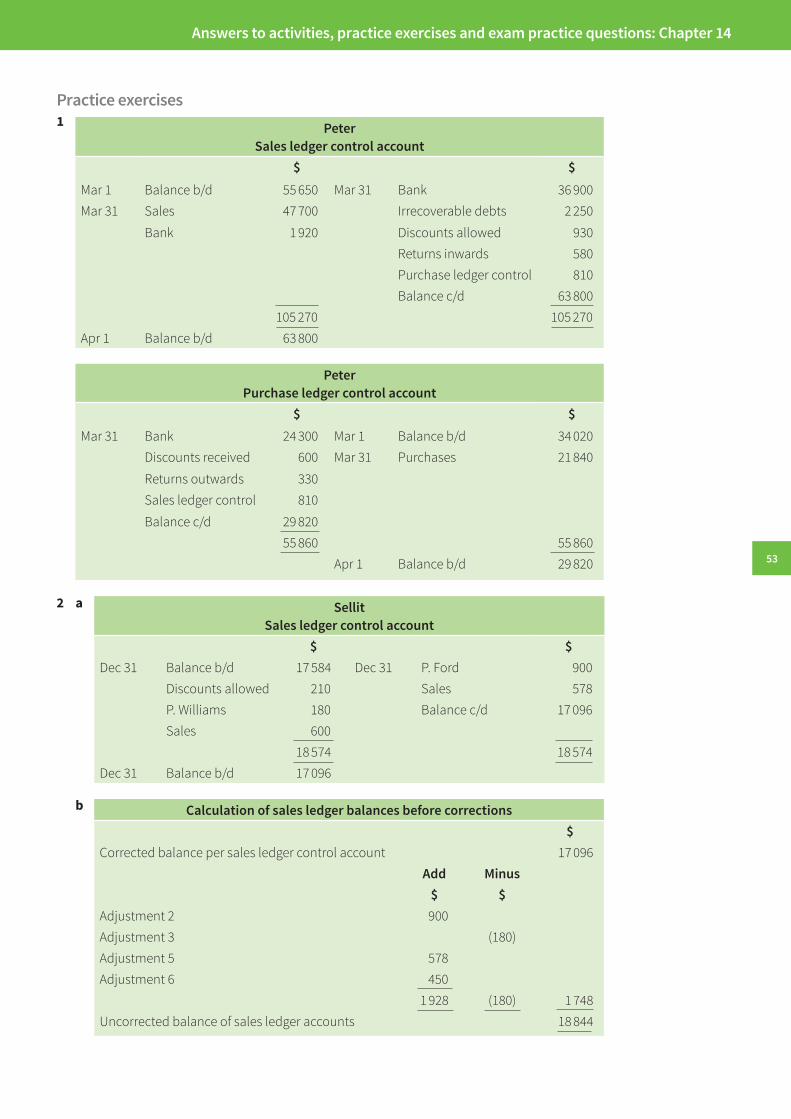

Practice exercises1 Peter

Sales ledger control account$ $

Mar 1 Balance b/d 55 650 Mar 31 Bank 36 900Mar 31 Sales 47 700 Irrecoverable debts 2 250

Bank 1 920 Discounts allowed 930Returns inwards 580Purchase ledger control 810Balance c/d 63 800

105 270 105 270Apr 1 Balance b/d 63 800

PeterPurchase ledger control account

$ $Mar 31 Bank 24 300 Mar 1 Balance b/d 34 020

Discounts received 600 Mar 31 Purchases 21 840

Returns outwards 330Sales ledger control 810

Balance c/d 29 82055 860 55 860

Apr 1 Balance b/d 29 820

2 a SellitSales ledger control account

$ $Dec 31 Balance b/d 17 584 Dec 31 P. Ford 900

Discounts allowed 210 Sales 578P. Williams 180 Balance c/d 17 096Sales 600

18 574 18 574Dec 31 Balance b/d 17 096

b Calculation of sales ledger balances before corrections$

Corrected balance per sales ledger control account 17 096Add Minus

$ $Adjustment 2 900Adjustment 3 (180)Adjustment 5 578Adjustment 6 450

1 928 (180) 1 748Uncorrected balance of sales ledger accounts 18 844

Answers to activities, practice exercises and exam practice questions: Chapter 14

53

54

Proof

Sales ledger control account Sales ledger balances$ $

Balances from above 17 584 18 844Adjustment 1 210Adjustment 2 (900) (900)Adjustment 3 180 180Adjustment 4 600Adjustment 6 (450)

17 674 17 674

Note:

The goods treated as a sale to Will Dither will be in both balances at the time they are calculated.

c Journal entriesAccount Debit Credit

$ $P. Ford 900B. Ford 900Receipt from customer posted to wrong accountNote: the control accounts do not require correctionP. Williams 180Sales 180Correction of sales invoice recorded in errorNote: the sales ledger personal and control accounts and the revenue account all require correction

Sales 578Will Dither 578Correction of goods on sale or return treated as sale in errorNote: the sales ledger personal and control accounts and the revenue account all require correction. In addition, the goods held by Dither will have to be included in the year end inventory

W. Yeo 450Correction of sales invoice for $3160 recorded as $3600 in errorNote: the only error was in the personal account

Cambridge International AS and A Level Accounting

3 a There may be a credit balance on the sales ledger control account because of:

• an overpayment by a customer

• a payment in advance by a customer.

54

55

b JulieCorrected sales ledger control account

2016 $ 2016 $May 31 Balance b/d 18 640 May 31 Purchase ledger control 650

Irrecoverable debts 400Cash sales 1 760 Balance c/d 20 586Balance c/d 436

21 236 21 236June 1 Balance b/d 20 586 June 1 Balance b/d 436

Exam practice questionsMultiple-choice questions1 B

2 C

3 C

Structured questions1 a Two advantages to a business of maintaining sales and purchase ledger control accounts:

• provides quick totals of trade receivables and payables

• helps to detect errors in the accounts.

b Haeun JooPurchase ledger control account

2016 $ 2015 $Apr 30 Bank 1 118 970 May 1 Balance b/d 64 680

Discounts received 47 100 2016Returns outwards 18 600 Apr 30 Purchases 1 236 210Sales ledger control 7 815Balance c/d 108 405

1 300 890 1 300 890May 1 Balance b/d 108 405

c Haeun Joo

Amended purchase ledger control account$ $

Contra with sales ledger 1 275 Balance from (a) 108 405Bank 2 175 Discounts received 1 500Balance c/d 109 515 Purchases 3 060

112 965 112 965

Balance b/d 109 515

Answers to activities, practice exercises and exam practice questions: Chapter 14

55

56

d Statement to reconcile balancesAdd Minus Purchase

ledger balances$ $ $

Starting balances at 30 April 2016 101 490Adjustment 2 3 060 3 060Adjustment 3 150 150Adjustment 6 4 815 4 815Amended balance on purchase ledger control account at 30 April 2016

109 515

2 Three reasons for keeping a control account are (any two):

• provides a quick total for year-end financial statements

• helps identify possible fraud

• helps to detect errors in the accounts.

3 a It is sometimes the case where the customer of a business is also a supplier to the business. They will, therefore, have an account in both the sales and purchase ledger. In order to cut down on paperwork and the need to send cheques to each other, the balance on the sales ledger will be offest against the balance in the purchase ledger. This means that only one party needs to send a cheque to the other. Whatever action is taken in the individual accounts in the sales and purchase ledgers, the same thing has to be done in the respective control accounts in the nominal ledger.

b Dinh TruongPurchase ledger control account

2016 $ 2015 $Apr 30 Bank 745 980 May 1 Balance b/d 43 120

Discounts received 31 400 2016Purchases returns 12 400 Apr 30 Purchases 824 140Sales ledger control 5 210Balance c/d 72 270

867 260 867 260May 1 Balance b/d 72 270

c Amended purchase ledger control account2016 $ 2016 $

May 1 Balance b/d 72 270Sales ledger control

850 Discounts received

1 000

Bank 1 450 Purchases 2 040Revised balance c/d 73 010

75 310 75 310May 1 Balance b/d 73 010

Cambridge International AS and A Level Accounting

56

57

d Purchase ledger control account

Purchase ledger balances

$ $Starting balances (purchase ledger control account was calculated in part a, purchase ledger balances is the balancing figure)

72 270 67 660

Adjustment 1 1 000Adjustment 2 2 040 2 040Adjustment 3 – 100Adjustment 4 (850) –Adjustment 5 (1 450) –Adjustment 6 3 210

73 010 73 010

Answers to activities, practice exercises and exam practice questions: Chapter 14

57

15 Suspense accountsActivitiesActivity 1a Lee

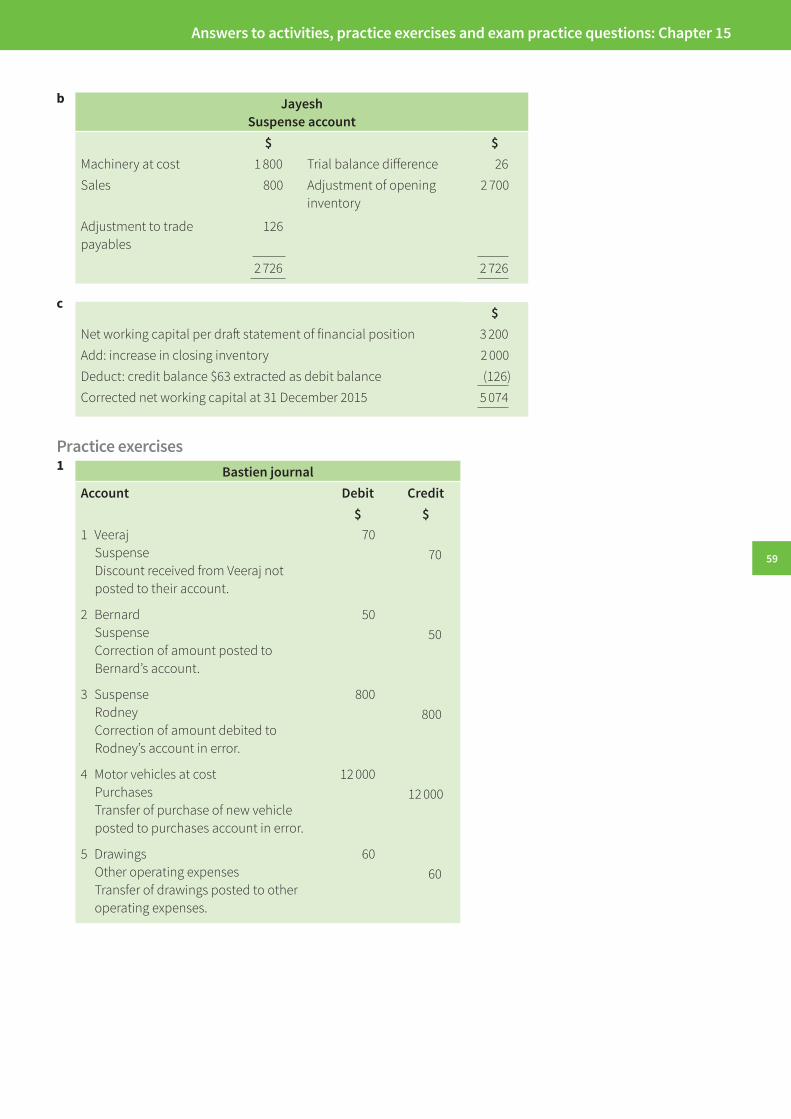

Suspense account$ $

Sales 90 Difference on trial balance 58*Doyle 18 Irrecoverable debt (expense) 50

108 108

*Balancing figure

b Debit Credit$ $

Purchases 150Bilder, purchase ledger 150Machinery at cost 400Machinery repairs 400Income statement 40Provision for depreciation of machinery 40

c Decrease IncreaseDr Cr$ $ $

Profit for the year per draft accounts 3 775(1) Increase in sales 90(2) Increase in purchases 150(4) Increase in irrecoverable debts 50(5) Decrease in machinery repairs 400(5) Increase in provision for depreciation of machinery 40

240 490(240) 250

Correct profit for the year 4 025

Activity 2

a Journal entries to correct the errorsDr Cr$ $

1 Suspense 2 700Note. No debit entry is required.

2 Note. The trial balance was not affected because the closing inventory was not shown in it.

3 Repairs to machinery 3 500Suspense 1 800Machinery at cost 5 300

4 Suspense 800Sales 800

5 Suspense 126Note. No credit entry is required.

Cambridge International AS and A Level Accounting

58

59

b JayeshSuspense account

$ $Machinery at cost 1 800 Trial balance difference 26Sales 800 Adjustment of opening

inventory2 700

Adjustment to trade payables

126

2 726 2 726

c $

Net working capital per draft statement of financial position 3 200Add: increase in closing inventory 2 000Deduct: credit balance $63 extracted as debit balance (126)Corrected net working capital at 31 December 2015 5 074

Practice exercises1 Bastien journal

Account Debit Credit$ $

1 Veeraj Suspense Discount received from Veeraj not

posted to their account.

7070

2 Bernard Suspense Correction of amount posted to

Bernard’s account.

5050

3 Suspense Rodney Correction of amount debited to

Rodney’s account in error.

800800

4 Motor vehicles at cost Purchases Transfer of purchase of new vehicle

posted to purchases account in error.

12 00012 000

5 Drawings Other operating expenses Transfer of drawings posted to other

operating expenses.

6060

Answers to activities, practice exercises and exam practice questions: Chapter 15

59

60

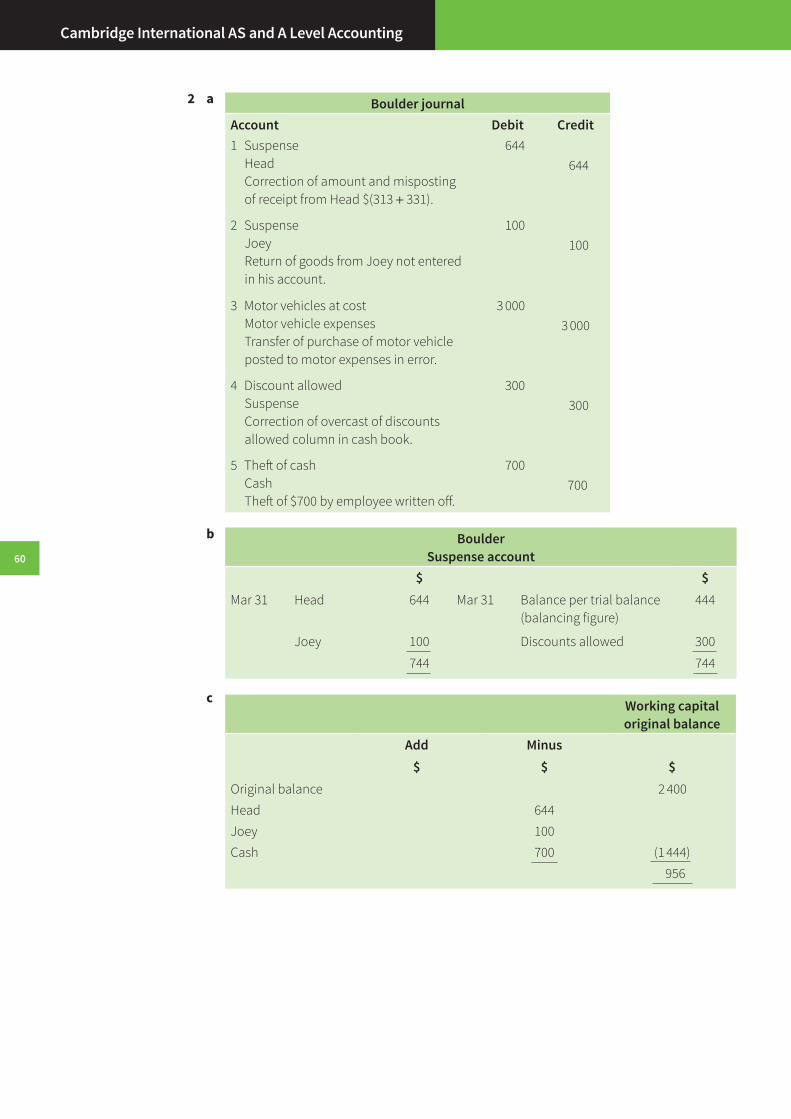

2 a Boulder journalAccount Debit Credit1 Suspense Head Correction of amount and misposting

of receipt from Head $(313 + 331).

644644

2 Suspense Joey Return of goods from Joey not entered

in his account.

100100

3 Motor vehicles at cost Motor vehicle expenses Transfer of purchase of motor vehicle

posted to motor expenses in error.

3 0003 000

4 Discount allowed Suspense Correction of overcast of discounts

allowed column in cash book.

300300

5 Theft of cash Cash Theft of $700 by employee written off.

700700

b BoulderSuspense account

$ $Mar 31 Head 644 Mar 31 Balance per trial balance

(balancing figure)444

Joey 100 Discounts allowed 300

744 744

c Working capital original balance

Add Minus$ $ $

Original balance 2 400Head 644Joey 100Cash 700 (1 444)

956

Cambridge International AS and A Level Accounting

60

61

3 a Account Debit Credit$ $

1 Bank Purchase ledger control, Victor

9090

2 Purchase ledger control Suspense General expenses

420180240

3 Sales returns Purchases

900900

4 Purchase ledger control Purchases returns

350350

5 Discounts received Purchase ledger control

600600

b AmberSuspense account$ $

Mar 31 Per trial balance 180

Mar 31 Purchase ledger control 180

4 a Account Debit Credit$ $

1 Discount received Discount allowed Suspense

5555

1102 Suspense Sales returns Purchases returns

216108108

3 Sales control account Bank

400400

4 Equipment Purchases

4 4004 400

5 Drawings Purchases

800800

6 Suspense General expenses Drawings General expenses

9090

9090

b LoganSuspense account$ $

Mar 31 Sales returns 108 Mar 31 Balance per trial balance

196

Purchases returns 108 Discounts received 55General expenses 90 Discounts allowed 55

306 306

Answers to activities, practice exercises and exam practice questions: Chapter 15

61

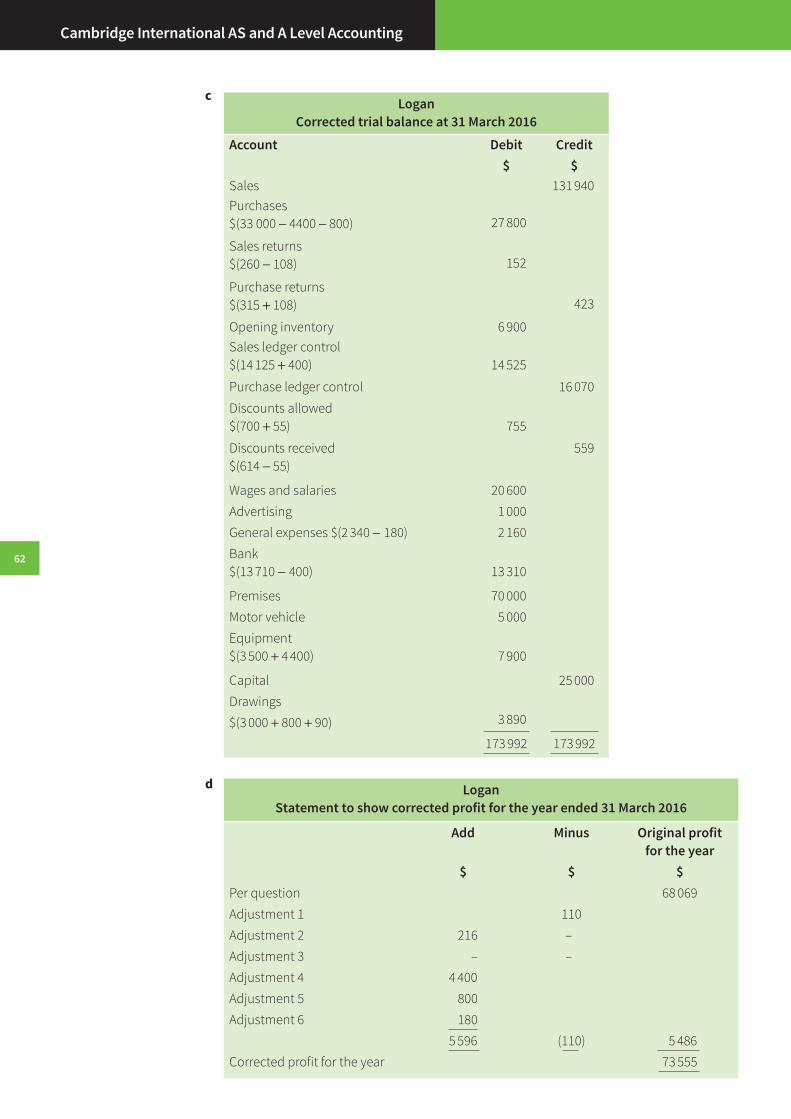

c LoganCorrected trial balance at 31 March 2016

Account Debit Credit$ $

Sales 131 940Purchases $(33 000 − 4400 − 800) 27 800

Sales returns$(260 − 108) 152

Purchase returns$(315 + 108) 423

Opening inventory 6 900Sales ledger control$(14 125 + 400) 14 525

Purchase ledger control 16 070Discounts allowed$(700 + 55) 755

Discounts received$(614 − 55)

559

Wages and salaries 20 600Advertising 1 000General expenses $(2 340 − 180) 2 160Bank$(13 710 − 400) 13 310

Premises 70 000Motor vehicle 5 000Equipment$(3 500 + 4 400) 7 900

Capital 25 000Drawings

3 890$(3 000 + 800 + 90)173 992 173 992

d LoganStatement to show corrected profit for the year ended 31 March 2016

Add Minus Original profit for the year

$ $ $Per question 68 069Adjustment 1 110Adjustment 2 216 –Adjustment 3 – –Adjustment 4 4 400Adjustment 5 800Adjustment 6 180

5 596 (110) 5 486Corrected profit for the year 73 555

Cambridge International AS and A Level Accounting

62

63

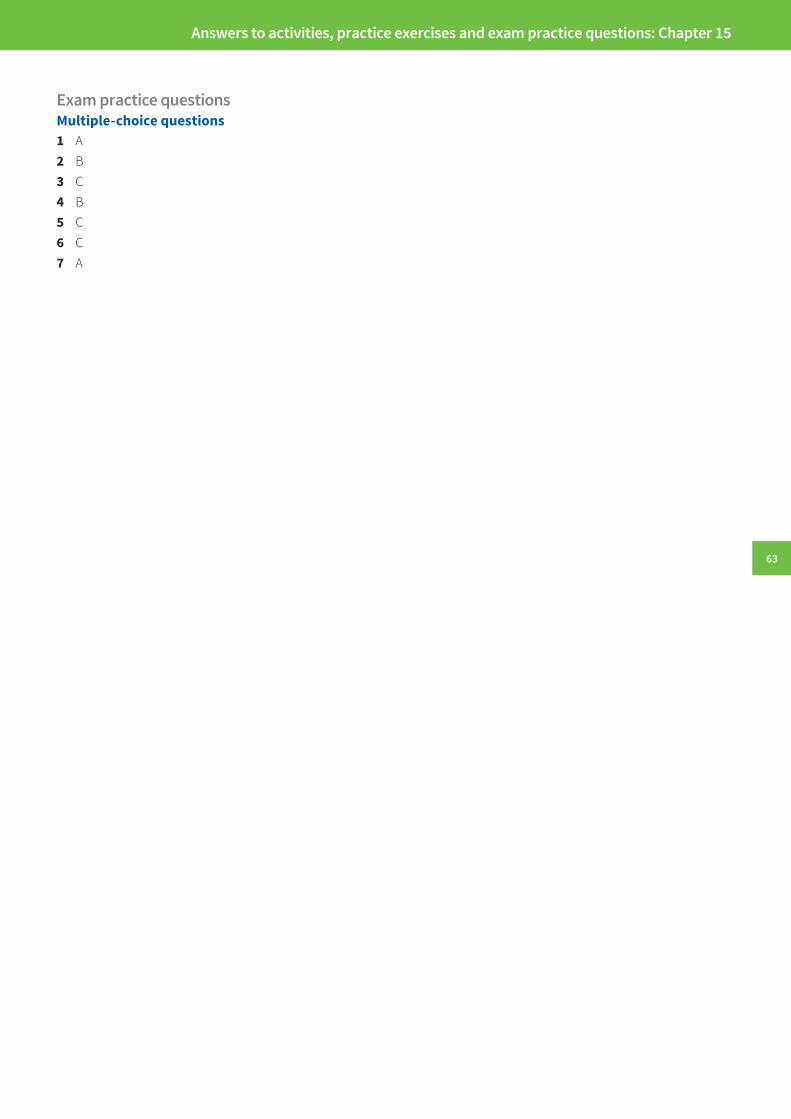

Exam practice questionsMultiple-choice questions1 A2 B3 C4 B5 C6 C7 A

Answers to activities, practice exercises and exam practice questions: Chapter 15

63

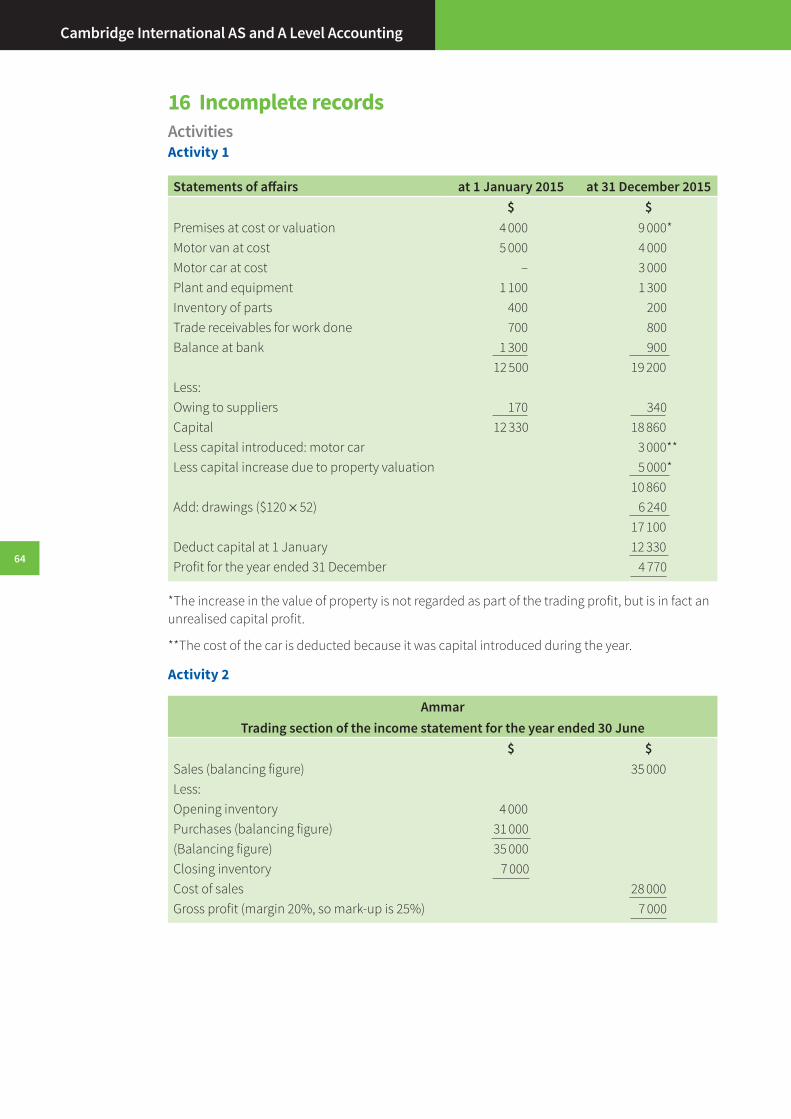

16 Incomplete recordsActivitiesActivity 1

Statements of affairs at 1 January 2015 at 31 December 2015$ $

Premises at cost or valuation 4 000 9 000*Motor van at cost 5 000 4 000Motor car at cost – 3 000Plant and equipment 1 100 1 300Inventory of parts 400 200Trade receivables for work done 700 800Balance at bank 1 300 900

12 500 19 200Less:Owing to suppliers 170 340Capital 12 330 18 860Less capital introduced: motor car 3 000**Less capital increase due to property valuation 5 000*

10 860Add: drawings ($120 × 52) 6 240

17 100Deduct capital at 1 January 12 330Profit for the year ended 31 December 4 770

*The increase in the value of property is not regarded as part of the trading profit, but is in fact an unrealised capital profit.

**The cost of the car is deducted because it was capital introduced during the year.

Activity 2

AmmarTrading section of the income statement for the year ended 30 June

$ $Sales (balancing figure) 35 000 Less:Opening inventory 4 000Purchases (balancing figure) 31 000(Balancing figure) 35 000Closing inventory 7 000Cost of sales 28 000Gross profit (margin 20%, so mark-up is 25%) 7 000

Cambridge International AS and A Level Accounting

64

65

Activity 3

NehaPro forma trading section of the income statement for the period

30 June 2015 to 5 November 2015

$ $Sales $(122 000 − 16 000 + 37 000 + 17 000) 160 000Less: cost of salesInventory at 30 June 2015 47 000Purchases $(138 000 − 23 000 + 28 000) 143 000

190 000Less: inventory at 5 November 2015(Balancing figure) 70 000 120 000Gross profit (25% of $160 000) 40 000

Cost of inventory lost in fire: $(70 000 − 12 000) = $58 000.

Practice exercices1 a (i and ii) and b

SengStatement of affairs at: 1 January 2015 31 December 2015

$ $Assets Shop premises 20 000Motor van 8 000Shop fittings 3 000Inventory 4 000Trade receivables 1 000Bank 60 000 5 000 60 000 41 000Liabilities Trade payables (6 000)Loan from brother (20 000) (16 000) 40 000 19 000 Opening capital 40 000 40 000Loss for the year (balancing figure) (15 800)Less: drawings (5 200) 40 000 19 000

Answers to activities, practice exercises and exam practice questions: Chapter 16

65

66

2 Miriam

Statement of affairs at: 1 July 2015 30 June 2016 Assets $ $Land and buildings at cost 60 000 60 000Fixtures and fittings 10 000 12 000Office machinery 8 000 7 000Inventory 17 000 21 000Trade receivables 4 000 5 000Rent prepaid 1 000 600Bank 14 000 16 000 114 000 121 600Liabilities (3 000) (1 600)

Trade payables Wages owing (2 000) (1 000) 109 000 119 000Opening capital 109 000Capital introduced 1 400Profit for the year 21 000Less: drawings (12 400)Closing capital 109 000 119 000

Note: The revaluation of the land and buildings is ignored as this is a capital profit.

3 Workings:

Trade payables control account$ $

Payments from bank 54 000 Opening balance 3 600Closing balance 5 200 Credit purchases 55 600

59 200 59 200

Calculation of closing inventory

$Per question 11 000Less: damaged inventory at cost (5 000)

6 000Add: damaged inventory at NRV 2 500Value for trading account 8 500

Calculation of revenue

$Opening inventory 16 000Add: purchases $(55 600 − 1 300) 54 300

70 300Less: closing inventory1, 2 (11 000)Cost of sales 59 300

Mark up = $59 300 ÷ 60% = $98 833

Cambridge International AS and A Level Accounting

66

67

Check:

Sales 98 833Less: cost of sales (59 300)Gross profit 39 533

Gross profit margin = $39 533 ÷ $98 833 × 100 = 40%

Kim

Trading section of income statement for the year ended 30 June 2016

$ $Sales 98 833Opening inventory 16 000Add: purchases $(55 600 − 1300) 54 300

70 300Less: closing inventory3 (8 500)Cost of sales (61 800)Gross profit (36 600)

Notes:

1 The value given for closing inventory in the question ($11 000) is assumed to be the value of goods at their full price.

2 The mark-up has been calculated using the full value of closing inventory.

3 $(11 000 − (5 000 × 50%)) It is further assumed that all damaged goods were still inventory (i.e. that none of them had been sold before the year end).

4 a CorneliusStatement of affairs at: 1 April 2014 31 March 2015

$ $Assets Equipment 15 000 28 000Premises 80 000Inventory 37 500 52 000Trade receivables 22 400Other operating expenses 700Bank 30 000 116 000 82 500 299 100Liabilities Bank loan (40 000)

Trade payables (56 000)Other operating expenses (2 280)Loan from father (20 000) (20 000) 62 500 180 820 Opening capital 62 500 62 500Capital introduced 40 000Profit for the year (balancing figure) 99 120Less: drawings (20 800)

62 500 180 820

Answers to activities, practice exercises and exam practice questions: Chapter 16

67

b CorneliusIncome statement for the year ended 31 March 2016

$ $Sales 468 650Less: Cost of salesOpening inventory 52 000Purchases 382 750

434 750Less: closing inventory 74 250 360 500Gross profit 108 150Less: expensesOther operating expenses $(27 000 − 2 280 + 700 + 875 − 4 050) 22 245

Bank loan interest 6 000Loan interest – father 1 600Depreciation – equipment $(28 000 + 24 000 − 45 900) 6 100 35 945Profit for the year 72 205

Workings:

i Trade payables control account$ $

Payments from bank 371 340 Opening balance 56 000Closing balance 67 410 Credit purchases 382 750

438 750 438 750

ii Calculation of cost of sales

$Opening inventory 52 000Add: purchases 382 750

434 750Less: closing inventory (74 250)Cost of sales 360 500

iii Calculation of sales

Cost of sales + 30% = $468 650

iv Trade receivables control account$ $

Opening balance 22 400 Receipts banked 456 850Credit sales for the year 468 650 Closing balance 34 200

491 050 491 050

Cambridge International AS and A Level Accounting

68

69

v Bank account$ $

Opening balance 116 000 Suppliers 371 340From customers 456 850 Drawings 26 000

Equipment 24 000Other operating expenses 27 000Bank loan interest 6 000Interest on loan from father 1 600Drawings for holiday 5 000Additional drawings (bal fig) 800Closing balance 111 110

572 850 572 850

c CorneliusStatement of financial position at 31 March 2016

Cost Accumulated depreciation

Net book value

AssetsNon-current assetsPremises 80 000 – 80 000Equipment 45 900

80 000 125 900Current assetsInventory 74 250Trade receivables 34 200Other receivables 4 050Cash and cash equivalents 111 110

223 610Total assets 349 510Capital and liabilitiesOpening capital 180 820Add: net profit 72 205 253 025Less: drawings $(26 000 + 5 000 + 800) (31 800) 221 225Non-current liabilities Bank loan 40 000Loan from father 20 000 60 000Current liabilities Trade payables 67 410Other payables 875 68 285Total capital and liabilities 349 510

Answers to activities, practice exercises and exam practice questions: Chapter 16

69

70

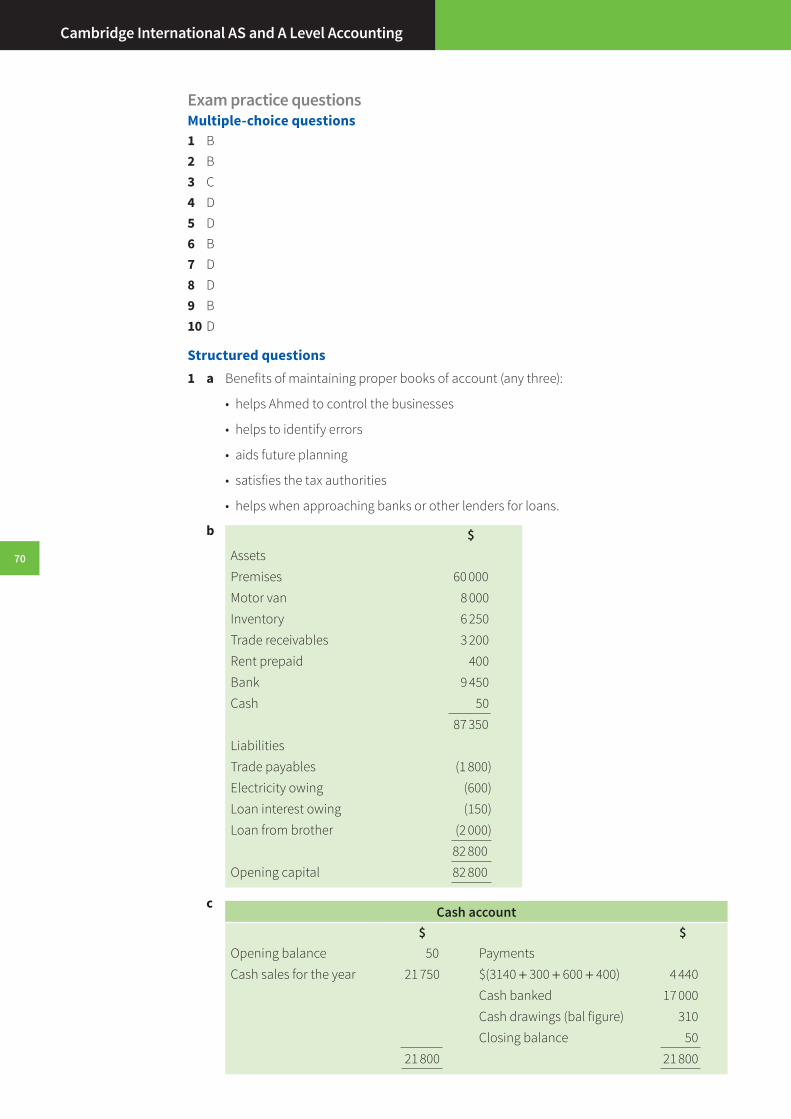

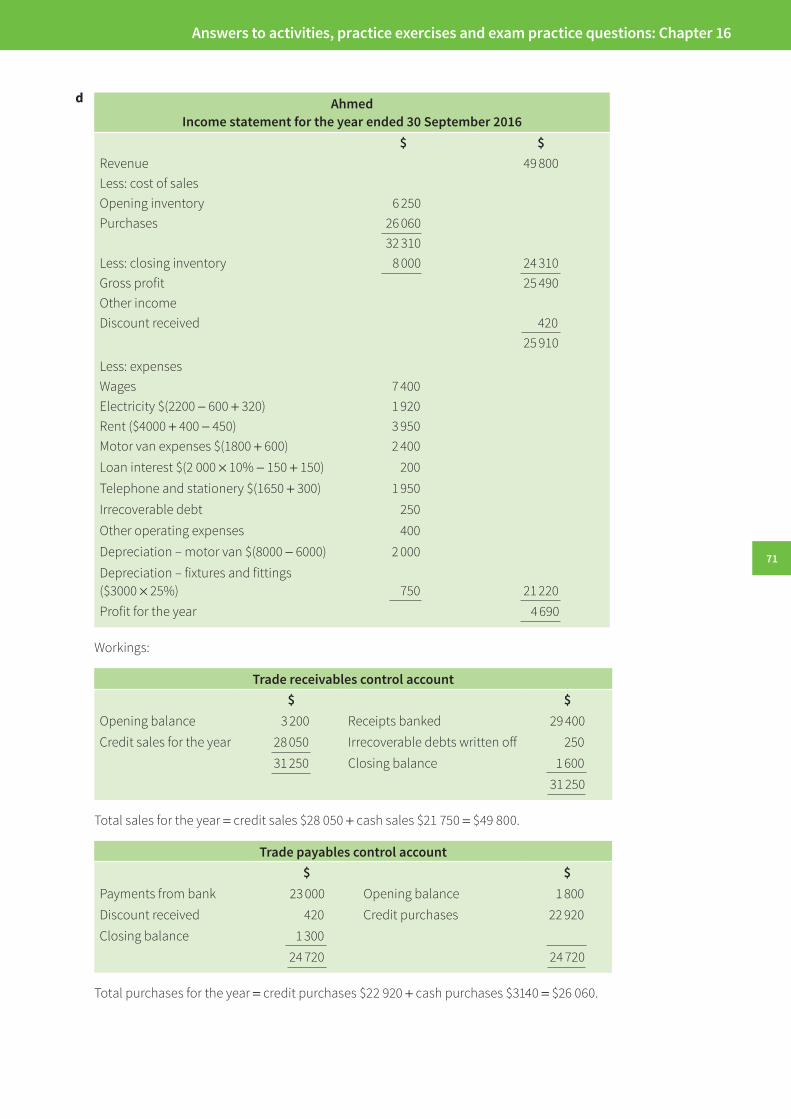

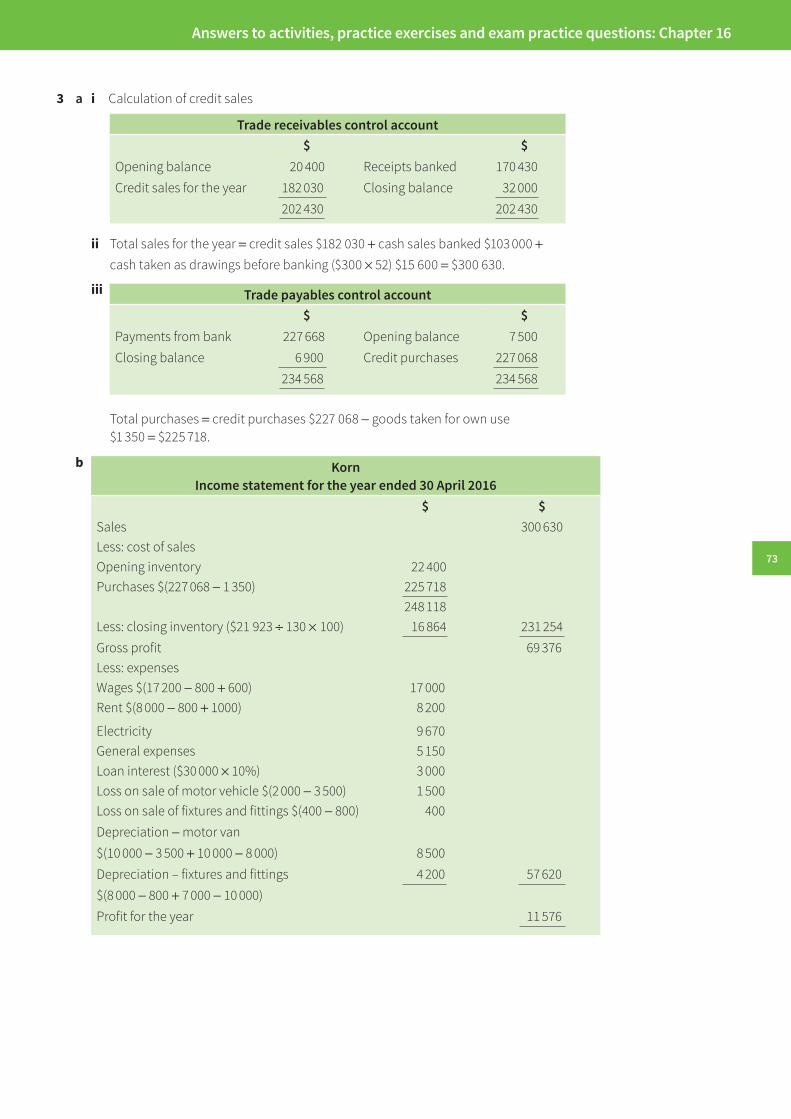

Exam practice questionsMultiple-choice questions1 B2 B3 C4 D5 D6 B7 D8 D9 B10 D

Structured questions1 a Benefits of maintaining proper books of account (any three):

• helps Ahmed to control the businesses

• helps to identify errors

• aids future planning

• satisfies the tax authorities

• helps when approaching banks or other lenders for loans.

b $Assets Premises 60 000Motor van 8 000Inventory 6 250Trade receivables 3 200Rent prepaid 400Bank 9 450Cash 50 87 350Liabilities Trade payables (1 800)Electricity owing (600)Loan interest owing (150)Loan from brother (2 000) 82 800Opening capital 82 800

c Cash account$ $

Opening balance 50 PaymentsCash sales for the year 21 750 $(3140 + 300 + 600 + 400) 4 440