ANNUAL REPORT SERBIA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANNUAL REPORT

SERBIA

2

3

ANNUAL REPORT 2008

Contents

THE YEAR IN REVIEW 5

RETAIL BANKING SERVICE NETWORKS 17

CORPORATE BANKING 23

INVESTMENT BANKING & CAPITAL MARKETS 27

INTERNATIONAL PRESENCE 31

Financial Highlights 6Letter to Shareholders 10Members of the Executive Board and Board of Directors 12Financial Review 14

Retail Banking Network 18Consumer Lending 18Mortgage Lending 19Small Business Banking 20

Corporate Banking 24EFG Leasing 24

Treasury 28Custody Services 28

Eurobank EFG presence in New Europe 32Bulgaria 32Romania 32Turkey 33Poland 33Ukraine 34Cyprus 34

OTHER SUBSIDIARIES 37

OTHER ACTIVITIES OF THE BANK 41

RISK MANAGEMENT 47

CORPORATE GOVERNANACE 51

APPENDICES 55

EUROBANK EFG GROUP AND EFG GROUP 61

EFG Property Services 38EFG Securities 38EFG Business Services 38

Payment Services 42e-Banking 44

Financial Statements 58

The Year in Review

6

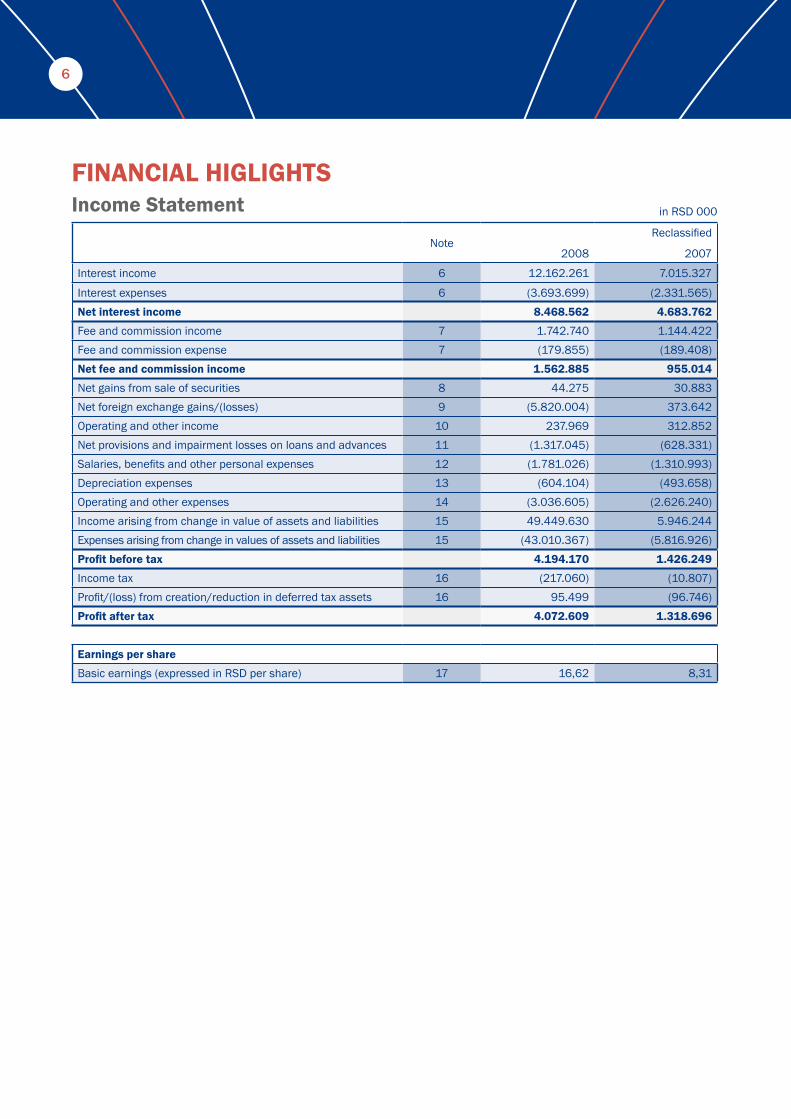

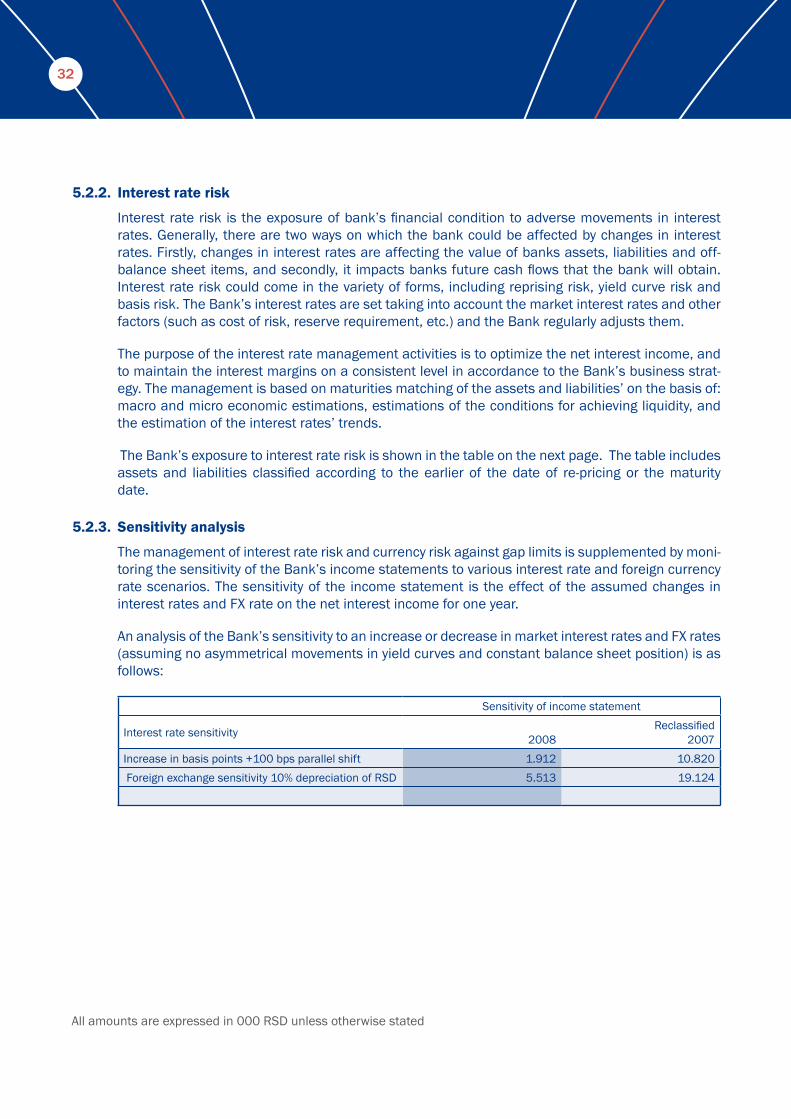

FINANCIAL REVIEWFINANCIAL HIGLIGHTS

Note2008

Reclassified

2007

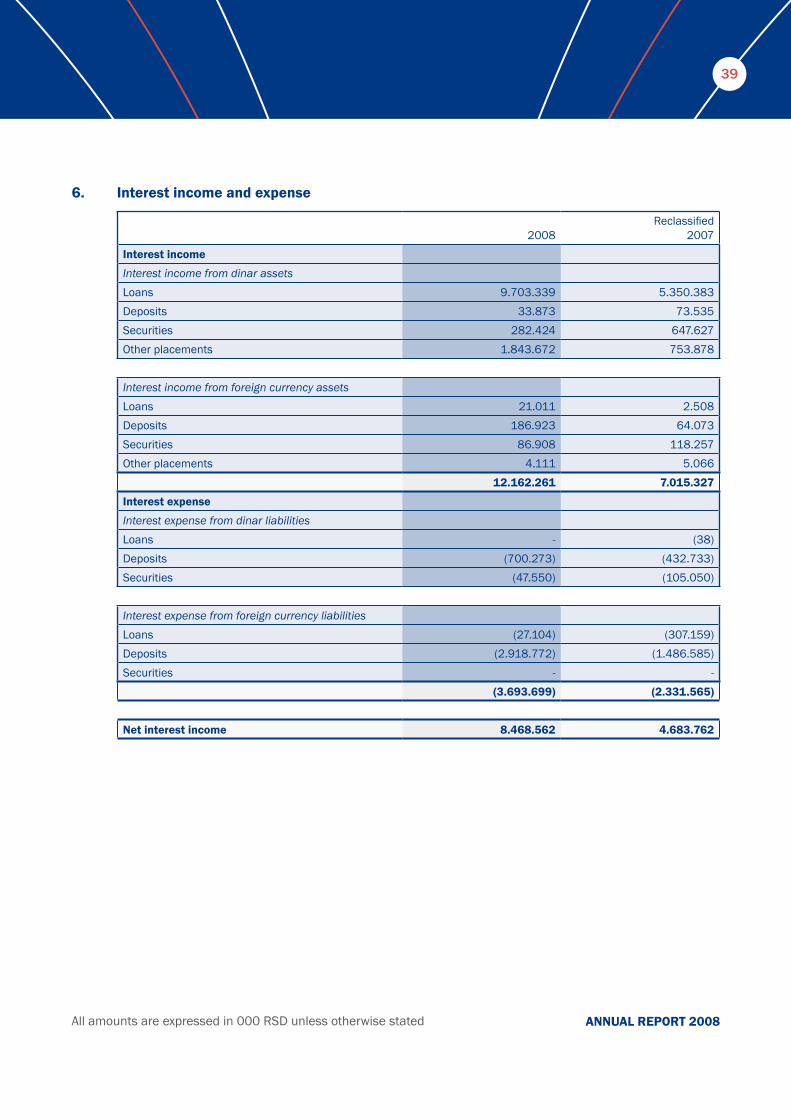

Interest income 6 12.162.261 7.015.327

Interest expenses 6 (3.693.699) (2.331.565)Net interest income 8.468.562 4.683.762

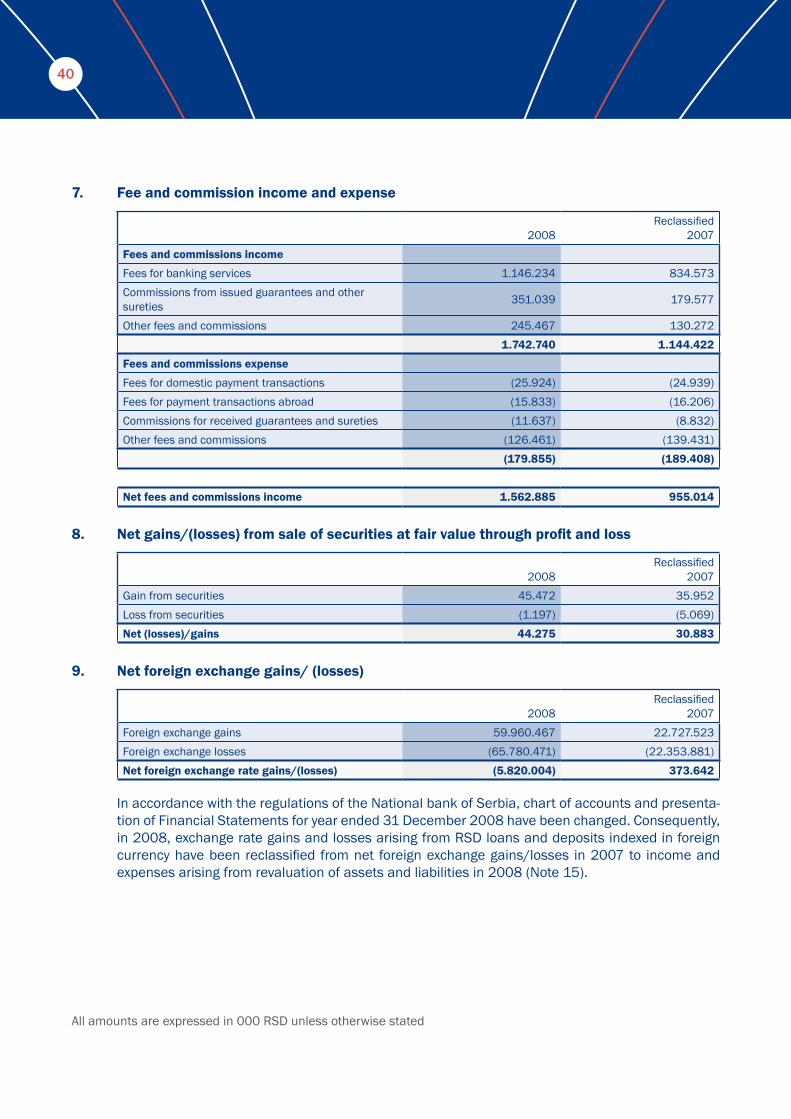

Fee and commission income 7 1.742.740 1.144.422Fee and commission expense 7 (179.855) (189.408)Net fee and commission income 1.562.885 955.014

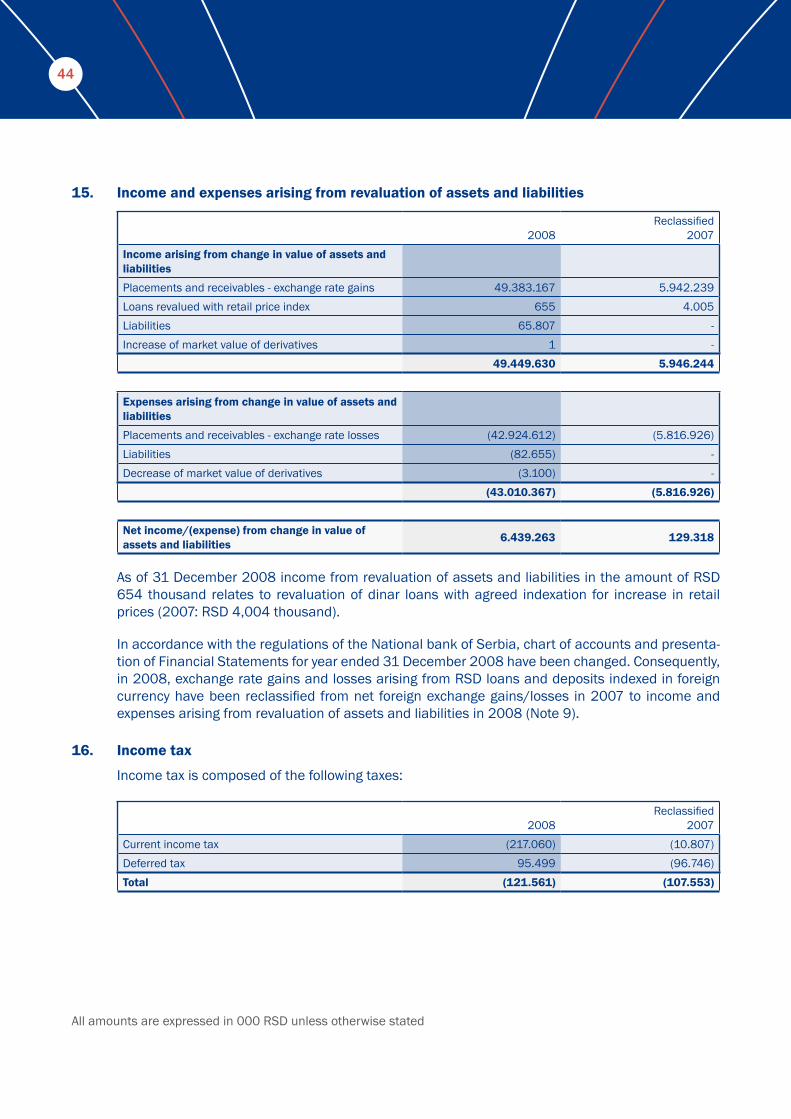

Net gains from sale of securities 8 44.275 30.883Net foreign exchange gains/(losses) 9 (5.820.004) 373.642Operating and other income 10 237.969 312.852Net provisions and impairment losses on loans and advances 11 (1.317.045) (628.331)Salaries, benefits and other personal expenses 12 (1.781.026) (1.310.993)Depreciation expenses 13 (604.104) (493.658)Operating and other expenses 14 (3.036.605) (2.626.240)Income arising from change in value of assets and liabilities 15 49.449.630 5.946.244Expenses arising from change in values of assets and liabilities 15 (43.010.367) (5.816.926)Profit before tax 4.194.170 1.426.249

Income tax 16 (217.060) (10.807)Profit/(loss) from creation/reduction in deferred tax assets 16 95.499 (96.746)Profit after tax 4.072.609 1.318.696

Earnings per share

Basic earnings (expressed in RSD per share) 17 16,62 8,31

Income Statement in RSD 000

7

ANNUAL REPORT 2008

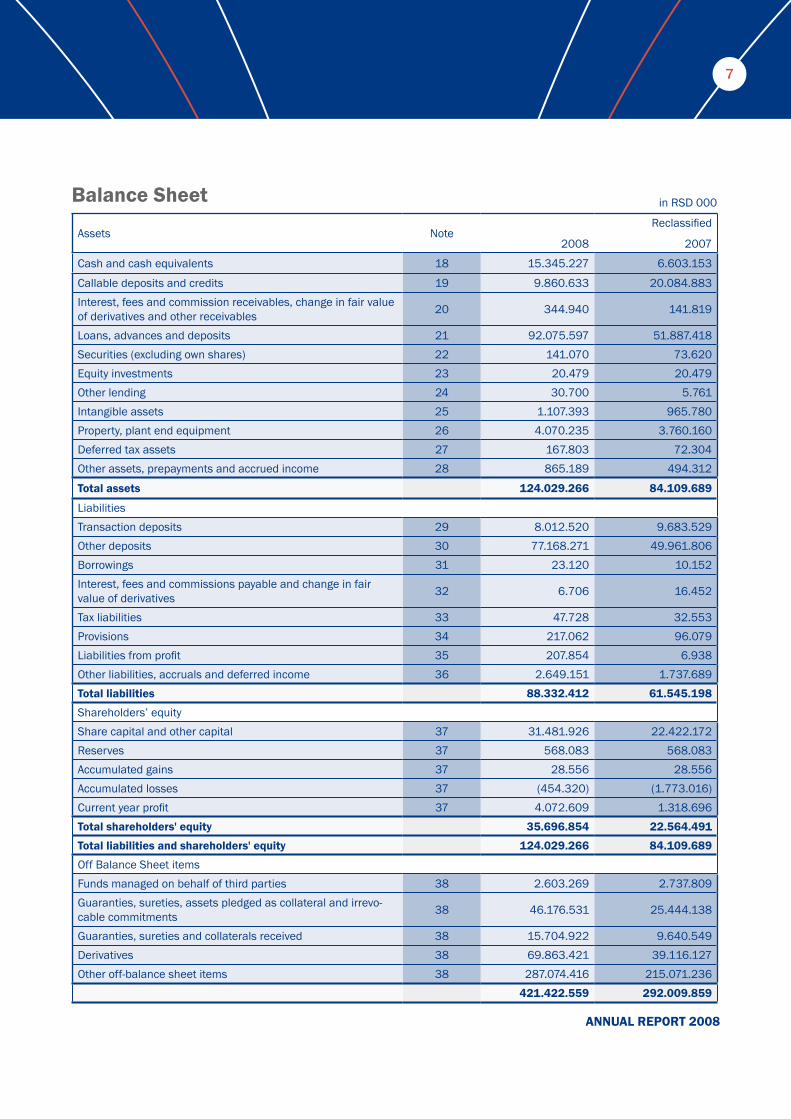

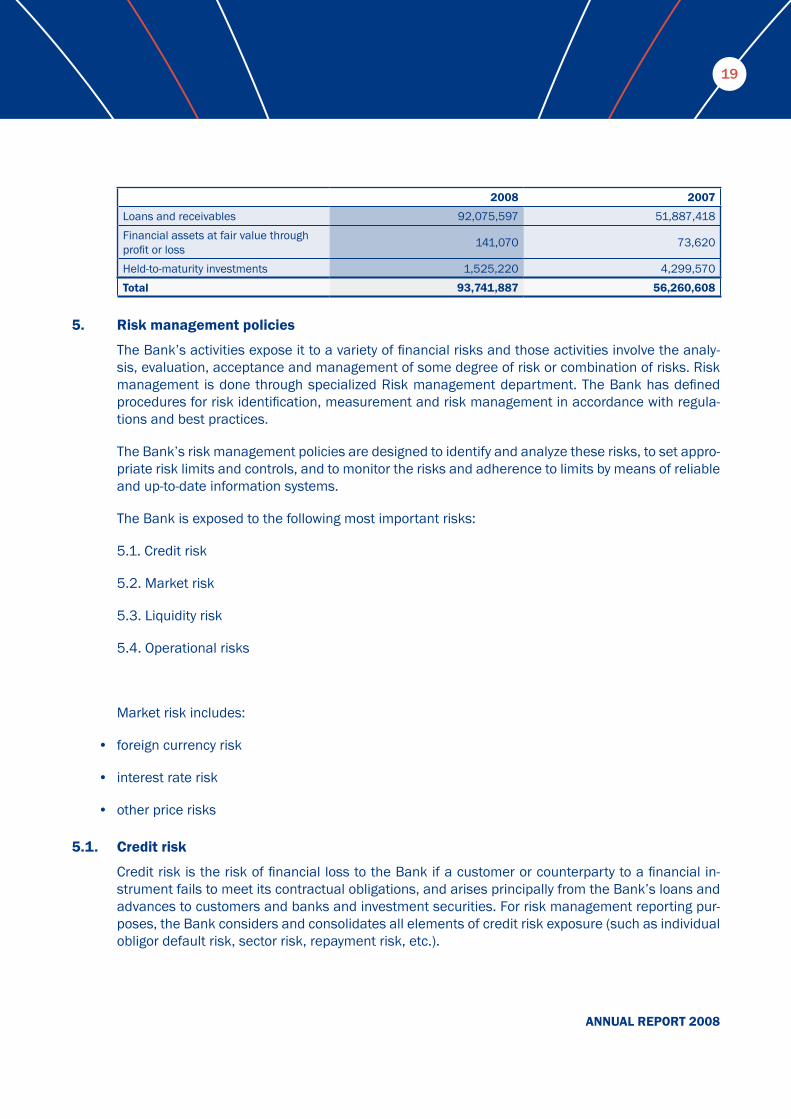

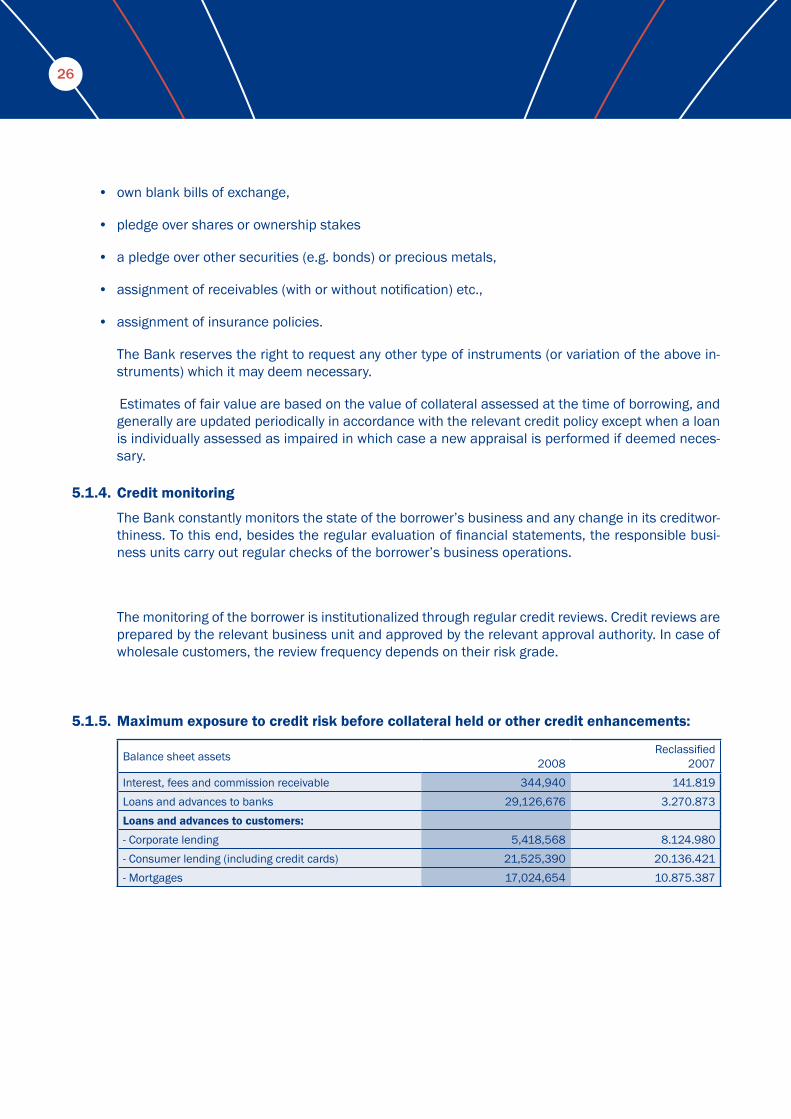

Assets Note2008

Reclassified

2007

Cash and cash equivalents 18 15.345.227 6.603.153

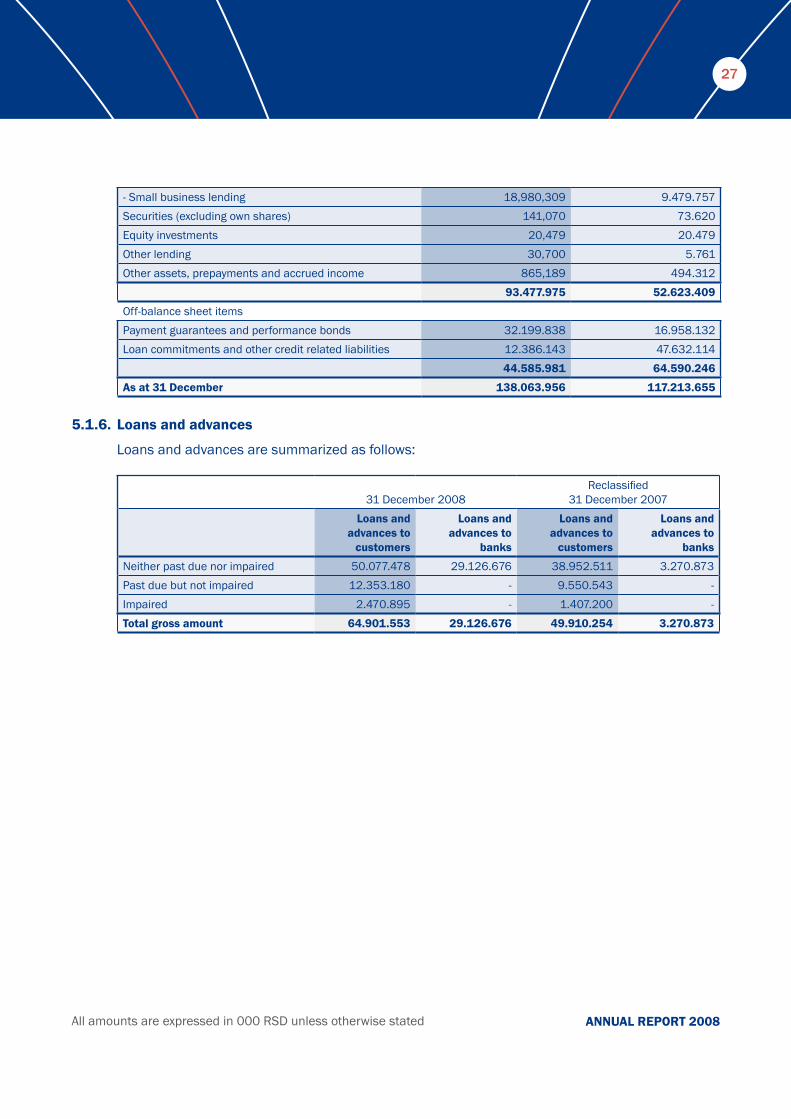

Callable deposits and credits 19 9.860.633 20.084.883Interest, fees and commission receivables, change in fair value of derivatives and other receivables 20 344.940 141.819

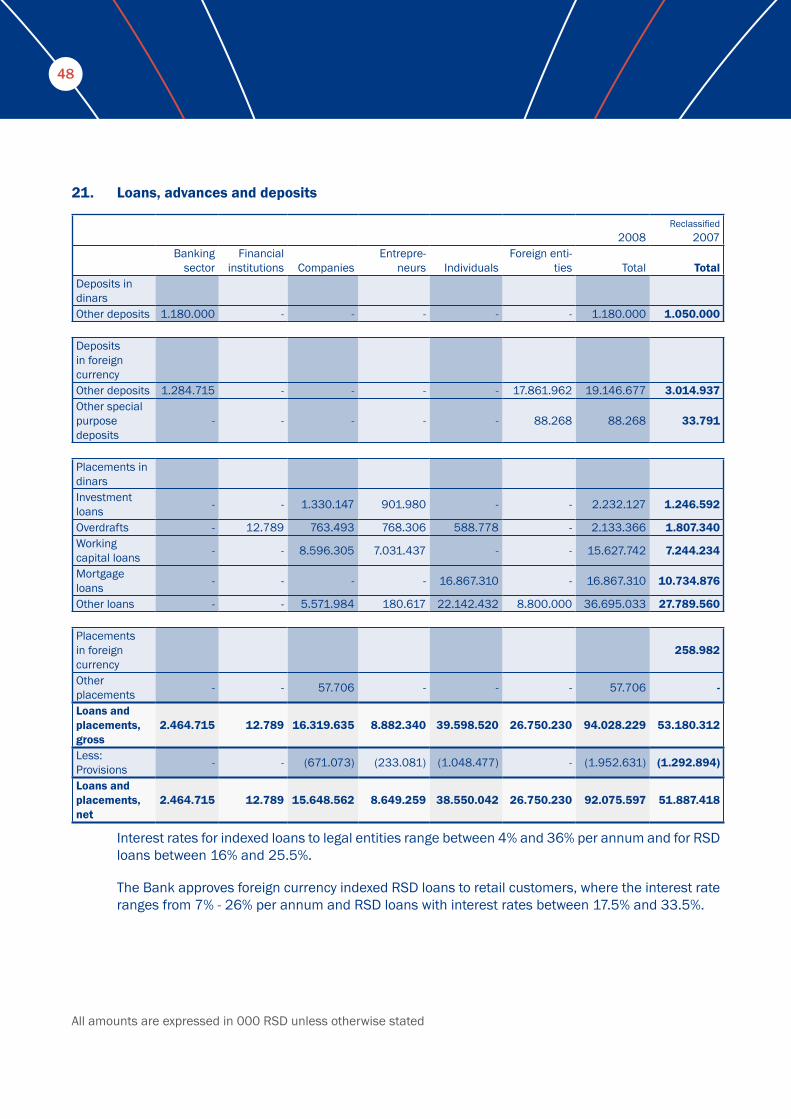

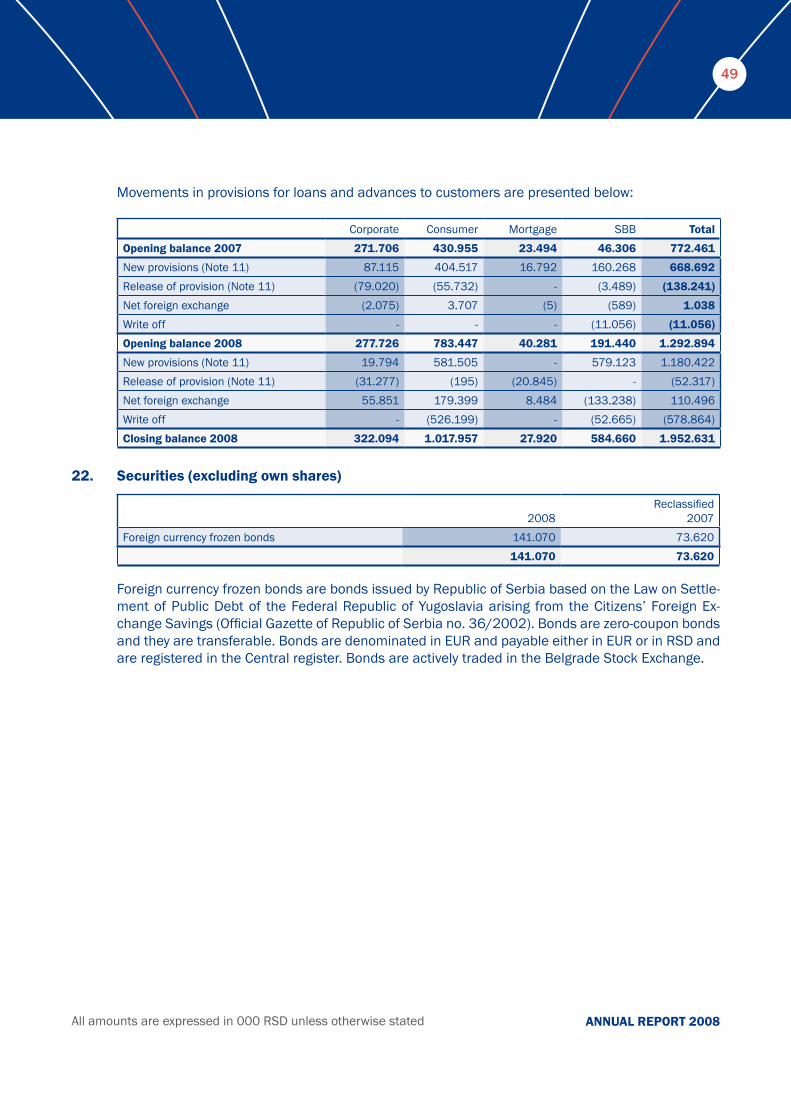

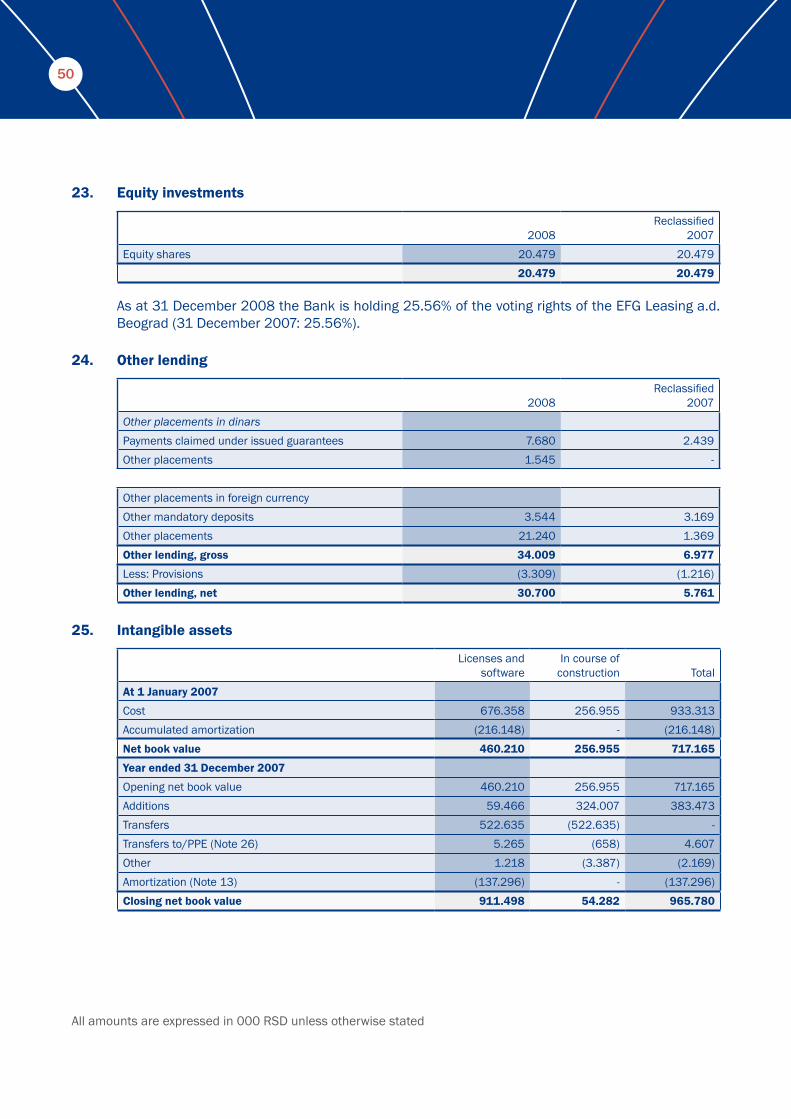

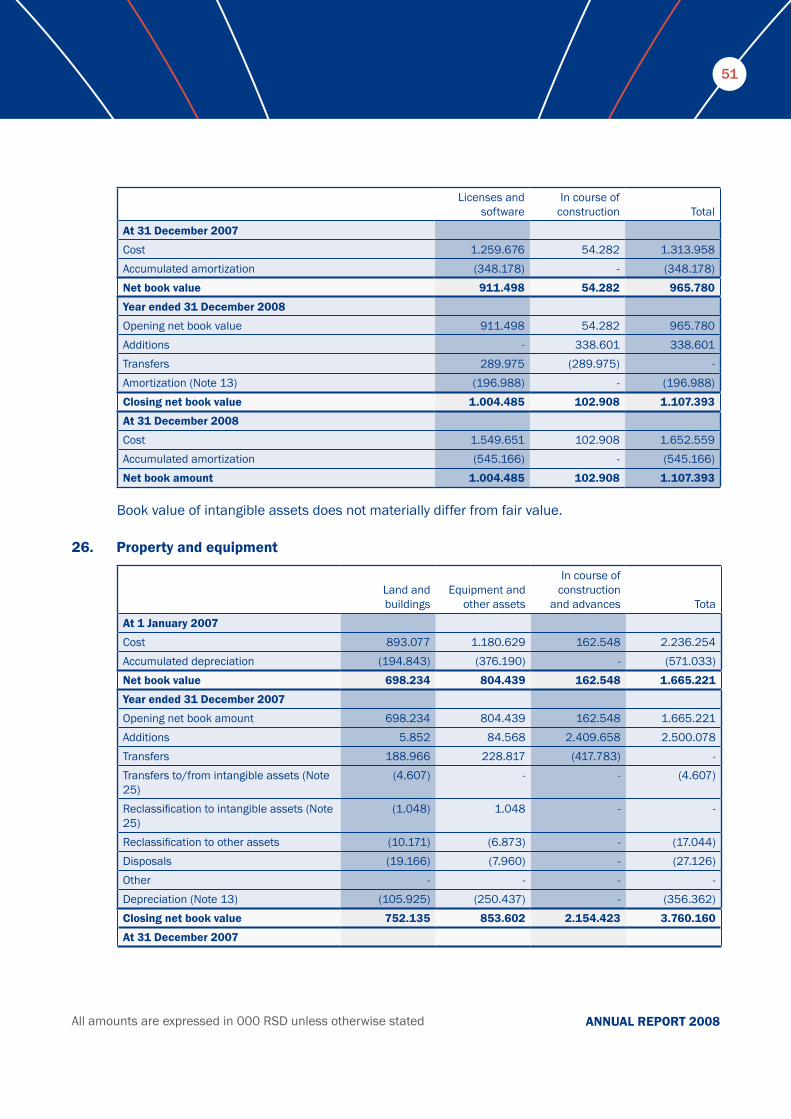

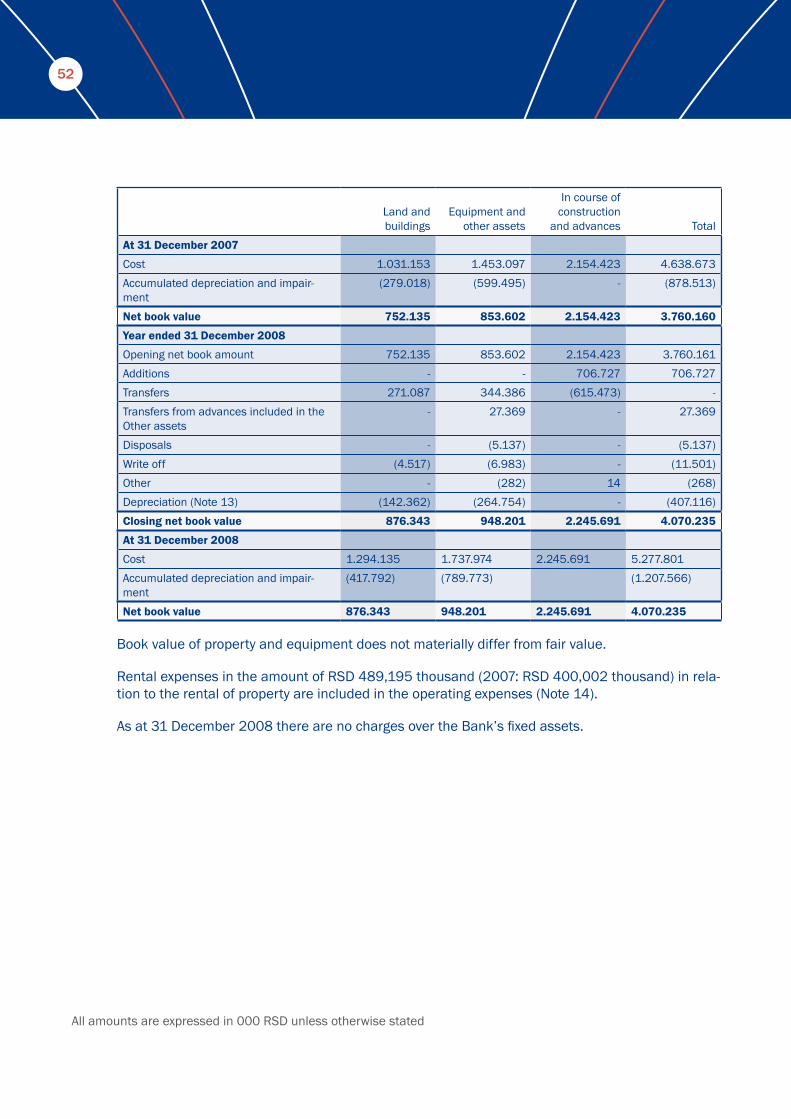

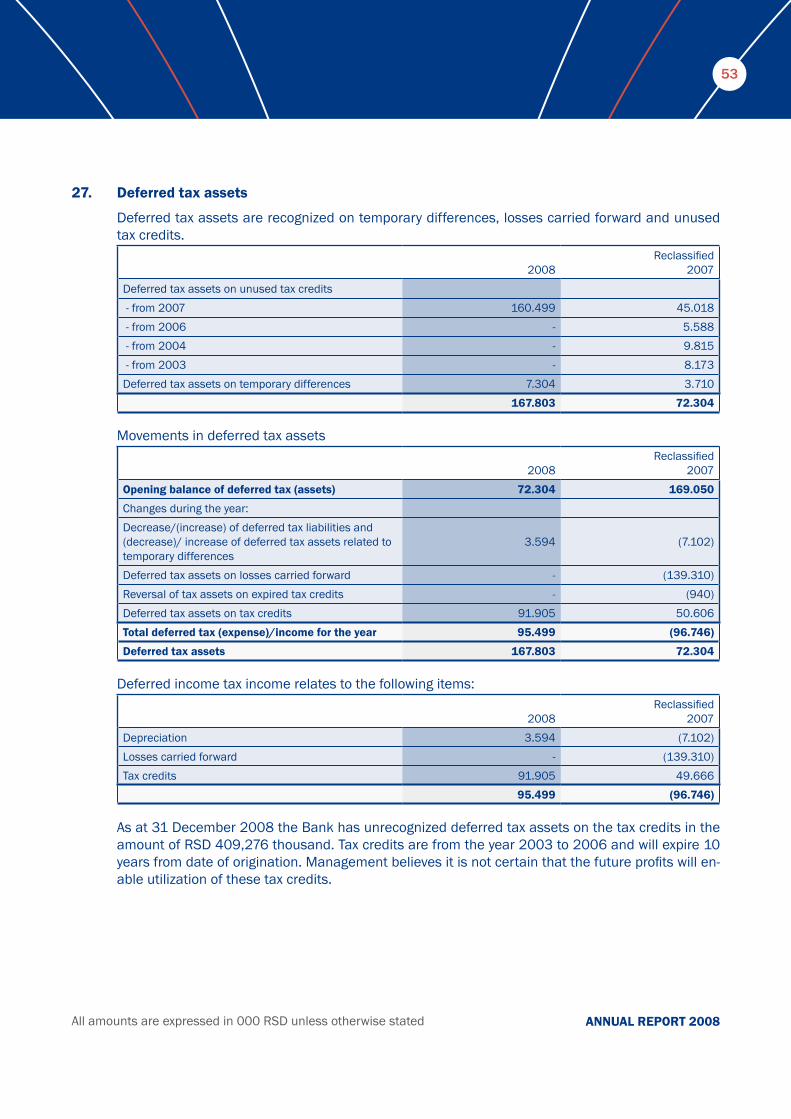

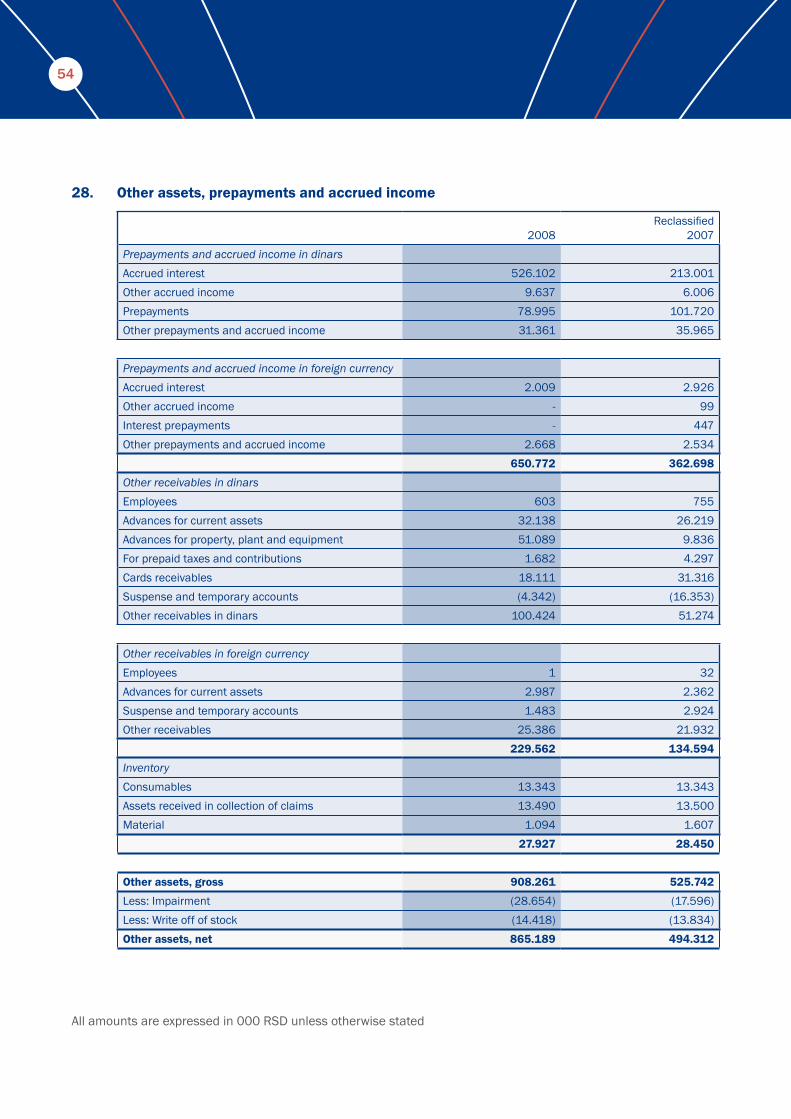

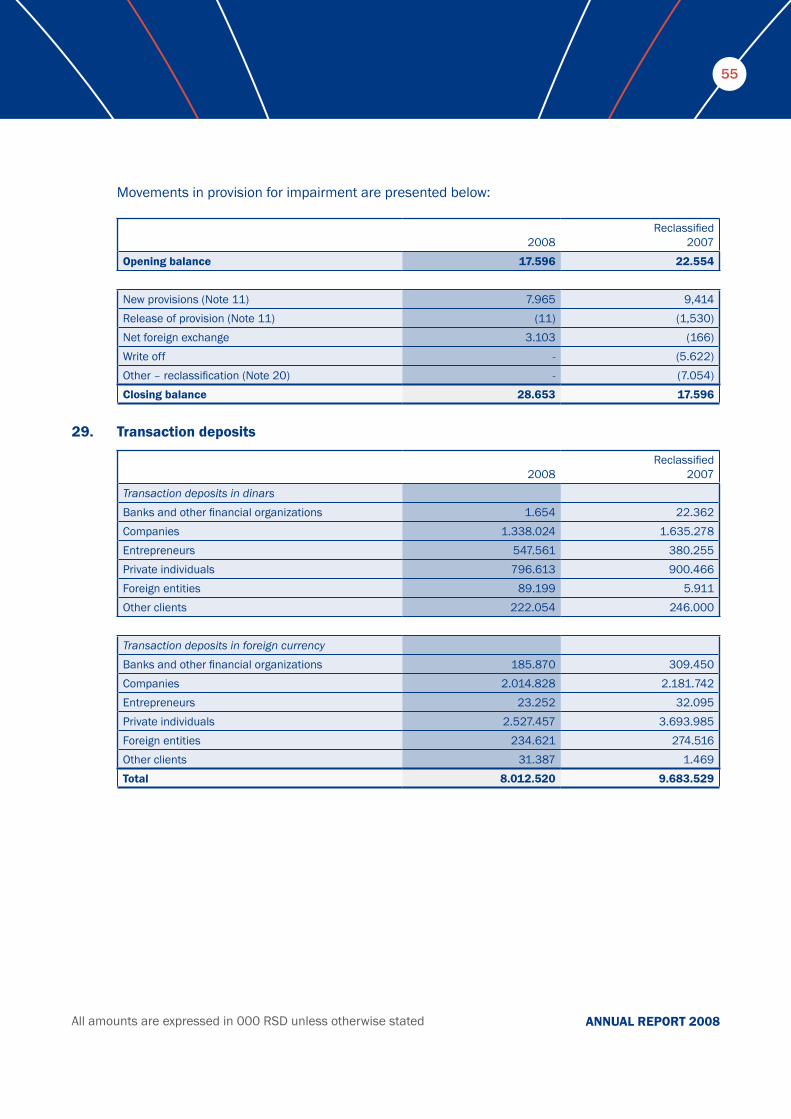

Loans, advances and deposits 21 92.075.597 51.887.418Securities (excluding own shares) 22 141.070 73.620Equity investments 23 20.479 20.479Other lending 24 30.700 5.761Intangible assets 25 1.107.393 965.780Property, plant end equipment 26 4.070.235 3.760.160Deferred tax assets 27 167.803 72.304Other assets, prepayments and accrued income 28 865.189 494.312

Total assets 124.029.266 84.109.689

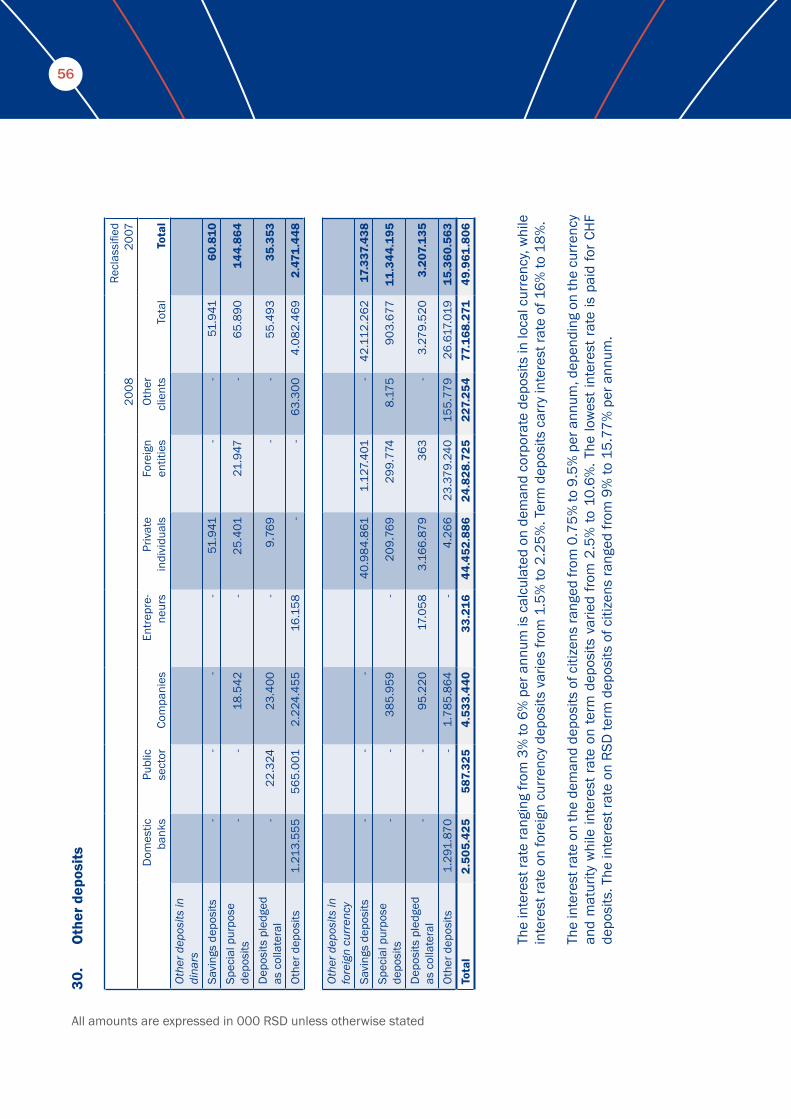

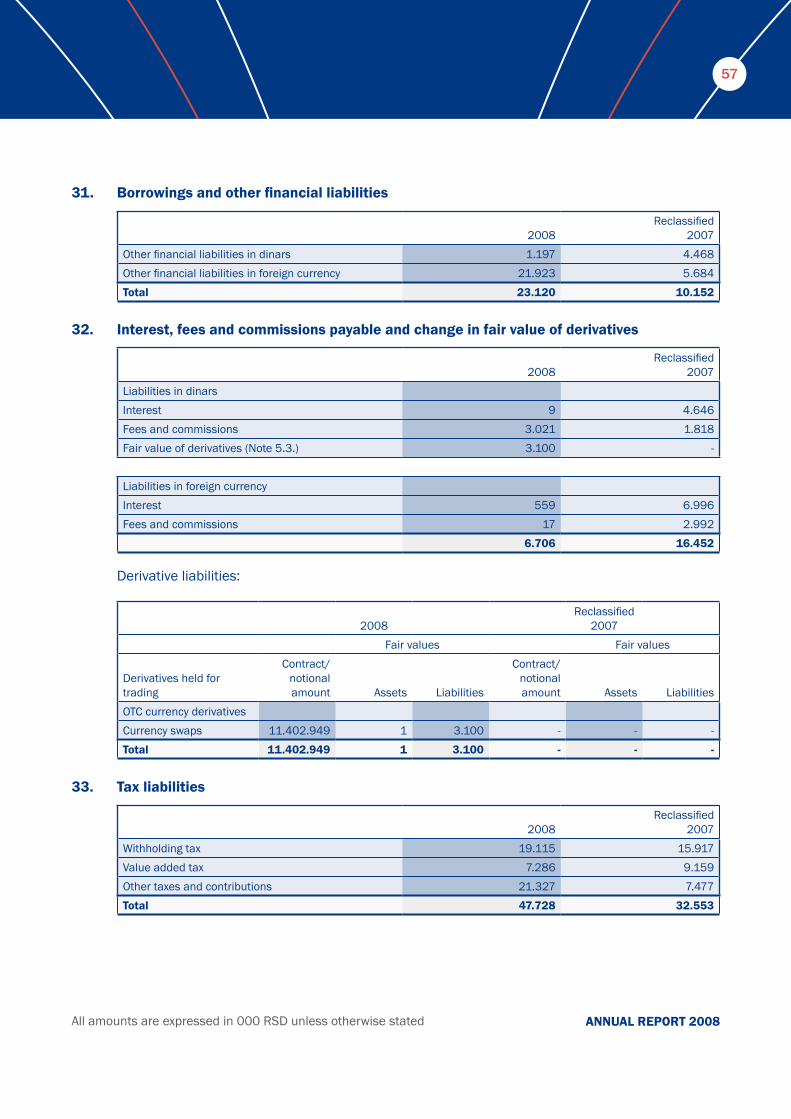

LiabilitiesTransaction deposits 29 8.012.520 9.683.529Other deposits 30 77.168.271 49.961.806Borrowings 31 23.120 10.152Interest, fees and commissions payable and change in fair value of derivatives 32 6.706 16.452

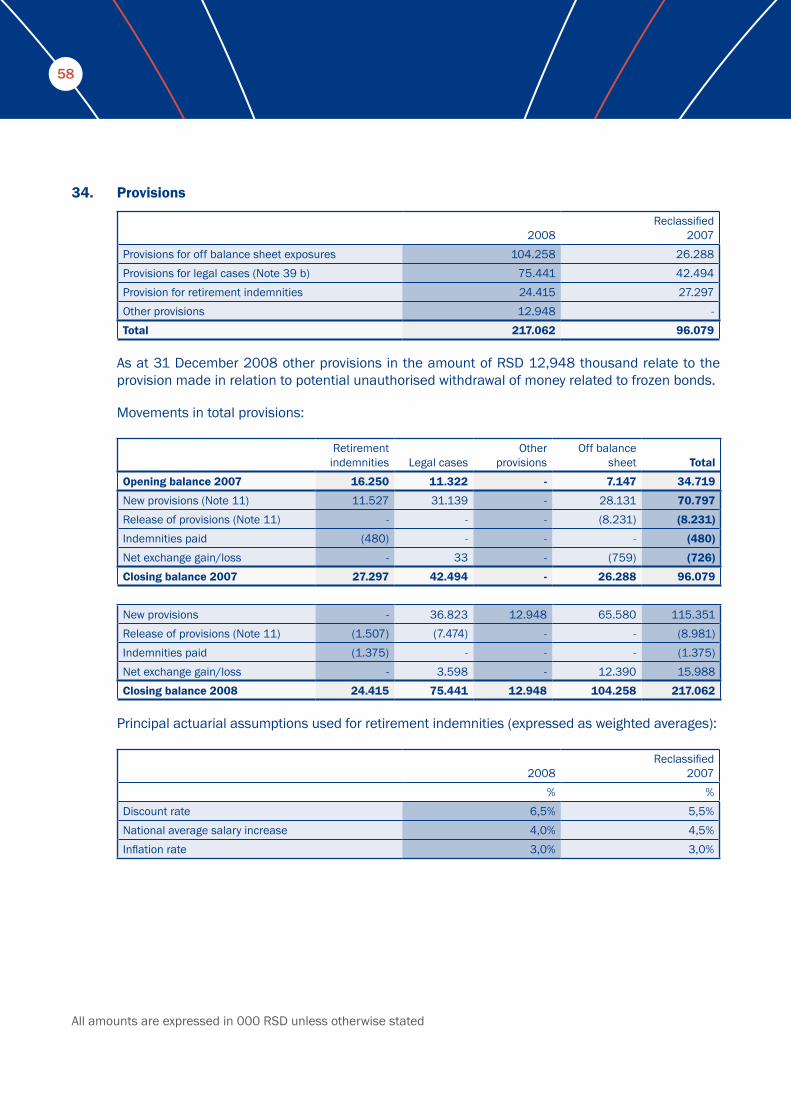

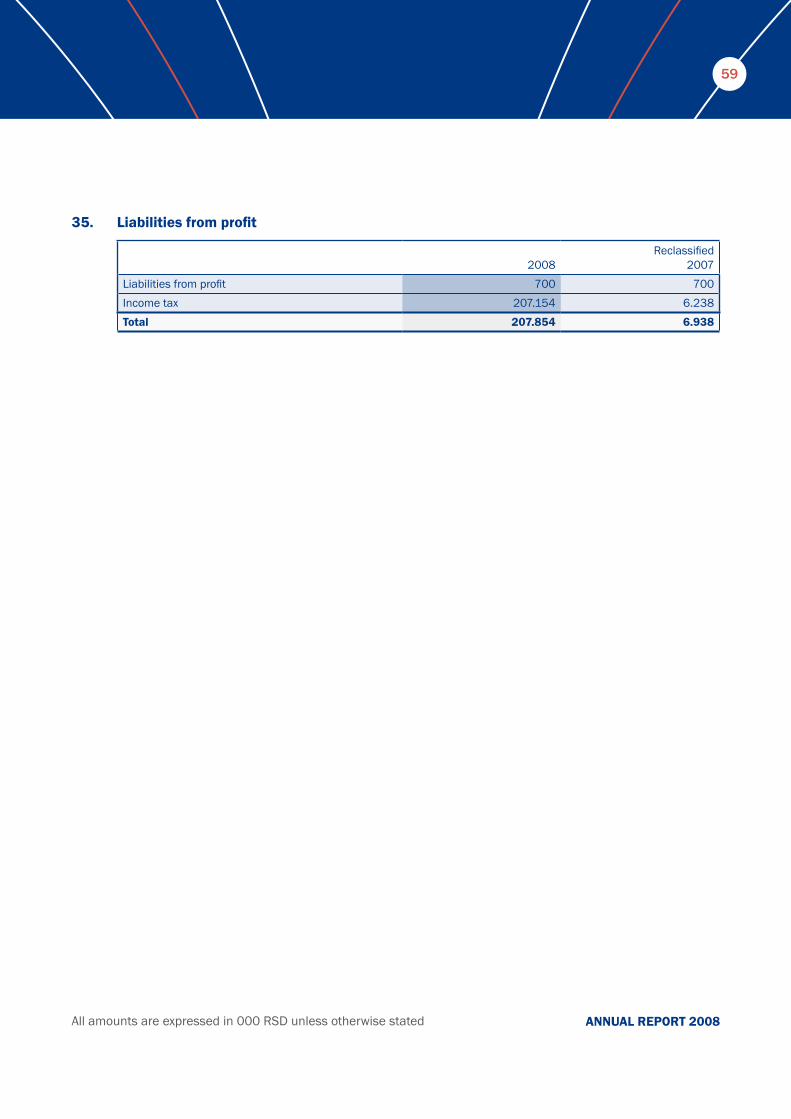

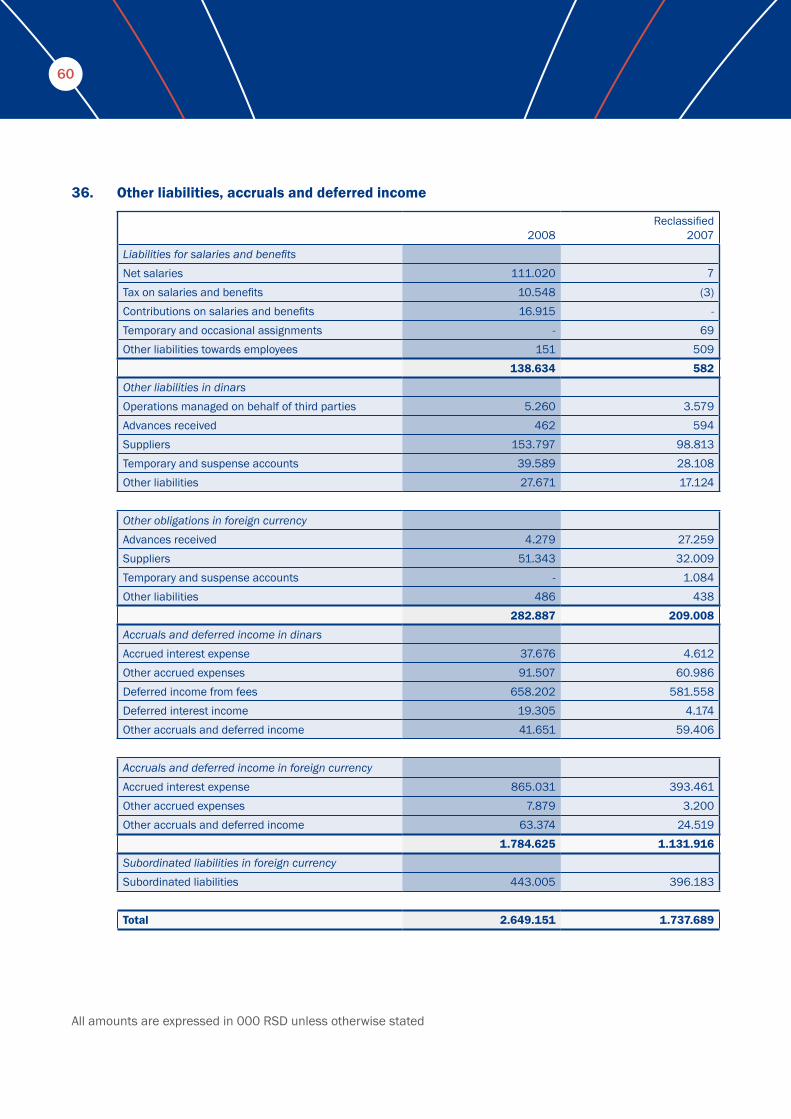

Tax liabilities 33 47.728 32.553Provisions 34 217.062 96.079Liabilities from profit 35 207.854 6.938Other liabilities, accruals and deferred income 36 2.649.151 1.737.689Total liabilities 88.332.412 61.545.198

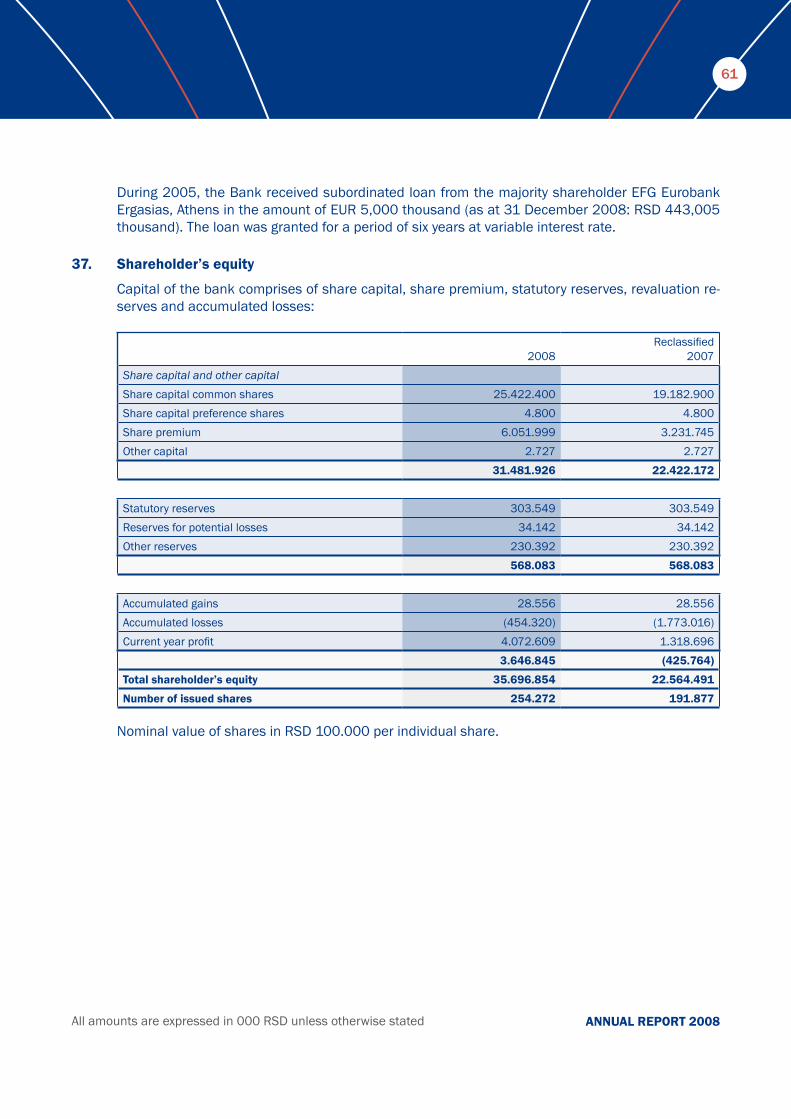

Shareholders’ equityShare capital and other capital 37 31.481.926 22.422.172Reserves 37 568.083 568.083Accumulated gains 37 28.556 28.556Accumulated losses 37 (454.320) (1.773.016)Current year profit 37 4.072.609 1.318.696Total shareholders' equity 35.696.854 22.564.491

Total liabilities and shareholders' equity 124.029.266 84.109.689

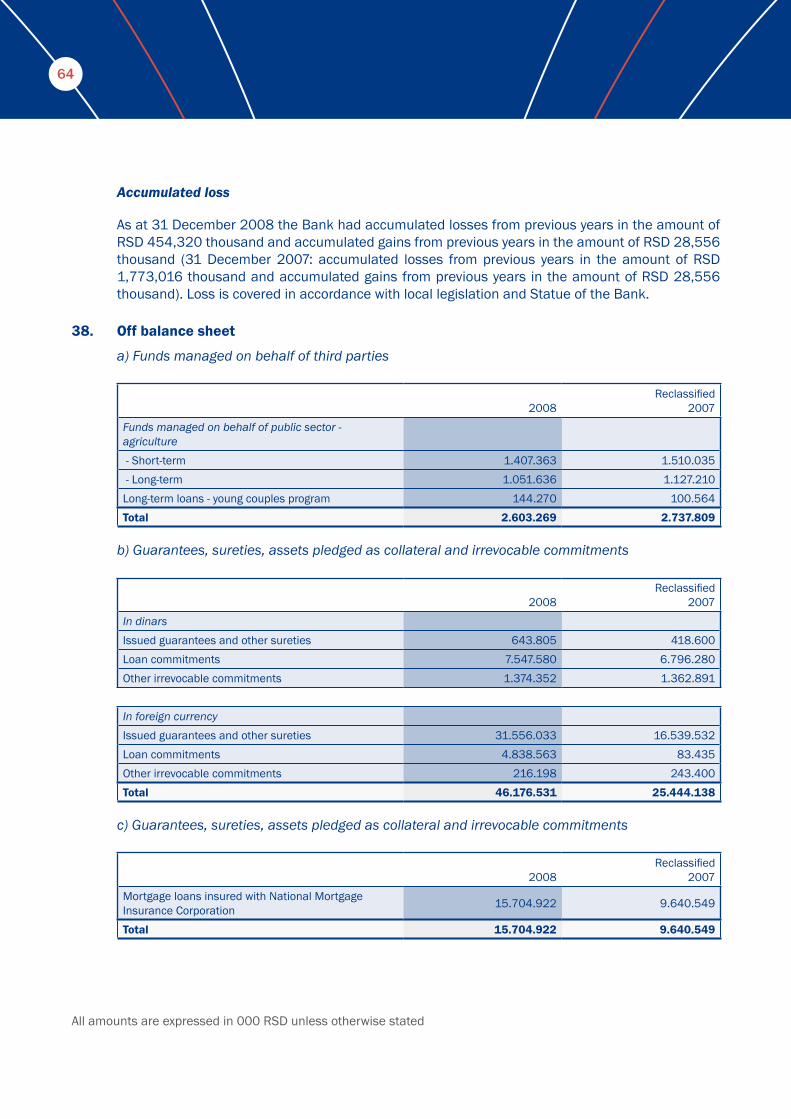

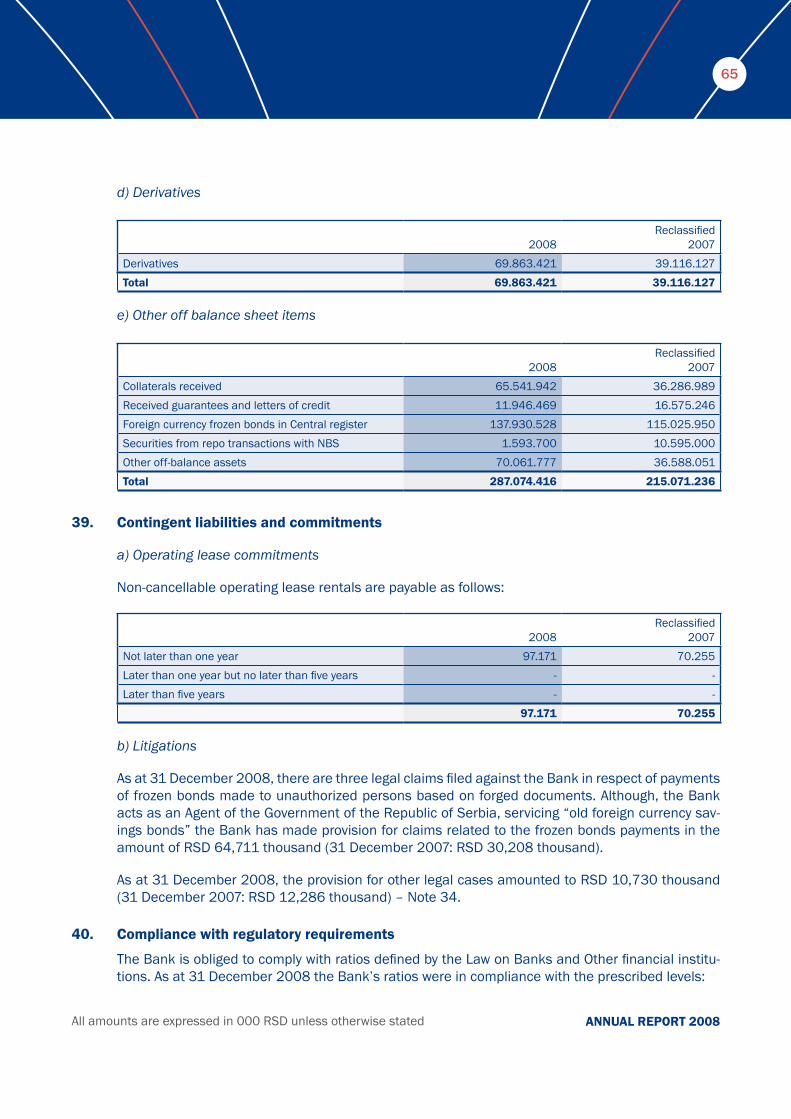

Off Balance Sheet itemsFunds managed on behalf of third parties 38 2.603.269 2.737.809Guaranties, sureties, assets pledged as collateral and irrevo-cable commitments 38 46.176.531 25.444.138

Guaranties, sureties and collaterals received 38 15.704.922 9.640.549Derivatives 38 69.863.421 39.116.127Other off-balance sheet items 38 287.074.416 215.071.236

421.422.559 292.009.859

Balance Sheet in RSD 000

8

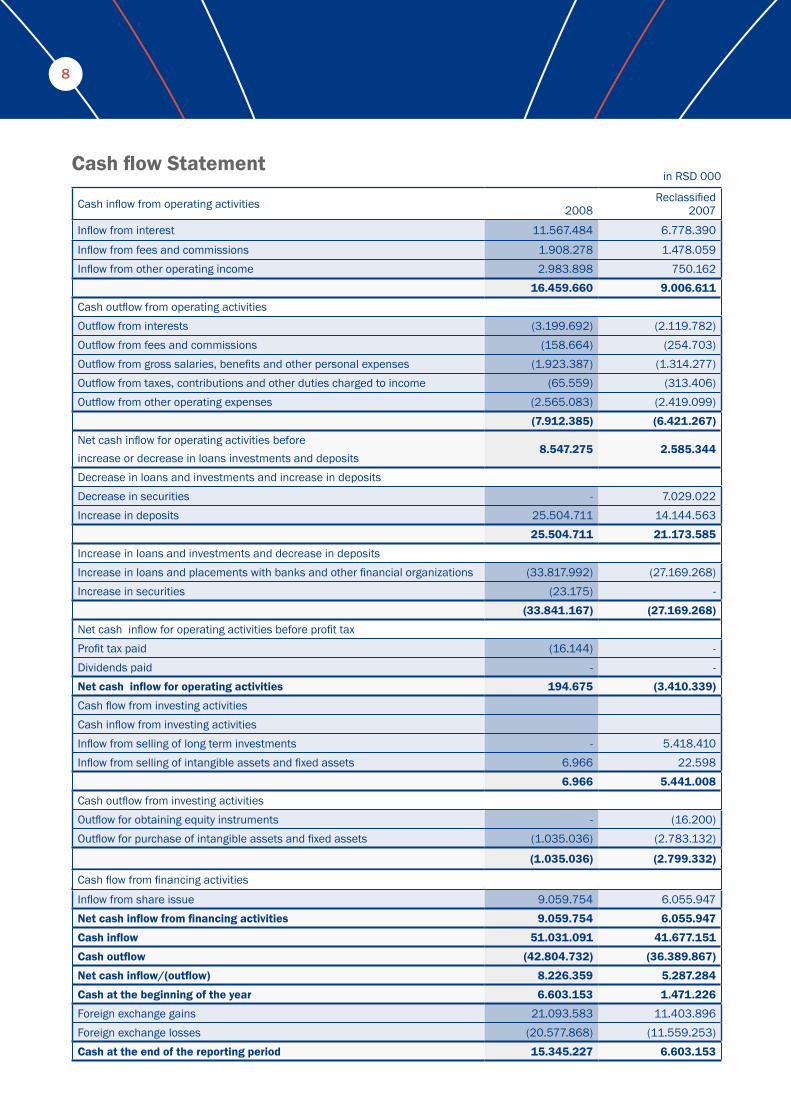

Cash inflow from operating activities 2008Reclassified

2007

Inflow from interest 11.567.484 6.778.390

Inflow from fees and commissions 1.908.278 1.478.059Inflow from other operating income 2.983.898 750.162

16.459.660 9.006.611

Cash outflow from operating activitiesOutflow from interests (3.199.692) (2.119.782)Outflow from fees and commissions (158.664) (254.703)Outflow from gross salaries, benefits and other personal expenses (1.923.387) (1.314.277)Outflow from taxes, contributions and other duties charged to income (65.559) (313.406)Outflow from other operating expenses (2.565.083) (2.419.099)

(7.912.385) (6.421.267)

Net cash inflow for operating activities before increase or decrease in loans investments and deposits

8.547.275 2.585.344

Decrease in loans and investments and increase in deposits Decrease in securities - 7.029.022Increase in deposits 25.504.711 14.144.563

25.504.711 21.173.585

Increase in loans and investments and decrease in depositsIncrease in loans and placements with banks and other financial organizations (33.817.992) (27.169.268)Increase in securities (23.175) -

(33.841.167) (27.169.268)

Net cash inflow for operating activities before profit taxProfit tax paid (16.144) -Dividends paid - -Net cash inflow for operating activities 194.675 (3.410.339)

Cash flow from investing activitiesCash inflow from investing activitiesInflow from selling of long term investments - 5.418.410Inflow from selling of intangible assets and fixed assets 6.966 22.598

6.966 5.441.008

Cash outflow from investing activitiesOutflow for obtaining equity instruments - (16.200)Outflow for purchase of intangible assets and fixed assets (1.035.036) (2.783.132)

(1.035.036) (2.799.332)

Net cash flow from investing activities (1.028.070) 2.641.676Cash flow from financing activities

Inflow from share issue 9.059.754 6.055.947Net cash inflow from financing activities 9.059.754 6.055.947

Cash inflow 51.031.091 41.677.151

Cash outflow (42.804.732) (36.389.867)

Net cash inflow/(outflow) 8.226.359 5.287.284

Cash at the beginning of the year 6.603.153 1.471.226

Foreign exchange gains 21.093.583 11.403.896Foreign exchange losses (20.577.868) (11.559.253)Cash at the end of the reporting period 15.345.227 6.603.153

Cash flow Statementin RSD 000

9

ANNUAL REPORT 2008

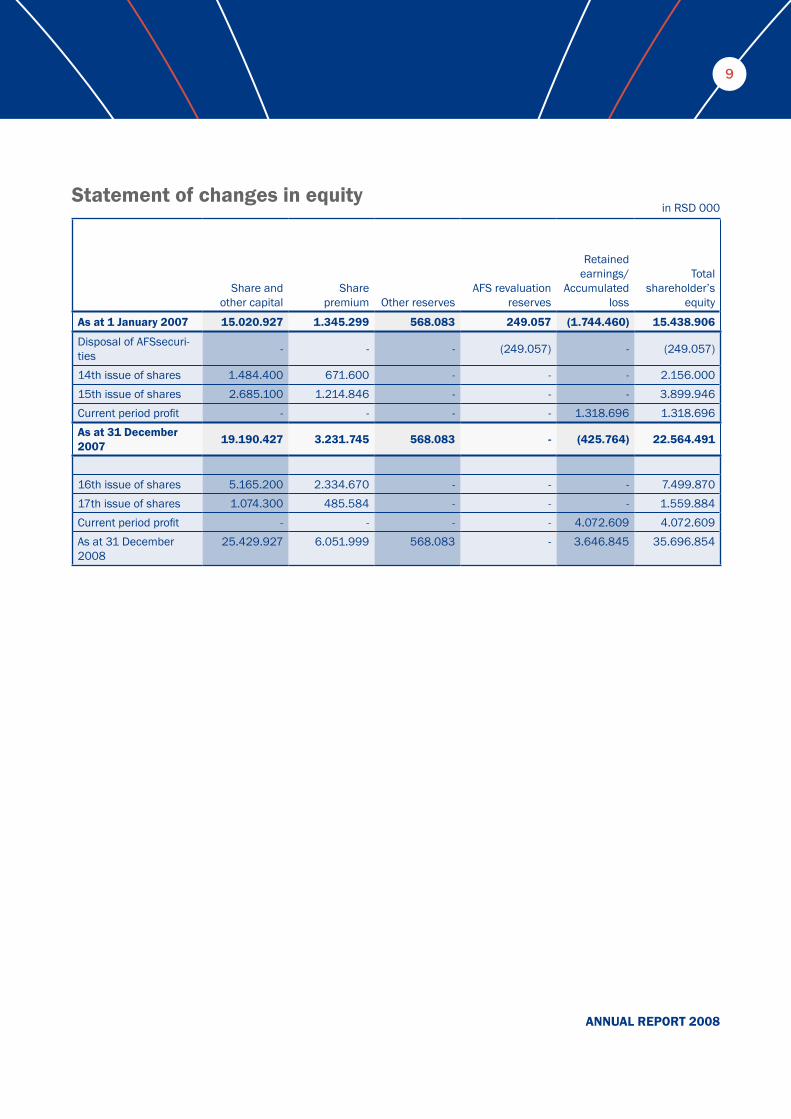

Share and other capital

Share premium Other reserves

AFS revaluation reserves

Retained earnings/

Accumulated loss

Total shareholder’s

equity

As at 1 January 2007 15.020.927 1.345.299 568.083 249.057 (1.744.460) 15.438.906

Disposal of AFSsecuri-ties - - - (249.057) - (249.057)

14th issue of shares 1.484.400 671.600 - - - 2.156.00015th issue of shares 2.685.100 1.214.846 - - - 3.899.946Current period profit - - - - 1.318.696 1.318.696As at 31 December 2007 19.190.427 3.231.745 568.083 - (425.764) 22.564.491

16th issue of shares 5.165.200 2.334.670 - - - 7.499.87017th issue of shares 1.074.300 485.584 - - - 1.559.884Current period profit - - - - 4.072.609 4.072.609As at 31 December 2008

25.429.927 6.051.999 568.083 - 3.646.845 35.696.854

Statement of changes in equityin RSD 000

10

Dear Shareholders,

Despite the extraordinary market conditions we experienced at the end of the year, 2008 was another very successful year for Eurobank EFG in Serbia. Our bank climbed to the fourth position in the market in terms of assets and is well positioned for continuing its successful operations with a strong network of retail branches and corporate Business Centres, a wide range of products and services and significant market shares in all key business segments.

Financial results were excellent with the total profit after tax reaching RSD 4.1 billion (cca € 50 million) showing a 209% increase over 2007. As a result, ROE increased to 14% compared to 6.9% in 2007 whilst ROA stood at 3.9%.

Total assets increased by 32% to RSD 124 billion (cca €1.4 billion) as a result of strong lending and deposit growth across all categories. Our bank achieved one of the highest growths in market share from all banks operating on the market, as our share grew from 5.4% to 7%.

Deposits grew by 27% compared to 2007 amounting to RSD 62 billion (cca €700 million). Despite the fact that in the last quarter of the year the banking sector experienced a significant outflow of deposits (over 1bn EUR of deposits were withdrawn, representing over 15% of the total market) we managed to protect our deposit base and service our clients without any disruptions. We should also note the very good results we achieved in retail deposits where our market share of 11% - as compared to our share of branches in the country of 5% - is a reflection of the confidence and trust of the Serbian public towards our Bank.

Loans (including cross border lending) also increased by 32% to reach RSD 97.5 billion (just over €1.1

Letter to Shareholders

billion). In retail lending our Bank achieved further growth of its share in the most dynamic segments of the market and is now within the top banks in lending to entrepreneurs (with a market share close to 20%), credit cards (over 15%), mortgage loans and consumer loans (close to 10% in both areas).

Significant progress was also made in the area of wholesale lending, as we extended our network of Business Centres dedicated to servicing corporate clients, grew our portfolio by 50% and are now one of the top lenders in the country co-financing major projects such as the USCE Shopping Mall and the renovation of the “Metropol” hotel in Belgrade.

Tight control of expenses resulted in a substantial improvement in operating efficiency as the Cost-to-Income ratio decreased from 68.3% in 2007 to 49.6% in 2008.

Filippos Karamanolis President of the Executive Board

11

ANNUAL REPORT 2008

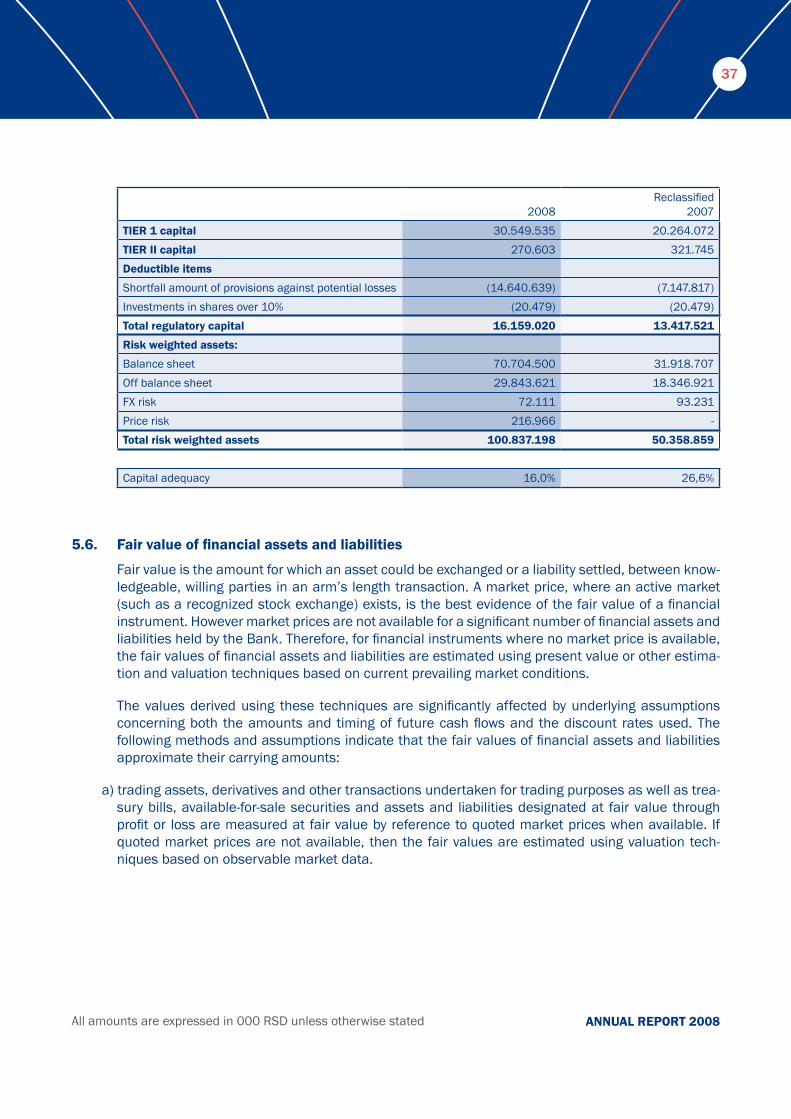

Our bank is amongst the best capitalised banks on the market with a statutory capital adequacy ratio of 16% at the end of 2008. During the year, 2 further capital increases were carried out to a total amount of RSD 9.1 billion.

At the end of 2008, Eurobank EFG had a network of 123 branches with wide national coverage and eleven business centres offering high quality services to private individuals and companies. During the year a number of new products and services were introduced such as the APS (Automatic Payment System) terminals for the payment of credit card and loan installments, various enhancements to our e-banking service and the “Ask the Expert” section on our website where customers can address questions to our executives regarding banking products. There was also a change to the legal name of the bank, that is now “Eurobank EFG a.d. Beograd”.

Continuing the expansion of our business activities, a new company – “EFG Asset Fin” – was established, specializing in operating leasing. Together with our other Group companies in Serbia: “EFG Leasing” (specializing in financial leasing), “EFG Securities” (specializing in brokerage), “EFG Property Services” (real estate services) and “EFG Business Services” (Payroll management) we can readily cover all the business needs of our clients.

We also continued with the successful imple me- n t a tion of our Corporate Social Responsibility (CSR) program “We invest in European values” because we truly believe that it is our duty to give back to the community in which we successfully operate. During the course of this program almost €2.8 milli-on have been allocated to projects which support education, public health, environmental protection and the social inclusion of persons with disabilities. In 2009 the successful implementation of our CSR programme was recognized through the receipt of the “Virtus” award for our long-standing cooperation with the Centre for Inclusive Society, the CSR award by the “Serbian Association of business jou rnalists” the “Golden Globe” CSR award by magazine “Bi-znis”.

Looking ahead, it is clear that 2009 will be a very challenging year for the banking sector. The world

is in the midst of a financial crisis of unprecedented scale in recent history, the worst in the last 70 years. Most countries in the region of Central and Eastern Europe are facing significant challenges such as the financing of large current account deficits, a slowdown in both domestic demand and exports and pressure on their currencies. Some of these countries – including Serbia – have already turned towards the IMF and other international financial organisations for assistance and there will surely be more to follow.

In this environment of great uncertainty and low visibility, our main objective in 2009 is to operate with a full sense of responsibility towards our major stakeholders: our clients (both those that have trusted us with their deposits and our lending clients), our staff and our shareholders. To this end, we will be focusing on:

Maintaining and further enhancing our strong ��capital and liquidity positionRisk management and the whole credit cycle ��from underwriting (where more stringent credit criteria are already in place to reflect the in-creased credt risk in the market) to strengthe-ning our Collections activitiesIncreasing pre-provision revenue by active ��management of our Balance SheetTight control of expenses��

We are also fully committed to supporting the Serbian economy and intend to participate actively in any Government programs with this objective.

Despite the current global downturn we remain optimistic about the longer-term prospects of the Serbian economy and are fully committed to continuing our successful operations in the county.

Belgrade, June 2009

12

Filippos KaramanolisPresident of the Executive Board

Slavica PavlovićChief Financial Officer and Board Member

Antonios ChatzistamatiouHead of Corporate Banking Division and Board Member

Danilo ĐurovićHead of Risk Management Division and Board Member

Vuk Zečević Head of Treasury Division and Board Member

EXECUTIVE BOARD

Georgios Michalakopoulos Head of Operations and Organisation Division and Board Member

Nataša KovačevićHead of Human Resources Divisionand Board Member

13

ANNUAL REPORT 2008

BOARD OF DIRECTORS

David WatsonPresident

Members:

Independent Members:

Piergiorgio Pradelli

Nikolaos Aliprantis

Slobodan Slović

Georgios Michelis

Angelos Tsichrintzis

Theodoros Karakassis

Stavros Ioannou

Evvagelos Kavvalos

14

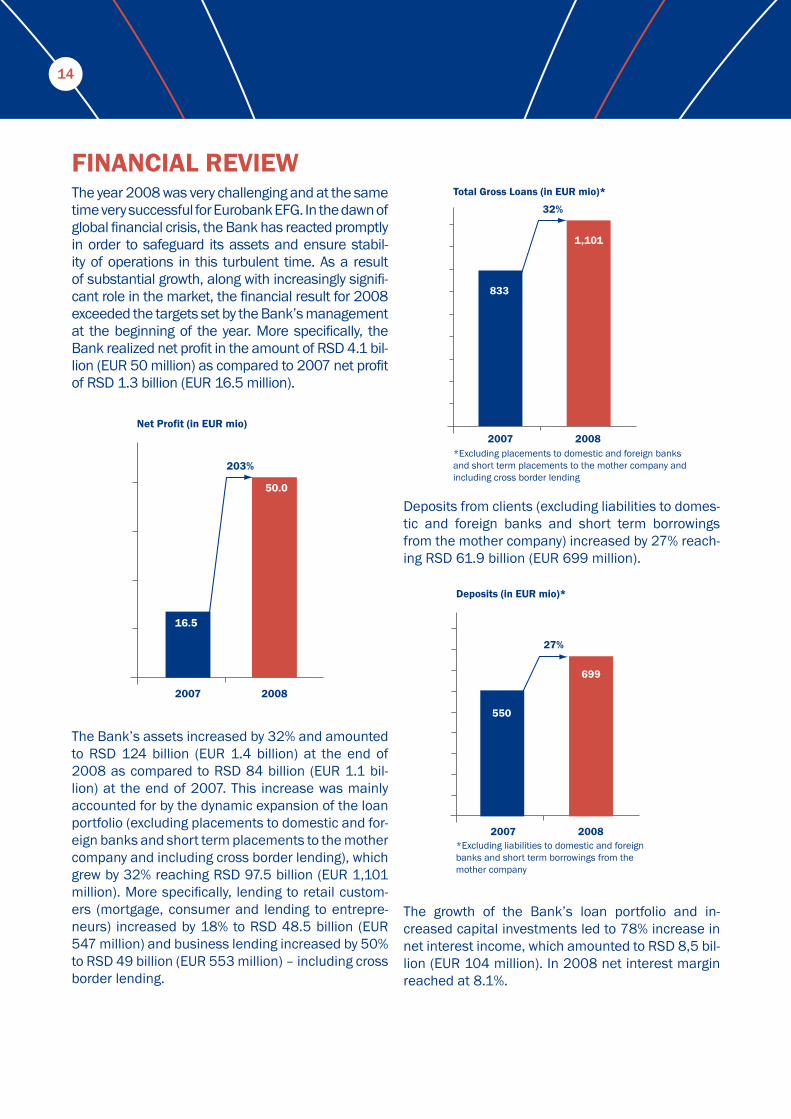

FINANCIAL REVIEWThe year 2008 was very challenging and at the same time very successful for Eurobank EFG. In the dawn of global financial crisis, the Bank has reacted promptly in order to safeguard its assets and ensure stabil-ity of operations in this turbulent time. As a result of substantial growth, along with increasingly signifi-cant role in the market, the financial result for 2008 exceeded the targets set by the Bank’s management at the beginning of the year. More specifically, the Bank realized net profit in the amount of RSD 4.1 bil-lion (EUR 50 million) as compared to 2007 net profit of RSD 1.3 billion (EUR 16.5 million).

The Bank’s assets increased by 32% and amounted to RSD 124 billion (EUR 1.4 billion) at the end of 2008 as compared to RSD 84 billion (EUR 1.1 bil-lion) at the end of 2007. This increase was mainly accounted for by the dynamic expansion of the loan portfolio (excluding placements to domestic and for-eign banks and short term placements to the mother company and including cross border lending), which grew by 32% reaching RSD 97.5 billion (EUR 1,101 million). More specifically, lending to retail custom-ers (mortgage, consumer and lending to entrepre-neurs) increased by 18% to RSD 48.5 billion (EUR 547 million) and business lending increased by 50% to RSD 49 billion (EUR 553 million) – including cross border lending.

Deposits from clients (excluding liabilities to domes-tic and foreign banks and short term borrowings from the mother company) increased by 27% reach-ing RSD 61.9 billion (EUR 699 million).

The growth of the Bank’s loan portfolio and in-creased capital investments led to 78% increase in net interest income, which amounted to RSD 8,5 bil-lion (EUR 104 million). In 2008 net interest margin reached at 8.1%.

16.5

Net Profit (in EUR mio)

203%

2007 2008

50.0

833

Total Gross Loans (in EUR mio)*

2007

32%

2008

1,101

*Excluding placements to domestic and foreign banks and short term placements to the mother company and including cross border lending

550

Deposits (in EUR mio)*

2007

27%

2008

699

*Excluding liabilities to domestic and foreign banks and short term borrowings from the mother company

15

ANNUAL REPORT 2008

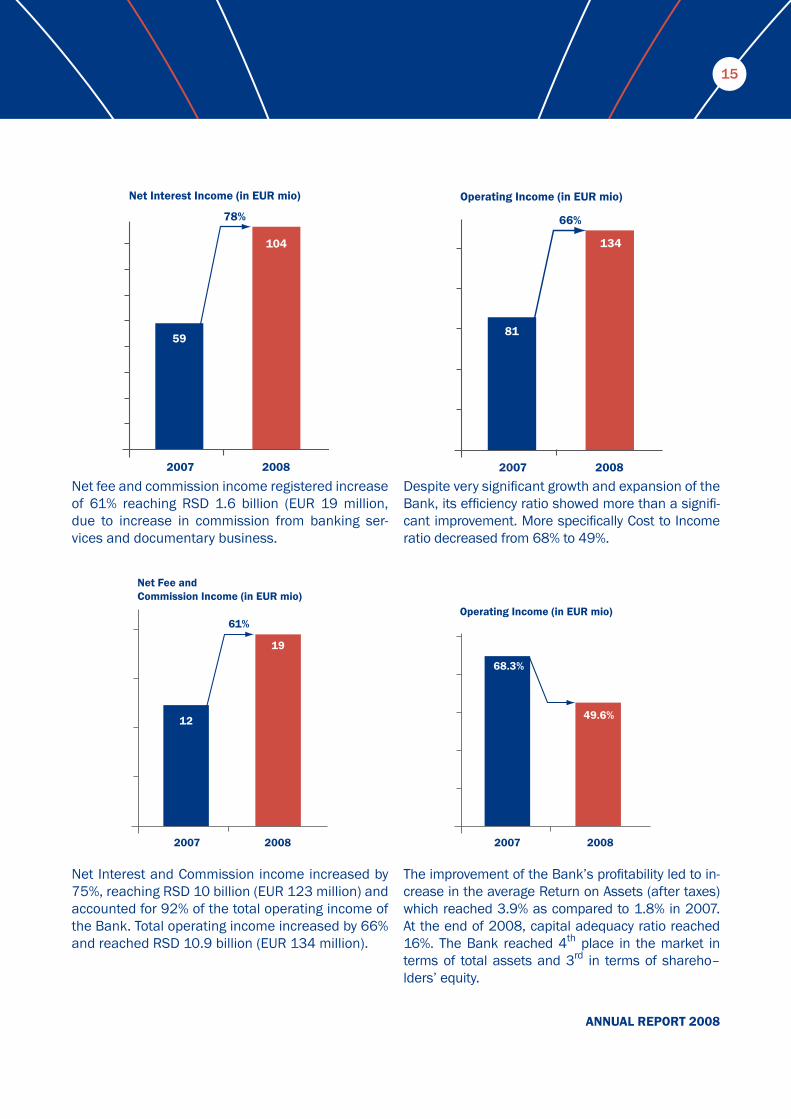

Net fee and commission income registered increase of 61% reaching RSD 1.6 billion (EUR 19 million, due to increase in commission from banking ser-vices and documentary business.

Net Interest and Commission income increased by 75%, reaching RSD 10 billion (EUR 123 million) and accounted for 92% of the total operating income of the Bank. Total operating income increased by 66% and reached RSD 10.9 billion (EUR 134 million).

Despite very significant growth and expansion of the Bank, its efficiency ratio showed more than a signifi-cant improvement. More specifically Cost to Income ratio decreased from 68% to 49%.

The improvement of the Bank’s profitability led to in-crease in the average Return on Assets (after taxes) which reached 3.9% as compared to 1.8% in 2007. At the end of 2008, capital adequacy ratio reached 16%. The Bank reached 4th place in the market in terms of total assets and 3rd in terms of shareho–lders’ equity.

12

Net Fee andCommission Income (in EUR mio)

2007

61%

2008

19

59

Net Interest Income (in EUR mio)

2007

78%

2008

104

81

Operating Income (in EUR mio)

2007

66%

2008

134

68.3%

Operating Income (in EUR mio)

2007 2008

49.6%

Retail Banking Service Networks

18

Retail Banking Network

In 2008 Eurobank EFG continued with Branch Network expansion, finishing the year with 123

branches, 11 business centers and 5.1% of the market share of the total number of branches in Serbia. In 2008, we have implemented a new ser-vice named Automated Payment System (APS), with the aim of raising the overall quality of services at Eurobank EFG Serbia to a higher level.

Direct Sales Agents (DSAs), as the bank’s alte-rnative distibution channel, began the sale of Small Business Banking loans in February 2008. New DSAs as well as cu rrent DSA top performers in Customer Lending were trained in the sale of Small Business Banking loans. DSA participation in total Retail Net-work Products Sale was as fo llows: Consumer Lend-ing - 13.29% on average (Credit Cards - 11.85%, Payrolls– 19.06%, Consumer Loans - 8.96%) and Small Business Banking – 8.63%. The Direct Sales force ended the year with 51 agents.

The Retail Deposits Unit continued executing its strategic decision to become the top of mind Serbian bank for savings. In 2008, Eurobank EFG managed to increase its deposits level under the manage-ment of Retail deposits by 23.32%, despite Octo-ber turmoil that caused the entire market to face a decline. This overall increase in deposits led to an increase in the market share of private individuals’ deposits from 8.87% in December 2007 to 10.91% in December 2008.

The Small Business Banking Sales Department trained over 100 Small Business Banking Officers (SBBOs) and all of the Branch Managers in the Net-work Division over the course of 2008. The number of SBBOs has increased from 96 to 170 since the training commenced this year.

We have achieved the first place in the Small Busi-ness Banking segment with a 20% of market share, and more than 100% of increasing portfolios. These exce llent results were aided by Direct Sales Agents, who acted as an alternative sales channel, as well

as by the accounting agencies, real estate agencies and Group Sales clients whom we had exce ptional coo peration with.

Consumer Lending2008 was a challenging year for the Consumer Lending market as the Division saw significant changes. The main characteristic of these changes was a tightening of the monetary policy imposed by the National Bank, aimed at restricting customers’ exposure to lending. As a consequence of this, the Consumer Lending market decreased by 4.5% in 2008. The main driver of this decrease was the si-gni ficant reduction in cash loans, following a trend that started in 2007. Despite all this, Eurobank EFG has managed to maintain its leading position in the Consumer Lending market and is among the top three banks in the area of Consumer Lending - increasing its market share to 9.03% in 2008 ver-sus 8.96% in 2007.

A main contributor to this success was the growth of credit cards. Quicker application processing and the availability of instant cash within 24 hours after card approval made Eurobank’s credit card product very attractive and massively accepted by custo-mers. As a result of this heightened performance, in 2008 Eurobank positioned itself as a leader in credit cards while issuing for Visa, Master Card and DinaCard across the Serbian market. Eurobank si-gnificantly increased its market share of the indu-stry to 18.91% this year, compared with 16.71% in 2007.

Although outstanding balances in Consumer Lend-ing in 2008 have decreased by almost 4%, profi-tability was maintained at very good levels, exhibi-ting the quality of our portfolio.

Apart from greater emphasis on the credit quality of our portfolio this year, efforts and resources were focused on fraud prevention. A major success du-ring this period was the completion of the project to have chip cards accepted in all Eurobank ATM

19

ANNUAL REPORT 2008

Keeping this in mind and remembering that Serbian ML/GDP ratio is 4% (in contrast to across Eastern Europe where the same ratio is 7%, the EU where the ratio is 36% and some other developed cou-ntries where the ratio is up to 80%), it is evident that there still remains a wide gap to be filled by the mortgage loan industry in Serbia.

Currently, the number of mortgage loans made in Serbia is around 65,000, of which 6,500 are co-mming from Eurobank EFG. The total outstanding balance of disbursed loans in Serbia is around EUR 2 billion, of which EUR 192 million are Eurobank EFG mortgage loans.

The world economic crisis, which also impacted the Serbian market, together with restrictive measures from the Serbian Central Bank caused a significant decrease in all of the bank’s lending activities, inclu-ding mortgage loans.

According to Credit Bureau data, market growth declined in 2008 to around 48.8%, compared with 105% in 2007 and 131% in 2006.

machines for Visa and MasterCard. This new mea-sure prevents Eurobank EFG from beeing liable for fradulent transactions.

In 2008, Eurobank EFG continued its effort to in-crease and improve customer service for all its exi-sting products and for newly introduced ones. This year the product mix was enriched by the addition of another very well known and popular product, Visa Electron. By offering this product to current account holders, Eurobank EFG is able to further prove its continuous effort to maintain high levels of customer loyalty and satisfaction.

Additionally, during 2008 Eurobank EFG further strengthened and expanded in the area of mer-chant clientele. Despite the market slow down, Eu-robank EFG continues to be perceived as one of customers’ first choice when it comes to consumer loans. As a result of this, 2008 market share in this segment increased to 8.93% versus 6% in the pre-vious year. In the car loan business, Eurobank EFG continued financing customers through cla ssic car loan products, maintaining the top position in this and in leasing financing categories among the first five banks.

Mortgage LendingThe Serbian real estate market is slowly developing (growing), but demand continues to be four times higher than supply. This, in combination with credit expansion, has contributed to an increase in real esta te prices in last few years.

To satisfy increasing demand it is estimated that it would be necessary to build 30,000 apartments each year. Currently, around 10,000 apartments are built each year across Serbia. Taking into co-nsideration current supply and demand on real estate market, saturation of mortgage loan ma–rket is not expected in near future.

The average salary in the country is around EUR 400 monthly and the average mortgage loan is made for around EUR 30,000 across an average of 20 years. The average mortgage loan installment is for EUR 200 – amounting to 50% of the average salary.

10%

90%

10% Eurobank EFG 90% Other banks

Mortgage lending market share in 2008

20

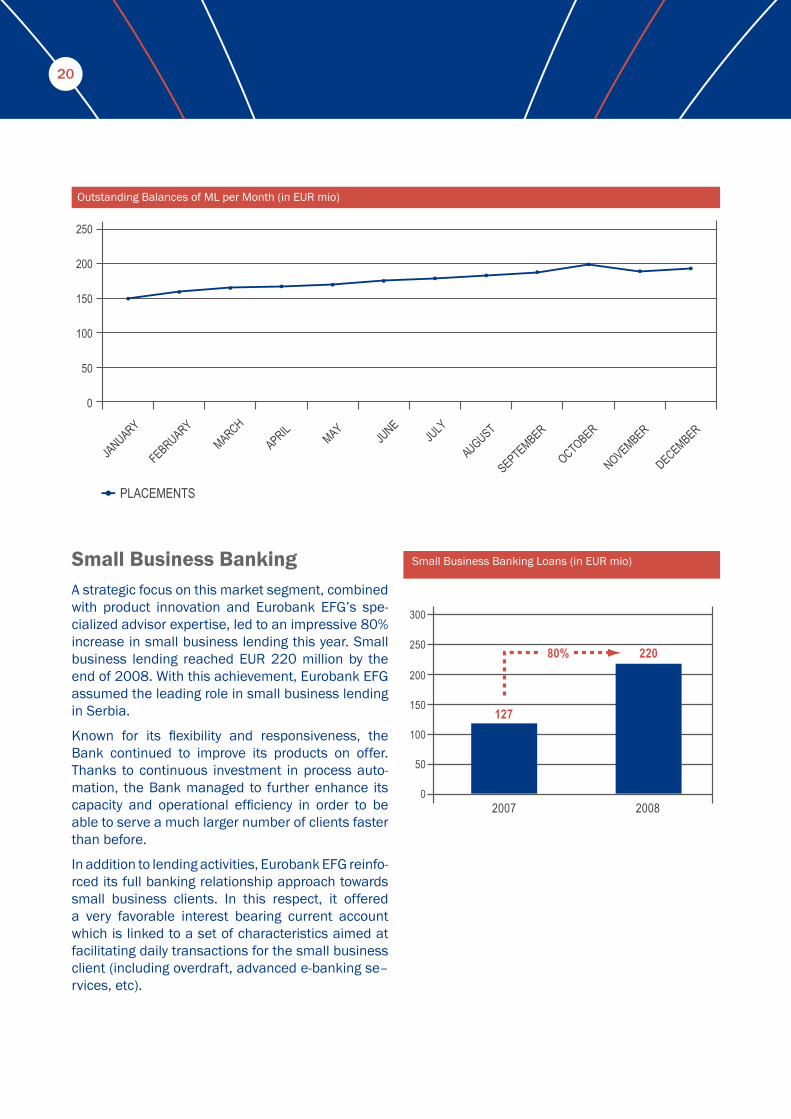

Small Business Banking A strategic focus on this market segment, combined with product innovation and Eurobank EFG’s spe-cialized advisor expertise, led to an impressive 80% increase in small business lending this year. Small business lending reached EUR 220 million by the end of 2008. With this achievement, Eurobank EFG assumed the leading role in small business lending in Serbia.

Known for its flexibility and responsiveness, the Bank continued to improve its products on offer. Thanks to continuous investment in process auto-mation, the Bank managed to further enhance its capacity and operational efficiency in order to be able to serve a much larger number of clients faster than before.

In addition to lending activities, Eurobank EFG reinfo-rced its full banking relationship approach towards small business clients. In this respect, it offered a very favorable interest bearing current account which is linked to a set of characteristics aimed at facilitating daily transactions for the small business client (including overdraft, advanced e-banking se–rvices, etc).

Small Business Banking Loans (in EUR mio)

127

220

0

50

100

150

200

250

2007 2008

300

80%

Outstanding Balances of ML per Month (in EUR mio)

PLACEMENTS

0

50

100

150

200

250

JANUARY

FEBRUARYMARCH

APRILMAY

JUNE

JULY

AUGUST

SEPTEMBER

OCTOBER

NOVEMBER

DECEMBER

21

ANNUAL REPORT 2008

Corporate Banking

24

Leasing facilities (see later section),��

M & A advisory services via the Bank’s affili-��ates.

Finally, in 2008, the Division was reinforced with the establishment of the Business Development Department which supports sales units via targeted campaigns addressing the needs of specific market segments, new product developments and internal workflow re-engineering.

EFG Leasing2008 has been a prosperous year for Eurobank EFG’s leasing activities in Serbia. This is mainly due to an expansion of the local market, a wider range of products on offer and the establishment of a new company EFG Asset Fin d.o.o. to cover operational leasing.

EFG Leasing and EFG Asset Fin can now offer a variety of flexible solutions to clients and can com-pete successfully on the local market. Besides the standard financial leasing products (passenger and commercial vehicles, construction and industrial equipment), EFG Leasing has developed a variety of additional attractive products, including a Sale & Lease Back option, Subleasing and Vendor Financ-ing.

In 2008 EFG Leasing achieved dynamic growth evidenced by satisfactory profitability and a higher market share.

A close relationship with other members of the Eurobank EFG Group makes the company’s susta-inability much more likely than that of its compe-titors.

EFG Asset Fin was officially established in March 2008 and its operations commenced in April 2008. EFG Asset Fin offers operational leasing with a focus on vehicles and construction machinery.

For the first time, EFG Asset Fin has succeeded over the last six months to cover all market needs and be-come a respectable player within the Serbian leas-ing market. Furthermore, strong cooperation with several official distributors has been established.

Corporate Banking

The Corporate Banking Division of Eurobank EFG continued its expansion during 2008. The high

quality of its lending portfolio, developed during the previous two years, was expanded to include sev-eral medium large entities and numerous small me-dium enterprise (SME) companies. The SME port-folio has been significantly increased by more than 150% during 2008. Overall, the Corporate Banking portfolio grew from EUR 322 million at the end of 2007 to EUR 494 million at the end of 2008. The Corporate Banking Division offers a wide range of flexible banking services and products to both ex-isting and potential clients through its specialized sales network.

This network includes:

Large Corporate Department, located in Be-��lgrade, which addresses the global banking needs of companies with a turnover of more than EUR 10 million; andSME Department, covering the banking require-��ments of companies with a turnover of EUR 0.5 million to EUR 10 million. This Department ope rates via a specialized network of business centers in Belgrade (2 locations), Novi Sad, Niš, Kragujevac, Čačak, Šabac, Subotica and Novi Pazar (i.e., in all geographical regions in Serbia).

Corporate clients enjoy a wide range of regular and complex banking services which are summarized below:

Working capital credit lines,��

Investment loans for expansion of production, ��warehousing, or office facilities,Treasury products,��

Cash management and transactional banking ��services, Project financing covering residential, comme–��rcial and retail projects,Trade finance,��

Payroll services,��

25

ANNUAL REPORT 2008

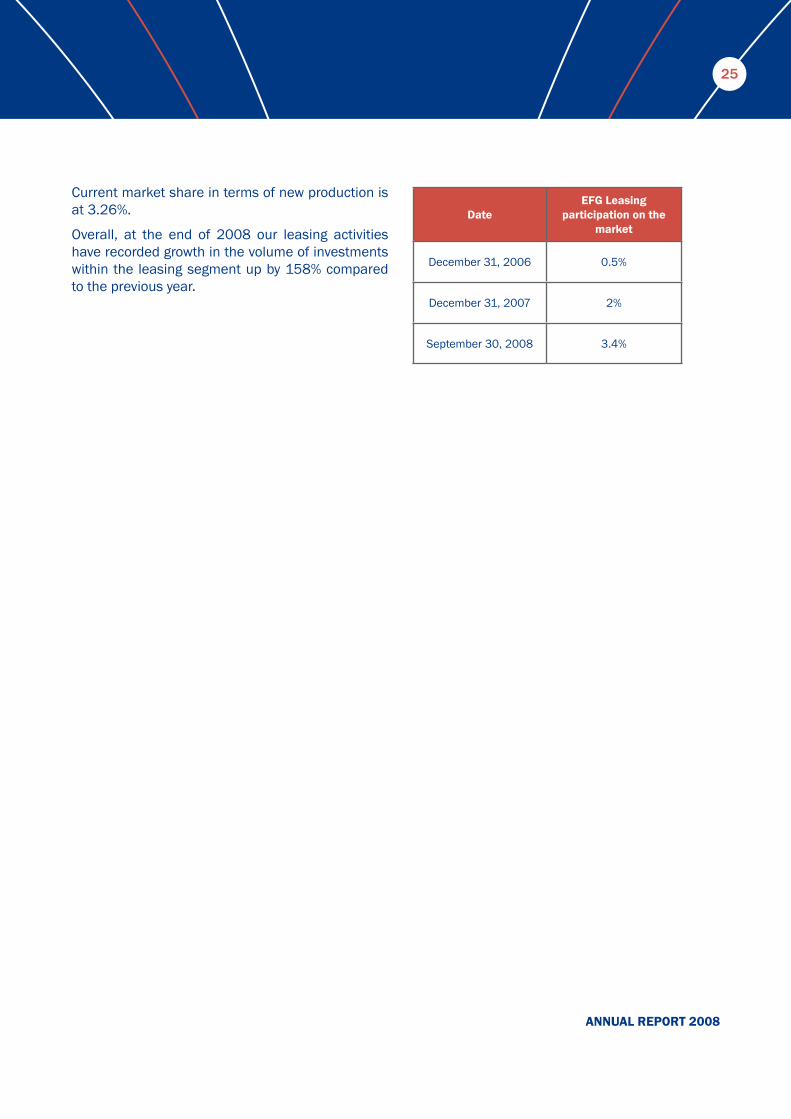

Current market share in terms of new production is at 3.26%.

Overall, at the end of 2008 our leasing activities have recorded growth in the volume of investments within the leasing segment up by 158% compared to the previous year.

DateEFG Leasing

participation on the market

December 31, 2006 0.5%

December 31, 2007 2%

September 30, 2008 3.4%

Investment Banking & Capital Markets

28

2008 turned into a year full of challenges for the Treasury Division of Eurobank EFG in Serbia.

A strategic objective for the Treasury Division was to consolidate and obtain a leading po-

sition for Eurobank EFG in Capital Markets so that during these volatile times additional liquidity could be provided to the Bank. Most of the money markets were not functioning during 2008 (especially from the end of September on) and trust between banks worldwide was severely diminished. Eurobank EFG had implemented a clear and strong strategy from the beginning of 2008 to improve its deposit port-folio and to gather liquidity. This stra tegy has been accomplished thanks to the well organized deposit units within the Bank, as well as to our long-term cooperation and strong relationships with existing and new clients.

The Trading Department (FX, MM and Bonds) generated increased profits in 2008 thanks to its active involvement in all aspects of market development, its strategy seeking to disperse risk and most importantly in this year, its ability to provide liquidity. These excellent results were mainly due to the department’s utilization of opportunities that arose during 2008. Eurobank EFG was, and still is a leader in the FCSB Bond market holding a 95% market share in 2008.

Still very high in its two week REPO rate, the Division sustained significant trading volumes in its operations with the Central bank (from a 9.50% increase to 17.75% at the end of 2008).

Proper staffing and organization structure allowed the Treasury Sales Department to increase its profits. This was encouraged by a wide range of new clients, including large and medium size enterprises, institutional customers and private customers - all of whom require a wide range of products and services (FX, interest rates, bonds and derivatives).

During the past year, the Division continued to develop front-office systems – a centralized information system for the real time recording and

monitoring of transactions. In addition, the Division implemented back-office systems for the execution and clearing of deals (GATOS).

Despite the credit-crunch and liquidity crisis, the Treasury Division managed to ensure major functions, including necessary funds and liquidity, would enable the Bank to sustain high loan growth rates in order to increase its market share in Serbia.

Custody Services

Eurobank EFG Serbia is a leading local bank in providing securities services to the local market. In August 2007, the Securities and Exchange Commission licensed Eurobank EFG Serbia to initiate custody operations in the Securities Market (decision number 5/0-11-4295/4-07).

Within one year, up to 2008, the Bank has managed to be among the top 3 local custodian banks according to assets under custody. Our Custody is fully committed to the idea of taking a leading position on the securities services market while offering a wide range of services to our clients.

Eurobank EFG has become a confidential partner to our custody clients by offering competitive quality products such as: safekeeping and settlement services, income processing, corporate actions, recordkeeping, reporting and tax reclaims. Since last year when new, high-class, secure software for supporting custody services was implemented, the Bank was able to meet the most comprehensive and complex custodial needs. High straight-through-processing rates (STP), the largest amount of experience in the local market in working with securities and the availability and reliability of our services, all significantly contribute to its results.

Treasury

29

ANNUAL REPORT 2008

International Presence

32

Eurobank EFG presence in New Europe

In 2008, the Eurobank EFG group sustained its balanced growth in the seven countries of New Eu-

rope where it operates,i.e. Bulgaria, Serbia, Roma-nia, Turkey, Poland, Cyprus and the Ukraine, offering sophisticated and attractive products and services, through an extensive network of 1,244 branches, business centres and points of sale, and a work-force of more than 14,000 people. Special empha-sis was placed throughout the year on enhancing the deposit base and further reinforcing internal risk management structures, with the aim of safeguard-ing the Group in anticipation of the gradual deterio-ration of the international financial climate.

Slowly, but surely, the global economic crisis is also being felt in New Europe, affecting economic activ-ity, investment and the financial sector. Dealing with the crisis promptly and efficiently will require coop-eration among supranational organizations, govern-ments and regulators, with the active involvement of financial institutions.

The Eurobank EFG group has made strategic invest-ments in the region, addressing a market with a to-tal population of more than 195 million, which fea-tures a low degree of financial service penetration and shows excellent long-term growth prospects. Taking into account the major economic slowdown anticipated of in all countries, as well as the adver-sity of the overall economic environment, in 2009 Eurobank EFG will continue to emphasize on main-taining adequate liquidity and ensuring asset qual-ity, as well as operating cost discipline, and to stand by its clients by offering functional and rationally-priced products and services.

Moreover, Eurobank EFG is consistently pursuing its active involvement in the social process of the re-gion, through multiple social responsibility initiatives and the sponsorship of selected foundations and organizations from the fields of Education, Health, Culture, the Environment and Sports.

BulgariaThe year 2008 has been another year of successful operation for Postbank, which retained its leading position among the three top banks in the country, offering innovative and competitive products and services.

The Bank is ranked fifth in terms of assets, with a market share of 7.8%. In 2008, the Group’s loans in Bulgaria recorded a 37% increase to €3.3 billion, while deposits increased by 15% to €1.9 billion. In deposits, the market share reached 9.1% by the end of the year. The sound expansion of the Bank and its subsidiaries’ operations, along with cost growth containment, led to an impressive 43% increase in profits, which amounted to €71 million.

The upgrade of 231 branches and 17 business cen-tres that employ 3,000 people, as well as their reno-vation during 2008, helped optimize the services rendered.

In 2008, the Bank, in cooperation with EFG Eu-robank Securities, introduced EFG’s mutual funds to the Bulgarian market, thus covering a wide range of investment proposals and stock market services.

The nomination of Postbank as the top investment intermediary; its distinction as “Bank of the Year” at the financial exhibition “Banks, Investment, Mon-ey”; its distinction for innovation and quality in in-vestment products; and the award it received as the “Best Bank in Tourism”, attest to the high quality of its products and services, and the commitment of its personnel and management towards customers and shareholders.

Always adhering to the principles of corporate social responsibility, Postbank took initiatives related to the natural environment, and offered on-the-job training to students and scholarships to school pupils.

RomaniaIn 2008, Bancpost established itself as one of the leading financial institutions of Romania, reaching the eighth place in terms of assets, with a market

33

ANNUAL REPORT 2008

share of 4.7%. This was due to the growth of its net-work, which reached 293 branches and 17 business centres, and to the management’s prompt response to the extremely volatile conditions prevailing in the market.

Bancpost covered the needs of the Group’s retail customers in Romania and supported the busi-nesses’ plans, contributing to the growth of the lo-cal economy. The 26.5% increase of the Group’s assets in Romania, which reached €6.0 billion, was mainly based on deposit growth through the offer of targeted savings programs. The public’s response to these programs led to a 68% increase in deposits and a consequent increase in market share from 4.0% in 2007 to 4.9% in 2008, but also led to a large drop of the loans to deposits ratio to 159% from 214% in the previous year. Loans amounted to €4.0 billion, increased by 25.8%.

Expense growth was contained to 2007 levels, de-spite the expansion of the Branch network, leading to a 12 percentage point improvement of the cost/income ratio, which stood at 59% by the end of 2008.

Special mention should be made to the awards granted to the Organization for its performance dur-ing 2008. More specifically, Bancpost was select-ed as “Retail Bank of the Year” by the prestigious “Saptamana Financiara” magazine, and was named “Bank of the Year” by “The Diplomat” magazine. Distinctions were also granted to high-ranking ex-ecutives of the Bank for their contribution and busi-ness activity, with Mr. Yannis Kougionas selected as “Greek Businessman of the Year” by “The Diplomat” magazine, and Mrs. Manuela Plapcianu,

Managing Director, receiving the “Most Admired Businesswomen 2008 – Leading Corporate Execu-tive Award” by the “Bucharest Business Week”.

TurkeyIn 2008, Tekfenbank was fully aligned to the vision and business strategy of the Eurobank EFG Group. In this vein, the Group’s Turkish subsidiary bank was renamed from Tekfenbank to Eurobank Tekfen

A.Ş. in January 2008. The Bank continued to grow, opening seven new Business Centres in Istanbul and Ankara, while the existing branch network was renovated in accordance with the new corporate identity. Moreover, many infrastructure projects, as well as the organizational structures required for op-erations growth, were realized. More specifically, all back office operations, as well as the loan approval, review and monitoring functions were centralized.

The lending portfolio, which mostly consists of loans to medium-sized and large enterprises, stood at to €1.0 billion, increased by 43% year-on-year, while the Bank also improved its position in the leasing and factoring sectors. There was enhanced presence in the capital markets’ segment, as EFG Istanbul Secu-rities captured 8.3% of foreign investor transactions executed at the Istanbul Stock Exchange in 2008.

As part of its growth strategy, the Bank expanded its products and services offer. In the past year it cre-ated a Custody Department, and restructured the Affluent Banking sector, emphasizing on the sale of capital market products. Moreover, the range of investment products was expanded through the cre-ation of type A Mutual Funds and the restructuring of type B Fund management, in cooperation with EFG Istanbul Securities.

PolandIn 2008, less than three years since its launching, Polbank EFG turned profitable, delivering €13.4 mil-lion. This is a remarkable achievement given that the Bank’s growth has been purely organic, gradu-ally opening 325 branches and six business centres all over the country.

Polbank EFG outperformed the Polish banking mar-ket in terms of business growth, increasing its as-sets by 124% to €4.9 billion and capturing a 4.3% market share in retail lending and 1.5% in depos-its.

The Bank’s brand awareness was improved in 2008, reaching 51% of the public, according to the relevant surveys. Polbank EFG won many awards and distinctions, including: a “Nomination for Bank-

34

ing IT leader” by the Gazeta Bankowa publication, the “Golden Consumer’s Laurel” award for its retail savings account and the “Consumer Award 2008” of the Grupa Media Partner organization, the “Effie nomination” for financial services advertising and a ranking as the “2nd Best Account” by the Gazeta Wyborcza newspaper.

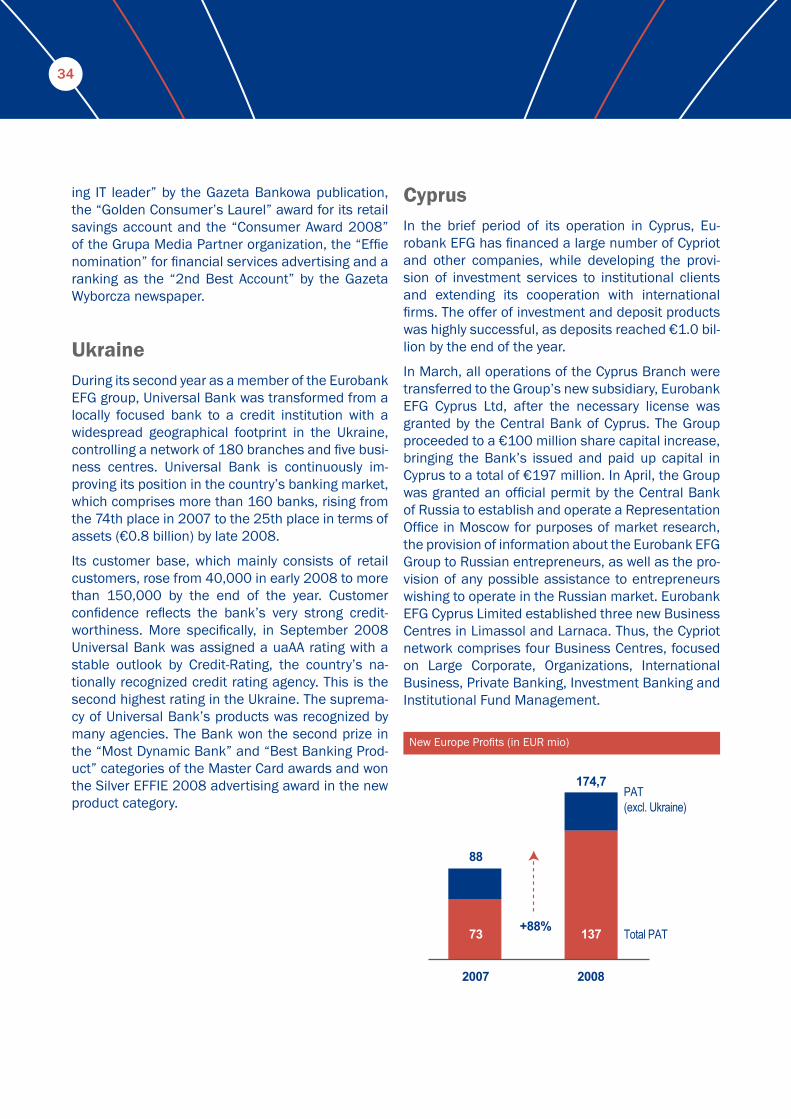

UkraineDuring its second year as a member of the Eurobank EFG group, Universal Bank was transformed from a locally focused bank to a credit institution with a widespread geographical footprint in the Ukraine, controlling a network of 180 branches and five busi-ness centres. Universal Bank is continuously im-proving its position in the country’s banking market, which comprises more than 160 banks, rising from the 74th place in 2007 to the 25th place in terms of assets (€0.8 billion) by late 2008.

Its customer base, which mainly consists of retail customers, rose from 40,000 in early 2008 to more than 150,000 by the end of the year. Customer confidence reflects the bank’s very strong credit-worthiness. More specifically, in September 2008 Universal Bank was assigned a uaAA rating with a stable outlook by Credit-Rating, the country’s na-tionally recognized credit rating agency. This is the second highest rating in the Ukraine. The suprema-cy of Universal Bank’s products was recognized by many agencies. The Bank won the second prize in the “Most Dynamic Bank” and “Best Banking Prod-uct” categories of the Master Card awards and won the Silver EFFIE 2008 advertising award in the new product category.

CyprusIn the brief period of its operation in Cyprus, Eu-robank EFG has financed a large number of Cypriot and other companies, while developing the provi-sion of investment services to institutional clients and extending its cooperation with international firms. The offer of investment and deposit products was highly successful, as deposits reached €1.0 bil-lion by the end of the year.

In March, all operations of the Cyprus Branch were transferred to the Group’s new subsidiary, Eurobank EFG Cyprus Ltd, after the necessary license was granted by the Central Bank of Cyprus. The Group proceeded to a €100 million share capital increase, bringing the Bank’s issued and paid up capital in Cyprus to a total of €197 million. In April, the Group was granted an official permit by the Central Bank of Russia to establish and operate a Representation Office in Moscow for purposes of market research, the provision of information about the Eurobank EFG Group to Russian entrepreneurs, as well as the pro-vision of any possible assistance to entrepreneurs wishing to operate in the Russian market. Eurobank EFG Cyprus Limited established three new Business Centres in Limassol and Larnaca. Thus, the Cypriot network comprises four Business Centres, focused on Large Corporate, Organizations, International Business, Private Banking, Investment Banking and Institutional Fund Management.

New Europe Profits (in EUR mio)

88

Total PAT

PAT(excl. Ukraine)

2007 2008

+88%73

174,7

137

35

ANNUAL REPORT 2008

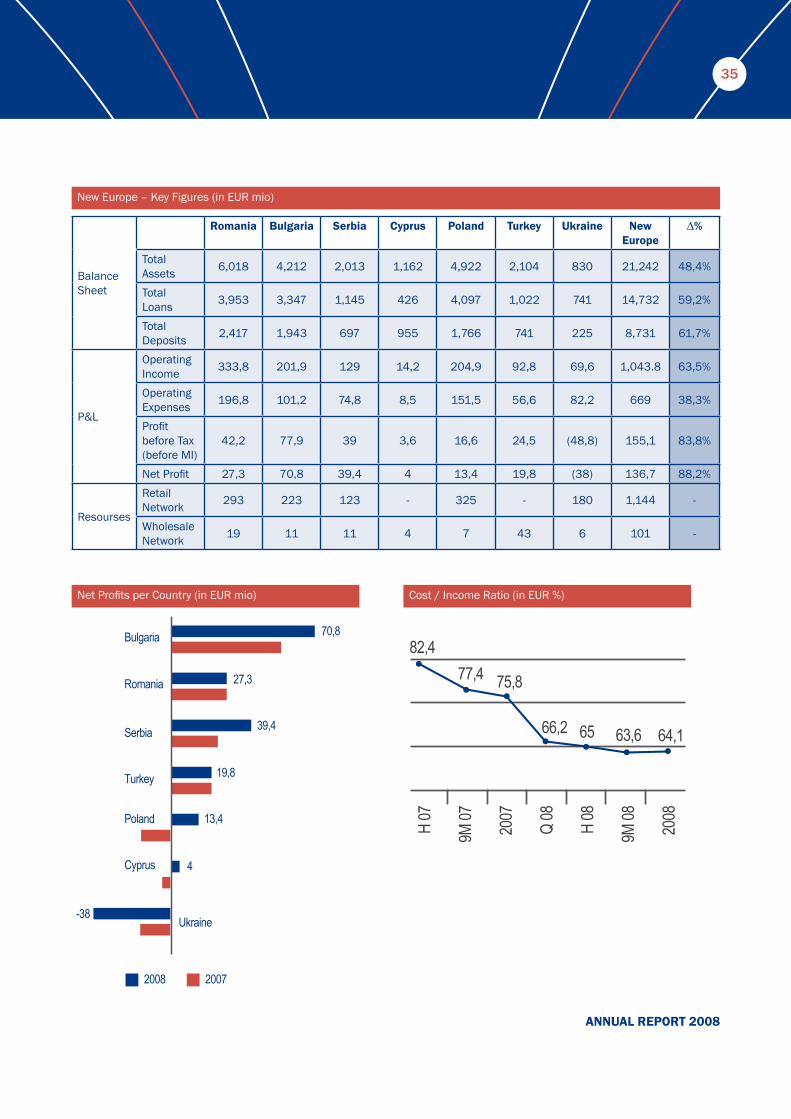

Balance Sheet

Romania Bulgaria Serbia Cyprus Poland Turkey Ukraine New Europe

∆%

TotalAssets 6,018 4,212 2,013 1,162 4,922 2,104 830 21,242 48,4%

TotalLoans 3,953 3,347 1,145 426 4,097 1,022 741 14,732 59,2%

TotalDeposits 2,417 1,943 697 955 1,766 741 225 8,731 61,7%

P&L

Operating Income 333,8 201,9 129 14,2 204,9 92,8 69,6 1,043.8 63,5%

Operating Expenses 196,8 101,2 74,8 8,5 151,5 56,6 82,2 669 38,3%

Profitbefore Tax(before MI)

42,2 77,9 39 3,6 16,6 24,5 (48,8) 155,1 83,8%

Net Profit 27,3 70,8 39,4 4 13,4 19,8 (38) 136,7 88,2%

Resourses

Retail Network 293 223 123 - 325 - 180 1,144 -

Wholesale Network 19 11 11 4 7 43 6 101 -

Bulgaria 70,8

27,3

39,4

19,8

13,4

4

-38

Romania

Serbia

Turkey

Poland

Ukraine

2008 2007

Cyprus

New Europe – Key Figures (in EUR mio)

Net Profits per Country (in EUR mio) Cost / Income Ratio (in EUR %)

H 07

82,477,4 75,8

66,2 65 63,6 64,1

9M 07 2007

Q 08

H 08

9M 08 2008

Other Subsidiaries

38

EFG Property Services

EFG Property Services Belgrade continued its su-ccessful expansion and market presence in Serbia during 2008. Despite heavy competition, EFG Pro–perty Services increased its activities on the local market and acquired several large-scale projects from internationally renowned companies. After suc-cessful completion of leasing the “Ušće” Shopping Center in cooperation with Merrill Lynch, EFG Pro-perty Services became an exclusive leasing agent, as well as consultant for Plaza Centers for their three projects currently under construction.

EFG Property Services has assisted the Network Development Department in locating over 35 new branches for Eurobank EFG, thus greatly strength-ening the Bank’s presence on the market.

As Eurobank’s exclusive appraisers, we have per-formed over 4,000 appraisals for the Bank as well as for third parties and have expanded our appraisal network to cover the entire territory of Serbia while maintaining the highest professional and ethical standards. We are strictly compliant with IVSC stan-dards in performing all of our valuations. We have expanded our scope of services to include plant and machinery appraisals, business and industrial

complexes, highest and best use analyses and prop-erty and facility management for two properties ac-quired by our Investment Real Estate Fund with third parties.

EFG Securities

In 2008, Eurobank EFG’s broker finalized the trans-formation from Prospera Securities to EFG Securi-ties. The focus was put on altering the company to fit the demanding standards of the Group and this was reflected throughout all departments, including trading, sales, research and investment banking.

However, the capital markets crisis severely affe-cted the performance of EFG Securities, as the majority of United States and European Union insti-tutional clientele moved to the sidelines after suffe-ring heavy losses all over the world markets. This resulted in a decrease of the market share of EFG Securities from 4.1% to 2.7% in 2008. The liquidity of EFG Securities on the Belgrade Stock Exchange dropped substantially, thus further affecting the performance of the brokerage.

Simultanesouly, EFG Securities’ Research Depa-rtment began producing highly accurate research reports in line with Group standards. It is one of the few research departments in the country publishing its reports for renowned world institutions.

EFG Business Services

Since April 2008, one more company within the Eu-robank EFG Banking Group is operating in Serbia - EFG Business Services. Our new company provides integrated operational support services in the field of payroll administration by using the superior software solutions of EFG Business Services S.A.

HIGH

MEDIUM

LOW

25% 50% 75%

EFG PROPERTYSERVICES

MARKET SHARE

QUAL

ITY

OF S

ERVI

CE

39

ANNUAL REPORT 2008

Athens, which holds a leading position in payroll calculation in Greece.

Employees of companies who decide to receive their salary through Eurobank EFG acquire the special benefits package of banking products and services called ‘’Euro PLATA.’’

Our goal is to identify clients who are seeking a ‘’know-how“ in payroll administration. With supe-rior software solutions and a team of experienced officers, EFG Business Services provides compa-nies with measurable benefits in time and money through its recognizable package of services known as OPM (Outsourcing Payroll Management).

We achieved successful cooperation in the area of payroll calculation with subsidiary companies of Eu-robank EFG, as well as with other strong companies operating in the country.

Other Activities Of The Bank

42

Payment Services Our long term strategy in payment services is to fu-rther improve our global transaction banking envi-ronment in order to deliver customized solutions for client segment-specific needs. We hope that these solutions will embrace a wide range of banking se-rvices such as payment transactions, liquidity ma-nagement, trade finance and securities services.

Eurobank EFG delivers an ample range of services through an international network linked by advanced technology, including significant online banking ca-pability. Our payments businesses consist of:

A significant customer base��

Significant business volumes��

Full coverage of all business lines (Cash Ma–��nagement, Trade Finance, Capital Markets Sales and Securities Services) And a wide range of products for Financial In-��stitutions and Corporations (Current Accounts, Sight Deposits / Overdrafts, Global Payments & Collection Services, Check Services, Liqui-dity Management, Information and Reporting Se rvices, Wholesale Solutions, International Trade Products, Equities and Custody Service)

Through the centralization of our middle and back-office functions, there is streamlined co-operation within the Corporate Banking Division, the Treasury & Capital Markets Division and among the Private & Business clients. Through our continued and disci-plined cost management, we are aiming for ambi-tious targets.

We put sustained effort into identifying the impo-rtant need differences between large corporate businesses, SMEs and individual customers and payment instruments in order to safeguard cu–stomers so they can enjoy flexible and tailored pay-ment services. We protect payment users and pro-viders from fraud by developing a ‘future proofed’ approach that sets clear principles and guidelines rather than defining problems and prescribing pre-set solutions. We are clear and detailed in providing

information for what happens and who is liable if things go wrong. We have increased our competitive value while maintaining sufficient stability in the system and only implement efficient processes with the highest quality controls.

Currently, we are intensively working on the long-term project of changing our customers’ habits through standardization of processes. We are ho-ping to streamline these in order to make cash only used primarily for small payments so that we can increase efficiency by minimizing the number of pay-ments affected by cash.

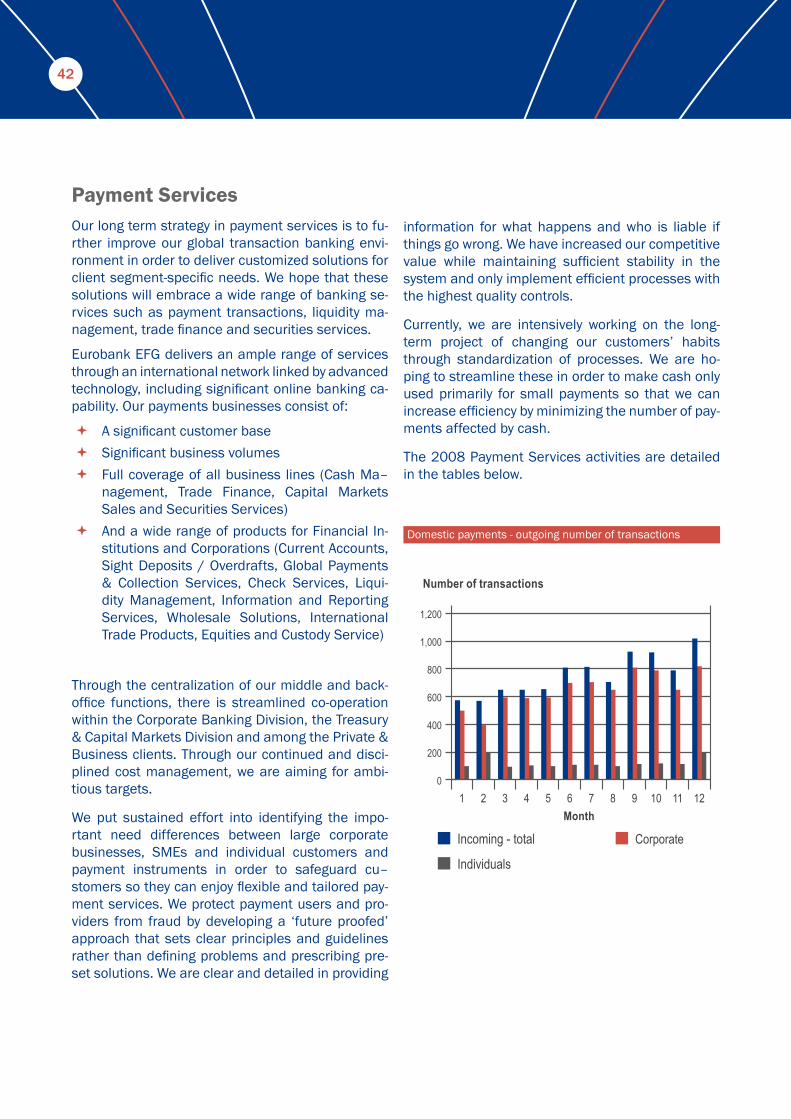

The 2008 Payment Services activities are detailed in the tables below.

Month

Number of transactions

Incoming - total

Individuals

Corporate

0

200

400

600

800

1,000

1,200

121110987654321

Domestic payments - outgoing number of transactions

43

ANNUAL REPORT 2008

Month

Number of transactions

Incoming - total

Individuals

Corporate

0

500

1,000

1,500

2,000

2,500

1211109876543210

50,000

100,000

150,000

200,000

250,000

300,000

350,000

121110987654321Month

Number of transactions

Outgoing - total

Individuals

Corporate

Month

Number of transactions

Incoming - total

Individuals

Corporate

0

200

400

600

800

1,000

1,200

121110987654321

Domestic payments - incoming number of transactions

International payments – outgoing number of transactions

International payments - incoming number of transactions

44

Percent

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

121110987654321

Value of trn Number of trnMonth

e-Banking Since our operational merger with Nacionalna štedionica and the establishment of the FC@e-bank-ing application – as the Group’s standard and the Bank’s alternative customer service cha nnel - an emphasis has been placed on the stabilization and localization of the services. This includes services being offered to the Bank’s customers (both Retail and Corporate) and this new competitive emphasis fares well against existing e-banking solutions in the local market. These improvements and empahsis on e-banking were guided by the Bank’s need to reduce its operating costs stemming from day-to-day trans-actional business. The provi ssion of an easy-to-use application has been able to benificially extend the Bank’s business communication with its customers in an accessible manner.

Through constant improvement of its functions, our Bank is able to offer today a full scope of electronic services to end-users which follow in line with cu stomers’ habits and new market trends. The e-Banking channels are designed to provide access to all business lines and its flexibility has allowed acco modations for specific customer needs distinctively.

e-Banking share in Bank’s domestic outgoing payments

Domestic payments - value of outgoing transaction

Month

Number of transactions

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

121110987654321Month

Value of transactions

- €

10,000,000 €

20,000,000 €

30,000,000 €

40,000,000 €

50,000,000 €

60,000,000 €

70,000,000 €

121110987654321

Domestic payments - outgoing number of transaction

45

ANNUAL REPORT 2008

Risk Management

48

Effective risk management is a top priority, as well as a major competitive advantage, for

Eurobank EFG. The Bank has allocated ample re-sources for upgrading its policies, methods and infrastructures in order to ensure compliance with best international practices and the regulations of the National Bank of Serbia. Eurobank EFG imple-ments a well-defined credit approval process, in-dependent credit reviews and overall effective risk management policies for market and operational risk. The risk management policies implemented by the Bank, as well as those implemented by the internal audit and compliance departments, are re-viewed annually.

Credit RiskEurobank EFG follows international best practices by implementing a well-defined credit approval pro-cess, independent credit reviews and an overall effective risk management functions. The segrega-tion of duties in the process imposes independence across account officers responsible for the relation-ship between duties, the approval process and the disbursement and credit monitoring done over the life of the loan. The Bank’s credit policies are re-viewed on an annual basis.

The adequacy of the Bank’s provisioning policy is reviewed yearly, while provisions are calculated on a monthly basis and booked on a quarterly basis. Provisions are based on delinquency analysis in the case of retail customers and based on credit rating in case of corporate customers. In case of impaired loans, Eurobank EFG calculates provisions based on impairment analysis, taking into account expected cash-flows, projected recoverability period and re-coverable amount, etc. in compliance with IAS 39 requirements. Special reserves for potential losses are calculated in accordance with NBS require-ments.

In all lending activities, the Bank ensures that the “four-eyes” principle is always applied.

For the evaluation of consumer credit quality and performance, Eurobank EFG uses proper statistical

models (scorecards). The approval process is ce–ntralized and the portfolio is also monitored though a set of statistical analyses.

In mortgage lending, Eurobank EFG employs centra-lized approval. All property collateral valuations are performed by authorized evaluators. Loan amounts depend upon the collateral appraisal and the bo-rrower’s creditworthiness. Portfolio quality is also monitored through a range of statistical analyses.

With respect to small business banking loans, credit approval is based on the following framework: ce-ntralized approval procedures and clear guidelines on collateral.

Corporate lending makes greater use of financial analysis. Liquidity and financial strength are evalu-ated together with various qualitative factors. The evaluation of the corporate lending portfolio is based on a credit rating system that takes the above mentioned factors into account. This system is also used for the quarterly calculation of provisions for the Corporate Banking portfolio.

Moreover, the Credit Control Department regularly audits the various lending units of the Bank, ensu–ring the proper implementation of lending policies.

Credit Review PoliciesFollowing approval, the quality of the Wholesale Banking and Retail Banking exposures is monitored and assessed by the Credit Control Department. The Credit Control Department evaluates the quality of the portfolios through field reviews (case-by-case) for wholesale lending and statistical analyses on a portfolio basis for retail banking.

The Department is also responsible for monitoring the credit review policy. The Credit Control Depa-rtment operates independently from all business units of the Bank and reports to the Risk Executive.

The Bank has set limits and controls regarding the concentration of risk to individual parties, groups or industries. Such risks are monitored on a continual basis and are subject to quarterly or semi-annual re-

49

ANNUAL REPORT 2008

views and approvals by the Board of Directors’ Risk Committee.

Market RiskMarket Risk is the potential loss that may occur from changes in market fundamentals (interest rates, exchange rates, share prices, product/commodity prices and the volatilities of these risk factors).

In order to ensure the efficient monitoring of risks that emanate from the market’s overall activities, the Bank adheres to certain principles and policies. The objectives of these policies are to:

Set the framework and minimum standard for ��market risk control and management through-out the Bank Enable compliance with local regulations and ��EFG Group standardsEstablish a framework that will eventually ��allow the Bank to gain competitive advantage through risk-based decision-making

Liquidity RiskLiquidity risk is the risk that the Bank will be unable to fund assets to meet obligations at reasonable cost or at all; for financial assets the risk is that an instrument cannot be sold or otherwise exchanged for its full market value.

The Bank places funds for mandatory reserve with the National Bank of Serbia for protection against sudden and significant withdrawals of deposits. The Bank manages the liquidity risk by constantly moni-toring a mix of assets and liabilities and by analyzing projected cash flows in order to enable the Bank to fulfill its obligations at any moment.

It is the responsibility of the Assets and Liabilities Management Committee to set liquidity policies and to monitor liquidity in order to guarantee that there are no liquidity issues. The Bank’s liquidity policies are designed to ensure that:

Sufficient liquid assets are maintained to meet ��liabilities as they arise The liquidity position is monitored closely on a ��daily basisSufficient lines are available with Eurobank ��EFG Athens and other counterparties in order to meet all obligations as necessary

Operational RiskOperational risk is the risk of loss resulting from ina-dequate or failed internal processes, people and systems, or from external events.

Above and beyond the need to comply with local regu latory requirements and international best practices, Eurobank EFG recognizes that opera-tional risk management has a crucial effect on the Bank’s overall performance.

The active management of operational risks inherent in operations of the Bank is gradually and methodi-cally embedded into the procedures of organizatio-nal under operation. The individual business units retain principal responsibility for the management of operational risk inherent in their own activities. The Operational Risk Unit reports to the Risk Executive of the Bank and is responsible for the implementa-tion of the operational risk management principles and policy, the establishment of the appropriate tools and the providing of support to individual units regarding the identification, assessment, mitigation, monitoring and reporting of operational risks and for the improvement of internal controls.

Corporate Governance

52

Since its beginning, Eurobank EFG a.d. Belgrade has paid special attention to corporate gove–

rnance issues complying with prescribed guidelines and regulations of the local and Group regulatory bodies.

Operating in an emerging market that is continuou–sly adjusting to the best legal and corporate practic-es of the EU laws, the transparent and accountable governance was one of the most important items on the management agenda. As a member of EFG Group, the bank respects and follows regulations of the Swiss Federal Banking Commission, as well.

Corporate governance sets to secure responsible and good relations between the banks’ manage-ment bodies and its shareholders. It is responsible for the implementation of sound governance rules which comply with the National Bank of Serbia Law on Banks, the Law on Companies of the Republic of Serbia and other prescribed guidelines applied in the regulatory frame of the country in which the bank operates and on the Group level.

MANAGEMENT BODIES OF THE BANKBoard of Directors regularly meets every quarter and makes sure to summon extraordinary meetings whenever needed. In 2008, a total of eight meetings were held at the premises of the Bank in Belgrade.

The Board of Directors consists of nine members including the President, four of whom are indepe–ndent, thus securing highly transparent decision- making process.

Executive Board of the Bank also appoints its sub committees which have a mandate to monitor and discuss other bank business areas.

The Bank has a separate Corporate Governance Unit which facilitates smooth implementation of the best practices. It records managerial, operational and internal control frameworks for the bank and its subsidiaries in the country and makes sure to secure:

Responsible and value-driven management ��and controlEffective cooperation between all governing ��bodes of the Bank

Based on “Internal Governance Manual”, the Bank lays foundation to its overall structure and gove–rnance. In addition, Banks’ “Code of Conduct” was updated in 2008 in an aim to incorporate both the general and sensitive directions towards account-able business conduct, operations and any pote–ntial issues of conflict of interest. It serves as a legal and ethical set of directions that is applicable to all employees equally thus ensures its practical imple-mentation and purpose.

BOARD OF DIRECTORS

AUDIT COMMITTEE EXECUTIVE BOARD ASSET-LIABILITYCOMMITTEE RISK COMMITTEE

CREDIT COMMITTEE REMUNERATIONCOMMITTEE

53

ANNUAL REPORT 2008

Appendices

EUROBANK EFG A.D. BEOGRAD

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2008

3, Kolarčeva Street, Belgrade, Serbiawww.eurobank.gr, Tel: (+30) 210 333 7000

www.eurobankefg.rs; EuroPHONE: 0800 1111 44Company Registration No: 17171178

Tax Registration No: 100002532

58

FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2008

Independent auditor’s report 1 1. General information 2 2. Summary of significant accounting policies 3 3. Critical accounting estimates and judgments 17 4. Financial assets per categories and classes 18 5. Risk management policies 19 6. Interest income and expense 39 7. Fee and commission income and expense 40 8. Net gains/(losses) from sale of securities at fair value through profit and loss 40 9. Net foreign exchange gains/ (losses) 4010. Operating and other income 4111. Net provisions and impairment losses on loans and advances 4112. Salaries, benefits and other personal expenses 4213. Depreciation and amortization expenses 4214. Operating and other expenses 4315. Income and expenses arising from revaluation of assets and liabilities 4416. Income tax 4417. Earnings per share 4518. Cash and cash equivalents 4619. Callable deposits and loans 4620. Interest, fees and commission receivables, change in fair value of derivatives and other receivables 4721. Loans, advances and deposits 4822. Securities (excluding own shares) 4923. Equity investments 5024. Other lending 5025. Intangible assets 5026. Property and equipment 5127. Deferred tax assets 5328. Other assets, prepayments and accrued income 5429. Transaction deposits 5530. Other deposits 5631. Borrowings and other financial liabilities 5732. Interest, fees and commissions payable and change in fair value of derivatives 5733. Tax liabilities 5734. Provisions 5835. Liabilities from profit 5936. Other liabilities, accruals and deferred income 6037. Shareholder’s equity 6138. Off balance sheet 6439. Contingent liabilities and commitments 6540. Compliance with regulatory requirements 6541. Related parties transactions 6642. Foreign Exchange rates 6843. Reconciliation of loans, deposits and other liabilities with clients 6844. Board of directors 6845. Post balance Sheet Events 68

Contents:

2

1. General information

Eurobank EFG A.D. Beograd has been established by merger of Eurobank EFG a.d. Beograd and Nacionalna Štedionica Banka a.d. that was completed on 20 October 2006.

The Shareholders’ Assembly of the Nacionalna Štedionica Banka a.d. Beograd and the Sharehold-ers’ Assembly of the EFG Eurobank a.d. Beograd that were held on 28th July 2006 have adopted the Decision on Merger of the Nacionalna Štedionica Banka a.d. Beograd with EFG Eurobank a.d. Beograd.

On 20th October 2006, the Business Register Agency issued the Decision on merger with acquisi-tion of the Nacionalna Štedionica Banka a.d. Beograd with EFG Eurobank a.d. Beograd by which the process of merger with acquisition has been effected.

On the same date the Business Registers Agency issued the decision regarding the change of the Bank’s name to Eurobank EFG Štedionica a.d. Beograd.

The Bank is registered in Serbia for carrying out payment, credit and deposit operations in the country and abroad. The bank operates in accordance with Law on Banks and other Financial Insti-tutions based on principles of liquidity, safety and profitability.

As at 31 March 2007 the Bank has changed registered office to Kolarceva 3 in Belgrade. Previous registered office of the Bank was in Durmitorska 20 in Belgrade.

As at 31 December 2008, the Bank has changed business name to “Eurobank EFG A.D. Beograd”. Previous business name of the Bank was “Eurobank EFG Štedionica A.D. Beograd”

As at 31 December 2008 the Bank had 1,535 employees (31 December 2007: 1,369 employees). The Bank’s network comprises of 123 branches (31 December 2007: 103 branches)

The Bank’s Registration number is 17171178. The Bank’s Tax identification number is 100002532.

The Financial statements have been approved by Board of Directors on 26th February 2009.

3

ANNUAL REPORT 2008

2. Summaryofsignificantaccountingpolicies

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless other-wise stated.

2.1. Basis of preparation

The financial statements have been prepared in accordance with Accounting and Auditing Law • which requires full compliance with IFRS, as well as in accordance with regulations of the National bank of Serbia. These regulations are as follows: Rules on the Forms and Content of Items in Finan-cial Statement Forms to be Completed by Banks (Official gazette of RS no. 74/2008 and 3/2009), Rules on the Chart of Accounts and Content of Accounts within the Chart for Banks (Official gazette of RS no. 98/2007, 57/2008 and 3/2009), Accounting and Auditing Law (Official gazette of RS no. 46/2006)

The applied accounting policies differ from the IFRS requirements in the following materially signifi-• cant areas:

1. The Bank has not made certain disclosures in accordance with IAS 1 – Presentation of financial statements since the presentation of the financial statements is defined by the National Bank of Serbia.

2. “Off balance sheet assets and liabilities” are disclosed in the balance sheet form (Note 38). In ac-cordance with IFRS, off balance sheet items do not represent either assets or liabilities.

In accordance with the regulations of the National bank of Serbia, presentation of Financial State-• ments for year ended 31 December 2008 has been changed. Comparative figures for 2007 have been reclassified to reflect these changes.

The preparation of financial statements in conformity with IFRS requires the use of certain critical • accounting estimates. It also requires management to exercise its judgment in the process of apply-ing the Bank’s accounting policies. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note 3.

a) Amended and new standards and interpretations effective after 1 January 2008

The amended and new standards and interpretations effective from 1 January 2008 listed below • are not relevant for the Bank’s operations therefore they did not result in changes to the Bank’s accounting policies:

IFRIC 16 - Hedges of a net investment in a foreign operation•

IFRIC 13 - Customer loyalty programmes•

4

IFRIC 12- Service Concession Arrangements•

IFRIC Interpretation 14, IAS 19 — The Limit on a Defined Benefit Asset, Minimum Funding Require-• ments and their Interaction,

The application of the changes in the Reclassification of Financial Assets: Amendments to IAS • 39- Financial Instruments: Recognition and Measurement and IFRS 7 Financial Instruments: Dis-closures, effective from 1 July 2008, did not have material effect on the Bank’s Financial State-ments.

b) Standards and Interpretations issued but not yet effective

The following standards and interpretations that were issued but not yet effective for accounting periods beginning on 1 January 2008 have not been early adopted:

IAS 27 (Revised) - Consolidated and separate financial statements (effective from 1 July 2009)•

IFRS 2 (Amendment) - Share-based Payment-Vesting Conditions and Cancellations (effective from • 1 January 2009)

IFRS 5 (Amendment) - Non-current assets held for sale and discontinued operations and conse-• quential amendment to IFRS 1 - First-time adoption (effective from 1 July 2009)

IFRS 3 (Revised), ‘Business combinations’ (effective from 1 July 2009).•

IFRS 8, ‘Operating segments’ (effective from 1 January 2009).•

IAS 23 (Amendment) - Borrowing costs (effective from 1 January 2009)•

IAS 28 (Amendment) - Investments in associates and consequential amendments to IAS 32 - Fi-• nancial Instruments: Presentation and IFRS 7 - Financial instruments: Disclosures (effective from 1 January 2009)

AS 36 (Amendment) - Impairment of assets (effective from 1 January 2009)•

IAS 38 (Amendment) - Intangible assets (effective from 1 January 2009)•

IAS 19 (Amendment) - Employee benefits (effective from 1 January 2009)•

IAS 37 - Provisions, contingent liabilities and contingent assets•

IAS 39 (Amendment) - Financial instruments: Recognition and measurement (effective from 1 Janu-• ary 2009)

IAS 1 (Amendment) - Presentation of financial statements (effective from 1 January 2009)•

There are a number of minor amendments to IFRS 7 - Financial instruments: Disclosures, IAS 8 - • Accounting policies, changes in accounting estimates and errors, IAS 10 - Events after the reporting

5

ANNUAL REPORT 2008

period, IAS 18 - Revenue and IAS 34 - Interim financial reporting, which are part of the IASB’s an-nual improvements project published in May 2008 (not addressed above). These amendments are unlikely to have an impact on the Bank’s accounts and have therefore not been analyzed in detail.

IAS 16 (Amendment) - Property, plant and equipment and consequential amendment to IAS 7 - • Statement of cash flows (effective from 1 January 2009)

IAS 27 (Amendment) - Consolidated and separate financial statements (effective from 1 January • 2009)

IAS 28 (Amendment) - Investments in associates and consequential amendments to IAS 32- Finan-• cial Instruments: Presentation and IFRS 7 - Financial instruments: Disclosures (effective from 1 January 2009)

IAS 29 (Amendment) - Financial reporting in hyperinflationary economies (effective from 1 January • 2009)

IAS 31 (Amendment) - Interests in joint ventures and consequential amendments to IAS 32 and • IFRS 7 (effective from 1 January 2009)

IAS 38 (Amendment) - Intangible assets (effective from 1 January 2009)•

IAS 40 (Amendment) - Investment property and consequential amendments to IAS 16 (effective • from 1 January 2009)

IAS 41 (Amendment) - Agriculture (effective from 1 January 2009)•

IAS 20 (Amendment) - Accounting for government grants and disclosure of government assistance • (effective from 1 January 2009)

IFRIC 15 - Agreements for construction of real estates (effective from 1 January 2009)•

IFRIC 17 – Distribution of non cash assets to owners (effective from 1 July 2009),•

IFRIC 18 - Transfers of Assets from Customers (effective from 1 July 2009)•

The application of these new standards and interpretations which are relevant for the Bank’s op-erations will not have a material impact on the Bank’s financial statements in the period of initial application.

These financial statements do not comply with all requirements of IFRS. Therefore, these financial statements are not prepared to present financial position of the Bank, result and cash flows in ac-cordance with accounting principles accepted outside of Republic of Serbia.

6

c) Basis of measurement

The financial statements have been prepared on the historical cost basis except for the following:

• derivate financial instruments are measured at the fair value,

• financial instruments at fair value through profit or loss are measured at fair value and

• liabilities from trading activities are measured at the fair value.

2.2. Comparatives

Comparatives for the year ended as at 31 December 2007 have been reclassified in accordance with changes of the presentation of Financial Statements issued by the National Bank of Serbia.

The financial statements for the year ended 31 December 2007, have been prepared in accordance with Rules on Forms and Content of Individual Items in Financial Statement Forms to be Completed by Banks and Other Financial Organizations (Official gazette of RS no. 18/2007), Rules on the Chart of Accounts and Content of Accounts within the Chart for Banks and Other Financial Organizations (Official gazette of RS no. 133/2003 and 4/2004) and Accounting and Auditing Law (Official ga-zette of RS no. 46/2006)

The financial statements for the year ended 31 December 2008, have been prepared in accor-dance with Rules on the forms and content of items in financial statement forms to be completed by banks (Official gazette of RS no. 74/2008 and 3/2009), Rules on the Chart of Accounts and Content of Accounts within the Chart for Banks (Official gazette of RS no. 98/2007, 57/2008 and 3/2009) and Accounting and Auditing Law (Official gazette of RS no. 46/2006).

2.3. Foreign currency translation

a) Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized in the income statement.

Assets and liabilities denominated in foreign currencies have been translated into the functional currency at the market rates of exchange ruling at the balance sheet date and exchange differences are accounted for in the income statement.

b) Functional and presentation currency

Items included in the financial statements of the Bank are measured using the currency of the pri-mary economic environment in which the entity operates (“the functional currency”).