ANNUAL REPORT 2010 - 2011 ANDHRA PRADESH GRAMEENA VIKAS BANK € +<óŠ |Ÿ<ûXÙ >±MTD $¿±dt u²«+¿ù E狇À œÀt zÆ TÀçªym uÄNþçÌ ¤øNþ Rejuvenating Rural Economy Come, join us we are with you!

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANNUAL REPORT2010 - 2011

ANDHRA PRADESH GRAMEENA VIKAS BANK

€ +�<óŠ�|Ÿ<ûXÙ �>±MTD $¿±dt u²«+¿ù

E狇 À œÀtzÆ TÀçª ym uÄNþçÌ ¤øNþ

Rejuvenating Rural Economy

Come, join us

we are with you!

we are with you!

th6 Annual Report 2010-11

With Best Compliments from

Chairman

Andhra Pradesh Grameena Vikas Bank

Head Office

Warangal AP

K. Lakshmana Rao

Empowering Rural Lives

01

Srikakulam

Vizianagaram

Visakhapatnam

Khammam

Nalgonda

Saraswathi complex, Baker sahed peta

Srikakulam 532001, Tel 08942-221041

Fax 08942-221040

8-12-64/1, Himagiri theatre, New S.P. Bungalow

Vizianagaram 536002, Tel 08922-273956

Fax 08922-274221

TPT colony, Near Enadu, Seethamdhara

Visakhapatnam, Tel 0891-2713942

Fax 0891-2746341

Wyra Road, Khammam 507002

Tel 08742-226816,

Fax 08742-228972

Ramgiri, Nalgonda,

Tel 08682-229943

Fax 08682-229945

Warangal

Mahabubnagar

Sangareddy

Ashoknagar

Bhadrachalam

2-739-1-3, First Floor, Ramnagar

Hanamkonda, Warangal 506001

Tel 0870-2577884, Fax 0870-2568010

Mettugadda, Mahabubnagar 509001

Tel 08542-242861

Fax 08542-242862

Sangareddy, (Dist) Medak 502007

Tel 08455-276263

Fax 08455-276603

Ramachandrapuram Mandal

Medak 502032, Tel 040-20040773

Fax 040-23020238

Bhadrachalam, Khammam 507111

Tel 08743-231492

Fax 08743-231020

&Geographical Area

Regional Offices

02

we are with you!

Contents

Particulars Pages

Financials

Letter of Transmittal 04

Vision, Mission, Values 05

Board of Directors 06

Highlights 08

Key Performance Indicators 09

From the Chairman's Desk 12

17

Audit Report 57

Balance Sheet and Profit & Loss Account 59

Schedules & Notes 61

85

Board of Directors Report

Events and Happenings

03

Annual Report 2010-11we are with you!

The Secretary

Ministry of Finance, Dept. of Economic Affairs

Banking Division, Government of India

Parliament Street, New Delhi-110001

Dear Sir,

In accordance with the provisions of Section 20 of the Regional Rural Banks Act 1976, I

forward herewith the following documents.

A Report of Board of Directors as to the Bank's working and its activities during the period st st1 April 2010 to 31 March 2011.

stA copy of the audited Balance Sheet and Profit and Loss Account for the year ended 31

March 2011.

stA copy of the Auditor's report in relation to the Bank's accounts for the period 1 April 2010 stto 31 March 2011.

Andhra Pradesh Grameena Vikas BankHead Office : Warangal

Yours faithfully,

Chairman

(K. Lakshmana Rao)

Date: 31.07.2011

Letter of Transmittal

04

we are with you!Annual Report 2010-11

&Vision

Mission

Values

Vision

Mission

Values

Repositioning the Bank in competitive rural market and accomplish the leadership spot in

Rural Banking. Aspiring to realize the vision of excelling in Rural Credit and SME. Pursuing the

best practices for delivering the value added service to the customers by transforming the

key branches into profit and business centers.

With efficiency and service each one of us works in tandem to deliver quality rural service,

no matter where our customers choose to experience it. With the advantage of a large

network in the rural hinterland, it is our duty and obligation to serve the rural masses, the

deprived and denied, retail and agriculture sectors through improved processes,

deployment of technology, with an emphasis on employment of rural youth, augmentation

of agricultural production, up liftment of the downtrodden and unabated service to rural

poor with commitment to the sacred task of rural development and women's empowerment.

Profit orientation

Commitment for rural development

Excellence in customer service

Respect to systems and procedures

Team Synergy

05

we are with you!

Chairman

DGM on deputation from

State Bank of India

Nominees of Central Government under

Section 9 (1) (a) of the Regional Rural

Bank's Act, 1976

Nominees of Reserve Bank of India under

Section 9 (1) (b) of the Regional Rural Bank's Asst. General Manager

Act 1976 Reserve Bank of India

Regional Office, Secretariat Road, Hyderabad

Nominees of NABARD under section 9 (1)

(c) of the Regional Rural Bank's Act, 1976. Deputy General Manager

National Bank for Agriculture and Rural

Development, Regional Office, Hyderabad

Nominees of State Bank of India

under Section 9 (1) (d) of the Deputy General Manager (RBU)

Regional Rural Bank's Act, 1976 State Bank of India, Local Head Office

Hyderabad

Deputy General Manager (PBU)

State Bank of India, Local Head Office

Hyderabad

Nominees of State Government

under Section 9 (1) (e) of Regional Secretary, Institutional Finance

Rural Bank's Act, 1976 Department, Govt. of Andhra Pradesh.

District Collector & Magistrate, Warangal

1 Shri K. Lakshmana Rao

2 Shri B.Raja Rao

3 Shri B. Radhakrishna Murthy

4 Shri K.N. Singh Sardar

5 Shri D. Hari

6 Shri Manoj Khattar

7 Shri K.T. Ajit

8 Smt Vasudha Mishra, IAS

9 Shri Rahul Bojja, IAS,

BOARD OF DIRECTORS

06

we are with you!Annual Report 2010-11

BOARD OF DIRECTORS

Shri K. Lakshmana Rao

Shri B. Radhakrishna Murthy Shri K.N. Singh Sardar Shri D. Hari

Shri Manoj Khattar Shri K.T. Ajit Smt Vasudha Mishra, IAS Shri Rahul Bojja, IAS,

Shri B.Raja Rao

07

we are with you!Annual Report 2010-11

HIGHLIGHTS 2010 -2011

v

v

v

v

v

v

v

v

v

v

v

Registered a business growth of Rs. 2,012 Crores (26%) -

Highest among all RRBs in A.P.

Branches of the bank reached to 553 - Largest network among

all RRBs in A.P.

Deposits of the bank are Rs 4,794.72 Crores - Highest for any

RRB in A.P.

Advances of the bank are Rs. 4,894 Crores - Highest for any RRB

in A.P.

Recorded Highest net profit of Rs. 108 Crores in 2010 - 2011

Networth of the Bank surpassed Rs. 500 Crore, exactly

Rs. 513.09 Crore

Established Staff learning centre at Warangal to impart

training and knowledge to all staff - First among all RRBs

sponsored by SBI

172260 SHGs have been financed by the bank with an

outstanding of Rs. 1472 Crore. This is largest for any RRB in the

country

Number one RRB in the country among SBI sponsored RRBs in

earning maximum commission on SBI life products

CBS implemented at all the 553 Branches - Branches stabilised.

Bank recovered Rs. 7.35 Crores during 2010-2011 from written

off accounts

08

we are with you!Annual Report 2010-11

KEY PERFORMANCE INDICATORS(Rs in '000)

Indicators 2008-09 2009-10 2010-11

No. of Districts covered 8 8 8

No.of branches 527 538 553

a) Rural 408 414 429

b) Semi urban 86 88 88

c) Urban 33 36 36

d) Metropolitan …… …. ….

Total staff: Excluding Sponsor

Bank Staff 2160 2221 2234

Of which Officers 1385 1322 1298

Deposits 33938850 38045125 47947222

Growth % 15.69 12.1 26.07

Borrowings outstanding 13986471 15999777 19546416

Growth % 9 14.4 22.16

Gross loans and Advances outstanding 33038840 38697224 48944327

Growth % 22.33 17.13 26.48

CD Ratio 97.35 101.64 102.08

Investments outstanding 17077816 16621685 21472834

Growth % 11.23 -2.67 29.19

SLR Investment outstanding 6211799 7589071 9996983

Non-SLR Investment outstanding 10866017 9032614 11475851

Average Deposits 29337087 34159081 39000837

Growth % 14.9 16.44 14.17

Average Borrowings 10623021 13170900 16607091

Growth % 5.6 23.98 26.08

Average Gross Loans And Advances 29531173 34117695 43335628

Growth % 23.54 15.53 27.01

Average Investments 14912212 15857429 15817799

Growth % 4.38 6.34 -0.25

Average working funds 58912403 62376495 80457660

Loans issued during the year 20777800 17992000 38271901

Growth % -15.40 -13.41 112.71

Of the above, loans to Priority Sector 16622240 15970200 29779956

Of the above, loans to Non-target Group 8259700 3166100 8491945

Averages

Loans issued during the year

09

we are with you!Annual Report 2010-11

KEY PERFORMANCE INDICATORS

Indicators 2008-09 2009-10 2010-11]

Of the above, SF/MF/AL 5882373 7049110 12309498

Per branch 127092 142643 175207

Per staff 31008 34553 43370

Demand 17965792 22137900 25472765

Recovery 14870454 18049100 20595069

Over dues 3095338 408880 4877696

Recovery %(June position) 82.77 81.53 80.85

Asset classification

a) Standard 32156991 37814596 46981468

b) Sub-Standard 368759 319029 1557742

c) Doubtful 380027 525900 389227

d) Loss 133063 37699 15890

Total 33038840 38697224 48944327

Std.Assets % to Gross Loans & Advances outstanding 97.33 97.72 95.99

Interest paid on

a) Depostits 1699395 2126277 2274695

b) Borrowings 922423 1133711 1298240

Salary 701460 861664 1005186

Other operating expenses 761967 495587 546091

a) Against NPAs 401332 402948 476104

b) Other provisions 475462 588277 704346

a) Loans and Advances 3197146 4283306 5157559

b) Current A/c with SBI/Other Banks …. …. ….

c) Investments 1274575 1490635 1272310

Other income 420132 445226 750752

Profit/Loss 692742 1028407 1081292

Share Capital deposit received 890850 890850 890850

Productivity

Recovery Performance

Profitability analysis

Provisions made during the year

Interest received on

Other information

10

(Rs in '000)

we are with you!Annual Report 2010-11

KEY PERFORMANCE INDICATORS

Indicators 2008-09 2009-10 2010-11

CumulativeProvisions against NPAs 401332 402948 476104

Interest de-recognized cumulative (INCA) 52180 65802 124406

a) No. of accounts 8525 8453 2851

b) Amount 99251 229800 76200

Reserves/Accumulated profits 2210139 3108850 4190143

Loans Written off during the year

Parameters 2009-10 2010-11 % Change

Total Income (Rs.crore) 622 718 15.43

Total expenditure (Rs.crore) 474 562 18.56

Net profit (Rs.crore) 103 108 4.85

Profit per employee (Rs.lakhs) 4.63 4.86 4.97

Return on average Assets 10.16 8.92 -12.2

For the year

Parameters March-10 March-11 % Change

Capital, Reserves and Surplus(Rs. Crore) 316 424 34.23

Deposits (Rs.crore) 3807 4795 26.03

Advances (Rs.crore) 3870 4894 26.48

No.of branches 538 553 2.79

Capital Adequacy Ratio 11.22 11.85 5.61

Net NPA % 1.08 2.82 161

At the end of

11

(Rs in '000)

we are with you!Annual Report 2010-11

Chairman's

Message

It is indeed a privilege to be the Chairman of this Bank, which assumed the proportion of a mini commercial bank after

amalgamation on 31.03.2006, with its presence in over one third of Andhra Pradesh. I am at the helm for a little less

than six months. The fiscal 2010-11 has been the best year for the Bank in terms of business and the Profit.

With a growth rate of 26% each in deposits and advances ( Rs 2012 Core in absolute terms) and net profit of Rs108

Crore, both “the highest ever” since its inception on 31.3.2006, the Bank has done well, vis-à-vis previous years. The

net profit would have been more by around Rs 60 Crore but for the incidence of additional provisioning on rural

advances and the impact of wage revision. The Bank's growth rates are well above the industry growth of 16% in

deposits and 21% in credit.

The Bank has also done exceedingly well in bringing down the NPAs to Rs 198 Crore from an alarming level of nearly

Rs 900 Crore, thrown up by CBS during the year, although it has doubled vis-à-vis Rs 88.26 Cr as on 31.3.2010.

Resources mobilization, correction of technical NPAs, upgradation of NPAs and recovery in AUCA( Rs 7.35 cr),

strengthening of Balance Sheet as well and internal control mechanism had been our focused areas during the year,

while reconciling the System Suspense and Cash differences as on 31.3.2011 in CBS environment, has been a significant

achievement.

Although the growth rates and business volume are certainly positive and encouraging features of the Bank, there are

certain concerns that need to be addressed immediately. With structural changes in administrative set up as envisaged

in Thorat Committee Recommendations and adoption of Core Banking Solutions – two major decisions in administration

and functioning of branches respectively, the Bank has gone back to budding stage, learning the new technology which

is entirely different from bygone environment of manual or semi computerized operations.

Another important ingredient of the APGVB's present transformation-stage is the infusion of new blood into the Bank

by means of recruitments, after a gap of nearly two decades – around 300 people are dotting the map of APGVB with

another 419 joining the team of APGVB. They are tech-savvy, energetic, youthful, craving for recognition and young in

12

we are with you!Annual Report 2010-11

age and fresh in thoughts. There is a blend of enormously experienced staff - some on the verge of retirement, some in

their prime between 45-55 – and fresh employees beginning to blossom. I reckon this is a crucial period for the Bank's

future. The new entrants to the Bank, need to be properly nurtured, trained, groomed and oriented so that they can

assume the role of professional bankers and own the responsibility of running the Bank in the future. The average age

of staff which has been 53+ is coming down to 51 with this splendid additions.

The outlook for RRBs in the Indian financial system is bright as they have come to occupy the attention of regulators and

policymakers alike in recent times. Dr. K.C. Chakravarthi Committee's recommendations, accepted by the

Government of India, have far reaching impact on them. RRBs are being brought within the internationally accepted

framework of Basel-I norms and proactive measures were suggested to make the RRBs more vibrant and professional.

To inject professionalism and competitive spirit in the functioning of RRBs, they have been permitted to pay dividend

to Share holders with effect from 1.4.2013, which will increase the stake holders interest in the RRBs. Massive

promotional avenues have been opened up through Thorat Committee Recommendations and the Bank is geared to

complete the man power planning be it recruitments from the market or internal promotions.

The RRB structure in Indian banking scenario in general and rural credit delivery system in particular has deepened

with the GOI and RBI stipulating adoption of Core Banking Solutions Technology in all RRBs, which can virtually

facilitate RRBs to hook to any other financial and banking networks in India to accentuate its presence in Indian banking

and financial system. Leading technology providers like TCS, Infosys have provided CBS solutions to RRBs unlike in the

past where RRBs used to outsource technology from small ticket companies. RRBs can synergise with Sponsor Banks in

sharing technology and offer co-branded tech-enabled banking services.

RRBs are shedding their old skin to do the functions of a normal Commercial Bank, within the rules and regulations

stipulated by RBI.

RRBs were subject to quite a number of limitations in the past, prior to amalgamation, in terms of area of operation,

limited opportunities for diversification of business, human resources base, technology adoption, demographic profile

of clientele, a niche market etc., with limited option to scale up or scale down banking operations depending upon the

market requirements. Some of these barriers have already been broken with structural changes, while it is time for ndthe Bank to follow robust and sophisticated banking practices. RRBs are commercial banks in nature, included in 2

Schedule of RBI Act 1934 and they have come of age to truly become commercial banks in character and fulfill its

mandate effectively in serving the rural poor, especially micro- entrepreneurs, in the agricultural and non-farm

sectors.

There is no dearth of banking business potential in rural areas. It is a fact and widely gets reported in media that

banking facilities are lacking in rural areas and villages. Statistics reveal that of around 6 Lakh villages in India, only

10% have access to banking services, giving scope for abundant business potential. Banking majors have been

targeting the rural areas for exploiting the potential. Having been in the rural space for the last thirty five years, we

have edge over others who are now entering the markets. There would not have been a better time for RRBs than now,

to change its face and build strong banking institutions.

The theme of BANCON 2010 i.e., “Transform to Outperform” is apt to be a tagline to the Bank.

In retrospection, the RRBs can be termed as victim of circumstances. When the agriculture and rural sectors were in

13

we are with you!Annual Report 2010-11

dire need of institutional financial support, with the commercial banks and cooperatives not being able to penetrate

and do the job and money lenders thriving on the rural poverty, RRBs were made to take birth and go there. They drove

the money lender out, atleast partially, if not fully and played a very key role in financing agriculture and rural

development. RRBs acted as instruments in the hands of Government in their direct attack on rural poverty. Wherever

RRBs have existed, the people have had the banking facilities and financial support, irrespective of the quality of the

other dimension of banking i.e., repayment of loans, by virtue of various policies. RRBs suffered in the process, by

accumulating losses – a change of place for poverty. This was not an un-anticipated phenomenon, going by a remark

contained in a report issued by the Narasimham Committee in 1976, which stated that “any losses incurred by the RRBs

would be a price worth paying, given the social benefits that would be attained”. The RRBs indeed have caused social /

moral benefits to accrue in rural areas by covering vast geographical area.

In the subsequent phase in this process, RRBs witnessed visible changes in the approach of policy makers, impacting

the RRB, injecting the sense of sustainability and viability as an Institution – capital infusion, restructuring,

deregulation of interest rates, revision of priority sector norms on par with other commercial banks, recommending

implementation of CBS, proposed introduction of Basel norms etc., all point to a direction to the RRBs to change for the

better and be one among the many players competing for rural pie.

Over a period, technology has arrived and demographic profile has changed in the rural areas and there are more

players to bank on the unbanked. Added to it, ICT solutions and BC model of branchless banking is going to increase the

number of players more, forcing RRBs to compete for the business. The mandate and objectives have not changed but

rules of the game did change.

Let me conclude by hoping that the Bank will be resilient to meet the challenges posed by the changing environment,

capitalise on the opportunities and emerge as the strongest of all RRB s in the Country.

Yours sincerely,

K. Lakshmana RaoChairman

14

we are with you!Annual Report 2010-11

Executives speak...

Shri N. RameshGeneral Manager (Credit)

The Bank's advances grew by 26%, which is the highest ever growth in any year

after amalgamation in 2006. The Bank is playing major role in implementation of

Annual Action Plan in the eight districts of our area of operation. The Bank has

started Financial Inclusion Project in four districts of the State and the process of

identification of BCs and BFs and issue of Smart Cards is in progress. We are

hopeful of covering all villages with population of over 2000 allotted to the Bank,

to serve the poorest of the poor at their doorsteps, by offering various services like

GOAP EBT, apart from introducing Bank's deposit and other products.

Growing NPAs is a major cause of concern to all of us, which have increased mainly due to non recovery of

crop loans issued during 2007-08 due to the negative impact developed in the minds of good farmers after

the implementation of Agriculturl Debt waiver / Debt relief scheme by Govt. of India during the year

2008.However, we are hopeful of regularizing the position during the next FY 2011-12 by intensifying the

recovery efforts from the beginning of the year itself.

15

Shri K. SolomonGeneral Manager (Operations)

The Bank could fulfill all its statutory requirements during the year viz.,

CRR, SLR, CAR etc., and made a huge difference in funds management,

resulting in maintenance of fine cash balances and increased profitability.

It is heartening that the Bank posted highest profit during the year,

increasing the efficiency levels year after year.

The Bank with its meager resources during the year, is able to generate

the income for the individual rural customers, increase their purchasing

capacity, empowering a large number of women financially and could provide inclusive

banking to the rural masses who cannot afford the banking services, through low/no-cost

innovative technology thus was able to not only benefit farmers immensely, but the bank was

even posted an increased income over the last year through the dedicated and committed

staff although handicapped by their age profile and financial constraints.

we are with you!Annual Report 2010-11

The year 2010-11 is of great importance in the Bank's history with

various initiatives taken in HR front. The Bank has recruited 163

Office Assistants and initiated measures for recruitment of another

193 Office Assistants and 73 Officers, apart from promotions in all

cadres as per Thorat Committee norms and categorization of

Branches, which includes 23 Scale-IV Promotions. The Bank is

contemplating recruitment of Staff in all cadres during the next

Financial year 2011-12, in terms of Thorat Committee manpower

norms and to meet the gap caused on account of mass retirements

in the Bank.

Leveraging Technology - The entire banking industry has adopted

technology to increase operational efficiency and superior customer

service. So has APGVB, the first RRB in the country with 500+

Branches to achieve full-fledged Core Banking Solutions in its

operations. The adoption of technology would enable the Bank to

improve financial analysis capability, minimize transaction cost,

focus more on marketing the Bank's products and services. The

Bank has a challenging task of sensitizing staff in all cadres to derive

maximum benefits from the CBS environment.

Shri P.A.S. Sudhakar RaoGeneral Manager (HR)

Further, setting up of Bank's own Staff Learning Centre, fully equipped with computer lab,

residential accommodation with own faculty, is a milestone in Bank's history. The Bank is

designing a unique personality development programme by name “Vikas Patham” through SLC.

The capacity utilization was more than 80%. The Bank has taken various Staff Welfare

thMeasures including Group Mediclaim Policy for Staff, implementation of salary revision as per 9

Bipartite Settlement and payment of arrears.

The Bank is also taking steps to introduce value added services like RGTS/NEFT, anywhere

Banking and co-branded ATM Services to meet the requirement of new generation customers.

Shri M. Krishna RaoGeneral Manager (IT)

Executives speak...

16

we are with you!Annual Report 2010-11

BOARD OF

DIRECTORS' REPORT

2010 - 11

BOARD OF DIRECTORS' REPORT: 2010 - 11

Business growth

thWe have pleasure in presenting the 6 Annual Report of Andhra Pradesh Grameena Vikas Bank (APGVB) together with

the Audited Statement of Accounts, Auditors' Report and the report on business and operations of the Bank for the

financial year ended 31 March 2011.

The fiscal 2010-11 has been eventful with many milestones created. The Bank has registered a growth of Rs 2012 Crore

in total business vis-à-vis the business growth of Rs 979 Crore during last financial year. When APGVB was formed by

amalgamation of five erstwhile RRBs on 31.3.2006, the total business as on that date was Rs 4001 Crore – a level

achieved by erstwhile RRBs over three decades, while more than half of it, has been achieved in a single year. Viewed

differently, the total business growth achieved from 1.4.2006 to 31.3.2010 was Rs 3676, 55% of which was achieved in

one year i.e., in 2010-11, which is a remarkable achievement by any standard.

For an RRB, in addition to profitability, volumes matter most, which directly is a measure of banking activity in “rural

areas”. Increasing rural savings and impacting economic activity in rural areas by lending, each to the tune of around

Rs 1000 Crore, is fairly gratifying facet of the Bank's performance.

The Bank has registered a business level of Rs 9689 Crore as on 31.3.2011 with a growth rate of 26% over March 2010

level of Rs 7677 Crore.

The deposits have reached a level of Rs 4794.72 as at the end of Mar 2011, vis-à-vis Rs 3807 as on 31.3.2010, registering

a growth of 26%.

Advances registered a growth of 26% during the year with a total outstanding of Rs 4894.43 Crore over March 2010 level

of Rs 3870 Crore.

(Rs in Crores)

9689

7677

6698

5635

4813

0

2000

4000

6000

8000

10000

12000

2006-07 2007-08 2008-09 2009-10 2010-11

2718 29343394 3807

479548943870

330427012095

19

we are with you!Annual Report 2010-11

Profitability

The Bank's operating profit (before provisions) has

increased by Rs 35 Crore to reach Rs 206 Crore

during the year, as against the previous year's Rs 171

Crore. The Bank posted a net profit of Rs 108.13

Crore during the year as against Rs 89.87 Crore for

the year 2009-10. The growth in net profit has been

shadowed by the huge provisions made towards

NPAs and agricultural loans during this year.

Income and Expenditure

Particulars 2010-11 2009-10

Interest Income 642.98 577.39

Interest Expenditure 357.29 326.00

Non-Interest Income 75.07 44.52

Non-Interest Expenditure 155.12 135.72

Provisions written back 0 (-)10.94

Gross Profit/Operating profit 205.64 171.13

Taxes 48.35 45.42

Provisions and Contingencies 49.16 22.87

Provision for Salary hike 12.74*

Previous year's taxes 23

Net Profit 108.13 89.87

*To the extent of provisions made during the year 2009-10, on account of revision of salary, the operating expenditure

has increased by Rs 14 Crore on account of Salary Payments during the year 2010-11, offsetting extra charge to the

previous year's profit.

Net Interest Income

During the year, the Bank has recorded a growth of Rs 65.59 Crore (11.36%) in Interest Income from Rs 577.40 crore in

the year 2009-10 to Rs 642.99 crore, as against the Interest expenses which grew by 9.6% from Rs 326 Crore during the

financial year 2009-10 to Rs 357.29 crore during the year 2010-11. The Bank recorded a Net Interest Income of

Rs 285.70 Crore during the year as against Rs 251.40 Crore during 2009-10 with a growth of Rs 34.30 Crore.

11.8

36.95

69.27

103 108120

100

80

60

40

20

0

2006-07 2007-08 2008-09 2009-10 2010-11

20

we are with you!Annual Report 2010-11

Interest earned on advances has gone up by

Rs 87.43 Crore (20.41%) to reach Rs 515.76 Crore

from Rs 428.33 crore. The growth in interest on

advances was higher at Rs108.62 during 2009-10.

Interest income from Investments rose by 27.82%

to reach Rs 82.16 Crore from Rs 64.28 Crore during

the year 2009-10.

Interest expenditure on deposits registered a

moderate growth of 6.98% as against 25.12% in the

year 2009-10. The interest expenditure on

deposits was Rs 227.47 Crore as against Rs 212.63

Crore in the previous year. This is due to the major

share of Demand Deposits with lower interest

rates, in the total deposits growth at 70%.

Interest expenditure on borrowings was Rs 124.09

Crore with a growth of Rs 16.36 Crore (at 15.19%).

The growth of 15.19% is moderate vis-à-vis the previous year's growth at 19.26%.

The year 2010-11 witnessed moderate increase in net interest income and drastic decrease in net interest expenditure

– which is due to higher growth of demand deposits vis-à-vis term deposits.

(Rs in Lakhs)

Other Income

The component of Other Income has reached

to Rs 75.06 Crore with a remarkable growth

of 68.06% as against the previous year's level

of Rs 44.52 Crore. This growth has been due

to plugging of income leakage in CBS

environment, coupled with increase in

commission on account of processing charges

on advances growth of Rs 1024.68 Crore and

non-fund business including cross selling of

SBI Life products. The Bank has been No.1 in

the country among RRBs in marketing SBI Life

products for the two consecutive years.

Operating Expenditure

The total Operating expenditure during the year was Rs155.12 Crore as against Rs 135.73 Crore in the previous year

with an increase of Rs 19.39 Crore (at 14.29%). The growth is conspicuous as against the negative growth of 7.25%

during 2009-10. The two factors that propelled the Operating expenditure are the impact of wage revision th(9 Bipartite Settlement) and payment of the full-fledged monthly rentals for maintenance of CBS software and

hardware, for all branches and Regional Offices. Higher provision towards employee benefits such as Leave

Encashment and Gratuity Fund have also impacted the growth in Operating expenditure. The other overheads have

been maintained at the normal level and are under control.

21

Int Expenditure on DepositsInt Expenditure on Refinance

12931

16994

2126322747

1240910773

90337753

2008 2009 2010 20110

5000

10000

15000

20000

25000

6513 7105 6428 8216

31360 31971

4283351576

10000

20000

30000

40000

50000

60000

2008 2009 2010 20110

Int Income on AdvancesInt Income on Investments

we are with you!Annual Report 2010-11

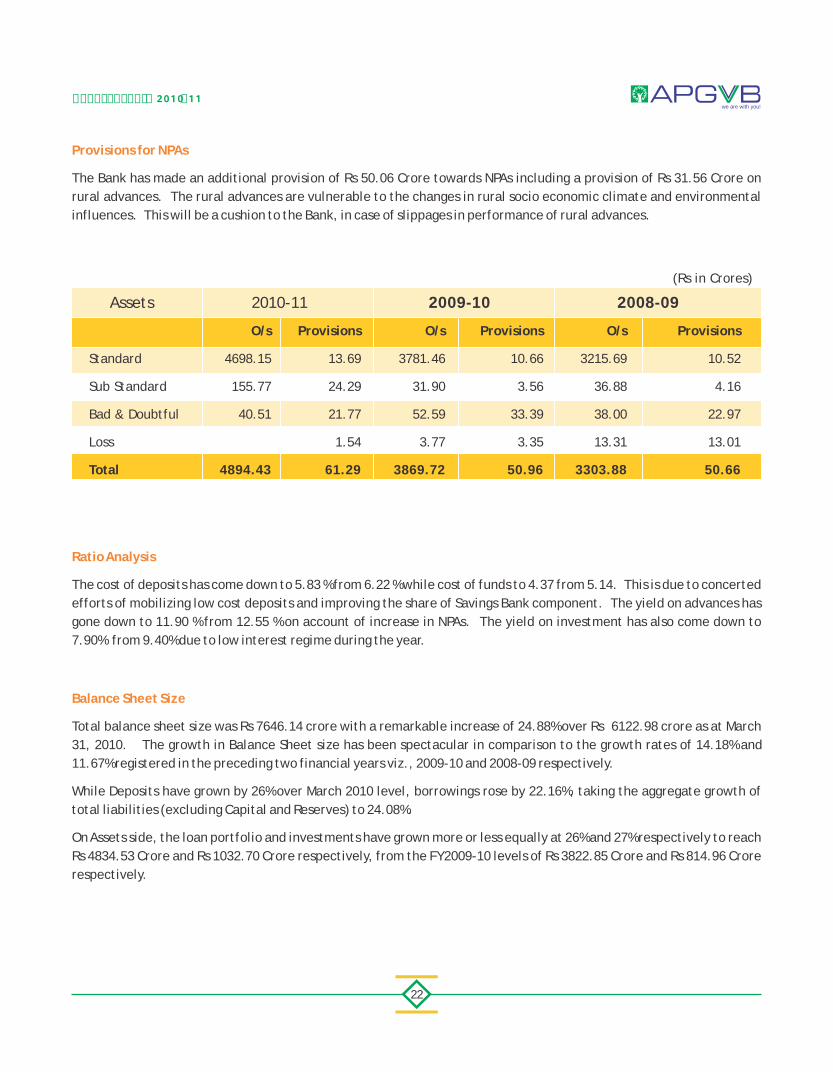

Provisions for NPAs

The Bank has made an additional provision of Rs 50.06 Crore towards NPAs including a provision of Rs 31.56 Crore on

rural advances. The rural advances are vulnerable to the changes in rural socio economic climate and environmental

influences. This will be a cushion to the Bank, in case of slippages in performance of rural advances.

Ratio Analysis

The cost of deposits has come down to 5.83 % from 6.22 % while cost of funds to 4.37 from 5.14. This is due to concerted

efforts of mobilizing low cost deposits and improving the share of Savings Bank component. The yield on advances has

gone down to 11.90 % from 12.55 % on account of increase in NPAs. The yield on investment has also come down to

7.90% from 9.40% due to low interest regime during the year.

Balance Sheet Size

Total balance sheet size was Rs 7646.14 crore with a remarkable increase of 24.88% over Rs 6122.98 crore as at March

31, 2010. The growth in Balance Sheet size has been spectacular in comparison to the growth rates of 14.18% and

11.67% registered in the preceding two financial years viz., 2009-10 and 2008-09 respectively.

While Deposits have grown by 26% over March 2010 level, borrowings rose by 22.16%, taking the aggregate growth of

total liabilities (excluding Capital and Reserves) to 24.08%.

On Assets side, the loan portfolio and investments have grown more or less equally at 26% and 27% respectively to reach

Rs 4834.53 Crore and Rs 1032.70 Crore respectively, from the FY2009-10 levels of Rs 3822.85 Crore and Rs 814.96 Crore

respectively.

Assets

O/s Provisions O/s Provisions O/s Provisions

Standard 4698.15 13.69 3781.46 10.66 3215.69 10.52

Sub Standard 155.77 24.29 31.90 3.56 36.88 4.16

Bad & Doubtful 40.51 21.77 52.59 33.39 38.00 22.97

Loss 1.54 3.77 3.35 13.31 13.01

Total 4894.43 61.29 3869.72 50.96 3303.88 50.66

2008-092009-102010-11

(Rs in Crores)

22

we are with you!Annual Report 2010-11

Liabilities

Tier-I and Tier-II Capital

The Bank's authorized and paid up capital continued to be Rs 5 Crore comprising of 5 Lakh shares of Rs 100 each,

subscribed by Government of India, Government of Andhra Pradesh and State Bank of India in the ratio of 50 : 15 : 35.

The Bank has a Share Capital Deposit amount of Rs 89.08 Crores, subscribed by the promoters in the same ratio, in the

pre-amalgamation stage of RRBs i.e., in 1996-97, as a measure of capital infusion for strengthening the balance sheets.

The building up of Reserves and Surplus has been steady, strengthening the Bank's Balance Sheet year after year,

although the rate of accretion to the Fund has been moderating. The Reserves and Surplus has increased by 34.78% to

Rs 419.01 Crore over Rs 310.89 Crore as on 31.3.2010, indicative of the Bank's sustained earnings and steady forward

moving on the path of sustainability.

23

Assets Liabilities (Rs in Crores)

151.74

221.01

310.89

419.01

0

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011

Reserves

(Rs in Crores)

Deposits4795,62%

Borrowings,1955,26%

Others,384, 5%

Capital &Reserves513, 7%

Investments1033, 14%

Advamces4835,63%

Cash withBanks, 1637

21%

Fixed & OtherAssets, 142,

2%

we are with you!Annual Report 2010-11

The following table gives the position of Tier-I, Tier-II capital, Reserves and computation of CAR.

Capital 2010-11 2009-10

a. Paid up Capital 5.00 5.00

b. Share Capital Deposit 89.08 89.08

c. Statutory Reserves & Surplus 85.13 63.51

d. Capital Reserves 0.01 0.01

e. Other Reserves 14.31 14.31

f. Surplus in P&L 319.55 233.04

Total Tier-I Capital 513.09 404.97

a. Undisclosed Reserves - -

b. Revaluation Reserves - -

c. General Provisions & Reserves 71.33

d. Investment fluctuations Reserves / Fund - -

Total Tier-II Capital 71.33

Grand Total (Tier I + Tier II) 584.43

3. a. Adjusted value of funded risk assets i.e., balance sheet items 4838.75

b. Adjusted value of non-funded risk assets i.e., balance sheet items 0

c. a+b 4838.75

d. Percentage of Capital (Tier-I + Tier II) to Risk Weighted Assets 11.85 11.22

1. Tier-I

2. Tier-II

The Bank has achieved a healthy Capital to Risk-weighted Asset Ratio (Capital Adequacy Ratio) of 11.85% calculated as

per RBI guidelines. The CAR has been on upward movement increasing from 10.67% in FY 2008-09 to 11.22% in 2009-10

and further to 11.85%.

The Bank's CAR is well above the levels envisaged to be achieved by RRBs, by Dr. K.C. Chakravarthi Committee st stRecommendations i.e., 7% by 31 March 2011 and atleast 9% from 31 March 2012 onwards.

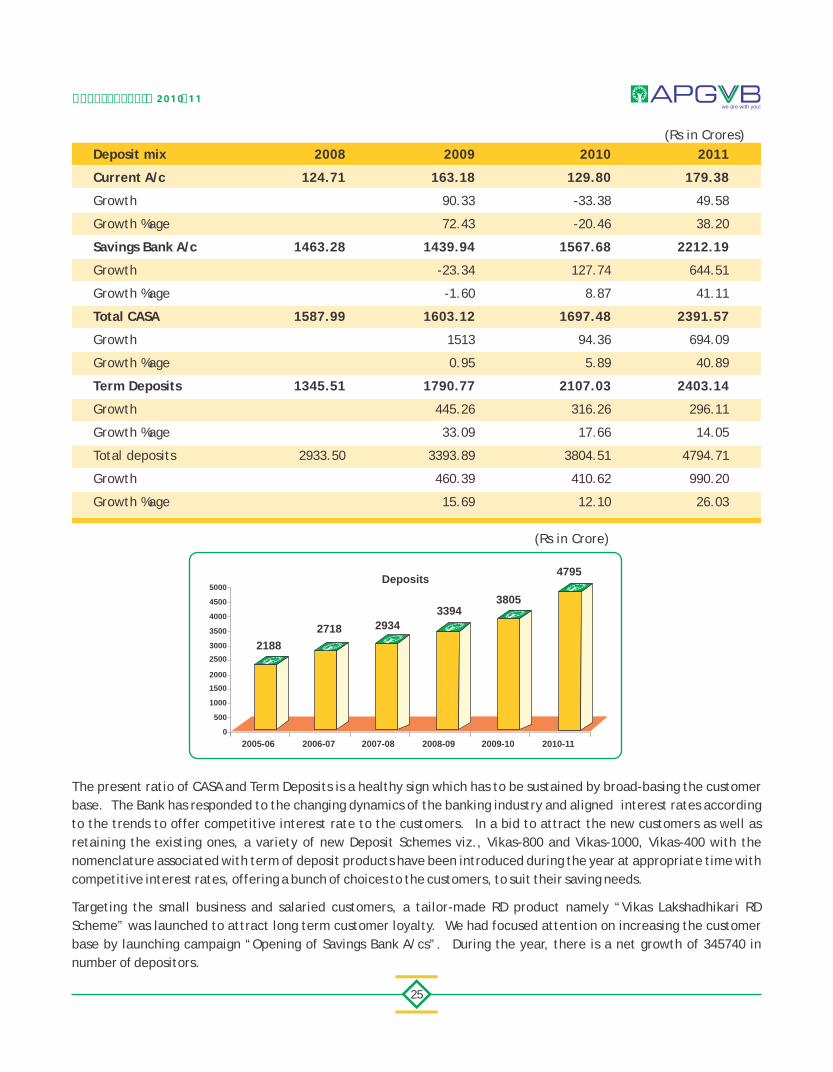

Deposits

Total Deposits of the Bank as at the end of March 2011 was Rs 4794.72 Crore with a growth of Rs 990.20 Crore at 26.03%

as against Rs 3804.51 Crore as on 31.3.2010. Savings Bank Deposits have grown by 41.11% to Rs 2212.19 Crore and

Current Account by 38.20% to Rs 179.38 Crore from their respective levels of Rs 1567.68 Crore and Rs 129.80 Crore as on

31.3.2010. Term Deposits grew relatively at a lower rate of 14.05% to Rs 2403.14 from its previous year's level of

Rs 2107.03 Crore. The share of CASA Deposits is exactly 50% of the total deposits as against its share of 45% in

FY2009-10, on account of which Cost of Deposits has come down to 5.83% from its previous year's level 6.22%. This has

contributed to the profitability of the Bank.

23

(Rs in Crores)

we are with you!Annual Report 2010-11

Deposit mix 2008 2009 2010 2011

Current A/c 124.71 163.18 129.80 179.38

Growth 90.33 -33.38 49.58

Growth %age 72.43 -20.46 38.20

Savings Bank A/c 1463.28 1439.94 1567.68 2212.19

Growth -23.34 127.74 644.51

Growth %age -1.60 8.87 41.11

Total CASA 1587.99 1603.12 1697.48 2391.57

Growth 1513 94.36 694.09

Growth %age 0.95 5.89 40.89

Term Deposits 1345.51 1790.77 2107.03 2403.14

Growth 445.26 316.26 296.11

Growth %age 33.09 17.66 14.05

Total deposits 2933.50 3393.89 3804.51 4794.71

Growth 460.39 410.62 990.20

Growth %age 15.69 12.10 26.03

The present ratio of CASA and Term Deposits is a healthy sign which has to be sustained by broad-basing the customer

base. The Bank has responded to the changing dynamics of the banking industry and aligned interest rates according

to the trends to offer competitive interest rate to the customers. In a bid to attract the new customers as well as

retaining the existing ones, a variety of new Deposit Schemes viz., Vikas-800 and Vikas-1000, Vikas-400 with the

nomenclature associated with term of deposit products have been introduced during the year at appropriate time with

competitive interest rates, offering a bunch of choices to the customers, to suit their saving needs.

Targeting the small business and salaried customers, a tailor-made RD product namely “Vikas Lakshadhikari RD

Scheme” was launched to attract long term customer loyalty. We had focused attention on increasing the customer

base by launching campaign “Opening of Savings Bank A/cs”. During the year, there is a net growth of 345740 in

number of depositors.

25

(Rs in Crore)

2188

2718 2934

33943805

4795

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Deposits

(Rs in Crores)

we are with you!Annual Report 2010-11

As the technology goes up and commercial banks update / upgrade their technology-oriented products / services, RRBs

stand at a disadvantageous position in taking on the competition in resources mobilization and attracting new

customers. (A detailed discussion on this, appears in the Management Discussion and Analysis).

Borrowings

Borrowings is the only other variable source of funds for the Bank's operations, apart from deposits. As per laid down

policy, the Bank has access to avail refinance from State Bank of India (being Sponsor Bank) and National Bank for

Agriculture and Rural Development(NABARD) for Short Term Seasonal Agricultural Operations (Crop loans) and medium

& long term loans to Self Help Groups etc. SBI provides refinance to the extent of 60% and NABARD 30% of the loan

disbursements of crop loans (10% being own stake) while NABARD provides 100% for loans disbursed to SHGs. The

refinancing agencies lay down policy, criteria and terms & conditions for availing refinance, every year, basing on

which the Bank seeks sanction of certain credit limits for that particular year from the Board Of Directors, keeping in

view the Bank's Annual Action Plan.

During the year, the amounts borrowed as refinance from SBI & NABARD stood at Rs 718.65 Crore and Rs 1235.99 Crore

(outstanding as on 31.3.2011) respectively.

The Bank has also availed refinance from National Housing Bank towards financing rural housing to the extent of Rs 50

Crore, taking the total outstanding as on31.3.2011 to Rs 200 Cr.

The total borrowings as at the end of Mar 2011, grew by Rs 22.17% to Rs 1954.64 Crore from FY2009-10 level of Rs

1599.98.

The usual growth in borrowings is in tandem with the growth in agricultural and SHG lending.

(Rs in Crores)

Particulars 2008 2009 2010 2011

SLR Investments 568.45 621.17 758.90 999.69

Growth 52.72 137.72 240.79

Growth %age 9.28 22.17 31.73

Non SLR Investments 966.84 1086.60 903.26 1147.58

Growth 119.75 -183.34 244.32

Growth %age 12.39 -16.87 27.05

Total Investments 1535.29 1707.78 1662.16 2147.28

Growth 172.48 -45.61 485.11

Growth %age 11.23 -2.67 29.19

As on 31.3.2011, total investments of the Bank (both SLR and Non SLR) have gone up by 29.19% to 2147.28 Crore from

Rs1662.17 Crore during the FY 2009-10. The 29.19% growth in investments during 2010-11 is conspicuous vis-à-vis

negative growth of 2.67% registered during 2009-10. Significant improvements in funds management have been

brought in, which enabled Non SLR investments to grow up by 27.05% from FY09-10 level of Rs 903 Crore to Rs 1148

Crore as on 31.3.2011. The Accounts department at Head Office monitored the funds flow everyday and idle funds

Assets Investments

26

we are with you!Annual Report 2010-11

have been transferred to Head Office by Sweep facility and these funds are deployed profitably.

The Bank's investments have two channels – one for the purpose of maintaining Statutory Liquidity Ratio under Section

24 of the Banking Regulation Act in the form of Government Securities and the other with Sponsor Bank Branches in the

form of Term Deposits.

Investment of our Bank's funds is managed by Investment Committee headed by Chairman with four General Managers

(viz., Credit, Operations, HR and IT) and three Chief Managers (viz., Accounts, Planning & Credit) as members. The

Committee meets periodically to review and deploy the funds in SLR or Non SLR instruments. The actual investment in

Government securities, including selection of securities etc., is being done by Sponsor Bank's Portfolio Management

Services, Mumbai in accordance with an agreement entered into, to this effect. The premium paid in purchasing the

Government Securities, is amortised during the tenure of the investment. A sum of Rs 3.74 Crore has been amortised

during the year.

Non SLR investments at present are invested in TDRs with Sponsor Bank Branches. However, a sum of Rs 18 Crore is in

PSU bonds invested by erstwhile RRBs and Rs 15 Crore in SBI Mutual Funds invested after amalgamation, all of which will

mature by June 2013.

The investment policy approved by the Board is in conformity with the RBI guidelines and is reviewed by the Board on

half yearly basis, apart from controlling the investment decisions.

The Bank has been monitoring and following up for prompt receipt of interest due from Government Securities /

Bonds.

CRR and SLR

Credit Portfolio

The Bank has complied with the regulatory requirement of maintenance of adequate balances towards CRR and SLR.

There was no default in maintenance during the FY 2010-11. The Bank has a well-laid down system of assessing the CRR

and SLR requirements on fortnightly basis taking into account the Net Demand and Time Liabilities. The Bank has kept

Rs 283.22 cr in CRR as on 31.03.2011 while Rs 1185.03 cr in SLR.

The credit portfolio of the Bank rose by 26.46% to Rs 4834.53 Crore during the financial year ended 31.03.2011, from

the previous year's level of outstanding of Rs 3822.85 Crore. Agriculture & allied activities, housing, SME segments,

micro credit, are the areas which occupied the major share in the credit growth. With favourable monsoon, all the

districts of our Bank's area of operation received more than normal rains during the year and there has been consistent

demand for crop loans and SME segments.

27

we are with you!Annual Report 2010-11

Credit to Agriculture

The Bank has been achieving the Agricultural credit targets set by State Government through State Level Bankers

Committee. The targets of Annual Action Plans of our Bank has been the highest among all Banks in the state of Andhra

Pradesh, next only to SBI, Andhra Bank and SBH. The Bank has disbursed Rs 1443 Crore towards production credit

during the year, of which Rs 1191.27 Crores to the existing customers by way of renewals and Rs 252 Crore to cover new

farmers. The production credit disbursed during this year, is 70% more than the last year's disbursement of Rs 848 Crore

during 2009-10. The Bank has extended Rs 512.49 Crore towards investment credit during the year.

Total credit to agriculture (including a portion of SHGs) is Rs 3563.00 Crore, constituting 73% of the total loan portfolio,

as against Rs 2772.84 Crore during 2009-10.

For the year 2010-11, the Bank has accepted a total target of Rs 2281.20 Crores for financing agriculture - production

credit of Rs 1778.72 Crore and investment credit Rs 502 Crore, constituting 5.44% of the total State target of

Agriculture Credit. The Bank has achieved the target by 66.04% by covering 41096 customers.

28

Regional Office wise CD Ratio for the year 2010-11

The Bank has been consistent in credit dispensation and expanding outreach.

CD Ratio

77.0992.06 97.35

101.64 102.08

2006-07 2007-08 2008-09 2009-10 2010-110

20

40

60

80

100

120

102153151

134133

129119

110103

94

88

Total Bank

Bhadrachalam

WarangalVizinagaram

Srikakulam

Mahabubnagar

Khammam

Nalgonda

Sangareddy

Visakhapatnam

Ashoknagar

0 20 40 60 80 100 120 140 160 180

CD Ratio The Credit Deposit Ratio has been around 102 % for the last two financial years.

we are with you!Annual Report 2010-11

Kisan Credit Cards

The Bank aims at issuing Kisan Credit Cards to all eligible crop loan borrowers, providing hassle free, adequate and

timely short term credit support to the farmers for their crop production needs including purchase of inputs in a

flexible and cost effective manner. The Bank has issued new Kisan Credit Cards to 98277 borrowers with a disbursed

amount of Rs 251.67 Crore, during the year for a period of three years, taking the total Cards issued to 580846. The

total outstandings as at the end of 2010-11 was Rs 1705 Crore, included in the credit to agriculture. All KCC holders

upto the age of 70 are automatically covered under Personal Accident Insurance Scheme, during the three year card

holding period, with risk coverage of Rs 50000. The annual premium of Rs 15/- per Card is jointly borne by the Bank

Rs 10/- and the borrower Rs 5/-

Interest subvention

Self Help Groups

As per the directives of Government of India, the Bank extended 1.5% interest subvention Scheme to all crop loans

including agricultural gold loans sanctioned to the farmers upto the limit of Rs 3 Lakhs, sanctioned during Kharif and

Rabi seasons from 1.4.2010 to 31.3.2011. An amount of Rs 8.18 Crore has been passed on as interest subvention to

297172 farmers during the year. The crop loan segment has witnessed prompt repayment of Rs 83.80 Crore by 19118

farmers and the Bank as per Government of India directives, has passed on 2% interest incentive to them, amounting to

Rs 63,11,583.

The Bank has been a pioneer in promoting Self Help Groups and providing Linkage with Bank credit, with the primary

objective of empowering rural women to graduate to micro enterprises to generate income on sustainable basis. The

initiatives of the Bank, in alignment with the Government's priorities and focus, have resulted in around 2550000 rural

women, in other words that many households in rural areas, finding a solution to their economic problems by

inculcating thrift and providing adequate credit. It is a common feature in every rural branch of the Bank, on any given

day that a large number of women folk visit and transact their business with the Bank.

(No. of KCC)

572948634143

433142486448

580846

0

100000

200000

300000

400000

500000

600000

700000

2006-07 2007-08 2008-09 2009-10 2010-11

29

we are with you!Annual Report 2010-11

No.of Groups Outstanding (Rs in Crore)

The Bank has financed to 89,781 Groups with a disbursement of Rs 1169.14 Crore, including 23236 new Groups which

are credit linked during the year with a disbursement of Rs 174.27 Crore. As on 31.3.2011, the total number of groups

financed by the Bank stood at 172260 with an outstanding of Rs 1472 Crore, constituting 30.69% of total credit

portfolio. The loan outstanding balance per group has increased from Rs 0.72 Lakhs to Rs 0.85 Lakhs.

Priority Sector Lending

Priority sector lending by the Bank during the year, continued to occupy the major share of the total credit portfolio.

The total outstandings in the Priority Sector advances reached to Rs 4039 Crore as at the end of March 2011 vis-à-vis

previous year's level of Rs 3209.88 Crore, keeping pace with the growth in advances. The share of priority sector

finance in the total outstanding, continued to be around 80% since inception, which indicates the Bank's continued

thrust and commitment to priority sector lending. During the year, the Bank has disbursed Rs 2977.99 Crore to 510220

borrowers under priority sector, with agriculture sector garnering 52%, other priority sectors like SHGs, Education

Loans and Housing 43% and remaining 5% to Non farm sector.

30

SHG/HL/EL Agri. Sector

NFS (ISB)

1749.2243% 2091.66

52%

191.935%

14721164

905

606

332216

0

200

400

600

800

1000

1200

1400

1600

2006 2007 2008 2009 2010 2011

172260

161077

139708

106350

82835

60140

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

2006 2007 2008 2009 2010 2011

The Bank's contribution and commitment to the SHG movement has been on the rise year

after year as shown below.

we are with you!Annual Report 2010-11

Lending to weaker sections constitutes 80% (i.e., Rs 2382 Crore) of total priority sector disbursements of Rs 2977.99

Crore, while 38% (i.e., Rs 1141 Crore) went to women borrowers. The following table shows the outstanding of the

loans to various sections of the borrowers:

2010-11 2009-10

Sector No. of A/cs O/s No. of A/cs O/s

1. Weaker Sections 775273 3347.23 559480 2448.6

2. Women borrowers 480329 2282.12 468637 2082.62

3. Minorities 43782 194.61 38739 147.28

4. SCs/STs 211876 873.10 202744 748.00

The following table shows the outstanding credit extended to Central and State Government Sponsored Schemes as on

31.3.2011.

2010-11 2009-10

(Rs in Crore)

(Rs in Crore)

Participation in State Credit Plans

The Bank has actively participated in the State Credit Plans for promotion of agriculture and rural development. The

following table shows the level of achievement of targets allotted to the Bank:

31

Scheme No. of A/cs O/s No. of A/cs O/s

1. SC Action Plan 19876 66.72 19351 54.32

2. ST Action Plan 21326 31.91 10745 26.50

3. BC Action Plan 4976 11.77 2941 8.71

4. Rajiv Yuva Sakthi 432 4.16 341 3.26

5. Handloom Weavers Groups 2246 8.04 2211 7.67

2010-11 2009-10

Segment

1. Crop Loans 1778.72 2027.53 1736.03 1502.21

2. Total Agr & allied activities 502.48 63.59 267.87 125.28

3. NFS 167.41 89.73 143.19 123.15

4. OPS 627.04 797.15 697.69 605.45

5. Total Priority Sector 3075.66 2978.00 2842.85 2356.09

% of achievement 96 82

Target Achievement Target Achievement

APGVB Position

(Rs in Crore)

we are with you!Annual Report 2010-11

Retail Lending

The Bank's retail loans portfolio consists of Housing Loans, educational loans, mortgage loans, personal loans, demand

loans, personal gold loans and term loans in Non Farm Sector.

O/s Mar - 2010-11 O/s Mar - 2009-10

S.No Segments No of A/Cs Amount No of A/Cs Amount

1 Housing Loans 6380 205 5387 116.35

2 Mortgage Loans 4923 98 4882 89.85

3 Education Loans 4506 72 3964 56.63

4 Demand Loans 33560 129 43648 140.25

5 Non Farm Sector - Term Loan 54726 164 56900 151.51

6 Personal Loans 17156 160 16056 136.02

7 Personel Gold Loans 84142 326 79072 225.93

Total 205393 1124 209909 916.54

(Rs in Crore)

Small & Medium Enterprises and Small Business Finance

Human Resources Development

The outstanding credit to the SME & SBF stood at Rs 191.93 Crore vis-à-vis Rs 78.65 Crore as on 31.3.2010 registering a

growth of 95%. During the year, a sum of Rs 153.42 Crore has been financed to 7254 units.

During the year 2010-11, the Bank has witnessed significant developments in HR initiatives, many of which will have far

reaching impact on the future of the Organisation. Strongly believing in motivating the staff at every available

opportunity and enhancing the efficiency levels, APGVB has adopted a very proactive approach in promoting career

progression to employees at all levels. The Bank is passing through a phase akin to transformations in terms of human

capital, opening up huge promotional avenues and career growth opportunities. There was embargo on recruitments

of staff from early 1990s and the Bank somehow managed to cope up with the business growth manifold with the

existing personnel. The staff who joined the erstwhile RRBs between 1976 and 1980 has reached the superannuation

stage now, retiring en-masse in lots every month, creating vacuum at managerial level. This has created promotional

and recruitment opportunities in the Bank in a big way. This juncture has coincided with the notification of Regional

32

2010-11 2009-10

Segment

1. Crop Loans 26261.00 30229.00 23500.00 24845.00

2. Total Agr & allied activities 11574.00 17701.00 9000.00 12728.00

3. NFS 8150.00 11051.00 8000.00 7148.00

4. OPS 15700.00 13897.00 15000.00 12200.00

5. Total Priority Sector 61685.00 72878.00 55500.00 56921.00

% of achievement 118 102

Target Achievement Target Achievement

State Position

(Rs in Crore)

we are with you!Annual Report 2010-11

Rural Banks (Appointment and Promotion of Officers and Employees) Rules, 2010 in July 2010, as per the

recommendations of Amresh Kumar Committee accepted by Government of India, preceded by implementation of

Thorat Committee Recommendations on Comprehensive Manpower Policy, to pave way for quick career growth to the

existing as well newly recruited employees.

The Thorat Committee norms accorded scope for career prospects to RRB employees upto Scale-V grade, prior to which

Officer Scale-III was the highest level an RRB cadre could reach. The Bank had taken early initiatives, first in the

country among RRBs to be precise, to implement the Thorat Committee recommendations / norms in terms of re-

engineering administrative set up by creating Regional Offices to be headed by Scale-IV RRB cadre and categorization

of Branches as per new business norms, in 2008-09 itself. Since the new Appointment and Promotion Rules were thawaited, senior Scale-III Officers were made to officiate the Scale-IV positions till 18 December 2010, on which 23

candidates have been promoted to Scale-IV grade to fill up the following Scale-IV vacancies:

Promotions to Officers Senior Management Grade (Scale-IV)

1. Regional Managers 10

2. Heads of Departments at Head Office including three specialized areas viz.,

Training Centre, NPAs Management and IT Cell. 10

3. Scale-IV Branches 3

Total 23

This initiative is in conformity with the broad policy concept, envisaged by various Committees, of allowing RRBs to

govern and manage themselves, rationalizing the number of officials on deputation to RRBs from Sponsor Bank.

The Bank has also taken up the exercise of promotions to staff at all levels, as under, as per manpower requirement

arrived at based on categorization of Branches and vacancies created by gradual retirements, resignations, natural

wastages etc., as on 31.3.2010.

Promotions in other grades

No.

1. Office Attendants (Messenger) to Office Assistants (Clerical) 114

2. Office Assistants to Officer Scale-I (Asst. Manager) 219

3. Officer Scale-I (Asst. Manager) to Officer Scale-II (Manager) 305

4. Officer Scale-II (Manager) to Officer Scale-III (Senior Manager) 78

Total 716

Pre-promotion training has been imparted with sufficient reading material to all SC/ST staff members, who appeared

for promotion tests in all cadres to make them perform better in the written tests.

Nearly 40 % of the total staff (excluding new recruits) has been promoted to next higher grade during the year, highest

ever in the history of APGVB.

All the above initiatives and drive, which were much-awaited well over two decades, by the respective personnel,

have enhanced the self-esteem and motivation levels among staff, which, the Bank expects, will translate into

cognizable and quantifiable performance results.

33

we are with you!Annual Report 2010-11

Recruitments

Second leg of recruitments, after implementation of Thorat Committee norms, have been completed in Group B Grade

(Office Assistants) during the year. The process of recruitment of 163 Office Assistants was carried out through IBPS,

Mumbai, taking the cumulative figure of new Office Assistants recruited to 313.

The Bank has ensured statutory requirement of providing pre-examination training to the SC/ST candidates who

applied for the written test, by availing the services of professional retired Bankers in Hyderabad.

The number of candidates enrolling online, for written test, ran into tens of thousands, which created a huge

awareness about the Bank in the general public (non-clientele of the Bank). Certain vernacular news papers have

carried out large and noticeable headlines in their career /employment opportunities, guiding the prospective

employees of the Bank about written tests. The Bank has carved a niche with a strong brand image and emerged as a

conspicuous institution.

As on 31.3.2011, the total number of staff and composition is as under:

1. Total Number of Staff 2235

2. Of which

a) Officers

i) Chief Managers (Scale-IV) 23

ii) Senior Managers (Scale-III) 93

iii) Managers (Scale-II) 481

iv) Managers (Scale-I) 701 1298

b) Office Assistants 759

c) Office Attendants 178

2235

3. No. of SC / ST employees 348

4. No. of women staff. 248

From 1922 staff members (excluding new recruits), 439 staff members in various cadres, are retiring in ensuing three

years i.e., by March 2014.

Staff Learning Centre

The year 2010-11 has been significant in the history of APGVB on account of one more milestone created by establishing

Bank's own Staff Learning Centre in Warangal. Some 20 years ago, State Bank of India had an exclusive Training

Institute in Khammam, to cater to the training needs of employees of RRBs sponsored by it, which was subsequently

wound up. Since then the training needs of the staff, pre and post amalgamation, are met by availing the training

facilities in far off places like BIRD(Lucknow), CAB(Pune), NABARD, BIRD(Mangalore), SBLCs of Sponsor Bank, etc.,

34

we are with you!Annual Report 2010-11

which resulted in inadequate / lack of training to majority staff. Added to this, these training programmes were

primarily meant for Officers, leaving out the Clerical and Subordinate Staff.

Following the encouragement / initiatives in the policy documents, recommendations of the various Committees,

constituted by Government of India/NABARD, the Bank had taken a bold step to create its own training infrastructure.

There could not have been a more appropriate time to do this, with the continuous recruitments and promotions on the

cards, which need training and handholding of staff to take on their new roles.

Adoption of Core Banking Solutions in all banking operations from November 2009, has made it imperative for

continuous training – basics of computers, orientation, re-orientation, enhancing the skills on technology aspects. All

the staff of the Bank needed the training as CBS is new concept to every one. Accordingly, we have established a full-

fledged Staff Learning Centre at Warangal on 09.07.2010. There is a CBS laboratory at Staff Learning Centre to take

care of the CBS training needs of staff. NPA tracking has been introduced in the Bank in CBS in January 2011 and

necessary basic skills have been imparted to the Field Supervisors to control and contain NPA s.

The Staff Learning Centre has two air conditioned Lecture halls, one for General Sessions and another for Core Banking

Solutions (Computer Lab). There are 14 well furnished Hostel Rooms, which can accommodate 30 participants, a

Library, Dining hall with Kitchen. Entertainment facilities like TV, Indoor games, are taken care of. Medical services

are also made available by engaging the services of a Physician and a Cardiologist. Round the clock Security is also

provided to the Staff Learning Centre by hiring a Security Agency. One Administrative Officer is posted to look after the

management and maintenance of the Centre.

A team of senior officials from within the bank was drawn as Faculty from a group of officials who opted for the

assignment. Course contents of the Programmes and methodologies are designed in accordance with the emerging

needs. A module on behavioral sciences is included in every training programme, by outsourcing the faculty to refresh

the participants with regard to their attitude, self-help methods for personal life improvement and career growth.

thSince 09 July, 2010, our Staff Learning Centre has conducted 42 programmes up to 31.03.2011 on various subjects and

trained 994 employees/officials of all cadres with a Capacity Utilization of 86%. A system of feed back from

participants has been introduced to give their feedback / suggestions, not only on the training programme but also on

general issues pertaining to the Bank.

An offshoot of the Staff Learning Centre has been the opportunity for the top management of the Bank viz., Chairman

and General Managers to reach out and interact with the Staff members, either at the inaugural or valedictory session

to share the Bank's priorities and concerns.

Vikas Patham

APGVBSLC is developing a capsule programme, on personality development, primarily aimed at sensibly touching the

very basic elements of human nature and perception. This is being so designed with inspirational and motivational

contents compiled from various sources. Paradigm shift in perceiving the things, removing mental blocks, overcoming

fear of failure, continuous learning, need for change etc., are a few aspects that the staff will be exposed to. At the

end of the programme, it is expected that the staff will stop, think and retrospect on the basic values. The inspiration

for designing such a programme is derived from State Bank of India's Parivartan programme. However, motive and

contents are different from that of Parivartan. In the next financial year, the Bank is going to ensure that all staff

members undergo this capsule programme.

35

we are with you!Annual Report 2010-11

HRMS

Staff Welfare Measures

The amalgamation had posed many challenges in integrating the data on HR front. Till 31.3.2010, the Payment of

Salary and Allowances to staff were being paid at Regional Office level, which was centralised at Head Office level wef

April 2010, by merging the data. This exercise has greatly reduced the man hours required previously for preparation

and posting of transactions in respect of payment of salary and posting of instalments to staff loan accounts, leveraging

the CBS technology. The data pertaining to the Staff in respect of their bio-data, promotions, postings etc., have been

digitalized and required reports are generated for MIS purpose.

thIn accordance with the Government of India instructions, the Bank has implemented the Wage Revision as per 9

Bipartite Settlement in the month of August 2010, with effect from 01.11.2007. The arrears accrued upto August 2010

to the extent of Rs 32.00 Crore has been worked out and paid in the month of September 2010. This exercise has been

completed within a month to comply with the GOI instructions.

The Bank has fully provided for the liabilities on account of superannuation viz., Gratuity and Leave Encashment as per

actuarial assessment. The additional provisions made during the year are Rs 3.69 Crore and Rs 5.26 Crore respectively.

The closing balance in the corpus is Rs 161.92 Crore as on 31st March 2011.

The Bank has maintained cordial relations with the Officers Association and Employees Union and working/moving with

great coordination towards Bank's development. The Management and Staff Association have released a joint appeal

and jointly conducted several business development meetings with the branch staff at all Regional Offices to motivate

the staff members to improve operating efficiency and productivity. The Structured Meetings with the representatives

are held at periodical intervals to sort out any issues, thereby creating excellent working atmosphere. During the year,

there was no instance of loss of any man-days on account of strike or agitation or non-cooperation in the Bank.

The Bank has maintained cordial relations with the SC/ST Welfare Association and OBC Welfare Association and

complied with statutory requirements in all aspects of recruitment, promotions etc., and redressed the grievances in

amicable and cordial manner.

The Bank has held a series of structured Meetings with the representatives of Welfare Associations and Liaison Officers

and paved the way for smooth and congenial atmosphere in the Bank.

Technology in the Banking Sector is playing a dominant role in driving down costs, building efficiency and working as an

enabler in achieving business growth and excellence in customer service. The Bank has achieved a major landmark by

covering all branches and offices under CBS. The entire Bank is on Core Banking Solutions platform and the new

branches are opened with CBS from the beginning. CBS has enabled the Bank in providing a wide array of tech-enabled

services to customers, such as mobile alerts and other services providing cutting edge in terms of service delivery,

product innovation and better customer service. These initiatives drive the improvement in customer service, besides

widening business opportunities. While the entire focus was on implementation of CBS in all Branches in the year 2009-

10, the current year witnessed significant improvement in stabilization of the CBS broadly in the following areas

thImplementation of 9 Bipartite Settlement

Industrial Relations

Welfare of SC/ST and OBC employees

100% Core Banking Solutions

36

we are with you!Annual Report 2010-11

• Continuous training to the operating staff to make them comfortable

• Internal Controls – cleaning of system suspense generated in intermediary accounts

at the time of implementation and during the course of day to day operations

• Plugging of income leakage - Purification of data

• Reconciliation of old Bankers Cheques Accounts and introduction of new one

• Introduction of BCGA (Office Account) and its reconciliation

• Management Information System

• New Initiatives like RTGS, NEFT, SMS Alerts

• Customer Service Initiatives such as DD Printing, Pass Book Printing etc.

• Creation of a post of Chief Manager (IT)

Training Support:

Internal Controls:

IT cell is looking after the Satellite wing of Staff Learning Center. Training is imparted to all staff

members in CBS simulated environment in Staff learning center. Orientation training on new initiatives has been

conducted to all staff members at regional Office level to ensure complete participation.

Training is also imparted to all branch auditors to understand the systems and procedures, risk involved in the changed

environment to facilitate smooth conduct of Audit and Inspection of branches.

Help Desk is being maintained by IT Cell, at Ashoknagar to extend online job support to the staff members.

The quality of improvement resulted in this area has been spectacular due to migration of branches

/ offices to 100% CBS. The speed and efficiency with which the cleaning operation of various intermediary accounts

was done is unmatched in terms of saving cost, manpower and efficiency.

· System Suspense: The system suspense Account outstanding as on 31.03.2011 is NIL. It is being monitored daily by

IT cell /Help Desk to avoid accumulation of entries. This has been a Zero tolerance area for the bank.

· Cash differences: The cash difference between Cash on hand and cash on hand in CGL at branches has been

reconciled and made nil as on 31.3.2011. Special drives have been conducted at Regional Office level to ensure

timely rectification and reconciliation of cash on hand at branches with cash in CGL of the branches as a preventive

vigilance mechanism and to prevent breed ground for frauds and malpractices.

· CBS Monitoring Registers: All the standard / prescribed registers in CBS environment have been introduced at the

branches for improving overall functioning of branches. Some of the registers are also customized to suit the

requirement of branches to comply audit compliances.

Focus on Income leakage

• Purification of data:

• Zero interest accounts:

• Zero Balance Accounts:

Purification and correction of data in respect of interest rates is completed at all branches

as on 31.3.2011. Staff members are sensitized to data perfection on ongoing basis to generate error-free MIS to

facilitate quality decision making management.

Accounts with zero interest rates were segregated branch wise and taken up the matter

with respective branches to ensure against income leakage to improve the profitability of the Bank.

Zero balance accounts were taken up with respective branches for the closure of

accounts to ensure against spillage of income and to prevent frauds.

37

we are with you!Annual Report 2010-11

Reconciliation of old Bankers Cheques (Demand Draft) Account:

Branch Clearing General Account (Office Account):

Management Information System:

Bankers Cheque Accounts maintained by erstwhile

RRBs and continued after amalgamation, have been frozen at a cut off date(30th April 2011) and a new system of

issuing Drafts /Bch s on continuous security forms has been introduced ( from 01st May 2011 )

BCGA module is introduced for transfer of funds among branches

in place of Inter Office Account which is frozen and being reconciled. Reconciliation of new BCGA is being monitored

by IT cell on daily basis.

The Bank's think-tank analysed every piece of information and report generated

under CBS to facilitate correct financial reporting and to exploit its utility. IT cell has customized all the reports for

review and monitoring of the Bank's performance to enable / draw suitable strategies to improve the business and

profitability of the Bank.

New Initiatives

Fixed Assets:

NPA tracking:

Assets and Liability Management:

Service Tax & TDS:

Signature scanning:

Bank's own website :

Disposal of old hardware:

NEFT:

Annual Closing:

Fixed Assets accounting system / computation of depreciation is carried out by IT cell during the year to

improve the error-free accounting system for statutory audit compliance.

NPA tracking module is activated during the year 2010-11 for automatic tracking of NPAs. IT cell

customized NPAs reports for better NPA management by placing the reports to branches on weekly intervals and

highlights of NPA performance daily through SMS.

Assets and liability management is being stabilized for better management of

liquidity of funds to assess interest risk and operational risk to improve the profitability and operating efficiency of the

Bank.

The Bank has centralized its service tax computation at monthly intervals to avoid the delay in

payment of Tax. The Bank has taken steps to activate Tax deduction at source module from 01.04.2011 to comply with

statutory obligation and bring transparency in accounting system.

Scanners were provided to all branches for scanning signatures / photographs of depositors to

facilitate Non-Home transactions and improve customer service and operating efficiency to avoid frauds.

The Bank has introduced new portal of the Bank for disseminating the information about the

Bank to the general people and staff to build brand image. All the circulars and other internal developments are also

placed on web site for information of the staff only. Suggestions are also invited from customer as well as from staff for

improving the functioning of the Bank.

A Circular has been issued to all Branches to dispose off unused and old Hardware by way of

donating it to schools and SHG groups if the computer and its peripherals are fit to be used, and otherwise unused one

in open auction to be conducted at respective regional office to keep the premises neat and tidy.

NEFT facility is being introduced for improving customer service and easy flow of funds from Govt. Department

and other agencies which go long way in providing cutting edge image of the Bank in terms of service delivery..

Annual Closing returns / statement of the bank has been generated from the system for the first time

in CBS environment during the year 2010-11 and the entire process of audit and finalization of accounts is completed in

record 19 days, thus enable the branches and staff to concentrate on business development and customer service.

38

we are with you!Annual Report 2010-11

Customer Service Initiatives:

SMS Alerts-

Pass Book Printers:

Demand Draft / Bankers Cheques Printers:

Non Home Transaction Facility:

Toll Free Number :

The Bank has activated SMS alerts for timely information to the customers about the transactions

effected in their account and also about the changes in the interest rate of loan / deposit products of the Bank.

This has improved the image of the Bank and would go a long way in building trust and widening the customer base.

Pass Book Printers were supplied to all branches and to improve the customer service and also

guard against malpractices in noting the entries in passbooks.

The Bank has introduced printing of Demand Drafts/ Bankers Cheques

at all branches to improve remittance business and also to facilitate automatic reconciliation of entries .

Non Home transaction facility is extended to the customers Rs 25,000/ per day as

add-on service to the customers.

The Bank has introduced a Toll free telephone No. 1800 425 7900 for receiving the suggestions

and complaints from the customers and general public. This has helped the bank in getting the direct feedback

from the public about the functioning of the Bank.

Expansion of Outreach

Information & Communication Technology - Smart Card Project

Financial Inclusion Technology Fund (FITF)

While the concept of RRBs coupled with nationalization of Banks itself was one of the biggest initiatives of Government

of India towards inclusive banking and inclusive growth, the Bank's latest IT-enabled-initiatives date back to 2006 when