1 Annual Report and Statement of Accounts 2012/13

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Annual Report

and

Statement of Accounts

2012/13

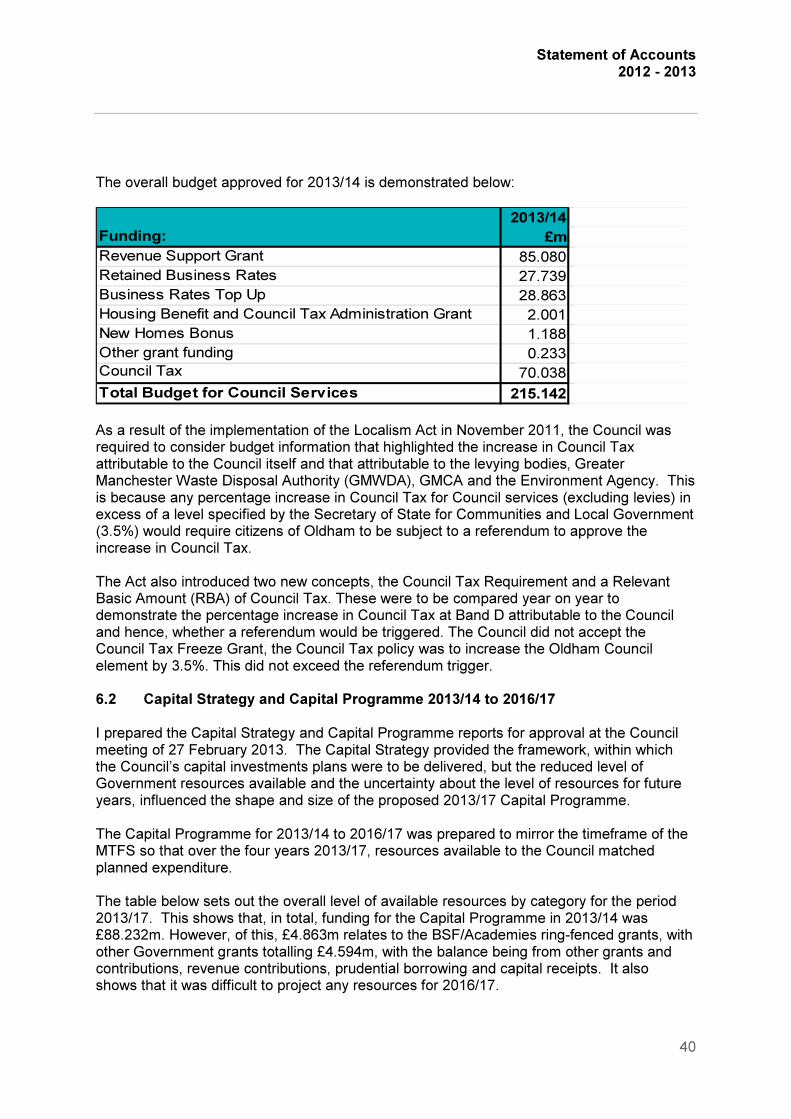

Statement of Accounts 2012 - 2013

2

________________________________________

If you require an audio, Braille, large printed or different language version of this document please contact Mel Creighton 0161 770 4251. ________________________________________

Statement of Accounts 2012 - 2013

3

Contents

Pages 1.0 Preface 5 1.1 Introduction to the 2012/13 Statement of Accounts by Councillor Abdul

Jabbar, Cabinet Member for Finance and Human Resources 5

1.2 Explanatory Foreword by the Borough Treasurer 6 2.0 Statements to the Accounts 76 2.1 Statement of Responsibilities for the Statement of Accounts 76 2.2 Auditor’s Statement 77 3.0 Core Financial Statements and Explanatory Notes 81 3.1 Movement in Reserves Statement 82 3.2 Comprehensive Income and Expenditure Statement 83 3.3 Balance Sheet 84 3.4 Cash Flow Statement 85 3.5 Index of Explanatory Notes to the Core Financial Statements 86 3.6 Explanatory Notes to the Core Financial Statements 88 4.0 Supplementary Financial Statements and Explanatory Notes 215 4.1 Housing Revenue Account (HRA) 216 4.1.1 Housing Revenue Account Income and Expenditure Account 216 4.1.2 Statement of Movement in the Housing Revenue Account 217 4.1.3 Index of Explanatory Notes to the Housing Revenue Account 219 4.1.4 Explanatory Notes to the Housing Revenue Account 220 4.2 Collection Fund 224 4.2.1 Collection Fund Income and Expenditure Account 224 4.2.2 Index of Explanatory Notes to the Collection Fund 225 4.2.3 Explanatory Notes to the Collection Fund 226

Statement of Accounts 2012 - 2013

4

Pages 5.0 Other Statements 229 5.1 Annual Governance Statement 229 5.2 Glossary of Terms 240

Statement of Accounts 2012 - 2013

5

1.0 Preface

1.1 Introduction to the 2012/2013 Statement of Accounts by Councillor Abdul Jabbar, Cabinet Member Finance, Human Resources and Strategic Partnerships

Councillor Abdul Jabbar

Welcome to Oldham Council’s Statement of Accounts for 2012/13. Oldham Council continues on its journey of recovery and improvement and there have been many significant changes over the 2012/13 financial year. This has included the approval of an additional £106m capital investment programme which will be absolutely fundamental in supporting the regeneration of the borough. This capital investment includes; Hotel Futures, significant investment in Leisure facilities across the borough, regeneration of the Old Town Hall, development to key ICT systems, Highways and Schools among other further improvements to the town centre. The revenue budget in 2012/13 delivered a net budget saving of £24.493m, this was on top of the £40m in the previous financial year. During 2012/13 I presented to Council a two year budget proposal with savings of £17.735m in 2013/14 and £12.976m 2014/15. Following the Local Government settlement announced in late 2012 it was identified that a further £7.528m was required in 2014/15, totalling £20.504m of savings required in this year. As a Co-operative Council we have continued to work closely with our District Partnerships, residents, partners and staff to identify opportunities to change the way we set priorities for spending and the way that we deliver services. Last year we continued our success in closing our accounts early and being the first Local Government body to publish their Statement of Accounts for 2011/12, on the 25 June 2012. This year has seen a further improvement in this timescale, publishing as we have on the 31 May 2013 and this is a fantastic achievement. I would like to take this opportunity to thank all of our finance and audit staff who have worked particularly hard under very challenging circumstances over the past few months in order to achieve a two year balanced budget and also to close the accounts so quickly and to such a high standard.

Statement of Accounts 2012 - 2013

6

This careful management of our finances enables us to make fully informed decisions about the appropriate use of Council resources and deliver the quality of services that residents have come to expect. Councillor Abdul Jabbar Cabinet Member for Finance, Human Resources and Strategic Partnerships

Statement of Accounts 2012 - 2013

7

1.2 Explanatory Foreword Message from the Borough Treasurer Oldham Council has continued to drive forward its financial transformation and these accounts represent a key element of that greater programme of work. The accounts were completed and handed over for external audit on the 26 April 2013 and were signed off and published on the 31 May 2013, 4 months in advance of the statutory deadline. This level of achievement is only possible because of the dedication of all the finance and internal audit staff who together form the team that continues to deliver sustained and continuous step change improvements across the whole spectrum of financial management. By delivering audited accounts in such a time frame the Council is able to report to all its stakeholders at the earliest opportunity and the resources of the service are then directed towards the fiscal challenges that face the Council for the foreseeable future. The financial standing of the Council is very robust, with a two year budget agreed, sound and improving financial management practices, a financial change programme that aims for excellence in all areas along with developing plans to address the challenges to be faced from 2015/16 and beyond.

Capitalising on the good practice now established in closing the accounts, the style and format of the accounts that has been used for 2012/13 is similar to that used last year. In my report accompanying the financial statements for the year ended 31 March 2013, I have provided an overall explanation of the Council’s financial position both during 2012/13 and into 2013/14, including information about the operation of Oldham Council as well as major influences affecting the accounts. The report is prepared in a style to enable readers to understand and interpret the accounting statements. By producing this report, I aim to give electors, local residents, Council Members, partners, stakeholders and other interested parties confidence that public money which has been received and spent, has been properly accounted for and that the financial standing of the Council is secure.

I have prepared the Explanatory Foreword so that it is structured as follows: 1. An Introduction to Oldham 2. Some Key Facts about Oldham 3. Some Key Facts about Oldham Council 4. Key Issues that Influenced the Financial Position in 2012/13 5. Key Events Affecting the Council in 2012/13 and Influencing Future Years 6. The Impact of the 2013/14 Budget Setting Process 7. Other Issues Affecting Oldham Council with an Impact in Future Years 8. Key Accounting Information for the Financial Year 2012/13 9. Receipt of Further Information 10. Acknowledgements

Steven Mair Borough Treasurer

Statement of Accounts 2012 - 2013

8

1 An Introduction to Oldham Oldham Council is one of the 10 Local Authorities in the Greater Manchester region. The Metropolitan Borough of Oldham occupies a key position between Greater Manchester and the Leeds City Region and provides a gateway to the North West and to Yorkshire and Humberside. It lies in the North East of Greater Manchester and covers an area of approximately 55 square miles (142.365km sq). It is located within the foothills of the Pennines and stretches from the Northern edge of the Peak District National Park (indeed almost a quarter of the borough is within the National Park) to the outskirts of the City of Manchester. It shares its borders with the City of Manchester, the Metropolitan Boroughs of Tameside and Rochdale and to the east, Kirklees and Calderdale. No residential location in the borough is more than two miles away from open countryside.

The borough is strategically located near the M62 and is connected to it by the A627M and the M60. The transport network has now been greatly enhanced with the Metrolink Extension connecting Oldham Mumps, Shaw and Derker to Manchester City Centre, with completion to the town centre due early 2014.

Oldham has a proud industrial heritage but, along with many towns and cities, the industries on which the wealth of the area was built have now declined. Regeneration, both in terms of employment opportunities and physical redevelopment, is recognised as being very important to the future prosperity of the borough and is a key aim of the Administration. The Council has to provide services such that it meets the needs of its citizens, serving both an urban and rural environment and this is influenced by the make up of the population, education, the economy, health and housing issues.

The Council’s ambition is to develop a co-operative future where everyone does their bit to create a confident and ambitious borough.

Oldham is part of the dynamic Sub-Region and works with partners to play a positive role in the future economic success and regeneration of Greater Manchester. The Council plays an active role in shaping the strategic direction of Greater Manchester, both in terms of its formal governance via the Greater Manchester Combined Authority, and also in relation to developing the relationship between the city region and Government. During 2012/13 Oldham Council and its partners have continued to play a key role in developing and delivering the Greater Manchester Strategy delivery plans. The year has also seen the review of the Greater Manchester Strategy which was originally approved in 2009. The revised strategy will be approved during 2013/14.

2 Some Key Facts about Oldham

I have included those key factors that readers of the Statement of Accounts would need to be aware of, in order to appreciate the issues that influence the services provided by Oldham Council. I have set these out as follows, using the most up to date statistical information:

Statement of Accounts 2012 - 2013

9

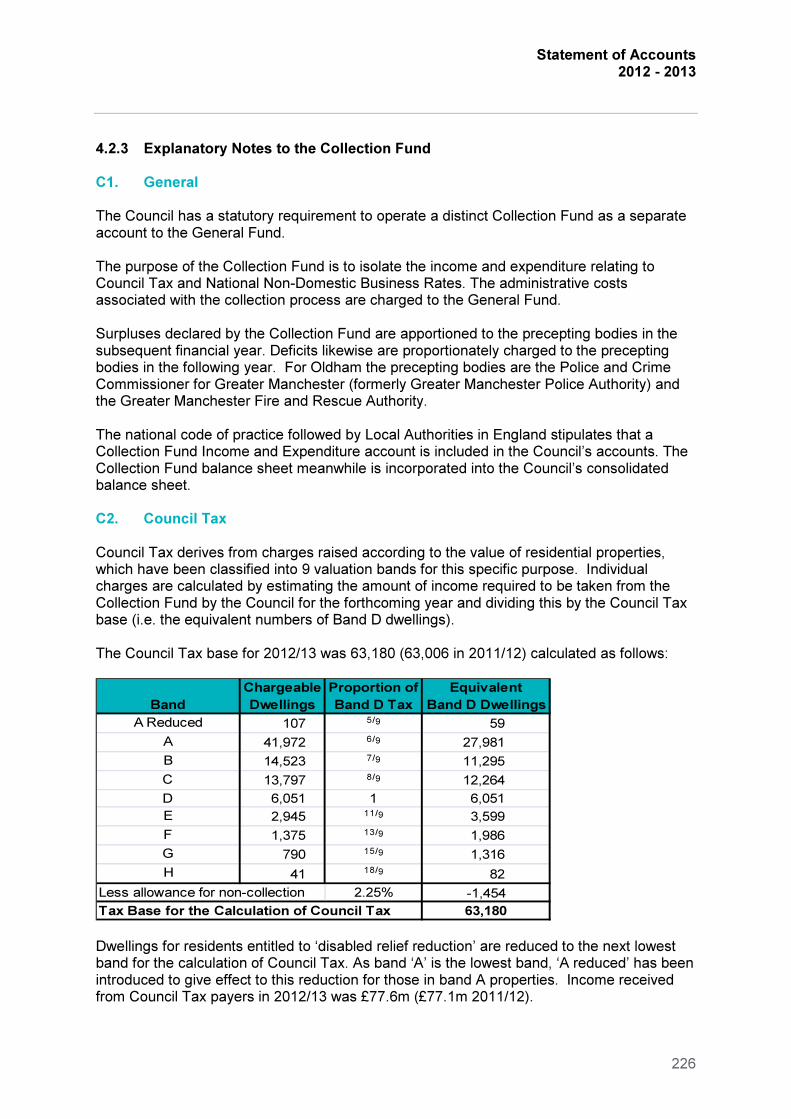

Population

Office for National Statistics Mid-Year Estimates for 2011 show that Oldham had a total estimated population of 225,200. Within Oldham’s population: � 50,400 were aged 0-15 years (22.4% of Oldham’s population); � 141,600 were aged 16-64 (62.9% of Oldham’s population); � 33,200 were aged 65 or over (14.7% of Oldham’s population).

Oldham has a relatively youthful age structure, with proportionally more people aged 0-15 years (22.4% of Oldham’s population, compared with 18.8% England-wide) and proportionally fewer people aged 65 or over (14.7% compared with 16.5% England-wide).

Oldham’s population is projected to increase to around 237,000 by 2021, with much of this growth due to projected increases in the number of people aged 65 and over.

According to the 2011 Census Population Estimates by Ethnic Group, Oldham has a higher proportion of non-white Black and Minority Ethnic (BME) residents (22.4%) than the North West (9.8%) or England (14.6%). Within Oldham’s population:

� Three in four people (75.6%) are White British; � Pakistani-heritage residents (10.2%) are the second largest group in Oldham; � Bangladeshi-heritage residents (7.4%) are the third largest group in Oldham; � Smaller proportions of Oldham residents are from mixed backgrounds (1.6%), White

Irish (0.7%), Other White (1.3%), Indian (0.7%), Other Asian (0.8%), Black African (0.7%), Black Caribbean and Other Black (0.5%), Chinese (0.3%) and Other backgrounds (0.2%).

Oldham’s population is more ethnically diverse within younger age bands.

Deprivation

According to the Indices of Deprivation 2010:

� More than one in five Oldham residents (21.4%) live in income-deprived households; � Around three in ten Oldham children aged 0-15 (30.1%) live in income-deprived

households (Income Deprivation Affecting Children Index); � More than one in five Oldham residents aged over 60 (23.4%) live in income-

deprived households (Income Deprivation Affecting Older People Index); � Five of Oldham’s twenty wards are among the 5% most income deprived wards in

England (Coldhurst, St. Mary’s, Alexandra, Werneth and Hollinwood); � Almost three in five children aged 0 to 15 (59.4%) in Coldhurst and over half (53.5%)

in St. Mary’s are living in households experiencing income deprivation; and � Almost three in five older people aged 60 and over (59.8%) in Coldhurst live in

income deprived households, as do more than two in five older people in St. Mary’s (46.3%) and Werneth (45.3%).

Statement of Accounts 2012 - 2013

10

Education

In relation to education:

� Around 21.9% of school pupils in Oldham are eligible for free school meals; � 85.8% of school children in Oldham achieved five or more GCSE grades A*-C and

55.9% of school children in Oldham achieved five or more GCSE grades A*-C including English and Maths in 2012 (national average 81.8% and 59.4% respectively).

Economy

Economic data tells us:

� The unemployment rate, (Job Seekers Allowance (JSA)), in Oldham was 5.8% in

October 2012. This was an increase of 5.1% since October 2011, and the rate in Oldham is significantly higher than the national average of 3.8%. Female unemployment had increased by 11.4% since October 2011, such that Oldham had the highest unemployment rates in Greater Manchester in October 2012.

� 5.1% of young people aged 16 to 18 in Oldham were not in education, training or employment (NEET) in October 2012 with the highest ward rates in Alexandra (8.8%) and Hollinwood (8.2%).

� The average household income in Oldham is £32,648, which is less than the Great British average of £35,990.

Housing

Housing information indicates that: � ONS survey- There are 93,025 households. Of these 89,703 households are

inhabited, of which 58,259 (64.9%) are privately-owned, 18,918 (21.1%) are social-rented, 10,944 (12.2%) are privately rented and 1,582 (1.8%) in shared ownership or others. In addition, a total of 3,322 are currently vacant.

� 17% of private homes are in poor repair and 19.8% of households are in fuel poverty. � Over 300 empty homes have been brought back into use in the last year. � The Council has reduced homelessness cases from 961 households in 2003/4 to

only 62 in 2012/13.

3 Some Key Facts about Oldham Council Oldham Council is a multifunctional and complex organisation. Its policies are directed by the Political Leadership and implemented by the Executive Management Team and officers of the Council. In the following section of my report, I present the political and management structures of the Council, the political ethos driving the policy and the agenda of the Council and the means by which these are implemented and managed. I also outline some of the key achievements that have been made by the Council over the past few years, and also highlight the development and continuing improvement in strategic financial management.

Statement of Accounts 2012 - 2013

11

3.1 The Political Structure of the Council in the 2012/13 Municipal Year

Oldham has 20 wards and the Council consists of 60 elected Members and following the local election on 3 May 2012 the political make-up of the Council was:

Labour Party 44 Councillors

Liberal Democrat Party 14 Councillors

Conservative Party 2 Councillors

As a result of the local election, the Labour Party increased their majority and remained in control, continuing with the driving ethos of a Co-operative Council.

The Council has adopted the Leader and Cabinet model as its political management structure arising from the Local Government and Public Involvement in Health Act 2007. The requirements of the Act are such that the Leader of the Council has responsibility for the appointment of Members of the Cabinet, the allocation of Portfolios and the delegation of Executive Functions.

In accordance with the Local Government Act 2000, the Cabinet is not required to be politically balanced. The Executive Portfolios were agreed at the Annual General Meeting on 23 May 2012 and a Cabinet member took responsibility for each one of these Portfolio areas. The Cabinet for 2012/13 was comprised of 8 Labour Party Members, with the following Portfolio areas:

� Strategic Projects and External Relations � Business Skills and Town Centre � Co-operatives and Community � Housing, Transport and Planning � Finance, Human Resources and Strategic Partnerships � Social Services and Community Health � Education and Safeguarding � Neighbourhoods and Devolved Services

Most decisions of the Council were delegated to the Cabinet, which met on a three weekly cycle of meetings. However, there were also meetings of all Council Members every six weeks where major policy decisions were taken such as approving the annual budget and setting the level of the Council Tax.

Cabinet Advisory Panels (CAPs) continued to meet to enable early engagement with non-Executive Members in key policy areas of the Council’s policy framework. These were not formally constituted committees but had been created to inform the Executive Members on appropriate policy issues for eventual decision making. There are five CAPs, namely:

� Housing, Transport and Regeneration � Children, Education and Leisure � Adult Care and Health � Neighbourhood Working and Co-operatives � Finance, Human Resources and Partnerships

Statement of Accounts 2012 - 2013

12

Previous overview and scrutiny arrangements remained and were still aimed at examining and providing challenge to the operation of the Council. To achieve this, scrutiny groups were made up of non-Executive Members. The Council’s Annual General Meeting on 23 May 2012 agreed that there were two bodies, as follows:

� Overview and Scrutiny Board � Performance and Value for Money Select Committee

The Council’s Audit Committee met regularly throughout 2012/13 to consider matters such as the 2011/12 Statement of Accounts, treasury management reports, internal control reports on activities within the Council’s Directorates and feedback from the external auditors. There was also a Standards Committee which met occasionally to consider the ethical agenda for the Council including the compliance with the Code of Conduct by elected Members and five Regulatory Committees, as follows:

� Licensing � Planning � Selection � Appeals � Traffic Regulation Order Panel

3.2 The Management Structure of the Council

Supporting the work of elected Members is the organisational structure of the Council headed by the Executive Management Team (EMT). This is comprised of Oldham Council’s most senior officers, the Chief Executive, the Deputy Chief Executive, three Executive Directors and the Chief of Staff. I attend meetings of the Management Team in my role as Borough Treasurer (the Section 151 Officer) together with the Borough Solicitor as the Monitoring Officer, the Director of Adult Services and the Director of Public Health as required. This ensures that the key Statutory Officers are represented at the most senior level of the Council.

A restructure of the directorates has occurred as at 1 April 2013. The directorates and Executive Management Team for the beginning of 2013/14 financial year are detailed below:

� Charlie Parker – Chief Executive � Carolyn Wilkins - Assistant Chief Executive � Michael Jameson - Executive Director Commissioning (including Director of

Children's Services) � Emma Alexander - Executive Director Commercial Services � Elaine McLean - Executive Director Neighbourhoods � Mark Reynolds – Chief of Staff

For the 2012/13 financial year the Assistant Chief Executive and each of the Executive Directors led a Directorate team that is split into management divisions, each headed by an Assistant Executive Director. The Directorates were:

� People, Communities and Society; � Performance, Services and Capacity; � Economy, Place and Skills; and � Assistant Chief Executive.

Statement of Accounts 2012 - 2013

13

EMT members are not only responsible for managing a range of services, they also direct the overall improvement and future plans for Oldham. They work together to deliver the most effective services possible for the borough’s diverse communities and to ensure that Oldham plays a full part in national, regional and sub-regional activities. The EMT commissions, leads, directs and undertakes programmes/projects to achieve the objectives of the corporate work programme, modernise the Council and address the issues of borough community cohesion.

The EMT works with other local organisations to promote the interests of Oldham including:

� The Public Service Board;

� Local people and businesses; � The voluntary sector; and � Regional Authorities.

Each Executive Director is responsible for leading on some of the main partnership arrangements throughout the borough including key neighbourhood based activity. The organisational structure as at 31st March 2013 is shown in the diagram below.

Chief Executive’s Office:

• Lead for Repositioning Oldham.

• Strategic Health Issues.

• Link between the Executive and Political Leadership.

Charlie Parker Chief Executive

Mark Reynolds Chief of Staff

Michael Jameson Executive Director Commissioning

Emma Alexander Executive Director

Commercial Services

Elaine McLean Executive Director Neighbourhoods

EMT manages the delivery of Council services as well as directing the overall improvements and future plans for Oldham. It provides managerial leadership and supports the elected Members of the Council in:

• Developing strategies.

• Identifying and planning resources.

• Delivering plans.

• Reviewing the authority’s effectiveness with the overall objective of providing excellent services to the public.

Carolyn Wilkins Deputy

Chief Executive

Executive Management Team

Statement of Accounts 2012 - 2013

14

3.2.1 Commissioning

This Directorate has three management divisions as follows:

a) Children, Young People and Families - ensures the Council meets its statutory requirements as a Children’s Services Authority in respect of children and young people. This includes supporting schools in raising educational standards, keeping children safe, looking after children in care and co-ordinating and developing help for children with special needs.

The Children Act 1989 Section 27 imposes a general duty on Local Authorities to safeguard and promote the welfare of children in need in their area, and so far is consistent with that duty to promote the upbringing of children by their families by providing a range and level of services appropriate to the needs of those children. The required functions are implemented by commissioning or directly delivering universal, targeted and specialist services. Services are arranged into three streams - Safeguarding and Vulnerable Children, Family and Youth Support, Learning and Attainment.

b) Adult Social Care - provides a range of care services to some 4,000 older people and disabled people, usually by means of an individual budget to help them choose their own mix of services. It also supports a broader group of 8,000 people who have moderate frailty or disability by means of information, support and preventative services. Similarly, the service provides information, support and respite services to the carers/family members of both these groups.

The service has particular regard to ensuring the protection of vulnerable adults through the Adult Safeguarding Board and the Safeguarding team that investigate individual cases.

The main statutory obligations are to carry out Community Care and Carer assessments and these are completed by the Social Work service, including those who are jointly located with the NHS Mental Health Community teams. Nearly three quarters of care provision is commissioned from the external sector, charities, voluntary organisations and private companies. The remaining quarter is provided by internal services such as Reablement, Employment and Vocation projects, Community Response, Day Services, the Link Centre and Supported Accommodation.

c) Joint Commissioning – this division is continuing to develop a programme of joint commissioning with colleagues in the National Health Service. It identifies those areas where efficiency, effectiveness and quality of service can be improved by jointly commissioning and/or integrating and streamlining service delivery. The work programme covers both children’s and adult’s services and the current workstreams include continuing health care and complex care, out of borough placements and substance misuse (drug and alcohol services).

The Supporting People programme commissions housing-related support services to vulnerable people. The core objective is to enable them to attain and to sustain independent living in the community. Services are preventative and underpin many other service interventions by ensuring people can access and retain a safe, stable and secure home environment.

Statement of Accounts 2012 - 2013

15

3.2.2 Neighbourhoods

The Neighbourhoods Directorate consists of the following four divisions:

a) Strategic Projects, Asset and Facilities Management - provides a series of strategic and operational property, regeneration and inward investment functions, that align the asset base and physical development with the Council’s corporate and financial goals/objectives and Greater Manchester Strategies.

b) Liveability (Environment) - provides the key frontline services of Waste Management, Street Scene, Parks and Countryside, Parking, Street Lighting and Highways Operations.

c) Housing and Public Protection – develops a clear vision for planning and investment in housing, co-ordinating activity around affordable warmth, eliminating homelessness, investment and renewal of private sector housing areas and overseeing the delivery and monitoring of two Private Finance Initiative schemes. The Public Protection services provide regulatory services for Environmental Health, Trading Standards, Licensing and Registrars as well as having responsibility for the Council’s corporate Civil Resilience and First Response functions.

d) Place Shaping (Economic Development and Planning) - helps shape the natural and built environment of the borough. This includes developing the statutory land use planning framework, co-ordinating the physical regeneration of the borough and developing transport strategy and delivery plans. It also processes planning applications, takes enforcement action on planning contraventions, helps protect local heritage and conservation areas, and is responsible for supporting growth of local businesses, increasing local skill levels and the employment rate.

3.2.3 Commercial Services

The Commercial Services Directorate consists of the following five divisions:

a) Borough Solicitor – provides legal advice and representation for the Council, including Monitoring Officer duties, constitutional services and democratic services to support the Committees of the Council, Elections, Land Charges services and Members services.

b) Borough Treasurer – my division leads the financial planning process and provides financial management information and advice to elected Members, governors and managers, ensuring optimum use of available resources and management of revenue and capital budgets. I also have responsibility for treasury and cash flow management, the Internal Audit service, safe custody of assets/risk management, insurance, income collection and payment services and the client management function for the Unity Partnership Service for debtors, creditors and payroll.

c) Customer and Business Change – provides services including Customer Services including strategy, implementation and delivery, complaints handling, including Ombudsman complaints and Freedom of Information advice and monitoring. It also provides Value for Public Money strategy and implementation, strategic ICT

Statement of Accounts 2012 - 2013

16

(excluding schools) and the client function for the Unity Partnership for business relationships for the ICT Service.

d) Internal Services – provides the Business Support Service, Facilities Management, including catering and cleaning (schools and non-schools), performance monitoring including the Overview and Scrutiny performance management framework and the co-ordination of external reviews.

e) Procurement – ensures all goods and services are procured in an open and transparent manner to ensure the most cost effective and commercial solution, manages the tendering process in line with the rules and regulations and manages supplier relationships and contracts to deliver best value.

3.2.4 Deputy Chief Executive’s Directorate

The Deputy Chief Executive’s (DCE) Directorate consists of the following seven divisions:

a) Corporate Policy and Research – provides policy and research information to the Council by analysing the national and regional landscape and developing the Council’s approach to policy and strategy across a wide range of areas that impact on all Directorates in the Council.

b) Communication and Marketing – manages the reputation and communication needs of Oldham Council. It is responsible for media relations handling approximately 2,000 queries per year and issuing around 40 press releases per month. It also handles the design requirements of the Authority and its partners, it manages and maintains the content and design of the Council’s website and employee intranet, and manages the marketing of Council services and facilities. The team is also responsible for internal communications and employee engagement, including events and employee communication channels. An increasing area of focus for the team is the use of social media to market the borough and communicate with local residents.

c) Community Cohesion – leads work across Oldham Council and the Oldham Partnership to manage community tensions and build good community relations. It contributes to work to build a strong voluntary, community and faith sector, and to tackling inequality, for example through commissioning legal and advice services which meet the needs of residents.

d) Customer Services – is responsible for the development and implementation of the Council’s Customer Services Strategy which influences the way services are designed and delivered, ensuring they are accessible to customers and are delivered through the most cost effective channels. It is also responsible for managing the business relationship with the Unity Partnership for Customer Services, Revenues and Benefits and undertaking statutory functions retained by the Council in relation to these services, such as monitoring benefit claims processing to ensure accurate and timely payment of benefit.

e) DCE Management and Administration – incorporates the administrative support for the Directorate and is a fully recharged service.

Statement of Accounts 2012 - 2013

17

f) Neighbourhoods Service – co-ordinates local service delivery across each of the six District Partnerships covering the borough. The service works with elected Members, partners and local service providers to connect with local citizens so that they play an active role in shaping, influencing and delivering services that meet local priorities. The Neighbourhoods service also includes libraries, arts and heritage services and works with a range of local, regional and national partners to provide a wide range of accessible leisure, learning and information opportunities. Services and activities are delivered in Council facilities and community settings, and are tailored to be accessible and relevant to all ages and sections of the community.

g) People Services – provides strategic guidance to the organisation of all people related matters as set down within the People Framework. Putting mechanisms in place to ensure the business has the right people with the right capabilities in the right role, with appropriate terms and conditions of employment and the ability to advise and guide managers at all levels on any people related issue.

3.3 Repositioning to a Co-operative Borough Following a period of recovery in 2009, through two years of intensive improvement the Council has made a great deal of changes - but this is just the beginning of our journey. The council now faces a significant reduction in its funding and, after having to make savings of over £100 million over the last four years, has an additional £38 million to find over the next two years.

Alongside these financial challenges, the Council has a new ambition – to become a Co-Operative Council. This means working more closely with residents, partners and businesses to improve Oldham. To meet these challenges we need to change the way we do business, by working smarter and delivering services differently we will not only become more efficient and cost effective, we will also change the way in which we are viewed by our customers and the residents of our borough.

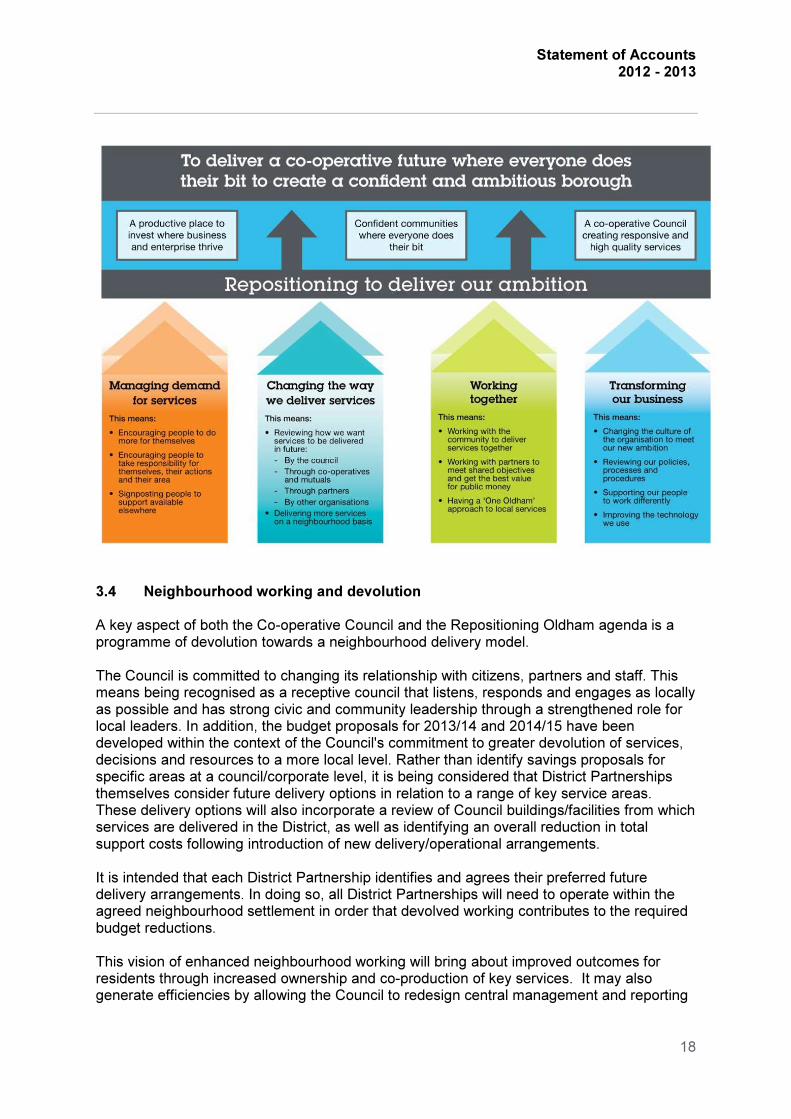

Repositioning Oldham has four overall objectives which will enable us to deliver the programme and in doing so will help us on our way to achieving our ambition to becoming a Co-Operative Council. These objectives are key to the programme - some of you will have heard me talking about them at staff conferences or may have come across them on the intranet.

The Repositioning diagram gives a high level overview of each of the objectives. All of the Council's change activity should contribute to at least one of the Repositioning objectives.

Statement of Accounts 2012 - 2013

18

3.4 Neighbourhood working and devolution

A key aspect of both the Co-operative Council and the Repositioning Oldham agenda is a programme of devolution towards a neighbourhood delivery model.

The Council is committed to changing its relationship with citizens, partners and staff. This means being recognised as a receptive council that listens, responds and engages as locally as possible and has strong civic and community leadership through a strengthened role for local leaders. In addition, the budget proposals for 2013/14 and 2014/15 have been developed within the context of the Council's commitment to greater devolution of services, decisions and resources to a more local level. Rather than identify savings proposals for specific areas at a council/corporate level, it is being considered that District Partnerships themselves consider future delivery options in relation to a range of key service areas. These delivery options will also incorporate a review of Council buildings/facilities from which services are delivered in the District, as well as identifying an overall reduction in total support costs following introduction of new delivery/operational arrangements.

It is intended that each District Partnership identifies and agrees their preferred future delivery arrangements. In doing so, all District Partnerships will need to operate within the agreed neighbourhood settlement in order that devolved working contributes to the required budget reductions.

This vision of enhanced neighbourhood working will bring about improved outcomes for residents through increased ownership and co-production of key services. It may also generate efficiencies by allowing the Council to redesign central management and reporting

Statement of Accounts 2012 - 2013

19

structures across devolved services. Some initial work launched in 2012/13 saw youth services budgets devolved to District Partnership areas.

The objectives of devolution have been agreed as:

� Strengthened relationship between the Council and citizens and places; � Greater recognition of Councillors as civic and community leaders; � Improved integration across services and partners at a local level; and � Greater citizen involvement in local decisions as well as design, commissioning and

delivery of local services.

The four key work areas within the Council’s devolution agenda are:

� Neighbourhood Teams and local service delivery; � District Town Halls and local identity; � Local involvement and engagement: including decision making and the Co-operative

agenda; and � Strengthening democracy including member development and support.

3.5 Oldham Council’s Corporate Plan One of the key strategic documents that frame the actions of the Council is the Council’s Corporate Plan. This is a working document that exists to help elected Members, staff and partners work together to deliver the vision for Oldham. Its primary purpose is to set out our story of place and our priorities for Oldham - what we are doing and why we are doing it.

Our new corporate ambition and objectives were agreed at Full Council on 23 May 2012.

Our ambition is to deliver a co-operative future where everyone does their bit to create a confident and ambitious borough.

There are three corporate objectives that underpin the delivery of the ambition. They are:

1. A productive place to invest where business and enterprise thrive. 2. Confident communities where everyone does their bit. 3. A co-operative council creating responsive and high quality services.

The objectives have been developed to reflect the key priorities of the Council including economic growth and regeneration, strong local leadership and delivering value for money services.

3.6 Managing Performance

Proactively and effectively managing performance is central to delivering the Council’s service improvements, statutory obligations, greater value for public money and the strategic objectives of the Corporate Plan.

The business planning processes have also been strengthened to meet local requirements, and created in such a way to ensure robust links between both political obligations and the strategic objectives of the Council, through the development of a Corporate Plan and internal business plans. The table below sets out this business planning framework that the Council works to:

Statement of Accounts 2012 - 2013

20

As the Council’s key planning document, the Corporate Plan is the backbone of the Performance Management Framework and supporting the delivery of the Corporate Plan are the comprehensive business plans for each of the Council’s Directorates. These set out the medium term priorities for each Directorate, and are supported by the Divisional and Operational Plans that identify how each Service and Business Unit within the Council will contribute to the achievement of key objectives.

Operational Plans translate the key objectives of the Directorate and Divisional Plans into more detailed objectives, and all staff receive a performance appraisal through which each individual’s contribution to delivering these objectives and priorities are identified and agreed.

Reports on performance are used by senior managers and elected members to ensure that services are delivered and offer value for money which meet the needs of all the Oldham communities. By adopting a systematic approach, which includes regular performance reports at various levels of detail, the Council constantly reviews service delivery and the expected/achieved outcomes for citizens. In this way, the strengths in a particular area can be identified and good practice shared. Equally areas of concern can be identified to facilitate appropriate action where necessary, to ensure that the best possible outcomes are delivered.

Part of the performance management framework is the consideration by Cabinet of financial monitoring reports outlining financial performance from months 3 to month 9 so that Members are advised of all key issues that may affect the outturn for the year. This allows any necessary remedial action to be taken. 3.7 The Council’s Key Achievements

Oldham is well positioned to be able to adapt and adjust to meet some of the new challenges. Since 2008, the Council has been on a journey of recovery and improvement

Corporate Plan 2012-2015

Directorate Business Plans

Appraisal

Operational Plans

Informed by:

•District Plans

•GM Strategy

•Statutory Plans

•External Inspection

Medium Term

Financial Strategy

Divisional Plans

Statement of Accounts 2012 - 2013

21

that has led to a number of positive outcomes and achievements recognised through the Most Improved Council Award in March 2012. The improvement journey has also provided a firm base from which to reposition the Council. This means developing different ways of working and preparing for how the Council will deliver services in future, for example, moving from being a provider of services to more of a commissioner.

The Council’s key achievements over the last year include:

� Found savings of £26.601m to balance the budget in 2012/13 (a net budget reduction

of £24.493m after the financing of investments). � First local government body to publish its 2011/12 accounts and likely to remain so

with an earlier date in 2012/13. � Introduction of employee volunteering scheme. � GCSE results improved for the twelfth consecutive year (56% of all children gained 5

A* - C qualifications including Maths and English in 2012 up from 55% in 2011). � Over 300 empty homes have been brought back into use in the last year. � Metrolink Extension brought the first trams to Oldham in June 2012 with further

expansion taking place. � Introduced the living wage for staff. � Introduced Greater Manchester’s first local authority mortgage scheme. � Introduced ‘Open Council’ sessions with questions being submitted by the public

through a range of channels including twitter and email, and live web streaming of the meetings.

� Undertook a highly successful Invest in Oldham event in London. � Winner of Britain in Bloom Best City award. � Created 172 apprenticeships in just 100 days.

3.8 Strategic Financial Management

The Council continues to improve its strategic financial management. Finance services have been transformed over the past three and a half years. Integral to the Council’s wider programme of improvement and transformation, the finance service is now instrumental in delivering the innovation and change which have transformed Oldham into one of the highest achieving councils in the country. Building on this success, the Finance team has continued to deliver exceptional results over the past year, including:

� Accurately forecasting the savings required for 2010/11, 2011/12 and 2012/13

budget through an intelligence-led and realistic approach to current financial challenges, better enabling the organisation to identify and prepare for these savings ahead of their implementation.

� Assisting Council services to identify budget options by November 2012 of £14.863m against a target of £17.735m for 2013/14 and £12.693m against an original target of £12.976 for 2014/15. Full proposals for the two years were approved by Council on 17 April 2013.

� Ensuring the Council’s 2011/12 accounts were closed, audited and published with unprecedented speed and accuracy, being the first Council ever to publish audited accounts in June and doing so with a balanced budget. This achievement has been lauded by the Audit Commission, who ensure that the Council’s key financial systems are fully audited regularly during the view to support the focus on sound financial management and control.

Statement of Accounts 2012 - 2013

22

� Continuing the accurate monthly monitoring reporting of the 2012/13 revenue budget, building on improved budgetary processes.

� Continuing the reduction in the Council’s net overall debtor arrears. This has enhanced the Council’s balance sheet position, reducing exposure to bad debts and ensuring that managers focus on cash collection in addition to income generation.

� Providing on-going financial advice for major capital initiatives, particularly those that were approved at the 11 July 2012 Council meeting financed by prudential borrowing investment of £105.556m. This included the transformation of Oldham Town Centre and other major regeneration schemes.

� Issuing fully detailed budget and financial advice packs in February, enabling schools to access financial information and advice much earlier in the budget cycle, thus facilitating earlier and better-informed financial planning.

� Instigation of a systems integration programme to enhance financial and related information and improve efficiency and effectiveness.

� Fully comprehensive monthly closedowns as part of the continuous improvement in the Council’s accounts.

� Enhanced budget and accounting information through to EMT and members � Revised training programme and contracts for all finance staff and trainees, as

appropriate.

The improvement will of course continue and develop in 2013/14, hence the accelerated production of these accounts for 2012/13. 4 Key Issues that Influenced the Financial Position in 2012/13 Having introduced you to the Council and its operating ethos, I would now like to explain the key financial issues that have framed 2012/13. In my role as Borough Treasurer, it is my responsibility to ensure that Members of the Council receive robust and timely information to enable them to approve the budget for each financial year. I therefore prepared a range of reports for the Council to consider at its meeting of 22 February 2012. There were three budget reports covering the revenue budget, capital programme and the Housing Revenue Account (HRA) budget and also the Capital Strategy, Treasury Management Strategy, Medium Term Financial Plan and the Chief Financial Officer’s report setting out the recommended level of general balances and reserves. The key budgetary issues for 2012/13 are set out as follows. 4.1 Revenue Budget

The Council was always aware that the 2012/13 budget process would, in many respects, be just as challenging as that for 2011/12. Although the savings target was lower (£24.493m compared to £39.560m) it would be a harder test to propose achievable savings proposals. The information issued in the Comprehensive Spending Review (CSR) and confirmed by the Chancellors Autumn Statement and the Local Government Finance Settlement, highlighted that there would be a considerable savings target for 2012/13 but that future years would also be challenging. The 2012/13 revenue budget process was therefore influenced and framed by the need to make radical reductions in expenditure, whilst still aiming to address priority issues for the Council. The financial pressures building up the budget gap for 2012/13 are set out below.

Statement of Accounts 2012 - 2013

23

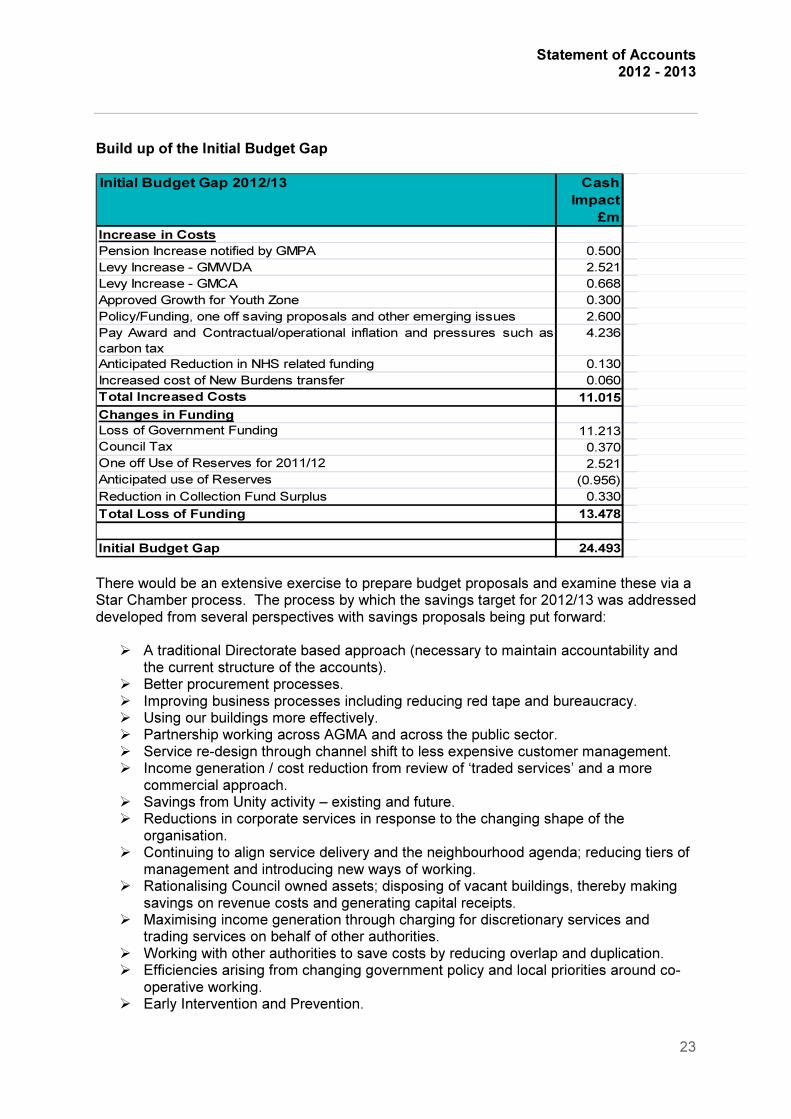

Build up of the Initial Budget Gap

Initial Budget Gap 2012/13 Cash

Impact

£m

Increase in Costs

Pension Increase notified by GMPA 0.500

Levy Increase - GMWDA 2.521

Levy Increase - GMCA 0.668

Approved Growth for Youth Zone 0.300

Policy/Funding, one off saving proposals and other emerging issues 2.600

Pay Award and Contractual/operational inflation and pressures such as

carbon tax

4.236

Anticipated Reduction in NHS related funding 0.130

Increased cost of New Burdens transfer 0.060

Total Increased Costs 11.015

Changes in Funding

Loss of Government Funding 11.213

Council Tax 0.370

One off Use of Reserves for 2011/12 2.521

Anticipated use of Reserves (0.956)

Reduction in Collection Fund Surplus 0.330

Total Loss of Funding 13.478

Initial Budget Gap 24.493 There would be an extensive exercise to prepare budget proposals and examine these via a Star Chamber process. The process by which the savings target for 2012/13 was addressed developed from several perspectives with savings proposals being put forward: � A traditional Directorate based approach (necessary to maintain accountability and

the current structure of the accounts). � Better procurement processes. � Improving business processes including reducing red tape and bureaucracy. � Using our buildings more effectively. � Partnership working across AGMA and across the public sector. � Service re-design through channel shift to less expensive customer management. � Income generation / cost reduction from review of ‘traded services’ and a more

commercial approach. � Savings from Unity activity – existing and future. � Reductions in corporate services in response to the changing shape of the

organisation. � Continuing to align service delivery and the neighbourhood agenda; reducing tiers of

management and introducing new ways of working. � Rationalising Council owned assets; disposing of vacant buildings, thereby making

savings on revenue costs and generating capital receipts. � Maximising income generation through charging for discretionary services and

trading services on behalf of other authorities. � Working with other authorities to save costs by reducing overlap and duplication. � Efficiencies arising from changing government policy and local priorities around co-

operative working. � Early Intervention and Prevention.

Statement of Accounts 2012 - 2013

24

� New Ways of Working. � Integrated Commissioning. � Partnership Working with health and schools.

There was a considerable build up to setting the revenue budget with the first formal report to Members presented on 17 November 2011 at the meeting of the Overview and Scrutiny Performance and Value for Money (PVFM) Select Committee. There then followed a series of other reports, culminating in the approval of the budget and 2012/13 Council Tax at the Council meeting on 22nd February 2012. The key stages in the revenue budget process are set out as follows.

The Overview and Scrutiny Performance and Value for Money (PVFM) Select Committee Meeting was presented with a report to advise Members that there was likely to be a £24.493m gap in the resources available to meet demands, and therefore best estimates at the time were that savings of £24.493m would be required. The revenue spending forecast was based on a range of assumptions about the level of income and expenditure required to deliver services, but was also influenced by the anticipated Local Government Finance Settlement and expected increases in the levies to be paid to the Greater Manchester Waste Disposal Authority (GMWDA) and Greater Manchester Integrated Transport Authority (GMITA).

The report advised that a major exercise had been instigated to review the budget and numerous work streams had been initiated to consider potential savings options. These had been subject to examination via a Star Chamber process. Indeed, prior to the Select Committee, there had been a number of Star Chamber meetings and as a consequence £24.493m of savings proposals were put forward for scrutiny split by Directorate. The Members of the Select Committee requested that ten of these savings be reconsidered and, as a result, £1.949m of savings were withdrawn by the Administration for further consideration and not approved at the Council meeting on 14 December 2011. In addition, a further £431k of savings were also withdrawn bringing a total of £2.380m of savings to be reconsidered.

On 14 December 2011 at the Council Meeting, the Council approved the revision to the Council’s 2011/12 net revenue budget to £232.346m to reflect changes to funding arrangements since the start of the financial year, the budget proposals totalling £22.113m detailed in the report be approved and further consideration be given to the £2.380m of budget proposals. The PVFM Select Committee meeting in January received further information about the £2.380m budget proposals, responses to other issues raised at the PVFM meeting of 17 November 2011 and any further savings proposals required to bridge any remaining budget gap, the outcome of which to be reported to the Council budget meeting in February 2012. At the 3 January 2012 Cabinet meeting, the Cabinet approved a report which set out the revised Tax Base for 2012/13 at 63,180. On the basis of no change in Council Tax, Members were advised that this would result in additional Council Tax income of £268k for the Council.

Work to review existing budget proposals and their service impact continued throughout January and early February and a further examination of consultation comments took place so that, where appropriate, they were taken into account in budget decisions. At the 24 January 2012 Overview and Scrutiny Performance and Value for Money (PVFM) Select

Statement of Accounts 2012 - 2013

25

Committee Meeting, the Members were asked to consider the savings totalling £2.380m, to bridge this remaining budget gap. These were then agreed at the Cabinet meeting on 6 February 2012. Cabinet recommended to Council for approval:

a) acceptance of the Council Tax Freeze Grant; b) savings proposals of £2.380m; c) the total budget for Council services for 2012/13 be set at £225.354m subject to

confirmation of precepts and levies; d) the total draw on the Collection Fund for borough wide services of £97.476m,

with £85.031m for Council services subject to confirmation of precepts and levies;

e) the Council Tax, subject to confirmation from preceptors, be set at the same level as for 2010/11.

Cabinet approved that the Cabinet Member for Finance and Human Resources and the Borough Treasurer in conjunction with the Leader of the Council, the Chief Executive and the Executive Director for Performance Services and Capacity be authorised to make any adjustment to the Budget for submission to Council.

Closing the Budget Gap

The approved overall budget for Council Services for 2012/13 together with financing is set out below:

Initial Budget

2012/13

Budget £000

£000

Directorate budget requirements 250.803

Budget options other than use of reserves (24.368)

Budget options from use of reserves (0.125)

Use of Reserves (0.956)

Base Budget Forecast 225.354

This would be funded by:

Total Formula Grant 115.146

Early Intervention Grant 14.861

Housing Benefit and Council Tax Administration Grant 2.100

Learning Disability and Health Reform Grant 5.335

LSSG 0.462

New Homes Bonus 0.294

Council Tax Freeze Grant 2.125

Council Tax 85.031

Total Budget for Council Services 225.354

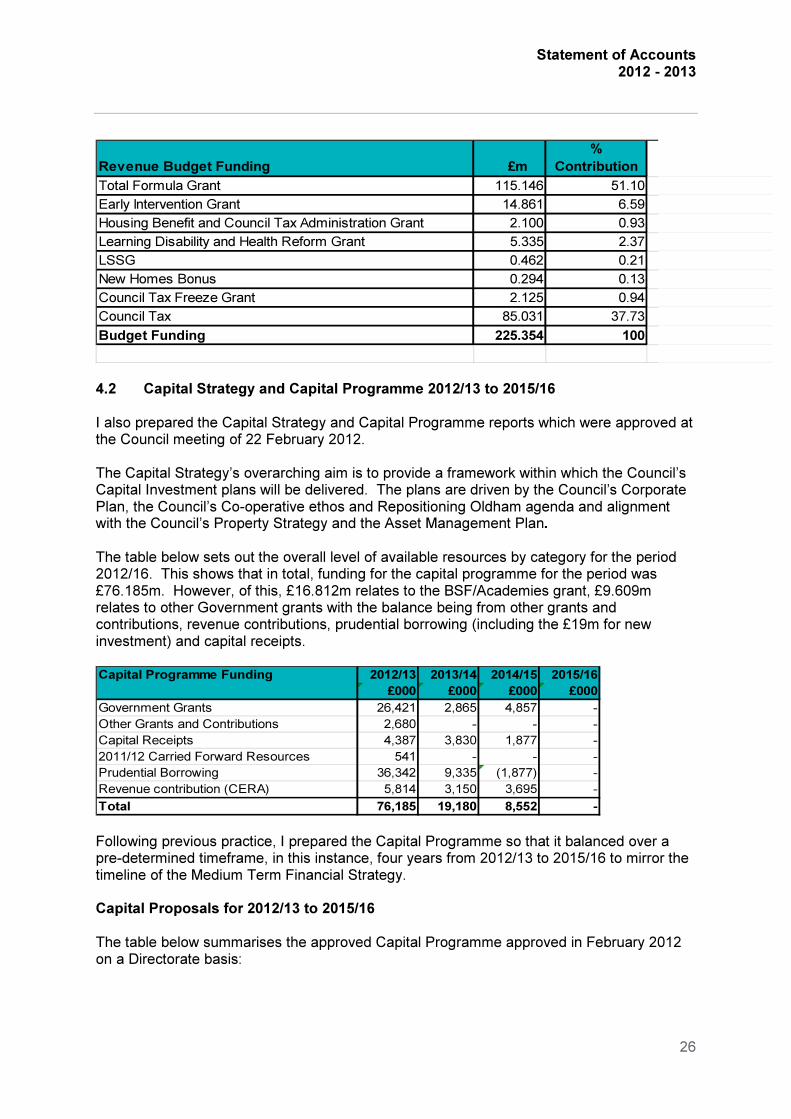

The table below shows the source of the funding for Council services in 2012/13 as a percentage contribution.

Statement of Accounts 2012 - 2013

26

Revenue Budget Funding £m

%

Contribution

Total Formula Grant 115.146 51.10

Early Intervention Grant 14.861 6.59

Housing Benefit and Council Tax Administration Grant 2.100 0.93

Learning Disability and Health Reform Grant 5.335 2.37

LSSG 0.462 0.21

New Homes Bonus 0.294 0.13

Council Tax Freeze Grant 2.125 0.94

Council Tax 85.031 37.73

Budget Funding 225.354 100

4.2 Capital Strategy and Capital Programme 2012/13 to 2015/16

I also prepared the Capital Strategy and Capital Programme reports which were approved at the Council meeting of 22 February 2012.

The Capital Strategy’s overarching aim is to provide a framework within which the Council’s Capital Investment plans will be delivered. The plans are driven by the Council’s Corporate Plan, the Council’s Co-operative ethos and Repositioning Oldham agenda and alignment with the Council’s Property Strategy and the Asset Management Plan.

The table below sets out the overall level of available resources by category for the period 2012/16. This shows that in total, funding for the capital programme for the period was £76.185m. However, of this, £16.812m relates to the BSF/Academies grant, £9.609m relates to other Government grants with the balance being from other grants and contributions, revenue contributions, prudential borrowing (including the £19m for new investment) and capital receipts.

2012/13 2013/14 2014/15 2015/16

£000 £000 £000 £000

Government Grants 26,421 2,865 4,857 -

Other Grants and Contributions 2,680 - - -

Capital Receipts 4,387 3,830 1,877 -

2011/12 Carried Forward Resources 541 - - -

Prudential Borrowing 36,342 9,335 (1,877) -

Revenue contribution (CERA) 5,814 3,150 3,695 -

Total 76,185 19,180 8,552 -

Capital Programme Funding

Following previous practice, I prepared the Capital Programme so that it balanced over a pre-determined timeframe, in this instance, four years from 2012/13 to 2015/16 to mirror the timeline of the Medium Term Financial Strategy. Capital Proposals for 2012/13 to 2015/16

The table below summarises the approved Capital Programme approved in February 2012 on a Directorate basis:

Statement of Accounts 2012 - 2013

27

2012/13 2013/14 2014/15 2015/16

£000 £000 £000 £000

Corporate Expenditure 1,149 1,000 0 0

Assistant Chief Executives 720 360 360 360

Economy Places & Skills 47,843 19,520 8,552 0

People, Communities & Society – Schools 2,220 0 0 0

People, Communities & Society – Adults Social

Care

400 400 400 400

Performance, Service & Capacity 215 180 180 180

Resources to Allocate 19,478

Total Expenditure 72,025 21,460 9,492 940

Total Funding (76,185) (19,180) (8,552) 0

Balance of Resources available by year -

(Over)/under programming

(4,160) 2,280 940 940

Cumulative balance of resources available for

new projects.

(4,160) (1,880) (940) 0

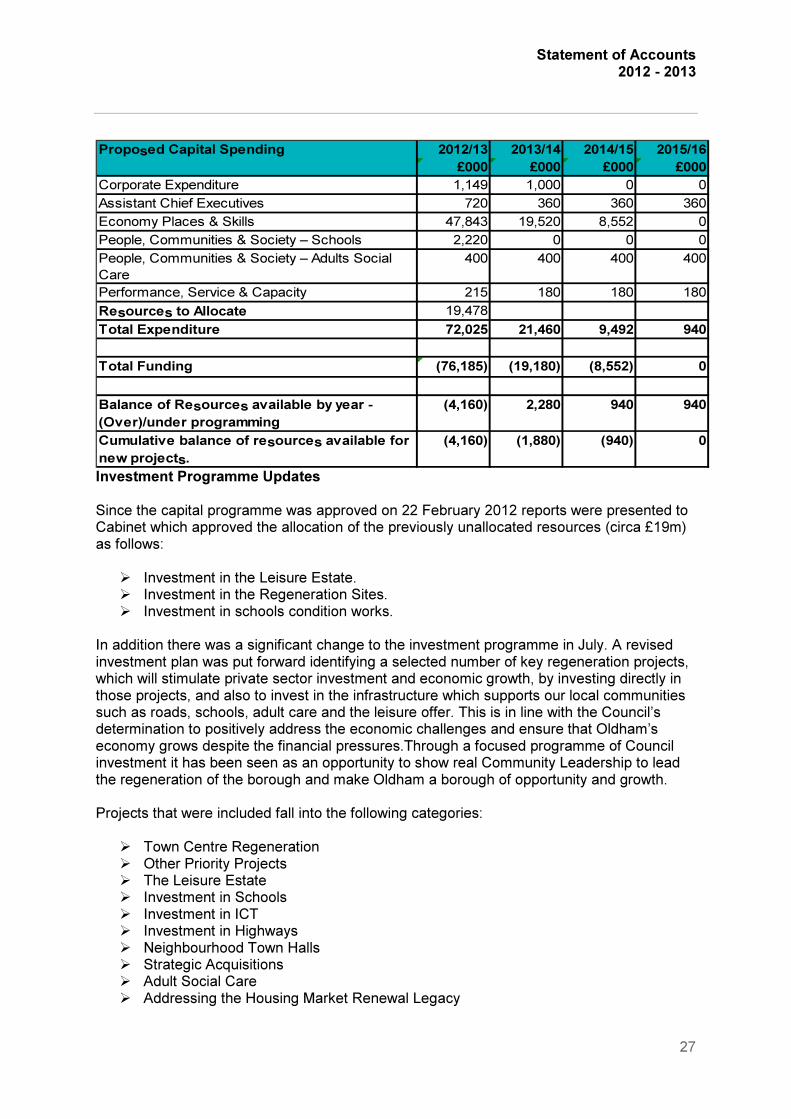

Proposed Capital Spending

Investment Programme Updates

Since the capital programme was approved on 22 February 2012 reports were presented to Cabinet which approved the allocation of the previously unallocated resources (circa £19m) as follows:

� Investment in the Leisure Estate. � Investment in the Regeneration Sites. � Investment in schools condition works.

In addition there was a significant change to the investment programme in July. A revised investment plan was put forward identifying a selected number of key regeneration projects, which will stimulate private sector investment and economic growth, by investing directly in those projects, and also to invest in the infrastructure which supports our local communities such as roads, schools, adult care and the leisure offer. This is in line with the Council’s determination to positively address the economic challenges and ensure that Oldham’s economy grows despite the financial pressures.Through a focused programme of Council investment it has been seen as an opportunity to show real Community Leadership to lead the regeneration of the borough and make Oldham a borough of opportunity and growth.

Projects that were included fall into the following categories: � Town Centre Regeneration � Other Priority Projects � The Leisure Estate � Investment in Schools � Investment in ICT � Investment in Highways � Neighbourhood Town Halls � Strategic Acquisitions � Adult Social Care � Addressing the Housing Market Renewal Legacy

Statement of Accounts 2012 - 2013

28

In total the capital expenditure proposed for the period 2012/13 to 2016/17 is £105.655m. It was highlighted that some of the costs of the projects still needed to be confirmed which may lead to cost increases, however, the Council could also potentially receive grants, capital receipts and other contributions which could conversely reduce the costs. Anticipated additional costs associated with financing the capital expenditure would be addressed through the revenue budget planning process. Further to this, it was proposed that in accordance with established procedures, the CIPB (Capital Investment Programme Board) leads on the review and schemes and that expenditure is not finally committed until the CIPB is satisfied that the objectives of the project are achievable and the project is financially robust.

4.3 HRA Budget 2012/13

The HRA Budget report was presented for approval at the Cabinet of February 6th 2012 and the Council meeting of 22 February 2012.

Following on from the transfer on 7 February 2011 of the non PFI housing stock to a Registered Social Landlord (First Choice Homes Oldham), the HRA budget has been prepared so that it only deals with properties within the two PFI Schemes and so should remain fairly balanced on an annual basis. Eligible debt will continue to be met from subsidy, with rents and other subsidy allowances effectively passed through to the PFI reserves.

April 2012 marked the most significant change in a generation to the way that council housing is financed; the Localism Act which received royal assent on 15 November 2011 delivered a new local devolved system which replaced the current subsidy regime. In practical terms the HRA is now a self-sufficient ring fenced account which will retain and use rental income, and in the case of Oldham, PFI credits to meet all its management, maintenance and repairs commitments, including the respective unitary charges. The aim of the reforms was to enable councils to manage their housing stock for the benefit of local residents in a transparent, accountable and cost effective way. The determination for Oldham was in line with predictions and the Council received a payment from Central Government of £20.227m. This was received on 28 March 2012.

The HRA reserve is a consolidation of a general HRA fund and separate reserves for each of PFI 2 and PFI 4. The estimated balance on the combined HRA reserve as at 31 March 2013, the first year of the HRA self-financing regime was £9.774m. The estimated consolidated balance, in the context of the HRA self-financing business plan was considered sufficient to meet future possible financial pressures as identified in the risk assessment that accompanied the business plan.

HRA Budget

for 2012/13

£000

Income (27,631)

Expenditure 30,925

Other Charges /Income (152)

(Surplus)/Deficit for the Year on HRA Services 3,142

HRA Balance Brought Forward (12,916)

HRA Balance Carried Forward (9,774)

Statement of Accounts 2012 - 2013

29

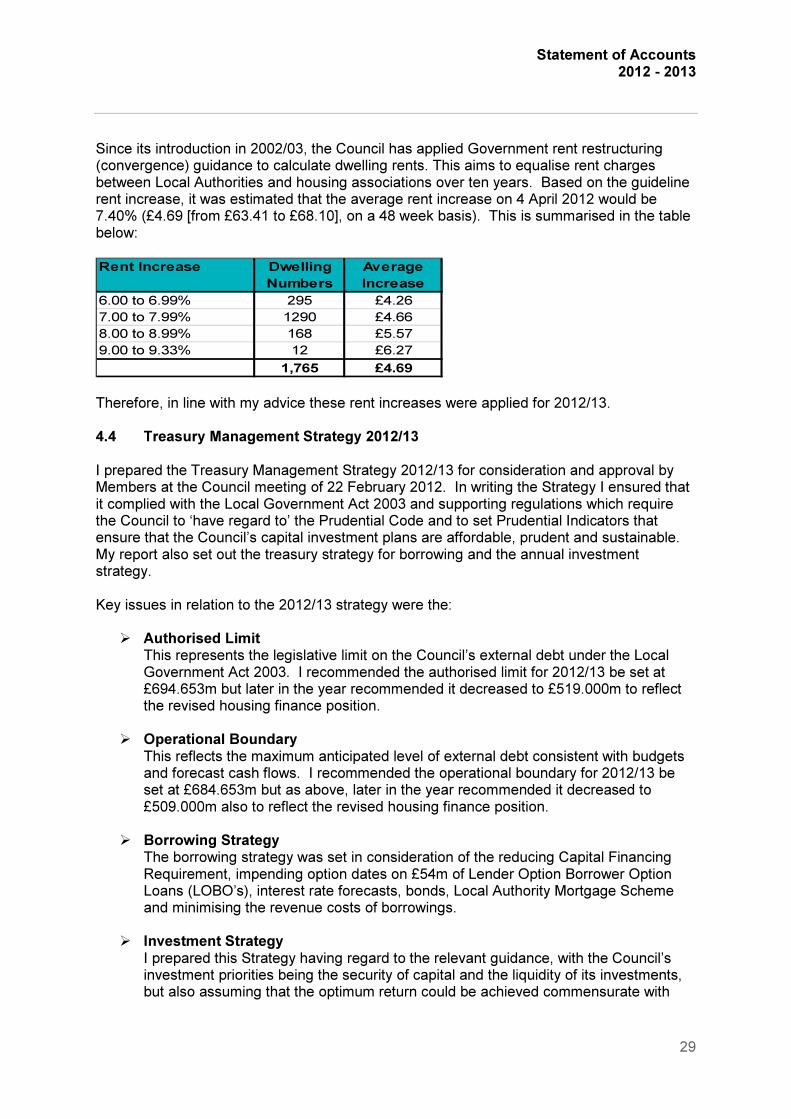

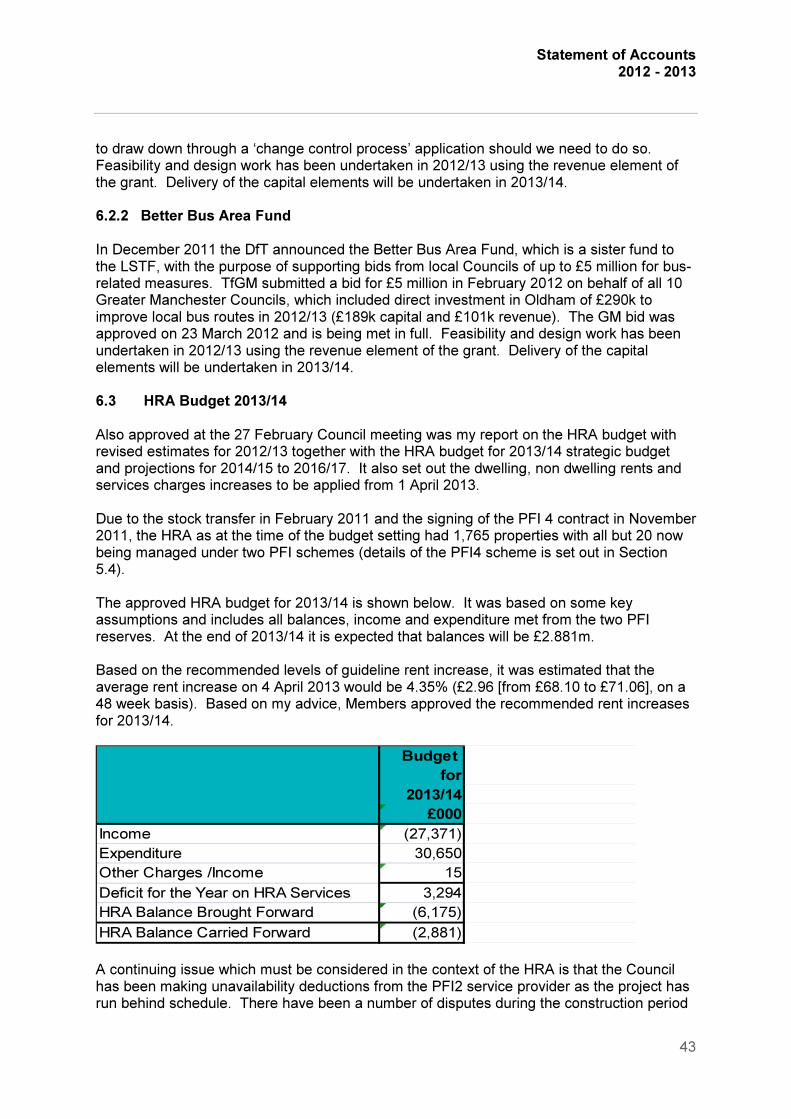

Since its introduction in 2002/03, the Council has applied Government rent restructuring (convergence) guidance to calculate dwelling rents. This aims to equalise rent charges between Local Authorities and housing associations over ten years. Based on the guideline rent increase, it was estimated that the average rent increase on 4 April 2012 would be 7.40% (£4.69 [from £63.41 to £68.10], on a 48 week basis). This is summarised in the table below:

Rent Increase Dwelling Average

Numbers Increase

6.00 to 6.99% 295 £4.26

7.00 to 7.99% 1290 £4.66

8.00 to 8.99% 168 £5.57

9.00 to 9.33% 12 £6.27

1,765 £4.69

Therefore, in line with my advice these rent increases were applied for 2012/13.

4.4 Treasury Management Strategy 2012/13

I prepared the Treasury Management Strategy 2012/13 for consideration and approval by Members at the Council meeting of 22 February 2012. In writing the Strategy I ensured that it complied with the Local Government Act 2003 and supporting regulations which require the Council to ‘have regard to’ the Prudential Code and to set Prudential Indicators that ensure that the Council’s capital investment plans are affordable, prudent and sustainable. My report also set out the treasury strategy for borrowing and the annual investment strategy.

Key issues in relation to the 2012/13 strategy were the:

� Authorised Limit

This represents the legislative limit on the Council’s external debt under the Local Government Act 2003. I recommended the authorised limit for 2012/13 be set at £694.653m but later in the year recommended it decreased to £519.000m to reflect the revised housing finance position.

� Operational Boundary This reflects the maximum anticipated level of external debt consistent with budgets and forecast cash flows. I recommended the operational boundary for 2012/13 be set at £684.653m but as above, later in the year recommended it decreased to £509.000m also to reflect the revised housing finance position.

� Borrowing Strategy The borrowing strategy was set in consideration of the reducing Capital Financing Requirement, impending option dates on £54m of Lender Option Borrower Option Loans (LOBO’s), interest rate forecasts, bonds, Local Authority Mortgage Scheme and minimising the revenue costs of borrowings.

� Investment Strategy I prepared this Strategy having regard to the relevant guidance, with the Council’s investment priorities being the security of capital and the liquidity of its investments, but also assuming that the optimum return could be achieved commensurate with

Statement of Accounts 2012 - 2013

30

proper levels of security and liquidity. Given the low interest rates available because of the economic climate, I anticipated that investments were to be kept short term.

4.5 Medium Term Financial Strategy for 2012/13 to 2015/16 including the Projected

Level of Balances

My aim was to align the Medium Term Financial Strategy (MTFS) for 2012/13 to 2015/16 to the objectives set out in the Corporate Plan. The MTFS was also approved at the Council meeting on 22 February 2012 and it set the framework to enable the Council to determine an appropriate course of action to address significant financial challenges not only for 2012/13 but for future financial years.

The revenue spending reductions included in the MTFS highlighted that the Council would have to continue the programme to significantly reconfigure its business and organisational arrangements for 2012/13 onwards, in order to continue to provide value for public money services.

The MTFS projected that, in addition to the £24.493m savings for 2012/13 the Council would have to find another £18.418min 2013/14, £14.043m in 2014/15 and £15.000m in 2015/16 and a further £15.000m in 2016/17. It also identified that in line with the previous year, considerable reductions in the level of Government funding for the capital programme would mean that there would be much reduced opportunities for capital spending for 2012/13 and future years, unless the Council itself financed new investment.

Following the Local Government Finance Settlement received in December 2012, the £12.976m 2014/15 saving figure was increased by a further £7.528m.

One important issue that was significant both in relation to the MTFS and also the 2012/13 budget was the assumption about the level of balances that the Council would require to address any unexpected spending pressures. These balances need to reflect spending experience and risks to which the Council might be exposed. I prepared a report for consideration at the 23 February Council meeting, recommending that balances for 2012/13 should be £15.650m, rising to £16.839m in 2013/14 and £16.764m in 2014/15. The Council approved this recommended approach.

5. Key Events Affecting the Council in 2012/13 and Influencing Future Years

In addition to the impact of the Council’s own budget setting arrangements which were heavily influenced by National Government policy, there were several significant local and national issues that have a bearing on the financial position for 2012/13 and future years. In the following section, I set out those issues which I consider to be of most relevance in the context of the 2012/13 accounts. 5.1 Transformation of Oldham Town Centre A key Council policy is the transformation of the town centre and recent years have seen the completion of high profile cultural, health and education development. The Council is committed to a positive and pro-active ‘Town Team’ approach to place making, shaping, enabling, investing and delivering development proposals that will deliver a vibrant Town Centre.

Statement of Accounts 2012 - 2013

31

This encompasses 5 large scale projects outlined below, the financial implications of which total £48.634m beginning in 2012/13 and phased over the financial years to 2016/17. Through a co-operative, ‘Town Team’ approach, the Council will work with partners to ensure realisation of the long term vision for a more economically, socially and environmentally connected Oldham of the future. At the heart of Oldham is the Town Centre where there is great capacity for growth. Metrolink, ultrafast next generation broadband and vastly improved public realm will create the setting for new development and investment opportunities. The Council has already committed resources to make sure this happens and is now working with development and investor partners who are leading edge, creative and keen to work with a Co-operative Council on key development projects including:

a) Hotel Futures

The Council, together with the Manchester Hoteliers Association and The Oldham College has entered into a Memorandum of Understanding to work co-operatively to deliver a National Hospitality Training Academy (NHTA).

The development in Oldham will form a blueprint for the proposed expansion of the initiative throughout the UK. The Academy will provide a unique opportunity for students to gain training in the hospitality industry through a combination of structured courses and on-the-job training in the professional and commercial environment of an upscale hotel and convention centre, designed and constructed specifically to accommodate the NHTA. The NHTA will be designed to provide world-class training facilities and skills development in a high quality professional and commercial environment. It is expected to attract students and apprentices from across the UK and throughout the world, as well as furthering careers for existing hospitality industry employees.

The project will entail the financing, design, construction and operation of a circa 120 upscale bedroomed hotel incorporating the Queen Elizabeth Hall as a convention centre. The Hotel will be run on a commercial basis with paying guests served by a combination of full time trained staff, together with students and apprentices enrolled in the NHTA training and apprenticeship programmes.

b) Oldham Town Hall

Redevelopment of the Oldham Town Hall is a key Town Centre development opportunity. Extensive work has previously been carried out to stabilise the building and make it weather tight. Planning approvals have been secured for a new use. It is planned that the development will include cinema, retail and restaurant uses. Work is continuing to complete a final business plan and the aim is that the development will be completed in 2014/15. Planning permission has been granted for the scheme to progress for which full designs are being progressed.

c) Heritage Centre / Relocation of the Coliseum Theatre

The capital project combines the re-location of the Coliseum Theatre and the creation of a resource to promote the heritage of Oldham and allow the bringing together of heritage materials held in a number of different locations. This is to be based around the Old Library to minimise new build and to bring efficiencies.

Statement of Accounts 2012 - 2013

32

It is planned that the new theatre will provide a 600 seat traditional proscenium theatre with fly tower, a 150 seat studio theatre, foyers with catering for all day use, dedicated education spaces, rehearsal room, production and office space and dressing rooms. Some of these facilities can be shared with the heritage centre and provide a more flexible use of space.

The Council has recently been successful in securing external grant funding of £1.08m (a grant of £615k was confirmed by The Heritage Lottery Fund on 13 December 2012 and on 18 January 2013 ACE confirmed a grant of £465k). The funding will be utilised in 2013/14 for further development of the scheme to Full Business Case.

d) Public Realm

New public realm infrastructure investment is vital to the realisation of the Council’s ambitions. It will provide the glue to bring together the old and the new, creating a cohesive, compact and attractive Town Centre with all the right conditions for stimulating growth. Delivery of this infrastructure concurrently with Metrolink work will produce a ‘big bang’ effect and a real Oldham sense of place.

A transformational Public Realm Implementation Framework has been produced which sets out how the Council’s ambitions for a regenerated public realm can be realised. This covers landscaping, feature lighting projects, public art and statues, and overall improvements of connecting areas. Further public realm improvements will be incorporated into new developments including Metrolink, the Old Town Hall, Hotel Futures and Alexandra Retail Park. There is also a bid currently under consideration for Townscape Heritage Initiative funding to improve the Conservation area which, as referred to above, has already been highlighted within the Councils capital strategy.

e) Eastern Gateway

The eastern gateway into the Town Centre has secured a budget of £1.5m for redevelopment. A full Masterplan is under development to fully utilise the opportunities for investment following the arrival of Metrolink to the area.

f) Strategic Acquisitions within Oldham Town Centre

The Council is keen to take a pro-active approach to regenerating Oldham Town Centre, taking advantage of the current market conditions to acquire properties. In the longer-term, it is hoped that an increased land holding could be used to influence and stimulate development within the Town Centre and separately, allow the Council to benefit from any general market improvements and Metrolink added value. The plan is to acquire what are perceived to be ‘strategic’ properties, those which could potentially be opportune and, post Metrolink, would either be;

� best placed to benefit from any scheme value or; � may benefit the Town Centre by adding value in other areas, or; � adjoin existing Council owned land.

The July 2012 Council capital report included a capital budget to facilitate an acquisition programme over 2012/13 and 2013/14. Some of the resources have been reallocated to the Royton Town Centre project and this has left a balance of £6.734m available for 2013/14.

g) Regeneration Development - FCHO

Statement of Accounts 2012 - 2013

33

The Council is selling an area of land at Union Street / Phoenix Street to First Choice Homes Oldham (FCHO) and will work jointly with FCHO in facilitating the construction of a new landmark office headquarters building.

5.2 Other priority regeneration projects

There are several other priority regeneration projects that the Council has agreed to support. These will require investment of £7.118m over the financial years 2012/13 to 2016/17.

a) Hollinwood / Langtree

This is a proposed redevelopment of vacant sites surrounding junction 22 of the M60 motorway at Hollinwood. The scheme is being brought forward in conjunction with the appointed Strategic Development Partner, Langtree Plc, as well as other key land owners and the stakeholders at this location, via the Hollinwood Board and the establishment of a newly formed Hollinwood Partnership. The Council’s capital costs outlay, to assist in accelerating delivery, is over the period 2012/13 to 2016/17. This, however, will result in capital receipts as end users are secured and developments on Council owned sites are completed, thus minimising the actual net capital contribution required by the Council.

b) Alexandra Retail Park

This scheme will lead to the redevelopment of the existing retail park and adjacent vacant Council owned land. The scheme is in conjunction with the private owners Brookhouse Group. The Council’s capital outlay is expected to be over the period 2012/13 to 2016/17 to fund pre construction fees but there will be costs in kind in relation to land. Further capital investment will be funded through the sale of the Council’s shareholding in Oldham Property Partnerships.

c) Lancaster Club Site

The acquisition of the Lancaster Club by the Council is to facilitate the redevelopment of the site and further redevelopment of the Boundary Park site. The anticipated investment will secure the future of the club within the borough. It is planned that some of this will be self financed, but to be prudent, the impact in the overall position has not relied on the self financing.

The Council has received outline planning permission for the site and is actively seeking developers to acquire all or parts of the residential element of the site and an occupier for the planned commercial unit fronting Broadway. The timing of the capital receipts and the Council's return on investment would be dependent on developer interest, although third party agents have indicated that demand should be present.

d) Working Smarter with Assets

The Council already has programmes for asset rationalisation and asset disposal in place and expenditure required from 2014/15 to 2016/17 is to continue with the initiatives. A fairly modest sum is required to enable the Council to achieve revenue savings, including contributing to targets already in the budget and also generate capital receipts to support the capital programme.

Statement of Accounts 2012 - 2013

34

e) Foxdenton

A Local Development Framework (LDF) for Foxdenton was adopted on 9 November 2011. There has been a site allocation of c.130 acres (including around 10 acres of Council owned land) and this has now been confirmed in planning policy terms as a Business Employment Area. The LDF also accepts the principle that there will be up to 25% residential development on the site in order to help cross-subsidise the provision of infrastructure etc. and to make the wider development viable. A Transport Study for Oldham, including Foxdenton has now been commissioned.

There is the potential for the development to deliver in the region of 300 new homes, over 1m square feet of new business space and the creation up to 1500 jobs over the next 5-10 year period.

f) Neighbourhood Town Halls