…ONE CALL …ONE SOLUTION …ONE SOURCE ANNUAL REPORT 2001 CLARCOR TOTAL FILTRATION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

…ONE CALL

…ONE SOLUTION

…ONE SOURCE

ANNUAL REPORT 2001

CLARCORTOTAL FILTRATION

Worldwide Market Size–$4 billion CLARCOR 2001 Revenues–$251 million

Customers: Aftermarket distributors and dealers, OEM truck and engine manufacturers,major fleets, private label accounts, parts wholesalers and jobbers, railroads,national accounts, truck quick lube and service centers

Product Brands: Baldwin Filters, Hastings Filters, Clark Filter

Major Product Lines: Heavy-duty and light-duty oil, air, hydraulic, coolant, transmission,fuel and desiccant filters, fuel/water separators

Applications: Trucks, buses, automobiles, construction equipment, locomotives, marine equipment, mining equipment, agricultural equipment, industrial equipment

CLARCOR is a global provider of filtration products and services. We have a worldwide customer base, superb product quality, well-known brands, an extensive distribution network, theindustry’s broadest product line and its largest sales force. Our focus on a consumable, disposableproduct that is continually purchased, used and then repurchased provides CLARCOR with a stablesource of recurring business. Our goal is to record compound annual growth rates in earnings pershare of 10% to 15% driven by internal growth programs, cost reduction efforts and acquisitions.

Worldwide Market Size–$25 billion CLARCOR 2001 Revenues–$346 million

Customers: Commercial and industrial distributors, OEM and dealer networks,private label accounts, retailers, national accounts

Environmental Product Brands: Purolator, Airguard, Facet, UAS (United Air Specialists), ATI (Air Technologies, Inc.)Worldwide Market Size–$7 billion

Major Product Lines: Air filters, antimicrobial filters, dust collection systems and filters, electrostatic air filtration, carbon filters, paint overspray filters, HEPA filters,air pollution control systems

Applications: Residences, commercial and industrial buildings, factories and plants,clean rooms, hospitals and medical facilities, industrial machinery,power generation

Process Product Brands: Purolator Facet, Facet, Purolator, FPI (Filter Products, Inc.)Worldwide Market Size–$18 billion

Major Product Lines: Hydraulic filters, sand control filters, aviation fuel filters, waste water filters, fuel/water separators, oil/water separators and coalescers,blood filtration, depth filters, microfiltration and ultrafiltration products

Applications: Airports and aircraft, oil drilling and refining, chemical, paper,pharmaceutical, food and beverage processing, general manufacturing, medical,utilities, office equipment, shipyards, military, power generation, water treatment

INDUSTRIAL/ENVIRONMENTAL FILTRATION

Agricultural and construction vehiclesRailroad locomotives

ENGINE/MOBILE FILTRATION

Heavy-duty and light-duty trucks

CLARCOR 1

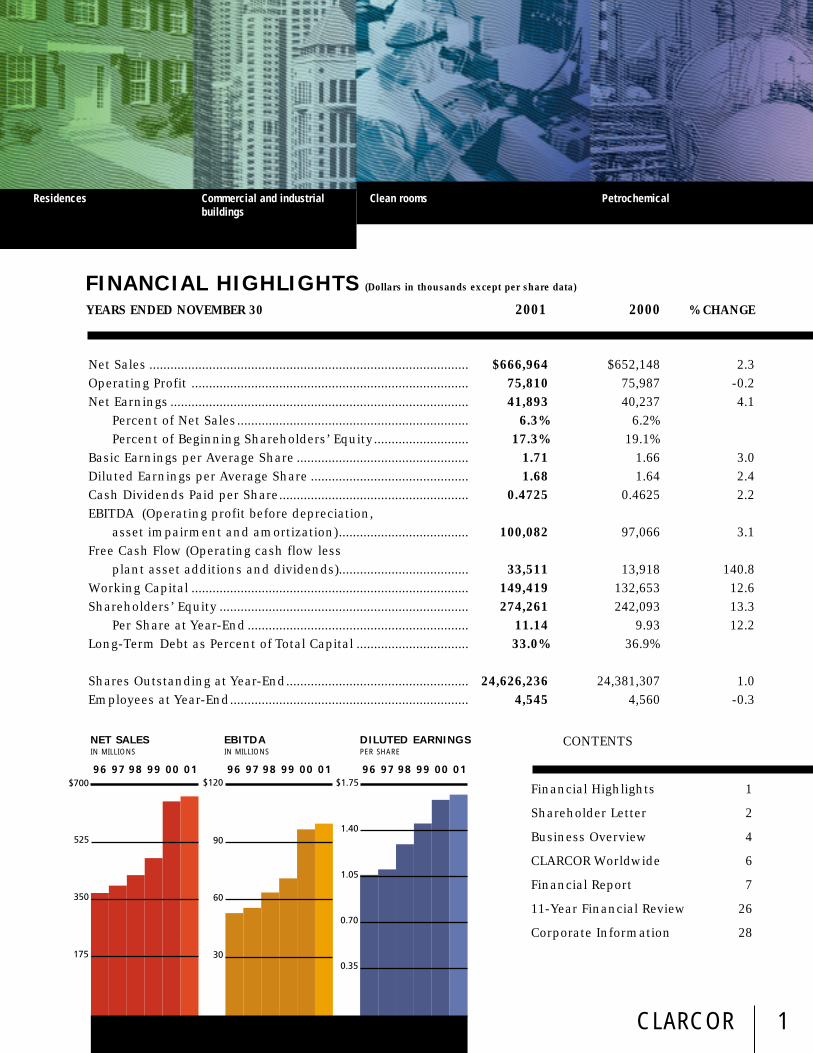

YEARS ENDED NOVEMBER 30 2001 2000 % CHANGE

Net Sales ........................................................................................... $666,964 $652,148 2.3Operating Profit ............................................................................... 75,810 75,987 -0.2Net Earnings ..................................................................................... 41,893 40,237 4.1

Percent of Net Sales.................................................................. 6.3% 6.2%Percent of Beginning Shareholders’ Equity........................... 17.3% 19.1%

Basic Earnings per Average Share ................................................. 1.71 1.66 3.0Diluted Earnings per Average Share ............................................. 1.68 1.64 2.4Cash Dividends Paid per Share...................................................... 0.4725 0.4625 2.2EBITDA (Operating profit before depreciation,

asset impairment and amortization)..................................... 100,082 97,066 3.1Free Cash Flow (Operating cash flow less

plant asset additions and dividends)..................................... 33,511 13,918 140.8Working Capital ............................................................................... 149,419 132,653 12.6Shareholders’ Equity ....................................................................... 274,261 242,093 13.3

Per Share at Year-End ............................................................... 11.14 9.93 12.2Long-Term Debt as Percent of Total Capital ................................ 33.0% 36.9%

Shares Outstanding at Year-End.................................................... 24,626,236 24,381,307 1.0 Employees at Year-End.................................................................... 4,545 4,560 -0.3

FINANCIAL HIGHLIGHTS (Dollars in thousands except per share data)

CONTENTS

Financial Highlights 1

Shareholder Letter 2

Business Overview 4

CLARCOR Worldwide 6

Financial Report 7

11-Year Financial Review 26

Corporate Information 28

Residences Commercial and industrialbuildings

Clean rooms Petrochemical

NET SALESIN MILLIONS

EBITDAIN MILLIONS

DILUTED EARNINGSPER SHARE

CLARCOR2

n my letter to you last year I wrote,“We approach 2001 optimistically, butwe are conscious of a slowing world

economy.” In addition to a recession in2001, none of us could have imagined theevents of September 11th and its impacton our country and our economy. Still,CLARCOR had a solid fiscal 2001. Sales,earnings and cash flow all ended higherin 2001 than in fiscal 2000 and we madesubstantial progress in building our TotalFiltration Program. Moreover, even after asignificant acquisition, we strengthenedour balance sheet with increasedshareholders’ equity and lower borrowings.

Overall filter markets continue to growabout 2-3% faster than the economy. There is anincreasing demand for a cleaner environment andworkplace, and filter maintenance requirements fortransportation and manufacturing equipment alsocontinue to expand. The majority of the products we sellare consumable and disposable, and are sold mostly tothe aftermarket. Since our customers will always need tomaintain their facilities and equipment, this provides uswith a stable base of business when the economy isslow. Equally important, we have a strong platform togrow our business when the economy recovers.

THE CLARCOR TOTAL FILTRATION PROGRAM

I wrote last year about the CLARCOR Total FiltrationProgram and our initial efforts to become the total filtersupplier to companies throughout North America. TheTotal Filtration Program is one of our principal growthstrategies: to provide a company’s entire filterrequirements, not just certain filters for specificapplications. The worldwide filtration market is verylarge with sales approaching $30 billion annually. TheCLARCOR Total Filtration Program now gives us theopportunity to sell to nearly all of this market.

Let me tell you some of the things we accomplished in 2001:

• CLARCOR became the exclusive filter supplier to a $13billion manufacturing company for its 40 plants in NorthAmerica. After each plant is converted to the CLARCORprogram, we expect customer purchases to exceed $4 millionannually. Before this year, CLARCOR had not sold filters tothis company.

• CLARCOR became the exclusivefilter supplier to a $20 billiondiversified manufacturing companywith over 150 facilities in NorthAmerica. We will supply thefiltration needs for itsmanufacturing plants, warehousesand offices. We expect that totalcustomer purchases will exceed $5million annually.

• We developed Total FiltrationPrograms for specific industries andapplications, including power plants,petrochemical companies andintegrated suppliers. By the end of2001, we had signed several total

filter contracts in these areas and were negotiating filtercontracts with additional companies. These contracts arewith companies which previously had little or no businesswith CLARCOR.

• In June 2001, we strengthened our Total FiltrationProgram with the acquisition of Total Filtration Services(TFS). The leading total filter supplier to the North Americanautomotive industry, TFS serves over 90 manufacturing andassembly plants. TFS has developed the logistics andtechnical support systems critical to providing acomprehensive total filter management program tocustomers with multiple locations and sophisticatedfiltration requirements.

We are currently presenting the CLARCOR Total FiltrationProgram to many potential customers. Some are currentcustomers who already buy part of their filtration needsfrom CLARCOR. Some are companies who have neverpreviously purchased our filters, and some are ourcurrent distributors who previously purchased only oneof our filter brands. What they find attractive about ourprogram is the ease and convenience of ordering, theexpertise we have to provide the right filter solutionwherever they operate, the breadth and quality of ourfilters, and our ability to offer the level of service andresponsiveness they require. The appeal of the TotalFiltration Program is obvious to every company anddistributor we speak to. It makes their life simpler and,in most cases, will save them money.

OUR FISCAL 2001 OPERATING RESULTS

Overall, we were pleased with this year’s results.However, growth was less than in prior years, and theincreases in sales and earnings were less than weexpected when the year began. Despite the slowingeconomy which affected most industrial companies in2001 and the aftermath of the terrible events of

Norman E. Johnson,Chairman, President and Chief Executive Officer

I

TO OUR SHAREHOLDERS...

CLARCOR 3

September 11th, sales grew by 2.3% and net earnings by4.1%. After capital expenditures for new facilities andequipment, investment in working capital and paymentof dividends, free cash flow more than doubled to $34million, a new record.

We paid particular attention to discretionary spendingas the economy slowed during the year. As a result, wereduced selling and administrative costs in 2001 as apercentage of sales below 2000 levels. We believe thiswill benefit us when the economy recovers.

In addition to our focus on developing the TotalFiltration Program, we also accomplished a lot in otherareas in 2001. Several filter manufacturing plants thatopened during 2000 in our Industrial/Environmentalsegment became progressively more efficient andproductive throughout the year. By year-end, each ofthese plants was profitable, and we expect they willbecome more so in 2002. We developed more new filterproducts than we had in any other year in our history.When it became apparent that 2001 was going to be adifficult year, our operating companies initiated newcost reduction programs. We successfully beganmanufacturing our electrostatic air pollution controlsystems in our Weifang, China plant for sale in Chinaand throughout Southeast Asia. With increased oildrilling in 2001, sales of our sand control filters grew,and we introduced a less costly version for certainenvironments, which should increase sales further.Overall, 2001 was a solid year for CLARCOR and providesa base for greater growth as we move into 2002.

OUR PEOPLE

We were fortunate to have Keith Wandell join our Boardof Directors in March 2001. Keith is the President of theAutomotive Systems Group, Battery at Johnson Controls,Inc. in Milwaukee, Wisconsin. His experience inoperations and marketing is an asset to CLARCOR.

At our Annual Meeting in March 2002, Milt Brown willretire from our Board of Directors. Milt joined our Boardin 1990 and we deeply appreciate the counsel andguidance he has given us over the years.

I am very pleased that we were able to hire Sam Ferriseas the new President for our Baldwin Filters operationand Rich Larson as the new President for United AirSpecialists. Both Sam and Rich bring great experience,enthusiasm and drive to these companies. We arefortunate to have both working with us.

I also want to recognize all the employees at CLARCOR.Through their perseverance, imagination anddedication to delivering continuing value to our

customers, they have made CLARCOR, over a period ofnearly 100 years, into what I firmly believe is the bestcompany in our industry.

OUR FUTURE

As the economy recovers, we expect 2002 will be a betteryear than 2001 and that both sales and net earnings willgrow at a faster rate than in 2001. We also expectCLARCOR to grow faster than the filtration industry. Theinvestments we have made in people, systems andmarketing programs for our Total Filtration Program willprovide an increasing return over the next several years.

The result is that internal growth will come from two areas:

• First, it will come from the individual efforts of eachcompany developing and selling its own products to its owncustomers with new product development and aggressivemarketing programs.

• Second, each company will work, through the TotalFiltration Program, to reach those customers seekingcomplete filter solutions that require the combined effortsand product offerings of all of our operating companies.

Over the years, one of CLARCOR’s hallmarks has beenour consistent growth and profitability. Sales haveincreased for 15 consecutive years and profits for nineconsecutive years. We have a strong foundation: aworldwide customer base, superb product quality, anextensive distribution network, the industry’s broadestproduct line and its largest sales force. Our filters areused everywhere you look. Our focus on a consumable,disposable product that is continually purchased, usedand then repurchased provides CLARCOR with a strongsource of recurring business. When combined with ourTotal Filtration Program, I am tremendously excitedabout our future prospects and the ability of ourcompany to bring value to our shareholders, ourcustomers and our employees.

Norman E. Johnson,Chairman, President and Chief Executive Officer

February 1, 2002

CLARCOR4

he CLARCOR Total Filtration Program enablesour customers to purchase 100% of their filterrequirements from one company. Whether the

filters are used to clean fluids used in manufacturingequipment; to purify the air in offices, factories,hospitals and homes; to protect trucks, construction and farm equipment, automobiles and locomotives; or to provide the specialized filtration needs for oil drilling,power plants, pharmaceutical production, aviation refueling, or biohazard air contamination, CLARCOR provides the filters to meet these and many other filtration needs.

We believe CLARCOR has the largest number of filters for more filter applications than any other company in the world. For our customers, this meansthat rather than purchasing filters from a variety of different suppliers, they can purchase their entire filterneeds from one company. With more than 20 filter manufacturing plants, dozens of warehouses, over 25company-owned filter outlets, thousands of distributorsthroughout North America and the largest filter salesforce in the industry, CLARCOR provides customers withthe right filter at the right location at the right time.

OUR ACCOMPLISHMENTS IN 2001

• Expanded the CLARCOR Total Filtration Program with new customers, including several Fortune 500 companies. Equally important, we began discussionswith a number of the largest corporations in the UnitedStates about the Program’s benefits and expect to signadditional agreements in 2002.

• Acquired Total Filtration Services (TFS) in June. TFS provides filtration management services to all of themajor automotive companies and has developed theproduct procurement and delivery systems critical tomaking the Total Filtration Program successful.

• Through continual efforts during the year to reduce costs, our selling and administrative expenseswere a lower percentage of sales in 2001 than they were in 2000. Maintaining appropriate cost disciplinesregardless of the state of the economy is an importantobjective for CLARCOR.

• Significantly increased productivity in our newer manufacturing and distribution facilities and we expectfurther productivity gains in 2002.

• Other accomplishments:

• Developed a new, less costly version of our successful sand control filter which is used extensivelyin the oil drilling industry.

• Secured the largest number of FAA approvals everreceived by CLARCOR for aerospace filter applications.

• Began manufacturing our electrostatic air pollution control systems in our Weifang, China plantfor sale throughout China and Southeast Asia. Demand for these systems in this region has greatly exceededour expectations.

• Set a new record in 2001 by generating free cash flow of $34 million, after investments in new plant andequipment and working capital and payment of divi-dends. This enabled us to increase the dividend to ourshareholders for the 18th consecutive year, reduce ourbank borrowings and pay for a significant acquisition.

• We compare the filters youcurrently use to the filters manufactured in ourplants and available through our distribution net-work which is the largest in the industry.

• A team of experienced filtration experts will visit yourfacilities to make a record of your filter applications andassess your filtration needs. We will recommend alterna-tives to improve filter efficiency and longevity and will pro-vide a copy of our report for your review.

One Call …

ProductList …

CrossReference …

T

…more filter products

for more filter applications

in more filter markets

than anyone else

anywhere!

• A single call to CLARCOR Total Filtration puts theresources and expertise of our filtration manufacturing,distribution and service companies at your disposal.

TOTAL FILTRATION:WHAT IT IS AND HOW IT WORKS…

CLARCOR 5

OUR GOALS FOR 2002

• Our #1 goal for 2002 is to grow the CLARCOR TotalFiltration Program. We will allocate resources to expand our product procurement systems, our product development efforts and our distribution systems, andto train our people to make the Program the single, bestway for companies throughout the world to meet alltheir filtration needs.

• We will offer TFS’ filtration management programs to non-automotive industrial companies throughCLARCOR’s extensive distribution and sales network.

• We will focus on continuing to improve our manufacturing productivity by rationalizing plant capacity. Though we have made great strides in the pastyear in increasing production efficiencies and achievingcost savings, we believe there are still significant opportunities to do even better.

• Cost reductions have always been a way of life atCLARCOR. This will continue in 2002. We expect the U.S.economy to recover later this year, but as in 2001, wewill work throughout the year to reduce our costs. Ourgoal is the same as last year: to reduce our costs even assales increase.

• Though we already offer more filters and more filterapplications than any other company in our industry, in2002 we will increase our new product developmentefforts. In addition, our acquisition strategy will focus on opportunities to further expand our filter range.

• Financial strength continues to be one of CLARCOR’shallmarks. We operate CLARCOR prudently with a constant focus on providing increasing value to ourshareholders. We expect to generate significant free cash flow in 2002, as we did in 2001, which we will useto pay dividends to our shareholders, expand our operations in North America and internationally, and to further reduce our outstanding borrowings.

THE CLARCOR STRATEGY

Our strategy is two-fold:

• Each of our operating units will strive to become thebest filter company within its own market segment. Eachwill work to always be the lowest cost manufacturer,with the highest quality and most extensive product linefor our customers. Our companies will continue to investto strengthen their product brands and to differentiatetheir filter offerings from competitors.

• Our companies will work together to promotethe CLARCOR Total Filtration Program. Drawing on the broadest product range, the largest sales force and the most extensive distribution network in the filter industry, CLARCOR can offer its customers the ability to purchase 100% of their filter requirements from onecompany. For our customers, the advantages are obvious: a simpler purchasing experience, consistentlyhigh product quality, cost savings and the technicalexpertise and experience to solve the most difficult filtration problems.

• We will then provide you with a quotation to meet your entire filtrationrequirements whether to clean the air in your buildings, to provide filtra-tion for your transportation fleet and production machinery or to meetyour specialized filtration needs.

• CLARCOR Total Filtration will reduce your costs, simplify your purchasingand reduce the number of your suppliers. CLARCOR Total Filtration is yoursingle source supplier for all your filtration needs: Total Coverage, TotalQuality, Total Service, Total Savings, Total Innovation.

ONE SOURCE …

FacilitySurvey… One Solution …

THE CLARCOR TOTAL FILTRATION VISION“We will be the best filter company in the

world, with the widest product offering,

the highest quality products and unsur-

passed customer service. Above all, we will

strive to meet the entire filter needs of

every one of our customers at any time

and at any place.”

CLARCOR6

CLARCOR WORLDWIDE

CLARCOR CORPORATE OFFICESRockford, Illinois

ENGINE/MOBILE FILTRATION

BALDWIN FILTERSHeadquarters:

Kearney, NebraskaOther U.S. Locations:

Gothenburg, NebraskaYankton, South Dakota

International Locations:AustraliaBelgiumChinaMexicoSouth AfricaUnited Kingdom

CLARK FILTERHeadquarters:

Lancaster, Pennsylvania

PACKAGING

J.L. CLARKHeadquarters:

Rockford, IllinoisOther U.S. Locations:

Lathrop, CaliforniaLancaster, Pennsylvania

AIRGUARDHeadquarters:

Louisville, Kentucky Other U.S. Locations:

Birmingham, AlabamaCorona, CaliforniaCommerce City,ColoradoAtlanta, GeorgiaRockford, Illinois New Albany, IndianaOttawa, KansasCampbellsville & Jeffersontown, KentuckyKansas City, MissouriGastonia, North CarolinaCincinnati, Columbus & Toledo, OhioPortland, OregonNashville, TennesseeDallas, Texas

International Locations:MalaysiaSingapore

FACET INTERNATIONALU.S. Locations:

Stillwell & Tulsa,Oklahoma

International Locations:AustraliaFranceGermanyItalyNetherlandsSpainUnited Kingdom

FILTER PRODUCTS, INC.Headquarters:

Sacramento, California

PUROLATOR AIR FILTRATIONHeadquarters:

Henderson, North CarolinaOther U.S. Locations:

Fresno, Hayward & Sacramento, CaliforniaDavenport, IowaWichita, KansasSparks, NevadaMetuchen, New JerseyKenly, North CarolinaFairfax, VirginiaAuburn, Washington

INDUSTRIAL/ENVIRONMENTAL FILTRATION

PUROLATOR FACET, INC.Headquarters:

Greensboro, North Carolina

TOTAL FILTRATION SERVICESHeadquarters:

Rochester Hills, MichiganOther U.S. Locations:

Cincinnati, OhioGoodlettsville, Tennessee

International Locations:Mexico

UNITED AIR SPECIALISTSHeadquarters:

Cincinnati, OhioOther U.S. Locations:

Phoenix, ArizonaAnaheim & Hayward,CaliforniaLouisville, KentuckyTroy, MichiganJackson, MississippiHouston, Texas

International Locations:GermanyUnited Kingdom

CLARCOR’s operating results for fiscal 2001 reached recordlevels for sales, cash flow and earnings. Fiscal 2001 includedsix-month results from Total Filtration Services, Inc. (TFS)which was acquired at the beginning of the third quarter offiscal 2001. This acquisition increased CLARCOR’s sales andoperating profit, and after related interest and amortizationexpenses, also increased net earnings and diluted earningsper share in fiscal 2001. Purchase accounting adjustments forthe acquisition will be completed in fiscal 2002 as describedin Note C to the Consolidated Financial Statements. TheCompany also made several smaller acquisitions in fiscal 2000that were not material to the Company’s operating results.Fiscal 2000 included the full-year results from three industrialfiltration companies (hereafter, the Industrial FiltrationAcquisitions) that were acquired at the beginning of thefourth quarter 1999. TFS, the Industrial Filtration Acquisitionsand the smaller fiscal 2000 acquisitions are included in theIndustrial/Environmental Filtration segment.

The information presented in this financial review should be read in conjunction with other financial information pro-vided throughout this 2001 Annual Report. The following dis-cussion of operating results focuses on the Company’s threereportable business segments: Engine/Mobile Filtration,Industrial/Environmental Filtration and Packaging. Fiscal2001 was a fifty-two week year for the Company and fiscalyears 2000 and 1999 were fifty-three and fifty-two weekyears, respectively.

OPERATING RESULTS SalesNet sales in fiscal 2001 were $667.0 million, a 2.3% increasefrom $652.1 million in fiscal 2000. The 2001 net sales includedapproximately $28 million for TFS which was acquired at thebeginning of the third quarter. Fiscal 2000 included approxi-mately $12-$13 million in additional sales compared to fiscal2001 as fiscal year 2000 was a fifty-three week year for theCompany. The 2001 sales increase was the 15th consecutiveyear of sales growth for the Company. Net sales grew 36.5% in2000 over the 1999 level of $477.9 million primarily due to afull year of sales from the Industrial Filtration Acquisitionscompared to 1999 which included only the fourth quarteractivity. Excluding the additional sales from the IndustrialFiltration Acquisitions, sales increased approximately 11% in2000 from 1999.

Comparative net sales information related to CLARCOR’soperating segments is shown in the following tables.

2001 vs. 2000Change

NET SALES 2001 % Total $ %Engine/Mobile Filtration .................... $ 251.0 37.6% $ (8.8) -3.4%Industrial/Environmental Filtration .... 346.4 52.0% 26.7) 8.3%Packaging ............................................ 69.6 10.4% (3.0) -4.1%

Total ................................................ $ 667.0 100.0% $14.9 2.3%

2000 vs. 1999

Change

NET SALES 2000 % Total $ %

Engine/Mobile Filtration........................ $259.8 39.9% $ 21.1 8.8%

Industrial/Environmental Filtration .... 319.7 49.0% 144.8 82.8%

Packaging ................................................ 72.6 11.1% 8.3 12.9%

Total .................................................. $652.1 100.0% $174.2 36.5%

The Engine/Mobile Filtration segment’s sales decreased 3.4% in 2001 from 2000, or approximately 1.5%, excluding theadditional week in fiscal 2000. The segment’s sales werelower than expected for fiscal 2001 due to the slowdown inthe U.S. economy that led to competitive pricing pressuresand a reduction in inventory levels and product demand byour customers. Fiscal 2000 sales included increases for heavy-duty, light-duty and railroad filter products from bothdomestic and international markets compared to fiscal 1999.The segment’s sales were favorably impacted in 2000 by newproduct introductions, additional OEM sales, and penetrationinto new domestic and international distribution channels,primarily through sales to quick lube and truck service cen-ters, fleets and automotive parts buying groups.

The Company’s Industrial/Environmental Filtration segmentrecorded an 8.3% increase in sales in 2001 over 2000. Includedin 2001 were sales of approximately $28 million for sixmonths of activity from TFS. Excluding sales from TFS andthe additional week in fiscal 2000, sales for the segmentincreased approximately 1.5% compared to fiscal 2000. Fiscal2001 also included additional sales from new products intro-duced late in fiscal 2000 and greater distribution coverage forenvironmental filters. This increase was partially offset bylower sales due to the U.S. economic recession which primari-ly affected sales of filtration equipment and systems. Thesegment’s sales increased 82.8% in 2000, or excluding acquisi-tions, approximately 11% over fiscal 1999. The 11% salesincrease resulted primarily from higher sales of environmen-tal air filtration and electrostatic air quality products.

The Packaging segment’s sales of $69.6 million decreased 4.1% in fiscal 2001 from 2000. Included in 2001 was a non-recurring $7.0 million payment arising from the early termi-nation of a supply and license agreement by a customer.Sales to this customer of plastic closures decreased substan-tially beginning in the first quarter 2001. The segment wasunable to completely replace this business during the yearalthough sales increased for non-promotional metal packag-ing products and flat sheet decorating. The segment focuseson sales of non-promotional packaging products such asmetal closures for food and beverage containers, wire spools,and film and battery cartridges. This focus resulted in a 12.9% increase in sales in 2000 from 1999.

Operating ProfitOperating profit of $75.8 million in 2001 was slightly lowerthan $76.0 million in 2000. Operating profit in 2001 includedapproximately $1.2 million from the TFS acquisition and oper-ating profit in 2000 included approximately $1.5 million ofadditional profit due to the fifty-three week fiscal year in2000. Operating profit increased 35.5% in fiscal 2000 from1999. Excluding the Industrial Filtration Acquisitions, fiscal

CLARCOR 7

(Dollars in millions except per share data)

FINANCIAL REVIEW

2000 operating profit rose approximately 19% over fiscal 1999.Operating margin was 11.4% of sales in 2001 and 11.7% ofsales in both fiscal 2000 and 1999.

In both fiscal 2001 and 2000, continued cost reductions,improved manufacturing productivity and the integration ofacquired businesses positively impacted operating margin.These profit improvements offset, in part, competitive pricingpressures and cost increases the Company experienced forenergy, employee insurance and pensions. Selling and admin-istrative expenses were reduced to $119.7 million in 2001 from$122.3 million in 2000 primarily due to discretionary costreductions and reduced incentive compensation expenses.Selling and administrative expenses increased to $122.3 mil-lion in 2000 from $92.5 million in 1999 primarily due to theIndustrial Filtration Acquisitions that were included for anadditional nine months in 2000 and related amortizationcharges, and also due to new product development and salesand marketing programs. Although foreign currency fluctua-tions reduced sales and operating profit in fiscal 2001 and2000, currency adjustments did not have a material impact onconsolidated operating profit in 2001, 2000 or 1999.

Comparative operating profit information related to theCompany’s business segments is as follows.

2001 vs. 2000Change

OPERATING PROFIT 2001 % Total $ %Engine/Mobile Filtration .................... $ 51.8 68.3% $ 2.6 5.3%Industrial/Environmental Filtration .... 16.8 22.1% (1.6) -9.1%Packaging ............................................ 7.2 9.6% (1.2) -13.4%

Total ................................................ $ 75.8 100.0% $ (0.2) -0.2%

2000 vs. 1999

Change

OPERATING PROFIT 2000 % Total $ %

Engine/Mobile Filtration........................ $ 49.2 64.7% $ 5.6 12.8%

Industrial/Environmental Filtration .... 18.4 24.3% 13.3 260.0%

Packaging ................................................ 8.4 11.0% 1.0 13.9%

Total .................................................. $ 76.0 100.0% $19.9 35.5%

OPERATING MARGIN AS A PERCENT OF NET SALES 2001 2000 1999

Engine/Mobile Filtration........................ 20.6% 18.9% 18.3%

Industrial/Environmental Filtration .... 4.8% 5.8% 2.9%

Packaging ................................................ 10.4% 11.6% 11.5%

Total .................................................. 11.4% 11.7% 11.7%

Operating profit for the Engine/Mobile Filtration segmentincreased to $51.8 million in 2001 from $49.2 million in 2000,an increase of 5.3%. Operating margin as a percent of sales infiscal 2001 improved to a record 20.6% from 18.9% in 2000 and18.3% in 1999. In fiscal 2001, the segment’s operating marginimproved as a result of material and labor cost reductions andimproved productivity in its main distribution and light-dutyfilter manufacturing facilities. These improvements morethan offset increased energy and employee insurance costsand competitive pricing pressures. In fiscal 2000, the seg-ment’s operating profit was favorably impacted compared to

1999 by higher sales volumes, productivity improvements andreduced legal costs, which more than offset the negativeimpacts of increased energy, labor and raw material costs.

The Industrial/Environmental Filtration segment’s operatingprofit in 2001 was $16.8 million, a decrease from $18.4 millionin 2000 primarily as a result of start-up costs early in fiscal2001 related to two new production facilities and reducedsales of filtration equipment and systems. The start-up costsassociated with the new facilities and new product introduc-tions decreased during the third quarter of 2001 as productionefficiencies and capacity utilization improved. Fiscal 2001also included approximately $1.2 million of operating profitfrom TFS for the six-month period since the acquisition. Thesegment’s operating profit of $18.4 million in 2000 increasedsignificantly from $5.1 million in 1999. Approximately $9 mil-lion of the increase was due to the Industrial FiltrationAcquisitions. The remaining increase of $4.3 million, or anincrease of approximately 90%, was due to improvements inpreviously existing businesses. The increased profit in thesebusinesses reflected a significantly higher sales volume ofindustrial and environmental air filtration products, improvedmanufacturing operations and significant reductions in over-head and administrative costs, many of which were imple-mented beginning in fiscal 1999.

The Packaging segment’s operating profit in fiscal 2001decreased to $7.2 million from $8.4 million in fiscal 2000.Fiscal 2001 results included approximately $7.0 million relatedto a non-recurring termination payment from a customer thatwas reduced by $2.4 million for related asset impairmentcharges. Excluding this item, operating profit was lower than2000 due to the lower sales of plastic closures to this cus-tomer, reduced capacity utilization, higher energy and pen-sion costs, and increased costs related to the installation ofnew lithography equipment in early 2001. Due to difficultieswith the start-up of this new equipment, plant utilization wasreduced throughout 2001 from expected levels and costs wereincurred for product scrap and rework. In fiscal 2000, the seg-ment’s operating profit increased to $8.4 million from $7.4million in 1999, or 13.9%. This increase resulted from bettercapacity utilization, a significant increase in sales volume andreduced discretionary spending.

Other Income & ExpenseNet other expense totaled $10.1 million in 2001, $12.5 millionin 2000 and $0.5 million in 1999. Interest expense of $10.3million was lower in 2001 compared with $11.5 million in2000, due to declining interest rates and reduced overall bor-rowings during the year. Interest expense increased in 2000from $3.7 million in 1999 due to additional borrowings in thefourth quarter of 1999 for the Industrial FiltrationAcquisitions. Interest income was $0.7 million for both 2001and 2000, which was reduced from $1.5 million in 1999 as aresult of lower interest rates and lower average cash andshort-term cash investment balances primarily due to the useof cash for acquisitions in 1999. Currency gains of $0.2 mil-lion in 2001 and losses of $1.2 million in 2000 resulted prima-rily from fluctuations in European currency exchange ratesagainst the U.S. dollar. There were no significant gains orlosses on the disposition of plant assets in fiscal 2001 or 2000;however, a gain of $1.7 million recorded in 1999 was primarilyfrom the sale of a building.

CLARCOR8

(Dollars in millions except per share data)

FINANCIAL REVIEW

Provision for Income TaxesThe provision for income taxes in 2001 was $23.8 millionand resulted in an effective tax rate of 36.2%, which wasslightly lower than the effective tax rate of 36.5% in 2000.The effective tax rate was 36.2% in 1999. The effective taxrate in 2002 is expected to be approximately the same rateas recorded in 2001.

Net Earnings and Earnings Per ShareNet earnings were a record $41.9 million in 2001, or dilutedearnings per share of $1.68, compared to $40.2 million, or $1.64per diluted share in 2000. Net earnings in 1999 were $35.4 mil-lion, or $1.46 per diluted share. Diluted average shares out-standing for fiscal 2001 were 24,892,062 compared to 24,506,171for 2000, an increase of 1.6%. Diluted average shares outstand-ing for fiscal 1999 were 24,313,607. The increase in outstandingshares was primarily due to stock options.

FINANCIAL CONDITIONCorporate LiquidityThe Consolidated Statements of Cash Flows are shown on page15, and this discussion of corporate liquidity should be read inconjunction with information presented in those statements.

Cash and short-term cash investments decreased to $7.4 mil-lion at year-end 2001 from $10.9 million at year-end 2000.Cash provided by operating activities totaled $63.3 million in2001 compared to $54.1 million in 2000 and $38.6 million in1999. As a result of an increased emphasis on working capitalmanagement during fiscal 2001, accounts receivable andinventories decreased excluding the TFS assets acquired inthe third quarter 2001. Accounts receivable and inventoriesincreased during 2000 due to the higher level of businessactivity throughout the Company. Other current assets andpension liabilities were reduced in 2000 as restricted trustassets were used for the payment of nonqualified pension lia-bilities. Depreciation and amortization increased in fiscal2000 from 1999 primarily due to the fourth quarter 1999Industrial Filtration Acquisitions.

The Company used cash of $51.4 million for investing activi-ties in 2001, $42.1 million in 2000 and $160.7 million in 1999.Cash used for acquisitions in 2001, primarily for TFS, totaled$33.4 million, while cash used for the acquisition of severalsmall filtration businesses in 2000 totaled $12.7 million. Infiscal 1999, $142.7 million, net of cash acquired, was used foracquisitions, primarily the Industrial Filtration Acquisitions.Additions to plant assets totaled $18.2 million in 2001 andincluded residual payments on several projects begun in fis-cal 2000. Additions to plant assets in 2000 totaled $29.0 mil-lion and included payments on new state-of-the-art lithog-raphy equipment, the purchase and refurbishment of a man-ufacturing building in Campbellsville, Kentucky, and addi-tional manufacturing capacity throughout the Company.Additions to plant assets in 1999 of $21.8 million includedadding plant capacity and the completion of an expansion toa manufacturing and distribution facility in Kearney,Nebraska. Cash of $3.9 million was received in 1999 primari-ly from the sale of a building.

Net cash used in financing activities totaled $15.3 million and$15.9 million in 2001 and 2000, respectively. The Companyreceived $8.0 million in 2001 from the issuance of industrialrevenue bonds related to the manufacturing facility inCampbellsville, Kentucky. During 2001 the Company also bor-rowed an additional $27.5 million against a revolving creditagreement, primarily for the TFS acquisition; however, pay-ments of $36.5 million were made during the year whichreduced the total borrowed from the agreement at year-end2001 to $107.0 million. The Company borrowed a net addi-tional $1.0 million against the revolving credit agreement dur-ing 2000. Net cash provided by financing activities in fiscal1999 totaled $103.5 million and included $115.0 million in bor-rowings used for the Industrial Filtration Acquisitions. TheCompany did not repurchase any shares in 2001 or 2000 underthe remaining authorization of approximately 920,000 sharesfrom the December 1997 Board of Directors’ approved stockrepurchase plan. The Company purchased 50,000 shares ofCLARCOR common stock for $0.9 million in 1999. Dividendpayments totaled $11.6 million, $11.2 million and $10.8 mil-lion in 2001, 2000 and 1999, respectively. Payments on long-term debt were $5.3 million in 2001, $7.0 million in 2000 and$0.5 million in 1999.

CLARCOR’s current operations continue to generate cash andsufficient lines of credit remain available to fund currentoperating needs, pay dividends, provide for additions and thereplacement of necessary plant facilities, and to service andrepay long-term debt. Capital expenditures for normal facilitymaintenance, productivity improvements and new productsare expected to be approximately $21-$23 million in fiscal2002. Due to the September 1999 Industrial FiltrationAcquisitions, a $185.0 million multicurrency revolving creditfacility was established with several financial institutions. Ofthe $185.0 million, a total of $107.0 million of the credit facili-ty was outstanding as of year-end 2001 and $11.2 million wasoutstanding for letters of credit. Principal payments on long-term debt will be approximately $5.6 million in 2002 based onscheduled payments in current debt agreements. No pay-ments are required in fiscal 2002 on the multicurrency revolv-ing credit facility and the Company is in compliance with allcovenants related to the credit facility, as described in Note Hto the Consolidated Financial Statements. Other than operat-ing leases, as described in Note I to the Consolidated FinancialStatements, the Company has no material off-balance sheetarrangements. Commitments for noncancellable leases in2002 total approximately $7.3 million.

While customer demand for our products will affect operatingcash flow, the Company is not aware of any known trends,demands or reasonably likely events that would materiallyaffect cash flow from operations in the future. It is possiblethat business acquisitions or dispositions could be made inthe future that may require changes in the Company’s debtand capitalization.

Capital ResourcesThe Company’s financial position at November 30, 2001 con-tinued to be sufficiently liquid to support current operations.Total assets increased to $530.6 million at the end of fiscal2001, an increase of 5.7% from the year-end 2000 level of$501.9 million. Total current assets increased to $244.4 mil-

CLARCOR 9

lion from $230.5 million at year-end 2000 and total current lia-bilities decreased to $94.9 million from $97.8 million at year-end 2000. The current ratio was 2.6 at year-end 2001 com-pared to 2.4 at year-end 2000. Excluding the TFS assetsacquired at the beginning of the third quarter 2001, accountsreceivable and inventories decreased during fiscal 2001 par-tially due to increased emphasis on working capital manage-ment. Current liabilities at year-end 2001 were lower primari-ly due to reduced accruals for incentive plans and incometaxes. Plant assets decreased to $137.3 million as a result ofincreased depreciation and the write-off of certain Packagingmanufacturing equipment, which offset the plant asset addi-tions made during the year. Acquired intangibles increased to$116.7 million primarily due to the acquisition of TFS duringfiscal 2001. Current liabilities include accruals for costs relat-ed to litigation matters arising in the normal course of busi-ness. See Note L in the Notes to Consolidated FinancialStatements for further information on these matters.

Long-term debt of $135.2 million at year-end 2001 includedthe borrowing against the revolving credit facility.Shareholders’ equity increased to $274.3 million from $242.1million at year-end 2000. The increase in shareholders’ equityresulted primarily from net earnings of $41.9 million offset bydividend payments of $11.6 million, or $0.4725 per share.Long-term debt decreased to 33.0% of total capitalization atyear-end 2001, compared to 36.9% at year-end 2000.

At November 30, 2001, CLARCOR had 24,626,236 shares ofcommon stock outstanding at $1.00 par value, compared to24,381,307 shares outstanding at the end of 2000.

OTHER MATTERSMarket RiskThe Company’s market risk is primarily the potential lossarising from adverse changes in interest rates. TheCompany’s long-term debt obligations are primarily at vari-able LIBOR-associated rates and fixed interest rates and aredenominated in U.S. dollars. In order to minimize the long-term costs of borrowing, the Company manages its interestrate risk by monitoring trends in rates as a basis for deter-mining whether to enter into fixed rate or variable rateagreements. In addition, during fiscal 2000 the Companyentered into several interest rate agreements related to therevolving credit agreement as described in Note H to theConsolidated Financial Statements. Market risk is estimatedas the potential change in fair value of the Company’s long-term debt obligations resulting from a hypothetical 1%increase in interest rates. A hypothetical 1% increase ininterest rates on the Company’s variable rate agreementswould adversely affect fiscal 2002 net earnings and cashflows by approximately $0.4 million and reduce the fair valueof fixed rate long-term debt, as measured at November 30,2001, by approximately $0.3 million. Last year, a hypothetical1% increase in interest rates would have adversely affectedfiscal 2001’s net earnings and cash flows by approximately$0.3 million and reduced the fair value of fixed rate long-term debt by approximately $0.9 million.

Although the Company continues to evaluate derivativefinancial instruments, including forwards, swaps and pur-chased options, to manage foreign currency exchange rate

changes, the Company did not hold derivatives for tradingpurposes during 2001, 2000 or 1999. The Company uses for-ward exchange contracts on a limited basis to manage foreigncurrency exchange risk related to certain transactions, prima-rily equipment purchases denominated in currencies otherthan U.S. dollars. As a result of increased foreign sales andbusiness activities, the Company will continue to evaluate theuse of derivative financial instruments to manage foreign cur-rency exchange rate changes in the future.

Critical Accounting PoliciesThe Company’s critical accounting policies, including theassumptions and judgments underlying them, are disclosed inthe Notes to the Consolidated Financial Statements. Thesepolicies have been consistently applied in all material respectsand address such matters as revenue recognition, depreciationmethods, inventory valuation, asset impairment recognition,business combination accounting and pension and postretire-ment benefits. While the estimates and judgments associatedwith the application of these policies may be affected by dif-ferent assumptions or conditions, the Company believes theestimates and judgments associated with the reportedamounts are appropriate in the circumstances.

Recent Accounting PronouncementsIn June 2001, the Financial Accounting Standards Board issuedStatement of Financial Accounting Standards (SFAS) No. 141,“Business Combinations” and SFAS No. 142, “Goodwill andOther Intangible Assets.” SFAS 141 requires that the purchasemethod of accounting be used for business combinations ini-tiated after June 30, 2001. Under SFAS 142, amortization ofgoodwill, including goodwill recorded in past business combi-nations, will discontinue upon adoption of this standard. Inaddition, goodwill and intangible assets with indefinite liveswill be tested for impairment in accordance with the provi-sions of SFAS 142. Although not required to adopt the provi-sions of SFAS 142 until fiscal 2003, the Company expects toadopt SFAS 142 in the first quarter of fiscal 2002. TheCompany has not completed an assessment of the impact ofthese statements including the impairment test of goodwilland other intangible assets; however, at this time, it is expect-ed that amortization expense will be reduced by approximate-ly $2.5 million in fiscal 2002 as a result of adopting SFAS 142.

Two other recently issued pronouncements, SFAS No. 143,“Accounting for Asset Retirement Obligations” and SFAS No. 144, “Accounting for the Impairment or Disposal ofLong-Lived Assets” will be effective for the Company begin-ning in fiscal 2003. The Company has not yet evaluated theimpact of these standards on its financial statements.

OutlookThe Company’s long-term objective to record compoundannual growth rates in diluted earnings per share of 10% to15% will require both sales growth and improved profitabilityin the Company’s existing operations and additional acquisi-tions. Due in part to the recession in the U.S. economy during2001, growth in diluted earnings per share was less in fiscal2001 than in 2000 and in 1999. During fiscal 2001 theCompany incurred significant start-up costs related to newproduction facilities and equipment, and incurred higher

CLARCOR10

(Dollars in millions except per share data)

FINANCIAL REVIEW

energy, employee insurance and pension costs than in prioryears. If the U.S. economy improves during 2002 as expected,the Company anticipates that improved economic conditionswill positively impact sales and earnings, and that 2002 will be the tenth consecutive year of earnings per share growth for the Company.

The Company’s Total Filtration Program that was started infiscal 2000 is expected to continually add to sales levels in theCompany’s two filtration segments over the next severalyears. The acquisition of TFS in June 2001 increased theCompany’s ability to provide filtration management servicesto industrial companies throughout North America. Since theTFS acquisition, the Company’s various other total filtrationactivities have been combined with TFS to provide a singlefocus throughout the Company. Several total filtration man-agement contracts were completed late in 2001 and negotia-tions continue on others. The impact of these contracts willgrow over the next several years as customers’ facilities areconverted to CLARCOR’s Total Filtration Program. The TotalFiltration Program is expected to serve as an added distribu-tion channel for all of the Company’s filtration products. TheCompany expects to make investments at TFS in 2002 that areplanned to significantly accelerate its sales growth, but willslow the improvement in its operating margin in 2002. It isanticipated that TFS’ margins will improve beginning in 2003.

The Engine/Mobile Filtration segment is expected to increaseits sales and profit by providing outstanding customer service,introducing new products and expanding marketing pro-grams. These sales initiatives are expected to offset any con-tinued reduction in sales due to reduced customer demand asa result of the economic recession, especially due to reducedfreight mileage. The Industrial/Environmental Filtration seg-ment is expected to grow sales and profits as a result of con-tinued expansion of sales programs throughout various distri-bution channels, including the Total Filtration Program, and bycontinuing to achieve synergies and cost savings from inte-grating production facilities and processes. This segment con-tinues to have the most potential for improved operating mar-gins over the next few years, although this continues to be ahighly competitive industry. The Packaging segment’s focuson non-promotional metal decorating sales is expected toincrease utilization of both the new lithography equipmentand other production capacity. Due to decreased customerorders for plastic closures and the non-recurring terminationpayment received in 2001, overall sales and operating profitfor the segment are expected to be lower in fiscal 2002 than in2001. Excluding the $7.0 million non-recurring terminationpayment in 2001, Packaging sales are expected to increase toapproximately $67-$69 million in fiscal 2002 compared toapproximately $63 million in fiscal 2001.

The Company will continue to implement cost reductions andproductivity improvements, although competitive pricingpressures, increases in labor, healthcare, insurance and ener-gy costs, and worldwide business conditions may reduce theoverall profit improvement. Due to significantly reduced pen-sion asset valuations and lower discount rates, pensionexpense will increase by approximately $3.0 million in fiscal2002 from 2001. Capital investments will continue to be madein each segment’s facilities during 2002 to improve productivi-

ty and support new products. It is expected that the invest-ments made in fiscal 2001 and 2000 for new manufacturingfacilities and production lines will continue to improve pro-ductivity and profitability. While the Company fully antici-pates that sales and profits will improve as a result of theseefforts, the Company has developed contingency plans toreduce discretionary spending if recessionary economic con-ditions persist.

The Company continues to look at acquisition opportunities,primarily in related filtration businesses. It is expected thatthese acquisitions would expand the Company’s market base,distribution coverage and product offerings. The Companyhas established financial standards that will continue to bevigorously applied in the review of all acquisition opportuni-ties. Additionally, even though debt increased significantly in1999 due to the Industrial Filtration Acquisitions, theCompany believes that it has sufficient additional borrowingcapacity to continue this acquisition program.

FORWARD-LOOKING STATEMENTSCertain statements quoted in this Annual Report are forward-looking. These statements involve risk and uncertainty.Actual future results and trends may differ materiallydepending on a variety of factors including: the volume andtiming of orders received during the year; the mix of changesin distribution channels through which the Company’s prod-ucts are sold; the success of the Company’s Total FiltrationProgram; the timing and acceptance of new products andproduct enhancements by the Company or its competitors;changes in pricing, labor availability and related costs, prod-uct life cycles, raw material costs, insurance, pension andenergy costs and purchasing patterns of distributors and cus-tomers; competitive conditions in the industry; businesscycles affecting the markets in which the Company’s productsare sold; the effectiveness of plant conversions, plant expan-sions and productivity improvement programs; the manage-ment of both growth and acquisitions; the fluctuation in for-eign and U.S. currency exchange rates; the fluctuation ininterest rates, primarily LIBOR, which affect the cost of bor-rowing under the revolving credit facility; extraordinaryevents such as litigation, acquisitions or divestitures includingrelated charges; and economic conditions generally or in vari-ous geographic areas. All of the foregoing matters are difficultto forecast. The future results of the Company may fluctuateas a result of these and the other risk factors detailed fromtime to time in the Company’s filings with the Securities andExchange Commission.

Due to the foregoing items, it is possible that, in the future,the Company’s operating results will be below the expecta-tions of stock market analysts and investors. In such event,the price of CLARCOR common stock could be materiallyadversely affected.

CLARCOR 11

CLARCOR12

CONSOLIDATED BALANCE SHEETS

The accompanying notes are an integral part of the consolidated financial statements.

NOVEMBER 30, 2001 AND 2000(Dollars in thousands except per share data)

ASSETS 2001) 2000)

Current assets:Cash and short-term cash investments .............................................................. $ 7,418) $ 10,864)

Accounts receivable, less allowance for losses of $7,920for 2001 and $5,027 for 2000............................................................................ 115,003) 110,083)

Inventories ............................................................................................................... 104,291) 100,561)

Prepaid expenses and other current assets ........................................................ 4,120) 3,640)

Deferred income taxes ........................................................................................... 13,518) 5,331)

Total current assets.................................................................................... 244,350) 230,479)

Plant assets, at cost less accumulated depreciation ............................................. 137,316) 140,121)

Acquired intangibles, less accumulated amortization ......................................... 116,746) 101,877)

Pension assets............................................................................................................. 18,939) 19,519)

Other noncurrent assets............................................................................................ 13,266) 9,934)

Total assets.................................................................................................. $530,617) )$501,930)

LIABILITIES

Current liabilities:Current portion of long-term debt ....................................................................... $ 5,579) $ 5,482)

Accounts payable and accrued liabilities ............................................................ 84,826) 84,187)

Income taxes ........................................................................................................... 4,526) 8,157)

Total current liabilities .............................................................................. 94,931) 97,826)

Long-term debt, less current portion....................................................................... 135,203) 141,486)

Postretirement health care benefits ........................................................................ 3,851) 3,574)

Long-term pension liabilities.................................................................................... 4,955) 4,374)

Deferred income taxes............................................................................................... 15,114) 10,663)

Other long-term liabilities......................................................................................... 1,868) 1,519)

Minority interests ....................................................................................................... 434) 395)

Contingencies

SHAREHOLDERS’ EQUITY

Capital stock:Preferred, par value $1, authorized 5,000,000 shares,

none issued ....................................................................................................... –) –)

Common, par value $1, authorized 60,000,000 shares,issued 24,626,236 in 2001 and 24,381,307 in 2000 ........................................ 24,626) 24,381)

Capital in excess of par value ............................................................................... 9,565) 5,700)

Accumulated other comprehensive earnings .................................................... (9,179) (6,919)Retained earnings................................................................................................... 249,249) 218,931)

Total shareholders’ equity ........................................................................ 274,261) 242,093)

Total liabilities and shareholders’ equity ............................................... $530,617) $501,930)

CLARCOR 13

CONSOLIDATED STATEMENTS OF EARNINGS

The accompanying notes are an integral part of the consolidated financial statements.

FOR THE YEARS ENDED NOVEMBER 30, 2001, 2000 AND 1999(Dollars in thousands except per share data)

2001) 2000) 1999)

Net sales ........................................................................................................ $666,964) $652,148) $477,869)

Cost of sales .................................................................................................. 471,477) 453,803) 329,282)

Gross profit.......................................................................................... 195,487) 198,345) 148,587)

Selling and administrative expenses ........................................................ 119,677) 122,358) 92,510)

Operating profit .................................................................................. 75,810) 75,987) 56,077)

Other income (expense):Interest expense ....................................................................................... (10,270) (11,534) (3,733)Interest income......................................................................................... 654) 698) 1,451)

Other, net ................................................................................................... (460) (1,664) 1,820)

(10,076) (12,500) (462)

Earnings before income taxes and minority interests ................. 65,734) 63,487) 55,615)

Provision for income taxes ......................................................................... 23,804) 23,201) 20,137)

Earnings before minority interests.................................................. 41,930) 40,286) 35,478)

Minority interests in earnings of subsidiaries ......................................... (37) (49) (66)

Net earnings ................................................................................................. $ 41,893) $ 40,237) $ 35,412)

Net earnings per common share:Basic ........................................................................................................... $ 1.71) $ 1.66) $ 1.48)

Diluted ....................................................................................................... $ 1.68) $ 1.64) $ 1.46)

Average number of common shares outstanding:Basic ........................................................................................................... 24,535,199) 24,269,675) 23,970,011)

Diluted ....................................................................................................... 24,892,062) 24,506,171) 24,313,607)

CLARCOR14

FOR THE YEARS ENDED NOVEMBER 30, 2001, 2000 AND 1999(Dollars in thousands except per share data)

The accompanying notes are an integral part of the consolidated financial statements.

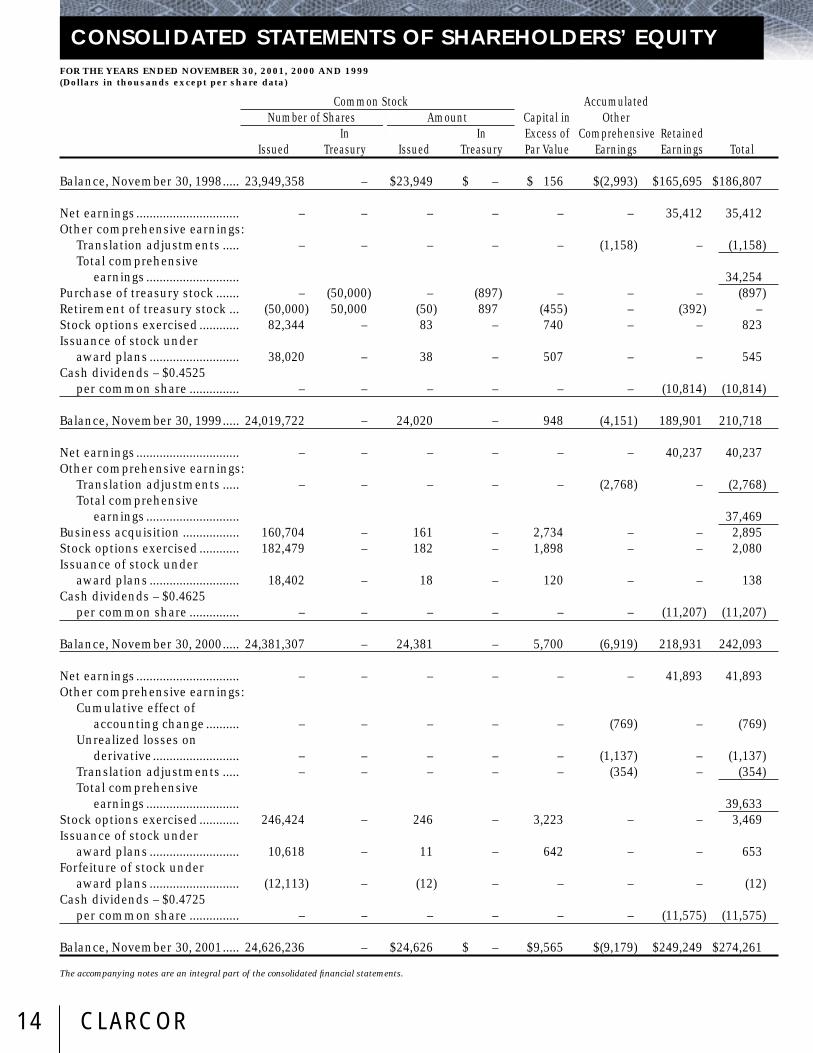

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

Common Stock AccumulatedNumber of Shares Amount Capital in Other

In In Excess of Comprehensive RetainedIssued Treasury Issued Treasury Par Value Earnings Earnings Total

Balance, November 30, 1998..... 23,949,358) –) $23,949) $ –) $ 156) $(2,993) $165,695) $186,807)

Net earnings............................... –) –) –) –) –) –) 35,412) 35,412)Other comprehensive earnings:

Translation adjustments ..... –) –) –) –) –) (1,158) –) (1,158)Total comprehensive

earnings ............................ 34,254)Purchase of treasury stock ....... –) (50,000) –) (897) –) –) –) (897)Retirement of treasury stock ... (50,000) 50,000) (50) 897) (455) –) (392) –)Stock options exercised ............ 82,344) –) 83) –) 740) –) –) 823)Issuance of stock under

award plans ........................... 38,020) –) 38) –) 507) –) –) 545)Cash dividends – $0.4525

per common share ............... –) –) –) –) –) –) (10,814) (10,814)

Balance, November 30, 1999..... 24,019,722) –) 24,020) –) 948) (4,151) 189,901) 210,718)

Net earnings............................... –) –) –) –) –) –) 40,237) 40,237)Other comprehensive earnings:

Translation adjustments ..... –) –) –) –) –) (2,768) –) (2,768)Total comprehensive

earnings ............................ 37,469)Business acquisition ................. 160,704) –) 161) –) 2,734) –) –) 2,895)Stock options exercised ............ 182,479) –) 182) –) 1,898) –) –) 2,080)Issuance of stock under

award plans ........................... 18,402) –) 18) –) 120) –) –) 138)Cash dividends – $0.4625

per common share ............... –) –) –) –) –) –) (11,207) (11,207)

Balance, November 30, 2000..... 24,381,307) –) 24,381) –) 5,700) (6,919) 218,931) 242,093)

Net earnings............................... –) –) –) –) –) –) 41,893) 41,893)Other comprehensive earnings:

Cumulative effect of accounting change .......... –) –) –) –) –) (769) –) (769)

Unrealized losses on derivative.......................... –) –) –) –) –) (1,137) –) (1,137)

Translation adjustments ..... –) –) –) –) –) (354) –) (354)Total comprehensive

earnings ............................ 39,633)Stock options exercised ............ 246,424) –) 246) –) 3,223) –) –) 3,469)Issuance of stock under

award plans ........................... 10,618) –) 11) –) 642) –) –) 653)Forfeiture of stock under

award plans ........................... (12,113) –) (12) –) –) –) –) (12)Cash dividends – $0.4725

per common share ............... –) –) –) –) –) –) (11,575) (11,575)

Balance, November 30, 2001..... 24,626,236) –) $24,626) $ –) $9,565) $(9,179) $249,249) $274,261)

CLARCOR 15

FOR THE YEARS ENDED NOVEMBER 30, 2001, 2000 AND 1999(Dollars in thousands)

The accompanying notes are an integral part of the consolidated financial statements.

2001) 2000) 1999)

Cash flows from operating activities:Net earnings.............................................................................................. $ 41,893) $ 40,237) $ 35,412)

Adjustments to reconcile net earnings to net cash provided by operations:

Depreciation ....................................................................................... 18,187) 17,537) 13,729)

Amortization....................................................................................... 3,663) 3,542) 1,643)

Minority interests in earnings of subsidiaries ............................... 37) 49) 66)

Net (gain) loss on dispositions of plant assets............................... 338) 109) (1,660)Impairment of plant assets .............................................................. 2,422) –) –)

Changes in assets and liabilities, net of business acquisitions:Accounts receivable..................................................................... 5,116) (3,448) (6,062)Inventories .................................................................................... 5,190) (9,636) (4,585)Prepaid expenses and other current assets ............................. (374) 8,040) (1,369)Other noncurrent assets ............................................................. (2,523) (554) (18)Accounts payable and accrued liabilities ................................. (8,693) (1,170) 4,790)

Pension assets and liabilities, net.............................................. 1,163) (7,430) (583)Income taxes ................................................................................ (2,683) 4,663) (2,366)Deferred income taxes ................................................................ (446) 2,191) (355)

Net cash provided by operating activities........................... 63,290) 54,130) 38,642)

Cash flows from investing activities:Additions to plant assets......................................................................... (18,204) (29,005) (21,822)Business acquisitions, net of cash acquired......................................... (33,388) (12,735) (142,709)Dispositions of plant assets .................................................................... 539) 55) 3,873)

Other, net .................................................................................................. (300) (440) –)

Net cash used in investing activities ................................... (51,353) (42,125) (160,658)

Cash flows from financing activities:Proceeds from multicurrency revolving credit agreement................. 27,500) 43,200) 115,000)

Payments on multicurrency revolving credit agreement ................... (36,500) (42,200) –)

Proceeds from borrowings under long-term debt ............................... 8,000) –) –)

Reduction of long-term debt................................................................... (5,349) (7,034) (468)Sales of capital stock under stock option plan..................................... 2,598) 1,379) 680)

Purchases of treasury stock .................................................................... –) –) (897)Cash dividends paid................................................................................. (11,575) (11,207) (10,814)

Net cash provided by (used in) financing activities........... (15,326) (15,862) 103,501)

Net effect of exchange rate changes on cash .......................................... (57) (24) (61)

Net change in cash and short-term cash investments .......................... (3,446) (3,881) (18,576)Cash and short-term cash investments, beginning of year................... 10,864) 14,745) 33,321)

Cash and short-term cash investments, end of year.............................. $ 7,418) $ 10,864) $ 14,745)

CONSOLIDATED STATEMENTS OF CASH FLOWS

A. ACCOUNTING POLICIESPrinciples of ConsolidationThe consolidated financial statements include all domesticand foreign subsidiaries that are more than 50% owned andcontrolled. CLARCOR Inc. and its subsidiaries are hereinaftercollectively referred to as the “Company” or CLARCOR.

Minority interests represent an outside shareholder’s 10%ownership of the common stock of Filtros Baldwin de Mexico(FIBAMEX) and outside shareholders’ 20% ownership ofBaldwin-Unifil S.A.

Foreign Currency TranslationFinancial statements of foreign subsidiaries are translatedinto U.S. dollars at current rates, except that revenues, costsand expenses are translated at average current rates duringeach reporting period. Net exchange gains or losses resultingfrom the translation of foreign financial statements and theeffect of exchange rate changes on intercompany transactionsof a long-term investment nature are accumulated with othercomprehensive earnings as a separate component of share-holders’ equity and are presented, net of tax, in theConsolidated Statements of Shareholders’ Equity.

Plant AssetsDepreciation is provided by the straight-line and acceleratedmethods for financial statement purposes and by the acceler-ated method for tax purposes. The provision for depreciationis based on the estimated useful lives of the assets (15 to 40years for buildings and improvements and 3 to 15 years formachinery and equipment). It is the policy of the Company tocapitalize renewals and betterments and to charge to expensethe cost of current maintenance and repairs. When propertyor equipment is retired or otherwise disposed of, the net bookvalue of the asset is removed from the Company’s books andthe resulting gain or loss is reflected in earnings.

Excess of Cost Over Fair Value of Assets Acquired andOther Intangible AssetsThe excess of cost over fair value of assets acquired is beingamortized over a forty-year period using the straight-linemethod. Other acquired intangible assets are being amortizedover the estimated periods to be benefited using the straight-line method. These intangibles include trademarks (40 yearlife), patents (average 14 year life), and other identifiableintangible assets with lives ranging from one to thirty years.

In June 2001, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 142(SFAS 142), “Goodwill and Other Intangible Assets,” which dis-continues amortization of the excess of cost over fair value ofassets acquired and of intangible assets with indefinite lives. Italso requires goodwill and intangible assets with indefinitelives to be tested for impairment annually or whenever there isan impairment indicator. Although not required to adopt theprovisions of SFAS 142 until fiscal 2003, the Company expectsto adopt SFAS 142 in the first quarter of fiscal 2002. TheCompany has not completed an assessment of the impact ofthis statement, including the impairment tests. However, as aresult of adopting SFAS 142, the Company expects amortizationexpense will be reduced by approximately $2,500 in fiscal 2002.

In accordance with Statement of Financial AccountingStandards No. 121 (SFAS 121), “Accounting for the Impairmentof Long-Lived Assets and Long-Lived Assets to Be DisposedOf,” the Company determines any impairment losses based onunderlying cash flows related to specific groups of acquiredplant assets and identifiable intangibles and excess of costover fair value of assets acquired, and would first apply anysuch impairment losses to related goodwill.

Statements of Cash FlowsAll highly liquid investments with a maturity of three monthsor less when purchased or that are readily saleable are con-sidered to be short-term cash equivalents. The carryingamount of the investments approximates fair value.

Income TaxesThe Company provides for income taxes in accordance with Statement of Financial Accounting Standards No. 109(SFAS 109), “Accounting for Income Taxes.” SFAS 109 requiresthe recognition of deferred tax liabilities and assets for theexpected future tax consequences of temporary differencesbetween the financial statement carrying amounts and thetax basis of assets and liabilities.

Revenue RecognitionRevenue is recognized when product ownership and risk ofloss has transferred to the customer or performance of servic-es is complete and the Company has no remaining obliga-tions regarding the transaction. In December 1999, theSecurities and Exchange Commission issued Staff AccountingBulletin No. 101 (SAB 101), “Revenue Recognition in FinancialStatements,” relating to revenue recognition under generallyaccepted accounting principles in financial statements. Nosignificant changes to the Company’s revenue recognitionpolicies were necessary to comply with SAB 101.

Product WarrantiesThe Company provides for estimated warranty costs whenthe related products are recorded as sales or for specific itemsat the time their existence is known and the amounts are rea-sonably determinable.

Comprehensive EarningsForeign currency translation adjustments and unrealized loss-es on derivative instruments are included in other compre-hensive earnings, net of tax, in accordance with Statement ofFinancial Accounting Standards No. 130 (SFAS 130), “ReportingComprehensive Income.”

Use of Management’s EstimatesThe preparation of the financial statements in conformitywith accounting principles generally accepted in the UnitedStates of America requires management to make estimatesand assumptions that affect the reported amounts of assetsand liabilities and disclosure of contingent liabilities at thedate of the financial statements and the reported amounts ofrevenues and expenses during the reporting period. Actualresults could differ from those estimates.

(Dollars in thousands except per share data)

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

CLARCOR16

Accounting PeriodThe Company’s fiscal year ends on the Saturday closest toNovember 30. The fiscal year ended December 1, 2001 includ-ed fifty-two weeks. The fiscal years ended December 2, 2000and November 27, 1999 were comprised of fifty-three andfifty-two weeks, respectively. In the consolidated financialstatements, all fiscal years are shown to begin as of December1 and end as of November 30 for clarity of presentation.

ReclassificationsCertain reclassifications have been made to conform prioryears’ data to the current presentation. These reclassifica-tions had no effect on reported earnings.

B. ACCOUNTING CHANGE AND DERIVATIVE INSTRUMENTS

The Company makes limited use of derivative financialinstruments to manage certain interest rate and foreign cur-rency risks. Interest rate swap agreements are utilized to con-vert certain floating rate debt into fixed rate debt. Cash flowsrelated to interest rate swap agreements are included in inter-est expense over the terms of the agreements.

Effective December 1, 2000, the Company adopted Statementof Financial Accounting Standards No. 133 (SFAS 133),“Accounting for Derivative Instruments and HedgingActivities.” SFAS 133 requires the recognition of all derivativesin the balance sheet as either an asset or a liability measuredat fair value and requires a company to recognize changes inthe derivative’s fair value currently in earnings unless itmeets specific hedge accounting criteria. If the derivative isdesignated as a cash flow hedge, the effective portions ofchanges in the fair value of the derivative are recorded inother comprehensive earnings and are recognized in theincome statement when the hedged item affects earnings.

The Company documents all relationships between hedginginstruments and hedged items, as well as its risk-manage-ment objective and strategy for undertaking various hedgetransactions. In addition, the Company assesses (both at thehedge’s inception and on an ongoing basis) the effectivenessof the derivatives that are used in hedging transactions. If itis determined that a derivative is not (or has ceased to be)effective as a hedge, the Company would discontinueaccounting for it as a hedge prospectively. Ineffective por-tions of changes in the fair value of cash flow hedges are rec-ognized in earnings.

During 2000, the Company entered into interest rate agree-ments to manage its interest exposure related to the multicur-rency credit revolver. The agreement in place at November 30,2001 provides for the Company to pay a 7.34% fixed interestrate on a notional amount of $60,000. The agreement expiresSeptember 11, 2002. Under the agreement the Company willreceive interest at floating rates based on LIBOR.

The adoption of SFAS 133 resulted in a cumulative effect of anaccounting change to accumulated other comprehensiveearnings of a negative $769 ($1,183 pretax) and the recogni-tion of a liability. The Company’s derivative instrument isdesignated as a cashflow hedge and determined to be effec-tive. Therefore, there was no adjustment to net earnings. At

November 30, 2001, the fair value of the agreement was a neg-ative $2,932 and is included in other current liabilities. Thenet loss included in other comprehensive earnings for the fis-cal year ended November 30, 2001 was $1,137 ($1,750 pretax).Derivative gains and losses will be reclassified into earningsas payments are made on its variable rate interest debt.Approximately $711 ($1,094 pretax) was reclassified into earn-ings during the fiscal year ended November 30, 2001. Theamount of net derivative losses included in other comprehen-sive income at November 30, 2001 will be reclassified intoearnings in fiscal year 2002.