Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AnnualReport2015

2

GLOBALIA CORPORACIÓN EMPRESARIAL S.A.Y SOCIEDADES DEPENDIENTES

Entre ellas:AIR EUROPA LÍNEAS AÉREAS, S.A.U.GLOBALIA BUSINESS TRAVEL, S.A.U.

GLOBALIA TRAVEL CLUB SPAIN, S.L.U.WELCOME INCOMING SERVICES, S.L.U.

VIAJES HALCÓN, S.A.U.VIAJES ECUADOR, S.A.U.VIAJES TU BILLETE, S.L.BE LIVE HOTELS, S.L.U.

GLOBALIA HANDLING, S.A.U.

Centro Empresarial Globalia07620 Llucmajor (Mallorca), Baleares. España / Spain.

Tel. +34 971 178 103 · Fax +34 971 178 352www.globalia.com

Impresión: Globalia Artes GráficasDiseño y maquetación: som2.com

3

2015 ANNUAL REPORT

1. Nature, Activities and Composition of

the Group

2. Basis of Presentation

3. Application of Losses of the Parent

4. Significant Accounting Policies

5. Joint Ventures

6. Non-Current Assets Held for Sale

7. Intangible Assets

8. Goodwill, Goodwill on Consolidation

and Impairment

9. Property, Plant and Equipment

10. Investment Property

11. Finance Leases - Lessee

12. Operating Leases - Lessee

13. Risk Management Policy

14. Equity-Accounted Investees

15. Financial Assets by Category

16. Investments and Trade Receivables

17. Derivative Financial Instruments

18. Inventories

19. Prepayments

20. Cash and Cash Equivalents

21. Equity

22. Non-Controlling Interests

23. Provisions

24. Financial Liabilities by Category

25. Payables and Trade Payables

26. Late Payments to Suppliers. “Reporting

Requirement”, Third Additional Provision

of Law 15/2010 of 5 July 2010

27. Accruals

28. Taxation

29. Environmental Information

30. Related Party Balances

and Transactions

31. Income and Expense

32. Employee Information

33. Audit Fees

34. Other Contingencies

35. Other

Director’s Report 2015

Appendix

Corporate Social

Responsibility Report

Executive Letter of the 2015 Annual Report

Introduction to the 2015 Management Report

and Main Magnitudes

Audit report on the Consolidated

Annual Accounts

Consolidated Annual Accounts

Notes to the Consolidated Annual Accounts

INDEX46

14

1622

22

2425

4647

49

45

525354

55

565859

61

60

62

65

7069

7172

73

748297

4

2015 has been a decisive year for Globalia’s consolidation as the leading tourism group. During

the year, we managed to increase our turnover by 2.6% as compared to 2014, reaching the fig-

ure of 3,379 Million Euros. The excellent performance in the tourist sector, with a record 68.1

million tourists visiting Spain in 2015, no doubt contributed to these improvements.

Air Europa: over 10 million travellers carried

Globalia, the leading tourism group in Spain, is on the rise

and this is reflected not just in its turnover but also the ex-

pansion of activity in its different divisions. In 2015, apart

from increasing the number of hours of flight as compared

to previous years, with over 175,000 hours, Air Europa

also increased the number of passengers carried by 6.6%,

breaking the barrier of 10 Million. Furthermore, the global

occupancy rate in 2015 was 84%.

In 2015, the opening of new routes to Asunción and Tel Aviv

and the commencement of inter-isle flights in the Balear-

ics were fundamental milestones in our drive to continue

raising Air Europa’s presence in the sector. We can also

highlight the inauguration of the new Operations Control

Centre (OCC) in Llucmajor, equipped with the latest tech-

nology available on the market.

Air Europa flies higher every year, not just in Spain, Europe

and Latin America, but also in another strategic market: the

United States. In 2015, Air Europa saw an increase of 84% in

the number of passengers, reaching the figure of 232,459.

These good figures, together with external variables such

as the falling price of fuel, encourage us to face 2016 with

optimism and the idea that it may be a key year for the

airline. The arrival of the new 787s, the initiation of the

construction of a new hangar in Barajas Airport to support

these types of aeroplanes and the creation of new destina-

tions, such as Zurich, Bogota and Guayaquil are also inspiring optimism. Furthermore, in the

next year, we should see Air Europa’s aeroplanes updated with new livery, to adapt them to the

new corporate image that the airline created in 2015.

Retail division: more job positions

Globalia’s retail division (formed by Viajes Halcón, Viajes Ecuador and tubillete.com) increased

its turnover in 2015, surpassing 1,100 Million Euros. These figures have improved thanks to the

adjustments carried out in the previous years, to adapt to the market’s new reality. In 2015, the

redistribution of assets translated into a reduction in the number of offices, to 1,087, whilst the

average number of employees of Viajes Halcón increased: specifically by 9% as compared to

2014. In addition, with the creation of the associated agency model in 2015, Globalia expects

to duplicate the number of sales points within three years.

Presentation of the ANNUAL REPORT 2015

5

2015 ANNUAL REPORT

Again this year, we can highlight the growth of Halcón in the corporate travel segment, which al-

ready represents 30% of the total business. In 2015, Globalia’s retail division became the supplier

of travel and accommodation services for all the Spanish Public Administration organisations.

Viajes Halcón was also awarded other contracts, such as managing the travel plans of employ-

ees of different public companies. And the prospects for 2016 are even better, as the company

signed several agreements with various sports clubs at the beginning of the year. Halcón has

already been awarded the management of logistics and accommodation for 80% of the clubs

in the most important leagues in the country.

Higher turnover in the wholesale division

In 2015, the sales of the business’ wholesale division began to recover. Led by the Travelplan

tour operator, the division saw a notable rise in net turnover over the past year, with an in-

crease of 17% in respect of 2014. Likewise, in 2015 the number of passengers carried increased

as compared to the preceding year. Another highlight was the consolidation of the Latitudes

Brand in the exclusive holiday package market.

Incoming grows by 25%

The Incoming division, which includes the online ho-

tel sales platform WelcomeBeds among its assets,

registered strong progress in its business in 2015. To

be specific, it sold over 1.7 million hotel nights, 25%

more than the previous year. This confirms the up-

ward trends already detected in 2014, and the fact

that Globalia has positioned itself as a leader in this

sector in a short period of time. This growth has also

translated into an increase in the number of employees in the division.

Be Live, ready to add three hotels

The group’s hotel division registered an increase in the number of rooms booked in 2015,

surpassing 8,400, and thanks to the renovations undertaken in the preceding years, this should

continue to rise into 2016, with the addition of new hotels to the chain: Be Live Experience

Varadero (365 rooms); Be Live Family Aqua Fun Marrakech (262 rooms); and Be Live Collection

Son Antem, Mallorca (151 rooms).

Handling

2015 was a year brimming with good news for our handling division also, which operates

under the brands Globalia Handling and Groundforce in 16 airports. In this year, Globalia Han-

dling was awarded third party handling licenses, increasing the number of airports it operates

in from 7 to 12: Las Palmas, Bilbao, Zaragoza, North Tenerife, Valencia, Fuerteventura, Barce-

lona, Malaga, Madrid, Alicante, Palma and Ibiza. Likewise, the number of services carried out

increased as compared to 2014, reaching the figure of 144,355.

These figures and magnitudes, along with the rest that are explained in this annual report, re-

flect the efforts and hard work put in by the group’s over 12,000 employees in 2015. Thanks to

the intense activities, we are approaching 2016 with the sense that it is a year filled with oppor-

tunities for our divisions. We knew how to adapt and grow and now we are ready to become

the strongest leaders ever

“Excellentperformance inthe tourist sector

6

INTRODUCTIONTO THE 2015

MANAGEMENTREPORT AND MAIN

MAGNITUDESGLOBALIA CORPORACIÓN EMPRESARIAL, S.A.

AND SUBSIDIARIES

Globalia, the company founded and chaired by

Juan José Hidalgo, operates in the transport,

hotel, travel and tourism sectors, and essentially

comprises the following business units:

Globalia Corporación Empresarial S.A., the parent company and leader of the Group.

Air Division captained by Air Europa, the first

wholly Spanish-owned private airline, specialis-

ing in tourist and transatlantic travel. It is a mem-

ber of the Sky Team alliance.

Wholesale Division, headed by Travelplan,

the Spanish market leader.

In March 2003 this was added to by the com-

pany Iberotours and its Touring Club brand.

In 2007, a partnership was established with tour

operator MK Tours, based in Miami and focusing

on the North American domestic market.

Incoming Division,

The Welcome Incoming Services brand was set

up in 2010 to provide us with our own infrastruc-

ture in the most significant destinations where

Globalia currently operates. It operates two main

business lines: sale of accommodation online

and incoming services such as trips, transporta-

tion and vehicle rentals.

Retail Division, including Viajes Halcón, Viajes

Ecuador, which became part of Globalia in 2003

and Viajes Tu Billete.

The Division has the largest network of branches

operating in Spain and Portugal, giving it a lead-

ing position on the Iberian market.

Hotel Division, operating under the brand

name Be Live Hotels. Management of premium

category hotels in the Balearic and Canary Is-

lands, mainland Spain, Morocco, the Dominican

Republic and Cuba.

Handling Division, operating under the

brand name Groundforce. Providing ground ser-

vices to the Group’s airline and third-party clients

in airports in Spain and Morocco.

7

2015 ANNUAL REPORT

1971Juan José Hidalgo opens the first branch of Vi-

ajes Halcón.

1988Juan José Hidalgo sets up the tour operator

Travelplan.

1991A majority stake in Air Europa is acquired by Juan

José Hidalgo.

1993Air Europa begins scheduled domestic opera-

tions in Spain, competing with Iberia.

1999Viajes Halcón and Travelplan begin operations in

Portugal.

In May the central services move into their newly

built corporate offices of Llucmajor (Baleares).

Incorporation of the first Boeing 737-800 NG

aircraft.

2000 - 2005In May 2000, the first hotel operated by the

Group’s Hotel Division opens its doors.

In October 2001, following the events of Sep-

tember 11, the Air Division is restructured.

In the year 2003, Globalia Handling is set up and

Viajes Ecuador is acquired.

During 2005, Strong international expansion at

the Group’s Handling Division.

Air Europa and Travelplan begin to operate in

France following the creation of Globalia France.

2006 - 2007Globalia strengthens its position in two particu-

larly key areas: the Handling Division, with new

contracts won at Spanish airports, and the Hotel

Division, which now boasts more than 10,000

rooms.

Acquisition of Iberrail and a stake in MK Tours.

A contract is signed to acquire 8 Boeing 787

“Dreamliner” aircraft.

2008A contract is signed to acquire 11 Embraer 195

aircraft with 120 seats and with the most ad-

vanced technology. The Hotel Division operates

more than 11.400 rooms.

2009Viajes Halcón begins the process of expansion

through franchised branches operating under

the brand name.

Acquisition of 75% of Tubillete.com, an online trav-

el agency specialising in the sale of airline tickets.

The first four Embraer 195 aircraft begin operations.

2010International expansion of Travelplan, via the

opening of offices in Italy and France. New “Lati-

tudes” tour operator. Air Europa starts the opera-

tion of new routes to Lima and Miami.

Set up of “Welcome Incoming Services” as a new

business unit focused on incoming travel agency

activity. Air Europa becomes a full member of

SkyTeam.

2011New in-house incoming services previously

managed by third parties in Mexico, Dominican

Republic and London.

Inclusion of the Welcomebeds online platform.

2012Acquisition of the additional 50% of the tour

operator MK Tours in Miami. Sale of Globalia

Handling Mexico and Pepemobile. Major re-

structuring of all Group Divisions.

2013Restructuring of a significant number of travel

agents in the Retail Division. The Aerial Division

continues to expand its long-distance routes

and to reinforce its short and medium-distance

routes.

2014Air Europa signs a contract with Boeing to purchase

fourteen B787-9 planes with delivery expected be-

tween February 2020 and October 2022.

2015The airline Aeronova is absorbed into the Air Divi-

sion. In this same year, agreements are signed for

the purchase of twenty 737-8 MAX aeroplanes.

8

GLOBALIA IN FIGURES(Thousands of Euros)

CONSOLIDATED SHAREHOLDER’S EQUITY

2015 170,965

2011

2012

2013

2014

175,437

191,298

168,836

149,283

CONSOLIDATED FIXED ASSETS

2015 625,201

2011

2012

2013

2014

605,396

579,076

592,600

429,724

1,301

CONSOLIDATED PROFIT BEFORE TAXES AND EXTRAORDINARIES

2015

2011

2013

2014

46,779

-37,419 2012

62,685

69,864

2015 140,005

2011

2012

2013

2014

74,820

185,182

160,136

47,411

CONSOLIDATED NORMALISED EBITDA

2015 12,931

2011

2012

2013

2014

13,852

12,232

12,202

11,738

YEAR-ENDED TOTAL EMPLOYEES

2015 3,414,805

2011

2012

2013

2014

3,137,223

2,972,821

3,337,423

3,102,892

CONSOLIDATED INCOME

9

2015 ANNUAL REPORT

AIR DIVISIONAs for Globalia’s traditional businesses (Whole-

sale, Retail and Air), these have continued to

maintain their leading positions within their re-

spective market segments.

Air Europa was the country’s first privately owned

company to operate domestic scheduled flights

in Spain. It broke into the tourist sector when de-

mand was at its greatest, and its expansion and

growth have made decisive contributions to the

maturity of Spain’s commercial aviation market,

which there can be no doubt would never have

taken on the form it has today if Air Europa had

not played its pioneering role.

In its ongoing drive to achieve progress, focusing at

all times on customer satisfaction, Air Europa today

has one of the most modern fleets in the sector.

In 2007, Air Europa became an associate member

of the Sky Team alliance, alongside such airlines

as Air France, KLM, Alitalia, Continental Airlines,

Delta Airlines and Aeromexico, further consoli-

dating its market position as a scheduled airline.

In 2008 a deal was signed to purchase 11 Em-

braer 195 with 120 seats and with the most ad-

vanced technology.

The Embraer fleet allows the company to opti-

mise routes with a low passenger density.

In 2010, Air Europa became a full member of the

SkyTeam Alliance.

During 2014, the airline continued to expand and

plan new routes to South America, with desti-

nations such as Salvador de Bahía, Santiago de

Chile and Sao Paulo, and continued to bolster

its lines in Europe and its short-range flights in

Spain. New routes to Morocco and Germany

were also opened.

With an eye on adding 787-8s to its fleet from

2016, Air Europa has been operating an aircraft

with these characteristics on its Madrid-Miami

route, and using it to train its crews in 2015. In

this year, Air Europa has also been implement-

ing its own customer loyalty programme called

SUMA MILES.

9

America

Rest of Europe

Spain

Others

11%

24%

DETAILS REVENUE PER GEOGRAPHICAL MARKET 2015

64%

1%

Others

Wholesale Division

Air Division

Handling Division

45%

11%

4% 3%

Retail Division

Hotel Division

DETAILS REVENUE PERDIVISION 2015

36%

1%

10

WHOLESALE DIVISIONEver since it was set up as a wholesale travel

agency in 1986, Travelplan has been one of the

leading tour operators on the Spanish market

with regard to both its number of destinations

and number of passengers. Its offer is based on

Air Europa’s network of scheduled and charter

flights, but also covers every type of product and

destination.

As part of its expansion policy, in May 2007

Travelplan acquired a 50% stake in the US tour

operator MK Tours, based in Miami, specialising

in the Dominican Republic as a destination.

Greats advances have taken place since 2009

with the introduction of new technologies al-

lowing for the development of the Internet busi-

ness, this channel now accounting for 80% of

total sales.

The Division rolled out an international expan-

sion process with the opening of offices and sale

of tourism packages in France in 2010, along

with the launch of a new top-end line: Latitudes.

During 2012 and 2013 the Wholesale Division

underwent a substantial restructuring of its com-

panies. The remaining 50% of MK Tours was also

acquired, bringing the equity stake held to 100%.

In 2014, Touring Club consolidated its position as

the second leading Disney operator in the mar-

ket and Latitudes continued to grow as the Divi-

sion’s Premium segment.

During 2015, Globalia’s Wholesale Division, whose

brand portfolio includes Travelplan, Touring Club

and Latitudes, saw an expansion of 8% in seats sold

as compared to 2014, reinforcing its position as

the leader in the Spanish issue market, especially in

a year that was characterised by strong competi-

tion and plenty of offers for the destinations of the

Caribbean, the Canaries and the Balearic Islands.

PASSENGERS CARRIED BY AIR EUROPA

2015 10,221,104

2011

2012

2013

2014

8,744,512

8,114,059

9,586,044

8,690,044

AVERAGE FLEET AND FLIGHT TIME COMPLETED

Air fleet Flight time

20152011 2012 2013 2014

42.4

40.4 40.9

44.545.6

165,468

151,251

156,509171,959

175,490

Boeing 767

Boeing 737

Embraer E195 Airbus A330

Airbus A333

11,00 18,73 9,730,92

9,12 23,63 7,632,00

11,00 19,87 11,61

11,00 18,65 10,50

2,00

0,78

AVERAGE AIR FLEET COMPOSITION

2011

2012

2013

2014

201511,00 20,00

0,00

12,00 2,58

11

2015 ANNUAL REPORT

INCOMING DIVISIONThe Welcome Incoming Services brand was set

up in 2010 to provide us with our own infrastruc-

ture in the most significant destinations where

Globalia currently operates.

Welcome Incoming Services has been offering

comprehensive incoming services through its

network of offices in Spain: North, South and

East Coasts; Balearic and Canary Islands; Madrid

and Barcelona since 2010.

In 2011 it provided services in France, Mexico,

Dominican Republic and London, which were

previously managed by third parties. Also, during

2011 some 393,000 passengers contracted our

own incoming services, and saw the introduc-

tion of the online hotel accommodation sales

platform “WELCOMEBEDS” which will be provid-

ing services to all third parties, Travel Agencies

and Tour Operators, with a focus on markets

where our own incoming operations have a

physical presence.

In 2012 WELCOMEBEDS increased its sales and

established its position in the online market. The

Division also began to market the Coasts prod-

uct, covering the Northern, Central Eastern, Cat-

alan and Andalusian coastlines of Spain.

2014 represents the year in which the new online

accommodation sales business consolidated

with 1.4 million “room nights”.

On its 4th anniversary, Welcomebeds experienced

growth of 23% (1.8 Million Room Nights), whilst

Welcome Incoming Services, has rendered ser-

vices at destination to 10% more passengers, both

of the Group and of third parties, than in 2014.

RETAIL DIVISIONAlthough the company’s founder hailed from

Salamanca, it was in Cáceres that the first Viajes

Halcón agency opened for business in 1971. Not

long afterwards, Juan José Hidalgo set up his

company’s second branch on Paseo de Anaya, in

the city of his birth.

With the acquisition of Air Europa in 1991, Viajes

Halcón experienced its great boom.

Today, Halcón Viajes is established as the undisput-

ed leader on the Spanish holiday market in terms

of number of points of sale, creation of exclusive

products and the outstanding training of its staff.

Acquired by Globalia in 2003, Viajes Ecuador is

one of Spain’s best-represented travel agencies

OWN DESTINATION OFFICES

2011

2012

2013

2014

2015

WHOSALE DIVISION REVENUES

2015 689

2011

2012

2013

2014

649

600

591

588

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

4

4

4

4

6

6

6

66

Dominican Republic

France(Millions of Euros)

Cuba

United Kingdom

Mexico

Spain Coast

Spain

1111

46

12

thanks to its strong presence across the country,

in particular in the North. It provides its custom-

ers with comprehensive advice, guaranteeing

the utmost quality in travel and accommodation.

The Retail Division is today the undisputed Ibe-

rian market leader.

In 2009 the group acquired a 75% stake in Tubil-

lete.com, an online travel agency specialising in

the sale of airline tickets.

The Division embarked on a franchise branch ex-

pansion programme under the Viajes Halcón brand

name, making progress in the field of the “e-com-

merce”, through the following brands: halconvi-

ajes.com, viajesecuador.com and tubillete.com.

With the objective of staying in the market and

adapting to changing circumstances, 2013 has

been a year that has seen the large-scale restruc-

turing of Viajes Halcón and Viajes Ecuador, both

in terms of number of offices and number of

employees: approximately 160 sales points were

closed and 450 employees were made redundant.

Thanks to these tough and difficult measures,

the Division returned to profit in 2014.

2015 has been a year of significant growth in the

Retail Division. Apart from being a benchmark

in the holiday sector, the Division has substan-

tially increased the weight of its Corporate busi-

ness, and has consolidated itself as a benchmark

brand in the world of sport. All these factors have

allowed the Division to substantially improve its

results as compared to 2014.

HOTEL DIVISIONGlobalia started operating hotels in the year

2000, with the construction of the Hotel Palace

de Muro (Majorca) and the refurbishment of the

Hotel Orotava (Tenerife).

In 2010 the Division launched its new brand Be Live.

In 2011 Globalia’s portfolio of hotels included

22 establishments with almost 6.200 rooms,

operating in Spain (on the mainland, and in the

Balearic and Canary Islands), the Mexican Car-

ibbean, the Dominican Republic, Cuba and Mo-

rocco, with the brand Be Live Hotels.

In 2012 the Division embarked on a new business

model with two franchise hotels. It meanwhile

gave up its Mexican Caribbean operations.

In 2013 the Division took on the Luabay Hotel

Chain with a portfolio of 10 hotels under lease, 1

under management and a total of 2,262 rooms.

During that year, the Group opened its first hotel

Halcon ViagensViajes Halcón

Viajes Ecuador

YEAR-ENDED SALES OFFICES

2015 1,087

2011

2012

2013

2014

1,393

1,314

1,116

1,113

967

941

799

813

807

98

79

68

64

63

328

294

246

239

217

Business Vacacional

29%

32%

71%

68%

2015

2014

EVOLUTION BY TYPE OF BUSINESS

13

2015 ANNUAL REPORT

in Portugal under a management contract and ac-

quired ownership of the Canoa Hotel in the Do-

minican Republic. Furthermore, the works for the

extension and improvement of the hotels in the

Dominican Republic continued and consolidated.

In 2015, Be Live Hotels reorganised itself into six

brands, Collection Resorts (5 star), Be Live Expe-

rience Hotels (establishments to suit all kinds of

guests), Be Live Family Resorts (family hotels), Be

Live Adults Only (absolute relax), Be Smart Ho-

tels (more economical holidays), and Be Live City

Center (city hotels, situated at strategic points).

The objective of the brand makeover was to of-

fer customers differentiated products and the

segment that best suits their needs.

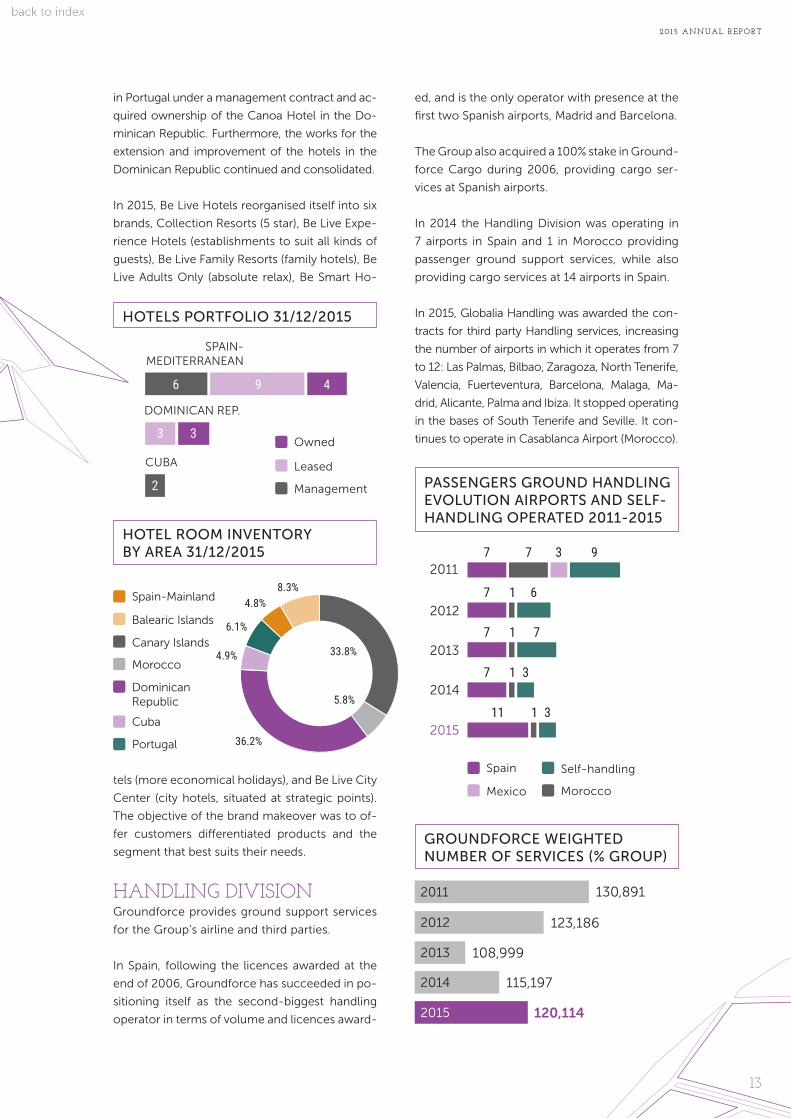

HANDLING DIVISIONGroundforce provides ground support services

for the Group’s airline and third parties.

In Spain, following the licences awarded at the

end of 2006, Groundforce has succeeded in po-

sitioning itself as the second-biggest handling

operator in terms of volume and licences award-

ed, and is the only operator with presence at the

first two Spanish airports, Madrid and Barcelona.

The Group also acquired a 100% stake in Ground-

force Cargo during 2006, providing cargo ser-

vices at Spanish airports.

In 2014 the Handling Division was operating in

7 airports in Spain and 1 in Morocco providing

passenger ground support services, while also

providing cargo services at 14 airports in Spain.

In 2015, Globalia Handling was awarded the con-

tracts for third party Handling services, increasing

the number of airports in which it operates from 7

to 12: Las Palmas, Bilbao, Zaragoza, North Tenerife,

Valencia, Fuerteventura, Barcelona, Malaga, Ma-

drid, Alicante, Palma and Ibiza. It stopped operating

in the bases of South Tenerife and Seville. It con-

tinues to operate in Casablanca Airport (Morocco).

HOTELS PORTFOLIO 31/12/2015

6 9 4

3

2

3

Leased

Owned

Management

SPAIN-MEDITERRANEAN

DOMINICAN REP.

CUBA

GROUNDFORCE WEIGHTED NUMBER OF SERVICES (% GROUP)

2015 120,114

2011

2012

2013

2014

130,891

123,186

115,197

108,999

Canary Islands

Dominican Republic

Balearic Islands

Spain-Mainland

Morocco

Cuba

Portugal 36.2%

4.9%

6.1%

4.8%8.3%

HOTEL ROOM INVENTORY BY AREA 31/12/2015

33.8%

5.8%

Mexico

Spain

Morocco

7

7

7

7

7

1

1

1

1

93

6

7

3

3

PASSENGERS GROUND HANDLING EVOLUTION AIRPORTS AND SELF-HANDLING OPERATED 2011-2015

2011

2012

2013

2014

201511

Self-handling

16

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Balance Sheets 31 December 2015 and 2014 (Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

Intangible assets Note 7 75,386 66,771

- Goodwill of consolidated companies Note 8 17,565 15,527

- Concessions 2,460 2,502

- Patents, licences, trademarks and similar rights 170 464

- Goodwill Note 8 11,087 11,087

- Computer software 32,296 31,661

- Greenhouse gas emission allowances 6,065 2,925

- Other intangible assets 5,743 2,605

Property, plant and equipment Note 9 546,555 499,656

- Land and buildings 227,122 231,039

- Technical installations, machinery, equipment,

furniture and other items 260,091 246,109

- Under construction and advances 59,342 22,508

Investment property Note 10 3,261 4,273

- Land 577 798

- Buildings 2,684 3,475

Non-current investments in Group companies and associates Note 14 571 384

- Equity instruments - (9)

- Equity-accounted investees 571 393

Non-current investments Note 16 92,182 83,967

- Equity instruments 3,135 3,141

- Loans to third parties 1,571 1,156

- Other financial assets 87,476 79,670

Deferred tax assets Note 28 44,870 47,768

Total non-current assets 762,825 702,819

Non-current assets held for sale Note 6 39,170 -

Inventories Note 18 22,125 23,202

- Raw materials and other supplies 19,749 16,480

- Advances to suppliers 2,376 6,722

Trade and other receivables Note 16 299,202 292,998

- Trade receivables – current 220,330 229,439

- Other receivables 22,794 20,052

- Personnel 961 895

- Current tax assets Note 28 5,307 6,440

- Public entities, other Note 28 49,810 36,172

Current investments Note 16 135,883 96,642

- Equity instruments 194 204

- Loans to companies 80,200 37,802

- Debt securities 55 55

- Derivatives Note 17 2,999 7,042

- Other financial assets 52,435 51,539

Prepayments for current assets Note 19 15,527 15,207

Cash and cash equivalents Note 20 49,933 63,540

- Cash 49,928 58,611

- Cash equivalents 5 4,929

Total current assets 561,840 491,589

TOTAL ASSETS 1,324,665 1,194,408

ASSETS 2015note 2014

17

2015 ANNUAL REPORT

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Balance Sheets 31 December 2015 and 2014 (Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

EQUITY AND LIABILITIES 2015note 2014

Capital and reserves Note 21 170,965 177,301

- Capital 16,894 16,894

- Reserves 109,728 130,850

- Reserves in consolidated companies 40,234 49,687

- Reserves in equity-accounted investees 3 (133)

- Profit/loss attributable to the Parent 4,106 (13,997)

(Interim dividend) - (6,000)

Valuation adjustments (23,001) (40,155)

- Hedging transactions Note 17 (31,860) (46,689)

- Translation differences 8,859 6,534

Non-controlling interests Note 22 1,416 1,872

Total equity 149,380 139,018

Non-current provisions Note 23 99,070 85,879

- Long-term employee benefits 180 180

- Other provisions 98,890 85,699

Non-current payables Note 25 201,769 129,450

- Loans and borrowings 94,998 30,059

- Finance lease payables 99,232 95,089

- Derivatives Note 17 95 281

- Other financial liabilities 7,444 4,021

Deferred tax liabilities Note 28 16,815 18,241

Total non-current liabilities 317,654 233,570

Liabilities associated with non-current assets held for sale Note 6 32,476 -

Current provisions 79,512 69,248

- Loyalty programmes 1,065 892

- Other provisions 78,447 68,356

Current payables Note 25 158,673 212,621

- Loans and borrowings 81,362 78,037

- Finance lease payables 17,693 14,897

- Derivatives Note 17 45,006 96,239

- Other financial liabilities 14,612 23,448

Trade and other payables Note 25 398,834 357,980

- Current payables to suppliers 272,643 238,255

- Other payables 14,881 17,763

- Personnel (salaries payable) 16,189 20,289

- Current tax liabilities Note 28 1,567 9,916

- Public entities, other Note 28 36,777 28,251

- Advances from customers 56,777 43,506

Current accruals Note 27 188,136 181,971

Total current liabilities 857,631 821,820

TOTAL EQUITY AND LIABILITIES 1,324,665 1,194,408

18

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Balance Sheets 31 December 2015 and 2014 (Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

Revenues Note 31 3,379,019 458,894

- Services rendered 3,379,019 458,894

Changes in inventories of finished goods and work in progress (30) -

Self-constructed assets 9,344 1,457

Supplies Note 31 (1,733,538) (225,122)

- Merchandise used (1,927) (214)

- Raw materials and consumables used (1,678,803) (218,820)

- Subcontracted work (52,808) (6,088)

Other operating income 35,786 597

- Non-trading and other operating income 35,786 597

Personnel expenses (459,962) (73,092)

- Salaries and wages (359,908) (57,765)

- Employee benefits expense Note 31 (100,054) (15,327)

Other operating expenses (1,089,385) (159,874)

- Losses, impairment and changes in trade provisions Note 15 (1,514) (1,062)

- Other operating expenses (1,087,871) (158,812)

Amortisation and depreciation Notes 7, 9 and 10 (50,124) (8,129)

Impairment and losses on disposal of fixed assets (808) (8,231)

- Impairment and losses Note 9 (234) (8,018)

- Losses on disposal and other Note 31 (574) (213)

Other income/expenses Note 31 (37,962) 73

Results from operating activities 52,340 (13,427)

Finance income 2,954 695

- Marketable securities and other financial instruments

- Group companies and associates - 3

- Other 2,954 692

Finance costs (30,214) (3,612)

- Other (27,560) (3,028)

- Provision adjustments (2,654) (584)

Change in fair value of financial instruments (323) (1,165)

- Trading portfolio and other Note 16 (323) (1,165)

Exchange gains/(losses) (17,274) 184

- Other exchange gains/(losses) (17,274) 184

Impairment and gains on disposal of financial instruments 17 4

- Impairment and gains Note 16 17 4

Net finance cost (44,840) (3,894)

- Share of profit/(loss) of equity-accounted investees 178 -

Profit/(loss) before income tax 7,678 (17,321)

Income tax Note 28 (3,985) 3,356

PROFIT/(LOSS) FOR THE YEAR 3,693 (13,965)

Profit/(loss) attributable to the Parent 4,106 (13,997)

Profit/(loss) attributable to non-controlling interests Note 22 (413) 32

2015note 2014

19

2015 ANNUAL REPORT

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Income Statements for the years ended

31 December 2015 and 2014(Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

2015 2014

Consolidated profit/(loss) for the year 3,693 (13,965)

Income and expense recognised directly in equity

- Cash flow hedges (42,103) (68,722)

- Translation differences

- Differences on translation into presentation currency 2,325 3,074

- Tax effect 10,526 19,199

Total income and expense recognised directly in consolidated equity (29,252) (46,449)

Amounts transferred to the consolidated income statement

- Cash flow hedges 64,461 -

- Tax effect (18,055) -

Total amounts transferred to the consolidated income statement 46,406 -

TOTAL CONSOLIDATED RECOGNISED INCOME AND EXPENSE 20,847 (60,414)

Total recognised income and expense attributable to the Parent 21,261 (69,446)

Total recognised income and expense attributable to non-controlling interests (413) 32

20

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Statements of Changes in Equity for the years

ended 31 December 2015 and 2014

A) Consolidated Statements of Recognised Income and Expense for the years ended 31 December 2015 and 2014

(Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

Balance at 31

decembre 2014 16,894 180,404 (13,997) (6,000) (40,155) 1,872 139,018

Adjustments to reserves - (442) - - - - (442)

Adjusted balance at

1 January 2015 16,894 179,962 (13,997) (6,000) (40,155) 1,872 138,576

Recognised income

and expense - - 4,106 - 17,154 (413) 20,847

Transactions with

shareholders or owners

- Distribution of profit

for the period

- Reserves - (13,997) 13,997 - - - -

- Dividends - (16,000) - 6,000 - - (10,000)

Changes to businesses

or companies

(see note 2 (b) - - - - - (43) (43)

Balance at

31 December 2015 16,894 149,965 4,106 - (23,001) 1,416 149,380

Capital Total

Reserves and prior years’ profit and

loss

Profit attributable

to the Parent

Interim dividend

Valuation adjustments

Non- controlling interests

21

2015 ANNUAL REPORT

GLOBALIA CORPORACIÓN EMPRESARIAL, S.A. AND SUBSIDIARIESConsolidated Statements of Changes in Equity for the years ended 31 December 2015 and 2014

B) Statement of Total Changes in Equity for the year ended 31 December 2014(Expressed in thousands of Euros)

The accompanying notes form an integral part of the consolidated annual accounts.

2015 2014Consolidated cash flows from operating activities

Consolidated loss for the period before tax 7,678 (17,321)

Consolidated adjustments for: 88,819 22,535

- Amortisation and depreciation 50,124 8,129

- Impairment 1,514 1,062

- Change in provisions 21,874 584

- Proceeds from disposals and sale of fixed assets 808 8,231

- Finance income (2,954) (695)

- Finance costs 27,560 3,028

- Exchange gains (10,320) (184)

- Change in fair value of financial instruments (17) 1,161

- Other income and expenses 408 1,219

- Share of profit/(loss) of equity accounted investees (178)

Changes in consolidated operating assets and liabilities (15,126) (53,967)

- Inventories 1,077 (2,069)

- Trade and other receivables (7,561) (13,242)

- Other current assets (37,536) 238

- Trade and other payables 49,203 (40,694)

- Other current liabilities (20,309) (12,373)

- Other non current assets and liabilities - 14,173

Other consolidated cash flows from operating activities (42,578) (2,333)

- Interest paid (27,281) (3,028)

- Interest received 2,954 695

- Income tax received (paid) (18,251)

Consolidated cash flows used in operating activities (38,793) (51,086)

Consolidated cash flows from investing activities

Payments for investments (164,545) (67,937)

- Intangible assets (21,473) (1,746)

- Property, plant and equipment (89,632) (16,972)

- Other financial assets (14,270) (49,219)

- Non-current assets held for sale (39,170)

Proceeds from sale of investments 20,158 34,645

- Intangible assets 3,034

- Property, plant and equipment 15,775 15,488

- Investment property 1,316

- Other financial assets 33 19,157

Consolidated cash flows used in investing activities (144,387) (33,292)

Cash flows from consolidated financing activities

Proceeds from and payments for financial liability instruments 101,987 63,212

- Issue 199,282 66,845

- Loans and borrowings 184,885 64,952

- Other 14,397 1,893

- Redemption and repayment of (97,295) (3,633)

- Loans and borrowings (84,424) (705)

- Group companies and associates (12,871) (2,928)

- Other

Dividends and interest on other equity instruments paid 10,000

- Dividends (10.000) -

Cash flows from consolidated financing activities 91,897 63,212

Net decrease in cash or cash equivalents (13,607) (21,166)

Cash and cash equivalents at beginning of the year 63,540 84,706

Cash and cash equivalents at year end 49,933 63,540

22

1. NATURE, ACTIVITIES AND COMPOSITION OF THE GROUP

Globalia Corporación Empresarial, S.A. (here-

inafter the Parent) was incorporated in Palma

de Mallorca on 14 May 1997. Its statutory activ-

ity consists of the rendering of management,

advisory and other business services as well as

the holding of fixed assets, investments, bonds,

shares and interests in other companies. In 1998

the Parent changed its name from GAE Corpo-

ración Empresarial, S.A. to its current name. The

Parent’s registered office is located in Polígono

de Son Noguera, Llucmajor, Balearic Islands.

The Globalia Group (hereinafter the Group)

operates in the transportation, travel and tour-

ism sector and basically comprises: the Parent,

as head of the Group; Air Europa Líneas Aére-

as, S.A.U., which acts as an air carrier and has a

fleet of 48 jet aircraft (45 aircraft at 31 December

2014); Globalia Business Travel, S.A.U. and Glo-

balia Travel Club Spain, S.L.U., which are present

in the tour operator sector Viajes

Halcón, S.A.U. and Viajes Ecuador

S.A.U., with 1,024 points of sale in

Spain (1,049 points of sale at 31 De-

cember 2014) and Halcón Viagens e

Turismo Lda, with 63 points of sale

in Portugal (63 points of sale at 31

December 2014), which sell tour-

ism-related products to customers;

Welcome Incoming Services, SLU,

which provides incoming services;

the Hotel division, headed by Be Live

Hotels, S.L.U. and operating a total of

27 hotels in Spain and the Caribbean

(29 hotels at 31 December 2014);

Globalia Handling, S.A.U., as head of the Han-

dling division, which provides ground handling

services at the main Spanish airports; Globalia

Autocares, S.L., which has a fleet of 43 coaches

(43 at 31 October 2014) and Globalia Manten-

imiento Aeronáutico, S.L.U., which owns and op-

erates the maintenance hangar located at Palma

de Mallorca airport. The Group also includes

other entities that provide ancillary services for

the core activities.

The Group also holds interests in associates and

jointly controlled entities and participates in sev-

eral joint ventures along with other venturers.

The administrative concessions operated by the

temporary joint ventures (UTEs), which provide

passenger handling and cargo services, have ex-

pired in 2015, except for Iberia Globalia Cargo

Barcelona U.T.E., which will expire in March 2016.

In 2015 the new concessions for handling ser-

vices in Spanish airports have been awarded (see

appendix V).

2. BASIS OF PRESENTATIONa) True and fair view The accompanying consolidated annual ac-

counts have been prepared on the basis of the

accounting records of Globalia Corporación

Empresarial, S.A. and subsidiaries. The consoli-

dated annual accounts for the year ended 31 De-

cember 2015 have been prepared in accordance

with prevailing legislation, the Spanish General

Chart of Accounts approved by Royal Decree

1514/2007 of 16 November 2007, and Royal

Decree 1159/2010 governing the preparation

NOTES TO THE CONSOLIDATED ANNUAL ACCOUNTSGLOBALIA CORPORACIÓN EMPRESARIAL, S.A.

AND SUBSIDIARIES

23

2015 ANNUAL REPORT

of consolidated annual accounts, to give a true

and fair view of the consolidated equity and con-

solidated financial position at 31 December 2015

and consolidated results of operations, changes

in consolidated equity and consolidated cash

flows for the period then ended.

The directors of the Parent consider that these

consolidated annual accounts, authorised for is-

sue on 3 March 2016, will be approved by the

Parent’s shareholders.

As required under prevailing legislation, the con-

solidated balance sheet, consolidated income

statement, consolidated statement of changes

in equity and consolidated statement of cash

flows for 2015 include comparative figures for

the previous year, which formed part of the con-

solidated annual accounts for the two-month

period ended 31 December 2014. The notes to

the consolidated accounts also include quantita-

tive information on the prior year, except where

an accounting standard specifically states that

this is not necessary.

b) Comparative information(i) Change of financial year

At their extraordinary general meeting held on 15

December 2014 the shareholders of the Parent

agreed to change the Company’s reporting date

to 31 December of each year (previously 31 Oc-

tober). As the figures in the consolidated annual

accounts for the year ended 31 December 2014

are for a period of two months only, they are not

comparable to those of the current year.

(ii) Changes in the consolidated Group

Changes in the consolidated group for the

year ended 31 December 2015 were as fol-

lows:

- Aeronova, S.L., Eurogestion Hoteliere, S.A.R.L.

and Panamericana de Servicios Energéticos,

S.A.S. were consolidated for the first time.

Changes in the consolidated group for the

two-month period ended 31 December 2014

were as follows:

- Pepechófer, S.L.U. merged with the Group

company Globalia Handling, S.A.U. The merg-

er became effective on 1 November 2014.

Orlean, B.V. merged with its sole shareholder

Globalia Travel, B.V. as proposed by the share-

holders at their general meeting. The merger be-

came effective on 24 December 2014.

- The first-time consolidation of LLucmajor Lim-

ited, which was incorporated 15 October 2014.

Synergy Global Comex, S.L.U. merged with Glo-

balia Servicios Corporativos, S.L. The merger be-

came effective on 1 November 2014.

c) Functional and presentation currencyThe figures disclosed in the consolidated annual

accounts are expressed in thousands of Euros,

the functional and presentation currency of

the Parent and most of the Group companies,

rounded off to the nearest thousand.

d) Critical issues regarding the valua-tion and estimation of relevant uncer-tainties and judgements used when applying accounting principlesRelevant accounting estimates and judgements

and other estimates and assumptions have to

be made when applying the Group’s accounting

principles to prepare the consolidated annual

accounts. A summary of the items requiring a

greater degree of judgement or which are more

complex, or where the assumptions and esti-

mates made are significant to the preparation of

the consolidated annual accounts is as follows:

i) Relevant accounting estimates and assumptions

The Group tests goodwill for impairment on an

annual basis. The calculation of the recoverable

24

amount of a division to which goodwill has been

allocated requires the use of estimates. The re-

coverable amount is the higher of fair value less

costs to sell and value in use. The Group generally

uses cash flow discounting methods to calculate

these values. Discounted cash flow calculations

are based on five-year projections in the budg-

ets approved by the Group. The cash flows take

into consideration past experience and repre-

sent the Group’s best estimate of future market

performance. From the fifth year cash flows are

extrapolated using individual growth rates. The

key assumptions employed when determining

fair value less costs to sell and value in use in-

clude growth rates, the weighted average cost

of capital and tax rates. The estimates, including

the methodology used, could have a significant

impact on values and impairment.

Group management estimates the useful life of

assets and their residual value. Given the com-

plexity and relevance of the residual value of the

aircraft owned or held under finance leases by the

Group, management uses reports prepared by in-

dependent third parties to estimate this value.

Air Europa Líneas Aéreas, S.A.U. is subject to

regulatory processes and inspections by govern-

ment bodies in charge of air traffic. The Parent

recognises a provision if it is probable that an

obligation will exist at year end which will give

rise to an outflow of resources embodying eco-

nomic benefits and the outflow can be reliably

measured. Legal processes usually involve com-

plex legal issues and are subject to substantial

uncertainties. As a result, management uses sig-

nificant judgement when determining whether it

is probable that the process will result in an out-

flow of resources embodying economic benefits

and estimating the amount. The calculation of

provisions for major repairs is subject to a high

degree of uncertainty given that it is based on an

individual analysis of the different components

subject to review for each aircraft. Air Europa

Líneas Aéreas, S.A.U. recognises provisions for

major repairs when the total cost can be reliably

measured.

Following usual sector practice, Air Europa

Líneas Aéreas, S.A.U. prepares an estimate of the

revenues from tickets sold and not used and that

will not be used in the future.

3. APPLICATION OF LOSSES OF THE PARENT

The application of losses of the Parent for the

two-month period ended 31 December 2014,

prepared by the directors and approved by the

shareholders at their annual general meeting

held on 29 April 2015, consisted of carrying for-

ward the full amount as prior years’ losses.

The board of directors will propose to the share-

holders at their annual general meeting that

losses of the Parent for the year ended 31 De-

cember 2015 be carried forward as prior years’

losses.

At 31 December non-distributable reserves of

the Parent are as follows:

Parent reserves: Legal reserve 3,379 3,379

2015

Thousands of Euros

2014

25

2015 ANNUAL REPORT

4. SIGNIFICANT ACCOUNTING POLICIES

a) Subsidiaries Subsidiaries are entities, including special pur-

pose entities (SPE), over which the Company,

either directly or indirectly through subsidiaries,

exercises control as defined in article 42 of the

Spanish Code of Commerce. Control is the pow-

er to govern the financial and operating policies

of an entity or business so as to obtain benefits

from its activities. In assessing control, potential

voting rights held by the Company or other enti-

ties that are exercisable or convertible at the end

of each reporting period are considered.

For presentation and disclosure purposes only,

Group companies are considered to be those

controlled by one or more individuals or entities

acting jointly or under the same management

through statutory clauses or agreements.

Control may also be exercised without owner-

ship by participating in the risks and rewards of

the entity; such companies are known as Special

Purpose Entities (SPE). Llucmajor Limited, which

was incorporated on 15 October 2014 to provide

guarantees to the aircraft manufacturer and the

financial institution regarding compliance with

the contract for the acquisition of two B737-800

aircraft until their delivery to Air Europa Líneas

Aéreas, S.A.U. in 2016, has been included in the

consolidated Group. However, at 31 December

2015 the Group has not consolidated the special

purpose entities called Palma Limited, El Prin-

cipio Limited and Bellver LTD that have assumed

the contractual position for the acquisition of

eight Boeing 787-8 because they are controlled

by the future lessors, which retain the risks and

rewards of this transaction. After delivery, Air Eu-

ropa Líneas Aéreas, S.A.U. will operate these air-

craft under operating leases.

The consolidated annual accounts include the

profit/loss of a subsidiary, See Europe Tours Lim-

ited, registered in the United Kingdom, which

has availed of the exemption from the audit of

individual annual accounts provided for in article

479a of the UK Companies Act of 2006.

Subsidiaries are fully consolidated.

Information on the subsidiaries included in the

consolidated Group is presented in Appendix I.

Information on companies that have not been

consolidated because their impact on the fair

presentation of the consolidated annual ac-

counts is immaterial has been included in Ap-

pendix II.

Transactions and balances with subsidiaries and

unrealised gains or losses have been eliminated

upon consolidation. Nevertheless, unrealised

losses have been considered as an indicator of

impairment of the assets transferred.

The Parent and its subsidiaries form an integrated

group engaged in transport, travel and tourism

and therefore transactions between the airline,

tour operators and travel agencies are very sig-

nificant. All accounts and transactions between

consolidated entities, particularly the aforemen-

tioned businesses, have been eliminated on con-

solidation, including investments between these

entities, giving rise, where applicable, to the cor-

responding goodwill on consolidation.

The subsidiaries’ accounting policies have been

adapted to Group accounting policies, for like

transactions and other events in similar circum-

stances.

The timing of the annual accounts or financial

statements of subsidiaries has been harmonised

and relevant adjustments have been made to

reflect the effect of transactions and significant

events occurred between the closing date of

subsidiaries and the closing date of the Parent.

b) Non-controlling interests Non-controlling interests in subsidiaries ac-

quired after the transition date are recognised at

the acquisition date at the proportional part of

the fair value of the identifiable net assets. Non-

controlling interests in subsidiaries acquired pri-

or to the transition date were recognised at the

proportional part of the equity of the subsidiaries

at the date of first consolidation. Non-control-

ling interests are presented separately from eq-

uity attributable to the Parent in the consolidated

balance sheet within equity. Non-controlling in-

terests’ share in profit or loss for the year is also

presented separately in the consolidated income

statement.

26

assets or disposal groups held for sale are recog-

nised at fair value less costs to sell.

Details of equity-accounted investees are includ-

ed in Appendix III. The Group’s share of the profit

or loss of an associate from the date of acquisi-

tion is recognised as an increase or decrease in

the value of the investment, with a credit or debit

to share in profit/loss of equity-accounted inves-

tees in the consolidated income statement. The

Group’s share of the total recognised income and

expense of associates from the date of acquisi-

tion is recognised as an increase or decrease in

investments in associates with a balancing entry

in consolidated equity accounts. The distribution

of dividends is recognised as a decrease in the

value of the investment. The Group’s share of

profit or loss, including impairment losses rec-

ognised by the associates, is calculated based on

income and expenses arising from application of

the acquisition method.

The accounting policies of associates have been

harmonised in terms of timing and measurement,

applying the policies described for subsidiaries.

The timing of the annual accounts or financial

statements of associates has been harmonised

and relevant adjustments have been made to

reflect the effect of transactions and significant

events occurred between the closing date of as-

sociates and the closing date of the Parent.

(i) Impairment

The Group applies the impairment criteria set

out in the section on financial instruments to de-

termine whether additional impairment losses to

those already recognised on the net investment

in the associate, or on any other financial asset

held as a result of applying the equity method,

should be recognised.

Impairment is calculated by comparing the car-

rying amount of the net investment in the associ-

ate with its recoverable amount. The recoverable

amount is the higher of value in use and fair value

less costs to sell.

Value in use is calculated based on the Group’s

share of the present value of future cash flows

expected to be derived from ordinary activities

and from the disposal of the asset, or the esti-

The profit or loss and changes in equity of the

subsidiaries attributable to the Group and non-

controlling interests after consolidation ad-

justments and eliminations, is determined in

accordance with the percentage ownership at

year end.

The profit/loss and recognised income and ex-

pense of subsidiaries are allocated to equity at-

tributable to the Parent and to non-controlling

interests in proportion to their investments, even

if this results in a balance receivable from non-

controlling interests. Agreements entered into

between the Group and non-controlling inter-

ests are recognised as a separate transaction.

Increases and reductions in non-controlling in-

terests in subsidiaries in which control is retained

are recognised as equity instrument transactions.

Consequently, no new acquisition cost arises on

increases nor is a gain recorded on reductions;

rather, the difference between the consideration

transferred or received and the carrying amount

of the non-controlling interests is recognised in

the reserves of the Parent, without prejudice to

reclassifying consolidation reserves and reallo-

cating other income and expenses between the

Group and the non-controlling interests. When

a Group’s interest in a subsidiary increases, non-

controlling interests are recognised at their share

of the consolidated net assets, including good-

will on consolidation.

c) Associates Associates are companies over which the Parent,

either directly, or indirectly through subsidiaries,

exercises significant influence. Significant influ-

ence is the power to participate in the financial

and operating policy decisions of the investee

but is not control or joint control over those

policies. The existence of potential voting rights

that are exercisable or convertible at the end of

each reporting period, including potential vot-

ing rights held by the Group or third parties, are

considered when assessing whether an entity

has significant influence.

Investments in associates are accounted for us-

ing the equity method from the date that sig-

nificant influence commences until the date that

significant influence ceases. However, associates

classified at the acquisition date as non-current

27

2015 ANNUAL REPORT

mated cash flows expected to be received from

the distribution of dividends and the final dispos-

al of the investment.

Nonetheless, and in certain cases, unless bet-

ter evidence of the recoverable amount of the

investment is available, when estimating impair-

ment of these types of assets, the investee’s eq-

uity is taken into consideration, adjusted, where

appropriate, to generally accepted accounting

principles and standards in Spain, corrected for

any net unrealised gains existing at the measure-

ment date.

d) Joint ventures Joint ventures are those in which there is a statu-

tory or contractual agreement to share the con-

trol over an economic activity, in such a way that

strategic financial and operating decisions relat-

ing to the activity require the unanimous consent

of the Parent and the remaining venturers.

Group joint ventures adopt the form of invest-

ments in jointly controlled entities, operations

and assets.

Details of jointly controlled entities are provided

in Appendix IV.

Jointly controlled operations and assets are

those in which there is a statutory or contrac-

tual agreement to share the control over an

economic activity, in such a way that strategic

financial and operating decisions relating to the

activity require the unanimous consent of the

Group and the remaining venturers.

Information relating to jointly controlled opera-

tions, referred to as temporary joint ventures, is

presented in Appendix V.

Investments in jointly controlled entities are pro-

portionately consolidated from the date joint con-

trol is obtained until the date joint control ceases.

However, investments that are classified as non-

current assets or disposal groups held for sale at

the date joint control is obtained are recognised at

fair value less costs to sell.

The Group recognises assets controlled and li-

abilities incurred in respect of jointly controlled

operations, as well as the proportional part of

jointly controlled assets and liabilities and of

expenses incurred and income earned from

the sale of goods or services by the joint ven-

ture. The statement of changes in equity and the

statement of cash flows also include the propor-

tional part corresponding to the Group by virtue

of the agreements reached.

Reciprocal transactions, balances, income, ex-

penses and cash flows have been eliminated in

proportion to the interest held by the Group in

joint ventures. All dividends have been eliminated.

Unrealised gains and losses from non-monetary

contributions or downstream transactions in

joint ventures are recognised based on the sub-

stance of the transaction. Where the assets are

retained by the joint ventures and the Group has

transferred the significant risks and rewards of

ownership, only the portion of the gain or loss

that is attributable to the interests of the other

venturers is recognised. Unrealised losses are

not eliminated if they provide evidence of an im-

pairment loss.

The Group only recognises the portion of gains

and losses on transactions in joint ventures that

is attributable to the interests of the other ven-

turers. In the event of losses, the Group applies

the same recognition criteria as those described

in the previous paragraph.

The Group has made the necessary measure-

ment and timing harmonisation adjustments to

incorporate its joint ventures in the consolidated

annual accounts.

The timing of the annual accounts or financial

statements of joint ventures has been harmo-

nised and the relevant adjustments have been

made to reflect the effect of transactions and

significant events occurred between the closing

date of the joint ventures and the closing date of

the Company.

e) Foreign currency transactions, balances and cash flows

(i) Foreign currency transactions,

balances and cash flows

Foreign currency transactions have been trans-

lated into Euros using the exchange rate pre-

vailing at the transaction date. Some Spanish

28

Group companies which operate in US Dollars

recognise purchases and sales using a standard

exchange rate, in accordance with the Group

policy of contracting the appropriate finan-

cial instruments to hedge against fluctuations

in the US Dollar exchange rate. The differences

between the standard exchange rate and the

settlement or hedging rate are recognised as ex-

change gains or losses in the income statement.

Monetary assets and liabilities denominated in

foreign currencies have been translated into

Euros at the closing rate, while non-monetary

assets and liabilities measured at historical cost

have been translated at the exchange rate pre-

vailing at the transaction date.

Non-monetary assets measured at fair value have

been translated into Euros at the exchange rate at

the date that the fair value was determined.

In the consolidated statement of cash flows,

cash flows from foreign currency transactions

have been translated into Euros at the exchange

rates at the dates the cash flows occur.

(ii) Translation of foreign operations

In accordance with the exception relating to

accumulated translation differences provided

for in the second transitional provision of Roy-

al Decree 1514/2007 approving

the Spanish General Chart of Ac-

counts, translation differences

recognised in the consolidated

annual accounts generated prior

to 1 January 2008 have been clas-

sified under reserves of the inves-

tor. Consequently, the historical

exchange rate applicable to the

translation of foreign operations is

the exchange rate prevailing at the

transition date.

As of that date, foreign operations

whose functional currency is not

the currency of a hyperinflationary

economy have been translated

into Euros as follows:

- Assets and liabilities, includ-

ing goodwill and net asset adjust-

ments derived from the acquisition

of the operations are translated at the closing

rate at the reporting date;

- Income and expenses are translated at the av-

erage exchange rate for the period; and

- All resulting exchange differences are recog-

nised as translation differences in consolidated

equity.

These criteria are also applicable to the trans-

lation of the financial statements of equity-ac-

counted investees, with translation differences

attributable to the Parent recognised in consoli-

dated equity.

The translation into Euros described in the pre-

ceding paragraph using the closing exchange

rate is performed on the functional currency.

Given the economic and financial characteristics

of certain companies’ activities, the functional

currency is considered to be the US Dollar rather

than the official currency of the country where

the registered office is located.

The translation from local currency to functional

currency implies the use of historical exchange

rates for the non-monetary balance sheet and

income statement items and the exchange rate

prevailing at year end for monetary items. Cash

29

2015 ANNUAL REPORT

and those items that are representative of ac-

counts receivable and payable are considered to

be monetary items.

When the date of the financial statements of for-

eign operations differs from that of the Parent,

the assets and liabilities, including goodwill and

net asset adjustments derived from the acquisi-

tion of the operations, are translated at the rate

prevailing at the reporting date of the foreign op-

eration and any necessary adjustments are made

to balances and transactions with the Group in

respect of exchange rate fluctuations up to the

reporting date.

f) Capitalised borrowing costs As permitted by the second transitional provision

of Royal Decree 1514/2007 approving the Span-

ish General Chart of Accounts, the Group opted

to apply this accounting policy to work in pro-

gress at 01 January 2008 that will not be avail-

able for use, capable of operating or available for

sale for more than one year. Until that date, the

Group opted to recognise borrowing costs as an

expense as they were incurred.

Borrowing costs related to specific and gener-

al financing that are directly attributable to the

acquisition, construction or production of in-

tangible assets (except capitalised research and

development expenditure), property, plant and

equipment, investment property, and inventories

that will not be available for use, capable of op-

erating or available for sale for more than one

year are included in the cost of the asset.

To the extent that funds are borrowed specifical-

ly for the purpose of obtaining a qualifying asset,

the amount of borrowing costs eligible for capi-

talisation is determined as the actual borrowing

costs incurred. Non-commercial general bor-

rowing costs eligible for capitalisation are calcu-

lated as the weighted average of the borrowing

costs applicable to outstanding borrowings dur-

ing the period, other than those specifically for

the purpose of obtaining a qualifying asset and

the portion financed using consolidated equity.

The borrowing costs capitalised cannot exceed

the borrowing costs incurred during that period.

When determining borrowing costs eligible for

capitalisation, adjustments to the finance costs

corresponding to the effective portion of hedges

entered into by the Group are considered. These

calculations are based on the Group’s financial

structure.

The Group begins capitalising borrowing costs

as part of the cost of a qualifying asset when it

incurs expenditures for the asset, interest is ac-

crued, and it undertakes activities that are nec-

essary to prepare the asset for its intended use,

operation or sale, and ceases capitalising bor-

rowing costs when all or substantially all the ac-

tivities necessary to prepare the qualifying asset

for its intended use, operation or sale are com-

plete, even though the necessary administrative

permits may not have been obtained. Interrup-

tions in the active development of a qualifying

asset are not considered.

g) Intangible assets Intangible assets are measured at cost of acquisi-

tion or production, using the same criteria as for

determining the cost of production of invento-

ries. Capitalised production costs are recognised

under self-constructed assets in the consolidat-

ed income statement. Intangible assets are car-

ried at cost, less any accumulated amortisation

and impairment.

Expenditure on activities that contribute to in-

creasing the value of the Group’s business as a

whole, such as goodwill, trademarks and other

similar items generated internally, as well as es-

tablishment costs, are recognised as expenses

when incurred.

(i) Industrial property, patents and trademarks

Industrial property rights primarily consist of

land rights over the plot on which the Be Live

Smart Talavera Hotel was built, amounting to Eu-

ros 2,425 thousand. These land rights are valid

for 75 years starting 16 November 2005 and are

amortised over the remaining useful life of this

concession from the date on which the Group

acquired the company, that is, 70 years.

This heading also includes the Iberrail trademark,

which was acquired from Viajes Unalia, S.A. in

October 2009 and is amortised over five years.

Administrative concessions include the costs in-

curred in their procurement.

30

(ii) Goodwill on consolidation and goodwill

Goodwill on consolidation arises from the con-

solidation of subsidiaries and joint ventures.

Goodwill arises from business combinations

recognised in the individual annual accounts of

consolidated companies. Goodwill is not am-

ortised but is tested for impairment annually or

more frequently where events or circumstances

indicate that an asset may be impaired. Good-

will on business combinations is allocated to the

cash-generating units (CGUs) or groups of CGUs

which are expected to benefit from the synergies

of the business combination applying the criteria

described in section (I) (impairment). After initial

recognition, goodwill is measured at cost less any

accumulated impairment losses. In accordance

with final provision one of Audit Law 22 /2015

of 20 July 2015, as of 1 January 2016, intangible

assets, including goodwill, shall be considered

assets with a finite useful life. Where the useful

life of intangible assets cannot be estimated re-

liably, they shall be amortised over a period of

ten years. Similarly, it will be presumed that the

useful life of goodwill, unless there is evidence to

the contrary, is also ten years. As indicated pre-

viously, the Group has recognised goodwill of

Euros 28,652 thousand. At the date of authorisa-

tion for issue of the annual accounts, the Direc-

tors are evaluating the accounting implications

of the Law, specifically as regards the estimation

of the useful lives of the aforementioned assets,

to determine its impact on the Group’s equity.

At the date of authorisation for issue of the an-

nual accounts, the Royal Decree implementing

the Law and, where appropriate, regulating the

transitional regime has not yet been passed.

(iii) Computer software

Computer software acquired and produced by

the Company, including website costs, is rec-

ognised when it meets the conditions for con-

sideration as development costs. Expenditure

on developing a website to promote and ad-

vertise the Group’s own products or services is

recognised as an expense when incurred. Com-

puter software maintenance costs are charged

as expenses when incurred.

(iv) Emission allowances

Under Directive 2003/87/EC and subsequent

amendments to the Directive of the European

Parliament and of the Council, which established

a trading scheme

for greenhouse gas

emission allowances in

the European Community,

measures aimed at reducing

the impact of aviation on climate

change came into effect in 2012, requir-

ing airlines to assume certain costs for CO2

emissions from flights from or to any country in

the European Union.

On 17 November 2014, the Company received

a notification from the Spanish Ministry for Ag-

riculture, Food and the Environment, stating

that Regulation (EU) No 421/2014 introduced a

number of amendments: the European emission

allowances trading scheme for 2013 to 2016 is

only applicable to emissions in the European

Economic Area. It is not applicable to emissions

from flights operated from 2013 to 2016 between

airports in the outermost regions, as defined in

article 349 of the Treaty on the Functioning of

the European Union (TFEU), and airports located

in another region in the European Economic

Area. From 1 January 2013 until 31 December

2020, the emission allowances trading scheme

will exclude flights undertaken by operators of

non-commercial aircraft with emissions of less

than 1000 tonnes per year

In accordance with the above, the number of

allowances granted free of charge to aircraft

operators should be reduced in proportion to