Making the world a better place to sit ANNUAL REPORT 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Making the world a better place to sit

AnnuAl RepoRt 2013

AnnuAl RepoRt 2013

Important events in 2013

Among the leaders in Europe

About Scandinavian Business Seating

The cEo’s report

corporate Management

corporate Governance

Scandinavian Business Seating chases new growth

Growth through clear differentiation

HÅG

RH

RBM

Directors’ report for 2013

consolidated annual accounts

Annual accounts Scandinavian Business Seating Group AS

Auditor’s report

corporate responsibility report

contacts

CONTENT

01

06

14

20

28

36

48

90

119

04

10

16

26

32

40

80

92

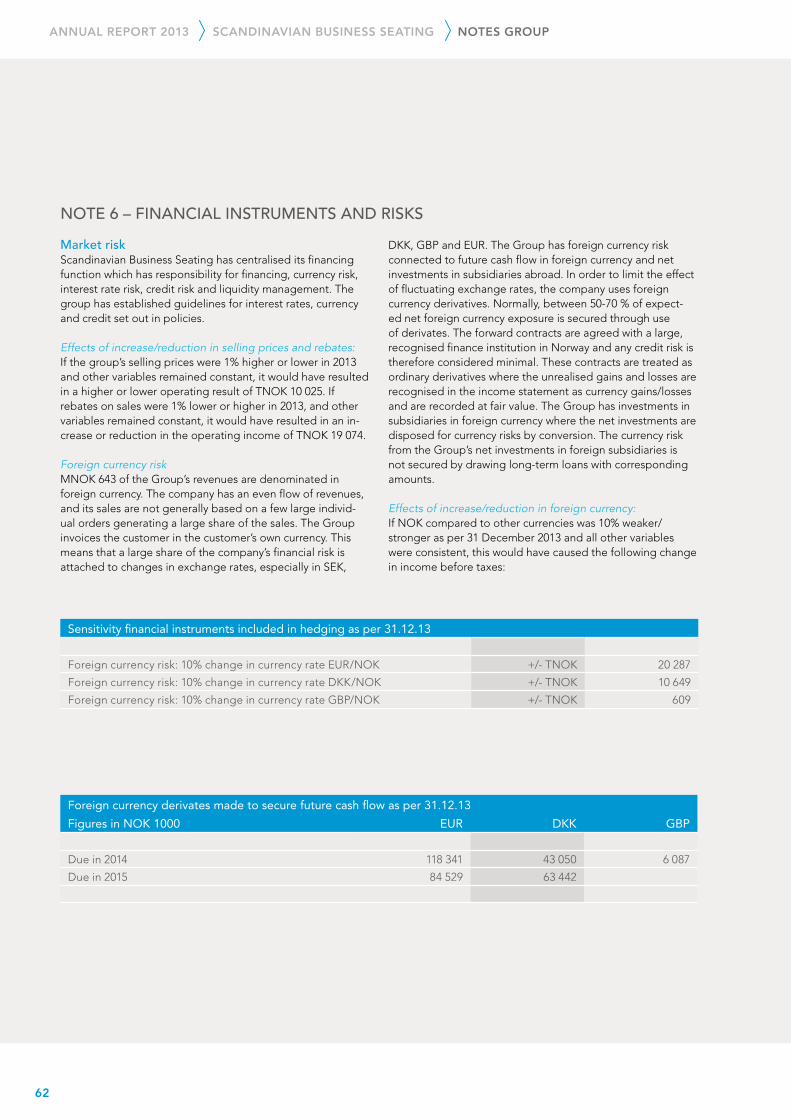

ImPORTANT EVENTS IN 2013

Increased market orientationthe office furniture market saw stable development in 2013. Sales performance in the different markets has varied according to the state of the market, and the group recorded a decline of just below 1 % in sales, compared with 2012. this is consid-ered satisfactory, particularly in relation to the challenges in the european markets. the reorganisation in the sales area, with the introduction of a new organisational model in the sales companies, was completed in 2013. this has given a clearer organisational model, with more defined roles and responsibili-ties, and a distinction between the Key Account Management teams (major projects) and the more dealer-focused teams.

New productsthe new HÅG SoFi, RH Mereo and RBM noor products were first launched at the Stockholm Furniture Fair in February 2013, and have received a very warm welcome on the market. the products have already managed to receive several awards and international recognition.

Still committed to AsiaIn 2013, the subsidiary in Singapore showed a positive devel-opment, and further potential in the region has been identi-fied. last year the group began the work of establishing own companies in Shanghai and Hong Kong.

Establishment in SwitzerlandIn June, the group established a subsidiary in Switzerland, Scandinavian Business Seating AG. on 1 July 2013, the group took over the dealer agreements and employees from our dis-tributor in Switzerland, and brought them to the new company. the running of our operation in Switzerland showed a positive development during the last half of 2013. Better margins and operating profitthe group has continued the work of increasing the efficiency of the entire value chain. A more structured procurement organisation, greater efficiency in the production processes and effective management of production capacity made a great contribution to margins in 2013. the operating profit was also positively affected by strict privatising and a focused approach to activities and fixed costs.

HÅG SoFi

RH Mereo

EBITAOperating revenues

Revenues and results (MNOK)

0

200

400

600

800

1 000

1 200

1 400

2013201220112010200920080

50

100

150

200

250

Some major customers/contracts in 2013

Norway: DNB Bank ASA Statkraft SF

Sweden: Ericsson Volvo Cars AB

Denmark: DSB Koncernen Tåstrup Danske Bank

Netherlands: Isala Klinieken ABN AMRO

UK: Schroders UK

France: LVMH – Moët Hennessy · Louis Vuitton

Switzerland: CERN

USA: AC Nielsen Chicago Northwestern University, Chicago

Malaysia: Telenor

Singapore: DNVDNV, Singapore

RBM Noor

3

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

RBM Low Back Bella/ RBM Allround bord

RBM Flip and Fold/HÅG Capisco

HÅG Capisco/HÅG SoFi – Deloitte, Norway

HÅG Futu

RH Support

Vision: To make the world a better place to sitMission: To offer the best seating solutions for working people

Scandinavian Business Seating is an international company in the office chairs, canteen- and conference furniture segment. Its head office is in Oslo, and it has production units in Norway and Sweden. The group also has sales companies in Denmark, Germany, the Netherlands, the UK, France, Singapore, Switzerland and China. The group is the largest supplier of office chairs in Western Europe.

HÅG, RBM and RH are rooted in the Scandinavia design tradition, based on unique design philosophies and concepts that target different buyer groups.

AMONG THE LEADERS IN EUROPE

4

Nor

way

Swed

en

Den

mar

k

Ger

man

y

Be-

Ne-

Lux

UK

Expo

rt

Fran

ce

Switz

erla

nd

Asi

a

Sales per market 2013

Sales per brand 2013

HÅG 59%

RH 31%

RBM 10%

Distribution number of units sold 2013

Swivel chairs 60%

Conference 35%

Other 5%

30%

18%15%

10%7% 6% 5%

3%1%1%HÅG Futu

Key figures 2013 2012 2011 2010 2009 2008

Operating revenues MNOK 1 003 1 010 1 091 1 010 989 1 289EBITDA MNOK 235 236 255 204 105 247Operating income MNOK 204 204 219 165 46 207EBITA margin % 20 20 20 16 5 16Income before taxes MNOK 80 83 81 72 (8) 26Net income MNOK 56 73 49 50 (9) 17Net interest bearing-debt MNOK 898 574 657 618 775 900Investments MNOK 61 58 28 19 31 60Total assets MNOK 1 880 1 829 1 864 1 835 1 859 1 985Net working capital 1)

% 16 11 14 14 13 15Equity share 2)

% 40 55 50 55 49 41No. of employees per 31.12. 472 475 479 463 457 633Full time equivalents per 31.12. 459 462 462 451 447 617No. of sold chairs Thousand 417 433 455 443 485

1) Inventory + accounts receivables - accounts payable in percent of operating revenues

2) Includes shareholder loan in 2012 and earlier.

5

ABOUT ScANDINAvIAN BUSINESS SEATING

Scandinavian Business Seating is the market leader in Scandinavia for the design, development and produc-tion of office chairs and seating for private and public office environments. Over the course of the last few years, the group has also cemented its position as the largest manufacturer of office chairs in Western Europe, in terms of value.

The group, which comprises Scandinavian Business Seating Group AS and its subsidiaries, owns the Scandinavian brands HÅG, RBM and RH, which all operate in the premium seg-ment of the office chair market.

Scandinavian Business Seating, with 470 employees, is ded-icated to realising the company’s vision: Making the world a better place to sit! The group has its head office in Oslo and production units at Røros in Norway and Nässjö in Sweden. In addition, the group has its own sales companies in Denmark, Germany, the Netherlands, the UK, France, Switzerland, Singapore and China, as well as a large network of independ-ent dealers and partners in other important markets for the company.

Ownership structureThe group was founded in June 2007 and changed its name to Scandinavian Business Seating in autumn 2008. All three merged companies were strong privately-owned start-ups with long traditions and extensive experience of developing, pro-ducing and marketing office chairs in Europe. HÅG has existed since 1943, RBM since 1975 and RH since 1977. The Swedish private equity conglomerate Ratos AB, which is listed on Nas-daq OMX Stockholm, acquired RH, RBM and HÅG in 2007.

Ratos owns companies in a range of industries and is one of Europe’s largest listed private equity conglomerates. Ratos had 18 companies in its portfolio in 2013, with 21 000 employ-ees, sales of SEK 42 billion and an operating income of SEK 3 billion. Ratos’s business concept is to generate, over time, the highest possible return through the professional, active and responsible exercise of its ownership role in companies. In ad-dition to a solid capital base, Ratos also contributes extensive experience and expertise to strategic, industrial, structural and financial processes at the companies it owns.

Market positionScandinavian Business Seating’s main market is Scandinavia, which accounts for 63 per cent of its total sales. Sales to other European markets account for around 31 per cent of total sales, with Germany, the Netherlands and the UK constituting the largest markets.

Office chairs and seating solutions account for about 40 percent of the total office furniture market in Western Europe, which is estimated to be worth around NOK 22 billion per annum. Today, the group is the market leader in office chairs in Scan-dinavia, with a market share of 34 per cent. Over the course of the last few years, the group has also bolstered its position as the largest manufacturer of office chairs in Western Europe, in terms of value. Scandinavian Business Seating is well posi-tioned in terms of price, function, design, environment and geographical cover to win new market shares within all its market segments.

6

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

HÅG SoFi

RH Mereo

The company´s three brands, HÅG, RBM og RH, are based on Scandinavian values and characteristics.

RBM Noor/RBM Twisted Little Star table

7

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

Business strategyScandinavian Business Seating has clear ambitions to expand still further, thereby cementing and strengthening its position as the leading office chair specialist in Europe. We abide by our motto of “different and better”, working with innovative new products and pursuing an offensive marketing strategy, inspired by two distinct market trends –health and the envi-ronment.

Sales and distributionThe group’s products are distributed via a network of inde-pendent dealers. The main markets are served by dedicated companies in Norway, Sweden, Denmark, Germany, the UK, the Netherlands, France, Switzerland and Singapore. The group has established a common export unit, Global Partner Organisation (GPO), for sales to other markets. GPO’s remit includes marketing and selling the company’s three brands to customers in the USA, Europe and the rest of the world via partners and importers. The company also enjoys close co-operation with interior designers, ergonomists and purchas-ers, who, together with our own organisation, provide good dialogue with and service for our end users.

Research and developmentInnovation and design are prerequisites for international success in our industry. Scandinavian Business Seating has a strong research and development culture, backed up by tradition and experience, within the spheres of design, ergonomics and the environment. Research and development work is deemed a top priority, both at brand and group level, with R&D facilities in Oslo and Røros in Norway and at Nässjö in Sweden.

We make the world a better place to sit!Nature did not design people to sit still in office chairs. We need movement and variation and for the person and worksta-tion to interact well in order to perform at our best and, at the same time, protect our health and the environment. Once we realise how much time we spend seated in office chairs, meet-ing chairs or other seating solutions, it becomes clear that the world deserves good chairs to sit on. Scandinavian Business Seating therefore wants to facilitate better performance at work by fulfilling the following mission: To offer the best seat-ing solutions for working people. Our vision, which is also our guiding light, is: To make the world a better place to sit.

Corporate social responsibilityAn overarching concept at Scandinavian Business Seating is that we have a clear responsibility above and beyond making money that involves protecting our shared environment and demonstrating corporate social responsibility and social accountability in areas where our activities come into contact with communities, locally and globally. We wish to achieve this through products and processes that are as resource efficient and environmentally-sound as possible, while also being safe in terms of health. We also work in a targeted man-ner to create a good working environment, with employees who are aware of their responsibilities as regards health and the environment. We provide our employees with training in environmental management systems, and we keep up to date with and comply with relevant laws and regulations within the quality and environment field.

Strong brands – HÅG, RBM and RHThe group’s three brands, HÅG, RBM and RH, are based on Scandinavian values and characteristics. At the same time they each occupy a niche in the office chair market, with dis-tinct design philosophies and concepts that meet the varying needs of the market and customers. Our seating solutions therefore focus strongly on ◆ visual design◆ ergonomics◆ environment◆ quality

A brand is all about the product’s function and user experi-ences, visual design and identity, and the story conveyed by the product.

All our products project a common Scandinavian identity:◆ User-oriented, functional design with optimum use of materials.◆ The right quality at the right price.◆ Balance between ergonomics, the environment and aesthetics, characterised by elegance and simplicity.◆ The most environmentally-correct products at this time.

It is the case that the above result in products that stand out in a market moving in so many different product directions.

8

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

ERGONOMIcS

qUALITy

ENvIRONMENT

vISUALDESIGN

9

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

THE cEO'S REPORT

Well positioned for growth, good profitability and new market sharesDespite stable and somewhat negative growth in the overall market, Scandinavian Business Seating achieved good results in 2013 through our improvement and development projects, and the largest product launches in the company's history. This makes us well positioned for growth, good profitability and new market shares, regardless of how the overall market develops in the time ahead.

Scandinavian Business Seating is the market leader in Scandinavia for the development, design and production of chairs for offices, canteens and conference rooms. The office furniture market in Europe showed more stable development in 2013 following negative growth in 2012. As Europe is our main market, this led to good profitability in 2013. The total turnover is in line with 2012, with growth in Denmark, the UK, France, Switzerland, the USA and Asia. We are noting a stable development in Germany, a negative development in the Netherlands, and a weak decline in Norway, Sweden and Finland due to a fewer number of major projects in the mar-ket. We have nevertheless taken a larger share of the project market in Norway.

Strengthened positionScandinavian Business Seating has reinforced its market posi-tion and also in 2013 has a significant share of the industry's total profitability. The good result is due to stable sales and an effective combination of sourcing and automation of our assembly. We also still note good effects of the past restruc-turing processes.

During 2013 we focused on growth and continuing to increase our market shares in the main markets. Despite a very chal-lenging market in Europe, we have succeeded at achieving growth in individual markets. We have also executed the

largest product launches ever in the history of the company, with three new main product series for all three of our brands, HÅG, RH and RBM. This has helped improve our position in the markets, and secure our leading position as an office chair specialist. Our commitment to the Asian market was further strengthened during the year. We have succeeded at establishing a presence, and have identified key potential for our product solutions in this region. We have also established a new subsidiary in Switzerland.

The company has conducted several projects for operational improvement that have yielded results. This has resulted in better margins and a stronger foundation for continued profitable growth and development. Scandinavian Business Seating now appears to be a company with the financial and organisational clout to take market shares and grow in the markets.

The successful product launches make us well-equipped to tackle different market scenarios, whether dealing with a mar-ket that is still volatile or a market with stronger growth.

Sales were slightly lower than the previous year in a market that on the whole saw negative growth in certain European markets. Despite the stable/negative development in the overall market, we achieved good results and reinforced our position for future good profitability through our improve-ment and development projects. The earnings before interest, tax and amortisation (EBITA) were 20.4 %, which is on the same level as last year. The good operating margin is due to our continued focus on the main markets and defined target markets (Asia and the USA), combined with operational improvement.

Lars I. Røiri

10

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

With its solid financial position and well-capitalised owners, Scandinavian Business Seating is well-positioned to take an active role in the coming consolidation process.

HÅG SoFi Communication/ RBM Twisted Little Star/RH Lounge

11

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

Favourable future prospectsWe anticipate the total market development in 2014 to remain uncertain but, as in 2013 with greater variations from market to market. The company's significant exposure in Scandinavia, and particularly Norway, is positive for the group because the macroeconomic prospects for Scandinavia are positive. As for Europe otherwise, we expect a strengthening of our market positions in 2014, partly due to our new products, which were well received on the market in 2013.

An increasingly stable and positive overall market in the medium term means that we continue to expect increased consolidation within the industry, following a lengthy period of very little activity. The market is still very fragmented, and consolidation will probably occur at the manufacturer level in particular. With its solid financial position and well-capitalised owners, Scandinavian Business Seating is well-positioned to take an active role in the coming consolidation process.As a major player in the industry, we strengthened our rela-tionships with customers and suppliers in 2013. Our strat-egy continues to focus on building closer partnerships and promoting long-term collaboration with our most important customers and suppliers. At the same time, we will continue the work of developing and increasing the efficiency of the work processes, when there is still room for improvement and further optimisation.

Scandinavian Business Seating will also continue our offensive focus on product development in 2014. This is an important part of our strategy to ensure that we expand our position as one of Europe's leading names within the development, design and production of seating solutions for office environ-ments. In 2013, we reinforced our position towards the goal to become the leading office chair specialist in the European markets. We will provide the best, most competitive seating solutions by "making the world a better place to sit".

2014 will give us substantial scope for strengthening the com-pany and reinforcing our market position, which will involve: ◆ growing in the European markets by selectively investing in

more resources in individual markets, and further develop-ing our sales and distribution process for increased sales productivity.

◆ actively developing our organisation, partner model and markets in Asia.

◆ keeping a high commitment and investment level in product development.

◆ developing and launching our future e-business model.

The environment and corporate social responsibilityThe group has focused on the environment for over 20 years. This can be seen in product solutions, choice of materials and processes that lead to lower greenhouse gas emissions, less use of chemicals and lower resource consumption. These atti-tudes are visible in everything from product development to production and sale, both in-house and through the require-ments we make on the rest of the value chain. We are pleased to see that also this work yields results and a competitive advantage. In 2013, we received the Norwegian Design Coun-cil's Environment Award for our new HÅG SoFi office chair. The group issues an annual corporate responsibility report based on the internationally recognised Global Reporting Initiative format. In addition to discussing environmental per-formance and goals, the report accounts for how the group works with suppliers in low-cost countries and how we handle our corporate social responsibility for both internal and exter-nal interested parties.

The group had 470 employees at the end of 2013. They are organised in an efficient matrix structure. We are an organi-sation with highly-skilled workers, and have further increased our expertise in key fields. In 2013, the organisation yet again proved its strength and competence through three major launches and several development projects. This is why it is not a cliché to state that our workers and our organisation are our main competitive advantage going ahead.

Scandinavian Business Seating is well-positioned for further growth and profitability, with a clear focus on creating the best possible growth potential for the group.

Lars I. RøiriCEO

12

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

HÅG SoFi Communication

201320122011201020092008

4,6%

16,1% 16,4%

20,0% 20,2% 20,4%

EBITA-MARGIn

13

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

1

2

cORPORATE MANAGEMENT

1. Ketil Årdal (b. 1970)Senior Vice President Commercial OperationsResponsible for sales in Europe and marketing. Joined in 2012. Training and experience from the Norwegian Armed Forces. Holds a diploma from BI / Varehandelens Høyskole and has completed business programmes at the London Business School and the IMD in Lausanne. Ketil began his career at Kellogg's, and has worked internationally at Findus and Duni.

2. Christian Eide Lodgaard (b. 1970)Senior Vice President Products & Brand Concepts Responsible for product development. Joined in 2007. MSc in Science and previously worked at Hydro Aluminium Automotive.

3. Patrik Röstlund (b. 1970)Senior Vice President Manufacturing & Purchasing OperationsResponsible for production, procurement and logistics. Joined in 2010. Holds a Bachelor in Business Administration. Previously worked at Saab Automobile and General Motors.

4. Lars I. Røiri (b. 1961)CEOJoined Scandinavian Business Seating (HÅG) in 1999 and was appointed Managing Director in 2001. Became CEO of Scandinavian Business Seating when the group was formed in June 2007. MSc in Business. Previously worked at Tomra, Saba-Mølnlycke, Jordan and Coloplast Norge.

5. Lillevi E. Øglænd Ivarson (b. 1964) Senior Vice PresidentHR & Organisation Development Responsible for the HR function. Joined in 2007. MSc in Business. Previously worked at Hydro and Yara.

6. Eirik Kronkvist (b. 1969)Chief Financial Officer / CFOResponsible for the accounts, finances, legal and IT. Joined in 2010. Bachelor in Business Administration and MBA in strategic management. Previous experience from Compaq Computer Norge, Hewlett Packard Norge and Steria.

7. Frederik Fogstad (b. 1965)Senior Vice President Global Partner Organisation (GPO)Responsible for sale to markets outside Europe. Joined in 2013. Education and experience from the Norwegian Armed Forces. MSc in Business. Past experience from Varier Furnitu-re AS, Kunde & Co, INTERSPORT, Kellogg’s, Middelfart and Coca Cola.

14

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

4

3

5

7

6

15

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

cORPORATE GOvERNANcE

The company complies with the Norwegian recom-mendations regarding corporate governance. As the company is not listed on the stock exchange, its corporate governance has been tailored to the company’s situation. 94 % of the company’s shares are owned by the Swedish listed investment company, Ratos AB. The remaining shares are owned by a large number of executives and board members.

Scandinavian Business Seating has defined its values. Together with the company's corporate culture, this forms the basis on which the board and management believes that Scandinavian Business Seating should be managed. The company's most important success factor has been its ability to develop, produce and market new seating solutions for office environments. Innovation, a cost-efficient procurement function, flexible production, familiarity with the market, and effective sales work are key success factors for Scandinavian Business Seating. Scandinavian Business Seating strives to maintain high ethical standards in its business practices. All of the companies and employees must comply with the relevant laws and regulations in the country in which they work. The company practises values-driven management based on its values. The company has drawn up guidelines for ethics and corporate social responsibility.

BusinessThe objects clause in Scandinavian Business Seating’s articles of association stipulates that: “The company’s activities are the production and sale of office furniture, including chairs. This also comprises directly or indirectly owning other com-panies that perform such activities, the provision of admin-istrative services and other services to such companies, and anything else naturally related to this.”

Scandinavian Business Seating designs, develops, produces and markets seating solutions for office environments. Growth and good profitability will be created through a high degree of innovation, modern Scandinavian design, good ergonomic solutions and a people and environment-oriented approach to the products.

The group's executive management team currently has seven members. They cover the group's main processes in the value chain: CEO, R&D, production and procurement, sales and marketing, HR and finance/IT. The group's executive management team is constantly tailored to suit the compa-ny's strategic and operational development. The CEO has day-to-day responsibility for Scandinavian Business Seating's activities and manages the organisation within the framework set by the board.

Equity and dividendsThe company's equity share as at 31.12.2013 was 40 %. No dividends will be paid in the short and medium term, as avail-able liquidity will primarily be used to invest and repay debt. The board does not have a mandate to increase capital.

Equal treatment of shareholders and transactions with close associatesScandinavian Business Seating has two share classes. Each A (ordinary) share is worth one vote, while B-shares do not have a vote. The company has laid down guidelines that require the board to be notified when board members or the CEO have significant interests in a transaction entered into by the company.

16

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

General meetingsScandinavian Business Seating’s supreme body is the general meeting. The ordinary general meeting must be held every year by the end of March.

Nomination committeeA nomination committee has not been established for the election of shareholder-elected board members. As a result of the ownership structure, it has been natural that the work related to the composition of the board’s shareholder-elected members be handled by the largest shareholder, Ratos AB.

Corporate assembly and board: composition and independenceThe company's articles of associations state that the board must consist of one to ten people, as determined by the general meeting, with the addition of board members that the employees may be entitled to elect. The current board of Scandinavian Business Seating has five members, all of whom are shareholder-elected. The board’s chair is selected by the general meeting. The board is broadly made up of technical, marketing and financial expertise. There are no limits on the terms of board members, as the board’s composition is reg-

ularly reviewed. The CEO is not a member of the board, but regularly attends the board meetings. Scandinavian Business Seating Group AS has no employees, and is a holding company. The employee's representatives sit on the boards of the operating companies Scandinavian Business Seating AS and Scandinavian Business Seating AB.

A dedicated group committee has been established to secure good and open dialogue between the management and the employee-elected representatives across the organisation and geographical location. The committee has permanent members from the sites (two from Røros, two from Nässjö, and one from Oslo), as well as members from the manage-ment and the HR department. Three meetings are normally held each year.

Scandinavian Business Seating and its underlying subsidiaries do not have their own corporate assemblies. An agreement has been concluded on extra board representation from the employees of Scandinavian Business Seating AS. The board of Scandinavian Business Seating AB also has employee representatives.

Group CEOLars I. Røiri

Manufacturing & Purchasing OperationsPatrik Röstlund

Commercial OperationsKetil Årdal

Products & Brand ConceptsChristian Eide Lodgaard

Finance, IT, Legal & RiskEirik Kronkvist

HR & Organisation DevelopmentLillevi Ivarson

Global Partner Organisation (GPO) Frederik Fogstad

ORGANISATIONAL STRUCTURE:

FUNCTIONALRESPONSIBILITY

COMMERCIALRESPONSIBILITY

17

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

The boards of Scandinavian Business Seating's other subsidi-aries consist of the CEO of Scandinavian Business Seating, as chairman of the board, and members of the group's executive management team.

The work of the boardThe board has overall responsibility for the management and control of the company. The management group updates the company’s three-year strategy plan every year on behalf of the board. This plan also contains the company’s financial target figures. The board approves general strategies and sets strategic and financial goals, which are maintained in the company's three year strategy plan and in the annual budget. Outside board meetings, the board serves as advisers to the management group.

Six board meetings are held according to a fixed meeting and work plan. They are linked to the approval of quarterly figures and regular strategy work. The board has rules of procedure, and annually assesses its work. The board appoints the com-pany’s CEO. The CEO performs his or her work pursuant to a job description, the company’s budget and strategy plan, and contact with the board.

The board has a dedicated audit committee made up of selected members of the board. This committee prepares business for review before final decisions are made at the board meeting. The committee performs tasks related to financial reporting, the annual accounts, internal control, and has contact with the company’s auditor. The board annually reviews and approves the company’s policies.

Risk management and internal controlEvery month, and as needed, the CEO reports on the com-pany’s position and financial performance to the board in writing.

Scandinavian Business Seating systematically revises its strategies based on a three-year rolling plan. Every year an extended group of key managers is involved in this work before the strategies are represented to the board. All employees are involved later and are informed of the content and the consequences for their areas of responsibility. The final, revised strategy provides the basis for the coming year's goals and priorities in the company's business plan. The strategy plan must be plain and simple, and provide clear guidelines for every function in the organisation. The ISO 9001 and ISO 14001 general management/quality system is reviewed and evaluated annually. The group’s interest and currency strategy is set by the board, provides guidelines to

secure a good financial structure and to reduce risk in relation to fluctuations in the interest levels and exchange rates.

Scandinavian Business Seating has a number of internal controllers who are organised under a group controller who reports to the CFO. The group has also drawn up a framework for risk management – a so-called Enterprise Risk Manage-ment framework. This framework determines how to work to identify, handle and follow up business risk at the group. The key strategic and operational risk is followed up closely through action plans and regular reporting. The board is regularly briefed on this work.

Remuneration of the boardThe board’s remuneration is reported in note 22 of the com-pany’s consolidated annual report. The board’s remuneration is fixed by the general meeting every year. The board’s remu-neration is not linked to performance. The board members hold no options in the company. The board members have shares in the controlling company Scandinavian Business Seating AS. The list can be found in note 22.

Remuneration of executivesThe remuneration of the CEO and other group management is reported in note 22 of the company’s annual report. The board fixes the terms of the CEO based on a proposal from the chairman of the board. There is no fixed bonus system for executives. However, various forms of bonus schemes are practised, where financial performance and qualitative goals are the most important indicators.

AuditorThe financial positions of almost all of the group’s companies are audited by the auditing firm Ernst & Young. The com-pany’s central finance department cooperates with Ernst & Young in Norway to ensure good and coordinated auditing in all of the group’s units. The auditor’s fees are reported in note 9 of the company s consolidated annual report. Informa-tion is provided at the general meeting about the breakdown of the auditor's remuneration into auditing and other services. The auditor regularly attends audit committee meetings, and attends board meetings that review the annual accounts.

Audits of health, safety and the environment and the mainte-nance of ISO certifications are carried out by Veritas auditors.

18

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

HÅG Sideways

RH Lounge

RBM Ana 19

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

ScANDINAvIAN BUSINESS SEATING cHASES NEW GROWTH

Encouraged by all of the company's positive achieve-ments during the past few years, and the fact that the company has taken the correct steps in a challenging market situation, the management of Scandinavian Business Seating appears offensive, proactive and with great self-confidence at the beginning of a new year. With a newly-trimmed sales organisation, three new product series that have been well received on the market, good profitability and satisfied custom-ers, the main drivers of continued growth, increased profitability and new market shares are in place.

"It has taken us several years to get where we are now. When competitors have had to make cuts during difficult times in recent years, we have had enough profitability to invest and build for the future. Without needing major new investments, we now have significant potential for volume growth as a result of the investments that have already been made in product development, new product launches, a completely new sales organisation, a better foothold in new markets and revitalisation of existing markets," says Scandinavian Business Seating CEO Lars Røiri.

Differentiation"We have committed to the most profitable segment of the office furniture industry: office, canteen and conference chairs, which is the largest segment in the industry, the segment with the most frequent replacement, and the segment where it is possible to differentiate oneself from the competition, as we have succeeded at our differentiation and our three brands HÅG, RH and RBM. During the past six years in particular, our product development has increased our focus on visual design, quality, health/ergonomics and environ-mentally-friendly and sustainable production and products,

so that we can now proudly say that we are industry leaders in documentation of sustainable production and sustainable products. We have incorporated this into our whole design philosophy and our design process. This has turned out to be a profitable venture, which is now paying off. In most tender processes we see an increasing demand for documentation of the environmental impact of the products," says Røiri.

Product development and sales"Despite our recently having launched three new product series, for which we have great hopes in all of our markets, we are definitely not resting on our laurels. Product develop-ment is the main driver of continued growth. We will therefore continue to invest at the same level as earlier in this area, which means that it is still our goal to invest five per cent of our annual turnover in product development. This means that the market can expect new products in office, meeting room and canteen chairs from Scandinavian Business Seating every single year in the near term," says Røiri.

He further has great expectations towards the results of the reorganisation that has taken place in the group's sales and marketing work, where the main focus is now on using the same sales method around the world, with a focus on project sales that yield volumes. This means visiting more customers, dealers and partners, and becoming an even better partner to them. This must take place through active participation on major projects, transfer of competence to the end-customer, training and development of the dealership network, selective focus on those who want to become large and professional, early and direct dialogue with the customer to solve and meet the customer's needs and, not least, close contact with both the network of dealers, contractors and architects to identify projects and generate leads at an early stage of the process.

20

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

From the left: Ketil Årdal, Frederik Fogstad and Lars I. Røiri.

When competitors have had to make cuts during difficult times in recent years, we have had enough profitabili-ty to invest and build for the future.

21

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

Europe and the USA"During the past few years, we have managed to take market shares in a challenging European market. This puts us in a good position when we now see that the European market is gradually improving. We still have a strong position in Scandinavia, which has been the best corner of the world after the financial crisis, with continued strong potential in both Sweden and Denmark. We also have a solid foothold in Germany, the United Kingdom, the Netherlands, France and Switzerland. We judge the opportunities to be good for organic growth in these markets, especially after we have put a better and more efficient sales organisation in place," says Røiri.

He receives support for this view from Ketil Årdal, who has a seat on the corporate management, with responsibility for the markets in Europe.

"Going ahead, it is motivating that we have managed to take market shares in a challenging European market. We have managed this by professionalizing the sales and marketing work, establishing own subsidiaries with their own showrooms in the main markets (Benelux, the United Kingdom, Germany and Switzerland), establishing KAM functions with a focus on the project market and through a clear strategy and plan for transferring competence to our dealers. This has allowed us to move closer to our end-customers. I also see that we have managed to exploit all of the commercial synergies by fully integrating all sales and marketing work with our other business models. This allows us to avoid fragmentation and suboptimalization of the sales work," says Årdal, who is also pleased that the new product launches have been successful in both Scandinavia and the European market.

"It was the dynamic philosophy behind the chairs, the func-tionality and user-friendliness, that led us to choose HÅG. HÅG chairs prepare us for a flexible future where no person has their own workspace, and where chairs intuitively can be understood and used by employees". (Edwin Swart, Product and Contract Manager, ABN AMRO, Central Facility Services)

"What is most important going ahead will be to keep and reinforce our good position and our market shares, both in Scandinavia and in the rest of Europe. With new people and new sales competence in place in key markets, we will now have to focus on working both smarter and better in the market, and delivering results following from the new form of work," says Årdal, who is also pleased that the company has gradually succeeded at revitalising parts of the US market, in which it has had a presence for a long time, but where the competition from US companies is strong.

Asian hub strategy "We have also consciously committed to new markets in Asia," says Fredrik Fogstad, who sits on the corporate man-agement, with responsibility for Asia and markets in which the company does not have subsidiaries.

UK Showroom. Clerkenwell, London22

We chose HÅG chairs in fierce competition with other alternatives because our employees wanted them. They are the chairs that offer the best combination of comfort and style. We chose HÅG because of its quality.

(Ernst A. Meyer, VP & Regional Manager, DNV GL Oil & Gas, South East Asia)

23

HÅG SoFi Communication

"There is significant growth in the large Asian market, where growth during the past few years has been 5–10 per cent in our industry. By way of comparison, the overall market in Europe has not moved during the same period, with some variations from market to market. There is also a large seg-ment in Asia for products in the medium and high end mar-ket; segments that are concerned with and demand quality, brands and design from Europe; something we represent," says Fogstad.

"Effectively profiting from the growth in the region going ahead requires a clear focus in the operational efforts, which is why we have a conscious hub strategy, where we want to establish ourselves in large population centres like Shanghai, Hong Kong, Singapore, Beijing and other 'highly potent' metropolises and development areas, also in South Korea. We have therefore made conscious choices based on resource use and options for a return."

"We chose HÅG chairs due to the good ergonomics of the chairs and how this can contribute to employees' health and productivity. Reliable logistics, deliveries and installation at the right time were also key factors in a challenging region like Myanmar. Telenor has had good experience with HÅG

chairs since 2001, which made the choice simple also this time. The 10-year guarantee says it all." (Petter Russ, Product Manager, Telenor Real Estate, International)

We established ourselves in Singapore already two years ago, and now have a KAM function for the project market, sales staff, a showroom and customer service at this hub. We are setting up operations in Shanghai with Chinese employees, copying the Singapore model. We are very conscious of hiring people with a large network of architects, designers, contrac-tors and others who can quickly help us enter into a dialogue with the project market and the end-customer, who ultimately makes decisions on our products and deliverables. The plan is then to set up operations this year in Hong Kong following the same model. We have had a good start in several of these places in that we have made deliveries to several of our Nor-wegian customers once they have established operations in these locations, says Fogstad, who believes that the strongest drivers for continued growth in Asia will be that Scandinavian Business Seating has a focus on and faith in what it does, and sells what it has and who it is. This means globalising and being faithful to the company's values and 'cornerstones' (quality, the environment, ergonomics and design), and telling

24

Reference projects delivered by Scandinavian Business Seating:

SCANDINAVIA:NCC's main office in Norway (Oslo) ◆ Voted one of the world's 100 best in sustainable solu-

tions by global environmental organisation Sustainia 100: "Cost-efficient building with spectacular architecture and a good indoor climate that inspires and invites cooperation, and shows the way to a sustainable future."

◆ Nominated, as the only Nordic building, to the "Best Innovative Green Building" at the MIPIM Awards (European real estate and city development fair), which is one of the most prestigious awards that can be won by architects and developers.

EUROPE:ABN Amro (Netherlands) ◆ ABN Amro is one of the largest banking companies in the

world. ◆ A key factor in the company's long-term strategy is its goal

to be a leading employer. In an uncertain economic climate and in a world that is constantly changing, the company believes that it cannot afford to lose talents, and believes that what is most important is to create the best place to work.

◆ The above also reflects the company's choice of office furniture and office chairs. ABN Amro has replaced 8,000 chairs at its main office in Amsterdam since 2011.

LVMH (France)"According to LMVH (Möet Hennessy · Louis Vuitton), Scandi-navian Business Seating was chosen as a supplier of chairs for all laboratories and sewing departments due to its exclusive seating solutions, represented by brands HÅG and RH. The opportunities afforded by being able to adapt the chairs to all the different work situations at LVMH led the company to choose HÅG and RH in order to secure the well-being of its highly-qualified employees. The quality and sustainability of our products was also appreciated by LVMH." (Olgica Pezin, Country Manager, Scandinavian Business Seating, France)

ASIA:Telenor (Myanmar, Asia)

◆ Telenor won the telecommunications contract in Myanmar, and needed to quickly establish a base for 1,000 employees.

◆ As a pioneer in innovative workplaces in Asia, represented by its regional headquarters in Bangkok, Telenor wanted to extend this thinking in Myanmar. This is part of the work to attract the best employees in the region.

◆ Telenor's interior designer was Hassel, who also designed its regional headquarters in 2005. The project in Myanmar is based on a three-year contract, with planning and build-ing of a new and larger office building to handle expected growth.

Det Norske Veritas (DNV) – HQ in Singapore / "Standard Green" ◆ DNV Technology Centre received an award from the Sin-

gapore Building & Construction Agency; the Green Mark Award.

◆ The new offices house a total of 500 employees, who were previously based at four different locations on the island.

◆ DNV's office in Singapore combines an intelligent building structure and effective energy consumption.

◆ HÅG has delivered over 500 office chairs and 200 meeting room chairs to the new DNV offices.

the same story in every market, because it has now been documented that this meets the different decision-makers, regardless of their geographical location.

"This is why we will spend this year training and teaching all of our partners our concepts, values, design philosophy, busi-ness models and, not least, the environment and sustainabil-ity," says Fogstad.

25

GROWTH THROUGH cLEAR DIffERENTIATION

Scandinavian Business Seating builds all of our work around our four cornerstones: quality, the environ-ment, ergonomics and visual design. This means that we can present HÅG, RH and RBM on a foundation of quality and environmental thinking, while highlighting a solid differentiation between the brands based on a unique history of dynamic ergonomics and clear visual design.

The differentiation makes sense to our buyer group's preferences, and significantly contributes to the work to take more market shares in the countries in which we operate.

The same history in every stageWe have spent considerable resources on training our employees to understand why we bring out new and inno-vative products faster than our competitors, what innovation means in terms of functionality and benefits, and how we will bring the products onto the market in a way that creates demand.

Our employees are gathered and united around the story of our cornerstones, and create enthusiasm through a focus on the clear benefits to all people who sit. Every day. Again and again.

Having a strategic focus on building competence both inter-nally and externally has given us a major competitive edge in our markets. On the whole, this has led to the creation of a pan-European understanding and a momentum that is paving the way for further growth.

Digital ventureThe Sales & Training Portal is the first of several digital tools that have come from our comprehensive work to improve our digital sales platform. In the time ahead, we will launch a number of new tools on all types of digital platforms that will make it easier to build added value into our brands – and even easier for our customers to come into direct contact with our concepts and products.

An appealing, engaging and clear presentation of our con-cepts, products and world-class Scandinavian design will help increase our appeal and interest among our target groups. It will be even more important to continue to create interest, an opinion, value and trust in our brands among all of our target groups.

26

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

27

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

HÅG SoFi

28

29

HÅG

The HÅG movementHÅG was founded in 1943 and has been manufactured in Røros, Norway since 1957. In the early 1970s, HÅG went against conventional wisdom and chose a different approach to ergonomic sitting: HÅG established what is still a unique ergonomic philosophy of balanced sitting, which is based on the conviction that people are not made to sit still, but for variation and movement.

HÅG is one of the strongest brands in the office chair market in Scandinavia and one of the top 10 in Europe. This position has been achieved thanks to the brand's unique approach to sitting. Every time we develop a new HÅG product, we bring consid-erable innovation, while remaining true to HÅG's still unique philosophy: HÅG inBalance® keeps you in balanced, contin-uous movement without needing to think about it. We call it "the HÅG movement".

A HÅG chair is designed for the active worker, and ensures that people are alert throughout the working day. Consistent Scandinavian design, accessible functionality and pioneering environmental thinking come together as a greater whole:

Furniture2013 focused on launching and implementing the new HÅG SoFi office chair, which was first shown at Orgatec in Cologne in 2012. With a formidable presentation and reception at the Stockholm Furniture Fair as a beginning, the good start continued in our other markets. The common denominator here is that the HÅG SoFi attends to the user's need for visual and perceived comfort, and provides a good user experience. Through fully-upholstered organic forms and integrated han-dles, the HÅG SoFi appears to be a piece of furniture more than other office chairs. It creates calm and a sense of home at work.

Good designThe HÅG SoFi received the Award for Design Excellence and the Environmental Award for sustainable production from the Norwegian Design Council in 2013. This makes HÅG the brand that has won the most awards from the Norwegian Design Council throughout the years. HÅG's products have received a number of international awards over the years, including the Red Dot Design Award and the iF Design Award.

At its best ageThe HÅG Capisco chair has won a number of prizes for its properties and its characteristic design. After almost 30 years on the market, more HÅG Capisco chairs were produced and delivered in 2013 than ever before. The semi-sitting concept represented by this model was designed and developed by Peter Opsvik in the 1980s, and is as unique and is actually more attractive today than ever before. The product has been a pioneer in environmentally-friendly design and still has a very good environmental profile, compared with its compet-itors. As the first office chair in the world, it was awarded the Nordic Swan label in 2010, and has also met the new stricter requirements for this environmental label.

Environmental pioneer For many years the HÅG brand has distinguished itself inter-nationally through a conscious commitment to the environ-ment and corporate social responsibility. HÅG's office chairs were among the first in Europe to be certified by the US GREENGUARD Environmental Institute. All HÅG collections are also certified according to ISO 14025-EDP (Environmental Product Declaration). This is a certification that shows that HÅG chairs stand out by having the lowest CO2 emissions in the industry.

30

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

HÅG Capisco

Balanced sitting keeps you moving– without having to think about it.

31

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

32

RH Mereo

33

RH

Designed for human performanceWith roots back to 1977, RH is an integral part of the Swed-ish design tradition. When the first RH chair was launched, it attracted warranted attention because it took users seriously. Today, the RH chair is recognised by ergotherapists, physio-therapists and other professionals for its unique ergonomic philosophy. It is based on the importance of an upright sitting position, support and movement. These are qualities that increase the users' job satisfaction, and thus also the employ-ees' efficiency and productivity. From the very beginning, RH's philosophy has been to combine ergonomics and functional design. The strong brand concept "Designed for Human Performance" was incorporated later, to underline the fact that good design and correct ergonomics lead to documenta-ble improvement in performance for organisations that use our products. This has helped make RH office and work chairs market leaders in several European countries, especially in RH's main segments – offices, health care and industry – where users make particularly high requirements on function and design.

Innovation and designAll RH chairs have been developed with a focus on function-ality. RH products are accordingly comfortable ergonomic chairs that offer many adjustment possibilities and are durable. Despite the advanced construction and maximum performance, they are easy to understand and use, with clear pictograms and intuitive handles and grips. The 2PP™ princi-ple was developed for RH. This is a two-point principle that helps the body maintain an upright sitting position and gives good support, while the chair's unique frictionless movement encourages motion. This technology is the basis for all chair series from RH.

Great success with the new RH MereoThe RH Mereo chair family was launched at the Stockholm Furniture Fair in February 2013. The chair became a

fantastic success for the RH brand following production start in August 2013, and has already won a number of major contracts, and become the standard chair for many companies. Our aim in developing the RH Mereo was that the chair would meet the requirements of the dynamic and flexible offices of the future. Our focus was therefore to develop a chair that can be quickly and easily adjusted to the needs of the individual, without compromising ergonomics or performance. The RH Mereo is a product that offers a high level of individual seating comfort, dynamic ergonomics, user friendliness and flexibility that has not been seen on the market before. Extensive use of recycled aluminium instead of steel in many structural parts, together with a high percentage of recycled plastic in large components such as the seat and back, helps give the RH Mereo a world-class carbon footprint.

World-class ergonomics The aim for RH is that the ergonomics and design of the products contribute to increasing the efficiency of the organ-isations that use the products. In 2013, RH received the FIRA Ergonomics Excellence Award for its chairs for the 13th year running. RH is the only brand to have received the award since it was established. This is a strong testament to the RH brand's commitment to first-class ergonomics.

Environmental commitmentThe RH brand focuses on new solutions to protect the environment. This is achieved through Scandinavian Business Seating's commitment to high-quality products and sustaina-ble production processes. The company is certified according to the ISO 14001 environmental standards. Many other com-ponents of the RH chair series are also made using recycled materials. RH was among the first office chair manufacturers whose products were certified in accordance with the interna-tional EPD system (Environmental Product Declaration).

34

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

RH is the ultimate work tool that always places you in the best seated position to perform.

RH Mereo

35

ANNUAL REPORT 2013 ScANdiNAviAN BUSiNESS SEATiNg ThE ORgANiSATiON

RBM Noor

36

37

RBM

Vitalising space and relations With its lightweight, playful designs and clean lines, RBM is the ideal choice for open environments where people work, meet, learn and socialise.

The RBM collection consists of a wide range of smart solu-tions in the form of tables and chairs designed to meet our customers' needs and please our users. RBM's products are functional, easy to use, easy to combine in flexible combi-nations for use in meeting rooms, canteens and conference environments.

RBM provides a good and inviting atmosphere, under the motto "Vitalising space and relations".

Philosophy and focus on peopleScandinavian Business Seating's brand RBM was established in Denmark in 1975, and has roots in Danish and Scandinaviandesign traditions. Continuous product development has helped create friendly, comfortable and inviting spaces that inspire communication and collaboration in different environ-ments.

RBM products are based on sound ergonomic and functional principles, with good comfort and the possibility of individual adaptation, which promotes a flexible working environment for users.The concept is based on the design having the power to change environments and the way people in the environ-ments feel, collaborate and perform.

All aspects of RBM's products, from materials, design and production to the sales and support apparatus, are founded on providing high quality and people-centred design.

The RBM NoorThe RBM Noor is our new colourful chair collection for can-teens, conference rooms and meeting rooms. The chair was launched at Stockholm's Furniture Fair in February 2013, and received an excellent welcome. In July, also the RMB Noor received the renowned design award "Red Dot; Best of the Best Award" in the product design category.

The RMB Noor is the result of an innovative joint-venture between our product development environment and three Scandinavian design agencies: Form Us With Love (FUWL) from Sweden, StokkeAustad from Norway and Grønlund Design from Denmark.

The RBM Noor's rounded and friendly form is an expression of our people-centred design, which guarantees the user

good seating comfort. The collection has a smart modular collection platform with 8 models, and has a large and inspir-ing composition of polypropylene and 3D plywood shell, textiles and underframe.

The RBM Noor meets all high environmental standards at Scandinavian Business Seating, and is therefore a very envi-ronmentally-friendly and sustainable design.

The RBM Low-back Bella The RBM Low-back Bella was also launched at the Stockholm Furniture Fair in February 2013. This is an expansion of the classic Bella series, designed by renowned industrial designer Tias Eckhoff. The chair has a low back, which gives the design a stylish low profile, so that it easily fits into most environ-ments.

RBM's design teamThe RBM Noor and the RBM Low-back Bella have further strengthened RBM's design history. Collaboration with other leading designers also ensures that the brand is always at the forefront of development, while continuing our Scandinavian design traditions. ◆ Millions of the 1980 RBM Ana by Tias Eckhoff have been

sold. ◆ Industrial designers Blum & Balle A/S from Denmark are

responsible for the RBM Ultima folding table, the RBM Cameo conference chair and the RBM 600 office chair.

◆ Acer Design A/S, Denmark designed the RBM Connect table collection.

◆ Harrit & Sørensen A/S, Denmark designed the RBM Sweep sofa and table collection.

◆ Bare Møbler AS designed the RBM Twisted Little Star and the Flip and Fold collections.

RBM, Scandinavian Business Seating and the environmentSustainable production is a natural assumption for Scandi-navian Business Seating, and the company constantly strives to reduce its impact on the environment. The company is certified according to the ISO 14001 environmental manage-ment system. In the process of designing and manufacturing new RBM products, we always focus on using as few parts as possible and the most eco-friendly materials.

The RBM Noor and the new RBM Ana chair series are among several RBM products that leave a very small carbon footprint (EPD), and are also certified in accordance with the GREEN-GUARD Indoor Air Quality (IAQ) programme for products with low emissions.

38

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING THE ORGANISATION

RBM Noor/RBM Eniment table

RBM is all about positive meetings and joyful moments between people. Space and relations.

39

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING THE ORGANISATION

Scandinavian Business Seating is the market leader in Scandinavia for the design, development and production of seating solutions for office environ-ments. Scandinavian Business Seating is a brand name supplier and markets HÅG, RH and RBM. The group’s head office is in Oslo and production takes place at its factories in Røros, Norway and Nässjö, Sweden. The group also has sales companies in Sweden, Denmark, Germany, the Netherlands, the UK, France and Singa-pore.

Scandinavian Business Seating Group AS is the parent company of the group. It is a holding company for three companies: Scandinavian Business Seating AS in Norway, Scandinavian Business Seating AB in Sweden and Scandinavi-an Business Seating A/S in Denmark. The company’s activities include direct or indirect ownership of other companies en-gaged in the production and sale of office furniture, including chairs, the provision of administrative and other services to such companies, and anything else naturally associated with this.

Going concernThe group has good levels of profitability and equity. In ac-cordance with section 3-3 of the Accounting Act, it is hereby confirmed that the prerequisites for the going concern as-sumption exist and accordingly the financial statements have been prepared based on the going concern principle.

Market and general conditionsThe office furniture market has seen a more stable develop-ment in 2013 than was the case in 2012. During the first half year, market development was level, due to the unrest in the Eurozone, but from autumn onward the group noticed a positive trend in some markets, such as Denmark, Sweden, Germany and the UK. From a sales point of view, the most

challenging markets in 2013 were Benelux, Sweden, Germany and Southern Europe.

Sales performance in the different markets has been varied, and the group recorded a decline of -0.8 % in total sales in 2013 compared with 2012, which is considered to be sat-isfactory in view of the challenges that have existed in the European markets.

For the year as a whole, there was a reduction of sales in Scandinavia of one per cent, compared with the previous year. Norway was the only Scandinavian market that did not show an increase compared with 2012. This is due to there being fewer large projects in the Norwegian market in 2013. In the group’s European subsidiaries, there was an increase of two per cent in sales compared with the previous year. The other export markets saw sales grow by one per cent compared with the previous year.

In 2013 the number of units sold fell by 3.8 %. The proportion of revenues from each brand remains unchanged from 2012. New orders in Q4 2013 were 19% higher than the same peri-od in 2012 after a relatively slow post-summer start.

At the end of Q4 2013, the group concluded the acquisition of the importer in Switzerland. The acquisition was an asset agreement with the purchase of dealer contracts. Scandinavi-an Business Seating AG was established on 1 July 2013. Sales in Switzerland showed a positive trend in the third and fourth quarters.

In November 2013, Scandinavian Business Seating Ltd opened its new showroom in Clerkenwell, London. This is an important part of the efforts in the UK, where the group intends to strengthen its position through Key Account Man-agement focus on the project market in London.

REPORT fROM THE BOARD Of DIREcTORS 2013

40

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING DIREcTORS’ REPORT

HÅG H09 Inspiration

41

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING DIREcTORS’ REPORT

The group has strengthened its efforts in Asia in 2013. In Q4 the process of establishing a subsidiary in China, Scandinavian Business Seating (Shanghai) Co. Ltd., was begun. The es-tablishment of a Shanghai office will supplement the group’s existing office in Singapore in serving the Asian market.

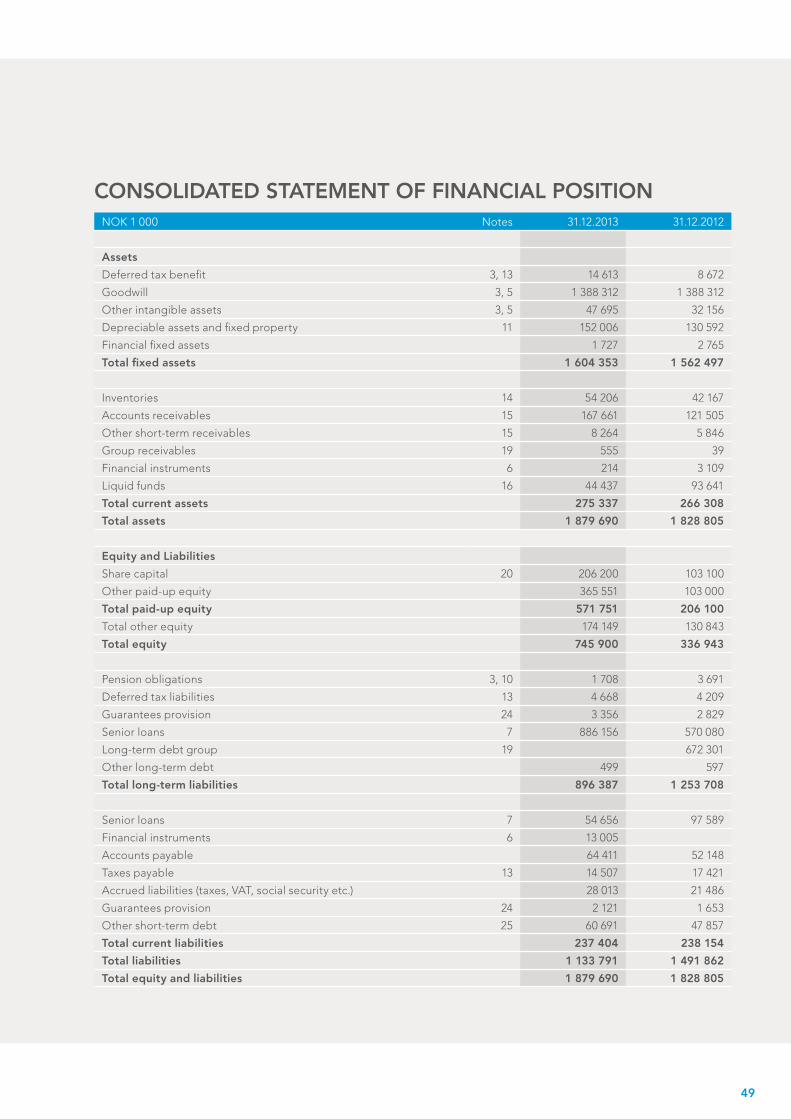

Income statementThe operating income for the period for Scandinavian Busi-ness Seating Group AS was NOK -5.6 million, compared with NOK -3.1 million in 2012. After net financial income of NOK 51.9 million, the income before tax was NOK 46.3 million. Net income for the year was NOK 33.5 million compared with NOK 18.5 million in 2012. The company’s income consists of group contributions and interest income from the subsidiaries.

Operating revenues for the group in 2013 were NOK 1,091 million compared with NOK 1,010 million in 2012. Operat-ing income (EBITA) for the period were NOK 204.4 million compared with NOK 203.7 million in 2012. The operating margin in 2013 was 20.4%, an improvement of 0.2 percentage points from the previous year. In 2013 the group had positive contributions from effective production, effective control of direct material, freight costs and the level of fixed costs. The development of prices of raw materials has made a positive contribution to margins in 2013.

Net financial expenses were NOK 124.9 million compared with NOK 121.1 million in 2012. The increase is due to higher inter-est expenses compared with the previous year. Income before tax was NOK 79.6 million compared with NOK 82.6 million the previous year. Net income was NOK 56.4 million, a decrease of NOK 16.7 million from 2012.

Balance sheet and liquidityTotal investments in 2013 amounted to NOK 61.5 million com-pared with NOK 58.1 million in 2012. Most of the investment was in connection with tools and moulds for new products and production equipment.Investments were made up of investment in fixed assets of NOK 43.0 million, acquisition of subsidiaries of NOK 7.0 mil-lion and recognised development costs of NOK 11.5 million.

The group has had good liquidity throughout the year. At year-end 2013 net interest-bearing debt amounted to NOK 898 million, an increase of NOK 320 million since year-end 2012. During the course of 2013 the group has repaid NOK 1,075 million of long term liabilities, of which NOK 385 million relates to repayment of a subordinated loan and NOK 690 million was for repayment of a bank loan. The group’s bank agreement was refinanced in December 2013 and a new long-term loan of NOK 950 million was taken up.

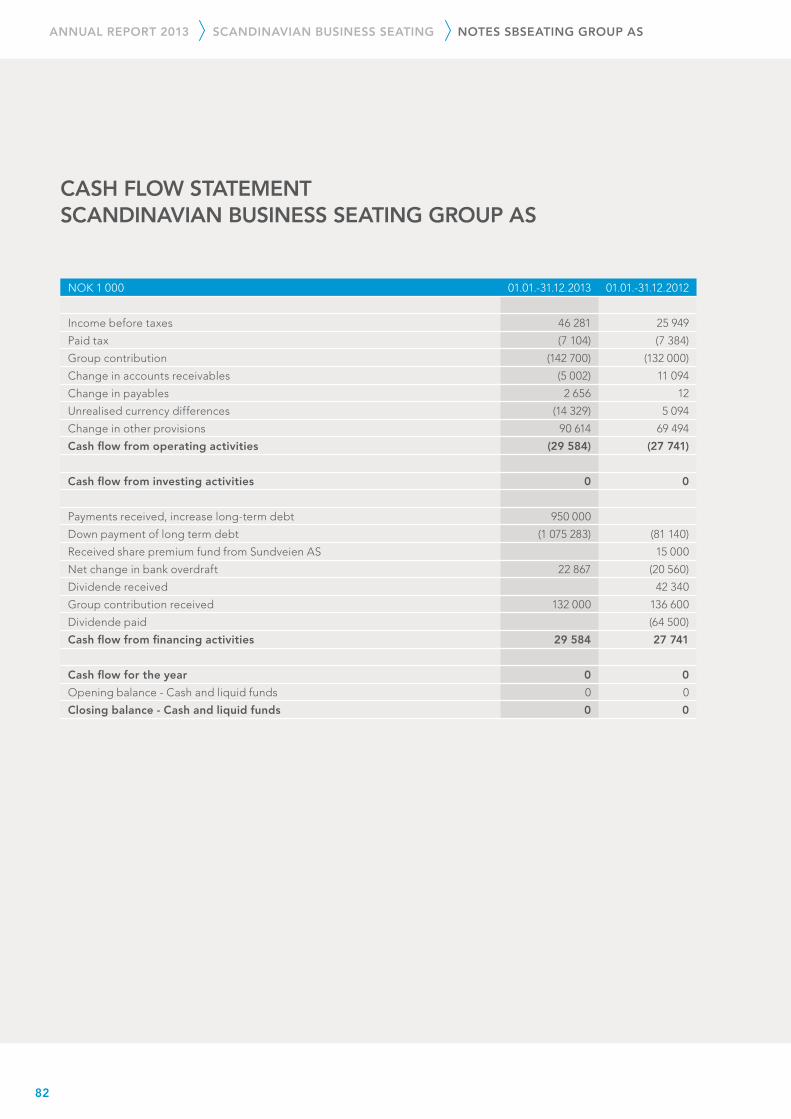

Total cash flow from operating activities amounted to NOK 134.8 million. Differences in relation to the operating income are mainly due to depreciation, taxes paid and changes in working capital.

Total assets at year-end amounted to NOK 1,864 million, an increase of NOK 51 million from year-end 2012. The equity ratio was 40% at the end of 2013 compared with 55% at the end of 2012. The company’s current liabilities at year-end were 21% of total liabilities, an increase of five percentage points on the year before. The total debt-equity ratio was 60% compared to 45% in 2012. The changes are mainly due to repayment of loans shareholders in 2013, which were classified as equity in 2012.

The greater part of the interest cost in connection with the subordinated loan from shareholders was not paid out, but was converted to equity in connection with a capital increase adopted by the general meeting of 31 December 2013. Debt financing is subject to requirements concerning the achieve-ment of key figures linked to the result and solvency. The company was within these requirements at year end 2013.

At the start of 2014 the group has total credit of NOK 1,053 million. This consists of borrowings of NOK 953 million and an overdraft limit of NOK 100 million. Available funds in the form of unused credit and bank deposits amounted to NOK 144 million at year end.

Increase of capital from conversion of liability into equityThe group’s financing structure was changed in December 2013, as a result of which the shareholder loan was replaced by a bank loan. NOK 385,000,000 of the shareholder loan was repaid and the remainder was converted into equity. This was done in connection with the refinancing of the group, by which the liability of the parent company Scandinavian Busi-ness Seating Holding AS to the shareholders was repaid in full or converted into B shares (preferential shares).

The board found it appropriate to convert the liability to the parent company Scandinavian Business Seating Holding AS into equity, so as to ensure that Scandinavian Business Seating Group AS was not affected by the new interest cut-off rules. The general meeting of 31.12.13 voted to increase the share capital of Scandinavian Business Seating Group AS through the conversion of loans from shareholders. Liabilities totalling NOK 365.7 million were converted into equity in Scandinavian Business Seating Group AS. This amount consisted of share-holder loans including accrued but unpaid interest as at the date of the general meeting of NOK 78.4 million.

Amendment to the articles of associationAs a result of the capital increase, article 4 has been amended to read as follows: “The share capital is NOK 206,200,000, made up of 10,310,000,000 shares each with a face value of NOK 0.02.”

Research and developmentIn line with the group’s differentiation strategy and product focus, there has been a strong emphasis on innovation and

42

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING DIREcTORS’ REPORT

RH Extend/RBM Noor

43

ANNUAL REPORT 2013 ScANDINAvIAN BUSINESS SEATING DIREcTORS’ REPORT

product development. Four new products were launched in 2013 and are in production. The RH Mereo chair series rep-resents a lift for the RH brand and appeals to the project and multi-use market. HÅG SoFi is a completely new work chair in the main product range of the HÅG brand, with an innovative new armrest function, which sets the standard for user-per-ceived quality and refined design. RBM Noor is an extensive collection of canteen, conference and meeting room chairs with an individual but friendly design, good comfort and unique combination possibilities and environmental prop-erties. RBM Low-back Bella was also launched. All products were well received by the media, their target group and the market generally. Altogether four patents were registered and four design awards were won by the new products.

Improvement work in 2013 has been focused on stronger organisation and processes for future development projects and product maintenance. Development expenses amount-ing to NOK 11.5 million were capitalised by the group in 2013 in line with IFRS.

Financial riskJust under 70% of sales revenues are invoiced in currencies other than NOK. A large proportion of the company’s financial

risk is therefore linked to fluctuations in exchange rates, especially with respect to SEK, DKK and EUR. The majority of raw material purchases are made in NOK, SEK and EUR. To reduce exchange rate risk, currency derivatives are used. The company’s balance sheet is exposed to exchange rate fluctua-tions in EUR, since loans in SEK exceed receivables in SEK, an exposure which is not hedged.

Credit risk associated with counterparts being unable to meet their financial obligations is regarded as acceptable. The majority of the company’s sales are in Northern and Central Europe. Sales are made to our own sales companies and to dealers and importers the group has worked with for some time. Historically, losses from receivables have been limited and accounted for 0.02 % of revenues in 2013. Gross accounts receivable as per 31.12.2013 amounted to NOK 168 million. The company regards its liquidity as good. No decision has been made to implement measures which will change the liquidity risk.

Scandinavian Business Seating has centralised its financing function which has responsibility for financing, currency risk, interest rate risk, credit risk and liquidity management.

RBM Noor/RBM Eminent table

44

The Board has adopted guidelines for financial risk management, which have been set out in policies.

Production, logistics and purchasing Work during the past year on streamlining purchasing has had effects on materials costs, transport costs and warehouse values. Considerable resources were invested in the factories in Røros and Nässjö so as to optimise production for the new products that were launched in 2013. With effect from December 2013, organisational changes were made in that the organisations for purchasing and production/logistics were merged together under common management. Work on optimising the new organisation will proceed in 2014, which is expected to have a positive effect on efficiency, as well as improving service levels to the mar-kets. Work on improving quality, reducing tie-up of capital, balanced logistics costs and optimising materials costs will also have a high priority in 2014.

Working environment, equality and discrimination

The holding company, Scandinavian Business Seating Group AS, has no em-

ployees. The company contracts administrative services from the subsidiaries.

The group has been working for many years at strengthening and further developing the company’s culture and working environment. Systematic working environment surveys with subsequent specific follow-up plans in the line ensure a good working environment and clear value creation in the group. The company’s core values, focus on leadership, competence development, equality of opportunity, health and safety, the environment and organisational conditions are all important factors in securing and steadily improving a good working environment.

2013 has been marked by organisational changes in the commercial area. The market organisations have been further strengthened with more resources i both dealer sales and Key Account Management. Good, clear training of new employ-ees has a high priority, so that they can easily find their place in the group, with a good understanding of the processes and strategies at an early stage of their employment. SB Seating Academy has been at the centre of a number of competence building measures in both sales and management. There is a

45

good, trustful relationship between the company and trade unions. This is an important area for dialogue and informa-tion.

At Scandinavian Business Seating everyone, regardless of gender, age and background, must have equal opportunities for employment and development. Furthermore, women and men performing the same work will in principle be paid the same salary, prior to assessing work performance. In the case of new appointments and with the composition of teams/departments, every effort must be made for a working envi-ronment with variation in gender, age and background. The group actively works to prevent discrimination due to age, gender, disability, ethnic background, national origin, skin colour, religion or personal beliefs.

At year-end 2013, the group had 472 employees, of which 309 were men and 163 women, equivalent to 34% of the workforce. The company’s board has one female member, a proportion of women equivalent to 20%. There is one female member of the group’s executive management, a proportion of women equivalent to 14%.

There were fifteen work-related injuries in the company dur-ing the course of 2013. These injuries resulted in a total of 71 days absence.

External environmentScandinavian Business Seating has been focusing on the environment for more than 20 years, in both its processes and its products. It has long been clear to the company that it is important to take the entire life cycle into consideration, since more than 90 per cent of the products’ impact on the envi-ronment occurs before the components arrive at the group’s factories.