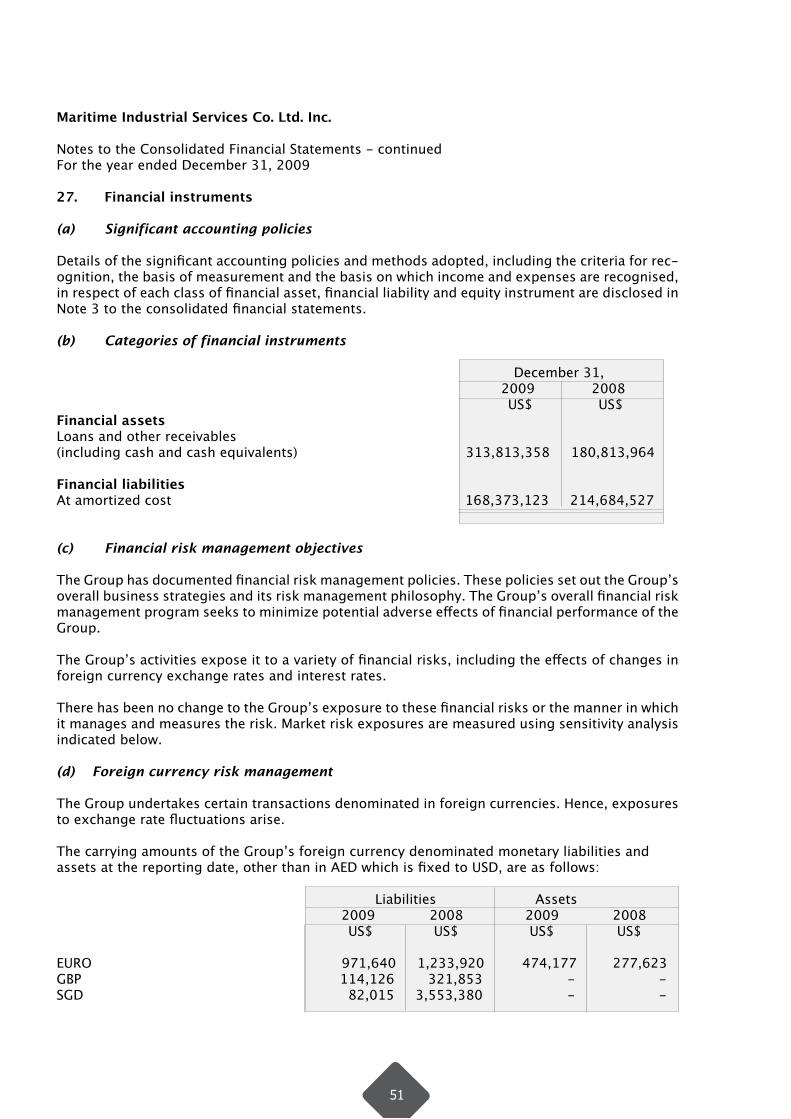

2009 Annual Report

Annual Report 2009

Mar 08, 2016

MIS Annual Report 2009

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2009Annual Report

www.miscoltd.com

Ma

ri

ti

me

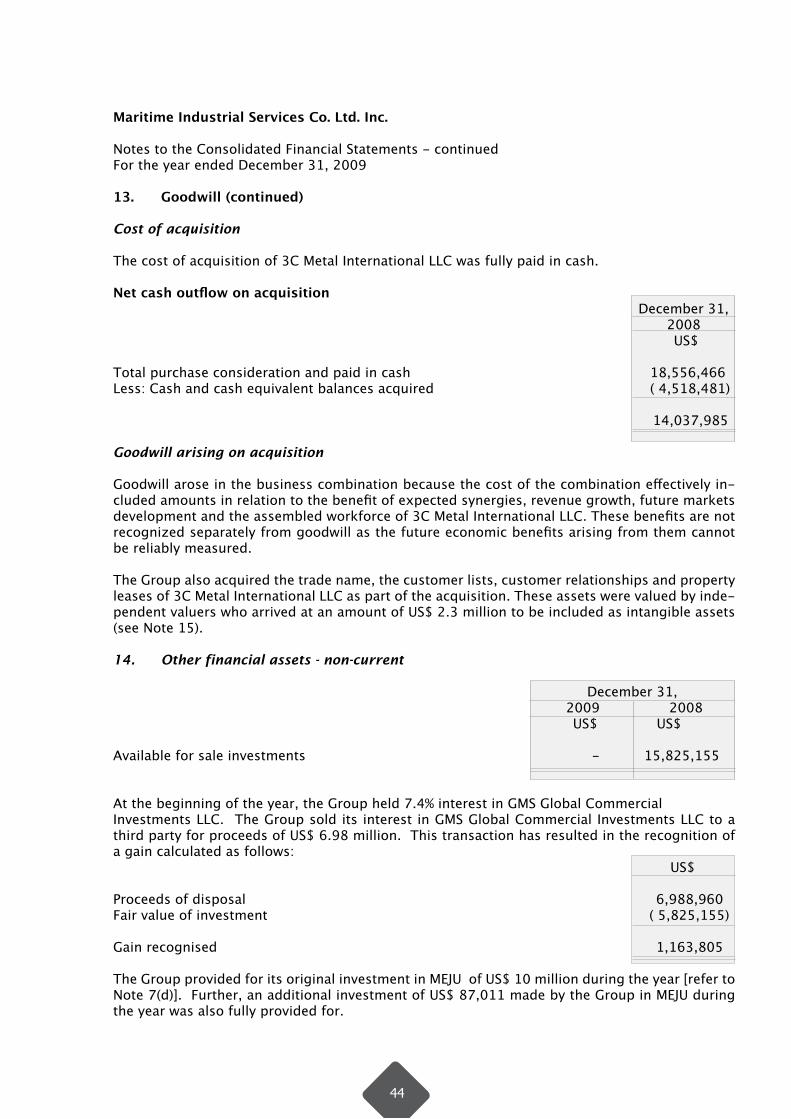

In

du

st

ri

al

Se

rv

ic

es

Co

.Lt

d.I

nc

|An

nu

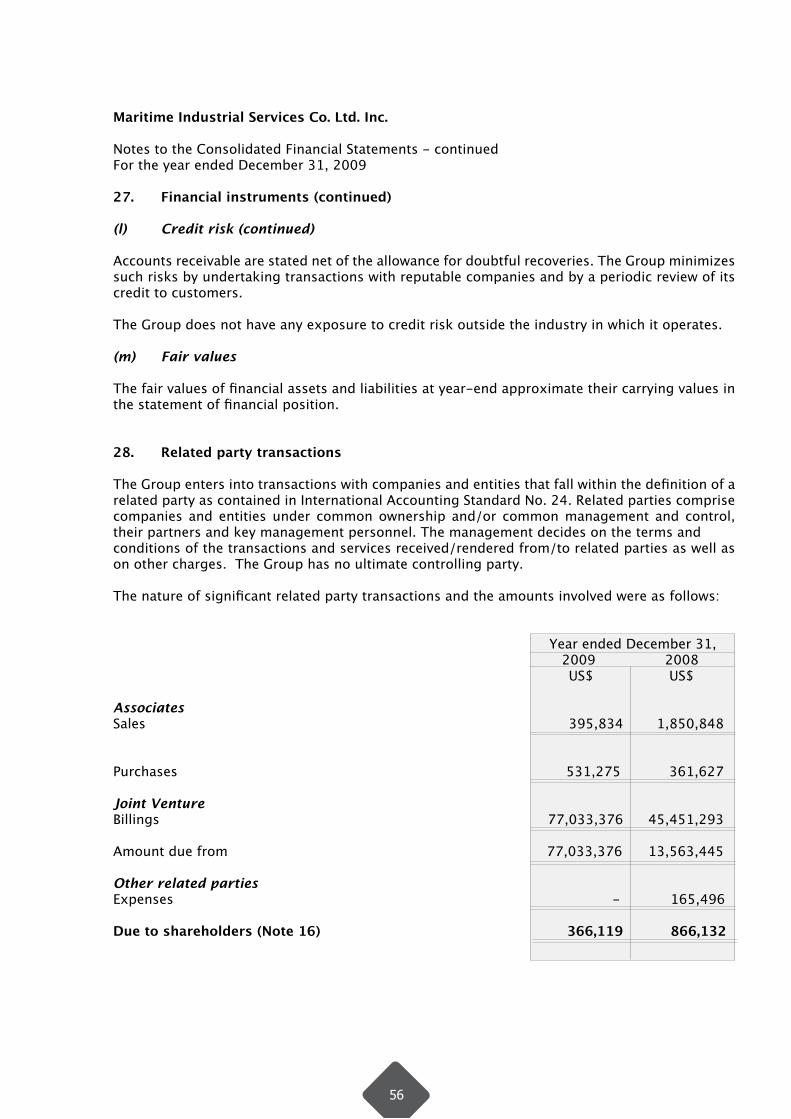

al

Re

po

rt

20

09

Page

Message from the Managing Director

Board of Directors’ Report

Board of Directors

Auditor’s Report

Corporate Governance Disclosures

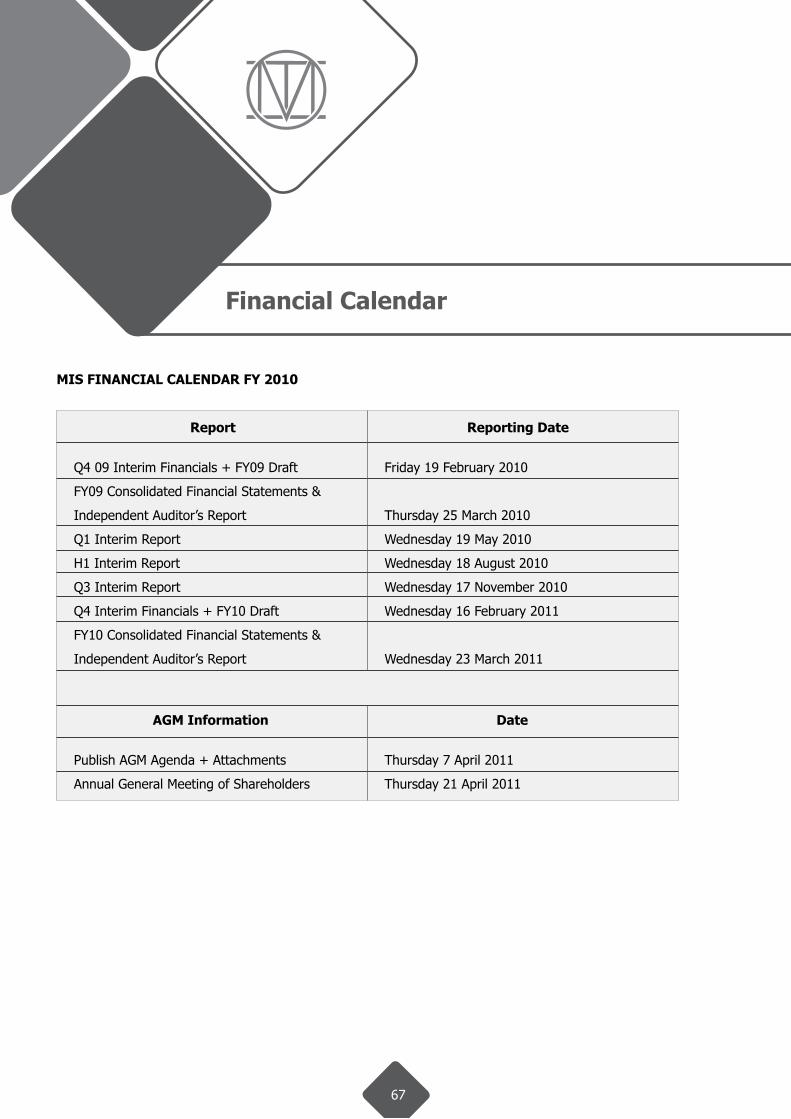

Financial Calendar

Company Addresses

4

7

13

14

60

67

68

Table of Contents

3

Dear Fellow Shareholders, Valued Clients, Employees,

2009 marked MIS’ 30th year of operations in the Middle East. As we celebrated this significant achievement, our eyes remained focused on the long term strategic goals of taking MIS to a $1 billion company with a net income of $100 million by 2013.

Financial Growth

We are therefore pleased to report that in 2009, MIS made major strides towards achieving our goals. MIS delivered record figures both in terms of revenues for the year of $478 million and net income of $29 million. The latter was a reflection of productivity and profitability gains not just in our New Build value stream but also across our traditional business. We are pleased that MIS was able to deliver such results despite 2009 being a challenging year not just for the industry at large but also for MIS which faced the suspension of work on two of its rigs, Hulls 106 and 108, in September after it terminated its contracts with Mosvold Middle East Jackup (MEJU). This resulted in our fourth quarter revenue being 27% lower than that of the same period last year and also dented our net income, but not enough to prevent us from recording a record level of profit and improving the group’s net worth by 24% on 2008.We’re particularly pleased with the fact that in these circumstances we were able to significantly improve MIS’ cash flow in 2009 and reduce its debt by some $43.6 million.

Organisational Development

In addition to the sound financial performance of MIS, 2009 saw other successes across the organisation. We delivered two offshore jack-up drilling rigs, the first ever to be built in the Middle East, a testament to MIS’ determination to establish itself as a viable global player amongst new build yards. We lived up to our promise of focusing on and developing our traditional business areas where we built a year-endbacklog of $60 million and also managed to establish new customer relationships within those value streams. We completed the first year of our Balanced Scorecard programme, introduced in late 2008 as part of our new management system to provide focus and clarity, and to align and engage our employees. We completed a ‘Change for Growth’ initiative designed to address specific behaviours that would help guide the organisation further towards its strategic growth targets. To further strengthen MIS’ ability to offer comprehensive solutions to our clients in the energy sector, MIS launched a new business unit, Energy Projects International (EPI), to build on its expertise in the EPC and EPCM markets with a particular focus on the growth markets of Abu Dhabi and Saudi Arabia. We expect this value stream to be a major contributor to our long-term strategic goals.

Message from the Managing Director

“On the path to growth”

4

Lastly, building on MIS’ tradition of investing in the continuous development of its people, MIS forged a strategic alliance with one of the UAE’s leading universities, the American University of Sharjah, to establish a customised executive development programme for selected leadership candidates.

These accomplishments, coupled with the introduction of other significant change initiatives to a company that is as successful and as well established as MIS, are things that I am particularly proud to have been part of. They would not have been possible without the trust and commitment of our shareholders and our valued clients, the dedication of our experienced employees and the guidance of MIS’ Board.

Outlook

MIS is aware of the challenges that are intrinsic to this industry, but has a cautiously optimistic view of 2010 and beyond, our strategy is still focused on developing backlog outside New Build, while broaden-ing our scope within New Build to target projects within the renewable energy sector and the like. The market is offering opportunities in all the business areas in which MIS operates and we are confident that our rich experience will help us to penetrate the Abu Dhabi and Saudi Arabia markets more effectively. While the concentration in these markets is on building an EPC and EPCM capability through our newest business unit, EPI, we believe that there are opportunities there for all of our businesses.

MIS emerged from a difficult year profitable and with a strong balance sheet, achieving record figures in terms of revenue and net income. With this, and with our market position supported by six value streams, today MIS’ unique positioning of offering comprehensive solutions to its clients in the energy industry remains as strong as ever.

Kevin J. HudsonManaging Director

5

6

7

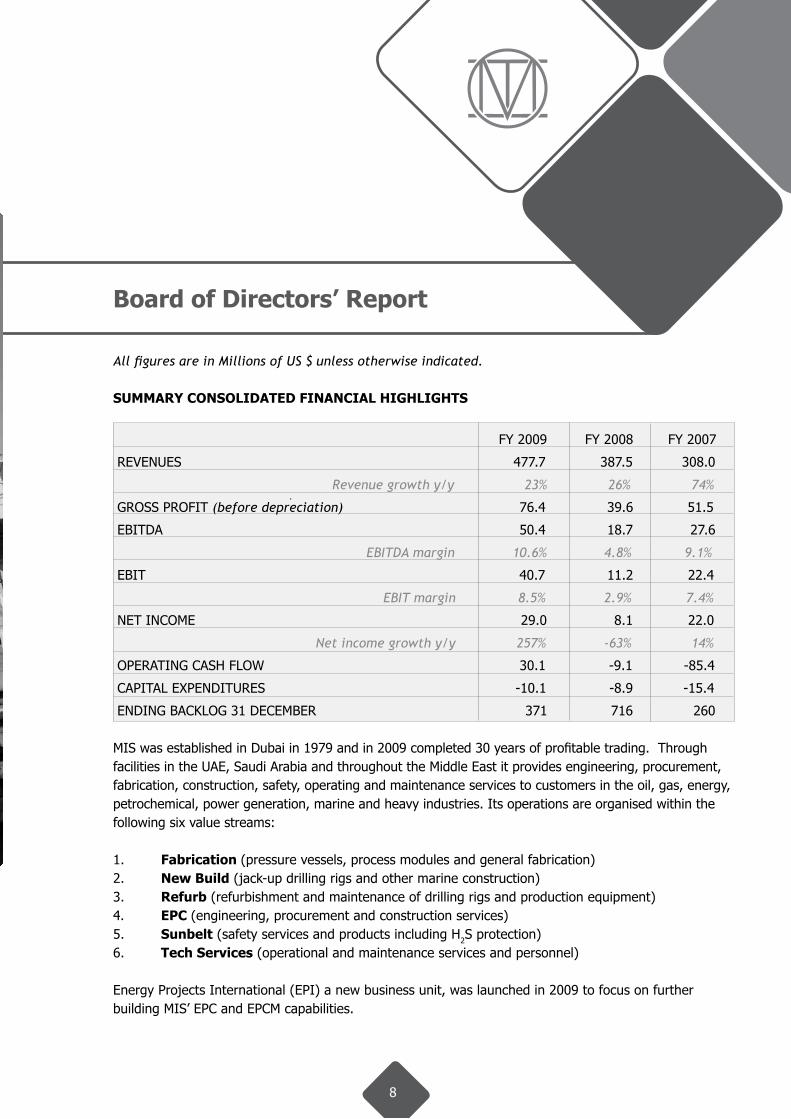

All figures are in Millions of US $ unless otherwise indicated.

SUMMARY CONSOLIDATED FINANCIAL HIGHLIGHTS

FY 2009 FY 2008 FY 2007

REVENUES 477.7 387.5 308.0

Revenue growth y/y 23% 26% 74%

GROSS PROFIT (before depreciation) 76.4 39.6 51.5

EBITDA 50.4 18.7 27.6

EBITDA margin 10.6% 4.8% 9.1%

EBIT 40.7 11.2 22.4

EBIT margin 8.5% 2.9% 7.4%

NET INCOME 29.0 8.1 22.0

Net income growth y/y 257% -63% 14%

OPERATING CASH FLOW 30.1 -9.1 -85.4

CAPITAL EXPENDITURES -10.1 -8.9 -15.4

ENDING BACKLOG 31 DECEMBER 371 716 260

MIS was established in Dubai in 1979 and in 2009 completed 30 years of profitable trading. Through facilities in the UAE, Saudi Arabia and throughout the Middle East it provides engineering, procurement, fabrication, construction, safety, operating and maintenance services to customers in the oil, gas, energy,petrochemical, power generation, marine and heavy industries. Its operations are organised within the following six value streams:

1. Fabrication (pressure vessels, process modules and general fabrication)2. New Build (jack-up drilling rigs and other marine construction) 3. Refurb (refurbishment and maintenance of drilling rigs and production equipment)4. EPC (engineering, procurement and construction services)5. Sunbelt (safety services and products including H2S protection)6. Tech Services (operational and maintenance services and personnel)

Energy Projects International (EPI) a new business unit, was launched in 2009 to focus on further building MIS’ EPC and EPCM capabilities.

8

Board of Directors’ Report

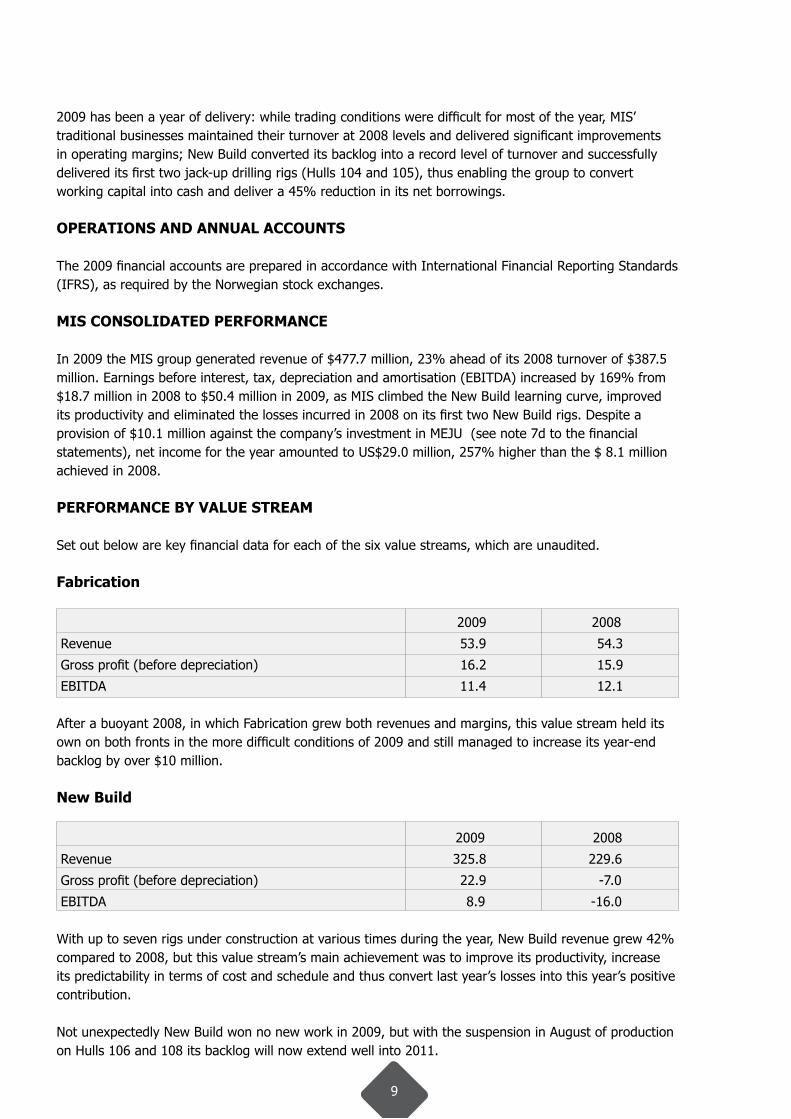

2009 has been a year of delivery: while trading conditions were difficult for most of the year, MIS’ traditional businesses maintained their turnover at 2008 levels and delivered significant improvements in operating margins; New Build converted its backlog into a record level of turnover and successfully delivered its first two jack-up drilling rigs (Hulls 104 and 105), thus enabling the group to convertworking capital into cash and deliver a 45% reduction in its net borrowings.

OPERATIONS AND ANNUAL ACCOUNTS

The 2009 financial accounts are prepared in accordance with International Financial Reporting Standards (IFRS), as required by the Norwegian stock exchanges.

MIS CONSOLIDATED PERFORMANCE

In 2009 the MIS group generated revenue of $477.7 million, 23% ahead of its 2008 turnover of $387.5 million. Earnings before interest, tax, depreciation and amortisation (EBITDA) increased by 169% from $18.7 million in 2008 to $50.4 million in 2009, as MIS climbed the New Build learning curve, improved its productivity and eliminated the losses incurred in 2008 on its first two New Build rigs. Despite a provision of $10.1 million against the company’s investment in MEJU (see note 7d to the financial statements), net income for the year amounted to US$29.0 million, 257% higher than the $ 8.1 million achieved in 2008.

PERFORMANCE BY VALUE STREAM

Set out below are key financial data for each of the six value streams, which are unaudited.

Fabrication

2009 2008

Revenue 53.9 54.3

Gross profit (before depreciation) 16.2 15.9

EBITDA 11.4 12.1

After a buoyant 2008, in which Fabrication grew both revenues and margins, this value stream held its own on both fronts in the more difficult conditions of 2009 and still managed to increase its year-end backlog by over $10 million.

New Build

2009 2008

Revenue 325.8 229.6

Gross profit (before depreciation) 22.9 -7.0

EBITDA 8.9 -16.0

With up to seven rigs under construction at various times during the year, New Build revenue grew 42% compared to 2008, but this value stream’s main achievement was to improve its productivity, increase its predictability in terms of cost and schedule and thus convert last year’s losses into this year’s positive contribution.

Not unexpectedly New Build won no new work in 2009, but with the suspension in August of production on Hulls 106 and 108 its backlog will now extend well into 2011.

9

Refurb

2009 2008

Revenue 29.4 25.1

Gross profit (before depreciation) 8.1 5.8

EBITDA 6.6 4.9

Refurb made further progress in both turnover and margins during 2009. Gross margin improved from 23% to 28% and EBITDA was up 35%. Backlog was virtually exhausted by the end of the year, but major prospects were being pursued prior to the year end, resulting in a $55 million award from Abu Dhabi’s National Drilling Company in early 2010.

EPC

2009 2008

Revenue 32.0 44.6

Gross profit (before depreciation) 12.4 10.6

EBITDA 10.0 6.9

EPC found volume harder to come by in 2009, particularly in the first half, and so turnover fell by 28%. EBITDA, however, increased by 45%, as 2009’s results benefited from the absence of the Qatar-based HFO contract, which contributed a loss of $8.5 million in 2008. Backlog more than doubled during the year, with work-winning improving steadily as the year progressed.

Sunbelt

2009 2008

Revenue 22.7 23.0

Gross profit (before depreciation) 10.8 10.1

EBITDA 8.4 7.6

While growth slowed in 2009, Sunbelt improved its margins on a maintained turnover, increasing its EBITDA by 10%. The strategy of geographical and product diversification continues unchanged.

Tech Services

2009 2008

Revenue 13.9 10.9

Gross profit (before depreciation) 6.0 4.2

EBITDA 5.1 3.2

The strengths of Tech Services’ business are reliability, quality of service and long-standing relationships with key clients in the local oil and gas sector. All those relationships were successfully maintained in 2009 and the largest single contract was extended for a further three years. While positively engaging with its client’s increasing focus on cost and value for money, Tech Services once again improved its margins, increasing EBITDA by 58% on turnover up 28%.

10

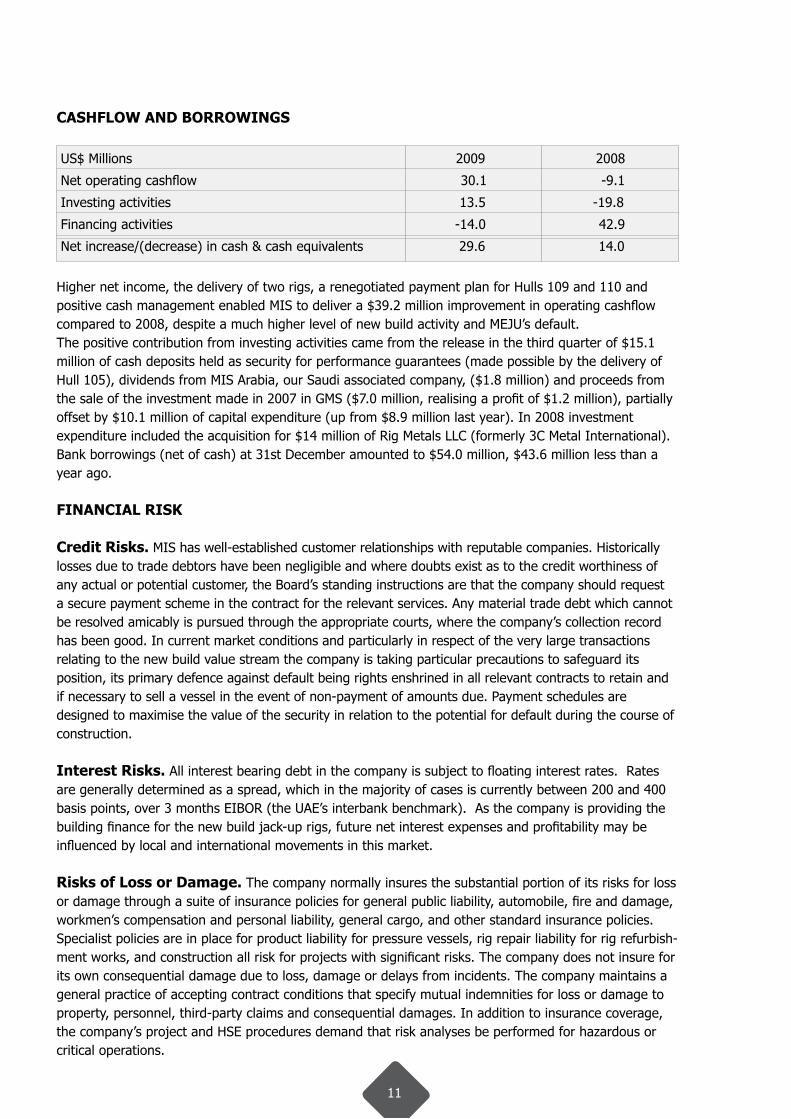

CASHFLOW AND BORROWINGS

US$ Millions 2009 2008

Net operating cashflow 30.1 -9.1

Investing activities 13.5 -19.8

Financing activities -14.0 42.9

Net increase/(decrease) in cash & cash equivalents 29.6 14.0

Higher net income, the delivery of two rigs, a renegotiated payment plan for Hulls 109 and 110 and positive cash management enabled MIS to deliver a $39.2 million improvement in operating cashflow compared to 2008, despite a much higher level of new build activity and MEJU’s default. The positive contribution from investing activities came from the release in the third quarter of $15.1 million of cash deposits held as security for performance guarantees (made possible by the delivery of Hull 105), dividends from MIS Arabia, our Saudi associated company, ($1.8 million) and proceeds from the sale of the investment made in 2007 in GMS ($7.0 million, realising a profit of $1.2 million), partially offset by $10.1 million of capital expenditure (up from $8.9 million last year). In 2008 investment expenditure included the acquisition for $14 million of Rig Metals LLC (formerly 3C Metal International). Bank borrowings (net of cash) at 31st December amounted to $54.0 million, $43.6 million less than a year ago.

FINANCIAL RISK

Credit Risks. MIS has well-established customer relationships with reputable companies. Historically losses due to trade debtors have been negligible and where doubts exist as to the credit worthiness of any actual or potential customer, the Board’s standing instructions are that the company should request a secure payment scheme in the contract for the relevant services. Any material trade debt which cannot be resolved amicably is pursued through the appropriate courts, where the company’s collection record has been good. In current market conditions and particularly in respect of the very large transactions relating to the new build value stream the company is taking particular precautions to safeguard its position, its primary defence against default being rights enshrined in all relevant contracts to retain and if necessary to sell a vessel in the event of non-payment of amounts due. Payment schedules are designed to maximise the value of the security in relation to the potential for default during the course of construction.

Interest Risks. All interest bearing debt in the company is subject to floating interest rates. Rates are generally determined as a spread, which in the majority of cases is currently between 200 and 400 basis points, over 3 months EIBOR (the UAE’s interbank benchmark). As the company is providing the building finance for the new build jack-up rigs, future net interest expenses and profitability may be influenced by local and international movements in this market.

Risks of Loss or Damage. The company normally insures the substantial portion of its risks for loss or damage through a suite of insurance policies for general public liability, automobile, fire and damage, workmen’s compensation and personal liability, general cargo, and other standard insurance policies. Specialist policies are in place for product liability for pressure vessels, rig repair liability for rig refurbish-ment works, and construction all risk for projects with significant risks. The company does not insure for its own consequential damage due to loss, damage or delays from incidents. The company maintains a general practice of accepting contract conditions that specify mutual indemnities for loss or damage to property, personnel, third-party claims and consequential damages. In addition to insurance coverage, the company’s project and HSE procedures demand that risk analyses be performed for hazardous or critical operations.

11

Currency Risks. The company is exposed to currency exchange risks only on sales and expenditures in currencies other than the UAE Dirham and US Dollar, as the Dirham has a longstanding fixed rate relationship of AED3.67:US$1. This risk is considered to be minor since the majority of contracts and expenditures are in Dirhams or Dollars. If the Dirham / US Dollar peg were to be abandoned that would create a risk to the company, but MIS does not consider that risk to be significant in the near term. The company’s policy is to minimise any exchange risks and all essential foreign currency exposures are therefore secured immediately through forward contracts or through the use of foreign currency accounts established with local banks.

FUTURE PROSPECTS

MIS has a cautiously optimistic view of 2010. Work winning outside New Build has shown a rising trend and opportunities in all value streams appear to have become more plentiful, in response to a greater level of confidence in the energy markets. In February we delivered our third rig, the KS Endeavor (Hull 107) and our existing New Build backlog will keep us productively employed throughout 2010, allowing some breathing space for the maturing of new vessel prospects in both the oil and gas and renewable energy sectors. We are continuing to work on the development of opportunities to penetrate the Abu Dhabi and Saudi Arabia markets more effectively. While our concentration is on building an EPC and EPCM capability, we believe that there are opportunities there for all of our value streams. Having emerged from a difficult year profitably and with a stronger balance sheet, MIS remains, more than ever, uniquelypositioned in its ability to offer comprehensive solutions to its clients in the energy sector.

SHAREHOLDER RELATIONS

At December 31, 2009, the company had just under 500 shareholders and its issued share capital was made up of 46,273,750 shares at a par value of US$ 2.00 per share.

YEAR-END PROFIT AND DISPOSAL

The year-end profit for MIS in 2009 was US$ 28,994,567. The Board of Directors recommended and the shareholders approved at the Annual General Meeting that no cash dividend should be paid in respect of 2009 and that consequently US$ 28,994,567 should be transferred to retained earnings.

12

The MIS Board of Directors and term expiry dates after the Annual General Meeting held in Dubai, United Arab Emirates, on April 22, 2010 are as follows:

The MIS Board of Directors is confident that MIS will continue to grow and prosper in its current market. Through its joint efforts, the Board will endeavour to guide MIS along the path of good corporate governance and successful operations.

Charles L. DavisDirector

expires AGM 2012

Jerry M. SmithDirector &

Special advisor to the Boardexpires AGM 2012

Kevin J. HudsonManaging Directorexpires AGM 2011

Abdul Salam El ZeidyDirector

expires AGM 2012

John O’LearyDirector

expires AGM 2012

Richard DallasDirector

expires AGM 2011

Dr. Karim El SolhChairman of the Board

expires AGM 2011

Ammar Al KhudairyDirector

expires AGM 2011

Timothy NoonanAlternate Directorexpires AGM 2011

Fadi ArbidAlternate Directorexpires AGM 2011

Dr. Karim El SolhChairman of the Board

Kevin J. HudsonManaging Director

13

Board of Directors

MARITIME INDUSTRIAL SERVICES CO. LTD. INC.

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORTFOR THE YEAR ENDED DECEMBER 31, 2008

Table of Contents Page

Independent Auditor’s Report

Consolidated Balance Sheet

Consolidated Income Statement

Consolidated Statement of Changes in Equity

Consolidated Cash Flow Statement

Notes to the Consolidated Financial Statements

15

16

17

18

19

20-58

Board of Directors

14

Auditor’s Report

Independent Auditor’s Report

The ShareholdersMaritime Industrial Services Co. Ltd. Inc.Jebel Ali Free ZoneDubai, United Arab Emirates

Report on the Financial Statements

We have audited the accompanying consolidated financial statements of Maritime Industrial Services Co. Ltd. Inc. (the “Company”) and Subsidiaries, (the “Group”), which comprise the consolidated statement of financial position as of December 31, 2009, and the consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Group as of December 31, 2009, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

Emphasis of Matters

Without qualifying our opinion, we draw attention to the following matters addressed in Notes 7 and 8 to the consolidated financial statements:

Note 7(d) describes a claim made against the Group by a customer for an alleged breach of technical specifications on two New Build rigs under construction. The same customer has defaulted on payment of instalments due during 2009 against already achieved and independently certified milestones. The Group has referred the claim to arbitration in which the arbitrators, on November 17, 2009, have issued a partial final award permitting the sale of the two rigs in question to third parties with the sale proceeds held for common account and placed in escrow pending further order of the arbitrators. Based on indicative offers received to date, management is confident that the sale proceeds will ultimately enable full recovery of amounts currently due under the terms of the contract.

Note 8(b) describes a contractual dispute with a client in Qatar currently subject to litigation proceedings, the ultimate outcome of which is uncertain.

No provisions have been taken in relation to the above uncertainties.

DubaiMarch 10, 2010

15

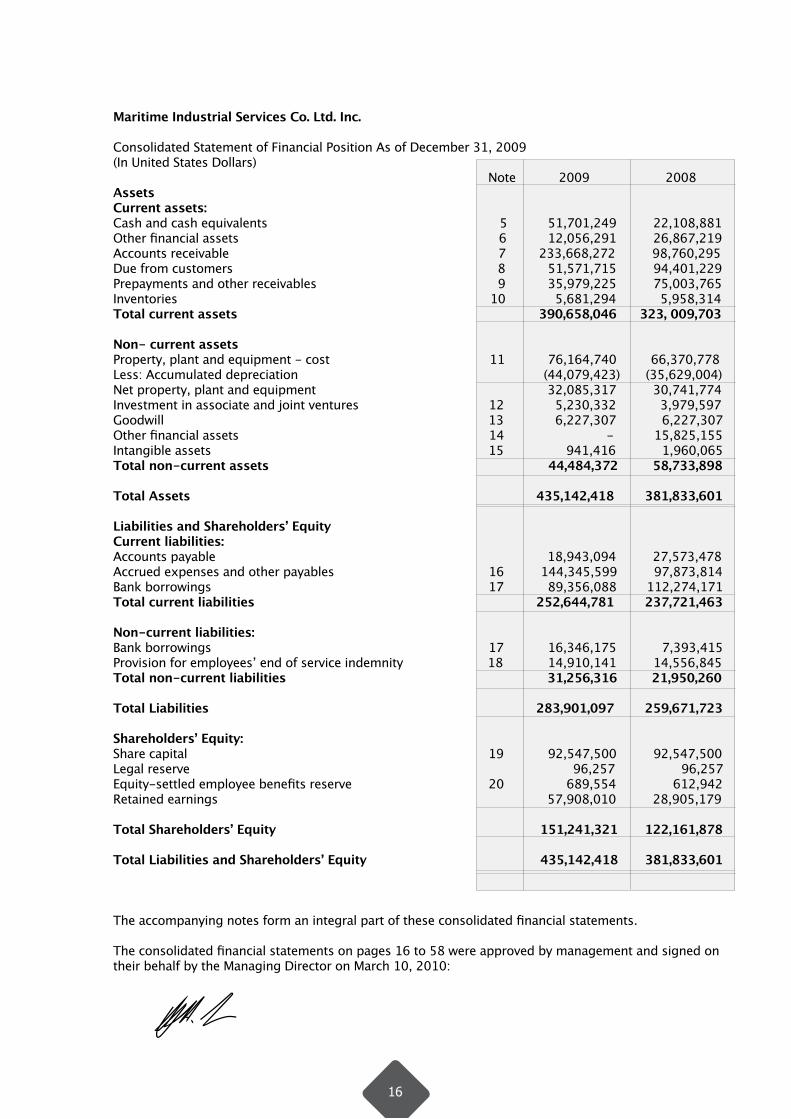

Maritime Industrial Services Co. Ltd. Inc.

Consolidated Statement of Financial Position As of December 31, 2009 (In United States Dollars) Note 2009 2008 Assets Current assets:Cash and cash equivalents 5 51,701,249 22,108,881Other financial assets 6 12,056,291 26,867,219 Accounts receivable 7 233,668,272 98,760,295 Due from customers 8 51,571,715 94,401,229 Prepayments and other receivables 9 35,979,225 75,003,765 Inventories 10 5,681,294 5,958,314Total current assets 390,658,046 323, 009,703

Non- current assets Property, plant and equipment - cost 11 76,164,740 66,370,778Less: Accumulated depreciation (44,079,423) (35,629,004)Net property, plant and equipment 32,085,317 30,741,774Investment in associate and joint ventures 12 5,230,332 3,979,597 Goodwill 13 6,227,307 6,227,307Other financial assets 14 - 15,825,155 Intangible assets 15 941,416 1,960,065 Total non-current assets 44,484,372 58,733,898 Total Assets 435,142,418 381,833,601

Liabilities and Shareholders’ Equity Current liabilities: Accounts payable 18,943,094 27,573,478Accrued expenses and other payables 16 144,345,599 97,873,814 Bank borrowings 17 89,356,088 112,274,171 Total current liabilities 252,644,781 237,721,463 Non-current liabilities:Bank borrowings 17 16,346,175 7,393,415 Provision for employees’ end of service indemnity 18 14,910,141 14,556,845 Total non-current liabilities 31,256,316 21,950,260 Total Liabilities 283,901,097 259,671,723 Shareholders’ Equity:Share capital 19 92,547,500 92,547,500 Legal reserve 96,257 96,257 Equity-settled employee benefits reserve 20 689,554 612,942Retained earnings 57,908,010 28,905,179 Total Shareholders’ Equity 151,241,321 122,161,878 Total Liabilities and Shareholders’ Equity 435,142,418 381,833,601

The accompanying notes form an integral part of these consolidated financial statements.

The consolidated financial statements on pages 16 to 58 were approved by management and signed on their behalf by the Managing Director on March 10, 2010:

16

Maritime Industrial Services Co. Ltd. Inc.

Consolidated Statement of Comprehensive Income For the year endedDecember 31, 2009 (In United States Dollars)

Note 2009 2008

Revenue 477,675,861 387,470,884 Cost of sales (409,099,839) (354,269,057) Gross profit 68,576,022 33,201,827General, selling and administrative expenses 21 (27,919,644) (21,955,184) Other income 22 950,864 962,315Finance charges (5,895,556) (5,319,780) Profit from associates and joint ventures - net 12 3,056,412 2,406,608Allowance for investment 7(d) & 14 (10,087,011) -Gain on disposal of other financial assets 14 1,163,805 - Income before income tax 29,844,892 9,295,786 Income tax expense 23 (850,325) (1,183,685) Net income for the year 28,994,567 8,112,101Other comprehensive income - - Comprehensive income for the year 28,994,567 8,112,101

Basic earnings per share 0.63 0.18

Diluted earnings per share 0.61 0.17

Weighted average number of shares used in the calculation of basic earnings per share 46,273,750 46,193,066

Employee stock options 1,393,750 1,417,500 Weighted average number of shares used in the calculation of diluted earnings per share 47,667,500 47,610,566

The accompanying notes form an integral part of these consolidated financial statements.

17

Mar

itim

e In

dust

rial

Ser

vice

s Co

. Ltd

. Inc

.

Cons

olid

ated

Sta

tem

ent o

f Cha

nges

in E

quity

For

the

year

end

ed D

ecem

ber 3

1, 2

009

(In U

nite

d St

ates

Dol

lars

)

E

quity

-set

tled

em

ploy

ee

S

hare

Leg

al

bene

fits

R

etai

ned

cap

ital

res

erve

r

eser

ve

ear

ning

s

T

otal

Bala

nce

at D

ecem

ber

31, 2

007

9

2,00

0,00

0

96,2

57

239

,742

2

4,20

1,29

1 11

6,53

7,29

0D

ivid

ends

pai

d (N

ote

24)

-

-

-

(3,

608,

183)

(3,6

08,1

83)

Net

pro

fit fo

r th

e ye

ar 2

008

-

-

-

8,

112,

101

8

,112

,101

To

tal c

ompr

ehen

sive

inco

me

for

the

year

-

-

-

8,11

2,10

1

8,1

12,1

01

Fore

ign

curr

ency

tran

slat

ion

-

-

-

199,

970

199

,970

Reco

gniti

on o

f em

ploy

ee s

tock

opt

ions

-

-

3

73,2

00

-

3

73,2

00Is

sue

of s

hare

cap

ital (

Not

e 19

)

547

,500

-

-

-

547

,500

Bala

nce

at D

ecem

ber

31, 2

008

9

2,54

7,50

0

96,2

57

612

,942

2

8,90

5,17

9 12

2,16

1,87

8N

et p

rofit

for

the

year

200

9

-

-

-

2

8,99

4,56

7 2

8,99

4,56

7To

tal c

ompr

ehen

sive

inco

me

for

the

year

-

-

-

2

8,99

4,56

7 2

8,99

4,56

7Fo

reig

n cu

rren

cy tr

ansl

atio

n

-

-

-

8,2

64

8

,264

Reco

gniti

on o

f em

ploy

ee s

tock

opt

ions

-

-

76,6

12

-

76,6

12Ba

lanc

e at

Dec

embe

r 31

, 200

9

92,

547,

500

96,

257

689,

554

57,9

08,0

10

151,

241,

321

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

con

solid

ated

fina

ncia

l sta

tem

ents

.

18

Maritime Industrial Services Co. Ltd. Inc.

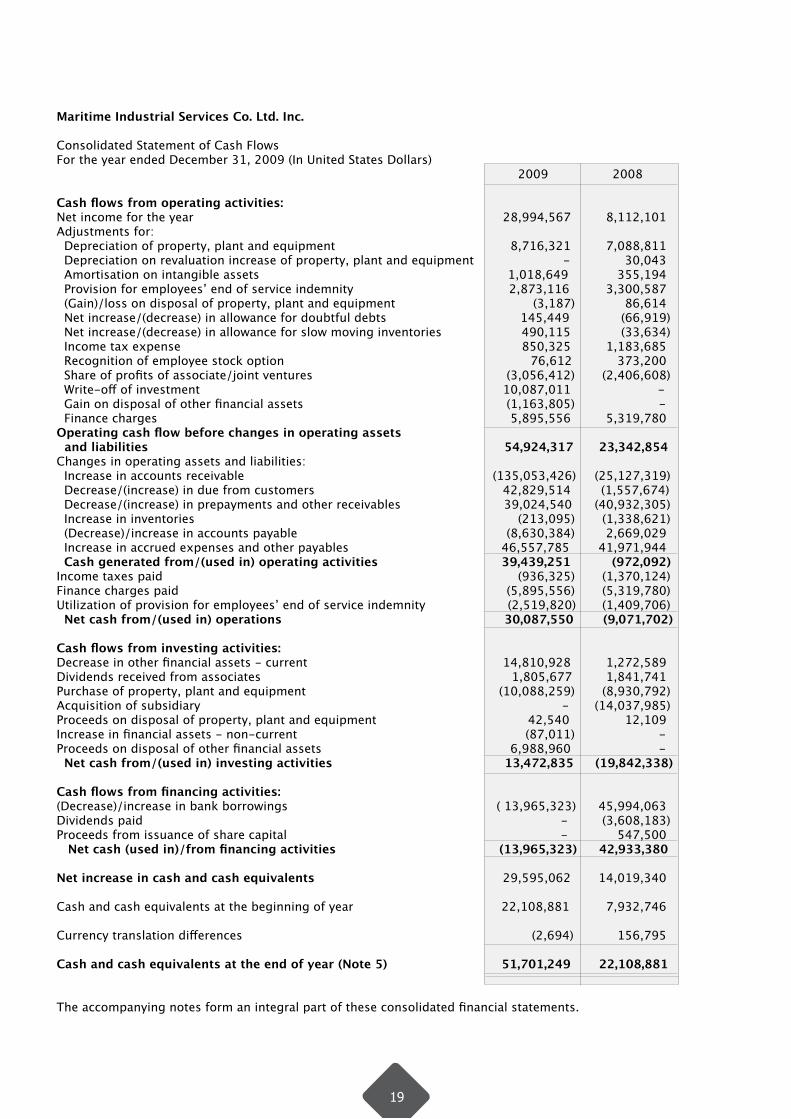

Consolidated Statement of Cash FlowsFor the year ended December 31, 2009 (In United States Dollars) 2009 2008

Cash flows from operating activities: Net income for the year 28,994,567 8,112,101 Adjustments for: Depreciation of property, plant and equipment 8,716,321 7,088,811 Depreciation on revaluation increase of property, plant and equipment - 30,043 Amortisation on intangible assets 1,018,649 355,194 Provision for employees’ end of service indemnity 2,873,116 3,300,587 (Gain)/loss on disposal of property, plant and equipment (3,187) 86,614 Net increase/(decrease) in allowance for doubtful debts 145,449 (66,919) Net increase/(decrease) in allowance for slow moving inventories 490,115 (33,634) Income tax expense 850,325 1,183,685 Recognition of employee stock option 76,612 373,200 Share of profits of associate/joint ventures (3,056,412) (2,406,608) Write-off of investment 10,087,011 - Gain on disposal of other financial assets (1,163,805) - Finance charges 5,895,556 5,319,780Operating cash flow before changes in operating assets and liabilities 54,924,317 23,342,854 Changes in operating assets and liabilities: Increase in accounts receivable (135,053,426) (25,127,319) Decrease/(increase) in due from customers 42,829,514 (1,557,674) Decrease/(increase) in prepayments and other receivables 39,024,540 (40,932,305) Increase in inventories (213,095) (1,338,621) (Decrease)/increase in accounts payable (8,630,384) 2,669,029 Increase in accrued expenses and other payables 46,557,785 41,971,944 Cash generated from/(used in) operating activities 39,439,251 (972,092) Income taxes paid (936,325) (1,370,124) Finance charges paid (5,895,556) (5,319,780)Utilization of provision for employees’ end of service indemnity (2,519,820) (1,409,706) Net cash from/(used in) operations 30,087,550 (9,071,702)

Cash flows from investing activities:Decrease in other financial assets - current 14,810,928 1,272,589 Dividends received from associates 1,805,677 1,841,741 Purchase of property, plant and equipment (10,088,259) (8,930,792) Acquisition of subsidiary - (14,037,985)Proceeds on disposal of property, plant and equipment 42,540 12,109Increase in financial assets - non-current (87,011) -Proceeds on disposal of other financial assets 6,988,960 - Net cash from/(used in) investing activities 13,472,835 (19,842,338)

Cash flows from financing activities: (Decrease)/increase in bank borrowings ( 13,965,323) 45,994,063 Dividends paid - (3,608,183) Proceeds from issuance of share capital - 547,500 Net cash (used in)/from financing activities (13,965,323) 42,933,380

Net increase in cash and cash equivalents 29,595,062 14,019,340

Cash and cash equivalents at the beginning of year 22,108,881 7,932,746

Currency translation differences (2,694) 156,795

Cash and cash equivalents at the end of year (Note 5) 51,701,249 22,108,881

The accompanying notes form an integral part of these consolidated financial statements.

19

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial StatementsFor the year ended December 31, 2009

1. Legal status and business activities

Maritime Industrial Services Co. Ltd. Inc. (the “Company”) is incorporated in Panama and has its Corporate Office at Jebel Ali Free Zone, Dubai, United Arab Emirates and branches in each of Dubai and Sharjah, U.A.E., Kazakhstan, Kuwait and Qatar. These financial statements are those of the Company, consolidated with the following subsidiaries (collectively the “Group”):

Proportion of legal Place of ownership Name of entity operation interest Principal activity % 1. Maritime Industrial Services Sultanate 49* Engineering and project Co. Ltd. of Oman management, safety and training products and services, fabrication onshore and offshore construction and other operating and maintenance services.

2. MIS International Ltd. Inc. Middle East 100 Fabrication, rig overhaul and repair business.

3. Maurlis International Ltd. Inc. Republic of 100 Investing in a joint venture Panama set up to build and operate a rig.

4. Marine Investment Co. Ltd. Inc. Republic of 100 Investing in a Group Panama engaged in fabrication, engineering and repair business.

5. Global Acquisition and Republic of 100 Investing in a Group Management Co. Ltd. Inc. Panama engaged in the operation of oil rigs.

6. Rig Metals LLC (Formerly United Arab 49* Manufacturing, repair of 3C Metal International LLC) Emirates rigs and oil and natural gas well drilling.

* By virtue of agreements between the shareholders, the Group has a 100% beneficial ownership in these companies.

Furthermore, the consolidated financial statements include an associate and joint ventures as set out in Note 12 to the financial statements.

20

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

1. Legal status and business activities (continued)

The accounting records of the Company are kept in United Arab Emirates Dirhams, which is the functional currency of the Company. As is disclosed in the accounting policy on Foreign Currency Transactions in Note 3, the presentation currency for these consolidated financial statements is United States Dollars. The United States Dollar figures for the Company were arrived at by converting all the Dirham figures into Dollars at a fixed rate of US$1 = AED 3.67, which is the official fixed rate of exchange.

The principal activity of the Group is to engage in maritime industrial services including industrial production, engineering, fabrication, and construction activities in the Gulf Coopera-tion Council (GCC) countries and Kazakhstan.

2. Adoption of new and revised International Financial Reporting Standards (IFRSs)

2.1 Standards affecting presentation and disclosures

The following new and revised Standards have been adopted in the current year in these finan-cial statements. Details of other Standards and Interpretations adopted but that had no effect on the financial statements are set out in section 2.2.

2.2 Standards and Interpretations adopted with no effect on financial statements

The following new and revised Standards and Interpretations have also been adopted in these financial statements. Their adoption has not had any significant impact on the amounts re-ported in these financial statements but may affect the accounting for future transactions or arrangements:

IFRS 8 Operating Segments

IFRS 8 is a disclosure Standard that requires re-designation of the Group’s reportable segments based on the segments used by the Chief Operating Decision Maker to allocate resources and assess performance.

IAS 1 (2007) has introduced terminology changes (including revised titles for the financial statements) and changes in the format and content of the financial statements.

The amendments to IFRS 7 expand the disclosures required in respect of fair value measurements and liquidity risk.

IAS 1 (as revised in 2007) Presentation of Financial Statements

Improving disclosures about Financial Instruments (Amendments to IFRS 7 Fi-nancial Instruments: Disclosures)

21

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

2. Adoption of new and revised International Financial Reporting Standards (IFRSs) (continued)

2.2 Standards and Interpretations adopted with no effect on financial statements (continued)

IFRS for SMEs Small and Medium-sized Entities

Amendments to IFRS 2 Share-based Payment - Vesting Conditions and Cancellations

IAS 23 (as revised in 2007) Borrowing Costs

Amendments to IAS 32 Financial Instruments: Presentation and IAS 1 Presentation of Financial Statements – Puttable Financial Instruments and Obligations Arising on Liquidation

IFRIC 13 Customer Loyalty Programmes

IFRIC 15 Agreements for the Construction of Real Estate

IFRIC 16 Hedges of a Net Investment in a Foreign Operation

This Standard is available immediately but the adoption has to be decided by the jurisdiction of implementation.

The amendments clarify the definition of vesting conditions for the purposes of IFRS 2, introduce the concept of ‘non-vesting’ conditions, and clarify the accounting treatment for cancellations.

The principal change to the Standard was to eliminate the option to expense all borrowing costs when incurred. This change has had no impact on these financial statements because it has always been the Group’s accounting policy to capitalise borrowing costs incurred on qualifying assets.

The revisions to IAS 32 amend the criteria for debt/equity clas-sification by permitting certain puttable financial instruments and instruments (or components of instruments) that impose on an entity an obligation to deliver to another party a pro-rata share of the net assets of the entity only on liquidation, to be classified as equity, subject to specified criteria being met.

The Interpretation provides guidance on how entities should account for customer loyalty programmes by allocating revenue on sale to possible future award attached to the sale.

The Interpretation addresses how entities should determine whether an agreement for the construction of real estate is within the scope of IAS 11 Construction Contracts or IAS 18 Revenue and when revenue from the construction of real estate should be recognised.

The Interpretation provides guidance on the detailed require-ments for net investment hedging for certain hedge accounting designations.

22

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

2. Adoption of new and revised International Financial Reporting Standards (IFRSs) (continued)

2.2 Standards and Interpretations adopted with no effect on financial statements (continued)

Improvements to IFRSs (2008) Amendments to IFRS 5, IAS 1, IAS 16, IAS 19, IAS 20, IAS 23, IAS 27, IAS 28, IAS 29, IAS 31, IAS 36, IAS 38, IAS 39, IAS 40 and IAS 41 resulting from the May and October 2008 Annual Improvements to IFRSs majority of which are effective for annual periods beginning on or after January 1, 2009.

2.3 Standards and Interpretations in issue but not yet effective

At the date of authorization of these financial statements, the following new and revised Stan-dards and Interpretations were in issue but not yet effective:

New Standards and amendments to Standards

• IFRS 1 (revised) First time Adoption of IFRS and IAS 27 (revised) Consolidated and Separate Financial Statements July 1, 2009 – Amendment relating to Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate

• IFRIC 18 Transfers of Assets from Customers July 1, 2009

• IFRS 3 (revised) Business Combinations – Comprehensive revision on applying the acquisition method and consequential amendments to IAS 27 (revised) Consolidated July 1, 2009 and Separate Financial Statements, IAS 28 (revised) Investments in Associates and IAS 31 (revised) Interests in Joint Ventures

• IAS 39 (revised) Financial Instruments: Recognition and Measurement - Amendments relating to Eligible Hedged Items(such as hedging Inflation risk and Hedging with options) July 1, 2009

• IFRS 1 (revised) First time Adoption of IFRS - Amendment on additional exemptions for First-time Adopters January 1, 2010

Effective forannual periods

beginning on or after

23

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

2. Adoption of new and revised International Financial Reporting Standards (IFRSs) (continued)

2.3 Standards and Interpretations in issue but not yet effective (continued)

New Standards and amendments to Standards (continued)

Effective for annual periods beginning on or after

• IFRS 2 (revised) Share-based payment - Amendment relating to Establishment cash-settled Share-based January 1, 2010 payments • IAS 32 (revised) Financial Instruments: Presentation - Amendments relating to classification of Rights Issue February 1, 2010

• IAS 24 Related Party Disclosures - Amendment on disclosure requirements for entities that are controlled, January 1, 2011 jointly controlled or significantly influenced by a Government

• IFRS 9 Financial Instruments: Classification and Measurement (intended as complete replacement for January 1, 2013 IAS 39 and IFRS 7)

• Amendments to IFRS 2, IFRS 5, IFRS 8, IAS 1, IAS 7, IAS 17, IAS 18, IAS 36, IAS 38 and IAS 39 resulting from April 2009 Annual Improvements to IFRSs

New Interpretations and amendments to Interpretations

• IFRS 17: Distributions of Non-cash Assets to Owners July 1, 2009

• IFRIC 19: Extinguishing Financial Liabilities with Equity Instruments July 1, 2010

• Amendment to IFRIC 14: IAS 19: The limit on a defined Benefit Asset, Minimum Funding January 1, 2011 Requirement and their interaction

Majority effective for annual periods

beginning on or after January 1, 2010

Effective forannual periods

beginning on or after

24

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

2. Adoption of new and revised International Financial Reporting Standards (IFRSs)(continued)

2.3 Standards and Interpretations in issue but not yet effective (continued)

New Interpretations and amendments to Interpretations (continued)

Effective for annual periods beginning on or after

• Amendment to IFRIC 16: Hedges of a Net Investment in a Foreign Operation July 1, 2009

• Amendment to IFRIC 9 (revised): Reassessment of Embedded Derivatives relating to assessment of embedded derivatives in case of reclassification of a financial asset out of the ‘FVTPL’ category July 1, 2009

The management anticipates that the adoption of these Standards and Interpretations will have no material impact on the financial statements of the Group in the period of initial application.

3. Significant accounting policies

Statement of compliance

The consolidated financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). A summary of the significant accounting policies is set out below:

Basis of preparation

The consolidated financial statements have been prepared on the historical cost basis except for the revaluation of certain non-current assets and financial instruments.

25

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Basis of consolidation

The consolidated financial statements incorporate the financial statements of the Company and entities controlled by the Company (its subsidiaries). Control is achieved where the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

The results of subsidiaries acquired or disposed of during the year are included in the consoli-dated statement of comprehensive income from the effective date of acquisition or up to the effective date of disposal, as appropriate.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with those used by other members of the Group.

All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

Business combinations

Acquisitions of subsidiaries and businesses are accounted for using the purchase method. The cost of the business combination is measured as the aggregate of the fair values (at the date of exchange) of assets given, liabilities incurred or assumed, and equity instruments issued by the Group in exchange for control of the acquiree, plus any costs directly attributable to the business combination. The acquiree’s identifiable assets, liabilities and contingent liabilities that meet the conditions for recognition under IFRS 3 Business Combinations are recognised at their fair values at the acquisition date, except for non-current assets (or disposal groups) that are classified as held for sale in accordance with IFRS 5 Non-current Assets Held for Sale and DiscontinuedOperations, which are recognised and measured at fair value less costs to sell.

Goodwill arising on acquisition is recognised as an asset and initially measured at cost, being the excess of the cost of the business combination over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities recognised. If, after reassessment, the Group’s interest in the net fair value of the acquiree’s identifiable assets, liabilities and contingent liabilities exceeds the cost of the business combination, the excess is recognised immediately as profit in the consolidated statement of comprehensive income.

26

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Investments in associates

An associate is an enterprise over which the Group is in a position to exercise significant influence, through participation in the financial and operating policy decisions of the investee.

The investments are initially recorded at cost and adjusted thereafter for the post acquisition change in the Group’s share of the net assets. The carrying amount of such investments isreduced to recognise any impairment in the value of individual investments.

To the extent practical, where a group enterprise transacts with an associate of the Group, unrealised profits and losses are eliminated to the extent of the Group’s interest in the relevant associate, except where unrealised losses provide evidence of an impairment of the asset transferred.

Interests in joint ventures

A joint venture is a contractual arrangement whereby the Group and other parties undertake an economic activity that is subject to joint control, that is when the strategic financial and operating policy decisions relating to the activities require the unanimous consent of the parties sharing control.

Joint venture arrangements that involve the establishment of a separate entity in which each venturer has an interest are referred to as jointly controlled entities. The Group reports itsinterests in jointly controlled entities using the equity method.

Where the Group transacts with its jointly controlled entities, unrealised profits and losses are eliminated to the extent of the Group’s interest in the joint venture.

Goodwill

Goodwill arising on the acquisition of a subsidiary or a jointly controlled entity represents the excess of the cost of acquisition over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities of the subsidiary or jointly controlled entity recognised at the date of acquisition. Goodwill is initially recognised as an asset at cost and is subsequently measured at cost less any accumulated impairment losses.

For the purpose of impairment testing, goodwill is allocated to each of the Group’s cash-generating units expected to benefit from the synergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired. If the recoverable amount of thecash-generating unit is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro-rata on the basis of the carrying amount of each asset in the unit. An impairment loss recognised for goodwill is not reversed in a subsequent period.

On disposal of a subsidiary or a jointly controlled entity, the attributable amount of goodwill is included in the determination of the profit or loss on disposal.

27

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Due from/to customers

Due from/to customers at the statement of financial position date comprises the cost of work done to date on construction projects in progress, plus any profit attributable recognized in accordance with the Group’s policy for revenue recognition, less progress billings made to date.

Inventories

Inventories are valued at the lower of cost and net realizable value. Cost is allocated on First-In First-out (FIFO) basis and comprises direct materials and, where applicable, direct labour costs and those overheads that have been incurred in bringing the inventories to their present location and condition. Net realizable value represents the estimated selling price less all estimated costs to completion and costs to be incurred in marketing, selling and distribution.

Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and any accumu-lated impairment losses.

Depreciation is calculated so as to write off the cost of property, plant and equipment on a straight-line basis over the expected useful economic lives of the assets concerned. The annual rates used for this purpose are:

Machinery and equipment Office computers Office and residential furniture and fittings Motor vehicles Premises and labour camps

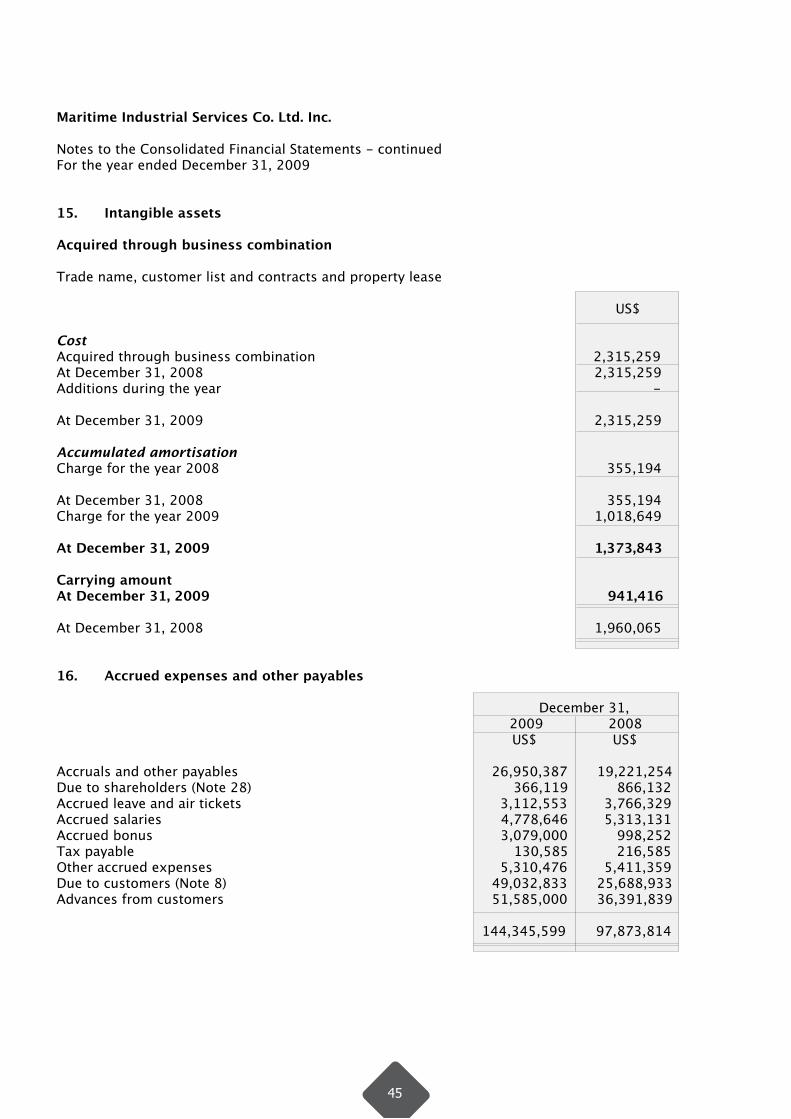

Intangible assets

Intangible assets acquired in a business combination

Intangible assets acquired in a business combination are identified and recognised separately from goodwill where they satisfy the definition of an intangible asset and their fair values can be measured reliably. The cost of such intangible assets is their fair value at the acquisition date.

Subsequent to initial recognition, intangible assets acquired in a business combination are reported at cost less accumulated amortisation and accumulated impairment losses. Amortisation is charged on a straight-line basis over their estimated useful lives of 1 to 6 years. The estimated useful life and amortisation method are reviewed at the end of each annual reporting period, with the effect of any changes in estimate being accounted for on a prospective basis.

10 - 50%10 - 50%25 - 30%25 - 30%

5 - 30%

28

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Impairment of tangible and intangible assets

At each statement of financial position date, the Group reviews the carrying amounts of itstangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not pos-sible to estimate the recoverable amount of an individual asset, the Group estimates the recov-erable amount of the cash-generating unit to which the asset belongs. Where a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

Intangible assets with indefinite useful lives and intangible assets not yet available for use are tested for impairment annually, and whenever there is an indication that the asset may be impaired.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognised immediately in the consolidated statement of comprehensive income, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset(or cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (or cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in the consolidated statement of comprehensive income, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

Provision for employees’ end of service indemnity

Provision for employees’ end of service indemnity is made in accordance with the Labour Laws applicable in the countries in which the Group operates, and is computed based on the current employee remuneration at the statement of financial position date and cumulative number of years of service at that date.

29

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Borrowing costs

Borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale.

Investment income earned on the temporary investment of specific borrowings pending their expenditure on qualifying assets is deducted from the borrowing costs eligible for capitalisa-tion.

All other borrowing costs are recognised in the consolidated statement of comprehensive income in the period in which they are incurred.

Legal reserve

In accordance with Article 154 of the Commercial Companies Law of the Sultanate of Oman, Mari-time Industrial Services Co. Ltd. has established a statutory reserve by appropriation of 10% of net income until such time as the reserve amounts to at least one third of the share capital. The reserve is not available for distribution.

Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable.

Products and services revenue represents the net amount invoiced during the year.

Where the outcome of a construction contract can be estimated reliably, revenue and costs are recognised by reference to the stage of completion of the contract activity at the statement of financial position date, measured as the proportion that contract costs incurred for work performed to date bear to the estimated total contract costs, except where this would not be representative of the stage of completion. Variations in contract work are recognized when agreed or, if not agreed at the reporting date, to the extent that it is probable that they will result in revenue and the minimum amount receivable can be reasonably determined. Contract claims and incentive payments are included to the extent that they have been agreed with the customer.

Where the outcome of a construction contract cannot be estimated reliably, contract revenue is recognised to the extent of contract costs incurred that it is probable will be recoverable. Contract costs are recognised as expenses in the period in which they are incurred.

When it is probable that total contract costs will exceed total contract revenue, the total expected loss is recognised as an expense immediately.

30

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Derivative financial instruments and hedge accounting

The Group’s activities expose it primarily to the financial risk of changes in foreign exchange rates. The Group uses derivative financial instruments (primarily foreign currency forward con-tracts) to hedge its risks associated with foreign currency fluctuations relating to certain firm commitments.

Derivative financial instruments are initially recorded at cost and are re-measured to fair value at subsequent reporting dates.

Changes in the fair value of derivative financial instruments that are designated and effective as cash flow hedges are recognized directly in equity. Amounts deferred in equity are recognized in the consolidated statement of comprehensive income in the same period in which the hedged firm commitment or forecasted transaction affects net profit or loss.

Changes in the fair value of derivative financial instruments that do not qualify for hedge accounting are recognized in the consolidated statement of comprehensive income as they arise.

Foreign currency transactions

The individual financial statements of each group entity are presented in the currency of the primary economic environment in which the entity operates (its functional currency). For the purpose of the consolidated financial statements, the results and financial position of each entity are expressed in United States Dollars (‘US$’), which is the presentation currency for these con-solidated financial statements.

In preparing the financial statements of the individual entities, transactions in currencies other than the entity’s functional currency (foreign currencies) are recorded at the rates of exchange prevailing at the dates of the transactions. At each statement of financial position date, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the state-ment of financial position date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated. Exchange differences are recognised in the consolidated statement of comprehensive income in the period in which they arise.

For the purpose of presenting consolidated financial statements, the assets and liabilities of the Group’s foreign operations are expressed in United States Dollars using exchange rates prevailing at the statement of financial position date. Income and expense items are trans-lated at the average exchange rates for the period, unless exchange rates fluctuated signifi-cantly during that period, in which case the exchange rates at the dates of the transactions are used. Exchange differences arising, if any, are classified as equity and transferred to the Group’s translation reserve. Such exchange differences are recognised in profit or loss in the period in which the foreign operation is disposed of.

31

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Taxation

Tax expense is based on results for the period in each tax jurisdiction in which the Group’s branches or entities are registered as adjusted for items which are non-assessable or disallowed. It is calculated using tax rates for each jurisdiction that have been enacted or substantially enact-ed by the statement of financial position date. Deferred tax is accounted for using the statement of financial position liability method in respect of temporary differences arising from differences between the carrying amount of assets and liabilities in the consolidated financial statements and the corresponding tax basis used in the computation of taxable profit.

Financial instruments

Financial assets and financial liabilities are recognized on the Group’s statement of financial po-sition when the Group becomes a party to the contractual provisions of the instrument. Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, and other short-term highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value.

Loans and receivables

Accounts receivable, loans, and other receivables that have fixed or determinable payments that are not quoted in an active market are classified as loans and receivables. Loans and receivables are measured at amortized cost using the effective interest method, less any impairment. Interest income is recognized by applying the effective interest rate, except for short-term receivables when the recognition of interest would be immaterial.

Classification as debt or equity

Debt and equity instruments are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangement.

Equity instruments

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Group are recorded at the proceeds received, net of direct issue costs.

Other financial liabilities

Other financial liabilities, including borrowings, are initially measured at fair value, net of trans-action costs.

Other financial liabilities are subsequently measured at amortized cost using the effective inter-est method, with interest expense recognized on an effective yield basis.

32

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

3. Significant accounting policies (continued)

Financial instruments (continued)

Other financial liabilities (continued)

The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period.

Provisions

Provisions are recognized when the Group has a present obligation as a result of a past event, and it is probable that the Group will be required to settle that obligation. Provisions are measured at the directors’ best estimate of the expenditure required to settle the obligation at the statement of financial position date, and are discounted to present value where the effect is material.

4. Critical accounting judgments and key sources of estimation uncertainty

Critical judgments in applying the Group’s accounting policies

In the process of applying the Group’s accounting policies, which are described in Note 3, man-agement has made the following judgments that have the most significant effect on the amounts recognized in the consolidated financial statements (apart from those involving estimations, which are dealt with below).

Contract variations

Contract variations are recognized as revenues when agreed or, if not agreed at the reporting date, to the extent that it is probable that they will result in revenue and the minimum amount receivable can be reasonably determined. This requires the exercise of judgement by manage-ment based on prior experience, application of contract terms and relationship with the contract owners.

As mentioned in Note 8 (b) in relation to a contract in Qatar, the directors have reviewed the contractual terms and consider that the amount of US$ 20 million reflects the minimum amount due from the client.

Percentage-of-completion

The Group uses the percentage-of-completion method in accounting for its contract sales based on cost of work performed to date as a proportion of total estimated cost which, in the judgement of management, is the most reliable method of estimation of percentage of completion.

33

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

4. Critical accounting judgments and key sources of estimation uncertainty (continued)

Key sources of estimation uncertainty

The key assumptions concerning the future, and other key sources of estimation uncertainty at the statement of financial position date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year, are discussed below.

Inventories

Inventories are stated at the lower of cost or net realizable value. Adjustments to reduce the cost of inventory to its net realizable value, if required, are made at the item level for estimatedexcess, obsolescence or impaired balances. Factors influencing these adjustments include changes in demand, technological changes, physical deterioration and quality issues. Based on the above factors, management has applied certain percentages against the cost of this inventory to calculate the allowance for slow moving and obsolete inventory. Revisions to the allowance for slow moving inventory would be required if the outcome of these indicative factors differs from the estimates.

Property, plant and equipment The cost of property, plant and equipment is depreciated over the estimated useful life of the asset. The estimated useful life is based on expected usage of the asset and expected physical wear and tear, which depends on operational factors. The management estimates the residual value of assets on a periodic basis and has considered a residual value no greater than 10% of the cost of the assets.

Allowance for irrecoverable debts

Allowance for irrecoverable debts is determined using a combination of factors to ensure that the accounts receivable are not overstated due to uncollectability. The allowance for irrecoverable debts for all customers is based on a variety of factors, including the overall quality and aging of receivables, continuing credit evaluation of the customers’ financial conditions and collateral requirements from customers in certain circumstances. Also, specific allowances for individual accounts are recorded when the Group becomes aware of the customer’s inability to meet its financial obligations.

Taxation

Management believes that it has adequately provided for tax liabilities in the accompanyingfinancial statements. However, the risk remains that relevant authorities could take differing positions with regard to interpretive issues and the effect could be significant. There are anumber of matters where the interpretation of the tax law and tax positions adopted by the Group may not be accepted by the tax authorities. Consequently, additional taxes may be assessed including penalties and interest which will impact the tax charge and provision in the period in which such assessment is finalised, which could be significant.

34

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

4. Critical accounting judgments and key sources of estimation uncertainty (continued)

Key sources of estimation uncertainty (continued)

Contract revenues/costs

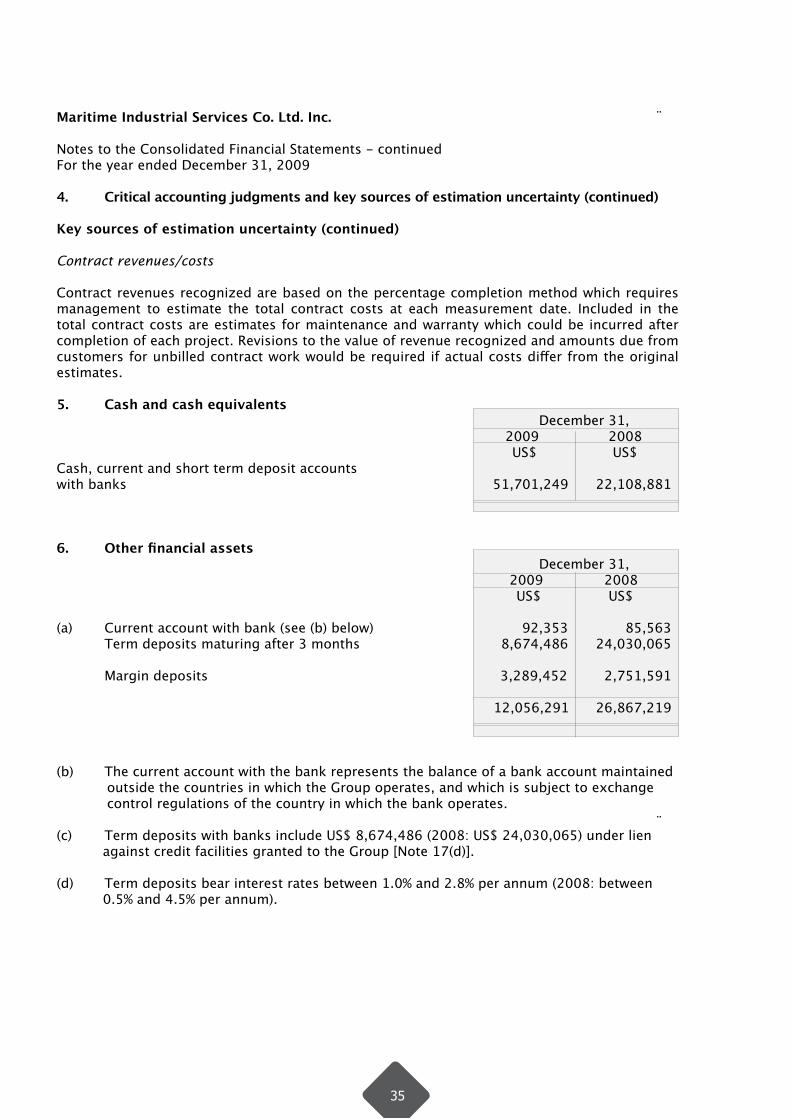

Contract revenues recognized are based on the percentage completion method which requires management to estimate the total contract costs at each measurement date. Included in the total contract costs are estimates for maintenance and warranty which could be incurred after completion of each project. Revisions to the value of revenue recognized and amounts due from customers for unbilled contract work would be required if actual costs differ from the original estimates.

5. Cash and cash equivalents December 31, 2009 2008 US$ US$Cash, current and short term deposit accounts with banks 51,701,249 22,108,881

6. Other financial assets December 31, 2009 2008 US$ US$

(a) Current account with bank (see (b) below) 92,353 85,563 Term deposits maturing after 3 months 8,674,486 24,030,065 Margin deposits 3,289,452 2,751,591

12,056,291 26,867,219

(b) The current account with the bank represents the balance of a bank account maintained outside the countries in which the Group operates, and which is subject to exchange control regulations of the country in which the bank operates.

(c) Term deposits with banks include US$ 8,674,486 (2008: US$ 24,030,065) under lien against credit facilities granted to the Group [Note 17(d)].

(d) Term deposits bear interest rates between 1.0% and 2.8% per annum (2008: between 0.5% and 4.5% per annum).

35

Maritime Industrial Services Co. Ltd. Inc. Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

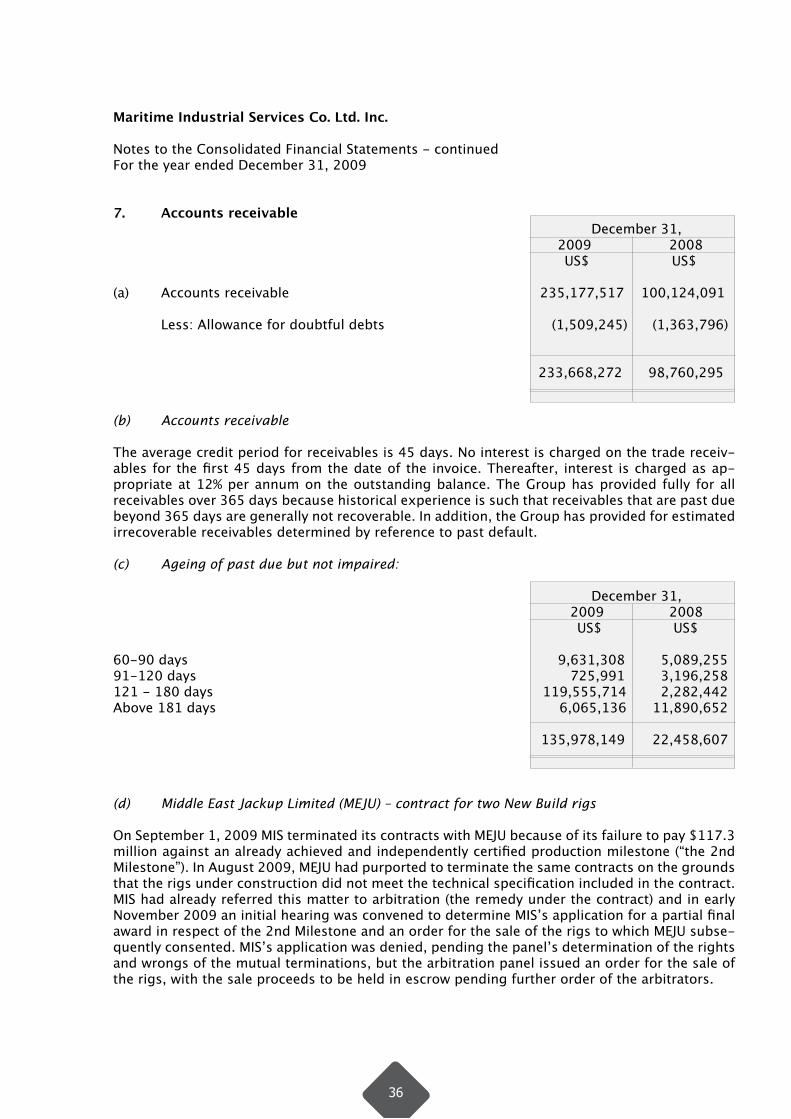

7. Accounts receivable December 31, 2009 2008 US$ US$

(a) Accounts receivable 235,177,517 100,124,091 Less: Allowance for doubtful debts (1,509,245) (1,363,796)

233,668,272 98,760,295 (b) Accounts receivable

The average credit period for receivables is 45 days. No interest is charged on the trade receiv-ables for the first 45 days from the date of the invoice. Thereafter, interest is charged as ap-propriate at 12% per annum on the outstanding balance. The Group has provided fully for all receivables over 365 days because historical experience is such that receivables that are past due beyond 365 days are generally not recoverable. In addition, the Group has provided for estimated irrecoverable receivables determined by reference to past default.

(c) Ageing of past due but not impaired:

December 31, 2009 2008 US$ US$

60-90 days 9,631,308 5,089,25591-120 days 725,991 3,196,258121 - 180 days 119,555,714 2,282,442Above 181 days 6,065,136 11,890,652 135,978,149 22,458,607

(d) Middle East Jackup Limited (MEJU) – contract for two New Build rigs

On September 1, 2009 MIS terminated its contracts with MEJU because of its failure to pay $117.3 million against an already achieved and independently certified production milestone (“the 2nd Milestone”). In August 2009, MEJU had purported to terminate the same contracts on the grounds that the rigs under construction did not meet the technical specification included in the contract. MIS had already referred this matter to arbitration (the remedy under the contract) and in early November 2009 an initial hearing was convened to determine MIS’s application for a partial final award in respect of the 2nd Milestone and an order for the sale of the rigs to which MEJU subse-quently consented. MIS’s application was denied, pending the panel’s determination of the rights and wrongs of the mutual terminations, but the arbitration panel issued an order for the sale of the rigs, with the sale proceeds to be held in escrow pending further order of the arbitrators.

36

Maritime Industrial Services Co. Ltd. Inc. Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

7. Accounts receivable (continued)

(d) Middle East Jackup Limited (MEJU) – contract for two New Build rigs (continued)

• Balances related to the above mentioned customer in the statement of financial position at December 31, 2009 totalled US$ 127.9 million comprising accounts receivable of $117.3 million and due from customers (Note 8) of US$ 10.6 million. Based on the indicative offers received management expects to fully recover these amounts from the proceeds of sale.

• MIS had contracts for the construction of Hulls 106 and 108 with respectively Mosvold Middle East Jackup I Limited and Mosvold Middle East Jackup II Limited, collectively referred to here as MEJU, in which MIS also has an indirect shareholding of 10%. This investment, valued at $10.1 million, has been fully provided.

(e) Movement in the allowance for doubtful debts:

December 31, 2009 2008 US$ US$

Balance at beginning of the year 1,363,796 1,430,715 Allowance for doubtful debts 626,123 402,131 Amounts written off as uncollectible (42,740) (17,642) Amounts recovered during the year (322,191) (451,408) Impairment losses reversed (115,743) - Balance at end of the year 1,509,245 1,363,796

In determining the recoverability of a accounts receivable, the Group considers any change in the credit quality of the accounts receivable from the date credit was initially granted up to the reporting date. The concentration of credit risk is limited due to the customer base being large and unrelated. Accordingly, the directors believe that there is no further credit provision required in excess of the allowance for doubtful debts.

(f) Ageing of impaired accounts receivable:

December 31, 2009 2008 US$ US$Impaired trade receivables 60-90 days - - 90-120 days - -121-365 days - -Above 365 days 1,509,245 1,363,796 Total 1,509,245 1,363,796

37

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

8. Due from customers

(a) Due from customers represents costs incurred and attributable profit recognized in excess of progress billings on jobs in progress.

December 31, 2009 2008 US$ US$Costs incurred plus recognized profits less recognized losses to date 612,942,774 575,143,681 Less: Progress billings (610,403,892) (506,431,385)

2,538,882 68,712,296 Disclosed as:Due from customers 51,571,715 94,401,229 Due to customers (Note 16) (49,032,833) (25,688,933)

2,538,882 68,712,296

(b) Qatar project

Included in the amount due from customers is an amount of US$ 20 million relating to variation orders on a construction project in Qatar, resulting from client imposed delays. The client made a formal settlement offer of US$ 20 million in October 2008 which MIS rejected. MIS is claim-ing approximately US$ 75 million and, although it continues to seek settlement on an amicable basis, it has now filed a formal lawsuit in Qatar and a hearing is set for March 23, 2010. MIS is confident that recovery will exceed the carrying value of US$ 20 million, but no revenue has been recognized in respect of the amounts claimed in excess of that amount.

38

Maritime Industrial Services Co. Ltd. Inc.

Notes to the Consolidated Financial Statements - continuedFor the year ended December 31, 2009

9. Prepayments and other receivables

December 31, 2009 2008 US$ US$

(a) Advances paid to suppliers [Note 9(b)] 22,606,763 59,085,865 Due from employees 1,207,952 1,467,401 Prepaid expenses 2,215,248 2,645,083 Deposits 999,416 1,239,713 Interest receivable 74,342 55,248 Other receivables 8,875,504 10,510,455

35,979,225 75,003,765 (b) Advances paid to suppliers in 2009 and 2008 are net of a provision of US$ 6.5 million in respect of advances made to a civil contractor engaged in a major Group construction contract which the directors consider may not be recoverable from the civil contractor.

10. Inventories

December 31, 2009 2008 US$ US$

Materials 3,844,408 3,223,577Spare parts 2,046,118 1,911,954Consumables 895,760 1,704,659Finished goods 890,397 623,398 7,676,683 7,463,588 Less: Allowance for slow moving inventories (1,995,389) (1,505,274) 5,681,294 5,958,314

39

Mar

itim

e In

dust

rial

Ser

vice

s Co

. Ltd

. Inc

.

Not

es to

the

Cons

olid

ated

Fin

anci

al S

tate

men

ts -

con

tinue

dFo

r th

e ye

ar e

nded

Dec

embe

r 31

, 200

9

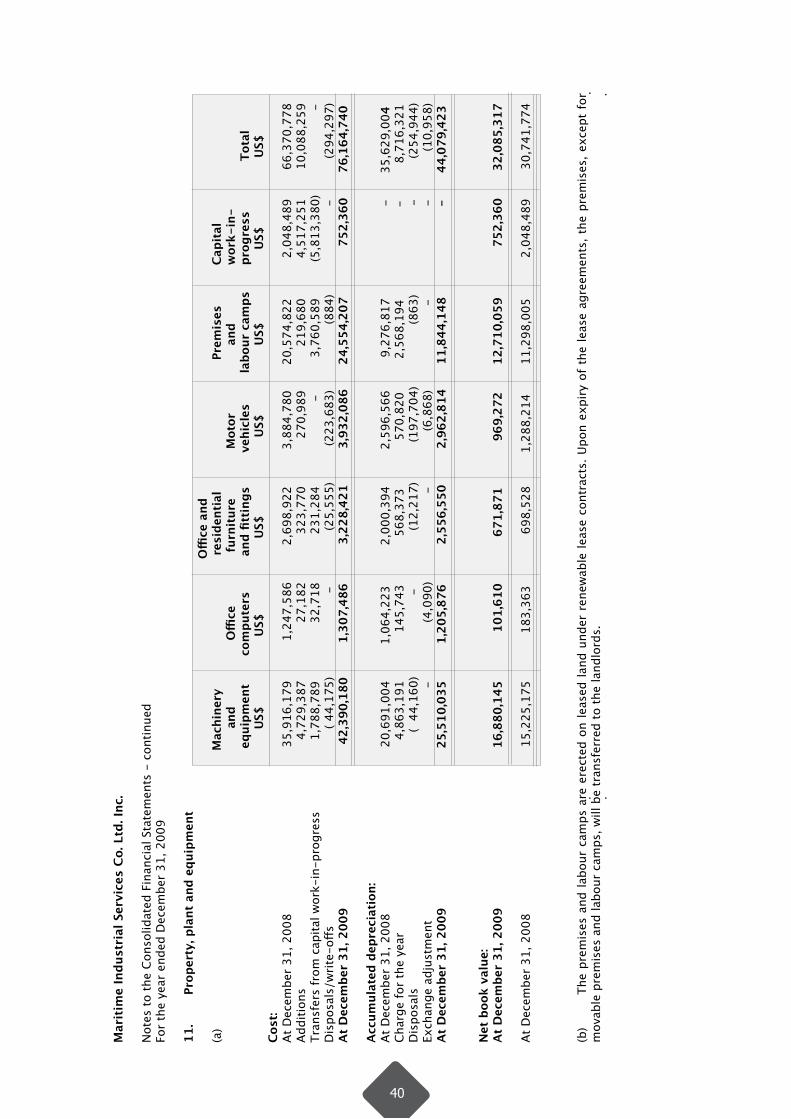

11.

Prop

erty

, pla

nt a

nd e

quip

men

t

Offi

ce a

nd

(a

)

M

achi

nery

resi

dent

ial

P

rem

ises

Capi

tal

and

O

ffice

furn

itur

e

M

otor

a

nd

w

ork-

in-

eq

uipm

ent

c

ompu

ters

a