The REVALTER Project “Multi-scale assessment of livestock development pathways in Vietnam” Action 3.2 : National Subsector Review Animal Feed Industry in Vietnam By Xavier BOCQUILLET Report presented at the Annual Meeting of the REVALTER Project held in Ba Vi (Vietnam) on Tuesday, 18 th and Wednesday, 19 th of March, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The REVALTER Project “Multi-scale assessment of livestock development pathways in Vietnam”

Action 3.2 : National Subsector Review

Animal Feed Industry in Vietnam

By Xavier BOCQUILLET

Report presented at the Annual Meeting of the REVALTER Project held in Ba Vi (Vietnam)

on Tuesday, 18th and Wednesday, 19th of March, 2013

Animal Feed Industry in Vietnam 2

Th

e R

ev

alt

er

Pro

ject

20

14

An

ima

l F

ee

d I

nd

us

try

in

Vie

tna

m

The present report proposes a global presentation of the animal feed industry in Vietnam, its actors and main characteristics.

Xavier Bocquillet

TABLE OF FIGURES

Figure 1 World Feed Production per region (tons) and numbers of Feedmills, Source: Alltech Global

Feed Summary, 2013 .............................................................................................................................. 9

Figure 2 Annual animal feed production per country in tons (and rank); Source: Alltech, Global Feed

Summary, 2013 ..................................................................................................................................... 10

Figure 3 Vietnam's import of feed and feed ingredient Source: GSO .................................................. 12

Figure 4: Origin, volume and price of imported corn in 2013 - 2014. Source: Agromonitor................ 14

Figure 5 Average Import Volumes of Corn from supplying countries in 2013 Source: Vietnam

Customs ................................................................................................................................................ 14

Figure 6: Origin, volume and price of imported soya in 2013 - 2014. Source: Agromonitor ............... 15

Figure 7: Average Import Volume of Soya Bean from Supplying countries in 2013. Source: Vietnam

Customs ................................................................................................................................................ 15

Figure 8 Corn production in Vietnam Source: USDA ............................................................................ 16

Figure 9 Typology of corn farmer in Vietnam. Source: CIMMYT, 2008 ................................................ 17

Figure 10 Soya production in Vietnam (tons) Source: USDA ................................................................ 17

Figure 11 World Corn and Soya Bean price, 2009-2014 Source: index mundi ..................................... 19

Figure 12 Average Import Price of Corn from supplying countries in 2013 (USD) ............................... 20

Figure 13 Vietnam Import Price of Feed ingredients Source: Vietnam Customs Feb 2014 ................. 20

Figure 14 Procurement price of whole-grain corn by week, 2012-2014 (VND/kg). Source:

Agromonitor .......................................................................................................................................... 21

Figure 15 Average Import Price of Soya Bean from supplying countries in 2013 (USD) Source:

Vietnam Customs .................................................................................................................................. 22

Figure 16 Soya meal price in Dong Nai 2012-2014, Source: Agromonitor ........................................... 23

Figure 17 Procurement prices of cassava chips in Vietnam, 2012 to 2014. Source: Agromonitor ...... 24

Figure 18 Price of rice bran at warehouses in The Mekong Delta (VND/kg). Source: Agromonitor .... 24

Figure 19 Price of animal feed ingredient at warehouse of buyer, Feb 2014, Source adapted from

Agromonitor .......................................................................................................................................... 25

Figure 20 Supply VS demand of industrial feed during 2010's and ratio of industrial feed, self-made

feed and import feed during the 2010's. Source: MARD ...................................................................... 30

Figure 21 Annual Animal feed production – Vietnam Source: MARD .................................................. 31

Figure 22 ratio of industrial and self-made feed and import feed during the 2010's. Source: MARD . 32

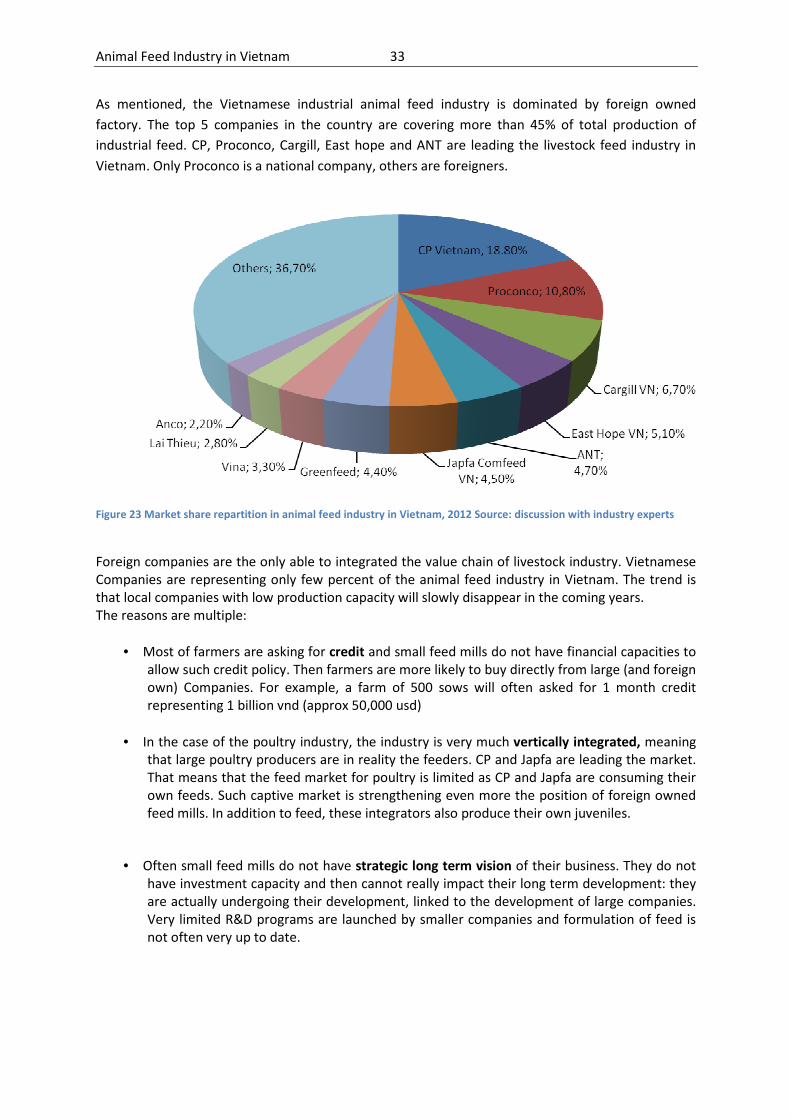

Figure 23 Market share repartition in animal feed industry in Vietnam, 2012 .................................... 33

Figure 24 CPV feedmills location in Vietnam, Source CP Hong Kong ................................................... 38

Figure 25 Location of Greenfeed factories and branch, Source: Greenfeed Co ................................... 40

Animal Feed Industry in Vietnam 4

Figure 26 Basic feed distribution organization in Vietnam ................................................................... 42

Figure 27 Vertical integrated Agri-Food Business of CPV, Source: CP Corporation ............................. 48

Table of Content

1. International context (in particular the Asian context) ........................................................... 9

1.1. Brief presentation of animal feed industry in the world and neighboring countries. ............ 9

1.2. Import figures and origins of main raw materials ................................................................ 11

1.3. Domestic production of raw materials ................................................................................. 16

1.4. Price overview of main import raw materials....................................................................... 19

2. Presentation of the sector................................................................................................... 26

2.1. Presentation of the animal feed value chain in Vietnam...................................................... 26

2.2. Production volume in the last 5 years and production capacity in 2013 ............................. 31

2.3. Farm made feed VS industrial feed ....................................................................................... 31

3. Presentation of actors involved ........................................................................................... 32

3.1. Listing of the existing producers or animal feed (aqua and livestock feed) ......................... 32

3.2. Location of main feedmill in Vietnam ................................................................................... 35

3.3. Presentation of the top 5 producers..................................................................................... 38

3.4. Production capacity of main actors ...................................................................................... 41

3.5. Marketing system of major companies ................................................................................ 41

3.6. Investments and major moves in the industry. .................................................................... 44

3.7. Value chain integration and Contract farming...................................................................... 47

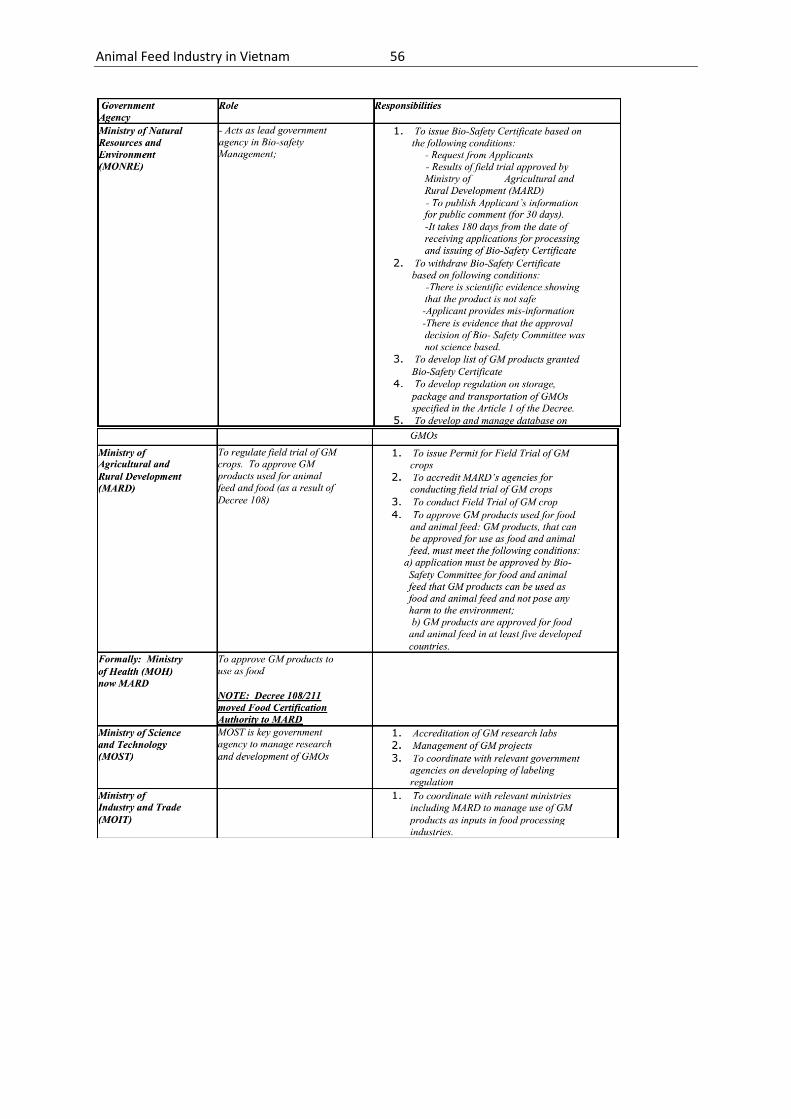

4. Governance of the value chain. ........................................................................................... 51

4.1. Priorities and programs from government ........................................................................... 51

4.2. Public investments, credit, loans .......................................................................................... 52

4.3. Quality management and traceability (including OGM) ....................................................... 54

5. Conclusion: issues and prospects for sustainability .............................................................. 57

INTRODUCTION

The Vietnamese agricultural sector was worth 31.4 Billion USD in 2013 representing 18.4% of GDP1.

Not like other developing countries, Vietnam having a population of 90 million with an economy

growing at 7-8% for more than two decades has a potential for livestock and feed sector expansions.

70% of the country’s population earns their life from agriculture with the majority of agricultural

production taking place on family farm of less than 0.5 ha. Labor is cheap and most production is not

industrialized. State-owned-enterprises still play a large role in the production, processing and

distribution of agricultural products, in particular for rice, coffee, rubber and tea2.

Experts have estimated that the earnings from livestock make up to 70% of the income of the

farmers in the countryside. However, despite being an important role in the livelihood of the

farmers, the livestock industry in Vietnam remains obsolete and not yet able to meet demand of the

domestic consumption.

From the Ministry of Agriculture and Rural Development (MARD), livestock in Vietnam exists mainly

in two forms: industrial farms and farmer (family) households. Two-thirds of the farms are in the

North and the rest is in the South. Although performance on a small scale with uncertainty in

quantity and quality, 8.5 million farmer households still account for about 65% of the pigs, 70% of

the chicken and 90% of the buffalos and cattle raised in the country3.

Vietnamese per capita meat consumption (seafood not included) is 40 kg annually, below China’s

60.4kg, but the same like South Korea’s, Japan’s and the world average. Vietnam’s meat

consumption habits are very unbalanced and surprising. According to Mr Hoang Kim Giao, Director

of the General Department for Livestock, under MADR, chicken account for 12-15%, cattle and

buffalo 5-8%, whereas pork for 80% of the total consumption. The low poultry consumption (5kg per

capita) contradicts most of the less developed countries, who eat mainly white meat such as chicken

or fish. Vietnam is an exception in Southeast Asia. It consumes surprising 32 kg pork per head,

comparable to China and the US, ahead of the wealth-off Singapore. It is estimated by MARD that

the meat consumption grows yearly by the year 2020 at 2.9%, from which, pork at 2%, poultry 5%

and cattle & buffalo 11%. Vietnam imports every year 3-5% of the total meat consumption, mainly

beef and chicken.

This important meat consumption in the country is the direct reason for the pressure on the animal

feed industry. With an annual growth rate of 17%, the Vietnamese animal feed industry is one of the

most dynamic in the world. By importing, in average, 50% to 55% of the raw material needed to

produce compound feed, the country is facing challenges and large foreign own companies are

imposing their rules in the atomized livestock production sector.

The Ministry of Industry and Trade forecasted that the growth rate of feed business will grow at 20%

per year in the next 2 years.

1 CCIFV, Feb 2014

2 Macdonalds, Background: Agriculture in Vietnam, Oct 2013

3 OSEC, Vietnam Feed Industry, Mar 2012

Animal Feed Industry in Vietnam 8

The present report will present the animal feed industry in Vietnam. After a brief presentation of the

international context of such industry, we will propose a detailed presentation of the Vietnamese

animal feed industry, considering its specificity: small farmers represent the majority of producers

but are not entirely in adequation with large integrated companies.

The report will detail the role of the main actors of the industry and will conclude by analyzing

impact of their integration strategy on the livestock landscape in Vietnam. Finally issues and

prospects for the sustainability of the industry will be discussed.

1. INTERNATIONAL CONTEXT (IN PARTICULAR THE ASIAN CONTEXT)

1.1. Brief presentation of animal feed industry in the world and neighboring countries.

The world production of animal feed has been evaluated by industry player and the following figures

consider feed production in 134 countries. In 2013 approximately 950 million tons have been

produced, a 9 percent increase over the late 2011 estimates of 873 million. Among the 134 countries

reviewed, China was once again the leading producer of feed with 198.3 million tons manufactured

in the official estimate of more than 10,000 feed mills. Consistent with late 2011 assessments, the

United States and Brazil followed in second and third places, with 168.5 million tons from 5,251 feed

mills and 66 million tons from 1,237 feed mills respectively. China, USA and Brazil the top 3 world’s

producers represent 45% of the volume at 433 million tons.

Asia continues to be the world’s leading feed producing region at 356 million tons produced in 2013

by 12,149 feedmills.

Figure 1 World Feed Production per region (tons) and numbers of Feedmills, Source: Alltech Global Feed Summary, 2013

In 2012, considering the 25th largest animal feed producing countries, 9 countries belong to the

Asian area. China being the largest producing countries in the world (with over 198 million tons of

feed produced in 2013, is followed by India (ranked 6th, 27 million tons), Japan (7th, 25 million tons),

Thailand (12th, 15.7 million tons) and Indonesia (15th, 13.8 million tons). Vietnam is the 20th largest

country in the world with 230 feedmills in operation in 2013 producing over 12 million tons of feed4.

4 Source: Alltech Global Feed Summary, 2013

Animal Feed Industry in Vietnam 10

Figure 2 Annual animal feed production per country in tons (and rank); Source: Alltech, Global Feed Summary, 2013

Thailand feed industry overview

Thailand’s animal feed industry includes more than 1,000 manufacturers today of which around 200

are ranked medium to large sized businesses. The majority of businesses produce livestock feed.

About 150 of the businesses in the industry are aquafeed specialists, of which around 70 are

producers of complete aquaculture feeds. The largest animal feed factories are those that are

integrated into the poultry and pork businesses.

Some of these large businesses, e.g. CP and Betagro, are also marketing their feed products to a

broad base of independent farmers. Betagro claims to be the largest feed manufacturer in Thailand

with a recently expanded production capacity of close to 2.2 million tones. CP also claims market

leadership in Thailand. CP Foods is the largest feed producer in the world with over 23 million tons

produced all over the world representing annual sales of US$ 5.6 billion5. Amongst the other larger

companies that operate in the industry are Bangkok Feedmill, Krungthai Feedmill, Lee Pattana Feed

Mill, Laemthong Agri-Products, Thai Feedmills and United Feed Mill.

The animal feed industry’s commercial activities are constrained by price control regulations. Animal

feed is one of the products whose price is controlled and monitored by the Internal Trade

Department of the Ministry of Commerce. These controls are in place as part of efforts by the

government to control the price of meat/poultry in the end market to keep it affordable for a broad

range of consumers in different income groups. The government controls over animal feed prices

cause feed input and additive buyers to become highly price sensitive. This is a particular problem

for buyers that might want to purchase inputs and additives from the developed world6.

5 Feed International, Oct 2010

6 www.allaboutfeed.net, Dec 2009

Animal Feed Industry in Vietnam 11

Indonesia feed industry overview

In 2012, the consumption of animal and aquaculture feed in Indonesia was approximately 13.8 million tons, a 13% hike on 2011. Based on data from Indonesian Feed Mills Association (GPMT), total consumption of animal feed in 2012 was approximately 12.7 million tones, an increase of 12.39% compared to 2011, which was 11.3 million tones. The break-down of animal feed consumption was 45% broilers, 44% layers, 9% breeders and the rest are other livestock. While total consumption of fish and shrimp feed reached 1.2 million tons, up 20% compared to 2011, which was 1 million tons. This year the consumption of animal and aquaculture feed in Indonesia has the potential to grow by 12%, to 15.5 million tons. Animal feed consumption is projected to grow 8.66%, to 13.8 million tons.

According to GPMT, the growth of animal and aquaculture feed consumption has been fuelled by the increased consumption of animal and aquaculture products. Japfa Comfeed is the largest Indonesian feedmill with over 1.7 million tons of feed produced annually (2010)7.

Philippines feed industry overview

In total there are 1,730 feed manufacturers in the Philippines, all located in Central Luzon area. There is a need for more feedmills in other region (Eastern Visayas and the Autonomous Region in Muslim Mindanao) and more investments for the production of halal feed or those with no pork component like lard. Investments in the feed industry are hindered by the lack of land since large areas have been converted for other purposes and not agricultural production. Feed millers in the Philippines have revised their output projection for 2014, saying animal feeds would go down by 23% to 9.24 million tons from 12 million tons.

"Production was down for lack of demand. Pig production not only failed to pickup but in fact was depressed due to a slack in the production of piglets," an official of the Philippine Association of Feed Millers Inc. said. Feed millers said the industry remains persistent not to bring in additional corn despite a projected shortfall in production due to low demand for animal feeds.

1.2. Import figures and origins of main raw materials

Raw material sourcing

Vietnam is a country with one of the most dynamic agriculture sector. However, facing a limited land

expansion capacity, the country does not manage to be self sufficient in agriculture raw materials

7 www.allaboutfeed.net, 2013

Animal Feed Industry in Vietnam 12

needed to process animal feed. Corn, Soya bean and wheat, the main ingredient for animal feed,

have to be massively imported to satisfy the demand of the animal feed industry.

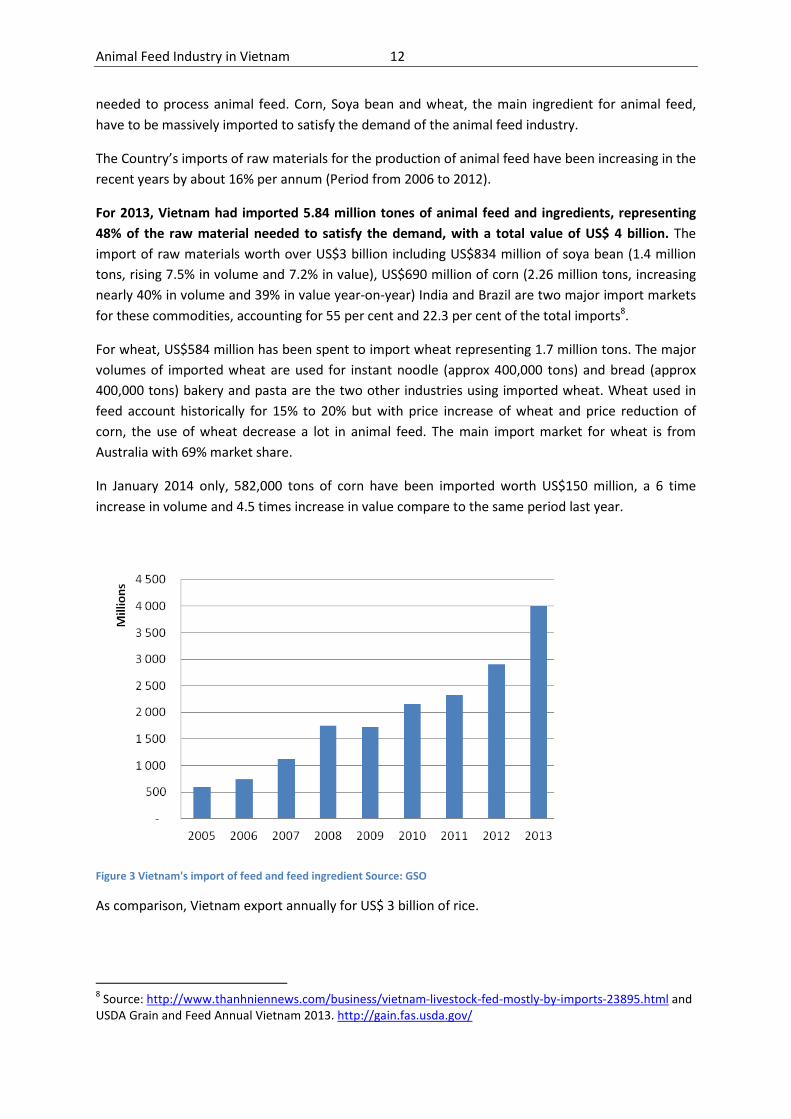

The Country’s imports of raw materials for the production of animal feed have been increasing in the

recent years by about 16% per annum (Period from 2006 to 2012).

For 2013, Vietnam had imported 5.84 million tones of animal feed and ingredients, representing

48% of the raw material needed to satisfy the demand, with a total value of US$ 4 billion. The

import of raw materials worth over US$3 billion including US$834 million of soya bean (1.4 million

tons, rising 7.5% in volume and 7.2% in value), US$690 million of corn (2.26 million tons, increasing

nearly 40% in volume and 39% in value year-on-year) India and Brazil are two major import markets

for these commodities, accounting for 55 per cent and 22.3 per cent of the total imports8.

For wheat, US$584 million has been spent to import wheat representing 1.7 million tons. The major

volumes of imported wheat are used for instant noodle (approx 400,000 tons) and bread (approx

400,000 tons) bakery and pasta are the two other industries using imported wheat. Wheat used in

feed account historically for 15% to 20% but with price increase of wheat and price reduction of

corn, the use of wheat decrease a lot in animal feed. The main import market for wheat is from

Australia with 69% market share.

In January 2014 only, 582,000 tons of corn have been imported worth US$150 million, a 6 time

increase in volume and 4.5 times increase in value compare to the same period last year.

Figure 3 Vietnam's import of feed and feed ingredient Source: GSO

As comparison, Vietnam export annually for US$ 3 billion of rice.

8 Source: http://www.thanhniennews.com/business/vietnam-livestock-fed-mostly-by-imports-23895.html and

USDA Grain and Feed Annual Vietnam 2013. http://gain.fas.usda.gov/

Animal Feed Industry in Vietnam 13

Soya, corn, cassava and wheat are raw materials imported in Vietnam. Due to fragmented farming

structure, Vietnam is facing difficulties to ensure self sufficiency in raw material. Raw material

industry is characterized by small producers, with low yield and poor quality of grain.

One on the main issue is the status of post harvest facilities: driers and silo are not sufficient in the

country leading to poor quality of grain and post harvest losses.

The corn value chain is structured around small farmers, collectors and traders. If we look at the

drying activity we can notice that corn is dried one time at the farm level, often on the road close to

the field. The uniformity of the humidity cannot be ensured by farmers as grain is dried under the

sun without any humidity monitoring. Then collectors are collecting small volumes of corn from

numerous farmers. That means that different grain with different origin and humidity level are

mixed together. Then traders are buying even bigger volume mixing again origin and quality of grain.

Finally feed mills are buying the corn but are often facing large heterogeneity of products, quality,

colors, etc. Moreover, due to poor post harvest treatment we often have development of mycotoxin

in the grain leading to poor quality feed as mycotoxin can have massive impact on health of animals

(reproductive effects, hepatotoxic effects or performance effects). The mycotoxin impact on animal

husbandry together with higher price of local corn and inconsistency in supply are the main reasons

for feed mills to import corn from India, Thailand or South America.

In parallel, the corn value chain is not well organized in Vietnam. In 2010, 1 million tons of corn has

been lost due to lack of post harvest facilities. It is amazing to compare this figure to the volume of

corn imported: approximately 1 million tons have been imported in Vietnam in the same year9.

Finally, the supply chain is not efficient enough as logistic infrastructure and equipment are

still lacking. Access to farming area is difficult and only very few large stocking facilities exists. Very

limited private of public organization own professional dryers and silos in Vietnam in order to

properly dry and stock agricultural raw materials used in feed preparation. CP Vietnam invested in

these facilities and then reinforced their supremacies in animal feed business by controlling more

the upstream of the value chain.

Very few foreign own company have port facilities to unload grain from large boat and store it in

good conditions.

All these lead to a complex sourcing work for feedmill in Vietnam. Quality and quantity are key

issues that need to be tackled for development of feed industry in the country.

Origin of Raw materials: volume and value for main countries

As presented before, Vietnam is not self-sufficient in agricultural raw material for its animal feed

industry. Since many years the country has to import large part of soya, corn, cassava, wheat and

other feed additive.

9 Source: Industry experts

Animal Feed Industry in Vietnam 14

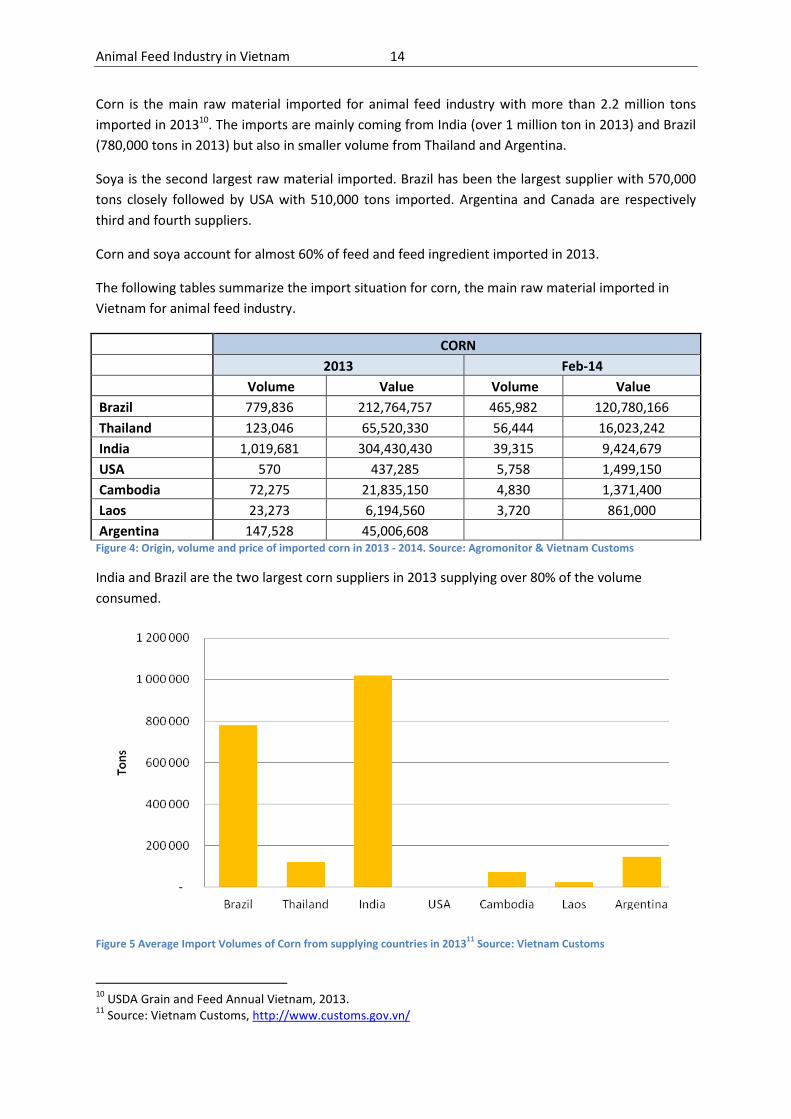

Corn is the main raw material imported for animal feed industry with more than 2.2 million tons

imported in 201310. The imports are mainly coming from India (over 1 million ton in 2013) and Brazil

(780,000 tons in 2013) but also in smaller volume from Thailand and Argentina.

Soya is the second largest raw material imported. Brazil has been the largest supplier with 570,000

tons closely followed by USA with 510,000 tons imported. Argentina and Canada are respectively

third and fourth suppliers.

Corn and soya account for almost 60% of feed and feed ingredient imported in 2013.

The following tables summarize the import situation for corn, the main raw material imported in

Vietnam for animal feed industry.

CORN

2013 Feb-14

Volume Value Volume Value

Brazil 779,836 212,764,757 465,982 120,780,166

Thailand 123,046 65,520,330 56,444 16,023,242

India 1,019,681 304,430,430 39,315 9,424,679

USA 570 437,285 5,758 1,499,150

Cambodia 72,275 21,835,150 4,830 1,371,400

Laos 23,273 6,194,560 3,720 861,000

Argentina 147,528 45,006,608 Figure 4: Origin, volume and price of imported corn in 2013 - 2014. Source: Agromonitor & Vietnam Customs

India and Brazil are the two largest corn suppliers in 2013 supplying over 80% of the volume

consumed.

Figure 5 Average Import Volumes of Corn from supplying countries in 201311

Source: Vietnam Customs

10

USDA Grain and Feed Annual Vietnam, 2013. 11

Source: Vietnam Customs, http://www.customs.gov.vn/

Animal Feed Industry in Vietnam 15

Soya bean were mainly coming from Brazil and USA in 2013. These two countries supplied over 90%

of total volume last year. Argentina and Canada were also supplying soya bean but is much smaller

volume.

SOYA

2013 Jan-14

Volume Value Volume Value

Brazil 570,911 331,741,981

USA 511,508 321,744,780 157,293 91,194,296

Argentina 67,602 40,605,494

Canada 36,298 25,195,760 2,463 1,518,084 Figure 6: Origin, volume and price of imported soya in 2013 - 2014. Source: Agromonitor

Figure 7: Average Import Volume of Soya Bean from Supplying countries in 2013. Source: Vietnam Customs,

http://www.customs.gov.vn/

Cassava is the third largest raw material used in animal feed production. Cassava is important

income sources of poor farmers thanks to its easy cultivation, low requirement on soils, low

investment costs, suitability to bio-ecology and farmer’s livelihoods. Cassava is widely grow from the

North to the South of Vietnam with more than half of million ha and production of almost 10 million

tons. In 2013 1.5 million tons of cassava has been sourced from local markets for animal feed

processing. In additions some volumes are coming from Cambodia but volumes are not really known

as statistics are missing.

Animal Feed Industry in Vietnam 16

Rice bran is also used in animal feed industry replacing wheat or corn depending on price. Rice bran

is mainly source locally (Mekong Delta mainly) but some imports have been recorded from India and

Pakistan.

1.3. Domestic production of raw materials

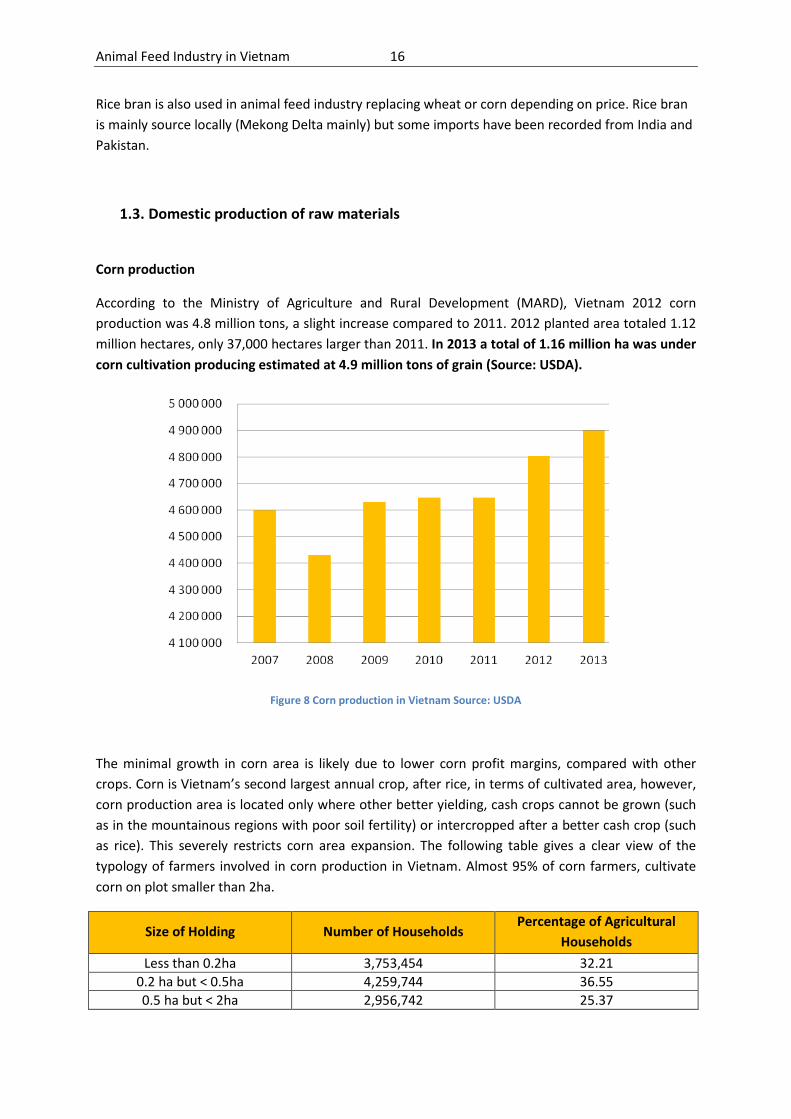

Corn production

According to the Ministry of Agriculture and Rural Development (MARD), Vietnam 2012 corn

production was 4.8 million tons, a slight increase compared to 2011. 2012 planted area totaled 1.12

million hectares, only 37,000 hectares larger than 2011. In 2013 a total of 1.16 million ha was under

corn cultivation producing estimated at 4.9 million tons of grain (Source: USDA).

Figure 8 Corn production in Vietnam Source: USDA

The minimal growth in corn area is likely due to lower corn profit margins, compared with other

crops. Corn is Vietnam’s second largest annual crop, after rice, in terms of cultivated area, however,

corn production area is located only where other better yielding, cash crops cannot be grown (such

as in the mountainous regions with poor soil fertility) or intercropped after a better cash crop (such

as rice). This severely restricts corn area expansion. The following table gives a clear view of the

typology of farmers involved in corn production in Vietnam. Almost 95% of corn farmers, cultivate

corn on plot smaller than 2ha.

Size of Holding Number of Households Percentage of Agricultural

Households

Less than 0.2ha 3,753,454 32.21

0.2 ha but < 0.5ha 4,259,744 36.55

0.5 ha but < 2ha 2,956,742 25.37

Animal Feed Industry in Vietnam 17

2 ha and over 683,538 5.88

11,653,478 100 Figure 9 Typology of corn farmer in Vietnam. Source: CIMMYT, 2008

According to MARD, Vietnam uses hybrid seed to plant 90 percent of the annual corn area. The local

production for hybrid corn seed, however, can only supply up to 20 percent of the total demand. The

outstanding 80 percent is imported from other countries. Thailand and Indonesia are two biggest

suppliers of hybrid corn seed into Vietnam. They account for about 62 percent and 19 percent,

respectively, of the total hybrid corn seed import volume.

The Ministry of Agriculture and Rural Development has said Vietnam will in 2014, use 130,000

hectares of rice land to grow corn and cassava for animal feed production. The corn production area

will increase to 1.23 million hectares, increasing 73,000 hectares compared to 2013. Vietnam will

also use high-yield seeds in order to produce 5.7 million tons of corn this year12.

Soya production

According to official government statistics, soybeans are currently grown in twenty five of Vietnam’s

sixty three provinces, with approximately 65 percent cultivated in the north and 35 percent in the

south13. Vietnam’s 2012 soybean production decreased 34.3 percent from the previous year to 175.2

thousand metric tons as severe cold weather at the end of 2011 and in early 2012, reduced yield and

harvested area. The scale of production remains relatively very small and continues to fall far short

of domestic demand. In 2013, the growing area expanded back to the level of 2011, with about 180

thousand ha and production to increase to 270 TMT. The soybean cultivation area is currently

concentrated with 65 percent in the North and 35 percent in South.

Figure 10 Soya production in Vietnam (tons) Source: USDA

12

Source: http://www.asian-agribiz.com/ 13

Source : USDA, Oilseeds and Product annual, Apr 2012

Animal Feed Industry in Vietnam 18

Despite, the uncompetitive nature of local soybean production, the Vietnamese Government’s

Master Plan for Oilseeds prioritizes further development of the sector with the objective of 350,000

ha and a production of 700,000 tons by 2020. The Master Plan focuses further development on the

Red River Delta, midland, and mountainous areas in the North and Western Highlands. However,

Post doubts that production will increase as much as the Government of Vietnam desires due to the

high input costs and generally low yields of oilseeds crops, and slow expansion in growing areas.

Vietnamese scientists are continuing research on biotech and other modern soybean varieties with

higher output levels and lower production costs in specific regions in Vietnam. MARD has approved

three biotech crop types for field trials – corn, cotton, and soybeans. However, no companies are

applying to implement Bt. soybean field trials at this time (only for Bt. corn). The field trial period is

expected to last for two or three years before final approval for commercialization is granted, if a

company does apply. As a result, there is no expectation that commercial production of any of

biotech oilseed crops will begin in the near future in Vietnam.

Cassava production

In the world, the three leading export countries are Thailand, Vietnam and Indonesia. Thailand

accounts for 60- 85% total global cassava export in recent years, followed by Indonesia and Vietnam.

Recently Cambodia cassava becomes a prospective export product.

Over 11 million tons have been produced in 2013. Cassava is the fourth agricultural products

exported from Vietnam in volume after rice, coffee and cashew nuts and belong to the 1 billion

export products club. In the end of 2012 exports of cassava and cassava based products was 4.23

million tons and valued at 1.35 billion USD. Vietnam is now the second largest exporting country of

cassava products while animal feed factories also contribute significantly to the increasing demand

for cassava roots.

Cassava production and yield of Vietnam significantly increase in recent years. The production in

2011 was 9.87 million tons from 559,800 ha, average yield: 17.81 ton/ ha. In 2000, cassava

production was 1.98 million tons, yield was 8.35 ton/ ha while the production in 2011 increased 4.98

folds and the yield doubled.14

Vietnam cassava yield growth. Cassava yield increased significantly recently. In 1976, the yield was

7.86 ton/ha, in 2000 was 8.35 ton/ha, close to Africa’s yield (8.65 ton/ha) but in 2011 the yield

reached to 17.73 ton/ha, much more than the average one in Africa at 10.77 ton/ha and higher than

12.92 tons/ha of America. The one of Vietnam now is lower than that of India (36.47 ton/ha), the

leading country in cassava yield of the world, Cambodia (21.30 ton/ ha), Indonesia (20.30 ton/ ha)

and Thailand (19.29 ton/ha) but cassava yield of many smallholders in Vietnam reach to 36.00- 50.00

ton/ ha, more than 400% than before.

Vietnam cassava was developed sustainably in the first years of the 21st century (2000-2013).

Cassava achievement of Vietnam is huge: it has been transformed from food crop, feed crop into 4F

14

http://www.asian-agribiz.com/

Animal Feed Industry in Vietnam 19

crop (Food, Feed, Flour, Fuel) as now biodiesel factories are processing cassava into ethanol (13

factories in operation in Vietnam).

1.4. Price overview of main import raw materials

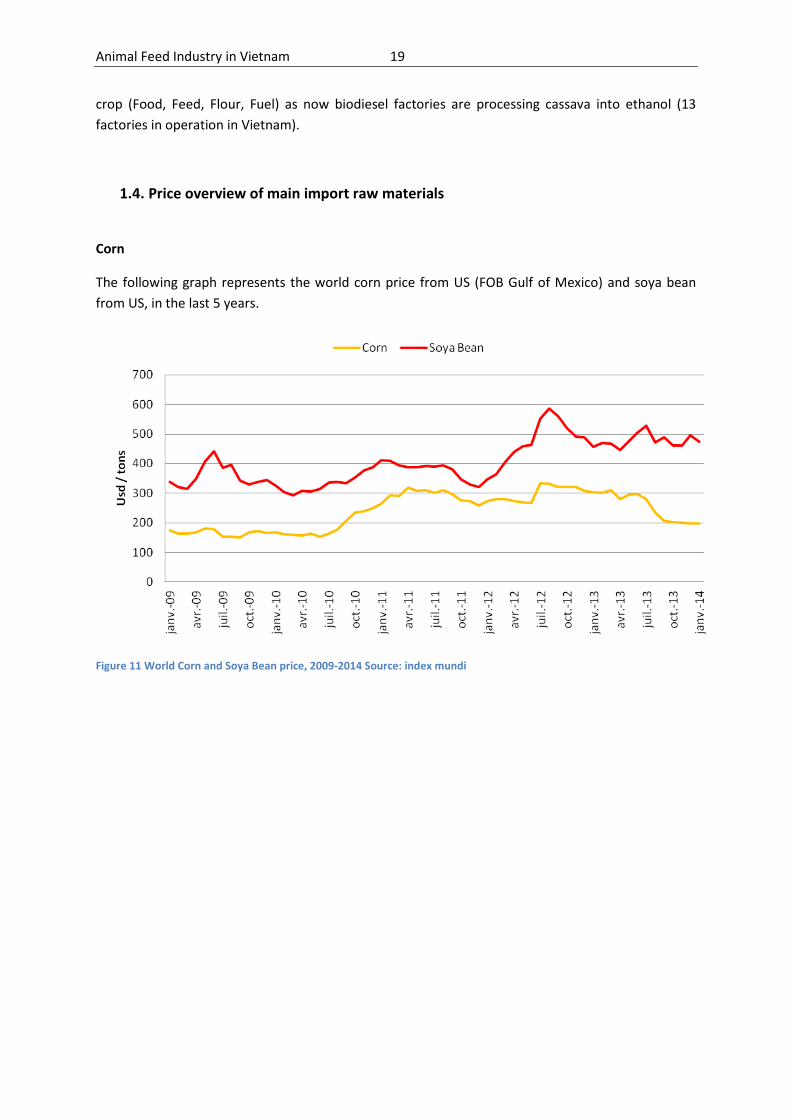

Corn

The following graph represents the world corn price from US (FOB Gulf of Mexico) and soya bean

from US, in the last 5 years.

Figure 11 World Corn and Soya Bean price, 2009-2014 Source: index mundi

Animal Feed Industry in Vietnam 20

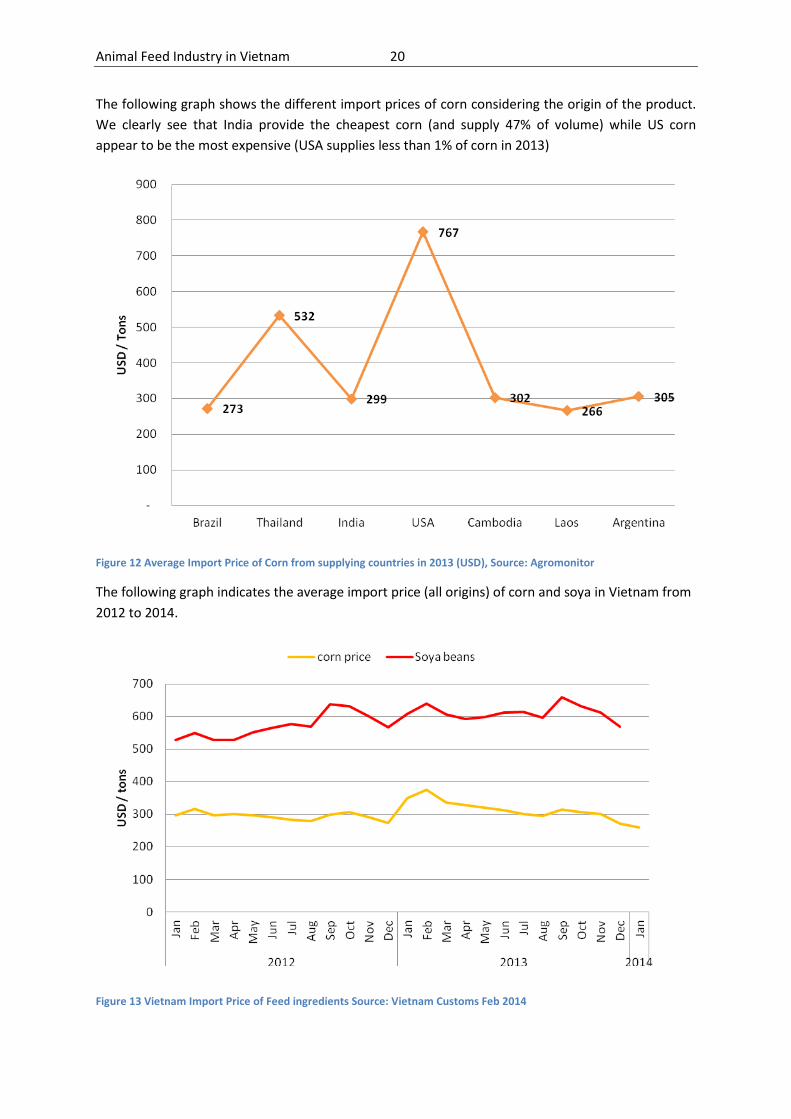

The following graph shows the different import prices of corn considering the origin of the product.

We clearly see that India provide the cheapest corn (and supply 47% of volume) while US corn

appear to be the most expensive (USA supplies less than 1% of corn in 2013)

Figure 12 Average Import Price of Corn from supplying countries in 2013 (USD), Source: Agromonitor

The following graph indicates the average import price (all origins) of corn and soya in Vietnam from

2012 to 2014.

Figure 13 Vietnam Import Price of Feed ingredients Source: Vietnam Customs Feb 2014

Animal Feed Industry in Vietnam 21

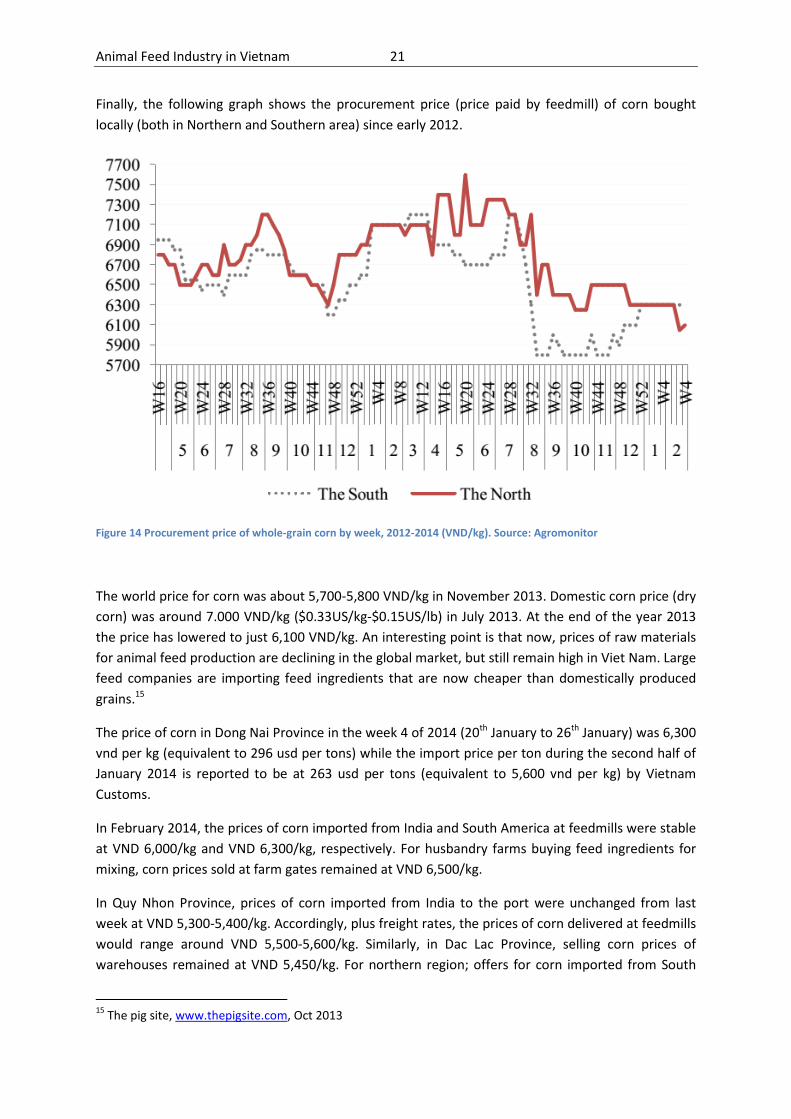

Finally, the following graph shows the procurement price (price paid by feedmill) of corn bought

locally (both in Northern and Southern area) since early 2012.

Figure 14 Procurement price of whole-grain corn by week, 2012-2014 (VND/kg). Source: Agromonitor

The world price for corn was about 5,700-5,800 VND/kg in November 2013. Domestic corn price (dry

corn) was around 7.000 VND/kg ($0.33US/kg-$0.15US/lb) in July 2013. At the end of the year 2013

the price has lowered to just 6,100 VND/kg. An interesting point is that now, prices of raw materials

for animal feed production are declining in the global market, but still remain high in Viet Nam. Large

feed companies are importing feed ingredients that are now cheaper than domestically produced

grains.15

The price of corn in Dong Nai Province in the week 4 of 2014 (20th January to 26th January) was 6,300

vnd per kg (equivalent to 296 usd per tons) while the import price per ton during the second half of

January 2014 is reported to be at 263 usd per tons (equivalent to 5,600 vnd per kg) by Vietnam

Customs.

In February 2014, the prices of corn imported from India and South America at feedmills were stable

at VND 6,000/kg and VND 6,300/kg, respectively. For husbandry farms buying feed ingredients for

mixing, corn prices sold at farm gates remained at VND 6,500/kg.

In Quy Nhon Province, prices of corn imported from India to the port were unchanged from last

week at VND 5,300-5,400/kg. Accordingly, plus freight rates, the prices of corn delivered at feedmills

would range around VND 5,500-5,600/kg. Similarly, in Dac Lac Province, selling corn prices of

warehouses remained at VND 5,450/kg. For northern region; offers for corn imported from South

15

The pig site, www.thepigsite.com, Oct 2013

Animal Feed Industry in Vietnam 22

America to ports hovered at VND 5,900-5,950/kg. Accordingly, plus freight rate, prices of corn

delivered at feedmills in Hung Yen and Hai Duong would be about VND 6,100/kg, nearly unchanged

from last week. However, compared to early February, the prices decreased by about VND 200/kg as

the corn import volume was ample while the demand for feed slowed down.

According to data from the General Department of Vietnam Customs, for the first half of February,

Vietnam imported as much as 338.1 thousand tons of corn, up by 47.2 thousand tons compared to

the same period of January. This figure was much higher compared to the figure of 33.3 thousand

tons in the same period of 2013. From the beginning of 2014 to February 15, accumulated corn

imports of Vietnam were 910.7 thousand tons, up nearly 10 times year on year.16

Soya

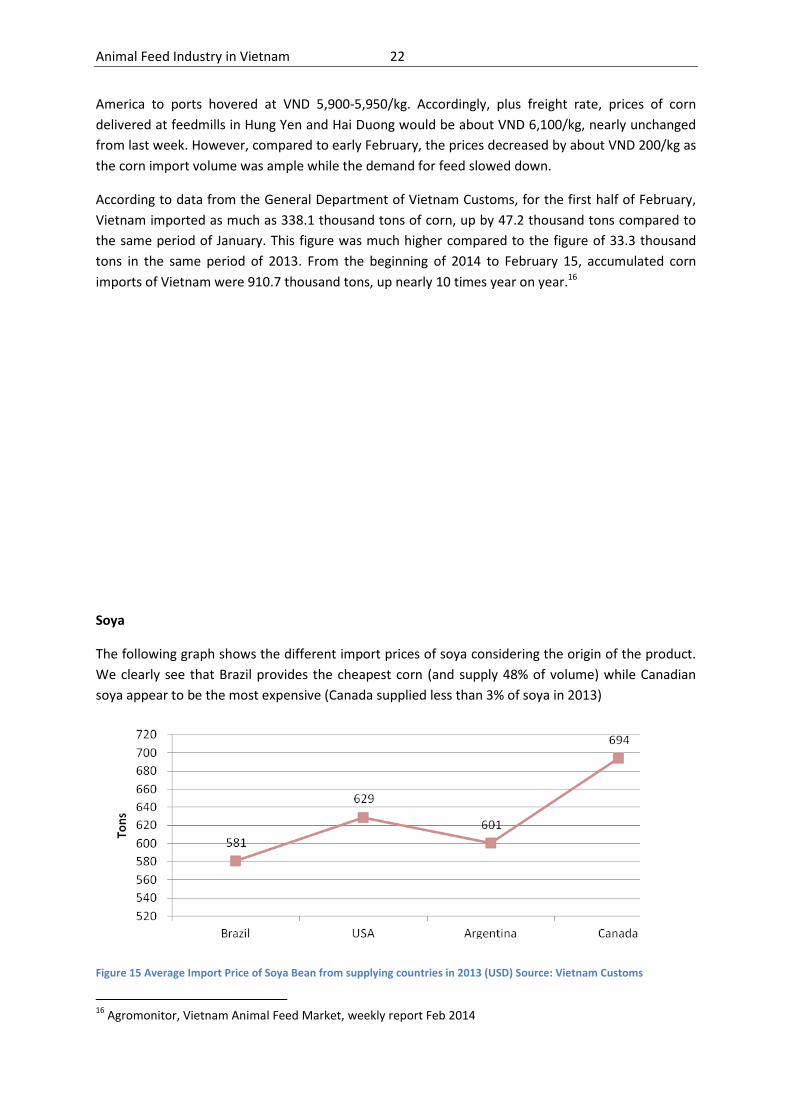

The following graph shows the different import prices of soya considering the origin of the product.

We clearly see that Brazil provides the cheapest corn (and supply 48% of volume) while Canadian

soya appear to be the most expensive (Canada supplied less than 3% of soya in 2013)

Figure 15 Average Import Price of Soya Bean from supplying countries in 2013 (USD) Source: Vietnam Customs

16

Agromonitor, Vietnam Animal Feed Market, weekly report Feb 2014

Animal Feed Industry in Vietnam 23

According to local industry, in 2013 the locally produced soybeans were not as price competitive as

imported soybeans. For example, local soybeans were quoted at 16,000 vnd ($0.77) – 17,000 vnd

($0.82) per kilogram (kg), while the imported soybeans cost 14,600 vnd - 15,000 vnd ($0.70-$0.71)

per kg. Competitiveness is a major disincentive to the expansion of the soybean sector overall.

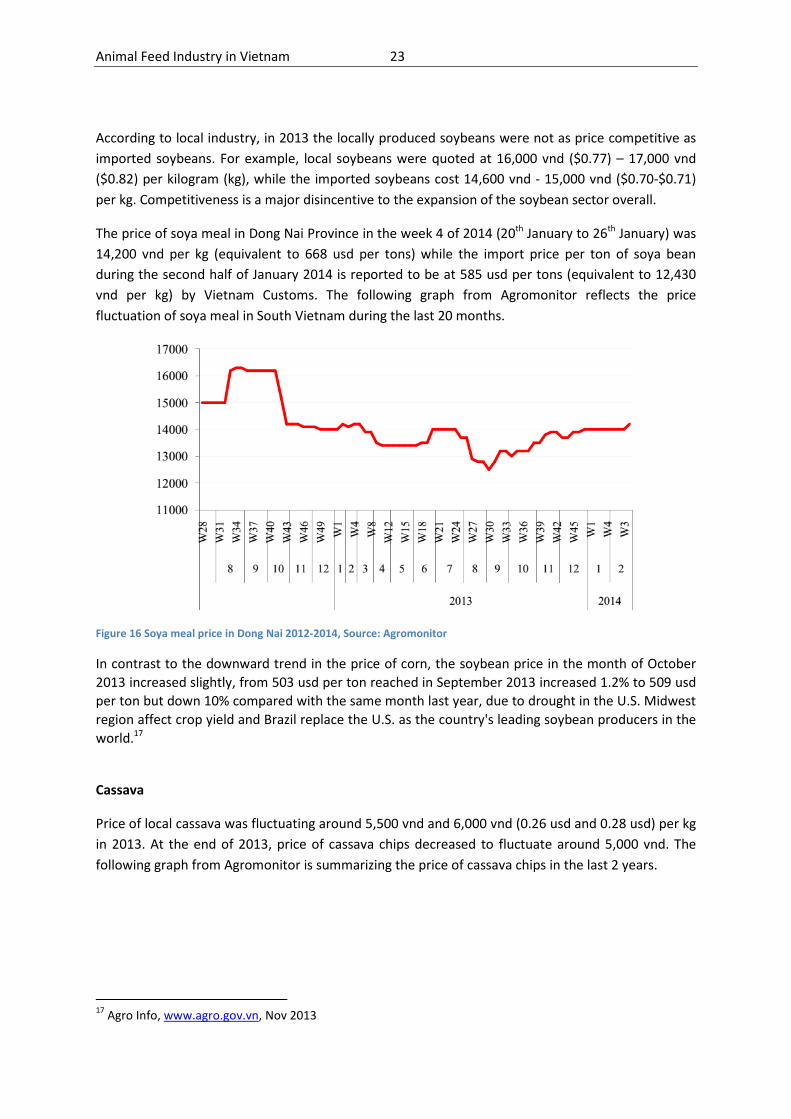

The price of soya meal in Dong Nai Province in the week 4 of 2014 (20th January to 26th January) was

14,200 vnd per kg (equivalent to 668 usd per tons) while the import price per ton of soya bean

during the second half of January 2014 is reported to be at 585 usd per tons (equivalent to 12,430

vnd per kg) by Vietnam Customs. The following graph from Agromonitor reflects the price

fluctuation of soya meal in South Vietnam during the last 20 months.

Figure 16 Soya meal price in Dong Nai 2012-2014, Source: Agromonitor

In contrast to the downward trend in the price of corn, the soybean price in the month of October

2013 increased slightly, from 503 usd per ton reached in September 2013 increased 1.2% to 509 usd

per ton but down 10% compared with the same month last year, due to drought in the U.S. Midwest

region affect crop yield and Brazil replace the U.S. as the country's leading soybean producers in the

world.17

Cassava

Price of local cassava was fluctuating around 5,500 vnd and 6,000 vnd (0.26 usd and 0.28 usd) per kg

in 2013. At the end of 2013, price of cassava chips decreased to fluctuate around 5,000 vnd. The

following graph from Agromonitor is summarizing the price of cassava chips in the last 2 years.

17

Agro Info, www.agro.gov.vn, Nov 2013

Animal Feed Industry in Vietnam 24

Figure 17 Procurement prices of cassava chips in Vietnam, 2012 to 2014. Source: Agromonitor

Rice bran

The following graph summarizes the price of rice bran at warehouses in the last 10 months in Kien

Giang and An Giang Province in Mekong Delta.

Figure 18 Price of rice bran at warehouses in The Mekong Delta (VND/kg). Source: Agromonitor

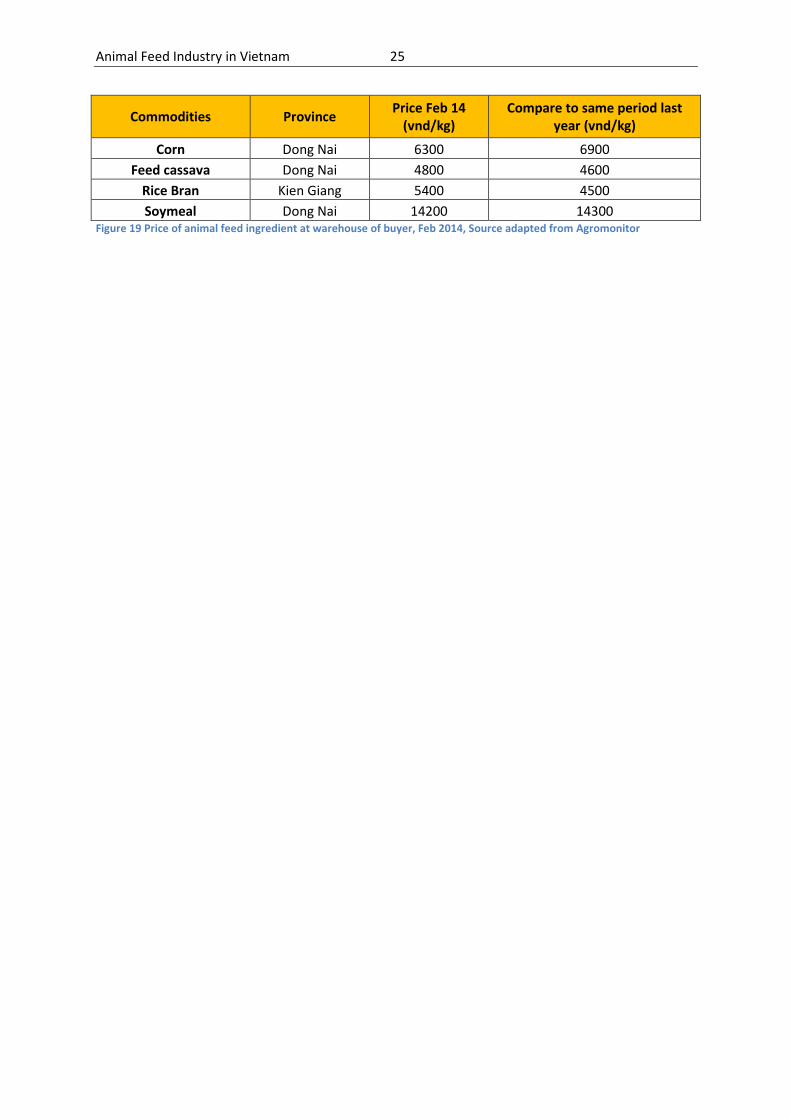

Finally the following table summarizes the different price of main raw material used in animal feed I

Vietnam

Vn

d /

kg

Animal Feed Industry in Vietnam 25

Commodities Province Price Feb 14

(vnd/kg)

Compare to same period last

year (vnd/kg)

Corn Dong Nai 6300 6900

Feed cassava Dong Nai 4800 4600

Rice Bran Kien Giang 5400 4500

Soymeal Dong Nai 14200 14300 Figure 19 Price of animal feed ingredient at warehouse of buyer, Feb 2014, Source adapted from Agromonitor

2. PRESENTATION OF THE SECTOR

2.1. Presentation of the animal feed value chain in Vietnam.

Agriculture sector in Vietam is very strong representing 18.4% of GDP. Livestock industry is

representing 20% of agriculture GDP, being a major contributor of the revenue of the sector with

over US$6 billion income. Within livestock production, pig production is the most important with

over 30 million animals produces every year. Vietnam is the 5th largest producer of pig in the world.

Demand for protein

Vietnam experienced GDP growth above 7% (5-year average), and GDP per capita growth of 8% (5-

year average). Domestic meat (pork, beef and poultry) consumption has increase by 7.5% CAGR over

the last 5 years, drive by increases in population and per capita meat consumption. This is

considered strong growth, compared to neighboring countries like China (1.7%), the Philippines

(1.0%) and Thailand (-0.1%).

Vietnamese are meat lovers: almost 4.5 million tons of meats have been consumed last year.

With 40 kg of meat per capita, Vietnam is approaching the world average meat consumption of 46.6

kg per person per year.

In 2013, Vietnam imported 90,000 tons of meat to face the shortage18. Such figure will not

decrease in the coming years as import is mainly due to disease outbreak and poor sanitary

condition in small farms. For the entire year, the total meat supply is estimated to be at 4.3 million

tons, an increase of 1.49% compared with 2012. In 2013, pork supply reached 3.2 million tons (up

1.8 per cent); poultry meat production reached 747,000 tons (sales rose 2.4 per cent- up slightly);

buffalo meat reached 85,300 tons (down 3.5 per cent); and beef reached 285,400 tons (down 2.9 per

cent) compared with 2012. Pork supply still represents about 74.4 per cent of the total meat supply

in Viet Nam.19

Poultry and eggs industry is growing very fast. Today 500 million poultries and 5.5 billion eggs are

produce yearly. The dairy industry is becoming a major industry of the agro sector with 220% growth

in volume in the last 10 years20.

With an expected 50% increase in meat production over the next 10 years, traditional

farming and production system will no longer be suitable to feed the country. Solutions will have to be found to address this massive volume increase, feed 100 million people in 2020 and answer consumers’ escalating expectations in both quality and quantity.

18

Source: http://www.agroviet.gov.vn/ 19

Source: http://english.thesaigontimes.vn/ 20

Source: interview with industry experts

Animal Feed Industry in Vietnam 27

This fragmented structure impact the feed industry as it is difficult to distribute very small

amount of industrial feed to many farmers all over the country. Thus feed distributors are important

relay for the feed factories.

Today approximately 55% of pigs are fed with industrial feed. This represents very potential

growth drivers as the trends are intensification of the production.

The Ministry of Agriculture and Rural Development expects strong continues growth in protein

consumption, with per capita consumption to increase through 2020 as follow:

1. Meat – an increase from 36kg of meat in 2010 to 56kg by 2020

2. Eggs – an increase from 82 eggs in 2010 to 142 eggs by 2020

3. Milk – an increase from 4.3 kg milk in 2010 to 10 kg milk by 2020

To meet these expected requirements, the MARD has developed its “Livestock Development

Strategy” with a key focus of shifting livestock production towards industrial production by 2020.

Livestock production is projected to increase by an average of 6% though 2020, including

4. Meat production to increase from 3.2 million tons in 2010 to 7 million tons by 2020

5. Milk production to increase from 380,000 tons in 2010 to 1 million tons by 2020

6. Egg production to increase from 7 billion in 2010 to 14 billion in 2020

7. Pig population to increase from 27 million in 2010 to 35 million by 2020

8. Beef cattle population to increase 4.8% to 12.5 million heads by 2020.

Farming, the limiting factor to answer market demand

During the next ten years, to follow the meat and milk consumption trends, livestock production

will need to deliver tremendous growth. Pig production should rise by 55%, the poultry production

by 66%, the cattle production by 76% and the quantity of dairy cows by 244%21.

However the livestock industry in Vietnam is characterized by the atomization of the production.

More than 80% of farmers have land smaller that 2ha and have less than 20 animals. Issue related to

small farmers are: poor investment capacity to upgrade farms, high vulnerability to disease (poor

biosecurity measures in place), difficult access to specialist (technician, vet) leading to poor

performance and growth potential. In 2013, Vietnam was obliged to import 90,000 tons of meat, in

which poultry accounted for about 70% as national production was not sufficient to cover demand.

21

Source: MARD

Animal Feed Industry in Vietnam 28

However, farming in Vietnam has certain short-comings, which hinder a sustainable development of the livestock sector:

• The production is fragmented, 95% of farms are backyard with few animals per farm and poor facilities.

• Meat supply is not consistent, the quality is variable (frequent disease outbreak for example)

• There are frequent environmental scandals due to poor treatment facilities on farms.

• Small farms do not have the capability of increasing their output significantly.

Demand for feed

This expected growth in animal protein production and consumption, and the MARD’s push to move

livestock production towards greater industrialized farming, support strong growth in demand for

industrial feed.

Medium to large scale farmers usually use industrial feed to raise livestock (pigs, cows and poultry)

to ensure meat, milk and egg quality and reduce risk of disease. Smaller farmers will use industrial

feed in critical phases of livestock development (e.g. piglets, breeding pigs), but in other phases will

use other available ingredients like rice bran of cassava to produce self-made feed to save cost,

though such practices does not ensure healthy development of the livestock and does not guarantee

a good yield. The long-term trend for the livestock farming industry is toward larger scale,

industrialized farming to have better yield, which will increase demand for industrial feed. The

demand for feed is also subject to seasonality, with stronger demand in May, June, November,

December and January (the farmers increase farming activities to prepare for the Tet holidays)

Industrial feed production

Today 230 feed mills are in operation in Vietnam producing 13.5 million tons of feed, 5.7

million tons in the North and 7.8 million tons in the South. Out of these 230 companies, 60 are

foreign owned (including 44 wholly controlled by foreign companies and 16 in Joint Venture). These

60 companies control over 60% of market shares in 2013 (they were controlling 40% market share in

2011) while the 170 locals companies remaining hold approximately 40% market shares.

The Vietnamese animal feed industry is the one growing the fastest in the world. However, the

industry is covering only 55% of the national demand for animal feed. The remaining is covered by

home-made feed and imported feed. In 2020 Ministry of Agriculture and Rural Development expect

that the country will produce 20 million tons of industrial feed.

The capacity utilization ratio of all plants is approximately 66%. This low number results from

the fact that a number of smaller companies operate at low capacity utilization. The top feed

companies in Vietnam enjoy economies of scale to control costs and maintain good margins,

compared to smaller companies.

Animal Feed Industry in Vietnam 29

Typologies of feedmills

The sector is dominated by larges foreign own companies, with important investment capacity

and strong knowledge of the industry. Vietnamese feedmills are characterized by small production

capacity (between 50,000 tons and 80,000 tons), poor R&D capabilities and limited investment

capacities.

Foreign feedmills often have production capacity higher than 300,000 tons per years. Majority of

foreign own feedmill are planning to open new production facilities in 2014 or have open ones in

2012/2013. Foreigners are signing deals with international companies like professional genetic

suppliers, giving them an important competitive edge. The consequence is that the gap is growing

between local and foreign owned companies.

It is important to note that most of large feedmill are located in South Vietnam while smaller

one are based in North Vietnam. This is reflecting the farming structure of the country: large farms

are in the South while smaller one in the North.

In a report done by IPSARD and CAP gave a typology of feedmill that we would like to present:

The mills have been categorised in the following way in the analyses:

• small mills are those producing less than 10,000 tons per annum;

• medium mills are those producing from 10,000 to less than 60,000 tons per annum,

• Large mills are those producing 60,000 or more tons per annum.

It is important to note that such classification has been done according to production capacity and

not in term of incomes, number of staff or fixed assets.

Larger foreign rivals have access to cheaper commodity supplies. While domestic firms are struggling

to find sufficient local supply and have to depend on imported resources, foreign firms have cost

advantage from accessing cheaper sources globally. Cargill, for example, has facilities that span 66

countries. Its subsidiaries procure grain in Australia, soybean meal in Brazil and Argentina, cocoa in

Indonesia, palm oil in Malaysia and much more. The size of the firms and the nature of global trade

create high barriers of entry for newcomers, reinforcing the existing firms’ market power.

Trends and development

Vietnam is a rural country. The small size of farms characterizes the crop and livestock industry

structure. In such configuration, the growing demand for animal protein is not entirely covered by

the local production.

By definition, small farms are not intensive. As consequences, smallholders are vulnerable to

epidemic, cannot buffer strong feed price fluctuation and do not have access to specialize

knowledge like veterinary science.

This situation today reaches a paroxysm. With several diseases outbreaks and price fluctuation

in the last 5 years, Vietnam livestock industry witnessed the bankrupt of the smallest farm. On the

other side, large intensive and integrated farms were able to protect from disease outbreak thanks

Animal Feed Industry in Vietnam 30

to proper biosecurity and were also able to buffer price fluctuation thanks to strong cash flow

and/or access to credit. In addition, with large volume produced regularly, large farms are more

interesting for the market as they can deliver regularly with stable quality

Thus, development of large integrated farms seems to be the future of Vietnam agriculture as it

was a compulsory step in the development of occidental’s countries. CP Group understood it 15

years ago and started their vertical integration in their livestock business.

The consequences for Animal Feed industry is that, in the near future, the core customer will be

more and more large intensive farms while the ratio of small farms will decrease dramatically.

Then growth drivers for the feed industry will be triple:

• Absolute growth of the market: more animals will be reared in Vietnam, increasing the

volume of industrial feed consumed.

• More and more small and medium size farm will stop the to produce inefficient

homemade feed and will switch to a larger proportion of industrial feed

• The numbers of small farms will decrease because of the development of efficient,

profitable and more flexible large intensive farms.

These trends would have to be considered in the strategy of the animal feed industry in Vietnam.

The following two graphs adapted from the report 2020 Livestock Industry Development Strategy

from MARD shows that demand of industrial feed is not sufficient today and will certainly not be

sufficient in the coming years.

Figure 20 Supply VS demand of industrial feed during 2010's and ratio of industrial feed, self-made feed and import feed

during the 2010's. Source: MARD

Many competitors, foreign firms enjoy economies of scale. The good prospect of the domestic

animal feed sector has attracted huge interest from foreign firms. With newer technology in

breeding, feeding, and housing of livestock, foreign firms typically build large-scale operations that

result in economies of scale and lower production cost. In contrast, local firms are relatively small in

Animal Feed Industry in Vietnam 31

terms of production capacity. Among the seven biggest animal feed producers, six are foreign firms

or foreign-invested enterprises.

Pricing power in the hands of “Big Four”: In developed countries such as the US and Canada, animal

feed accounts for 50-55% of the cost of pork. In Vietnam, it is near 75% - underscoring the impact of

animal feed price fluctuations on livestock breeding. With 30% market share combined, the foreign

“Big Four” firms (CP, Proconco, East Hope and Cargill), have enough pricing power to fully pass

through increase in input costs. Other smaller, domestic producers like Dabaco, can generally follow

the Big Four’s pricing but are only able to pass through about three-quarters of the price increase.

This explains the stable gross margins in the domestic animal feed industry.

As example, during first part of 2012, animal feed producers were able to protect margin by

increasing prices by 10% while farmers have had to sell pork below cost at VND37,000-38,000/kg

(the total cost to raise one pig is up to VND41,000/kg).

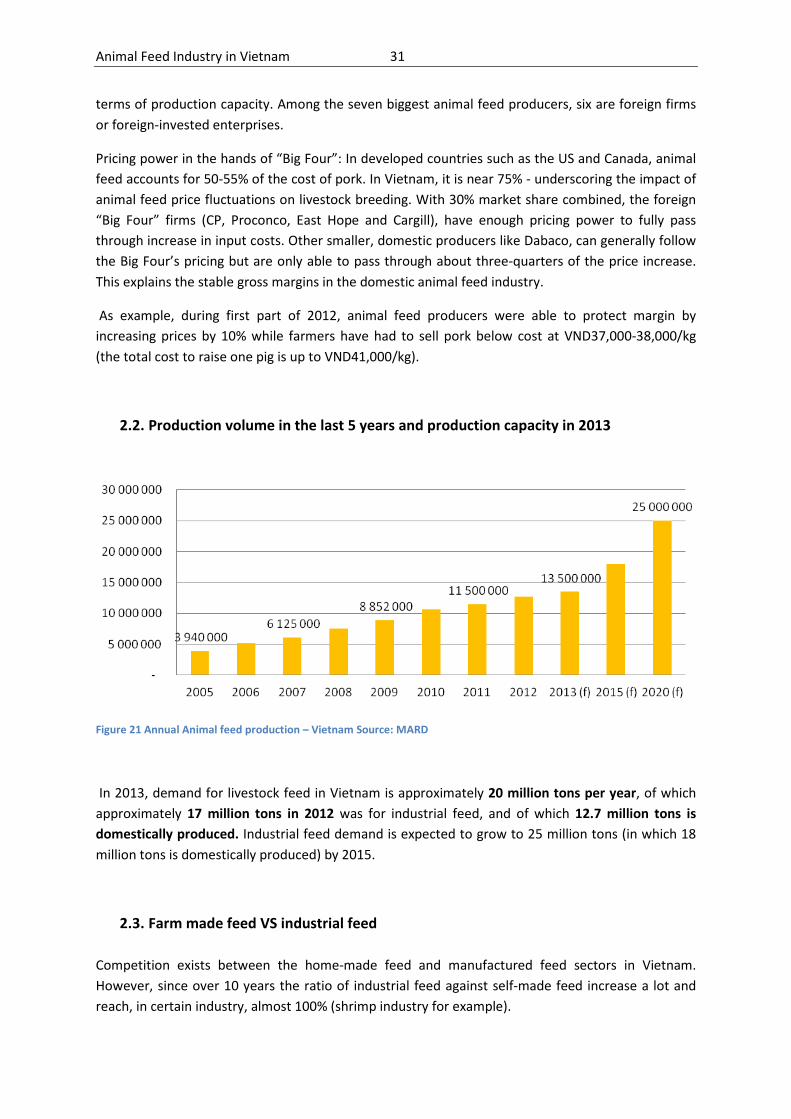

2.2. Production volume in the last 5 years and production capacity in 2013

Figure 21 Annual Animal feed production – Vietnam Source: MARD

In 2013, demand for livestock feed in Vietnam is approximately 20 million tons per year, of which

approximately 17 million tons in 2012 was for industrial feed, and of which 12.7 million tons is

domestically produced. Industrial feed demand is expected to grow to 25 million tons (in which 18

million tons is domestically produced) by 2015.

2.3. Farm made feed VS industrial feed

Competition exists between the home-made feed and manufactured feed sectors in Vietnam.

However, since over 10 years the ratio of industrial feed against self-made feed increase a lot and

reach, in certain industry, almost 100% (shrimp industry for example).

Animal Feed Industry in Vietnam 32

In the pig industry such ratio is lower as a lot of pig farm in the North are still using local rice bran

and kitchen garbage to feed their animals. When animals reach sensitive phase (early age and

reproduction) often farmers buy industrial feed in order to supply all necessary nutrient and amino

acids to ensure good performance of animals.

In general self-made feed rarely provide all necessary nutrient for optimum growth of animals. Then

yield of herd fed with farm-made feed in almost always inferior to industrially raised animals.

However it would be interesting to go deeper in the reflexion and study the profit made by farmers

using self-made feed and industrial feed considering financial capacity to engage in the second

option and risk that goes along.

The following graph show that during the 2010’s the proportion of industrial feed should increase

from 56% in 2010 to approx 70% in 2020 while imported feed should decrease from 30% in 2010 to

18% in 2020. Home-made feed should remain almost stable and should decrease from 14% in 2010

to 12% in 2020.

Figure 22 ratio of industrial and self-made feed and import feed during the 2010's. Source: MARD

However, if we consider volume produced in such period we would have the following volume of

self-made feed22:

• 2010 = 1.5 million tons of self-made feed

• 2015 = 2.3 million tons of self-made feed

• 2020 = 3 million tons of self-made feed.

3. PRESENTATION OF ACTORS INVOLVED

3.1. Listing of the existing producers or animal feed (aqua and livestock feed)

22

Source: Industry Experts

Animal Feed Industry in Vietnam 33

As mentioned, the Vietnamese industrial animal feed industry is dominated by foreign owned

factory. The top 5 companies in the country are covering more than 45% of total production of

industrial feed. CP, Proconco, Cargill, East hope and ANT are leading the livestock feed industry in

Vietnam. Only Proconco is a national company, others are foreigners.

Figure 23 Market share repartition in animal feed industry in Vietnam, 2012 Source: discussion with industry experts

Foreign companies are the only able to integrated the value chain of livestock industry. Vietnamese Companies are representing only few percent of the animal feed industry in Vietnam. The trend is that local companies with low production capacity will slowly disappear in the coming years. The reasons are multiple:

• Most of farmers are asking for credit and small feed mills do not have financial capacities to allow such credit policy. Then farmers are more likely to buy directly from large (and foreign own) Companies. For example, a farm of 500 sows will often asked for 1 month credit representing 1 billion vnd (approx 50,000 usd)

• In the case of the poultry industry, the industry is very much vertically integrated, meaning that large poultry producers are in reality the feeders. CP and Japfa are leading the market. That means that the feed market for poultry is limited as CP and Japfa are consuming their own feeds. Such captive market is strengthening even more the position of foreign owned feed mills. In addition to feed, these integrators also produce their own juveniles.

• Often small feed mills do not have strategic long term vision of their business. They do not have investment capacity and then cannot really impact their long term development: they are actually undergoing their development, linked to the development of large companies. Very limited R&D programs are launched by smaller companies and formulation of feed is not often very up to date.

Animal Feed Industry in Vietnam 34

• Margins in animal feed industry are very high compare to margins in Europe. Discussion with industry professional lead to the following figures: 2% net margin in Europe (in average) while in Vietnam Companies are often doing 5% to 7% net margin. This has double effect

o Large international group are very attracted by such remunerative market and invest massively in the country (Nutreco, Deheus, Cargill or Tequ Group are acquiring existing feed mills in the last years). These large companies have lot of financial resources and can invest into long term effort (R&D, Marketing, credit, etc.)

o Feed millers are “killing their clients” with very high price for feed. Feed in Vietnam is known to be 20% higher than neighboring countries. This is also due to the fact that companies are keeping high margin to satisfy shareholders expectation.

• Management capacities are limited in Vietnam. There is not many education in the field of animal nutrition in Vietnam, and technician are often learning by doing without proper theoretical approach. As example, many small feedmills are not really and regularly calculating their production cost or efficiency to produce their feed. In parallel, formulation matrix not being up to date, does not allow formulation department to quick adapt their formula (without hampering efficiency and quality of feed) and then do not optimize the cost of production.

So in summary the small local feedmill does not really have chance to develop their business and if no massive investment are done on production tools and long term actions (R&D, training, Credit) these small companies will slowly disappear, certainly bought back by large international feed mills. The following part provides a non exhaustive list of active feedmill in Vietnam. We decided to present it according to their origin, either local companies or foreign owned23:

Foreign invested feed manufacturers

• Charoen Pokphand CP (Thailand): has invested in VN since 1993 with 8 feedmills

countrywide (5 animal feed plants and 3 aquafeed plants). CP Vietnam is engaged in

providing seeds; feed, aqua-farming, breeds of pigs, chicken, equipment for livestock

and aqua-farming, and food processing.

• Cargill (US): has invested in VN since 1995 with 6 factories supplying

approximately 750’000 tons a years (5 animal feed plants and 1 aquafeed plants).

• Anova (EWOS Norway): has entered the VN market since 2010 in the area of feed for

fishes.

• De Heus started with its first factory Dong Nai province, 2008. By now, DH has

countrywide 3 factories for livestock feed and 1 for fishes.

• Uni-President Enterprise (Taiwanese backed) opened its third plant in 2011

manufacturing 258’000 tons of feed for animals.

So far, foreign companies supplying breeds (Chicken, pigs or shrimps) are Japfa, CP Vietnam

(Thailand) and Emivest

Vietnamese important feed producers

23

Source: Swiss Business Hub ASEAN / Vietnam Office, Mar 2012

Animal Feed Industry in Vietnam 35

• Proconco – founded in 1992 by French SCPA Company, Proconco used ot be market

leader (with up to 60% market share) till mid 2000’s. With 5 factories producing up to

1.2 million tons, Proconco is the second leading companies in Vietnam behind CPV.

• VIC Company – Golden Pig Ltd: is established in 1999 in Hai Phong province. Now, the

company has 4 manufacturing factories country-wide.

• Dabaco is established in 2004 and has two factories in Bac Ninh province with a total

capacity of 290’000 tons of feeds a year.

• Quang Dung Company is established in 1999 in Ho Chi Minh City. The company

specializes in feed related distribution and logistics. The company is a local partner of

Bunge Agri Business.

• Quang Minh Corporation is established in 2002 in Hanoi. It has now 4 manufacturing

factories in 4 Northern provinces.

• Viet Thang feed joint Stock Company is established in 2002 in Dong Thap, Southern of

Vietnam. The company has 7 factories in the South with a total capacity of 290’000 tons

a year.

• Vasa feed Joint Stock Company is established since 1985 in Ho Chi Minh City, South of

Vietnam.

• Vietland Joint Stock Company is established since 2008 in Bac Giang province,

North of Vietnam. The company has a capacity of 70’000 tons a year.

• Hong Ha Nutrition Joint Stock Co inaugurated an advanced animal feed production line

at the beginning of 2012 to produce 400’000 tons per year, becoming the largest feed

manufacturer in Viet Nam. The factory is located Dong Van Industrial Zone, Duy Tien

District, in the northern Ha Nam Province.

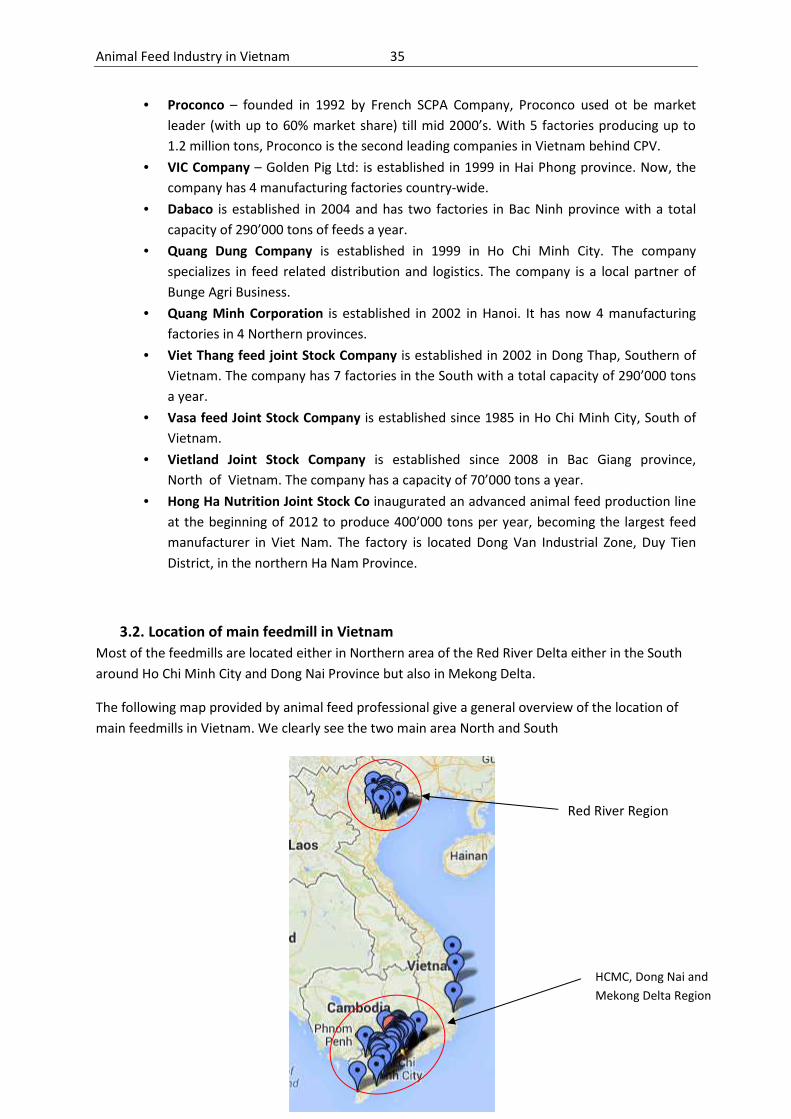

3.2. Location of main feedmill in Vietnam

Most of the feedmills are located either in Northern area of the Red River Delta either in the South

around Ho Chi Minh City and Dong Nai Province but also in Mekong Delta.

The following map provided by animal feed professional give a general overview of the location of

main feedmills in Vietnam. We clearly see the two main area North and South

HCMC, Dong Nai and

Mekong Delta Region

Red River Region

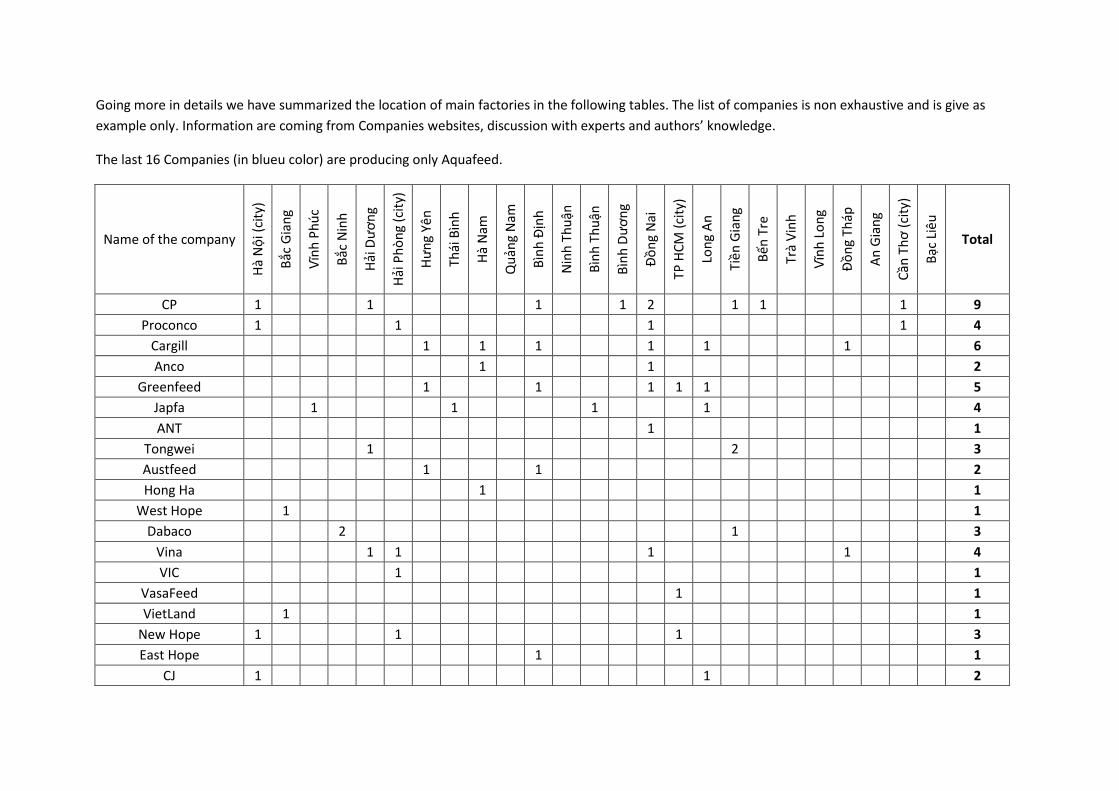

Going more in details we have summarized the location of main factories in the following tables. The list of companies is non exhaustive and is give as

example only. Information are coming from Companies websites, discussion with experts and authors’ knowledge.

The last 16 Companies (in blueu color) are producing only Aquafeed.

Name of the company

Hà

Nộ

i (ci

ty)

Bắc

Gia

ng

Vĩn

h P

hú

c

Bắc

Nin

h

Hải

Dư

ơn

g

Hải

Ph

òn

g (c

ity)

Hư

ng

Yên

Thái

Bìn

h

Hà

Nam

Qu

ảng

Nam

Bìn

h Đ

ịnh

Nin

h T

hu

ận

Bìn

h T

hu

ận

Bìn

h D

ươ

ng

Đồ

ng

Nai

TP H

CM

(ci

ty)

Lon

g A

n

Tiề

n G

ian

g

Bế

n T

re

Trà

Vin

h

Vĩn

h L

on

g

Đồ

ng

Tháp

An

Gia

ng

Cần

Th

ơ (

city

)

Bạc

Liê

u

Total

CP 1 1 1 1 2 1 1 1 9

Proconco 1 1 1 1 4

Cargill 1 1 1 1 1 1 6

Anco 1 1 2

Greenfeed 1 1 1 1 1 5

Japfa 1 1 1 1 4

ANT 1 1

Tongwei 1 2 3

Austfeed 1 1 2

Hong Ha 1 1

West Hope 1 1

Dabaco 2 1 3

Vina 1 1 1 1 4

VIC 1 1

VasaFeed 1 1

VietLand 1 1

New Hope 1 1 1 3

East Hope 1 1

CJ 1 1 2

Animal Feed Industry in Vietnam 37

Evialis 1 1 3 1 6

DeHeus 1 1 1 1 4

Sojitz 1 1

Viet Thang 2 2

Emivest 1 1 2

RTD 1 1

VIFOCO 1 1

THANH LOI 1 1

Quang Dung 1 1

Quang Minh 1 1

Lai Thieu 1 1

Skretting 1 1

Tan Loc 1 1

Domyfeed 1 1

Hung Vuong 1 1

Vinh Hoan 1 1

EWOS 1 1

Travifaco 1 1

Blue Star 1 1

Grobest 1 1

CL Pangafish 1 1

Dong Thap Seprimex 1 1

Dagrimex 1 1

An Giang AFIEX 1 1

Hoang Long 1 1

UP 1 1 1 1 4

Go Dang 1 1

TRAVIFACO 1 1

TOTAL 5 2 1 2 3 5 4 2 4 1 5 1 1 9 12 6 5 5 1 2 2 12 1 3 1 95

3.3. Presentation of the top 5 producers

The domestic industrial feed industry is currently dominated by foreign owned feed manufacturers.

The top 5 companies in terms of market share include 4 foreign owned companies: CP Vietnam,

Proconco, Cargill Vietnam, East Hope Vietnam, ANT (Dachan) with a combined market share of over

35%. Some companies such as CP Vietnam and Japfa have already established an integrated value

chain from breeding to farming and processing.

Economies of scale provide a high barrier of entry into the industry. Large Companies, including

Proconco, have established market shares, brand names and large existing production capacity.

These companies can achieve favorable conditions in material purchasing thanks to their larger

order and stronger financial capacity to stock materials during off-seasons, when prices are usually

lower thanks to abundant supply.

Information mentioned in the following part are coming from companies website and industry

experts.

1. Charoen Pokphand (CP)

CP Vietnam currently operates five animal feed plants, three aqua feed mills, with a total capacity of

3.8 million tons per year (2.3 million tons for livestock and 1.5 million tons for aquafeed) making it

the biggest feed miller in Vietnam with a 19% market share. CPV has approximately 1,300 dealers for

the distribution of feed products. The company also accounts for 22% of white-feather chicken, 7%

of pigs and 16% of the egg market in Vietnam (with figure as follow 250.000 sows, 3,8 million hens,

4,5 million chickens)

CPV operates about 3,000 farms, including shrimp farms,

shrimp hatcheries, fish farms and livestock farms, most of which

are contracted operations.

CP Vietnam Livestock Corporation targets to increase its

herd size to 350,000 sows in 2015 to meet a growing demand for

pork in Vietnam,

CPV distributes its products through both traditional

channels, such as wet markets, as well as modern channels, such

as supermarkets. The Company owns the CP Fresh Mart chain and

already opened over 70 of these convenient stores within

Vietnam. The company’s aquatic food products are exported

primarily to overseas markets such as European Union, Japan and

other Asian countries.

Figure 24 CPV feedmills location in

Vietnam, Source CP Hong Kong

Animal Feed Industry in Vietnam 39

2. Cargill:

In February 1995, Cargill established its presence in Vietnam with the

opening of their first representative offices in Hanoi and Ho Chi Minh

City. In October 1997, Cargill Vietnam Limited was formed. In

December 2009, they were the first U.S. Company to obtain a

distribution license in Vietnam, allowing them to distribute products directly in the country. Cargill

Vietnam employs over 900 employees across 15 locations. Their operations include premix, animal

nutrition, cocoa production, food and beverage ingredients, grain and oilseed trading and marketing,

and metals trading.

• Animal Nutrition: They are one of the leading animal nutrition Companies in Vietnam,

producing premix and compound feed. They own and operate one premix plant and eight

feed mills in Can Tho, Tien Giang, Long An, Dong Thap, Bien Hoa, Binh Dinh, Hung Yen and

Ha Nam. They have over 770,000 tons capacity.

• Grain and Oilseeds They supply soybean meal, wheat, sugar, corn, copra meal, canola and

soybeans. Their customers include animal feed producers, poultry and hog raisers,

integrated fish processors, flour millers, and food and beverage manufacturers.

• Animal Protein They import a range of cooked chicken products into Vietnam from their

poultry processing business in Thailand, where they maintain a fully integrated supply chain

to ensure food safety and quality products.

Recent Investments

2012 Cargill began expansion of its Binh Dinh feed plant. The plant is expected to be completed by

2014

2012 Cargill opened a feed mill in the Ha Nam Province, its eighth in Vietnam

2012 Cargill expanded its Hung Yen facility with the addition of an aquaculture feed processing

plant

2011 Cargill acquired its first shrimp feed mill in Vietnam (the former Higashimaru Feedmill)

2011 Cargill acquired Provimi Vietnam (Premix manufacturer)

PROCONCO

Proconco was established in 1991 as a JV between “Société Commerciale des

Potasses et de l’Azote” SCPA and a group of Vietnamese SOE. Proconco has

grown its production capacity from one factory in Dong Nai Province built in

1992, to its current five plants nationwide, in Bien Hoa, Hai Phong, Can Tho, Long

Chau and Hanoi. Proconco has a total annual production capacity of 1.2 million

tons (950,000 tons for livestock feed and 250,000 tons for aquafeed).

Animal Feed Industry in Vietnam 40

Today the company is ranked 47th largest feed mill in the world, ranked 96th largest enterprises

in Vietnam and has been awarded best feed miller in Asia in 2010 by Asian Feed magazine.

Proconco’s main business is in livestock and aqua feed production. Feed is sold to individual and

industrial farms all over Vietnam. 90% of total sales are generated through distributors while only

10% are directly sold - to large industrial farmers. The Company sells on a cash basis to more than

600 distributors nationwide.

Proconco managed in the 20 years of its existence to impose its brand “conco” as one of the

most recognized by farmers in Vietnam. The famous “Cảm ơn Conco” jingle (or “Thanks Conco”) is

very well known in Vietnam countryside.

In October 2012, Masan Consumer, one of Vietnam’s largest diversified consumer companies,

announced that it acquired 40% of the shares of Proconco reinforcing the Vietnamese ownership of

the Company. Proconco is the only large Vietnamese feed producers.

GREENFEED

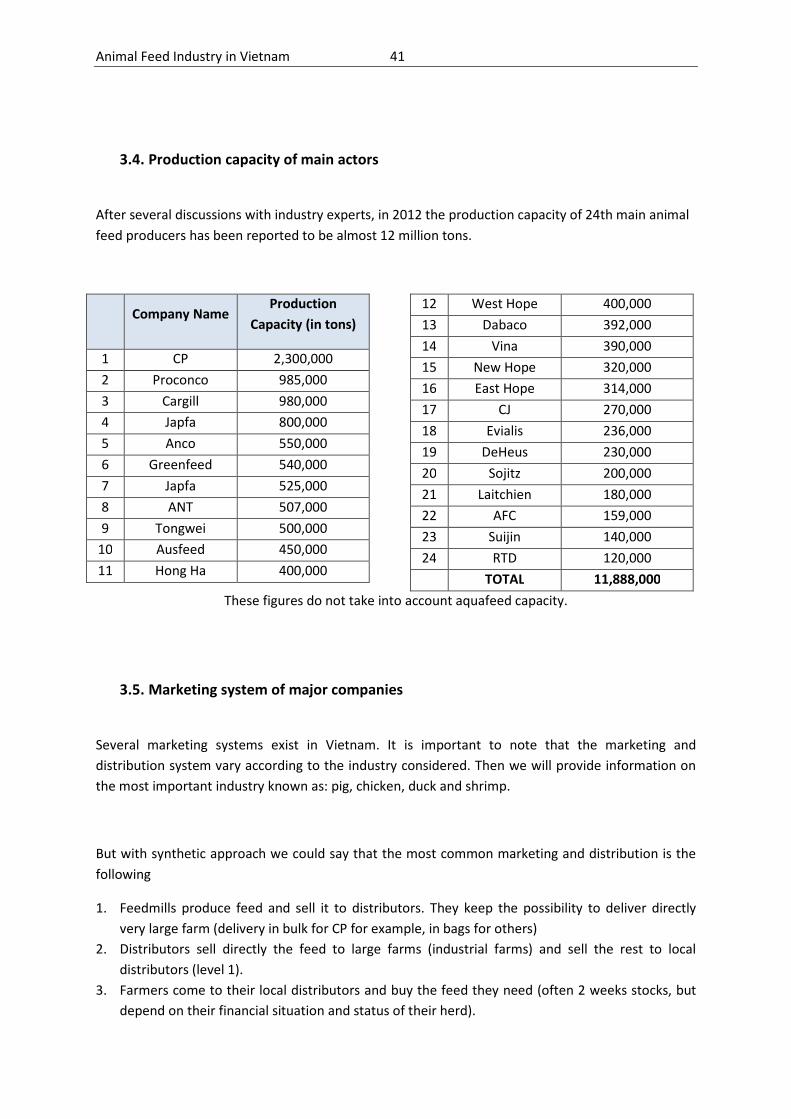

Greenfeed has been established in 2003 and is

now the number six feedmill in Vietnam with 5

factories and 540,000 tons production capacity (pig,

chicken and fish feed mainly) and about 5% market

share. Factories are located in HCMC, Long An, Hung

Yen, Binh Dinh and Dong Nai Province. In addition,

Greenfeed built a feedmill in Cambodia in Kampong

Cham in 2008.

Apart from these feed factories Greenfeed has

built branch network throughout the region from

north to south. The goal is to facilitate the delivery

system in order to be is fast and convenient.

The Company has one of the strongest

management team of the industry as well as a

leading position on raw material procurement,

technology and products quality. Greenfeed

currently has more than 2,000 dealers throughout 64

provinces in the territory of Vietnam and some

provinces in Cambodia and Laos.

Greenfeed has decided few years ago to integrate its business and to launch pig genetic

activities in collaboration with a world leader genetic supplier; PIC a US based pig genetic

company. Today with 3 reproduction farms the Company is steadily gaining market shares.

Similarly, Greenfeed has developed fish genetic activities and own 2 reproduction farms in

Mekong Delta. They are working on the pangasius reproduction.

Figure 25 Location of Greenfeed factories and

branch, Source: Greenfeed Co

Animal Feed Industry in Vietnam 41

3.4. Production capacity of main actors

After several discussions with industry experts, in 2012 the production capacity of 24th main animal

feed producers has been reported to be almost 12 million tons.

Company Name

Production

Capacity (in tons)

1 CP 2,300,000

2 Proconco 985,000

3 Cargill 980,000

4 Japfa 800,000

5 Anco 550,000

6 Greenfeed 540,000

7 Japfa 525,000

8 ANT 507,000

9 Tongwei 500,000

10 Ausfeed 450,000

11 Hong Ha 400,000

12 West Hope 400,000

13 Dabaco 392,000

14 Vina 390,000

15 New Hope 320,000

16 East Hope 314,000

17 CJ 270,000

18 Evialis 236,000

19 DeHeus 230,000

20 Sojitz 200,000

21 Laitchien 180,000

22 AFC 159,000

23 Suijin 140,000

24 RTD 120,000

TOTAL 11,888,000

These figures do not take into account aquafeed capacity.

3.5. Marketing system of major companies

Several marketing systems exist in Vietnam. It is important to note that the marketing and

distribution system vary according to the industry considered. Then we will provide information on

the most important industry known as: pig, chicken, duck and shrimp.

But with synthetic approach we could say that the most common marketing and distribution is the

following

1. Feedmills produce feed and sell it to distributors. They keep the possibility to deliver directly

very large farm (delivery in bulk for CP for example, in bags for others)

2. Distributors sell directly the feed to large farms (industrial farms) and sell the rest to local

distributors (level 1).

3. Farmers come to their local distributors and buy the feed they need (often 2 weeks stocks, but

depend on their financial situation and status of their herd).

Animal Feed Industry in Vietnam 42

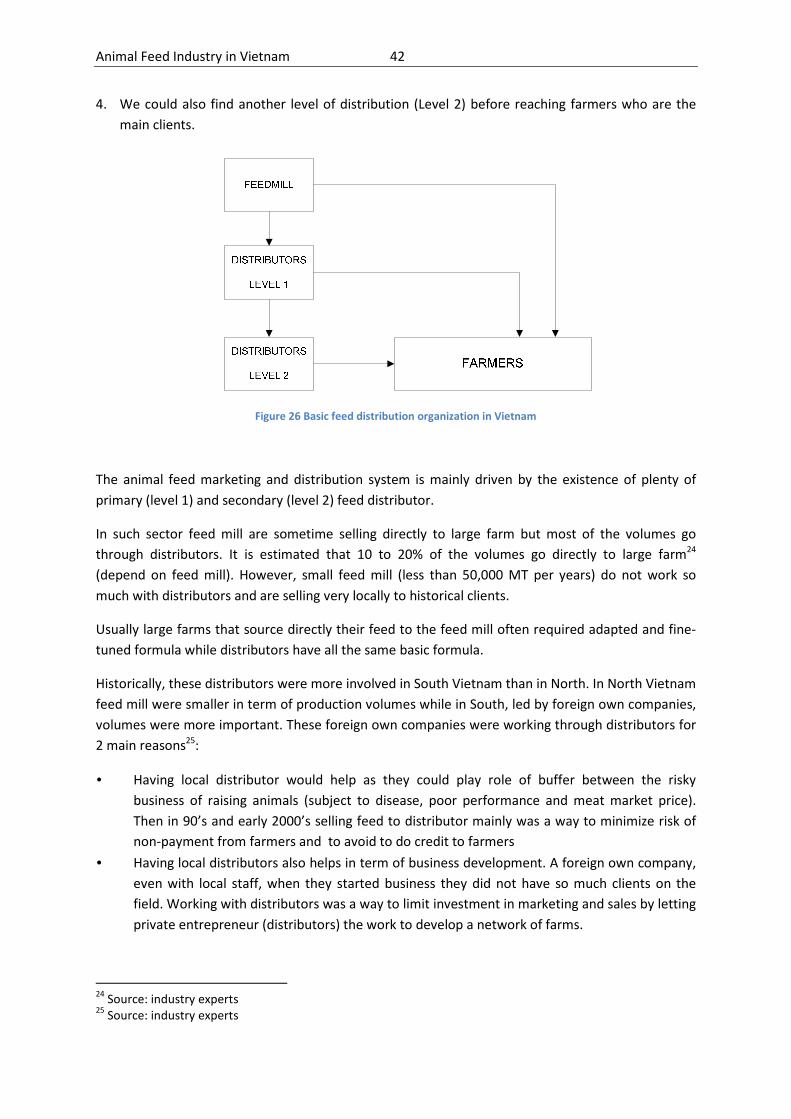

4. We could also find another level of distribution (Level 2) before reaching farmers who are the

main clients.

Figure 26 Basic feed distribution organization in Vietnam

The animal feed marketing and distribution system is mainly driven by the existence of plenty of

primary (level 1) and secondary (level 2) feed distributor.

In such sector feed mill are sometime selling directly to large farm but most of the volumes go

through distributors. It is estimated that 10 to 20% of the volumes go directly to large farm24

(depend on feed mill). However, small feed mill (less than 50,000 MT per years) do not work so

much with distributors and are selling very locally to historical clients.

Usually large farms that source directly their feed to the feed mill often required adapted and fine-

tuned formula while distributors have all the same basic formula.

Historically, these distributors were more involved in South Vietnam than in North. In North Vietnam

feed mill were smaller in term of production volumes while in South, led by foreign own companies,

volumes were more important. These foreign own companies were working through distributors for

2 main reasons25:

• Having local distributor would help as they could play role of buffer between the risky