The Rising Tide of OTC in Europe Presentation at OTC Conference: “The Enlightened and Well-Informed Consumer” Andy Tisman Senior Principal Consumer Health, IMS Health, Oslo February 2013

Andy tisman how_is_the_otc_market_developing

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Rising Tide of OTC in Europe Presentation at OTC Conference: “The Enlightened and Well-Informed Consumer”

Andy Tisman Senior Principal Consumer Health, IMS Health, Oslo February 2013

Norway OTC Conference - February 2013

Agenda

• World OTC Context

• Growth Drivers in Europe

• Bringing OTC closer to the consumer

• Focus on the sufferer/consumer and building trust through brands

• Evolution of distribution

• Rx/OTC Switches

• Implications for OTC

2

Norway OTC Conference - February 2013 3

Yes, we do get snow in London too... (...but not as often!)

Norway OTC Conference - February 2013

Definitions - Rx-bound, Semi-ethical OTC & Self-Medication

Non Rx-Bound (“total OTC”) Rx-Bound *

Self-Medication includes

registered and unregistered products

Bought with

Prescription

Bought without

Prescription

Self-Medication

* Prescription (Rx) necessary by law to receive product

Semi-ethical

4

Norway OTC Conference - February 2013

Basis for Figures in this presentation

5

• Annual sales to end Q3 2012

• Sales at manufacturer prices

• Growths based on previous years to Q3

• Growths use latest exchange rate across all time periods

• Local currency growth aggregated into Euros

• Some qualifications

• UK data does not include mass market

• Sweden data does not include non-pharmacy sales

• China data is China hospital, excludes retail; USA data excludes Wal-Mart

• Companies include all OTCs from the corporation

• i.e. “Novartis” includes Hexal, Sandoz, LEK, etc

Norway OTC Conference - February 2013

Agenda

• World OTC Context

• Growth Drivers in Europe

• Bringing OTC closer to the consumer

• Focus on the sufferer/consumer and building trust through brands

• Evolution of distribution

• Rx/OTC Switches

• Implications for OTC

6

11.1

8.2

9.4

7.3

6.46.8

5.25.5

6.2

4.6

3.3

2.2

3.3

4.2

6.0

4.6

5.4

6.37.0 7.0 6.9

4.6

12.2%11.6%

11.1% 10.9% 10.7% 10.6% 10.7% 10.9% 10.9% 11.2% 11.3%

0%

2%

4%

6%

8%

10%

12%

14%

0

2

4

6

8

10

12

14

16

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Valu

e G

row

th (

%)

Year on Year Value Growth & OTC Share of Total PharmaMAT Q3 2012

Total Pharma Total OTC OTC Share of Total Pharma

Total Pharma = €740Total OTC = €84

Norway OTC Conference - February 2013 7

Although growth has fallen in the latest year, OTC continues the recent trend of outgrowing Pharma.

Source: IMS OTC Global Analysis

*

* - NB. Trend break due to change in estimation methodology

While Pharma growth experiences a number of constraints, OTC benefits from a range of growth drivers.

Norway OTC Conference - February 2013 8

Top Corps contribution to growth falling rapidly

Low number and quality output from R&D

Generics dominating large therapy areas

Demand constrained by payers

Key players building strong brand identities

Payers keen to promote self medication

Emerging markets have the critical mass to influence growth

Companies seek to exploit switch opportunities

Increasing access through new channels

PHARMA

OTC

Norway OTC Conference - February 2013 9

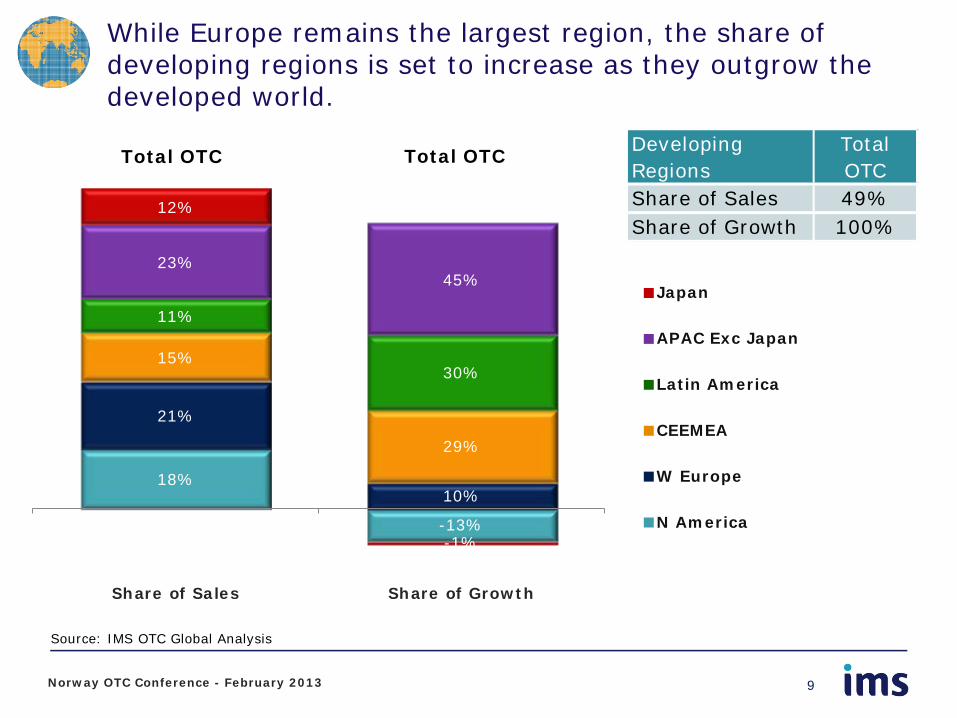

Source: IMS OTC Global Analysis

Japan

APAC Exc Japan

Latin America

CEEMEA

W Europe

N America

Total OTC Total OTC

18%

-13%

21%

10%

15%

29%

11%

30%

23%45%

12%

-1%

Share of Sales Share of Growth

Developing Regions

Total OTC

Share of Sales 49%Share of Growth 100%

While Europe remains the largest region, the share of developing regions is set to increase as they outgrow the developed world.

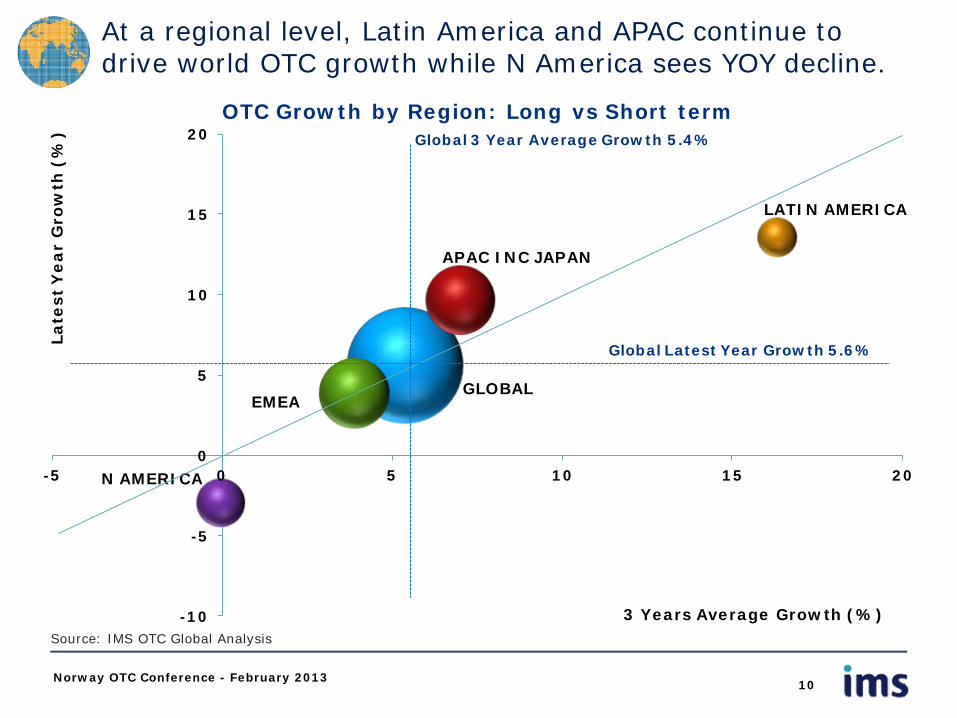

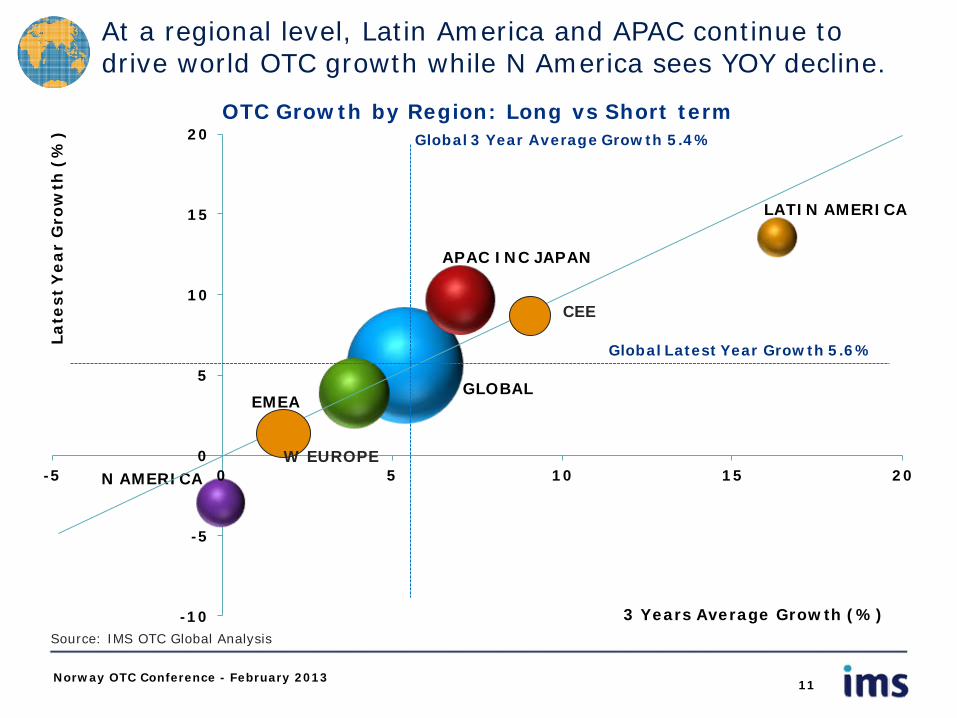

EMEA

APAC INC JAPAN

N AMERICA

LATIN AMERICA

GLOBAL

-10

-5

0

5

10

15

20

-5 0 5 10 15 20

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Region: Long vs Short term

Global Latest Year Growth 5.6%

Global 3 Year Average Growth 5.4%

At a regional level, Latin America and APAC continue to drive world OTC growth while N America sees YOY decline.

10 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

EMEA

APAC INC JAPAN

N AMERICA

LATIN AMERICA

GLOBAL

-10

-5

0

5

10

15

20

-5 0 5 10 15 20

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Region: Long vs Short term

Global Latest Year Growth 5.6%

Global 3 Year Average Growth 5.4%

At a regional level, Latin America and APAC continue to drive world OTC growth while N America sees YOY decline.

11 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

W EUROPE

CEE

Developed markets must innovate to drive growth while developing countries also enjoy underlying base sales growth.

Base Value Change

Price Change

New Products

Line Extensions

Total Change

Base Value Change

Price Change

New Products

Line Extensions

Total Change

Global W Europe N America

CEE L America APAC exc Japan

12 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

Elements of Growth by Region – 5 Year Cumulative Growth %

38

7

19

12

-1

5

6

12

4

-18

10

-7

15

11

-10

80

15

27

36

2

91

16

22

38

15

119

18

41

5

54

Norway OTC Conference - February 2013

Agenda

• World OTC Context

• Growth Drivers in Europe

• Bringing OTC closer to the consumer

• Focus on the sufferer/consumer and building trust through brands

• Evolution of distribution

• Rx/OTC Switches

• Implications for OTC

13

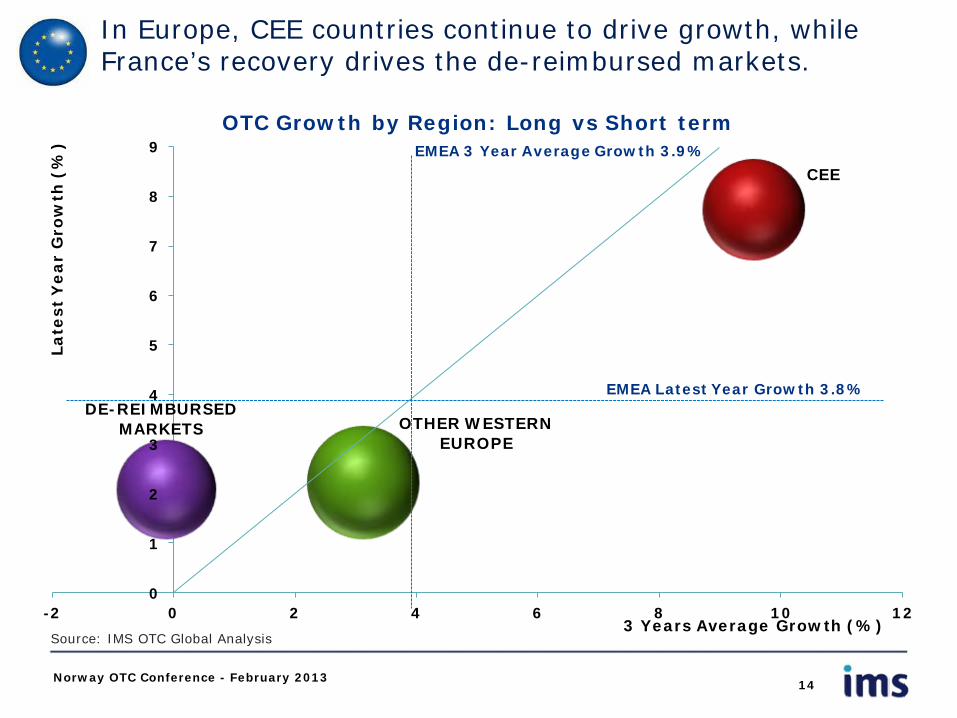

OTHER WESTERN EUROPE

CEE

DE-REIMBURSED MARKETS

0

1

2

3

4

5

6

7

8

9

-2 0 2 4 6 8 10 12

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Region: Long vs Short term

EMEA Latest Year Growth 3.8%

EMEA 3 Year Average Growth 3.9%

In Europe, CEE countries continue to drive growth, while France’s recovery drives the de-reimbursed markets.

14 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

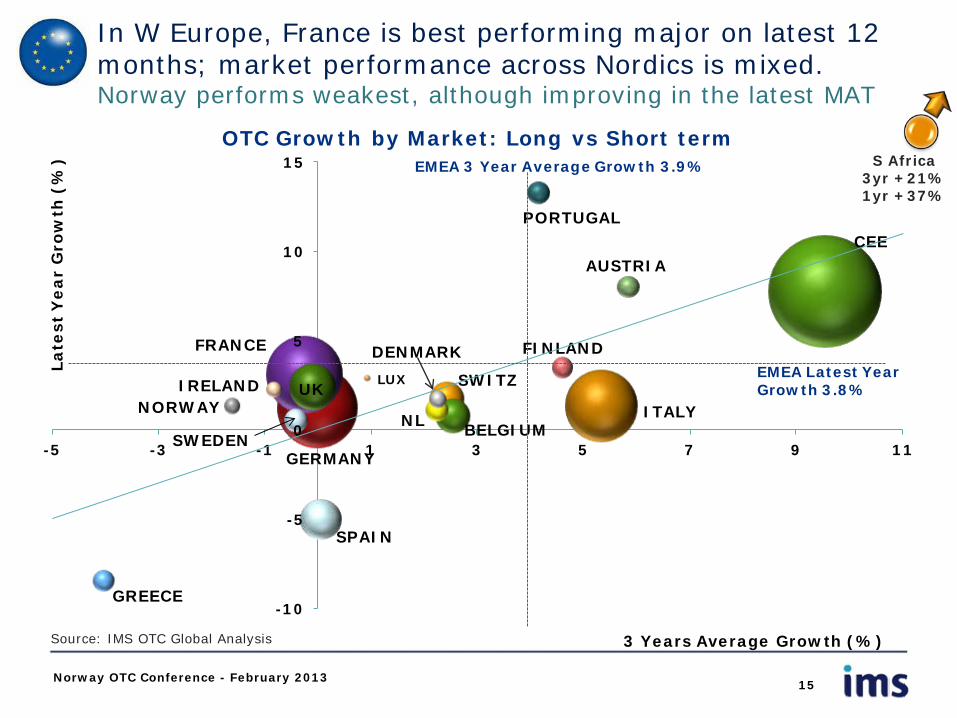

CEE

GERMANY

FRANCE

ITALYUK

SPAIN

SWITZ

BELGIUMSWEDEN

NL

PORTUGAL

AUSTRIA

GREECE

FINLANDDENMARK

NORWAYIRELAND LUX

-10

-5

0

5

10

15

-5 -3 -1 1 3 5 7 9 11

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Market: Long vs Short term

EMEA Latest Year Growth 3.8%

EMEA 3 Year Average Growth 3.9%

In W Europe, France is best performing major on latest 12 months; market performance across Nordics is mixed. Norway performs weakest, although improving in the latest MAT

15 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

S Africa 3yr +21% 1yr +37%

GERMANY

ITALY

RUSSIAPOLAND

CZECH REPUBLIC

ROMANIA

HUNGARY

TURKEY

BULGARIA

SLOVAK REPUBLIC

LITHUANIA

LATVIA

ESTONIA

SLOVENIA

CROATIA

-10

-5

0

5

10

15

20

-5 0 5 10 15 20

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Market: Long vs Short term

EMEA Latest Year Growth 3.8%

EMEA 3 Year Average Growth 3.9%

While in the East, there is a wide range of performances, with Russia continuing to drive most of the region’s growth.

16 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

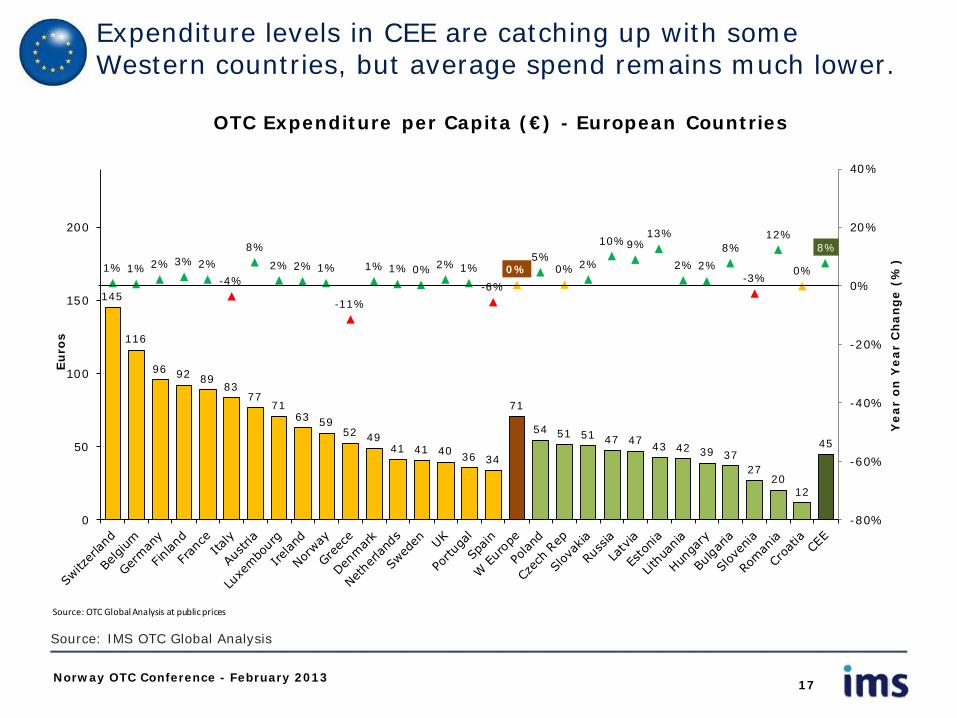

Expenditure levels in CEE are catching up with some Western countries, but average spend remains much lower.

17 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

145

116

96 92 8983

7771

63 5952 49

41 41 40 36 34

71

54 51 51 47 47 43 42 39 3727

2012

45

1% 1% 2% 3% 2%

-4%

8%

2% 2% 1%

-11%

1% 1% 0% 2% 1%

-6%

0%5%

0% 2%

10%9%13%

2% 2%

8%

-3%

12%

0%

8%

-80%

-60%

-40%

-20%

0%

20%

40%

0

50

100

150

200

Ye

ar

on

Ye

ar

Ch

an

ge

(%

)

Eu

ros

OTC Expenditure per Capita (€) - European Countries

Source: OTC Global Analysis at public prices

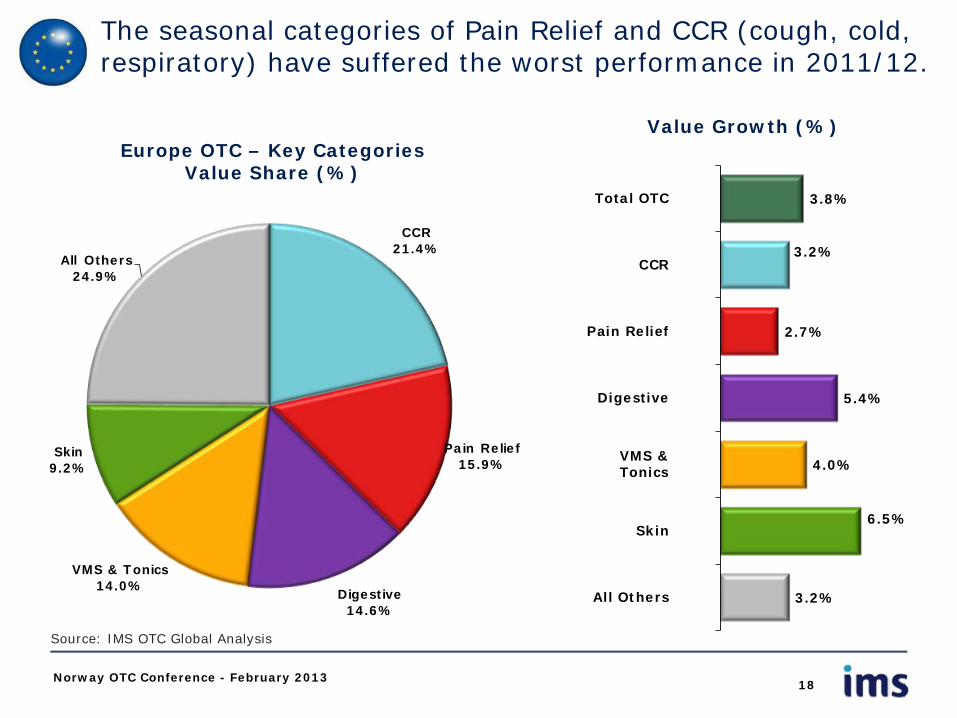

The seasonal categories of Pain Relief and CCR (cough, cold, respiratory) have suffered the worst performance in 2011/12.

Europe OTC – Key Categories Value Share (%)

Value Growth (%)

18 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

CCR21.4%

Pain Relief15.9%

Digestive14.6%

VMS & Tonics14.0%

Skin9.2%

All Others24.9%

3.8%

3.2%

2.7%

5.4%

4.0%

6.5%

3.2%

Total OTC

CCR

Pain Relief

Digestive

VMS &Tonics

Skin

All Others

EYE CARE

ANTI-VARICOSE

HABIT

WEIGHT LOSS

ANTI-HAEMORRHOIDS

ANTIFUNGALS (GYN)EAR CARE

OTHER OTC

-15

-10

-5

0

5

10

15

-6 -4 -2 0 2 4 6 8

La

test

Ye

ar

Gro

wth

(%

)

3 Years Average Growth (%)

OTC Growth by Category: Long vs Short term

EMEA Latest Year Growth 3.8%

EMEA 3 Year Average Growth 3.9%

Among “all others”, strong growth performances from some smaller categories while Weight Loss sales fall sharply.

19 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

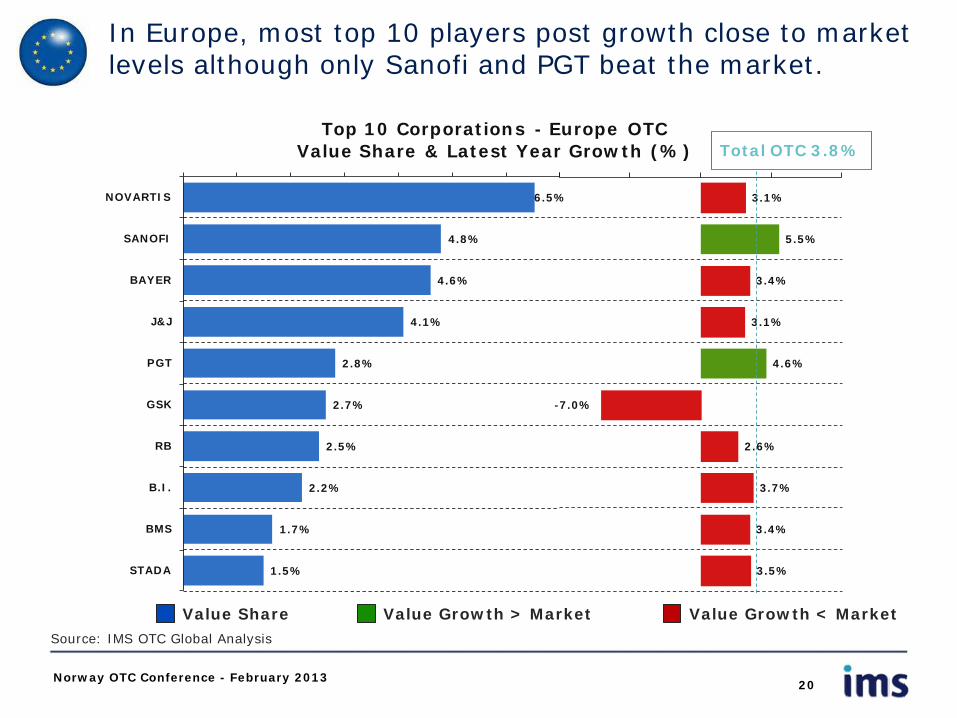

In Europe, most top 10 players post growth close to market levels although only Sanofi and PGT beat the market.

Value Share Value Growth > Market Value Growth < Market

20 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

6.5%

4.8%

4.6%

4.1%

2.8%

2.7%

2.5%

2.2%

1.7%

1.5%

NOVARTIS

SANOFI

BAYER

J&J

PGT

GSK

RB

B.I.

BMS

STADA

3.1%

5.5%

3.4%

3.1%

4.6%

-7.0%

2.6%

3.7%

3.4%

3.5%

Top 10 Corporations - Europe OTC Value Share & Latest Year Growth (%) Total OTC 3.8%

Norway OTC Conference - February 2013

Agenda

• World OTC Context

• Growth Drivers in Europe

• Bringing OTC closer to the consumer

• Focus on the sufferer/consumer and building trust through brands

• Evolution of distribution

• Rx/OTC Switches

• Implications for OTC

21

There is a growing push in society towards preventative health and nutrition

Awareness

•Media campaigns have heightened awareness of unhealthy lifestyles

•Growing number of advertisements, magazines and blogs for self-medication with vitamins, minerals and other dietary supplements

Adoption

•Initially adopted by US, European and Japanese markets where consumers regularly take supplements with meals

•Emerging markets have also taken off

Payers

•Payers are recognising the long-term cost-benefits to preventative treatments

•Many health insurance providers encourage active lifestyles and healthy eating as part of their membership schemes

Future

•As a result more companies are entering into the space which has now become a separate market to just “nutrition”

•The market is expected to continue strong growth

Norway OTC Conference - February 2013 22

Many of the key OTC growth drivers influence the trend towards a stronger focus on the sufferer

Top Corps contribution to growth falling rapidly

Low number and quality output from R&D

Generics dominating large therapy areas

Demand constrained by payers

Key players building strong brand identities

Payers keen to promote self medication

Emerging markets have the critical mass to influence growth

Companies seek to exploit switch opportunities

Increasing access through new channels

PHARMA

OTC

Norway OTC Conference - February 2013 23

A shift in thinking from: “Pharmaceuticals for the Consumer” Towards: Consumer products about health & wellness ...applying patient/sufferer based thinking and involving the whole organisation R&D, regulatory, production, logistics

24

Focus on the sufferer has always been part of OTC thinking but becomes more “centre stage”

Norway OTC Conference - February 2013

25

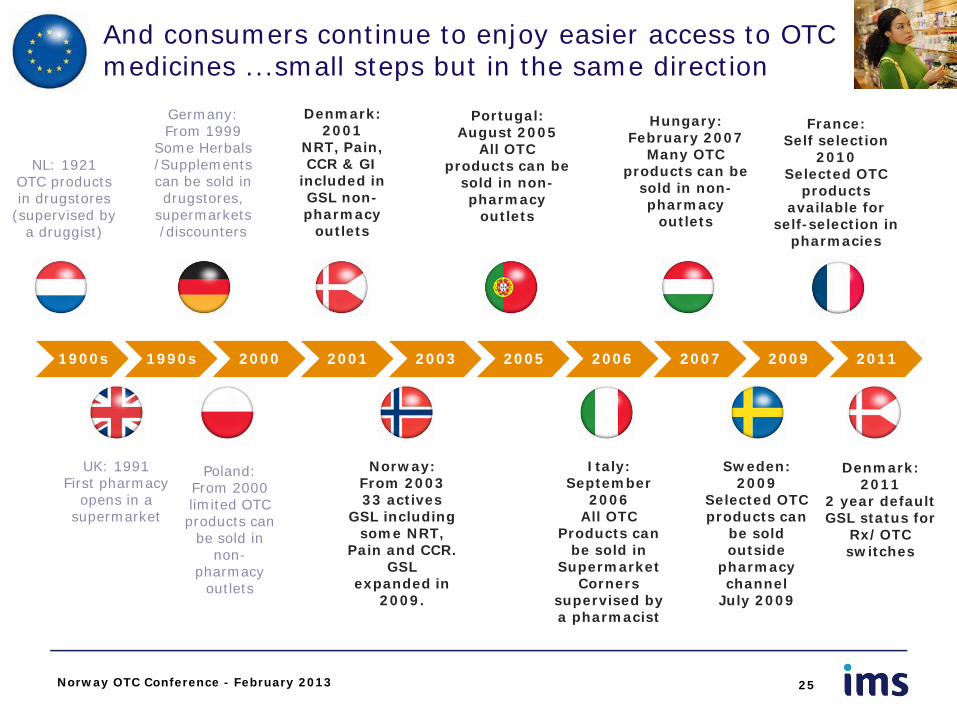

And consumers continue to enjoy easier access to OTC medicines ...small steps but in the same direction

1900s 1990s 2000 2001 2003 2005 2006 2007 2009 2011

NL: 1921 OTC products in drugstores

(supervised by a druggist)

UK: 1991 First pharmacy

opens in a supermarket

Germany: From 1999

Some Herbals /Supplements can be sold in drugstores,

supermarkets /discounters

Poland: From 2000 limited OTC products can

be sold in non-

pharmacy outlets

Portugal: August 2005

All OTC products can be

sold in non-pharmacy

outlets

Italy: September

2006 All OTC

Products can be sold in

Supermarket Corners

supervised by a pharmacist

Hungary: February 2007

Many OTC products can be

sold in non-pharmacy

outlets

Sweden: 2009

Selected OTC products can

be sold outside

pharmacy channel

July 2009

Norway: From 2003 33 actives

GSL including some NRT,

Pain and CCR. GSL

expanded in 2009.

Denmark: 2001

NRT, Pain, CCR & GI

included in GSL non-pharmacy

outlets

Norway OTC Conference - February 2013

France: Self selection

2010 Selected OTC

products available for

self-selection in pharmacies

Denmark: 2011

2 year default GSL status for

Rx/OTC switches

Pharmacy

Mass Market

Mail Order

Mass Market

Pharmacy

Drugstore

Pharmacy

Supermarket

Mass Market

Pharmacy

Pharmacy

Mass Market

Mass Market - New

Pharmacy

-20

-15

-10

-5

0

5

10

15

20

25

0 1 2 3 4 5 6

La

test

Ye

ar

Gro

wth

(%

)

Channel Contribution to OTC & Growth

Germany Italy NL Portugal UK Sweden

Size of Bubble represents

channel share of country sales

Consumer appreciation of convenience is shown by relative growth of non-pharmacy channels

Pharmacy

Mass Market

26 Norway OTC Conference - February 2013

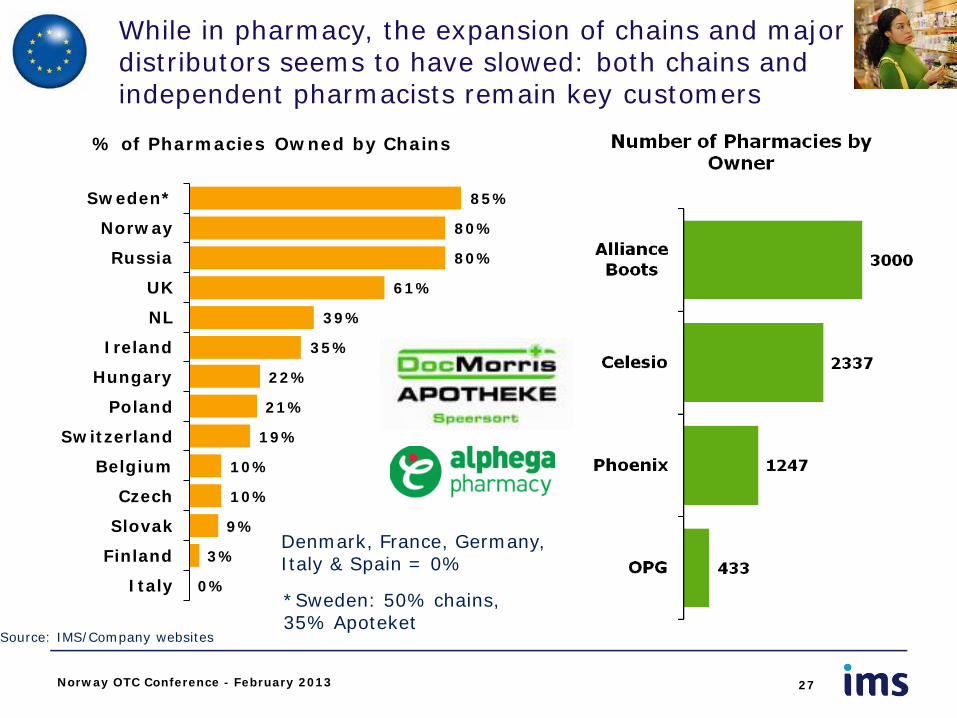

While in pharmacy, the expansion of chains and major distributors seems to have slowed: both chains and independent pharmacists remain key customers

27

Source: IMS/Company websites

85%

80%

80%

61%

39%

35%

22%

21%

19%

10%

10%

9%

3%

0%

Sweden*

Norway

Russia

UK

NL

Ireland

Hungary

Poland

Switzerland

Belgium

Czech

Slovak

Finland

Italy

% of Pharmacies Owned by Chains

Denmark, France, Germany, Italy & Spain = 0%

*Sweden: 50% chains, 35% Apoteket

Norway OTC Conference - February 2013

28

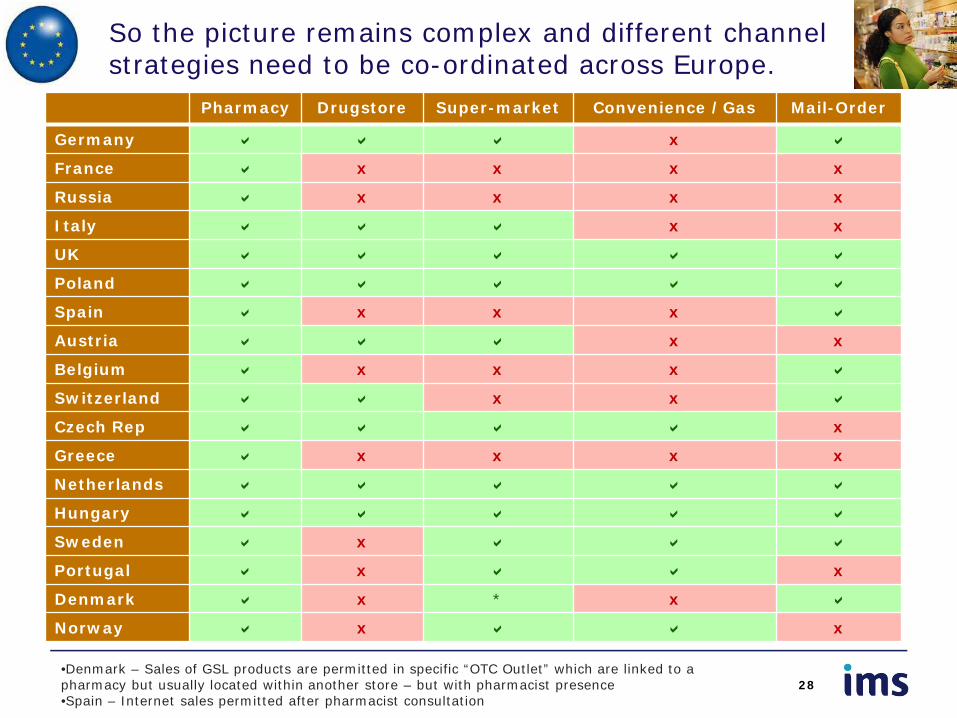

So the picture remains complex and different channel strategies need to be co-ordinated across Europe.

Pharmacy Drugstore Super-market Convenience /Gas Mail-Order

Germany x

France x x x x

Russia x x x x

Italy x x

UK

Poland

Spain x x x

Austria x x

Belgium x x x

Switzerland x x

Czech Rep x

Greece x x x x

Netherlands

Hungary

Sweden x

Portugal x x

Denmark x * x

Norway x x

Norway OTC Conference - February 2013 •Denmark – Sales of GSL products are permitted in specific “OTC Outlet” which are linked to a pharmacy but usually located within another store – but with pharmacist presence •Spain – Internet sales permitted after pharmacist consultation

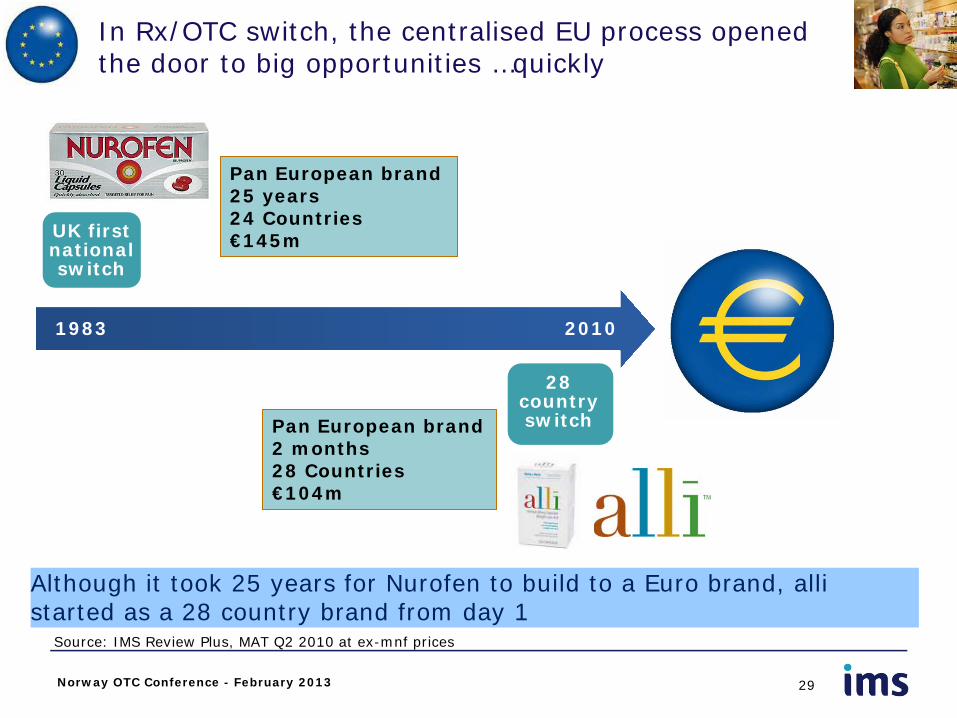

Although it took 25 years for Nurofen to build to a Euro brand, alli started as a 28 country brand from day 1

29

1983 2010

UK first national switch

Pan European brand 25 years 24 Countries €145m

28 country switch Pan European brand

2 months 28 Countries €104m

In Rx/OTC switch, the centralised EU process opened the door to big opportunities …quickly

Source: IMS Review Plus, MAT Q2 2010 at ex-mnf prices

Norway OTC Conference - February 2013

However ...other examples show that success is possible

30

2010

28 country switch

However recent switches have shown that success is not guaranteed or easy to achieve

Norway OTC Conference - February 2013

Complex protocol involving doctor visit/diagnosis

Matching product performance to

consumer expectation

Lack of exclusivity for innovators

CV Derm (Skin) Derm (Hair) GI Gyn Health

Metabolic Men’s Health Neuro/Cog Oral Care Pain

Psych / Dependence

Respiratory Age 50+ Health Sleep Eye, Ear

• Anti-Platelet • Borderline

Hypertension • Oedema • Hypertension • Lipid Management

Acne, Actinic Keratosis, Age Spots,, Chronic Wound Healing, Diaper Rash, Eczema, Onychomycosis, Psoriasis, Ring Worm), Rosacea, Seborrheic Keratosis

• Androgenic Alopecia • Hair Removal

Chronic Constipation, Diarrhoea, Diverticulitis, Heartburn, GERD, IBS, Morning Sickness, Motion Sickness, Peptic Ulcer, Ulcerative Colitis

Bacterial Vaginosis, Endometriosis, FSD, Fibrocystic Breast, Heavy Menstruation, Oral Contraception, PMS, PMDD, UTI, Vaginal Candidiasis

• Impaired Glucose Tolerance

• Obesity

• Male Contraception • Premature Ejaculation

• Adult ADHD • Cognition • Movement Disorders • RLS

Below Gum Tartar, Chronic Halitosis, Cold Sore, Dry Mouth, Gingivitis, Oral Candidiasis, Periodontal Disease, Sensitive Teeth

• Fibromyalgia • General Acute Pain • Migraine • Muscle Relaxant • Neuropathic Pain

(Sciatica) • OA Pain

• Alcohol Dependence • Mood Disorders • Tobacco Dependence

• Allergy • Asthma • COPD • Cough/Cold • Influenza

• BPH • ED • Haemorrhoids • Hormone Replacement • Osteoporosis • Overactive Bladder

• Fatigue/Extreme Sleepiness

• Primary Insomnia • Sleeplessness

Bacterial Conjunctivitis, Chronic Ear Infection, Dry Eye, Eye Allergy (Conjunctivitis), Ocular Inflammation, Glaucoma, Swimmer’s Ear

Norway OTC Conference - February 2013 31

...while many other therapy areas have been considered for potential Rx/OTC switch potential

So both local switches and the centralised EU process are routes for growth that cannot be ignored.

32

• 160,000 pharmacies

• 46m Pharmacy shoppers every day

• Growing pan European wholesalers and retailers

• €23bn OTC market

• Population of 501m

• 1 consistent marketing message

• If you don’t recognise the potential for your molecule in the EU someone else may

Danger

European supply chain European Consumer

Source: IMS OTC Review

Norway OTC Conference - February 2013

But whether the switch is central or local, getting it right at the local level is critical to success.

33

Differing consumer cultures

and habits

Differing advertising regulations

Differing pharmacy needs/ ex-pectations

Differing channel

mix

28 disparate markets

1 process

Norway OTC Conference - February 2013

Norway OTC Conference - February 2013

Agenda

• World OTC Context

• Growth Drivers in Europe

• Bringing OTC closer to the consumer

• Focus on the sufferer/consumer and building trust through brands

• Evolution of distribution

• Rx/OTC Switches

• Implications for OTC

34

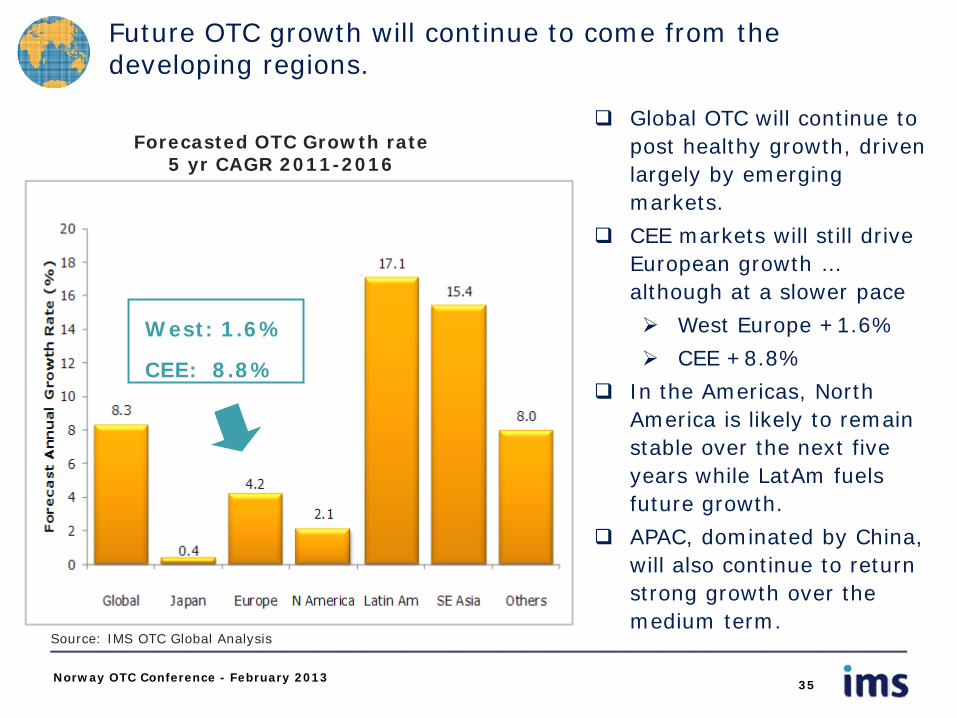

Future OTC growth will continue to come from the developing regions.

Forecasted OTC Growth rate 5 yr CAGR 2011-2016

35 Norway OTC Conference - February 2013

Source: IMS OTC Global Analysis

Global OTC will continue to post healthy growth, driven largely by emerging markets.

CEE markets will still drive European growth … although at a slower pace

West Europe +1.6%

CEE +8.8%

In the Americas, North America is likely to remain stable over the next five years while LatAm fuels future growth.

APAC, dominated by China, will also continue to return strong growth over the medium term.

West: 1.6%

CEE: 8.8%

• OTC remains attractive as it continues to outpace Pharma

• And as a result the market becomes more competitive

• PGT Healthcare ...potentially a major new player with a new model

• Within Europe, West Europe sees a resurgence of growth but the main long-term geo growth opportunities remain in CEE

• And the “fringes” of EMEA: CIS, Middle East, sub-Saharan Africa.

• The increased patient/sufferer focus of the OTC market raises new opportunities ...and new challenges

• How to input real and responsible “consumer-focused thinking”

• Taking advantage of new distribution and “consumer access” opportunities ...without losing the relationship with pharmacy

• Rx/OTC switch: growth opportunities ...how to find ways to make it pay? • Right portfolio; right regulatory strategy; right consumer thinking; right Go-to-

Market

• OTC in Europe offers a “rising tide” ...but as the picture becomes more complex, success requires new thinking and new business models

Conclusions: Market and Industry

Norway OTC Conference - February 2013 36

For contact:

Andy Tisman Senior Principal Consumer Health IMS Health

+44 (0)20 3075 5295

Good luck and great success in this challenging but exciting rising tide of an OTC marketplace in Europe in 2013!

37 Norway OTC Conference - February 2013

Related Documents