15th April 2010, Airneth Annual Conference, Andrew Gordon Director Market Analysis 15th April 2010, Airneth Annual Conference,

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

15th April 2010, Airneth Annual Conference,

Andrew GordonDirector Market Analysis

15th April 2010, Airneth Annual Conference,

y

• Where is the industry today?• Economy• Traffic outlook

• Industry drivers

oprie

tary

doc

umen

t.

• Industry drivers

• Airbus GMF, 2009 – 2028

s re

serv

ed. C

onfid

entia

l and

pro Airbus GMF, 2009 2028

• Emerging markets

© A

IRBU

S S.

A.S.

All

right

s

• Where is the industry today?• Economy• Traffic outlook

• Industry drivers

oprie

tary

doc

umen

t.

• Industry drivers

• Airbus GMF, 2009 – 2028

s re

serv

ed. C

onfid

entia

l and

pro Airbus GMF, 2009 2028

• Emerging markets

© A

IRBU

S S.

A.S.

All

right

s

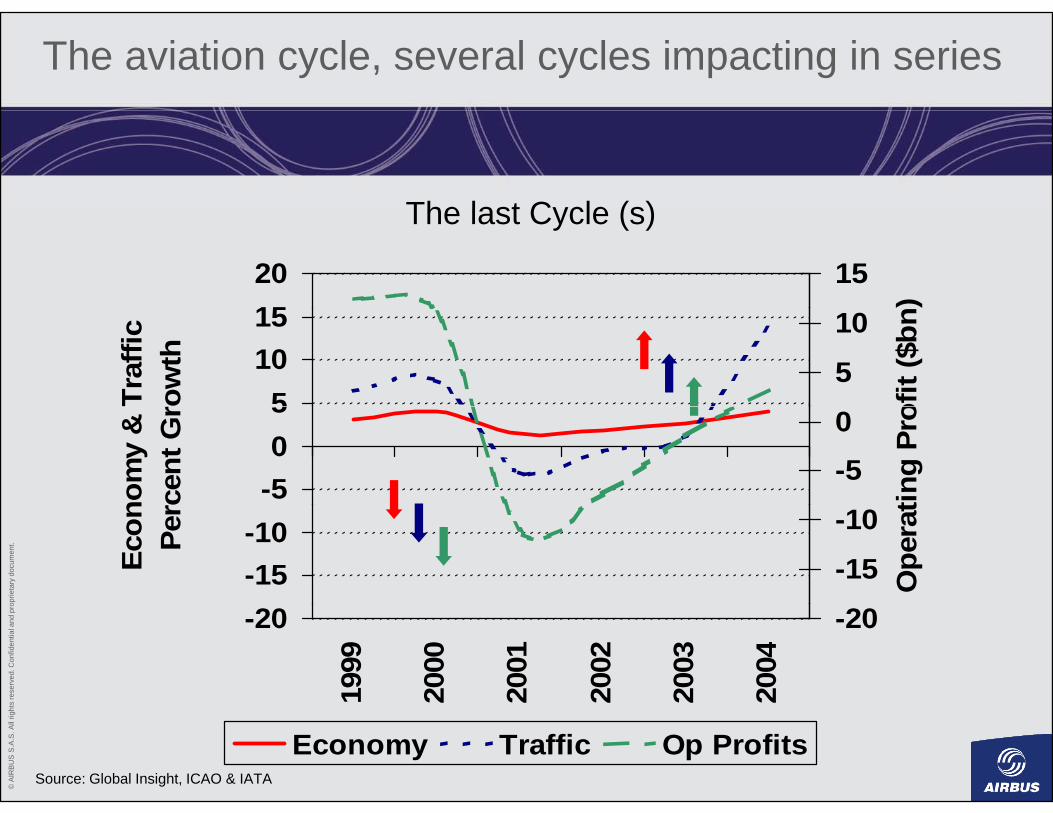

The aviation cycle, several cycles impacting in series

The last Cycle (s)

1520 15

)

The last Cycle (s)

51015

Traf

ficro

wth 5

10

ofit

($bn

-505

nom

y &

rc

ent G

r

-50

ting

Pro

oprie

tary

doc

umen

t.

-15-10

Econ Pe

r

-15

-10

Ope

rat

s re

serv

ed. C

onfid

entia

l and

pro -20

1999

2000

2001

2002

2003

2004

-20

© A

IRBU

S S.

A.S.

All

right

s

Source: Global Insight, ICAO & IATA

2 2 2 2 2Economy Traffic Op Profits

Economists believe recession has bottomed out

Real GDP year over year quarterly evolution (%)

14% World USA Western Europe Japan

Real GDP year-over-year quarterly evolution (%)

6%

10%

-2%

2%

oprie

tary

doc

umen

t.

-6%We are

here

s re

serv

ed. C

onfid

entia

l and

pro

2006 2007 2008 2009 2010 2011St th

-10%Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

here

© A

IRBU

S S.

A.S.

All

right

s Strong growthsince 2004 Slowdown Deep crisis Recovery Complete

recovery

Source: Global Insight (January 2010), Airbus

Economists believe recession has bottomed out

Real GDP year over year quarterly evolution (%)

14% World USA Western Europe Japan Emerging economies

Real GDP year-over-year quarterly evolution (%)

6%

10%

-2%

2%

oprie

tary

doc

umen

t.

-6%We are

here

s re

serv

ed. C

onfid

entia

l and

pro

2006 2007 2008 2009 2010 2011St th

-10%Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

here

© A

IRBU

S S.

A.S.

All

right

s Strong growthsince 2004 Slowdown Deep crisis Recovery Complete

recovery

Source: Global Insight (January 2010), Airbus

Economists believe recession has bottomed out

Real GDP year over year quarterly evolution (%)Real GDP year-over-year quarterly evolution (%)

14%World USA Western EuropeJapan Emerging economies China

6%

10%

-2%

2%

oprie

tary

doc

umen

t.

-6%We are

here

s re

serv

ed. C

onfid

entia

l and

pro

2006 2007 2008 2009 2010 2011St th

-10%Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

here

© A

IRBU

S S.

A.S.

All

right

s Strong growthsince 2004 Slowdown Deep crisis Recovery Complete

recovery

Source: Global Insight (January 2010), Airbus

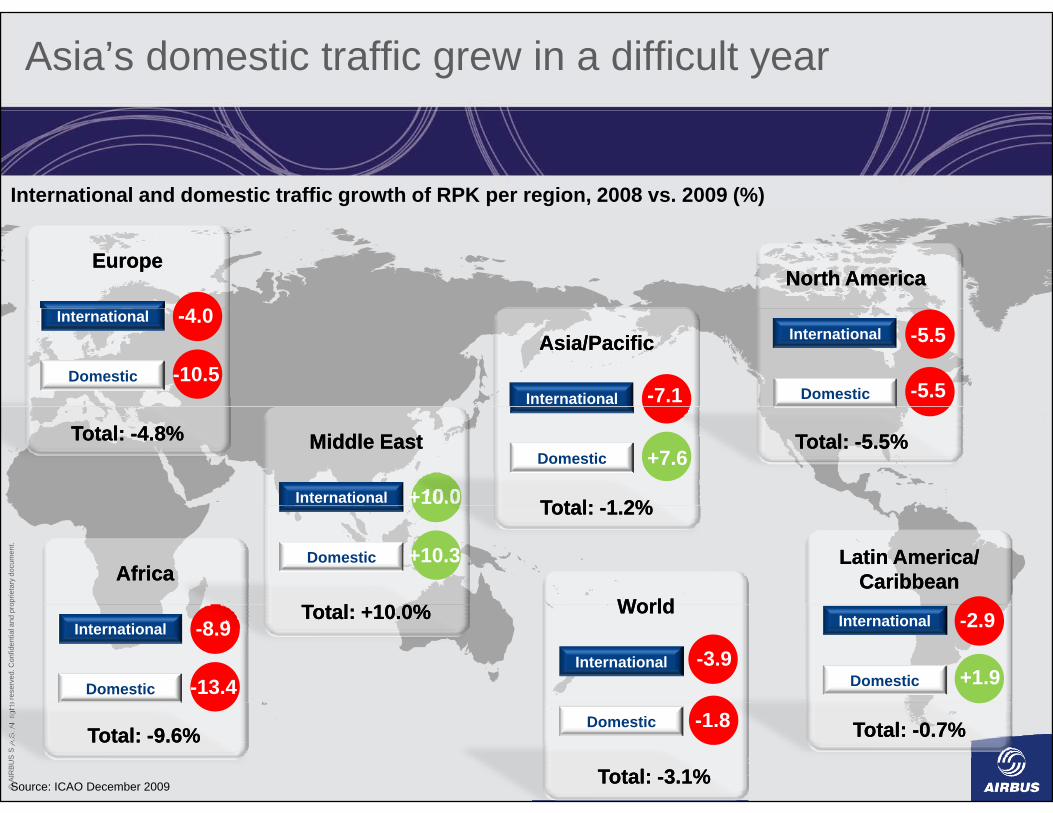

Asia’s domestic traffic grew in a difficult year

International and domestic traffic growth of RPK per region, 2008 vs. 2009 (%)

EuropeEurope

4 0

North AmericaNorth America

International

Domestic

-4.0

-10.5Asia/PacificAsia/Pacific

International -7.1

International

Domestic

-5.5

-5.5

Middle EastMiddle East

International +10.0

Domestic +7.6

Total:Total: 1 2%1 2%

Total: Total: --5.5%5.5%Total: Total: --4.8%4.8%

oprie

tary

doc

umen

t.

AfricaAfricaDomestic +10.3 Latin America/Latin America/

CaribbeanCaribbeanWorldWorld

Total: Total: --1.2%1.2%

%%

s re

serv

ed. C

onfid

entia

l and

pro

International

Domestic

-8.9

-13.4

International

Domestic

-2.9

+1.9

WorldWorld

International -3.9

Total: +10.0%Total: +10.0%

© A

IRBU

S S.

A.S.

All

right

s

Source: ICAO December 2009

Domestic -1.8 Total: Total: --0.7%0.7%Total: Total: --9.6%9.6%

Total: Total: --3.1%3.1%

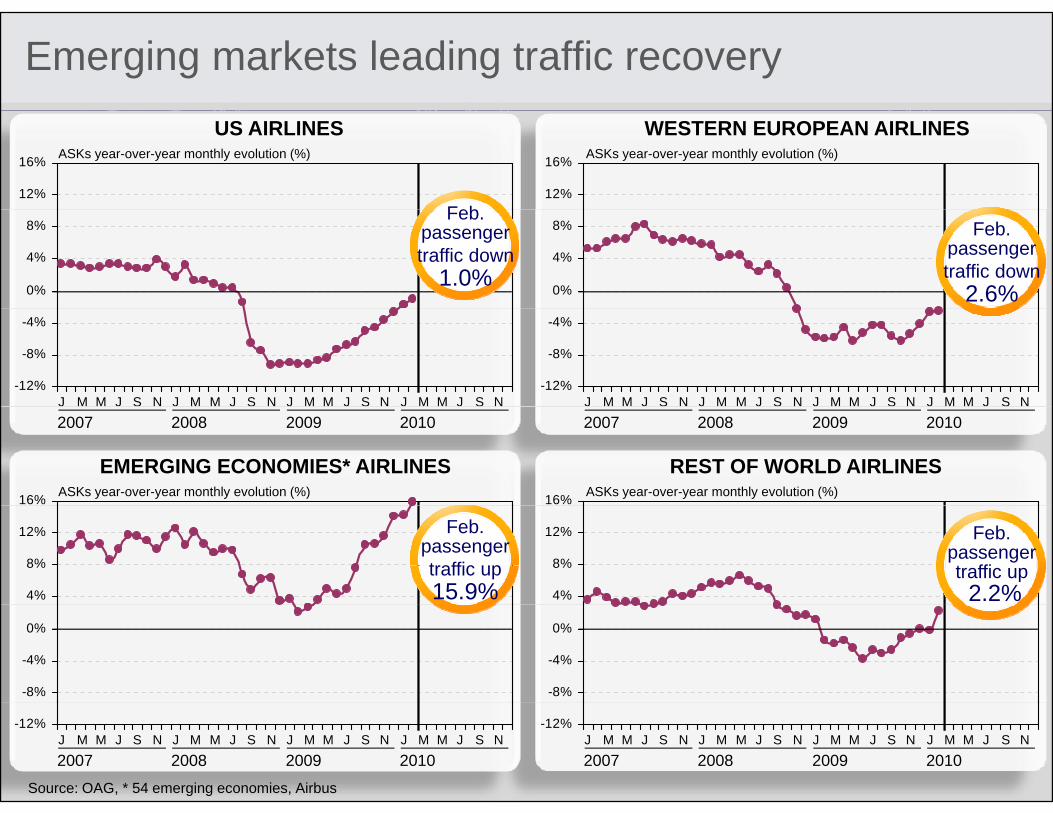

Emerging markets leading traffic recovery

12%

16% ASKs year-over-year monthly evolution (%)

12%

16% ASKs year-over-year monthly evolution (%)

US AIRLINES WESTERN EUROPEAN AIRLINES

Feb

0%

4%

8%

0%

4%

8%Feb.

passenger traffic down

1.0%

Feb. passenger traffic down

2.6%

-12%

-8%

-4%

J M M J S N J M M J S N J M M J S N J M M J S N-12%

-8%

-4%

J M M J S N J M M J S N J M M J S N J M M J S N2007 2008 2009 2010 2007 2008 2009 2010

16% ASKs year-over-year monthly evolution (%) 16% ASKs year-over-year monthly evolution (%)

EMERGING ECONOMIES* AIRLINES REST OF WORLD AIRLINES

oprie

tary

doc

umen

t.

4%

8%

12%

4%

8%

12%Feb. passenger traffic up15.9%

Feb. passenger traffic up2.2%

s re

serv

ed. C

onfid

entia

l and

pro

-8%

-4%

0%

-8%

-4%

0%

© A

IRBU

S S.

A.S.

All

right

s

Source: OAG, * 54 emerging economies, Airbus

-12%J M M J S N J M M J S N J M M J S N J M M J S N

-12%J M M J S N J M M J S N J M M J S N J M M J S N2007 2008 2009 20102007 2008 2009 2010

• Where is the industry today?• Economy• Traffic outlook

• Industry drivers

oprie

tary

doc

umen

t.

• Industry drivers

• Airbus GMF, 2009 – 2028

s re

serv

ed. C

onfid

entia

l and

pro Airbus GMF, 2009 2028

• Emerging markets

© A

IRBU

S S.

A.S.

All

right

s

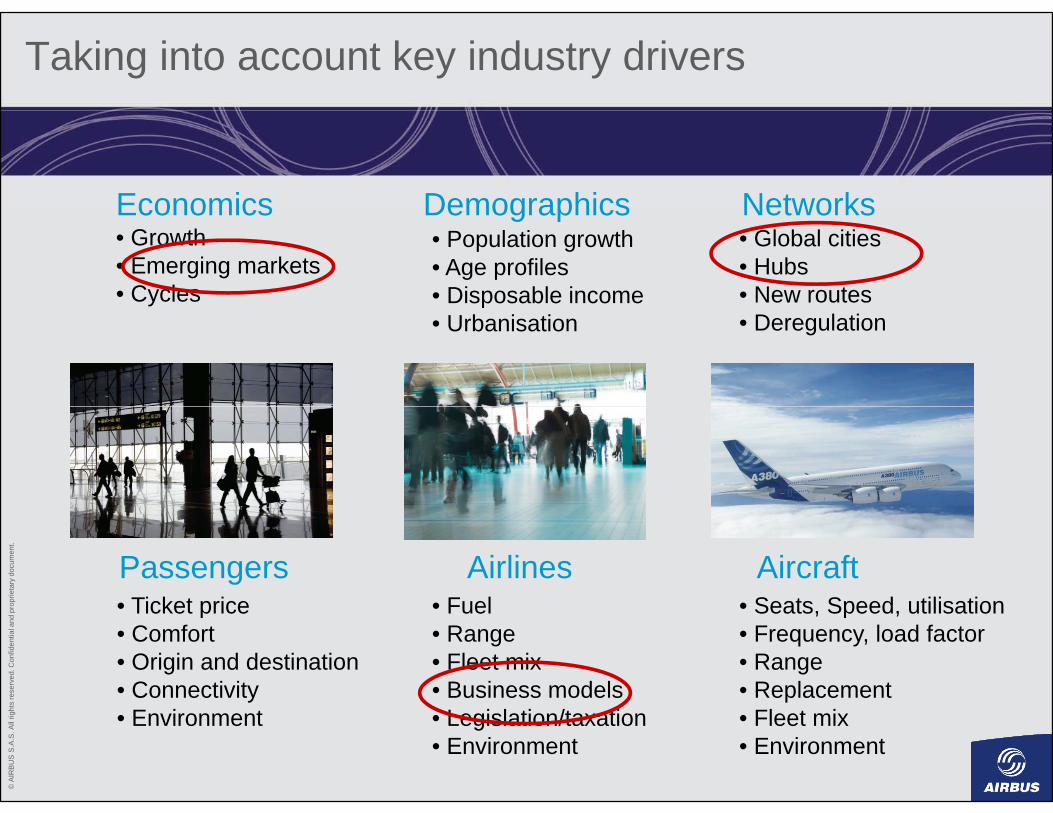

Taking into account key industry drivers

Economics Demographics NetworksEconomics• Growth• Emerging markets• Cycles

Demographics Networks• Population growth• Age profiles• Disposable income

• Global cities• Hubs• New routes

• Urbanisation • Deregulation

oprie

tary

doc

umen

t.

Airlines AircraftPassengers• Ticket price • Fuel • Seats Speed utilisation

s re

serv

ed. C

onfid

entia

l and

pro • Ticket price

• Comfort• Origin and destination• Connectivity

• Fuel• Range• Fleet mix• Business models

• Seats, Speed, utilisation• Frequency, load factor • Range• Replacement

© A

IRBU

S S.

A.S.

All

right

s

• Environment • Legislation/taxation• Environment

• Fleet mix• Environment

The world of 2028 will be very different from today

Ranking of countries by real GDPRanking of countries by real GDP

19881- US

20081- US

20281- US

a g o cou t es by ea Ga g o cou t es by ea G

US

2- Japan

3- Germany

2- Japan

3- China2- China 3- Japan

4- UK

5- France

6- Italy

4- Germany

5- UK

6- France

4- Germany

5- India 6- UK

oprie

tary

doc

umen

t.

7- Russia

8- Canada

9 Spain

7- Italy

8- Spain

9 C d

6 UK

7- France

8- Brazil

s re

serv

ed. C

onfid

entia

l and

pro 9- Spain

10- Brazil

11- Mexico

9- Canada

10- India

11- Brazil

9- Italy

10- Canada

11- South Korea

© A

IRBU

S S.

A.S.

All

right

s

12- China

Source: Global Insight (August 2009), Airbus

12- South Korea 12- Russia

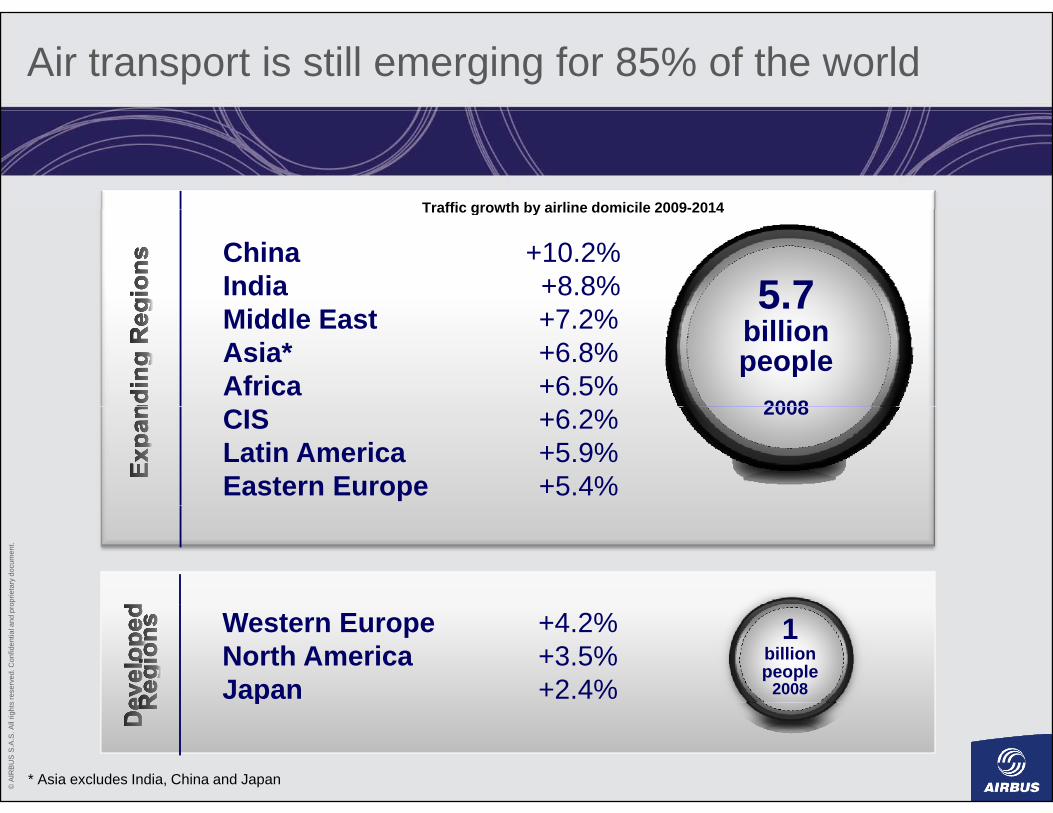

Air transport is still emerging for 85% of the world

Traffic growth by airline domicile 2009-2014

China +10.2%India +8.8% 5.7

Traffic growth by airline domicile 2009-2014

Middle East +7.2%Asia* +6.8%Africa +6.5%

5.7billionpeople

2008CIS +6.2%Latin America +5.9%Eastern Europe +5.4%

2008

oprie

tary

doc

umen

t.s

rese

rved

. Con

fiden

tial a

nd p

ro

Western Europe +4.2%North America +3.5%Japan +2.4%

1billionpeople

2008

© A

IRBU

S S.

A.S.

All

right

s

p

* Asia excludes India, China and Japan

Large potential to increase propensity to travel

10

SwitzerlandDenmark

Ireland

SwedenUKQatarCanada

UAE

Australia

MacaoSingapore

Hong Kong

New Zealand

Spain

Kuwait

Cyprus

Bahamas

Puerto Rico Greece

Malta

Bahrain

Barbados

Seychelles

Maldives

TrinidadFiji

St Lucia

M i i

USA

10

8

2 trips per

capita

Netherlands

Finland

JapanBelgium

France

GermanyItalyBrunei

KuwaitPuerto Rico

PortugalSouth Korea

Slovenia

IsraelTaiwan

Saudi Arabia

Czech Rep.

Estonia

HungarySlovakia

LatviaPanama

Suriname

j

Cape Verde

Samoa

Jordan

Poland

MauritiusMalaysia

Croatia

Mexico

Turkey

RussiaBrazil

1

pita

-20

08

0.11 trip per

World average

Equatorial GuineaBotswana

Bosnia

BrazilChina

India

Algeria

BelarusAngola

Nigeria

0,1

* per

cap

oprie

tary

doc

umen

t.

capita0.05 trip

per capitaIraq

BangladeshLesotho

Afghanistan

ChadNiger

0,01

Trip

s*

s re

serv

ed. C

onfid

entia

l and

pro

0,0010 5 000 10 000 15 000 20 000 25 000 30 000 35 000 40 000 45 000 50 000 55 000

© A

IRBU

S S.

A.S.

All

right

s

Passengers originating from a particular country Note: GDP in 2005 US$

Source: IATA PaxIS, Global Insight, Airbus

2008 Real GDP per Capita

A network of cities : 92% of the long haul traffic is from and/or to 37 “mega-cities”

37 “mega cities” in terms of37 mega-cities in terms of international air traffic demand

oprie

tary

doc

umen

t.s

rese

rved

. Con

fiden

tial a

nd p

ro©

AIR

BUS

S.A.

S. A

ll rig

hts

Destinations with more than 10 000 daily long haul pax

Emerging markets driving World urbanisation

5

6Population (billions)

Urban Population

4

5Today

2

3Rural Population

oprie

tary

doc

umen

t.

0

1Source: UN,Airbus

s re

serv

ed. C

onfid

entia

l and

pro

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

© A

IRBU

S S.

A.S.

All

right

s

With continuing growth & urbanisation, the number of mega-cities will more than double

82 bi iti h l h l

MoreMega-cities82 big cities where long-haul passengers

will want to fly between in 20 yearsMega-cities

AAA B

A

oprie

tary

doc

umen

t.s

rese

rved

. Con

fiden

tial a

nd p

ro©

AIR

BUS

S.A.

S. A

ll rig

hts

Destinations with more than 10 000 daily long haul pax

Growth in the size and number of mega-cities

Main long haul VLA routes by 2028Main long-haul VLA routes by 2028

AAA B

A

oprie

tary

doc

umen

t.s

rese

rved

. Con

fiden

tial a

nd p

ro©

AIR

BUS

S.A.

S. A

ll rig

hts

Destinations with more than 10 000 daily long haul pax

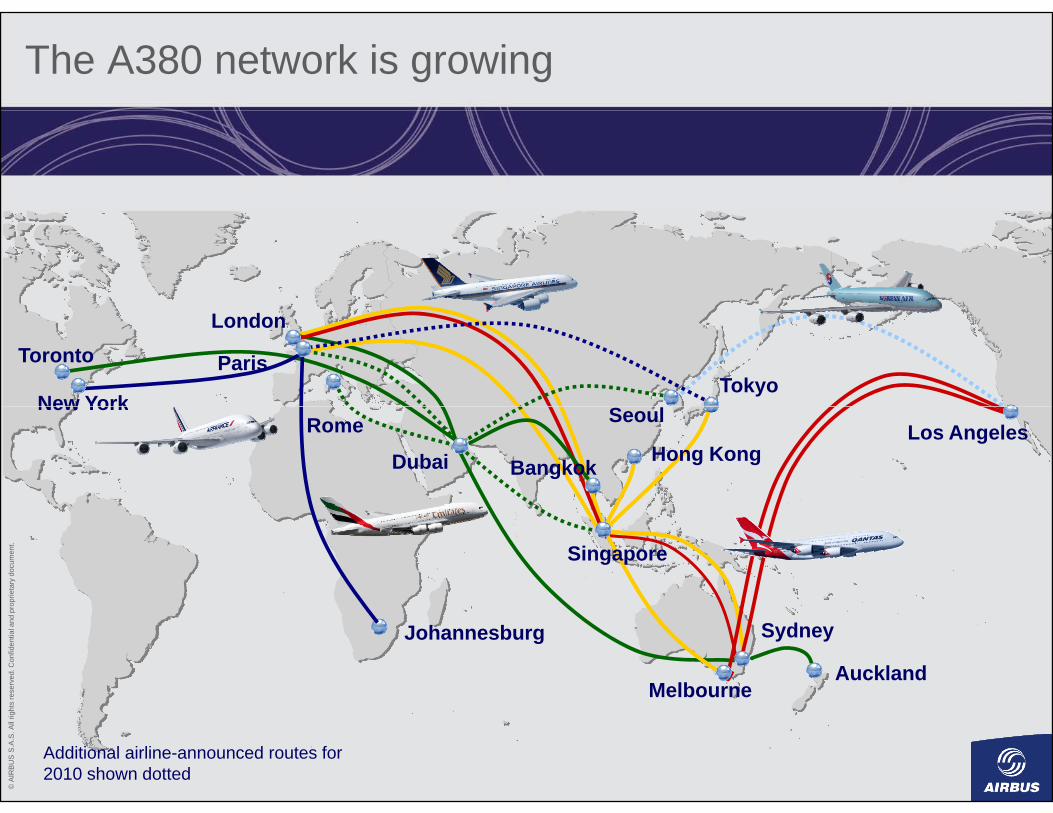

The A380 network is growing

Toronto

New York

London

ParisTokyo

New YorkRome

Dubai

Seoul

Hong KongBangkokLos Angeles

oprie

tary

doc

umen

t. Singapore

s re

serv

ed. C

onfid

entia

l and

pro

Auckland

Sydney

Melbourne

Johannesburg

© A

IRBU

S S.

A.S.

All

right

s

Additional airline-announced routes for 2010 shown dotted

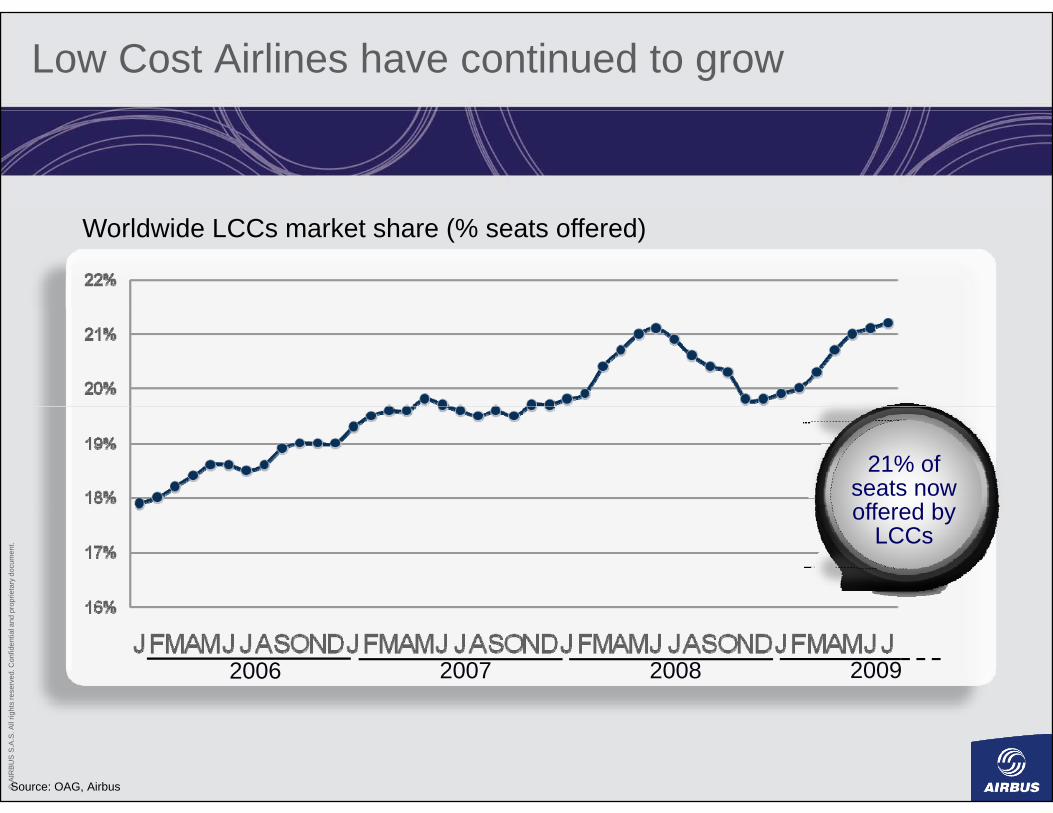

Low Cost Airlines have continued to grow

Worldwide LCCs market share (% seats offered)

21% of seats now

ff d b

oprie

tary

doc

umen

t.

offered by LCCs

s re

serv

ed. C

onfid

entia

l and

pro

2006 2007 2008 2009

© A

IRBU

S S.

A.S.

All

right

s

Source: OAG, Airbus

Low cost traffic as driver of traffic growth

Intra Asian traffic and LCC market share development, 2001 - 2009

6%

Seats (1,000s) LCC market share %Total Intra

Asian traffic

6%yearly growth*

LCC traffic

38%yearly growth*

oprie

tary

doc

umen

t.

LCC 2009

s re

serv

ed. C

onfid

entia

l and

pro

market share

14%

© A

IRBU

S S.

A.S.

All

right

s

Source: OAG (September traffic), Airbus

* Average annual growth rate

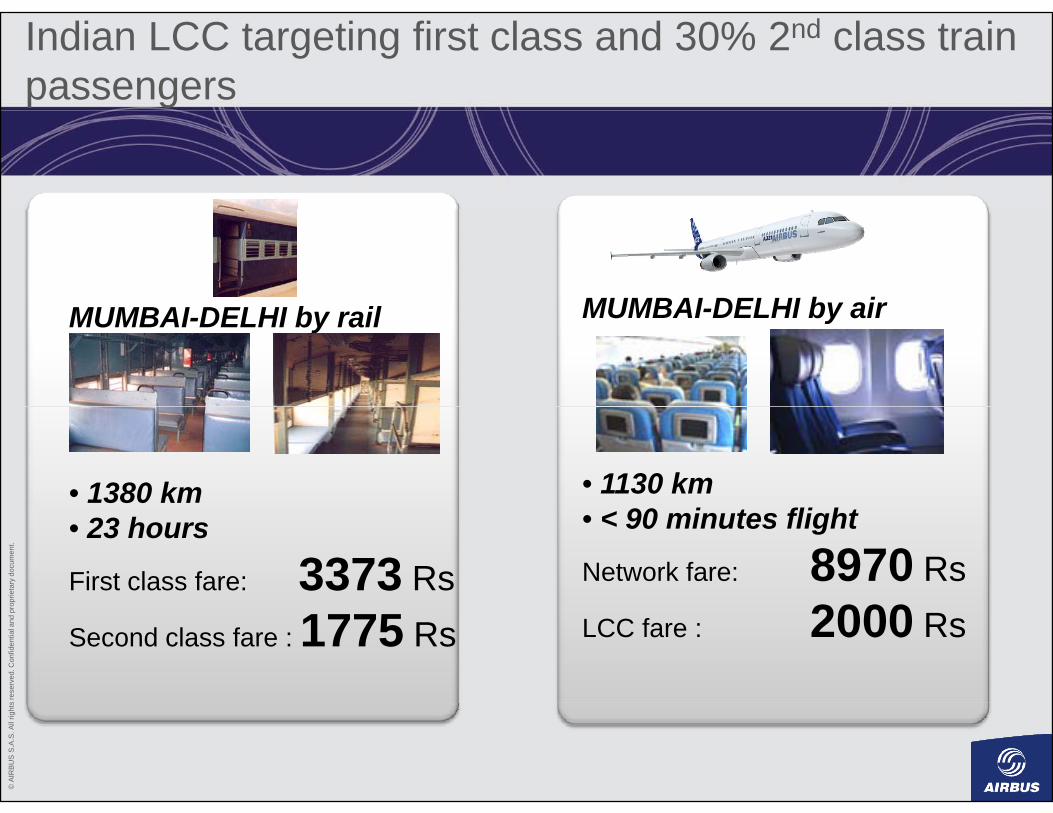

Indian LCC targeting first class and 30% 2nd class train passengers

MUMBAI DELHI b il MUMBAI DELHI by airMUMBAI-DELHI by rail MUMBAI-DELHI by air

• 1380 km • 1130 km

oprie

tary

doc

umen

t.

• 23 hours

First class fare: 3373 Rs

• < 90 minutes flight

Network fare: 8970 Rs2000

s re

serv

ed. C

onfid

entia

l and

pro

Second class fare : 1775 Rs LCC fare : 2000 Rs

© A

IRBU

S S.

A.S.

All

right

s

Low cost carriers spread their wings over Asia

Intra Asian LCC network, 09/2001 vs. 09/2009,

Sep. 2001 Sep. 2009

oprie

tary

doc

umen

t.

48 576Airport Airport

iiAirport Airport

ii

s re

serv

ed. C

onfid

entia

l and

pro 48 576 pairspairs

Average Average flight distanceflight distance

700km

pairspairs

Average Average flight distanceflight distance 1800

km

© A

IRBU

S S.

A.S.

All

right

s gggg km

Source: OAG

• Where is the industry today?• Economy• Traffic outlook

• Industry drivers

oprie

tary

doc

umen

t.

• Industry drivers

• Airbus GMF 2009 – 2028

s re

serv

ed. C

onfid

entia

l and

pro Airbus GMF 2009 2028

• Emerging markets

© A

IRBU

S S.

A.S.

All

right

s

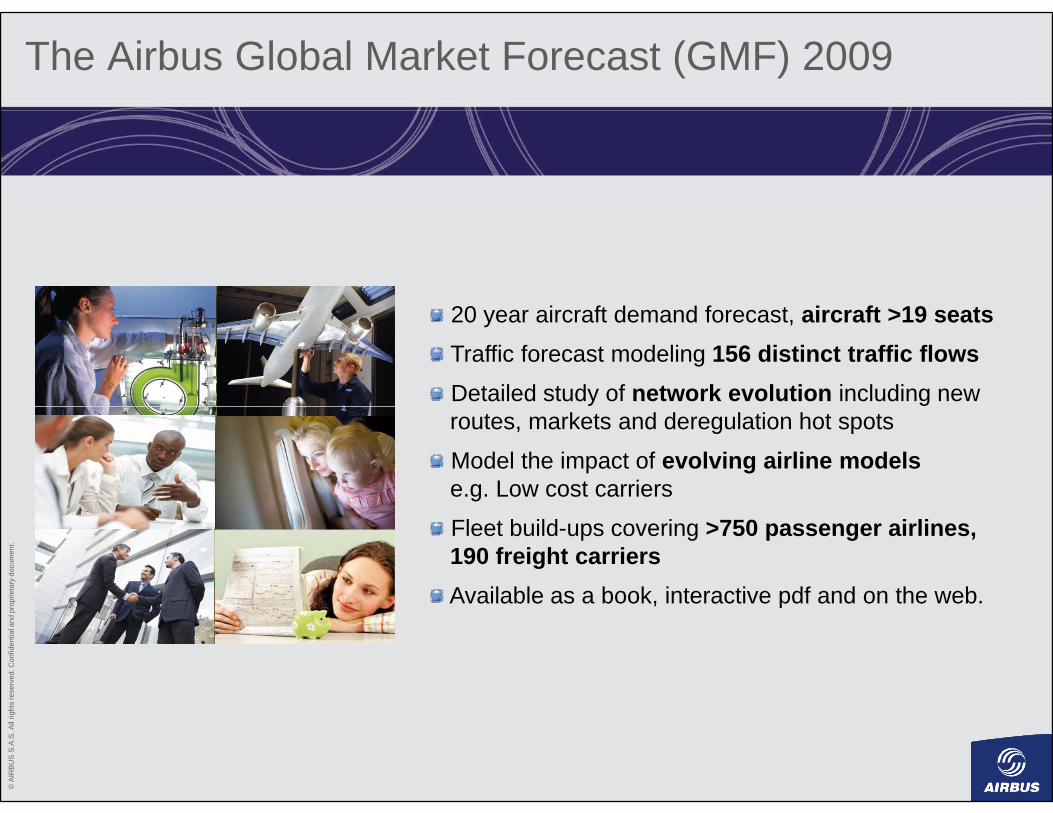

The Airbus Global Market Forecast (GMF) 2009

20 i ft d d f t i ft >19 t20 year aircraft demand forecast, aircraft >19 seatsTraffic forecast modeling 156 distinct traffic flowsDetailed study of network evolution including new routes, markets and deregulation hot spots

Model the impact of evolving airline modelse.g. Low cost carriers

oprie

tary

doc

umen

t.

Fleet build-ups covering >750 passenger airlines, 190 freight carriersAvailable as a book, interactive pdf and on the web.

s re

serv

ed. C

onfid

entia

l and

pro

, p

© A

IRBU

S S.

A.S.

All

right

s

Today’s passenger traffic 38% above 2000 level

RPK growth: 2008 vs. 2000

Europe29%

CIS+121%+29%

North America+7%

Middle East Int’lChina184%

+121%

Middle East Int’l+166%

+184%India

+192%

oprie

tary

doc

umen

t.

Latin America Int’l+40%

Africa Int’l+53%

Asia-Pacific Int’l+29%

192%

s re

serv

ed. C

onfid

entia

l and

pro 40% 53% +29%

© A

IRBU

S S.

A.S.

All

right

s

Source: ATA (North America), AEA (Europe), AAPA Int’l (Asia-Pacific), IATA Gabi (Latin America, Africa & Middle East), CAAC (China)

Air travel remains a growth market

20-year ld l

12

World annual traffic(RPKs - trillions)

ICAO t t l t ffi

AirbusGMF 2009

world annual traffic growth

4.7%

Ai t ffi

10

total traffic GMF 2009

Air trafficwill doublein the next15 years6

8Air traffic

has doubledevery 15 years

oprie

tary

doc

umen

t.

15 years

4

every 15 years

s re

serv

ed. C

onfid

entia

l and

pro

0

2

© A

IRBU

S S.

A.S.

All

right

s

Source: ICAO, Airbus

1970 1980 1990 2000 2010 2020 2030

Asia to lead in world traffic by 2028

20-year world annual traffic growth

Traffic by airline domicile

RPK (billi )

traffic growth4.7%

% of 2028 World RPKs

33%

20-year growth

6 0%

0 500 1,000 1,500 2,000 2,500 3,000 3,500

Asia

RPKs (billions)

2008 traffic 2009-2028 growth

% of 2008 World RPKs

26% 33%

26%

20%

6.0%

4.3%

2.4%

Europe

North America

2008 traffic 2009 2028 growth

28%

31%

oprie

tary

doc

umen

t. 8%

6%

6.9%

5.8%

Middle East

Latin America

5%

4%

s re

serv

ed. C

onfid

entia

l and

pro

4%

3%

5.9%

5.2%

CIS

Africa

3%

3%

© A

IRBU

S S.

A.S.

All

right

s

Flows including Africa, India and China to grow fastest

Domestic Turkey

Top 10 growth markets next 20 years

10.1%

N. Africa - P.R.China

Domestic India

9.4%

10.0%

Drivers:D l tiCIS - P.R.China

Sub S.Africa – P.R. China

9.4%

9.3%

• Deregulation• Economic growth• Population growth

oprie

tary

doc

umen

t. Middle East - S. Africa

Sub S.Africa – N. Africa

9.1%

9.0%

Population growth• Inter regional trade

s re

serv

ed. C

onfid

entia

l and

pro

P.R. China - S. Africa

N.Africa - S. Africa

8.7%

8.6%

© A

IRBU

S S.

A.S.

All

right

s

P.R.China - Russia 8.5%

India will be the fastest growing country for air travel for the next 10 years

RPK growth: annual average 2009RPK growth: annual average 2009--20182018

E rope

g o t a ua a e age 009g o t a ua a e age 009 0 80 8

CISEurope6.2%

North America8 7%

6.4%

Middle East6.1%

8.7%

12.2%

oprie

tary

doc

umen

t.

Asia-Pacific6.8%

Africa7.9%

s re

serv

ed. C

onfid

entia

l and

pro

India World

© A

IRBU

S S.

A.S.

All

right

s

2009-2018 2019-2028 20-year growth

7.9% 6.6% 7.3%

2009-2018 2019-2028 20-year growth

4.6% 4.8% 4.7%

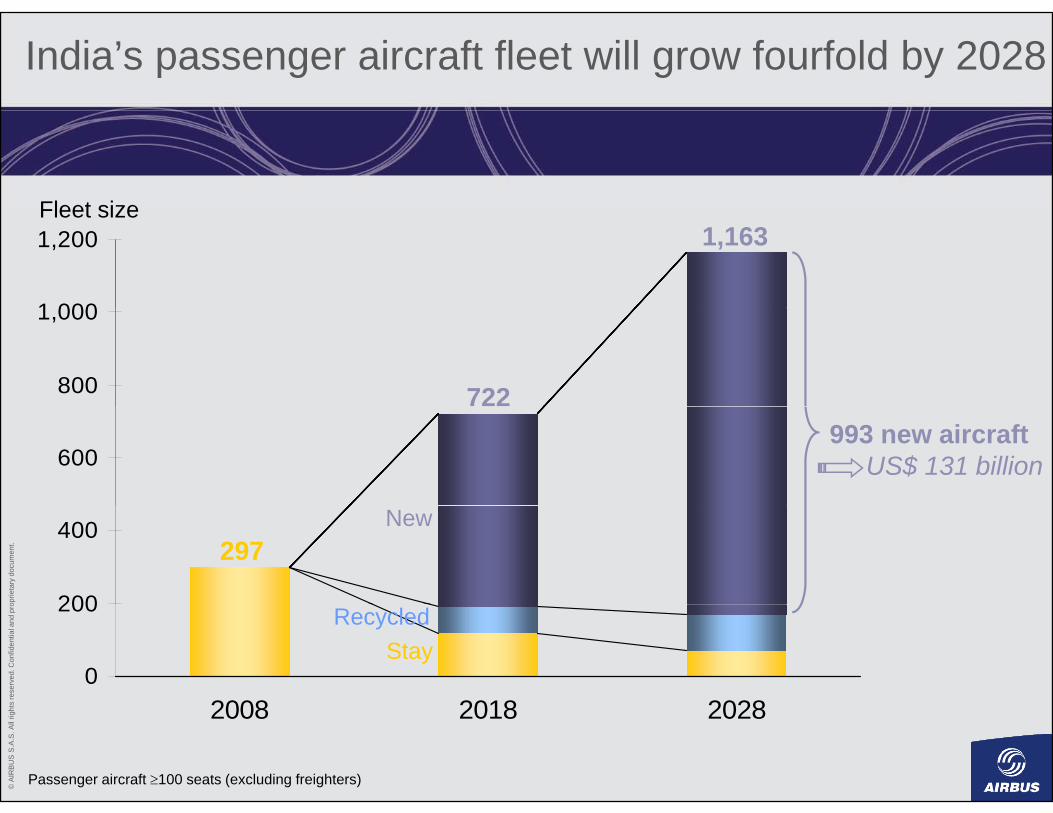

India’s passenger aircraft fleet will grow fourfold by 2028

Fleet size

1 000

1,200Fleet size

1,163

800

1,000

722

600993 new aircraft

US$ 131 billion

oprie

tary

doc

umen

t.

200

400297

New

s re

serv

ed. C

onfid

entia

l and

pro

0

200

2008 2018 2028

RecycledStay

© A

IRBU

S S.

A.S.

All

right

s 2008 2018 2028

Passenger aircraft ≥100 seats (excluding freighters)

Chinese market in next 20 years

• A passenger traffic to be multiplied by 4 p g p y• A passenger aircraft fleet to be multiplied by 3• A dedicated freighter fleet to be multiplied by 7g p y• A market for 2,798 aircraft over 100 seats worth

$353B

oprie

tary

doc

umen

t. • Large cities, congestion will demand larger aircraft• Very large aircraft for all Chinese markets

s re

serv

ed. C

onfid

entia

l and

pro

• 201 VLAs and 725 twin-aisles required in China

© A

IRBU

S S.

A.S.

All

right

s

Mainland China will need 2,798 new passenger & freighter aircraft over the next 20 years

1,8721,872 single-aisles

725725 twin-aisles725725 twin-aisles

oprie

tary

doc

umen

t.

201201 very large aircraft

s re

serv

ed. C

onfid

entia

l and

pro

y g

© A

IRBU

S S.

A.S.

All

right

s

Market value of $353 billion

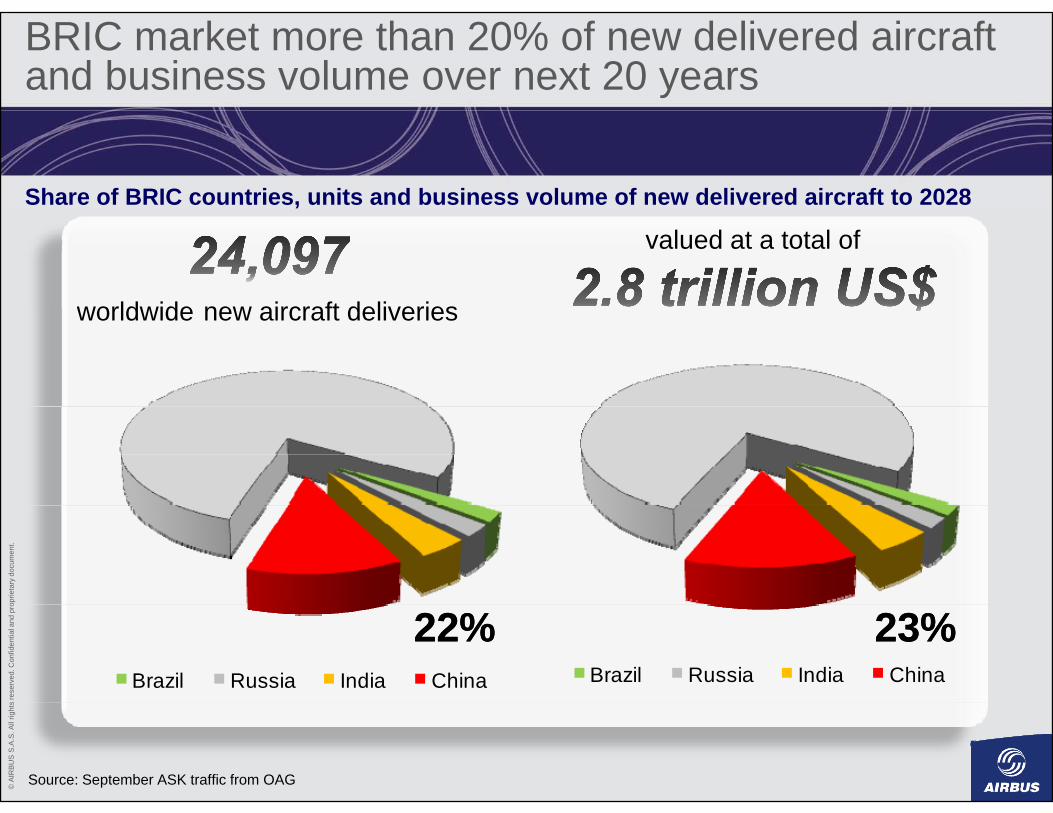

BRIC market more than 20% of new delivered aircraft and business volume over next 20 years

Share of BRIC countries, units and business volume of new delivered aircraft to 2028

worldwide new aircraft deliveries

valued at a total of

worldwide new aircraft deliveries

oprie

tary

doc

umen

t.s

rese

rved

. Con

fiden

tial a

nd p

ro

Brazil Russia India ChinaBrazil Russia India China

22%22% 23%23%

© A

IRBU

S S.

A.S.

All

right

s

Source: September ASK traffic from OAG

Other emerging countries as big as China and India combined

3 000Population (millions)

2,500

3,000

China and India today:

2,000China

more countries to

follow

1,50021 countries

2 billion people

oprie

tary

doc

umen

t.

500

1,000

IndiaBrazilUkraine

R iTurkey

s re

serv

ed. C

onfid

entia

l and

pro

0

500

ArgentinaIndonesiaRussia

© A

IRBU

S S.

A.S.

All

right

s

Emerging countries of tomorrow

Emerging countries of today

Related Documents

![Jianyi Zhang Andrew Gordon Wilson arXiv:1902.03932v2 [cs.LG] … · 2020. 5. 13. · Andrew Gordon Wilson New York University andrewgw@cims.nyu.edu ABSTRACT The posteriors over neural](https://static.cupdf.com/doc/110x72/5ff4ecea7fe9606d0f2a240f/jianyi-zhang-andrew-gordon-wilson-arxiv190203932v2-cslg-2020-5-13-andrew.jpg)