Analyst Presentation Q1 2016 Frankfurt – May 4, 2016 Dr. Matthias Zieschang CFO

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Analyst Presentation Q1 2016Frankfurt – May 4, 2016

Dr. Matthias Zieschang

CFO

Disclaimer

This document has been prepared by Fraport solely for use in this presentation.

The information contained in this document has not been independently verified. No representation or warranty – whetherexpress or implied – is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctnessof the information or opinions contained therein. Neither the company nor any of its affiliates, advisors or representatives shallhave any liability whatsoever (in negligence or otherwise) for any loss arising from any use of this document or its content orotherwise arising in connection with this document.

This document does not constitute an offer or invitation to purchase or subscribe for any shares and neither this document norany part of it shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever.

This document contains forward-looking statements that are based on current estimates and assumptions made by themanagement of Fraport to the best of its knowledge. Such forward-looking statements are subject to risks and uncertainties,the non-occurrence or occurrence of which could cause the actual results – including the financial condition and profitability ofFraport – to differ materially from or be more negative than those expressed or implied by such forward-looking statements.This also applies to the forward looking estimates and forecasts derived from third-party studies. Consequently, neither thecompany nor its management can give any assurance regarding the future accuracy of the opinions set forth in this documentor the actual occurrence of the predicted developments.

By accepting this document, you agree with the foregoing.

Fraport Analyst Presentation Q120162

Fraport Analyst Presentation Q120163

Agenda

- Traffic Insight

- Business Update

- Q1 2016 Financials

- FY 2016 Outlook

Traffic Insight

Group Passenger Results (stakes above 10%)

Fraport Analyst Presentation Q120164

IATA

CodeAirport Share

March

2016

Dprevious

year

YTD

2016

Dprevious

year

FY

2015

CAGR

2010-

2015

FRA Frankfurt, Germany 100% 4,787 +3.9% 12,926 +3.3% 61,032 +2.9%

LJU Ljubljana, Slovenia 100% 94 +3.3% 245 +3.9% 1,438 +0.7%

LIM Lima, Peru 70% 1,502 +12.1% 4,482 +11.5% 17,113 +10.7%

BOJ Burgas, Bulgaria 60% 12 +29.6% 35 +15.4% 2,360 +4.7%

VAR Varna, Bulgaria 60% 29 +20.1% 83 +23.4% 1,399 +3.1%

AYT Antalya, Turkey 51% 999 -4.0% 2,352 -2.8% 27,523 +4.4%

LED St. Petersburg, Russia 35.5% 830 -3.9% 2,316 -6.2% 13,500 +9.8%

HAJ Hanover, Germany 30% 406 +0.9% 1,008 +3.4% 5,453 +1.5%

XIY Xi‘an, China 24.5% 2,911 +7.5% 8,596 +13.0% 32,970 +12.9%

Traffic Insight

Focus Frankfurt

Passengers

Movements

MTOW

Cargo

MAR 2016 YTD 2016

12,296

105,844

6,861

497

4,787

37,503

2,447

183

+3.9

+0.8

+3.2

-1.6

+3.3

+1.0

+3.4

-1.2

D %D %

in `000

in `000 tons

65%

70%

75%

80%

85%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Seat load factor

2016 2015

FY 2015

in `000 tons

Passenger per movement

120 125 130 135 140

Passenger guidance FY2016:

Growth between ~1% and ~3%

+2.6 Pass.

YTD 2016

YTD 2015

61,032

468,153

29,543

2,077

Passenger figures according to ACI, commercial traffic only; cargo includes air freight and air mail

Fraport Analyst Presentation Q120165

Traffic Insight

Focus Frankfurt

Fraport Analyst Presentation Q120166

Northern Africa

-18%

-14%-21%

-17%

Far East

-3%

Middle East

+3%

-23%

FRA

• Weakness on outbound routes esp. to touristic destinations of Islamic countries

• Strong increase on routes to the Caribbean, Thailand, and Middle East

• Far East among others down due to stop of Malaysian services

• China with growth in April

• Pre-bookings for Summer period show continuation of negative trend with regard

to Northern Africa and Turkey

Change vs. April 2015

Central America

+20%

Major declining destinations

Traffic Insight

Focus Antalya

Fraport Analyst Presentation Q120167

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

January February March April May June July August September October November December

Domestic 2016 Domestic 2015 International 2016 International 2015

• Strong seasonality in passenger traffic: <10% of total traffic in q1

• Low seasonality in domestic traffic: each month only between 400k and 600k

• Domestic traffic = between 20 and 25% of total traffic on FY basis

• High seasonality in international traffic: 5% of total in q1, 15% in q4 and

80% in q2 and q3

• Q1 figures positively impacted by domestic traffic: +13% compared to 2015 and

negatively by international traffic -22%

Passengers in million

Traffic Insight

Focus Antalya

0

1

2

3

4

January February March April May June July August September October November December

2015 2016

Fraport Analyst Presentation Q120168

• High volatility due to Russian sanctions and terrorist attacks in Ankara and Istanbul

• Decrease driven by Russian (-85%) and German passengers (-27%)

• Compensating effects from domestic traffic (YTD April +13%)

• Increased uncertainty regarding traffic development in main season

• Feedback from tour operators and tourism fairs: No Russian charter flights

in 2016 expected, strong decrease of European passengers possible

• Last-minute bookings could mitigate the decrease

YTD April: c.-30%

International passengers in million

Fraport Analyst Presentation Q120169

Agenda

- Traffic Insight

- Business Update

- Q1 2016 Financials

- FY 2016 Outlook

10

Business Update

Frankfurt & External Activities

Fraport Analyst Presentation Q12016

Terminal 3

• Excavation work finished on time

• Special civil engineering to follow up from Q4/2016

• Landside access also to be started in next few months

Multichannel

• New stores included in online platform

• Test phase of lounge-delivery and inflight shopping started

Greek regional airports

• +21% passengers in q1 2016

• Antitrust approval granted

• Good process in project financing

• CEO and CTO appointed

Fraport Analyst Presentation Q1201611

Agenda

- Traffic Insight

- Business Update

- Q1 2016 Financials

- FY 2016 Outlook

Group P&L Q1 2016

Decline in EBITDA, good Net Result

Fraport Analyst Presentation Q12016

P&L in € mil. Q1 16 Q1 15 %

Revenue 573 576 -0.6

- excl. IFRIC 12 568 572 -0.8

EBITDA 146 153 -4.9

EBIT 64 72 -10.7

EBT 22 16 +39.7

Group result 15 11 +42.5

EPS in € 0.16 0.11 +45.5

› Adjusted for consolidation effects:

c.15m revenue growth

› Headwind from Retail revenue, non-

capitalizbl. capex & multi channel cost

› Improvement in financial result from

lower interest expenses and strong

negative 2015 CHF loan revaluation

› Bottom-line results with good growth

Comments

Revenue by segment in € mil.

Revenue

Q1 2015

Aviation Retail &

Real Estate

Ground

Handling

External

Activities &

Services

Revenue

Q1 2016

±0

-8

+6 573-1

External

Activities

Services

EBITDA by segment in € mil.

EBITDA

Q1 2015

Aviation Retail &

Real Estate

Ground

Handling

EBITDA

Q1 2016

153+2 +1 146

-9

-1

External

Activities &

Services

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

576

12

Group P&L Q1 2016

Growth in External & Ground Handling EBITDA

Fraport Analyst Presentation Q12016

EBITDA

Q1 2015

Other

income

Cost of

materials ex.

IFRIC 12

Staff

cost

EBITDA

Q1 2016

Revenue

ex. IFRIC 12

Other

opex

153

-2 -1

146

€ -7.5 mil.

-1

IFRIC 12

revenue

IFRIC 12

cost of

materials

-5+1

20.0%

58.2%

21.8%

Segment share in Group EBITDA Q1 2015 Segment share in Group EBITDA Q1 2016

20.4%

55.1%

1.3%

23.2%Aviation

Retail &

Real Estate

External

Activities &

Services Aviation

Retail &

Real Estate

External

Activities &

Services

Ground

Handling:

negative

Ground

Handling

Due to commercial rounding slight discrepancies may occur when summing up

+1

13

€ mil.

-1

Group P&L Q1 2016

Group Result up due to Improvement in Financial Result

Fraport Analyst Presentation Q12016

Split of financial result Comments

Group result

Q1 2015

EBITDA D&A Financial

result

Taxes Group result

Q1 2016

EPS

Q1 2015

EPS

Q1 2016

€ mil Q1 16 Q1 15 %

Interest income 9 8 +10.3

Interest

expenses-38 -42 -

At equity result -12 -13 -

Other result -1 -9 -

Financial result -43 -56 -

› Improved interest result from lower interest

rates and lower indebtedness

› Antalya in off-season mildly negative on at

equity result

› Positive results in Hanover and Xi’an with

compensating effects

› Other financial result up, due to lack of strong

negative CHF loan revaluation effect in

previous year

11 -7

15

±0

-2

+€4.5 mil.

€0.16

€0.11

+€0.05

+13

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

14

€ mil.

Group Asset & Financial Situation Q1 2016

Lower Off-Season OCF leads to decline in Free Cash Flow

Fraport Analyst Presentation Q12016

FY 2016 OutlookQ1 2016 development

PPEInvestment

property

Operating

cash flow

Intangible

assets

Airport

operating

projects

90

45

114 -3 -46

-4-4

-1 -58

-5±0

+19

DVDs from

investments

Free cash

flow

+8 65

› 2016 capex on 2015 level or slightly above

› Subject to dividends from Antalya, 2016 FCF

expected to be on 2015 level

› Including DVD payout, 2016 FCF with

potential to de-lever Group by up to c.10 % to

net debt/EBITDA < 3x w/o Greek deal

› Lower OCF due to c.€13 mil. increase in one-

off tax payments and minor changes in

working capital

› Spending on PPE ahead of q1 2015 due to

mild winter

› Seasonal increase in DVDs from investments

leads to FCF of €45 mil.

Due to commercial rounding slight discrepancies may occur when summing up

Q1 2016 Q1 2015

€ mil.

15

Group Asset & Financial Situation Q1 2016

Slight De-Leverage to €2.75 bn

Fraport Analyst Presentation Q12016

Balance sheet

› Equity unchanged at €3.5 bn.

› Gearing ratio at 83%, slightly down on

Dec. 31, 2015

› Equity ratio w/o profit earmarked for

distribution and minority interests at 38%

(Dec. 31, 2015: 37%)

Cash development

› FCF slightly takes up liquidity

› Net debt slightly down at €2.75 bn.

› Despite positive FCF: FY 2016 liquidity to go

down due to debt repayments, DVD cash out

+ potential Greek upfront payment

4565

1,070 1,043

3,819 3,817

2,749 2,774

3,520 3,512

83% 84%

March 31, 2016

Liquidity Gross debt Net debt Equity Gearing2FCF1

Dec. 31, 2015

€ mil.

Due to commercial rounding slight discrepancies may occur when summing up

1) FCF pre-dividend payout; figures correspond to Q1 figures 2) Net debt divided by equity less non-controlling interests and profit earmarked for distribution

16

Segment Aviation Q1 2016

Flat Revenue and Earnings

Fraport Analyst Presentation Q12016

P&L in € mil. Q1 16 Q1 15 %

Revenue 200 200 -0.2

- Airport charges 166 164 +0.9

- Security Services 25 27 -5.6

- Other revenue 9 10 -4.1

EBITDA 30 31 -3.3

EBIT -1 0 -

Employees 6,091 5,976 +1.9

› Increase in airport charges due to +3%

passengers and +1% movements

› Security business down due to loss of

T1 concourse B contract

› Headwind from non-capitalizable capex

and higher maintenance cost

Comments

EBITDA

Q1 2016

Revenue Other

income

Staff

cost

Other EBITDA

Q1 2016

31 ±0 -2 30

EBITDA performance in € mil. Revenue split

Aviation charges83.0%

12.5%

4.5%

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

17

Other

+2 -1Security Services

Segment Retail & Real Estate Q1 2016

Weak Retail & additional Cost decrease EBITDA

Fraport Analyst Presentation Q12016

P&L in € mil. Q1 16 Q1 15 %

Revenue 113 113 -0.6

- Retail 44 46 -6.0

- Real Estate 49 47 +4.1

- Parking 19 19 -1.1

- Other revenue 2 1 +30.8

EBITDA 80 89 -10.0

EBIT 59 68 -13.2

Employees 645 611 +5.6

› Decline in Retail revenue despite

growth in passenger volume

› Higher cost from non-capitalizable

capex, cost to start multi-channel

program & allocation of internal cost

› EBITDA and EBIT down on previous

year

› EBITDA margin at 71%

Comments

EBITDA

Q1 2015

Revenue Other

income

Staff

cost

Other EBITDA

Q1 2016

89 -1 -1 -6 80

EBITDA performance in € mil. Revenue split

38.7%

43.1%

16.7%

1.5%

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

-1

18

Other

Parking

Real Estate

Retail

Segment Retail & Real Estate Q1 2016

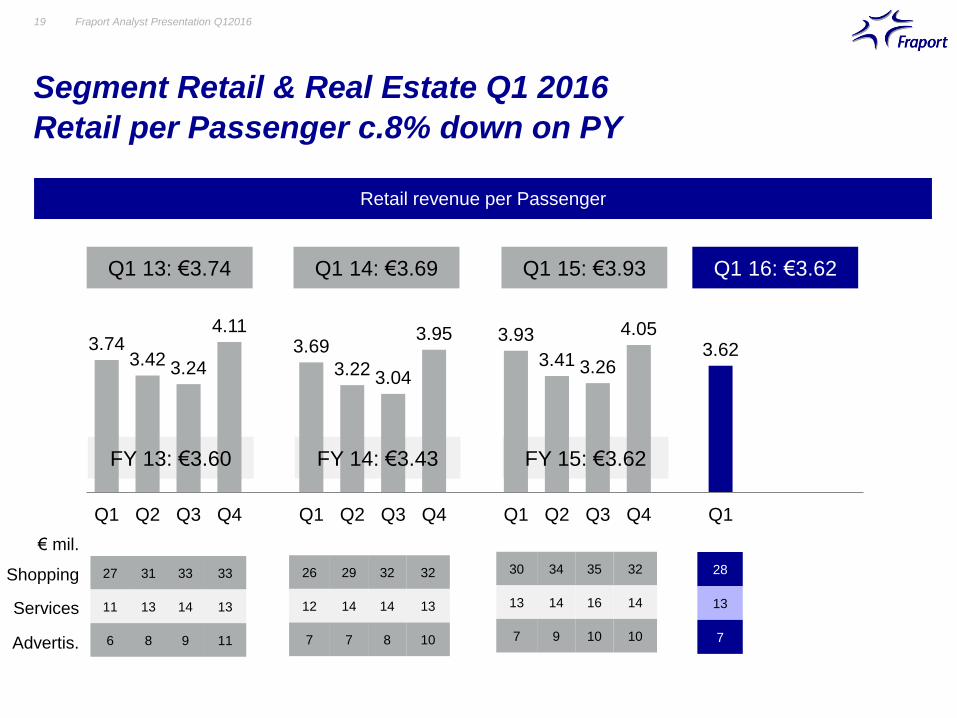

Retail per Passenger c.8% down on PY

Fraport Analyst Presentation Q1201619

Retail revenue per Passenger

3.743.42 3.24

4.113.69

3.22 3.04

3.95 3.93

3.41 3.26

4.053.62

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

€ mil.

Shopping

Services

Advertis.

Q1 13: €3.74 Q1 14: €3.69 Q1 15: €3.93 Q1 16: €3.62

FY 13: €3.60 FY 14: €3.43 FY 15: €3.62

27 31 33 33

11 13 14 13

6 8 9 11

26 29 32 32

12 14 14 13

7 7 8 10

30 34 35 32

13 14 16 14

7 9 10 10

28

13

7

Segment Retail & Real Estate Q1 2016

Negative Development of Core Spending Destinations

Fraport Analyst Presentation Q1201620

Volume

Development

Change vs. q1 2015

in %

Retail Revenue

per Passenger

in EUR

Change vs. q1 2015

in %

-2-13

5 1

-7

-16

-25

-2-11

10

China Russia South

Korea

Japan Vietnam USA Turkey Germany India

71

4

-2

7

12

-3

210 6

Source: sales/revenue data of Gebr. Heinemann by destinations

Top 5 by Retail Value Top 5 by Volume

UAE

Segment Ground Handling Q1 2016

Disposal of Cargo Subsidiary grows EBITDA & margin

Fraport Analyst Presentation Q12016

P&L in € mil. Q1 16 Q1 15 %

Revenue 146 155 -5.4

- Ground Handling 73 88 -17.0

- Infrastructure 69 66 +3.8

- Other revenue 4 - >100

EBITDA 2 0 >100

EBIT -8 -10 -

Employees 8,993 9,505 -5.4

› Adjusted for consolidation effect:

c.6m revenue & 0.5m EBITDA growth,

EBIT: flat

› Traffic performance leads to underlying

revenue and EBITDA growth

› Slightly higher D&A leads to flat

underlying EBIT

Comments

EBITDA

Q1 2015

Revenue Other

income

Staff

cost

Other EBITDA

Q1 2016

0 -8

+0

+2

+82

EBITDA performance in € mil. Revenue split

Ground Handling50.1%

47.0%

2.9%

Infrastructure

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

21

Other revenues

Segment External Activities & Services Q1 2016

Lima, Ljubljana and Twin Star continue to perform

Fraport Analyst Presentation Q12016

Comments

LAP Other EBITDA

Q1 2016

33+4

34

EBITDA performance in € mil. Revenue split

63.1%

2.0%

11.9%

6.5%16.5%

Due to commercial rounding slight discrepancies may occur when summing up, percent changes based on unrounded figures

Lima

Other

Twin Star

Ljubljana

+1

LJU Twin

Star

AMU Air IT

+1 -5

Airmall

P&L in € mil. Q1 16 Q1 15 %

Revenue 113 107 +5.6

- excl. IFRIC 12 109 104 +4.5

EBITDA 34 33 +1.2

EBIT 14 13 +4.6

Employees 4,516 4,550 -0.7

› Adjusted for consolidation effect:

c.9m revenue, 0.7m EBITDA & 0.8m

EBIT growth

› Good growth in Lima from traffic and

positive US$ effect

› Ljubljana, Twin Star & AMU with solid

operations

› Additional maintenance cost in FRA

22

EBITDA

Q1 2015

±0 ±0

External Activities Q1 2016

Fully consolidated Investments

Fraport Analyst Presentation Q1201623

Figures refer to IFRS accounting, not local GAAP, percent changes based on unrounded figures

€ mil. Q1 16 Q1 15 % Q1 16 Q1 15 % Q1 16 Q1 15 % Q1 16 Q1 15 %

Revenue

-ex IFRIC 12

14

-

13

-

0.7

-

7

-

7

-

8.8

-

72

67

64

60

12.6

11.2

2

2

2

2

21.1

27.8

EBITDA

margin

adjusted

2

17.8%

-

3

20.1%

-

-11.1

-

-

2

29.7%

-

2

25.0%

-

29.4

-

-

27

37.1%

39.7%

23

36.1%

38.2%

15.7

-

-

-1

-

-

-2

-

-

-

-

-

EBIT

margin

adjusted

0

2.2%

-

1

4.5%

-

-50.0

-

-

0

-

-

-1

-

-

-

-

-

22

31.0%

33.3%

19

29.1%

30.8%

20.0

-

-

-4

-

-

-4

-

-

-

-

-

Result 1 1 -25.0 0 -1 - 13 10 25.5 -5 -6 -

Passengers

in mil.

- - - 0.2 0.2 3.9 4.5 4.0 11.5 0.1 0.1 20.9

Airmall Twin StarLjubljana Lima

External Activities Q1 2016

At Equity consolidated Investments

Fraport Analyst Presentation Q1201624

Except for Xi’an all figures refer to IFRS accounting, percent changes based on unrounded figures

€ mil. Q1 16 Q1 15 % Q1 16 Q1 15 % Q1 16 Q1 15 % Q1 16 Q1 15 %

Revenue

-ex IFRIC 12

18

-

21

-

-16.2

-

33

33

46

44

-27.9

-24.5

32

-

31

-

2.6

-

51

-

44

-

16.6

-

EBITDA

margin

adjusted

8

46.0%

-

12

55.2%

-

-30.2

-

-

12

35.9%

35.9%

19

42.1%

44.0%

-38.5

-

-

5

14.8%

-

3

8.7%

-

74.1

-

-

24

46.7%

-

19

43.7%

-

24.5

-

-

EBIT

margin

adjusted

-16

-

-

-13

-

-

-

-

-

4

12.5%

12.5%

9

20.2%

21.1%

-55.4

-

-

0

-

-

-2

-

-

-

-

-

11

21.3%

-

8

18.0%

-

38.0

-

-

Result -33 -31 - -9 34 - -1 -4 - 7 4 86.6

Passengers

in mil.

2.4 2.4 -2.8 2.3 2.5 -6.2 1.0 1.0 3.4 8.6 7.5 13.0

Xi‘AnPulkovo HanoverAntalya

Fraport Analyst Presentation Q1201625

Agenda

- Traffic Insight

- Business Update

- Q1 2016 Financials

- FY 2016 Outlook

FY 2016 Outlook*

Unchanged Outlook

Fraport Analyst Presentation Q1201626

2016 Outlook

Passengers FRA between +~1% and +~3%

Revenue up to € 2.65 bn

EBITDA between ~€ 850 and ~ 880 mil.

EBIT between ~€ 520 and ~ 550 mil.

Group result** on PY level or slightly above

Dividend proposal at least stable

*Without taking account of potential closing of Greek deal

** Group result before minorities

Thank you for your Attention!

www.meet-ir.com

Fraport Analyst Presentation Q1201628

Appendix

– Subsequent financial information –

Appendix

Special Effects Q1 2016

Fraport Analyst Presentation Q1201629

€ mil. Q1 2016 Q1 2015

Group financial result

Market valuation of derivatives & F/X fluctuations -1.3 -9.0

Segment Ground Handling

FCS – disposed Nov. 2015

Revenue - 14.7

EBITDA - -1.5

EBIT - -1.9

Segment External Activities

IFRIC 12 revenue 4.9 3.6

Air Transport IT – disposed April 2015

Revenue - 3.4

EBITDA - 0.3

EBIT - 0.2

1,070.4

3,819.4

441.5295.0

517.0

1,132.6

185.8422.5 400.7

32.6 2.6

348.6

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Liquidityas of Mar31, 2016

FinancialLiabilities

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025++

nominal

Bookvalue

Fraport debt conditions on average

~ 3.4% interest rate

~ 4.5 years maturity

€ mil.

Appendix

Maturity Profile & Cash Position as at March 31, 2016

Fraport Analyst Presentation Q1201630

Appendix

Status Greece Acquisition

Fraport Analyst Presentation Q1201631

Airports 14 Greek regional airports, 77% international share, around 23 million passengers in 2015

Fraport Share &

Partner

Fraport will hold minimum 65 percent

Upfront payment € 1.2 bn. upfront payment

Concession Payment 22.9 mil. fixed annual concession payments (indexed with Greek inflation rate)

From 2020 variable payment of ~28.5% of EBITDA (before variable concession payment )

Concession Length 40 years

Capex ~€ 330 mil. capex requirements between 2017-2020, afterwards maintenance capex,

capex for further extension depending on traffic growth

Regulation Dual Till

Airport

Charges

Capped at € 13 per departing passenger in 2017, after initial capex capped at € 18.50, thereafter

indexation with 90% of the Greek inflation rate annually

Retail Development Very small retail outlets existing; space will roughly triple after first construction phase; new

operating concepts like walk through will be introduced

Traffic Growth

Assumption

Not disclosed in detail - business case assumes conservative growth over concession period of

about 2.5% p.a.

Appendix

IR Contact

Fraport Analyst Presentation Q1201632

Fraport AG

Frankfurt Airport Services Worldwide

60547 Frankfurt am Main

www.meet-ir.com

+49 69 690 – [email protected]

Stefan J. Rüter

Head of Finance

& Investor Relations

+49 69 690-74840

Svenja Ebeling

Investor Relations Assistant

+49 69 690-74842

Florian Fuchs

Investor Relations Manager

+49 69 690-74844

Maximilian Schultheis

Financial Reporting Manager

+49 69 690-29996

Tanja Nagel

Financial Reporting Manager

+49 69 690-74846

Related Documents