Analyst Presentation Full Year 2015 Results (Audited) Jakarta 24 February 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Analyst Presentation Full Year 2015 Results (Audited)

Jakarta

24 February 2016

2

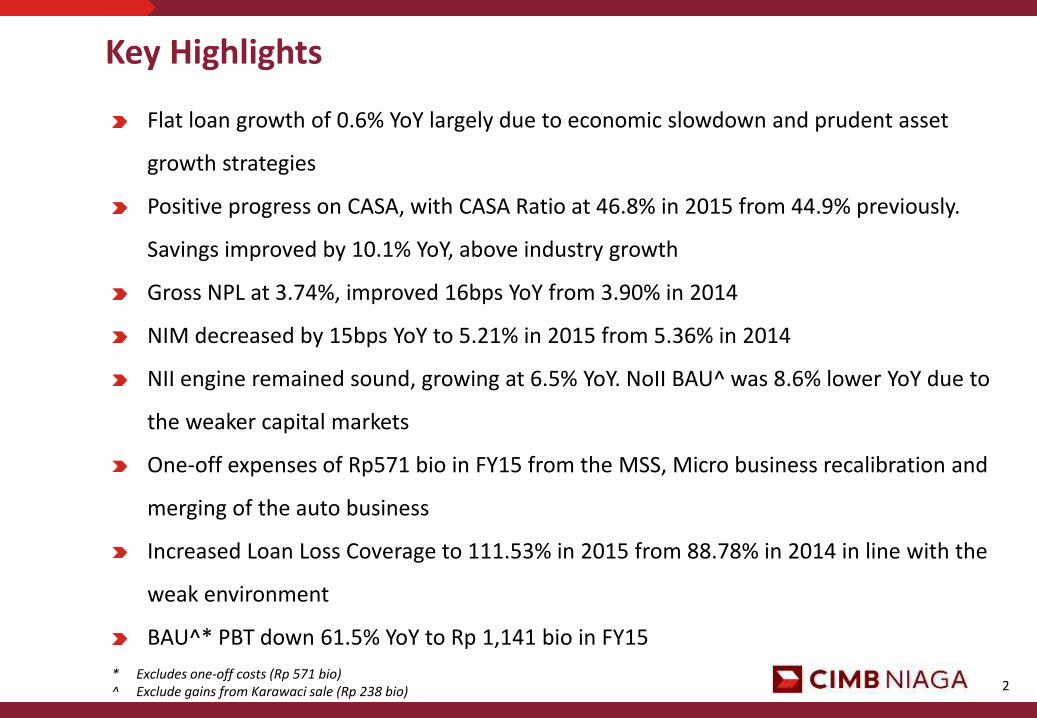

Key Highlights

Flat loan growth of 0.6% YoY largely due to economic slowdown and prudent asset

growth strategies

Positive progress on CASA, with CASA Ratio at 46.8% in 2015 from 44.9% previously.

Savings improved by 10.1% YoY, above industry growth

Gross NPL at 3.74%, improved 16bps YoY from 3.90% in 2014

NIM decreased by 15bps YoY to 5.21% in 2015 from 5.36% in 2014

NII engine remained sound, growing at 6.5% YoY. NoII BAU^ was 8.6% lower YoY due to

the weaker capital markets

One-off expenses of Rp571 bio in FY15 from the MSS, Micro business recalibration and

merging of the auto business

Increased Loan Loss Coverage to 111.53% in 2015 from 88.78% in 2014 in line with the

weak environment

BAU^* PBT down 61.5% YoY to Rp 1,141 bio in FY15

* Excludes one-off costs (Rp 571 bio) ^ Exclude gains from Karawaci sale (Rp 238 bio)

CIMB Niaga: FY 2015 Results Financial Results

4

(Rp bil) 3Q15 BAU*

4Q15 BAU*

QoQ FY14 BAU^

FY15 BAU*

YoY

Interest Income 5,696 5,604 -1.6% 20,813 22,319 7.2%

Interest Expense (2,718) (2,742) 0.9% (10,124) (10,933) 8.0%

Net Interest Income 2,978 2,862 -3.9% 10,689 11,386 6.5%

Non Interest Income 556 614 10.4% 2,571 2,350 -8.6%

Operating Income 3,534 3,476 -1.6% 13,260 13,736 3.6%

Operating Expenses (1,728) (1,794) 3.8% (6,832) (7,234) 5.9%

GA & Promotion Expenses (899) (1,003) 11.6% (3,714) (3,816) 2.7%

Personnel Expenses (829) (791) -4.6% (3,118) (3,418) 9.6%

Pre Provision Operating Profit 1,806 1,682 -6.9% 6,428 6,502 1.2%

Provision Expenses (1,191) (1,389) 16.6% (3,466) (5,361) 54.7%

PBT 615 293 -52.4% 2,962 1,141 -61.5%

Net Profit 442 238 -46.1% 2,105 856 -59.3%

EPS (Rp, full amount) 17.59 9.46 -46.2% 83.74 34.07 -59.3%

PBT (Actual) 144 193 34.0% 3,200 570 -82.2%

Net Profit (Actual) 89 163 83.1% 2,342 428 -81.7%

Income Statement - Consolidated

* Excludes one-off costs (Rp 571 bio) ^ Exclude gains from Karawaci sale (Rp 238 bio)

5

Financial Position - Consolidated

(Rp tril) Dec-14 Sep-15 Dec-15 QoQ YoY

Cash & Short Term Funds 25.68 27.65 27.09 -2.0% 5.5%

Govt Bonds & Marketable Securities 22.35 26.67 25.91 -2.8% 15.9%

Loans 176.38 178.89 177.36 -0.9% 0.6%

Loan Provision (6.11) (6.85) (7.40) 8.0% 21.1%

Fixed & Other Assets 14.86 17.93 15.89 -11.4% 6.9%

Total Assets 233.16 244.29 238.85 -2.2% 2.4%

Current Account 39.22 45.19 40.44 -10.5% 3.1%

Saving Account 39.17 43.31 43.12 -0.4% 10.1%

Time Deposit & Structured Deposit 96.33 97.22 94.97 -2.3% -1.4%

Total Customer Deposits 174.72 185.72 178.53 -3.9% 2.2%

Other Liabilities 29.99 30.33 31.64 4.3% 5.5%

Total Liabilities 204.71 216.05 210.17 -2.7% 2.7%

Equity 28.45 28.24 28.68 1.6% 0.8%

6

(%) 3Q15 BAU*

4Q15 BAU*

QoQ FY14 BAU^

FY15 BAU*

YoY

ROA 1.01 0.49 1.33 0.47

ROE (shareholders’ fund) 6.19 3.34 7.66 2.99

NIM 5.40 5.25 5.36 5.21

Fee Income / Total Income 15.73 17.66 19.38 17.11

Cost to Income (CIR) 48.88 51.63 51.52 52.67

CASA Ratio 47.66 46.81 44.87 46.81

Loan to Deposit (LDR) 94.93 97.98 99.46 97.98

LDR (Bank Only) 92.04 94.87 95.62 94.87

Gross NPL 3.17 3.74 3.90 3.74

Net NPL 1.47 1.59 1.94 1.59

Cost of Credit 2.67 3.17 2.12 3.02

Impairment – Gross 5.18 5.03 4.79 5.03

Loan Loss Coverage 120.96 111.53 88.78 111.53

Impaired LLC 73.96 82.99 72.38 82.99

Key Ratios - Consolidated

* Excludes one-off costs (Rp 571 bio) ^ Exclude gains from Karawaci sale (Rp 238 bio)

7

(Rp bil)

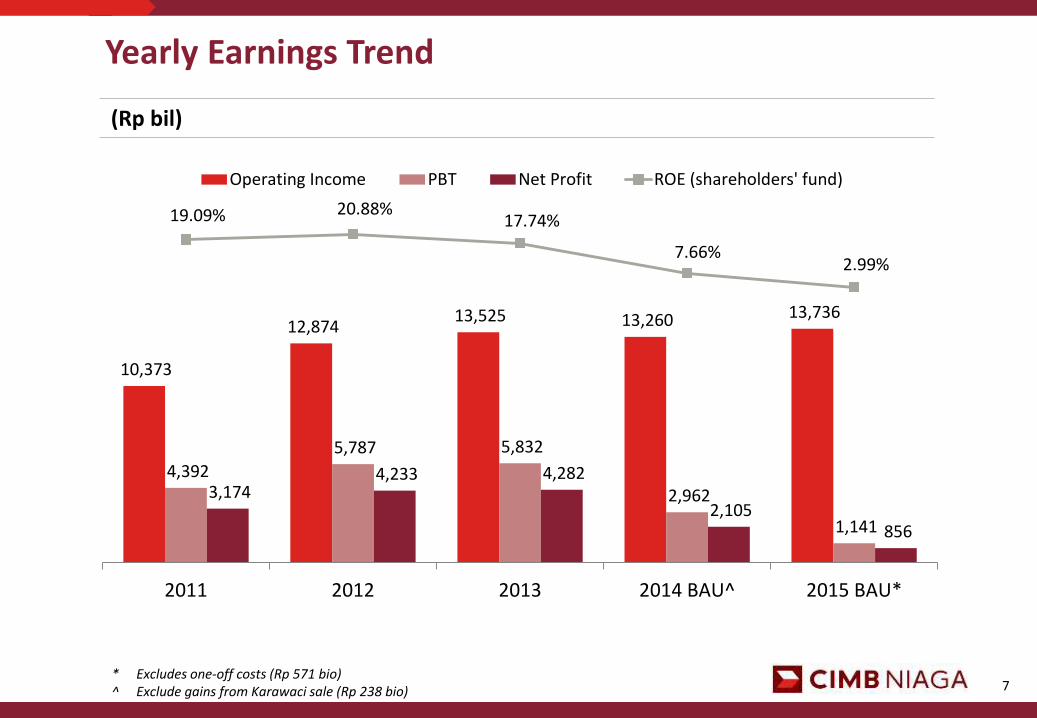

Yearly Earnings Trend

10,373

12,874 13,525 13,260 13,736

4,392

5,787 5,832

2,962

1,141

3,174 4,233 4,282

2,105 856

19.09% 20.88% 17.74%

7.66% 2.99%

2011 2012 2013 2014 BAU^ 2015 BAU*

Operating Income PBT Net Profit ROE (shareholders' fund)

* Excludes one-off costs (Rp 571 bio) ^ Exclude gains from Karawaci sale (Rp 238 bio)

8

Net Interest Margin (%, YTD Annualized)

Net Interest Income Breakdown (incl. FTP)

5.36% 5.22%

5.08% 5.19% 5.21%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Net Interest Income

FY14: Rp 10,689 billion

FY15: Rp 11,386 billion

Quarterly Annualized NIM

4Q14 1Q15 2Q15 3Q15 4Q15

5.63% 5.22% 4.94% 5.40% 5.25%

NIMs Steady

Retail 36%

Commercial 10%

MSME 18%

Corporate 16%

Treasury 20%

9

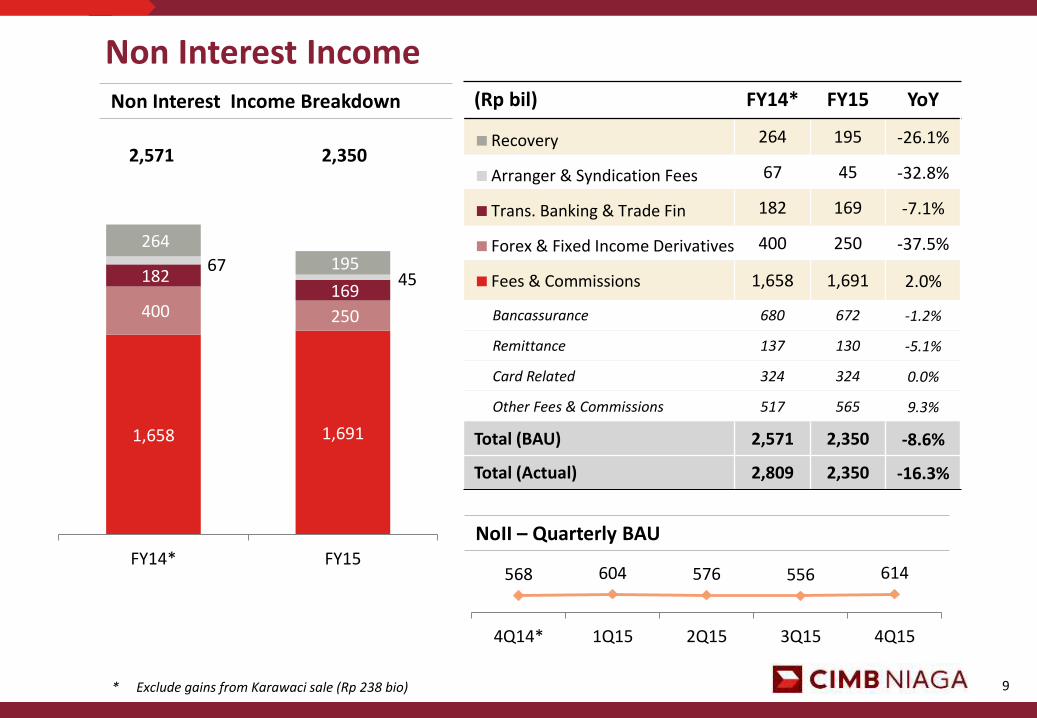

(Rp bil) FY14* FY15 YoY

264 195 -26.1%

67 45 -32.8%

182 169 -7.1%

400 250 -37.5%

1,658 1,691 2.0%

Bancassurance 680 672 -1.2%

Remittance 137 130 -5.1%

Card Related 324 324 0.0%

Other Fees & Commissions 517 565 9.3%

Total (BAU) 2,571 2,350 -8.6%

Total (Actual) 2,809 2,350 -16.3%

NoII – Quarterly BAU

568 604 576 556 614

4Q14* 1Q15 2Q15 3Q15 4Q15

1,658 1,691

400 250

182 169

67 45

264 195

FY14* FY15

Recovery

Arranger & Syndication Fees

Trans. Banking & Trade Fin

Forex & Fixed Income Derivatives

Fees & Commissions

Non Interest Income Non Interest Income Breakdown

2,350 2,571

* Exclude gains from Karawaci sale (Rp 238 bio)

10

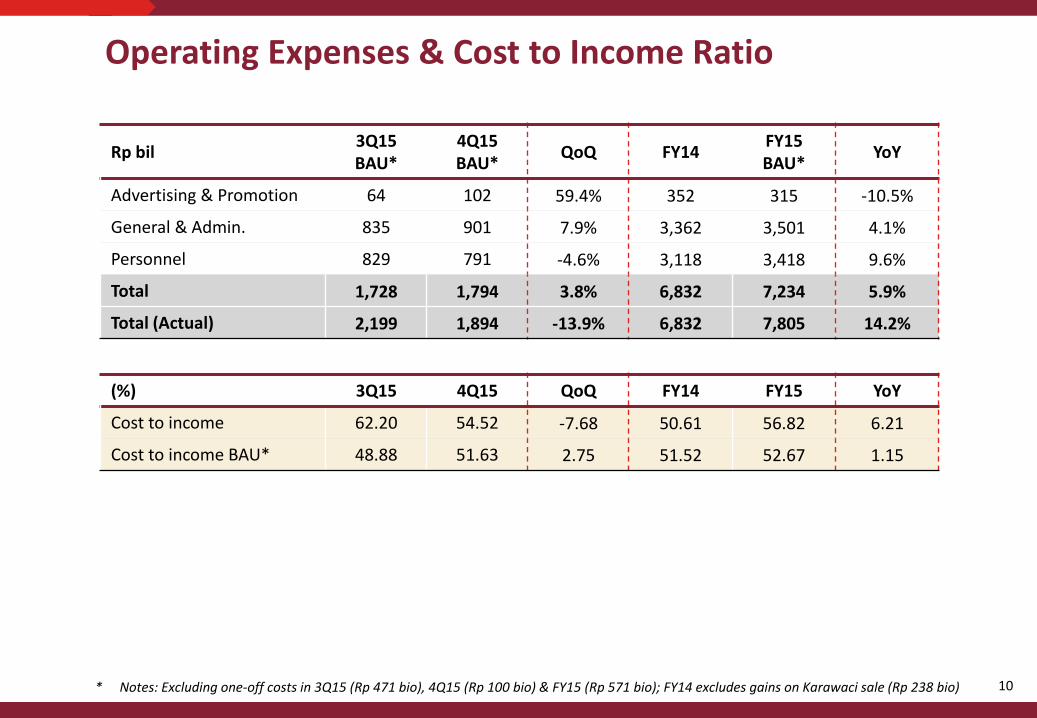

Operating Expenses & Cost to Income Ratio

* Notes: Excluding one-off costs in 3Q15 (Rp 471 bio), 4Q15 (Rp 100 bio) & FY15 (Rp 571 bio); FY14 excludes gains on Karawaci sale (Rp 238 bio)

Rp bil 3Q15 BAU*

4Q15 BAU*

QoQ FY14 FY15 BAU*

YoY

Advertising & Promotion 64 102 59.4% 352 315 -10.5%

General & Admin. 835 901 7.9% 3,362 3,501 4.1%

Personnel 829 791 -4.6% 3,118 3,418 9.6%

Total 1,728 1,794 3.8% 6,832 7,234 5.9%

Total (Actual) 2,199 1,894 -13.9% 6,832 7,805 14.2%

(%) 3Q15 4Q15 QoQ FY14 FY15 YoY

Cost to income 62.20 54.52 -7.68 50.61 56.82 6.21

Cost to income BAU* 48.88 51.63 2.75 51.52 52.67 1.15

11

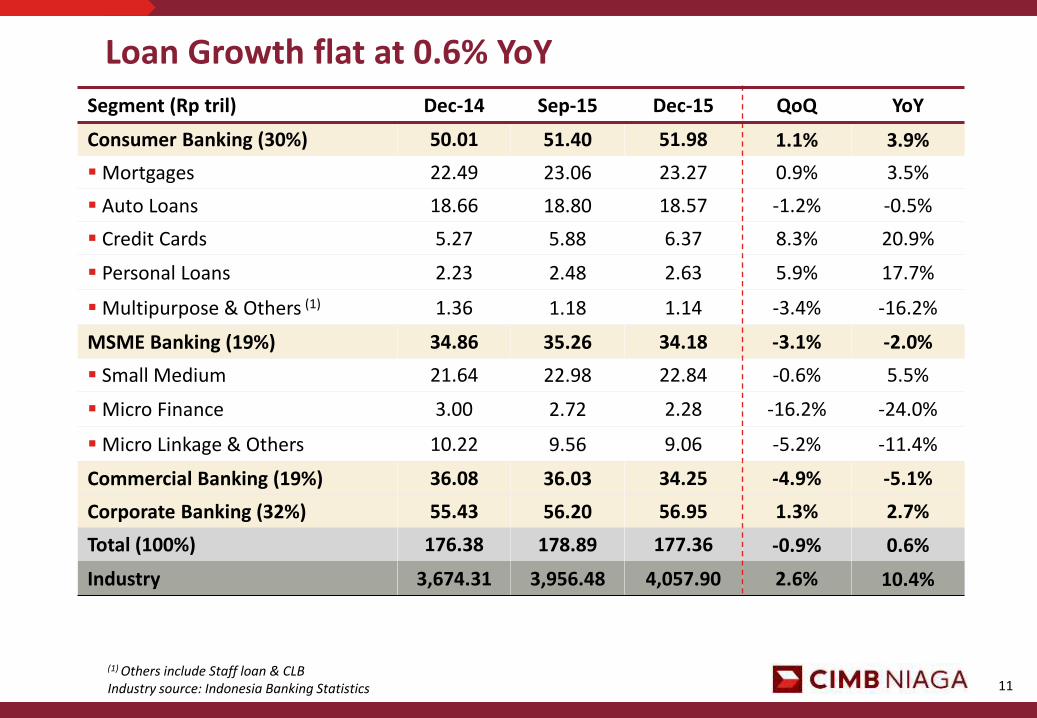

Loan Growth flat at 0.6% YoY

Segment (Rp tril) Dec-14 Sep-15 Dec-15 QoQ YoY

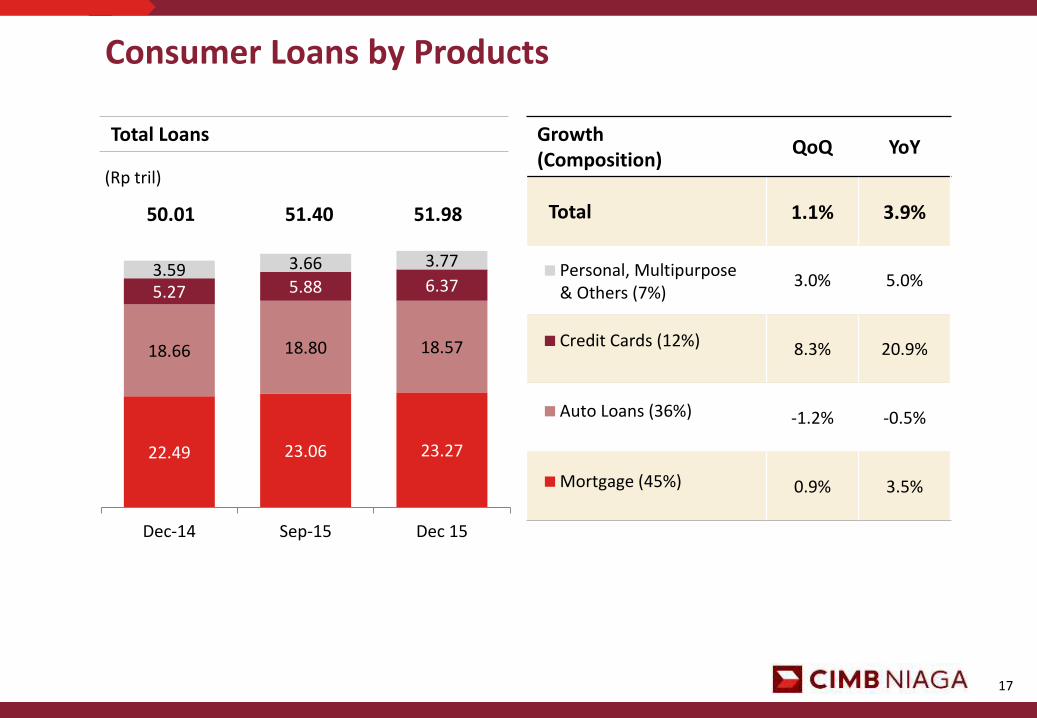

Consumer Banking (30%) 50.01 51.40 51.98 1.1% 3.9%

Mortgages 22.49 23.06 23.27 0.9% 3.5%

Auto Loans 18.66 18.80 18.57 -1.2% -0.5%

Credit Cards 5.27 5.88 6.37 8.3% 20.9%

Personal Loans 2.23 2.48 2.63 5.9% 17.7%

Multipurpose & Others (1) 1.36 1.18 1.14 -3.4% -16.2%

MSME Banking (19%) 34.86 35.26 34.18 -3.1% -2.0%

Small Medium 21.64 22.98 22.84 -0.6% 5.5%

Micro Finance 3.00 2.72 2.28 -16.2% -24.0%

Micro Linkage & Others 10.22 9.56 9.06 -5.2% -11.4%

Commercial Banking (19%) 36.08 36.03 34.25 -4.9% -5.1%

Corporate Banking (32%) 55.43 56.20 56.95 1.3% 2.7%

Total (100%) 176.38 178.89 177.36 -0.9% 0.6%

Industry 3,674.31 3,956.48 4,057.90 2.6% 10.4%

(1) Others include Staff loan & CLB Industry source: Indonesia Banking Statistics

12

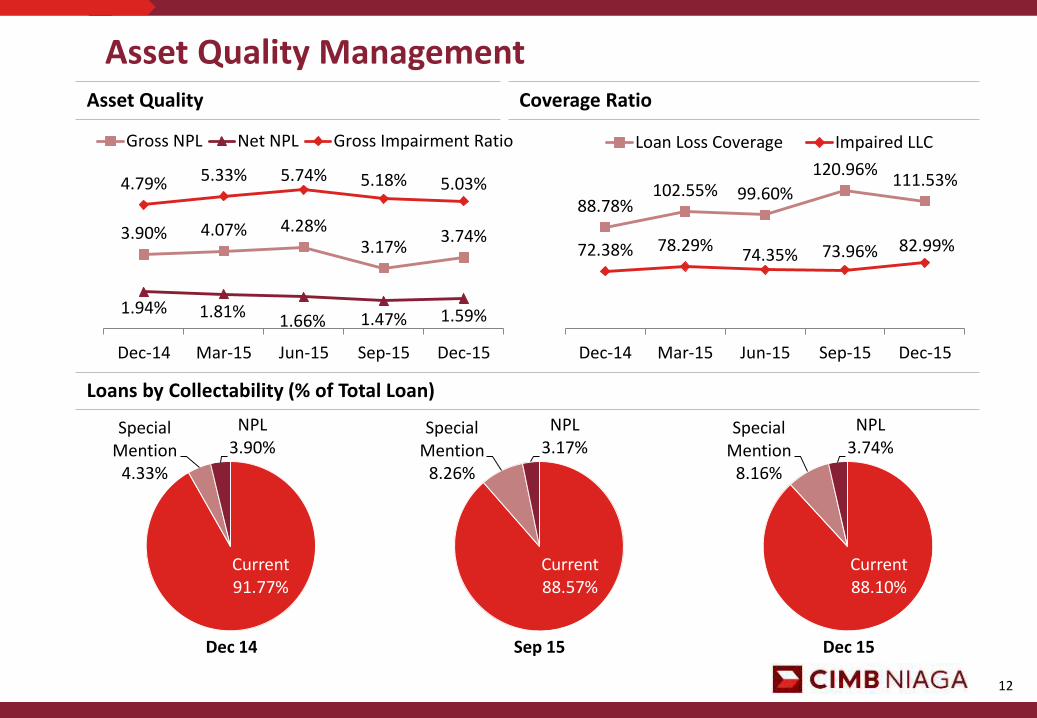

88.78% 102.55% 99.60%

120.96% 111.53%

72.38% 78.29% 74.35% 73.96% 82.99%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Loan Loss Coverage Impaired LLC

Asset Quality Management Asset Quality

Loans by Collectability (% of Total Loan)

Coverage Ratio

3.90% 4.07% 4.28% 3.17%

3.74%

1.94% 1.81% 1.66% 1.47% 1.59%

4.79% 5.33% 5.74% 5.18% 5.03%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Gross NPL Net NPL Gross Impairment Ratio

Current 91.77%

Special Mention

4.33%

NPL 3.90%

Dec 14

Current 88.10%

Special Mention

8.16%

NPL 3.74%

Dec 15

Current 88.57%

Special Mention

8.26%

NPL 3.17%

Sep 15

13

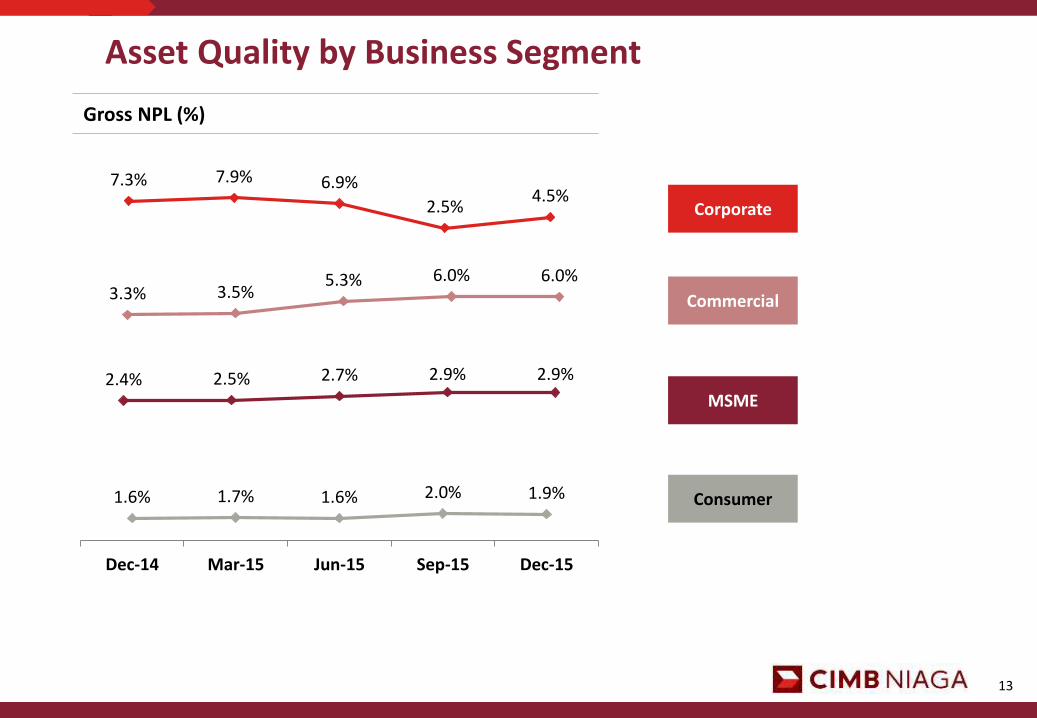

Asset Quality by Business Segment

Gross NPL (%)

7.3% 7.9% 6.9%

2.5% 4.5%

3.3% 3.5% 5.3% 6.0% 6.0%

1.6% 1.7% 1.6% 2.0% 1.9%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

2.4% 2.5% 2.7% 2.9% 2.9%

Corporate

Commercial

MSME

Consumer

14

Rp tril Dec-14 Sep-15 Dec-15 QoQ YoY

CASA 78.39 88.50 83.56 -5.6% 6.6%

Current Account 39.22 45.19 40.44 -10.5% 3.1%

Saving Account 39.17 43.31 43.12 -0.4% 10.1%

Time Deposits & Structured Deposits

96.33 97.22 94.97 -2.3% -1.4%

Total 174.72 185.72 178.53 -3.9% 2.2%

Industry 4,114 4,464 4,413 -1.1% 7.3%

CASA 2,174 2,382 2,384 0.1% 9.7%

Time Deposits 1,940 2,083 2,030 -2.5% 4.6%

Total CASA grew 6.6% YoY

15

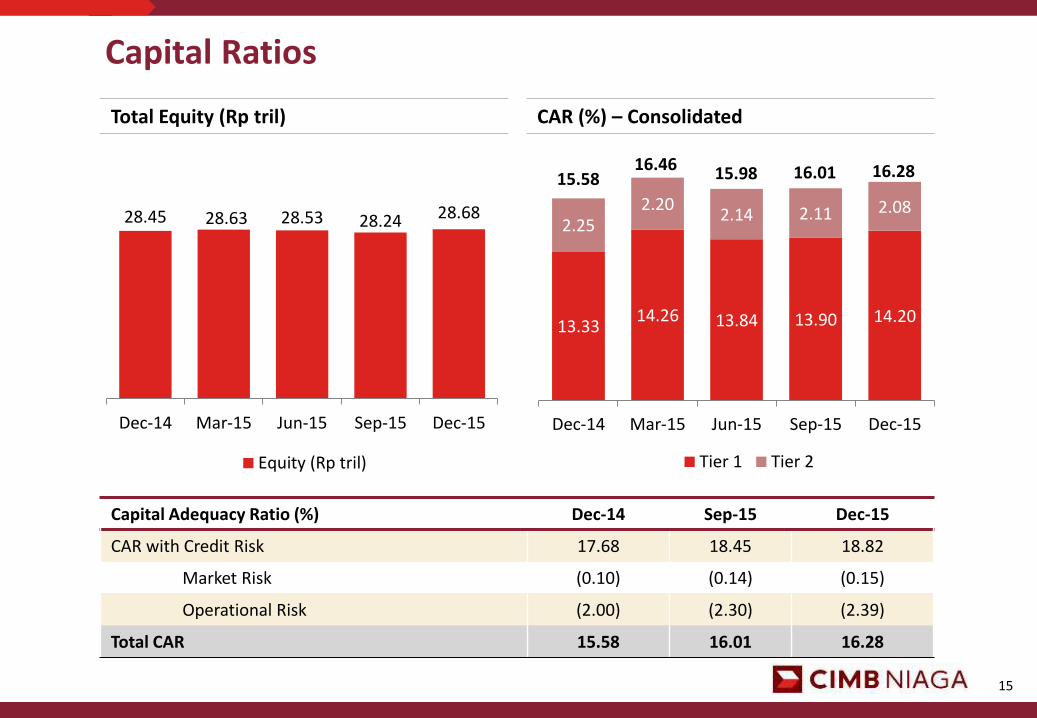

Capital Ratios

Total Equity (Rp tril) CAR (%) – Consolidated

Capital Adequacy Ratio (%) Dec-14 Sep-15 Dec-15

CAR with Credit Risk 17.68 18.45 18.82

Market Risk (0.10) (0.14) (0.15)

Operational Risk (2.00) (2.30) (2.39)

Total CAR 15.58 16.01 16.28

13.33 14.26 13.84 13.90 14.20

2.25 2.20

2.14 2.11 2.08

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Tier 1 Tier 2

16.28 16.46 15.98 16.01 15.58

(1) Quarterly annualized * Excludes one-off costs (Rp 571 bio)

28.45 28.63 28.53 28.24 28.68

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Equity (Rp tril)(1)

28.45 28.63 28.53 28.24 28.68

0.66% 1.15% 1.31% 6.19% 3.34%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Equity (Rp tril) ROE Shareholders Fund BAU

CIMB Niaga: FY 2015 Results Consumer Banking

17

Consumer Loans by Products

Growth (Composition)

QoQ YoY

Total 1.1% 3.9%

3.0% 5.0%

8.3% 20.9%

-1.2% -0.5%

0.9% 3.5%

Total Loans

22.49 23.06 23.27

18.66 18.80 18.57

5.27 5.88 6.37 3.59 3.66 3.77

Dec-14 Sep-15 Dec 15

Personal, Multipurpose& Others (7%)

Credit Cards (12%)

Auto Loans (36%)

Mortgage (45%)

50.01 51.40

(Rp tril)

51.98

18

Mortgages

Total Loans

Market Share

Mortgage Lender Sep-15

BTN 35.4%

BCA 17.4%

BNI 10.1%

Mandiri 7.9%

CIMB Niaga 6.9%

2.5% 2.6% 2.2%

Dec-14 Sep-15 Dec-15

22.49 23.06 23.27

Dec-14 Sep-15 Dec-15

(Rp tril)

7.1% 6.9% 6.8%

NPL Ratio

Market Share

+3.5% YoY

Industry Source: Indonesia Banking Statistics

+0.9% QoQ

19

Creating a Dominant Player in Auto Business

Total Loans

(Rp tril) Growth QoQ YoY

Total -1.2% -0.5%

-35.4% -15.2%

-4.8% -14.2%

-2.5% -11.7%

3.2% 4.6%

13.42 13.61 14.04

1.80 1.63 1.59

2.32 2.09 1.99

1.12 1.47 0.95

0.8%

1.5% 1.9%

Dec-14 Sep-15 Dec-15

Indirect Auto Loans

KITAF

Direct Loans

CNAF

NPL ratio

18.66 18.80 18.57

NPL Ratio

As of 1 January 2016 KITAF is effectively merged into CNAF

Merger

20

1,805

1,924 2,001

Dec-14 Sep-15 Dec-15

Become Top 3 Player in Credit Cards

Number of Cards Outstanding Balance

2013

# Bank Mkt Share

3 BNI

4 Mega

5 CIMBN 10.7%

5.27 5.88

6.37

1.2% 1.1% 1.1%

Dec-14 Sep-15 Dec-15

Outstanding Balance NPL

(thou) (Rp tril)

2014

# Bank Mkt Share

3 Mega

4 CIMBN 11.3%

5 BNI

* Market share based on card issued

+4.0% QoQ

+10.9% YoY

Sep-15

# Bank Mkt Share*

3 CIMBN 11.5%

4 Mega

5 BNI

21

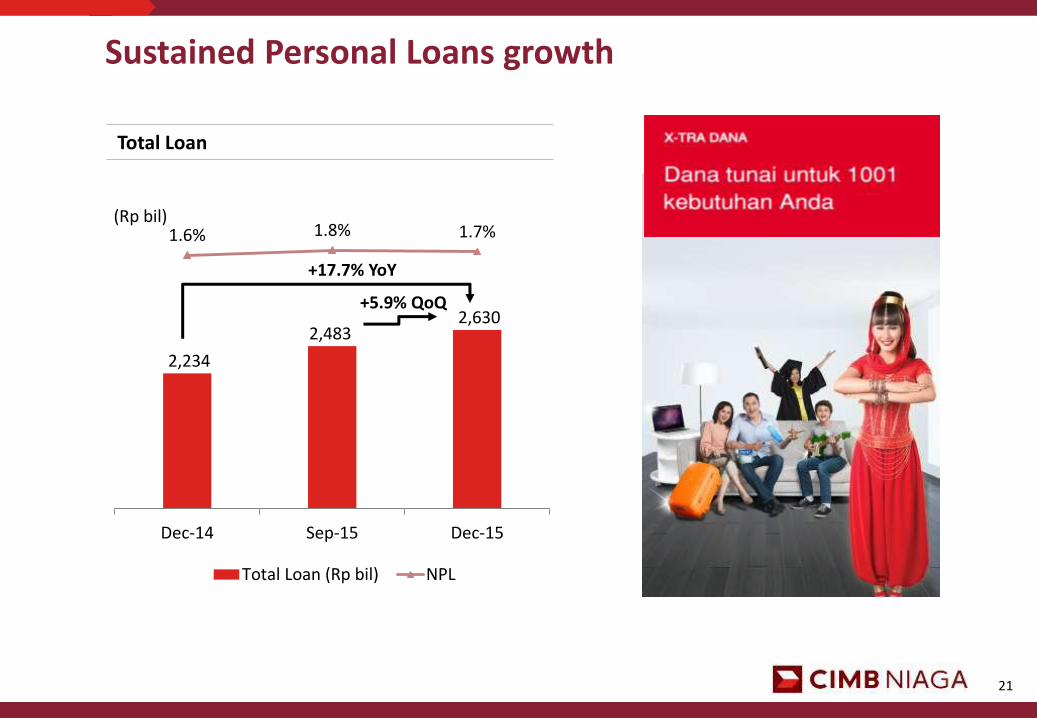

Sustained Personal Loans growth

Total Loan

2,234

2,483 2,630

1.6% 1.8% 1.7%

Dec-14 Sep-15 Dec-15

Total Loan (Rp bil) NPL

(Rp bil)

+17.7% YoY

+5.9% QoQ

22

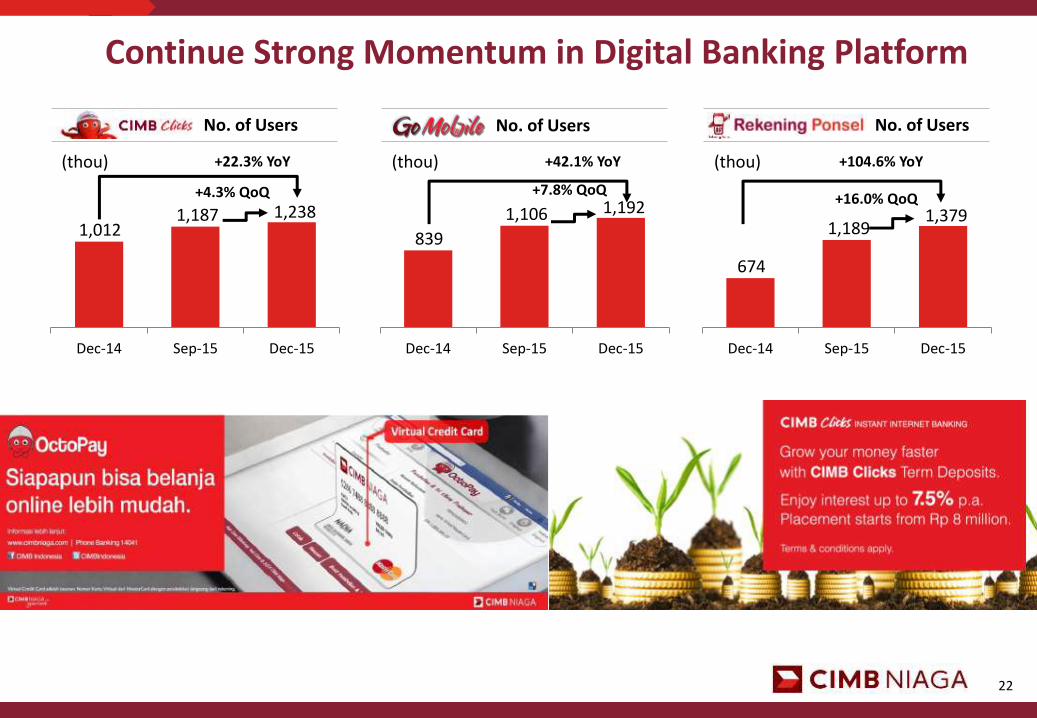

No. of Users

1,012 1,187 1,238

Dec-14 Sep-15 Dec-15

(thou) +22.3% YoY

+4.3% QoQ

Continue Strong Momentum in Digital Banking Platform

839

1,106 1,192

Dec-14 Sep-15 Dec-15

+7.8% QoQ

+42.1% YoY

No. of Users

(thou)

No. of Users

674

1,189 1,379

Dec-14 Sep-15 Dec-15

+16.0% QoQ

+104.6% YoY (thou)

CIMB Niaga: FY 2015 Results MSME Banking

24

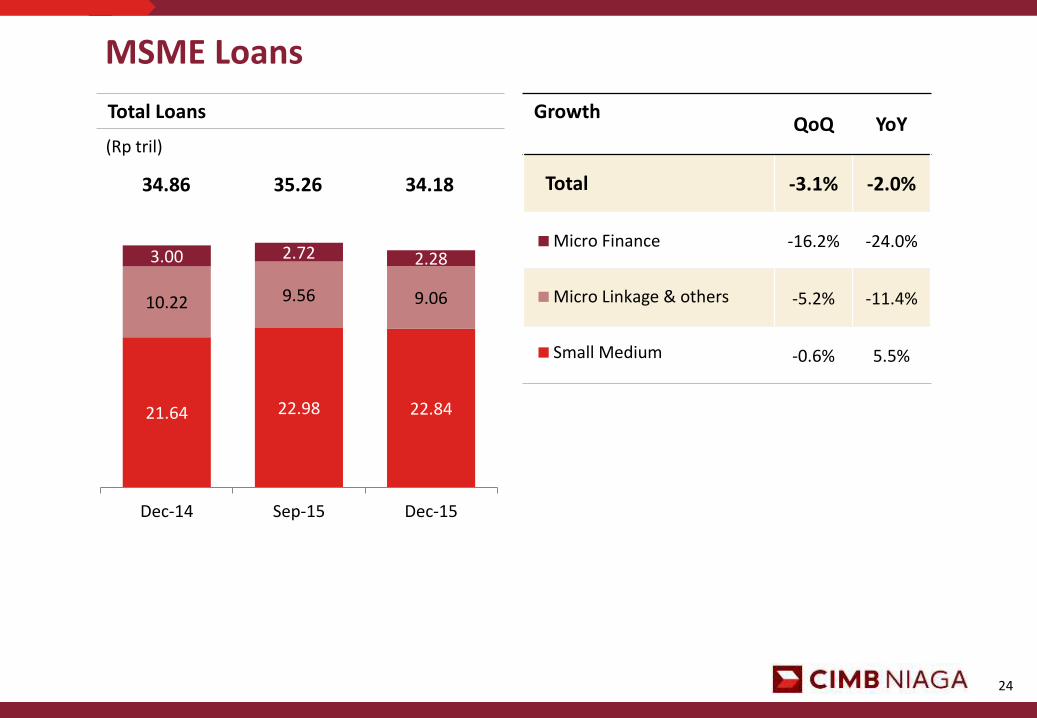

Growth QoQ YoY

Total -3.1% -2.0%

-16.2% -24.0%

-5.2% -11.4%

-0.6% 5.5%

Total Loans

21.64 22.98 22.84

10.22 9.56 9.06

3.00 2.72 2.28

Dec-14 Sep-15 Dec-15

Micro Finance

Micro Linkage & others

Small Medium

34.86 35.26 34.18

(Rp tril)

MSME Loans

CIMB Niaga: FY 2015 Results Commercial Banking

26

Commercial Loans

Growth (Composisiton) QoQ YoY

Total -4.9% -5.1%

-2.9% -1.4%

-7.6% -9.7%

Total Loans

15.93 15.58 14.39

20.15 20.45 19.86

Dec-14 Sep-15 Dec-15

Working Capital (58%)

Investment (42%)

36.08 36.03 34.25

(Rp tril)

CIMB Niaga: FY 2015 Results Corporate Banking

28

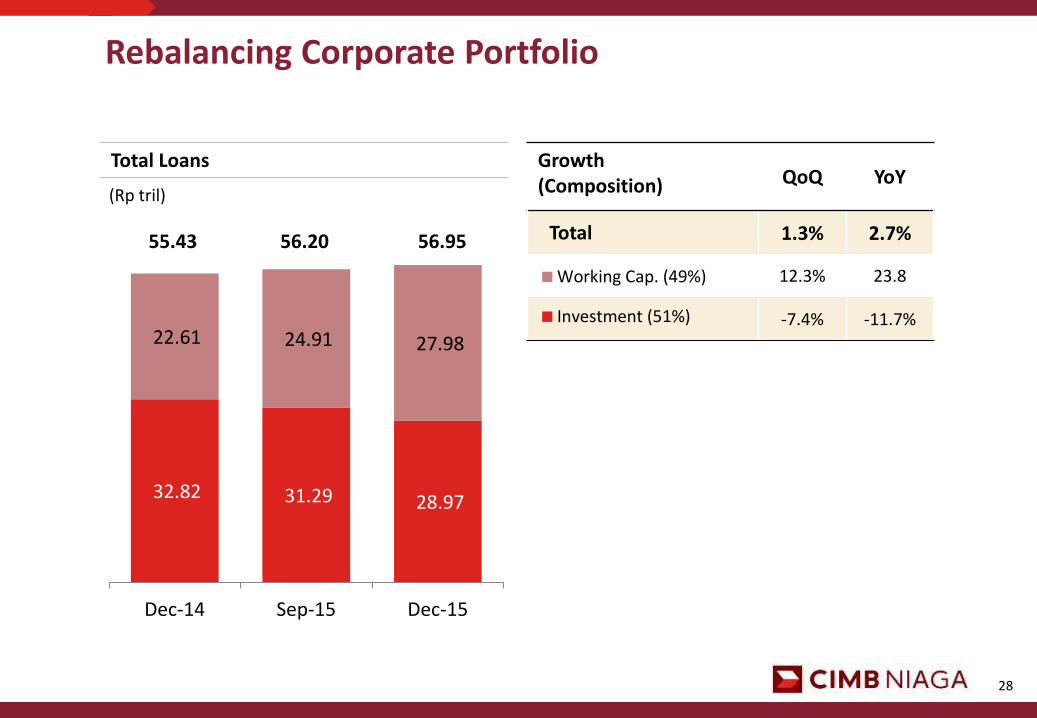

Rebalancing Corporate Portfolio

Growth (Composition) QoQ YoY

Total 1.3% 2.7%

12.3% 23.8

-7.4% -11.7%

Total Loans

(Rp tril)

32.82 31.29 28.97

22.61 24.91 27.98

Dec-14 Sep-15 Dec-15

Working Cap. (49%)

Investment (51%)

55.43 56.20 56.95

CIMB Niaga: FY 2015 Results Syariah Banking

30

Syariah Banking

Total Deposits

(Rp tril)

6.77 7.85

7.58

Dec-14 Sep-15 Dec-15

Total Financing

(Rp tril)

6.44 6.91 7.28

Dec-14 Sep-15 Dec-15

+12.0% YoY

-3.4% QoQ

+13.0% YoY

+5.4% QoQ

CIMB Niaga: FY 2015 Results Final Remarks

32

Final Remarks

2015 was challenging given the economic slowdown and softer commodity sector

Undertaken strategic steps to improve efficiency and scale: completed MSS,

disposed bad bank, recalibrated Micro business and streamlined auto business

Foundation setting for future growth: Successful completion of core banking system

in Jan 2016, building digital banking platform

2016 outlook appears more positive with a favorable monetary policy and continued

government growth initiatives and stimulus packages

CIMB Niaga will emphasize CASA growth, prudent asset expansion, close asset

quality monitoring and cost management in 2016

33

THANK YOU

CIMB Niaga: FY 2015 Results Appendices

35

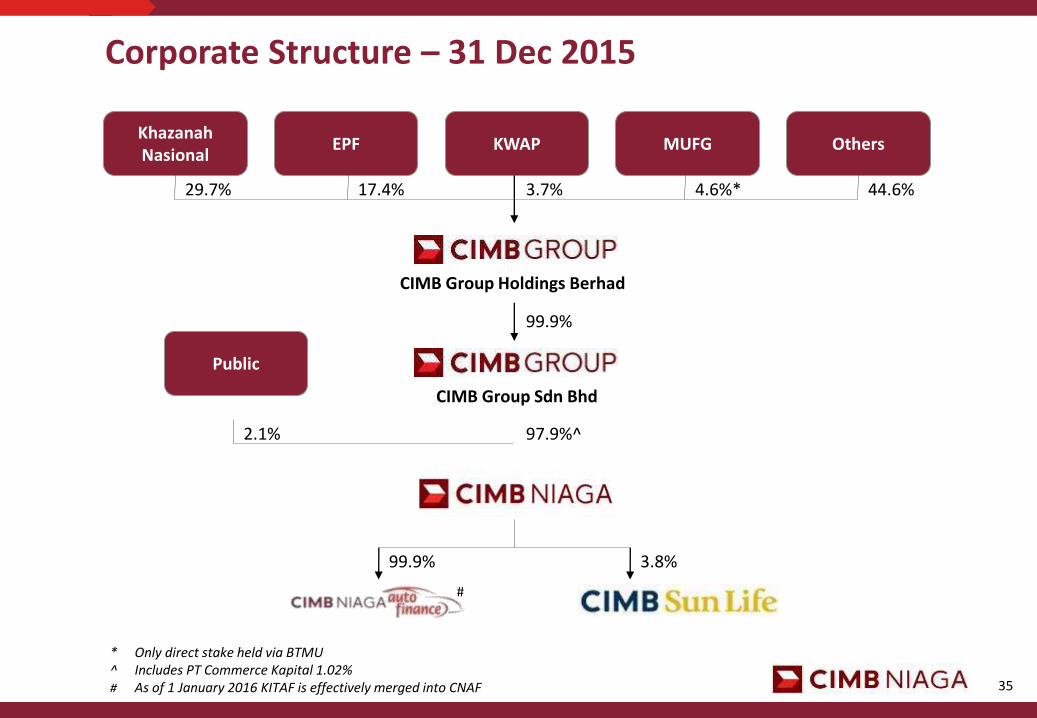

Corporate Structure – 31 Dec 2015

* Only direct stake held via BTMU ^ Includes PT Commerce Kapital 1.02% # As of 1 January 2016 KITAF is effectively merged into CNAF

EPF KWAP MUFG Others Khazanah Nasional

Public

29.7% 17.4% 3.7% 4.6%* 44.6%

99.9%

2.1% 97.9%^

99.9% 3.8%

CIMB Group Holdings Berhad

CIMB Group Sdn Bhd

#

36

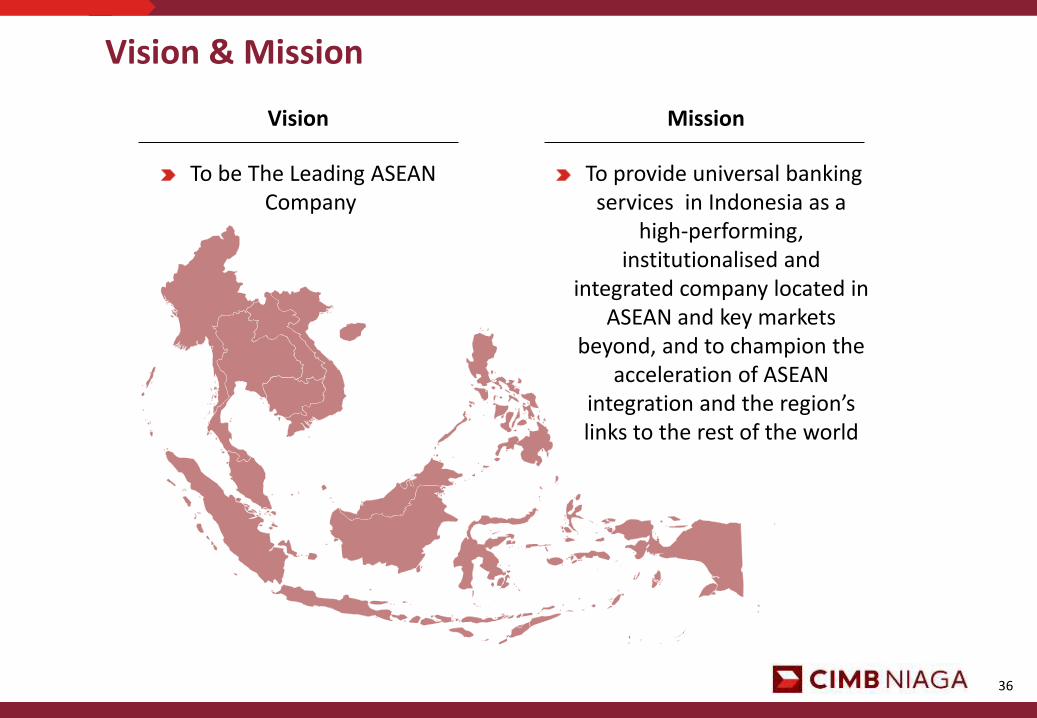

Vision & Mission

To be The Leading ASEAN Company

Vision Mission

To provide universal banking services in Indonesia as a

high-performing, institutionalised and

integrated company located in ASEAN and key markets

beyond, and to champion the acceleration of ASEAN

integration and the region’s links to the rest of the world

37

Dato’ Sri Nazir Razak Glenn M.S. Yusuf

President Commissioner Vice President Commissioner

Roy Edu Tirtadji Sri Hartina Urip Simeon Zulkifli M. Ali

Independent Commissioner Independent Commissioner Independent Commissioner

Pri Notowidigdo David Richard Thomas Ahmad Zulqarnain Onn

Independent Commissioner Commissioner Commissioner

Board of Commissioners

38

Tigor M. Siahaan D. James Rompas Lo Nyen Khing *

President Director Vice President Director & SMME

Vice President Director & Corporate Banking

Wan Razly L. Wulan Tumbelaka Rita Mas’Oen

Strategy & Finance Compliance, Corp. Affairs & Legal

IT & Operations

Samir Gupta Megawati Sutanto Harjanto Tanuwidjaja **

Consumer Banking Credit Human Resources

Vera Handajani John Simon

Risk Management Treasury & Capital Market

Directors

* Resigned effective 31 July 2015 ** Resigned effective 1 December 2015

39

5th in terms of Asset

Assets (Rp trillion)

Source: Published Financial Statement by Bank Indonesia as of November-15; Bank only # Industry as of November-15

792 775

574

440

233 185 167 166 159 146

BRI Mandiri BCA BNI CIMBN Permata BTN Panin Danamon Maybank

Market Share# 13.1% 12.9% 9.5% 7.3% 3.9% 3.1% 2.8% 2.8% 2.6% 2.4%

Top 10 banks control 60.4% of industry’s Asset

40

Maintained position as the 5th largest bank

595 581

462

323

182 143 122 119 115 114

BRI Mandiri BCA BNI CIMBN Permata BTN Panin Danamon BII

528 507

372

297

168 135 129 114 104 104

BRI Mandiri BCA BNI CIMBN BTN Permata Panin Danamon Maybank

Loans (Rp trillion) Customer Deposits (Rp trillion)

Top 10 banks control 62.2% of industry’s loans Top 10 banks control 63.1% of industry’s deposits

Source: Published Financial Statement by Bank Indonesia as of November-15; Bank only * Branches exclude Micro, Cash Counters, Payment Point & Mobile Cash; Danamon incl. Danamon Simpan Pinjam (DSP); Panin as of Dec-14

13.4% 12.8% 9.4% 7.5% 4.3% 3.4% 3.3% 2.9% 2.6% 2.6% 13.6% 13.3% 10.6% 7.4% 4.2% 3.3% 2.8% 2.7% 2.6% 2.6% Market Share#

Branches* (Sep-15)

21,685

17,341 16,783

14,219

3,366 1,830 1,600 1,473 1,019 1,008

BRI Mandiri BCA BNI CIMBN BTN BII Danamon Panin Permata

ATM (Sep-15)

2,380

1,329 1,160 1,083 1,080

560 553 433 378 314

Mandiri Danamon BCA BRI BNI Panin CN BII BTN Permata

# Industry as of November-15

41

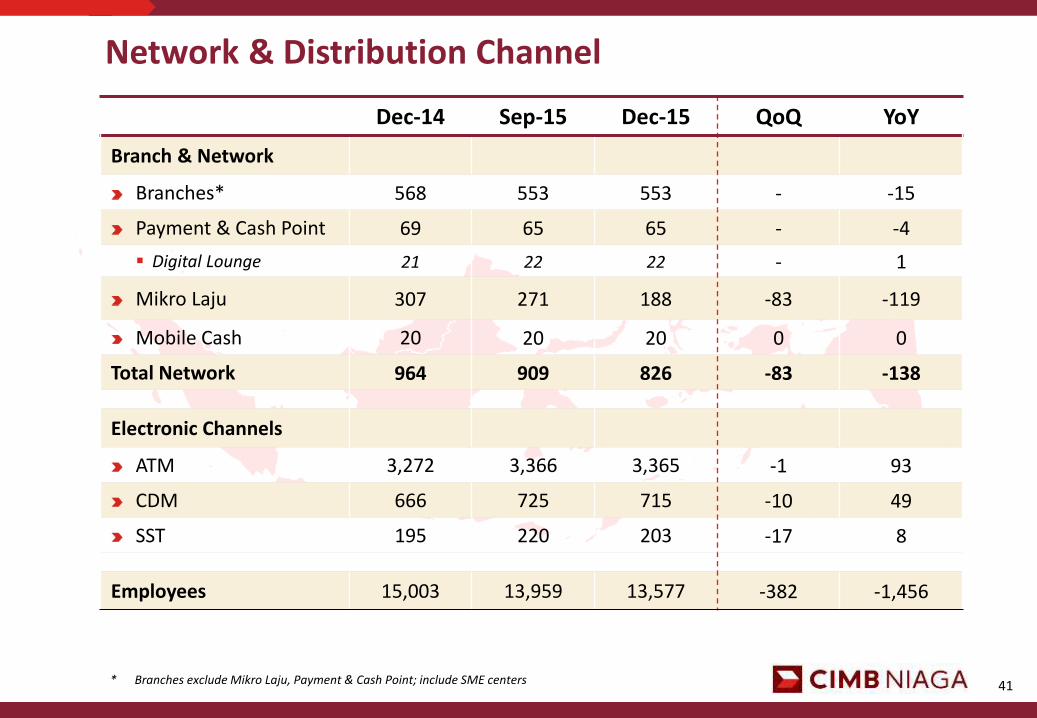

Network & Distribution Channel

* Branches exclude Mikro Laju, Payment & Cash Point; include SME centers

Dec-14 Sep-15 Dec-15 QoQ YoY

Branch & Network

Branches* 568 553 553 - -15

Payment & Cash Point 69 65 65 - -4

Digital Lounge 21 22 22 - 1

Mikro Laju 307 271 188 -83 -119

Mobile Cash 20 20 20 0 0

Total Network 964 909 826 -83 -138

Electronic Channels

ATM 3,272 3,366 3,365 -1 93

CDM 666 725 715 -10 49

SST 195 220 203 -17 8

Employees 15,003 13,959 13,577 -382 -1,456

42

Share Price and Ratings

Rating Agencies Rating / Outlook

Moody’s 5 Jan 2016

Outlook

Bank Deposits

Baseline Credit Assessment

Adj. Baseline Credit Assessment

Issuer Rating

Stable

Baa3/P-3

ba2

baa3

Baa3

Fitch 4 Dec 2015

Long Term Foreign Currency IDR Short Term Foreign Currency IDR Support Rating Viability Rating National Long Term National Short Term Rupiah Subordinated Bonds Rupiah Senior Bond Program 1 2012 Rupiah Senior Bond Prg. 1 tranche 1 & 2

BBB / Stable F3 2 bb AAA(idn) / Stable F1+(idn) AA(idn) AAA(idn) AAA(idn)

Pefindo 02 Jul 2015

Corporate Rating Senior Bond Rating Shelf Registration Bond Rating

idAAA idAAA idAAA

Share Price & Trading Volume

BNGA Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Price (Rp) 835 800 675 540 595

PBV (x) 0.74 0.70 0.59 0.48 0.54

PER 8.96 15.15 29.95 43.51 34.95

43

Notable Awards in 2015

Global CSR Award 2015 Category : Excellence in Provision off literacy and Education Award (silver) - TPGI The Pinnacle Group International

Digital Brand of Year 2015 CIMB Niaga Rekening Ponsel Category: Rank 1 E-Money – Infobank Magazine

” Indonesia Green Award”: Pengembangan Keanekaragaman Hayati , Juni 2015 – The La Tofi School of CSR

“Best Digital Banking Initiative (Digital Lounge)” and “Best Credit Card Product (AirAsia Credit Card)” – The Asian Banker Excellence in Retail Financial Services Awards 2015

Top 50 ASEAN Public Listed Companies and Top 3 Public Listed Companies from Indonesia - ASEAN Corporate Governance Awards 2015

”Best Supporting Bank in Property for Excellence Service and Innovative.” - Indonesia Property Watch bekerja sama dengan majalah Property and The City

44

Corporate Activities in 4Q 2015

PT Bank CIMB Niaga Tbk celebrate 60th anniversary with the theme of “Sasti Raya CIMB Niaga” on Wednesday, 1 October 2015

CIMB Niaga held workshop “Digitalizing Your Transaction Needs” for Transaction Banking clients. On Tuesday, 10 November 2015

CIMB Niaga participates on Investor Gathering “Together Building Indonesia” held by Minister of Finance on Sunday - Tuesday, 7 - 8 December 2015

THANK YOU

PT Bank CIMB Niaga Tbk Investor Relations Menara Sentraya 31st Floor Jl. Iskandarsyah Raya I A Jakarta 12160 Tel. : (62-21) 270 0555 Fax. : (62-21) 250 5205 Email : [email protected]

www.cimbniaga.com

Related Documents