ANALYST MEETING FY2020 February 23 , 2021

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANALYST MEETING

FY2020

February 23, 2021

2

TABLE OF CONTENT

01

03 Business Direction and 2021 Guidance

2020 A Busy Year

02 2020 Business & Financial Performance

3

Achievements

Innovation & Excellence Awards 2020

3G CSR Award 20203G Green Innovation

Award 2020

• Responsible Business Leadership category Mr. Chaiwat Kovavisarach, President & CEO

• Circular Economy Leadership category – Rak Pun Sook

Sustainable Development Excellence Award

Thailand Sustainability Investment (THSI)

Sustainability Disclosure Award

Local Awards:

Regional Awards:

Global Awards:

Most Outstanding

Renewable Energy Solutions - Thailand

• Country TOP3 PLCs

• ASEAN Asset Class PLCs

• ASEAN Top 20 PLCs

TQC plus Innovation - Refinery business

TQC- Marketing business

4

2020 DJSI Ranking: Oil & Gas Refining & Marketing Industry

83

Thailand

Thailand

Korea

Finland

Korea

Thailand

Chile

Chile

India

New Zealand

Thailand

Thailand

Finland

Thailand

Korea

Korea

Chile

US

Brazil

India

2020 DJSI Ranking2018 DJSI Ranking

Source: spglobal.com/yearbook

5

0

20

40

60

80

100

120

140

160

180

200

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

Brainstorm on mid to long term strategy and budgeting

Strategy

Daily COVID Cases Adopt Business Continuity Management (BCM) and Work From Home Policy

Safety Measures & CSR

Distribute free Alcohol sanitizer in service stations and the COVID-19 Protection Kits to partners and communities near BCP refinery

BCPG - capital increase ~10,000 MB

Portfolio adjustment - LAC

RF: Reduce 20% of production & zero jet, Reschedule TAM plan, Purchase the distressed cargoes of crude with high margin

MK: Launch new product: E20s Evo, Touchless Payment in Service stations

Operation

• Implement Innovation Continuity Task Force

• Issue 8,000 MB bondFinancial

2020 A Busy Year: The Great Reset

Strategy

Financial

Safety Measures & CSR

Revise budgeting - OPEX & CAPEX reduction for 20%

Financial

Strategy

Partner with Manus Bio Inc.

6

Reevaluate and adjust BCP Group OPEX & CAPEX

o Cut, delay, or postpone low priority projects

o Follow the principles of law and must give utmost

regard to safety

CAPEX Adjustment 20%

Saving cash in 2020

Turnaround Postponed to 2021: +1,100 MB

Subsidiary’s project postponed: +5,500 MB

OPEX Reduction – 900 MB from original budget

* Warrants exercised period are designed to meet timing of fund usage

BCPG – First proceed from capital raising completed

Capital Raising (RO/PP/Warrants*): ~10,000 MB

Portfolio Rationalization

o To develop innovation green business with sustainability

o Enhance profitability by High Value-Added Products

(Potential Partners/ Technology & Innovation/ Market)

As of 15 Oct 2020 (Adjust after RO & PP1)

Being Lean and Versatile

7

Consolidated Performance 2020

Adjusted

PAT

Inventory Loss(incl. NRV)

PAT

Prep Bond Interest

Impairment

on investment,

asset, AR

Tax benefitGain from

LAC Divestment

Profit(Unit: MB)

EBITDA(Unit: MB)

2019 2020

8,709

4,104

9,856 8,874

Accounting EBITDA Operating EBITDA*

PAT 1,732 (6,967)

(attributable to owners of parent)

Note: *excludes Inventory gain/loss and Gain/loss from FX forward contracts

7,56421,651

2019 2020

48,041

63,244

Net IBD

41,593Net IBD

40,477

BCP group utilized suitable financial instruments

to cope with the uncertainties from COVID-19, and

ended 2020 with a strong cash position

Cash

IBD

Unit: MB

8

01

TABLE OF CONTENT

2020 A Busy Year

03 2021 Business Direction and Guidance

02 2020 Business & Financial Performance

1,732

(757)

(68)

(1,701)

(5,032)

-

(34)

614

8,709

Consolidated Performance 2020

Accounting EBITDA

Depreciation & Amortization

Gain on Exchange rate & others

Impairment on Asset

Impairment on TFRS9

Finance Costs

Taxes Income (Expense)

Non Controlling interest

Profit (Loss)

(Unit: MB)

2019

(attributable to owners of parent)

9

Unit: MB

2019 2020

8,709

4,104

9,856 8,874

Accounting EBITDA Operating EBITDA*

PAT 1,732 (6,967)

(attributable to owners of parent)

(6,967)

(1,197)

1,589

(1,969)

(6,821)

(891)

(2,375)

593

4,104

2020

EPS (5.50)

(THB/Share))

1.18

10

2,871

(36)

2,279 2,964

1,000

(2,169)

(1,004)

2,174

3,640

1,828

EBITDA by Business Group

Refinery & Trading

o Crude run 97.2 KBD

(81% run rate)

o Operating GRM 3.20 $/BBL:

crack spread declined across the

board

o Inventory loss (Net NRV)

4,379 MB

Natural Resources

o 914 MB share of loss

from OKEA

o OKEA performance weakened as

the COVID-19 and OPEC+ oil

price war significantly impacted

the market

Power Plant

o Electricity sales increase

+100% YoY, mostly attributed

to the acquisition of Laos

hydropower plants and RPV

solar farm

o Share of profit of 270 MB

Marketing

o Total sales volumes decreased

17% YoY, mainly from decrease

in JET sales. Retail sales slightly

dropped 2%

o MKM 0. 84 Baht/Litre,

improved as higher proportion

sold through retail channel

o Inventory loss (Net NRV)

365 MB

Bio-Based Products

o EBITDA has reached an all-time

high level

o Gross profit increased for both

Biodiesel and Ethanol business

mainly from the higher selling price

o Sales volume declined in response

to declining transportation fuel

demand

(Unit: MB)

FY2020: Performance declined significantly compared to 2019, as the Refinery and E&P business were affected by the year

round global oil price fluctuation due to COVID-19 pandemic and OPEC+ oil price war

2019 2020 2019 2020 2019 20202019 20202019 2020

11

104.3

89.395.3

100.0

112.6

97.2

87%

74%79% 83%

94%

81%

-50%

-30%

-10%

10%

30%

50%

70%

90%

0.010.020.030.040.050.060.070.080.090.0100.0110.0120.0130.0140.0

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

11% 9%

4% 5%

51% 60%

13%4%

18% 20%

2% 3%

2019 2020

-5

0

5

10

15

20

Q1/19 Q2/19 Q3/19 Q4/19 Q1/20 Q2/20 Q3/20 Q4/20

o The slowdown in economic activities and oil consumption level, esp. JET, led

BCP to adjust production level to the optimal level at 97.2 KBD

o The crack spreads declined significantly across the board weakened operating

GRM in general, but BCP’s GRM was supported by LSFO and UCO

(BCP’s GRM 3.20 $/BBL vs. Singapore GRM 0.38 $/BBL)

o BCPT’s trade transaction +20%YoY

2.87 3.93

2.33

3.74 5.41

3.20

0.26 0.001

0.22

(0.39)

0.11

0.03

(9.29)(7.15)

0.97

(0.03) (0.98) (3.91)

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Operating GRM Hedging Inventory Gain/Loss

Refinery and Trading Business: FY2020 EBITDA -2,169 MB

GO/DBUNL95/DB

IK/DB

LSFO/DB

Cra

ck S

pre

ads

($/B

BL)

GRM

Perf

orm

ance

($/B

BL)

Pro

duct

ion P

rofile

Crude run

LPG

Gasoline

Diesel

UCO

FO & intermediate

Product Yield

JetNon-transportation fuels

(6.16) (3.22) 3.52 4.55 (0.68)3.32

<1%

20

30

40

50

60

70

Q1/19 Q2/19 Q3/19 Q4/19 Q1/20 Q2/20 Q3/20 Q4/20

Av. DB

Av. D

UBAI

($/B

BL)

12

15.9

%

12.2

%

11.8

%

10.0

%

4.1

%

2.0

%

1.8

%

1.7

%15.6

%

11.0

%

11.6

%

9.6

%

4.2

%

2.4

%

2.0

%

1.5

%

FY2019 FY2020

Retail

Industrial

Marketing Business: FY2020 EBITDA 2,174MB

o Net Marketing Margin per unit 11% improved from 2019 since

BCP focused on pushing sales through retail market, which has higher

margin than the industrial market, and high-margin products

0.790.90 0.89

0.77 0.750.84

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

*Net MKM excludes Inventory Gain/(Loss) and NRV

Net Marketing Margin (Baht/Litre) Total Sales Volume (ML/Mo)

Source: DOEB & BCP

Retail Sales Volume Market Share (%)

0

100

200

300

400

Non-oil business

o Expanding Inthanin sales channel: Online, Pick-up store, Stand alone

• + 111 new Inthanin branches (673 branches @YE2020)

• Pushed sales promotion on online channels

715 708 731 746

410 353 461

426

216

7 14 30 0

400

800HSD

MOGAS

JET

HSD, MOFUEL & JET Sale Volume (ML)

o In 2020, Bangchak service station: + 45 new S/S (1,233 sites @YE2020)

• Launched Gasohol S EVO FAMILY

• Opened 36 unique design service stations

o Restructuring convenient store business model

~190 stores: Mini BigC, Family Mart, Tops Daily

40.5

%

42.0

%

o Jet sales volumes dropped 72% YoY, mainly from travel restriction,

led sales volume in the industrial sector to fall 51%, while the retail

sector was slightly dropped 2%

13

Power Plant Business: FY2020 EBITDA 3,640 MB

152 152172 172 150 172

15 1515 15

1515

158 158158 158

158158

14 1414 14

1414

114 114114 114

69

114

452 452472 472

406

472

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Solar & Wind

Solar

Geothermal

Wind

Hydro

Operating Capacity (MW PPA)

75 74 76 77

297 303

3 5 5 4

1817

34 73189 157

72

453

113 151

270 239

387

773

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Laos JP TH

Electricity Sales (Million kWh)

Operating capacity increased 16% from the acquisitions of

Nam San 3B hydropower plant in Laos (45 MW) and Solar

power plant in Thailand (20 MW)

Electricity sales +100% YoY

o Laos hydroelectricity sales increased 529%: realized Nam San 3A

full year performance and Nam San 3B from February

o Thai electricity sales rose slightly. Lower average irradiation hours

was offset buy new solar MW from RPV project, and first full year

performance recognition of 2 projects (Bang Pa-In private solar plant and

Lom Ligor wind plant)

o Japan solar sales dropped from the reduction of electric power

purchased (curtailment) following low electricity demands in Q2

Share of profit 270 MB

o Geothermal power plant: 233 MB dropped by 95 MB.

• Better operating performance, but had to realized extra expense of 236

MB from refinance-relate expense, allowance for account receivable

and tax provision

o PH Wind power plant: 37 MB

• electricity price was improved in November, also applied retroactively

14

POWER PLANT BUSINESSBio-Based Product Business: FY2020 EBITDA 1,828 MB

61

60

66

72

29

9

25

8

69

63

67

77

32

8

27

6

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Production Sales volume

41.49

42.29

15

20

25

30

35

40

45

Ja

n-1

9

Ap

r-1

9

Ju

l-1

9

Oct-

19

Ja

n-2

0

Ap

r-2

0

Ju

l-2

0

Oct-

20

Ja

n-2

1

Source: EPPO

Revenue +39% & Gross profit +177% YoY

o Volume was pressured by oil consumption demand

o but B100 price surged, as a result of B10 diesel mandate, crude palm oil

export promotion and used in electricity generation, and well managed

raw material cost pushed the business performance

B100 Average Price (Baht/Litre)

Biodiesel Production & Sales Volume (Million Litres) Ethanol Production & Sales Volume (Million Litres)

48

47

51

32

19

4

17

9

40 44

52

49

18

9

18

5

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Production Sales volume

Ethanol Average Price (Baht/Litre)

23.8

25.42

20

22

24

26

Ja

n-1

9

Ap

r-1

9

Ju

l-1

9

Oct-

19

Ja

n-2

0

Ap

r-2

0

Ju

l-2

0

Oct-

20

Ja

n-2

1

Source: EPPO

Revenue +7% & Gross profit +28% YoY

o Production decreased as longer maintenance period YoY, sales volume

also declined from lowered demand during the COVID-19 outbreak

o The ethanol price increase was the key driver to lift sales

o Industrial-grade ethanol, used in disinfectant products, help support

Ethanol demand and price

B10 as standard diesel @ 1 Oct

15

OKEA performance weakened as the COVID-19 and OPEC+ oil price war

significantly impacted the market

Year production (~16 Kboe/d) and sales declined: due to turnaround

maintenance and adjusted production plan to be in line with lower crude oil demand

Revenue decrease mainly to lower volume and realized prices

Impairment expenses:

• Draugen and Gjoa technical & ordinary goodwill in 1H2020 from the

significant fall in market price of crude oil and gas

• Yme asset under development, primarily driven by an increasing capital

expenditures and the delayed production

Currency gain on loans: strengthening of NOK against USD

Unwind deferred tax from impairment

Natural Resources Business: FY2020 EBITDA -1,004 MB

Realized Price

Source: OKEA

8.97.9

6.77.6

9.1

7.8

9.8

7.8

6.4

8.3

9.2

8.1

19.1

16.0

13.3

16.2

18.7

16.2

Q1/20 Q2/20 Q3/20 Q4/20 2019 2020

Ivar Assen

Gjoa

Draugen

56.2 60.7 56.4 61.248.4

24.932.3

39.0

56.6

36.36.5

4.1 3.0 3.5 2.71.4 2.2

5.1 4.3 2.8

Gas Price ($/MMBTU)

Liquid Price ($/boe)

Production Volume - Net to OKEA (kboe/d)

BCPR holds 46.32 % in OKEA ASA

BCP took share of loss 914 MB from OKEA

16

Unit: MB

Assets

31 Dec 19 31 Dec 20 Change

Total Assets 127,788 148,323 16%

Total Liabilities 68,973 90,007 30%

Total Equity 58,815 58,316 <1%

Trade and other current receivables -42%

• Declining attributed to BCP’s product price and sales volume decreased

Inventory +2% mainly from BCP’s higher crude and oil product inventory volume

Other Non Current Assets +24%

Current Assets

Right-of-use assets and Leasehold rights 7,962 MB from TFRS 16 financial standard

Intangible assets and Goodwill 2,894 MB as BCPG acquired Namsan 3B hydropower

plant and RPV solar farm

Investments in associates and joint ventures 3,706 MB primarily from impairment

assets, realizing a share of loss from associated company OKEA, and the effects of

translation financial statement of BCPG Plc’s associated companies

PP&E +4%

Refinery assets 4,407 MB, mainly in 3E project

BCPG’s investment 1,506 MB & BBGI’s ethanol additional capacity and refined

glycerin 840 MB

Depreciation of 4,336 MB

52,584 54,567

37,583 46,460

3,437

3,080 15,835

16,162 11,073

6,402 7,276

21,651

31 Dec 19 31 Dec 20

Cash

Others Current Assets

PP&E

Inventories

Other Non Current Assets

148,323127,788

Trade and Other Current Receivables

Entities Change (MB) Value @ Dec 20

Star Energy -1,863 10,595

OKEA ASA -1,896 1,610

Consolidated Statement of Financial Position

17

Unit: MB

Liabilities & Equities

Equities -1%

- Net loss of 5,770 MB

- Dividend payment of 743 MB

- Interest expense for perpetual bond 501 MB

+ Gain on LAC divestment 3,142 MB

Trade & Other current payables -9% mainly from the lower crude price

in December 2020 compared to December 2019

Non Current Liabilities +154%

• Lease liabilities 6,581 MB under TFRS 16

Loans & Debentures +32%

• Short-term loan 1,076 MB

• Loans and debentures (incl. current portion) 16,279 MB

• Current portion of lease liabilities 1,287 MB under TFRS 16

31 Dec 19 31 Dec 20 Change

Total Assets 127,788 148,323 16%

Total Liabilities 68,973 90,007 30%

Total Equity 58,815 58,316 <1%

58,815 58,316

4,098 10,409

48,041

63,244

3,387

4,076

13,447

12,277

31 Dec 19 31 Dec 20

Trade & Other Current Payables

Loans & Debentures

Equity

Current Liabilities

Non Current Liabilities

148,323127,788

Consolidated Statement of Financial Position

18

Beginning Cash7,276 MB

Ending Cash21,651 MB

FX adjustment-178 MB

Cash movement 14,553 MB

Consolidated Statement of Cash Flow

13,784

8,000

6,122

1,658

5,149

4,252

(1,213)

(5,597)

(6,051)

(11,552) Debt Service

PP&E

Investment & Loan to Associates

Dividend paid & OthersTax received & Others

Funding21,786 MB

Unit: MB

Sources of Cash38,965

Uses of Cash(24,412)

Net cash generated from operating

Loans from institution

Debentures

Capital increase of subsidiaries

LAC Divestment

19

01

03

TABLE OF CONTENT

2020 A Busy Year

02 2020 Business & Financial Performance

Business Direction and 2021 Guidance

20

Refocus

Reimagine

Restructure Rejigging business puzzle

Taking advantage of capital

market bull run

Emphasizing on core

competency/Extension of

green portfolio

Accelerating Greenovation

Restructuring for Long-Term Sustainability

21

2017 2023 2035-40

Demand/Market Size

Time

Peak Road Oil Demand

5-yearsStrategy

High Value Added but Small Market Size

20-yearsStrategy

Competitiveness of BCP

Potential TechnologySelection

Fossil fuel

RenewableEnergy

S1

50%50%

EnergyStorage

BioChem/Material

40%60%

70%

30%

S2S3

BCP Portfolio

22

BCP Portfolio - Accelerate Green Portfolio

2017 2023 2035-40

Demand/Market Size

Time

5-yearsStrategy

Fossil fuel

RenewableEnergy

S1

50%50%

EnergyStorage

High ValuedAdded

40%60% 70%

30%

S2S3

“Accelerate Green Portfolio”

23

Long Term Aspiration

HIGH LOW

Level of natural ownership

Core Businesses

Extension to

the Core

Adjacent to

Current

Businesses

Lube

Food

Ingredients

Cosmetics

Ingredients

Pharmaceuticals

Ingredients

Refined

Glycerin

EV

Charging

Station

Lithium

Processing

New

Industries

Alternative

Protein

Virtual

Power Plant

Solvent

Power

plant

Franchisee

(Food &

Beverage)

Biofuel

Energy

Efficiency

Transmission

line

Sanitizer

EV Related

Solar

RooftopBiogas

Community

Power plantBESS

1

Green Power Value Chain2

Bio-Based Value Chain3

Lithium Value Chain

24

Short to Medium-Term Direction

• Niche-Products Refinery

(UCO, Solvent, Wax, Oil

Blending)

• 3E & Rocket project

benefit recognition

• Minor modification & less

capital spending to meet

EURO5 standard

• Trading Growth 3x with

in 5 years

Refinery & Trading Marketing Green Power Plant Bio-Based Products New S-Curve

• Greenovative destination

• Increasing portion of

Non-Oil & Lube EBITDA

to 30%

• Inorganic Growth Service

stations expansion

• Digital Marketing & Customer

Experience

• Offsetting earning

dilution

• Accelerating growth

thru organic and inorganic

actions

• Continuing asset

optimization

• Stepping towards more

digitalization and

innovation

• High value added

products (refined

glycerin, alcohol sanitizer

product, etc.)

• Partnership with Manus

Bio to establish Syn Bio-

business in regional

• Explore growth platform

through M&A / trading on

downstream business /

products

• Portfolio

rationalization

• Exploring new S-Curve

business

• Moving midstream &

downstream in Lithium

25

RFBG34%

MKBG (Oil)18%MKBG (Non-Oil)

3%

BCPG32%

BBGI10%

E&P2.7%

Accelerate Green Portfolio

RFBG56%

MKBG17%

BCPG21%

BBGI4%

E&P2%

Accounting EBITDA unit: MB

RFBG78%

MKBG22%

6,165 MB

Green portion0%

13,421 MB

Green portion

~45%Green portion

25%

2010 2017

1.7x

2025

RFBG16%

MKBG15%

BCPG64%

BBGI3%

Others2%

2021-2025

48,000 MB

(excluding CAPEX for New S-Curve businesses)

CAPEX unit: MB

26

Refinery

• Average crude run of 95 – 100 KBD

• TAM for ~40 days during first quarter

• DB @ 46$/BBL

• Benefit 200 MB from 3E project and 500 MB from rocket project

• Shifting to high-margin products

Power Plant

• Proceed from capital increased of THB 7.4 bn

soon to be gearing and deployed to projects

• EBITDA target Growth by 30 – 40%

Bio-Based Products

• Seek new opportunities in high-value bio-based products for B2B and B2C customers, Thailand as the regional production hub

• Plan to submit IPO filing in late 2021

Marketing• Network expansion (Cluster expansion and JV models)

100 more service stations

• Sales growth ~ 6%

• Focus more on Greenovative and higher margin products

• Traffic boost through synergies with retail developers

• Inthanin ~150 new stores

2021 Business Guidance: Heading toward The Light

OKEA

• To benefit from higher oil & gas price

• Two new production wells in Gjøa in Q1/21

• Yme first oil in 2H/2021

• Production guiding of 15.5-16.5 Kboe/d

• New additional licenses added to portfolio

27

CAPEX 2021: The Essentials for Business Growth

RFBG11% MKBG

6%

BCPG78%

BBGI4%

Others0.4%

23,000 MB

Group CAPEX 2021 CAPEX

Refinery (RF+Trading) 2,600

Maintenance 1,400

Growth & New project 1,200

Marketing (MK+BCR+BGN) 1,400

Maintenance 400

Growth (expanding) 1,000

BCPG 18,000

BBGI 900

Other 100

Total 23,000

(excluding CAPEX for New S-Curve businesses)

RFBG31%

MKBG6%

BCPG49%

BBGI14%

Others0.3%

12,400 MB

Actual Y2020 Y2021

28

Appendix

2021 Business Update

29

Trading Growth:

Expanded Logistics

Management

Expand product line &

specialty products

(Solvent, Asphalt, etc.)

New Business Development:

LNG and Biofuel trading

Trade Volume 82 KBD (2020)

to increase 30-50% in 2021

Crudes & Feedstocks:

Increase high-margin crude variety & feedstocks for flexibility in production

Distressed cargo, opportunity from over supply ,

Crude overweight

Customized Products:

Produce more high-value UCO – Lube & Wax and LSFO for new markets

Develop Non-transportation fuels

9% 9% 9%5% 5% 9%

60% 60% 55%

<1% <1% <1%2% 4% 4%22% 20% 21%

3% 3% 2%

4Q2020 Y2020 Y2021

LPG

Gasoline

Jet

Non-transportation fuels

Diesel

UCO

Fuel Oil & Intermediate

100.0

(Q4/20)

97.2

(FY2020)

60 - 65

(Q1/21)

90 - 95

(1H2021)

95 - 100

(FY2021)

Turnaround Maintenance (TAM) in 2021 from 15 Feb – 25 Mar 2021

Mogas18%

+0.2 $/BBL +0.45$/BBL

GRM Improvement

Current Crude run @ 100 KBD

Mogas Yield Improvement

Energy Saving

3E project - completed CCR test run

- tie in debottlenecking HCU with TAM

Crude run @ 120 KBD

To increase outputs and improved operation for optimal benefits

Refinery projects:

Crude run: (KBD)

Refinery Business Going Forward

Capacity optimal level increased to 120 KBD

HCU capacity increased 10% (25 KBD to 27.5 KBD)

30

as of Dec 2020

1,233

Standard Type 619 sites

COOP Type 614 sites

Unique Design Service Stations

Network Expansion

Strengthening Marketing Network

2020 2021

1,233

stations

+100

stationsDec 2020 2021

33

stations

+17

stations

Service station

Focus on:• Standard type• Non-Company Own

• Cluster development in main roads, commercial and tourism area

• Unique Design/Flagship service stations in high-potential area

Increase non oil & lube EBITDA portion

New retail strategic partner

• To draw more customers to service station

Uplifting current businessvia car care expansion

• Opening more sites in service stations

Stores as of Dec 2020

6732020 2021

673 sites +150 sites

456 sites in S/S

217 sites out S/S• Leading in Arabica 100% Coffee bean and

Best in class cocoa beverage• Adaptive outlet types for new customer bases• Get more into delivery & take away market

with “Inthanin the natural cups” concepts

31

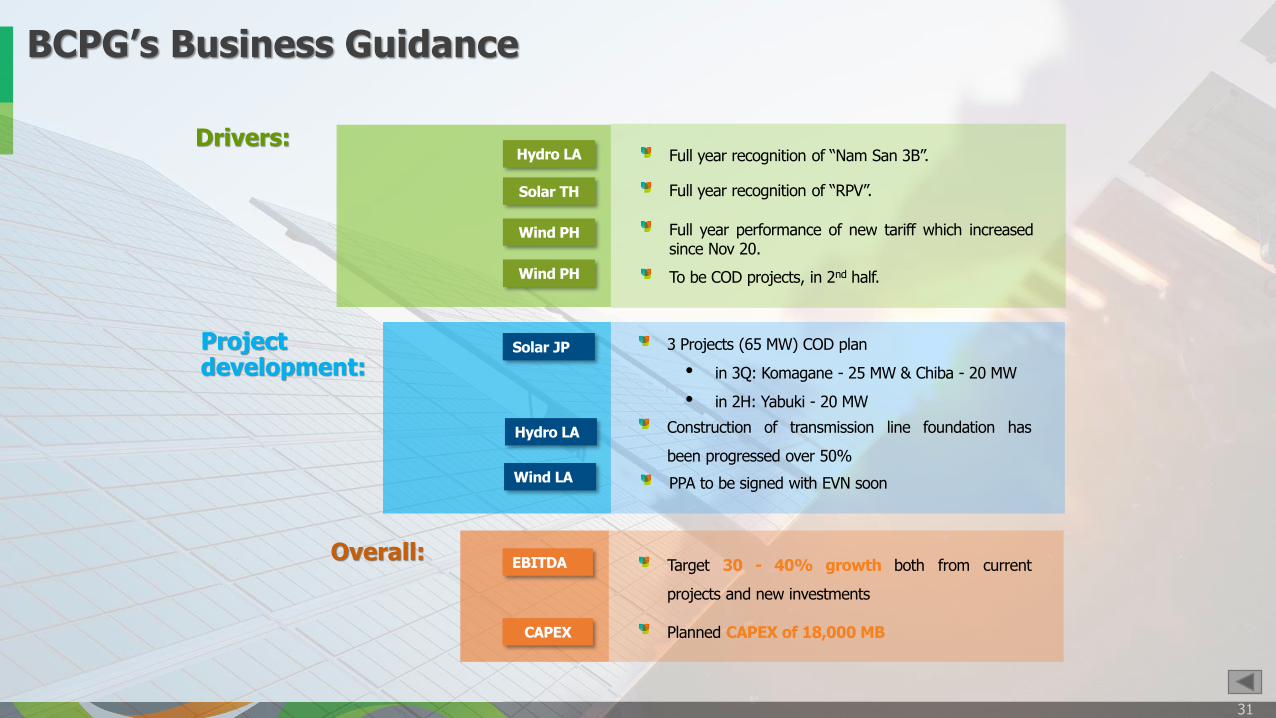

BCPG’s Business Guidance

Full year recognition of “Nam San 3B”.Hydro LA

Wind PH Full year performance of new tariff which increased since Nov 20.

Hydro LA Construction of transmission line foundation has

been progressed over 50%

Wind LA PPA to be signed with EVN soon

EBITDA

CAPEX

Target 30 - 40% growth both from current

projects and new investments

Planned CAPEX of 18,000 MB

Drivers:

Project development:

Overall:

Solar TH Full year recognition of “RPV”.

Wind PH To be COD projects, in 2nd half.

Solar JP 3 Projects (65 MW) COD plan

• in 3Q: Komagane - 25 MW & Chiba - 20 MW

• in 2H: Yabuki - 20 MW

32

BBGI Business LandscapeBBGI Business LandscapeBBGI Business Landscape

Equity Investment in Manus Bio Inc. US

25 MUSD

HQ, Boston

Plant Site, Augusta

WIN Ingredients Co., LtdExclusive Product Distribution in SEA, Japan and Korea

and Advanced Fermentation Manufacturing Plant in Thailand

51% 49%

Biodiesel Business

(Existing)

Bioethanol Business

(Existing)

New Businesses

Food & Flavor Ingredients

Nutraceuticals & Pharmaceuticals Ingredients

Personal-care and Cosmetics Ingredients

Capacity: Biodiesel 1.00 ML/D

Refined Glycerin 27,000 Tons/Yr in Q1/2021

Product: Biodiesel

Refined Glycerin

Product: Ethanol Fuel-Grade

ENA-Grade

Capacity: Ethanol 0.60 ML/D

0.80 ML/D in Q1/2022

Biofuel production capacity target @ 2.05 ML/D

Plan to submit IPO filing in 2H2021

Add Biofuel Production Capacity

Plan for selling SynBio product in

mid2021

33

Appendix

Financials

34

Consolidated Statement of Income (Unit: THB Million) Q4/2020 Q3/2020 QoQ Q4/2019 YoY

Revenue from sale of goods and rendering of services 33,134 33,652 -2% 50,146 -34%

Cost of sale of goods and rendering of services (30,741) (31,058) -1% (47,130) -35%

Gross Profit 2,393 2,593 -8% 3,017 -21%

Other income 120 121 -1% 140 -14%

Selling and administrative expenses (2,180) (1,613) 35% (2,262) -4%

Gain (loss) from derivatives 165 (72) N/A 142 N/A

Gain (loss) on foreign exchange 140 134 N/A 274 N/A

Loss on impairment assets 115 (1,003) N/A (34) N/A

Profit (loss) before finance costs and income tax expense 752 160 369% 1,277 -41%

Finance costs (484) (504) -4% (425) 14%

Impairment gain and reversal of impairment loss (impairment loss) determined in accordance with TFRS 9

23 (24) N/A - N/A

Share of profit of associates and joint ventures 264 58 N/A 52 N/A

Profit (loss) before income tax expense 555 (310) 279% 903 -39%

Tax income (expense) 46 (19) N/A (36) N/A

Profit (loss) for the period 601 (329) 282% 867 -31%

Owners of parent 251 (647) 139% 620 -59%

Non-controlling interests 349 318 247

Basic earnings (loss) per share (Baht per Share) 0.09 (0.57) 0.38

Profit and Loss (Consolidated)

2020 2019 YoY

136,450 190,489 -28%

(132,122) (180,257) -27%

4,328 10,232 -58%

533 495 8%

(7,141) (7,614) -6%

17 160 N/A

732 614 N/A

(2,375) (34) N/A

(3,907) 3,853 -201%

(1,969) (1,701) 16%

(891) - N/A

(592) 404 N/A

(7,359) 2,556 -388%

1,589 (68) N/A

(5,770) 2,488 -332%

6,967) 1,732 -502%

1,197 757

(5.50) 1.18

35

Note: 1/ EBITDA from Refinery Business of the Company, BCP Trading Pte. Ltd. and share of profit from associated companies2/ EBITDA from Marketing Business of the Company, Bangchak Green Net Co.,Ltd., Bangchak Retail Co., Ltd., and share of profit from

associated companies3/ EBITDA from Power Plant Business of BCPG Plc., its subsidiaries, and share of profit from associated companies4/ EBITDA from BBGI Plc., its subsidiaries, and share of profit from associated companies5/ EBITDA from Natural Resources business of Nido Petroleum Pty. Ltd., BCP Energy International Pte. Ltd., BCP Innovation Pte. Ltd.,

BCPR Co., Ltd. and share of profit from associated companies

Unit: THB Million Q4/2020 Q3/2020 QoQ Q4/2019 YoY

Total Revenue 33,134 33,652 -2% 50,146 -34%

Accounting EBITDA 2,750 2,769 -1% 2,420 14%

Refinery and Trading Business 1/ 600 606 -1% 1,073 -44%

Marketing Business Group 2/ 602 766 -21% 359 68%

Green Power Business3/ 868 1,138 -24% 796 9%

Bio-Based Product Business4/ 590 390 51% 374 58%

Natural Resource Business5/ 221 (58) 481% (57) 488%

Others (131) (73) -81% (124) -6%

Profit attributable to owners of the Company 251 (647) 139% 620 -59%

Earnings (Loss) per share (Baht) 0.09 (0.57) 0.38

EBITDA Structure (Consolidated)

2020 2019 YoY

136,450 190,489 -28%

4,104 8,709 -53%

(2,169) 2,871 -176%

2,174 2,279 -5%

3,640 2,964 23%

1,828 1,000 83%

(1,004) (36) N/A

(365) (369) 1%

(6,967) 1,732 -502%

(5.50) 1.18

36

Financial Ratio (Consolidated)

Profitability Ratios (%) Q4/2020 Q3/2020 Q4/2019

Gross Profit Margin 7.22% 7.71% 6.02%

EBITDA Margin 8.30% 8.23% 4.83%

Net Profit Margin 1.81% -0.98% 1.73%

Return on Equity (ROE) -14.22% -14.90% 3.67%

Return on Assets (ROA) -3.90% -3.87% 3.47%

2020 2019

3.17% 5.37%

3.01% 4.57%

-4.23% 1.31%

31-Dec-20 31-Dec-19

Liquidity Ratios (Times)

Current Ratio 1.85 1.39

Quick Ratio 1.10 0.69

AR Turnover 18.33 23.76

Collection Period (Days) 20 15

AP Turnover 13.44 20.92

Payment Period (Days) 27 17

Financial Policy Ratios (Times)

Debt to Equity 1.54 1.17

Interest bearing Debt to Equity 1.22 0.82

Net Interest bearing Debt to Equity 0.85 0.69

Release of Debenture Ratio (Times)

Net Interest bearing Debt to Net Equity 0.66 0.57

THANK YOU

Disclaimer

The information contained herein is being furnished on a confidential basis for discussion purposes only and onlyfor the use of the recipient, and may be subject to completion or amendment through the delivery of additionaldocumentation. Except as otherwise provided herein, this document does not constitute an offer to sell or purchaseany security or engage in any transaction.

The information contained herein has been obtained from sources that Bangchak Corporation Public CompanyLimited (“BCP”) considers to be reliable; however, BCP makes no representation as to, and accepts noresponsibility or liability for, the accuracy or completeness of the information contained herein.

Any projections, valuations and statistical analyses contained herein have been provided to assist the recipient inthe evaluation of the matters described herein; such projections, valuations and analyses may be based onsubjective assessments and assumptions and may utilize one among alternative methodologies that producediffering results; accordingly, such projections, valuations and statistical analyses are not to be viewed as facts andshould not be relied upon as an accurate representation of future events. The recipient should make anindependent evaluation and judgment with respect to the matters contained herein.

Tel. +66 2335 8663 / 8518 / 4370

www.bangchak.co.th

Related Documents