Analysis of Platform Strategies of Major Heavy-duty Truck Manufacturers Nearly One in Three Heavy-duty Trucks Manufactured in 2018 to Feature Platform Based Lineage Ananth Srinivasan, Senior Research Analyst Sandeep Kar, Global Director Commercial Vehicle Research 27Nov, 2012 © 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Analysis of Platform Strategies of Major Heavy-Duty Truck Manufacturers

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Analysis of Platform Strategies of Major Heavy-duty Truck Manufacturers

Nearly One in Three Heavy-duty Trucks Manufactured in 2018 to Feature Platform Based Lineage

Ananth Srinivasan, Senior Research Analyst

Sandeep Kar, Global Director

Commercial Vehicle Research

27Nov, 2012

© 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Today’s Presenters

Ananth Srinivasan

Senior Research Analyst

Commercial Vehicle Research

Frost & Sullivan

Experience base covers a wide range of sectors, leveraging long-standing working relationships with

Sandeep Kar

Global Director

Commercial Vehicle Research

Frost & Sullivan

10 years of global commercial vehicle technologies

and markets expertise, which include particular

2NA53-18

Source: Frost & Sullivan analysis..

leveraging long-standing working relationships with leading industry participants’ senior executives

• Functional expertise • Commercial vehicles

• Transmission systems• Safety systems• Comfort and Convenience

technologies • Business expertise

• Competitive analysis• Product portfolio, and market expansion

strategy• Go-to-market strategy

and markets expertise, which include particular

focus on areas such as:

• Global commercial vehicle industry growth

opportunities, and market penetration and

growth strategy development

• Advanced truck technologies- powertrain,

chassis, safety, telematics and regulation

compliance technologies

• Global research and consulting management,

global business development and team-

building, CXO level revenue and market share

growth strategy development

Why Know About This Today?Competitive Dynamics, Demand Shift in Favour Emerging Markets; Converging Preferences

and Regulations Emerge as Key Trends

1. Changing Competitive Environment

TRIAD OEMs looking to enter emerging markets

Indian and Chinese participants going global

2. Convergence of 4. Saturated demand in

27.6%

27.3%

63.8%

63.2%

8.6%

9.5%

0.0% 50.0% 100.0%

2010

2018 TRIAD

BRIC

RoW

Globalization is not an

14

Unit Production

3NA53-18

Region NOx (g/kWh)

Particulate(g/kWh)

NorthAmerica

0.27 0.013

EU 0.4 0.01

Japan 0.4 0.01

India 3.5 0.02

China 2 0.02

2. Convergence of legislative and

environmental regulations across regions

3. Customer preferences focused towards optimizing TCO

0

5

10

2008

2015-e

TCO

Product Quality

Comfort and Convenience

Regulatory Compliance

Duty Cycle Applicability

Service/ Networking

4. Saturated demand in TRIAD,

significant opportunities in BRIC

Globalization is not an option anymore; it is a

necessity.

2

3

Source: Frost & Sullivan analysis.

Long-term

Imp

act

of

Str

ate

gy o

n P

rofi

tab

ilit

y

Global service and distribution

Global product platforms with multi-regional branding within each segment

Common R&D, strong regional brands/partners, multiple product platforms

Vertical synergy between brands and across segments

Regional presence/ partners, localized

Su

sta

ined

Pro

fita

bili

ty Z

on

e

Su

sta

ined

Pro

fita

bili

ty Z

on

e

Current Industry ScenarioOEMs’ Desire to Move to Sustainable Profitability Zone with Regional Customization Flexibilities

and Synergy Across Different Regional Brands

Heavy-duty Truck Market: Impact of Platform Strategy on Globalization versus Profitability, Global, 2011

4NA53-18

F&S Analysis and RecommendationCurrent Industry Trend Expected Industry Movement

Very High

Impact of Strategy on Globalization

Medium

Short-term

Imp

act

of

Str

ate

gy o

n P

rofi

tab

ilit

y

High

and distribution network

multiple product platformspartners, localized product development

Daimler Group, Volvo Group, MAN SE Dongfeng Motor Corp, Ashok

Leyland

Scania AB ,IVECO, Navistar Inc, PACCAR

Inc, CNHTC, Beiqi Foton, TATA Motors

Source: Frost & Sullivan analysis.

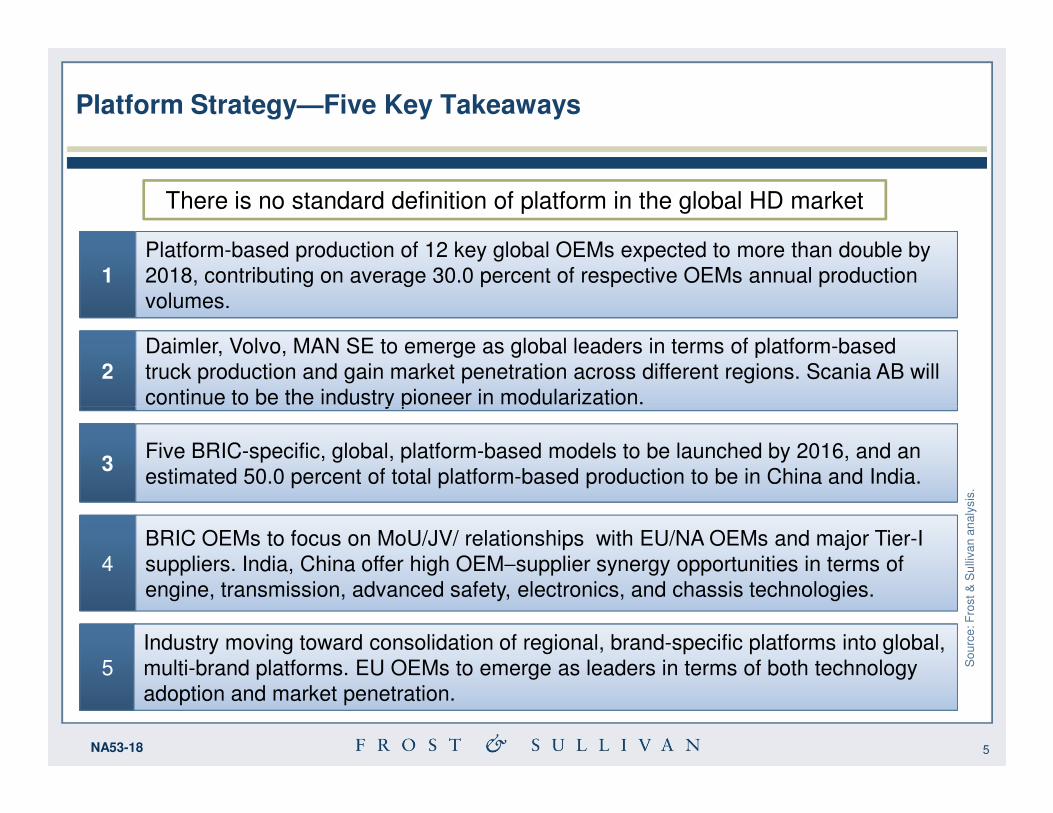

Platform Strategy—Five Key Takeaways

There is no standard definition of platform in the global HD market

2Daimler, Volvo, MAN SE to emerge as global leaders in terms of platform-based

truck production and gain market penetration across different regions. Scania AB will

continue to be the industry pioneer in modularization.

1Platform-based production of 12 key global OEMs expected to more than double by

2018, contributing on average 30.0 percent of respective OEMs annual production

volumes.

5NA53-18

So

urc

e: F

rost &

Su

lliva

n a

na

lysis

.

continue to be the industry pioneer in modularization.

3Five BRIC-specific, global, platform-based models to be launched by 2016, and an

estimated 50.0 percent of total platform-based production to be in China and India.

4

BRIC OEMs to focus on MoU/JV/ relationships with EU/NA OEMs and major Tier-I

suppliers. India, China offer high OEM−supplier synergy opportunities in terms of

engine, transmission, advanced safety, electronics, and chassis technologies.

5

Industry moving toward consolidation of regional, brand-specific platforms into global,

multi-brand platforms. EU OEMs to emerge as leaders in terms of both technology

adoption and market penetration.

Definitions and Key Assumptions

A platform can be defined as “a single set of common design, engineering, and manufacturing elements shared between different products/ brands/ marquee within the same organization or between organizations.” Example: Howo A7 platform from CNHTC

A vehicle architecture can be defined as “the overall framework of a vehicle, which includes its chassis, suspension, engine, transmissions, cab and other systems. This essentially translates into the DNA of the vehicle and is responsible for the holistic performance characteristics of the vehicle.” Example: Cab-Over-Engine architecture

Platform

Architecture

Module

6NA53-18

A module can be defined as “a set of functional systems/subsystems that can be integrated into the vehicle platform to perform a set of functions.”

Example : Human−machine interfacing module

A system is “a combination of individual components integrated to perform a specific function.” A system can be tested for its performance characteristics with respect to the vehicle’s requirements. Example: Anti-lock braking system

Source: Frost & Sullivan analysis.

Component

A component is “an individual part that forms the elementary building block of a functional system.” Example: Crankshaft

Module

System

40

50

60

70

Beiqi Foton

Dongfeng Motor Corp.CNHTC

Ashok Leyland

TATA Motors

58 57

By 2018, 29 Global HD Truck Platforms are Expected, with Individual Regional Products Built

with up to 70% Localized Components

Heavy-duty Truck Market: Key Truck Platforms, Global, 2011 and 2018

OEMs whose global strategy was in early stages of execution in 2011 are expected to show more pronounced, platform-based product development as they expand geographically.

Nu

mb

er

of

Pla

tfo

rms (

Un

its)

7NA53-18

0

10

20

30

Observed no. of distinct platforms, 2011

Estimated no. of global platforms available,

2011

Observed no. of distinct platforms, 2018

Estimated no. of global platforms available,

2018

TATA Motors

Navistar Inc.

PACCAR Inc.

IVECO

Scania AB

MAN SE

Volvo Group

Daimler Group

2429

Note: All figures are rounded. The base year is 2011. Source: Frost & Sullivan analysis.

Nu

mb

er

of

Pla

tfo

rms (

Un

its)

Year

Note: Within the split Auman GTL, and MAN SITRAK platforms are accounted to both individual OEMs involved, but are counted only once for computing the total.

7

8

6

3

4

3

3

3

0 5 10

Daimler Group

Volvo Group

MAN SE

Scania AB

Observed no. of distinct platforms, 2011Estimated no. of global platforms available, 2011

OEM GroupKey Global Truck and Associated

Platforms Considered

Daimler GroupActros, Axor, Auman GTL (Foton-Daimler JV), BharatBenz

Volvo Group Volvo FM, FH, VE (Eicher-Volvo JV)

MAN SE TGM, SITRAK (CNHTC-MAN JV), CLA (MAN-Force JV)

Scania AB R, P, G series

Expected to Increase by 2018

Expected to stay at current level

Over 50.0 percent of Top 12 Global OEMs Expected to Increase Number of Global Platforms

by 2018; Asia Market Penetration Emerging as Key Strategic Rationale behind the Increase

Heavy-duty Truck Market: Key Truck Platforms, Global, 2011

Number of platforms (Units)

8NA53-18

2

7

6

6

4

5

3

3

3

1

2

3

2

1

2

1

1

Scania AB

IVECO

PACCAR Inc.

Navistar Inc.

TATA Motors

Ashok Leyland

CNHTC

Dongfeng Motor Corp.

Beiqi Foton

IVECO Stralis

PACCAR Inc. XF, LF (DAF Trucks N.V.)

Navistar Inc.9800, CT series (CAT-NC2partnership), MN (Mahindra Navistar brand)

TATA Motors Prima, Novus

Ashok Leyland U series

CNHTC Howo A7, SITRAK (CNHTC-MAN JV)

Dongfeng Motor Corp.

Tianlong

Beiqi Foton Auman GTL

Source: Frost & Sullivan analysis.

OE

M

7

8

6

7

6 6

5

7 7

5

7

6

5 5 55

6

7

8

9

Observed no. of distinct platforms, 2011

Estimated no. of global platforms available, 2011

Observed no. of distinct platforms, 2018

Estimated no. of global platforms available, 2018

Heavy-duty Truck Market: Key Truck Platforms by OEM, Global, 2011 and 2018

Average no. of distinct platforms, 2011 Average no. of global platforms, 2011

5.0

Leading OEMs Expected to Consolidate Regional Platforms and Launch New Multi-national

Platforms, Thereby Increasing the Number of Global Platforms Going Forward

Nu

mb

er

of

pla

tfo

rms (

Un

its)

9NA53-18

3

2

4

3 3

4

3 3 3

1

2

3

2

1

2

1 1

3

2

4

3

4

3

4

3

2

3 3

2

1

2 2 2

0

1

2

3

4

Daimler Group

Volvo Group

MAN SE Scania AB IVECO PACCAR Inc.

Navistar Inc.

TATA Motors

Ashok Leyland

CNHTC Dongfeng Motor Corp.

Beiqi Foton

2.2

Source: Frost & Sullivan analysis.

OEM

Nu

mb

er

of

pla

tfo

rms (

Un

its)

Region Daimler Group Volvo Group MAN SE Scania AB Outlook 2018

EU

Daimler: E,T,A,C-B,S,ELVolvo: E,T,A,C-B,S,ELMAN SE: E,T,A,C-B,S,ELScania: E,T,A,C-B,S,EL

NA

Daimler: E,A,ELVolvo: E, EL, S, AMAN SE:---Scania: ---

Daimler: E,T*,A,C-B,EL

Actros,

AxorFM, FH TGM R, P, G

Platform Strategy Outlook—Key Global OEMsWeighted Average Number of Global Platforms of Leading OEMs is Expected to Grow from

2.1 in 2011 to 2.6 in 2018

Heavy-duty Truck Market: Comparative Outlook of Key Platforms, Global, 2011 and 2018

10NA53-18

India

Daimler: E,T*,A,C-B,ELVolvo: E,EL,T*,C-B,S MAN SE: E,A,EL,C-BScania: E,T,C-B,EL,S

China

Daimler: E,T*, ELVolvo: E, T*, EL, C-BMAN SE: E, EL,C-B, AScania: E,T,C-B,EL,S

RoW

Daimler: E,C-B,EL,SVolvo: E,T*,ELMAN SE: E,C-B,ELScania: E,T,C-B,EL,S

Scenario, 2011

E, T, S, EL E, T, EL, E, A, C-B E,T,C-B,EL,S

BharatB

enz

Auman

GTL

VE CLA

SITRAK

Legend:E: Engine, T: Transmissions, A: Axles, C-B: Cab and body, S: Safety, EL: Electronics

T* : Indicative of variation in technology/module sharing w.r.t other regions 2011 2018

Source: Frost & Sullivan analysis.

Region IVECO Navistar Inc. TATA Motors CNHTC Outlook 2018

EU

IVECO: E, T, ELTATA: E,T, C-B,EL, SCNHTC: E,T,C-B, EL,A

NA

Navistar Inc., : E,T,C-B,EL

TATA Motors: E,T,A,C-B,EL,S

Stralis

Heavy-duty Truck Market: Comparative Outlook of Key Platforms, Global, 2011 and 2018

Platform Strategy Outlook—Key Global OEMs (continued)Weighted Average Number of Global Platforms of Leading OEMs is Expected to Grow from

2.1 in 2011 to 2.6 in 2018

11NA53-18

India

TATA Motors: E,T,A,C-B,EL,SNavistar Inc., : E, T, C-B

China

IVECO:E, T, EL, SNavistar Inc.,: E,C-B,EL,SCNHTC: E,T,A,C-B,S,EL

RoW

IVECO: E,T, ELNavistar Inc.,: E,T,A,C-B,EL,S TATA Motors: E,T,A, C-B,EL,SCNHTC: E,T,C-B,A,S,EL

Scenario, 2011

E E E,T,A E,T,C-B,EL

Legend: E: Engine, T: Transmissions, A: Axles, C-B: Cab and body, S: Safety, EL: Electronics 2011 2018

MN

CTGenlyon

Prima

Source: Frost & Sullivan analysis.

SITRAK

HowoA7

9800

• Platform-based production of key models (global and regional) expected to constitute 38.0 percent of total truck production by 2018

• Major contributors to this increase will be growth in India- and China-specific products, harmonization and sharing of technology platforms by European OEMs, and synergies emerging from joint ventures and mergers in the industry. This is expected to lead towards vertical integration for EU and NA OEMs and supplier dependencies for BRIC OEMs

By 2018, Platform-based Production to Account for More than One Third of Total Production

Volume of Key Global OEMs

Criteria 2011 Scenario 2018 Scenario

Global platform-basedmodels with more than 40K 3 7

Heavy-duty Truck Market: Platform-based Production Snapshot, Global, 2011 and 2018

12NA53-18

Source: Frost & Sullivan analysis.

models with more than 40K units production

3 7

No. of OEMs exceeding 40K units production across different regions (all modelsinclusive)

4 8

Share of global platforms to total production (all OEMs inclusive)

12.0% 14.0

%74.0%

16.0%

22.0%62.0

%

Platform-based production global models

Platform-based production regional models

Non-platform-based production

Modular Production System—Scania AB Case StudyStandardized Interfaces with Flexibility across Various Model Configurations Enable Scania AB to Modularize All Major Component Subsystems

• Standardized interfaces across product models

• Maximum flexibility, since parts fit together independent of model variations

Strategy

Doors, side walls, and few combination of components compose the three cab families

Number of Before After

Sheet metal components

1400~1450 350~400

Interiors 1750~1800 580~620

Cab – top 7 3

Cab – front 8 3Execution

P, G, R series cab

Heavy-duty Truck Market: Scania Cab Family Modularization Snapshot, 2011

13NA53-18

Strategy Cab – front 8 3

Cab – door 12 8

Windscreen 3 1

• Estimated 50.0 percent model-focused part reduction achieved

• 30.0−50.0 percent reduction in design and development cost estimated

• 10.0 percent manufacturing cost reduction, and 30.0 percent reduction in sales and service expenses

Problem

• Dynamic customer preferences, leading to high manufacturing costs

• Increasing inventory, and bill-of-materials on product portfolio expansion, resulting in high operational costs

Source: Scania and Frost & Sullivan analysis.

Execution

Results

Parameter Daimler Group

Volvo Group

MAN SE Scania AB Navistar Inc. TATA Motors

CNHTC

No. of global platforms 2011

4 3 3 3 3 2 2

Platformdescription

Actros,Axor, Auman GTL,BharatBenz

FM, FH, VE TGM, SITRAK,CLA

R, P, G series MN, CT series Prima, Novus SITRAK, HowoA7

Platform hub (production)

Europe, China, India

Europe, India Europe, China, India

Europe India, North America, Latin America

India, South Korea

China

Target market Europe, South Europe, South Europe, Asia Europe, South India, Asia India, Asia China, Asia

Comparative Analysis—Key Global OEMsParameters Representative of Global Platform Strategy and Future Outlook

No

te: In

form

atio

n a

nd

ra

tin

gs a

re b

ase

d o

n F

rost &

Su

lliva

n a

na

lysis

.

Heavy-duty Truck Market: Comparative Analysis of HD Truck Platforms by Key OEMs, Global, 2011

14NA53-18

Target market (sales)*

Europe, South America, Asia Pacific

Europe, South America, Asia Pacific

Europe, Asia Pacific, Latin America

Europe, SouthAmerica, China, India

India, AsiaPacific, Americas

India, Asia Pacific, Middle East, Africa

China, Asia Pacific, SouthAmerica

Approx. % of common systems across regions, 2011

35.0−40.0 30.0−40.0 25.0−30.0 55.0−60.0 20.0−25.0 30.0−40.0 10.0−15.0

Approx. % of common systems across regions, 2018

50.0−55.0 50.0−55.0 45.0−50.0 65.0−70.0 37.0−43.0 35.0−40.0 30.0−35.0

No. of global platforms 2018

4 3 4 3 3 2 2

F&S success potential rating of platform

4.4 4.2 4.2 4.0 3.6 3.3 3.6

1 52 3 4 1 52 3 4 1 52 3 4 1 52 3 4 1 52 3 4 1 52 3 4 1 52 3 4

No

te: In

form

atio

n a

nd

ra

tin

gs a

re b

ase

d o

n F

rost &

Su

lliva

n a

na

lysis

. A

ssu

mp

tio

ns li

ste

d in

th

e f

ollo

win

g s

lide

.

Source: Frost & Sullivan analysis.

Parameter Daimler Group

Volvo Group

MAN SE Scania AB Navistar Inc.

TATA Motors

CNHTC

Emission

compliance (best)

Euro 6, EPA 2010

EEV, EPA 2010

Euro 6, EPA 2010

Euro6 EPA 2010, Euro 4

Euro 4, Euro 5 protected

Euro 4

Base transmission type

AMT for EU, Manual for India and

China

AMT for EU, Manual for India

AMT for EU, Manual for India and

China

AMT and AT Manual Manual Manual, AMT

Comparative Analysis—Key Global OEMs (continued)Parameters Representative of Global Platform Strategy and Future Outlook

Heavy-duty Truck Market: Comparative Analysis of HD Truck Platforms by Key OEMs, Global, 2011

15NA53-18

China China

Supplieropportunity index

3.9 3.7 4 3.2 4.1 4.4 4.2

Note:• Only key global OEMs listed based on Frost & Sullivan assumptions.• Frost & Sullivan proprietary list of key factors and attributes considered for analysis of data. • Indices are representative and are for comparative purposes only.• Indices on scale of 1 to 5, with 1 being lowest, 5 being highest.• * is indicative of only the key target markets for sales of the respective model.

1 52 3 4 1 52 3 41 52 3 41 52 3 4 1 52 3 41 52 3 41 52 3 4

Source: Frost & Sullivan analysis.

Outlook for 2018Participants with Global Platform Portfolio, Strong Presence in Growth Markets, and Regional

Branding Expected to Sustain Profits Globally

6

7

8

9

10

Daimler Group

Volvo Group

MAN SENavistar Inc.

IVECO

Clear global strategy, strong product mix

Global strategy evolving, strong regional products

Size of bubble represents expected production volume attributable to platform-based HD truck models by 2018

Sought-after zone

Sustained profits, globally

Ove

rall

Glo

ba

l P

res

en

ce

In

de

x

Heavy-duty Truck Market: OEM Outlook Comparative Analysis, Global, 2018

16NA53-18

Expected Number of Global Platforms Available, 2011 Source: Frost & Sullivan analysis.

0

1

2

3

4

5

6

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

Scania AB

PACCAR Inc.

Dongfeng Motor Corp.

Beiqi Foton

IVECO

Ashok Leyland

TATA Motors

Profitable, only at

regional level

Ove

rall

Glo

ba

l P

res

en

ce

In

de

x

CNHTC

Contents

Section Slide Number

Executive Summary 4

Research Objective, Scope, Methodology and Background 25

Definitions and Segmentation 32

Vehicle Platform—Introduction 39

Megatrends and Industry Convergence Implications 50

17NA53-18

Market Dynamics—Global Heavy-duty Truck Market 53

Industry Forecasts 63

Platform Strategies of Major Global HCV OEMs 77

Comparative Analysis of Platform Strategy, Global Footprint, and Penetration Potential of Major Global HCV OEMs

120

Impact of OEMs’ Platform Strategy on Supplier Community 133

Conclusions and Strategic Recommendations 141

Appendix 151

Key OEM Groups Compared in this Study

The OEM groups compared in this study are as follows:

Group OEMs

Daimler GroupDaimler Trucks North America LLC, Daimler AG Commercial Vehicles Europe, Beijing Foton Daimler Automotive Co. Ltd, Daimler India Commercial Vehicles, Mitsubishi Fuso Truck Company Ltd.

Volvo GroupVolvo Trucks North America, Mack Trucks North America, Volvo Trucks Europe, Renault Trucks, UD Trucks, Volvo Trucks India, Eicher Volvo Commercial Vehicles

MAN SE MAN Truck & Bus Europe, MAN Latin America

Scania AB Scania AB Europe

18NA53-18

Source: Frost & Sullivan analysis.

Scania AB Scania AB Europe

IVECO IVECO, SAIC-IVECO Commercial Vehicles China

PACCAR Inc. Peterbilt Truck Company, Kenworth Truck Company, DAF Trucks N.V

Navistar, Inc. Navistar International, Mahindra Navistar Automotive Ltd.

TATA Motors TATA Motors Commercial Vehicle India, TATA Daewoo Commercial Vehicles

Ashok Leyland Ashok Leyland Trucks India

CNHTC China National Heavy Truck Company

Dongfeng Motor Corp. Dongfeng Trucks

Beiqi Foton Foton Trucks China

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

Your Feedback is Important to Us

19NA53-18

Source: Frost & Sullivan analysis.

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

20NA53-18

Source: Frost & Sullivan analysis.

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Ananth S.

Senior Research Analyst,

Automotive & Transportation

(9144) 6681.4175

Jeannette Garcia

Corporate Communications

Automotive & Transportation

(210) 477-8427

21NA53-18

Source: Frost & Sullivan analysis.

Sandeep Kar

Research Director, Commercial Vehicles

Automotive & Transportation

(001)416.490.7796

Related Documents

![Bosch ESI[truck] Heavy Duty Truck Software Update – Q1 ...€¦ · Bosch ESI[truck] Heavy Duty Truck Software Update | Ver 2019/1 6 | 41 41135 42908 45411 47482 37000 38000 39000](https://static.cupdf.com/doc/110x72/600ed0e779e62601223e82fb/bosch-esitruck-heavy-duty-truck-software-update-a-q1-bosch-esitruck-heavy.jpg)