By Rahil Ahamed

Analysis of FMCG industry in India

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

By Rahil Ahamed

• FMCG stands for Fast-moving consumer goods. It is also known as consumer packaged goods(CPG).

• These are products that are sold quickly and at a relatively low cost.

• Though the profit margin made on FMCG products is relatively small(more so for retailers than the producers/suppliers), they are generally sold in large quantities; thus, the cumulative profit on such products can be substantial.

• FMCG is probably the most classic case of low margin and high volume business.

• Examples include non-durable goods such as soft drinks, toiletries, over the counter drugs, toys, processed foods and many other consumables.

• The FMCG industry is poised to grow 10 to 12 percent annually.

• The organised retail has created new channels for FMCG players through diverse retail such as departmental stores , hypermarkets etc.

• Rivalry among players is very high in the FMCG industry.

• Competition is cut throat(this results in brand wars)

• Price competition

• Advertisement and promotional stuff – Price wars (eg: coke vs pepsi)

• Distribution

• New product

• Storage

• Exit barriers are low

• Warranty and guarantee

• No barriers to entry.

• Low resistance and high complexity leads to easy to enter.

• New entrants offer tough competition due to cost effectiveness.

• Not a capital intensive sector, therefore, even small players can enter.

• Potential entry is highly viable.

• Consumer needs are complex and never ending.• Lack of one company to satisfy all needs gives sufficient room for new product development.• There are plenty of substitutes available and a wide range of choices in this industry.Eg(HUL,ITC).• Range of choices leads to higher consumer expectation and gives rise to substitutes.

• The bargaining power of suppliers of raw materials and intermediate goods is

not very high.

• There is ample number of substitute suppliers available and the raw materials

are also readily available and most of the raw materials are homogeneous.

• There is no monopoly situation in the supplier side because the suppliers are

also competing among themselves.

• Bargaining power of consumers is also very high.

• The switching costs of most of the goods is very low in the FMCG industry.

• There is no threat of buying one product over the other.

• Customers are never reluctant to buy or try new things off the shelf.

Growth rate over the

past 3-5 years

• The FMCG industry is currently growing at double digit growth rate and is expected to maintain a high growth rate.

• It has grown at an annual average of 11 % over the last decade.

• The past 3 to 5 years has seen fluctuations in the growth rate of FMCG industry due to inflation.

• The urban FMCG industry has been growing at a fairly steady and healthy rate over the last 3 years.

• The latest growth figure (September 2013) was 4.7 % in the urban market and 6.7% in the rural market.

Expected growth rate in the

future

• The Indian FMCG sector is the fourth largest sector in the economy with a total market size of US$18 billion as of 2007.

• FMCG industry is expected to maintain a robust growth rate as the population is increasing.

• The organised sector is account to 14-18 % of the share.

• The FMCG industry was a laggard in 2000-2005. However , it witnessed phenomenal growth rate in the next half of the decade.

• The FMCG industry is expected to witness further accelerated growth rate in the coming decade aided by urbanisation , changing demographics and increase in private final consumption .

• Overall, the FMCG industry is expected to increase at a compound annual growth rate at 14.7 percent , with a rural FMCG market expected to increase at 17.7 %.

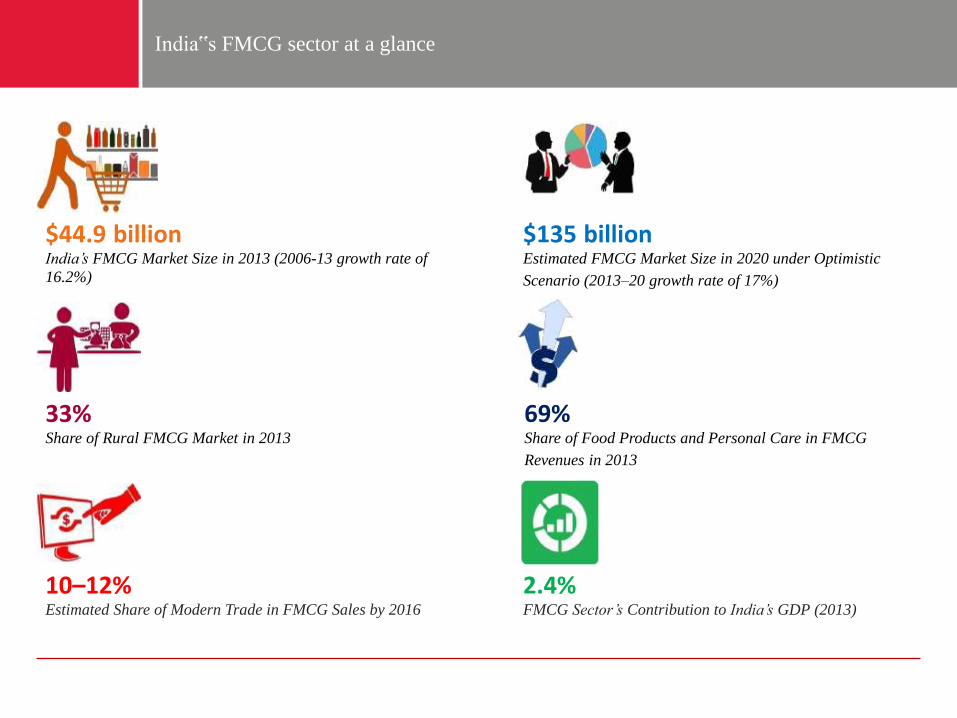

33%Share of Rural FMCG Market in 2013

$44.9 billionIndia’s FMCG Market Size in 2013 (2006-13 growth rate of

16.2%)

2.4%FMCG Sector’s Contribution to India’s GDP (2013)

10–12%Estimated Share of Modern Trade in FMCG Sales by 2016

69%Share of Food Products and Personal Care in FMCG

Revenues in 2013

$135 billionEstimated FMCG Market Size in 2020 under Optimistic

Scenario (2013–20 growth rate of 17%)

India‟s FMCG sector at a glance

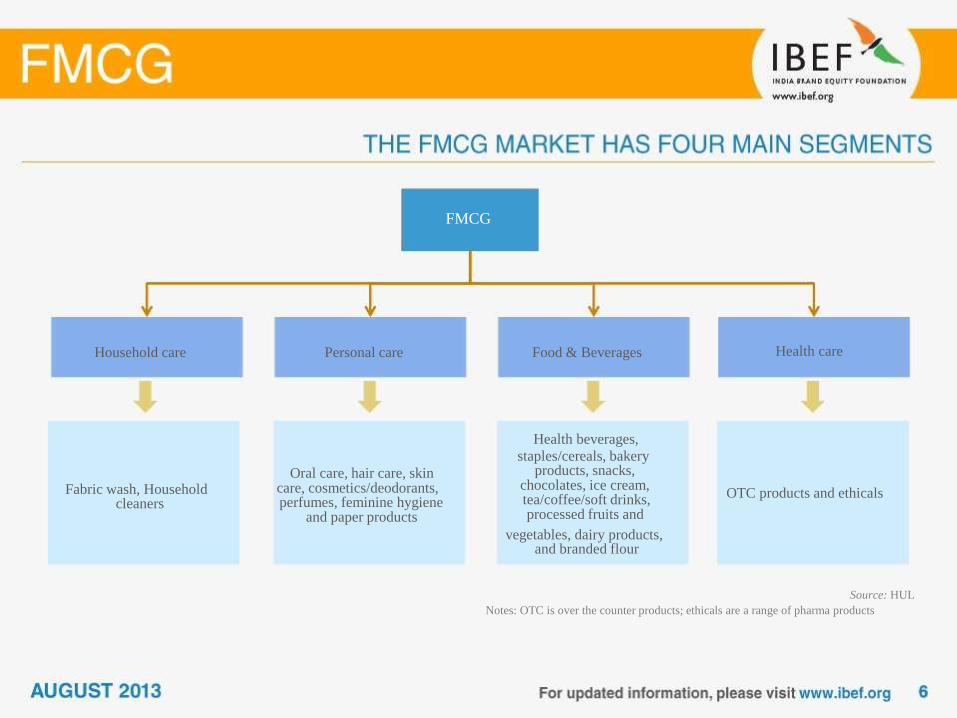

FMCG

Household care

Fabric wash, Householdcleaners

Personal care

Oral care, hair care, skincare, cosmetics/deodorants,perfumes, feminine hygiene

and paper products

Food & Beverages

Health beverages,

staples/cereals, bakeryproducts, snacks,

chocolates, ice cream,tea/coffee/soft drinks,processed fruits and

vegetables, dairy products,and branded flour

Source: HUL

Notes: OTC is over the counter products; ethicals are a range of pharma products

Health care

OTC products and ethicals

Source: Booz & Company, Dabur, AC Nielsen, Aranca Research

Trends in FMCG revenues over the years(USD billion)

The FMCG sector in India generated revenues worth

USD36.8 billion in 2012, a 5.7 per cent rise compared to the

previous year

The strong growth in 2012 should come as no surprise

given the impressive performance of the sector over the

years

Over 2006-12, the sector’s revenues posted a CAGR of

15.2 per cent 15.7

17.8 21.3

24.2

30.2

34.836.8

2006 2007 2008 2009 2010 2011 2012

CAGR: 15.2%

Market break-up by revenue (2009)‘Food products’ is the leading segment, accounting for 43.0

per cent of the overall market

Personal care (22.0 per cent) and fabric care (12.0 per cent)

are the other leading segments

43%

22%

8%

12%

4%

4%

2%5% Food products

Personal care

Fabric care

Hair care

Households

OTC products

Baby care

Others

Source: Dabur, Aranca Research

8

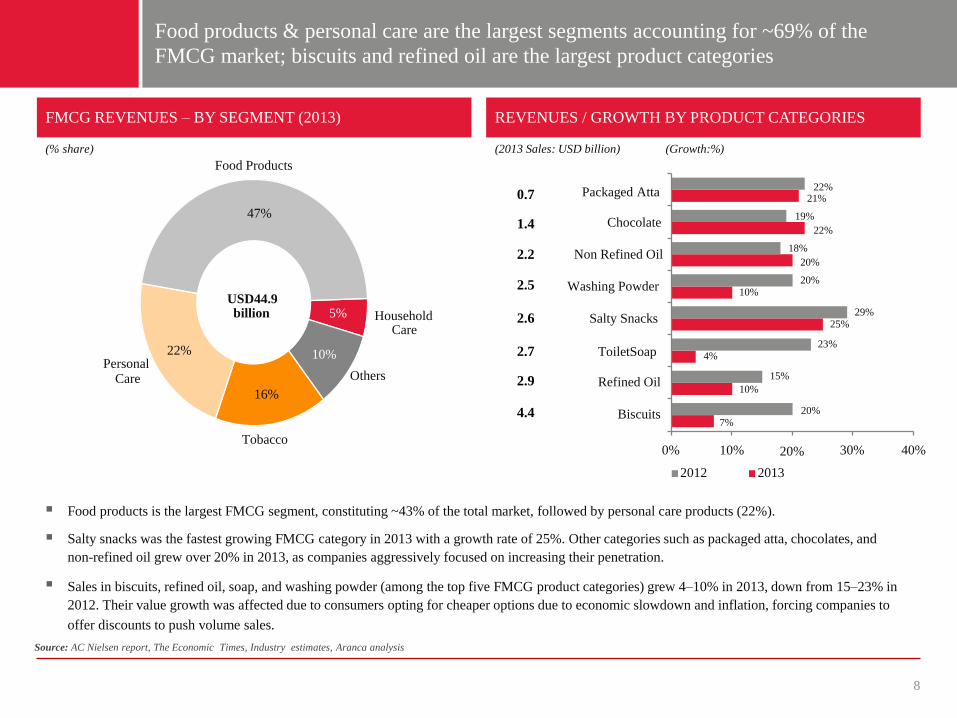

Food products is the largest FMCG segment, constituting ~43% of the total market, followed by personal care products (22%).

Salty snacks was the fastest growing FMCG category in 2013 with a growth rate of 25%. Other categories such as packaged atta, chocolates, and

non-refined oil grew over 20% in 2013, as companies aggressively focused on increasing their penetration.

Sales in biscuits, refined oil, soap, and washing powder (among the top five FMCG product categories) grew 4–10% in 2013, down from 15–23% in

2012. Their value growth was affected due to consumers opting for cheaper options due to economic slowdown and inflation, forcing companies to

offer discounts to push volume sales.

FMCG REVENUES – BY SEGMENT (2013) REVENUES / GROWTH BY PRODUCT CATEGORIES

Source: AC Nielsen report, The Economic Times, Industry estimates, Aranca analysis

10%

4%

25%

10%

15%

23%

29%

22%21%

19%

22%

18%

20%

20%

Biscuits

ToiletSoap

Refined Oil

Salty Snacks

Packaged Atta

Chocolate

Non Refined Oil

Washing Powder

0%

7%

10%

20%

20% 30% 40%

2012 2013

0.7

1.4

2.2

2.5

2.6

2.7

2.9

4.4

(Growth:%)(% share) (2013 Sales: USD billion)

Food products & personal care are the largest segments accounting for ~69% of the

FMCG market; biscuits and refined oil are the largest product categories

5%

10%

16%

22%

47%

USD44.9billion

PersonalCare

HouseholdCare

Food Products

Others

Tobacco

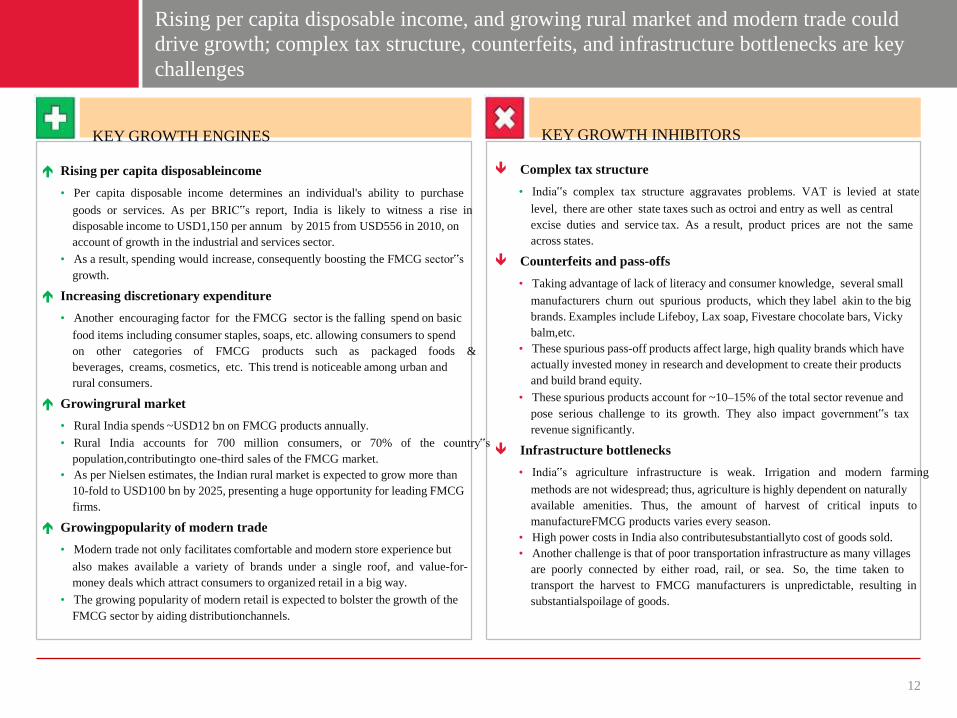

KEY GROWTH ENGINES

Rising per capita disposableincome

• Per capita disposable income determines an individual's ability to purchase

goods or services. As per BRIC‟s report, India is likely to witness a rise in

disposable income to USD1,150 per annum by 2015 from USD556 in 2010, on

account of growth in the industrial and services sector.

• As a result, spending would increase, consequently boosting the FMCG sector‟s

growth.

Increasing discretionary expenditure

• Another encouraging factor for the FMCG sector is the falling spend on basic

food items including consumer staples, soaps, etc. allowing consumers to spend

on other categories of FMCG products such as packaged foods &

beverages, creams, cosmetics, etc. This trend is noticeable among urban and

rural consumers.

Growingrural market

• Rural India spends ~USD12 bn on FMCG products annually.

• Rural India accounts for 700 million consumers, or 70% of the country‟s

population,contributingto one-third sales of the FMCG market.

• As per Nielsen estimates, the Indian rural market is expected to grow more than

10-fold to USD100 bn by 2025, presenting a huge opportunity for leading FMCG

firms.

Growingpopularity of modern trade

• Modern trade not only facilitates comfortable and modern store experience but

also makes available a variety of brands under a single roof, and value-for-

money deals which attract consumers to organized retail in a big way.

• The growing popularity of modern retail is expected to bolster the growth of the

FMCG sector by aiding distributionchannels.

KEY GROWTH INHIBITORS

Complex tax structure

• India‟s complex tax structure aggravates problems. VAT is levied at state

level, there are other state taxes such as octroi and entry as well as central

excise duties and service tax. As a result, product prices are not the same

across states.

Counterfeits and pass-offs

• Taking advantage of lack of literacy and consumer knowledge, several small

manufacturers churn out spurious products, which they label akin to the big

brands. Examples include Lifeboy, Lax soap, Fivestare chocolate bars, Vicky

balm,etc.

• These spurious pass-off products affect large, high quality brands which have

actually invested money in research and development to create their products

and build brand equity.

• These spurious products account for ~10–15% of the total sector revenue and

pose serious challenge to its growth. They also impact government‟s tax

revenue significantly.

Infrastructure bottlenecks

• India‟s agriculture infrastructure is weak. Irrigation and modern farming

methods are not widespread; thus, agriculture is highly dependent on naturally

available amenities. Thus, the amount of harvest of critical inputs to

manufactureFMCG products varies every season.

• High power costs in India also contributesubstantiallyto cost of goods sold.

• Another challenge is that of poor transportation infrastructure as many villages

are poorly connected by either road, rail, or sea. So, the time taken to

transport the harvest to FMCG manufacturers is unpredictable, resulting in

substantialspoilage of goods.

12

Rising per capita disposable income, and growing rural market and modern trade could

drive growth; complex tax structure, counterfeits, and infrastructure bottlenecks are key

challenges

Rural market

Innovative products

Premium products

Sourcing base

Penetration

•

•

•

•

•

•

•

•

Leading players of consumer products have a strong distribution network in rural India;

they also stand to gain from the contribution of technological advances such as internet

and e-commerce to better logistics

Rural FMCG market size is expected to touch USD100 billion by 2025

Indian consumers are highly adaptable to new and innovative products. For instance there

has been an easy acceptance of men’s fairness creams, flavoured yoghurt, and cuppa

mania noodles

With rise disposable incomes mid- and high-income consumers in urban areas have

shifted their purchase trend from essential to premium products

In response, firms have started enhancing their premium products portfolio

Indian and multinational FMCG players can leverage India as a strategic sourcing hub for

cost-competitive product development and manufacturing to cater to international markets

Low penetration levels offer room for growth across consumption categories

Majors players are focusing on rural markets to increase their penetration in those areas

Source: Assorted articles and reports; AC Nielsen, Aranca Research

CRITICAL SUCCESS FACTORS

2

c

Innovation track recordTo maintain customer interest and to stay ahead of the competition, companies need toconstantlyintroduce new and better products.A company's product innovation capabilities and track record in creating successful brands.One good indicator of innovation is the contribution to revenues, of brands that have been

introduced in the last three to five years.

DifferentiationThe first and foremost factor is a product's perceived benefit and differentiation vis-a-vis others in the market.A product can command a premium only if the consumers are convinced of its superiority.

Market share• The market share trends of a company's products.• A consistently high market share has several advantages. It ensures a stable relationship with and

better control over the distribution channel.• Also, the company does not need to offer very high margins to the trade since this is compensated

by• higher volumes.• Established products with high market share also entail lower marketing and advertising• expenses since it is cheaper to maintain an established brand than to create a new one.

3

Pricing PowerA high market shares do not necessarily translate into price protection.Companies with small market shares can still pose strong price competition to the market leaders.

Brand equityBrand equity is the degree of consumer loyalty that a company's products maintain.This is an important factor since established brands act as high entry barriers.If brand loyalty is strong, consumers tend to be willing to pay a high price for the product, and arereluctant to switch to competitive products.

During periods of slow growth and economic recession, the companies are often tempted to showhighershort-term profits by reducing their advertising expenditure.The companies with successful brands have an edge over their competitors, supported by greaterassociation with customers and lower advertisingexpenses.

Operating efficiencyWide and extensive distribution reach, continuous cost-cutting efforts, optimal manufacturingfacilitiesand efficient raw material sourcing are critical elements that determine an FMCG company'soperatingefficiency.

SIZE OF THE TOP 5 PLAYERS FOR THE FMCG INDUSTRY

Market Capitalization – 256,769 crores

Market Capitalization – 127,144 crores

Market Capitalization – 49,768 crores

Market Capitalization – 28,107 crores

Market Capitalization – 27,261 crores

GROWTH OVER THE LAST 3-5 YEARS

•Hindustan Unilever's distribution covers over 2 million retail outlets across India directly and its products are available in over 6.4 million outlets in the country.

As per Nielsen market research data, two out of three Indians use HUL products.

•Nestlé’s sales in India had been growing at about 20 per cent a year in the three years to 2012, but this growth decelerated sharply – to 8 per cent – in the third quarter of last year.Sales in India account for only 1.5 per cent of Nestlé’s global sales, but the group has invested Rs35bn ($569m) in the past four years to increase its manufacturing capacity there, expanding seven existing plants and setting up one new facility.

•In the last three years, GCPL has been growing about 28 to 29 per cent annually.From 15 per cent in 2009-10, almost 50 per cent of flagship company Godrej Consumer Products' revenues now come from international markets. At the group level, it has a stated 10x10 strategy, to grow ten times in ten years both organically and inorganically, and international business is an important focus area.

•With FMCG revenues of Rs 7,000 crore in 2012-13, it has already nosed ahead of Nestle.ITC’s non-cigarette FMCG business grew 26.4% during last fiscal, while net overall revenue reported a growth of 19.4% at Rs 29,605.58 crore.

•Dabur has been one of the few companies in the Fast Moving Consumer Goods industry who have managed a double-digit growth this year. Dabur has been able to manage a healthy growth of 11.9%over last year.The industry focused on reaping the benefits of internal economies that resulted in average industry bottom line growth of 25%.

SEGMENTAL PRESENCE OF THE TOP PLAYERS

FMCG- Cigarettes & Cigars- Foods- Lifestyle Retailing- PersonalCare-Education and Stationery- Safety Matches- Agarbattis

Food and drink-Home care-Personal care-Water purifier

Hair Care-Home Care-Personal Care

Milk Products and Nutrition-Beverages-Prepared Dishes and Cooking Aids-Chocolates and Confectionery

Health Care-Personal Care-Foods-Home Care-Consumer Health –Ethical-Professional Range-Guar Gum

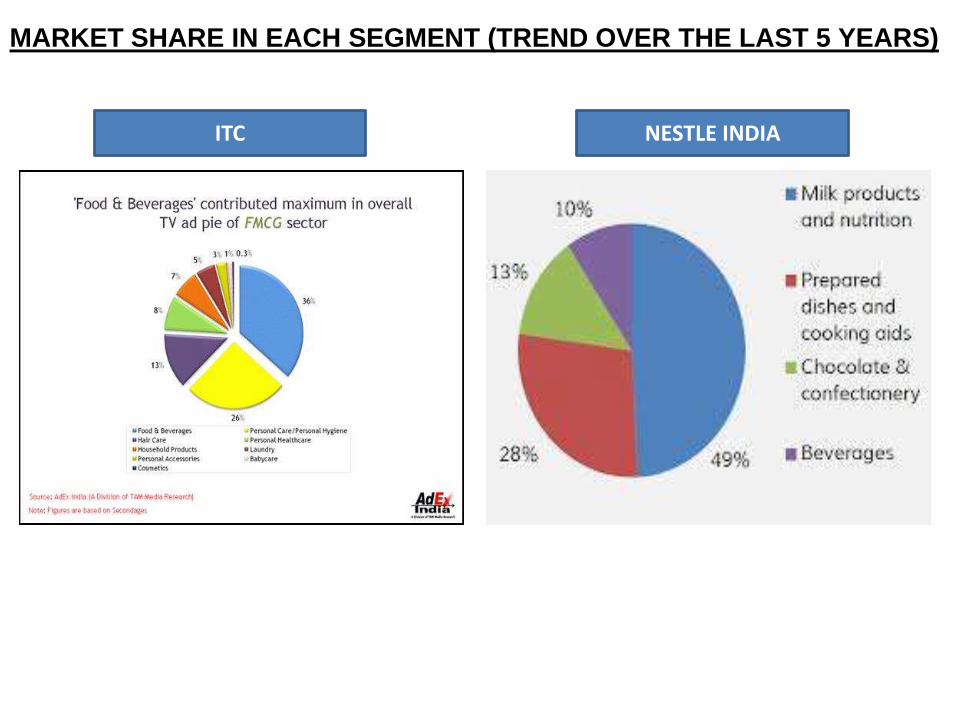

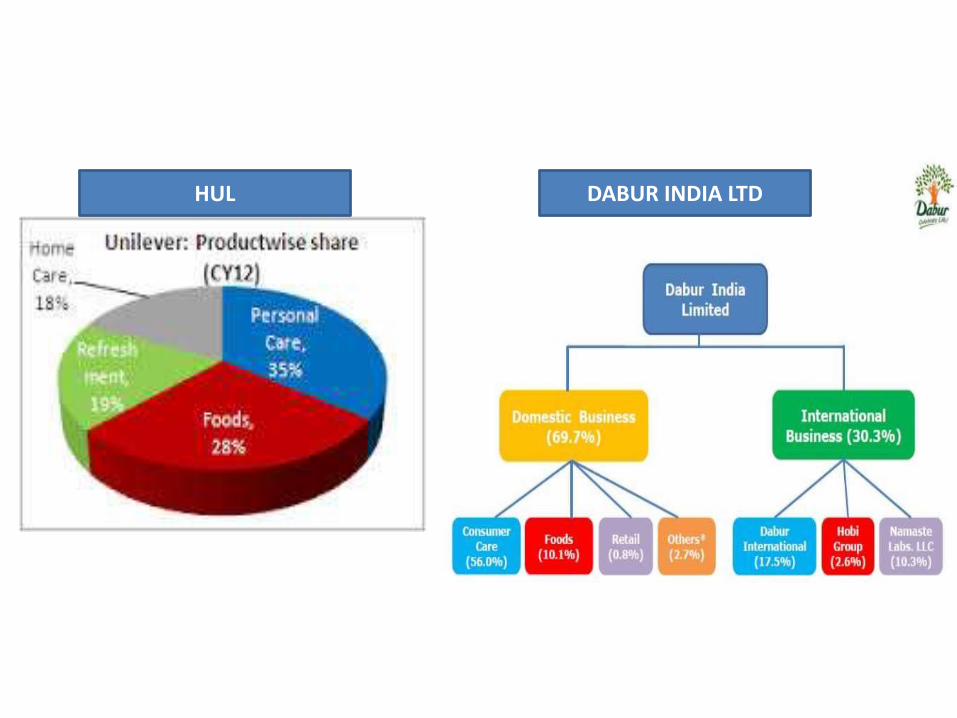

MARKET SHARE IN EACH SEGMENT (TREND OVER THE LAST 5 YEARS)

ITC NESTLE INDIA

HUL DABUR INDIA LTD

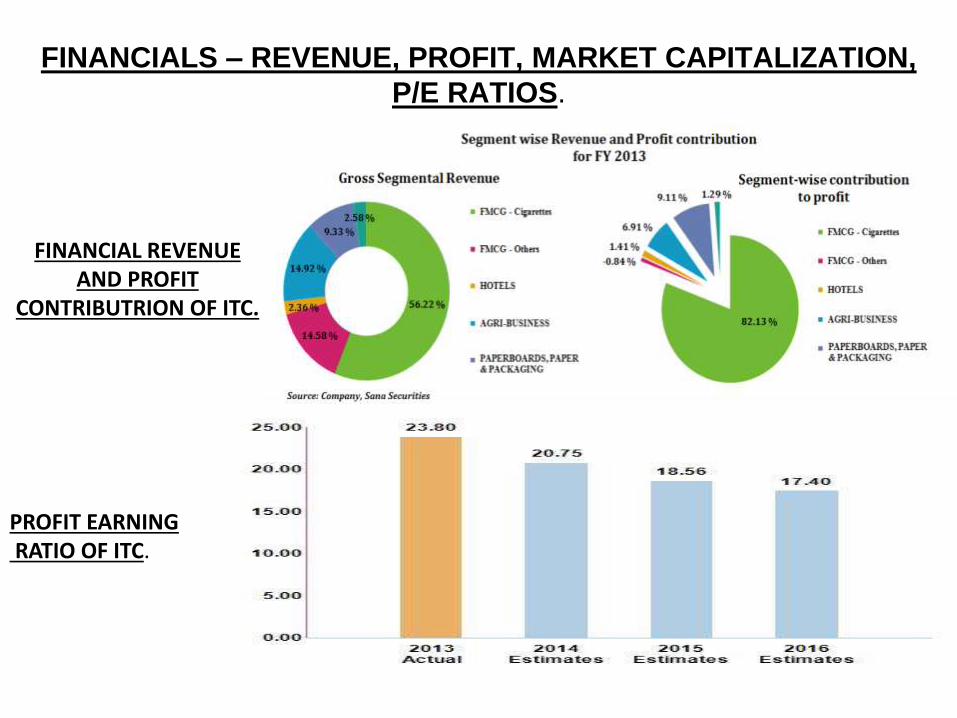

FINANCIALS – REVENUE, PROFIT, MARKET CAPITALIZATION,

P/E RATIOS.

PROFIT EARNINGRATIO OF ITC.

FINANCIAL REVENUE AND PROFIT

CONTRIBUTRION OF ITC.

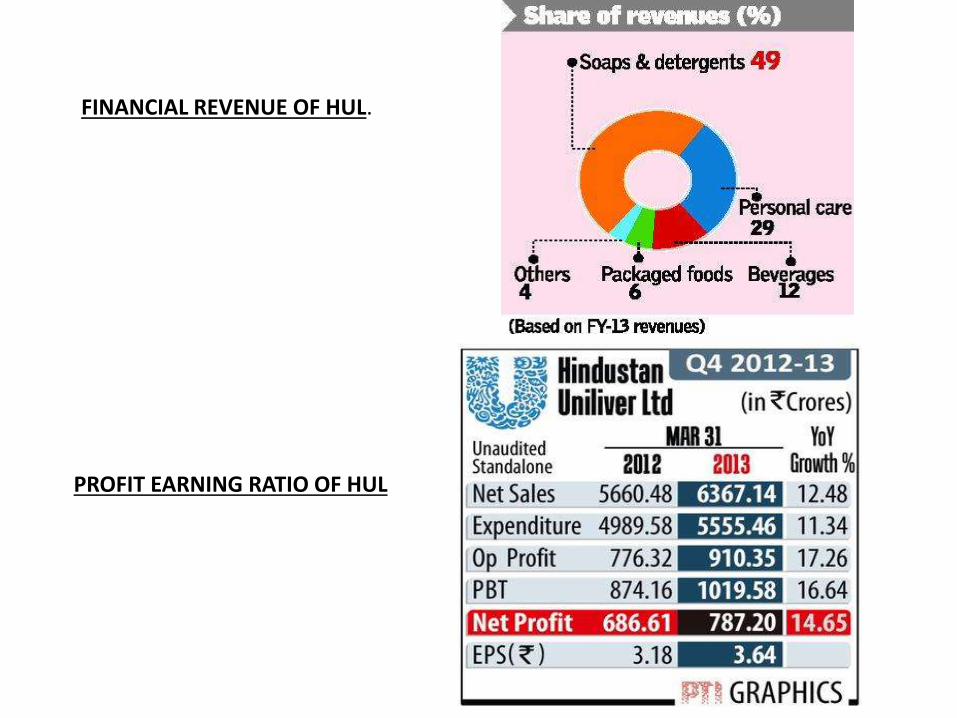

PROFIT EARNING RATIO OF HUL

FINANCIAL REVENUE OF HUL.

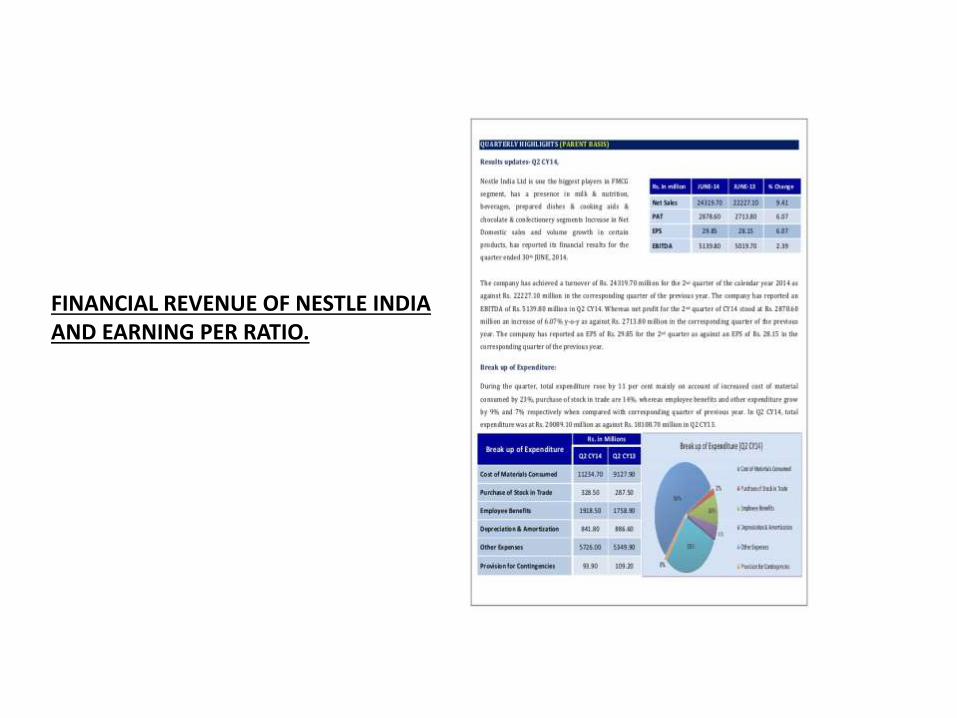

FINANCIAL REVENUE OF NESTLE INDIA AND EARNING PER RATIO.

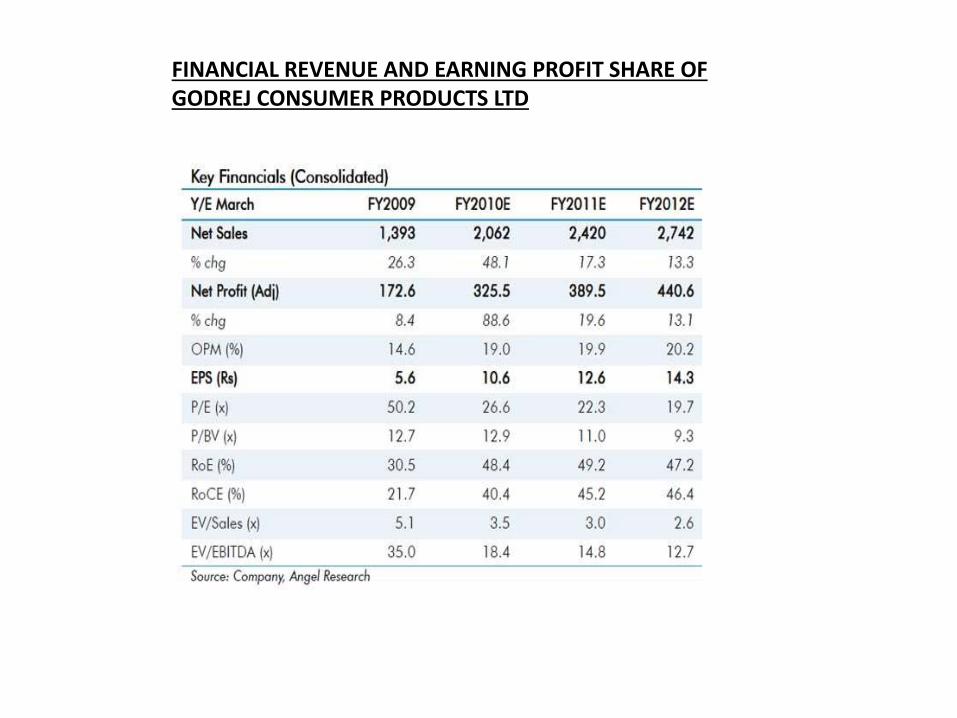

FINANCIAL REVENUE AND EARNING PROFIT SHARE OF GODREJ CONSUMER PRODUCTS LTD

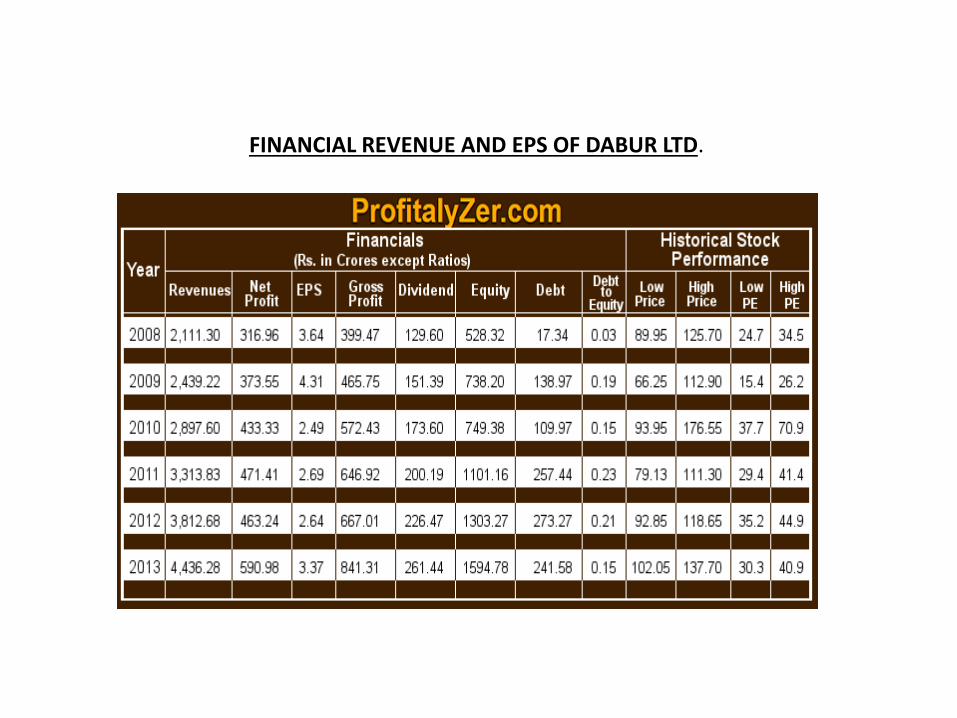

FINANCIAL REVENUE AND EPS OF DABUR LTD.

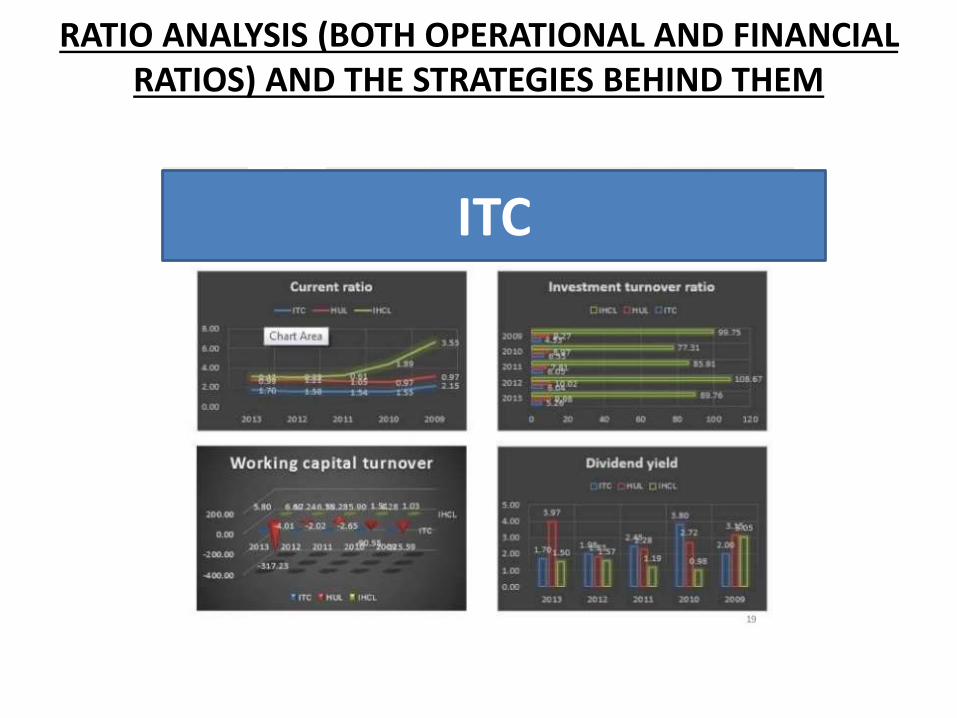

RATIO ANALYSIS (BOTH OPERATIONAL AND FINANCIAL RATIOS) AND THE STRATEGIES BEHIND THEM

ITC

HUL

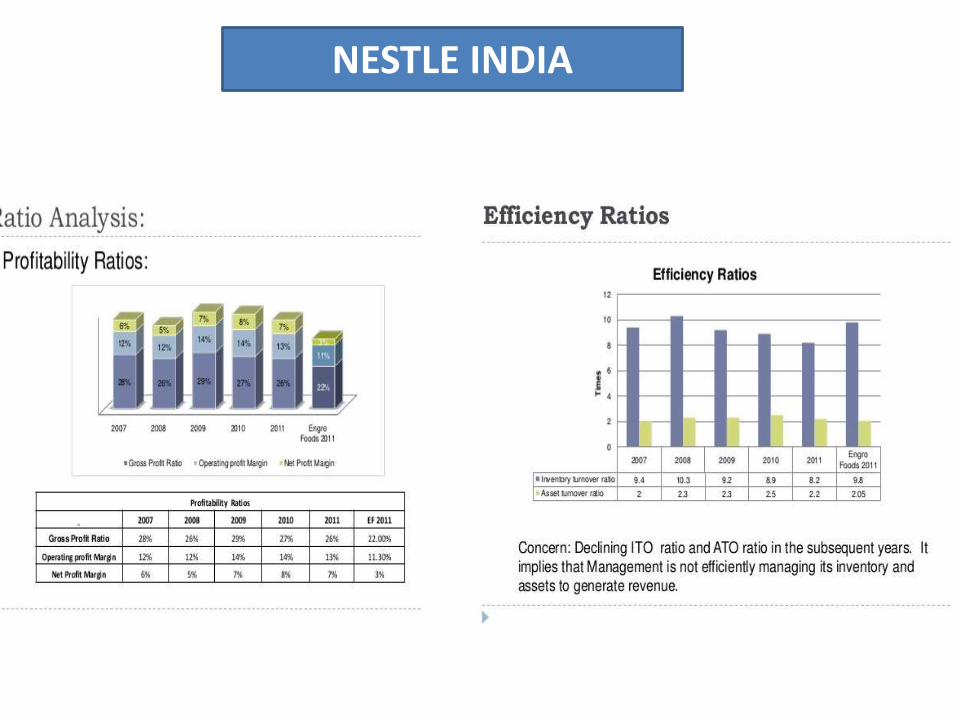

NESTLE INDIA

t

Particulars FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

ROCE 4.57 3.91 13.29 10.96 7.86

ROE / RONW

7.92 11.51 15.20 12.32 12.60

GODREJ

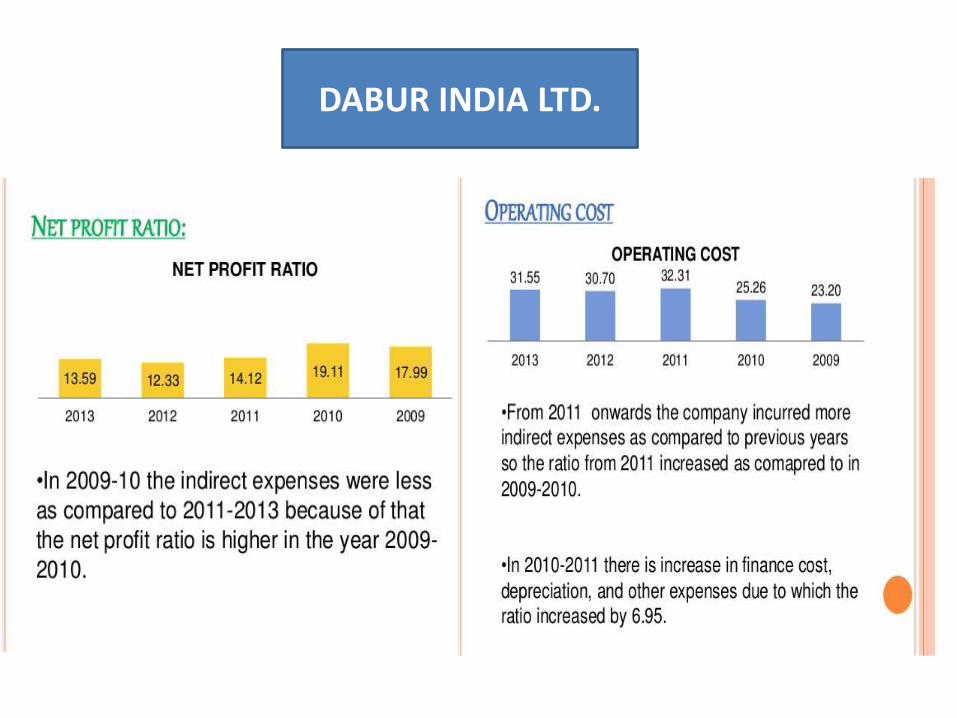

DABUR INDIA LTD.

SWOT ANALYSIS

ITC

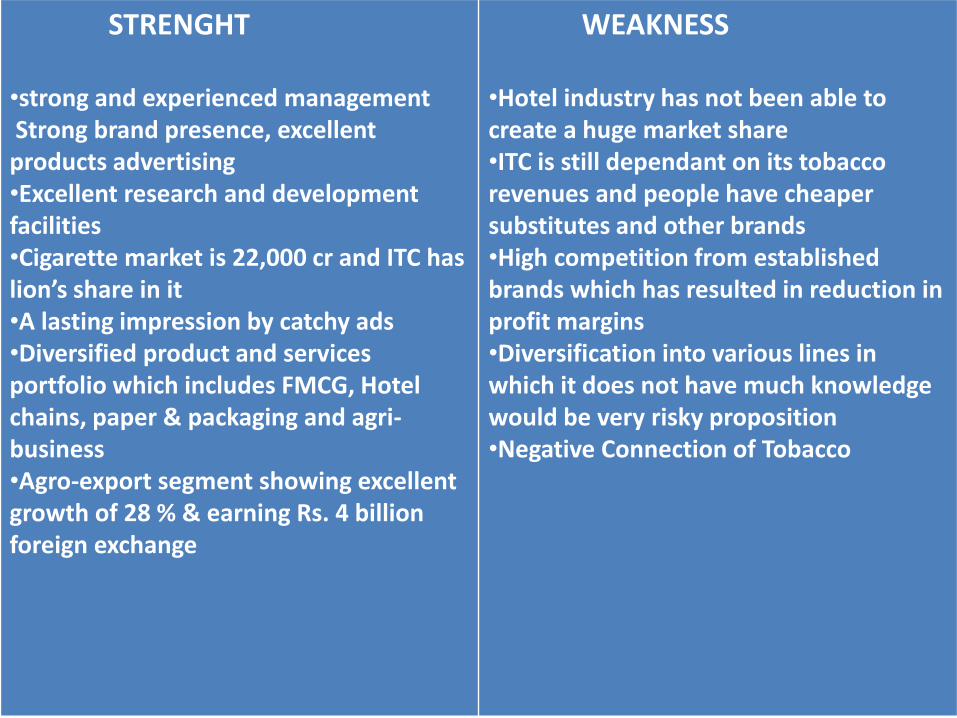

STRENGHT

•strong and experienced managementStrong brand presence, excellent products advertising•Excellent research and development facilities•Cigarette market is 22,000 cr and ITC has lion’s share in it•A lasting impression by catchy ads•Diversified product and services portfolio which includes FMCG, Hotel chains, paper & packaging and agri-business•Agro-export segment showing excellent growth of 28 % & earning Rs. 4 billion foreign exchange

WEAKNESS

•Hotel industry has not been able to create a huge market share•ITC is still dependant on its tobacco revenues and people have cheaper substitutes and other brands•High competition from established brands which has resulted in reduction in profit margins•Diversification into various lines in which it does not have much knowledge would be very risky proposition•Negative Connection of Tobacco

OPPORTUNITY

•Tap rural markets and increase penetration in urban areas•Mergers and acquisitions to strengthen the brand•More publicity of hotel chains to increase market share•Good source of revenue & foreign exchange available by way of exports of agricultural products, hotels & cigarettes•Its competitors don’t have the financial banking like it so it can take advantage of this

THREATS

•Ban on smoking•Increasing Tax on cigarettes•Poor monsoon leads to poor agricultural growth which would affect the agro-exports•Competition from unbranded products•High competition from established brands

HUL

STRENGHT

•HUL is a part of the Unilever group, hence strong brand equity•It has over 15000 employees•Reach 6.4 million retail outlets which includes direct reach to over 1.5 million retail outlets•Products with presence in over 20 consumer categories with over 700 million Indian consumers using its products•As a part of CSR, HUL has initiatives like project Shakti, plastic recycling, women empowerment etc.

WEAKNESS

•Market share is limited due to presence of other strong FMCG brands•HUL products has stiff competition from big domestic players and international brands•Inability to transform its strategies at right time•Lacked the ability to call shots and power pricing

OPPORTUNITY

•Tap rural markets and increase penetration in urban areas•Mergers and acquisitions to strengthen the brand•Increasing purchasing power of people thereby increasing demand•New brand segments: medicines etc.•Diversification

THREATS

•Intense and increasing competition amongst other FMCG companies•FDI in retail thereby allowing international brands•Competition from unbranded and local products

NESTLE

STRENGHT•More than 140 years in the industry•World biggest brand, top brand in Fortune 500 list•Global reach with presence in over 86 countries•An employee strength of around 328,000 people worldwide•Wide product range including baby food, pet food, dairy products, confectioneries, pharmaceuticals, beverages, etc.•Popular brands owned like Maggi, Haagen-Dazs, Boost, Kit Kat, Nescafe, etc.•Largest R&D network facilitating continuous innovation•Strong supply chain network•Mergers and acquisitions and joint ventures to increase market share•Strong marketing and advertising power•Strong brand loyalty and brand recall

WEAKNESS

•Inability to provide consistent quality in food products•Weak implementation of CSR•Being a big global brand, Numerous controversies in different countries of operation can cause issues•Strong competition by other brands

OPPORTUNITY

•Extend Vatika brand to new categories like Skin Care and body wash segments• Increasing income level of the middle class•Dabur is the world’s largest ayurvedicmedicine and its export quantities are constantly in demand in foreign market•The affinity towards yoga and Hinduism is proving more advantageous towards the reach of ayurvedic medicines globally•People have started realizing that ayurvedic medicines like Dabur, Himalayas etc doesn’t have much of side effects•Ayurveda as a field is receiving much more attention across the world in the last 2–3 years. Thus huge opportunity for Dabur to capitalize on the market sentiments

THREATS

•The allopathy players are of major threat as they invest heavily on advertising and distribution of their products through medical representatives etc.•Some ayurvedic doctors give their own medicines or give a mixture of AyurvedicCompany’s product without packaging (loose medicines). This reduces the sales in the market and dilutes the brand image•Kerala is an ayurvedic hub, for most of the treatments. Hence people visit directly and attend health camps to get cured•Competition from unbranded and local products

THANK YOU

Related Documents

![Industry Session - FMCG [Compatibility Mode]](https://static.cupdf.com/doc/110x72/577d2f5f1a28ab4e1eb186e3/industry-session-fmcg-compatibility-mode.jpg)