www.ajbms.org Asian Journal of Business and Management Sciences ISSN: 2047-2528 Vol. 2 No. 10 [38-50] ©Society for Business Research Promotion | 38 Analysis of Customer Satisfaction with the Islamic Banking Sector: Case of Brunei Darussalam Mohamed Sharif Bashir Imam Centre for Banking and Finance Al-Imam Muhammad Ibn Saud Islamic University Riyadh 11432, Kingdom of Saudi Arabia E-mail: [email protected]. ABSTRACT During the last decade, the Islamic banking sector in Brunei Darussalam experienced remarkable and increasingly challenging development in the face of strong competition from conventional banks. The main objective of this paper is to examine the effects of both service quality and product quality, and of satisfaction awareness of Islamic banking in Brunei Darussalam. This study also examines the reasons that consumers select Islamic banking. A questionnaire survey was conducted among Islamic banks’ customers. The findings show that the indirect effects of service quality and product quality on satisfaction awareness were positive and significant. They also revealed that consumers were aware of Islamic banking products and services to a certain degree; and the reasons for preferring them were profitability and religious principles. As a result, these findings provide the Islamic banking industry with helpful guidelines in its efforts to formulate suitable promotional policies to attract more banking customers. Keywords: Islamic banking, Islamic finance, customer awareness, customer satisfaction, service quality, Brunei Darussalam. 1. INTRODUCTION Customer satisfaction has been perceived as a key factor in finding out why customers leave or stay with a bank. Generally, any bank needs to know how to keep their customers, even if they seem to be satisfied. As competition within the financial services industry is more intense than ever, and as banking companies’ service menus are becoming increasingly comparable, the need to understand bank customer satisfaction is vital (Rose & Marquis, 2006). Service quality and product quality are vital elements in determining customer satisfaction, as is customer awareness. In this context, quality is the key factor and is synonymous with the consumer’s ability to select from a wide array of products and services that provide a closer match to his or her needs and desires (Ho, Lau, Lee & Ip, 2005). Following this, it is argued that the increasing perception of service quality and product quality will increase customer awareness, which finally increases satisfaction. The relationship between bank customers’ awareness, the quality of service they receive and their level of satisfaction has been investigated in different countries, but there are few studies on Islamic banks. In regards to Brunei Darussalam, empirical research has never been done, nor have the issues of customer awareness, service quality and product quality, and customer satisfaction of Islamic banking been addressed. This paper aims to fill this gap in the literature. Its main objective is to examine the awareness and satisfaction of Islamic banking in Brunei Darussalam. It is interesting to note that this paper differentiates from other studies on the same topic as it investigates the indirect effects of service quality and product quality on satisfaction through customer awareness (Bashir, 2012). The remainder of the paper has been organized in the following way: Section 2 provides a literature review. The research method is discussed in Section 3. Section 4 presents the discussion and findings. The conclusion is presented in the final section.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 38

Analysis of Customer Satisfaction with the Islamic Banking Sector:

Case of Brunei Darussalam

Mohamed Sharif Bashir

Imam Centre for Banking and Finance Al-Imam Muhammad Ibn Saud Islamic University

Riyadh 11432, Kingdom of Saudi Arabia

E-mail: [email protected].

ABSTRACT During the last decade, the Islamic banking sector in Brunei Darussalam experienced remarkable and increasingly challenging development in the face of strong competition from conventional banks. The main objective of this paper

is to examine the effects of both service quality and product quality, and of satisfaction awareness of Islamic banking in Brunei Darussalam. This study also examines the reasons that consumers select Islamic banking. A questionnaire survey was conducted among Islamic banks’ customers. The findings show that the indirect effects of service quality and product quality on satisfaction awareness were positive and significant. They also revealed that consumers were aware of Islamic banking products and services to a certain degree; and the reasons for preferring them were profitability and religious principles. As a result, these findings provide the Islamic banking industry with helpful guidelines in its efforts to formulate suitable promotional policies to attract more banking customers. Keywords: Islamic banking, Islamic finance, customer awareness, customer

satisfaction, service quality, Brunei Darussalam.

1. INTRODUCTION

Customer satisfaction has been perceived as a key factor in finding out why customers

leave or stay with a bank. Generally, any bank needs to know how to keep their customers, even if they seem to be satisfied. As competition within the financial services industry is

more intense than ever, and as banking companies’ service menus are becoming

increasingly comparable, the need to understand bank customer satisfaction is vital (Rose

& Marquis, 2006). Service quality and product quality are vital elements in determining

customer satisfaction, as is customer awareness. In this context, quality is the key factor and is synonymous with the consumer’s ability to select from a wide array of products and

services that provide a closer match to his or her needs and desires (Ho, Lau, Lee & Ip,

2005). Following this, it is argued that the increasing perception of service quality and

product quality will increase customer awareness, which finally increases satisfaction. The

relationship between bank customers’ awareness, the quality of service they receive and

their level of satisfaction has been investigated in different countries, but there are few studies on Islamic banks. In regards to Brunei Darussalam, empirical research has never

been done, nor have the issues of customer awareness, service quality and product quality,

and customer satisfaction of Islamic banking been addressed. This paper aims to fill this

gap in the literature. Its main objective is to examine the awareness and satisfaction of

Islamic banking in Brunei Darussalam. It is interesting to note that this paper differentiates from other studies on the same topic as it investigates the indirect effects of service quality

and product quality on satisfaction through customer awareness (Bashir, 2012).

The remainder of the paper has been organized in the following way: Section 2 provides a

literature review. The research method is discussed in Section 3. Section 4 presents the

discussion and findings. The conclusion is presented in the final section.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 39

1.1 Overview of Brunei’s Islamic Banking Sector

Over the past ten years, Islamic banking industry in Brunei Darussalam has grown rapidly.

Although it makes up a small proportion of the country’s financial market, consumer

interest in this industry is shown by the fact that they hold 40% of whole banking sector’s

assets compared to conventional counterparts that account for 60%. Islamic bank deposits

also constitute 36% of total bank deposits compared to conventional bank with 64%, while

loans accounted for 48% from Islamic banks compared to 52% from conventional banks.

Brunei’s Islamic banking system is currently served primarily by two groups: the Bank

Islam Brunei Darussalam (BIBD) and Tabung Amanah Islam Brunei (TIAB). Over the years,

these two institutions have gone through a number of structural changes. On 23 September

1991, the first Islamic financial institution in Brunei Darussalam, TAIB, was established.

TAIB is not a commercial bank but an Islamic trust fund. It offers services to the public in

mainly savings and financial accounts. All of TAIB's savings accounts are based on the

Islamic contract of guaranteed safe custody (al-wadi'ah yad dhamanah- AWYD). The

financial accounts are mainly based on the principles of deferred payment sales (bai'

bithaman 'ajil- BBA) and hire-purchase contracts (al-ijarah thumma al-bai' -AITAB). These

contracts are extended for the purchase of cars, land, building and house renovations,

computers, for personal loans, for education and other purposes. In addition, TAIB offers

corporate financing, such as trade financing, and asset-based financing, among others.

TAIB also distributes its own term deposit certificates, which were introduced to create

awareness of financial planning and to promote saving habits among the public (Tabung

Amanah Islam Brunei, 2008).

Since its establishment, TAIB has acquired two subsidiary companies, for both of which it

owns 100% of shares. These companies include Insurance Islam TAIB Sdn. Bhd. (Islamic

insurance), which provides insurance coverage in conformity with Shari'ah principles, and

Darussalam Holdings Sdn. Bhd., which manages buildings and hotels in Mecca and

Medina, acts as a travel-ticketing agent, and also manages the Brunei pilgrimage in the

Holy Cities. This latter function includes ensuring pilgrims’ welfare and safety during

Mecca’s Hajj and Umrah (Tabung Amanah Islam Brunei, 2008).

On 13 January 1993, two years after establishing TAIB’s trust fund, the Islamic Bank of

Brunei Bhd. (IBB) was established. The bank was to assist the locals in using Islamic

banking facilities and in depositing their funds in a fully owned government bank. The IBB

provides a complete range of commercial banking facilities, from the basic savings account

to more sophisticated trade financing facilities. Besides being a commercial bank, the IBB

has invested in other related financial activities through its subsidiaries, each of which

specializes in a separate distinct activity (Bashir & Mail, 2011; Latiff, 2007).

On 15 July 2000, officially decreed that the Development Bank of Brunei be converted to

the Islamic Development Bank of Brunei Bhd. (IDBB) (Islamic Bank of Brunei Bhd, 2000).

In March 1995, the IDBB was initially established as a conventional bank known as the

Development Bank of Brunei (DBB). On 4 April 2000, the Government of Brunei instructed

the bank to operate on Islamic banking principles. This conversion required changes in its

transactions processing and accounting systems. Training in Islamic banking concepts was

also arranged for all management and staff. On 1 July 2000, successful conversion of the

IDBB as Brunei’s second Islamic bank was completed (Latiff, 2007).

In February 2001, a year after the conversion, the IDBB opened Takaful IDBB Sdn Bhd., its

first subsidiary company. This company is wholly owned by the bank and acts as an

insurance company that provides a wide range of Islamic insurance products that cover

property, business and life, and conform to Shari’ah principles, About three years after the

conversion, the IDBB introduced many new Islamic products such as Eze-Net Islamic

Internet Banking and Brunei’s first Islamic credit card (Bashir & Mail, 2011; Latiff, 2007).

On 7 July 2005, the Ministry of Finance announced that the state ruler had consented to

the proposed merger between the Islamic Bank of Brunei Bhd (IBB) and the Islamic

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 40

Development Bank of Brunei Bhd. (IDBB). On 10 September 2005, the Bank Islam Brunei

Darussalam Bhd. (BIBD) was incorporated. On 1 May 2006, a vesting order was obtained

from the High Court of Brunei Darussalam, and on 3 July 2006, the BIBD became a fully

operational Islamic Bank (Bank Islam Brunei Darussalam, 2007). The BIBD’s core values

are to ensure that its personnel maintain high ethical standards in carrying out their

responsibilities and that it adopts the standards of Shari’ah or Islamic law, in accordance

with best industry practices, in offering its products and services to its customers. As a

market-driven Islamic financial institution that constantly strives to address the needs of

its customers in a highly competitive environment, the BIBD also aims to maximize

shareholder returns through customer retention and customer acquisition. The BIBD is a

meritocratic organization that demands professionalism and teamwork. In line with its

mission, the BIBD harnesses its knowledge and resources for the benefit of its customers. It

has two subsidiaries: Takaful BIBD Sdn. Bhd., which primarily provides insurance

coverage, and BIBD At-Tamwil Bhd., a finance company that provides hire or purchase

financing for vehicles and consumer products (Bank Islam Brunei Darussalam, 2007;

Bashir & Mail, 2011).

2. LITERATURE REVIEW

Customer satisfaction is a well-known, established concept in such areas as marketing,

consumer research, economic psychology, and welfare and general economics. The most

common interpretations obtained from various authors note that satisfaction is a feeling

that results from a process of evaluating what has been received against what was

expected, including the purchase decision itself and the needs and wants associated with

the purchase (Armstrong & Kotler, 1996; Oliver, 1997). Bitner & Zeithaml (2003) stated that

satisfaction is the customers’ evaluation of a product or service in terms of whether that

product or service has met their needs and expectations. Kessler (1999) noted that

increasing satisfaction requires an understanding of what satisfaction is and how it is to be

handled. This signifies that in order to increase satisfaction, we should understand its

antecedent variables.

Several studies have emphasized the significance of customer awareness in Islamic banking

(Göksu & Becic, 2012; Hamid, Yaakub, Mujani, Sharizam & Jusoff, 2011; Doraisamy,

Shanmugam & Raman, 2011; Khattak & Rehman, 2010; Rashid & Hassan, 2009; Khan,

Hassan & Shahid, 2007; Rammal & Zurbruegg, 2007; Saduman, 2005; Naser, Jamal & Al-

Khatib, 1999; Metwa & Almossawi, 1998). Nevertheless, there has been little effort to

investigate Islamic banks in Brunei with special reference to the factors that might lead to

customer satisfaction.

The key factors that influence customers’ bank selection include the range of services, the

rates, and the fees and prices charged (Abratt & Russell, 1999). It is apparent that, to

satisfy customers, superior service, alone, is not sufficient. Prices are essential, if not more

important than service; relationship quality is also important. Furthermore, service

excellence, meeting client needs, and providing innovative products are essential to success

in the banking industry. Most private banks claim that creating and maintaining customer

relationships is important to them and that they are aware of the positive value

relationships provide (Colgate, Stewart & Kinsella, 1996). Customers in Islamic banks

seriously consider whether the bank complies with Shari’ah principles in all its banking

activities (Ahmad & Haron, 2002; Metawa & Almossawi, 1998). Some researchers have

placed emphasis on customer satisfaction in the Islamic banks and stated that Islamic

banking is no longer a business entity serving the religious obligations of the Muslim

community. Rather, customers of Islamic banks include a wide array of people across

various cultures and religions (Wilson, 1995).

It is suggested that, in order to gain a competitive position in the market, banks should

concentrate on service quality and customer satisfaction (Caruana, 2002). Similarly, it is

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 41

suggested that an organization in the banking sector’s service performance appraisal

system should be improved in line with customer satisfaction (Kayis, Kim & Shin, 2003).

Also noteworthy is the finding that there is a direct positive relationship between perceived

quality and level of satisfaction (Iglesias & Guille’n, 2004).

Customer perception on both service quality and product quality is important because it is

linked to awareness. All organizations must clearly understand differing customer

perception of service quality and product quality because this perception influences

consumer awareness. Othman & Owen (2001) confirmed that there is a strong link between

service quality and customer satisfaction. As a result, Islamic banks must pay close

attention to this factor and begin to think strategically in order to satisfy their customers by

providing high quality products and services. In their study of Malaysian banking

consumers. Hamid and Nordin (2001) found a high level of awareness of Islamic banking

but a poor knowledge of specific Islamic banking products, including a poor understanding

of the difference between Islamic and conventional banks. They also believed that better

consumer education assists in making people more aware of Islamic banking products.

Othman & Owen (2001) examined the performance of the Islamic banking industry in

Kuwait. They found a strong link between service quality and customer satisfaction. Naser

et al. (1999) found that customer satisfaction is often related to factors such as service

quality and service features. Attention has been given to the importance of awareness and

usage in shaping customer behaviour. Metawa and Almossawi (1998) measured customer

awareness and usage of various Islamic bank products and services in Bahrain.

Dusuki and Abdullah (2007) found that the selection of Islamic banks in Malaysia is based

on a combination of Islamic and financial reputation and the quality of services offered by

each bank. Studies by Erol and El-Bdour (1989) discovered that the most important criteria

considered by consumers in bank selection are fast and efficient services, a bank’s

reputation and image, and confidentially. Naser et al. (1999) support these findings. They

conducted research on Jordanian consumers’ satisfaction in regards to a bank’s name,

image, confidentiality policy and reputation. Fast and efficient service is always regarded as

high quality among bank consumers who value time and who expect a transaction to be

completed quickly. The context of quality services is reflected in the friendliness of

personnel, the dress code, communication techniques and relationships with consumer

(Haron, Ahmed & Planisek, 1994). Consumers’ preferences often depend on the quality of

services offered. In the context of services, consumers’ satisfaction as an antecedent of

service quality (Bitner, 2001; Cronin & Taylor, 1992). The success of any product and

service highly depends on customer acceptance and satisfaction. High quality service helps

generate customer satisfaction, customer loyalty and growth of market share by soliciting

new customers. It also improves productivity and financial performance (Bashir, Machali &

Mwinyi, 2012; Hassan, Chachi & Latiff, 2008; Hassain & Leo, 2009).

3. RESEARCH METHODS

3.1 Data Collection

The data for the present paper were gathered in Bandar Seri Begawan, the capital of Brunei

Darussalam. The customers of two Islamic banks, namely Bank Islam Brunei Darussalam

(BIBD) and Tabung Amanah Islam Brunei (TAIB) were the target population. Respondents

were chosen by convenience sample, wherein these two Islamic banks’ customers were

selected based on ease of access and availability, meaning that those two Islamic banks’

customers who visited the sampling locations during the chosen time intervals of the

survey. A total of 136 questionnaires were distributed, of which 116 responses were

received, yielding a response rate of 85%. The questionnaire gathered information on

consumers’ awareness and satisfaction of Islamic banks in Brunei Darussalam. Likert-

format items were presented with 5-point scales, where 1= ‘strongly disagree’, 2= ‘disagree’,

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 42

3= ‘neither disagree nor agree’, 4= ‘agree’, and 5= ‘strongly agree’. Customer satisfaction,

awareness and quality of service were measured using a five-item criterion for each

question. The overall mean of perceived satisfaction, awareness, service quality and product

quality were 3.952, 3.376, 3.386, and 3.384 respectively. Individually, each of the five items

had mean scores that were above the neutral pivot on the rating scale. The data set was

analysed using the Statistical Package for Social Science (SPSS) Version 19.0.

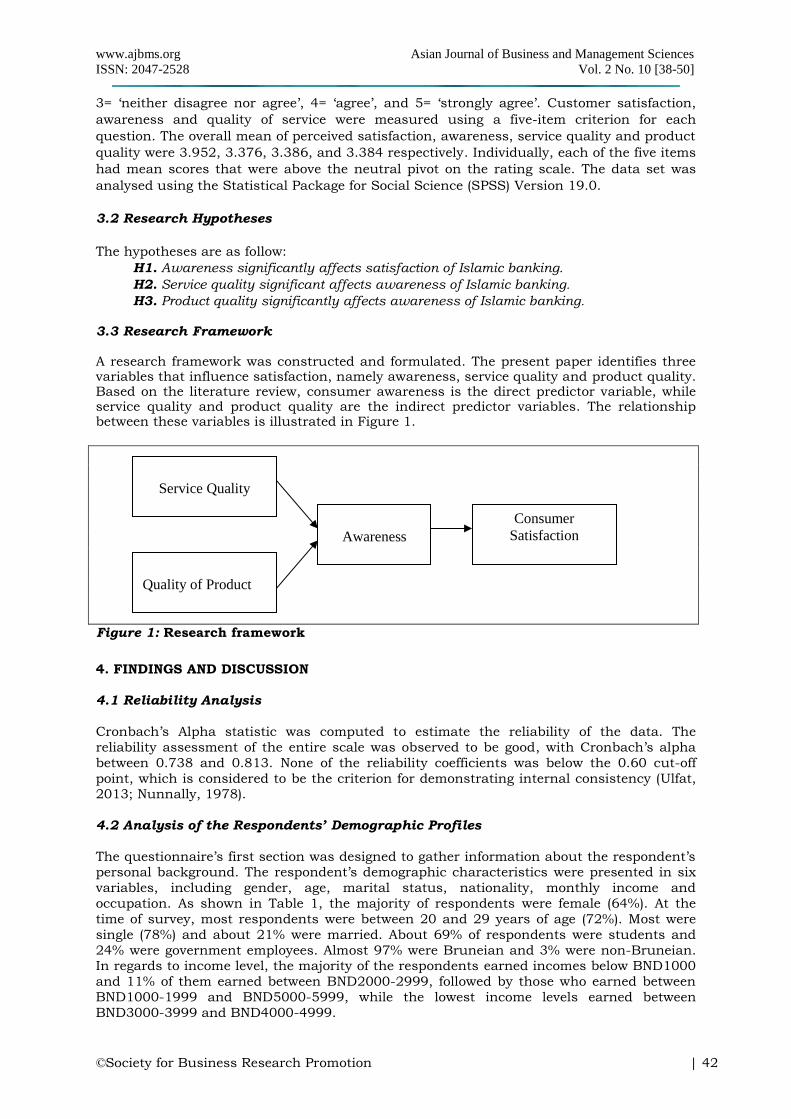

3.2 Research Hypotheses

The hypotheses are as follow:

H1. Awareness significantly affects satisfaction of Islamic banking.

H2. Service quality significant affects awareness of Islamic banking.

H3. Product quality significantly affects awareness of Islamic banking. 3.3 Research Framework A research framework was constructed and formulated. The present paper identifies three variables that influence satisfaction, namely awareness, service quality and product quality. Based on the literature review, consumer awareness is the direct predictor variable, while service quality and product quality are the indirect predictor variables. The relationship between these variables is illustrated in Figure 1.

Figure 1: Research framework

4. FINDINGS AND DISCUSSION

4.1 Reliability Analysis

Cronbach’s Alpha statistic was computed to estimate the reliability of the data. The

reliability assessment of the entire scale was observed to be good, with Cronbach’s alpha

between 0.738 and 0.813. None of the reliability coefficients was below the 0.60 cut-off

point, which is considered to be the criterion for demonstrating internal consistency (Ulfat, 2013; Nunnally, 1978).

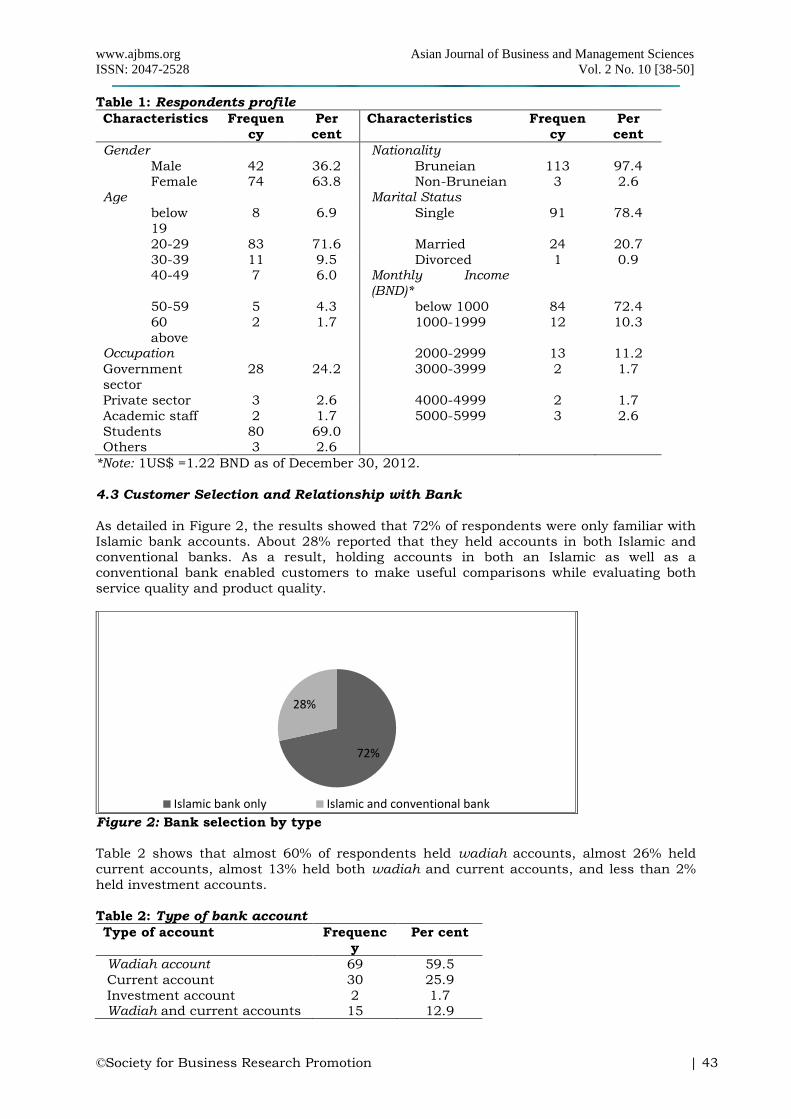

4.2 Analysis of the Respondents’ Demographic Profiles

The questionnaire’s first section was designed to gather information about the respondent’s personal background. The respondent’s demographic characteristics were presented in six

variables, including gender, age, marital status, nationality, monthly income and

occupation. As shown in Table 1, the majority of respondents were female (64%). At the

time of survey, most respondents were between 20 and 29 years of age (72%). Most were

single (78%) and about 21% were married. About 69% of respondents were students and

24% were government employees. Almost 97% were Bruneian and 3% were non-Bruneian. In regards to income level, the majority of the respondents earned incomes below BND1000

and 11% of them earned between BND2000-2999, followed by those who earned between

BND1000-1999 and BND5000-5999, while the lowest income levels earned between

BND3000-3999 and BND4000-4999.

Service Quality

Quality of Product

Awareness

Consumer

Satisfaction

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 43

Table 1: Respondents profile

Characteristics Frequen

cy

Per

cent

Characteristics Frequen

cy

Per

cent

Gender Nationality

Male 42 36.2 Bruneian 113 97.4 Female 74 63.8 Non-Bruneian 3 2.6

Age Marital Status

below

19

8 6.9 Single 91 78.4

20-29 83 71.6 Married 24 20.7

30-39 11 9.5 Divorced 1 0.9 40-49 7 6.0 Monthly Income

(BND)*

50-59 5 4.3 below 1000 84 72.4

60

above

2 1.7 1000-1999 12 10.3

Occupation 2000-2999 13 11.2

Government

sector

28 24.2 3000-3999 2 1.7

Private sector 3 2.6 4000-4999 2 1.7

Academic staff 2 1.7 5000-5999 3 2.6

Students 80 69.0 Others 3 2.6

*Note: 1US$ =1.22 BND as of December 30, 2012.

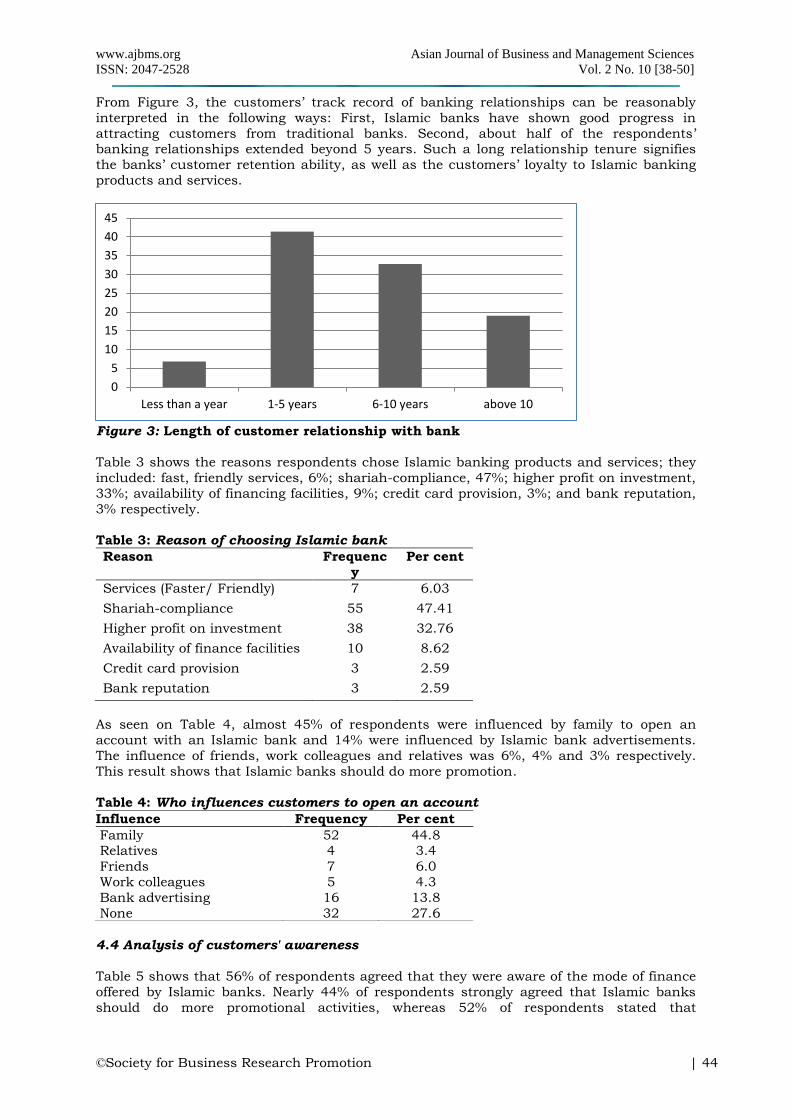

4.3 Customer Selection and Relationship with Bank

As detailed in Figure 2, the results showed that 72% of respondents were only familiar with

Islamic bank accounts. About 28% reported that they held accounts in both Islamic and conventional banks. As a result, holding accounts in both an Islamic as well as a

conventional bank enabled customers to make useful comparisons while evaluating both

service quality and product quality.

Figure 2: Bank selection by type

Table 2 shows that almost 60% of respondents held wadiah accounts, almost 26% held

current accounts, almost 13% held both wadiah and current accounts, and less than 2%

held investment accounts.

Table 2: Type of bank account

Type of account Frequenc

y

Per cent

Wadiah account 69 59.5

Current account 30 25.9

Investment account 2 1.7 Wadiah and current accounts 15 12.9

72%

28%

Islamic bank only Islamic and conventional bank

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 44

From Figure 3, the customers’ track record of banking relationships can be reasonably

interpreted in the following ways: First, Islamic banks have shown good progress in

attracting customers from traditional banks. Second, about half of the respondents’ banking relationships extended beyond 5 years. Such a long relationship tenure signifies

the banks’ customer retention ability, as well as the customers’ loyalty to Islamic banking

products and services.

Figure 3: Length of customer relationship with bank

Table 3 shows the reasons respondents chose Islamic banking products and services; they

included: fast, friendly services, 6%; shariah-compliance, 47%; higher profit on investment,

33%; availability of financing facilities, 9%; credit card provision, 3%; and bank reputation,

3% respectively.

Table 3: Reason of choosing Islamic bank

Reason Frequenc

y

Per cent

Services (Faster/ Friendly) 7 6.03

Shariah-compliance 55 47.41

Higher profit on investment 38 32.76

Availability of finance facilities 10 8.62

Credit card provision 3 2.59

Bank reputation 3 2.59

As seen on Table 4, almost 45% of respondents were influenced by family to open an

account with an Islamic bank and 14% were influenced by Islamic bank advertisements.

The influence of friends, work colleagues and relatives was 6%, 4% and 3% respectively.

This result shows that Islamic banks should do more promotion.

Table 4: Who influences customers to open an account

4.4 Analysis of customers' awareness

Table 5 shows that 56% of respondents agreed that they were aware of the mode of finance

offered by Islamic banks. Nearly 44% of respondents strongly agreed that Islamic banks

should do more promotional activities, whereas 52% of respondents stated that

0

5

10

15

20

25

30

35

40

45

Less than a year 1-5 years 6-10 years above 10

Influence Frequency Per cent

Family 52 44.8 Relatives 4 3.4

Friends 7 6.0

Work colleagues 5 4.3

Bank advertising 16 13.8

None 32 27.6

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 45

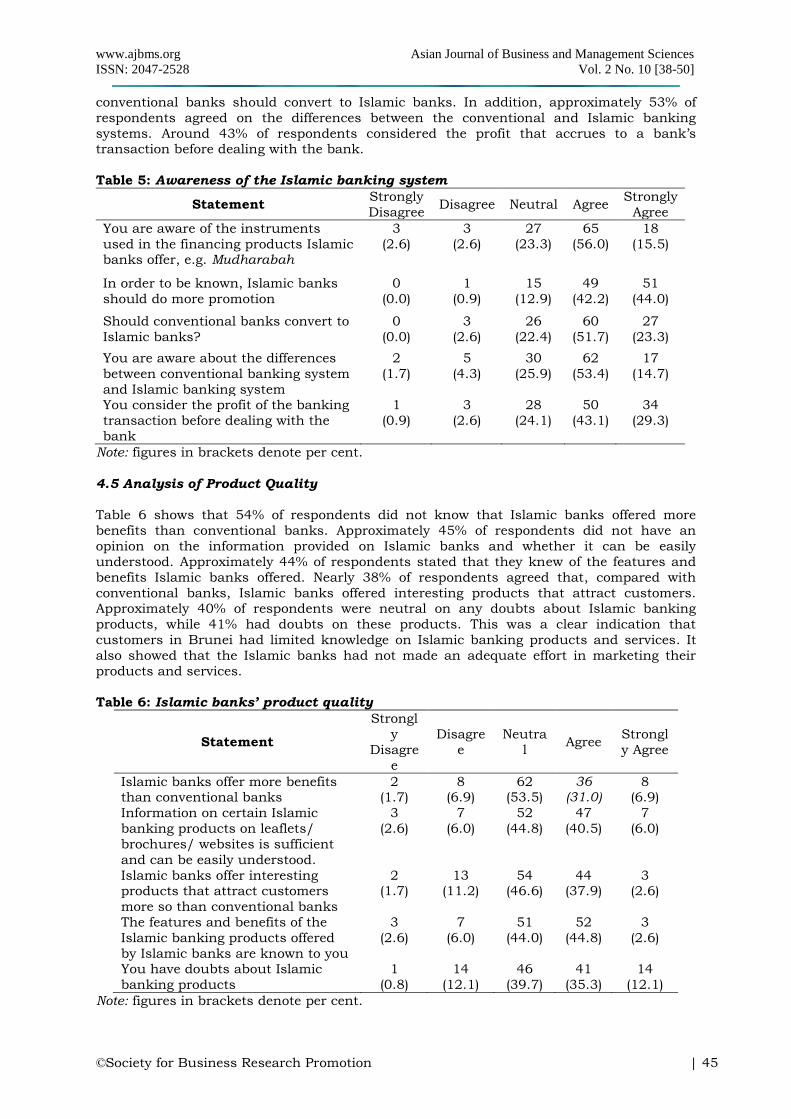

conventional banks should convert to Islamic banks. In addition, approximately 53% of

respondents agreed on the differences between the conventional and Islamic banking

systems. Around 43% of respondents considered the profit that accrues to a bank’s transaction before dealing with the bank.

Table 5: Awareness of the Islamic banking system

Statement Strongly

Disagree Disagree Neutral Agree

Strongly

Agree

You are aware of the instruments

used in the financing products Islamic banks offer, e.g. Mudharabah

3

(2.6)

3

(2.6)

27

(23.3)

65

(56.0)

18

(15.5)

In order to be known, Islamic banks

should do more promotion

0

(0.0)

1

(0.9)

15

(12.9)

49

(42.2)

51

(44.0)

Should conventional banks convert to

Islamic banks?

0

(0.0)

3

(2.6)

26

(22.4)

60

(51.7)

27

(23.3)

You are aware about the differences

between conventional banking system

and Islamic banking system

2

(1.7)

5

(4.3)

30

(25.9)

62

(53.4)

17

(14.7)

You consider the profit of the banking

transaction before dealing with the

bank

1

(0.9)

3

(2.6)

28

(24.1)

50

(43.1)

34

(29.3)

Note: figures in brackets denote per cent.

4.5 Analysis of Product Quality

Table 6 shows that 54% of respondents did not know that Islamic banks offered more

benefits than conventional banks. Approximately 45% of respondents did not have an

opinion on the information provided on Islamic banks and whether it can be easily

understood. Approximately 44% of respondents stated that they knew of the features and

benefits Islamic banks offered. Nearly 38% of respondents agreed that, compared with

conventional banks, Islamic banks offered interesting products that attract customers. Approximately 40% of respondents were neutral on any doubts about Islamic banking

products, while 41% had doubts on these products. This was a clear indication that

customers in Brunei had limited knowledge on Islamic banking products and services. It

also showed that the Islamic banks had not made an adequate effort in marketing their

products and services.

Table 6: Islamic banks’ product quality

Statement

Strongl

y

Disagre

e

Disagre

e

Neutra

l Agree

Strongl

y Agree

Islamic banks offer more benefits than conventional banks

2 (1.7)

8 (6.9)

62 (53.5)

36 (31.0)

8 (6.9)

Information on certain Islamic

banking products on leaflets/

brochures/ websites is sufficient

and can be easily understood.

3

(2.6)

7

(6.0)

52

(44.8)

47

(40.5)

7

(6.0)

Islamic banks offer interesting products that attract customers

more so than conventional banks

2 (1.7)

13 (11.2)

54 (46.6)

44 (37.9)

3 (2.6)

The features and benefits of the

Islamic banking products offered

by Islamic banks are known to you

3

(2.6)

7

(6.0)

51

(44.0)

52

(44.8)

3

(2.6)

You have doubts about Islamic

banking products

1

(0.8)

14

(12.1)

46

(39.7)

41

(35.3)

14

(12.1)

Note: figures in brackets denote per cent.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 46

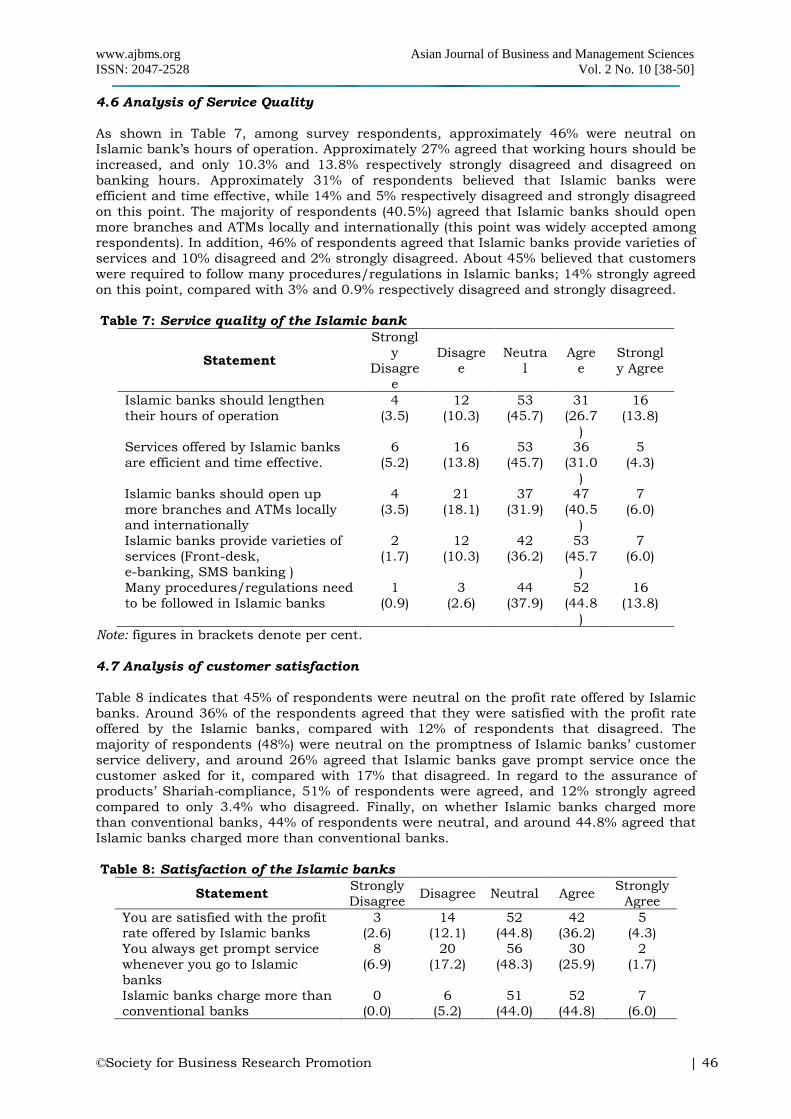

4.6 Analysis of Service Quality

As shown in Table 7, among survey respondents, approximately 46% were neutral on Islamic bank’s hours of operation. Approximately 27% agreed that working hours should be

increased, and only 10.3% and 13.8% respectively strongly disagreed and disagreed on

banking hours. Approximately 31% of respondents believed that Islamic banks were

efficient and time effective, while 14% and 5% respectively disagreed and strongly disagreed

on this point. The majority of respondents (40.5%) agreed that Islamic banks should open

more branches and ATMs locally and internationally (this point was widely accepted among respondents). In addition, 46% of respondents agreed that Islamic banks provide varieties of

services and 10% disagreed and 2% strongly disagreed. About 45% believed that customers

were required to follow many procedures/regulations in Islamic banks; 14% strongly agreed

on this point, compared with 3% and 0.9% respectively disagreed and strongly disagreed.

Table 7: Service quality of the Islamic bank

Statement

Strongl

y

Disagre

e

Disagre

e

Neutra

l

Agre

e

Strongl

y Agree

Islamic banks should lengthen

their hours of operation

4

(3.5)

12

(10.3)

53

(45.7)

31

(26.7

)

16

(13.8)

Services offered by Islamic banks

are efficient and time effective.

6

(5.2)

16

(13.8)

53

(45.7)

36

(31.0

)

5

(4.3)

Islamic banks should open up

more branches and ATMs locally and internationally

4

(3.5)

21

(18.1)

37

(31.9)

47

(40.5)

7

(6.0)

Islamic banks provide varieties of

services (Front-desk,

e-banking, SMS banking )

2

(1.7)

12

(10.3)

42

(36.2)

53

(45.7

)

7

(6.0)

Many procedures/regulations need

to be followed in Islamic banks

1

(0.9)

3

(2.6)

44

(37.9)

52

(44.8)

16

(13.8)

Note: figures in brackets denote per cent.

4.7 Analysis of customer satisfaction

Table 8 indicates that 45% of respondents were neutral on the profit rate offered by Islamic

banks. Around 36% of the respondents agreed that they were satisfied with the profit rate offered by the Islamic banks, compared with 12% of respondents that disagreed. The

majority of respondents (48%) were neutral on the promptness of Islamic banks’ customer

service delivery, and around 26% agreed that Islamic banks gave prompt service once the

customer asked for it, compared with 17% that disagreed. In regard to the assurance of products’ Shariah-compliance, 51% of respondents were agreed, and 12% strongly agreed

compared to only 3.4% who disagreed. Finally, on whether Islamic banks charged more than conventional banks, 44% of respondents were neutral, and around 44.8% agreed that

Islamic banks charged more than conventional banks.

Table 8: Satisfaction of the Islamic banks

Statement Strongly

Disagree Disagree Neutral Agree

Strongly

Agree

You are satisfied with the profit rate offered by Islamic banks

3 (2.6)

14 (12.1)

52 (44.8)

42 (36.2)

5 (4.3)

You always get prompt service

whenever you go to Islamic

banks

8

(6.9)

20

(17.2)

56

(48.3)

30

(25.9)

2

(1.7)

Islamic banks charge more than conventional banks

0 (0.0)

6 (5.2)

51 (44.0)

52 (44.8)

7 (6.0)

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 47

Islamic banks provide

assurance on their products’

shariah-compliance

0

(0.0)

4

(3.4)

39

(33.6)

59

(50.9)

14

(12.1)

Terms and conditions set by the Islamic banks are acceptable

1 (0.9)

14 (12.1)

46 (39.7)

44 (37.9)

11 (9.4)

Note: figures in brackets denote per cent.

4.8 Hypothesis Testing

4.8.1 Test of Hypothesis 1

As shown in Table 9, it can be concluded that a p-value 0.000 (significant) means the

independent variable (awareness) can significantly affect customer satisfaction with Islamic banking. Since the p-value calculated is smaller than alpha 0.01, H1 is accepted at a 5%

level of significance. The samples provided sufficient evidence that there is a significant

relationship between awareness and satisfaction of Islamic banking.

Table 9: Regression Analysis

Variables B Std. Error T value P-value

(Constant) 7.982 1.832 4.357 0.000

Awareness 0.452 0.092 4.918 0.000

R2 =0.175 F=24.183

(Sig. 0.000) α=5%

4.8.2 Test of Hypothesis 2

The model’s second hypothesis requires a test of the expected positive and significant effects of service quality on awareness. Table 10 presents the test results. As shown in

Table 10, the impact of service quality on awareness is positive and significant (p-value =

0.035 < 0.05). Thus, the regression model’s results provide strong support for Hypothesis 2.

Table 10: Regression Analysis

Variables B

Std.

Error T value P-value

(Constant) 10.413 1.630 6.389 0.000

Product 0.382 0.101 3.795 0.000

Service 0.172 0.081 2.130 0.035

R2 =0.229 F=16.760

(Sig. 0.000) α=5%

4.8.3 Test of Hypothesis 3

In Hypothesis 3, it is expected that product has an effect on awareness. Table 10 presents

the results of the test of Hypothesis 3. Table 10 also reveals that the effect of product on

awareness is significant (p-value = 0.000 < 0.05), therefore H3 could not be rejected.

Furthermore, based on the results, it can be inferred that the effect of service quality and

product on satisfaction is not direct but rather an indirect effect through awareness.

5. CONCLUSIONS AND RECOMMENDATIONS

The purpose of the present study is to empirically examine the impact of service quality,

product quality, and awareness on customer satisfaction of Islamic banking in Brunei

Darussalam. A questionnaire survey was conducted among Islamic banks’ customers. Its intention was to measure the awareness and level of customer satisfaction with Islamic

banks’ various basic elements of service delivery systems. The study’s findings indicate that

the establishment of higher levels of awareness will lead to a higher level of customer

satisfaction. As a result, they indicate that awareness is positively associated with customer

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 48

satisfaction in Brunei’s Islamic banking. In addition, the findings of this paper are

consistent with previous studies that found a strong link between awareness and customer

satisfaction in Islamic banking. Furthermore, the results also show that the effect of service quality and product quality on awareness is positive and significant.

Islamic banking needs to promote an awareness of Islamic banking products and services

offered. These products and services need to compete with those of conventional banks.

Islamic banking has the potential to expand its market share and to convince consumers to

transfer their business to this sector by offering quality services and products, and by keeping in line with Shariah-compliance. Further research needs to be carried out in order

to identify other factors that influence consumers’ satisfaction of Islamic banking.

As the findings show, the majority of Islamic banking customers in Brunei have limited

knowledge of Islamic banking products and services. This is because Islamic banks have not done enough marketing. There is a need to educate customers on Islamic banking

products and services. Additionally, since customer satisfaction is an essential element of

the total package, Islamic banks could use a segment of satisfied customers in its promotional efforts to attract new ones (Hassan, Chachi & Latiff, 2008).

5.1 Limitations and Future Research

This paper points to several avenues for future research. The importance of service quality,

product quality and awareness of customer satisfaction has been identified. Awareness

alone cannot achieve the objective of creating customer satisfaction and awareness. Further

research should be considered to identify other variables that might influence these factors, such as information technology. Currently, banks intensively use technological

advancements and information systems.

In this paper, three limitations have been identified. First, the study only tested its model

and hypotheses in Islamic banks. Future research should test the same model using

different Islamic financial institutions. Second, both the sample size and the number of actual respondents were limited. Further research may be conducted on a wider sample.

This would provide more generalized conclusions for Islamic banks. Finally, in order to

reach a strong conclusion, a more robust analysis is needed. In order to greatly contribute

to the existing body of knowledge about customer satisfaction within the banking sector in

Brunei Darussalam, similar future research should be conducted on both the Islamic and the conventional banking sectors.

REFERENCES

Abratt, R., & Russell, J. (1999). Relationship marketing in private banking in South Africa. International Journal of Bank Marketing, 17(1), 5-19.

Ahmad, N. and Haron, S. (2002), Perceptions of Malaysian corporate customers towards Islamic banking products and services, International Journal of Islamic Financial Services, 3(4), 13-29.

Armstrong, G., & Kotler, P. (1996). Principles of marketing. (7th ed.). India: Prentice Hall.

Bank Islam Brunei Darussalam. (2007). Annual report. Brunei Darussalam: Author.

Bashir, M. S. (2012). Awareness, service quality and product effects on satisfaction of Islamic banking in Brunei Darussalam. Proceedings of the 2nd International

Conference on Management (2nd ICM 2012) 11th-12th June. Holiday Villa Beach Resort & Spa, Langkawi Kedah, Malaysia (pp. 544-556). Retrieved from

http://www.internationalconference.com.my/proceeding/2nd_icm2012_proceeding/

042_175_2ndICM2012_Proceeding_PG0544_0556.pdf

Bashir, M. S., & Mail, N. H. (2011). Consumer perceptions of Islamic insurance companies in Brunei Darussalam. International Journal of Emerging Sciences, 1(3), 285-306.

Bashir, M. S., Machali, M. M., & Mwinyi, A. M. (2012). The effect of service quality and

government role on customer satisfaction: Empirical evidence of microfinance in Kenya. International Journal of Business and Social Science, 3(14), 312-319.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 49

Bitner, M. J. (2001). Service and technology: Opportunities and paradoxes. Managing

Service Quality, 11(6), 375-379.

Bitner, M. J., & Zeithaml, V. A. (2003). Service marketing. (3rd ed.). New Delhi: Tata

McGraw Hill.

Caruana, A. (2002). Service loyalty: The effects of service quality and the mediating role of customer satisfaction. European Journal of Marketing, 36(7/8), 811-828.

Colgate, M., Stewart, K., & Kinsella, R. (1996). Customer defection: A study of the student market in Ireland. The International Journal of Bank Marketing, 14(3), 23-29.

Cronin, J. J., & Taylor, S. A. (1992). Measuring service quality: A re-examination and extension. Journal of Marketing, 56. 55-68.

Doraisamy, B., Shanmugam, A., & Raman, R. (2011). A study on consumers’ preferences of Islamic banking products and services in Sungai Petani. Academic Research International, 1(3), 290-302.

Dusuki, A. W., & Abdullah, N. I. (2007). Why do Malaysian customers patronize Islamic banks? International Journal of Bank Marketing, 25(3), 142-160.

Erol, C., & El-Bdour, R. (1989). Attitudes, behaviour, and patronage factors of bank customers towards Islamic banks. International Journal of Bank Marketing, 7(6), 31-

39.

Göksu, A., & Becic, A. (2012). Awareness of Islamic Banking in Bosnia and Herzegovina. International Research Journal of Finance and Economics, 7(100), 26-39.

Hamid, A., and Nordin, N. (2001). A study on Islamic banking education and strategy for the new millennium: Malaysian experience. International Journal of Islamic financial Services, 2(4), 3-11.

Hamid, M. A., Yaakub, N. I., Mujani, W. K., Sharizam, M., & Jusoff, K. (2011). Factors

adopting Islamic home financing: A case study among consumers of Islamic banks in Malaysia. Middle-East Journal of Scientific Research, 7. 47-58.

Haron, S., Ahmed, N., & Planisek, S. (1994). Bank patronage factors of Muslims and non-Muslim customers. International Journal of Bank Marketing, 12(1), 32-40.

Hassain, M., & Leo, S. (2009). Consumer perception on service quality in retail bank in Middle East: The case of Qatar. International Journal of Islamic and Middle Eastern Finance and Management, 2(4), 338-350.

Hassan, A., Chachi, A., & Latiff, S. A. (2008). Islamic marketing ethics and its impact on customer satisfaction in the Islamic banking industry. Journal of King Abdulaziz University: Islamic Economics, 21(1), 23-40.

Ho, G. T. S., Lau, H. C. W., Lee, C. K. M., and Ip, A. W. H. (2005). An intelligent forward quality enhancement system to achieve product customization. Industrial Management & Data Systems, 105(3), 384-406.

Iglesias, M. P., & Guille’n, M. J. Y. (2004). Perceived quality and price: Their impact on the satisfaction of restaurant customers. International Journal of Contemporary Hospitality Management, 16(6), 373-379.

Islamic Bank of Brunei Bhd. (2000). Annual report. Brunei Darussalam: Author.

Kayis, B., Kim, H., & Shin, T. H. (2003). A comparative analysis of cultural, conceptual and practical constraints on quality management implementations-findings from Australian and Korean banking industries. TQM and Business Excellence, 14(7),

765-777. Kessler, S. (1996). Measuring and managing customer satisfaction: Going for the gold.

Milwaukee, WI: ASQ Quality Press.

Khan, M. S. N., Hassan, M. K., & Shahid, A. I. (2007). Banking behaviour of Islamic bank customers in Bangladesh. Journal of Islamic Economics, Banking and Finance, 3(2),

159-194.

Khattak, N. A., and Rehman, K. (2010). Customer satisfaction and awareness of Islamic banking system in Pakistan. African Journal of Business Management, 4(5), 662-671.

Latiff, S. A. (2007). Islamic banking in Brunei and the future role of Centre for Islamic Banking, Finance and Management (CIBFM). In S. S. Ali & A. Ahmad (Eds.), An overview of Islamic banking and finance: Fundamentals and contemporary issues (pp.

277-300). Jeddah, Saudi Arabia: Islamic Research and Training Institute.

Metawa, S. A., & Almossawi, M. (1998). Banking behaviour of Islamic bank customers: Perspectives and implications. International Journal of Bank Marketing, 16(7), 299-

313.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 2 No. 10 [38-50]

©Society for Business Research Promotion | 50

Naser, K., Jamal, A., & Al-Khatib, K. (1999). Islamic banking: A study of customer satisfaction and preferences in Jordan. International Journal of Bank Marketing, 17(3), 135-150.

Nunally, J. C. (1978). Psychometric theory. (2nd ed.). Englewood Cliffs, NJ: McGraw Hill

Book Company. Oliver, R. (1997). Satisfaction: A behavioural perspective on the consumer. Boston: McGraw-

Hill.

Othman, A., & Owen, L. (2001). Adopting and measuring customer service quality in Islamic banks: A case study in Kuwait Finance House. International Journal of Islamic Financial Services, 3(1), 20-26.

Rammal, H. G., & Zurbruegg, R. (2007). Awareness of Islamic banking products among Muslims: The case of Australia. Journal of Financial Services Marketing, 12(1), 65-74.

Rashid, M., & Hassan, M. K. (2009). Customer demographics affecting bank selection

criteria, preference and market segmentation: Study on domestic Islamic banks in Bangladesh. International Journal of Business and Management, 4(6), 131-146.

Rose, P. S., & Marquis, M. H. (2006). Money and capital markets: Financial institutions and instruments in a global marketplace. (9th ed.). NY: McGraw-Hill Irwin.

Saduman, H. O. (2005). Interest free banking in Turkey: A study of customer satisfaction and bank selection criteria. Journal of Economic Cooperation, 26(4), 51-86.

Tabung Amanah Islam Brunei. (2008). Annual report of Tabung Amanah Islam Brunei.

Brunei Darussalam: Author.

Ulfat, S. (2013). Pairing of customer' satisfaction with brand consciousness and price sensitivity: A feminine study in Pakistan on beauty care products selection. Asian Journal of Business Management, 5(1), 144-152.

Wilson, R. (1995). Marketing strategy for Islamic financial product. New Horizon, 39. 7-9.

Related Documents