Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANALYSIS OF A STRATEGY TO FORECAST SCHOOL DISTRICT

FISCAL HEALTH IN TEXAS

by

WILLIAM H. MAURER, B.S. in Ed., M.Ed.

A DISSERTATION

IN

EDUCATION

Submitted to the Graduate Faculty of Texas Tech University in

Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF EDUCATION

Approved

Accepted

August, 1988

T3

©1989

WILLIAM H. MAURF.R

All Rights Reserved

ACKNOWLEDGMENTS

I wish to recognize and thank Dr. William Sparkman who

encouraged me to enter doctoral studies. Without his

guidance and support, I would not have been able to complete

this project. Appreciation is extended to members of the

dissertation committee. Dr. David Welton, Dr. John Champlin,

Dr. Thomas Irons and Dr. Paula Lawrence. Special thanks

also are extended to Penny Taulman, who typed this manu

script, and to Robert Leung, who offered his skills in

computer programming.

Special appreciation goes to my wife, Patricia

Alexander Maurer, and our daughter, Sarah Elizabeth Maurer,

for their faithful love, support, patience and under

standing. During the two years of research and writing,

they made many sacrifices that enabled me to complete my

studies.

11

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

LIST OF TABLES V

LIST OF FIGURES viii

CHAPTER

I INTRODUCTION 1

Statement of the Problem 1 Delimitations 3 Limitations 4

Justification for the Study 4 Assumptions 6 Definition of Terms 6 Procedures 8 Organization of the Research Report 10

II REVIEW OF RELEVANT RESEARCH AND LITERATURE 11

Planning the School Budget 11 Fiscal Strain 13 Forecasting Techniques 15 Studies of School District Fiscal Health ... 18 Identification of Variables 24 Summary 30

III PROCEDURES AND PRESENTATION OF THE DATA , 32

Source of the Data 32 Sorting the Data and Identifying the Variables 33 Statistical Procedures 36 Analysis of the Data 61

IV PRESENTATION AND ANALYSIS OF DATA 66

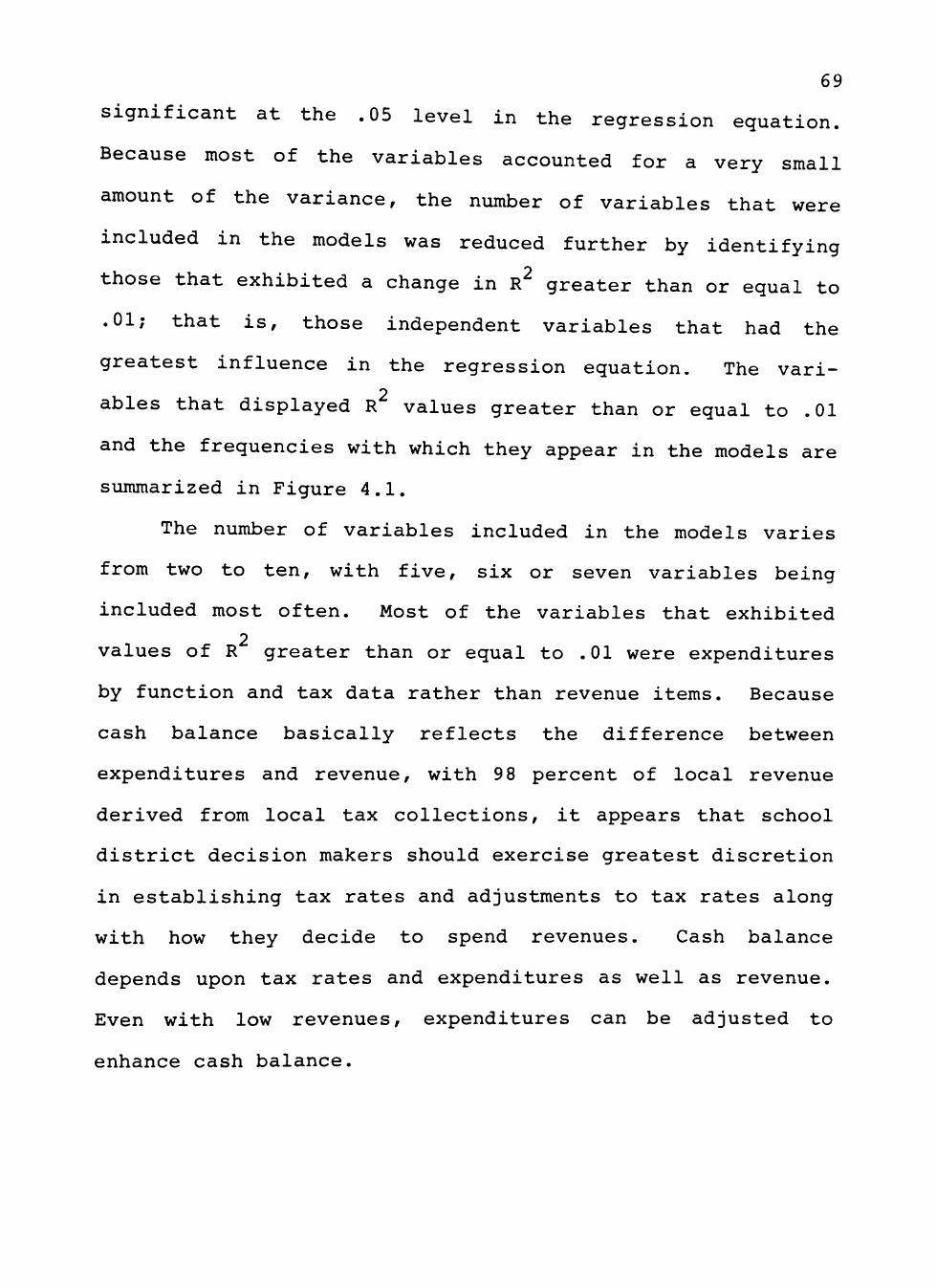

Discussion of Research Questions 67

111

V SUMMARY, MAJOR FINDINGS, CONCLUSIONS AND RECOMMENDATIONS 80

Summary 80 The Problem of the Study 81 Procedures 81

Major Findings 82 Conclusions 91 Recommendations 92

REFERENCES 94

APPENDICES

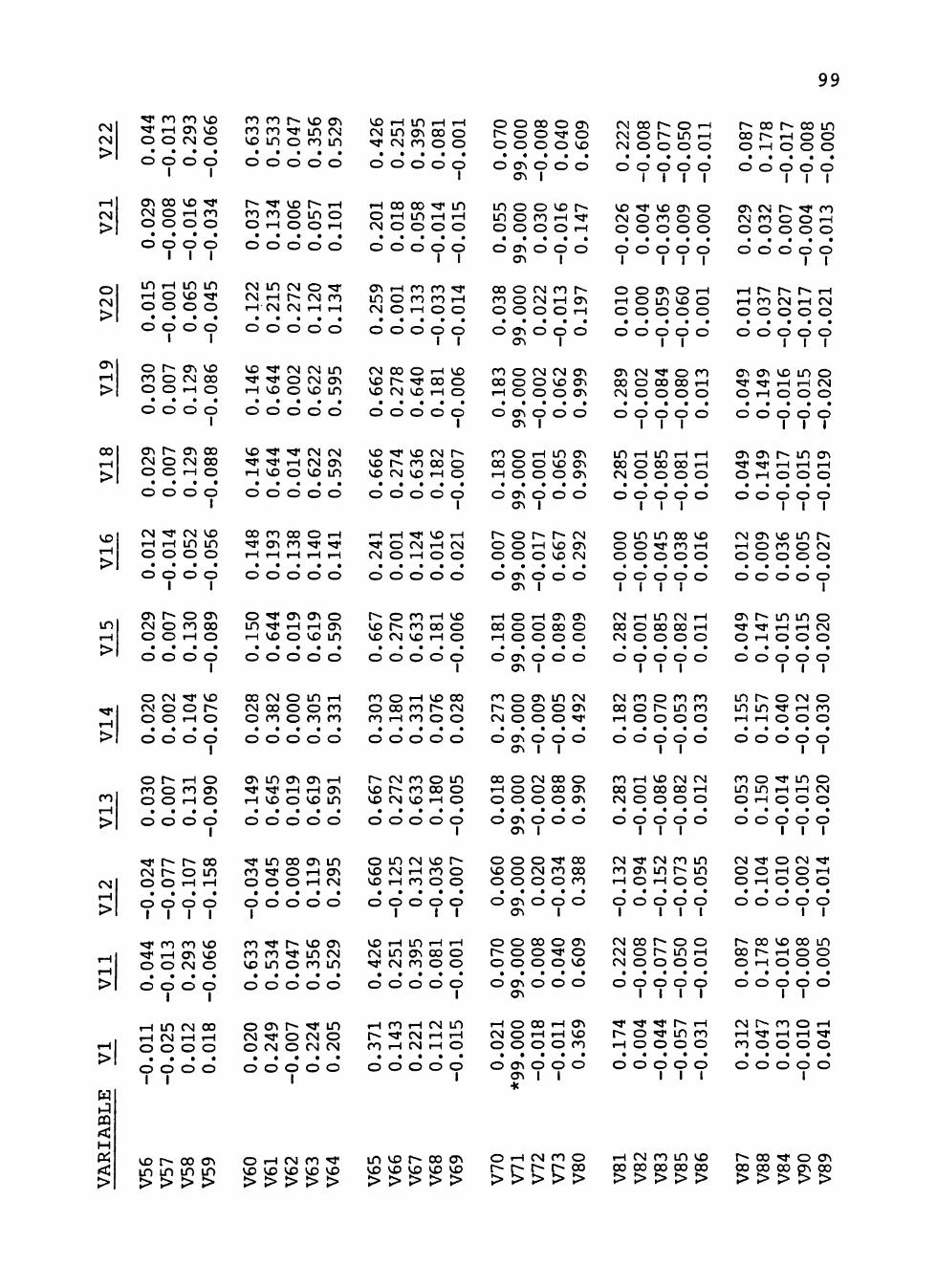

A TABLE A.l CORRELATION MATRIX 1980-1981 INDEPENDENT VARIABLES 1981-1982 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS 97

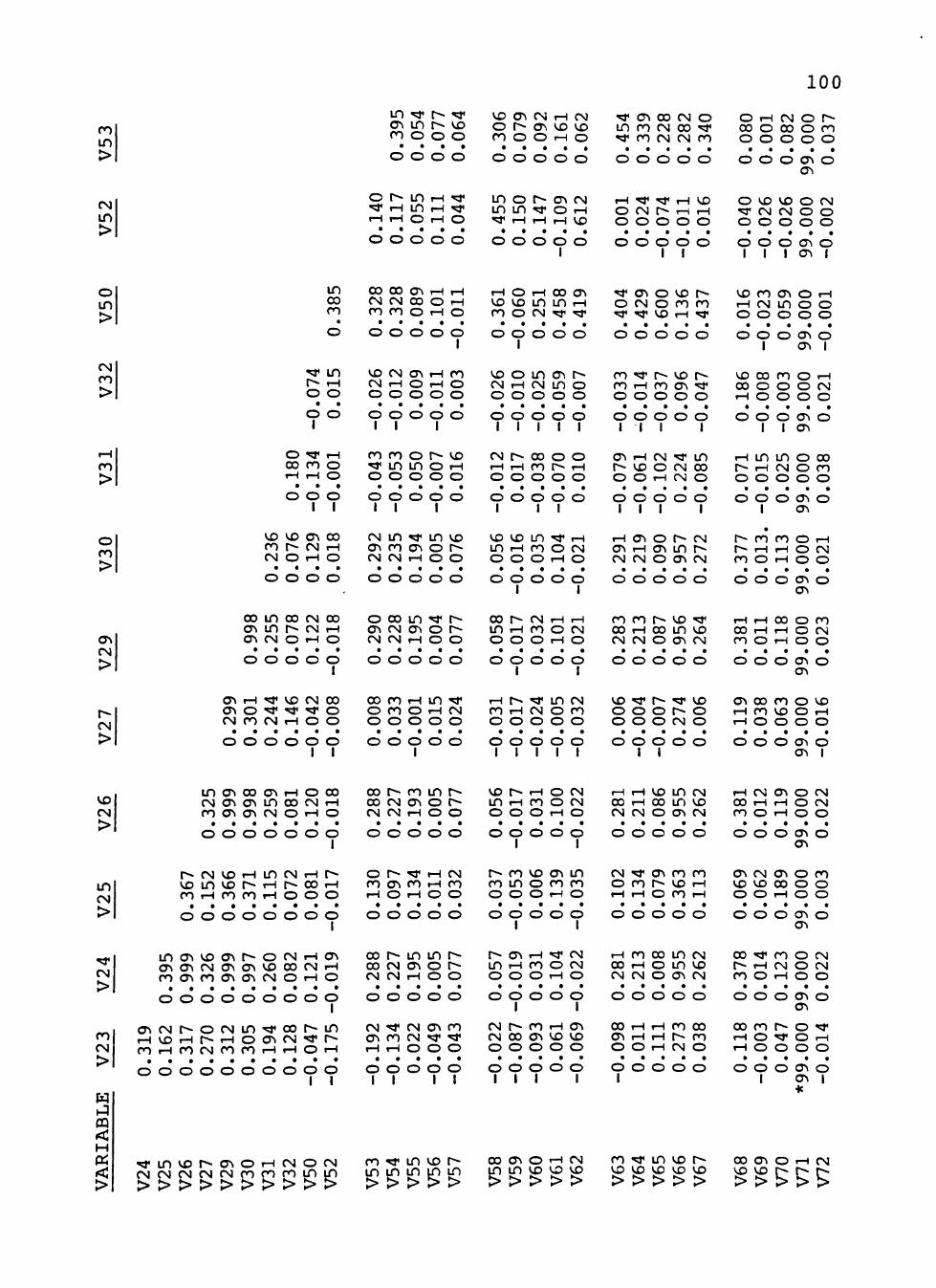

B TABLE B.l CORRELATION MATRIX 1981-1982 INDEPENDENT VARIABLES 1982-1983 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS 104

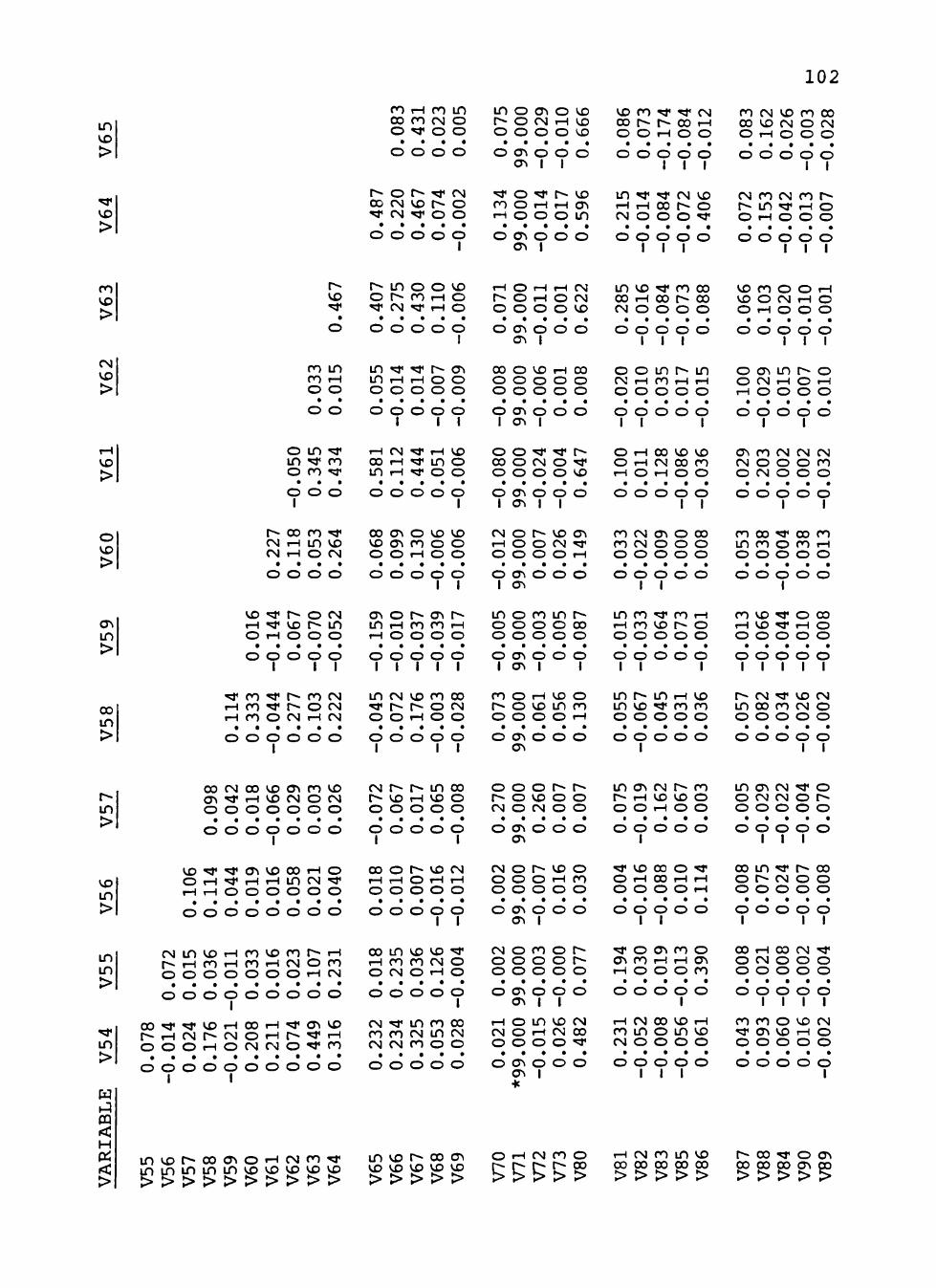

C TABLE C.l CORRELATION MATRIX 1982-1983 INDEPENDENT VARIABLES 1983-1984 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS H I

IV

LIST OF TABLES

2.1 VARIABLES 26

3.1 NUMBER OF SCHOOL DISTRICTS INCLUDED IN THE STUDY 34

3.2 MEAN AND STANDARD DEVIATION, 1980-1981 INDEPENDENT VARIABLES, 1981-1982, DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS, N=979 37

3.3 MEAN AND STANDARD DEVIATION, 1981-1982 INDEPEDENT VARIABLES, 1982-1983 DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS, N=979 39

3.4 MEAN AND STANDARD DEVIATION, 1982-1983 INDEPENDENT VARIABLES, 1983-1984 DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS, N=978 41

3.5 MULTIPLE REGRESSION SUMMARY TABLE 1980-1981 INDEPENDENT VARIABLE 1981-1982 DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS 45

3.6 MULTIPLE REGRESSION SUMMARY TABLE 1980-1981 INDEPENDENT VARIABLE 1981-1982 DEPENDENT VARIABLE, FIRST QUARTILE 46

3.7 MULTIPLE REGRESSION SUMMARY TABLE 1980-1981 INDEPENDENT VARIABLE 1981-1982 DEPENDENT VARIABLE, SECOND QUARTILE 47

3.8 MULTIPLE REGRESSION SUMMARY TABLE 1980-1981 INDEPENDENT VARIABLE 1981-1982 DEPENDENT VARIABLE, THIRD QUARTILE 48

3.9 MULTIPLE REGRESSION SUMMARY TABLE 1980-1981 INDEPENDENT VARIABLE 1981-1982 DEPENDENT VARIABLE, FOURTH QUARTILE 49

3.10 MULTIPLE REGRESSION SUMMARY TABLE 1981-1982 INDEPENDENT VARIABLE 1982-1983 DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS 50

V

3.11 MULTIPLE REGRESSION SUMMARY TABLE 1981-1982 INDEPENDENT VARIABLE 1982-1983 DEPENDENT VARIABLE, FIRST QUARTILE 51

3.12 MULTIPLE REGRESSION SUMMARY TABLE 1981-1982 INDEPENDENT VARIABLE 1982-1983 DEPENDENT VARIABLE, SECOND QUARTILE 52

3.13 MULTIPLE REGRESSION SUMMARY TABLE 1981-1982 INDEPENDENT VARIABLE 1982-1983 DEPENDENT VARIABLE, THIRD QUARTILE 53

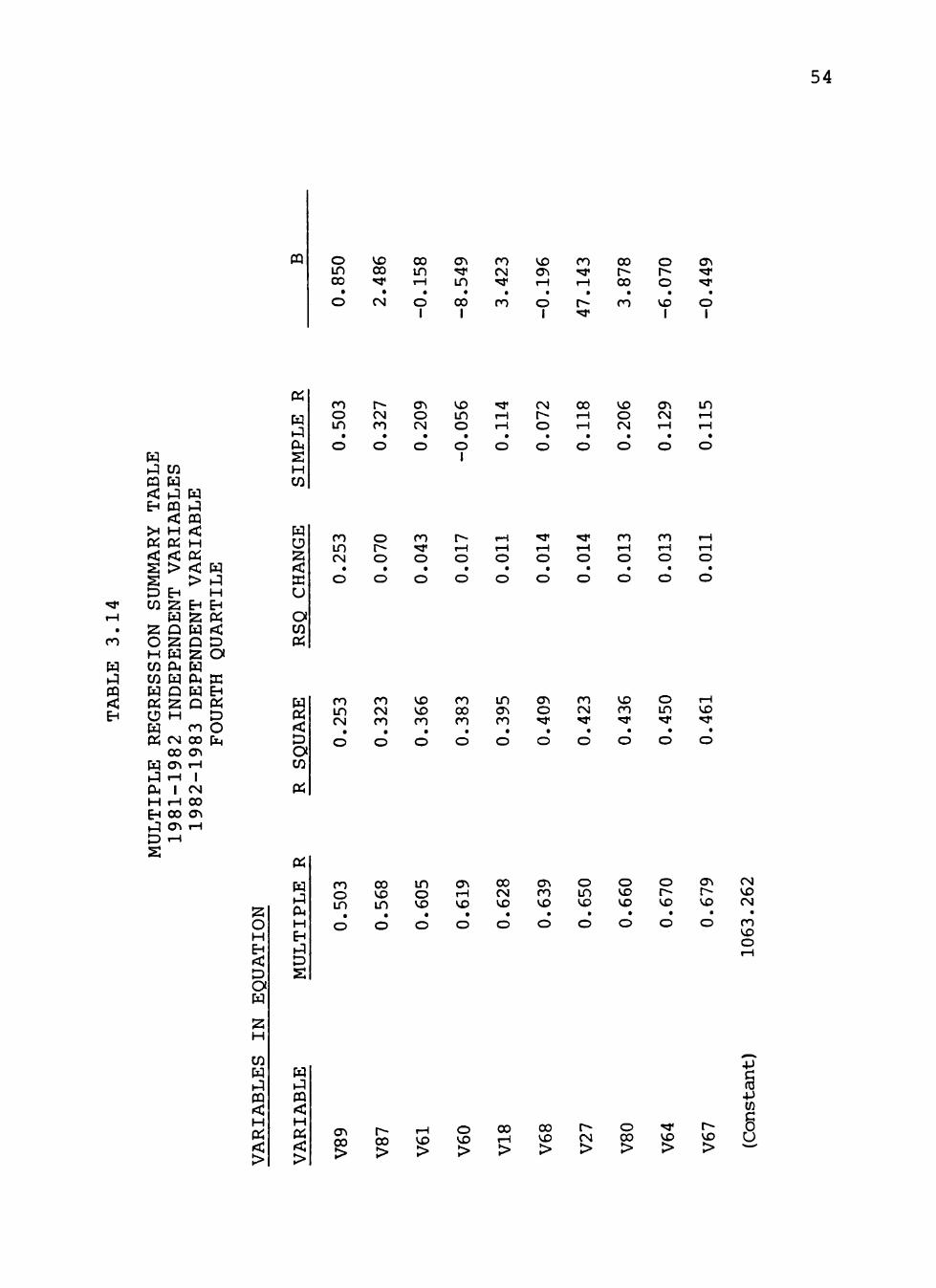

3.14 MULTIPLE REGRESSION SUMMARY TABLE 1981-1982 INDEPENDENT VARIABLE 1982-1983 DEPENDENT VARIABLE, FOURTH QUARTILE 54

3.15 MULTIPLE REGRESSION SUMMARY TABLE 1982-1983 INDEPENDENT VARIABLE 1983-1984 DEPENDENT VARIABLE, ALL SCHOOL DISTRICTS 55

3.16 MULTIPLE REGRESSION SUMMARY TABLE 1982-1983 INDEPENDENT VARIABLE 1983-1984 DEPENDENT VARIABLE, FIRST QUARTILE 56

3.17 MULTIPLE REGRESSION SUMMARY TABLE 1982-1983 INDEPENDENT VARIABLE 1983-1984 DEPENDENT VARIABLE, SECOND QUARTILE 57

3.18 MULTIPLE REGRESSION SUMMARY TABLE 1982-1983 INDEPENDENT VARIABLE 1983-1984 DEPENDENT VARIABLE, THIRD QUARTILE 58

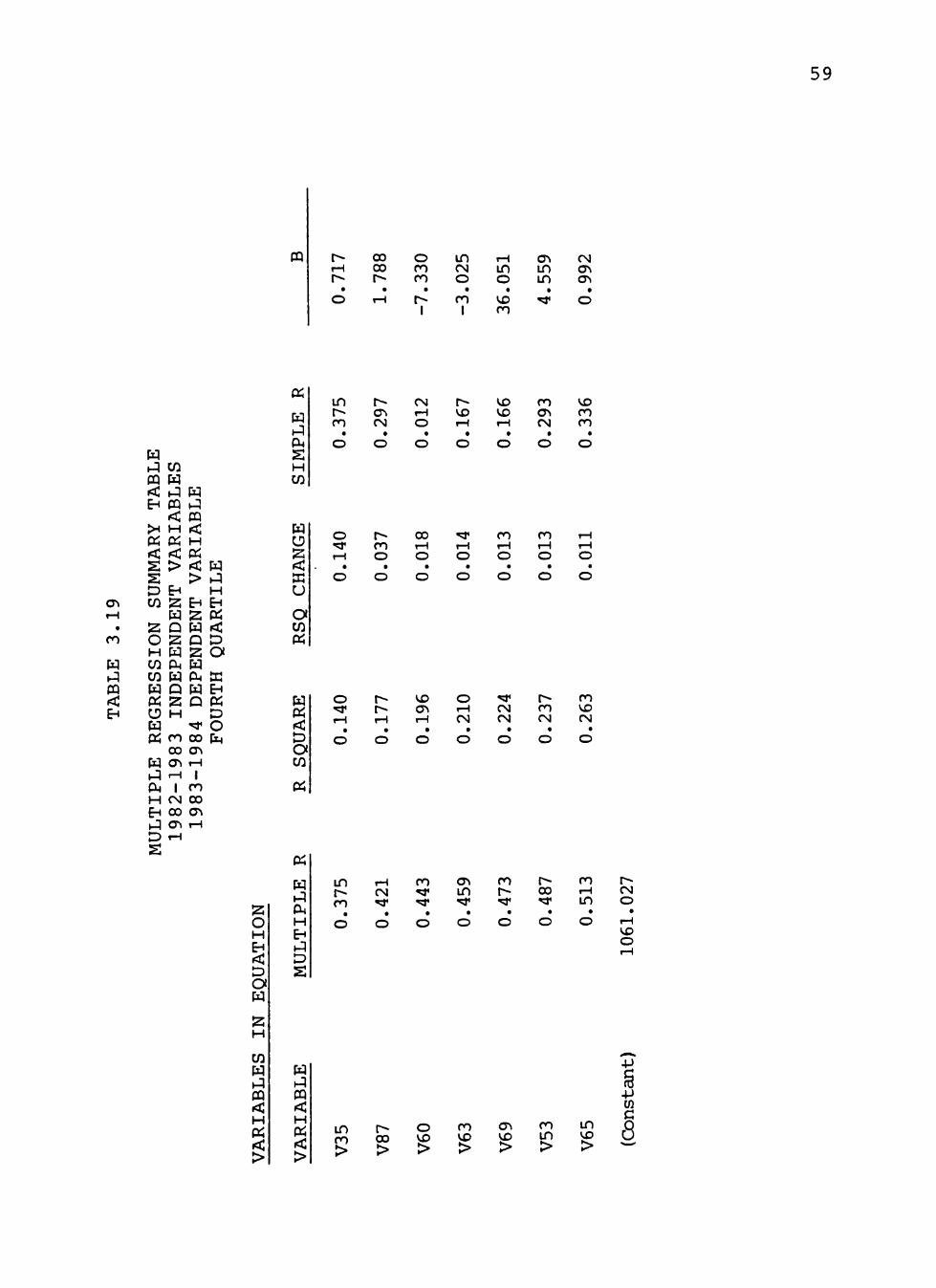

3.19 MULTIPLE REGRESSION SUMMARY TABLE 1982-1983 INDEPENDENT VARIABLE 1983-1984 DEPENDENT VARIABLE, FOURTH QUARTILE 59

3.20 TOTAL R^ VALUES 63

3.21 INDEPENDENT VARIABLES WITH RSQ CHANGE GREATER THAN OR EQUAL TO .01 64

VI

3.22 MEANS AND STANDARD DEVIATIONS OF CASH BALANCE 65

5.1 INDEPENDENT VARIABLES WITH R^ CHANGE GREATER THAN OR EQUAL TO .05 85

5.2 FREQUENCIES OF INDEPENDENT VARIABLES WITH R^ CHANGE GREATER THAN OR EQUAL TO .05 THAT OCCURRED IN MORE THAN ONE MODEL 89

A.l CORRELATION MATRIX 1980-1981 INDEPENDENT VARIABLES 1981-1982 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS 98

B.l CORRELATION MATRIX 1981-1982 INDEPENDENT VARIABLES 1982-1983 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS 105

C.l CORRELATION MATRIX 1982-1983 INDEPENDENT VARIABLES 1983-1984 DEPENDENT VARIABLE ALL SCHOOL DISTRICTS 112

Vll

LIST OF FIGURES

4.1 FREQUENCIES OF VARIABLES THAT ARE INCLUDED IN THE MODELS 70

4.2 VARIABLES INCLUDED IN THE MODELS FOR ALL SCHOOL DISTRICTS, FIRST QUARTILE AND FOURTH QUARTILE 75

Vlll

CHAPTER I

INTRODUCTION

Statement of the Problem

Legal mandates, constrained public funds, and increased

public demands for efficient management of our schools

require that planning be an integral component of the school

budgeting process. Forecasting school district fiscal

health is an essential part of the planning process. In the

final analysis, the school budget is "the translation of

educational needs into a financial plan..." (Candoli et al.,

1984, p. 127).

Fiscal health may be defined in terms of absolute

fiscal health or relative fiscal health (Smith, 1985) .

Texas identifies a school district as being fiscally healthy

if its ending fund balance is $0.00 or more. A deficit fund

balance is illegal according to state law (Texas Education

Code, 23.45b, 1978). However, authorities in education

finance advocate that a district should maintain a balance

or reserve equal to one to three months of expenditures

(Gaylord, 1983; Roland, 1986; Walker, 1986). If a budget

does not reflect fiscal health, the school district will be

less likely to meet the needs of its students. Likewise, it

can be assumed that a school district with a higher level of

fiscal health or higher cash balance, is more able to meet

1

the needs of its students than a school district with a

lower level of fiscal health or lower cash balance. Whether

it does or not is another question.

A part of budget planning and control is the local

education agency's assurance that revenues are equal to or

greater than expenditures because the legal mandate in Texas

requires that school districts -operate on a cash basis.

Decision makers at the local level prepare school district

budgets and bear the greatest responsibility for the alloca

tion of limited financial resources. Research efforts that

can provide assistance to local districts in forecasting

budget needs have been limited. A direct causal relation

ship has not been established between certain local school

district characteristics and the fiscal health of school

districts.

This study attempted to answer a number of questions.

First, is school district fiscal health predictable?

Second, what fiscal indicators, subject to the control of

local decision makers, can be used to forecast school

district fiscal health? Third, do different indicators have

predictive significance for school districts with a higher

level of fiscal health than for those school districts with

a lower level of fiscal health? Finally, does the

methodology employed in this study provide a viable strategy

for differentiating levels of school district fiscal health?

This study included 66 specific variables, deemed as

independent, from the area of local revenue, local

expenditures by function, and local tax data, which are

found on the Texas Education Agency Official Budget for

Texas Public Schools. Stepwise multiple regression was used

as the primary statistical procedure to obtain predictive

values (Nie et al., 1975; Hull and Nie, 1981). The

independent variables were regressed against ending fund

balance, the dependent variable.

Delimitations

1. The population consisted of all public school

districts in the State of Texas, excluding state-operated

schools and school districts serving fewer than twelve

grades.

2. Data were derived from summary reports submitted

on the Texas Education Agency Official Budget for Texas

Public Schools.

3. Data were included for the years 1980-1981,

1981-1982, 1982-1983, 1983-1984, prior to the reforms of

1984. Computerized data were unavailable from Texas Educa

tion Agency for the 1984-1985 and 1985-1986 school years.

4. Only indicators that are subject to control by

local decision makers were examined.

5. Quantitative measures were used as opposed to

qualitative measures.

Limitations

1. The number of school districts varied during the

years selected for the study because of the consolidation or

creation of school districts.

2. Texas Education Agency revised the budget docu

ments during the years selected for this study; therefore,

specific budget items vary from year to year.

3. While some independent variables were identified

on the basis of justifications provided by the literature or

authorities in the field, some a priori decisions were made

concerning other variables that were included in the study.

4. This correlational study, while both descriptive

and inferential, cannot demonstrate cause and effect.

5. This study did not examine economic conditions

such as employment, sales and property values.

6. This study did not examine qualitative measures of

fiscal health.

7. Results of this study cannot be generalized to

other states because data were confined to Texas.

Justification for the Study

Costerison (1984) identified major causes of fiscal

stress on school budgets. These include declining enroll

ment, voter resistance to tax increases, inflation, declin

ing state and federal aid, and employee demands. In a

period of fiscal retrenchment, school budget officers need

to make decisions which will protect the fiscal health of

their organizations. Traditional research on fiscal health

has focused on demographic variables and factors relating to

state funding formulas (Lee, 1983). The value of such

research to local budget officers is limited because it

reports on factors beyond their control. There is, conse

quently, a real need for research which gives the local

school administrator predictive control over local school

district fiscal health (Hentshcke and Yagielski, 1982a).

In Texas the fiscal burden on local school districts is

increasing (Jordan, 1985) . From 1973-74 to 1983-84 average

per pupil expenditures, not adjusted for inflation, have

increased from $910.00 to $2,960.00. Local contribution to

the total school budget increased from 41.5 percent to 46.4

percent during that same time period. This shift means that

local school administrators must assume a more proactive

responsibility for efficient use of available resources.

They can no longer depend on money from state and federal

sources to bridge the gap between mandates for new programs

and their costs. This study attempted to identify specific

indicators that local school administrators can control to

improve fiscal health.

Wegenke and Smith (1983) have identified characteris

tics of useful fiscal data. They suggest that fiscal data

must be translatable into understandable language in order

to be useful. In addition, useful data are described as

being credible throughout the term of the budget, timely and

subject to change.

This study seeks to increase the usefulness of budget

data available to local school administrators because

it defines that data in terms of its credibility or lack of

credibility to produce timely change.

Assumptions

1. Standardized data and other data provided to the

Texas Education Agency are accurate.

2. Fiscal data selected as independent variables can

be used as indicators of fiscal health.

3. Fiscal health can be influenced or controlled by

local school district administrators.

4. Fiscal health can be quantitatively defined as

cash balance.

5. School district decision making is more accurately

described as consumer behavior rather than producer behav

ior.

Definition of Terms

Budget is a plan of financial operation embodying an

estimate of proposed expenditures for a given period or

purpose and the proposed means of financing them.

Expenditures are total charges incurred for current

expense, capital outlay and debt service.

7

Fiscal data include quantitative information such as

local property taxes, total instructional payroll costs,

supplies and materials, tuition and fees that are taken from

the official school budgets.

Fiscal health, for purposes of this study, is defined

as the total fund balance that is indicated on the official

budget. School districts with higher fund balances are

fiscally healthier than school districts with lower fund

balances.

Fiscal indicators are budget items listed on the Texas

Education Agency Official Budget for Texas Public Schools

that can be controlled by local school district administra

tors .

Fiscal strain, as used in this study, is synonymous

with fiscal stress, conditions under which school district

decision makers are forced to purchase fewer or less desir

able inputs than in the past due to declining revenues,

increasing costs or a combination of both.

Function classification as applied to expenditures

refers to an activity or service aimed at accomplishing a

certain purpose or end; for example, instruction, instruc

tional administration, plant maintenance and operation.

Local revenue includes revenue generated from real and

personal property taxes, services to other local education

agencies, tuition and fees from patrons, within state

8

transfers, co-curricular enterprises and other local

sources.

Object classication as applied to expenditures refers

to an article or service received; for example, payroll

costs, purchased and contracted services, materials and

supplies.

Refined average daily attendance is the aggregate days

attendance of eligible students divided by the number of

days that school is in session. It is equal to the gross

average daily attendance less ineligible average daily

attendance.

Tax is a compulsory charge levied by a governmental

unit for the purpose of financing services performed for the

common benefit.

Procedures

This study was conducted using the following proce

dures:

1. Phase one of the study consisted of two tasks to

determine the feasibility of the project. Previous research

was examined in a review of the relevant school finance and

school budget literature. Texas Education Agency was con

tacted to determine that data were available.

2. Phase two of the study consisted of sorting the

data to extract independent and dependent variables and the

school districts that were included. Independent variables

consisted of budget data selected from tax information,

expenditures by function and local revenues. The dependent

variable was ending fund balance. Data files had to be

constructed in order to prepare the data for running the

stepwise multiple regression program. Independent and

dependent variables for all school districts in the State of

Texas that offered grades kindergarten through twelve were

identified. For each school district selected data from the

official budget report were divided by the refined average

daily attendance of the school district as means of provid

ing standard units for comparison. School districts were

ranked according to end of year fund balance divided by

refined average daily attendance and sorted into quartiles.

3. In phase three of the study, data for the whole

population and for quartiles were subjected to stepwise

multiple regression: 1980-1981 independent variables were

regressed against fiscal health in 1981-1982; 1981-1982

independent variables were regressed against fiscal health

in 1982-1983; 1982-1983 independent variables were regressed

against fiscal health in 1983-1984. Longitudinal data were

used because budget decisions to determine tax rates,

expenditures and revenues are made in the year preceding the

actual implementation of the budget. The major purpose of

this study was to analyze a strategy used to forecast school

district fiscal health.

10

4. Phase four of the study consisted of analyzing and

summarizing the data for presentation and analysis. Results

of multiple regressions were compared across quartiles and

across years.

Organization of the Research Report

This research is reported in five chapters. Chapter I,

the introduction, includes the statement of the problem,

delimitations, limitations, justification for the study,

assumptions, definition of terms, procedures and organiza

tion of the research report. Chapter II presents a review

of relevant literature and research. Chapter III consists

of the procedures and presentation of the data. Chapter IV

contains the findings and analysis of the data. Chapter V

presents a summary, major findings, conclusions and

recommendations.

CHAPTER II

REVIEW OF RELEVANT RESEARCH AND LITERATURE

This chapter presents a review of the literature

related to forecasting school district fiscal health. It

presents a brief discussion of managing and planning the

school budget, and discusses fiscal strain and its causes.

It identifies forecasting techniques and the consumer

approach to school district decision making and presents

summaries of pertinent research that focuses on forecasting

school district fiscal health. A summary concludes Chapter

II.

Planning the School Budget

In times of economic turbulence, public schools as well

as the private business sector have been subjected to finan

cial hardship. School district decision makers face the

dilemma of reconciling a decline in revenues while maintain

ing or even expanding programs. The public calls on school

district administrators to reduce costs while demanding that

the school improve the basic skills of pupils, expand pro

grams and provide more opportunities for special student

populations (Chabotar, 1987) . The problem is exacerbated as

staffs request higher salaries and more benefits (Hartman

and Rivenburg, 1985) , and by state and federal mandates to

implement new programs without providing additional funds to

11

12

cover the costs of expanding the school program. Inflation

takes its toll on budgets even when there is no demand for

growth and expansion. In its national annual survey, the

National School Boards Association reported that in 1981,

1982 and 1983 the greatest concern of school board members

was lack of funding (Smith, 1985).

The budget is the fiscal plan that reflects the educa

tional needs of the school district (Candoli, et al., 1984).

It operationalizes philosophies, priorities and strategies

and is the strongest measure of the priorities of local

education agencies (Hartman and Rivenburg, 1985). All

accepted definitions of budgeting include planning as a

component part, in addition to receiving funds, spending

funds and evaluating results (Burrup and Brimley, 1982).

Decisions at the local level are subject to the idiosyn

crasies of the school district such as local politics,

economic and social conditions, beliefs, attitudes and

priorities of the decision makers. However, the budget does

provide a common basis for making comparisons, and is the

strongest measure of comparison since it closely corresponds

with operations of the school district (Hartman and

Rivenburg, 1985). In states such as Texas, which mandate a

uniform format for reporting the school district budget,

these comparisons have the potential for predictive

applications.

13

Forecasting while focusing on immediate fiscal concerns

is an important part of the fiscal planning process (Wegenke

and Smith, 1983). Prudent decisions affecting the budget

consider past, present and projected trends. This process

requires that a school district establish financial review

and analysis procedures. Wegenke and Smith also specify

that fiscal data be understandable, credible, timely and

part of the overall financial picture making it subject to

change in the future. Because a budget defines fiscal

limits, local decision makers must manipulate those limits

to maximize their levels of consumption.

Fiscal Strain

The fiscal health of a school district can range from a

negative budget balance, which is illegal in Texas, to a

high budget balance. Dickmeyer (19 79) defined fiscal health

as the "ability to pay bills" (p. 161) . A school district

that is considered to be fiscally unhealthy can be described

as experiencing fiscal strain or fiscal stress. It is

difficult to define fiscal strain operationally since it is

a matter of degree; a relative term. Hentschke and

Yagielski (1982a) defined fiscal strain as the condition

that forces decision makers to purchase inputs that are less

desirable than the inputs that are currently being

purchased; that is, the combination of resources for next

year are less preferred. Zerchykov, et al. (1982) defined

14

fiscal strain as organizational shrinkage. Fiscal strain

reduces the discretion of school boards. Costerison (1984)

reported that the State of Indiana defines fiscal strain as

the condition under which a school district cannot carry out

its educational duty without emergency aid; and, that

Pennsylvania defines fiscal strain using various indicators

that range from inability to meet payroll to default on bond

payments.

It is important that planners be cognizant of causes of

fiscal strain because decisions should be based on qualita

tive as well as quantitative considerations. Lee (1983)

specified four major causes of fiscal strain. They included

decline in public confidence, unemployment, fewer voters

with school age children and declining enrollments.

Hentschke and Yagielski (1982a) added increasing prices of

inputs and changes in the input mix. Inflation, decreasing

state and federal revenues, increasing state and federal

mandates for new programs were added to the list by Hartman

and Rivenburg (1985) . Costerison (1984) expanded the list

of major causes to include 31 specific causes of fiscal

strain. Exogenous factors are listed above; however, the

local school district decision maker must exercise caution

not to introduce internal causes of fiscal strain such as

overspending, failing to adjust the tax rate, failing to

project student enrollment and staffing requirements.

15

Forecasting Techniques

Chabotar (1987) identified forecasting as a critical

issue, but cautioned that forecasting should be used as one

input in the decision making process along with economic and

political factors. He confirmed, along with the studies of

Lee (1983), Smith (1985) and Ward (1985), that forecasting

can be used effectively by school district decision makers

to make fiscal decisions and that there is a great need for

linking the annual budget to long-term fiscal plans.

Chabotar identified four forecasting techniques. The

first is subjective judgment, which is not a quantitative

procedure. It is based upon the expertise and experience of

the forecaster. One example is the Delphi panel. Causal

models constitute a second forecasting technique. These

types of forecasts are based upon relationships between

revenue, expenditures and independent variables selected by

the forecaster. Examples of this type are ratio methods,

multiple correlation, regression and path analytic models.

Extrapolation is the third technique. This type of forecast

predicts the future based upon revenues and expenditures

continuing at the same rate. It depends upon using stable

data such as birth rates, economic conditions and policies.

This technique assumes the existence of a particular trend

and that the trend will continue through the years of the

forecast. Chabotar included normative approaches as a

fourth technique although he contended that they really are

16

not forecasts. Instead they are descriptions of scenarios

in terms of what should be. Predictions may or may not

reflect historical trends. Normative approaches may use

statistical relationships and extrapolations for background

information. Gaylord (1983) provided caveats to

forecasting: forecasting is a conservative approach since

it cannot predict sudden and unanticipated deviations from

historical trends; it is not causal; and it requires

consistent and precise data.

School district decision making is more accurately

described as consumer rather than producer behavior because

budget decisions are a function of the interactions between

preferences and budget constraints (Hentschke and Yagielski,

1982b). These authors described three characteristics of

decision making that justify this conclusion. First, the

behavior of local decision makers reveals preferences in

dealing with theoretically unlimited wants and budget

constraints. The budget reflects what was given up in some

items in order to gain other items; that is, the consid

eration of opportunity costs. Second, the principle of

diminishing marginal utility is applicable. The satis

faction gained from the first unit of a good or service is

greater than the satisfaction that is derived from addi

tional units. Third, the consumer model suggests causes and

descriptions of fiscal strain: increasing, maintaining or

decreasing levels of consumption. Hentschke and Yagielski

17

(1982a) also indicated that the consumer model assumptions

are more theorectically valid and empirically descriptive

than the assumptions of the producer model which assumes an

agreed upon definition of quality and a constant level of

the quality of the output of schooling. The consumer model

allows a situation to be described as fiscal strain even

when there is an increase in the total budget. Thomas

(1980) supported the application of the consumer approach.

He stated that the producer approach is inadequate because

it is based on the factory model which oversimplifies the

decision making behavior. It fails to recognize and con

sider the "multiplicity of decision makers, the diversity of

goals, the complex nature of educational inputs and intri

cate relationships ... between resources and outcomes" (p.

252) . It is very difficult to determine the utility of

inputs. Alternatives are not comprehensive nor of equal

financial magnitude or consequence (Hentschke and Yagielski,

1982b).

The literature and research cited above provide justi

fication for choosing multiple linear regression and corre

lation as a strategy for forecasting school district fiscal

health. Chabotar (1987) indicated that using regression and

correlation statistics to create a causal model is the best

forecasting technique. Its credibility is based on the use

of hard data and the statistical power of the procedures.

Ward (1985) used multiple regression to create a causal

18

model using bond ratings. Ward's model exhibited 85%

accuracy in predicting presence or absence of fiscal strain.

Studies of School District Fiscal Health

Murphy (1980) tried to determine if financial, demo

graphic, economic, electoral or environmental variables

could be identified that would characterize school districts

in Ohio that were financially troubled or that were experi

encing fiscal strain. He identified financially troubled

districts as those that were forced to close between 1976

and 1978, and districts that received emergency loans from

the state. All other school districts were considered to be

fiscally healthy. The study used analysis of variance to

differentiate variables that distinguished the two groups of

school districts. Murphy concluded that:

1. Financially troubled districts are primarily classified as central city and rural.

2. Over-staffing is not a factor contributing to the fiscal problems of financially troubled districts.

3. Financially troubled districts are concentrated in the northern and southern sections of the state.

4. Financially troubled districts are spread over more geographical space. This difference was not translated into significantly higher per pupil transportation expenses.

5. Financially troubled districts are characterized by high proportions of special cost students.

6. Financially troubled districts cannot be characterized as declining enrollment districts.

19

7. Financially troubled districts can be characterized as low fiscal capacity districts in terms of having lower median family income. There was not a significant difference when fiscal capacity was defined in ... equalized assessed valuation per pupil.

8. Financially troubled districts had a significantly lower equalized millage rate. Unequalized and debt millages were not significantly different between financially troubled and non-troubled districts.

9. Financially troubled districts are low revenue districts. Almost all the difference is in locally raised revenue.

10. Financially troubled districts are characterized as high health and interest expense districts and as low instruction, general control, and plant maintenance expense districts.

11. Financially troubled districts appear to pass fewer requests for millage.

(Murphy, 1980, pp. 177-184)

The variables in Murphy's study that met the criteria

of being subject to change or under the control of local

decision makers are particularly relevant to the current

study. Murphy concluded that the level of staffing was not

a factor that contributed to fiscal strain. However,

personnel costs were significant because they constituted

the largest portion of a school district's expenditures due

to the labor intensive nature of schooling. Murphy also

noted that locally raised revenue accounted for most of the

difference between financially troubled and non-troubled

districts. Financially troubled school districts were

characterized by high health and interest expenses while

20

expenditures for instruction, general control and plant

maintenance were low.

Berny attempted to identify the variables that could be

used to discriminate between financially troubled and

non-troubled rural school districts using a causal-

comparative research method. Multiple discriminant analysis

was conducted to determine the relative influence of six

fiscal and demographic variables: geographical size,

special cost children, fiscal capacity, tax effort, total

general revenue and excess staff. Financially troubled

school districts were those districts that closed and those

districts that applied for preclosing audits. Berny

concluded that:

1. There was no discernible statistical difference between the rural districts defined as financially troubled and non-troubled for any of the years studied on any of the variables tested.

2. None of the selected variables possessed a higher discriminating capacity than any of the others.

3. When examined from a nonlinear point of view, there was no interactive or cumulative effect of the selected variables that exceeded the effect of any one alone.

(Berny, 1982, p. 480)

It is significant that the variables investigated in

Berny's study did not discriminate troubled from non-

troubled rural school districts. It appears that the

variables were not relevant to the question studied.

However, his results contradicted certain conclusions of

21

Murphy (1980) who used a larger sample that included rural,

urban and suburban districts. Murphy found that financially

troubled districts were characterized by large geographic

area, high proportions of special cost students, low fiscal

capacity, low tax effort and low revenue. Berny agreed with

Murphy (1980) that staffing levels did not discriminate

levels of fiscal health.

Lee (1983) attempted to predict fiscally distressed

school districts using ratio analysis. School districts

that received emergency state loans in 1981 were identified

as experiencing fiscal distress; 36 of the 615 school

districts in Ohio were eliminated from the study because of

problems with data. Lee analyzed financial and staffing

ratios using multiple discrimination analysis and correla

tion. He used the qualitative dependent variable of dis

tressed or not distressed. Five ratios, which displayed

predictive significance, were used in the fiscal distress

predictive model included the following:

1. True Day's Cash Ratio = (12/31/80 Cash Balance-Encumbrances) / (1980 Current Expenditures/365 days)

2. True Ending Cash Balance Ratio (12/31/80 Cash Balance-Encumbrances) / (1980 Total Operating Funds)

3. Salaries/Operating Ratio = 1980 Salaries & Wages / 1980 Total Operating Funds

4. Salaries-Fringes/Operating Ratio = 1980 Salaries & Wages + Fringe Benefits / 1980 Total Operating Funds

22

5. Investment Earnings Ratio = 1980 Investment Earnings / 19 80 Total Operating Funds

Lee concluded that:

1. Financial ratios have the ability to forecast fiscal distress as early as one year in advance. ... historical data were able to forecast over 90 percent of the districts that eventually experience financial problems.

2. Liquidity ratios demonstrated strength in forecasting financial problems in school districts. Unlike private business enterprise ... education ... is more sensitive to cash balance fluctuations.

3. Elementary/secondary institutions are labor intensive. In this study, the percent of operating funds spent for salaries, wages and fringe benefits proved to be potent indicators of impending fiscal doom.

4. Although not the primary cog in the fiscal distress model, the Investment Earnings ratio enhances the accuracy of the model.

5. ... expenditures and revenues per pupil have little or no value in forecasting fiscal distress. These conclusions do not recommend the banishment of per pupil expenditure data, but caution their use in respect to fiscal health.

6. There were no relationships found between elevated staffing levels and fiscal distress.

7. Trend ratios, measuring changes between the beginning and ending fiscal periods of 1980 did not demonstrate any predictive significance in the Fiscal Distress model.

8. The borrowing or loan repayment ratios were not found to have any predictive relationships with fiscal distress.

(Lee, 1983, pp. 261-262)

Authorities in school finance have labelled Lee's study

a milestone in predictive research (Lee, 1983). Conclusions

23

4, 5, 6 and 8 are of interest since they discuss variables

used in this study. Lee's study was the impetus for Smith's

work.

Smith (1985) based his forecasting study on Lee's

research. Smith redefined fiscal health, the dependent

variable, in quantitative terms, defined the variables using

raw data, examined more areas and analyzed a time frame of

three years rather than one year. His population consisted

of all 616 school districts in Ohio. Independent variables

included specific indicators in the categories of liquidity,

salaries and capital projects funds. Smith concluded that:

1. ... school district fiscal health lends itself to considerable predictability.

2. ... predictability improves with shorter prognostic periods.

3. ... predictive models, as developed in this study, are highly temporal — that is, they are unique to each fiscal period.

4. ... the consistent nature gf the findings, particularly the pattern of R values and the rankings ... demonstrate the general validity for the approach taken by this study.

5. ... a relatively few indicators, when considered together with all the indicators examined, contribute to the predictability of school district fiscal health. The five most important, in descending order, are: (1) personnel costs; (2) local receipts; (3) liquidity; (4) purchased services; and (5) investment earnings.

6. ... some of the indicators examined are weak predictors of school district fiscal health, when considered together with the other variables examined. They are, in descending order of importance: (1) material, supply and textbook expenditures; (2) capital outlay expenditures; (3)

24

voted and effective millage; and (4) capital project fund indicators.

7. ... indicators maintain their relative importance irrespective of the prognostic period.

(Smith, 1985, pp. 139-140)

This study builds upon Smith's work. Raw data were

used as independent variables; levels of fiscal health have

been identified in order to make comparisons within each

year and across years. The techniques were applied to the

present study of school district budgets in Texas using a

function/object type of budget format.

Identification of Variables

The selection of independent variables was based

primarily upon criteria established by Smith (1985) which

require that:

1. Its numerical value must be capable of being changed by local decision makers.

2. Its potential usefulness (in making forecasts) is indicated by relevant literature; and

3. The data used to compute it must be readily available and accurate.

(Smith, 1985, p. 84)

In addition to Smith's criteria, fiscal indicators were

selected as independent variables because the best projec

tions are based upon the lowest level of detail; that is,

the most specific information that is available, not lump

sums (Chabotar, 1987). Also, these independent variables

25

are used consistently throughout the state, are relatively

easy for all school districts to provide, and are compre

hensible and usable in terms of budget decisions ("Is Your

Budget in Tune?", 1981).

Research studies cited above validate the variables

that were selected for this study. Those studies were

conducted in other states; therefore, the variables do not

have exactly the same labels as those that are used in the

Texas budget format. Some of the variables used by Murphy

(1980) were tax rate, locally-raised revenue, health

expense, plant maintenance and personnel costs. Berny

(1982) included fiscal capacity and tax effort. Lee (1983)

constructed ratios using cash balance and expenditures.

Smith (1985) included personnel costs, local receipts,

material, supply and textbook expenditures and local

receipts.

Table 2.1 lists and defines the independent variables

and indicates the years in which they are found in the

budgets. A total of 66 variables was identified and used in

this study. Texas Education Agency revised the budget

reporting form during the years included in this study;

therefore, the same fiscal indicators are not found in each

year, although the budget format remained the same. The

major revisions that affected this study were made after

1981-1982, when tax data categories for maintenance taxes

and debt service taxes were combined into totals for the

fiscal years 1982-1983 and 1983-1984.

26

Fiscal Year

1980- 1981- 1982-1981 1982 1983

X X

Maintenance Taxes

1983-1984

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

Table 2.1

VARIABLES

Variable Identification and Explanation

VI Balance of funds

Vll Assessed valuation

V12 Tax rate/$100

V13 Gross taxes assessed

V14 Discounts and adjustments

V15 Net taxes assessed

Vl6 Estimated uncollectible current taxes

V17 Net taxes collectible on current year's levy

V18 Total current year deferred revenue (...to be collected in subsequent years)

VI9 Current year tax revenue

V20 Prior years tax revenue

V21 Penalties, interest and other tax revenue

Debt Service Taxes

X

X

X

X

X

X

X

X

X

V22 Assessed valuation

V23 Tax rate/$100

V24 Gross taxes assessed

V25 Discounts and adjustments

X X

X X

X X

27

TABLE 2.1 (continued)

^ ^ V26 Net taxes assessed

^ ^ V27 Estimated uncollectible current taxes

X V28 Net taxes collectible on current year's levy

V29 Total current year deferred revenue (...to be collected in subsequent years)

V30 Current year tax revenue

V31 Prior years tax revenue

^ ^ V32 Penalties, interest and other tax revenue

Total Tax Data (Maintenance Plus Debt Service)

X V33 Total appraised value per tax roll

X V34 Total appraised value for school tax purposes

X V35 Calculated tax levy

X V36 Additional tax levy generated due to bond rate charged against exempted homestead property

X V37 Tax levy loss due to tax freeze

X V38 Other adjustments, and discounts

X V39 Net taxes assessed

Expenditures by Function

X X X V50 Instruction

X V51 Instructional computing

X X X V52 Instructional administration

28

TABLE 2.1 (continued)

X X X V53 Instructional resources and

media services

X X X V54 School administration

X X X V55 Instructional research and development

X X X V56 Curriculum and personnel development

X X X V57 Communications and dissemination

X X X V58 Guidance and counseling services

X X X V59 Attendance and social work services

X X X V60 Health services

X X X V61 Pupil transportation -regular

X X X V62 Pupil transportation -

exceptional children

X X X V63 C o - c u r r i c u l a r a c t i v i t i e s

X X X V64 Food s e r v i c e s

X X X V65 G e n e r a l a d m i n i s t r a t i o n

X X X V66 Debt s e r v i c e

X X X V67 P l a n t m a i n t e n a n c e and o p e r a t i o n

X X X V68 Facilities acquisition and

construction

X X X V69 Management (Data Processing)

X X X V70 Computer processing X X V71 Development (Data Processing)

29

TABLE 2 . 1 ( c o n t i n u e d )

X X X V72 I n t e r f a c i n g ( T e c h n i c a l

a s s i s t a n c e )

X X X V73 Community s e r v i c e s

Revenue from L o c a l and I n t e r m e d i a t e S o u r c e s

X X X V80 L o c a l m a i n t e n a n c e t a x

X X X V81 Debt s e r v i c e t a x

X X X V82 L o c a l r e v e n u e from s e r v i c e s t o o t h e r LEA's and ESC's

X X X V83 T u i t i o n and f e e s from p a t r o n s

X X X V84 T r a n s f e r s from w i t h i n t h e s t a t e

X V85 Transportation fees from patrons

X X

X X

X X

X X

X X

X V86 Enterprise funds

X V87 Other revenue from local sources

X V88 Revenue from intermediate sources

X V89 Non-revenue receipts (proceeds from bonds, loans, lease/purchases, etc.)

X V90 Revenues from outside the state

X V91 Transfers in

30

Consequently, the number of variables examined each year of

this study is less than 66. Variables were assigned numbers

arbitrarily; VI is the fund balance; Vll through V39 are tax

data; V50 through V73 are expenditures by function; and V80

through V91 are revenues.

Summary

Chapter II discussed the recent evolution of a rela

tively new area of school finance. The importance of con

tinuous planning was emphasized because the school budget

reflects educational needs and priorities and can be used as

a measure of comparison among school districts. Causes of

fiscal stress were identified along with forecasting techni

ques in order to facilitate the budget planning process. It

was discussed that school district budget planners take a

consumer approach to decision making. Studies by Murphy

(1980), Berny (1982), Lee (1983) and Smith (1985) indicated

that multiple regression and correlation techniques were

appropriate statistical procedures to use in this study.

These studies also identified criteria to use in selecting

variables. Tax data, expenditures by function, and revenue

subject to the control of local decision makers were

selected as variables for this study and divided by refined

average daily attendance to provide common units of

comparison. The methodology was selected based upon the

31

studies cited in this chapter and because of the structure

of the budget that is mandated by Texas.

CHAPTER III

PROCEDURES AND PRESENTATION OF THE DATA

The purpose of this study was to analyze a strategy for

forecasting school district fiscal health in Texas. Cash

balance was selected as the quantitative measure of school

district fiscal health, the dependent variable, and the

fiscal indicators of tax data, expenditures by function and

revenues divided by refined average daily attendance were

the independent variables. The goal of this study was to

determine if the relationships between the dependent vari

ables and the independent variables could be used to predict

fiscal health.

The purpose of this chapter is to describe the research

procedures. Phases of the study are outlined; the popula

tion is defined; statistical strategies are identified; and

data are presented.

Source of the Data

In phase one, fiscal data for the official budgets were

obtained from Texas Education Agency Division of Policy

Analysis. Master computer files included all fiscal data

that were submitted by each school district to the Texas

Education Agency, district names and identification numbers,

32

33

and refined average daily attendance for all school dis

tricts and Education Service Centers in the state.

Fiscal data were taken from the Texas Education Agency

Official Budget for Texas Public Schools for the fiscal

years 1980-1981, 1981-1982, 1982-1983 and 1983-1984.

Sorting the Data and Identifying the Variables

Phase two of the study consisted of sorting the data.

Variables were identified and data files were constructed.

Texas Education Agency provided dumps of their fiscal files

which included extraneous data that had to be eliminated.

The population for this study consisted of all school

districts in the State of Texas that offered programs for

grades kindergarten through twelve. Deleted from the study

were school districts that did not offer those grades and

Education Service Centers which were identified according to

information in the Texas Education Agency School Directory

for the years included in the study. As shown in Table 3.1,

the total number of school districts included in the study,

the N of cases, varies from year to year because school

districts were either consolidated or created. Differences

in the N of cases did not affect the results of the multiple

regressions because this study examined budget characteris

tics in general and not the fiscal performance nor budgets

of individual school districts.

34

TABLE 3.1

NUMBER OF SCHOOL DISTRICTS INCLUDED IN THE STUDY

1980- 1981- 1982- 1983-Quartile 1981 1982 1983 1984

1 245 245 245 245 2 245 245 245 245 3 245 245 244 245 4 244 244 244 245 Total N 979 979 978 979

35

A number of data files were set up in order to process

the data and to provide a means of checking the process.

The data files include the following information: names of

all school districts and their refined average daily

attendance listed by county-district identification number;

all school districts with all budget items included in the

study listed in order of county-district identification

number; all school districts ranked according to fund

balance divided by refined average daily attendance

(dependent variable); all school districts with all budget

items selected for this study divided by refined average

daily attendance and ranked according to fund balance

divided by refined average daily attendance; and, all school

districts with all dependent and independent variables

listed in order by county-district identification numbers.

Budget categories selected for use in this study were

divided by the refined average daily attendance. This

provided a common means of comparison. School districts

were ranked according to the dependent variable and the data

for each year were divided into quartiles so that compari

sons could be made among four levels of fiscal health within

each year and across years.

Statistical Procedures

Phase three of the study consisted of statistical

analysis of the data. The data files were organized to

36

facilitate the use of stepwise multiple regression. Statis

tical Package for the Social Sciences (Nie et al. 1975;

Hull and Nie, 1981) was employed using the facilities of the

Texas Tech University Academic Computing Services.

The first step in the statistical analysis of the data

was to generate descriptive statistics that were examined to

determine whether multiple regression procedures were appro

priate. The mean and standard deviation of dependent and

independent variables for all school districts, displayed in

Tables 3.2, 3.3 and 3.4 were generated along with

correlation matrices for all variables for all school

districts, which are located in Appendix A, Appendix B and

Appendix C. These statistics provide a preliminary

understanding of the data that were selected for the study.

Pearson product-moment correlations were calculated for all

possible pairs of dependent and independent variables.

Because no controls were made for the influence of other

variables, these are called zero-order correlations (Nie et

al. 1975).

TABLE 3.2

MEAN AND STANDARD DEVIATION, 1980-1981 INDEPENDENT VARIABLES, 1981-1982 DEPENDENT VARIABLES,

ALL SCHOOL DISTRICTS N = 979

37

VARIABLE

VI Vll V12 V13 V14 V15 V16 V18 V19 V20 V21 V22 V23 V24 V25 V26 V27 V29 V30 V31 V32 V50 V52 V53 V54 V55 V56 V57 V58 V59 V60 V61 V62 V63 V64 V65 V66 V67 V68 V69 V70

MEAN

518.715 125976.959

2.414 1001.284 10.644 990.640 19.520 971.120 945.612 16.676 3.944

126339.420 0.328

151.860 1.574

150.285 3.028

147.257 142.781 3.125 0.796

1289.235 23.664 35.742 105.178 1.008 0.096 0.207 34.499 1.723 13.970 124.580 3.194 49.469 18.224 266.287 161.739 290.020 248.929 0.264 0.321

STD. DEV.

752.814 237334.284

3.481 1051.052 27.935

1037.147 39.186

1024.908 1010.951 23.642 8.435

237286.628 0.528

173.009 5.667

170.845 4.919

169.306 166.265 4.726 3.678

460.413 42.810 28.115 59.733 11.934 4.146 1.389 39.134 5.424 32.569 98.852 14.240 48.369 44.175 214.863 171.176 271.208 797.294 4.763 3.254

38

TABLE 3 . 2 ( c o n t i n u e d )

VARIABLE MEAN STD. DEV,

V71 0.000 0.000 V72 0.017 0.483 V73 5.868 61.708 V80 966.233 1016.473 V81 146.702 167.781 V82 2.894 20.743 V83 2.846 6.106 V85 0.372 1.657 V86 3.168 18.179 V87 43.558 155.899 V88 18.898 63.339 V84 3.481 15.371 V90 0.158 4.831 V89 52.585 445.019

39

TABLE 3 . 3

MEAN AND STANDARD DEVIATION, 1 9 8 1 - 1 9 8 2 INDEPENDENT VARIABLES,

1 9 8 2 - 1 9 8 3 DEPENDENT VARIABLES, ALL SCHOOL DISTRICTS

N = 979

VARIABLE MEAN

VI Vll V12 V13 V14 V15 V16 V17 V18 V19 V20 V21 V22 V23 V24 V25 V26 V27 V28 V29 V30 V31 V32 V50 V52 V53 V54 V55 V56 V57 V58 V59 V60 V61 V62 V63 V64 V65 V66 V67 V68

628.047 236004.075

16.487 1142.359 11.274

1131.085 19.428

1111.656 30.751

1080.905 16.551 4.249

236601.623 2.362

176.065 1.822

174.243 3.172

171.071 5.698

165.372 3.481 6.734

1450.647 26.342 41.454 124.465 0.775 1.661 0.329 38.559 1.786 15.534 138.904 3.702 58.869 21.893 296.041 191.928 333.330 274.286

STD. DEV.

965.273 711478.493

23.440 1166.779

29.309 1151.273

30.269 1138.290

40.473 1128.079

28.973 8.432

711423.671 4.145

208.300 5.844

205.482 5.678

203.067 8.768

199.138 5.742 1.294

565.893 40.668 33.503 71.732 11.129

9.760 0.067

40.547 5.081

36.743 106.878

12.396 56.439 49.158

228.559 216.809 257.858 930.963

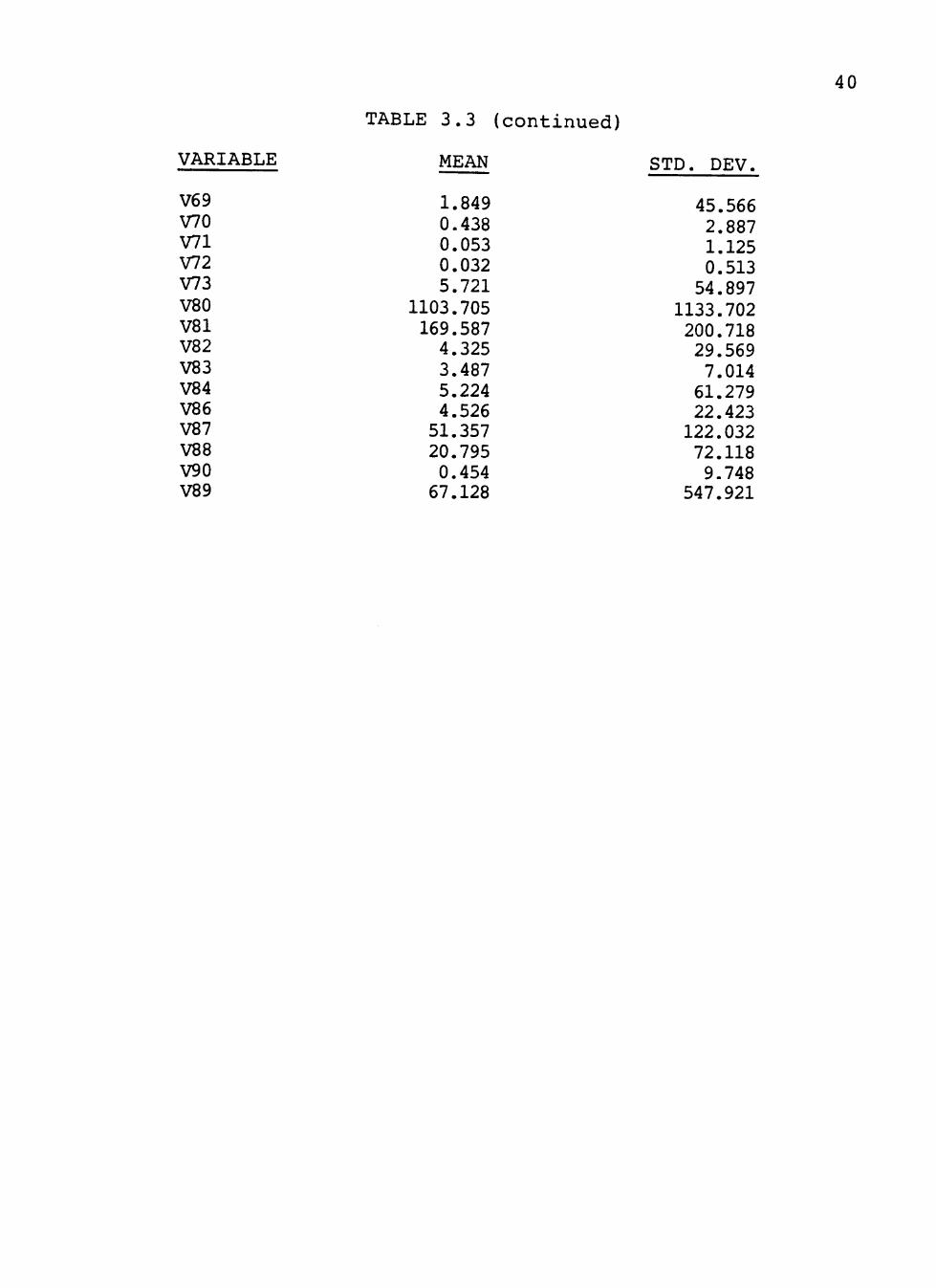

40

TABLE 3 . 3 ( c o n t i n u e d )

VARIABLE MEAN STD. DEV.

45.566 2.887 1.125 0.513

54.897 1133.702

200.718 29.569

7.014 61.279 22.423

122.032 72.118

9.748 547.921

V69 V70 V71 V72 V73 V80 V81 V82 V83 V84 V86 V87 V88 V90 V89

1.849 0.438 0.053 0.032 5.721

1103.705 169.587 4.325 3.487 5.224 4.526 51.357 20.795 0.454 67.128

41

TABLE 3.4

MEAN AND STANDARD DEVIATION, 1982-1983 INDEPENDENT VARIABLES, 1983-1984 DEPENDENT VARIABLES,

ALL SCHOOL DISTRICTS N = 978

VARIABLE MEAN STD. DEV.

VI V50 V51 V52 V53 V54 V55 V56 V57 V58 V59 V60 V61 V62 V63 V64 V65 V66 V67 V68 V69 V70 V71 V72 V73 V80 V81 V82 V83 V84 V86 V87 V88 V90 V91 V89 V33 V34 V12 V23

669.925 1591.870

2.833 29.128 45.652 139.761 0.714 2.084 0.445 42.288 2.029 16.956 145.628 4.331 96.985 181.620 307.741 207.628 355.756 310.063 0.184 0.938 0.361 0.022 5.647

1217.141 192.205 4.667 4.485 8.123

110.843 77.056 19.986 0.394 4.199 72.743

346473.771 291496.260

14.172 1.940

865.890 534.814

12.442 44.986 33.839 75.090 11.048

8.504 2.491

42.888 5.663

39.731 108.363

13.204 71.469 71.827

217.773 262.320 243.840 907.272

2.298 4.579

10.209 0.285

52.334 1207.168

246.312 23.245

8.850 35.570 88.024

145.264 71.780

7.671 32.156

446.868 948656.139 936934.602

21.130 3.541

42

TABLE 3 . 4 ( c o n t i n u e d )

VARIABLE MEAN STD. DEV.

1345.724 7.250

29.171 45.310

1323.975

V35 V36 V37 V38 V39

1466.868 1.169 18.537 16.835

1432.980

43

In the final phase of statistical analysis, data were

subjected to stepwise multiple regression which yielded

prediction equations (Cornett and Beckner, 1975; Kerlinger,

1973; Kim and Kohout, 1975) based on correlation. Multiple

linear regression was selected because this multivariate

procedure can be used to analyze effects of more than one

independent variable on a dependent variable. It is the

most useful and flexible method because any number of

continuous or categorical variables can be analyzed; and it

is appropriate for non-experimental variables to examine

within-group variance (Kerlinger, 1973).

The stepwise regression program examined each variable

that was selected for analysis. The computer entered one

variable at a time in single steps beginning with the

variable that explained the greatest amount of variance with

the dependent variable and continuing in descending order of

importance. Three options were used to determine which

variables were included in the regression equation generated

by the program (Nie, et al. 1975). The first option

permits the programmer to select or limit the number of

variables that may be included in the predictor list. The

second option is the determination of the minimum value of

the F ratio that the programmer will accept for variables to

be included in the equation. F ratios were computed for

independent variables not yet included. The F ratio was the

value that would be obtained if the variable were included

44

on the next step. The tolerance of an independent variable

was the third option. Tolerance is the proportion of the

variance of that variable not explained by the variables

already included.

The values of the options selected for this study

exceeded the default values. All variables were included in

the analysis. The F value was set at .05; the default value

is .01. The tolerance index was set at .20; the default

value is .001. More conservative default values were

selected to make the data more manageable and to include in

the equation those variables that had greater explanatory

power.

A total of 15 stepwise regressions was conducted.

Independent variables for 1980-1981 were regressed against

the dependent variable for 1981-1982; independent variables

for 1981-1982 were regressed against the dependent variables

for 1982-1983; independent variables for 1982-1983 were

regressed against the dependent variable for 1983-1984. The

regression program yielded a number of statistics that

described the relationship between fiscal indicators, the

independent variables and cash balance, the dependent

variable.

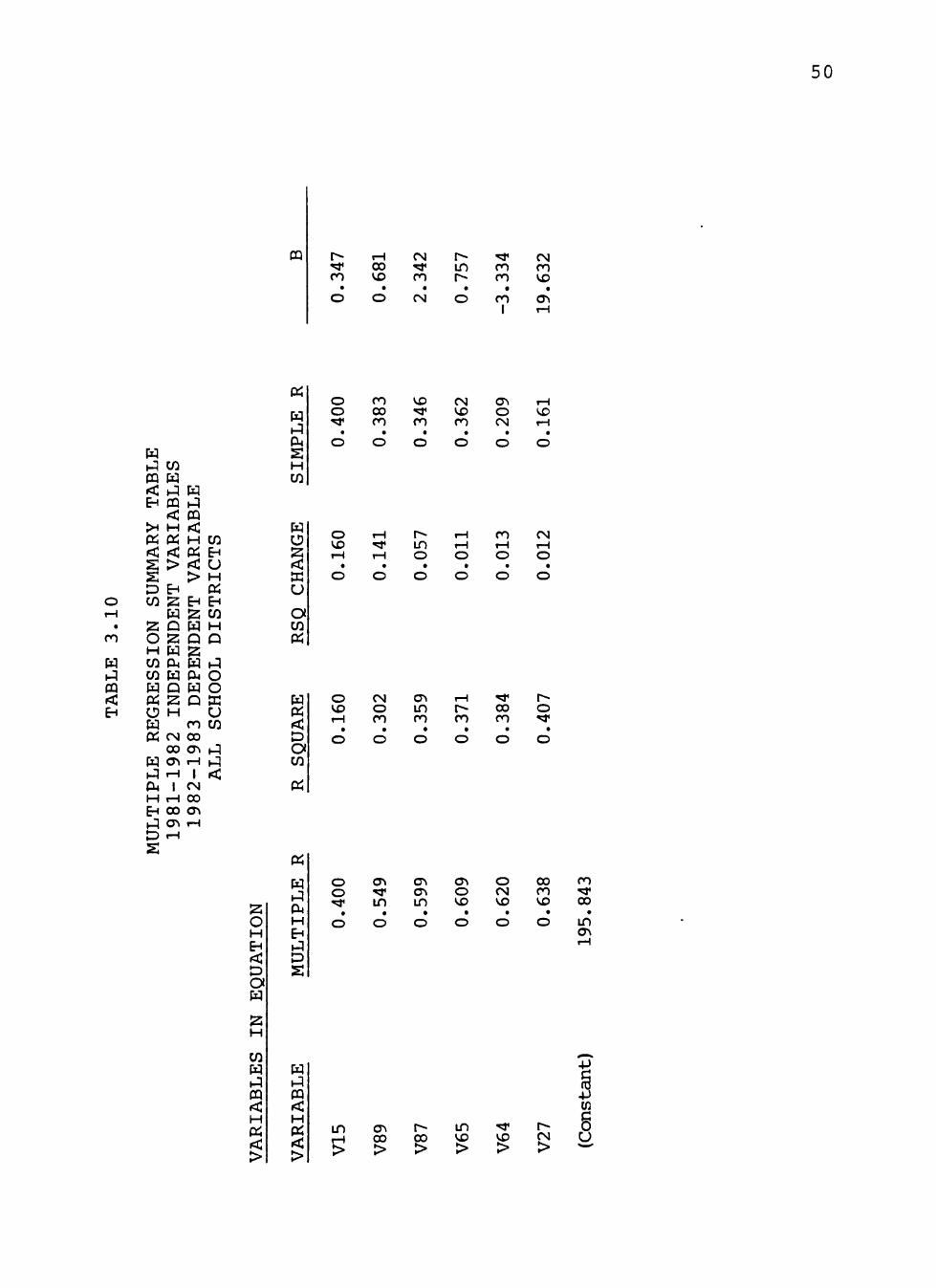

Summary Tables 3.5 through 3.19 display values of

2 2 multiple R, R , R change, simple R and B, the regression

2 coefficient, for independent variables with R change

greater than or equal to .01. Multiple R, the multiple

45

CQ t-H ' ^ o^

• «—1

CN m KD

• rH

O a\ ^

• i n

o en r^

• 1

vo cr> vo

• o

«

IT) •

ro

W 1 ^ ffi < E-t

W h^ ffi < E-i

>H K

en w t ^ CQ < H ff;

H

< H W

< <: « EH S > < U s p w

s o H W W w «

o w K

w h^ fi^ M EH t ^ D S

EH

2 H Q 2; H CM H D IS H

i H 00 cr» i - i 1

o 00 <T> i H

> M «

EH EH

S W W M Q P IS H t- CU O K O Q ffi

U CN CO 00 cr. f j rH t^ 1 <

T-H 00 CT\ rH

W tJ CU s H W

w o 2 <: re u a w «

w p rt: D O W

tf

2: o H EH

<:

a is H

W

w OQ <

>

H

H EH

D

H

OQ

H Pi < >

CN

ro rH

ro o

ro CM o

cy> 00 o ro

00 ro t-H

• O

KD 00 O

• O

00 CM O

• o

rH CM o

• o

CM rH O

« o

00 ro r H

IT) CM CM

ro i n CM

"^ r-CM

r^ 00 CM

CM

ro ro o in

CN in

ro in

o in

00 r-t >

V^ 00 >

o CM >

* * T-i >

in

in

46

PQ cri CM ro

• o 1

r^ i n 00

• CM 1

O ^ CM

• rH

^ V£) :< •

o 1

cr» o> 00

• i n r-\

^ 00 I ^

• i-{

Pi

V£> •

ro

W 1^ PQ < EH

W t-q W m H <: h i H EH PQ 1-5

< P3 >^ H <C Pi p; H < < «

s > < S > H D EH •q W IS EH H

H IS EH 2 : P W « O IS Q < H H ^ ; D w cu w a W W P< W D W EH p; IS Q W O H « W CM H Pi rH 00 fa

00 <T\ W cr> tH i-:i «-! 1 eu 1 -H H O 00 EH 00 CTi ^q cr. rH D H

s

H Hi PU S H W

H U S < K U

a w Pi

H Pi < P

a w Pi

Pi

IS

o M ^ < o a H

2 : H

W W i-:i CQ < H p; < >

w hi (h M tH ^J D S

W t-q PQ < M Pi < >

r-CM CM

• o 1

VD V£) rH

• O 1

r>-r-o

• o

o 00 o

• o 1

o CO T-i

• o 1

VD CM O

• o 1

in o

ro CM o

rH O

o

o rsi o

o o o

o o o

^ r-o

00 00 o

<y\ o rH

<y\ rH T-^

V£> i n r-t

r^ CM CN

• o

ro t^ CM

• o

00 a\ CN

• o

o ro ro

• o

i n * * ro

• o

i n a\ ro

• o

^ o 00

• in CM

>

CN T-\

CM >

O y£> >

m CM >

i n CN >

-p (n

§

PQ CM 00

in

o I

CM in 00

CM

r •

ro

W hi PQ < ir^

W t^ W CQ W <; hi H EH CQ t^

< PQ X M <: Pi Pi H < rt: Pi s > <; w S > h P EH H W S EH EH

H IS P: IS Q H <: O IS Q P M w IS a Ui CU K CO fa CU Q fa O fa 2 Pi s p o O H U fa CM fa Pi rH 00 W

00 a \ fa <r> rH ^^ H 1 PH I H H O 00 EH 00 O^ t-1 C5 H P H

Pi

fa 1-1

H W

fa

u o w Pi

fa Pi < p o w Pi

ro CM

o I

00

o 00 o

ro o

00 x-\

o •

o

ro 1-i

o •

o

** r-i

o •

o

ro T-^

o •

o

o r-{ O

• o

00 r H O

• o

(N ro o

• o

VD 'sr O

• o

o i n o

• o

o r o

• o

IS

o H EH <: p a fa IS H

W fa t-1 CQ < H Pi < >

Pi

fa Hi P4 H E H hi

P

s

fa hi PQ < H

Pi

>

ro in rH CM

CM VD CM

ro >

O 00 VD CN 00 rH > > >

in crv o •

in ro CM

8

48

PQ

169

• o

468

• o 1

398

• o 1

702

• o

Pi

00 •

ro

fa hi PQ < b^

fa hi PQ

w fa

< hi fa EH

>H Pi (rf s s p w IS

PQ hi < PQ H < Pi H <: Pi > <

> fa ^ hQ IS EH H fa IS EH P fa Pi

o IS p <: H W W fa Pi o fa Pi

fa t ^ PH H EH h:i P S

fa IS P cu fa a fa P4 P fa P IS P Pi H H

CM ffi r H 00 EH 00 CTi CJ\ y-^ H 1

1 H O 00 00 a\ (T» T-i rH

fa hQ P4

s H W

fa o IS < K u o w Pi

fa Pi < p a w Pi

«

IS o H EH < P a fa

2; H

W fa hQ PQ < H PS < >

fa ^A Cu H EH hi P s

fa hi CQ < H Pi < >

1—1

in i H

• o

'^r o^ o

• o 1

00 CM 1-i

• o 1

T-i

in o

• o

CM CM O

CM O O

o o o

CN CN O

r-^ o

00 in o

o r^ o

r-{ in rH

• O

r^ rH CM

• O

CM ^ CN

• O

'5J< \D CM

• O

•«* \D r-i

•

430

o ro in K£> i n > >

00

>

49

CQ VD r-i o

• CM

a\ VD ro

• o

00 00 VD

• o

^ in in

• ^

CM CN CTi

•

-36

Pi

C3> •

ro

fa hi OQ < iri

fa hQ W PQ fa < h:i fa EH PQ h^

< CQ >< H <C Pi Pi H < < ^ S > < fa § > 1-1 P EH W IS EH

H EH

fa IS Pi IS P fa O Z P H fa 2 W CU fa CO fa PU fa P fa Pi IS p U H fa CM Pi TH 00

00 <y> fa 0^ rH ^A H 1 P< 1 H H O 00 EH 00 a\ nq cr. rH P -H S

< P O

E EH Pi P O fa

fa hQ CU S H in

fa o IS < ffi u a en Pi

fa « < p a w p;

Pi

z o H EH < P a fa

fa hi OA H EH h l p S

cn fa 1-3 CQ < H Pi < >

fa hi CQ < H Pi < >

VD 00 ro

VD o ro

in in CM

vo a\ «H

VD o rH

CN r^ ^ r-i o o

rH O O

o^ ^ rH

. o

cr> in CN

• o

rH O ro

. o

a\ rH ro

• o

r-i ro ro

• o

vo 00 ro

cr> o in

<j\ ^ in

in VD in

vo r-in

o t-\

00

V87

V20

V65

V16

V12

(Cons

50

CQ r -" r ro

• o

H 00 VO

• o

CM ^ ro

• CM

t ^ in r~

• o

'^ ro ro

• ro 1

CM ro VD

• T-i

ro

fa hi PQ < E H

fa 1-1 cn CQ fa < h^ ^ OQ

< >H H Pi Pi < <

>

IS fa p IS

p cn

IS O H fa cn P4 cn fa fa p Pi IS o H fa Pi CN

00

fa cr> i^ H

fa 1 ^ OQ < H

Pi

>

IS fa P IS fa P4 fa p

Cl4 H EH hi P

s

I T-i 00 cr>

cn EH O H Pi EH cn

hi o o ffi u

ro cn 00

I CN 00

hi

<

Pi

fa hQ

s H cn

fa

<

u a cn Pi

fa Pi < p a cn

Pi

Pi

IS

o H EH < P

a fa

^ H

cn fa hQ CQ < H Pi < >

fa hi Oi H EH h^ P S

fa (-1 CQ < H Pi < >

o o

ro 00 ro

vo

ro

CM vo ro

o CM

VD rH

O

o vo 1-i

• o

rH "* r-i

• O

r-in o

• o

rH rH O

• O

ro T-\

o •

o

CM r H O

• o

o vo

CN O ro

in ro ro

00 ro

o

o o ' d '

• o

cr» '^ in

• o

G^ cr> in

• o

a\ o vo

• o

o CM VO

• o

00 ro vo

• o

ro ^ 00

• in

in T-i

>

<Ti 00 >

r-00 >

in VD >

rr VD >

r>> CM >

g u

51

CQ ro rsi ro

• o

^ 00 ^

• o 1

CM i n ro

• o 1

00 ro ^

t

o

CM ^ ro

• ^

i n VD CM

• o 1

Pi

rH T-i

• ro

fa hi CQ < b^

fa hQ cn OQ fa < h i fa EH PQ h i

< PQ >H H < P^ Pi H << •< Pi S > < fa S > hi P EH H cn 3 EH EH

fa IS p; IS P fa < O IS P P H fa IS a cn p< fa cn fa Pn EH

fa p fa cn Pi IS P Pi O H H fa ro fa Pi CM 00

00 a\ fa CTi rH h i H 1 CU I CM H rH 00 EH 00 0^ h i C^ rH P H

s

fa hi Oi

s H cn

fa o s < ffi u a cn Pi

fa « < p a cn

Pi

Pi

IS o H EH < P a fa

IS H

cn fa (-1 CQ < H Pi < >

fa h l PH H EH hi P s

fa hQ CQ < H Pi < >

'cr * * T~<

• o

rH [ ^

o • o

1

CM " 5 ^

T-i •

O 1

CTt i n o

• o

00 VD o

• o

ro 00 o

• o 1

o (N O

CM o

ro T-i

o o

T-i

o o

o o

o rH

o o

o CN o

00 ^ o

T-i VD O

i n r-o

CN CN i-H

CM ro T-i

^ ^ x-i

9

O

<y> rH CM

• O

r--«* CN

• O

i n r-" CM

• o

o> * * ro

• o

ro vo ro

• o

i n ro vo

• 00 VD

§

00 o VD >

' ^ VD >

i n i n >

r CM >

CM VD >

-P CO G 0 U

52

PQ

.164

o

.726

CN

862

o

191

CN

118

o 1

340

o

501

rH

111

o 1

368

r-i

.916

CM 1

CM rH

t

ro

fa hi CQ < iri

fa hQ PQ

cn fa

< h i fa bi

>H Pi

P cn

PQ yA < PQ H < p; H < Pi > <: fa

> h i ^ H IS EH EH fa IS Pi

IS P fa <

o H cn cn fa « O fa P:

fa hQ P4 H ^ hQ p

s

IS P P fa S O PH fa fa PH P P fa IS 2 P O H U

ro fa CN 00 cn 0 0 <T> OS T-i rH 1

1 CN rH 00 CO CJ O^ T-i rH

IS

o H < P

o fa IS H

cn fa hQ OQ < H

Pi

>

fa hQ P4

H

cn

fa O IS < ffi u a cn Pi

fa Pi < p a cn

Pi

p;

fa h i P4 H EH hi P

fa h i CQ < H Pi < >

CM in

o CM o

T-i

o

VD

o

o o 00

o

00 CM VD O

ro

o cr> o

o I

o I

o I

ro

o

VD T-i

o

o

ro T-i

o

o

o T-i

o o

rH

o

o

o rH

o

o

T-i

o

o

in T-i

o

o

o

o

ro CM o

o ^ o

ro i n o

' 5 * '

VD O

^ r-o

r-00 o

r--cr> o

T-i

rH rH

I ^ CM rH

00 VD T-i

CN in T-i

o o CM

o ro CM

ro in CM

ro CM

in CN

CN rH ro o

ro ro

in ro

i n ro 00

• o CN

CM T-i

r^ CM i n ro > >

IT) >

vo 00 >

ro vo >

i n CM >

vo vo >

a\ CN >

r-CM >

§

53

PQ vo o ^

• o 1

<y\ in ^

• o 1

00 ro o • o 1

^ T-i

o • o

Pi

ro rH

• ro

fa hQ PQ < iri

fa 1-1 cn OQ fa < hQ fa EH CQ hQ

< CQ >i i-i f^ Pi tf H < <: Pi s > < s > w P EH hQ cn IS EH H

fa IS EH IS P fa Pi O IS P < H fa S P cn cu fa a cn fa P4 fa p fa p Pi IS p Pi O H H fa ro « Pi CM 00 EH

00 cr. fa Cr» rH 1-1 H 1 C^ 1 CM H rH 00 EH CO a> hQ <y> rH P H S

fa hi P4

s H cn

fa O S < ffi u o cn Pi

fa Pi < p a cn Pi

IS

o H < P a fa

Pi

fa hQ pu H EH hi P

cn fa hi CQ < H Pi < >

fa 1 ^ CQ < H Pi < >

00 VD CM

• O

^ 04 rH

• o 1

i n r^ rH

• o

CM o CM

• o

CN

o CM T-i

o o

o rH O

o

rH O

o

CM r-o

* * 00 o

* * <T\ o

00 o rH

CO VD CN

O

CM o ro

CM

ro

in in

CTi

CM

§

ro »H >

VD CO >

'^r (N >

O i n >

4J cn g p U

54

PQ

.850

o

.486

CM

.158

o 1

.549

00 1

423

ro

196

o 1

143

r^ ^

878

ro

070

vo 1

449

o 1

Pi

'sr T-i

. ro

fa hi PQ < EH

fa hi cn PQ fa < hQ fa EH CQ hQ

< PQ >i ^-^ < Pi Pi H < < Pi s > < w S > hQ P EH H cn IS EH EH

fa S Pi IS P fa < o 2: p P H fa IS O cn pu fa cn fa P ffi fa P fa EH « 21 p Pi O H P fa ro O Pi <N 00 fa

00 as fa CJ rH hQ «H 1 PH I CM H rH 00 EH 00 <r» ^q a* rH P H S

fa hQ Cm S H

cn

fa o z < K u a cn Pi

fa Pi < P a cn

Pi

Pi

IS o H ^ < P a fa

2: H

cn fa hi CQ < H Pi < >

fa hQ CU H b^ 1-1 P s

fa t J ffl < H p; < >

.503

o

.327

o

209

o 056

o 1

114

o

072

o

118

o

206

o

.129

o

.115

o

ro in CM

o o

ro

o TH

o o

o o

rH

o o

TH

o

o

ro rH

o

o

ro rH O

o o o

ro in CN

ro CN ro

vo vo ro

ro 00 ro

in as ro

as o 'd '

ro CM ^

VD ro »*

o in ' ^

T-i

vo ' ^

ro o in o

00 vo in

• o

in o vo

• o

as rH VO

• o

00 CN VO

• o

as ro vo

• o

o in VD

• o

o vo VD

• o

o r~> VD

• O

as r^ VD

• o

CM VU (M

•

063

§

as 00 >

,-i vo >

o VD >

CO rH >

CO vo >

r-CM >

o CO >

' ^ vo >

r-vo >

4J CO C u u

55

OQ ro 00 in • o

as 1-i CO • o

in

ro

fa hi CQ < E H

fa hi cn OQ fa <

P cn

o H

1 ^ CQ <

>H H Pi Pi < <

>

iri

fa P IS fa

cn cu cn fa

fa hQ CQ < cn H b^ Pi u

fa Pi

p IS

O H fa p; ro

00 fa as hQ tH PH I H CM EH CO hi as P H S

< >

EH IS fa P ^ fa Oi fa ffi P U

cn

CO as

H Pi iri cn H p hQ O o

I ro 00 as

hi hQ <

Pi

fa hi P4

s H cn

fa o IS < u

a cn Pi

fa p; < p o cn

Pi

Pi

r-rH in • o

ro vo CM • o

r vo CM • o

00 rH o • o

VD CM

VD 00 CN

IS o H B^ < P a fa IS H

cn fa hi OQ < H Pi < >

fa t - 1 Oi H ^ ( P s

fa hi CQ <: H Pi < >

r-

.51

o

as ro >

in ro in

ro vo a\

• in

CO >

CO

g

56

OQ VO VD ro • o

^ rH rH • o 1

CN VD ro •

rH 1

r cr> rf • o 'sr

ro as ro • o

fO CO VD • o 1

00 ro o • o 1

Pi

fa hQ

s H cn

ro vo ro as

vo o

ro o

'vt* o a\ o

o I

o I

o I

o I

vo

ro

fa O IS < U

a cn Pi

vo CM o • o

r-rH O •

O

o I-I o • o

rH rH O • o

CM rH o • o

rH T-i

o • o

o rH O • o

fa hi OQ < ti

fa Pi < P a cn Pi

vo CM O

^ •cy O

"^ in o

in vo o

r-r-o

as 00 o

as as o

IS

o H < P

a fa

Pi

fa hQ

H

P

ro VD rH

• o

as o CM

CM ro CM

vo i n CN

as

rsi

00 a\ CM

i n rH

ro o

vo

00

CN

2: H

cn fa hQ CQ < H Pi < >

fa

OQ < H

Pi

>

00 i n >

VD CM

g g 5 00 ro >

CM T-i >

00 >

-P CO

57

OQ rH * * CM

• O

rH T-i rH

• o

VD CM O

• o 1

ro

fa hi OQ <

fa hi cn OQ fa < hi

OQ <

>H H p; Pi <

s p cn

IS

o

>

iri IS fa P IS

H fa cn Oi cn fa fa p

fa hQ OQ < H Pi < fa > hi

IS H

Pi o fa Pi ro

CO fa as h:i H P4 I H CN EH 00

Pi < p a p 2: o u

^ fa 00 cn

T-i I

ro 00 as

EH

fa P IS fa Oi fa p

hi p

cr>

2 O H EH < P a fa

Pi

fa hi

PH

H

cn

fa o

u a cn Pi

fa Pi < p a cn

Pi

Pi

fa 1 ^ p^ H

hQ P S

cn fa (^ OQ <: H Pi < >

fa hi 03 < H Pi < >

cr> o

o a\ o o

vo rH O o

ro T-i

o o

o o

VD CN O

as ro o

<T> ro rH

CM VD

as ro

ro

CM o as

• ro CM

g

CN ' ^ in >

in ro >

4-> CO

c P U

58

PQ CM 00 CO • o

^ r vo • CM 1

ro vo CO • o 1

ro o .H •

O

ro '* ro • o

r-r CM • o 1

Pi

CO

ro

fa hQ PQ <

fa h i cn CQ fa

hQ CQ <

X H

Pi Pi

> p cn

IS o

IS fa p

fa cn P cn fa fa P Pi ^ o H fa Pi ro

00 fa as hQ H PLI I H CM EH 00 h i as P H

fa h : | OQ < H Pi < >

p

fa hi

EH IS EH fa (^

< P

fa O Oi fa p p Pi

H

00 EH as T-i I

ro 00 as

cn

fa O IS <

u

a cn Pi

fa Pi < p a cn

fa t ^ CU s

'r in 1-i

• o

ro rH 1-H

O 1

'r a\ o

t o 1

^ in T-i

• o

** as o • o

ro ^ o • o 1

Pi

IS o H ^ < P a fa s H

cn fa hi CQ < H Pi < >

fa hi 0* H EH ^A P S

fa iJ CQ < H Pi < >

ro CN o CN

o

ro rH O O

rH O

O

CM rH

o

o

o T-i

o o

ro rsi o

in ^ o

00 in o

vo r o

CO CO o

a\ as o

'r in T-i

• o

CM T-i CM •

O

CM ^ CN •

O

r>-r CN • o

CO as CN • o

in rH ro • o

o CN 'a* •

542