An Introduction to Cost Terms ,cost classification and Purposes © 2009 Pearson Prentice Hall. All rights reserved.

An Introduction to Cost Terms,cost classification and Purposes © 2009 Pearson Prentice Hall. All rights reserved.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

An Introduction to Cost Terms ,cost classification and Purposes

© 2009 Pearson Prentice Hall. All rights reserved.

© 2009 Pearson Prentice Hall. All rights reserved.

What is cost?All businesses have costs. A cost is any spending on goods and services for the business. Or

'the resources consumed or used up to achieve a certain objective' or

Cost – sacrificed resource to achieve a specific objective or

A cost is incurred when a firm uses a resource for some purpose.

© 2009 Pearson Prentice Hall. All rights reserved.

Basic Cost TerminologyActual cost – a cost that has occurred

Budgeted cost – a predicted cost

Cost object – anything of interest for which a cost is desired

A cost object is any product, service, customer, activity, or organizational unit to which costs are assigned for some management purpose

© 2009 Pearson Prentice Hall. All rights reserved.4

Costs are assembled into meaningful groups called cost pools (e.g., by type of cost or source)

Any factor that has the effect of changing the level of total cost is called a cost driver

Basic Definitions

© 2009 Pearson Prentice Hall. All rights reserved.5

There are four main ways to classify costs (“different costs for different purposes”):

For product and service costing (GAAP) For strategic decision-making (cost-driver

analysis)For planning and decision-making For control/feedback

Cost Concepts: Overview

© 2009 Pearson Prentice Hall. All rights reserved.

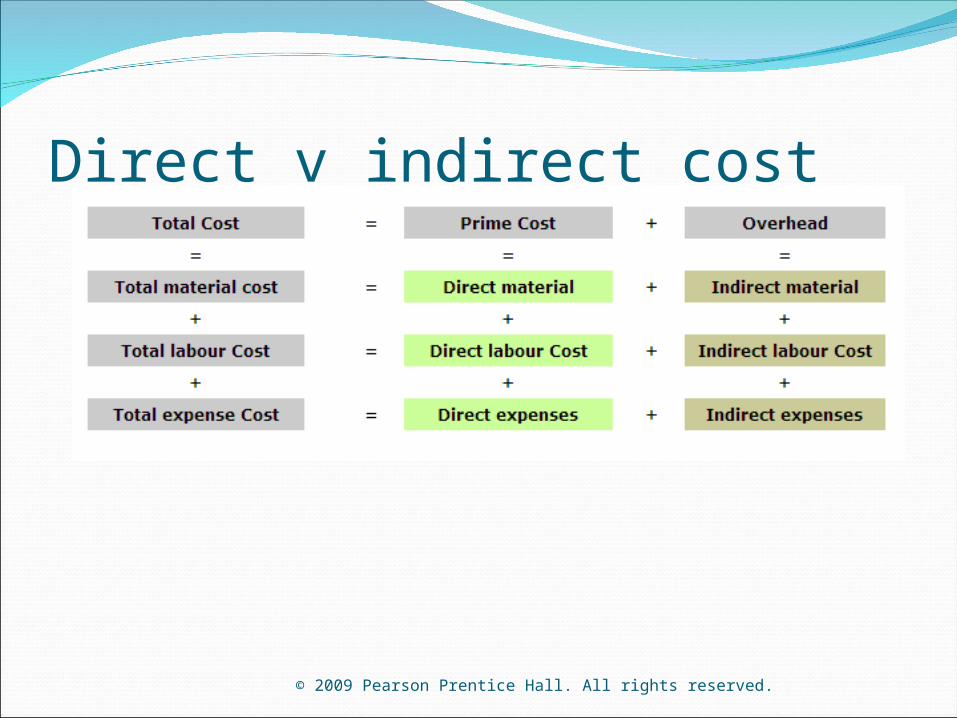

Direct cost‘expenditure that can be attributed to a

specific cost unit’ CIMA Official Terminology

© 2009 Pearson Prentice Hall. All rights reserved.

Indirect cost‘expenditure on labour, materials or

services that cannot be economically identified with a specific saleable cost

unit’. CIMA Official Terminology

© 2009 Pearson Prentice Hall. All rights reserved.8

The process of assigning costs to cost pools or from cost pools to cost objectsDirect costs can be conveniently and

economically traced to a cost pool or a cost object

Indirect costs cannot be traced conveniently or economically to a cost pool or a cost object

Because indirect costs cannot be traced, assignment is made through the use of cost drivers (cost allocation)

These cost drivers are often called allocation bases

Product/Service Costing: Cost Assignment

© 2009 Pearson Prentice Hall. All rights reserved.9

Cost Assignment: General Principles

Costs

Electric Motor

Materials Handling

Supervision

PackingMaterials

Cost Pools

AssemblyAssembly

PackingPacking

Cost Objects

Dishwasher

Washing Machine

FinalInspection

Cost Drivers and Cost Assignment

© 2009 Pearson Prentice Hall. All rights reserved.

Period CostPeriod costs are not manufacturing cost. However,

they are incurred and paid based on the periodThey are deductible from revenue.Example: Rent, salaries, telephone etc.

© 2009 Pearson Prentice Hall. All rights reserved.

Product CostsProduct costs are manufacturing costs They are incurred for the manufacturing of goodsThey include direct material, direct labour, and

manufacturing overheads. Example: direct material, labour cost,

manufacturing overhead etc.

© 2009 Pearson Prentice Hall. All rights reserved.12

Product costs include only the costs necessary to complete the product at the manufacturing step in the value chain (manufacturing) or to purchase and transport the product to the location of sale (merchandising)

Period costs include all other costs incurred by the firm in managing or selling the product (indirect costs outside the manufacturing step of the value chain)

Product and Service Costing Concepts (GAAP)

© 2009 Pearson Prentice Hall. All rights reserved.

Types of Manufacturing InventoriesDirect Materials – resources in-stock and

available for use

Work-in-Process (or progress) – products started but not yet completed. Often abbreviated as WIP

Finished Goods – products completed and ready for sale

© 2009 Pearson Prentice Hall. All rights reserved.14

Direct material costs = cost of materials that can be readily traced to outputs = purchase price of materials + freight – purchase discounts + reasonable allowance for scrap and defective units

Indirect material costs = cost of materials that cannot readily be traced to outputs (e.g., lubricants, and small tools)

Direct labor costs = labor that can be readily traced to outputs = wages paid plus a reasonable allowance for nonproductive time

Indirect labor costs = labor costs that cannot be readily traced to outputs (i.e., they are manufacturing support costs)

Direct and Indirect Product Costs for a Manufacturer

© 2009 Pearson Prentice Hall. All rights reserved.15

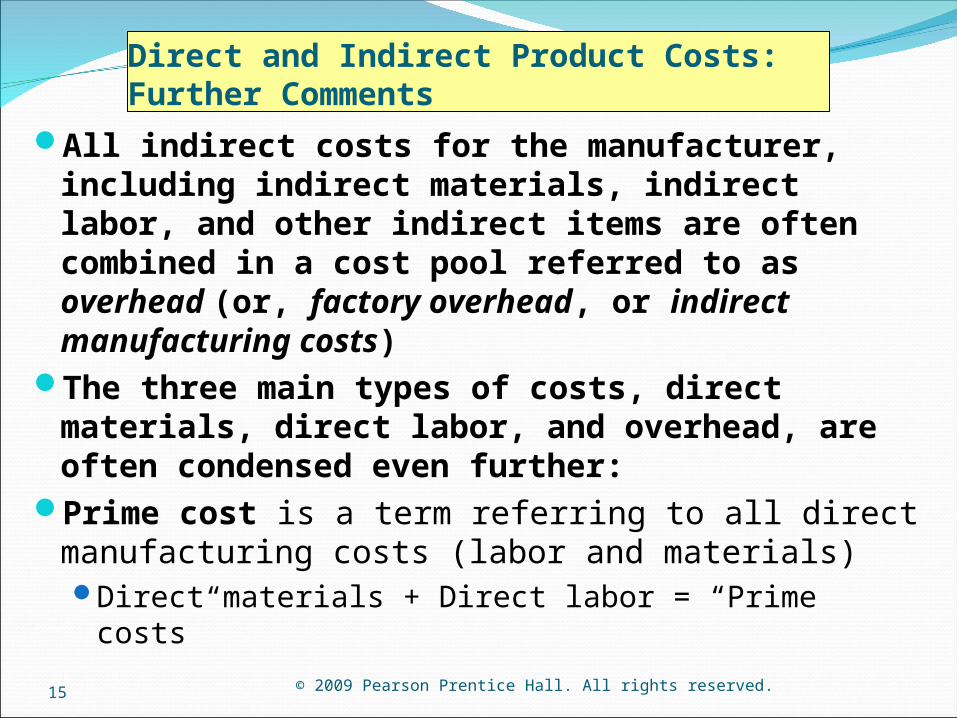

All indirect costs for the manufacturer, including indirect materials, indirect labor, and other indirect items are often combined in a cost pool referred to as overhead (or, factory overhead, or indirect manufacturing costs)

The three main types of costs, direct materials, direct labor, and overhead, are often condensed even further:

Prime cost is a term referring to all direct manufacturing costs (labor and materials)Direct materials + Direct labor = “Prime costs”

Direct and Indirect Product Costs: Further Comments

© 2009 Pearson Prentice Hall. All rights reserved.

Other Cost Considerations

Direct labor + Overhead = “Conversion costs”

Conversion cost is a term referring to direct labor and factory overhead costs, collectively or

cost of converting raw material to finished goods = Production cost- direct material.

Conversion cost which converts the direct material into finished goods

© 2009 Pearson Prentice Hall. All rights reserved.

Classifying costs by element

© 2009 Pearson Prentice Hall. All rights reserved.18

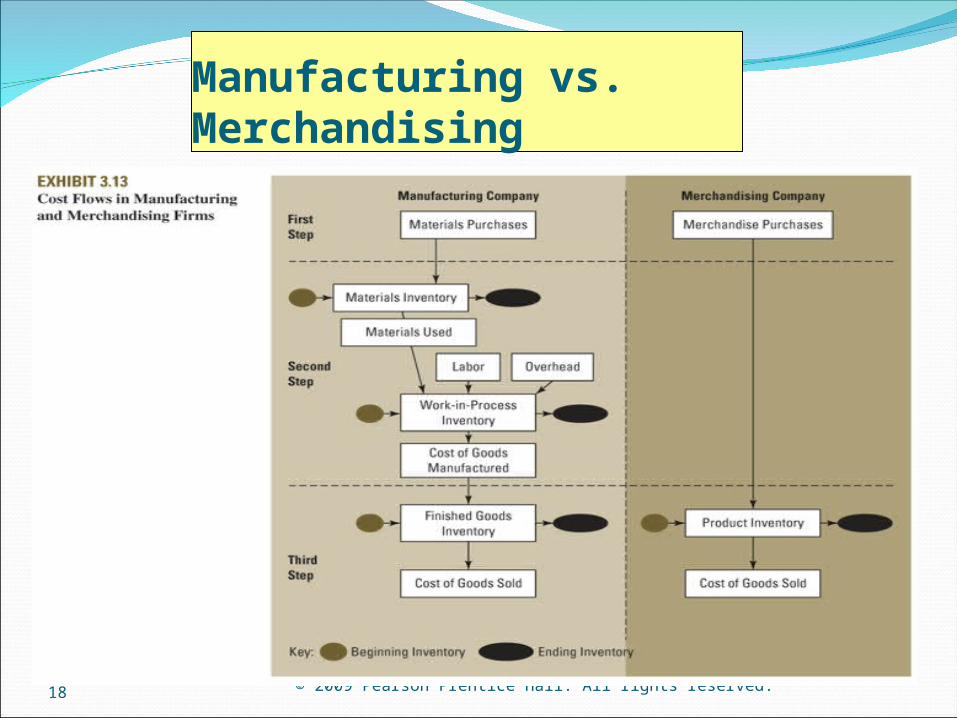

Manufacturing vs. Merchandising

© 2009 Pearson Prentice Hall. All rights reserved.

Direct v indirect cost

© 2009 Pearson Prentice Hall. All rights reserved.20

Costs for Strategic Decision-Making

Inventory valuation (GAAP) vs. strategic costing?

Cost drivers provide two roles for the management accountantAssigning costs to cost objectsExplaining cost behavior, i.e., how total cost

changes as the cost driver changesThere are four types of cost drivers:

Activity-basedVolume-basedStructuralExecutional

© 2009 Pearson Prentice Hall. All rights reserved.21

Cost Drivers

Activity-based cost (ABC) drivers are developed at a detailed level of operations using activity analysis–a cost driver is determined for each activity

Volume-based cost drivers relate to the amount produced or quantity of service provided: The relationship between the cost driver and

total cost is approximately linear within the relevant range

© 2009 Pearson Prentice Hall. All rights reserved.22

Structural cost drivers facilitate strategic decision making because they involve plans and decisions that have long-term effectsScale, experience, technology, and complexity are

considered in hopes of improving competitive position

Executional cost drivers facilitate operational decision making by focusing on short-term effectsWorkforce involvement, design of the production

process, and supplier relationships are considered in an attempt to reduce costs

Cost Drivers (continued)

© 2009 Pearson Prentice Hall. All rights reserved.

Cost classification by behaviour'the way in which cost per unit of output is

affected by fluctuations in the level of activity'.

Variable costFixed cost

© 2009 Pearson Prentice Hall. All rights reserved.

Factors Affecting Direct / Indirect Cost ClassificationCost MaterialityAvailability of information-gathering

technologyOperational Design

© 2009 Pearson Prentice Hall. All rights reserved.25

Cost Information for Short-term Planning: Classification by Behavior

What is meant by “cost behavior”?Common classifications of cost behavior:

Fixed (capacity) cost is the portion of total cost that does not change with changes in output

Variable cost is the change in total cost associated with each change in quantity of the cost driver

Mixed cost is used to refer to a total cost figure that includes both a fixed and variable component

Step costs vary with the cost driver but do so in steps

Applications:BudgetingCost-Volume-Profit analysis (profit planning)

© 2009 Pearson Prentice Hall. All rights reserved.26

Fixed Costs

$6,600

$6,500

$3,000

3,500 3,600Units of the Cost Driver

Total Cost

Total Fixed Cost

© 2009 Pearson Prentice Hall. All rights reserved.27

Variable Costs

Total Variable Cost

$6,600

$6,500

$3,000

Units of the Cost Driver

Total Cost Total CostTotal Cost

3,500 3,600

© 2009 Pearson Prentice Hall. All rights reserved.28

Relevance is the most important characteristic for information used in decision makingRelevant costs have two properties: they differ for

each decision option and they will be incurred in the future

Opportunity cost is the benefit lost when choosing one option precludes receiving the benefits from the alternative option

Sunk costs are costs that have been incurred or committed in the past and are therefore irrelevant in current decision making

Short-Run Decision-Making Cost Concepts

© 2009 Pearson Prentice Hall. All rights reserved.29

There are three other characteristics that are important for planning and decision making

Accuracy (and the need to monitor internal accounting controls)

Cost and value of cost information (the cost of information should be monitored by the management accountant to ensure that costs do not outweigh the associated benefits)

Timeliness (often involves sacrificing in the other two areas)

Qualitative Characteristics of Cost Information for Planning

and Decision-Making

© 2009 Pearson Prentice Hall. All rights reserved.30

Controllability is a basic consideration in evaluating managers and providing feedbackA cost is considered “controllable” if the

manager or employee has discretion in choosing to incur it or can influence the amount in a short period of time

The controllability of some costs is subject to debate, for example, changes in interest rates, foreign exchange fluctuations, or changes in state or local taxes; should the manager be responsible for these changes?

Cost Information for Control/Feedback Purposes

© 2009 Pearson Prentice Hall. All rights reserved.31

There are different ways to classify (or categorize) cost information, depending on the information needs of management (“different costs for different purposes”):To prepare financial statements (GAAP)For strategic decision-makingFor short-term planningFor short-term decision-makingFor control/feedback purposes

Product and service costing (GAAP) focuses on differentiating product costs from period costs

Costs flow through three inventory accounts in a manufacturing firm; merchandising firms have one inventory account

Chapter Summary

© 2009 Pearson Prentice Hall. All rights reserved.32

Chapter Summary (continued)

• For strategic decision-making, we think about costs in terms of the following types of drivers: activity-based, volume-based, structural, and executional

• Cost concepts used in short-term planning relate to the behavior of costs (i.e., how they change in response to one or more activities)

• For decision-making we generally classify costs into one of the following categories: relevant, opportunity, or sunk– Relevance, accuracy, timeliness, and value that exceeds cost

are important information characteristics

• Controllability and risk preferences must be assessed when using cost information for management and operational control

© 2009 Pearson Prentice Hall. All rights reserved.

Different Types of FirmsManufacturing-sector companies – create and

sell their own productsMerchandising-sector companies – product

resellersService-sector companies – provide services

(intangible products)

© 2009 Pearson Prentice Hall. All rights reserved.

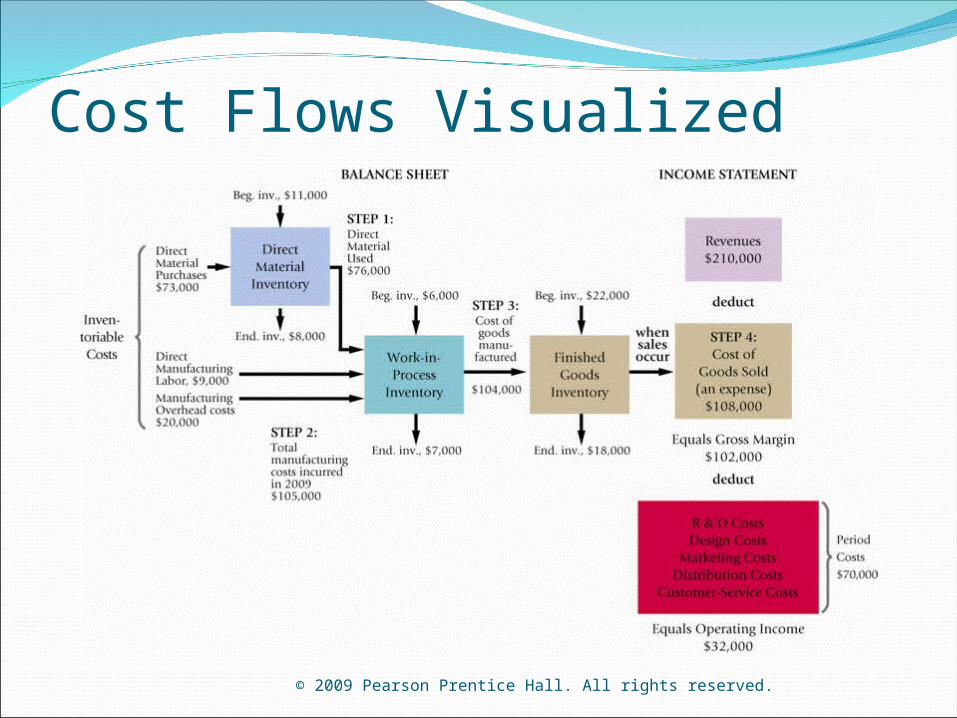

Cost FlowsThe Cost of Goods Manufactured and the

Cost of Goods Sold section of the Income Statement are accounting representations of the actual flow of costs through a production system.

Note the importance of inventory accounts in the following accounting reports, and in the cost flow chart

© 2009 Pearson Prentice Hall. All rights reserved.

Cost FlowsDemonstrate how costs flow through the formal accounting system?

© 2009 Pearson Prentice Hall. All rights reserved.

Cost Flows Visualized

© 2009 Pearson Prentice Hall. All rights reserved.

Cost of Goods Manufactured

© 2009 Pearson Prentice Hall. All rights reserved.

Multiple-Step Income Statement

© 2009 Pearson Prentice Hall. All rights reserved.

Opportunity CostNot recordable in the books of account but are

considered in every decisions of managers.It is the amount of benefit that is sacrificed

when one alternative is selected.

© 2009 Pearson Prentice Hall. All rights reserved.

The economic problemThe basic economic problem is the scarcity of

social resources to satisfy human wants and needs.

An economic system must make choices about the allocation of resources among the many possible uses.

The economic system also chooses how the goods and services are distributed -- who gets what.

© 2009 Pearson Prentice Hall. All rights reserved.

Cost and the necessity of choice, even in health care

When a high percentage of all spending in our economy is for health care, we wonder if some of the resources going into health care could be better used elsewhere, as

other kinds of health care, that might give more benefit for the same resources

other kinds of health-enhancing investments besides health care, such as education

consumption goods and services that might enhance our lives more than spending on certain kinds of health care would,

or as investments outside of health care that might improve our future ability to produce goods and services more than some investments in health do.

© 2009 Pearson Prentice Hall. All rights reserved.

Opportunity cost Opportunity cost is the most fundamental

cost concept. The opportunity cost of doing or getting

something is: what you could have done or gotten instead

© 2009 Pearson Prentice Hall. All rights reserved.

Opportunity cost is what you forgo.Example: The opportunity cost of buying a

box of Cracklin Oat Bran is one-and-a half boxes of Wheat Chex, if that's your second favorite cereal.

© 2009 Pearson Prentice Hall. All rights reserved.

Opportunity cost is what you forgo.Example: Your opportunity cost for taking

this class includes: Whatever else you could have bought with

your tuition and fee moneyplus

the work, family participation, and recreation that you are not doing because you are here.

© 2009 Pearson Prentice Hall. All rights reserved.

Opportunity cost is not resources usedStrictly speaking, the cost of something is not

the resources used up to get it. Instead, the cost is what else you could have

done with those resources. Resources have value only because you can

use them to make goods and services that have value.

© 2009 Pearson Prentice Hall. All rights reserved.

Sunk costsCosts are the cost incurred a result of past

decisions.Cost can not be changed by taking operating

decisionSunk costs are irrelevant from decision making.Sunk costs are depreciation of assets, lease rent

etc.

Related Documents