© Bates Wells & Braithwaite 2008 Tom Pratt & Tessa Gregory Monday 23 June 2008 An Introduction to Charity Law

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Bates Wells & Braithwaite 2008

Tom Pratt & Tessa Gregory

Monday 23 June 2008

An Introduction to Charity Law

© Bates Wells & Braithwaite 2008

An Introduction to Charity Law

Main features of charitable statusCharities Act 2006Legal forms for charitiesRegistration process

© Bates Wells & Braithwaite 2008

PART I: What is a charity?

An organisation established for purposes which are regarded as exclusively charitable under the law of England and Wales.

Various legal forms available.

A status not a legal form.

© Bates Wells & Braithwaite 2008

What are the main features of charitable status?

registration with the Charity Commissionregulation by the Charity Commissiontax breaksfiduciary duties for trusteesrestrictions on trustee benefitsother restrictions e.g. trading, campaigning

© Bates Wells & Braithwaite 2008

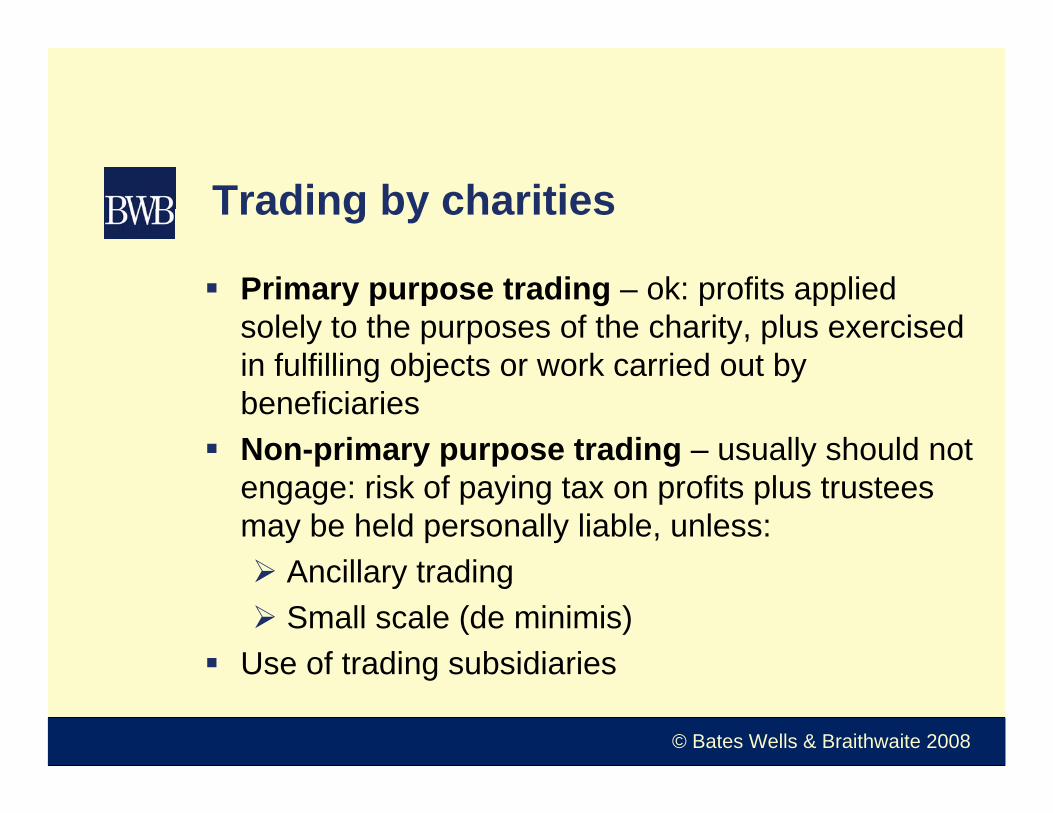

Trading by charities

Primary purpose trading – ok: profits applied solely to the purposes of the charity, plus exercised in fulfilling objects or work carried out by beneficiariesNon-primary purpose trading – usually should not engage: risk of paying tax on profits plus trustees may be held personally liable, unless:

Ancillary tradingSmall scale (de minimis)

Use of trading subsidiaries

© Bates Wells & Braithwaite 2008

PART II: Charities Act 2006

Royal Assent in November 2006Phased implementation in 2007/8Not a stand alone piece of legislation -amendments to Charities Acts 1992 and 1993Govt has committed to produce a consolidated Act in 2007/2008 session of Parliament

© Bates Wells & Braithwaite 2008

Charities Act 2006: Key changes

Statutory definition of charitable purposesRemoval of presumption of public benefit

© Bates Wells & Braithwaite 2008

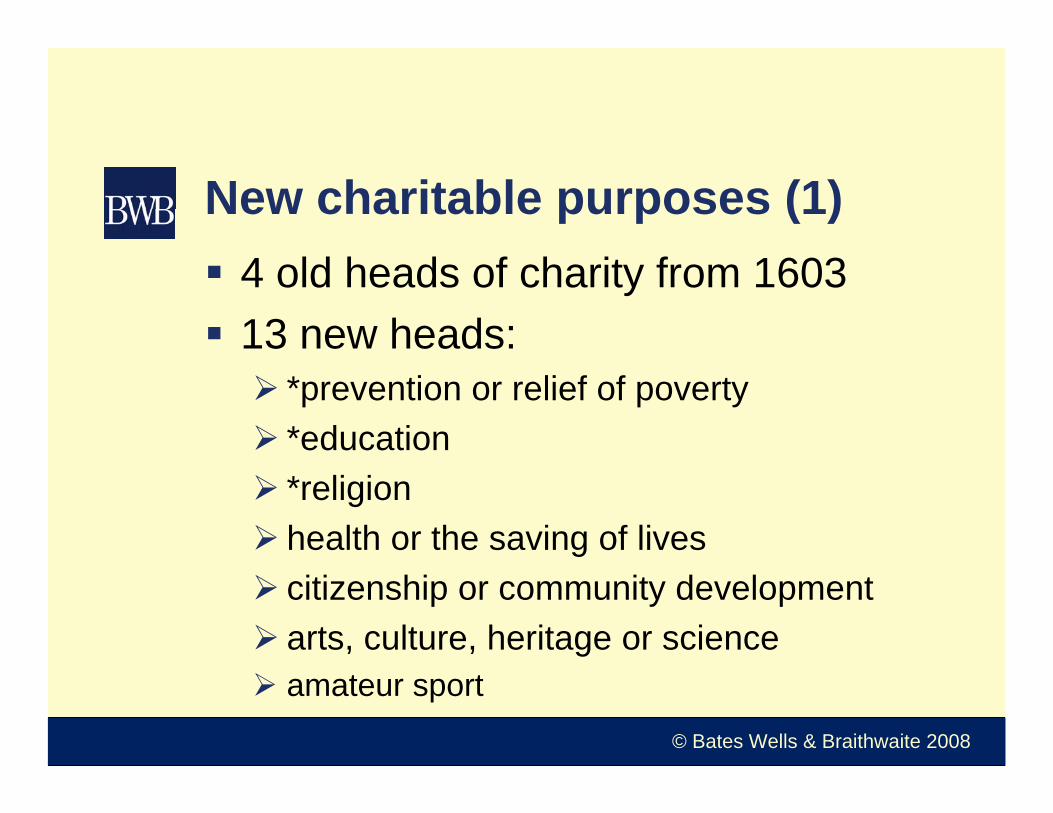

New charitable purposes (1)4 old heads of charity from 160313 new heads:

*prevention or relief of poverty*education*religionhealth or the saving of livescitizenship or community development arts, culture, heritage or scienceamateur sport

© Bates Wells & Braithwaite 2008

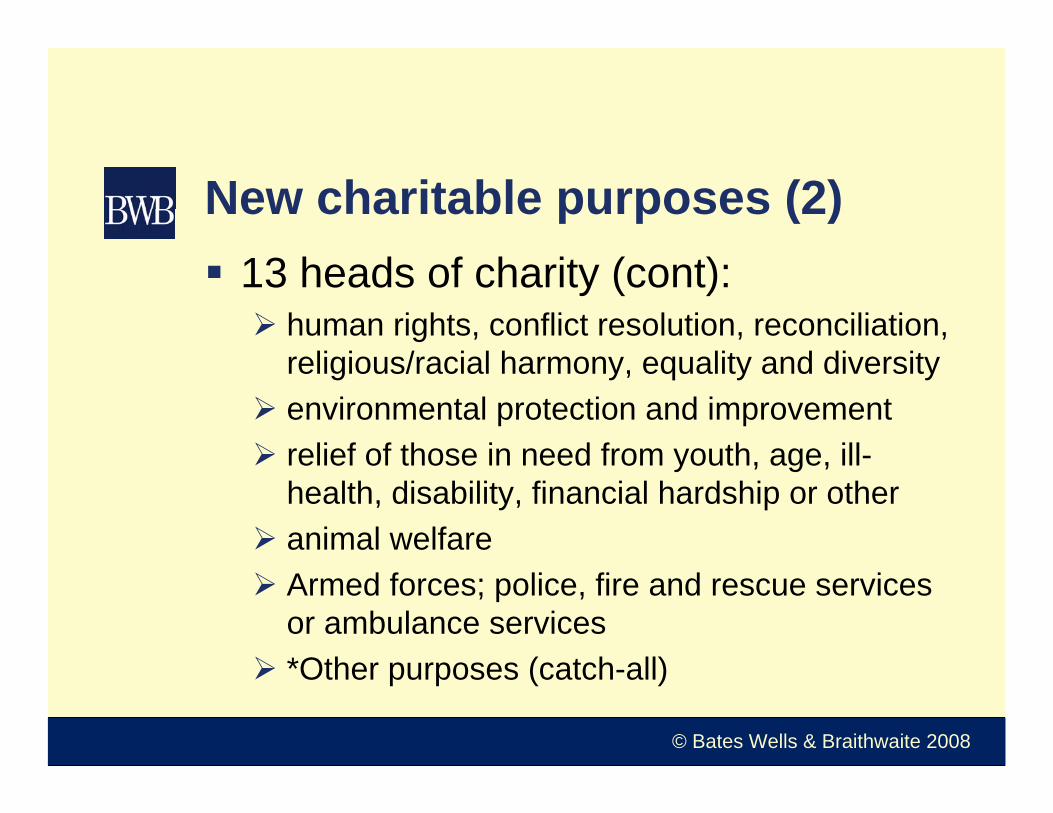

New charitable purposes (2)13 heads of charity (cont):

human rights, conflict resolution, reconciliation, religious/racial harmony, equality and diversityenvironmental protection and improvementrelief of those in need from youth, age, ill-health, disability, financial hardship or otheranimal welfare Armed forces; police, fire and rescue services or ambulance services*Other purposes (catch-all)

© Bates Wells & Braithwaite 2008

Public Benefit – What’s changed?

All charities will need to demonstrate that their purposes are for public benefitEnd of the presumption that religious, education and poverty charities are for the public benefitCharity Commission has published general guidance and is consulting on sub-sector guidance

© Bates Wells & Braithwaite 2008

Public Benefit - cont

Charity Trustees must “have regard to” the guidanceNew requirement to included statement of public benefit in annual report – threshold distinctionNo change in law – charities have always had to be for the public benefitMeaning of “public benefit” not defined

© Bates Wells & Braithwaite 2008

The Two Principles of Public Benefit

Principle 1There must be an identifiable benefit or benefits:

It must be clear what the benefits areThe benefit must be related to the aimsBenefits must be balanced against any detriment or harm

© Bates Wells & Braithwaite 2008

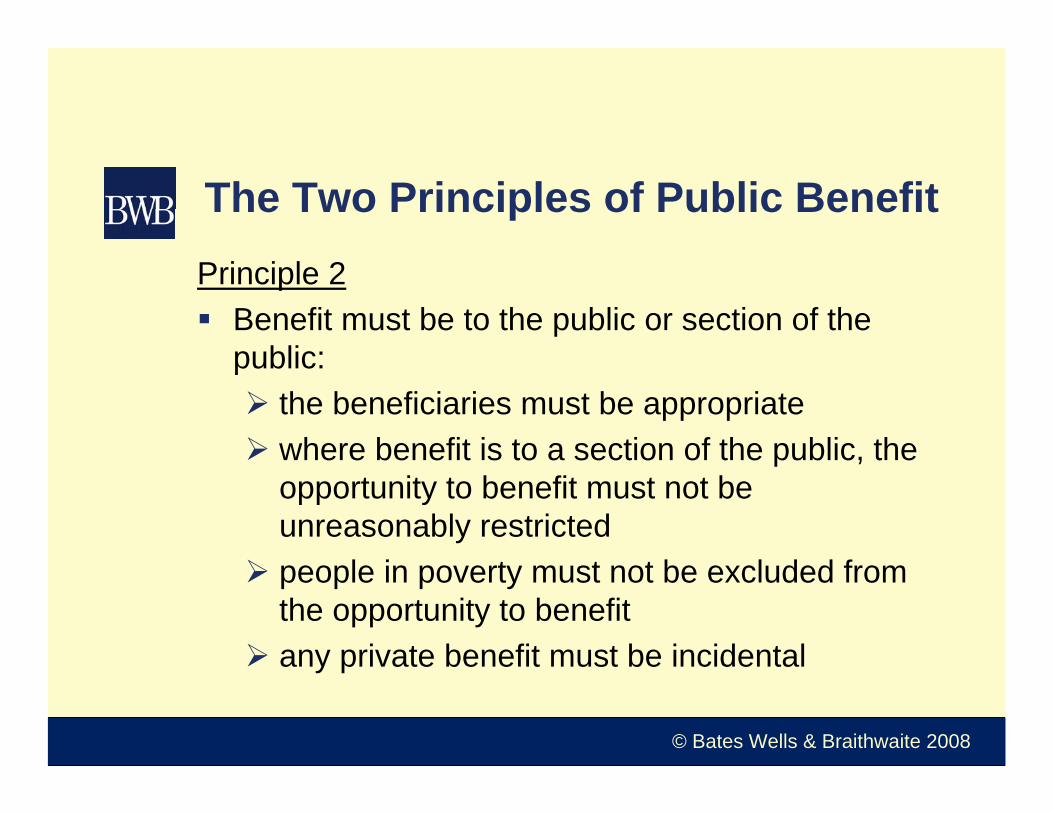

The Two Principles of Public BenefitPrinciple 2

Benefit must be to the public or section of the public:

the beneficiaries must be appropriatewhere benefit is to a section of the public, the opportunity to benefit must not be unreasonably restrictedpeople in poverty must not be excluded from the opportunity to benefitany private benefit must be incidental

© Bates Wells & Braithwaite 2008

Thorny issue of fee-charging

The Concordat PrinciplesServices mainly on a fee-charging basis can be for the public benefitRelieving the public purse is not itself sufficientDirect and indirect benefits may be taken into accountAn organisation which wholly excluded poor people from direct or indirect benefit would not operate for the public benefitTokenism not an adequate response

© Bates Wells & Braithwaite 2008

Practical implications for Charities

Must demonstrate public benefit – internal audit recommendedSpecific duty to have regard to the guidanceDecision making still rests with TrusteesCharities will not be expected to make changes overnight – Commission should work with charityActive accountabilitySignificant issue arises if “indirect benefits” are outside of the objects

© Bates Wells & Braithwaite 2008

Charities Act 2006: other important changes (1)

New look Charity Commission Powers

variousmortgages of land, Cy-pres, publicity requirements for schemes

Charity Tribunal

© Bates Wells & Braithwaite 2008

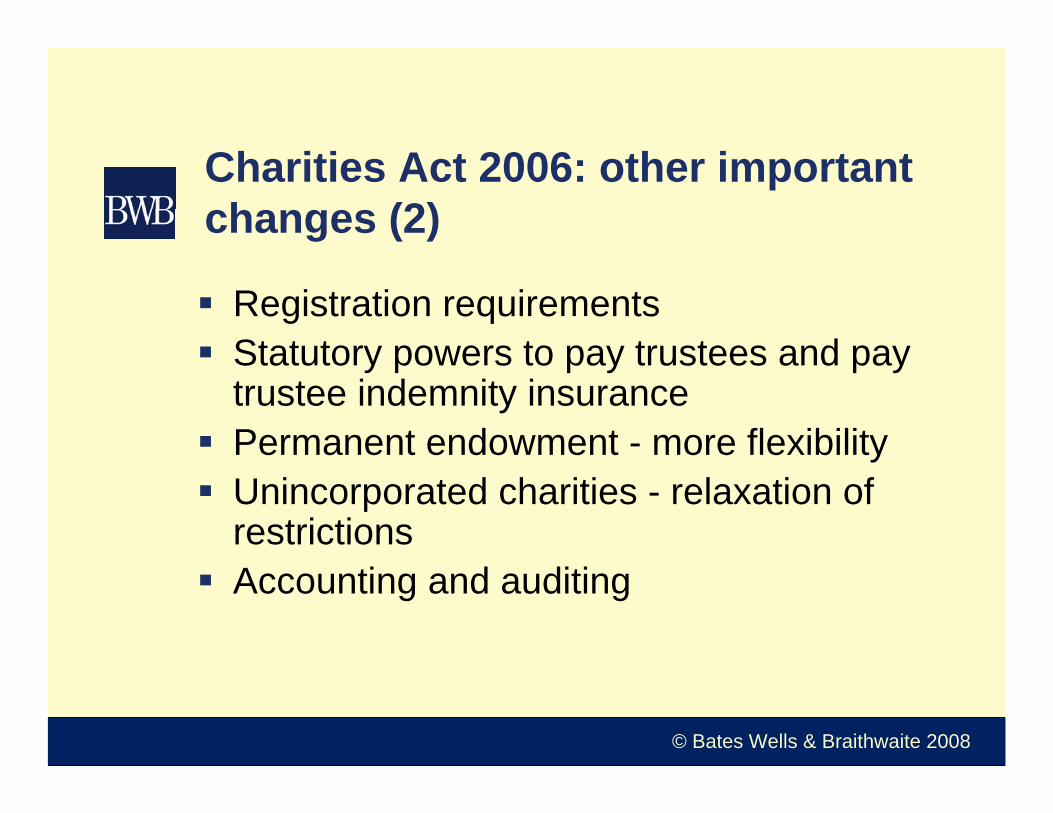

Charities Act 2006: other important changes (2)

Registration requirementsStatutory powers to pay trustees and pay trustee indemnity insurancePermanent endowment - more flexibilityUnincorporated charities - relaxation of restrictionsAccounting and auditing

© Bates Wells & Braithwaite 2008

Charities Act 2006: other important changes (3)

Changes to fundraising rulesCommercial participators, professional fundraisersPublic charitable collections

Mergers – new frameworkCharitable incorporated organisation (CIO)

© Bates Wells & Braithwaite 2008

PART III: Legal Forms for charitiesCompaniesIndustrial and Provident Societies (IPS)TrustsUnincorporated AssociationsRoyal Charter BodiesCharitable Incorporated Organisations (CIO) Also: Community Interest Companies (CIC), Limited Liability Partnerships (LLP)

© Bates Wells & Braithwaite 2008

Companies

Limited by shares or guaranteeSeparate corporate legal entityDirectors and members (shareholders)Regulated by Companies HouseMemorandum and Articles of AssociationExamples

© Bates Wells & Braithwaite 2008

Reasons for Incorporation

Legal personalityLimitation of riskClear ownership structure/governanceAccountability/disclosureFinance – recognition and equityCan enter into contracts, own or lease property and employ staff in its own name

© Bates Wells & Braithwaite 2008

Industrial and Provident Societies

An organisation conducting an industry, business or trade and registered under Industrial and Provident Societies Act 1965 either as a:

Co-operativeFor the benefit of the community

FSA is the registering authorityMembersRules‘Exempt’ if set up for charitable purposes

© Bates Wells & Braithwaite 2008

Trusts

TrusteesCannot own land or sign documents in its own name – appoint holding or custodian trusteesTrust DeedExamples: small organisations, no membership, grant-making bodies etc.

© Bates Wells & Braithwaite 2008

Unincorporated Associations

Executive or Management CommitteeUnincorporated – no limited liability or legal personality of its ownCannot own property in its own name –appoint holding or custodian trusteesConstitution or RulesExamples: small organisations, local branches, membership organisations etc.

© Bates Wells & Braithwaite 2008

Limited Liability Partnerships (LLPs)

Legal personality and limited liabilityRegistered at Companies HouseTransparent for tax purposes – joint venturesCannot be a charity

© Bates Wells & Braithwaite 2008

Community Interest Companies (1)

Rise of the social enterpreneurOver 1,500 registered Memorandum and Articles of AssociationLimited by shares or guaranteeRegulated by Companies House and CIC RegulatorExamples

© Bates Wells & Braithwaite 2008

Community Interest Companies (2)

Tailored for social enterpriseAsset lockCommunity interest testControl“light touch” RegulatorPayment of directors, dividends (CLS)Equity financeRecognised form (CLS/CLG)

© Bates Wells & Braithwaite 2008

Charitable Incorporated Organisations (CIOs)

New legal form for charities introduced by Charities Act 2006CIO will give charities benefits of incorporation (limited liability and legal personality) with a single regulator –Charity CommissionNew charities should be able to set up as CIO’s from early 2008

© Bates Wells & Braithwaite 2008

Advantages of a CIO

Single registration with Charity Commission and 1 annual returnLess onerous accounting and reporting requirementsLower costsCodified duties for trustees and membersMore straightforward arrangements for mergers and reconstructions

© Bates Wells & Braithwaite 2008

Key features of CIOs

A body corporate with a constitution that states name and purposePrincipal office in England or WalesTrustees and one or more membersMembers not liable to contribute to assets of CIO on winding up or have limited liabilityConstitution to include certain provisions

© Bates Wells & Braithwaite 2008

Registration of a CIORegistration will be by application to the Charity Commission w/ copy of proposed constitution and any other prescribed documentation or informationApplications may be refusedCIO is then entered in register of charities and becomes a body corporateCIO’s entry in register will include date of registration and that it is constituted as a CIO

© Bates Wells & Braithwaite 2008

Running a CIO

Codified duties for trustees and membersAmending constitution – resolution passed by 75% majority of those voting at a general meeting or unanimously if not passed at a general meetingCIO may not amend its constitution in ways where it would cease to be a charityResolution making ‘regulated alterations’ need prior written consent of Charity Commission.

© Bates Wells & Braithwaite 2008

Conversion to CIO

Charitable companies and IPSs – charity will need to pass resolution to become a CIO and adopt new constitutionUnincorporated charities – charity will need to register a new CIO and then transfer its property to the CIO before winding up the unincorporated charity (note TUPE applies)

© Bates Wells & Braithwaite 2008

Analysis and warning points

A ‘significant deregulatory measure’ ?Large parts of company and insolvency law incorporated by reference.Not clear how disclosure requirements will compare with those for a CLGAmending constitution is complicatedMergers

© Bates Wells & Braithwaite 2008

Comparing Alternatives - companies

Generally unrestricted (market rates should satisfy CIC test)

YesNo – but watch this space

NoCompanies House and CIC Regulator

Community interest company

UnrestrictedNoNoNoCompanies House

Company

RestrictedYesYesYesCharity Commission

Charitable incorporated organisation (from 2008)

RestrictedYesYesYesCharity Commission & Companies House

Charitable company

Remuneration of trustees/directors

Lock on assetsTax breaksCharitable Status

RegulatorStructure

© Bates Wells & Braithwaite 2008

PART IV: The Registration Process

Establishing the charityDeciding on the form and structure

Incorporated or unincorporatedMembershipAppointment of trusteesInvolvement of stakeholders/funders

Names – some limitations

© Bates Wells & Braithwaite 2008

The Registration Process

Governing documentApplication formTrustee DeclarationsSupporting informationCovering letter

© Bates Wells & Braithwaite 2008

Governing document

Standard considerationObjects clause – examples, registerOligarchy vs. MembershipAppointment and removal of Trustees

© Bates Wells & Braithwaite 2008

Application form

Tick-boxObjects and activitiesEvidence of incomeCRB checksPrivate benefit

© Bates Wells & Braithwaite 2008

Trustee Declaration

Consent to become a trusteeOriginalsIntroduction to trustee responsibilities

© Bates Wells & Braithwaite 2008

Supporting information

Business planPromotional materialsConsistencyWebsite

© Bates Wells & Braithwaite 2008

Covering letter

Pre-exempt concernsExpedite application

© Bates Wells & Braithwaite 2008

Charity Commission response

Trying to be more customer friendlyFlexible – responding to circumstancesShorter response times

© Bates Wells & Braithwaite 2008

Useful sources of informationCharity Commission:www.charitycommission.gov.uk0870 333 0123

NCVOwww.ncvo-vol.org.uk020 7713 6161

Active Community Unitwww.homeoffice.gov.uk.comrace/active020 7035 5328

Charity Law Associationwww.charitylawassociation.org.uk

Inland Revenue Charities Unitwww.inlandrevenue.gov.uk/menus/charity.htm0845 302 0203

© Bates Wells & Braithwaite 2008

Tom Pratt and Tessa GregorySolicitorsCharity and Social Enterprise DepartmentBates Wells & Braithwaite London LLP2 – 6 Cannon StreetLondon EC4M 6YHTel: 020 7551 7777

E-mail: [email protected] & [email protected]

Related Documents