Pacific Economic Review, 4: 2 (1999) pp. 215–232 PERSPECTIVES ON PUBLIC POLICY AN INTERTEMPORAL CURRENCY BOARD ALEX CHAN The University of Hong Kong NAI-FU CHEN University of California Irvine, USA Abstract. The paper shows that the traditional wisdom of raising interest rates to defend a currency enriches rather than punishes the speculators. Furthermore, using high interest rates as a currency defense tool often produces the opposite effect in times of crisis. A new approach is proposed of using Hong Kong dollar ‘‘put’’ options as an explicit commitment by the government. The put option itself acts like an intertemporal currency board in keeping the linked exchange rate over time. This costly signaling produces a separating equilibrium that distinguishes the strength of the Hong Kong dollar from the other Asian currencies that were under pressure in 1997. 1. INTRODUCTION The devaluation of the Thai baht in the summer of 1997 set off the Asian currency crisis. The crisis substantially affected many other currencies: the South Korean won, the Indonesian rupiah, the Malaysian ringgit, the Philippine peso, and others. There were two questions facing decision-makers in Hong Kong: * Should the Hong Kong dollar (HK$) maintain its link with the US dollar (US$)? * If so, how to defend the Hong Kong dollar when the surrounding currencies are falling? The answer to the first question is obvious – Hong Kong should not devalue its currency. Faced with the decrease in value of the surrounding currencies, Hong Kong has two choices in maintaining its competitiveness: (a) to allow the Hong Kong dollar to float, or (b) to allow its domestic prices to deflate. At first glance, option (a) may be easier because the other option means substantial pain to the local economy. However, option (a) can quickly lead to a bottomless pit with competitive devaluation all around. Thus it is far better to anchor the HK$ to the US$ and allow the domestic price structure to find its level (option (b)) than to allow the HK$ and the domestic price structure to fall freely. Furthermore, the economic foundation of Hong Kong lies in its value as an international finance center and a world trading post for China. Both of these roles require a stable currency so that investors and traders do not have to bear any additional currency risks. Thus the prosperity of Hong Kong depends # Blackwell Publishers Ltd 1999. 108 Cowley Road, Oxford OX4 1JF, UK and 350 Main Street, Malden, MA 02148, USA Address for correspondence: School of Economics and Finance, The University of Hong Kong, Pokfulam Road, Hong Kong, Tel: (852)-28578510; E-mail: [email protected]. We thank K. C. Chan, Yuk-shee Chan, Leonard Cheng, Francis Lui, Fred Kwan and especially Merton Miller for their helpful comments on earlier versions of this paper.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

{Journals}per/4-2/n177/n177.3d

Pacific Economic Review, 4: 2 (1999) pp. 215±232

PERSPECTIVES ON PUBLIC POLICY

AN INTERTEMPORAL CURRENCY BOARD

ALEX CHAN� The University of Hong KongNAI-FU CHEN University of California Irvine, USA

Abstract. The paper shows that the traditional wisdom of raising interest rates to defend a currency

enriches rather than punishes the speculators. Furthermore, using high interest rates as a currency

defense tool often produces the opposite effect in times of crisis. A new approach is proposed of

using Hong Kong dollar ``put'' options as an explicit commitment by the government. The put

option itself acts like an intertemporal currency board in keeping the linked exchange rate over

time. This costly signaling produces a separating equilibrium that distinguishes the strength of the

Hong Kong dollar from the other Asian currencies that were under pressure in 1997.

1. INTRODUCTION

The devaluation of the Thai baht in the summer of 1997 set off the Asiancurrency crisis. The crisis substantially affected many other currencies: the SouthKorean won, the Indonesian rupiah, the Malaysian ringgit, the Philippine peso,and others. There were two questions facing decision-makers in Hong Kong:

* Should the Hong Kong dollar (HK$) maintain its link with the US dollar(US$)?

* If so, how to defend the Hong Kong dollar when the surroundingcurrencies are falling?

The answer to the first question is obvious ± Hong Kong should not devalueits currency. Faced with the decrease in value of the surrounding currencies,Hong Kong has two choices in maintaining its competitiveness: (a) to allow theHong Kong dollar to float, or (b) to allow its domestic prices to deflate. At firstglance, option (a) may be easier because the other option means substantial painto the local economy. However, option (a) can quickly lead to a bottomless pitwith competitive devaluation all around. Thus it is far better to anchor the HK$to the US$ and allow the domestic price structure to find its level (option (b))than to allow the HK$ and the domestic price structure to fall freely.Furthermore, the economic foundation of Hong Kong lies in its value as an

international finance center and a world trading post for China. Both of theseroles require a stable currency so that investors and traders do not have to bearany additional currency risks. Thus the prosperity of Hong Kong depends

# Blackwell Publishers Ltd 1999. 108 Cowley Road, Oxford OX4 1JF, UK and 350 Main Street,Malden, MA 02148, USA

�Address for correspondence: School of Economics and Finance, The University of Hong Kong,Pokfulam Road, Hong Kong, Tel: (852)-28578510; E-mail: [email protected]. We thankK. C. Chan, Yuk-shee Chan, Leonard Cheng, Francis Lui, Fred Kwan and especially MertonMiller for their helpful comments on earlier versions of this paper.

{Journals}per/4-2/n177/n177.3d

critically on maintaining a stable currency through its link with the US$. In thissense, the only question is how most effectively to defend its link.

1.1. The fundamental principle

To defend the Hong Kong dollar, we must first reiterate the economicfoundation that determines the value of a currency. The value of a Hong Kongdollar derives from the HK goods and services an HK dollar can buy. Thisdetermines the world price of an HK dollar. Thus the first principle ofdefending the HK dollar must be to keep the HK economy strong and itsproducts desirable in order to maintain the strength of the dollar.Hong Kong has been operating under a currency board system1 since 1983,

with the HK dollar linked at 7.8HK$=US$. Hong Kong enjoys a stableeconomy (a beneficiary of the strong Chinese economy). It has well-fundedbanks, sound fiscal policies, no foreign debts and a huge foreign currencyreserve. There is no reason why Hong Kong needs to break the link anddevalue its currency. As long as the local people do not lose faith, the HKdollar can easily maintain its link with the US dollar.Since the huge foreign currency reserve belongs to the people of Hong Kong,

it indirectly lends strength to the HK dollar. The main function of the reserve isto act as a shock-absorber to protect the local economy whenever the currencyis under pressure. As long as the local markets and people are protected frompanics, everything is fine.Defending a currency is very much like defending a bank from a destructive

run. The strength of a bank depends on its sound investment strategies (like theeconomic fundamentals for a currency). Yet the bank maintains enoughliquidity (like the reserve for a currency) to absorb temporary runs (if any) onthe bank. The liquidity is there to avoid panics, but the strength of the bankultimately relies on the strength of its investments. Therefore, the fundamentalprinciple of defending a strong currency is to keep the economy strong, themarkets calm and the local people from panics.Bensaid and Jeanne (1997) and Jeanne (1997)2 discuss the instability of fixed

exchange rate systems3 when a government tries to defend the currencythrough raising the nominal interest rate. As speculators are aware of the costof high interest rate policy to the country and the incentives for the governmentabort the defense, using a high interest rate policy to defend a currency canreinforce the speculative attack. Indeed, they show that raising the interest ratecan eventually generate self-fulfilling currency crises.In this paper, we offer an alternative solution using derivative securities to

supplement the classical currency board system. The use of derivatives toachieve a central bank's exchange rate policy is also the subject of discussion of

1 See Hanke and Schuler (1994) for a detailed discussion of issues related to currency boards.2 See also Blackburn and Sola (1993), Obstfeld (1986), and Obstfeld (1996).3 See related issues in Dornbusch (1976), Drazen and Masson (1994), Flood and Garder (1984),Svensson (1994), and Von Hagen (1992).

216 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

several recent studies. Zapatero and Reverter (1997) compare the effects ofdirect central bank interventions in the spot exchange market and interventionswith currency options. They find that central bank interventions with optionsare more efficient and have the advantage of strengthening the domesticcurrency and lowering the domestic interest rates at the same time. Breuer(1997) suggests that central banks can create a target zone of their exchangerate through selling ``strangle'' option portfolios. He finds that the interventionscheme with options can lower the volatility of the spot exchange rate, has alower expected cost than spot market interventions, and provides the rightincentives for a central bank to adhere to its target rate.Our proposed currency defense strategy requires that the Hong Kong

Monetary Authority (HKMA) offer limited guarantees (currency ``put''options) against the devaluation of the HK dollar. A put option to sell HKdollars for US dollars at the exercise price of HK$7.8 (the linked exchangerate) is a financial contract that is worthless to the holder if the HK dollar stayson the strong side. However, it is worth the difference between the spotexchange rate and HK$7.8 if the HK dollar weakens to a level beyond theexercise price. Thus it is like an insurance policy offered by the HKMA againstthe weakening of the currency beyond the linked exchange rate of HK$7.8=US$. This could serve as a signal to the market of the explicit commitment ofthe HKMA to maintain the link, thereby injecting confidence into the marketin times of crisis. Instead of direct market intervention, the HKMA would beproviding the proper foundation for the banks to engage in interest ratearbitrage between the HIBOR (Hong Kong Inter-bank Offer Rate) and theLIBOR (London Inter-bank Offer Rate). The domestic interest rate, however,could be determined by market forces.In section 2, we show that raising interest rates (in response to attacks on the

HK dollar) enriches (rather than punishes) the speculators. We argue that thetraditional mechanism of maintaining high interest rates as a currency defensein times of crisis often produces the opposite effect. In the case of Hong Kong,the HK$ link has been supported by the HK economy, not by high interestrates. High interest rates are slowly ruining the HK economy and weakeningthe link. In section 3, we propose a new approach of using currency put optionsto guide Hong Kong markets away from panics, thereby lowering the highinterest rates, strengthening the economy and maintaining the link. In section4, we show that the introduction of those options will not increase thespeculative incentive to attack the currency. Furthermore, it will push themarket towards a good equilibrium rather than a bad equilibrium. Section 5concludes the paper.

2. EFFECT OF EXISTING DEFENSE STRATEGIES

2.1. An increasing interest rate can only enrich the speculators

With the enormous growth in derivative products like swaps and forwards,speculators can easily attack a currency and its interest rate simultaneously

AN INTERTEMPORAL CURRENCY BOARD 217

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

with forward contracts. We must, therefore, reconsider the implications of thetraditional strategy of using interest rates as a defense. In the case of HongKong, speculators taking short positions in a HK dollar forward contract canenjoy huge gains if either (i) the HIBOR (Hong Kong Inter-bank Offer Rate)increases over the LIBOR (London Inter-bank Offer Rate), or (ii) the value ofthe spot HK$ exchange rate weakens. Consider the following numericalexample. Under normal conditions, at t� 0:

Spot exchange rate�HK$7.73=US$HK$ interest rate� 6.20%US$ interest rate� 6%.

At t� 1, speculators took a HK$7.9650 billion (or US$1 billion) short positionin the HK$ one-year forward market and created public ``panic:''

Spot exchange rate�HK$7.7485=US$ (exchange rate on 21October 19974)

HK$ interest rate� 9.05769% (1-year HIBOR on same day)

US$ interest rate� 6.09375% (1-year LIBOR on same day)

Forward exchange rate� 7:7485� (1� 9:05769%)

(1� 6:09375%)

24 35�HK7:9650=US$:

In practice, a short HK$ one-year forward is implemented by (a) exchangingHK dollars for US dollars in the spot exchange market, and (b) commiting to aswap, selling US dollars for HK dollars today and selling HK dollars for USdollars one year from now. The spot exchange transaction and the first leg ofthe swap cancel out each other. The net transaction is equivalent to selling HKdollars for US dollars at a predetermined exchange rate one year from now.This forward contract is also equivalent to (a) borrowing HK dollars today forone year, (b) selling the borrowed HK dollars for US dollars in the foreignexchange market, and (c) depositing the received US dollars for one year. Afterone year, the HK$ cash outflow (repayment of the HK$ loan) and the US$cash inflow (from the maturing deposit) together are exactly equivalent to thecommitment under a forward contract. The forward position is ``fully funded''for one year as no cash flow is required until one year later.At t� 2, the HKMA attempted to strengthen the HK dollar by contracting

the HK dollar money supply and increasing interest rates. The new positionwas:

Spot exchange rate�HK$7.7325=US$ (exchange rate on 23October 19975)

HK$ interest rate� 27.4375% (1-year HIBOR on same day)

US$ interest rate� 6.0625% (1-year LIBOR on same day)

4Data from DataStream Inc.5Data from DataStream Inc.

218 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

Forward exchange rate� 7:7325� (1� 27:4375%)

(1� 6:0625%)

24 35�HK$9:2908=US$:

Thus, speculators closed out the position with a huge gain. The gain (in termsof present value) was:6

[HK$(9:2908ÿ 7:9650)� 1B]

[1� 27:4375%]

�HK$1:0404 billion�US$0:1345 billion (� 1:0404=7:7325):

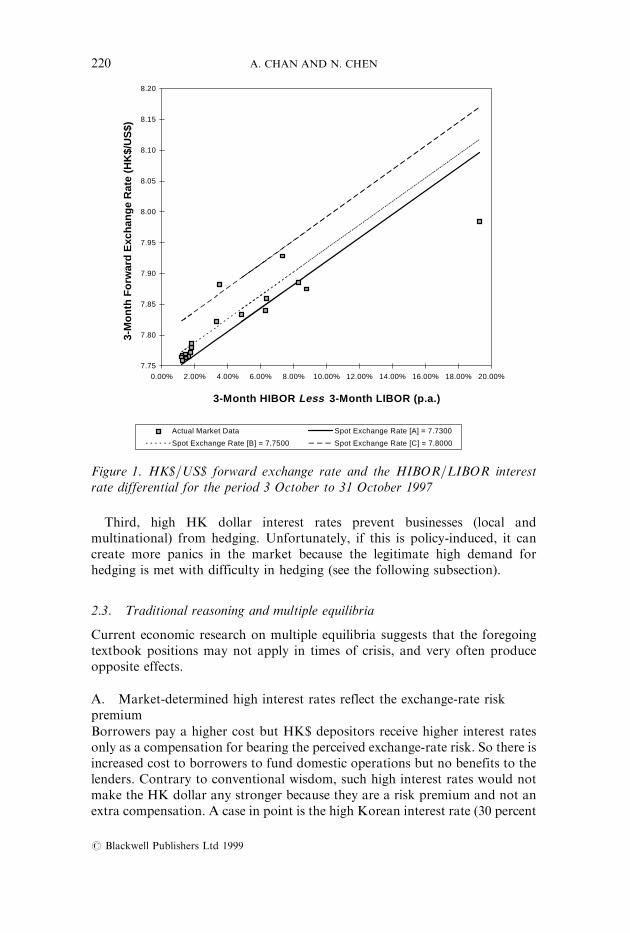

This example illustrates that speculators who locked in their forward positionsup to the point when the HKMA intervened would gain have gained. This isnothing less than borrowing HK dollars at 9.06 percent before the contractionof the money supply and lending out HK dollars at 27.44 percent afterwards.Thus unwinding of the forward position, which is similar to lending out HKdollars, can be easily accomplished when money is tight.Figure 1, using data published by the HKMA for October 1997, illustrates

the weakening of HK$ forwards when the HIBOR went up.7 One can clearlysee how speculators with a short HK$ forward position were enriched wheninterest rates went up. Only speculators would agree that governments shouldconsistently use the strategy of increasing interest rates as a defense againstspeculations.

2.2. Maintaining a high interest rate is an ineffective deterrent to speculations

There are several textbook reasons why high interest rates are used as adeterrent against speculation in normal times.First, high interest rates mean a high HK$ borrowing cost for speculators.

However, a simple calculation shows that the interest rate within a reasonablerange will not be an important consideration for short-term speculators,especially in times of crisis. For example, if (HIBORÿLIBOR) is 3 percent,this implies a carrying cost of approximately 0.01 percent a day. For aUS$1 billion position, the cost per day is only US$0.1 million, which is trivialrelative to the potential gain. (Paradoxical as it might seem, the HKMA maybe able to penalize those speculators taking short positions in HK$ forwardsby reducing the interest rate differential.)Second, high HK dollar interest rates attract capital inflow. In times of crisis,

however, a high interest rate is more a sign of desperation and danger (ratherthan attraction) and so has the opposite effect (see the next subsection).

6 This is an approximate calculation, ignoring the passage of two days between 21 and 23 October1997.7Data for the 3-month HIBOR and the 3-month HK$=US$ forward exchange rate are fromMonthly Statistical Bulletin, November 1997, Hong Kong Monetary Authority; data for the 3-month LIBOR are from Datastream Inc.

AN INTERTEMPORAL CURRENCY BOARD 219

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

Third, high HK dollar interest rates prevent businesses (local andmultinational) from hedging. Unfortunately, if this is policy-induced, it cancreate more panics in the market because the legitimate high demand forhedging is met with difficulty in hedging (see the following subsection).

2.3. Traditional reasoning and multiple equilibria

Current economic research on multiple equilibria suggests that the foregoingtextbook positions may not apply in times of crisis, and very often produceopposite effects.

A. Market-determined high interest rates reflect the exchange-rate riskpremium

Borrowers pay a higher cost but HK$ depositors receive higher interest ratesonly as a compensation for bearing the perceived exchange-rate risk. So there isincreased cost to borrowers to fund domestic operations but no benefits to thelenders. Contrary to conventional wisdom, such high interest rates would notmake the HK dollar any stronger because they are a risk premium and not anextra compensation. A case in point is the high Korean interest rate (30 percent

7.75

7.80

7.85

7.90

7.95

8.00

8.05

8.10

8.15

8.20

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00% 20.00%

3-Month HIBOR Less 3-Month LIBOR (p.a.)

3-M

onth

For

war

d E

xcha

nge

Rat

e (H

K$/

US

$)

Actual Market Data Spot Exchange Rate [A] = 7.7300

Spot Exchange Rate [B] = 7.7500 Spot Exchange Rate [C] = 7.8000

Figure 1. HK$=US$ forward exchange rate and the HIBOR=LIBOR interestrate differential for the period 3 October to 31 October 1997

220 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

or more) in December 1997 and the Indonesian interest rates in January andFebruary of 1998.

B. Policy-induced (artificially) high interest rates means efficiency loss in theeconomyThere is an implied decrease in GDP growth for every percentage pointincrease in the interest rate. The higher this artificial interest rate, the faster isthe economic suicide which the policy is committing. If the economy isdestroyed, so is the currency.In normal times, the artificially high interest rate might make the HK dollar

more attractive because of the extra compensation. In times of crisis, a smallextra compensation is often overwhelmed by the risk premium (signal beingburied by noise) and therefore ineffective. A large extra compensation means ahuge efficiency loss, weakening the economy. Firms whose profit margins arenot sufficient to cover the interest rates are effectively cut off from this sourceof funding. Thus a high interest rate, instead of making the currency moreattractive, can actually be perceived as a sign of weakness reflecting thedesperate state of the economy in a time of crisis.The Korean and the Indonesian interest rates were 30 percent or higher at

the end of 1997 but this did not attract much US$ inflow. The high interestrates (of which a major component is risk premium) were an indication that theperceived risk was pushing towards a bad equilibrium (further devaluation andcollapse of the economy) rather than a good equilibrium. In the case of HongKong, if the difference between the HIBOR and the LIBOR is large, the signalto the world is that it requires a high interest rate to attract deposits into theHK dollar, in a manner similar to the high interest rate needed to attractinvestors to buy junk bonds because of the high risk.

C. An artificially high interest rate creates an artificial barrier to theconvertibility of the HK$ into US$Although it might seem to be protecting the HK dollar, its ultimate effect is todestroy the desirability of Hong Kong as a place to conduct business. With thisbarrier, the multinationals would find it difficult to hedge their currencyexposures. The local corporations would find it difficult to protect the realvalue (world price) of their profits. This is equivalent to partially shutting downthe market.As we observed in 1997, the introduction of capital and exchange controls

(15 May in Thailand) and the ``limits on swaps by nonresidents not related tocommercial transactions'' (Malaysia) did not do much to restore confidence inthe currencies. Malaysia also temporarily prohibited short sales in the stockmarket, but was forced to lift this restriction in the wake of large sell-offs byforeign investors. To impose a higher interest rate on investors who want tohedge is similar to imposing a higher transaction fee on futures contracts toprotect the market. The protection arising from partially shutting down themarket is merely an illusion. Instead of building up the investors' confidence, itactually destroys it.

AN INTERTEMPORAL CURRENCY BOARD 221

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

The analogy with bank runs makes the point more obvious. For a stablebank (analogous to the Hong Kong economy), if there is a bank run, theproper response is to leave the bank doors wide open 24 hours a day to allowdepositors to withdraw as much money as they wish and the bank run will bequickly contained. If the response is to make withdrawal more difficult, thisserves only to make the lines outside of the bank longer and the collapse of thebank more imminent.In the short run, the artificially high domestic interest rate might strengthen

the domestic currency if corporations are induced to borrow in foreigncurrency and convert it into local currency to fund domestic operations. This,unfortunately, is only a temporary illusion as the mismatch in currency riskcreates a reservoir of pent-up demand for hedging the currency risk ± a timebomb waiting to explode on the day of reckoning. It is, therefore, notsurprising to find that when the exchange rates broke in the recent Asiancurrency crisis, the currencies often experienced a freefall from the flood ofdemand for the US dollar.

D. It is not feasible to maintain an artificially high interest rate (the barrier)for a long timeThis would kill the economy even without the speculators. If the policy were toincrease the interest rate (thus erecting a barrier) every time the HK dollar wasunder attack, it would be equivalent to enriching the speculators whenever theycame. This would entice the speculators to come again and again. After awhile, the locals would be forced to hedge against such government policy andthe HK dollar would quickly collapse.

3. AN INTERTEMPORAL CURRENCY BOARD

The classical currency board has two built-in mechanisms to stabilize the localcurrency so long as the local people have confidence in the governmentmaintaining the link. First, if the market rate for the local currency becomesweaker than the linked exchange rate, people can purchase the local currency inthe market and exchange it with the currency board at an arbitrage profit,thereby strengthening the local currency. Thus, instead of intervening in themarket (as a currency board should not do), the currency board provides aplatform for the people to build confidence and support the currency. Second,if the above mechanism is contracting the supply of the local currency toomuch relative to demand, the domestic interest rate will rise and attract aninflow of foreign currency. These two built-in mechanisms will work as long asthe people have confidence and the currency board does not deviate from itsstrict discipline and start behaving like a central bank.The classical currency board, however, is not designed to handle a crisis in

confidence when the currency is under such pressure that the link might bebroken in the near future. The usual symptom is that the domestic interest ratejumps to reflect the risk premium. While the classical currency board has acommitment to the link today, it does not deal with the potential risk of de-

222 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

linking tomorrow. Our idea of an intertemporal currency board addresses thisissue directly. At the heart of the proposal is a domestic currency put optionthat the board is required to offer (by auction) to the market as an explicitcommitment from the government to maintain the link in the future.The main contractual feature of the currency put option is in its payoff. At the

expiration, if the domestic currency spot exchange rate (relative to the reservecurrency) is stronger than the exercise price (usually the linked exchange rate),the put option is worthless. If the spot exchange rate of domestic currency isweaker than the linked exchange rate, the holder of the put option receives thedifference between the spot exchange rate and the linked exchange rate.In practice, the option can take many different forms. It can be a simple

European-type domestic currency put (or equivalently a reserve currency call).It can be an embedded option within a structured note (see Miller, 1998). It canbe an insurance contract against currency devaluation. The exact details ofhow the intertemporal currency board can be applied to the existingmechanisms of the HKMA are described in the Appendix.The main concept can be best explained with an example. Let HK$ be the

domestic currency, let US$ be the reserve currency, and assume the linkedexchange rate to be 7.8HK$=US$. In times of crisis, if there is doubt about theresolve of the HKMA to maintain the link, the HKMA should issue (byauction) HK$ puts (or equivalently US$ calls) with an exercise price of7.8HK$=US$. The option essentially guarantees the holder that the currencyboard arrangement, 7.8HK$=US$, will hold for the amount of the option atthe future expiration date.This intertemporal currency board arrangement would serve several purposes.

It is a costly signal from the government that it is ``putting its money where themouth is.'' It is backing up its promise of the link over time with commitment. Ifthe link is broken, the government would face a payout equal to the fall in thecurrency. Such commitment would strengthen the confidence in the link, and thedomestic interest rate (HIBOR) would fall back to a level close to the reservecurrency interest rate (LIBOR). Consequently, the domestic economy would nothave to suffer from high interest rates arising from the risk premium.Ideally, when the currency is under attack, the (HIBORÿLIBOR) rate

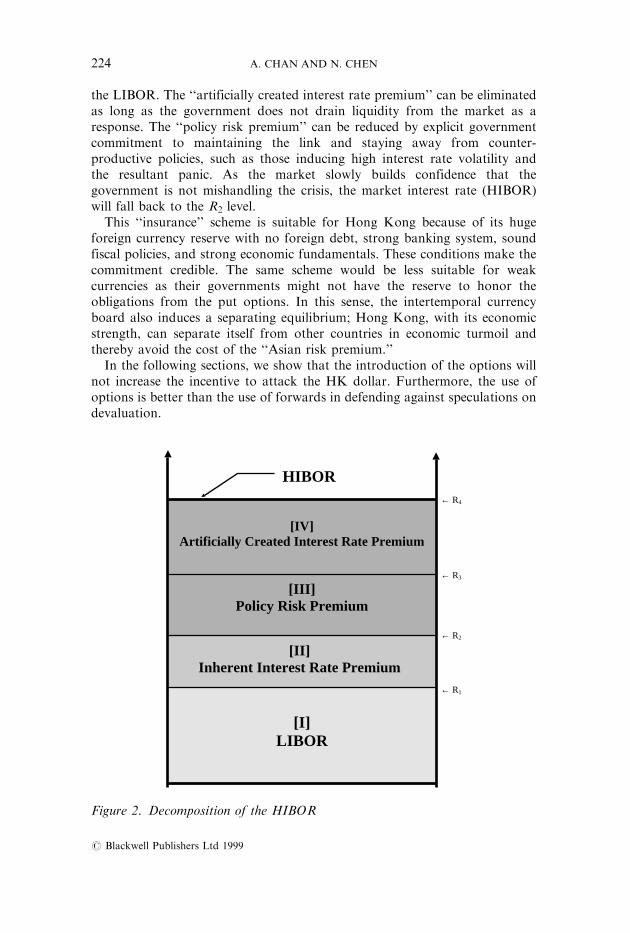

differential should reflect only the inherent risk of devaluation, not the lack ofresolve of the HKMA to maintain the link, nor the lack of confidence in itshandling of the crisis. In other words, it should reflect only the risk of theinherent inability to maintain the link rather than the risk of mishandling thecrisis. If the HIBOR is too low, it provides speculators and hedgers with lowfunding cost (cheap insurance) to add pressure on the currency. If the HIBORis too high, it partially shuts down the market, creates panics and ruins theeconomy. Thus the response from the HKMA should be to provide acommitment to maintain the link and a foundation for the market to find thecorrect market level for the HIBOR in the absence of panics.Consider figure 2, in which the ``correct'' level of the HK dollar interest rate

is at R2, which is the sum of the ``inherent interest rate premium'' (reflecting thetrue inherent risk of devaluation under the correct government response) and

AN INTERTEMPORAL CURRENCY BOARD 223

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

the LIBOR. The ``artificially created interest rate premium'' can be eliminatedas long as the government does not drain liquidity from the market as aresponse. The ``policy risk premium'' can be reduced by explicit governmentcommitment to maintaining the link and staying away from counter-productive policies, such as those inducing high interest rate volatility andthe resultant panic. As the market slowly builds confidence that thegovernment is not mishandling the crisis, the market interest rate (HIBOR)will fall back to the R2 level.This ``insurance'' scheme is suitable for Hong Kong because of its huge

foreign currency reserve with no foreign debt, strong banking system, soundfiscal policies, and strong economic fundamentals. These conditions make thecommitment credible. The same scheme would be less suitable for weakcurrencies as their governments might not have the reserve to honor theobligations from the put options. In this sense, the intertemporal currencyboard also induces a separating equilibrium; Hong Kong, with its economicstrength, can separate itself from other countries in economic turmoil andthereby avoid the cost of the ``Asian risk premium.''In the following sections, we show that the introduction of the options will

not increase the incentive to attack the HK dollar. Furthermore, the use ofoptions is better than the use of forwards in defending against speculations ondevaluation.

[II]Inherent Interest Rate Premium

[III]Policy Risk Premium

[IV]Artificially Created Interest Rate Premium

[I]LIBOR

← R1

← R2

← R3

← R4

HIBOR

Figure 2. Decomposition of the HIBOR

224 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

4. THE EFFECT OF THE OPTIONS IN THE MARKET

4.1. Pushing the market towards a good equilibrium

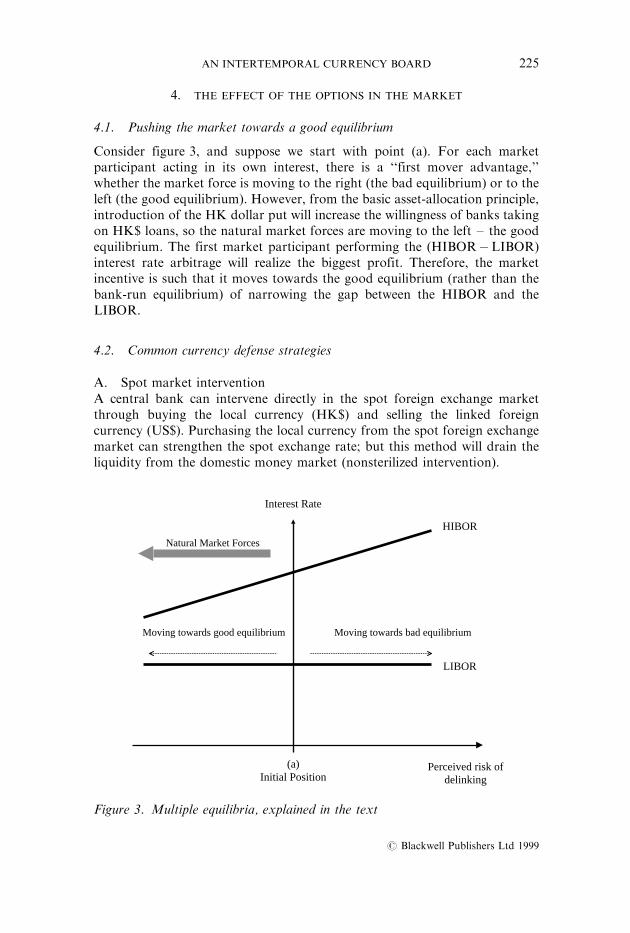

Consider figure 3, and suppose we start with point (a). For each marketparticipant acting in its own interest, there is a ``first mover advantage,''whether the market force is moving to the right (the bad equilibrium) or to theleft (the good equilibrium). However, from the basic asset-allocation principle,introduction of the HK dollar put will increase the willingness of banks takingon HK$ loans, so the natural market forces are moving to the left ± the goodequilibrium. The first market participant performing the (HIBORÿLIBOR)interest rate arbitrage will realize the biggest profit. Therefore, the marketincentive is such that it moves towards the good equilibrium (rather than thebank-run equilibrium) of narrowing the gap between the HIBOR and theLIBOR.

4.2. Common currency defense strategies

A. Spot market interventionA central bank can intervene directly in the spot foreign exchange marketthrough buying the local currency (HK$) and selling the linked foreigncurrency (US$). Purchasing the local currency from the spot foreign exchangemarket can strengthen the spot exchange rate; but this method will drain theliquidity from the domestic money market (nonsterilized intervention).

Moving towards good equilibrium Moving towards bad equilibrium

HIBOR

LIBOR

(a)Initial Position

Interest Rate

Natural Market Forces

Perceived risk ofdelinking

Figure 3. Multiple equilibria, explained in the text

AN INTERTEMPORAL CURRENCY BOARD 225

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

The higher interest rates resulting from this nonsterilized monetaryoperation will also hurt the domestic economy. It can further create panicsand enrich speculators if the interest rates are allowed to jump. If the HKMA isusing sterilized monetary operations (i.e. the received HK dollars are recycledback into the banking system), the net effect is similar to using forwards asdiscussed below.

B. Forward market intervention

Sophisticated speculators take short positions in domestic-currency (HK$)forward contracts to attack the currency. If the HKMA takes the oppositeposition (long position in forward contracts of HK$), it can offset the effectfrom the speculators on the foreign exchange market and the money market.The liquidity, and therefore the domestic interest rate, is determined by theamount of forward contracts.

C. HK$ put options

Alternatively, as we suggest, the HKMA can write (taking short positions in)HK dollar put option contracts (or equivalently US$ call option contracts). Inthis case, the HKMA has to bear roughly the same8 ``value-at-risk'' under theworst situation (de-linking of the HK$ exchange rate) as in taking longpositions in HK$ forward contracts. We would argue that using HK$ putoptions is a better strategy than using forward contracts to defend against thecurrency speculations on devaluation of the HK dollar.

4.3. Comparison between the defense strategies of taking short positions in US$call options and taking short positions in US$ forward contracts

Suppose the HK dollar is under attack and the HKMA decides to defend theexchange rate link. Let us analyze the difference between using US$ calloptions and using US$ forward contracts. We can show that the formerstrategy provides an additional mechanism to reduce the aggregate incentive inthe market to attack the HK dollar.If the HKMA uses forward contracts to defend the currency, there is a net9

positive supply of long positions in US$ forward contracts in the market of HongKong (excluding the HKMA). If the HKMA uses US$ call option contracts todefend the HK dollar, there is a net positive supply of long positions in EuropeanUS$ call option contracts (or equivalently European HK$ put option contracts)in the market of Hong Kong. Theoretically, we can decompose the EuropeanUS$ call option into three components as shown in the following:

(1) a US$ forward at market forward price, plus

8 There is a small difference between their ``value-at-risk,'' coming from the difference between theexercise price of the US$ call option (HK$7.80=US$) and the delivery price of the US$ forwardcontract (e.g. HK$8.0=US$).9Net position is the aggregate long positions less the aggregate short positions of all parties (insideor outside the banking system, but excluding the HKMA).

226 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

(2) a time deposit with an amount equal to the difference between the forwardprice and 7.80, plus

(3) a US$ put option with exercise price (US$1=HK$7.80)�US$0.128205=HK$.

As component (1) is exactly the same as a US$ forward contract, to comparethe US$ call strategy and the forward contract strategy we have only to studythe impact from components (2) and (3). In the aggregate sense, will the overallmarket (excluding the HKMA) have more or less incentive to attack the HK$exchange rate link (and spread any unfavorable rumor to create public panicabout the possibility of de-linking) given (2) and (3)?``Component (2) ± HK$ time deposit'' has time to maturity the same as the

European US$ call option. The time deposit will repay an amount equal to thedifference between the prespecified forward price and the linked exchange rate,7.80. For example, if the market forward exchange rate at the time the HKMAsold the US$ call option were HK$8.0=US$, the repayment of the time deposit atits maturity would be HK$(8.00ÿ 7.80)�HK$0.20. The market value of``Component (2)'' is the present value of the final repayment, where the discountrate is the HK dollar interest rate. If market players attack the HK dollar orcreate any unfavorable rumor against it, the market sentiment on the currencybecomes more pessimistic; people expect that depreciation is more likely. Therequired risk premium for holding HK dollars increases and so the interest rateof the HK dollar increases relative to the US dollar interest rate. Holding thelatter interest rate constant, the market value of ``Component (2) ± HK$ timedeposit'' will drop. Through our proposed option defense strategy, the positivenet supply of ``Component (2)'' to the banking system can reduce the aggregateincentive to do harmful things to the HK$ exchange rate link.``Component (3) ± European US$ put option'' has the same exercise price

(US$1=HK$7.80) and time to maturity as the European US$ call option.This US$ put option will be more valuable if the probability of the HK$exchange rate staying stronger than HK$7.80=US$ becomes higher andhigher. If market players attack the HK dollar or create any unfavorablerumor against it, the market sentiment on the currency becomes morepessimistic; people expect that depreciation is more likely. Hence, if themarket perceives the probability of the HK$ exchange rate staying strongerthan HK$7.80=US$ becomes lower and lower, the ``Component (3) ±European US$ put option'' becomes less valuable. Through our proposedoption defense strategy, the positive net supply of ``Component (3) ±European US$ put option'' to the market can reduce the aggregate incentiveto do harmful things to the HK$ exchange rate link.From the decomposition of the US$ call, we can conclude that US$ calls are

better than forward contracts to defend currency speculation because of thebuilt-in deterrents (Component (2) and Component (3)) against speculativeincentives.From the same analysis, it is easy to see that if a speculator wants to attack

the HK dollar, he would rather use long US$ forwards than long US$ calls(HK$ puts) because the carrying cost is lower. Thus the introduction of the

AN INTERTEMPORAL CURRENCY BOARD 227

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

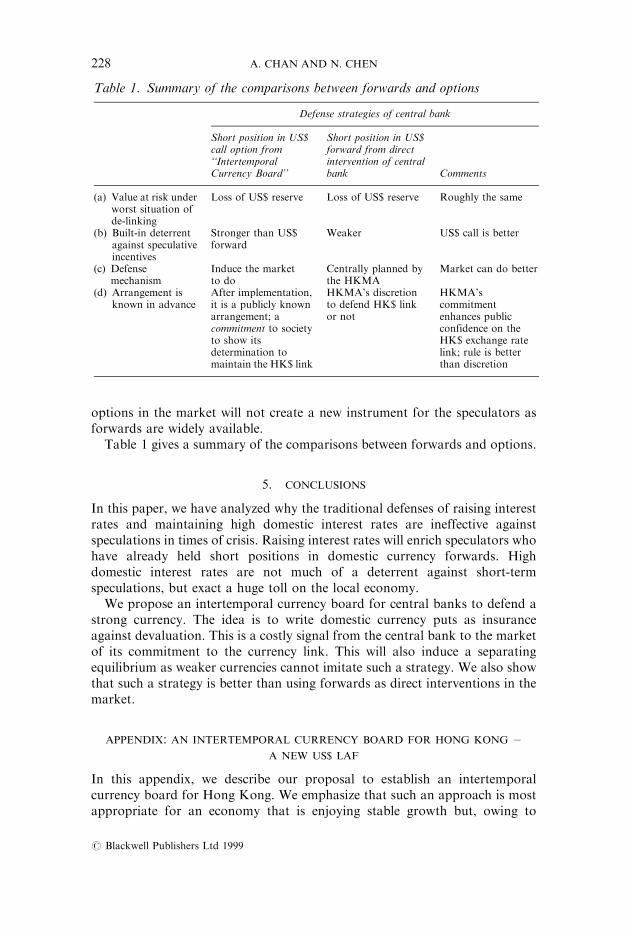

options in the market will not create a new instrument for the speculators asforwards are widely available.Table 1 gives a summary of the comparisons between forwards and options.

5. CONCLUSIONS

In this paper, we have analyzed why the traditional defenses of raising interestrates and maintaining high domestic interest rates are ineffective againstspeculations in times of crisis. Raising interest rates will enrich speculators whohave already held short positions in domestic currency forwards. Highdomestic interest rates are not much of a deterrent against short-termspeculations, but exact a huge toll on the local economy.We propose an intertemporal currency board for central banks to defend a

strong currency. The idea is to write domestic currency puts as insuranceagainst devaluation. This is a costly signal from the central bank to the marketof its commitment to the currency link. This will also induce a separatingequilibrium as weaker currencies cannot imitate such a strategy. We also showthat such a strategy is better than using forwards as direct interventions in themarket.

APPENDIX: AN INTERTEMPORAL CURRENCY BOARD FOR HONG KONG ±A NEW US$ LAF

In this appendix, we describe our proposal to establish an intertemporalcurrency board for Hong Kong. We emphasize that such an approach is mostappropriate for an economy that is enjoying stable growth but, owing to

Table 1. Summary of the comparisons between forwards and options

Defense strategies of central bank

Short position in US$call option from``IntertemporalCurrency Board''

Short position in US$forward from directintervention of centralbank Comments

(a) Value at risk underworst situation ofde-linking

Loss of US$ reserve Loss of US$ reserve Roughly the same

(b) Built-in deterrentagainst speculativeincentives

Stronger than US$forward

Weaker US$ call is better

(c) Defensemechanism

Induce the marketto do

Centrally planned bythe HKMA

Market can do better

(d) Arrangement isknown in advance

After implementation,it is a publicly knownarrangement; acommitment to societyto show itsdetermination tomaintain the HK$ link

HKMA's discretionto defend HK$ linkor not

HKMA'scommitmentenhances publicconfidence on theHK$ exchange ratelink; rule is betterthan discretion

228 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

exogenous factors, has its currency under pressure from speculative attacks (aswas the case of the Hong Kong dollar in October 1997). At that time, the HongKong economy was growing at an annual rate of 5 percent. Its currency reservewas about US$88 billion which was more than four times its monetary baseand ranked third in the world after Japan and China. Its currency came underattack when the currencies in the surrounding countries fell substantiallyagainst the US dollar in the second half of 1997.The main objective of our approach is to keep the local economy from

panics while preventing speculators from gaining profits, thereby stopping themarket from developing into a bank-run equilibrium.

Outline of our proposal

There are three sources of panics: (a) the HK dollar falls through some``barrier'' (7.75, 7.80) in the foreign exchange market; (b) there is a significantdepletion of the foreign currency reserve; (c) interest rates jump significantly.Our approach uses the concept of an intertemporal currency board

(described below) to supplement the Classical Currency Board to protectagainst (c) and (a). The main idea is to allay the fears of the domestic marketthat the link might be broken in the near future. This is accomplished byissuing a promise with commitment from the HKMA (issuing US$ call optionsor equivalently HK$ put options). The existence of this mechanism will notincrease the incentive to attack the HK dollar.Furthermore, the government can use short-term long HK$ forwards to

protect (a) and (b), and keep rolling them over until pressure subsides. (Notethat direct intervention in the spot exchange market and injecting liquidity issimilar to a forward position.) This can also be combined with further writingsof US$ calls (HK$ puts) simultaneously. (This is a remedial medicine tosupplement (if necessary) the preventive medicine when under attack.) If thepressure is too intense, the government can dollarize the economy (even if onlytemporarily)!In the proposal we submitted to the Financial Secretary of Hong Kong on

November 14, 1997, we offered the following ``Intertemporal Currency Board''as a mechanism to deal with pressure on the HK$.

Establishing the intertemporal currency board system10

Similar to the existing HK$ LAF (Liquidity Adjustment Facility), ourproposed US$ LAF provides a source of funding to the Hong Kong bankingsystem. However, in the proposed US$ LAF system, banks are allowed to

10Our main idea is to restore public confidence in the HK$ exchange-rate link system throughdefending the system with HK$ put options. For convenience, we suggest a system using existingmarket instruments ± HK$ Exchange Fund Bills of the HKMA to issue HK$ put options to thepublic when the HK$ money market is in panic. Certainly, there are many different ways for theHKMA to implement our idea of explicitly injecting the HK$ put options into the market.

AN INTERTEMPORAL CURRENCY BOARD 229

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

borrow US$ loans from the HKMA by the collateral of exchange fund bill=noteunder the following special terms:

If a bank takes a US$ loan (say a 3-month loan of US$1 billion) from theHKMA through the proposed US$ LAF, at the loan maturity, the bank canchoose to11

(1) repay US$1 billion plus an interest payment; or(2) repay the HK dollar equivalent of (1) calculated at a prespecified

exchange rate of HK$7.8=US$.

The interest rate of the US$ LAF borrowing should be set at a level slightlyhigher than the LIBOR. Ideally, it should be at the level of R2 (see figure 2)plus a small transaction cost. This can be estimated from economic data.The immediate effect is to induce a change of behavior of the banks through

the HKMA's offering of the US$ call options (or equivalently HK$ putoptions). Banks will be induced to: (1) borrow US dollars from the HKMA; (2)sell the US dollars on the spot exchange market directly for HK dollars; and (3)lend out the received HK dollars to satisfy borrowing demand and push downthe HIBOR. These three steps are similar to buying HK$ forward. Moreover,the overall HK dollar money supply in the economy can remain the same at thediscretion of the HKMA.Banks currently do not do this because of the potential exchange rate risk. If

a bank borrows US dollars to fund its HK dollar lending, it can suffer asignificant loss should the HK dollar link be suddenly broken. A piece ofevidence is the significant interest rate differential between HK$ and US$around the end of October 1997.Such interest rate arbitrage will strengthen the HK$ exchange rate and

reduce the interest rate differential between the HIBOR and the LIBOR.Furthermore, this ``costly'' signal will also restore public confidence throughthe explicit commitment by the HKMA (with its HK$ put option) to maintainthe link.By issuing the put options only to banks that have HK$ exchange fund bill=

notes, the HKMA can limit the outstanding put options in the market. TheHKMA can borrow US dollars from the Euro-dollar market, thus acting onlyas a middleman with a guarantee.

Remarks

(1) The proposed US$ LAF would induce banks to borrow US$ from theHKMA to buy HK$ and then lend out HK$ to clients. As liquidity is alubricant for the economy, this allows the quick introduction of lubricantin a tight market without flooding the market with HK dollars, whichmight inadvertently help speculators.

11 Technically speaking, the HKMA offers a US$ loan to the banks and gives them a European-style HK$ put option (equivalent to a European-style US$ call option) to sell HK$ for US$ at aprespecified rate (HK$7.8=US$).

230 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

(2) Offering the optional repayment scheme is a costly signal of thecommitment to maintain the link (HK$7.8=US$); it, in turn, providesthe needed confidence to the public. It also produces a separatingequilibrium in the sense that it is not feasible for a country with a weakcurrency to imitate the offering of the currency options as they wouldquickly bankrupt such a country.

(3) Banks can solve their liquidity problems through borrowing US$ from theUS$ LAF to fund their HK$ cash demand. Hence, the market forces arehelping the HKMA to maintain the HK$ link once this foundation isestablished. It can also stabilize the interest rate differential between HKdollars and Euro-dollars to a reasonable level. The HIBOR will be morestable and stays reasonably close to the Euro-dollar interest rate.

(4) As the opportunity to take out a US$ loan from the US$ LAF wouldrequire the collateral of a HK$ exchange fund bill=note, the value of theUS$ call option is paid in the auctioning of the HK$ exchange fund bill=notes.

(5) The eventual interest rates will be established by the market in the absenceof panics.

(6) Settlement of the put option can be in the form of cash-settlement. Forexample, with the option strike price as 7.8HK$=US$, if at expiration ofthe option the market exchange rate is 9.50HK$=US$, the issuer has to paythe holder of the put option (9.50ÿ 7.80)=9.50 in US$ for each US$ facevalue in option. This calculation also reflects the value-at-risk for each US$face value of the put option issued.

REFERENCES

Bensaid, B. and O. Jeanne (1997) ``The Instability of Fixed Exchange Rate Systems when Raisingthe Nominal Interest Rate is Costly,'' European Economic Review 41, 1461±78.

Blackburn, K. and M. Sola (1993) ``Speculative Currency Attacks and Balance of PaymentsCrises,'' Journal of Economic Surveys 7, 119±44.

Breuer, P. (1997) ``Central Bank Participation in Currency Options Markets,'' Working Paper,Brown University.

Dornbusch, R. (1976) ``Expectations and Exchange Rate Dynamics,'' Journal of Political Economy84, 1116±76.

Drazen, A. and P. R. Masson (1994) ``Credibility of Policies Versus Credibility of Policy Markers,''Quarterly Journal of Economics 109, 735±54.

Flood, R. and P. Garder (1984) ``Collapsing Exchange-Rate Regimes: Some Linear Examples,''Journal of International Economics 17, 1±13.

Hanke, S. and K. Schuler (1994) ``Currency Boards for Developing Countries: A Handbook''(International Center for Economic Growth, Sector Study 9), San Francisco, CA: ICEG.

Jeanne, O. (1997) ``Are Currency Crises Self-fulfilling? A Test,'' Journal of International Economics43, 263±86.

Miller, M. (1998) ``The Current Southeast Asia Financial Crisis,'' Pacific-Basin Financial Journal 6,225±33.

Obstfeld, M. (1986) ``Rational and Self-fulfilling Balance of Payments Crises,'' American EconomicReview 76, 72±81.

ÐÐ (1996) ``Models of Currency Crises with Self-fulfilling Features,'' European Economic Review40, 1037±47.

Svensson, L. (1994) ``Fixed Exchange Rates as a Means to Price Stability: What Have WeLearned?'' European Economic Review 38, 447±68.

AN INTERTEMPORAL CURRENCY BOARD 231

# Blackwell Publishers Ltd 1999

{Journals}per/4-2/n177/n177.3d

Von Hagen, J. (1992) ``Policy Delegation and Fixed Exchange Rates,'' International EconomicReview 33, 848±70.

Zapatero, F. and L. Reverter (1997) ``Exchange Rate Intervention with Options,'' Working Paper,Centro de Investigacio n Econo mica (ITAM) and Banco de Me xico.

232 A. CHAN AND N. CHEN

# Blackwell Publishers Ltd 1999

Related Documents